mortgage factsheet v

TRANSCRIPT

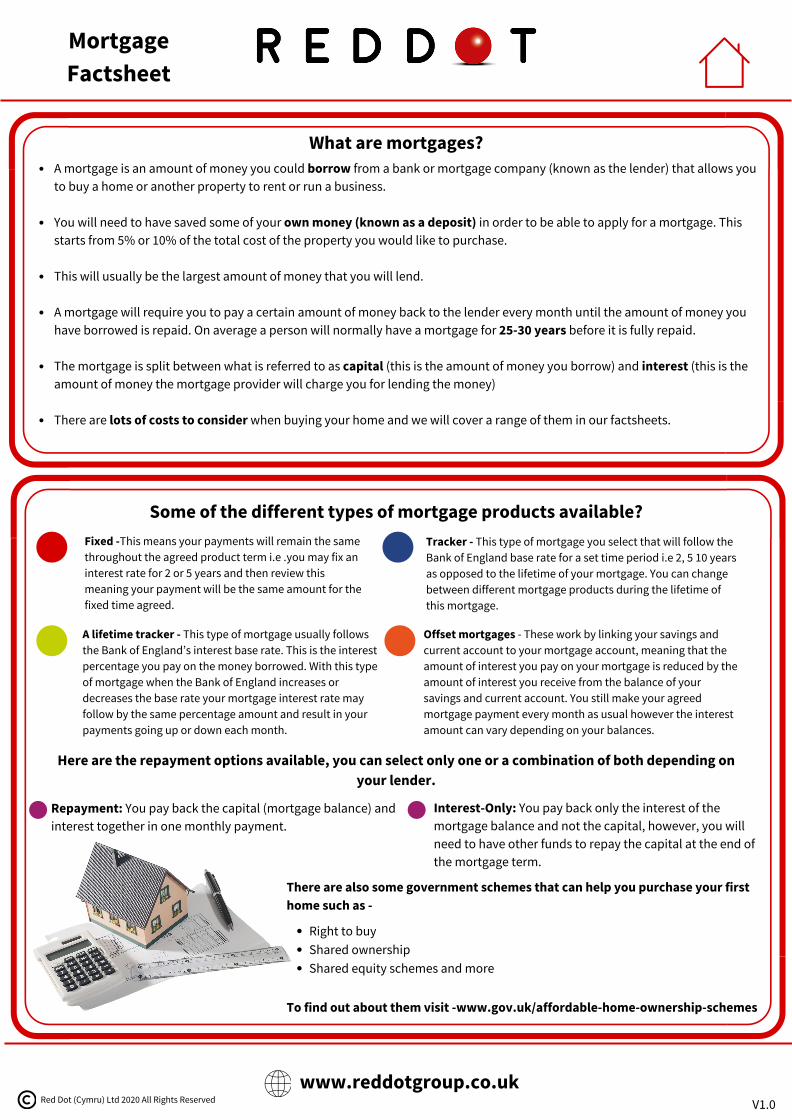

A mortgage is an amount of money you could borrow from a bank or mortgage company (known as the lender) that allows youto buy a home or another property to rent or run a business.

You will need to have saved some of your own money (known as a deposit) in order to be able to apply for a mortgage. Thisstarts from 5% or 10% of the total cost of the property you would like to purchase.

This will usually be the largest amount of money that you will lend.

A mortgage will require you to pay a certain amount of money back to the lender every month until the amount of money youhave borrowed is repaid. On average a person will normally have a mortgage for 25-30 years before it is fully repaid.

The mortgage is split between what is referred to as capital (this is the amount of money you borrow) and interest (this is theamount of money the mortgage provider will charge you for lending the money)

There are lots of costs to consider when buying your home and we will cover a range of them in our factsheets.

Mortgage Factsheet

What are mortgages?

Some of the different types of mortgage products available?Fixed -This means your payments will remain the samethroughout the agreed product term i.e .you may fix aninterest rate for 2 or 5 years and then review thismeaning your payment will be the same amount for thefixed time agreed.

Tracker - This type of mortgage you select that will follow theBank of England base rate for a set time period i.e 2, 5 10 yearsas opposed to the lifetime of your mortgage. You can changebetween different mortgage products during the lifetime ofthis mortgage.

A lifetime tracker - This type of mortgage usually followsthe Bank of England’s interest base rate. This is the interestpercentage you pay on the money borrowed. With this typeof mortgage when the Bank of England increases ordecreases the base rate your mortgage interest rate mayfollow by the same percentage amount and result in yourpayments going up or down each month.

Repayment: You pay back the capital (mortgage balance) andinterest together in one monthly payment.

Interest-Only: You pay back only the interest of themortgage balance and not the capital, however, you willneed to have other funds to repay the capital at the end ofthe mortgage term.

Here are the repayment options available, you can select only one or a combination of both depending onyour lender.

Offset mortgages - These work by linking your savings andcurrent account to your mortgage account, meaning that theamount of interest you pay on your mortgage is reduced by theamount of interest you receive from the balance of yoursavings and current account. You still make your agreedmortgage payment every month as usual however the interestamount can vary depending on your balances.

Right to buyShared ownershipShared equity schemes and more

There are also some government schemes that can help you purchase your firsthome such as -

To find out about them visit -www.gov.uk/affordable-home-ownership-schemes

www.reddotgroup.co.ukV1.0Red Dot (Cymru) Ltd 2020 All Rights Reserved

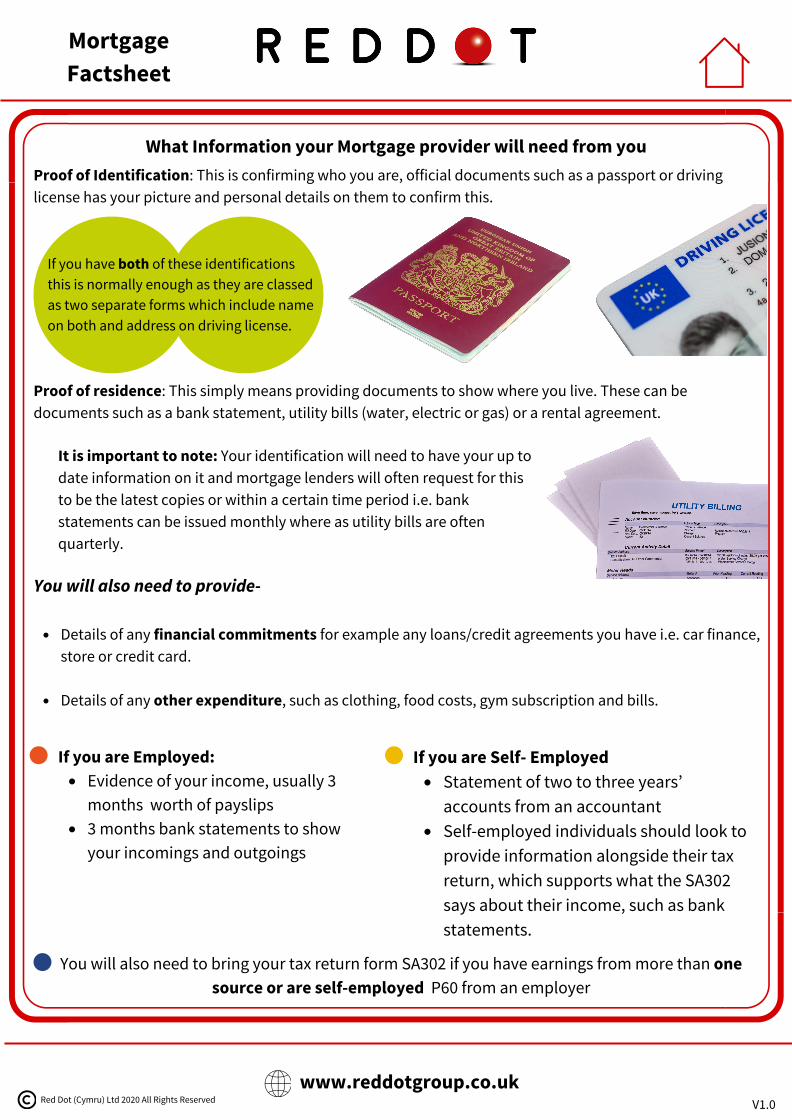

Details of any financial commitments for example any loans/credit agreements you have i.e. car finance,store or credit card.

Details of any other expenditure, such as clothing, food costs, gym subscription and bills.

Proof of Identification: This is confirming who you are, official documents such as a passport or drivinglicense has your picture and personal details on them to confirm this.

Proof of residence: This simply means providing documents to show where you live. These can bedocuments such as a bank statement, utility bills (water, electric or gas) or a rental agreement.

You will also need to provide-

Evidence of your income, usually 3months worth of payslips3 months bank statements to showyour incomings and outgoings

If you are Employed:Statement of two to three years’accounts from an accountantSelf-employed individuals should look toprovide information alongside their taxreturn, which supports what the SA302says about their income, such as bankstatements.

If you are Self- Employed

What Information your Mortgage provider will need from you

If you have both of these identificationsthis is normally enough as they are classedas two separate forms which include nameon both and address on driving license.

It is important to note: Your identification will need to have your up todate information on it and mortgage lenders will often request for thisto be the latest copies or within a certain time period i.e. bankstatements can be issued monthly where as utility bills are oftenquarterly.

You will also need to bring your tax return form SA302 if you have earnings from more than onesource or are self-employed P60 from an employer

www.reddotgroup.co.ukV1.0

Mortgage Factsheet

Red Dot (Cymru) Ltd 2020 All Rights Reserved

They will complete all of the relevant land searches to make sure the property you are buying doesn'thave any issues you are not aware of.They also undertake the legal work to transfer the ownership and funds along with acting as the go-tobetween the lender, buyer and seller- at this point check what the legal cost of this process would be.

Find a solicitor - You will need a solicitor to help you buy your home.

Buying- they will help you with the selection and find properties that fit your requirements. When youhave found a property you are interested in, they will take you for a viewing to see if it fits your needs andassist when you are ready to make an offer. Selling- they will advise you on a selling price and market the property online and sometimes throughsocial media channels- there is usually a fee associated with this process.

Find a house- In most cases you use an estate agent if you are buying or selling a property.

Basic surveys look at the property's condition, including any risks, potential legal issues andurgent defects.Higher levels of surveys completed will give you more information such as a conditionreport, any defects that might affect the property and advice on repairs and maintenance.The more in-depth the report is the more money you will have to pay.

A valuation survey - is completed on the property you are buying to ensure that the property isworth the amount being asked of it;

What does a mortgage journey look like......

1.

For a house purchase of £100,000 with a deposit need of 10%, you would need to have saved a minimum of £10,000 as a deposit.....

Deposit - Before purchasing a property you will need to have considered your deposit amount. You should saveenough for at least the minimum amount required and consider that you may need to save a little more for thingssuch as solicitor costs, furnishing your new home and any moving costs including the possible need for homerenovations to the property you select.

2. Find a mortgage lender - To get advice on you how much in principal you can borrow. This is referred to as 'in Principal' as no application or credit checks will be done at this stage, however, basicquestions will be asked to find out if you could be eligible and how much you can borrow as a mortgage with thatlender.

3.

4.

5. Complete a full mortgage application which will give you advice on the right typeof mortgage for you and requesting your solicitor information to proceed.

Back to your mortgage advisor - You will then need to -

6.

7. Your mortgage advisor- will continue to work with all parties such as your solicitor and mortgagecompany to ensure all key searches and transfers are completed successfully and there are no issuesbeen brought to light with the survey that may cause delays with the sale. Once this has all been completed, you will be given a date known as 'completion date' and be ready topick up the keys to your new home.

www.reddotgroup.co.ukV1.0

Mortgage Factsheet

Red Dot (Cymru) Ltd 2020 All Rights Reserved

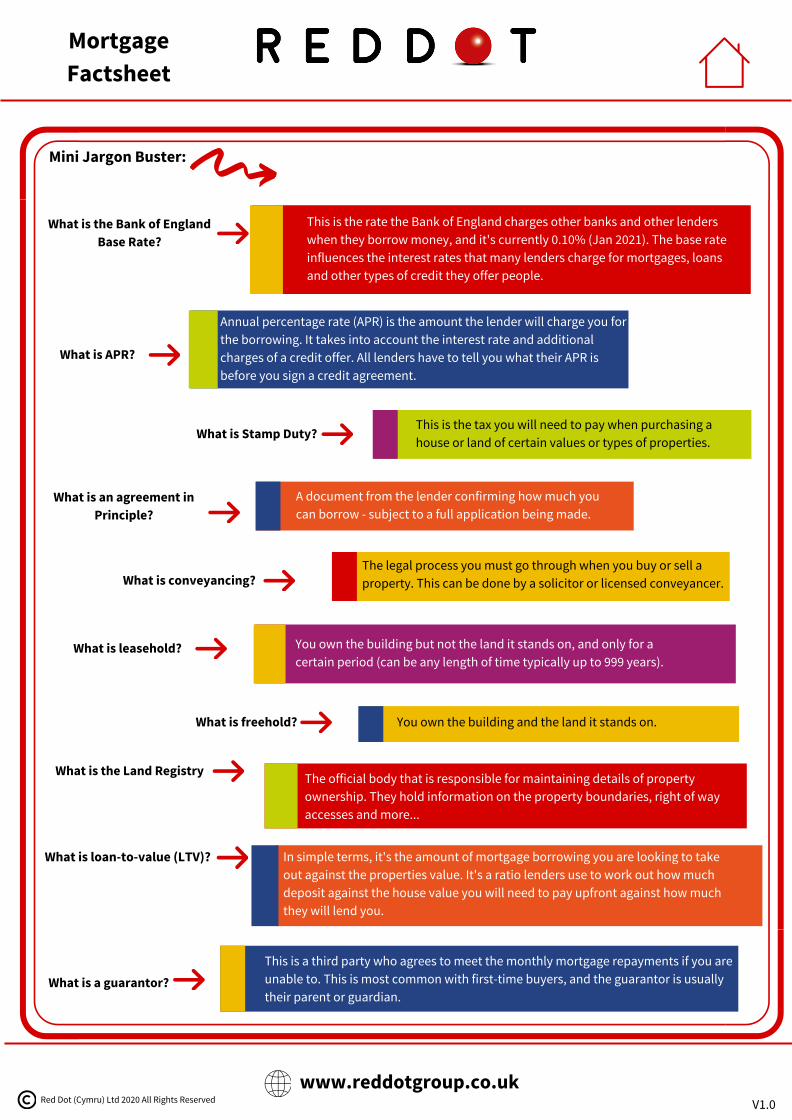

Mini Jargon Buster:

What is the Bank of EnglandBase Rate?

This is the rate the Bank of England charges other banks and other lenderswhen they borrow money, and it's currently 0.10% (Jan 2021). The base rateinfluences the interest rates that many lenders charge for mortgages, loansand other types of credit they offer people.

What is APR?

Annual percentage rate (APR) is the amount the lender will charge you forthe borrowing. It takes into account the interest rate and additionalcharges of a credit offer. All lenders have to tell you what their APR isbefore you sign a credit agreement.

What is Stamp Duty?This is the tax you will need to pay when purchasing ahouse or land of certain values or types of properties.

What is an agreement inPrinciple?

A document from the lender confirming how much youcan borrow - subject to a full application being made.

What is conveyancing?The legal process you must go through when you buy or sell aproperty. This can be done by a solicitor or licensed conveyancer.

What is leasehold? You own the building but not the land it stands on, and only for acertain period (can be any length of time typically up to 999 years).

What is freehold? You own the building and the land it stands on.

What is the Land Registry The official body that is responsible for maintaining details of propertyownership. They hold information on the property boundaries, right of wayaccesses and more...

What is loan-to-value (LTV)? In simple terms, it's the amount of mortgage borrowing you are looking to takeout against the properties value. It's a ratio lenders use to work out how muchdeposit against the house value you will need to pay upfront against how muchthey will lend you.

What is a guarantor? This is a third party who agrees to meet the monthly mortgage repayments if you areunable to. This is most common with first-time buyers, and the guarantor is usuallytheir parent or guardian.

www.reddotgroup.co.ukV1.0

Mortgage Factsheet

Red Dot (Cymru) Ltd 2020 All Rights Reserved