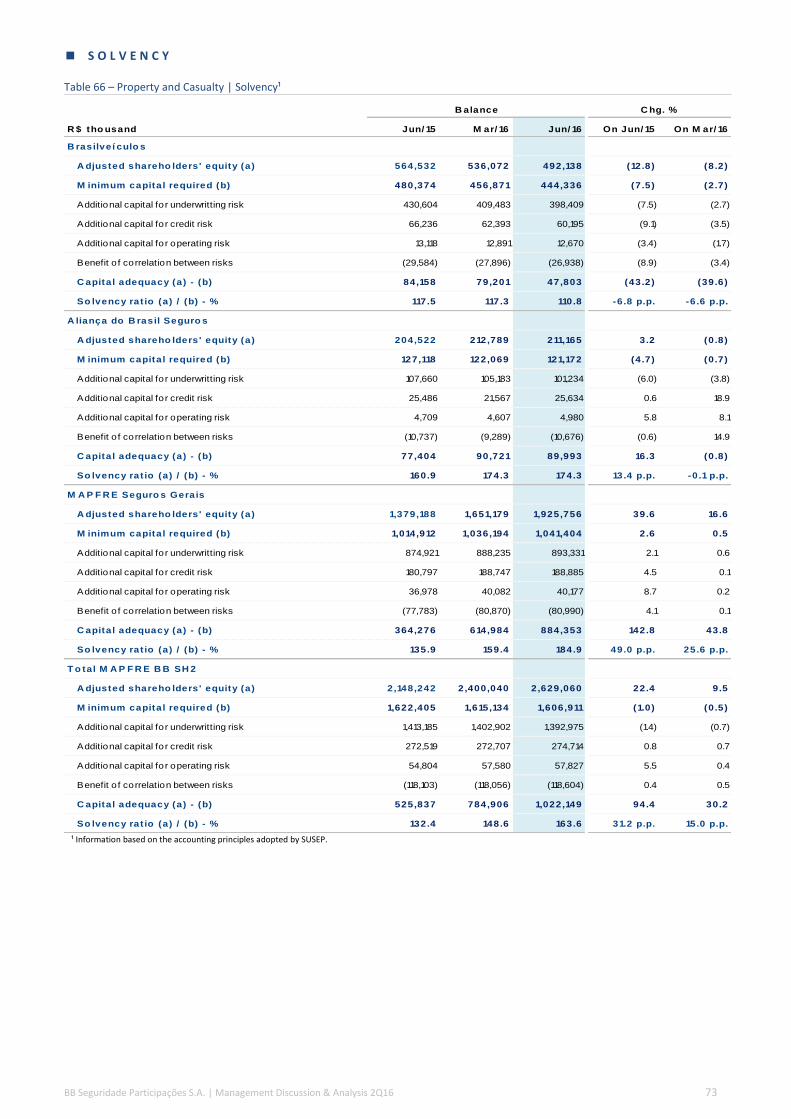

md&a - bb · Índice de comissionamento % 23.1 23.8 22.7 23.1 22.6 Índice de despesas gerais e...

TRANSCRIPT

2Q16

MD&A BB Seguridade Participações S.A

P R E S E N T A T I O N

The Management Discussion and Analysis – MD&A presents the economic and financial status of BB Seguridade Participações S.A. (BB

Seguridade). Directed to financial analysts, shareholders and investors, this quarterly report provides an analysis of economic and

financial indicators of BB Seguridade’s, stocks performance and other aspects considered relevant for the assessment of the company’s

performance.

Back to November 2012, Banco do Brasil S.A. (BB) announced its intention to create BB Seguridade, a wholly owned subsidiary

responsible for consolidating, under a single holding company all activities related to insurance, open-end private pension plans,

premium bonds, brokerage, and other. In the same document, BB disclosed its intention to promote an IPO of the holding company BB

Seguridade at BM&FBovespa S.A. – Bolsa de Valores, Mercadorias e Futuros.

The bookbuilding of the aforementioned public offering was concluded on April 25th

, 2013 and the price was set at R$17.00 per share.

The shares started being traded on April 29th

, 2013. In the offering, the controlling shareholder (Banco do Brasil) sold 675 million shares,

in a transaction that involved approximately R$11.5 billion, with 500 million shares sold in the base offering, 100 million in the hot issue,

and 75 million in the greenshoe. The announcement of the offering closing was published on May 17th

, 2013.

The consolidated financial statements were prepared in compliance with the International Financial Reporting Standards – IFRS.

All the analyses in this report are based on IFRS Financial Statements, but are occasionally supplemented by managerial data, besides

other information calculated based on accounting principles determined by the Superintendência de Seguros Privados – SUSEP (the

regulator of the insurance industry in Brazil).

O N - L I N E A C C E S S

This MD&A is available at BB Seguridade’s IR website, where additional information about the Company is also available such as:

corporate structure, corporate governance, historical series for download, among other important information for shareholders and

investors. The company’s website can be accessed through either http://www.bancodobrasilseguridade.com.br.

This report makes references and statements about growth estimates, earnings forecasts and future strategies regarding BB Seguridade. Such statements are based on current expectations, estimates and projections of the Management about future events and financial trends that may affect the businesses that the Group is involved in.

These forward looking statements are not guarantees of future performance and involve risks and uncertainties that could overextend the control of the management, and thus can result in balances and values different from those anticipated and discussed in this report. The expectations and projections depend on market conditions (technological changes, competitive constraints on products, prices, etc.), on the country’s macroeconomic performance (interest and exchange rates, political and economic changes, inflation, changes in tax rules, etc.) and on international markets.

Future expectations based on this report should consider the risks and uncertainties that involve the businesses of BB Seguridade. BB Seguridade has no responsibility to update any estimate contained either in this report or in reports published previously.

Tables and charts in this report shows, in addition to the accounting balances, financial and managerial figures. The changes of relative rates are calculated before rounding procedure in R$ million. The rounding method used follows the rules established by Resolution 886/66 of IBGE’s Foundation: if the decimal number is equal or greater than 0.5, it increases by one unit, if the decimal number is less than 0.5, there is no increase.

2Q16 Earnings Conference Call

Index

1. Summary 5

2. Earnings Analysis 18

3. Balance Sheet Analysis 23

4. Underwriting and Accumulation 28

5. Distribution 105

6. Definitions 113

August 09th, 2016

Portuguese

Time: 10 am (Brasília time)

9 am (Eastern time)

Dial-in: Brazil +55-11-3137 8025

USA +1-786-837 9597

UK +44-20-3318 3776

Webcast: www.bancodobrasilseguridade.com.br

English

Time: 11:30 am (Brasília time)

10:30 am (Eastern time)

Dial-in: Brazil +55-11-3137 8025

USA +1-786-837 9597

UK +44-20-3318 3776

Webcast: www.bancodobrasilseguridade.com.br

Contacts

Investor Relations

+55 (11) 3066-9894

Rua Alexandre Dumas, 1671 – Térreo – Ala B Chácara Santo Antônio – São Paulo – SP CEP: 04717-903

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 5

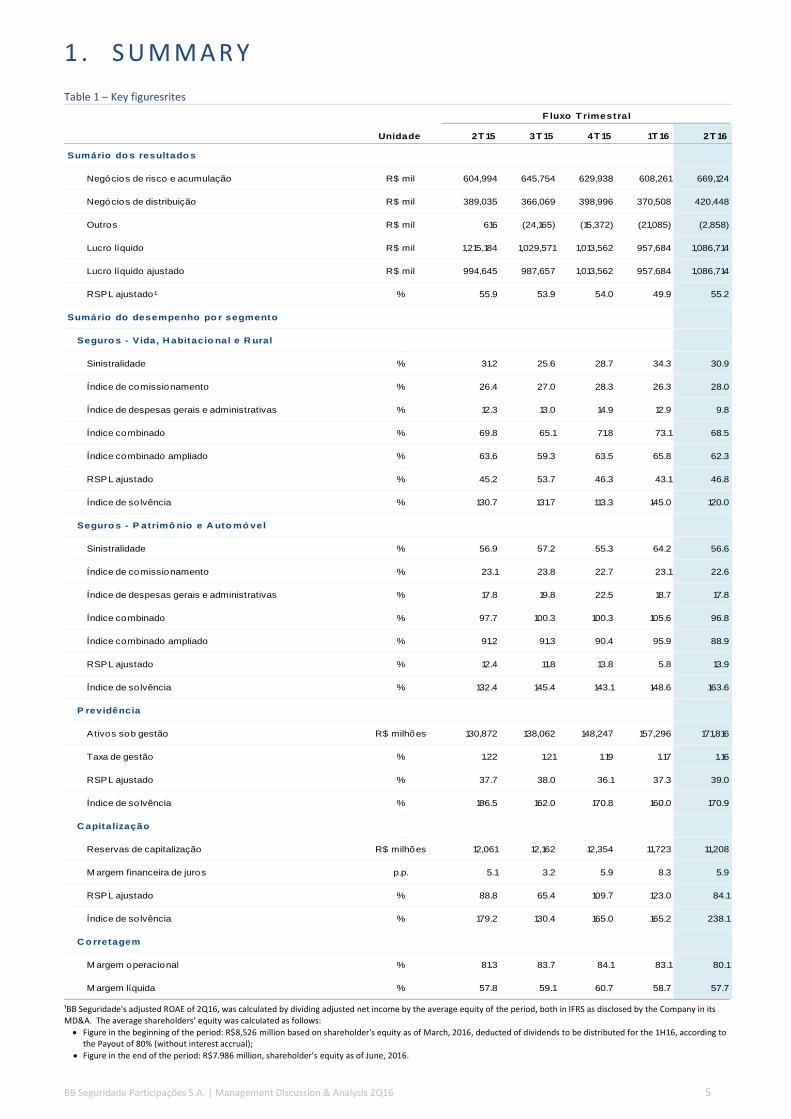

1 . S U M M A R Y

Table 1 – Key figuresrites

Unidade 2T 15 3T 15 4T 15 1T 16 2T 16

Sumário do s resultado s

Negócios de risco e acumulação R$ mil 604,994 645,754 629,938 608,261 669,124

Negócios de distribuição R$ mil 389,035 366,069 398,996 370,508 420,448

Outros R$ mil 616 (24,165) (15,372) (21,085) (2,858)

Lucro líquido R$ mil 1,215,184 1,029,571 1,013,562 957,684 1,086,714

Lucro líquido ajustado R$ mil 994,645 987,657 1,013,562 957,684 1,086,714

RSPL ajustado¹ % 55.9 53.9 54.0 49.9 55.2

Sumário do desempenho po r segmento

Seguro s - Vida, H abitacio nal e R ural

Sinistralidade % 31.2 25.6 28.7 34.3 30.9

Índice de comissionamento % 26.4 27.0 28.3 26.3 28.0

Índice de despesas gerais e administrativas % 12.3 13.0 14.9 12.9 9.8

Índice combinado % 69.8 65.1 71.8 73.1 68.5

Índice combinado ampliado % 63.6 59.3 63.5 65.8 62.3

RSPL ajustado % 45.2 53.7 46.3 43.1 46.8

Índice de so lvência % 130.7 131.7 113.3 145.0 120.0

Seguro s - P atrimô nio e A uto mó vel

Sinistralidade % 56.9 57.2 55.3 64.2 56.6

Índice de comissionamento % 23.1 23.8 22.7 23.1 22.6

Índice de despesas gerais e administrativas % 17.8 19.8 22.5 18.7 17.8

Índice combinado % 97.7 100.3 100.3 105.6 96.8

Índice combinado ampliado % 91.2 91.3 90.4 95.9 88.9

RSPL ajustado % 12.4 11.8 13.8 5.8 13.9

Índice de so lvência % 132.4 145.4 143.1 148.6 163.6

P revidência

Ativos sob gestão R$ milhões 130,872 138,062 148,247 157,296 171,816

Taxa de gestão % 1.22 1.21 1.19 1.17 1.16

RSPL ajustado % 37.7 38.0 36.1 37.3 39.0

Índice de so lvência % 186.5 162.0 170.8 160.0 170.9

C apitalização

Reservas de capitalização R$ milhões 12,061 12,162 12,354 11,723 11,208

M argem financeira de juros p.p. 5.1 3.2 5.9 8.3 5.9

RSPL ajustado % 88.8 65.4 109.7 123.0 84.1

Índice de so lvência % 179.2 130.4 165.0 165.2 238.1

C o rretagem

M argem operacional % 81.3 83.7 84.1 83.1 80.1

M argem líquida % 57.8 59.1 60.7 58.7 57.7

F luxo T rimestral

¹BB Seguridade's adjusted ROAE of 2Q16, was calculated by dividing adjusted net income by the average equity of the period, both in IFRS as disclosed by the Company in its MD&A. The average shareholders’ equity was calculated as follows:

Figure in the beginning of the period: R$8,526 million based on shareholder's equity as of March, 2016, deducted of dividends to be distributed for the 1H16, according to the Payout of 80% (without interest accrual);

Figure in the end of the period: R$7.986 million, shareholder’s equity as of June, 2016.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 6

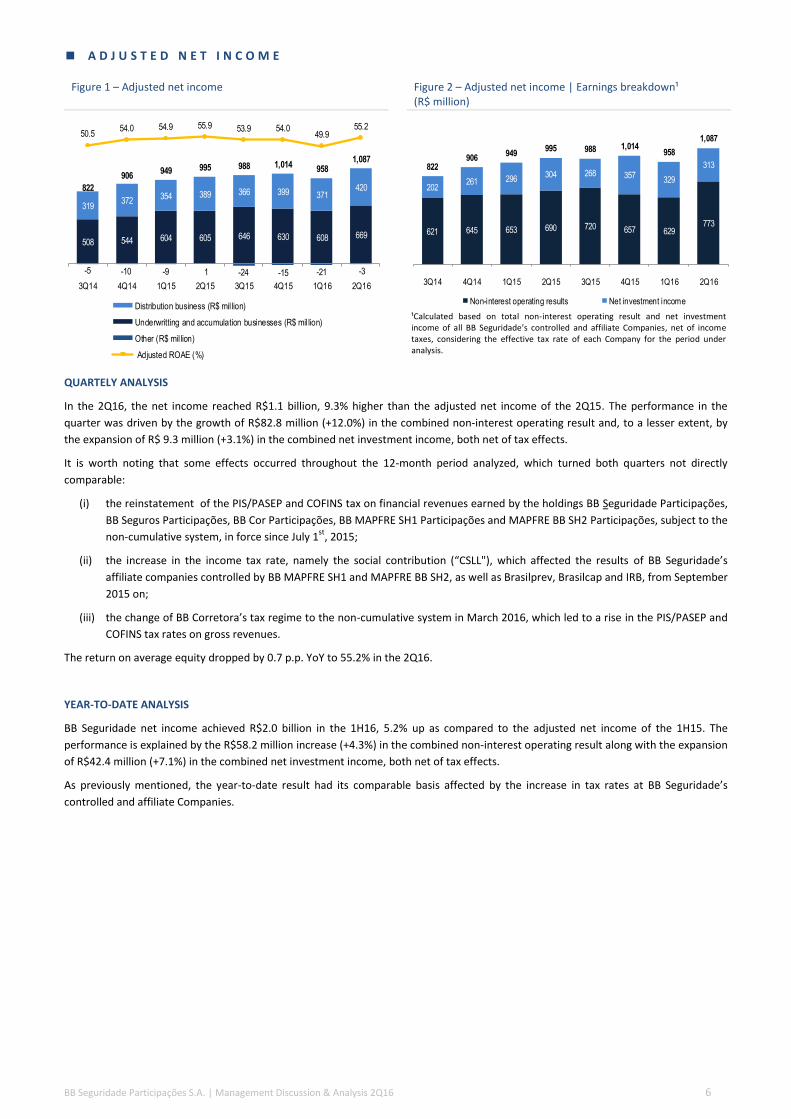

A D J U S T E D N E T I N C O M E

Figure 1 – Adjusted net income Figure 2 – Adjusted net income | Earnings breakdown¹ (R$ million)

-5 -10 -9 1 -24 -15 -21 -3

508 544 604 605 646 630 608 669

319372

354 389 366 399 371420822

906949 995 988 1,014

9581,087

50.554.0 54.9 55.9 53.9 54.0

49.955.2

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Distribution business (R$ million)

Underwritting and accumulation businesses (R$ million)

Other (R$ million)

Adjusted ROAE (%)

621 645 653 690 720 657 629773

202261 296

304 268 357329

313822906

949995 988 1,014

958

1,087

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Non-interest operating results Net investment income

¹Calculated based on total non-interest operating result and net investment income of all BB Seguridade’s controlled and affiliate Companies, net of income taxes, considering the effective tax rate of each Company for the period under analysis.

QUARTELY ANALYSIS

In the 2Q16, the net income reached R$1.1 billion, 9.3% higher than the adjusted net income of the 2Q15. The performance in the

quarter was driven by the growth of R$82.8 million (+12.0%) in the combined non-interest operating result and, to a lesser extent, by

the expansion of R$ 9.3 million (+3.1%) in the combined net investment income, both net of tax effects.

It is worth noting that some effects occurred throughout the 12-month period analyzed, which turned both quarters not directly

comparable:

(i) the reinstatement of the PIS/PASEP and COFINS tax on financial revenues earned by the holdings BB Seguridade Participações,

BB Seguros Participações, BB Cor Participações, BB MAPFRE SH1 Participações and MAPFRE BB SH2 Participações, subject to the

non-cumulative system, in force since July 1st

, 2015;

(ii) the increase in the income tax rate, namely the social contribution (“CSLL"), which affected the results of BB Seguridade’s

affiliate companies controlled by BB MAPFRE SH1 and MAPFRE BB SH2, as well as Brasilprev, Brasilcap and IRB, from September

2015 on;

(iii) the change of BB Corretora’s tax regime to the non-cumulative system in March 2016, which led to a rise in the PIS/PASEP and

COFINS tax rates on gross revenues.

The return on average equity dropped by 0.7 p.p. YoY to 55.2% in the 2Q16.

YEAR-TO-DATE ANALYSIS

BB Seguridade net income achieved R$2.0 billion in the 1H16, 5.2% up as compared to the adjusted net income of the 1H15. The

performance is explained by the R$58.2 million increase (+4.3%) in the combined non-interest operating result along with the expansion

of R$42.4 million (+7.1%) in the combined net investment income, both net of tax effects.

As previously mentioned, the year-to-date result had its comparable basis affected by the increase in tax rates at BB Seguridade’s

controlled and affiliate Companies.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 7

Figure 3 – Adjusted net income | Quarterly evolution breakdown (R$ million)

Figure 4 – Adjusted net income | Year-to-date evolution breakdown (R$ million)

995

83 9 1,087

2Q15 Adjusted netincome

Change in non-interestoperating result¹

Change in netinvestment income¹

2Q16 Adjusted netincome

¹Calculated based on total non-interest operating result and net investment income of all BB Seguridade’s controlled and affiliate Companies, net of income taxes, considering the effective tax rate of each Company for the period under analysis.

1,944

58 42 2,044

1H15 Adjusted netincome

Change in non-interestoperating result¹

Change in netinvestment income¹

1H16 Adjusted netincome

¹Calculated based on total non-interest operating result and net investment income of all BB Seguridade’s controlled and affiliate Companies, net of income taxes, considering the effective tax rate of each Company for the period under analysis.

U N D E R W R I T I N G A N D A C C U M U L A T I O N B U S I N E S S E S

Table 2 – Earnings analysis | Adjusted income statement

C hg. %

R $ tho usand 2Q15 1Q16 2Q16 On 2Q15 On 1Q16 1H 15 1H 16 On 1H 15

Equity inco me 1,001,759 966,901 1,089,192 8.7 12.6 1,958,003 2,056,092 5.0

Underwritting and accumulation businesses 604,994 608,261 669,124 10.6 10.0 1,208,958 1,277,385 5.7

Life, M ortgage Life and Rural 286,147 284,536 314,528 9.9 10.5 580,282 599,064 3.2

Property and Casualty 50,070 25,248 62,883 25.6 149.1 99,482 88,131 (11.4)

Pension Plans 157,150 167,105 181,388 15.4 8.5 322,192 348,493 8.2

Reinsurance 46,623 40,720 41,212 (11.6) 1.2 72,335 81,932 13.3

Premium Bonds 64,589 90,040 68,403 5.9 (24.0) 134,446 158,443 17.8

Dental Insurance 415 612 710 71.1 16.0 221 1,322 498.2

Distribution businesses 389,035 370,508 420,448 8.1 13.5 743,131 790,956 6.4

Other 7,730 (11,868) (380) - (96.8) 5,914 (12,249) -

G&A expenses (11,855) (20,005) (13,176) 11.1 (34.1) (23,569) (33,181) 40.8

Personnel expenses (10,137) (11,898) (10,330) 1.9 (13.2) (17,802) (22,228) 24.9

Administrative expenses (2,107) (2,139) (2,792) 32.5 30.5 (5,945) (4,931) (17.1)

Tax expenses (12) (5,974) (503) 3,938.9 (91.6) (485) (6,476) 1,234.1

Other operating income (expenses) 401 6 448 11.8 7,371.4 663 454 (31.5)

N et investment inco me 4,741 10,788 10,699 125.7 (0.8) 9,326 21,487 130.4

Financial income 4,741 48,997 10,699 125.7 (78.2) 36,284 59,696 64.5

Financial expenses - (38,209) - - - (26,958) (38,209) 41.7

A djusted net inco me 994,645 957,684 1,086,714 9.3 13.5 1,943,760 2,044,398 5.2

Quarterly F lo w C hg. % H alf -Yearly F lo w

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 8

E X T R A O R D I N A R Y E V E N T S

Table 3 – Earnings Analysis | Extraordinary events

C hg. %

R $ tho usand 2Q15 1Q16 2Q16 On 2Q15 On 1Q16 1H 15 1H 16 On 1H 15

A djusted net inco me 994,645 957,684 1,086,714 9.3 13.5 1,943,760 2,044,398 5.2

Extrao rdinary events 220,539 - - - - 220,539 - -

Brasilprev: reversal of provisions 220,539 - - - - 220,539 - -

N et inco me 1,215,184 957,684 1,086,714 (10.6) 13.5 2,164,299 2,044,398 (5.5)

Quarterly F lo w C hg. % H alf -Yearly F lo w

Brasilprev – Reversal of provision: in December 2014, pursuant to resolution CNSP nº 281/13 and SUSEP Rule 462/13, Brasilprev

recorded R$1.0 billion in reversals. The amount refers to the entire balance previously recorded in Provision for Insufficiency of

Contributions and Provision for Financial Fluctuation.

Simultaneously, Brasilprev conducted its half-yearly Liability Adequacy Test, based on financial statements of December 2014, in

compliance with SUSEP rule 457/12, and recorded R$514.1 million in Supplementary Coverage Provision (PCC).

The Liability Adequacy Test assesses the obligations arising from pension plan contracts and, when found insufficient technical

provisions, the company can adopt two alternatives:

the use of unrealized gains (strategy adopted until June 2014); or

the constitution of Supplementary Coverage Provision (strategy used in December 2014).

Until June 2014, Brasilprev had been using unrealized gains to offset possible insufficiency of technical provisions identified by the

Liability Adequacy Test. In December 2014, the deadline for reversal of Other Technical Provisions (where there were allocated the

balances of Provision for Insufficiency for Contributions and Provision for Financial Fluctuations), SUSEP has allowed the use of an

alternative forward yield curve structure, to minimize the inherent volatility of the original methodology. In this context, Brasilprev

chose to occasionally use the constitution of Supplementary Coverage Provision to offset the insufficiency of technical provisions

indicated by the December 2014 Liability Adequacy Test.

On the occasion of the Liability Adequacy Test, dated as of June 2015, and due to the volatility of the forward yield curve, Brasilprev,

supported by Paragraphs 2 and 3 of article 8th

of SUSEP Rule 457/12, re-adopted the procedure which employs the unrealized gains of

guaranteeing assets on technical provisions held to maturity to offset a possible insufficiency identified by the Liability Adequacy Test.

In this context, based on the Liability Adequacy Test, dated as of June 2015, the balance of R$514.1 million of Supplementary Coverage

Provision was fully reversed, with a positive impact of R$294.1 million in Brasilprev’s net income, equivalent to a net effect of R$220.5

million in BB Seguridade’s net income.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 9

BB MAPFRE SH1 | Life, Mortgage Life and Rural

Figure 5 – SH1 | Premiums written (R$ million) Figure 6 – SH1 | Adjusted net income and ROAE

1,553

2,175

1,542

1,867

2,094 2,098

1,497

2,097

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

288 287 277 287354

272 266317

75 80 115 95

104

129 113103

363 367392 382

457400 379

419

47.0 46.4 48.0 45.253.7

46.3 43.1 46.8

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Net investment income¹ (R$ million)

Non-interest operating result¹ (R$ million)

Adjusted ROAE (%)

¹Net of income taxes considering the Company’s effective tax rate for the period

under analysis.

QUARTELY ANALYSIS

The net income from Life, Mortgage Life and Rural business segment reached R$419.4 million in the 2Q16, 9.9% down YoY. The earnings

before taxes and profit sharing amounted to R$693.2 million, 16.3% higher YoY, justified by the improvement in the non-interest

operating result and in the net investment income.

In the 2Q16, premiums written amounted to R$2.1 billion, 12.3% higher YoY, boosted by the growth in rural insurance premiums

(+119.2%), mainly in crop insurance, and in life (+9.3%), partially offset by the drop in credit life premiums (-37.7%).

The combined ratio improved 1.3 p.p. YoY to 68.5% in the 2Q16. Such improvement was explained by the lower loss ratio in the life

segment in addition to the lower G&A ratio, partially offset by the increase in the commission ratio.

YEAR-TO-DATE ANALYSIS

The net income from Life, Mortgage Life and Rural business segment totaled R$798.9 million year-to-date, 3.2% up YoY. The earnings before taxes and profit sharing grew by 10.2%, driven by the increase in the underwriting result along with the evolution of the net investment income.

Premiums written amounted to R$3.6 billion, 5.4% higher YoY, boosted mainly by rural (+95.7%) and life (+10.0%).

The combined ratio deteriorated 1.2 p.p. to 70.9% in the 1H16, due to the increased loss ratio in credit life and in rural, in addition to

the higher commission ratio.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 10

MAPFRE BB SH2 | P&C

Figure 7 – SH2 | Premiums written (R$ million) Figure 8 – SH2 | Adjusted net income and ROAE

2,3632,203 2,121

2,325 2,4222,228 2,174

2,284

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

14-0.4

1 12-17 -17

-58

25

56 7298 89 116

136108

10171 71

99 10099

119

50126

9.5 9.312.6 12.4 11.8

13.8

5.8

13.9

3T14 4T14 1T15 2T15 3T15 4T15 1T16 2T16

Resultado financeiro¹ (R$ milhões)

Resultado operacional não decorrente de juros¹ (R$ milhões)

RSPL ajustado(%)

¹Net of income taxes considering the Company’s effective tax rate.

QUARTELY ANALYSIS

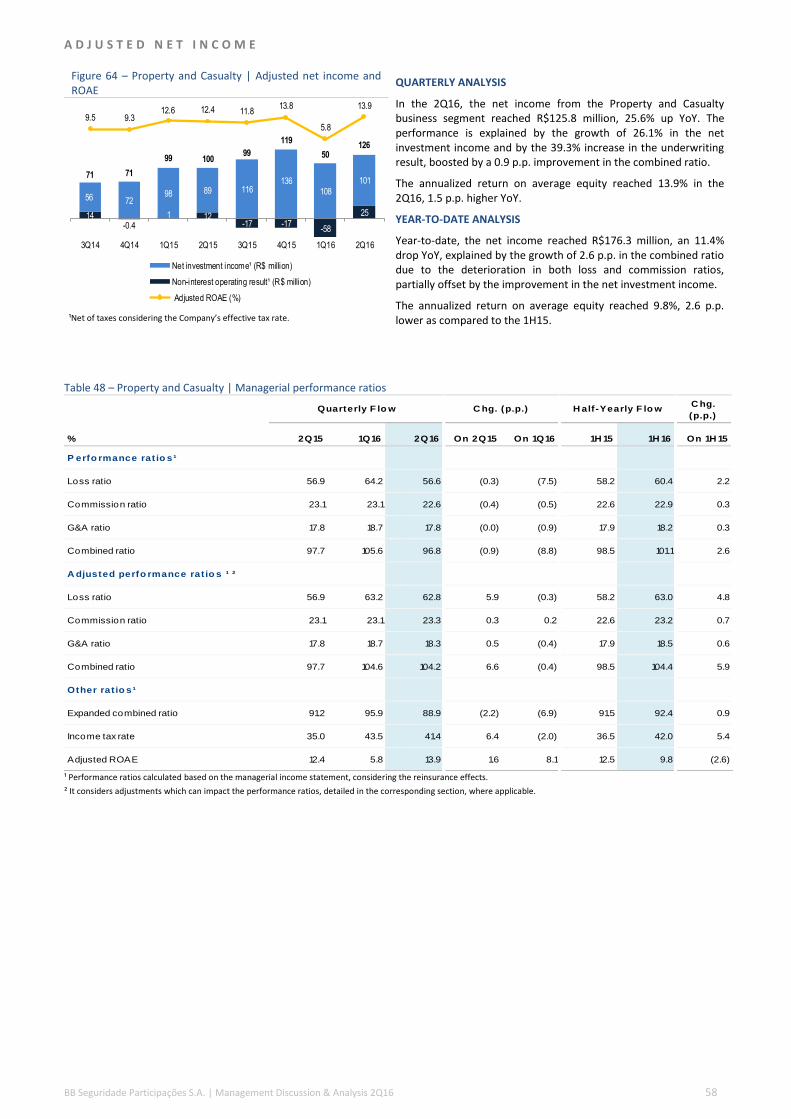

The net income from the P&C business segment amounted to R$125.8 million in the 2Q16, 25.6% up YoY. The performance is explained

by the 26.1% increase in the net investment income in addition to the 39.3% growth in the underwriting result, explained by the

improvement of 0.9 p.p. in the combined ratio, which was helped by the lower loss ratio as well as a lower commission ratio.

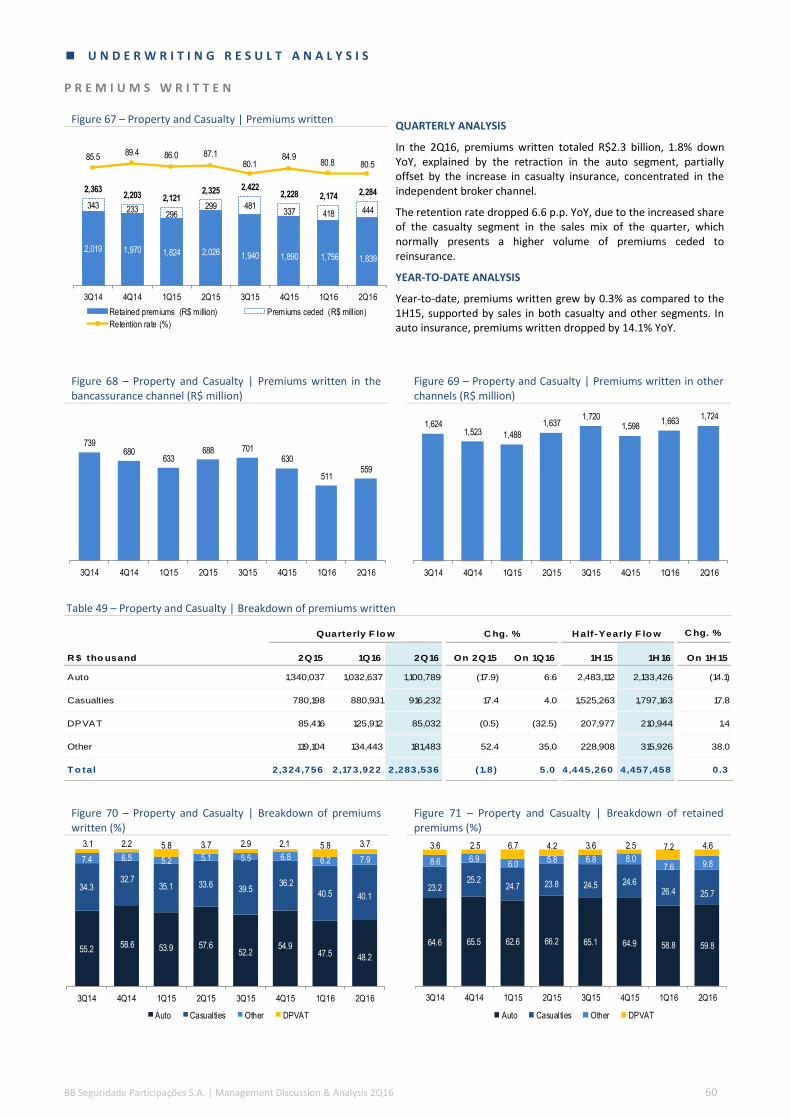

Premiums written amounted to R$2.3 billion in the 2Q16, 1.8% down YoY, dragged down by the auto insurance (-17.9%), partially offset

by the expansion of the casualty segment (+17.4%), concentrated in the independent broker channel.

YEAR-TO-DATE ANALYSIS

Year-to-date, the net income achieved R$176.3 million, 11.4% down YoY. The performance is explained by the 2.6 p.p. deterioration in

the combined ratio, due to worsen loss and commission ratios, partially offset by the better net investment income.

In the 1H16, premiums written grew by 0.3% YoY, supported by the sales from casualty and from the segment other. In auto, premiums

written dropped by 14.1% YoY.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 11

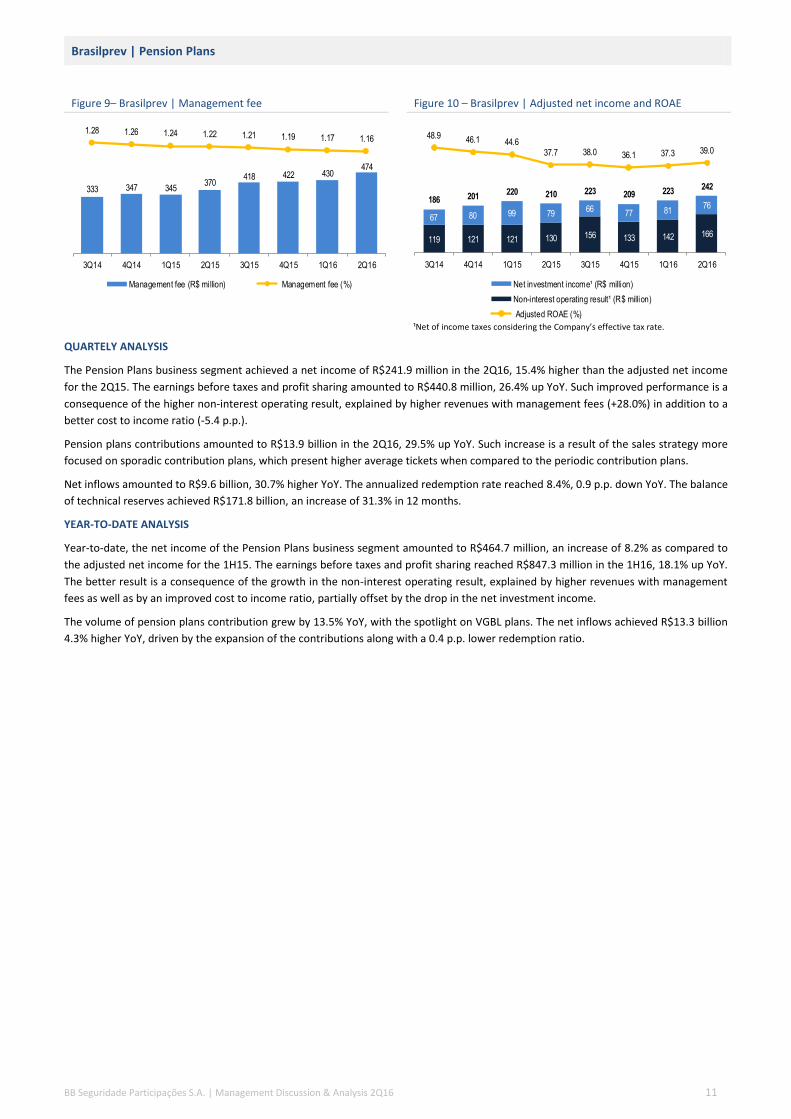

Brasilprev | Pension Plans

Figure 9– Brasilprev | Management fee Figure 10 – Brasilprev | Adjusted net income and ROAE

333 347 345370

418 422 430474

1.28 1.26 1.24 1.22 1.21 1.19 1.17 1.16

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Management fee (R$ million) Management fee (%)

119 121 121 130 156 133 142 166

67 80 99 7966

77 8176

186 201220 210 223 209 223

242

48.9 46.1 44.637.7 38.0 36.1 37.3 39.0

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Net investment income¹ (R$ million)

Non-interest operating result¹ (R$ million)

Adjusted ROAE (%) ¹Net of income taxes considering the Company’s effective tax rate.

QUARTELY ANALYSIS

The Pension Plans business segment achieved a net income of R$241.9 million in the 2Q16, 15.4% higher than the adjusted net income

for the 2Q15. The earnings before taxes and profit sharing amounted to R$440.8 million, 26.4% up YoY. Such improved performance is a

consequence of the higher non-interest operating result, explained by higher revenues with management fees (+28.0%) in addition to a

better cost to income ratio (-5.4 p.p.).

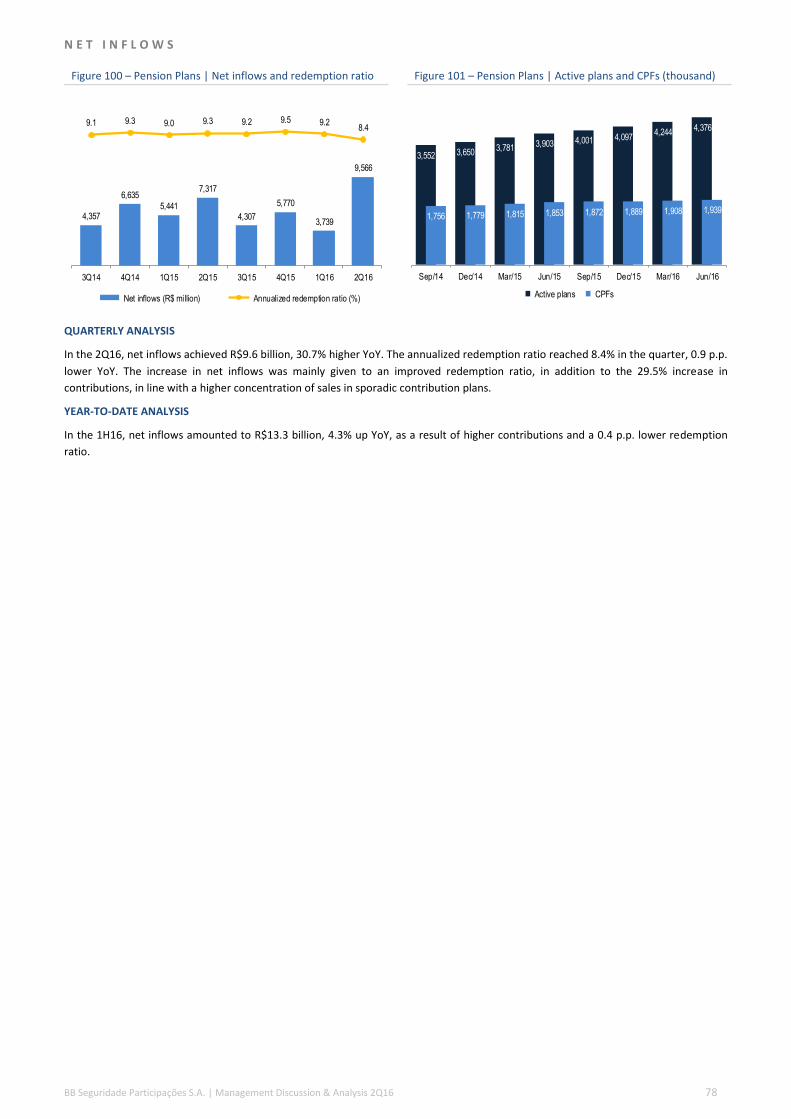

Pension plans contributions amounted to R$13.9 billion in the 2Q16, 29.5% up YoY. Such increase is a result of the sales strategy more

focused on sporadic contribution plans, which present higher average tickets when compared to the periodic contribution plans.

Net inflows amounted to R$9.6 billion, 30.7% higher YoY. The annualized redemption rate reached 8.4%, 0.9 p.p. down YoY. The balance

of technical reserves achieved R$171.8 billion, an increase of 31.3% in 12 months.

YEAR-TO-DATE ANALYSIS

Year-to-date, the net income of the Pension Plans business segment amounted to R$464.7 million, an increase of 8.2% as compared to

the adjusted net income for the 1H15. The earnings before taxes and profit sharing reached R$847.3 million in the 1H16, 18.1% up YoY.

The better result is a consequence of the growth in the non-interest operating result, explained by higher revenues with management

fees as well as by an improved cost to income ratio, partially offset by the drop in the net investment income.

The volume of pension plans contribution grew by 13.5% YoY, with the spotlight on VGBL plans. The net inflows achieved R$13.3 billion

4.3% higher YoY, driven by the expansion of the contributions along with a 0.4 p.p. lower redemption ratio.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 12

Brasilcap | Premium Bonds

Figure 11 – Brasilcap | Collections (R$ million) Figure 12 – Brasilcap | Net income and ROAE

1,396

2,028

1,321

1,961

1,379

1,856

1,043

1,571

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

30 44 29 27 28 19 18 25

4454 75 69

4189

11778

74

98 10597

68

109

135

103

85.1102.3 102.6

88.865.4

109.7 123.0

84.1

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Net investment income¹ (R$ million)

Non-interest operating results¹ (R$mill ion)

ROAE (%)

¹Net of income taxes considering the Company’s effective tax rate.

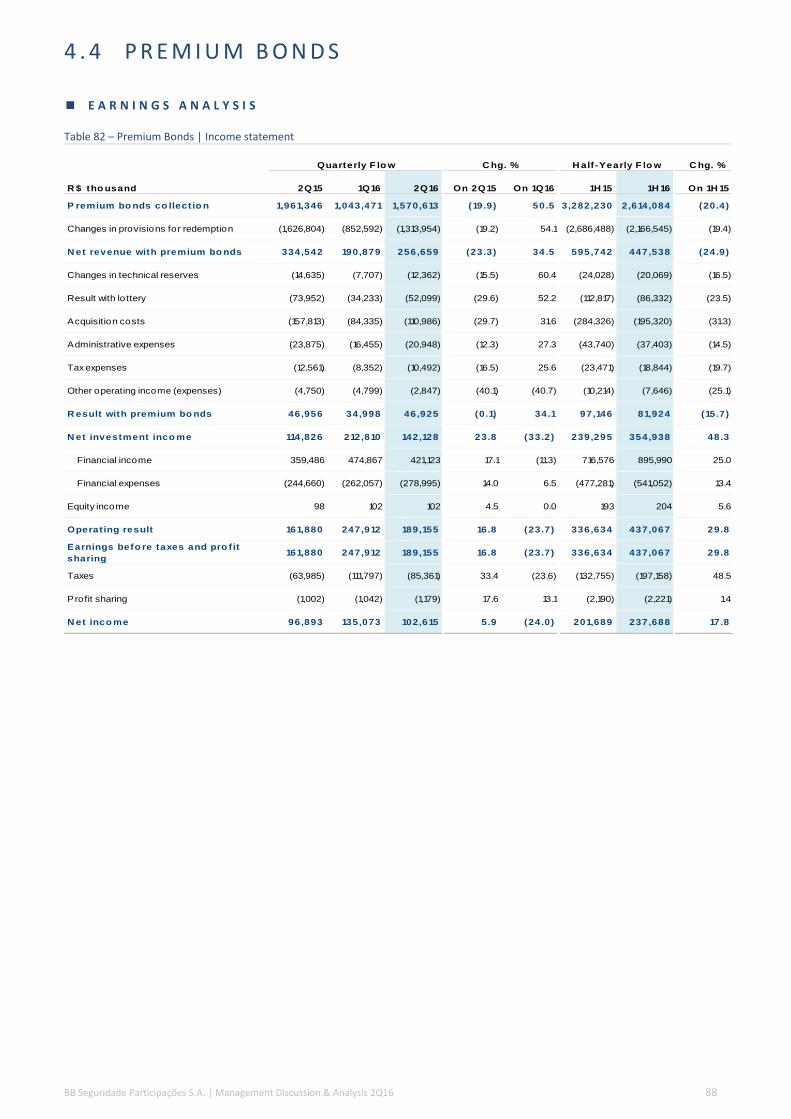

QUARTELY ANALYSIS

In the 2Q16, the net income for the Premium Bonds business segment reached R$102.6 million, 5.9% higher YoY. The earnings before

taxes and profit sharing was of R$189.2 million, 16.9% up YoY, boosted by the growth of 23.8% in the net investment income, as a result

of the wider spread.

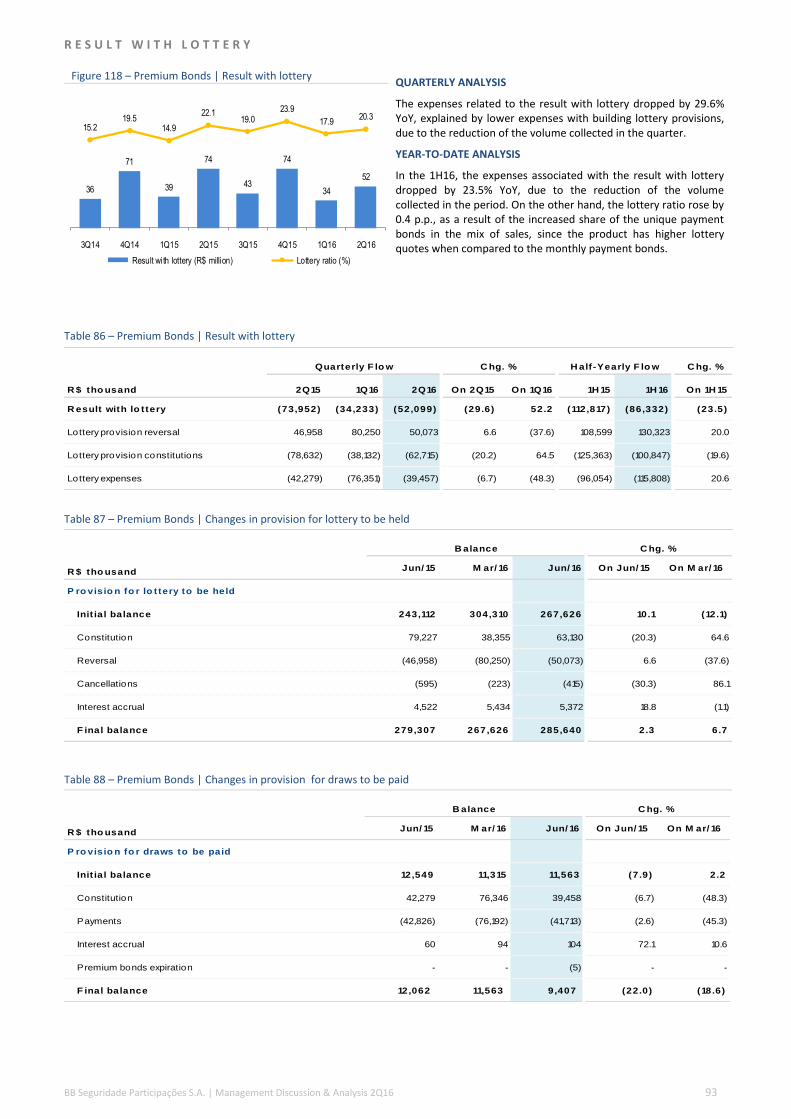

The result with premium bonds remained flat as compared to the same period of 2015. The net revenues with premium bonds decreased 23.3%, due to the drop of 19.9% in premium bonds collection in addition to an increased average reserve quote, which was partially offset by the drop of 29.7% in the acquisition costs as well as by the 29.6% fall in the result with lottery expenses.

YEAR-TO-DATE ANALYSIS

Premium Bonds business segment reached a net income of R$237.7 million in the 1H16, 17.8% higher YoY. The earnings before taxes

and profit sharing achieved R$437.1 million, 29.8% higher YoY, explained by the growth of 48.3% in the net investment income, due to a

1.8 p.p. wider spread along with the higher average balance of interest earning assets.

Year-to-date, the result with premium bonds dropped by 15.7% as compared to the same period of 2015. The performance was a result

of the retraction of 24.9% in the net revenues with premium bonds, due to the 20.4% decrease in premium bonds collection along with

a higher average reserve quote. The contraction of the net revenues with premium bonds was partially offset by lower expenses with

acquisition costs (-31.3%) along with the drop in the result with lottery expenses (-23.5%).

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 13

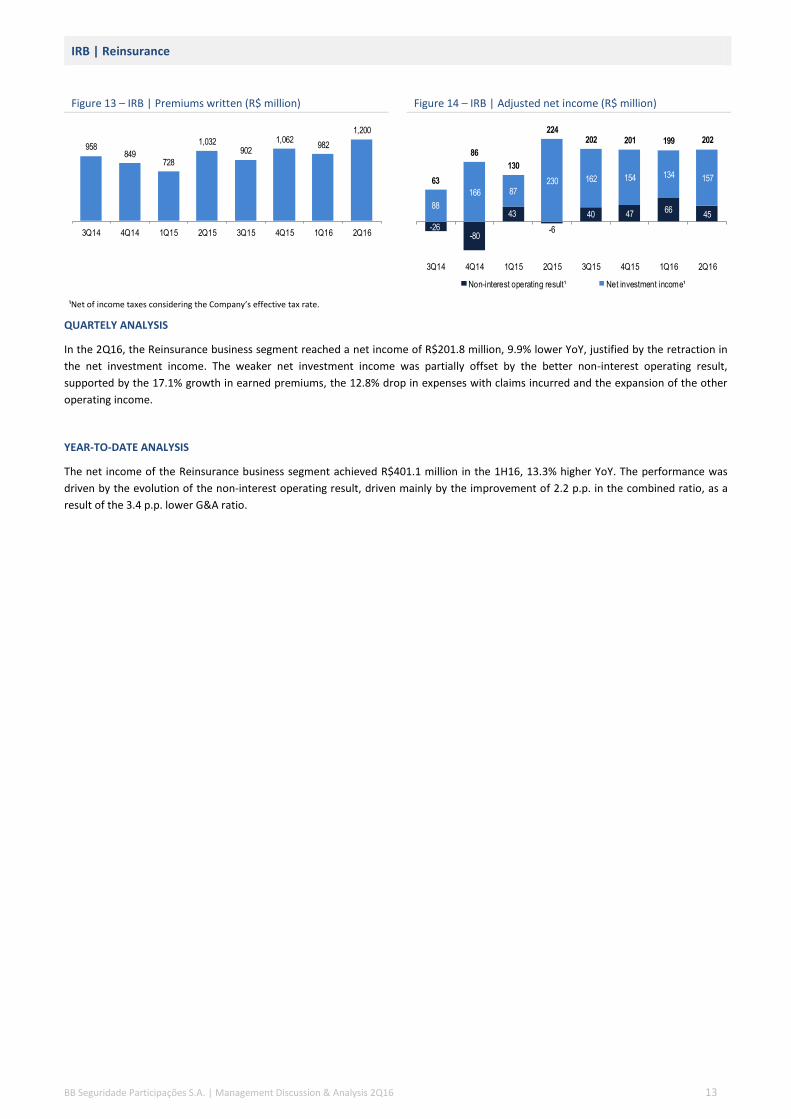

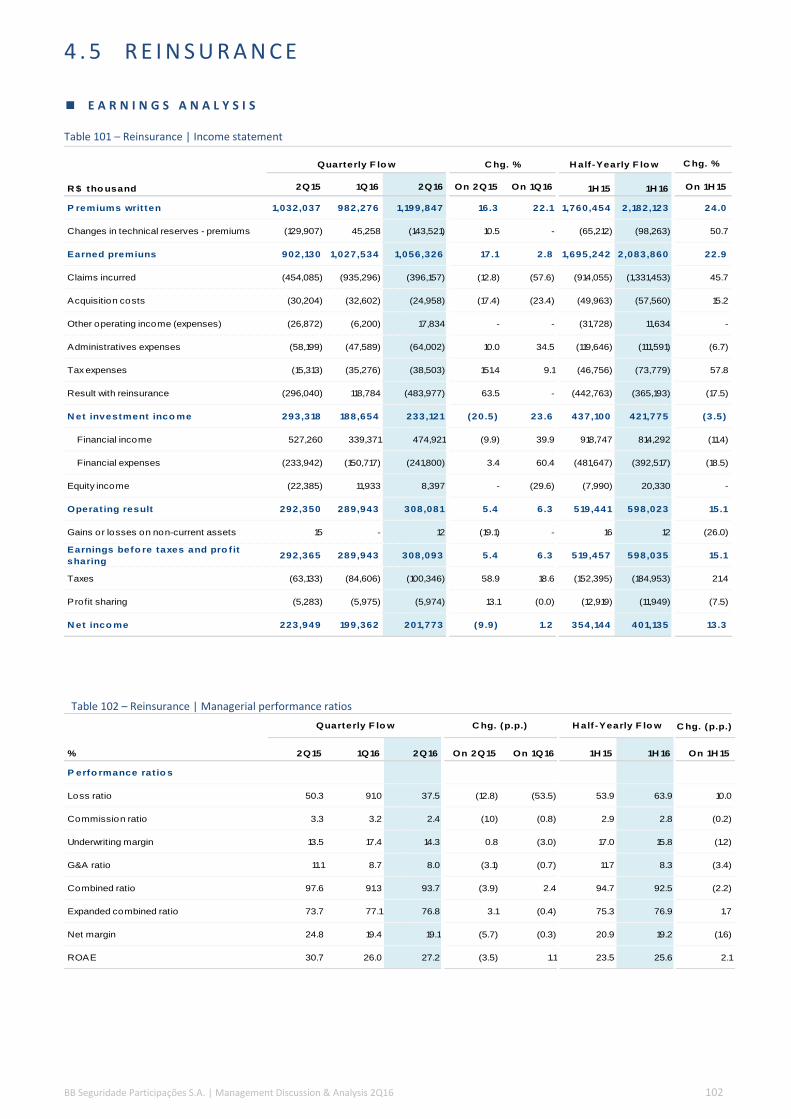

IRB | Reinsurance

Figure 13 – IRB | Premiums written (R$ million) Figure 14 – IRB | Adjusted net income (R$ million)

958849

728

1,032902

1,062982

1,200

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

-26-80

43

-6

40 4766

4588

166 87230 162 154 134 15763

86

130

224202 201 199 202

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Non-interest operating result¹ Net investment income¹

¹Net of income taxes considering the Company’s effective tax rate.

QUARTELY ANALYSIS

In the 2Q16, the Reinsurance business segment reached a net income of R$201.8 million, 9.9% lower YoY, justified by the retraction in

the net investment income. The weaker net investment income was partially offset by the better non-interest operating result,

supported by the 17.1% growth in earned premiums, the 12.8% drop in expenses with claims incurred and the expansion of the other

operating income.

YEAR-TO-DATE ANALYSIS

The net income of the Reinsurance business segment achieved R$401.1 million in the 1H16, 13.3% higher YoY. The performance was

driven by the evolution of the non-interest operating result, driven mainly by the improvement of 2.2 p.p. in the combined ratio, as a

result of the 3.4 p.p. lower G&A ratio.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 14

D I S T R I B U T I O N B U S I N E S S E S

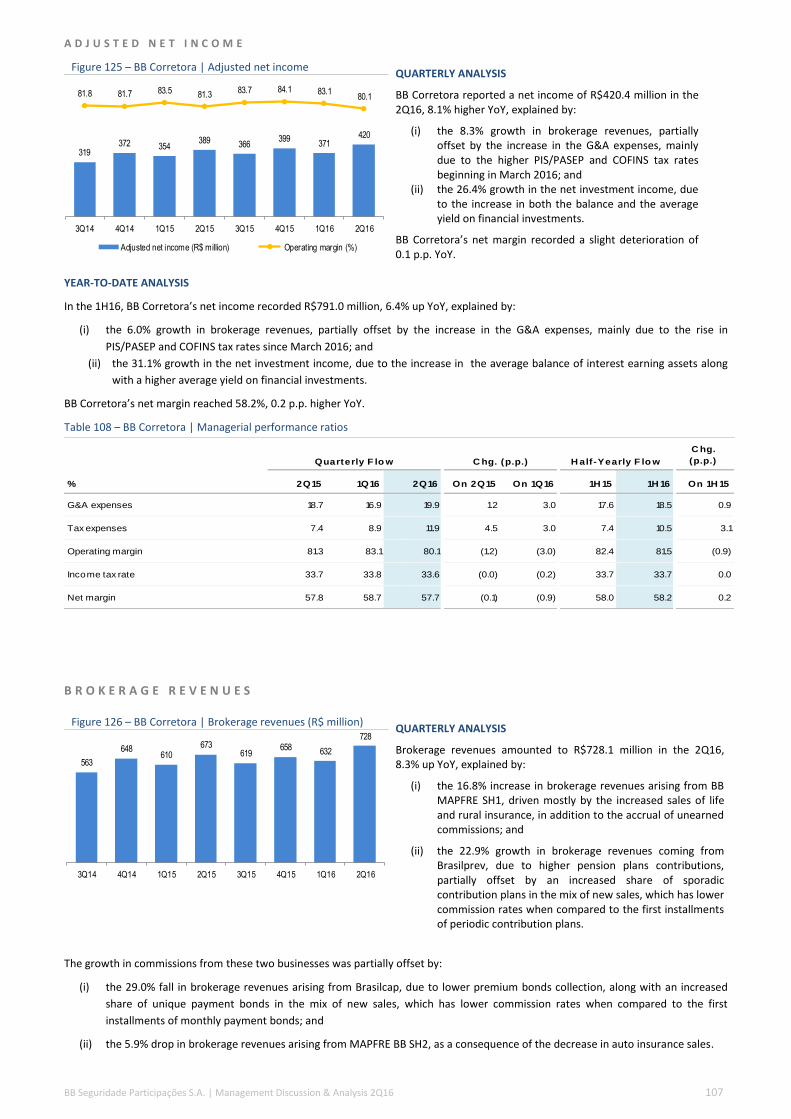

BB Corretora | Brokerage

Figure 15 – BB Corretora | Brokerage revenues (R$ million) Figure 16 – BB Corretora | Adjusted net income and operating margin

563

648610

673619

658 632

728

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

319372 354

389 366399

371420

81.8 81.7 83.5 81.383.7 84.1 83.1

80.1

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Adjusted net income (R$ million) Operating margin (%)

QUARTELY ANALYSIS

The net income for BB Corretora amounted to R$420.4 million in the 2Q16, 8.1% higher YoY, driven by:

(i) the growth of 8.3% in brokerage revenues, mainly the ones arising from the Life, Mortgage Life and Rural segment in addition

to the ones from Pension Plans; and

(ii) the increase of 26.4% in the net investment income, driven by a higher volume in addition to the higher return on financial

investments.

In the quarter, the EBIT margin fell by 1.2 p.p. YoY, impacted by the higher PIS/PASEP and COFINS tax rates since March 2016.

YEAR-TO-DATE ANALYSIS

Year-to-date, BB Corretora reported a net income of R$791.0 million, 6.4% higher YoY, explained by:

(i) the growth of 6.0% in brokerage revenues, boosted by revenues arising from Life, Mortgage Life and Rural segment in addition

to the ones from the Pension Plans segment; and

(ii) the increase of 31.1% in the net investment income, driven by the growth of both the volume and the average yield on interest

earning assets.

The EBIT margin achieved 81.5% in the 1H16, 0.9 p.p. down YoY, impacted by the higher PIS/PASEP and COFINS tax rates since March

2016.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 15

G U I D A N C E 2 0 1 6

Year to date, BB Seguridade’s net income grew by 5.2% as compared to the same period of 2015. The performance of the second

quarter contributed significantly to the impressive acceleration of the net income growth pace, although it still remained below the

2016 guidance. The main reasons for the deviation are:

(i) the bases are not directly comparable as a consequence of the following changes in tax rules: (i) the increase of the income tax

rate, namely the social contribution (“CSLL"), which affected the results of BB Seguridade’s affiliate companies controlled by BB

MAPFRE SH1 and MAPFRE BB SH2, as well as Brasilprev, Brasilcap and IRB, from September 2015 on; (ii) the reinstatement, in

force since July 1st

, 2015, of the PIS/PASEP and COFINS tax rates on financial revenues earned by the holdings BB Seguridade

Participações, BB Seguros Participações, BB Cor Participações, BB MAPFRE SH1 Participações and MAPFRE BB SH2

Participações, which are subject to the non-cumulative system; (iii) the change of BB Corretora’s tax regime to the non-

cumulative system in March 2016, which led to a rise in the PIS/PASEP and COFINS tax rates on gross revenues;

(ii) the weaker than expected premiums of credit life insurance; and

(iii) the deterioration in the loss ratio in auto and casualty insurance.

Taking into account the increase in PIS/PASEP and COFINS tax rates on BB Corretora’s gross revenues and the likelihood of a reduction

in the base interest rate in the second half of 2016, factors that were not expected at the time the 2016 budget was built, along with an

uncertain environment for sales of credit life insurance, the Company has decided to revise its estimates for the growth in the adjusted

net income in 2016, as follows:

Table 4 – Estimates for 2016

R atioValues o bserved

1H 16

2016 P revio us

estimates

2016 R evised

estimates

BB Seguridade - Adjusted net income growth (%) 5.2 8.0 - 12.0 4.0 - 8.0

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 16

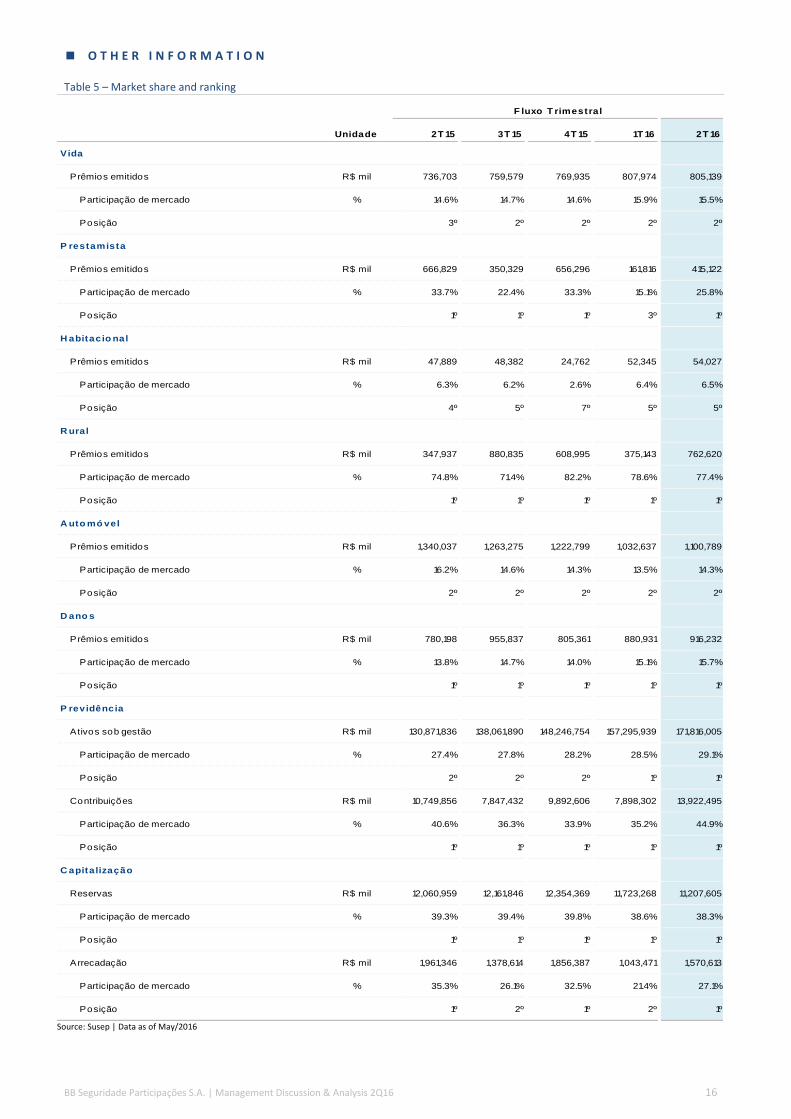

O T H E R I N F O R M A T I O N

Table 5 – Market share and ranking

Unidade 2T 15 3T 15 4T 15 1T 16 2T 16

Vida

Prêmios emitidos R$ mil 736,703 759,579 769,935 807,974 805,139

Participação de mercado % 14.6% 14.7% 14.6% 15.9% 15.5%

Posição 3º 2º 2º 2º 2º

P restamista

Prêmios emitidos R$ mil 666,829 350,329 656,296 161,816 415,122

Participação de mercado % 33.7% 22.4% 33.3% 15.1% 25.8%

Posição 1º 1º 1º 3º 1º

H abitacio nal

Prêmios emitidos R$ mil 47,889 48,382 24,762 52,345 54,027

Participação de mercado % 6.3% 6.2% 2.6% 6.4% 6.5%

Posição 4º 5º 7º 5º 5º

R ural

Prêmios emitidos R$ mil 347,937 880,835 608,995 375,143 762,620

Participação de mercado % 74.8% 71.4% 82.2% 78.6% 77.4%

Posição 1º 1º 1º 1º 1º

A uto mó vel

Prêmios emitidos R$ mil 1,340,037 1,263,275 1,222,799 1,032,637 1,100,789

Participação de mercado % 16.2% 14.6% 14.3% 13.5% 14.3%

Posição 2º 2º 2º 2º 2º

D ano s

Prêmios emitidos R$ mil 780,198 955,837 805,361 880,931 916,232

Participação de mercado % 13.8% 14.7% 14.0% 15.1% 15.7%

Posição 1º 1º 1º 1º 1º

P revidência

Ativos sob gestão R$ mil 130,871,836 138,061,890 148,246,754 157,295,939 171,816,005

Participação de mercado % 27.4% 27.8% 28.2% 28.5% 29.1%

Posição 2º 2º 2º 1º 1º

Contribuições R$ mil 10,749,856 7,847,432 9,892,606 7,898,302 13,922,495

Participação de mercado % 40.6% 36.3% 33.9% 35.2% 44.9%

Posição 1º 1º 1º 1º 1º

C apitalização

Reservas R$ mil 12,060,959 12,161,846 12,354,369 11,723,268 11,207,605

Participação de mercado % 39.3% 39.4% 39.8% 38.6% 38.3%

Posição 1º 1º 1º 1º 1º

Arrecadação R$ mil 1,961,346 1,378,614 1,856,387 1,043,471 1,570,613

Participação de mercado % 35.3% 26.1% 32.5% 21.4% 27.1%

Posição 1º 2º 1º 2º 1º

F luxo T rimestral

Source: Susep | Data as of May/2016

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 17

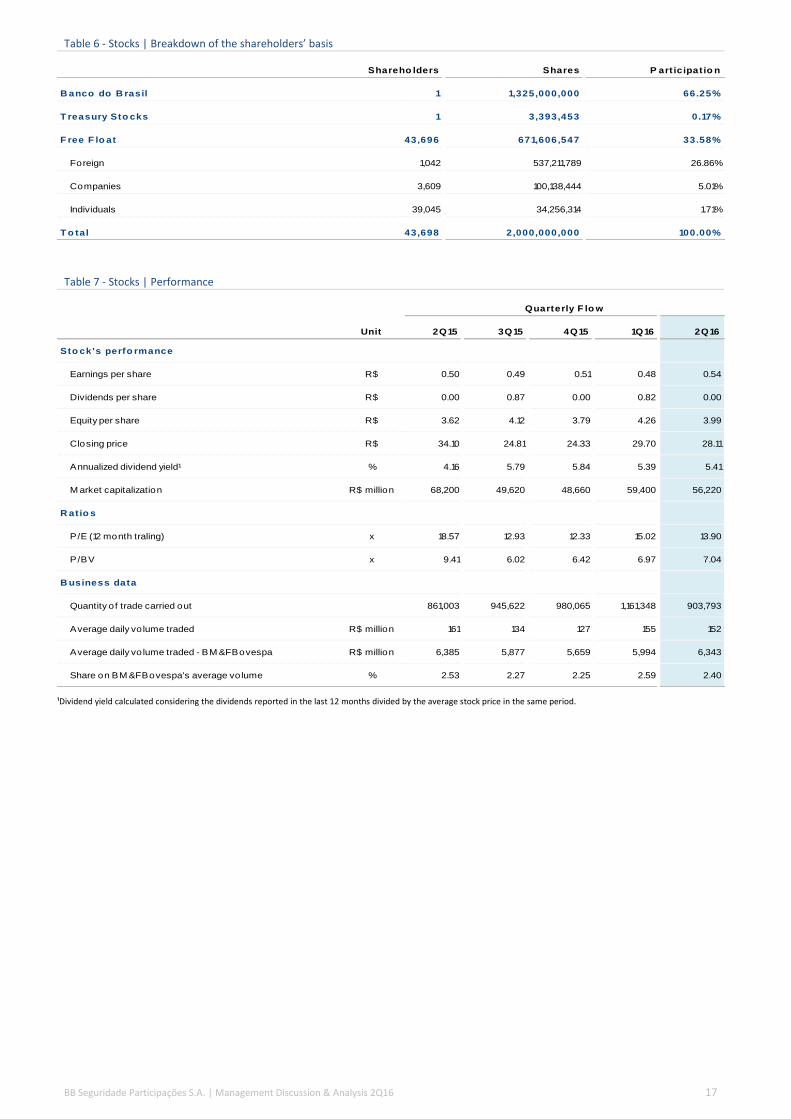

Table 6 - Stocks | Breakdown of the shareholders’ basis

Shareho lders Shares P art icipat io n

B anco do B rasil 1 1,325,000,000 66.25%

T reasury Sto cks 1 3,393,453 0.17%

F ree F lo at 43,696 671,606,547 33.58%

Foreign 1,042 537,211,789 26.86%

Companies 3,609 100,138,444 5.01%

Individuals 39,045 34,256,314 1.71%

T o tal 43,698 2,000,000,000 100.00%

Table 7 - Stocks | Performance

Unit 2Q15 3Q15 4Q15 1Q16 2Q16

Sto ck's perfo rmance

Earnings per share R$ 0.50 0.49 0.51 0.48 0.54

Dividends per share R$ 0.00 0.87 0.00 0.82 0.00

Equity per share R$ 3.62 4.12 3.79 4.26 3.99

Closing price R$ 34.10 24.81 24.33 29.70 28.11

Annualized dividend yield¹ % 4.16 5.79 5.84 5.39 5.41

M arket capitalization R$ million 68,200 49,620 48,660 59,400 56,220

R atio s

P/E (12 month traling) x 18.57 12.93 12.33 15.02 13.90

P/BV x 9.41 6.02 6.42 6.97 7.04

B usiness data

Quantity of trade carried out 861,003 945,622 980,065 1,161,348 903,793

Average daily vo lume traded R$ million 161 134 127 155 152

Average daily vo lume traded - BM &FBovespa R$ million 6,385 5,877 5,659 5,994 6,343

Share on BM &FBovespa's average volume % 2.53 2.27 2.25 2.59 2.40

Quarterly F lo w

¹Dividend yield calculated considering the dividends reported in the last 12 months divided by the average stock price in the same period.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 18

2 . E A R N I N G S A N A L Y S I S

E A R N I N G S B R E A K D O W N

Figure 17 – Earnings Analysis | Breakdown¹

¹Does not consider the individual results from BB Seguridade, BB Seguros and BB Cor holdings, as well as the dental plans operation when negative.

N E T I N V E S T M E N T I N C O M E

Figure 18 – Earnings Analysis | Net investment income (R$ million)

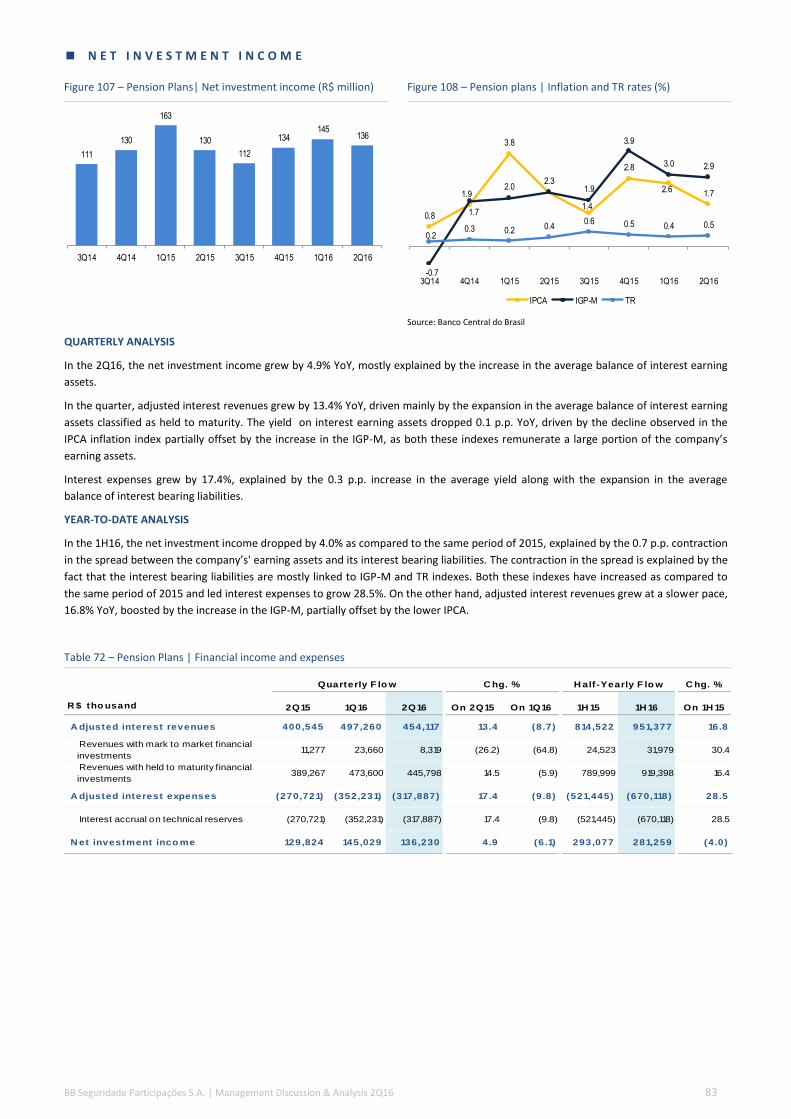

QUARTERLY ANALYSIS

In the 2Q16, the net investment income of the holding BB Seguridade grew by 125.6% YoY, explained by the increase of 122.3% in the average balance of cash and cash equivalents, along with a higher average Selic rate.

YEAR-TO-DATE ANALYSIS

Year-to-date, the net investment income of the holding company rose 130.4% YoY, driven by the expansion of 91.2% in the cash average balance along with a higher average Selic rate.

38.5

40.6

37.0

39.1

36.2

38.8

37.9

38.6

32.9

30.0

30.7

28.8

33.9

29.2

29.1

28.9

16.9

16.4

17.2

15.8

16.5

15.2

17.1

16.6

6.0

7.1

7.3

6.5

4.5

7.0

9.2

6.3

4.3

3.9

5.2

5.0

4.9

5.8

2.6

5.8

1.5

1.9

2.7

4.7

4.1

4.0

4.2

3.8

0.04

0.06

0.07

0.06

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

Brokerage Life, Mortgage Life and Rural Pension Plans Premium Bonds Property and Casualty Reinsurance Dental Insurance Other

2 2

5 5 54

11 11

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 19

G E N E R A L A N D A D M I N I S T R A T I V E E X P E N S E S

Figure 19 – Earnings Analysis | General and administrative expenses (R$ million)

QUARTERLY ANALYSIS

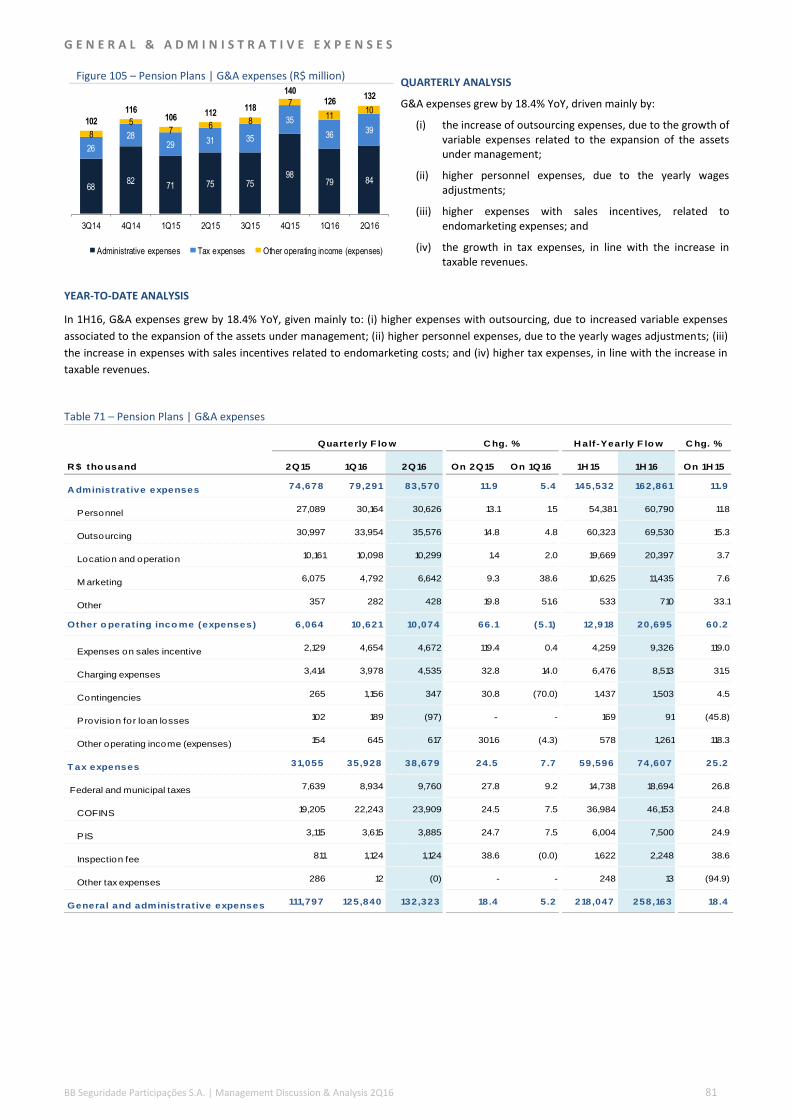

In the 2Q16, the G&A expenses of the holding company rose by 11.1% YoY, due to:

(i) the growth of 32.5% in administrative expenses, mostly

due to the higher expenses with specialized technical

services and other administrative expenses; and

(ii) higher tax expenses, as a result of the re-establishment,

from July 2015 on, of the PIS/PASEP (0.65%) and COFINS

(4.00%) tax rates on financial revenues at the holding

level.

YEAR-TO-DATE ANALYSIS

In the 1H16, BB Seguridade’s G&A grew 40.8% YoY, explained by:

(i) higher tax expenses, as a result of the re-establishment, from July 2015 on, of the PIS/PASEP (0.65%) and COFINS (4.00%)

tax rates on financial revenues at the holding level, besides the IOF tax payments on withdrawals of short-term financial

investments for dividend payment;

(ii) higher personnel expenses, explained by the increase in headcount, besides the migration of part of BB Corretora’s staff

to BB Seguridade, as along with the employees collective bargaining agreement.

Table 8 – Earnings Analysis | General and administrative expenses

8

12 12 12

15

1920

13

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

C hg. %

R $ tho usand 2Q15 1Q16 2Q16 On 2Q15 On 1Q16 1H 15 1H 16 On 1H 15

A dministrat ive expenses (2,107) (2,139) (2,792) 32.5 30.5 (5,945) (4,931) (17.1)

Specialized technical services (349) (98) (713) 104.3 627.2 (2,399) (811) (66.2)

Condominium fee (703) (877) (912) 29.7 3.9 (1,360) (1,789) 31.6

Communication (308) (292) (375) 21.7 28.5 (515) (667) 29.4

Other administrative expenses (747) (872) (792) 6.1 (9.1) (2,001) (1,664) (16.8)

P erso nnel expenses (10,137) (11,898) (10,330) 1.9 (13.2) (17,802) (22,228) 24.9

Compensation (5,615) (6,847) (5,591) (0.4) (18.4) (9,923) (12,438) 25.3

Welfare benefits (3,103) (3,413) (3,072) (1.0) (10.0) (5,317) (6,485) 22.0

Other compensation (706) (795) (881) 24.7 10.8 (1,281) (1,676) 30.8

Benefits (713) (843) (786) 10.3 (6.7) (1,281) (1,629) 27.2

T ax expenses (12) (5,974) (503) 3,938.9 (91.6) (485) (6,477) 1,234.3

COFINS (9) (1,922) (420) 4,382.7 (78.1) (29) (2,342) 7,872.3

PIS/Pasep (2) (310) (68) 2,755.2 (78.1) (6) (378) 5,828.0

IOF - (3,741) (2) - (99.9) (448) (3,743) 735.4

Other (1) (1) (13) 1,781.9 2,168.9 (2) (14) 753.7

Other o perat ing inco me (expenses) 401 6 448 11.8 7,371.4 663 454 (31.5)

G&A expenses (11,855) (20,005) (13,176) 11.1 (34.1) (23,569) (33,181) 40.8

Quarterly F lo w C hg. % H alf -Yearly F lo w

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 20

A D J U S T E D N E T I N C O M E C O M P O S I T I O N

Figure 20 – Earnings Analysis | Non-interest operating results vs net investment income (R$ million)¹

Figure 21 – Earnings Analysis | Non-interest operating results vs net investment income (%)¹

¹Net of taxes considering the Companies effective tax rate.

Table 9 – Earnings Analysis | Non-interest operating results vs net investment income¹

C hg. %

R $ tho usand 2Q15 1Q16 2Q16 On 2Q15 On 1Q16 1H 15 1H 16 On 1H 15

N o n-interest o perat ing results 690,454 628,560 773,234 12.0 23.0 1,343,597 1,401,793 4 .3

Life, M ortgage Life and Rural 214,918 199,670 237,492 10.5 18.9 422,976 437,162 3.4

Property and Casualty 5,795 (28,930) 12,583 117.1 - 6,297 (16,347) -

Pension Plans 97,818 106,627 124,597 27.4 16.9 188,743 231,223 22.5

Premium Bonds 18,296 12,144 16,410 (10.3) 35.1 37,827 28,555 (24.5)

Reinsurance (362) 13,425 9,098 - (32.2) 7,522 22,522 199.4

Dental Insurance 375 559 576 53.5 3.0 109 1,135 937.5

Holdings and broker 353,615 325,064 372,478 5.3 14.6 680,122 697,542 2.6

N et investment inco me 304,191 329,125 313,480 3.1 (4.8) 600,163 642,605 7 .1

Life, M ortgage Life and Rural 71,231 84,866 77,036 8.1 (9.2) 157,307 161,902 2.9

Property and Casualty 44,275 54,178 50,300 13.6 (7.2) 93,184 104,478 12.1

Pension Plans 59,332 60,479 56,791 (4.3) (6.1) 133,449 117,270 (12.1)

Premium Bonds 46,293 77,895 51,993 12.3 (33.3) 96,619 129,888 34.4

Reinsurance 46,985 27,295 32,115 (31.6) 17.7 64,813 59,410 (8.3)

Dental Insurance 40 53 134 238.3 155.5 112 187 67.7

Holdings and broker 36,034 24,359 45,111 25.2 85.2 54,679 69,470 27.1

A djusted net inco me 994,645 957,684 1,086,714 9.3 13.5 1,943,760 2,044,398 5 .2

Quarterly F lo w C hg. % H alf -Yearly F lo w

¹Net of taxes considering the Companies effective tax rate.

621 645 653 690 720 657 629773

202261 296

304 268 357329

313822906

949995 988 1,014

958

1,087

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Non-interest operating results Net investment income

75.5 71.2 68.8 69.4 72.964.8 65.6 71.2

24.5 28.8 31.2 30.6 27.135.2 34.4 28.8

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Non-interest operating results Net investment income

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 21

N O N - I N T E R E S T O P E R A T I N G R E S U L T

QUARTERLY ANALYSIS

The combined non-interest operating results amounted to R$773.2 million in the 2Q16, 12.0% higher YoY, as a result of:

(i) the growth of R$36.6 million in the operating result at BB Corretora, due to higher brokerage revenues arising mainly from the

Life, Mortgage Life and Rural and Pension Plans business segments;

(ii) the expansion of R$26.8 million in the non-interest operating result arising from the Pension Plans business segment, explained

mainly by the increase in revenues with management fees, driven by the expansion in the average balance of assets under

management; and

(iii) the growth of R$22.6 million in the non-interest operating result arising from the Life, Mortgage Life and Rural business

segment, driven mainly by the higher volume of earned premiums along with an improved combined ratio.

YEAR-TO-DATE ANALYSIS

The combined non-interest operating results amounted to R$1.4 billion in the 1H16, 4.3% up YoY, driven mainly by:

(i) the expansion of R$52.0 million in the operating result at BB Corretora, due to higher brokerage revenues arising mainly from

the Life, Mortgage Life and Rural and Pension Plans segments;

(ii) the growth of R$42.5 million in the non-interest operating result arising from the Pension Plans business segment, mostly due

to the increase in revenues with management fees, as a result of the higher average balance of assets under management; and

(iii) the increase of R$14.2 million in the non-interest operating result arising from the Life, Mortgage Life and Rural business

segment, driven mainly by the higher volume of earned premiums.

The increase of the non-interest operating results arising from the segments above mentioned was partially offset by the drop of R$22.6

million in the non-interest operating results from the Property and Casualty business segment, due mainly to the deterioration in the

loss and commission ratios.

N E T I N V E S T M E N T I N C O M E

Figure 22 – Earnings Analysis | Average Selic rate (%) Figure 23 – Earnings Analysis | Forward yield curve (%)

Source: Bacen Source: ValorPro

QUARTERLY ANALYSIS

The combined net investment income of BB Seguridade and its controlled and affiliated companies amounted to R$313.5 million in

2Q16, 3.1% higher YoY. The improved performance was driven mainly by the growth observed in the Property and Casualty, Life,

Mortgage Life and Rural, and Premium Bonds business segments, along with BB Corretora.

The increase in the balance of interest earning assets, the higher average Selic rate and the downward shift in the forward yield curve,

which positively impacted the mark-to-market results of pre-fixed bonds, boosted the net investment income in the 2Q16. On the other

hand, the lower inflation had a negative impact on the return on inflation protected bonds classified as held to maturity.

YEAR-TO-DATE ANALYSIS

The combined net investment income of BB Seguridade and its controlled and affiliated companies totaled R$642.6 million year-to-date,

an increase of 7.1% YoY. The growth in the net investment income came mainly from the Premium Bonds and Property and Casualty

business segments, along with BB Corretora, and is explained by the growth in the average balance of interest earning assets, the higher

average Selic rate and the downward shift in the forward yield curve, which positively impacted the mark-to-market results of the pre-

fixed bonds.

10.90 11.2112.19

13.1413.99 14.15 14.15 14.15

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

13.39 13.23

13.13 12.99 12.97

13.95

13.27

12.9412.76 12.69

13.94

12.92

12.41 12.25

12.15

13.87

13.71 13.83 13.90 13.88

DI1F17 DI1F18 DI1F19 DI1F20 DI1F21

Mar/15

Mar/16

Jun/15

Jun/16

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 22

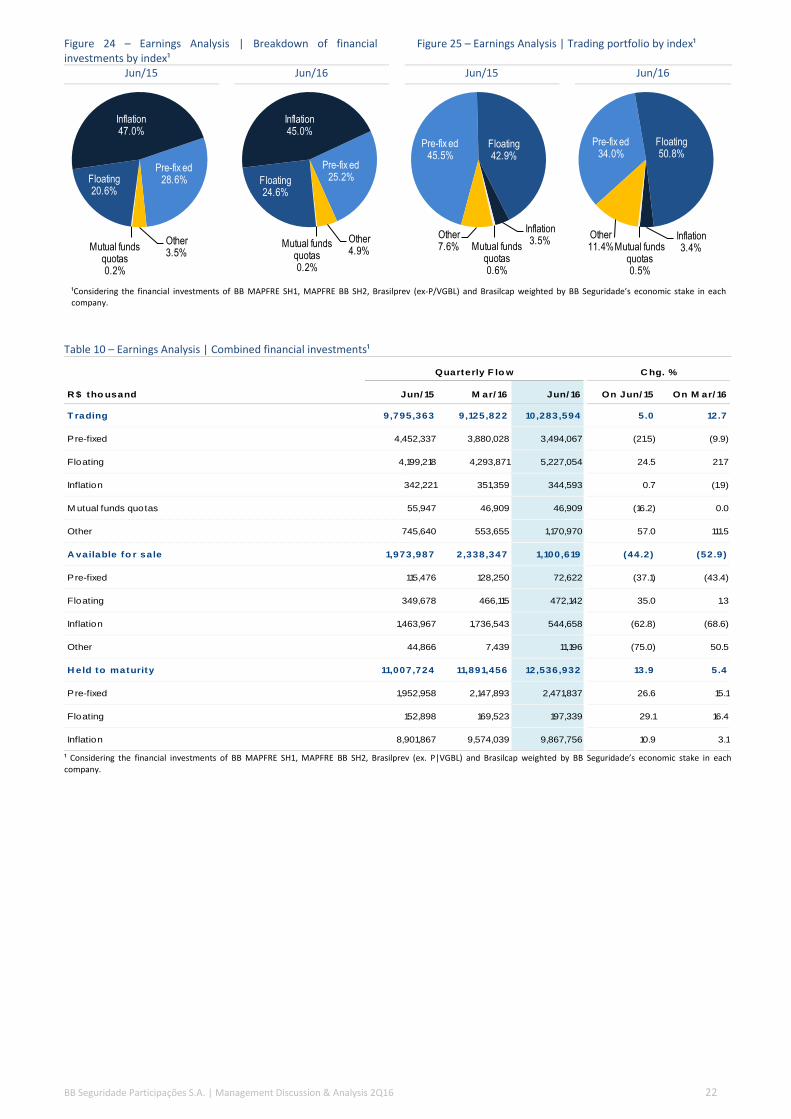

Figure 24 – Earnings Analysis | Breakdown of financial investments by index¹

Figure 25 – Earnings Analysis | Trading portfolio by index¹

Jun/15 Jun/16 Jun/15 Jun/16

¹Considering the financial investments of BB MAPFRE SH1, MAPFRE BB SH2, Brasilprev (ex-P/VGBL) and Brasilcap weighted by BB Seguridade’s economic stake in each company.

Table 10 – Earnings Analysis | Combined financial investments¹

¹ Considering the financial investments of BB MAPFRE SH1, MAPFRE BB SH2, Brasilprev (ex. P|VGBL) and Brasilcap weighted by BB Seguridade’s economic stake in each company.

Pre-fix ed28.6%

Other3.5%

Mutual funds quotas0.2%

Floating20.6%

Inflation47.0%

Pre-fix ed25.2%

Other4.9%

Mutual funds quotas0.2%

Floating24.6%

Inflation45.0%

Pre-fix ed45.5%

Floating42.9%

Inflation3.5%

Mutual funds quotas0.6%

Other7.6%

Pre-fix ed34.0%

Floating50.8%

Inflation3.4%Mutual funds

quotas0.5%

Other11.4%

R $ tho usand Jun/ 15 M ar/ 16 Jun/ 16 On Jun/ 15 On M ar/ 16

T rading 9,795,363 9,125,822 10,283,594 5.0 12.7

Pre-fixed 4,452,337 3,880,028 3,494,067 (21.5) (9.9)

Floating 4,199,218 4,293,871 5,227,054 24.5 21.7

Inflation 342,221 351,359 344,593 0.7 (1.9)

M utual funds quotas 55,947 46,909 46,909 (16.2) 0.0

Other 745,640 553,655 1,170,970 57.0 111.5

A vailable fo r sale 1,973,987 2,338,347 1,100,619 (44.2) (52.9)

Pre-fixed 115,476 128,250 72,622 (37.1) (43.4)

Floating 349,678 466,115 472,142 35.0 1.3

Inflation 1,463,967 1,736,543 544,658 (62.8) (68.6)

Other 44,866 7,439 11,196 (75.0) 50.5

H eld to maturity 11,007,724 11,891,456 12,536,932 13.9 5.4

Pre-fixed 1,952,958 2,147,893 2,471,837 26.6 15.1

Floating 152,898 169,523 197,339 29.1 16.4

Inflation 8,901,867 9,574,039 9,867,756 10.9 3.1

Quarterly F lo w C hg. %

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 23

3 . B A L A N C E S H E E T A N A L Y S I S

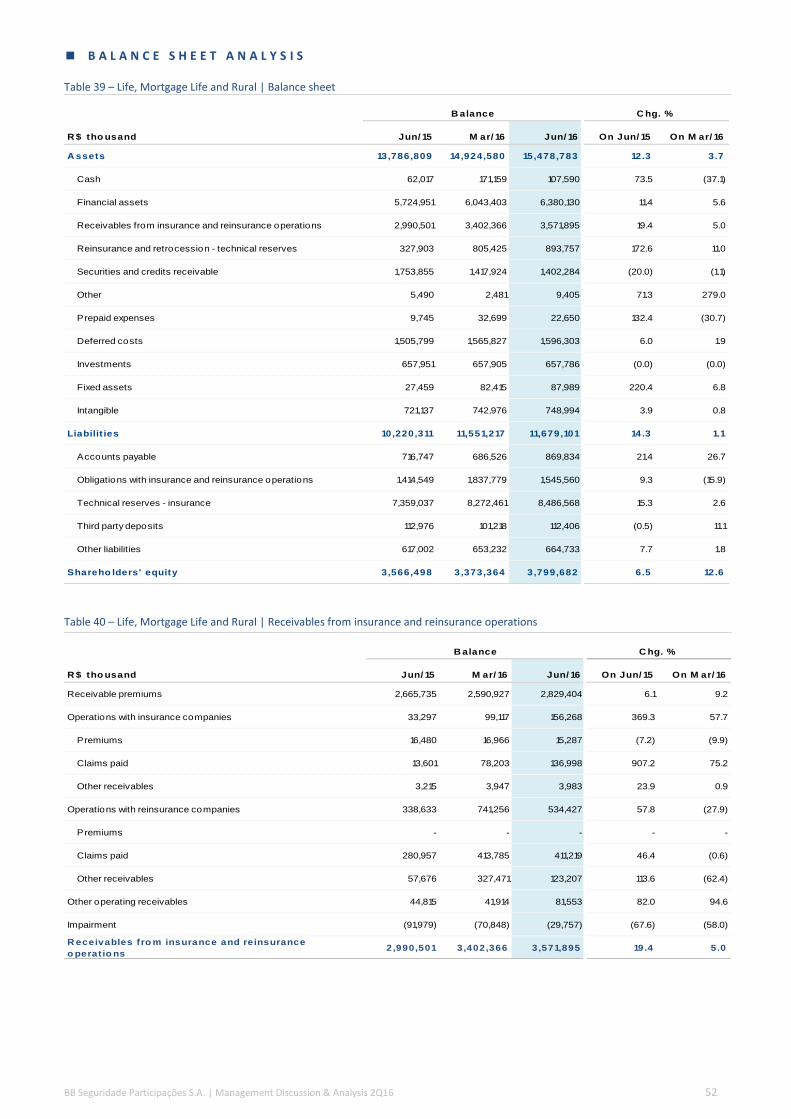

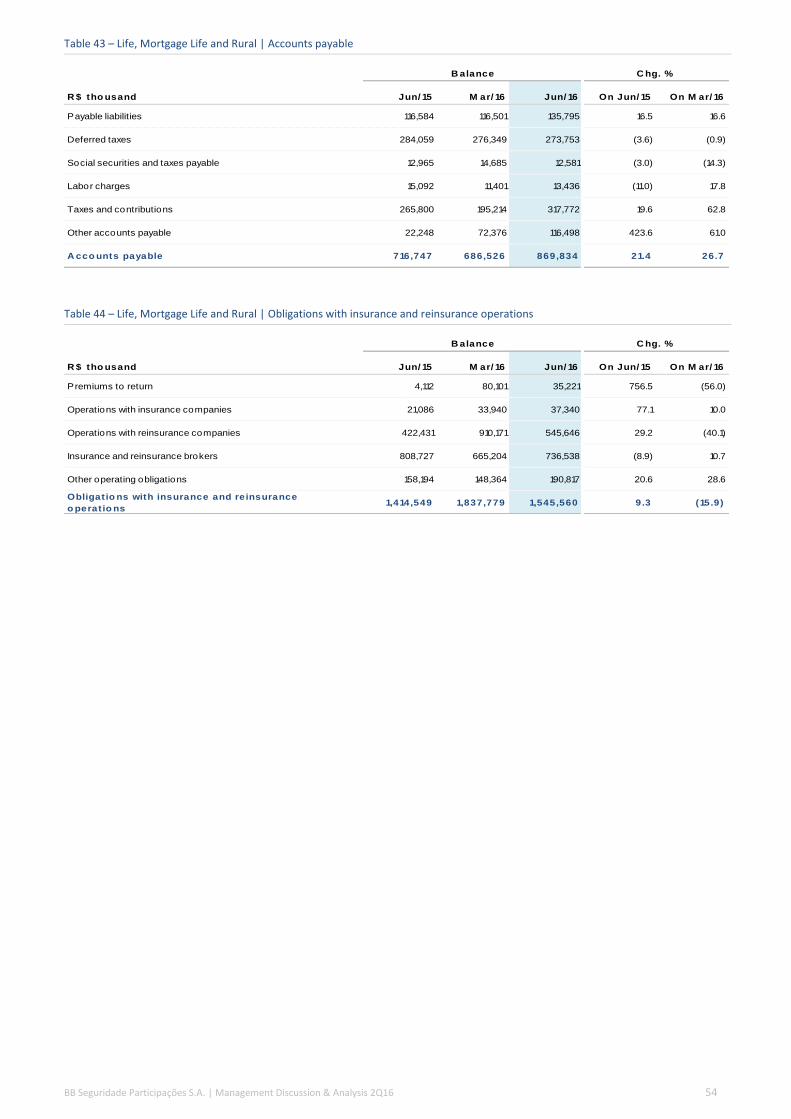

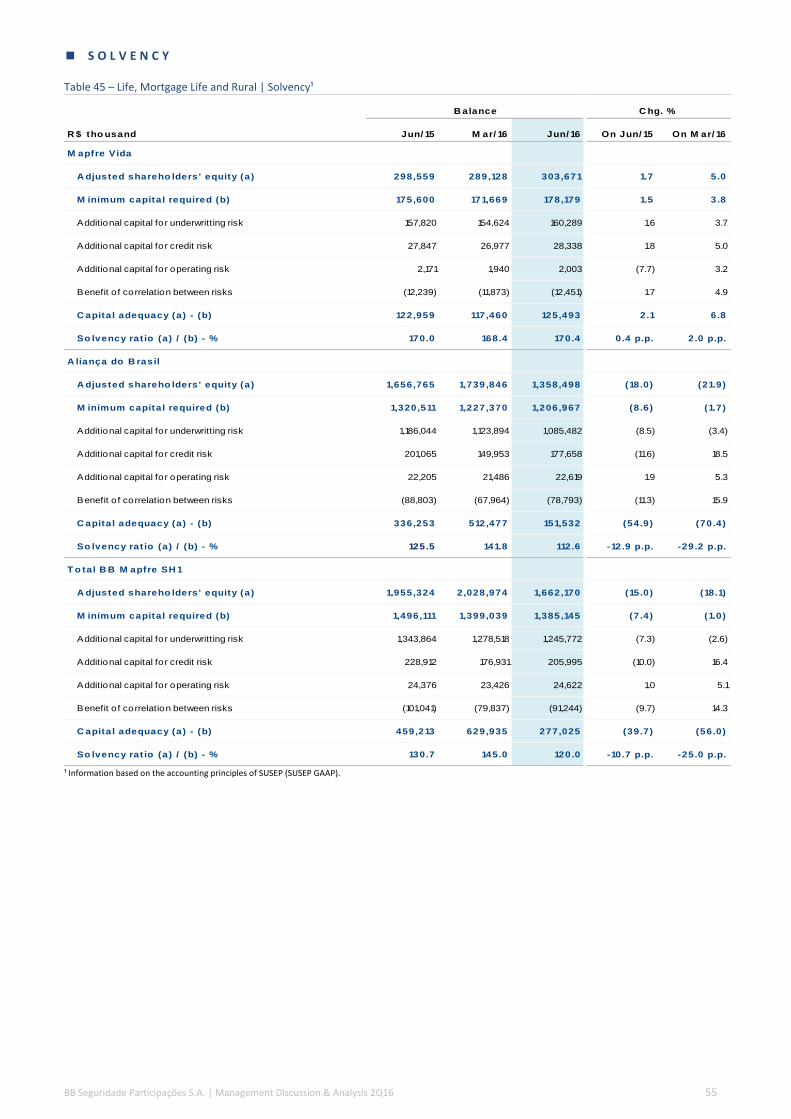

Table 11 – Balance Sheet Analysis |Balance sheet

C A S H A N D C A S H E Q U I V A L E N T S

By the end of June 2016, the balance of cash and cash equivalents reached R$297.3 million, 128.0% up YoY. The balance of cash and

cash equivalents is mainly composed of repos.

I N V E S T M E N T S

Table 12 – Balance Sheet Analysis |Direct investments

Note: (1) Controlled companies, fully consolidated

R $ tho usand Jun/ 15 M ar/ 16 Jun/ 16 On Jun/ 15 On M ar/ 16

A ssets 8,981,254 8,533,876 9,628,779 7.2 12.8

Cash and cash equivalents 130,381 303,095 297,315 128.0 (1.9)

Investments 7,096,937 8,192,062 7,739,443 9.1 (5.5)

Current tax assets 20,782 38,715 39,163 88.4 1.2

Dividends receivable 1,733,150 - 1,550,209 (10.6) -

Other assets 4 4 2,649 66,125.0 66,125.0

Liabilit ies 1,736,879 7,487 1,642,798 (5.4) 21,842.0

Dividends payable 1,731,444 5 1,635,524 (5.5) -

Current tax liabilities 9 483 191 2,023.0 (60.4)

Other liabilities 5,426 6,999 7,083 30.5 1.2

Shareho lders' equity 7,244,375 8,526,389 7,985,981 10.2 (6.3)

B alance C hg. %

T o tal

o wnership (%)

R $ tho usand Jun/ 16 Jun/ 15 M ar/ 16 Jun/ 16

Insurance, P ensio n P lans and

P remium B o nds

BB Seguros Participações Holding (1) 100.0 7,035,170 7,759,793 7,677,702

Insurance B ro kerage -

BB Cor Participações Holding (1) 100.0 61,767 432,269 61,741

A cco unting

treatmentA ctivity

Investment balance

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 24

Table 13 – Balance Sheet Analysis |BB Seguros Participações’ investments

Note: (1) Affiliated companies, booked by the equity method

Table 14 – Balance Sheet Analysis |BB Cor Participações’ investments

Note: (1) Controlled companies, fully consolidated

T o tal

o wnership (%)

R $ tho usand Jun/ 16 Jun/ 15 M ar/ 16 Jun/ 16

Insurance

B B M A P F R E SH 1 P art icipaçõ es S.A . H o lding (1) 75.0 2,946,875 2,802,045 3,121,739

Companhia de Seguros Aliança do Brasil Insurance - - -

M APFRE Vida S.A. Insurance - - -

M A P F R E B B SH 2 P art icipaçõ es S.A . H o lding (1) 50.0 2,105,911 2,208,269 2,325,815

Aliança do Brasil Seguros S.A. Insurance - - -

Brasilveículos Companhia de Seguros Insurance - - -

M APFRE Seguros Gerais S.A. Insurance - - -

BB M APFRE Assistência S.A. Insurance - - -

P ensio n P lans - - -

B rasilprev Seguro s e P revidênciaInsurance/

P ensio n P lans(1) 75.0 1,833,477 1,745,096 1,927,155

H ealth - - -

B rasildental Operado ra de P lano s

Odo nto ló gico s S.AH ealth (1) 75.0 1,954 5,520 6,231

P remium B o nds - - -

B rasilcap C apitalização P remium B o nds (1) 66.7 433,839 402,059 470,462

R einsurance - - -

IR B R einsurance (1) 20.4 626,849 596,368 626,384

A ctivity

A cco unting

treatment

Investment balance

T o tal

o wnership (%)

R $ tho usand Jun/ 16 Jun/ 15 M ar/ 16 Jun/ 16

Insurance bro kerage

B B C o rreto ra de Seguro s e A dm. de

B ens

Insurance

B ro ker(1) 100.0 35,001 405,483 34,976

A ctivityA cco unting

treatment

Investment balance

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 25

Figure 26 – Balance Sheet Analysis | Ownership structure at 06/30/2016

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 27

S H A R E H O L D E R ’ S E Q U I T Y

Shareholder’s equity amounted to R$8.0 billion in June 2016,10.2% higher YoY.

The paid-in capital, which amounts to R$5.6 billion, is divided into 2.0 billion common shares, without par value. The shareholders’

equity of R$8.0 billion is equivalent to a book value of R$3.99 per share.

Table 15 – Balance Sheet Analysis | Statement of changes in equity

Capital

Capital

reserve

Legal and

statutory

reserve

Treasury

stock

Retained

earnings

(losses)

Accumulate

d other

comprehensi

ve income Total

B alance o n D ecember 31, 2014 5,646,768 266 2,290,014 (266) - (12,798) 7,923,984

Transactions with stock payments - 446 - (446) - - -

Additional dividends in 2H14 - - (1,103,927) - - - (1,103,927)

Capital reserve - - 432,859 - (432,859) - -

Additional dividends proposed in 1H15 - - - - (1,731,440) - (1,731,440)

Other comprehensive income - - - - - (8,541) (8,541)

Net income for the period - - - - 2,164,299 - 2,164,299

B alance o n June 30, 2015 5,646,768 712 1,618,946 (712) - (21,339) 7,244,375

Changes in the Period - 446 (671,068) (446) - (8,541) (679,609)

B alance o n D ecember 31, 2015 5,646,768 712 2,027,573 (48,961) - (45,324) 7,580,768

Transactions with stock payments - 292 - (292) - - -

Share buyback program - - - (33,953) - - (33,953)

Capital reserve - - 408,880 - (408,880) - -

Additional dividends proposed in 1H16 - - - - (1,635,518) - (1,635,518)

Other comprehensive income - - - - - 30,286 30,286

Net income for the period - - - - 2,044,398 - 2,044,398

B alance o n M arch 31, 2016 5,646,768 1,004 2,436,453 (83,206) - (15,038) 7,985,981

C hanges in the P erio d - 292 408,880 (34,245) - 30,286 405,213

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 28

4 . U N D E R W R I T I N G A N D A C C U M U L A T I O N

L I F E , M O R T G A G E L I F E A N D R U R A L

BB Seguridade offers life, mortgage life and rural insurance through its affiliate company BB Mapfre SH1. This company was established

by a 20-year term partnership with Mapfre in 2010, and the joint operations began in 2011. BB Seguridade holds, through BB Seguros, a

74.99% economic stake in BB Mapfre SH1, composed of 100% of the preferred shares and 49.99% of the common shares. The segments

in which BB Mapfre SH1 operates is dominated by the Brazilian banks, what reflects the association of this kind of products with the

bancassurance channel.

The following topics show a brief description of the main products offered by BB Mapfre SH1:

a. Life insurance is a product focused on individuals which assures financial protection to the beneficiaries, chosen by the

policyholder, in case of death (natural or accidental), or permanent disability of the insured. If a claim occurs, the insurance

company pays the amount agreed in the insurance policy to the beneficiary. Differently from the products sold in other countries,

the life insurance sold by BB Mapfre SH1 is a term life insurance without accumulation. If the customer fails to make the monthly

payments, the coverage is suspended without any amount being reverted to the policyholder.

b. Credit life insurance is a life insurance policy intended to pay off a borrower’s loan in case of death or permanent disability of the

insured. This type of product is designed to protect both the lender and the insured dependents, preventing them to inherit this

liability. This product is already quite widespread in Brazil and it is expected to grow with the expansion of the loan portfolio. The

main beneficiary of this type of product is the lender.

c. Mortgage life insurance is an insurance policy intended to pay off a mortgage in case of death or disability of the insured. The

insurance policy gives the guarantee that his family will keep the property and the bank will receive the full payment of the

mortgage debt. A mortgage life insurance also protects against physical damage to the insured property. The premium is calculated

on a monthly basis and varies according to the outstanding loan balance and the borrower’s age.

d. Rural insurance encompasses a group of three main products: (i) the crop insurance, which protects the farmers from weather

hazards and falling prices of the crop; (ii) the rural lien insurance, which protects the asset given as collateral for a rural loan; and

(iii) the rural producer credit life insurance, which is an insurance designed for farmers intended to pay off the rural loan in case of

death of the insured.

A U T O , P R O P E R T Y A N D C A S U A L T I E S

BB Seguridade offers auto, property and casualties insurance through its affiliate Mapfre BB SH2. This company was established by a 20-

year term partnership with Mapfre Brasil signed in 2010, and the joint operations began in 2011. In this partnership BB Seguridade

holds a 50.00% economic stake in Mapfre BB SH2, being 51.0% of the preferred shares and 49.0% of the common shares.

In this segment, the insurance policies for large risks and auto require a more customized assistance and selling process, which result in

a higher concentration of sales in independent brokers than in the bancassurance channel.

The following paragraphs show a brief description of the main products offered by Mapfre BB SH2:

a. Property insurance is a type of insurance sold to individuals or companies that provides protection against risks to properties,

linked or not to loans. The main products of this segment are: home insurance (covers the risks related to a private residence),

business insurance (covers the risks related to a property that belongs to a company) and insurance for machinery and equipment

(protection to a property that belongs either to individuals or companies).

b. Auto insurance is an insurance policy designed to provide protection for vehicles, of commercial or particular use, against theft,

physical damage and/or bodily injury resulting from traffic collisions, besides other assistances provided to the policy holder. The

auto insurance market is dynamic and competitive, what benefit the client to shop around for the best price before closing the

deal. Besides that, the renewal of this kind of policies occur on an yearly basis, what makes easier for the competitors to go after

the clients and makes it difficult to establish and strengthen a long term relationship with costumers, unlike other segments.

c. DPVAT is a mandatory insurance in Brazil that covers personal injury caused by vehicles to passengers, drivers or pedestrians.

DPVAT offers coverage for three natures of damage: death, permanent disability, and reimbursement for medical and hospital

expenses. DPVAT is funded by vehicles owners through annual payments. Out of the amount collected, 45% is transferred to the

Ministry of Health (SUS), to fund the hospital care victims of traffic accidents across the country, and 5% are transferred to the

Ministry of Cities, for exclusive use in programs directed to the prevention of traffic accidents. The remaining 50% are directed to

the payment of claims.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 29

P E N S I O N P L A N S

BB Seguridade operates in the private pension plans segment through its affiliate Brasilprev, in partnership with the American company

Principal Financial Group (PFG). Brasilprev was established in 1993 as a partnership between Banco do Brasil and a group of insurance

companies. After going through a series of corporate restructuring, within 1999-2000, PFG, through its subsidiary in Brazil, Principal

Financial Group do Brasil, acquired an economic stake in the company and established a partnership with Banco do Brasil. In 2010, BB

Seguros and PFG renewed their partnership, extending it for 23 years more. As a result of this new agreement, Banco do Brasil

increased its stake in Brasilprev from 49.99% to 74.99%. Pension plans are growing in popularity in Brazil, due to increasing life

expectancy, level of financial education and tax benefits for individuals.

Brasilprev has three main sources of revenue: the load fee, charged on contributions and redemptions, the management fees on assets

under management, and the premiums paid to cover risks.

Nowadays, there are three types of private pension plans in Brazil: Free Benefit Generator Plan (PGBL), Free Benefit Generator Life Plan

(VGBL), and traditional plans, which are no longer sold. The private pension plans in Brazil are described as follows:

a. Free Benefit Generator Plan (PGBL): is recommended for people who declare income taxes in the complete form, as the

contributions are tax deductible up to the limit of 12% of the annual gross taxable income. In this modality, in case of redemption

or benefit received, the income taxes are calculated on the amount redeemed or income received.

In Brazil, there are two alternatives for an individual to present the tax statements, the simple form or the complete form. In the

complete form, a Brazilian citizen can inform not only the income but also deductible expenses, such as expenses with health

insurance, education, investments in PGBL, and other.

In addition, the participant may choose to be taxed either in the progressive tax system or in the regressive tax system when buying

a pension plan.

In the progressive tax system, the annuity is taxed when money is received according to the “Tabela Progressiva Mensal” (Montlhy

Progressive Table) made available by the Brazilian Internal Revenue Service. The tax brackets can vary from zero to 27.5% according

to the annual wages with adjustment in the income tax declaration. Redemptions are taxed at 15% regardless the amount

redeemed, with adjustment in the income tax declaration according to the Monthly Progressive Table.

In the regressive tax system, in the event of redemption or annuity received, tax is withheld and is definitive, with no possibility of

adjustment in the annual tax statement. The rates are determined by the length of stay of each inflow in the plan, starting at 35%,

with gradual reduction every two years, reaching a level of 10% after 10 years.

b. Free Benefit Generator Life Plan (VGBL): is recommended for those who declare income taxes in the simplified form or is

exempt, since the contributions are not tax deductible. As in PGBL, the customer can choose either the progressive or the

regressive tax system. In this modality, the tax benefit is that in case of redemption or annuity received, income tax will be

charged on interest earned only. Another advantage of the VGBL is its simplicity of the procedure for the inheritance

transmission, being suitable for customers who wish to make a succession planning. In this product, the customer can

determine who will be the beneficiaries after his death and, unlike other assets, funds invested in VGBL are not part of the

inventory, which is a procedure with legal costs and attorney's fees that can consume from 6% to 20% of the wealth received

by the heirs.

c. Traditional Plan: guarantees a fixed interest of 6% plus inflation (IGP-M) or Taxa Referencial (TR) per year. These plans are no

longer sold and account for R$9.0 billion of the assets under management of Brasilprev.

P R E M I U M B O N D S

BB Seguridade offers premium bonds through its affiliate company Brasilcap, in a partnership with Icatu and Aliança da Bahia. Premium

bonds are very peculiar to the Brazilian market, but there are also quite similar products in United Kingdom and in Spain.

Premium bonds are mainly sold through the bancassurance channel and it is an alternative way to accumulate reserves, with term and

interest rate previously determined, entitling the bondholder to participate in lotteries. Premiums are distributed through periodic

draws, being most frequent the usage of a combination of numbers in pre-determined series, based on the Brazilian Official Lottery.

Depending on the type of premium bond and the payment method chosen, the load fee and lottery quotas can exceed 10% of the

amount collected. The amount intended to cover lottery, administrative expenses, and operational and acquisition costs are covered by

these quotas.

In case of early redemption, the bondholder must obey a grace period (12 months in most products). Beyond the grace period, penalties

will be applied if the bondholder decides for early redemption, which will decrease as the bond approaches to maturity.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 30

R E I N S U R A N C E

The reinsurance industry in Brazil has been growing substantially since the market became opened in April 2008. With the approval of

the Complementary Law No. 126/2007, the state monopoly over reinsurance ceased to exist and a 40% market reserve for reinsurers

based in Brazil became effective in March 2011.

In some cases, due to contract or regulation, reinsurance becomes mandatory, and according to SUSEP data, the main risks covered

today are P&C, financial, rural and transportation.

BB Seguridade operates in the reinsurance industry through IRB-Brasil Resseguros S.A.. Founded in 1939, IRB used to have a monopoly

over reinsurance in Brazil until 2007.

In 2013, BB Seguridade, through its subsidiary BB Seguros Participações acquired a stake in IRB, entering the Brazilian reinsurance

market. After that, IRB went through a process of privatization and capital increase. At the end of this process, BB Seguros became the

holder of 20.51% of IRB’s total economics, and became part of its control block, together with the Brazilian Federal Government,

Bradesco Auto Re, Itaú Seguros, Itaú Vida e Previdência and Fundo de Investimentos em Participações Caixa Barcelona.

On December 29th

, 2014, it was approved in Extraordinary General Meeting, the amendment of IRB’s Bylaws to change the number of

stocks from 1.035.663 to 1.040.000, in order to include 4.337 treasury stocks. Therefore, the BB Seguro’s stake in IRB was changed from

20.51% to 20.43%.

The income statement, financial information, balance sheet and performance ratios on BB Seguridade’s affiliates presented in this report, are influenced by the investor company accounting entries, e.g., changes in goodwill. Therefore, the statements are not necessarily reconcilable with those published by the Companies.

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 31

4 . 1 L I F E , M O R T G A G E L I F E A N D R U R A L

E A R N I N G S A N A L Y S I S

Table 16 – Life, Mortgage Life and Rural |Income statement

C hg. %

R $ tho usand 2Q15 1Q16 2Q16 On 2Q15 On 1Q16 1H 15 1H 16 On 1H 15

P remiums writ ten 1,866,794 1,496,845 2,096,620 12.3 40.1 3,408,878 3,593,465 5.4

Changes in technical reserves - premiums (268,315) 361,891 (216,618) (19.3) - (225,870) 145,273 -

Earned premiuns 1,598,479 1,858,736 1,880,002 17.6 1.1 3,183,008 3,738,738 17.5

Revenue of po licies issuance 2,907 6,049 3,372 16.0 (44.2) 6,662 9,421 41.4

Claims incurred (531,331) (877,276) (874,922) 64.7 (0.3) (1,284,000) (1,752,198) 36.5

Acquisition costs (399,235) (449,869) (469,817) 17.7 4.4 (787,152) (919,686) 16.8

Result with reinsurance (28,291) 141,843 154,573 - 9.0 124,027 296,416 139.0

Administrative expenses (69,077) (93,118) (88,936) 28.7 (4.5) (143,590) (182,054) 26.8

Tax expenses (51,236) (62,762) (57,157) 11.6 (8.9) (102,613) (119,919) 16.9

Other operating income (expenses) (65,541) (64,085) (18,665) (71.5) (70.9) (95,080) (82,750) (13.0)

Underwrit ing result 456,675 459,518 528,452 15.7 15.0 901,262 987,970 9.6

N et investment inco me 146,979 190,477 168,258 14.5 (11.7) 325,206 358,735 10.3

Financial income 187,915 245,606 235,084 25.1 (4.3) 404,263 480,690 18.9

Financial expenses (40,936) (55,129) (66,826) 63.2 21.2 (79,057) (121,955) 54.3

Equity income (7,526) (7,740) (7,729) 2.7 (0.1) (15,170) (15,469) 2.0

Operat ing result 596,128 642,255 688,979 15.6 7.3 1,211,298 1,331,234 9.9

Gains or losses on non-current assets (4) (187) 4,186 - - 3 3,999 133,209.2

Earnings befo re taxes and pro f it

sharing596,124 642,068 693,165 16.3 8.0 1,211,301 1,335,233 10.2

Taxes (210,869) (260,592) (269,959) 28.0 3.6 (429,853) (530,551) 23.4

Profit sharing (3,673) (2,043) (3,781) 2.9 85.0 (7,635) (5,824) (23.7)

N et inco me 381,582 379,433 419,425 9.9 10.5 773,812 798,857 3.2

Quarterly F lo w C hg. % H alf -Yearly F lo w

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 32

To provide a better analysis, the following table shows a managerial view built considering the reallocation of the result with

reinsurance to the other accounts that compose the Income Statement. This reallocation allows the analysis of the performance ratios

already considering the reinsurance effects.

Table 17 – Life, Mortgage Life and Rural | Managerial income statement

Retained premiums = Premiums written + premiums ceded to reinsurance Changes in technical provisions = Changes in technical provisions + changes in technical provisions on reinsured operations Retained claims = Claims incurred + recovery of indemnity claims + recovery of claims expenses + changes in provisions for claims IBNR + salvages and reimbursed assets + changes in provision for claims IBNER provisions for claims to be settled + changes of expenses related to IBNR + changes in estimates for salvages and reimbursed assets + provisions for claims to be settled

C hg. %

R $ tho usand 2Q15 1Q16 2Q16 On 2Q15 On 1Q16 1H 15 1H 16 On 1H 15

P remiums writ ten 1,866,794 1,496,845 2,096,620 12.3 40.1 3,408,878 3,593,465 5.4

Premiums ceded to reinsurance (33,491) (113,056) (285,166) 751.5 152.2 (94,362) (398,222) 322.0

R etained premiums 1,833,303 1,383,788 1,811,454 (1.2) 30.9 3,314,516 3,195,243 (3.6)

Changes in technical reserves - premiums (323,391) 326,934 (132,319) (59.1) - (339,342) 194,616 -

R etained earned premiuns 1,509,912 1,710,722 1,679,136 11.2 (1.8) 2,975,174 3,389,858 13.9

Revenue of po licies issuance 2,907 6,049 3,372 16.0 (44.2) 6,662 9,421 41.4

Claims retained (471,054) (587,419) (519,480) 10.3 (11.6) (952,138) (1,106,899) 16.3

Acquisition costs (399,235) (449,869) (469,817) 17.7 4.4 (787,152) (919,686) 16.8

Administrative expenses (69,077) (93,118) (88,936) 28.7 (4.5) (143,590) (182,054) 26.8

Tax expenses (51,236) (62,762) (57,157) 11.6 (8.9) (102,613) (119,919) 16.9

Other operating income (expenses) (65,541) (64,085) (18,665) (71.5) (70.9) (95,080) (82,750) (13.0)

Underwrit ing result 456,676 459,518 528,451 15.7 15.0 901,263 987,968 9.6

N et investment inco me 146,979 190,477 168,258 14.5 (11.7) 325,206 358,735 10.3

Financial income 187,915 245,606 235,084 25.1 (4.3) 404,263 480,690 18.9

Financial expenses (40,936) (55,129) (66,826) 63.2 21.2 (79,057) (121,955) 54.3

Equity income (7,526) (7,740) (7,729) 2.7 (0.1) (15,170) (15,469) 2.0

Operat ing result 596,129 642,255 688,979 15.6 7.3 1,211,299 1,331,234 9.9

Gains or losses on non-current assets (4) (187) 4,186 - - 3 3,999 133,209.2

Earnings befo re taxes and pro f it

sharing596,125 642,068 693,165 16.3 8.0 1,211,302 1,335,233 10.2

Taxes (210,869) (260,592) (269,959) 28.0 3.6 (429,853) (530,551) 23.4

Profit sharing (3,673) (2,043) (3,781) 2.9 85.0 (7,635) (5,824) (23.7)

A djusted net inco me 381,583 379,433 419,425 9.9 10.5 773,814 798,858 3.2

Quarterly F lo w C hg. % H alf -Yearly F lo w

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 33

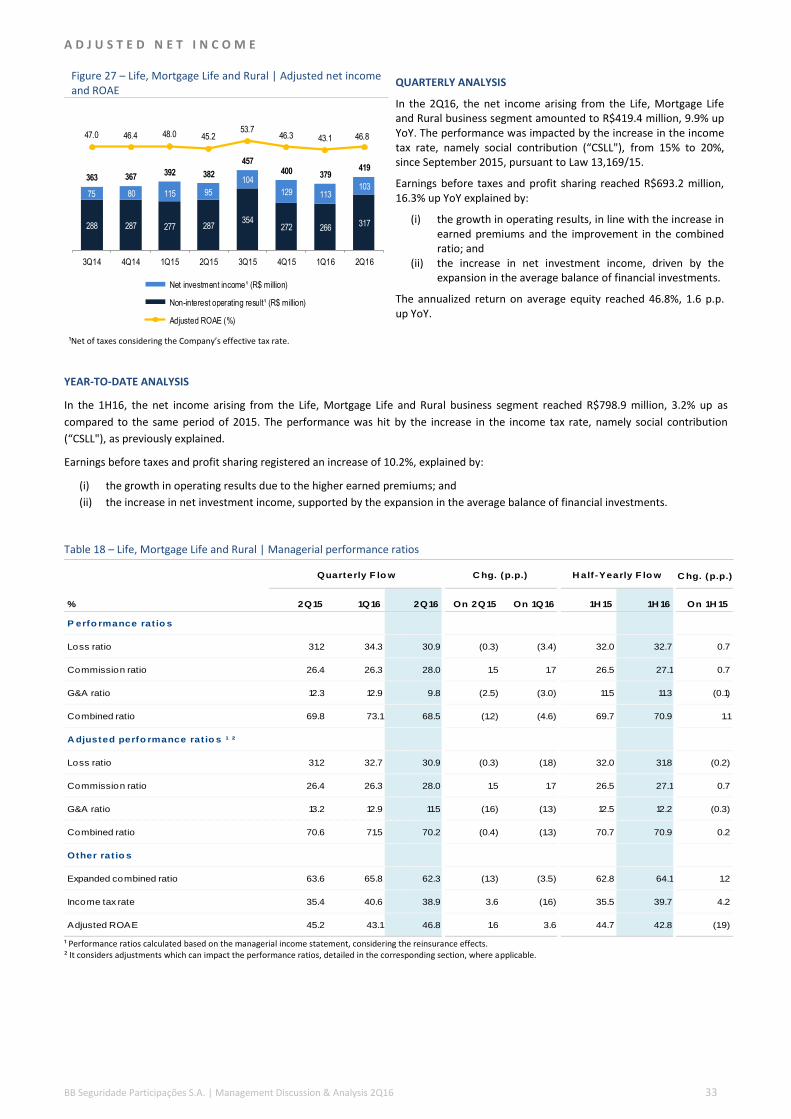

A D J U S T E D N E T I N C O M E

Figure 27 – Life, Mortgage Life and Rural | Adjusted net income and ROAE

QUARTERLY ANALYSIS

In the 2Q16, the net income arising from the Life, Mortgage Life and Rural business segment amounted to R$419.4 million, 9.9% up YoY. The performance was impacted by the increase in the income tax rate, namely social contribution (“CSLL"), from 15% to 20%, since September 2015, pursuant to Law 13,169/15.

Earnings before taxes and profit sharing reached R$693.2 million, 16.3% up YoY explained by:

(i) the growth in operating results, in line with the increase in earned premiums and the improvement in the combined ratio; and

(ii) the increase in net investment income, driven by the expansion in the average balance of financial investments.

The annualized return on average equity reached 46.8%, 1.6 p.p. up YoY.

¹Net of taxes considering the Company’s effective tax rate.

YEAR-TO-DATE ANALYSIS

In the 1H16, the net income arising from the Life, Mortgage Life and Rural business segment reached R$798.9 million, 3.2% up as

compared to the same period of 2015. The performance was hit by the increase in the income tax rate, namely social contribution

(“CSLL"), as previously explained.

Earnings before taxes and profit sharing registered an increase of 10.2%, explained by:

(i) the growth in operating results due to the higher earned premiums; and

(ii) the increase in net investment income, supported by the expansion in the average balance of financial investments.

Table 18 – Life, Mortgage Life and Rural | Managerial performance ratios

¹ Performance ratios calculated based on the managerial income statement, considering the reinsurance effects. ² It considers adjustments which can impact the performance ratios, detailed in the corresponding section, where applicable.

288 287 277 287354

272 266317

75 80 115 95

104

129 113103

363 367392 382

457400 379

419

47.0 46.4 48.0 45.253.7

46.3 43.1 46.8

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Net investment income¹ (R$ million)

Non-interest operating result¹ (R$ million)

Adjusted ROAE (%)

C hg. (p.p.)

% 2Q15 1Q16 2Q16 On 2Q15 On 1Q16 1H 15 1H 16 On 1H 15

P erfo rmance rat io s

Loss ratio 31.2 34.3 30.9 (0.3) (3.4) 32.0 32.7 0.7

Commission ratio 26.4 26.3 28.0 1.5 1.7 26.5 27.1 0.7

G&A ratio 12.3 12.9 9.8 (2.5) (3.0) 11.5 11.3 (0.1)

Combined ratio 69.8 73.1 68.5 (1.2) (4.6) 69.7 70.9 1.1

A djusted perfo rmance rat io s ¹ ²

Loss ratio 31.2 32.7 30.9 (0.3) (1.8) 32.0 31.8 (0.2)

Commission ratio 26.4 26.3 28.0 1.5 1.7 26.5 27.1 0.7

G&A ratio 13.2 12.9 11.5 (1.6) (1.3) 12.5 12.2 (0.3)

Combined ratio 70.6 71.5 70.2 (0.4) (1.3) 70.7 70.9 0.2

Other rat io s

Expanded combined ratio 63.6 65.8 62.3 (1.3) (3.5) 62.8 64.1 1.2

Income tax rate 35.4 40.6 38.9 3.6 (1.6) 35.5 39.7 4.2

Adjusted ROAE 45.2 43.1 46.8 1.6 3.6 44.7 42.8 (1.9)

Quarterly F lo w C hg. (p.p.) H alf -Yearly F lo w

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 34

U N D E R W R I T I N G R E S U L T

Figure 28 – Life, Mortgage Life and Rural | Underwriting result QUARTERLY ANALYSIS

In the 2Q16, the underwriting result grew by 15.7% YoY, driven by the 11.2% increase in earned premiums and the 1.2 p.p. improvement in the combined ratio. Such improvement in the combined ratio is explained by the lower loss and G&A ratios, partially offset by a higher commission ratio.

YEAR-TO-DATE ANALYSIS

In the 1H16, the underwriting result came 9.6% higher as compared to the same period of 2015, justified by the increase in the volume of earned premiums, partially offset by the 1.1 p.p. deterioration in the combined ratio, due to higher loss and commission ratios.

N E T I N V E S T M E N T I N C O M E

Figure 29 – Life, Mortgage Life and Rural | Net investment income (R$ million)

QUARTERLY ANALYSIS

In the 2Q16, the net investment income grew by 14.5% YoY, justified by the expansion of the average volume of financial investments, partially offset by the contraction in the net interest margin, as a result of the increase in the average yield on pending claims and obligations with insurance and reinsurance operations.

YEAR-TO-DATE ANALYSIS

In the 1H16, the net investment income grew by 10.3% YoY, explained by the increase in the average volume of financial investments, partially offset by the contraction in the net interest margin.

432 450 445 457

554

426460

528

71.0 69.8 69.7 69.8 65.171.8 73.1 68.5

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Underwriting result (R$ mill ion) Combined ratio (%)

109122

178

147 157

197 190168

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

BB Seguridade Participações S.A. | Management Discussion & Analysis 2Q16 35

U N D E R W R I T I N G R E S U L T A N A L Y S I S

P R E M I U M S W R I T T E N

Figure 30 – Life, Mortgage Life and Rural | Premiums written QUARTERLY ANALYSIS

In the 2Q16, premiums written amounted to R$2.1 billion, 12.3% higher YoY, boosted by the increase in premiums arising from rural, mainly in crop insurance, as well as in life, partially offset by the fall in credit life.

Retained premiums fell by 1.2% YoY, as a result of the larger share of the crop insurance in the mix of premiums written, as this segment presents a higher volume of premiums ceded to reinsurance.

YEAR-TO-DATE ANALYSIS

In the 1H16, premiums written amounted to R$3.6 billion, 5.4% up as compared to the 1H15, with a higher concentration in rural and in life insurance.

Figure 31 – Life, Mortgage Life and Rural | Premiums written in the bancassurance channel (R$ million)

Figure 32 – Life, Mortgage Life and Rural | Premiums written in other channels (R$ million)

Table 19 – Life, Mortgage Life and Rural | Breakdown of premiums written

Figure 33 – Life, Mortgage Life and Rural | Breakdown of premiums written (%)

Figure 34 – Life, Mortgage Life and Rural | Breakdown of retained premiums (%)

1,453

2,126

1,481 1,833 1,758 1,9341,384

1,811

99

49

61

33 336164

113

2851,553

2,175

1,542

1,867 2,094 2,098

1,497

2,097

93.6 97.7 96.1 98.2

84.0

92.2 92.486.4

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Retained premiums (R$ million) Premiums ceded (R$ million)

Retention rate (%)

1,342

1,993

1,257

1,655

1,896 1,929

1,194

1,879

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

210

182

285

212198

168

303

218

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

C hg. %