mis-selling of interest rate swaps sesca conference september2013 gary player players solicitors...

TRANSCRIPT

MIS-SELLING OF INTEREST RATE SWAPSSESCA CONFERENCE SEPTEMBER2013

Gary PlayerPlayers Solicitors

Definition

• What is an interest rate swap, (an interest rate hedging product).

A complex product sold by lenders, typically, to small and medium sized businesses (SME’s) alongside a loan which were designed to protect the SME against fluctuations in the interest rate.

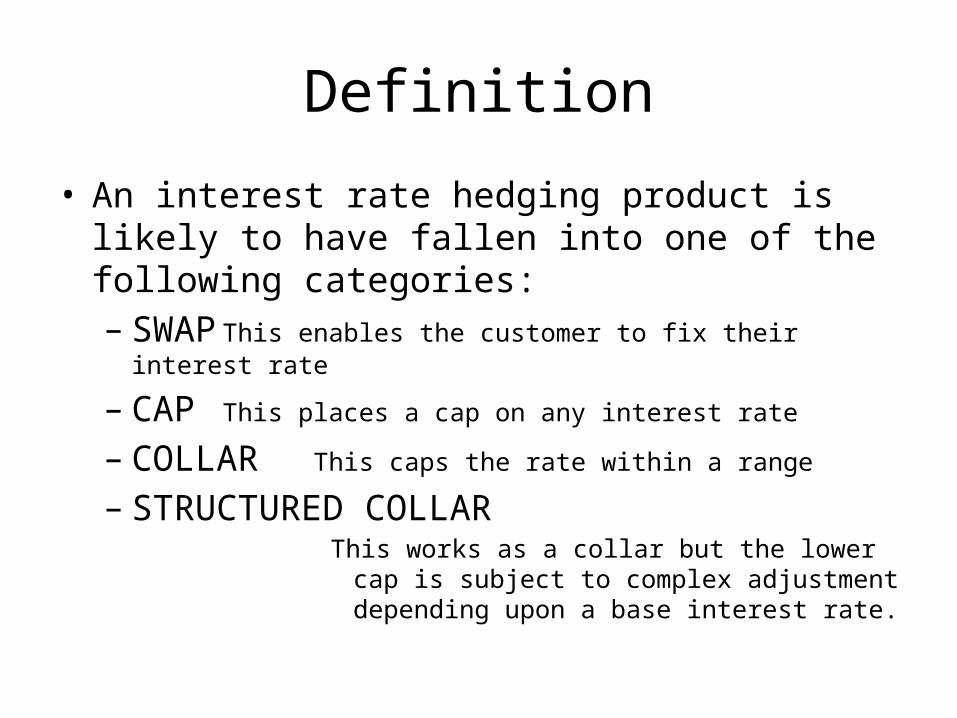

Definition

• An interest rate hedging product is likely to have fallen into one of the following categories:– SWAP This enables the customer to fix their interest rate

– CAP This places a cap on any interest rate

– COLLAR This caps the rate within a range

– STRUCTURED COLLARThis works as a collar but the lower cap is subject

to complex adjustment depending upon a base interest rate.

Definition

The purpose of the swap was supposedly to protect customers from interest rate rises with then current rates of up to 5.5%. The lenders were advising their clients that interest rates were likely to rise. However, as interest rates have tumbled to 0.5%, many customers who purchased these swaps have been left facing crippling monthly repayments and/or exorbitant costs to extricate themselves from their swap. In the most severe cases insolvency.

The FSA (now FCA) stated that:• when properly sold • in the correct circumstances• To the right customers

these complex products are appropriate to protect customers from interest rate fluctuations.However when sold to “non-sophisticated” customers without the necessary expertise the products may have been mis-sold.

Variously...• 28,000• 40,000• £10Billion worth• 90% of SME’s ...are estimated to have been mis-sold interest rate

swaps.

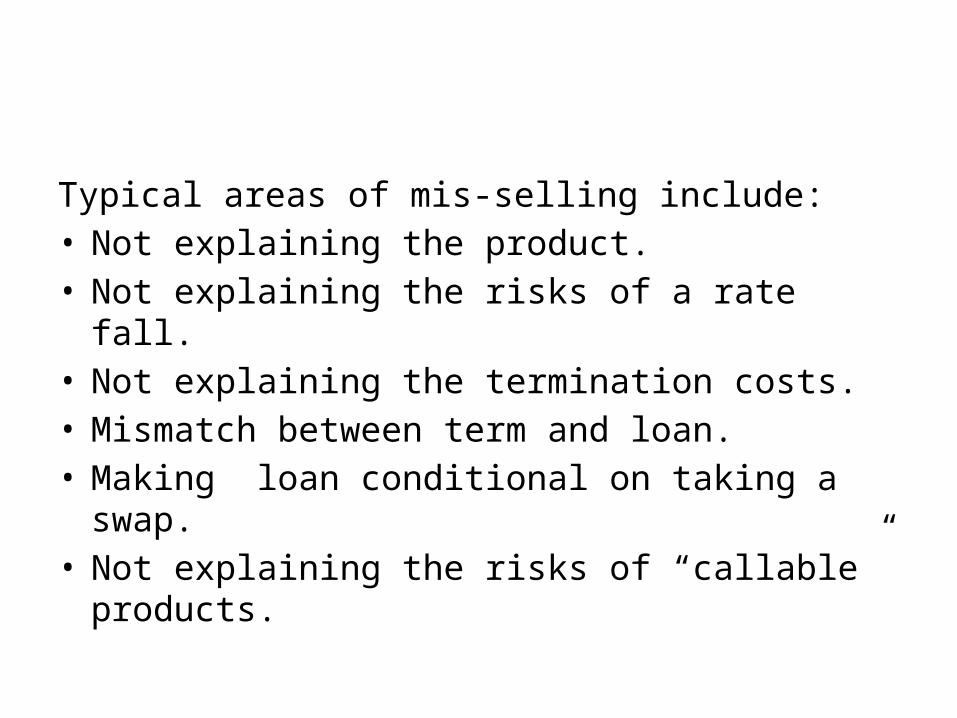

Typical areas of mis-selling include:• Not explaining the product.• Not explaining the risks of a rate fall.• Not explaining the termination costs.• Mismatch between term and loan.• Making loan conditional on taking a swap.• Not explaining the risks of “callable” products.

The allegation against the banks is that they highly incentivised sales staff to sell swaps without properly explaining the product to the non sophisticated customer. The benefits were emphasised but the risks were not explained.

In doing so the lenders breached the Conduct of Business rules and misrepresented the products to the customer giving rise to claims for damages.

Remedies

What are the remedies if you have been mis-sold a swap.

1. FCA Compensation Scheme.2. Banking Ombudsman.3. Litigation.

FCA Compensation Scheme

Following a review by the FSA in 2012 and an initial pilot scheme agreement was reached with the majority of lenders to review all sales since December 2001 and;

Provide “appropriate redress on the basis of what is fair and reasonable” to non-sophisticated customers who were sold a structured collar; and

• review sales of other swaps (except caps and structured collars) for ‘non-sophisticated’ customers and where it is considered appropriate, provide redress on the basis of what is fair and reasonable in the circumstances; and

• review the sale of caps if a complaint is made by a ‘non-sophisticated’ customer, and where it is considered appropriate, provide redress on the basis of what is fair and reasonable in the circumstances.

What is a non-sophisticated customer?If you have more than 2 of the following you are

deemed sophisticated.1 Turnover of more than £6.5M; or2 A balance sheet total of more tha £3.26M; or3 More than 50 employees.

But did the customer have the necessary knowledge and experience to understand the product.

Except where you are not.

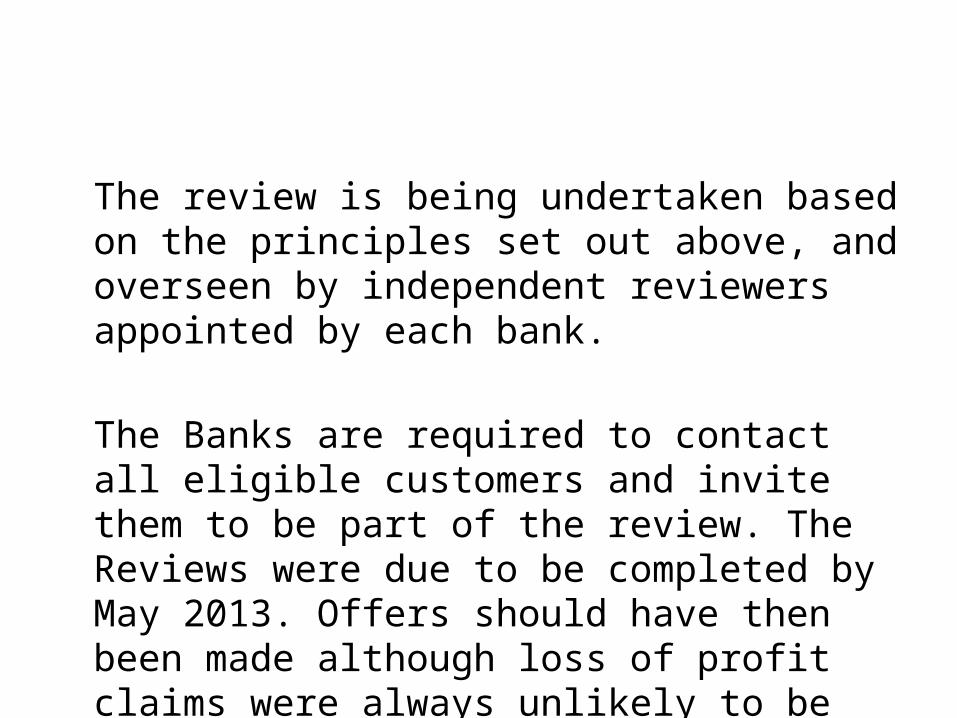

The review is being undertaken based on the principles set out above, and overseen by independent reviewers appointed by each bank.

The Banks are required to contact all eligible customers and invite them to be part of the review. The Reviews were due to be completed by May 2013. Offers should have then been made although loss of profit claims were always unlikely to be dealt with at this time.

The banks have agreed to prioritise cases where customers are in financial difficulty. The banks have also voluntarily agreed to consider suspending payments for customers in financial distress, on a case by case basis, pending the outcome of their case.

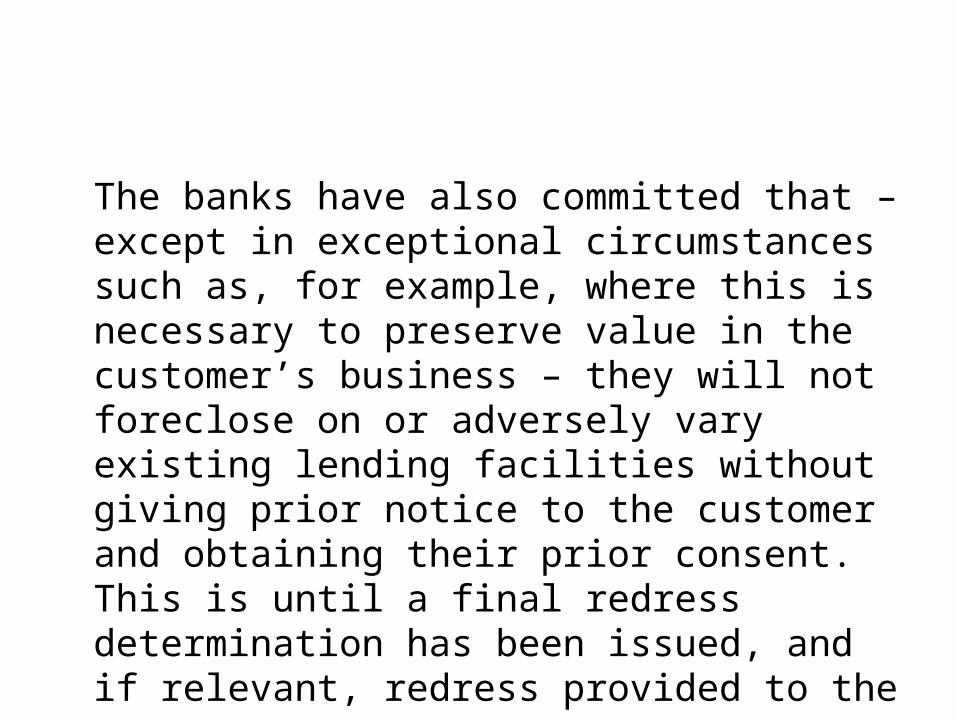

The banks have also committed that – except in exceptional circumstances such as, for example, where this is necessary to preserve value in the customer’s business – they will not foreclose on or adversely vary existing lending facilities without giving prior notice to the customer and obtaining their prior consent. This is until a final redress determination has been issued, and if relevant, redress provided to the customerCustomers are advised to continue to meet their contractual obligations.

Settlement

The banks want to settle with customers through a single offer which covers both basic redress and consequential loss on a full and final settlement basis. ”A full and final settlement provides certainty to all parties and allows customers to move on.”

In all cases, the aim of the review is to put customers back into the position they would have been in had the breach of regulatory requirements not occurred.

• ’.

The banks are expected to clearly explain to customers how they have reached their judgements, including what facts they relied on.

However the FCA do not ask the banks to show customers how they have technically calculated the redress offers, as “the independent reviewers will verify all the calculations used.”

Basic redressThere are three possible basic redress outcomes:• Some customers would never have purchased a

hedging product and will receive a ‘full tear up’ of their interest rate hedging product.

• Some customers would have chosen the same product they originally purchased whilst some customers may not have suffered any loss. These customers will receive no redress.

• Some customers would still have sought or been required to enter into a product that provided protection against interest rate movements, but would have chosen an alternative product. These customers will receive redress based on the difference between the payments they would have made on the alternative product, compared with the payments they did make

Consequential losses (the cost of being deprived of money and other losses suffered)

• Consequential losses will be assessed by referring to established legal principles relating to claims in tort and breach of statutory duty. Customers should be aware of some of the legal tests, which in broad terms are:

• The mis-sale must have caused the loss (i.e. the loss would not have happened had it not been for the bank’s regulatory breaches).

• The loss must not be too “remote”. That is, the loss must have been a reasonably foreseeable outcome of the bank’s regulatory breaches.

• Only claims that are supported by evidence will be considered.

• There is no exhaustive list of types of loss that can be claimed as consequential loss.

Other Recoveries• Bank charges.• Legal and professional fees s or claims management companies in the

review process, as the review process is being overseen by independent reviewers and such costs are unlikely to be recoverable.

• The banks will adopt the Financial Ombudsman Service’s approach to interest which is to add 8% simple interest per year to all basic redress offers.

• Customers who believe their ‘lost opportunity’ costs were more than 8% per year can make a consequential loss claim for loss of profits. For these claims, customers will need to demonstrate there were real opportunities that they were likely to have taken if it had not been for the mis-sale.

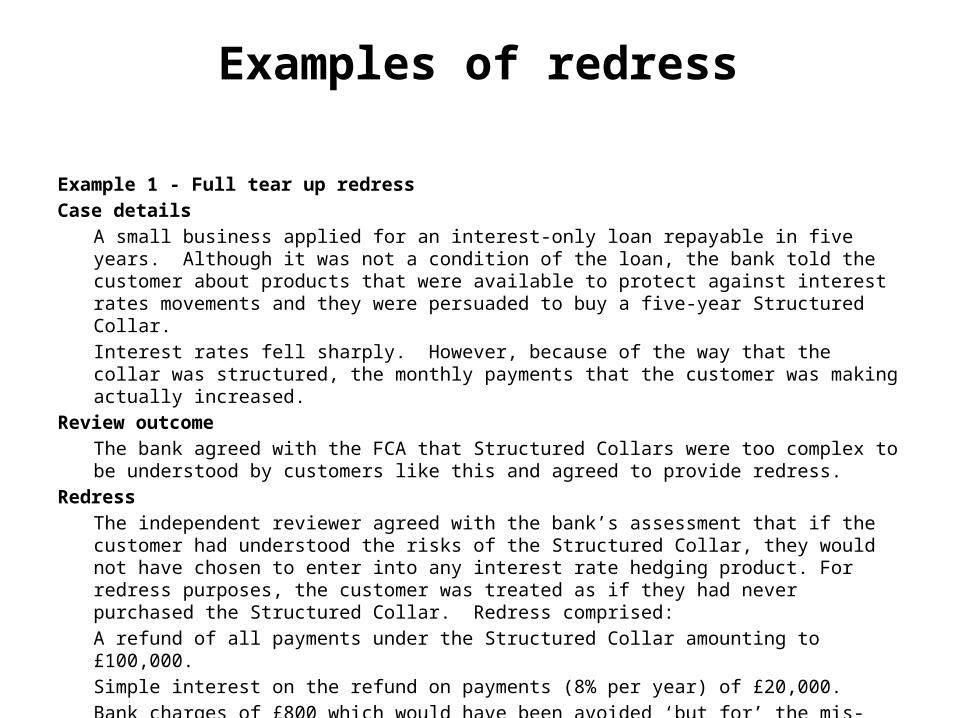

Examples of redress

Example 1 - Full tear up redressCase details

A small business applied for an interest-only loan repayable in five years. Although it was not a condition of the loan, the bank told the customer about products that were available to protect against interest rates movements and they were persuaded to buy a five-year Structured Collar. Interest rates fell sharply. However, because of the way that the collar was structured, the monthly payments that the customer was making actually increased.

Review outcomeThe bank agreed with the FCA that Structured Collars were too complex to be understood by customers like this and agreed to provide redress.

RedressThe independent reviewer agreed with the bank’s assessment that if the customer had understood the risks of the Structured Collar, they would not have chosen to enter into any interest rate hedging product. For redress purposes, the customer was treated as if they had never purchased the Structured Collar. Redress comprised:A refund of all payments under the Structured Collar amounting to £100,000.Simple interest on the refund on payments (8% per year) of £20,000.Bank charges of £800 which would have been avoided ‘but for’ the mis-sale (plus simple interest at 8%).

Example 2 - Alternative product redressCase details

A small business applied for an interest-only loan repayable in ten years. A condition of lending was that the customer was required to take out a product to protect it against interest rate movements. The customer agreed to proceed on this basis and bought a ten-year swap, to fix payments at £5,000 a month.Interest rates fell sharply. However, because the customer had fixed their payments, they were still paying £5,000 a month to service the loan and swap. The customer wanted to get out of the swap to benefit from lower interest rates and to reduce the monthly payments but was told that to do so they would have to pay an additional £200,000 of break costs.

Review outcomeThe bank and independent reviewer concluded that the customer was not given clear and fair information about the potential break costs associated with the product.

RedressThe independent reviewer agreed with the bank’s assessment that if the risks of break costs had been sufficiently disclosed, the customer would still have decided to fix their payments by entering into a swap but would have chosen a five-year term, so they were not tied in for an extended period. For redress purposes, the customer was treated as if they had originally entered into a five-year swap. Redress comprised:Cancellation of the 10 year swap.A refund of swap payments amounting to £17,000 - the difference between monthly payments made so far on the ten-year swap and the payments the customer would have made on the five-year swap until 2012 (which is when the replacement five-year swap would have ended).Simple interest (8% per year) £3,000.Refund of bank charges incurred of £200 which would have been avoided if the customer had been in the five-year swap from the start (plus simple interest at 8%).

Banking Ombudsman

Banking Ombudsman -fewer than 10 employees and an annual turnover or balance sheet that does not exceed €2 million.

Swamped with other claims and PPI.

Litigation

• So far generally unsuccessful, but...• A more sophisticated approach.• Independence• Banks reaction• Limitation and Standstill Agreements.• Jackson 1 April 2013 CFA’s.• Contingency Fees agreements/mixed agreements.

Insolvency Issues

• Identification– Current cases– New cases

• Taking Control– Administrators– Shareholders/directors

• FCA v Litigation• Funding

Groups

• Bully Banks• Claims handlers• CFA Solicitors• Banking Consultants

Case Study

Elements• Insolvent Company• Administrator/Liquidator Issue• Standstill Agreement• Funding and Investigation• FCA v Litigation

Direct Dial: 01403 711 869 Direct Fax: 01403 713 081Mobile: 07769 330 3501 Mill Lane, Partridge Green, West Sussex RH13 8JU

www.playerslaw.co.uk