mike poteshman, executive vp and cfo january 2015/media/files/t/tupperware-ir/... · mike...

TRANSCRIPT

March 2013

Building C O N F I D E N C E

Together

Mike Poteshman, Executive VP and CFO

January 2015

We are making some forward looking statements today that use words like “outlook” or “target” or similar predictive words. Such forward looking statements involve risks and uncertainties detailed in our recent periodic reports as filed in accordance with the Securities and Exchange Act of 1934. These risks and uncertainties may cause actual results to differ materially from our statements today.

2

www.tupperwarebrands.com

Forward Looking Statements

3

Our Going Forward Objective

Sustain Tupperware Brands position as the premier, relationship-based global marketer of

quality innovative products and brands.

Commonly Asked Questions

4

Organizational Structure - how are you organized, by country, by region and globally; and what is your level of visibility into the business

Levers for sustainable growth and to mitigate external forces

Runway left in the business…near term…next decade

Uses of Cash

How the Business is Organized

5

Market: Managing Director

• Head of Sales • Head of Marketing • Head of Finance

3 Global Regions: • Americas • Europe Africa & Middle East • Asia Pacific Group President Heads of major functional areas

Corporate: CEO – Leadership Development & Strategic focus COO – Day to day operations Heads of major functional areas

Visibility

Weekly: Reporting & Calls from markets Monthly: Monthly Performance Review, Formalized calls with markets

Weekly / Daily contact Managing Directors

Daily contact Sales Force

Decentralized Structure

Germany Distributor Structure

6

2 Team Leaders

450 Demonstrators

Average German distributor has

30 Unit Managers

Sales per Distributor varies by market

Typical Country Structure

Distributor Model

7

TUPPERWARE GERMANY Est. 1962

Headquarters in Frankfurt/Main

Logistics center in Eppertshausen

Approx. 270 Team Leaders

130 Distributors Each controls a specific geography

Approx. 4,050 Unit Managers

Approx. 62,000 Demonstrators

Belgium Manufacturing & Warehouse

Tours Manufacturing

Levers for Sustainable Growth

8

Multi Local System

Formula Based on 4 Drivers:

Product Innovation

Entertaining & Informative Selling Method

Compelling Sales Force Opportunity & Structure

Solid Business Fundamentals

Our Business Model

9

OPPORTUNITY

RELATIONSHIPS

Demonstration Product

Product Innovation

10

ENGAGED LEADERSHIP

FAMILY BUSINESS

FOCUSED TERRITORY

10

BAKING & OVENWARE

KITCHEN TOOLS & GADGETS

FOOD STORAGE

Approximately 25% of Sales each year to come from new products (products introduced in the last 2 years)

MICROWAVE ON-THE-GO

& WATER

KITCHEN PREP

TABLE TOP & SERVING

CUTLERY & COOKWARE

Entertaining & Informative

Demonstration

11

Group Presentation = Party Party every 1.3 seconds

Advertising Retail Rent

Compelling Sales Force Opportunity

Earnings Opportunity Career Opportunity

12

Part-time

Supplemental

Income

Super

Seller

Demonstrator

Unit Manager

Team Leader

Distributor

Solid Channel Fundamentals

• Training

• Recognition

• Competition

• Motivation

13

Levers to Mitigate External Forces

Foreign Currency

Raw Material Pricing

Inflation

Compression in

consumer spending

Hedge transaction FX exposure/ Manage business in local currency

Global Purchasing Council

We own the shelf / Price with consumer inflation

We are Sellers

14

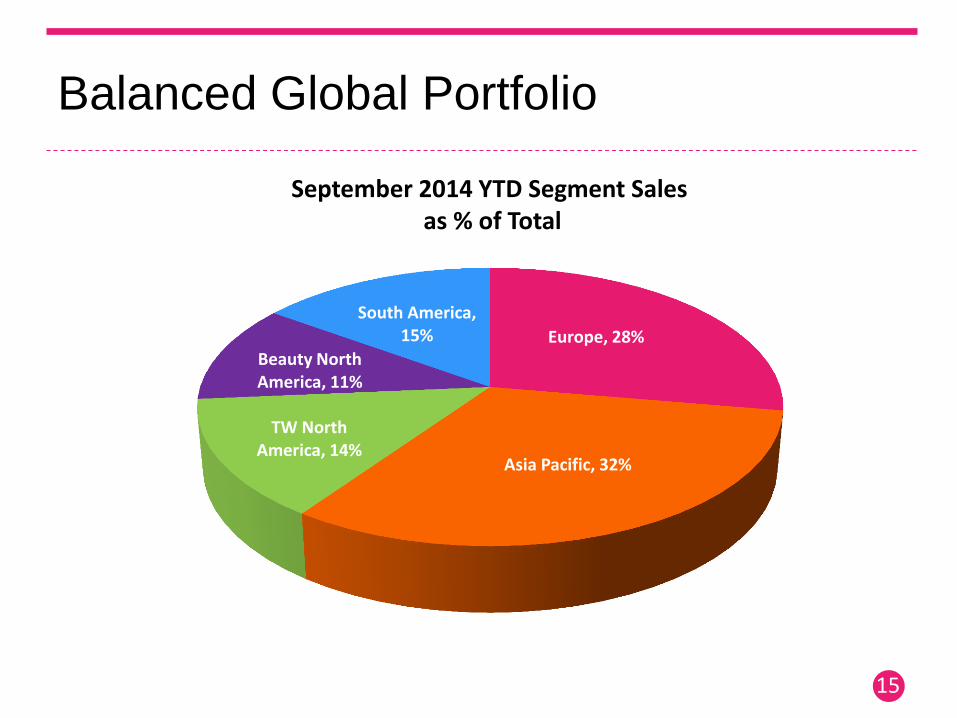

Balanced Global Portfolio

15

Europe, 28%

Asia Pacific, 32%

TW North America, 14%

Beauty North America, 11%

South America, 15%

September 2014 YTD Segment Sales as % of Total

Emerging AND Established Markets

Established Markets 14% WORLD POPULATION

Emerging Markets 86% WORLD POPULATION

WE'RE AN

AND STORY!

16

17

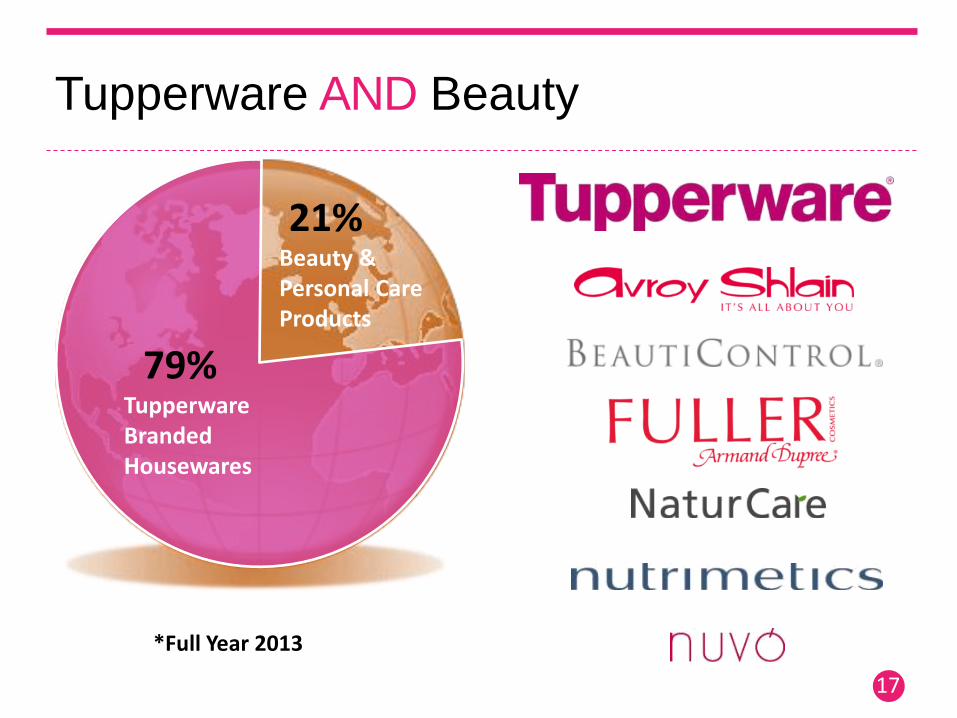

Tupperware AND Beauty

*Full Year 2013

79% Tupperware Branded Housewares

21% Beauty & Personal Care Products

TWB – Supported by Social Media

18

Tupperware Hostesses and

Fans

Host 2 Parties per Year

− Affiliation − Allegiance − Advocate

Promoters of Brand & Products

− No Rent − No Advertising

Interactive Selling System

− 2.9M Sales Force

− Party every 1.3 sec

− Driven by Earning Opportunity and Career path

Social Network

iTup

(Think Rosetta Stone)

Sales Force Webinars

Living Cook Books

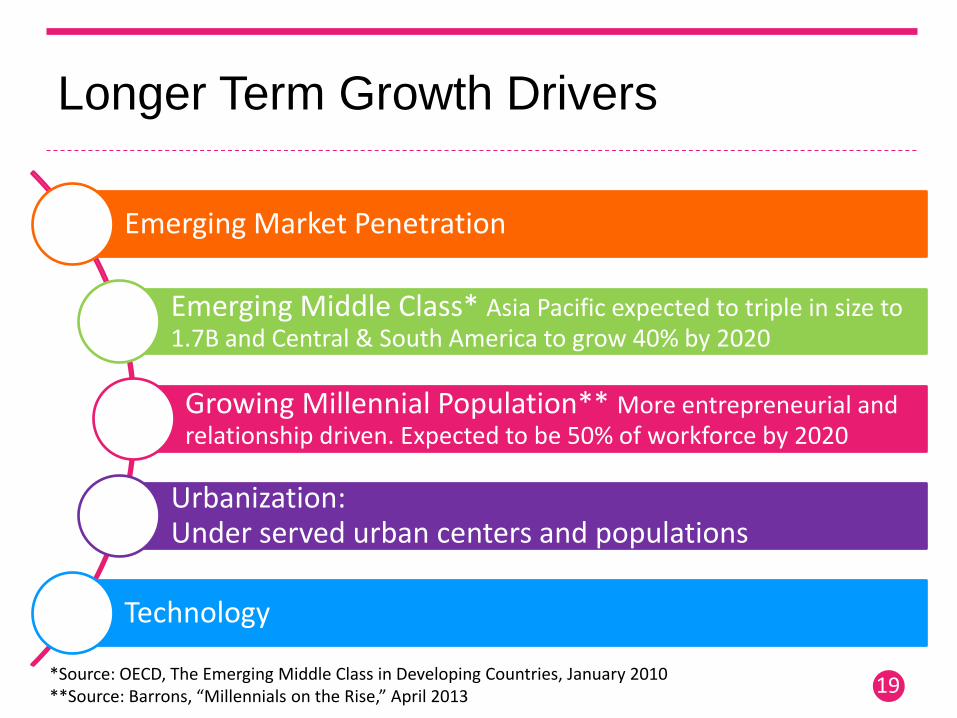

Longer Term Growth Drivers

19

Emerging Market Penetration

Emerging Middle Class* Asia Pacific expected to triple in size to 1.7B and Central & South America to grow 40% by 2020

Growing Millennial Population** More entrepreneurial and relationship driven. Expected to be 50% of workforce by 2020

Urbanization: Under served urban centers and populations

Technology

*Source: OECD, The Emerging Middle Class in Developing Countries, January 2010 **Source: Barrons, “Millennials on the Rise,” April 2013

Dynamic Emerging Market Sales

EMERGING MARKETS 66% OF

September 2014 YTD

SALES

20

+10% LC September 2014 YTD

Argentina +44%

TW Mexico +6%

Brazil +22%

Turkey +20% China

+27%

Indonesia +18%

20

Avroy Shlain +21%

Basket of Global Currencies

21

Key Sales & Profit Currencies

• Euro

• Indonesian Rupiah

• Mexican Peso

• Brazilian Real

• Malaysian Ringgit

>90% of 2013 sales and profit from

outside the U.S.

Consistently Growing Sales & EPS

$0

$1

$2

$3

$4

$5

$6

$7

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2009 2010 2011 2012 2013 2014*

Sales Diluted EPS Adjusted Diluted EPS

Sales $million Diluted EPS includes impact of non-cash purchase accounting asset impairment charges

22

EPS $Dollar

*High end of guidance range provided in October 22, 2014 Earnings Release. Impact of changes in foreign currency versus prior year are updated monthly and posted on: http://ir.tupperwarebrands.com/foreign-exchange-impact.cfm

Diluted EPS includes impact of Venezuelan devaluation from balance sheet items

Free Cash Flow (as Reported)

$0

$50

$100

$150

$200

$250

$300

2009 2010 2011 2012 2013 2014*

$M

illio

ns

Net Cash Flow before Financing Activities (Free Cash Flow) GAAP Net Income

* High end of guidance range provided in October 22, 2014 Earnings Release.

Impact of changes in foreign currency versus prior year are updated monthly and posted on:

http://ir.tupperwarebrands.com/foreign-exchange-impact.cfm 23

GAAP Net Inc. includes Impact of non-cash

Purchase Accounting Asset impairment

charges

GAAP Net Inc. includes impact from Venezuelan devaluation on balance sheet items

Business Use of Cash

Quarterly Dividends Declared

72% increase

$2.48 per share annualized

$128M

Open Market Share

Repurchases

$375M in 2013

4.6 Million Shares

Quarterly Dividends Declared

10% increase

$2.72 per share annualized

$133M

Open Market Share

Repurchases

$105M in 2014

Invest in the Business Invest in the Business

Full Year 2013 Full Year 2014

Cash Returned to Shareholders $9.54* Cash Returned to Shareholders $4.66*

*Based on full year diluted shares and for 2014 guidance provided on October 22, 2014 24

Quarterly Dividends Declared

25

$0.22 $0.25

$0.30

$0.36

$0.62

$0.68

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

1996-2009 2010 2011 2012 2013 2014*

Dividend per Share

+14%

Announce

50% Payout

target on trailing EPS ex. items

+20%

+20%

+72%

+10%

Annualized Dividend 2011 $1.20 2012 1.44 2013 2.48

2014 2.72

Local Currency Sales: +4% to 5% • Emerging Markets: up high single-digit

• Established markets: down low single-digit

EPS Excluding Items: $5.21 - $5.26 • Up 8 to 9% LC, -4 to -3% USD, vs. $5.43 in 2013

• GAAP $4.02 to $4.07

• 60 cents negative FX on EPS excluding items

Pre-Tax ROS, excluding items: 13.6% • GAAP pre-tax ROS 11.1%

• Longer range ROS increase target: 50 bp • 2013 Pre-Tax ROS 14.1%

2014 vs. 2013 translation FX -65 bp

2014 LC Operating Margin Improvement +30 bp

Incremental 2014 interest -25 bp

2014 High end pretax ROS 13.6%

2014 Full Year Outlook*

26 *Guidance range provided in October 22, 2014 Earnings Release. ROS high end.

Impact of changes in foreign currency versus prior year are updated monthly and posted on:

http://ir.tupperwarebrands.com/foreign-exchange-impact.cfm

Outlook*

Q4 2014 Full-year 2014

USD Sales* (6)% to (4)% (3)% to (2)%

GAAP EPS $1.45 – $1.50 $4.02 – $4.07

GAAP Pre-tax ROS 14.5 – 14.7% 11.0 – 11.1%

Local Currency Sales +3% to 5% +4 to 5%

EPS, excluding items** $1.55 - $1.60 $5.21 - $5.26

Pre-tax ROS, excluding items 15.4% – 15.6% 13.5% - 13.6%

FX Impact on EPS comparison, excluding items

($0.19) ($0.60)

27

*Venezuelan operating activity at 6.3, 10.8 and 50 bolivars/$ in 1Q, 2Q and 2H respectively

**GAAP to non-GAAP reconciliation attached to 3Q earnings release

27

Full Year 2014 EPS* Outlook

28

$5.43 ($0.60)

($0.10) ($0.04)

$0.13

$0.24

$0.20 $5.26

$4.50

$4.70

$4.90

$5.10

$5.30

$5.50

$5.70

$5.90

2013 FX 2013 at2014 Rates

Int Exp Tax Unalloc Ops Shares 2014

*High end of 2014 outlook range excluding items, GAAP to non-GAAP reconciliation attached to earnings release

$4.83

3% Decrease

9% Increase

* As of October 22, 2014

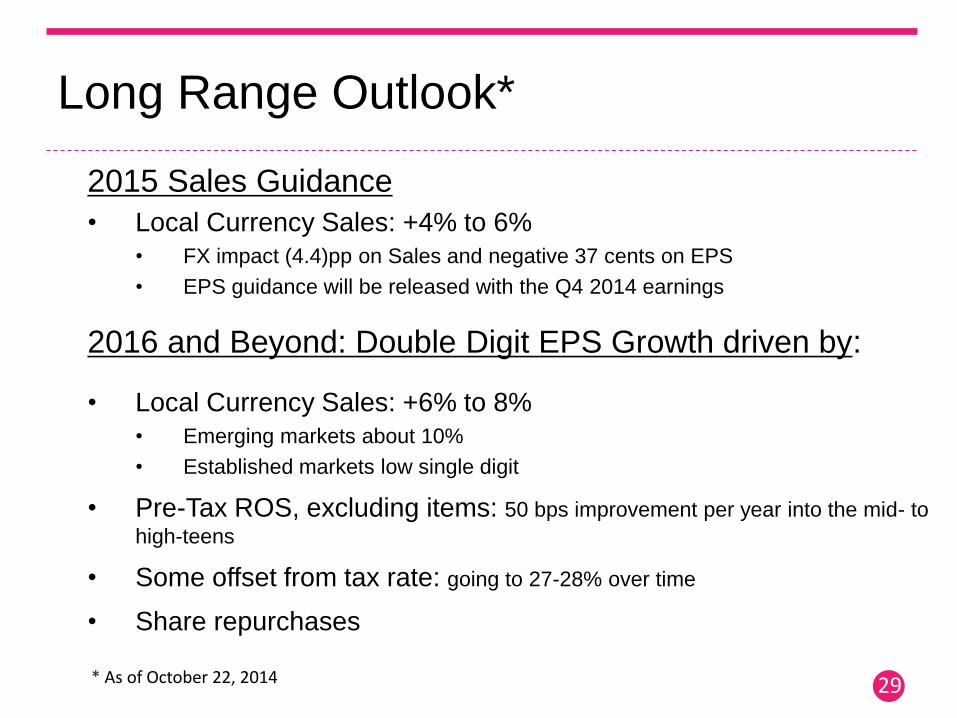

2015 Sales Guidance

• Local Currency Sales: +4% to 6%

• FX impact (4.4)pp on Sales and negative 37 cents on EPS

• EPS guidance will be released with the Q4 2014 earnings

2016 and Beyond: Double Digit EPS Growth driven by:

• Local Currency Sales: +6% to 8%

• Emerging markets about 10%

• Established markets low single digit

• Pre-Tax ROS, excluding items: 50 bps improvement per year into the mid- to

high-teens

• Some offset from tax rate: going to 27-28% over time

• Share repurchases

Long Range Outlook*

29

Non-GAAP Financial Measures

Reconciliation

2011 2012 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014* 2014*

Net Income (GAAP) $218.3 $193.0 $274.2 $52.2 $47.6 $32.3 $76.0 $208.1

Adjustments:

Gains on disposal of assets including insurance recoveries (3.8) (7.9) (0.7) (1.8) (0.5) (2.3)

Re-engineering and other restructuring costs 9.6 22.1 9.3 3.9 4.2 2.6 2.7 14.8

Impact of Venezuelan bolivar devaluation from balance

sheet positions 4.2 13.4 22.2 6.5 40.6

Swap impairment and debt cost write-off 19.8

Acquired intangible asset amortization 2.9 2.1 4.8 2.9 3.0 3.1 2.9 11.9

Purchase accounting intangibles and goodwill impairment 36.1 76.9

Income tax impact of adjustments (9.6) (4.8) (3.5) (3.7) (1.4) 1.3 (0.7) (4.4)

Net Income (Adjusted) $273.3 $281.4 $288.3 $66.9 $75.1 $45.8 $80.9 $268.7

Adjusted ROS 13.9% 14.1% 14.1% 13.5% 14.7% 10.2% 15.6% 13.6 %

Average number of diluted shares (millions) 61.4 56.4 53.1 51.1 51.1 51.0 50.7 51.1

30

*High end of guidance range provided in October 22, 2014 Earnings Release.

Impact of changes in foreign currency versus prior year are updated monthly and posted on: http://ir.tupperwarebrands.com/foreign-exchange-impact.cfm

Venezuela FX Impact in 2014

31

1H - 2014 Q3 - 2014 Q4 - 2014 FY 2014

Percentage Point Impact on

Sales from Changes in Rate (0.7pp) (3.5pp) (3.4pp) (2.1pp)

Translation Impact of Changes

in Rate on Diluted EPS

Comparison

($0.04) ($0.10) ($0.08) ($0.21)

Transaction Impacts on Net

Monetary Assets for 1H – 2014

and gain on conversion of

bolivars to U.S. dollars (Q3)*

($0.51) $0.09 ($0.08)** ($0.50)

Transaction Impacts on

Inventory Flowing thru at

Stronger Rates than Sales*

($0.12) ($0.23) $0.01** ($0.34)

*The pretax expense impact from amounts on the balance sheet when the bolivar devalued are

included in the U.S. GAAP earnings per share and return on sales data above, but not in the data

excluding items.

**Reflects tax recognized on an annualized basis under U.S. GAAP.

March 2013

Building C O N F I D E N C E

Together

Mike Poteshman, Executive VP & CFO

January 2015