monthly taxation - tax concept

TRANSCRIPT

Monthly Taxation

Newsletter August, 2020

How to stay updated with Compliance Norms?

Stay Connected with Xcede ConsultechLLP for regular Compliance Updates /Advisories / Compliance Norms &Updates.

VO

LU

ME

-0

1

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 1

1. COMPLIANCE REQUIREMENT UNDER INCOME TAX ACT, 1961

Applicable

Laws/Acts

Compliance Particulars Due Dates Revised Due

Dates

Income Tax

Act, 1961

Filing of original return for the

Assessment Year 2019-20 u/s 139 (1)

30-07-2020 30-09-2020

Income Tax

Act, 1961

Filing of belated return for the

Assessment Year 2019-20 u/s 139 (4)

30-06-2020 30-09-2020

Income Tax

Act, 1961

Filing of revised return for the

Assessment Year 2019-20 u/s 139 (5)

30-06-2020 30-09-2020

Income Tax

Act, 1961

TDS/ TCS Return for quarter ending

31.03.2020 (Q4 of F.Y. 2019-20) for

Government Offices

30-06-2020 15-07-2020

Income Tax

Act, 1961

TDS/ TCS Return for 31.03.2020

(Q4 of F.Y. 2019-20) quarter

30-06-2020 31-07-2020

Income Tax

Act, 1961

Date of issuance of TDS

certificate to employees in form 16A

and other in form 16

15-07-2020 15-08-2020

Income Tax

Act, 1961

Investments for claiming deduction

under Chapter-VIA-B of the IT Act which

includes section 80C, 80D, 80G etc. for

the A.Y. 20-21 i.e. F.Y. 19-20

30-06-2020 31-07-2020

Income Tax

Act, 1961

Investment/ construction/ purchase for

claiming roll over benefit/ deduction in

respect of capital gains under sections 54

to 54GB

30-06-2020 30-09-2020

Income Tax

Act, 1961

Furnishing of Form 24G by an office of

the Government for the month of:

February 2020

March 2020

April to November 2020

15-03-2020 30-04-2020 Within 15

days from the end of the month

15-07-2020

15-07-2020

31-03-2020

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 2

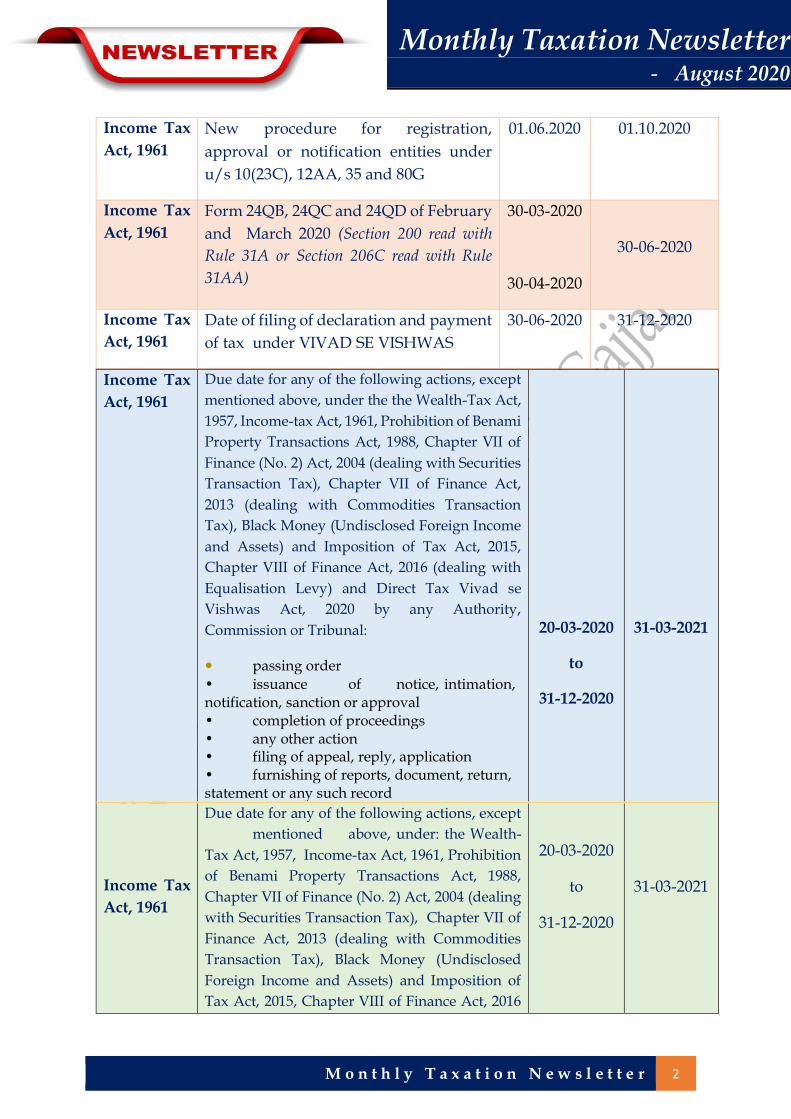

Income Tax

Act, 1961

New procedure for registration,

approval or notification entities under

u/s 10(23C), 12AA, 35 and 80G

01.06.2020 01.10.2020

Income Tax

Act, 1961

Form 24QB, 24QC and 24QD of February

and March 2020 (Section 200 read with

Rule 31A or Section 206C read with Rule

31AA)

30-03-2020

30-04-2020

30-06-2020

Income Tax

Act, 1961

Date of filing of declaration and payment

of tax under VIVAD SE VISHWAS

30-06-2020 31-12-2020

Income Tax

Act, 1961

Due date for any of the following actions, except

mentioned above, under the the Wealth-Tax Act,

1957, Income-tax Act, 1961, Prohibition of Benami

Property Transactions Act, 1988, Chapter VII of

Finance (No. 2) Act, 2004 (dealing with Securities

Transaction Tax), Chapter VII of Finance Act,

2013 (dealing with Commodities Transaction

Tax), Black Money (Undisclosed Foreign Income

and Assets) and Imposition of Tax Act, 2015,

Chapter VIII of Finance Act, 2016 (dealing with

Equalisation Levy) and Direct Tax Vivad se

Vishwas Act, 2020 by any Authority,

Commission or Tribunal:

• passing order • issuance of notice, intimation, notification, sanction or approval • completion of proceedings • any other action • filing of appeal, reply, application • furnishing of reports, document, return, statement or any such record

20-03-2020

to

31-12-2020

31-03-2021

Income Tax

Act, 1961

Due date for any of the following actions, except

mentioned above, under: the Wealth-

Tax Act, 1957, Income-tax Act, 1961, Prohibition

of Benami Property Transactions Act, 1988,

Chapter VII of Finance (No. 2) Act, 2004 (dealing

with Securities Transaction Tax), Chapter VII of

Finance Act, 2013 (dealing with Commodities

Transaction Tax), Black Money (Undisclosed

Foreign Income and Assets) and Imposition of

Tax Act, 2015, Chapter VIII of Finance Act, 2016

20-03-2020

to

31-12-2020

31-03-2021

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 3

(dealing with Equalisation Levy) and

Direct Tax Vivad se Vishwas Act, 2020

by the Taxpayers and/or Authority:

filing of appeal, reply, application

furnishing of reports, document, return, statement or any such record

Important updates:

1. ITR 1, 2, 3 & 4 are now available for e-Filing of Income Tax Returns for the AY 2020-21.

2. PAN-Aadhaar linking deadline FURTHER extended to 31st March 2021.

The due date for linking of PAN with Aadhaar as specified under sub-section 2 of Section 139AA of the Income-tax Act,1961 has been extended from 31st December, 2019 to 31st March, 2020 and further extended to 31st March, 2021 due to COVID – 19 outbreak.

3. Government to infuse Rs 50,000 crores liquidity by reducing rates of TDS, for non-salaried specified payments made to residents, and rates of Tax Collection at Source for specified receipts, to 25% of the existing rate.

4. Due date of Tax audit has been extended from 30th September 2020 to 31st October 2020.

4. The IT department has extended the date to issue Form 16 (TDS certificates) for

its employees till 15th August,2020. The due date for filing such Income tax returns has been extended to 30th November for FY 2019–20 (i.e. AY 2020-21).

5. The last date to deposit TDS Deducted under section 194IA for the month of

march is on or before 30th April of 2020. 6. In June, the government had extended the date for making investment,

construction, purchase for claiming deduction in respect of capital gains under

Sections 54 to 54GB of the Income Tax Act to September 30, 2020. Section 54 relates to tax exemptions available from capital gains if the capital gains are invested in purchase or construction of residential property. Therefore, the investment, construction, purchase made up to September 30, 2020 shall be eligible for claiming deduction from capital gains.

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 4

Important Notifications:

Sl. No. Particulars of the Notification(s) File No. / Circular No. Notification

Link(s)

1. One-time relaxation for Verification

of tax-returns for the Assessment

years 201S-16, 2016-17, 2017-18, 2018-

19 and 2019-20 which are pending

due to non-filing of ITRV form and

processing of such returns - reg.

Circular No. 13/2020/ F. No. 225/59/2020/ITA-1I

LINK

2. Clarification in relation to notification

issued under clause (v) of proviso to

section 194N of the Income-tax Act,

1961 (the Act) prior to its amendment

by Finance Act, 2020 (FA, 2020)-Reg

Circular No.14/2020 F. No. 370142/27/2020-TPL

LINK

3. Notification of Sovereign Wealth

Fund under section to(23FE) of the

Income-tax Act, 1961

Circular No. 15 of 2020 F No 370142/26/2020-TPL

LINK

4. Income-tax (16th Amendment) Rules,

2020

Notification No. 43/2020/F. No. 370142/11/2020-TPL

LINK

5. Notification of Harmonised Master

List of Infrastructure Sub-sectors for

the purposes of section 10(23FE) of

the Income-tax Act, 1961

Notification No. 44/2020/ F. No. 370142/24/2020-TPL

LINK

6. The National Pension Scheme Tier II-

Tax Saver Scheme, 2020.

Notification No. 45 /2020/ F. No.370142/26/2019-TPL

LINK

7. ‘National Aviation Security Fee Trust’

(PAN AADTN2508F)

Notification No. 46 /2020/F. No. 300196/07/2020-ITA-I

LINK

8. Notification u/s 138 (1)(ii) of the

Income-tax Act, 1961 under PM-

KISAN Yojana

F. No. 225/49/2019-ITA.II Notification No. 51 /2020

LINK

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 5

9. Notification u/s 138 of the Income-tax

ACt,1961 in respect of Intelligence

Bureau, Cabinet Secretariat, National

Investigation Agency and Narcotics

Control Bureau

F. No. 225/53/2020-IT A.II Notification No. 52 /2020

LINK

10. Income-tax (17th Amendment) Rules,

2020.

Notification No. 54/2020/F. No. 370142/22/2020-TPL

LINK

11. Income-tax (18th Amendment) Rules,

2020.

Notification No. 55/2020/ F. No.142/22/2015-TPL

LINK

12. TAXATION AND OTHER LAWS Notification No. 56/2020/ F. No. 370142/23/2020-TPL

LINK

Important Case-laws

1. SHREE CHOUDHARY TRANSPORT CO V/S ITO (SC) (SEC 194C, 40(a)(ia) (i) Disallowance u/s 40(a)(ia), 40A(3) etc are intended to enforce due compliance

of the requirement of other provisions of the Act and to ensure proper collection of tax as also transparency in dealings. The interest of a bonafide assessee who had made the deduction as required and had paid the same to the revenue is safeguarded. No question about prejudice or hardship arises

(ii) Payment made for hiring vehicles for the business of transportation of goods attracts TDS u/s 194C,

(iii) Disallowance u/s 40(a)(ia) is not limited to the amount outstanding ("payable") but also to expenses that had already been incurred and "paid" by the assessee,

(iv) Disallowance u/s 40(a)(ia) as introduced by the Finance (No.2) Act, 2004 w.e.f. 01.04.2005 is applicable to AY 2005-2006,

(v) Benefit of amendment made in the year 2014 to s. 40(a)(ia) is not available

2. MEDLEY PHARMACEUTICALS LTD V/S CIT (ITAT MUMBAI) (SEC 37)

The disallowance under the Explanation to 37(1) of "freebies" to doctors by relying on CBDT Circular No. 5 dated 01.08.2012 & the IMC (Professional Conduct, Etiquettes & Ethics) Regulation, 2002 is not justified. The code of conduct prescribed by the Medical Council is applicable only to medical practitioners/ doctors registered with the MCI and does not apply to pharmaceutical companies & the healthcare sector in any manner. The CBDT has no power to extend the scope of the MCI regulation to pharmaceutical companies without any enabling provision either under the Income tax Act or the Indian Medical Regulations (Imp judgements referred/ distinguished

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 6

3. DIT V/S SAMSUNG HEAVY INDUSTRIES CO (SC) (ARTICLE 5 – INTL. TAX)

The condition precedent for applicability of “fixed place” permanent establishments under Article 5(1) of the Double Taxation Avoidance Treaties is that it should be an establishment “through which the business of an enterprise” is wholly or partly carried on. Further, the profits of the foreign enterprise are taxable only where the said enterprise carries on its core business through a permanent establishment. The maintenance of a fixed place of business which is of a preparatory or auxiliary character in the trade or business of the enterprise would not be considered to be a permanent establishment under Article 5. Also, it is only so much of the profits of the enterprise that may be taxed in the other State as is attributable to that permanent establishment (All imp judgements referred)

4. RENU T THARANI V/S DCIT (ITAT MUMBAI) (SEC 68)

S. 68 Black Money: The sum of Rs 196 crore held by HSBC Pvt Bank, Switzerland, in the name of Tharani Family Trust, of which the assessee was a beneficiary, is assessable as the undisclosed income of the assessee. The assessee is not a public personality like Mother Terresa that some unknown person, with complete anonymity, will settle a trust to give her US $ 4 million, and in any case, Cayman Islands is not known for philanthropists operating from there; if Cayman Islands is known for anything relevant, it is known for an atmosphere conducive to hiding unaccounted wealth and money laundering. HSBC Pvt Bank has also been indicted by several Governments worldwide and how it has even confessed to be being involved in money laundering (All imp judgements on preponderance of human probabilities and ground realities referred)

2. COMPLIANCE REQUIREMENT UNDER GOODS & SERVICES TAX ACT, (GST) 2017

Keeping in view the preventive measures taken to contain the spread of Novel Coronavirus (COVID-19) and the difficulties being faced by the GST taxpayer, Ministry of Finance, Department of Revenue, Central Board of Indirect Taxes & Customs, has extended the due date for Filing GST Returns.

GSR 3B Due Dates for May 2020

A. Taxpayers having aggregate turnover > Rs. 5 Cr. in preceding FY

Tax period Due Date No interest

payable till

Interest payable @

9% from & till

Interest payable

@ 18% from

Feb, 2020 20th March,

2020

4th April,

2020

5th April to 24th June,

2020

25th June, 2020

March, 2020 20th April,

2020

5th May, 2020 6th May to 24th June,

2020

25th June, 2020

April, 2020 20th May,

2020

4th June, 2020 5th June to 24th June,

2020

25th June, 2020

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 7

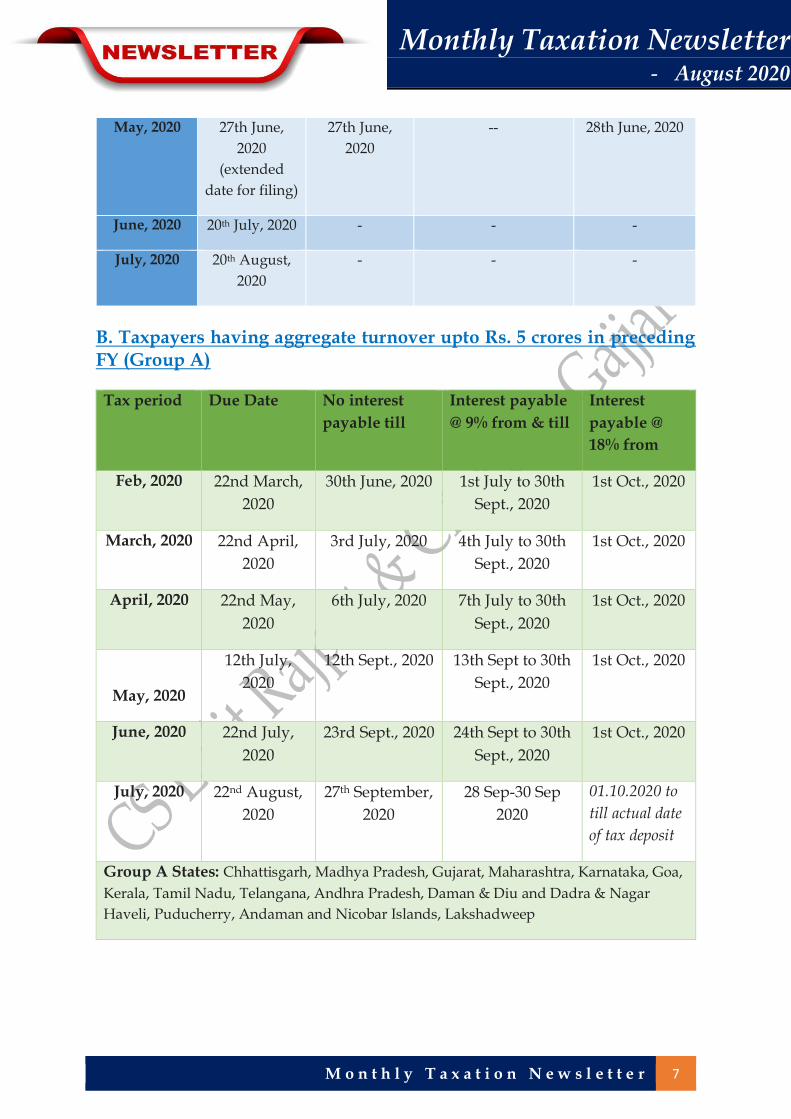

May, 2020 27th June,

2020

(extended

date for filing)

27th June,

2020

-- 28th June, 2020

June, 2020 20th July, 2020 - - -

July, 2020 20th August,

2020

- - -

B. Taxpayers having aggregate turnover upto Rs. 5 crores in preceding FY (Group A)

Tax period Due Date No interest

payable till

Interest payable

@ 9% from & till

Interest

payable @

18% from

Feb, 2020 22nd March,

2020

30th June, 2020 1st July to 30th

Sept., 2020

1st Oct., 2020

March, 2020 22nd April,

2020

3rd July, 2020 4th July to 30th

Sept., 2020

1st Oct., 2020

April, 2020 22nd May,

2020

6th July, 2020 7th July to 30th

Sept., 2020

1st Oct., 2020

May, 2020

12th July,

2020

12th Sept., 2020 13th Sept to 30th

Sept., 2020

1st Oct., 2020

June, 2020 22nd July,

2020

23rd Sept., 2020 24th Sept to 30th

Sept., 2020

1st Oct., 2020

July, 2020 22nd August,

2020

27th September,

2020

28 Sep-30 Sep

2020

01.10.2020 to

till actual date

of tax deposit

Group A States: Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa,

Kerala, Tamil Nadu, Telangana, Andhra Pradesh, Daman & Diu and Dadra & Nagar

Haveli, Puducherry, Andaman and Nicobar Islands, Lakshadweep

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 8

C. Taxpayers having aggregate turnover upto Rs. 5 crores in preceding FY (Group B)

Tax period Due Date No interest payable till

Interest payable @ 9% from & till

Interest payable @ 18% from

Feb, 2020 24th March, 2020 30th June, 2020 1st July to 30th

Sept., 2020 1st Oct., 2020

March, 2020 24th April, 2020 5th July, 2020 6th July to 30th

Sept., 2020 1st Oct., 2020

April, 2020 24th May, 2020 9th July, 2020 10th July to 30th

Sept., 2020 1st Oct., 2020

May, 2020 14th July, 2020 15th Sept.,

2020 16th Sept to 30th

Sept., 2020 1st Oct., 2020

June, 2020 24th July, 2020 25th Sept.,

2020 26th Sept to 30th

Sept., 2020 1st Oct., 2020

July, 2020 24th August, 2020 29th Sept.,

2020 30th Sept., 2020 1st Oct., 2020

Group B States: Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand, Odisha, Jammu and Kashmir, Ladakh, Chandigarh, Delhi

D. LATE FEE RELIEF TO NORMAL TAXPAYERS FILING FORM GSTR-3B

i) Taxpayers having aggregate turnover > Rs. 5 Cr. in preceding FY

Tax period Late fees waived if return filed on or before

Feb, 2020 24th June, 2020

March, 2020 24th June, 2020

April, 2020 24th June, 2020

May, 2020 30th September, 2020

(Interest is NIL for the first 15 days, 9% after 15 days till 24th June and

18% thereafter) June, 2020

July, 2020

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 9

ii) Taxpayers having aggregate turnover upto Rs. 5 crores in preceding Financial Year

Tax period Late fees waived if return filed on

or before (For Group A States)*

Late fees waived if return filed on

or before (For Group B States)*

Feb, 2020 30th June, 2020 30th June, 2020

March, 2020 03rd July, 2020 05th July, 2020

April, 2020 06th July, 2020 09th July, 2020

May, 2020 12th Sept., 2020 15th Sept., 2020

June, 2020 23rd Sept., 2020 25th Sept., 2020

July, 2020 27th Sept., 2020 29th Sept., 2020

States Group A- Chhattisgarh, Madhya Pradesh,

Gujarat, Maharashtra, Karnataka, Goa,

Kerala, Tamil Nadu, Telangana, Andhra

Pradesh, Daman & Diu and Dadra &

Nagar Haveli, Puducherry, Andaman and

Nicobar Islands, Lakshadweep

Group B- Himachal Pradesh, Punjab,

Uttarakhand, Haryana, Rajasthan, Uttar

Pradesh, Bihar, Sikkim, Arunachal

Pradesh, Nagaland, Manipur, Mizoram,

Tripura, Meghalaya, Assam, West Bengal,

Jharkhand, Odisha, Jammu and Kashmir,

Ladakh, Chandigarh, Delhi

Kindly note:

Taxpayers who are yet to file Form GSTR-3B for any month(s) from July, 2017 till Jan., 2020, can now file Form GSTR-3B from 1st July, 2020 till 30th Sept., 2020, without any late fee, for those months in which they did not have any tax liability. However, for the months they had a tax liability, their late fee is capped at Rs 500 per return.

iii) Late Fee Relief to Normal Taxpayers filing Form GSTR-1:

Tax period Due Date Waiver of late fee if return

filed on or before

March 2020 11.04.2020 10.07.2020

April 2020 11.05.2020 24.07.2020

May 2020 11.06.2020 28.07.2020

June, 2020 11.07.2020 05.08.2020

Quarterly taxpayers Jan to March 2020

30.04.2020 17.07.2020

Quarterly taxpayers April to June 2020

31.07.2020 03.08.2020

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 10

Kindly note: If the Form GSTR-3B and Form GSTR-1 for the period mentioned in Tables above is not filed by the notified dates, late fee will become payable from the due dates for these returns.

E. Compliances for Composition taxpayers

Form No. Compliance Particulars Due Date

GST CMP-08 2nd Quarter – July to September 2020 18.10.2020

GSTR-4 The yearly return for 2019-20 shall be

required to be filed in Form GSTR 4

31.08.2020

F. Non Resident Tax Payers, ISD, TDS & TCS Taxpayers - (for the month of March, April, May, June & July 2020)

Form No. Compliance

Particulars

Due Date Due Date (New)

GSTR -5

Non-Resident

Taxpayers

20th of succeeding

month

31.08.2020

GSTR -6

Input Service

Distributors

13th of succeeding

month

31.08.2020

GSTR -7

Tax Deductors at

Source (TDS

deductors)

10th of succeeding

month

31.08.2020

GSTR -8

Tax Collectors at

Source (TCS

collectors)

10th of succeeding

month

31.08.2020

G. Extension of validity period of EWB:

The validity of E-way bills (EWBs), generated on or before 24th March, 2020, and whose validity expiry date lies on or after 20th March, 2020, is deemed to have been extended till 31st August, 2020.

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 11

KEY UPDATE(s):

1. Filing NIL Form GSTR-3B through SMS on GST Portal

A taxpayer may now file NIL Form GSTR-3B, through an SMS, apart from filing it through online mode, on GST Portal. Taxpayer can file NIL Form GSTR-3B, through SMS for all GSTINs, for whom they are an Authorized Signatory, using same mobile number. Link: Click Here 2. Relief in opting for Composition by Taxpayers, filing other Returns & EWB.

Due to COVID-19 pandemic and challenges faced by taxpayers, Government has extended dates for GST filings. These are notified in Central Tax Notifications 30, 34 & 35/2020 dated 03.04.2020 & 47/2020 dated 09.06.2020 & 55/2020 dated 27.06.2020. Link: Click here 3. Normal Taxpayers wanting to opt for Composition should not file GSTR3B and GSTR 1 for any tax period of FY 2020-21 from any of the GSTIN on the associated PAN. 4. On completion of three years of GST implementation, GSTN has released a statistical report. Please click on the link below to see download. Link: Click here 5. Interim measure for filing revocation of cancellation order in appeal channel: In case your application for revocation of cancellation of registration was rejected by the tax authorities before 12/6/2020 and you wish to avail benefit of RoD order 01/2020 dated 25.06.2020, as an interim measure, you can request the appellate authority or the higher authority to pass a simple offline order on it for restoration of the application. Link: Click here

GST UPDATES TRACKER from 01.07.2020 to 31.07.2020:

Sl. No. Notification(s) Notification No. Link(s)

1.

Seeks to make eighth amendment

(2020) to CGST Rules

58/2020-Central Tax

dated 01.07.2020

LINK

2. Seeks to extend the due date for

filing FORM GSTR-4 for financial

year 2019-2020

59/2020-Central Tax

dated 13.07.2020

LINK

3. Seeks to make Ninth amendment

(2020) to CGST Rules

60/2020-Central Tax

dated 30.07.2020

LINK

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 12

4. Seeks to amend Notification no.

13/2020-Central Tax in order to

amend the class of registered

persons for the purpose of e-invoice

61/2020-Central Tax

dated 30.07.2020

LINK

5.

The Central Goods and Services Tax

(Ninth Amendment) Rules, 2020.

Gazette ID

CG-DL-E-30072020-

220781

LINK

6 The Delhi Goods and Services Tax

(Removal Of Difficulties) Order,

2019

Gazette ID

SG-DL-E-28072020-

220717

LINK

7 Amendment in the notification of

the Government of India in the

Ministry of Finance, No. 21/2019-

Central Tax, dated the 23.04.2019

[F. No. CBEC-

20/01/09/2019-GST

LINK

8 The Central Goods and Services Tax

(Eighth Amendment) Rules, 2020

Gazette ID

CG-DL-E-01072020-

220314

LINK

GST Bites

1. It seems a countrywide cartel specializing in defrauding the GST system is operating to bring the economy to its knees: Orissa HC (Case Title: Amit Beriwal v. State of Orissa & Case No.: BLAPL No. 2217/2020) Click here to read order copy : Order Copy

2. 'Retrospective amendment' in GST law: Companies file writ petition in Delhi High Court The companies claim the government amended the law prohibiting companies to avail tax credit if they had “forgotten” about it only after few companies started claiming it and even approached the courts. Many companies had claimed that when the new tax regime was introduced in July, 2017, they forgot to claim the transitional credit. Click here to read more : Source

3. CBIC notifies GST e-invoicing for businesses The government intends to implement e-invoicing or electronic submission of sales invoice to bring more transparency in sales reporting, automate data entry work, reduce errors and mismatches, capture sales related details in the system instantaneously and improve compliance. Click here to read more : Source

Monthly Taxation Newsletter - August 2020

M o n t h l y T a x a t i o n N e w s l e t t e r 13

Ease of doing Business : Initiatives under GST 1. Filing of Nil Return, GSTR-3B through SMS:

A taxpayer may now file NIL Form GSTR-3B, through an SMS,

apart from filing it through online mode, on GST Portal.

Filing of Form GSTR-3B is mandatory for all normal and casual taxpayers, even if there is no business activity in any particular tax period.

PRE-REQUISITE TO FILE NIL RETURN OF FORM GSTR-3B THROUGH SMS:

Must be registered as Normal taxpayer/ Casual taxpayer/ SEZ Unit / SEZ Developer.

Valid GSTIN.

Phone number of Authorized signatory is registered.

No pending tax liability for previous tax periods, interest or late fee.

All GSTR-3B returns for previous tax periods are filed.

No data should be in saved stage for Form GSTR-3B on the GST Portal, related to that respective month.

NIL Form GSTR-3B can be filed anytime on or after the 1st of the subsequent month for which the return is to be filed

2. Extension of various due dates:

Keeping in view the preventive measures taken to contain the spread of Novel Coronavirus (COVID-19) and the difficulties being faced by the GST taxpayer, Ministry of Finance, Department of Revenue, Central Board of Indirect Taxes & Customs, has extended the due date for Filing GST Returns. 3. GITA (GST Interactive Technical Assistant)- a Chatbot:

GSTN launched its Chatbot GITA (GST Interactive Technical Assistant), loaded with pre-drafted responses to the queries asked by taxpayers on common topics, such as- Payment, E-way bill, Registration, Refunds and Returns etc.

_______________________Thank You_____________________

“Transparency and

compliance with the

law are factors of

further development.”

- Christian Wolff

Stay

updated

with us

“Compliance” isjust a subset of“governance” andnot the other wayaround.”

― Pearl Zhu

CS Lalit Rajput !! Author!! Corporate Law !! AdvisorCompany Secretary having keen interest in the CorporateGovernance and Compliance Management and the soaringcraving to learn everyday. Aim is to dive deep in theCorporate Governance sphere and help the industry with theknowledge and practical exposure.

Cell: +91 8802581290Email: [email protected]: www.xcede.inLinkedIn: https://www.linkedin.com/in/cslalitrajput/

CA Heer Gajjar !! Author !! Taxation ExpertChartered Accountant by profession, author, learner andavid reader by obsession, explorer by passion. Withstrong adoration for entrepreneurship & self-reliance, Ialways look forward to cherishing new ideas andmentoring start-ups. Direct Taxation, Accounting andFinancial Management are my forte.

Cell: +91 9879576801Email: [email protected] LinkedIn: https://www.linkedin.com/in/heer-gajjar-516341ab/

*Every effort has been made to avoid errors or omissions in this material. In spite of this,errors may creep in. Any mistake, error or discrepancy noted may be brought to our noticewhich shall be taken care of in the next edition.IN NO EVENT THE AUTHOR SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL ORINCIDENTAL DAMAGE RESULTING FROM OR ARISING OUT OF OR IN CONNECTION WITH THE USEOF THIS INFORMATION.