morning note phillip securities research pte...

TRANSCRIPT

MICA (P) 057/11/2011 Ref No: SGMN2012_0157 1 of 16

Morning Note

Phillip Securities Research Pte Ltd Singapore

14 AUGUST 2012

Fundamental Call

Property Sector Update

Private home prices reversed from its downward correction of -0.1% in 1Q12 to +0.4% q-q growth in 2Q12, registered an all-

time high index of 206.9 points Primary sales saw consecutive lower m-m sales, possibly due to home buyers were attracted to the secondary market, where resale properties could provide immediate occupation and stable rental yield. We expect home prices to moderate by 5% to 10% by end 2013.

Office rents in the central region of Singapore continued to slide for a second quarter in 2Q12 by -0.7% q-q to $9.35psfpm. Vacancy rate in the central region dropped to 11.6% from 12.5% seen in 1Q12, due to no major completion of office property in the quarter. We expect office rent to moderate by 5% yearly in 2012 and 2013, due to slower hiring sentiments and economic growth.

The industrial property price index surged 8.4% to 168.4 and even broke the all-time high of 159.8 registered in 1Q97. While the rent index continued to gain momentum by registering 2.8% increase to 126.4 in 2Q12, rising at a faster pace than the growth registered for the past three quarters before.

High sales volume and higher capital values are likely to persist throughout the year. Industrial rents are expected to stay flat with less scope for growth as the occupiers are reluctant to significant increase in rents against the backdrop of global uncertainties.

Standard Revenue per available room (RevPAR) posted milder growth between 5.5% and 9.2% from March to May, down from 10.2% to 25.8% for the earlier three months ended in February.

RevPAR is nevertheless expected to edge up modestly given slower increase in Average Room Rate (ARR) and stable occupancy.

On the REIT front, we favour Sabana REIT for their visible and stable distributions with attractive dividend yield. We still prefer CMA with strong mall development pipeline and key retail exposures in Singapore, China and Malaysia, and

CapitaLand for its diversified portfolio. Sino Grandness Food Industry Group – Results (Lee Kok Joo) Recommendation: Accumulated Previous close: $0.455 Fair value: $0.49

Revenue growth led by higher beverage sales Beverage on track to achieve profit targets Maintain accumulate with unchanged target price of S$0.49 ComfortDelGro Corporation Ltd – Results (Derrick Heng) Recommendation: Buy Previous close: S$1.66 Fair value: S$1.78

PATMI growth of 8.5% beat our expectations Credible margins under cost pressures Stay invested in the stock

Maintain Buy with revised TP of S$1.78 Source: Phillip Securities Research Pte Ltd

MICA (P) 057/11/2011 Ref No: SGMN2012_0157 2 of 16

Market & Portfolio Outlook

- STI: +0.35% to 3064.8 - MSCI SE Asia: -0.09% to 824.6 - FTSE Asia Pac ex-Japan: -0.35% to 575.7 - Euro Stoxx 50: -0.30% to 2415.96 - S&P500: -0.13% to 1404.1 MARKET OUTLOOK: Global equities are looking fairly fatigued at this point from a technical point of view and tentative at their resistance regions - the S&P at 1400, Europe at 2400 and the APxJ at 575. The STI is presently hovering just below its upper downward trendline (connect the lower highs) and while we believe in its relative resilience (ASEAN market, SGD safe haven, yield), to break thru that trendline is likely to take some que from the broader risk market. In view of technical fatigue, some good data is required to push it higher. On the balance of risks though we would say near term upside risk for the S&P, Europe, and the ASEAN, STI is higher than downside as a slight pick-up in the US economy due to reduced inflation pressures will probably throw some hope to the market (our view though is that this will pass as a reduction in overall demand underlying trajectory). Tonight is retail sales, and economists predict a gain after 3 months of accelerating %m-m losses. In terms of events, ECB intervention into Spanish and Italian bond markets sometime early Sep is a highly likely risk-on inducing event. Short-term rallies aside, the global economic trajectory is a broad slowdown. Asia's export data has been abysmal with a big disappointment in China - NE Asia economies are suffering due to China's slowdown. EZ is for all intents and purposes in recession and a program of austerity is going to hold it back this year and next. As for the US, core capex new orders are falling, below average employment and incomes and an impending fiscal cliff make us believe in a below consensus recovery. Our SG Sector Strategist likes defensives (SCI, Comfort, Singtel), and is sector overweight Aviation Services (SIAEC, STE, SATS), and the REITS. PORTFOLIO OUTLOOK: From a medium-longer term portfolio stance we are neutral at best for stocks till 1q13 as we think absolute returns could prove fleeting due to a global slowdown and fiscal uncertainty in the US. But within the stock space we prefer & Overweight ASEAN markets - the KLCI, JCI, SETI, PSEI, STI - to be relatively more resilient. For the first 4, domestic demand and pro-growth govt policy counteracts a weak external environment. As for the STI: +60% earnings exposure to ASEAN & Emerging Markets, high dividend yields in strong business moats, and the SGD's relative safe haven status, makes the STI an attractive buy in these yield starved times. Between the asset classes, we overweight Fixed Income (ETF tickers in brackets) over Stocks, Commodities, given our global slowdown, receding inflation outlook. A repressed rate environment, is inducing a global search for yield beyond the traditional safe havens of Treasuries (TLT: NYSE), Bunds, Gilts, SGS (A35:SGX). Portfolios hard pressed for yield will likely have to explore beyond the traditional safe havens, thus within the bond space we're overweight dollar denominated EM sovereigns (EMB:NYSE), dollar denominated Asian Sovereigns & Corporates (N6M:SGX and O9P:SGX), and US Corporate Debt (VCLT:NYSE). REPORTS: Global Macro, Asset Strategy: 26 July Singapore Sector Strategy: 1 Aug

MICA (P) 057/11/2011 Ref No: SGMN2012_0157 3 of 16

Singapore Sector Reports: Banks / Transport / Telcos / Property / REITS / Thematic Regional Strategy: Indon, 17 July / HK, 22 June / Thai, 18 June / S'pore, 8 June / M'sia, 30 May / China, 24 May

Source: Phillip Securities Research Pte Ltd

Morning Note 14 August 2012

4 of 17

Macro Data

In Japan, GDP rose by an annualized 1.4% y-y in 2q12, trailing the market estimate of 2.3% y-y growth, compared to a revised 5.5% y-y expansion in 1q12. The data increases the risk that growth in the world’s third-largest economy will slow further as global demand cools just as government spending which has been underpinning the expansion wanes. The yen’s advance against the dollar is also eroding the value of overseas earnings, with exporters such as Sony Corp. and Canon Inc. cutting profit forecasts in the past month. Going forward, the government would likely conduct more loosening to bring down the currency and bolster domestic demand.

Source: Phillip Securities Research Pte Ltd

Morning Note 14 August 2012

5 of 17

Company Results

S/N Company Name Q/HY/FY Currency,

Units

Revenue Net Profit

Current Previous Change

(%) Current Previous

Change (%)

1 Comfort Delgro Q S$m 885 843 5.0% 65 60 8.5%

2 World Precision Q Rmb'000 449,649 659,290 -31.8% 71,597 100,638 -28.9%

3 Q&M Dental Q S$'000 13,003 11,096 17.2% 1,124 1,353 -16.9%

4 Banyan Tree Q S$'000 79,289 63,564 24.7% 644 -7,010 nm

5 Nam Cheong Q RM'000 149,844 131,391 14.0% 22,467 2,367 849.2%

6 Tat Hong Q S$'000 215,301 158,371 35.9% 16,655 5,478 204.0%

7 Noble Q US$'000 24,224,215 19,697,038 23.0% 194,803 139,839 39.3%

8 GSH Q US$'000 53,810 38,979 38.0% 4,083 -1,112 nm

9 Wheelock Q S$'000 116,603 67,635 72.4% 48,548 37,007 31.2%

10 Boustead Q S$'000 113,348 90,686 25.0% 12,194 8,506 43.4%

11 KSH Q S$'000 47,891 39,423 21.5% 4,315 2,599 66.0%

12 Juken Q S$'000 44,268 39,650 11.6% 2,614 2,024 29.2%

13 Tiong Seng Q S$'000 129,978 80,578 61.3% 9,740 9,220 5.6%

14 IEV FY RM'000 147,572 45,292 225.8% 11,352 6,693 69.6%

15 Centurion Q S$'000 17,030 3,133 443.6% 2,535 1,564 62.1%

16 Metro Q S$'000 44,179 42,604 3.7% 14,792 3,028 388.5%

17 CSE Global Q S$'000 144,204 101,619 41.9% 21,073 -6,999 nm

18 Hiap Seng Q S$'000 61,729 40,839 51.2% 5,662 2,490 127.4%

19 Armstrong Q S$'000 55,029 52,699 4.4% 2,133 2,092 2.0%

Morning Note 14 August 2012

6 of 17

Company Highlights

Otto Marine Limited warned on Monday that the group is likely to report a loss for the fiscal second quarter ended June 30,

2012. The group said this was due to lower utilization of the ship yard as a result of securing fewer new orders, as well as

losses from its seismic division from lower utilization of its seismic vessel. The group cited two further reasons for their

expectations: foreign exchange losses resulting from the net negative movement of the euro against the US dollar and the

Singapore dollar against the US dollar, as well as the potential impairment of its investment in certain investee companies in

view of their performance and the market conditions. (closing: S$0.086, -6.52%)

Sakari Resources Ltd announced on Monday two new coal exploration developments in Cambodia and Indonesia. The first is

a joint venture signed with The Royal Group of Cambodia - its first venture outside Indonesia - which would enable it to explore

and develop coal opportunities throughout Cambodia, as well as acquire exploration rights over prospective land holdings by

the joint venture. Sakari said that it has already started coal exploration activity over 100,000 hectares in Cambodia. It added

that it will have management control of the joint venture with 70 per cent of the initial equity, along with the obligation to fund

exploration and pre-feasibility activities. The second is a heads of agreement signed to acquire up to six mining exploration

licenses in Indonesia, covering an area of over 29,000 hectares. (closing: S$1.46, -4.89%)

Q & M Dental Group announced on Monday that it is looking to receive up to RMB 240 million (US$37.9 million) funding from

a Chinese private equity investment firm to expand its dental healthcare business into China. Q & M's wholly owned Chinese

subsiduary, Q & M Dental Group Holdings China Pte Ltd (QDHC), on Monday sealed a non-binding memorandum of

understanding with Kunwu Jiuding Capital Co Ltd for it to invest RMB192 million to RMB240 million in its other subsiduary,

Shanghai Q & M Investment Management and Consulting Co Ltd (SQM). In return, Kunwu Jiuding will get up to 20 per cent of

the increased share equity of SQM. The MOU is valid for 12 months. (closing: S$0.38, +1.88%)

Cosco Corporation (Singapore) Limited on Monday said its unit, Cosco (Dalian) Shipyard Co Ltd, has secured a US$170

million contract from Talland Navigation Limited Corporation, a subsidiary of Foresight Limited (London). The contract is for a

jack-up drilling rig based on the LeTourneau Super 116E Class design, scheduled to be delivered in the first quarter of 2015.

(closing S$0.99, +0%)

Sapphire Corporation Limited on Monday said its wholly-owned subsidiary, Neijiang Chuanwei Special Steel Co Ltd, is

acquiring Longwei Metal Product Co Ltd from Sichuan Chuanwei Group Co Ltd for 152.03 million yuan (US$23.99 million).

The purchase consideration is based on the net asset value of Longwei and the adjustment to the value of its land use rights,

and will be further adjusted on the closing date based on certain agreed upon-procedures to be performed by external auditors

to finalise the net asset value of Longwei in accordance with the terms of the Equity Transfer Agreement. Longwei is primarily

engaged in the manufacturing, selling and trading of welded pipes, welded wires, scraps and cold-rolled steel. It currently owns

two cold rolling production lines with an annual production capacity of approximately 200,000 tonnes of cold rolled steel

products, depending on the thickness of the CRC to be produced. (closing S$0.115, -0.86%) Source: SGX Masnet, The Business Times

Morning Note 14 August 2012

7 of 17

FSSTI 3,064.81 +0.35% 13,169.43 -0.29%

12.34 20,081.36 -0.27%

82.47 +0.04% 1,609.75 +0.11%

92.73 -0.15% 1.654 -0.01%Crude oil US Treasury 10yr Yield

HSIFSSTI (P/E)

Dollar Index Gold

DJI

Source: Bloomberg

2500

2700

2900

3100

3300

Aug-11

Sep-11

Oct-1

1

Nov-11

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

10500

11000

11500

12000

12500

13000

13500

Aug-11

Sep-11

Oct-1

1

Nov-11

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

15500

17500

19500

21500

23500

Aug-11

Sep-11

Oct-1

1

Nov-11

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

6

7

8

9

10

11

12

13

Aug-11

Sep-11

Oct-1

1

Nov-11

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

72

74

76

78

80

82

84

86

Aug-1

1

Sep-1

1

Oct-1

1

Nov-1

1

Dec-1

1

Jan-1

2

Feb

-12

Ma

r-12

Apr-1

2

Ma

y-12

Jun-1

2

Jul-1

2

1200

1350

1500

1650

1800

1950

Aug-11

Sep-11

Oct-1

1

Nov-11

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

70

80

90

100

110

120

Aug

-11

Sep

-11

Oct-1

1

Nov-1

1

Dec-1

1

Jan-1

2

Feb-1

2

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

1.5

2

2.5

Aug-11

Sep-11

Oct-1

1

Nov-11

Dec-11

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Morning Note 14 August 2012

8 of 17

Phillip Securities Research - Singapore Stocks Coverage

Company Analyst RatingTarget Price

(S$)

Current

Price (S$)

Difference to

Target Price

(%)

DBS GROUP HOLDINGS LTD Ken Ang Accumulate M 15.100 14.880 1.5%

OVERSEA-CHINESE BANKING CORP Ken Ang Reduce D 8.200 9.400 -12.8%

UNITED OVERSEAS BANK LTD Ken Ang Reduce M 17.900 19.980 -10.4%

GENTING SINGAPORE PLC Magdalene Choong Reduce D 1.090 1.245 -12.4%

SINGAPORE EXCHANGE LTD Ken Ang Accumulate N 6.790 6.950 -2.3%

COMFORTDELGRO CORP LTD Derrick Heng Buy M 1.650 1.655 -0.3%

SMRT CORP LTD Derrick Heng Sell M 1.350 1.660 -18.7%

NEPTUNE ORIENT LINES LTD Derrick Heng Neutral M 1.140 1.170 -2.6%

SINGAPORE AIRLINES LTD Derrick Heng Buy U 13.300 10.870 22.4%

TIGER AIRWAYS HOLDINGS LTD Derrick Heng Reduce M 0.550 0.700 -21.4%

M1 LTD Ken Ang Reduce M 2.380 2.540 -6.3%

SINGAPORE TELECOM LTD Derrick Heng Neutral D 3.310 3.390 -2.4%

STARHUB LTD Ken Ang Neutral M 3.210 3.720 -13.7%

SIA ENGINEERING CO LTD Derrick Heng Buy M 5.000 4.110 21.7%

SINGAPORE TECH ENGINEERING Derrick Heng Accumulate M 3.370 3.290 2.4%

SATS LTD Derrick Heng Neutral M 2.650 2.500 6.0%

COSCO CORP SINGAPORE LTD Phillip Research Team Reduce U 1.000 0.990 1.0%

SEMBCORP MARINE LTD Phillip Research Team Buy M 6.100 5.110 19.4%

SEMBCORP INDUSTRIES LTD Phillip Research Team Buy M 6.580 5.660 16.3%

KEPPEL CORP LTD Phillip Research Team Accumulate M 11.680 11.480 1.7%

GOLDEN AGRI-RESOURCES LTD Phillip Research Team Accumulate M 0.750 0.650 15.4%

WILMAR INTERNATIONAL LTD Phillip Research Team Buy U 4.370 3.330 31.2%

CHINA SUNSINE CHEMICAL HLDGS Lee Kok Joo Not Rated D - 0.255 -

FORELAND FABRICTECH HOLDINGS Lee Kok Joo Reduce D 0.080 0.052 53.8%

SINO GRANDNESS FOOD INDUSTRY Lee Kok Joo Accumulate M 0.490 0.455 7.7%

ZIWO HOLDINGS LTD Lee Kok Joo Sell M 0.095 0.083 14.5%

COMBINE WILL INTERNATIONAL H Chan Wai Chee Buy M 1.340 0.650 106.2%

HU AN CABLE HOLDINGS LTD Chan Wai Chee Buy U 0.275 0.131 109.9%

HENGYANG PETROCHEMICAL LOGIS Chan Wai Chee Buy I 0.610 0.210 190.5%

SUNPOWER GROUP LTD Chan Wai Chee Buy M 0.400 0.210 90.5%

STAMFORD LAND CORP LTD Chan Wai Chee Buy I 0.795 0.550 44.5%

CAPITAMALLS ASIA LTD Bryan Go Buy M 1.820 1.685 8.0%

HO BEE INVESTMENT LTD Bryan Go Neutral M 1.430 1.245 14.9%

KEPPEL LAND LTD Bryan Go Neutral M 3.300 3.470 -4.9%

OVERSEAS UNION ENTERPRISE Bryan Go Accumulate M 2.830 2.500 13.2%

SC GLOBAL DEVELOPMENTS LTD Bryan Go Neutral U 1.000 0.975 2.6%

CAPITALAND LTD Bryan Go Accumulate M 3.270 2.970 10.1%

CDL HOSPITALITY TRUSTS Travis Seah Accumulate D 2.000 1.965 1.8%

PARKWAYLIFE REAL ESTATE Travis Seah Neutral D 2.010 1.955 2.8%

SABANA SHARIAH COMP IND REIT Travis Seah Accumulate M 1.040 1.035 0.5%

US Stocks Coverage

Company Analyst RatingTarget Price

(US$)

Current

Price (US$)

Upside to

Target Price

(%)

BANK OF AMERICA CORP Magdalene Choong Neutral M - 7.720 -

CITIGROUP INC Magdalene Choong Neutral D - 28.780 -

LAS VEGAS SANDS CORP Magdalene Choong Neutral D 40.000 39.370 1.6%

WYNN RESORTS LTD Magdalene Choong Neutral D - 100.130 -

MGM RESORTS INTERNATIONAL Magdalene Choong Accumulate D 12.900 9.940 29.8%

Source: Phillip Securities Research Pte Ltd

Morning Note 14 August 2012

9 of 17

Director / Substantial Shareholders’ Transactions

Company Substantial Shareholder / Director From (%) To (%)

SAKAE HOLDINGS LTD. Goh Fuqiang, Kenneth 4.993 5.078

KEPPEL CORPORATION LIMITED Choo Chiau Beng 0.179 0.193

GIKEN SAKATA (S) LIMITED Tan Kay Guan 0 0.06

FRASER AND NEAVE, LIMITED Charoen Sirivadhanabhakdi 24.1 26.2

HERSING CORPORATION LTD Chua Wah Eng Harry 64.28 70.50

Source: SGX Masnet

Morning Note 14 August 2012

10 of 17

FTSE ST Breakdown (% Change)

STI 0.35%

0.24%

0.81%

-0.53%

-3.33%-0.19%

-0.29%

0.99%

-0.64%

-0.25%

0.68%

0.26%

1.01%

ST China

ST Real Estate

ST Re Invest Trust

ST Oil & Gas

ST Basic Materials

ST Industrials

ST Consumer Goods

ST Consumer Service

ST Telecommunicate

ST Utilites

ST Financials

ST Technology0.27%

ST Healthcare

Source: Bloomberg

FTSE ST Market Cap. Breakdown (% Change)

Top Gainers Last Chg

-0.44%

-0.40% -0.55%

ST All Share

ST Fledgling

ST Small Cap

ST Mid Cap

STI

0.35%

0.19%

▲Jardine C&C 49.450 1.000

▲DBS 14.880 0.180

▲Semb Corp 5.660 0.130

Top Losers Last Chg

▼APB 50.000 -0.990

▼JSH 500US$ 33.980 -0.690

▼JMH 400US$ 54.000 -0.250

Top Volume Last Vol

▼Genting SP 1.245 102,119

▼M Devt 0.006 56,774

▲Inno-Pac 0.050 48,501

TURNOVER (SHARES) 1,121,422,400

TURNOVER (S$) 1,003,534,579

UP 163

DOWN 224

UNCHANGED 403

Source: Bloomberg

Source: SGX

Morning Note 14 August 2012

11 of 17

Source: Bloomberg

Major World Indices

JCI -0.94% 4,102.53

HSI -0.27% 20,081.36

KLCI 0.06% 1,646.32

NIKKEI -0.07% 8,885.15

KOSPI -0.72% 1,932.44

SET 0.14% 1,219.37

SHCOMP -1.51% 2,136.08

SENSEX 0.43% 17,633.45

ASX -0.72% 4,277.30

FTSE 100 -0.26% 5,831.88

DOW -0.29% 13,169.43

S&P 500 -0.13% 1,404.11

NASDAQ 0.05% 3,022.52

COLOMBO -0.16% 4,846.45

STI 0.35% 3,064.81

ETF % Change Change Last

DB X-TRACKERS CSI300 ETF -1.34 -0.10 7.38

DB X-TRACKERS FTSE CHINA 25 -0.64 -0.17 26.58

DB X-TRACKERS FTSE VIETNAM +0.17 +0.04 23.37

DB X-TRACKERS MSCI INDONE -1.48 -0.22 14.65

DB X-TRACKERS MSCI JAPAN TRN +0.80 +0.28 35.45

DB X-TRACKERS MSCI TAIWAN +0.12 +0.02 17.09

DB X-TRACKERS MSCI WORLD TRN +0.31 +0.01 3.23

DB X-TRACKERS S&P 500 INV DA -0.22 -0.08 36.29

DB X-TRACKERS S&P CNX NIFTY +0.18 +0.18 98.44

DB X-TRACKERS S&P/ASX 200 +0.41 +0.14 34.64

DBX-TRACKERS EURO STXX 50 -0.94 -0.33 34.84

ISHARES MSCI INDIA INDEX ETF +0.36 +0.02 5.63

LYXOR ETF COMMODITIES CRB-CD +0.70 +0.02 2.88

LYXOR ETF MSCI AC ASIA EX JP +0.47 +0.02 4.30

LYXOR ETF MSCI TAIWAN +1.46 +0.01 0.90

NIKKO AM SINGAPORE STI ETF +0.97 +0.03 3.13

SPDR GOLD TRUST +0.75 +1.17 157.27

SPDR STRAITS TIMES INDEX ETF +0.32 +0.01 3.10

UNITED SSE 50 CHINA ETF -1.89 -0.03 1.56

ETF Performance

Source: Bloomberg

Morning Note 14 August 2012

12 of 17

Commodities % Chg Chg Last Price of S$1 Price of US$1

GOLD SPOT (US$/OZ) +0.11 +1.80 1,609.75 0.7639 1.0508

SILVER SPOT (US$/OZ) +0.12 +0.03 27.81 0.7968 0.9928

WTI Cushing Crude Oil Spot Price (US$/bbl) -0.15 -0.14 92.73 0.6504 1.2340

0.5114 1.5696

0.8027 1.0000

Commodities % Chg Chg Last 5.1080 6.3645

Malaysian Rubber Board Standard (MYR/kg) -2.04 -16.50 793.50 6.2276 7.7586

PALM OIL (MYR/Metric Tonne) -0.58 -16.00 2,743.50 62.8700 78.3300

906.6372 1129.6700

Index % Chg Chg Last 2.5027 3.1210

DOLLAR INDEX SPOT +0.04 +0.03 82.47 25.2408 31.4500

Source: Bloomberg

JAPANESE YEN

KOREAN WON

MALAYSIAN RINGGIT

THAI BAHT

US DOLLAR

CHINA RENMINBI

HONG KONG DOLLAR

CANADIAN DOLLAR

EURO

BRITISH POUND

Currencies

AUSTRALIAN DOLLAR

Commodities & Currencies

Maturity Today Yesterday Last Week Last Month

3 Months 0.07 0.08 0.05 0.06

6 Months 0.12 0.12 0.12 0.12

2 Years 0.26 0.26 0.23 0.23

3 Years 0.36 0.36 0.32 0.33

5 Years 0.71 0.70 0.65 0.62

10 Years 1.66 1.62 1.56 1.49

30 Years 2.75 2.73 2.65 2.57

Yield Spread (10 yrs - 3 mths)

Yield Spread (10 yrs - 2 yrs)

US Treasury Yields

1.59

1.40

Source: Data provided by ValuBond – http://w w w .valubond.com

EX Date Company Type Net Amount Currency Frequency Record Date Payout Date

8/13/2012 FISCHER TECH LTD#N/A Field Not

Applicable

#N/A Field Not

ApplicableSGD Irreg 8/15/2012 8/30/2012

8/13/2012 RAFFLES MEDICAL GROUP LTD#N/A Field Not

Applicable

#N/A Field Not

ApplicableSGD Semi-Anl 8/15/2012 8/31/2012

8/13/2012 PAN-UNITED CORP LTD#N/A Field Not

Applicable

#N/A Field Not

ApplicableSGD Semi-Anl 8/15/2012 8/28/2012

8/14/2012 SINGAPORE POST LTD Interim 0.0125 SGD Quarter 8/16/2012 8/31/2012

8/14/2012 SOUP RESTAURANT GROUP LTD Interim 0.0035 SGD Semi-Anl 8/16/2012 N.A.

8/15/2012 SWING MEDIA TECHNOLOGY GROUP Regular Cash 0.0020 SGD Annual 8/17/2012 10/5/2012

8/15/2012 HONGKONG LAND HOLDINGS LTD Interim 0.0600 USD Semi-Anl 8/17/2012 10/10/2012

8/15/2012 MANDARIN ORIENTAL INTL LTD Interim 0.0200 USD Semi-Anl 8/17/2012 N.A.

8/15/2012 DAIRY FARM INTL HLDGS LTD Interim 0.0650 USD Semi-Anl 8/17/2012 10/10/2012

8/15/2012 JARDINE MATHESON HLDGS LTD Interim 0.3500 USD Semi-Anl 8/17/2012 10/10/2012

8/15/2012 HSBC HOLDINGS PLC-SPONS ADR Regular Cash 0.4500 USD Quarter 8/17/2012 10/4/2012

8/15/2012 DBS GROUP HOLDINGS LTD Interim 0.2800 SGD Semi-Anl 8/17/2012 10/8/2012

8/15/2012 SEMBCORP MARINE LTD Interim 0.0500 SGD Semi-Anl 8/17/2012 8/31/2012

8/15/2012 STARHUB LTD 2nd Interim 0.0500 SGD Quarter 8/17/2012 8/31/2012

Corporate Action : Dividend

Source: Bloomberg

Morning Note 14 August 2012

13 of 17

Name Expected Report Date

CSE Global Ltd 8/13/2012

Armstrong Industrial Corp Ltd 8/13/2012

Best World International Ltd 8/13/2012

Pacif ic Century Regional Developments Ltd 8/13/2012

Advance SCT Ltd 8/13/2012

Informatics Education Ltd 8/13/2012

Hor Kew Corp Ltd 8/13/2012

Select Group Ltd 8/13/2012

Tat Hong Holdings Ltd 8/13/2012

Q & M Dental Group Singapore Ltd 8/13/2012

ComfortDelGro Corp Ltd 8/13/2012

Design Studio Furniture Manufacturer Ltd 8/13/2012

Inno-Pacif ic Holdings Ltd 8/13/2012

Asiasons Capital Ltd 8/13/2012

Southern Packaging Group Ltd 8/13/2012

Blumont Group Ltd 8/13/2012

CSC Holdings Ltd 8/13/2012

Ntegrator International Ltd 8/13/2012

Sinw a Ltd 8/13/2012

Wee Hur Holdings Ltd 8/13/2012

Wee Hur Holdings Ltd 8/13/2012

Rokko Holdings Ltd 8/13/2012

KSH Holdings Ltd 8/13/2012

Meiban Group Ltd 8/13/2012

Huan Hsin Holdings Ltd 8/13/2012

Hanw ell Holdings Ltd 8/13/2012

China Environment Ltd 8/13/2012

Penguin International Ltd 8/13/2012

Matex International Ltd 8/13/2012

Wilmar International Ltd 8/14/2012

Global Logistic Properties Ltd 8/14/2012

Singapore Technologies Engineering Ltd 8/14/2012

Ho Bee Investment Ltd 8/14/2012

TeleChoice International Ltd 8/14/2012

OM Holdings Ltd 8/14/2012

Zingmobile Group Ltd 8/14/2012

Vallianz Holdings Ltd 8/14/2012

Kreuz Holdings Ltd 8/14/2012

Global Testing Corp Ltd 8/14/2012

Singapore Telecommunications Ltd 8/14/2012

City Developments Ltd 8/14/2012

Indofood Agri Resources Ltd 8/14/2012

InnoTek Ltd 8/14/2012

Pan Asian Holdings Ltd 8/14/2012

First Resources Ltd 8/14/2012

WBL Corp Ltd 8/14/2012

Hong Leong Asia Ltd 8/14/2012

Sw iber Holdings Ltd 8/14/2012

CCFH Ltd 8/14/2012

Koon Holdings Ltd 8/14/2012

Guangzhao Industrial Forest Biotechnology Group Ltd 8/14/2012

Transcu Group Ltd 8/14/2012

TT International Ltd 8/14/2012

ASL Marine Holdings Ltd 8/15/2012

Maxi-Cash Financial Services Corp Ltd 8/15/2012

CNMC Goldmine Holdings Ltd 8/15/2012

Ascendas Hospitality Trust 8/15/2012

Libra Group Ltd 8/15/2012

Keong Hong Holdings Ltd 8/15/2012

Bumitama Agri Ltd 8/15/2012

Earning Announcement – Singapore

Morning Note 14 August 2012

14 of 17

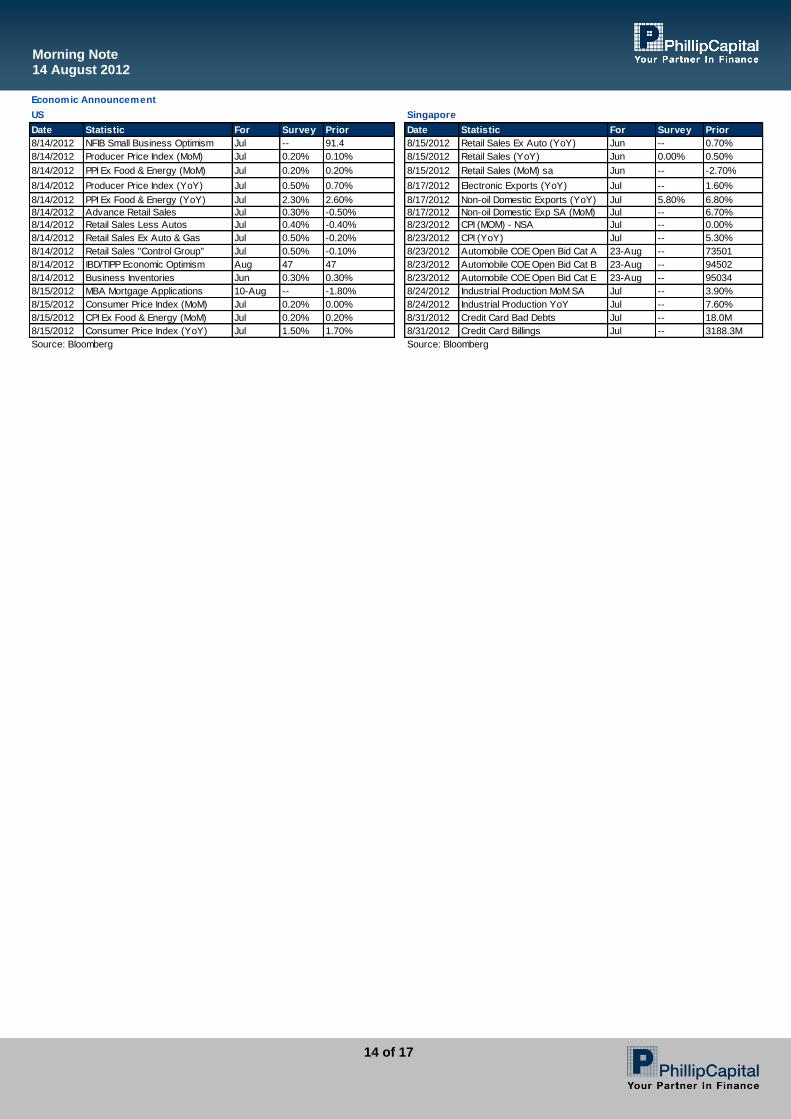

Date Statistic For Survey Prior Date Statistic For Survey Prior

8/14/2012 NFIB Small Business Optimism Jul -- 91.4 8/15/2012 Retail Sales Ex Auto (YoY) Jun -- 0.70%

8/14/2012 Producer Price Index (MoM) Jul 0.20% 0.10% 8/15/2012 Retail Sales (YoY) Jun 0.00% 0.50%

8/14/2012 PPI Ex Food & Energy (MoM) Jul 0.20% 0.20% 8/15/2012 Retail Sales (MoM) sa Jun -- -2.70%

8/14/2012 Producer Price Index (YoY) Jul 0.50% 0.70% 8/17/2012 Electronic Exports (YoY) Jul -- 1.60%

8/14/2012 PPI Ex Food & Energy (YoY) Jul 2.30% 2.60% 8/17/2012 Non-oil Domestic Exports (YoY) Jul 5.80% 6.80%

8/14/2012 Advance Retail Sales Jul 0.30% -0.50% 8/17/2012 Non-oil Domestic Exp SA (MoM) Jul -- 6.70%

8/14/2012 Retail Sales Less Autos Jul 0.40% -0.40% 8/23/2012 CPI (MOM) - NSA Jul -- 0.00%

8/14/2012 Retail Sales Ex Auto & Gas Jul 0.50% -0.20% 8/23/2012 CPI (YoY) Jul -- 5.30%

8/14/2012 Retail Sales "Control Group" Jul 0.50% -0.10% 8/23/2012 Automobile COE Open Bid Cat A 23-Aug -- 73501

8/14/2012 IBD/TIPP Economic Optimism Aug 47 47 8/23/2012 Automobile COE Open Bid Cat B 23-Aug -- 94502

8/14/2012 Business Inventories Jun 0.30% 0.30% 8/23/2012 Automobile COE Open Bid Cat E 23-Aug -- 95034

8/15/2012 MBA Mortgage Applications 10-Aug -- -1.80% 8/24/2012 Industrial Production MoM SA Jul -- 3.90%

8/15/2012 Consumer Price Index (MoM) Jul 0.20% 0.00% 8/24/2012 Industrial Production YoY Jul -- 7.60%

8/15/2012 CPI Ex Food & Energy (MoM) Jul 0.20% 0.20% 8/31/2012 Credit Card Bad Debts Jul -- 18.0M

8/15/2012 Consumer Price Index (YoY) Jul 1.50% 1.70% 8/31/2012 Credit Card Billings Jul -- 3188.3M

Source: Bloomberg

US Singapore

Economic Announcement

Source: Bloomberg

Morning Note 14 August 2012

15 of 17

Important Information

This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore (“Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication. The information contained in this publication has been obtained from public sources, which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision, including, but not limited to your reliance on the information, data and/or other materials presented in this publication. Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results. This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business

Morning Note 14 August 2012

16 of 17

from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this publication.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment. To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material. The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction. Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication. This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products. Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document. This report is only for the purpose of distribution in Singapore.

Morning Note 14 August 2012

17 of 17

Contact Information (Singapore Research Team)

Chan Wai Chee Lee Kok Joo, CFA Joshua Tan CEO, Research Head of Research Macro Strategist

Special Opportunities S-Chips, Strategy Global Macro, Asset Strategy +65 6531 1231 +65 6531 1685 +65 6531 1249

[email protected] [email protected] [email protected]

Magdalene Choong, CFA Go Choon Koay, Bryan Derrick Heng Investment Analyst Investment Analyst Investment Analyst

Gaming, US Property Transportation, Telecom. +65 6531 1791 +65 6531 1792 +65 6531 1221

[email protected] [email protected] [email protected]

Ken Ang Travis Seah Research Assistant Investment Analyst Investment Analyst General Enquiries

Financials REITS +65 6531 1240 (Phone) +65 6531 1793 +65 6531 1229 +65 6336 7607 (Fax)

[email protected] [email protected] [email protected]

Ng Weiwen Roy Chen Macro Analyst Macro Analyst

Global Macro, Asset Strategy Global Macro, Asset Strategy +65 6531 1735 +65 6531 1535

Morning Note 14 August 2012

18 of 18

Contact Information (Regional Member Companies)

SINGAPORE

Phillip Securities Pte Ltd Raffles City Tower

250, North Bridge Road #06-00 Singapore 179101

Tel : (65) 6533 6001 Fax : (65) 6535 6631

Website: www.poems.com.sg

MALAYSIA

Phillip Capital Management Sdn Bhd B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450

Kuala Lumpur Tel (603) 21628841 Fax (603) 21665099

Website: www.poems.com.my

HONG KONG

Phillip Securities (HK) Ltd Exchange Participant of the Stock Exchange of Hong Kong

11/F United Centre 95 Queensway Hong Kong

Tel (852) 22776600 Fax (852) 28685307

Websites: www.phillip.com.hk

JAPAN

Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku,

Tokyo 103-0026 Tel: (81-3) 3666-2101 Fax: (81-3) 3666-6090

Website:www.phillip.co.jp

INDONESIA

PT Phillip Securities Indonesia ANZ Tower Level 23B,

Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia

Tel (62-21) 57900800 Fax (62-21) 57900809

Website: www.phillip.co.id

CHINA

Phillip Financial Advisory (Shanghai) Co. Ltd No 550 Yan An East Road,

Ocean Tower Unit 2318, Postal code 200001

Tel (86-21) 51699200 Fax (86-21) 63512940

Website: www.phillip.com.cn

THAILAND

Phillip Securities (Thailand) Public Co. Ltd 15th Floor, Vorawat Building,

849 Silom Road, Silom, Bangrak, Bangkok 10500 Thailand

Tel (66-2) 6351700 / 22680999 Fax (66-2) 22680921

Website www.phillip.co.th

FRANCE

King & Shaxson Capital Limited 3rd Floor, 35 Rue de la Bienfaisance 75008

Paris France Tel (33-1) 45633100 Fax (33-1) 45636017

Website: www.kingandshaxson.com

UNITED KINGDOM

King & Shaxson Capital Limited 6th Floor, Candlewick House,

120 Cannon Street, London, EC4N 6AS

Tel (44-20) 7426 5950 Fax (44-20) 7626 1757

Website: www.kingandshaxson.com

UNITED STATES

Phillip Futures Inc 141 W Jackson Blvd Ste 3050

The Chicago Board of Trade Building Chicago, IL 60604 USA

Tel +1.312.356.9000 Fax +1.312.356.9005

AUSTRALIA

Octa Phillip Securities Ltd Level 12, 15 William Street,

Melbourne, Victoria 3000, Australia Tel (03) 9629 8288 Fax (03) 9629 8882

Website: www.octaphillip.com