module 20 capital assets. menu 1. capital assets 2. capital gains and losses 3. §1231 4....

TRANSCRIPT

Module 20Capital Assets

Menu

1. Capital assets

2. Capital gains and losses

3. §1231

4. Depreciation recapture

Capital Assets

Key Learning ObjectivesKey Learning Objectives In generalIn general Definition of a capital assetDefinition of a capital asset Special issuesSpecial issues

All Assets Are Capital Assets Except

Inventory Accounts/notes receivable from sale of

goods or services Depreciable or real property used in a trade

or business (§1231 property) Copyrights and creative works Certain U.S. government publications

Special Issues

Additional clarifications provided by Congress include: Sales or exchanges by dealers in Sales or exchanges by dealers in

securitiessecurities Sales of subdivided real estateSales of subdivided real estate Nonbusiness bad debtsNonbusiness bad debts

Capital Gains and Losses

Key Learning Objectives Sale or exchange Holding period Corporate taxpayers Individual taxpayers

Sale or Exchange

The recognition of a capital gain or loss Usually requires the sale or exchange Code doesn't define the terms "sale" and

"exchange." The Supreme Court, however, says that the

terms are to be given their ordinary meaning

Holding Period

Holding period runs from Day after acquisition date to trade date

Long vs. short controlled by code in effect on date of sale

Code states more than for holding period

Two Holding Periods for Capital Gains

Short termShort term < < 12 months12 months

Long termLong term > 12 months> 12 months

Four Tax Rates for Capital Gains for Individuals

Net short term gainsNet short term gains taxed as ordinary incometaxed as ordinary income

Net long term gainsNet long term gains taxed at 20%/10%taxed at 20%/10% taxed at 28% if “collectable”taxed at 28% if “collectable”

Some gain from real property taxed at 25%Some gain from real property taxed at 25% am’t related to unrecaptured depreciation am’t related to unrecaptured depreciation

deductionsdeductions

25% Rate onGains From Real Property

Applies to noncorporate taxpayersApplies to noncorporate taxpayers "unrecaptured Sec. 1250 gain,”"unrecaptured Sec. 1250 gain,”

Building original cost = $100,000 Building original cost = $100,000 Depreciation taken $30,000 (straight line)Depreciation taken $30,000 (straight line) Selling price $110,000Selling price $110,000 Gain = $40,000 ($110,000 - $70,000)Gain = $40,000 ($110,000 - $70,000)

$30,000 limited to 25% preference rate$30,000 limited to 25% preference rate $10,000 could be taxed at 20%/10% rates$10,000 could be taxed at 20%/10% rates

In Class Exercise: Preference Rate on Capital

Gains Single taxpayer’s taxable income for 2000 is Single taxpayer’s taxable income for 2000 is

$102,000 $102,000 If this is all ordinary income, what is her regular If this is all ordinary income, what is her regular

tax liability?tax liability? Note: use excerpt from 2000 tax rate schedules Note: use excerpt from 2000 tax rate schedules

on next slideon next slide Solution = $26,301Solution = $26,301

Note same answer if income included short term Note same answer if income included short term capital gainscapital gains

Excerpt from 2000 Tax Table

If taxable income is

At least But lessthan

The Tax is FilingStatus

63,550 132,600 14,381.5 Single90,800 147,050 20,854.5

+ 31%of excess ofincome over

Head ofHouse

taxablecolumn 1

In Class Exercise: Preference Rate on Capital

Gains Single taxpayer’s taxable income for 2000 is Single taxpayer’s taxable income for 2000 is

$102,000 $102,000 If $20,000 of this is a net long term gain, what is If $20,000 of this is a net long term gain, what is

her regular tax liability?her regular tax liability? Note: use excerpt from 2000 tax rate schedules Note: use excerpt from 2000 tax rate schedules

on previous slideon previous slide Solution = $24,101Solution = $24,101

[102,000-20,000-63,550]*.31 + 14,381.5 + 20,000 [102,000-20,000-63,550]*.31 + 14,381.5 + 20,000 *.20*.20

In Class Exercise: Preference Rate on Capital

Gains Single taxpayer’s T. I. for 2000 is $102,000 Single taxpayer’s T. I. for 2000 is $102,000 If $20,000 is from the sale of a collectible held If $20,000 is from the sale of a collectible held

more than 12 months, what is her regular tax more than 12 months, what is her regular tax liability?liability?

Note: use excerpt from 2000 tax rate schedules Note: use excerpt from 2000 tax rate schedules on earlier slideon earlier slide

Solution = $25,701Solution = $25,701 [102,000-20,000-63,550]*.31 + 14,381.5 + 20,000 [102,000-20,000-63,550]*.31 + 14,381.5 + 20,000

*.28*.28

Preference Rate forFilers in 15% Tax Bracket

Prior to 1997, filers had to have MTR> 28% Prior to 1997, filers had to have MTR> 28% before net capital gains had preference before net capital gains had preference treatmenttreatment

Long term capital gains now give all filers Long term capital gains now give all filers preferential ratespreferential rates

If filer is in 15% MTR, these gains are If filer is in 15% MTR, these gains are taxed at 10%taxed at 10%

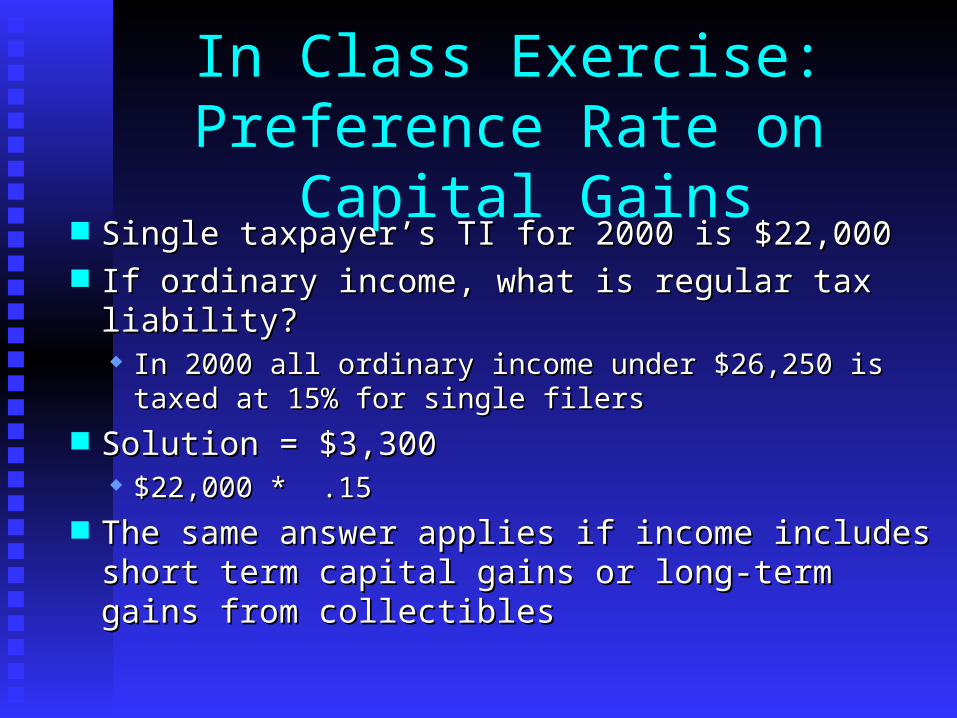

In Class Exercise: Preference Rate on Capital

Gains Single taxpayer’s TI for 2000 is $22,000 Single taxpayer’s TI for 2000 is $22,000 If ordinary income, what is regular tax liability?If ordinary income, what is regular tax liability?

In 2000 all ordinary income under $26,250 is taxed at 15% In 2000 all ordinary income under $26,250 is taxed at 15% for single filersfor single filers

Solution = $3,300Solution = $3,300 $22,000 * .15$22,000 * .15

The same answer applies if income includes short term The same answer applies if income includes short term capital gains or long-term gains from collectiblescapital gains or long-term gains from collectibles

In Class Exercise: Preference Rate on Capital

Gains Single taxpayer’s taxable income for 2000 Single taxpayer’s taxable income for 2000

is $22,000 is $22,000 If $10,000 of this is a net long term gain, If $10,000 of this is a net long term gain,

what is his regular tax liability?what is his regular tax liability? In 2000 all ordinary income under $26,250 is In 2000 all ordinary income under $26,250 is

taxed at 15% for single filerstaxed at 15% for single filers Solution = $2,800Solution = $2,800

[22,000-10,000]*.15 + 10,000 *.10[22,000-10,000]*.15 + 10,000 *.10

Netting Process

Net by holding period first Net across holding periods if they carry

opposite signs Negative and positiveNegative and positive

In Class Exercise 1: Netting Capital Gains and Losses

J&J have $100,000 of taxable income before capital gains transactions 5,000 ST Capital gain5,000 ST Capital gain 30,000 LT Capital Gain30,000 LT Capital Gain

What is J&Js net capital gain/loss position?

Solution: In Class Exercise 1: Netting Capital Gains and Losses

LT ST NET

Gain 30,000 5,000

Loss -0- -0-

Net 30,000 5,000 N/A* *Don’t net if both have same sign Only the 30,000 is a net capital gain entitled

to maximum 20% tax rate

In Class Exercise 2: Netting Capital Gains and Losses

Crumb had the following transactions for the year 2000

$25,000 long-term capital gain $12,000 long-term capital loss $8,000 short-term capital gain $15,000 short-term capital loss What is Crumb’s net capital gain/loss position?

Solution--In Class Exercise 2: Netting Capital Gains and Losses

LT ST NET Gain 25,000 8,000 Loss 12,000 15,000 Net 13,000 - 7,000 6,000* * Net again if long and short term have

different signs Only 6,000 is a net capital gain entitled to

maximum 20% (10%) tax rate

In Class Exercise 3: Netting Capital Gains and Losses

Crumb had the following transactions for the year 2000

$5,000 long-term capital gain $12,000 long-term capital loss $8,000 short-term capital gain $5,000 short-term capital loss What is Crumb’s net capital gain/loss position?

Solution--In Class Exercise 3: Netting Capital Gains and Losses

LT ST NET Gain 5,000 8,000 Loss 12,000 5,000 Net -7,000 3,000 -4,000 LTCL

Corporate Taxpayer

Net capital loss not deducted Applies to net aggregate loss, not individual

transactions Excess losses carry back (3 years) then

forward (five years) No preference rate on net LTCG

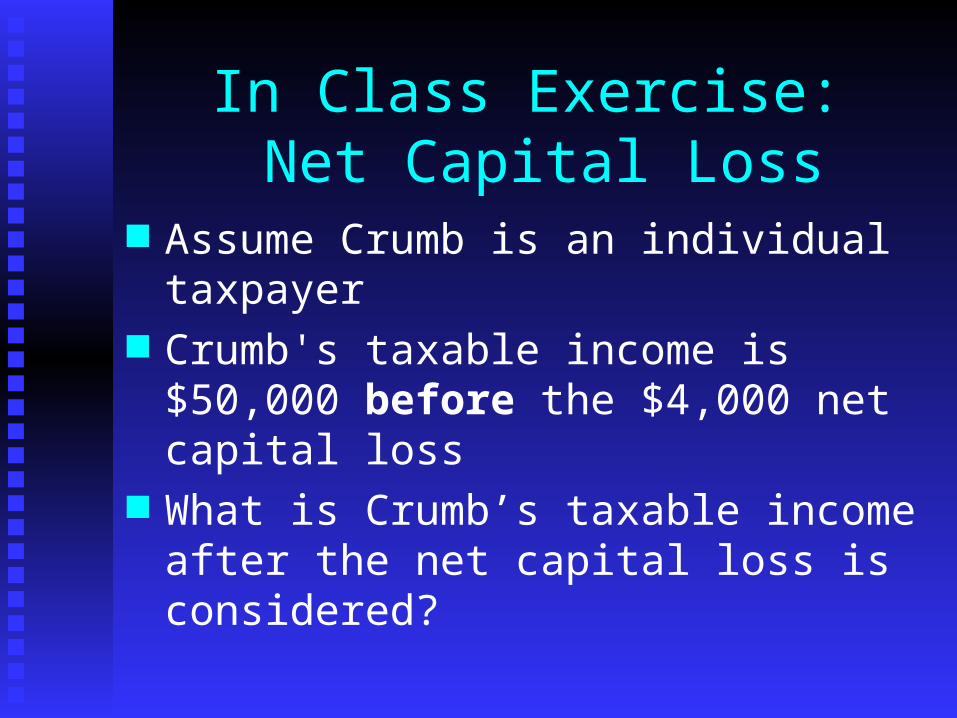

In Class Exercise:Net Capital Loss

Assume Crumb is a corporation Crumb's taxable income is $50,000 before

the $4,000 net capital loss What is Crumb’s taxable income after the

net capital loss is considered?

Solution: In Class Exercise:Net Capital Loss

Crumb’s taxable income is still $50,000 after the net capital loss is considered

Corporations may not deduct any net capital losses

However, the loss can be carried back and used against capital gains of earlier years

Individual Taxpayer

Capital losses allowed to extent of capital gains + $3,000.

Capital loss carry forward only No time limit to c/o Short/long term character retained Short-term losses are deducted first

In Class Exercise: Net Capital Loss

Assume Crumb is an individual taxpayer Crumb's taxable income is $50,000 before

the $4,000 net capital loss What is Crumb’s taxable income after the

net capital loss is considered?

Solution: In Class Exercise: Net Capital Loss

Crumb’s taxable income is $47,000 after the net capital loss is considered

Individuals can deduct up to $3,000 of net capital losses each year

The excess $1,000 loss CANNOT be carried back to earlier years

$1,000 capital loss is carried forward as a long-term capital loss to be used in future

§1231

Key Learning Objectives (1)Key Learning Objectives (1) In generalIn general §1231 property§1231 property §1231 loss§1231 loss §1231 gain§1231 gain

§1231 Property

Depreciable or real property Used in a trade or business ANDUsed in a trade or business AND Held for more than one yearHeld for more than one year

Other industry-specific property also qualifies as §1231 property

Ordinary gain/loss treatment for assets held one year or less

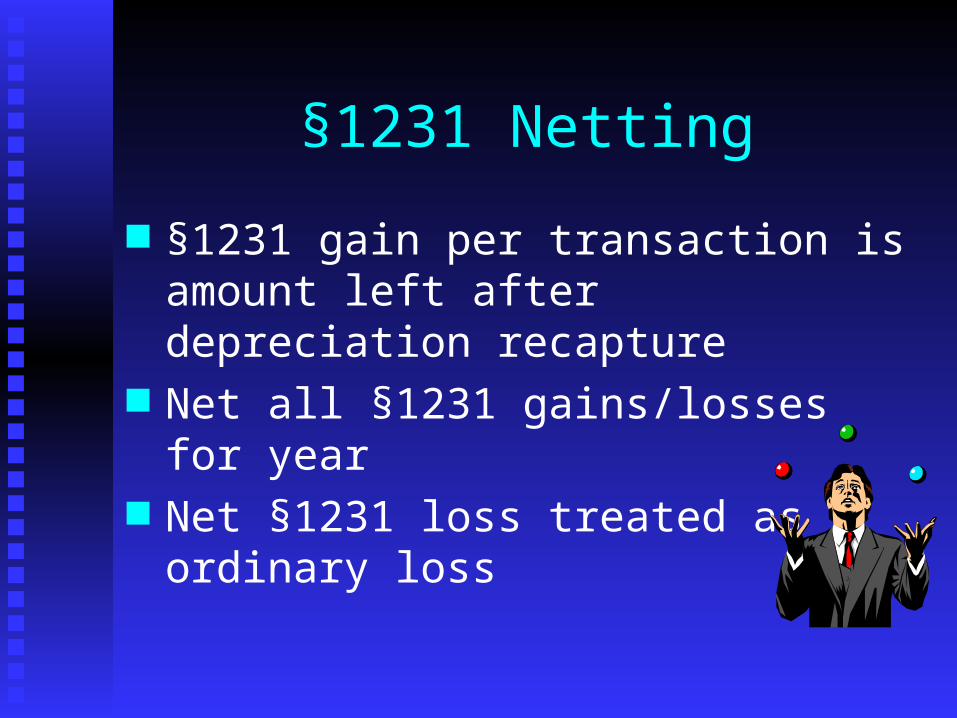

§1231 Netting

§1231 gain per transaction is amount left after depreciation recapture

Net all §1231 gains/losses for year Net §1231 loss treated as ordinary loss

§1231 Propertyif Net §1231 Gain

Lookback to determine if must recapture Prior years' §1231 ordinary losses Look back period is last 5 tax years Net §1231 gain is recharacterized as ordinary

income to extent of net §1231 losses in look back period not already recaptured

Remainder is LTCG

§1231

Key Learning Objectives (2) Gains in excess of lossesGains in excess of losses Recapture net §1231 lossesRecapture net §1231 losses Gains and losses from casualty or theftGains and losses from casualty or theft §1231 netting procedure summary§1231 netting procedure summary

In Class Exercise:Recapture Net §1231 Losses

Jan has $22,650 in net §1231 gains for 2000 Apply the lookback rule to determine how

much of this is Ordinary income?Ordinary income? LTCG?LTCG?

See next slide for Jan’s net §1231 gains and losses for the five-year look back period

In Class Exercise: Recapture Net §1231 Losses

Jan's history of § 231 net gains (losses) prior to 2000 (none before 1995)

1999 9,000 1998 (15,000) 1997 20,000 1996 (17,000) 1995 5,000

Solution--In Class Exercise: Recapture Net §1231 Losses

Start with 1995 to calculate un-recaptured net §1231 losses outstanding at 1-1-00

1995 $5,000

$5,000 net §1231 gain treated as LTCG 1996 ($17,000)

No un-recaptured §1231 losses at 1-1-96

$17,000 net §1231 loss treated as ordinary

Solution--In Class Exercise: Recapture Net §1231 Losses

1997 $20,000

$17,000 un-recaptured §1231 losses at 1-1-97

$17,000 of 20,000 treated as ordinary

$3,000 treated as LTCG 1998 ($15,000)

No un-recaptured §1231 losses at 1-1-98

$15,000 net §1231 loss treated as ordinary

Solution--In Class Exercise: Recapture Net §1231 Losses

1999 $9,000 $15,000 un-recaptured §1231 losses at 1-1-99

$ 9,000 is treated as ordinary income 2000 $22,650

$6,000 un-recaptured §1231 losses at 1-1-00

$ 6,000 of $22,650 treated as ordinary

$16,650 treated as LTCG

§1231 Property

Net §1231 gain or loss determination involves a complex 3-step netting process discussed in the text

§1231 Netting Process

Step 1 Net current year casualty gains and losses Net loss is ordinary loss Net gain is §1231 gain and goes to Step 2

§1231 Netting Process

Step 2 Net current year §1231 gains and losses Net loss is ordinary loss Net gain goes to Step 3

§1231 Netting Process

Step 3 Apply 5-year lookback Recharacterize gain as ordinary to extent of

un-recaptured §1231 losses in look back period

Remainder of gain is long-term capital gain and goes to capital gain and loss netting pool

Depreciation Recapture

Key Learning Objectives (1)Key Learning Objectives (1) In generalIn general Recovery propertyRecovery property Application to lossesApplication to losses §1245 Recapture§1245 Recapture

§1245 Depreciation Recapture

Applies to gains only, not losses Applies generally to non-real estate

i.e. 3,5,7 year MACRS propertyi.e. 3,5,7 year MACRS property §1245 recapture potential = total depreciation

taken Ordinary gain is recognized to the lesser of

§1245 recapture potential or realized gain Gain not subject to recapture is §1231 gain

In Class Exercise: §1245 Recapture

T bought a machine in 1998 for $120,000 T sold the machine in 2000 for $140,000 Total MACRS depreciation taken as of the

date of the sale was $75,000 How much should T report

As ordinary income under §1245?As ordinary income under §1245? As §1231 gain?As §1231 gain?

Solution: In Class Exercise: §1245 Recapture

T should report $75,000 of ordinary income under §1245$75,000 of ordinary income under §1245 $20,000 §1231 gain$20,000 §1231 gain

Amount realized 140,000 Cost 120,000 Depreciation 75,000 Basis 45,000 Gain 95,000 §1245 recapture 75,000

Depreciation Recapture

Key Learning Objectives (2) §1250 Property§1250 Property Additional issues §1245 and §1250Additional issues §1245 and §1250 Differences between §1245 and §1250Differences between §1245 and §1250 §291--Additional recapture for corporations§291--Additional recapture for corporations

§1250 Recapture

Applies to gains only, not losses Applies to real estate Never applies if straight-line method used Thus, no recapture for MACRS

Post-1986 realtyPost-1986 realty

Residential Realty§1250 Recapture Potential

§1250 recapture potential Excess of accelerated depreciation over

straight-line MACRS--S/L only so no recapture

In Class Exercise: §1250 Recapture--Residential

T purchased residential property for $300,000 in 1982

T sold the property in 2000 for $260,000 Total ACRS depreciation was $175,000 Straight-line depreciation would be $155,000 How much should T report

As ordinary income under §1250?As ordinary income under §1250? As §1231 gain?As §1231 gain?

Solution: In Class Exercise: §1250 Recapture Residential

T should report $20,000 of ordinary income under §1250$20,000 of ordinary income under §1250 $115,000 of §1231 gain.$115,000 of §1231 gain.

Amount realized 260,000 Cost 300,000 Depreciation 175,000 Basis 125,000 Gain 135,000

Solution: In Class Exercise: §1250 Recapture Residential

Accelerated depreciation 175,000 Straight-line depreciation 155,000 §1250 recapture 20,000 §1231 gain 115,000 Total gain 135,000

Nonresidential Realty§1250 Recapture Potential

Pre-1981 Excess of accelerated depreciation Excess of accelerated depreciation

over straight-line subject to recaptureover straight-line subject to recapture Same rule as residential realtySame rule as residential realty

ACRS (1981-1986) All depreciation subject to recaptureAll depreciation subject to recapture

MACRS--S/L only so no recapture

In Class Exercise: §1250 Recapture Non-Residential

T purchased nonresidential real property for $600,000 in 1986

T sold the property in 2000 for $460,000 Total ACRS depreciation was $345,000 Straight-line depreciation would be $315,000. How much should T report

As ordinary income under §1250?As ordinary income under §1250? As §1231 gain?As §1231 gain?

Solution: In Class Exercise: §1250 Recapture Non-Residential

T should treat this as §1245 property AND Recognize the entire $205,000 gain as ordinary Amount Realized 460,000 Cost 600,000 Depreciation 345,000 Basis 255,000 Gain 205,000

§291--Additional Recapture for Corporations

Applies to §1250 property Additional recapture is based on §1245

rules

§291--Additional Recapture for Corporations

The additional recapture amount is

20 % of the amount by which

§1245 recapture amount exceeds

§1250 recapture amount Total recapture is sum of

§1250 recapture AND

§291 amount