mba thesis

TRANSCRIPT

AN ASSESSMENT OF e-COMMERCE APPLICATIONS IN

COMMERCIAL BANKS IN ZIMBABWE

by

Nyasha TN Mukura (R902763X)

February 2002

“The Internet is like a weapon sitting on the table, ready to be

picked up by either you or your competitors.” Michael Dell, 1999.

i

ABSTRACT

The day was December 21, 1994 when the world changed. At a joint press release, the

University of Illinois at Urbana-Champaign and the Netscape Communications Corporation

(formerly known as Mosaic Communications) announced that they had reached agreement

that left Netscape free to market its products independent of the university, its collaborator.

Up until then the Internet had been the preserve of the military and the academic world and

there was no user-friendly interface. Mosaic, the first browser, was responsible for

transforming the Internet from a network for the academically privileged to an everyday tool

for anyone with a PC and a modem.

The growth of the Internet as a communications vehicle and a business medium

since 1995 has been nothing less than spectacular. It has purely been exponential, taking

only 5 years to reach the same coverage as radio did in 38 years and television in 13 years.

This growth has been due to the increasing number of PC owners who are connecting to

the Internet. With an estimated 926 million users by 2003, the Internet has clearly become

the new medium on which competitive battles are being fought, won and lost.

Conducting business via the medium of the Internet is commonly described as e-

commerce or e-business. It is the intention of this dissertation to assess the extent of

implementation of information technology to facilitate e-Commerce by commercial banks in

Zimbabwe. The study also attempts to establish the critical success factors for

implementing e-Commerce in commercial banks in Zimbabwe.

The literature review discusses the e-Commerce concept and its benefits to

organisations and consumers. The results of the study show that almost all commercial

banks recognise the importance of implementing e-Commerce enabling technologies. This

implementation, however, is being done with a defensive motive rather than an offensive

strategic thrust.

The study recommends that banks must approach e-Commerce as a paradigm shift

and use it to restructure both their thinking, their businesses and their markets. The Internet

is here to stay and as Michael Dell put in 1999: “The Internet is like a weapon sitting on the

table, ready to be picked up by either you or your competitors.”

ii

ACKNOWLEDGEMENTS

The author would like to thank the following people:

i) My teachers who taught me enough to be able to write this thesis.

ii) Individuals who took their time to answer the questionnaire. The information

provided invaluable data for this study.

iii) My close friend Dr JK Sakupwanya for believing in my abilities and me. Your never

failing encouragement will always be appreciated.

iv) My group of friends and their wives who have been a source of constant support –

Madondo, Mutepfa and Makore.

v) My church family for their prayers

vi) My supervisor Dr Kabanda for invaluable suggestions and ideas

vii) My wife for her determination to see my potential realised. Thank you for your faith,

encouragement and prayers. E-Moyo. Lakusasa.

viii) My children Wadzi and Nkosi for understanding when I could not take you out on

Sundays.

e-Commerce in Commercial Banks in Zimbabwe Page 1

Table of Contents

1. INTRODUCTION .............................................................................................................. 6

1.1 Profile of World Wide Internet Use .................................................................................. 6

1.2 Purpose of the Research .................................................................................................... 9

1.3 Importance and Justification of Research ....................................................................... 9 2. AIMS AND OBJECTIVES OF THE STUDY ............................................................... 11

2.1 The Problem ..................................................................................................................... 11

2.2 Research Objectives ......................................................................................................... 12

2.3 The Thesis ......................................................................................................................... 12

2.4 Research Methodology ..................................................................................................... 12

2.4.1 Primary Data .............................................................................................................. 12

2.4.2 Population .................................................................................................................. 13

2.4.3 Sampling Approach .................................................................................................... 13

2.4.4 Sample Size ................................................................................................................ 14

2.4.5 Pilot Survey ................................................................................................................ 14

2.4.6 Field Work ................................................................................................................. 14

2.4.7 Data Analysis ............................................................................................................. 14 3. LITERATURE SURVEY ................................................................................................ 15

3.1 Definitions ......................................................................................................................... 15

3.2 Value Creation .................................................................................................................. 16

3.2.1 Tangibles and Intangibles........................................................................................... 18

3.2.2 Paradigm Shift ............................................................................................................ 19

3.3 e-Commerce Framework ................................................................................................. 20

3.4 Value Creation .................................................................................................................. 22

3.4.1 Branding ..................................................................................................................... 23

3.4.2 Customer Relationships ............................................................................................. 23

3.5 Driving Forces of e-Commerce ....................................................................................... 24

3.5.1 Business Pressures and Organisational Responses .................................................... 25

3.6 E-Commerce Spectrum ................................................................................................... 28

3.6.1 Classification of EC Activities ................................................................................... 29

3.7 E-Commerce perspectives ............................................................................................... 33

3.7.1 Communications perspective ..................................................................................... 33

3.7.2 Business process perspective ..................................................................................... 34

3.7.3 Service perspective ..................................................................................................... 35

3.7.4 On-line perspective .................................................................................................... 36

3.8 Electronic Commerce In Service Industries .................................................................. 36

3.8.1 EC in Banking ............................................................................................................ 37

3.9 EC Strategy Implementation........................................................................................... 37

3.9.1 Planning...................................................................................................................... 37

3.9.2 Critical Success Factors ............................................................................................. 39

3.9.3 Moving to the Internet ................................................................................................ 40

e-Commerce in Commercial Banks in Zimbabwe Page 2

3.9.4 Pillars of Success ........................................................................................................ 41

3.9.5 Strategic Options ........................................................................................................ 43

3.10 Conclusion ......................................................................................................................... 45 4. RESEARCH METHODOLOGY.................................................................................... 46

4.1 Research Objectives ......................................................................................................... 46

4.2 Research Approach and Methodology ........................................................................... 46

4.2.1 Sampling Design ........................................................................................................ 46

4.2.2 Variability .................................................................................................................. 47

4.3 Research Tools .................................................................................................................. 47

4.4 Research Assumptions ..................................................................................................... 47

4.5 Limitations of Study ......................................................................................................... 47 5. DATA ANALYSIS AND FINDINGS ............................................................................. 49

5.1 Introduction ...................................................................................................................... 49

5.2 Reliability of Information ................................................................................................ 49

5.3 Data Analysis and Findings ............................................................................................. 50

5.3.1 Research Participants ................................................................................................. 50

5.3.2 Scoring System ........................................................................................................... 51

5.3.3 Overall Perceptions Across Banks ............................................................................. 51

5.3.4 Electronic Delivery Over Networks ........................................................................... 52

5.3.5 Transaction Workflow Automation ........................................................................... 54

5.3.6 Service Quality ........................................................................................................... 55

5.3.7 Implementation Strategy ............................................................................................ 56

5.3.8 Constraints.................................................................................................................. 57 6. CONCLUSION ................................................................................................................. 57

6.1 The Hypothesis Revisited ................................................................................................ 57

6.2 Conclusion ......................................................................................................................... 58

6.3 Suggested Areas of Further Study .................................................................................. 59 7. Bibliography ..................................................................................................................... 61

e-Commerce in Commercial Banks in Zimbabwe Page 3

Figure 3-1 Electronic Markets ............................................................................................................ 16

Figure 3-2 Framework for e-Commerce ........................................................................................ 21

Figure 3-3 Impact of IT on the Organisation ........................................................................................ 26

Figure 3-4 Dimensions of e-Commerce (Choi et al, 1997) .................................................................... 29

Figure 3-5 EC Strategic Cycle ....................................................................................................... 39

Figure 5-1 Analysis of Respondents (absolute numbers) ....................................................................... 50

Figure 5-2 Analysis of Respondents (percentages) ............................................................................... 51

Figure 5-3 Overall Perceptions ........................................................................................................... 52

Figure 5-4 Electronic Delivery over Networks (across banks) ............................................................... 53

Figure 5-5 Electronic Delivery Networks (across functions) ................................................................. 53

Figure 5-6 Automation of workflows .................................................................................................. 54

Figure 5-7 Automation of workflows .................................................................................................. 55

Figure 5-8 Service quality .................................................................................................................. 55

Figure 5-9 Service quality .................................................................................................................. 56

Figure 5-10 Implementation Strategy .................................................................................................. 56

Figure 5-11 Constraints ..................................................................................................................... 57

Table 3-1 Shift from Market place to Market space .............................................................................. 20

Table 3-2 Shift from Market place to Market space .............................................................................. 24

Table 3-3 Major Business Pressures ................................................................................................... 25

APPENDIX I………………………………..…………….ANALYSIS OF RESULTS

APPENDIX II……………………………………...RESEARCH QUESTIONNAIRE

e-Commerce in Commercial Banks in Zimbabwe Page 4

Definitions

24x7x365 24 hours, 7 days a week and 365 days a year

ATM Automatic teller machine

B2B Business-to-business

B2C Business-to-consumer

B2G Business-to-Government

BPR Business process reengineering

C2B Consumer-to-business

C2C Consumer-to-consumer

CEO Chief executive officer

CSF Critical success factors

Data Raw facts that can be shaped and formed to create information

e-Business (EB) Describes the broadest definition of EC in that it includes not just buying

and selling but also servicing customers and collaborating with business

partners, as well as conducing electronic transactions within and between

organisations.

e-Commerce

(EC)

Describes the manner in which transactions take place over networks,

mostly the Internet i.e. it describes the buying and selling of products,

services, and information via computer networks including the Internet.

EDI Electronic data interchange

EIP Enterprise information portal. It provides a single entry point for access to

all relevant information in an organisation for faster decision making.

ERP Enterprise resource planning

Extranet An extranet extends intranets so that they can be accessed by business

partners

G2B Government-to-business

HTML Hyper text markup language

HTTP Hyper text transfer protocol

Information Data that has been analysed into meaningful and useful form

Intranet A networked environment within an organisation which utilises Internet

technologies such as browsers and communications protocols

IOS Inter-organisational information systems

ISP Internet service provider

IT Information technology

LAN Local area network

Portal A hub or electronic marketplace where B2B transactions take place

e-Commerce in Commercial Banks in Zimbabwe Page 5

SCM The management of information and flow of materials between the

supplier and the manufacturer from the time the customer defines his

requirements throughout to the fulfilment of those requirements.

TCP/IP Transmission control protocol/Internet protocol

WAN Wide area network

WWW World wide web

e-Commerce in Commercial Banks in Zimbabwe Page 6

1. INTRODUCTION

According to the former Vice President of America, Al Gore, “We are on the

verge of a revolution that is just as profound as the change in the economy that came

with the industrial revolution. Soon electronic networks will allow people to transcend the

barriers of time and distance and take advantage of global markets and business

opportunities not even imaginable today, opening up a new world of economic possibility

and progress.” (Al Gore, 1997).

Louis Gerstner, Chairman and CEO of IBM during the great turnaround period of

the 90’s is attributed with crafting the IBM e-vision and for crafting the strategy for

launching IBM as an e-business. He also declared in 1999 that “Every day it becomes

clearer that the Net is taking its place alongside the other great transformational

technologies that first challenged, and then fundamentally changed the way things are

done in the world.” (www.ibm.com/lvg/).

These statements are not surprising given that information technology in general

and e-Commerce in particular have become major facilitators of business activities today

according to Tapscott and Caston (1993), Mankin (1996), and Gill (1996). E-Commerce

is also a catalyst of fundamental changes in the structure, operations and management

of organisations. (Dertouzos 1997).

1.1 Profile of World Wide Internet Use

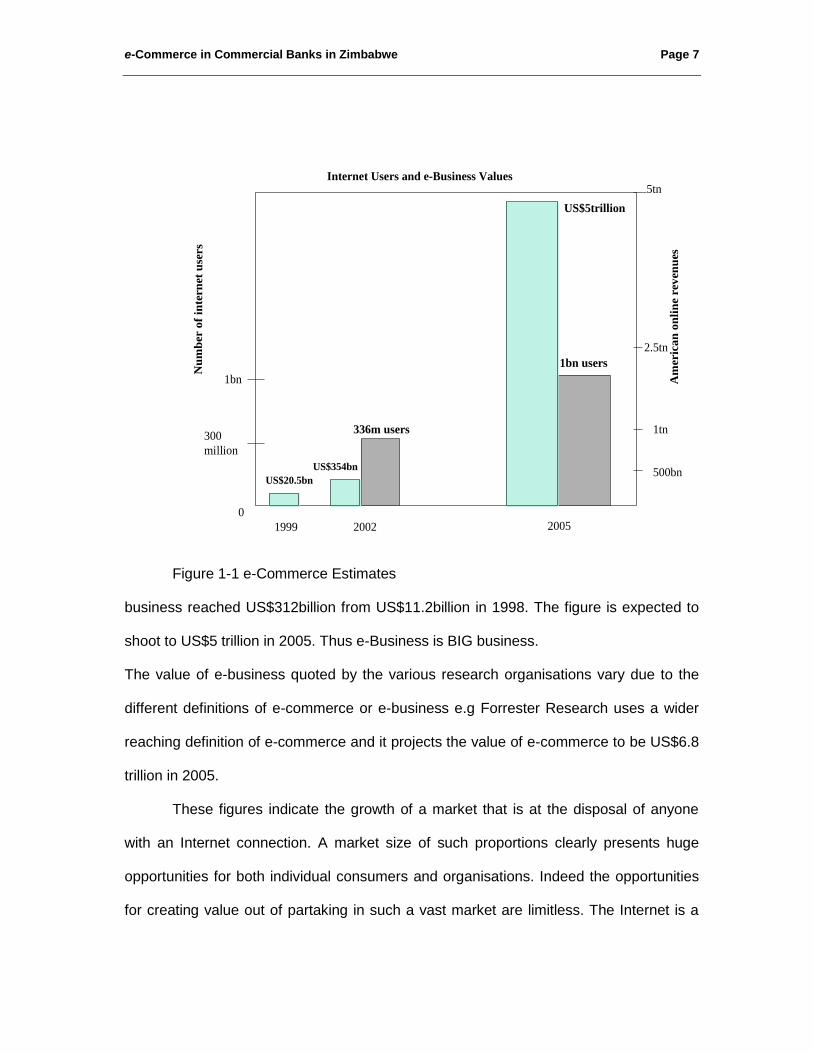

Internet use literally exploded in the late nineties and is not expected to slow

down. This phenomenal growth is expected to continue exponentially. In fact, the

number is expected to triple in the next three years from the current 336 million users to

1billion million users as shown in Figure 1-1. According to International Data (IDC), there

will be a rapid overall growth of e-business in the years leading up to 2005. In 1999

worldwide e-

e-Commerce in Commercial Banks in Zimbabwe Page 7

Internet Users and e-Business Values

1999 2002 2005

US$20.5bn

US$5trillion

336m users

1bn users

Nu

mb

er o

f in

tern

et

use

rs

0

300

million

1bn Am

eric

an

on

lin

e r

ev

en

ues

2.5tn

5tn

500bn

1tn

US$354bn

Figure 1-1 e-Commerce Estimates

business reached US$312billion from US$11.2billion in 1998. The figure is expected to

shoot to US$5 trillion in 2005. Thus e-Business is BIG business.

The value of e-business quoted by the various research organisations vary due to the

different definitions of e-commerce or e-business e.g Forrester Research uses a wider

reaching definition of e-commerce and it projects the value of e-commerce to be US$6.8

trillion in 2005.

These figures indicate the growth of a market that is at the disposal of anyone

with an Internet connection. A market size of such proportions clearly presents huge

opportunities for both individual consumers and organisations. Indeed the opportunities

for creating value out of partaking in such a vast market are limitless. The Internet is a

e-Commerce in Commercial Banks in Zimbabwe Page 8

window through which the world is seen and it is also a window through which the world

sees the individual or the organisation.

In the same report, IDC stated that the United States accounted for the bulk of

the early Internet growth (34% of surfers worldwide in 2000) but with the coming on of

other populous regions it is expected to drop into third position behind Europe and Asia-

Pacific. In terms of value, the US share of the world’s e-commerce will drop from 46% in

2000 to 36% in 2005.

Regions with traditionally poor infrastructure and outdated technology, such as Africa,

India and China have been slow to adopt the Internet as a business medium but they are

poised to be the powerhouses to drive Internet growth. The Internet also offers the

added benefit of avoiding costly bureaucratic procedures in ordering and paying for

foreign goods and services.

Benefits from the Internet are derived mainly from the ability to get products and

services to the market more quickly and the ability to reach new customers at no

additional cost. Once a business goes online, customers can browse, shop, and make a

purchase. This means that physical limitations need not keep anyone away from an

online company. Growth in online spending grew 70% from 2000 to 2001 according to

America On Line (AOL) and nearly three quarters of AOL’s 17 million users shop online.

To further show the power of the Internet, online spending was not dented by the

technology stock crash that occurred in the year 2001.

Growth of the Internet has been fuelled by technological improvements in

telecommunications which permits anyone with a PC and a telephone line to access the

Internet. The result has been the birth of a limitless market and the creation of equally

limitless business opportunities for both organisations and individuals. Consumers also

benefit in that they have more choices and consequently are positioned to enjoy lower

prices and better quality.

e-Commerce in Commercial Banks in Zimbabwe Page 9

For businesses, the Internet poses both a problem and an opportunity. Business-

to-business (B2B) commerce accounted for the close to 80% of e-commerce value in the

year 2000. Thus, the Internet presents even greater potential for businesses. From a

competitive perspective, the Internet has led to the creation of new organisations that

are nimble footed with completely new business models that drive down costs

drastically. Examples of these born on the net include Amazon, eBay and E*Trade.

Traditional brick and mortar companies are also scrambling to move to the Internet in

order to defend turf (market share) against these new net firms.

Another phenomenon is the formation of electronic marketplaces (portals) where

buyers and sellers conduct transactions.

1.2 Purpose of the Research

The purpose of this research is to assess the extent of e-commerce adoption in

commercial banks and recommend critical success factors for successful

implementation in the Zimbabwean environment.

1.3 Importance and Justification of Research

The rate of growth and competition on the Internet is both fast and furious.

Companies need to embrace the new business medium or else risk extinction. Even

Microsoft Corporation admitted that it nearly missed the boat by underestimating the

Internet and not undertaking the necessary paradigm shift in its strategic planning and

focus.

Consumer profile is also shifting, as they know that it is possible to get better

service, faster and cheaper. Thus any firm that does not take the necessary steps to

move to the Internet is preparing its own epitaph.

e-Commerce in Commercial Banks in Zimbabwe Page 10

In Zimbabwe, the economic decline means companies need to provide affordable

products and services at lower costs in order to maintain market share as well as

remaining profitable.

The financial sector in Zimbabwe has been deregulated and thus we continue to

witness new players coming into the market, resulting in increasing competition. It is

therefore important for the players in this sector to embrace the Internet wave.

This study will assist banks to:

a) Understand how far they have implemented technology to support e-Commerce.

This will assist them to identify the missing areas or links and provide areas of focus

for future e-Commerce initiatives.

b) Understand the critical implementation success factors for e-Commerce initiatives

and thus improve the chances of success in future endeavours.

c) Assess the perception of e-commerce by the different functional groups within the

same organisation.

e-Commerce in Commercial Banks in Zimbabwe Page 11

2. AIMS AND OBJECTIVES OF THE STUDY

In the early 1990s, leveraging IT in business was the major thrust of business

strategy. The growth of the Internet has brought another dimension which is forcing

companies to undergo a paradigm shift in their strategic thinking. Successful companies

have managed to leverage IT and gain competitive advantage through:

Improved financial performance from lower costs through efficiency and increased

margins through market share and turnover

Efficient management of organisational resources, such as management of inventory

levels

Streamlining of internal processes in order to achieve ‘world class’ performance

Value was derived from focusing on the tangible assets. The Internet now enables

companies to focus and derive values in the intangibles – customer relationships and

supply chain management.

2.1 The Problem

The new economic model brought about by the Internet is characterised by

speed and increasing competition. Just as the Internet opens up the world to a company,

it also opens up the company to the world. Thus the captive market is on the fast track

out. Clients are no longer restricted to local banks by geographical or political

boundaries and through the Internet can conduct banking transactions from anywhere in

the world with any bank with the appropriate technology in place. Deregulation has been

effected in the Zimbabwean financial sector and thus local banks have to compete on

world standards, otherwise they stand to lose their market share.

e-Commerce in Commercial Banks in Zimbabwe Page 12

2.2 Research Objectives

The objective of this study is to assess how far commercial banks in Zimbabwe

have implemented e-Commerce enabling technologies as well as establish the

implementation critical success factors. The study will:

i) Determine the extent of electronic delivery of products, services, and information

over networks

ii) Assess the extent of automation of transactions and process workflow

iii) Asses the impact of information technology on service quality in terms of speed

of delivery of service/product and convenience

iv) Review the implementation strategy for e-Commerce initiatives in each bank

v) Establish constraints on e-Commerce adoption in banks.

2.3 The Thesis

The major hypothesis to be tested by this research is stated below:

“Commercial banks in Zimbabwe understand the impact of the Internet and are

implementing e-commerce enabling technologies in order to successfully

compete in the new Internet economy.”

2.4 Research Methodology

The data used was from primary sources which was gathered using a

questionnaire and direct personal interviews. The questionnaire is included in Appendix I

2.4.1 Primary Data

Primary data was gathered using questionnaires and personal interviews (see

Appendix I). The target respondents for the questionnaire were bank employees in

different levels and functions.

Personal interviews were directed at IT senior managers and senior managers in

charge of technology. This gave the banks’ e-commerce perspectives from both a

e-Commerce in Commercial Banks in Zimbabwe Page 13

technical and business operation strategic points of view. It was important to establish

how far the technical perspective supported the strategic intent of the business.

2.4.2 Population

The population was from 9 commercial banks in Zimbabwe, as shown below. Five of

these are well established ‘old’ banks while four are young banks which are less than

five years old. The banks surveyed are:

Barclays Bank

Zimbank

The Jewel Bank (CBZ)

Standard Chartered Bank

Kingdom Bank

Century Bank

Time bank

Stanbic

2.4.3 Sampling Approach

The questionnaire was administered to the following groups of people:

PERSON OBJECTIVE

1. Front office (Branch) manager To obtain perspective from people responsible for service and

product delivery to clients. Front office staff provided input on

service quality aspects.

2. Senior IT Manager To obtain the perspective from the people responsible for

technical aspects for e-Commerce. Input from IT managers

provided assessment information from a technical point of view.

3. Manager responsible for

Marketing and Product and

Service development/Marketing

To obtain the perspective from people responsible for product

and service development. This provided valuable input into the

constraints which limit the extent of e-Commerce

implementation.

4. Director responsible for IT or

Product development

To obtain the business perspectives from the strategic level.

e-Commerce in Commercial Banks in Zimbabwe Page 14

2.4.4 Sample Size

All the four people were identified in each bank and the questionnaire

administered. In addition, personal interviews were conducted with the senior

managers/directors in order to establish the strategic intent vis-à-vis e-Commerce in

each bank.

2.4.5 Pilot Survey

A pilot survey was conducted on one bank. The aim was to assess the clarity and

appropriateness of the questions and ease of administering the questionnaires.

2.4.6 Field Work

The questionnaire was administered on the selected respondents who were

asked to answer and submit their responses on the spot.

2.4.7 Data Analysis

The data gathered was analysed using MS Excel statistical functions.

e-Commerce in Commercial Banks in Zimbabwe Page 15

3. LITERATURE SURVEY

3.1 Definitions

Electronic commerce (e-Commerce (EC))

Describes the manner in which transactions take place over networks, mostly the

Internet, i.e. it describes the buying and selling of products, services, and information

via computer networks including the Internet. The infrastructure for EC therefore, is a

networked computing environment in business, home, and government.

Different research organisations apply varying definitions to e-commerce. The IDC

group, for example defines e-commerce narrowly as follows:

“..a process by which an order is placed or accepted via the Internet…therefore

representing a commitment for a transfer of funds in exchange for goods or services.”

This excludes orders placed by fax or email even if they both use the Internet. The

Forrester Research group, on the other hand applies the broader definition given above

where if any part of the transaction takes place via the medium of the Internet, it will be

counted as e-commerce.

E-Business (e-Business (EB))

E-Business describes the broadest definition of EC in that it includes not just buying and

selling but also servicing customers and collaborating with business partners, as well as

conducting electronic transactions within and between organisations. Frequently the two

terms are used interchangeably.

Electronic markets

A market is a network of interactions and relationships where information, products and

services are exchanged. When the market is electronic, the business centre is not a

physical building but rather network-based location where business interactions occur.

(See Figure 3.1 below) The electronic market is a place where shoppers and

e-Commerce in Commercial Banks in Zimbabwe Page 16

Figure 3-1 Electronic Markets

sellers meet and the market handles all the necessary transactions, including the transfer of

money between banks. The principal participants – transaction handlers, buyers, brokers,

and seller are not only at different locations but seldom know even one another. Electronic

market has also been labelled the new retail channel.

It is quite true to state that before the advent of the Internet, such markets would not have

been possible. Thus, the Internet is an enabling medium which creates vast opportunities for

value creation and derivation, as evidenced by the growth in use by both consumers and

businesses alike.

3.2 Value Creation

Electronic commerce provides many advantages over traditional paper based

commerce. Dan Schutzer of the National Information Infrastructure (NII) lists the

following advantages in his paper “Electronic Commerce”:

Shopper/Purchaser Seller/Supplier

Electronic Market

(Transaction Hander)

Electronic commerce

network

(Infrastructure)

Product/service information request

Purchase request

Payment or payment advice

Purchase fulfillment request

Purchase change request

Response to fulfillment request

Shipping notice

Payment approval

Electronic transfer of funds Electronic transfer of funds

Shopper/Purchaser’s Bank

Payment remittance notice

Electronic transfer of funds

Transaction Handler’s Bank

(Automated Clearing House)

Seller/Supplier’s Bank

Electronic Markets

© Prentice Hall, 2000

Response to information request

Purchase acknowledgment

Shipping notice

Purchase/service delivery (if online)

Payment acknowledgment

e-Commerce in Commercial Banks in Zimbabwe Page 17

It provides the customer with more choices and customisation options by better

integrating the design and production processes with the delivery of products and

services. Dell computer company is one of the pioneers in offering the facility for

custom building your own computer depending on your requirements.

It decreases the time and cost of search and discovery, both in terms of customers

finding products and services (e.g. shopping and navigating) and companies finding

customers (e.g. advertising and target marketing). The Internet enables consumers

and businesses to interrogate international web sites at the cost of a local call

through the use of Internet service providers.

It expands the market place from local and regional to national and international

markets with minimal capital outlay, equipment, space or staff.

It reduces delivery lead time

It permits just-in-time (JIT) production systems such as the one implemented by Dell

computers.

It allows businesses to reduce overhead and inventory through improved supplier

chain and customer chain management.

It reduces the transportation and labour costs of creating, processing, distributing

and storing and retrieving paper based information.

It enables the creation and maintenance of reliable, shareable enterprise information

portals (EIP). Enterprise information portals bring together business intelligence and

knowledge management into a new, centralized desktop environment—the

knowledge portal. They provide a personalized single point of access to all relevant

information, enabling better and faster-decision making. EIPs, or knowledge portals,

are also beginning to help organizations capture and leverage their intellectual

assets by facilitating assembly of communities of interest, best practice, and expert

systems within a single, intuitive, Web-based user interface.

e-Commerce in Commercial Banks in Zimbabwe Page 18

It facilitates increased customer responsiveness, including on-demand delivery.

3.2.1 Tangibles and Intangibles

A closer analysis of the advantages outlined above reveals the following

differences between traditional paper based commerce and e-commerce. The traditional

(brick and mortar) business model creates value through tangible assets such as

personnel, products, materials and equipment. E-Business creates value through its

impact on the intangibles – branding, customer relationships and supplier integration.

i) Branding

Branding or corporate image can be quickly established on the Internet e.g what

Amazon.com established in three years took traditional companies generations to

achieve. Branding means trust which is necessary for direct sales.

ii) Customer Relationships

Customers are won and lost on one or more of the following three points:

Convenience

Customers are delighted by convenience such as one-stop shopping. They also want

the process to move smoothly with a few steps e.g. Amazon.com customers use the

patented ‘one-click’ shopping to select their shopping and then wait for the mail to show

up.

Speed

No one likes to wait. For customers, there is no such thing as ‘too fast’. To stay

competitive the company must deliver products and services efficiently and as quickly as

possible.

Personalisation

Customers want to be treated as individuals. The more choices they get for their

products, and the fewer decisions the company makes for them, the happier they are.

e-Commerce in Commercial Banks in Zimbabwe Page 19

These choices are made possible by enabling customisation e.g customers can order a

computer they configure themselves on the Dell website. Success stories on the Internet

are those organisations that have harnessed the Internet to impact positively on these

aspects of customer relationships. Direct marketing also improves the impact of

advertising and enhances the customer relationship.

iii) Supplier Integration

Supplier chain integration is the achievement of greater coordination and collaboration

among supply partners in order to reduce costs, increase flexibility and attain faster

response times. Companies realise dramatic returns through efficiency improvements,

better asset utilisation, faster time to market, reduction in delivery lead times, enhanced

customer service and responsiveness and penetrating new markets. These are achieved

through information sharing, synchronised planning, workflow coordination and evolution

of new business models.

3.2.2 Paradigm Shift

By impacting on the intangibles, the Internet is forcing a paradigm shift on

companies from the traditional model where value is created through the tangibles of

products, and materials. Table 3.1 below summarises the shift that has occurred in the

market space thereby forcing organisations to re-think their business models and

strategies.

Shift From Shift To

1 Mass marketing and advertisement Target one-to-one interactive marketing

2 Mass production – standard products and services

Mass customisation

3 Monologue Dialogue

4 Paper catalogue Electronic catalogues

5 One-to-many communication model Many-to-many

6 Supply-side thinking Demand side thinking

7 Customer as a target Customer as a partner

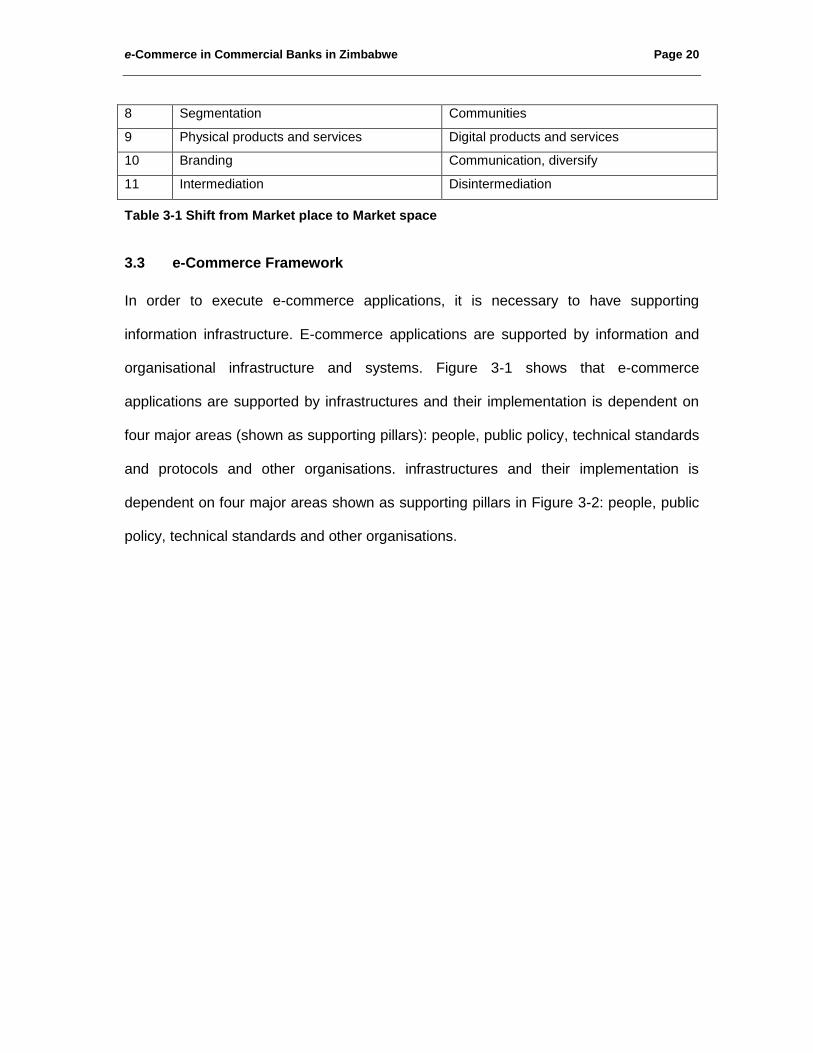

e-Commerce in Commercial Banks in Zimbabwe Page 20

8 Segmentation Communities

9 Physical products and services Digital products and services

10 Branding Communication, diversify

11 Intermediation Disintermediation

Table 3-1 Shift from Market place to Market space

3.3 e-Commerce Framework

In order to execute e-commerce applications, it is necessary to have supporting

information infrastructure. E-commerce applications are supported by information and

organisational infrastructure and systems. Figure 3-1 shows that e-commerce

applications are supported by infrastructures and their implementation is dependent on

four major areas (shown as supporting pillars): people, public policy, technical standards

and protocols and other organisations. infrastructures and their implementation is

dependent on four major areas shown as supporting pillars in Figure 3-2: people, public

policy, technical standards and other organisations.

e-Commerce in Commercial Banks in Zimbabwe Page 21

Figure 3-2 Framework for e-Commerce

Infrastructure comprises the following:

i) Common business services infrastructure

The common business services infrastructure includes security, smart card

authentication, electronic payment systems and catalogues.

ii) Messaging and information distribution infrastructure

The messaging infrastructure is responsible for information distribution e.g. e-mail,

EDI and transfer protocols such as TCP/IP.

Electronic Commerce Applications

• Stocks Jobs • On-line banking

• Procurement and purchasing• Malls • On-line marketing and advertising

• Home shopping • Auctions • Travel • On-line publishing

People:

Buyers, sellers,

intermediaries,

services, IS people,

and management

Public

policy,

legal, and

privacy

issues

Technical standards

for documents,

security, and

network protocols

payment

Organizations:

Partners,

competitors,

associations,

government services

IT Infrastructure

(1)

Common business

services infrastructure

(security smart

cards/authentication

electronic payment,

directories/catalogs)

(2)

Messaging and

information distribution

infrastructure

(EDI, e-mail, Hyper Text

Transfer Protocol)

(3)

Multimedia content

and network

publishing infrastructure

(HTML, JAVA, World

Wide Web, VRML)

(4)

Network infrastructure

(Telecom, cable TV

wireless, Internet)

(VAN, WAN, LAN,

Intranet, Extranet)

(5)

Interfacing

infrastructure

(The databases,

customers, and

applications)

Turban et all 1999

e-Commerce in Commercial Banks in Zimbabwe Page 22

iii) Multimedia content and network publishing infrastructure

Multimedia infrastructure comprises tools for authoring and publishing content on the

web and includes HTML and JAVA.

i) Network infrastructure

The network infrastructure is the physical medium where the information and content

ravel. It also includes wireless.

ii) Interfacing infrastructure

The interface infrastructure includes the actual applications which customers use to

interact on the Internet.

The infrastructure enables interoperability and flexibility as it is based on a common set

of services and standards.

3.4 Value Creation

The traditional (brick and mortar) business model creates value through tangible

assets such as personnel, products, materials and equipment. E-Business creates value

through its impact on the intangibles – branding, customer relationships and supplier

integration via the medium of electronic markets. This is a paradigm shift from the

traditional model where value is created through the tangibles of products, and

materials. This paradigm shift has implications on the information base required to

support the changed business model. Thus information technology underpins the whole

e-business models described in the following sections i.e. technology must be integrated

into the business.

Integration means the organisation must have a seamless set of applications that

must work fluidly not only at the customer and supply chain interface but also internally

to support the business processes.

e-Commerce in Commercial Banks in Zimbabwe Page 23

3.4.1 Branding

Branding or corporate image can be quickly established on the Internet e.g what

Amazon.com established in three years took traditional companies generations to

achieve. Branding means trust which is necessary for direct sales.

3.4.2 Customer Relationships

Customers are won and lost on one or more of the following three points:

Convenience

Customers are delighted by convenience such as one-stop shopping. They also want

the process to move smoothly with a few steps e.g. Amazon.com customers use the

patented ‘one-click’ shopping to select their shopping and then wait for the mail to show

up.

Speed

No one likes to wait. For customers, there is no such thing as ‘too fast’. To stay

competitive the company must deliver products and service s efficiently and as quickly

as possible.

Personalisation

Customers want to be treated as individuals. The more choices they get for their

products, and the fewer decisions the company makes for them, the happier they are.

These choices are made possible by enabling customisation e.g customers can order a

computer they configure themselves on the Dell website. Success stories on the Internet

are those organisations that have harnessed the Internet to impact positively on these

aspects of customer relationships. Direct marketing also improves the impact of

advertising and enhances the customer relationship.

e-Commerce in Commercial Banks in Zimbabwe Page 24

Table 3.1 below summarises the shift from marketplace to market space and this

provides white spaces for companies to create value for themselves through increased

sales and for their customers through improved service.

Shift From Shift To

1 Mass marketing and advertisement Target one-to-one interactive marketing

2 Mass production – standard products and

services

Mass customisation

3 Monologue Dialogue

4 Paper catalogue Electronic catalogues

5 One-to-many communication model Many-to-many

6 Supply-side thinking Demand side thinking

7 Customer as a target Customer as a partner

8 Segmentation Communities

9 Physical products and services Digital products and services

10 Branding Communication, diversify

11 Intermediation Disintermediation

(Modified from Kiani (1998))

Table 3-2 Shift from Market place to Market space

3.5 Driving Forces of e-Commerce

Today’s business environment is creating pressures on organisations and EC is one

response organisations are putting up in order to raise entry barriers, create competitive

edge and stay afloat. Market, economical, societal and technological factors are creating

a highly competitive business environment in which the consumer is the focal point.

Furthermore, these factors change quickly, sometimes quite unpredictably and

companies need to react frequently and quickly to both problems and opportunities

resulting from the new business environment (Drucker 1999). Because the pace of

change and the degree of uncertainty in tomorrow’s competitive environment are

expected to accelerate, organisations will be operating under increasing pressures to

produce more and faster with fewer resources.

e-Commerce in Commercial Banks in Zimbabwe Page 25

3.5.1 Business Pressures and Organisational Responses

Boyett and Boyett (1995) depict this change in the business environment using a set of

business pressures or drivers. (See Table 3-3)

Market and

economic pressures

Strong competition

Global economy

Regional trade agreements

Extremely low labor cost in some countries

Frequent and significant changes in markets

Increased power of consumers

Societal and

environmental pressures

Changing nature of workforce

Government deregulation of banking and other services

Shrinking government budgets subsides

Increased importance of ethical and legal issues

Increased social responsibility of organizations

Rapid political changes

Technological pressures

Rapid technological obsolescence

Increase innovations and new technologies

Information overload

Rapid decline in technology cost Vs. performance ratio

Table 3-3 Major Business Pressures

In order to succeed in such a dynamic world, companies must take not only critical

response activities but also innovative activities such as customising products, creating

new products and providing superb customer services. Critical response activities

include lowering of costs and closing unprofitable business units. These activities can be

performed in some or all of the business processes of the organisation from daily routine

payroll processing and order entry to strategic acquisition of a company. They can also

occur in the extended supply chain where the company interacts with its suppliers,

customers and other partners.

e-Commerce in Commercial Banks in Zimbabwe Page 26

Figure 3-3 Impact of IT on the Organisation

Organisational Responses

A response can be a reaction to a pressure already in existence or it can be an

initiative that will defend an organisation against future pressures. It can also be an

activity that exploits an opportunity created by changing conditions. Many response

activities can be greatly facilitated by EC and in some cases EC is the only solution to

these problems.

The Scott-Morton and Allen framework (DSS Revisited for the 1990s (1986)) depicted in

Figure 3-4 models organisations into five components that operate in equilibrium with

each other and the surrounding environment.

As soon as significant changes occur in any one or more of the components or in the

environment, the organisation becomes unstable and adjustment in the other

components becomes necessary for survival. For example a significant change in the

Management

and

Business Process

Organization

Structure and the

Corporate Culture

Individual

and Roles

Information

Technology

The Organization’s

Strategy

External Environment,

Social, Economic,

Political, etc

e-Commerce in Commercial Banks in Zimbabwe Page 27

organisational strategy may create a change in corporate structure and similarly,

introduction of EC either in the environment by a competitor or internally also produces

change.

Organisations’ major responses are divided into five categories:

Strategic systems for competitive advantage

Continuous improvement efforts

Business process reengineering

Business alliances

E-Commerce

i) Strategic systems for competitive advantage

Strategic systems provide organisations with strategic advantages enabling them to

increase their market share, better negotiate with their suppliers, or prevent their

competitors from eating into their territory. EC supports a variety of strategic systems e.g

FedEx overnight delivery system that allows the company to track the status of every

package anywhere in the system. The system started off being used internally, then it

was moved to the Internet and now they are introducing new activities such as web page

and catalogue hosting.

ii) Continuous improvement efforts

Many companies continuously conduct innovative programs in an attempt to improve

their productivity, and quality e.g Dell computers accept orders electronically and move

them via the SAP enterprise resource planning system into the just-in-time assembly

operations. However, continuous improvement programs may not be adequate in all

occasions and business pressures may require radical change. Such an effort is referred

to as Business Process Reengineering.

e-Commerce in Commercial Banks in Zimbabwe Page 28

iii) Business process reengineering

This refers to major innovation in the organisational structure and the way it conducts the

business. According to Hammer and Champy (1993), technological, human and

organisational dimensions of a firm may all be changed in BPR initiatives.

iv) Business alliances

Business alliances are best illustrated by interorganisational systems where companies

benefit from close links with their suppliers (via extranets) and clients via the Internet.

There are several types of alliances such as sharing of resources, establishing

permanent supplier-company relationships and creating joint research efforts. Virtual

corporations are exemplified by joint ventures which are a temporary coming together of

two or corporation for a specific mission, limited time mission. Such alliances are

supported by EC technologies ranging from EDI to electronic transmission of maps and

drawings.

v) E-Commerce

Information technology can be used to underpin an organisation’s response to business

pressures and EC can be the ultimate goal in effecting changes in all the areas of

business.

3.6 E-Commerce Spectrum

According to Choi et al (The Economics of Electronic Commerce, 1997), e-Commerce

can take many forms depending on the degree of digitisation of the product/service sold,

the business process and the delivery agent (Figure 3-3). A product can be physical or

digital, an agent can be physical or digital, and the process can be physical or digital.

These create eight cubes each of which has three dimensions. In traditional commerce,

all dimensions are physical (lower left cube) and in pure EC, all dimensions are digital

(upper right cube). All the other cubes are a mix of digital and physical dimensions and if

e-Commerce in Commercial Banks in Zimbabwe Page 29

there is at least one digital dimension, the situation can be considered EC albeit not a

pure one e.g. paying for groceries using a debit card in a supermarket is not pure

because the goods are physical and only the delivery agent is electronic.

Physical

agent

Digital

agent

Digital

Product

Physical

Product Physical process

Digital process

Virtual process

Virtual delivery agent

Vir

tual

pro

du

ct

Electronic

commerce areas

The core of

electronic commerce

Traditional

commerce

Figure 3-4 Dimensions of e-Commerce (Choi et al, 1997)

3.6.1 Classification of EC Activities

Turban et al (2000) divide e-Commerce activities into three categories:

i) Electronic markets where goods and services are bought and sold

A market is a network of interactions and relationships where information, products and

services are exchanged. When the market is electronic, the business centre is not a

physical building but rather network-based location where business interactions occur.

Senn (1996) identifies some distinctive features of electronic markets as follows:

e-Commerce in Commercial Banks in Zimbabwe Page 30

a. There are two types of relationships between the customer and the seller. The

first one is where the customer/seller linkage is established at the time of

transaction and may be for one transaction only. The second one is where a

customer/seller purchase agreement is established whereby the seller agrees

to deliver goods and services to the customer for a definite period e.g.

subscription transaction for magazines.

b. Electronic markets are typically built around publicly accessible networks.

When outside communications companies are involved, they are typically

online service providers which function as market makers.

c. Sellers determine, in conjunction with the market maker which business

transactions they will provide.

d. Customer and sellers independently determine which communication networks

they will use in participating in an electronic market. The network used may

also vary from transaction to transaction.

ii) Interorganisational systems

Interorganisational systems (IOS) facilitate inter and intra-organisational flow of

information, communication and collaboration. The major objective is efficient

transaction processing such as transmitting orders, bills and payments using EDI or

extranets. According to Senn (1996), all relationships are predefined and there is no

negotiation, just execution. Advance arrangements result in agreements in nature and

format of business transactions and documents. This can be contrasted with electronic

markets where buyers and sellers negotiate, submit bids, agree on an order and finish

the execution on or offline. An IOS encompasses several business partners, typically a

company, its suppliers and/or its customers, and it may be built around private networks.

Types of IOS include:

EDI – which provides secure business-to-business connection over networks.

e-Commerce in Commercial Banks in Zimbabwe Page 31

Extranets which provide B2B connection over the Internet

Electronic funds transfer

Electronic forms

Integrated messaging – delivery of email and fax documents through a single

electronic transmission system that can combine EDI, email and electronic forms.

Shared databases – information stored in repositories is shared between trading

partners and is accessible to all.

Supply chain management which is co-operation between a company and its

suppliers and/or its customers regarding demand forecasting, inventory

management and order fulfilment. Well known examples include Dell, the

computer manufacturer and the largest retail chain Wall Mart.

iii) Customer service

These are systems which use EC to provide a better service to clients e.g with

FedEx Internet based package tracking system, clients can log on and find out the

status of their package and electronic communications brings with it many

conveniences and efficiency. Through ATMS, banks provide some banking services

virtually all the time (24x7x365 – 24 hours per day, 7 days a week and 365 days per

year). Intelligent agents can answer standard e-mail questions in seconds and

human experts service can be expedited using help desk software.

E-Commerce can also be classified by the nature of transactions:

i) Business-to-Business

Most of EC today is this type and it includes IOS transactions and electronic markets

between organisations. This is accomplished through either vertical or horizontal

portals. Vertical portals offer a service of product to a single industry type, while

horizontal portals offer a service or product across multiple industries.

e-Commerce in Commercial Banks in Zimbabwe Page 32

ii) Business-to-Consumer

These are retailing transactions with individual shoppers e.g Amazon.com

iii) Consumer-to-Consumer

In this category, consumers sell directly to each other e.g at MSN e-Shop you get

cars and residential property sales. Auction sites allow consumers to put up items for

sale and other consumers bid for them. Many individuals are also using intranets and

other organisational networks to advertise items for sale or services.

iv) Consumer-to-Business

Individuals who sell goods and services to organisations are included in this

category.

v) Business-to-Government

An enterprise services the needs of Government and its agencies.

vi) Government-to-business

Government interacts with businesses through government portals.

vii) Nonbusiness EC

An increasing number of organisations such as academic institutions, not for profit

organisations, religious organisations, social organisations and government agencies

are using various types of EC to reduce their expenses or to improve operations and

customer service.

viii) Intrabusiness (organisational)

This category includes all internal organisational activities, usually performed on

intranets, that involve exchange of goods, services, or information. Activities vary

from selling corporate products to employees to online training and cost reduction

activities.

e-Commerce in Commercial Banks in Zimbabwe Page 33

3.7 E-Commerce perspectives

Kalakota and Whinston (1997) define EC from the following perspectives:

Communications

Business process, and

Service.

3.7.1 Communications perspective

From a communications perspective, EC is the delivery of information, products/services

or payments over telephone lines, computer networks or any other electronic means.

Integrating technology into the business is not as simple as it may seem. Integration

means the organisation must have a seamless set of applications that must work fluidly

not only at the customer and supply chain interface but also internally to support the

business processes.

Infrastructure which supports e-Commerce has five components:

Common business services infrastructure which includes security smart cards,

authentication, electronic payments and directories/catalogues.

Messaging and information distribution infrastructure which encompasses

electronic data interchange (EDI), email, and hypertext transfer protocol (http)

Multimedia content and network publishing infrastructure which includes Java,

HTML, World wide web (www) and VRML.

Network infrastructure (LAN, WAN, Intranet, extranet) which includes all

communications modes (wireless, cable television, telecom and Internet.)

Interfacing infrastructure to databases, customers and applications.

Organisations or individuals intending to be part of the e-Commerce revolution need to

invest in information technology infrastructure with some or all of the components

e-Commerce in Commercial Banks in Zimbabwe Page 34

described above. The role an organisation or individual wants to play in e-Commerce

will determine the infrastructure required.

3.7.2 Business process perspective

The business perspective is the application of technology toward the automation of

business transactions and workflow. As organisations move towards varying degrees of

e-commerce activities, the internal business process must necessarily change to adapt

to the new business models and markets. Indeed E-Commerce can be viewed as an

agent or catalyst for business process reengineering (BPR). This refers to major

innovation in the organisational structure and the way it conducts the business.

According to Hammer and Champy (1993), technological, human and organisational

dimensions of a firm may all be changed in BPR initiatives. The major areas in which e-

Commerce supports BPR include:

Reduction of cycle (business process) time and time to market

Reduction of the time taken to carry out a business process is important in raising

productivity and competitiveness. Similarly, reducing the time from inception of an

idea to its implementation (time to market) is important because those who are first

with a product or service on the market can enjoy distinct advantages that can be

sustainable over time.

Empowerment of employees and collaborative work

Empowerment is related to the concept of self-directed teams where employee are

given authority to act and make decisions on their own. Technology allows

decentralisation of decision making but at the same allowing for centralised control.

Knowledge management

Using the medium of intranets and the Internet, employees can access the

organisation’s know-how and thereby increase productivity.

e-Commerce in Commercial Banks in Zimbabwe Page 35

Customer focused approach

Companies are increasingly becoming customer oriented i.e. they must pay more

attention to their customer needs in order to secure repeat orders and win new

customers based on reputation.

Business alliances

These alliances have brought tremendous benefit to companies particularly

through supplier chain management.

3.7.3 Service perspective

From the service perspective, EC is a tool that addresses the desire of firms, consumers

and management to cut service costs while improving the quality of goods and

increasing the speed of delivery. The three points on which customers are won or lost

can be summarised under one word – service. Service is the embodiment of mainly

convenience for the customer, speed of delivery of product or service and

personalisation of the whole business transaction.

Consumer business – Selling Chain Management

Selling chain management is streamlining the sales process so that customers get what

they want, how they want it in the shortest possible time. SCM is an integrated approach

and involves viewing the whole selling process through the customer’s eyes, e.g a

customer can custom order a Compaq machine and have it shipped.

Supply Chain Mgmt and selling chain mgmt (SCM)

SCM is a series of companies, linked together and supplying parts, materials and

services to others in the chain.

Types of supply chains –

Responsive supply chain – respond quickly to a customer’s needs. An important

attribute of this is the available-to-promise factor. Businesses need to know what

e-Commerce in Commercial Banks in Zimbabwe Page 36

resources are available before delivery date is promised. Available to promise

systems provide a system wide real-time look across the entire supply chain to show

what is available and if it can be delivered on time.

Enterprising supply chains are able to be quickly reconfigured to respond to

customer demands. Businesses on the chain must look forward and must be able to

make the appropriate changes.

3.7.4 On-line perspective

From the online perspective, EC provides the capability of buying and selling products

and information on the Internet and other online services.

3.8 Electronic Commerce In Service Industries

According to the EC classification along three dimensions (Section 4.4), pure EC is

impossible where physical goods are involved and when they have to be transported

from the supplier to the consumer. The service industry provides the best opportunity for

pure EC and hence we find the potential for the greatest benefit as costs are reduced to

a minimum along all three dimensions.

Service industries are characterised by intermediation where an agent or broker

provides a link between suppliers of a good or service and consumers with a need.

Examples include magazine agents, insurance brokers, travel agents, stock brokers and

banks. Electronic commerce provides customers with an opportunity to have direct

access to providers of services or to superagencies. This is because most of the value

added tasks can be automated and as more people use EC, most of the different types

of brokers will be eliminated by technology.

The technology is also creating superagencies which provide products and services

through portals.

e-Commerce in Commercial Banks in Zimbabwe Page 37

3.8.1 EC in Banking

Electronic banking, also known as cyberbanking, virtual banking, home banking and

online banking, includes various banking activities conducted from home, business or on

the road instead of at the physical bank. Electronic banking saves time and money for

users. It offers banks an inexpensive alternative to branch banking and a chance to

enlist remote customers. The extent of automation of banking services depends on the

individual bank strategy and the constraints imposed by the environment on any EC

initiative.

Some advantages of electronic banking are:

Obtain account information any time e.g. statement showing transactions and

account balance

Pay bills e.g. water, electricity, insurance premiums and telephone accounts

Transfer money between accounts

Handle finances even when travelling

Additional services – banks typically offer incentives for customers to sign onto

online baking due to the significant cost reduction that results.

E-banking offers several benefits both to the bank and to its customers such as

expanding the customer base and saving the cost of paper based transactions.

3.9 EC Strategy Implementation

Successful EC initiatives do not happen spontaneously. A study of the executives of

successful EC companies shows them to be strategic thinkers who plan and focus on

the customers, markets and competitive positioning.

3.9.1 Planning

In his book e-Commerce: Formulation of Strategy, RT Plant quotes a research he

carried out which revealed that:

e-Commerce in Commercial Banks in Zimbabwe Page 38

Most companies have recognised that they need to create and execute an e-

Commerce strategy; however as they look for a strategy to follow, they find none,

especially for players in traditional industries. To blindly follow the strategy of new

Internet stars such as Amazon is impossible and can be dangerous.

Some companies still feel they can largely ignore the Internet and that they can

get away with it by offering token web sites with basic product offering and email

facilities only.

Other companies, however, have recognised some of the drivers in e-Commerce

and have adopted some of them to the exclusion of the others, e.g. positioning

themselves to have a low-cost Internet customer service position. This lack of

balance between service, branding, technology and marketing can be

detrimental.

Some organisations are winning the battle for the Internet market space and are

creating adaptive, intelligent solutions that will keep them ahead of the

competition, build successful barriers to entry against insurgents and allow them

to create new empires as the slow giants of the old economy fight to change

course and pick up steam.

Businesses are finding that the boundaries of strategic thinking, and of

competition have vastly expanded. The challenge is to keep up with the rapid

growth in converging technologies and to translate the potential of these

technologies into business vision and dynamic competitive strategy.

To be effective, an e-Commerce strategy has to be integrated with the strategic

vision of the company as a whole. However, the approach to the creation of an

effective e-Commerce strategy is not always clear. Classic examples of success

are visible (Amazon, eBay and America On Line) but these are new organisations

e-Commerce in Commercial Banks in Zimbabwe Page 39

born on the Internet and the question is if you are a traditional industry player,

how do you proceed ?

A generic EC strategic cycle is given in Fig 3-5 below:

Industry and Competitive analysis

Strategy formulation

Implementation

Performance assessment

Strategy reassessment

Figure 3-5 EC Strategic Cycle

3.9.2 Critical Success Factors

Critical success factors (CSFs) are the indispensable business, technology, and human

factors that help to achieve the desired level of organisational goals. The major CSF’s

are as follows:

Identify the specific products and services to be traded

Top management support

Project team reflecting various functional areas

Technical infrastructure

e-Commerce in Commercial Banks in Zimbabwe Page 40

Customer acceptance

User friendly web site interface

Integration with the corporate legacy systems

Security and control of EC systems

Competition and market situation

Pilot project and corporate knowledge

Promotion and internal communication

Cost

Level of trust between buyers and sellers.

3.9.3 Moving to the Internet

Organisations can be classified into three categories as they craft our their e-Commerce

strategies:

i) New organisations born on the Internet in the e-Commerce market space, e.g

Amazon and eBay

ii) Established organisations traditionally positioned in the off-line market space

and are now moving to the net.

iii) Those organisations coming together in a new organisational form – e-

consortia – whose aim is to leverage the unique strengths associated with each

company and partner through virtual structure of an offline organisation.

Although industry growth and competition in the new Internet sector is fast and furious, it

still appears that the traditional paths to and tenets of success are still valid even in this

new economic model. The primary factor is, as always, product and market vision.

Corporate strategy has two components: formulation of a winning conceptual strategy

and delivery of an executable or operational strategy. Conceptual strategy for the new e-

Commerce sector can itself be broken down into two types:

e-Commerce in Commercial Banks in Zimbabwe Page 41

i) A company attempting to create an entirely new product or service concept

such as America On Line, and

ii) A company attempting a new execution of an existing product or service

previously available to the market in an online form, such as e-Bay, which, via

the Internet, delivers an ancient transactional method of trade, that of an

auction house.

Differentiation in the new e-commerce sector is the key to success, and the degree to

which this affects success is remarkable.

3.9.4 Pillars of Success

Four pillars have been confirmed: technology, marketing, service and branding.

Technology

An organisation must understand what the total technology implications are for

the organisation. They need to know whether their operations are aligned to an

Internet based technology based or not. Customer understanding is also

important – how they view and use technology within the marketspace. This

knowledge will be leveraged to build an effective infrastructure that facilitates an

agile and flexible EC strategy.

Market

Organisations must understand what the implications of EC and technology are

for the marketspace in which the organisation is to compete in terms of branding

and relationship management. Considerations must include whether its target

market is the same as its traditional bricks-and-mortar marketspace, and if its

core marketspace has moved, whether it is still realistically open to traditional

organisations moving to the net. Lastly, organisations must understand how the

market is going to segment and grow over the near future due to the impact of

e-Commerce in Commercial Banks in Zimbabwe Page 42

the Internet and must determine whether the organisation will be able to move

rapidly enough to meet those changing needs.

Service

An organisation must determine the new service level expectations of the

customer. It is important to understand what the customers’ new value

proposition requirements are in terms of cost, service level expectations and

information-based service. The value chain must be assessed to provide

answers to such questions as:

- how are we going to acquire customers ?

- how are we going to develop customer relationships through the new

medium ?

- how can we best fulfil the customers’ needs online ?

- how do we retain customers ?

Brand

Organisations need to determine how to best leverage their existing brand by

answering the following questions:

- do we have the ability to create a strong dot.com brand ?

- what is the basis of the brand ?

- what are the implications for our brand in terms of technology we employ,

develop or use ?

- what are the challenges for creating a new dot.com brand ?

- does the Internet demand an amendment or a completely new service

proposition ?

- will new brand positioning change our existing brand ?

In addition to these four pillars, three dimensions (bonding factors) also play a role in the

determining the success of EC strategies: