msd 60-day response to state auditor 2-14-2012

TRANSCRIPT

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 1/59

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 2/59

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 3/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

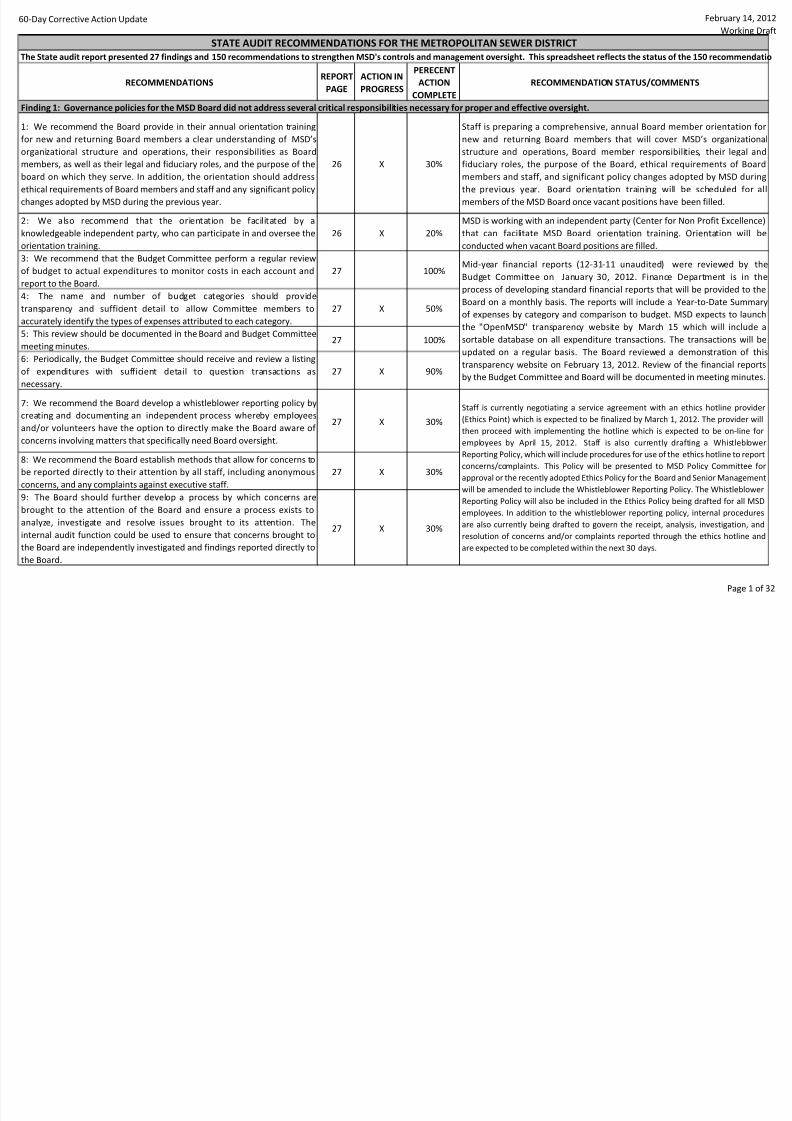

We recommend the Board provide in their annual orientation training

new and returning Board members a clear understanding of MSD’s

ganizational structure and operations, their responsibilities as Board

mbers, as well as their legal and fiduciary roles, and the purpose of the

ard on which they serve. In addition, the orientation should address

hical requirements of Board members and staff and any significant policy

anges adopted by MSD during the previous year.

26 X 30%

Staff is preparing a comprehensive, annual Board member orientati

new and returning Board members that will cover MSD’s organiz

structure and operations, Board member responsibilities, their leg

fiduciary roles, the purpose of the Board, ethical requirements of

members and staff, and significant policy changes adopted by MSD

the previous year. Board orientation training will be scheduled

members of the MSD Board once vacant positions have been filled.

We also recommend that the orientation be facilitated by a

owledgeable independent party, who can participate in and oversee the

entation training.

26 X 20%

MSD is working with an independent party (Center for Non Profit Exce

that can facilitate MSD Board orientation training. Orientation w

conducted when vacant Board positions are filled.

We recommend that the Budget Committee perform a regular review

budget to actual expenditures to monitor costs in each account and

port to the Board.

27 100%

The name and number of budget categories should provide

nsparency and sufficient detail to allow Committee members to

curately identify the types of expenses attributed to each category.

27 X 50%

This review should be documented in the Board and Budget Committee

eting minutes.27 100%

Periodically, the Budget Committee should receive and review a listing

expenditures with sufficient detail to question transactions as

cessary.

27 X 90%

We recommend the Board develop a whistleblower reporting policy by

ating and documenting an independent process whereby employees

d/or volunteers have the option to directly make the Board aware of

ncerns involving matters that specifically need Board oversight.

27 X 30%

We recommend the Board establish methods that allow for concerns to

reported directly to their attention by all staff, including anonymous

ncerns, and any complaints against executive staff.

27 X 30%

The Board should further develop a process by which concerns are

ought to the attention of the Board and ensure a process exists to

alyze, investigate and resolve issues brought to its attention. The

ernal audit function could be used to ensure that concerns brought to

e Board are independently investigated and findings reported directly to

e Board.

27 X 30%

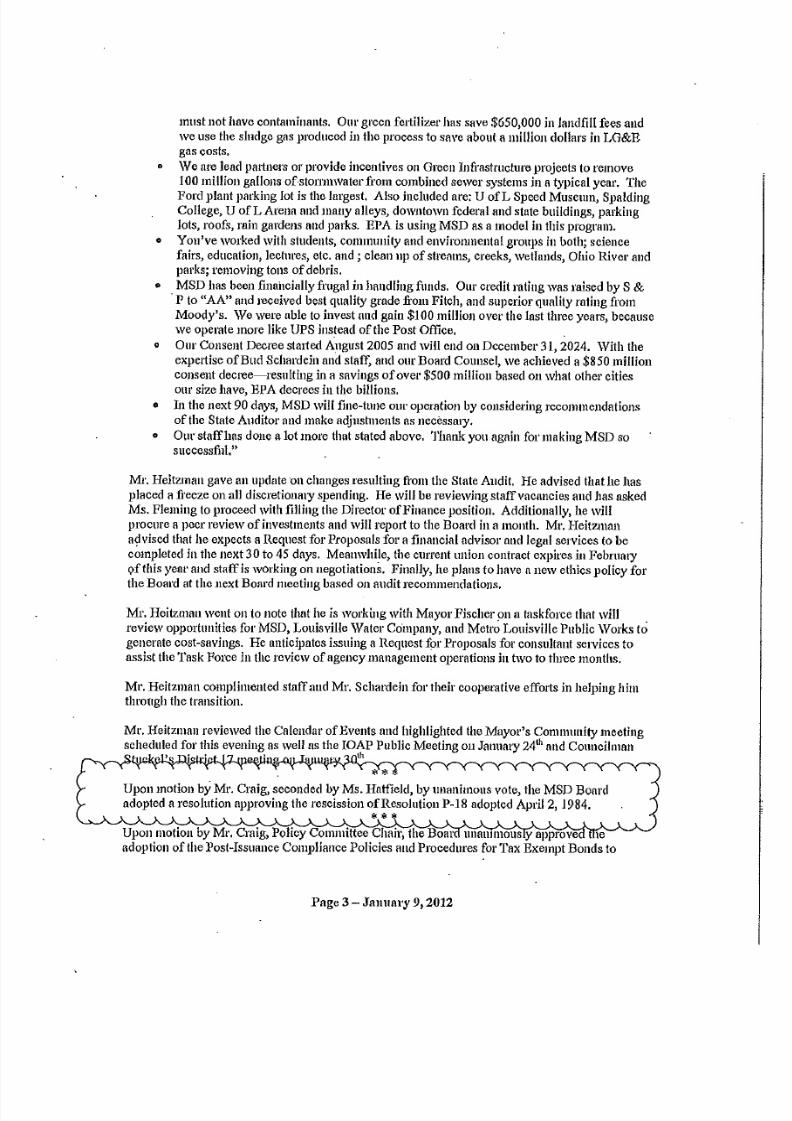

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

Mid-year financial reports (12-31-11 unaudited) were reviewed b

Budget Committee on January 30, 2012. Finance Department is

process of developing standard financial reports that will be provided

Board on a monthly basis. The reports will include a Year-to-Date Su

of expenses by category and comparison to budget. MSD expects to

the "OpenMSD" transparency website by March 15 which will inc

sortable database on all expenditure transactions. The transactions

updated on a regular basis. The Board reviewed a demonstration

transparency website on February 13, 2012. Review of the financial r

by the Budget Committee and Board will be documented in meeting m

Staff is currently negotiating a service agreement with an ethics hotline p

(Ethics Point) which is expected to be finalized by March 1, 2012. The provid

then proceed with implementing the hotline which is expected to be on-l

employees by April 15, 2012. Staff is also currently drafting a Whistle

Reporting Policy, which will include procedures for use of the ethics hotline to

concerns/complaints. This Policy will be presented to MSD Policy Commit

approval or the recently adopted Ethics Policy for the Board and Senior Mana

will be amended to include the Whistleblower Reporting Policy. The Whistle

Reporting Policy will also be included in the Ethics Policy being drafted for a

employees. In addition to the whistleblower reporting policy, internal proc

are also currently being drafted to govern the receipt, analysis, investigatio

resolution of concerns and/or complaints reported through the ethics hotl

are expected to be completed within the next 30 days.

ding 1: Governance policies for the MSD Board did not address several critical responsibilities necessary for proper and effective oversight.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 4/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend the Board adopt a policy to review and approve the

ary and bonus incentives of the executive staff on an annual basis to

sure that the compensation paid is equitable to the responsibilities and

ties of each position.

27 X 30%

The Personnel Committee of the Board met on January 23, 201

reviewed the compensation of Senior Management. The Committee pr

direction to the Human Resource Director to retain a professio

consultant to review MSD compensation practices for manageme

employees and report back to the Personnel Committee. Compen

adjustments for Executive Director and senior management will be pre

to the Personnel Committee and Board for approval. A Compensation

will be developed to review and approve the Executive Director and Management compensation.

We further recommend the Board annually review MSD’s personnel

d compensation policy, including the range of increases, by which salary

reases and bonus payments are made to all staff.

27 X 30%

The Personnel Committee will annually review and approve the bud

salary increase for non-union employees and approve the range of

increases for employees based upon annual performance. This procedu

be documented in the Compensation Policy.

The salaries should be reviewed specifically by the Board to ascertain

propriate use of funds given the mission of MSD, and such review

ould be documented in the minutes.

27 X 30%

These actions should be documented in the meeting minutes. 27 X 30%

We recommend the Board, or a designated committee of the Board,

e-approve executive staff travel, including estimated costs.27 X 20%

The Board meeting minutes should document the review conducted

the Board.27 X 20%

We also recommend the Board require a report of the actual travel

penses of executive staff, with Board approval, prior to expense

mbursement.

27 X 20%

The expense reports should sufficiently detail the expenses associated

th meals, lodging, transportation, and entertainment of each trip, as

ll as the business purpose of each expense item.

27 X 20%

The Executive and Senior Management salaries and annual adjustmen

be approved by the Board and will be reflected in the minutes of the

meetings.

A Travel Policy is being drafted to govern the travel of all employee

Travel Policy will be approved by the Board Policy Committee, and i

provisions to establish an annual travel budget for the Executive Direct

Senior Management and reporting of all travel expenses to the

Personnel or Audit Committee. The approval of the travel budget f

Executive Director and Senior Management will be documented

meeting minutes. Currently, all employee travel is reviewed by the Exe

Team, with the Executive Director approving all travel in advanc

reporting of all travel expenses and a travel summary report

completion.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 5/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend MSD strengthen their purchasing card procedure by

king it a formal policy.30 X 20%

We recommend the policy include information requiring a business

rpose be documented and address how MSD or the Board will handle

penses that are considered improper or disallowed expenses.

30 X 20%

We also recommend the Board review purchasing card expenditures

the Executive Director.30 X 20%

We further recommend MSD include a procedure concerning

mbursement by an employee when a purchasing card is used for

rsonal use in a formal policy.

30 X 20%

A timeframe when staff is required to reimburse MSD for any personal

penditure that may have been incurred should also be included in the

icy. Currently, MSD does not use credit cards and therefore has no

icy, but if credit cards ever become the preferred method of payment

goods, then we recommend a strong credit card policy should be

veloped.

30 X 20%

We recommend policies be implemented to ensure that the Board or a

signated committee of the Board review and approve all executive staff

mbursements and supporting documentation to ensure the

mbursements are for reasonable and necessary expenditures. Such

iews and approvals also will help ensure that duplicate payments are

t made.

30 X 20%

We recommend MSD adopt written policies for the backup of

ctronic financial information.30 X 20%

Moreover, policies should include a process to report any lost or

ssing financial information or records.30 X 20%

We recommend MSD adopt and implement property and inventory

ntrol policies and procedures to identify and account for all furniture,

uipment, or other items valued over a certain specified dollar amount,

h the specific dollar amount included in policy.

30 X 10%

Such policies and procedures should include recording of the following

nimum information for each property item: Name of individual in

eipt of furniture/equipment; Description of furniture/equipment;

ndor name; Model and serial numbers; Acquisition date; and,

quisition cost.

30-31 X 10%

A Procurement Card Policy will be developed to govern the approval a

of procurement cards. Procedures will include documentation of bu

purpose for purchases, supervisory/management approval, an annual

of the purchasing levels for employees, and procedures for disa

expenses and method and time for employee reimbursement to MS

annual audit will be conducted by the Internal Auditor of the procur

card expenses and reported to the Audit Committee. Annually, the In

Auditor will provide to the Audit Committee a summary of expenses

Executive Director, including procurement card purchases, travel ex

and reimbursements. Currently MSD does not issue credit ca

employees and has no plan to do so.

A Property and Inventory Control Policy will be developed to identi

account for all furniture, equipment, and other items valued over a sp

dollar amount. The procedures will include item description, v

model/serial number, acquisition date and cost where available. The

will include provisions for inventory control, disposal and reportin

policy is expected to be completed by August 15, 2012. The Policy

communicated to employees and included in the MSD Policy Manual.

ding 2: Certain policies were not documented or sufficient to ensure accountability.

Policy and procedures for the backup of electronic financial informatio

the reporting of lost or missing financial records will be incorporated

Disaster Recovery Policy and Procedure.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 6/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We further recommend such inventory policies and procedures

lude an annual, or periodic, physical inventory of all fixed assets.31 X 10%

Dispositions of property should also be reflected in inventory

counting.31 X 10%

The property inventory and control policy should be made available to

employees who have responsibility for property assets and should

lude sufficient detail to ensure accurate and appropriate accounting for

operty inventory.

31 X 10%

MSD should include its inventory and property control policies in its

icy Manual.31 X 10%

A Property and Inventory Control Policy will be developed to identi

account for all furniture, equipment, and other items valued over a sp

dollar amount. The procedures will include item description, v

model/serial number, acquisition date and cost where available. The

will include provisions for inventory control, disposal and reportin

policy is expected to be completed by August 15, 2012. The Policy

communicated to employees and included in the MSD Policy Manual.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 7/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

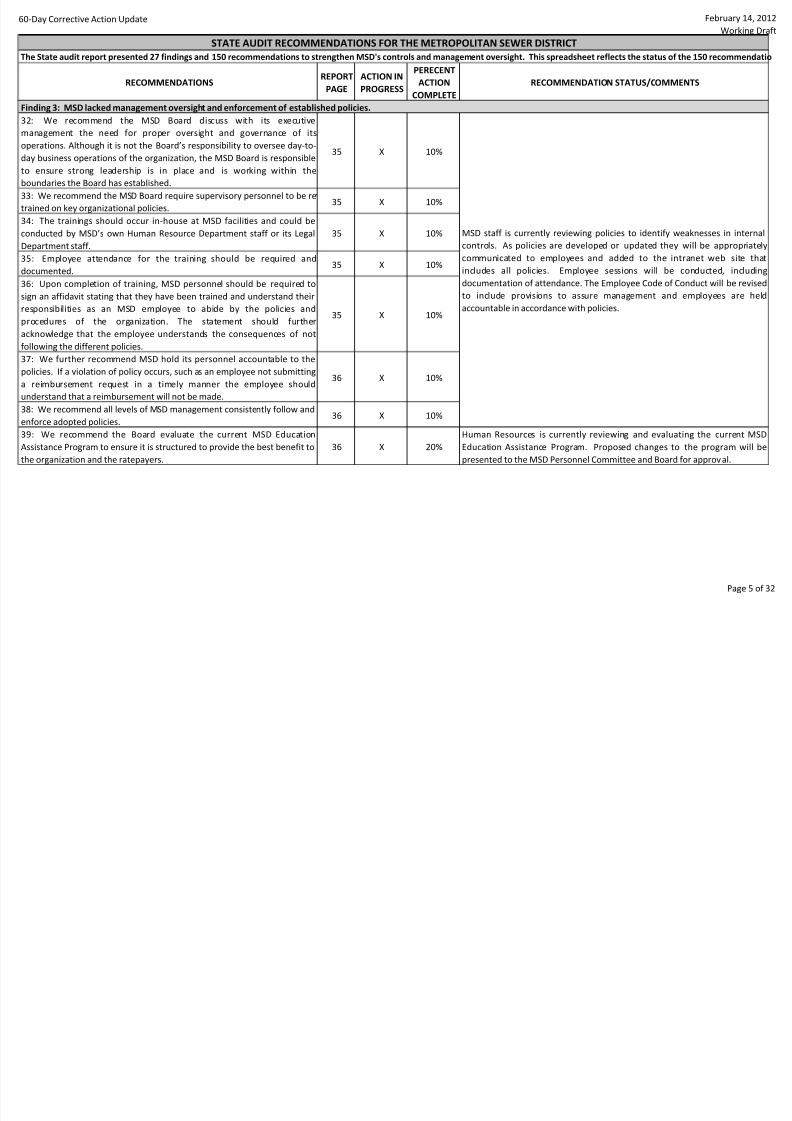

We recommend the MSD Board discuss with its executive

nagement the need for proper oversight and governance of its

erations. Although it is not the Board’s responsibility to oversee day-to-

y business operations of the organization, the MSD Board is responsible

ensure strong leadership is in place and is working within the

undaries the Board has established.

35 X 10%

We recommend the MSD Board require supervisory personnel to be reined on key organizational policies.

35 X 10%

The trainings should occur in-house at MSD facilities and could be

nducted by MSD’s own Human Resource Department staff or its Legal

partment staff.

35 X 10%

Employee attendance for the training should be required and

cumented.35 X 10%

Upon completion of training, MSD personnel should be required to

n an affidavit stating that they have been trained and understand their

ponsibilities as an MSD employee to abide by the policies and

ocedures of the organization. The statement should further

knowledge that the employee understands the consequences of not

owing the different policies.

35 X 10%

We further recommend MSD hold its personnel accountable to the

icies. If a violation of policy occurs, such as an employee not submitting

reimbursement request in a timely manner the employee should

derstand that a reimbursement will not be made.

36 X 10%

We recommend all levels of MSD management consistently follow and

force adopted policies.36 X 10%

We recommend the Board evaluate the current MSD Education

sistance Program to ensure it is structured to provide the best benefit to

e organization and the ratepayers.

36 X 20%

Human Resources is currently reviewing and evaluating the curren

Education Assistance Program. Proposed changes to the program w

presented to the MSD Personnel Committee and Board for approval.

ding 3: MSD lacked management oversight and enforcement of established policies.

MSD staff is currently reviewing policies to identify weaknesses in in

controls. As policies are developed or updated they will be approp

communicated to employees and added to the intranet web sit

includes all policies. Employee sessions will be conducted, in

documentation of attendance. The Employee Code of Conduct will be r

to include provisions to assure management and employees ar

accountable in accordance with policies.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 8/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

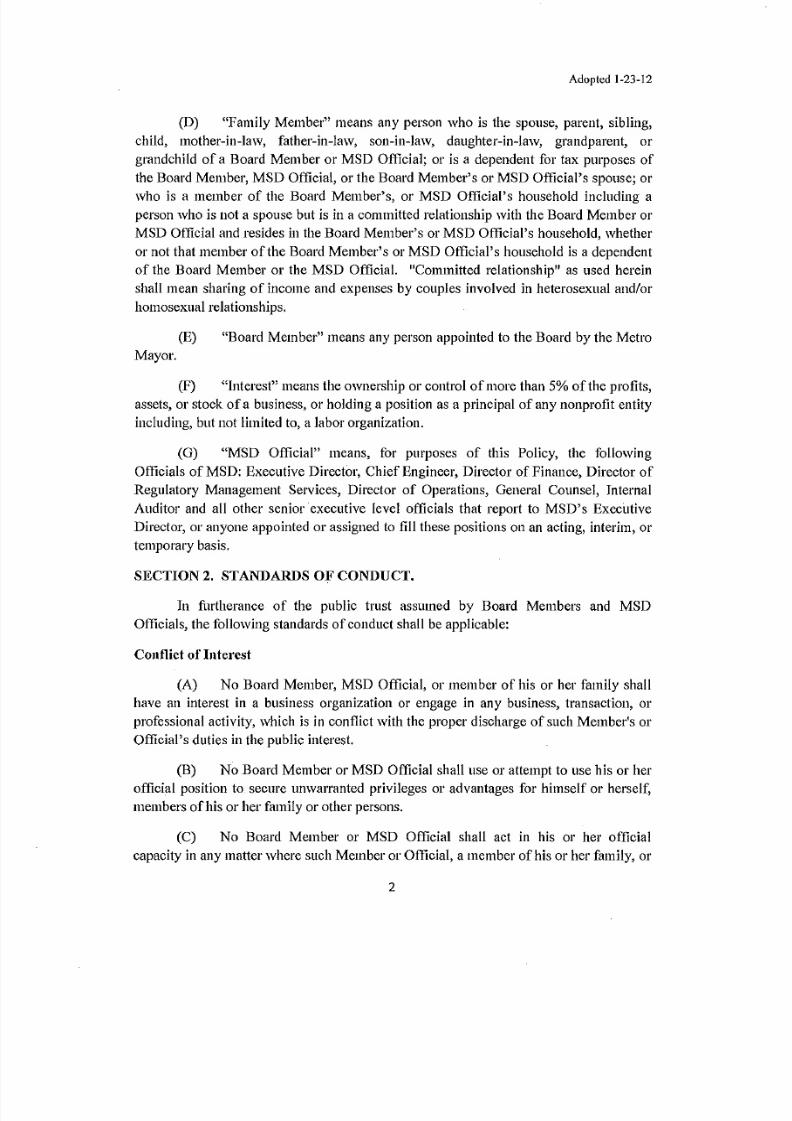

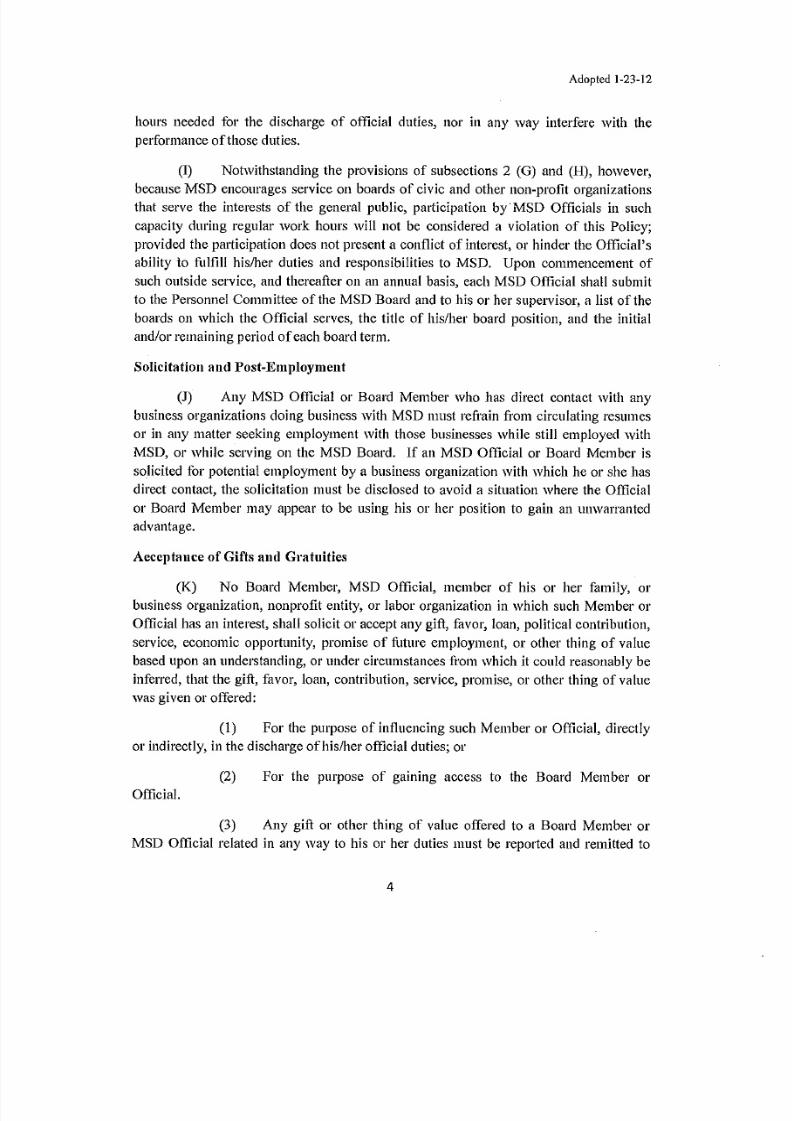

To remain independent in their decision-making regarding entities

ng business with MSD, or seeking to do business with MSD, Board

embers, executive staff, and other employees should avoid any

uations that are actual conflicts between their private interests and their

ties on behalf of MSD, or that have the potential to present conflicts.

ither should they accept gifts and gratuities that compromise the

partiality of their decision-making on behalf of MSD, or that give thepearance that MSD actions are based on personal benefit, favors, or

ationships, rather than objective decision-making.

39 X 80%

We recommend the Board establish a comprehensive code of ethics,

plicable to Board members, appointed executive staff members, and all

ployees. MSD may want to consider having someone skilled in

ablishing ethical standards for public employees and board members

ist in the drafting of such policy standards.

40 X 90%

Upon adoption by the Board, the code of ethics should be

orporated into the two Policies and Benefits Manuals for employees

it and non-unit), as well as any manual given to Board members during

entation.

40 X 20%

We recommend MSD provide initial training for Board members,

pointed executive staff and employees on the code of ethics, as well as a

iew annually.

40 X 20%

An ethics training program will be developed for the Board,

Management and employees. Ethics training will be included in

member orientation (once vacant Board positions are filled by the M

and employee sessions will be conducted with 120 days of adoption

Employee Ethics Policy.

In developing a comprehensive code of ethics applicable to Board

mbers, as well as appointed staff and employees, the following areas of

nduct should be considered for inclusion: General standards of conduct;

ntracting, subcontracting, having an agreement, or doing business with

SD; Use of official position to obtain financial benefit, privilege or

vantage for self or others; Involvement in matters where an ownership

erest exists; Use of confidential information; Use of MSD property, time,

uipment; Solicitation; Acceptance of gifts and gratuities; Employment of

atives; Transactions with subordinates; Outside employment; Service on

ards and Commissions; Honoraria; Investment/ Stock ownership;

presentation; Post-employment; Political activity; and, Financial

closure.

40 X 80%

The Board adopted a comprehensive Board and Senior Management

Policy on January 23, 2012 including these provisions. See respo

Finding 4, Recommendation 40.

ding 4: MSD ethics policies for Board members, appointed executive staff members, and employees were not sufficient to address conflicts.

MSD adopted an ethics policy governing the MSD Board, Executive Di

Chief Engineer, and Senior Management staff effective January 23,

Procedures for reporting ethics complaints through an ethics hotline, a

the receipt, analysis, investigation and resolution of such complaints a

being developed for inclusion in the newly adopted ethics policy a

policy to be developed for MSD employees and are expected to be com

by April 15, 2012. The employee ethics policy, a financial disclosur

modeled after the form utilized by Metro Government pursuant to the

Ethics Code, and formal hearing procedures to be utilized by the MSD

Audit Committee to hear written and/or anonymous ethics complain

also being developed and are expected to be completed within that

timeframe. The Ethics Policy will be incorporated into a Policy Man

employees. See Attachment A.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 9/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

In establishing a financial disclosure policy, we recommend the MSD

ard members, as well as all executive team members, annually file with

appropriate committee of the Board, and by a specified date, a

tement detailing financial interests held. Required information should

prescribed by an appropriate committee of the Board.

40 100%

The Board should consider including the following disclosures on the

escribed form: Name, business and home addresses, telephone numberd e-mail address of the filer; Title of position or office whereby filing is

quired; Any other occupation of the filer or filer’s spouse; Businesses in

ich the filer or filer’s spouse hold a specified percentage of interest. The

icy should numerically state the percentage of business ownership

quired to be reported; Sources of income to the filer, filer’s spouse, or

r’s immediate family members exceeding a specific amount (dollar

ount should be specified in the policy); Real property owned by the

r, the filer’s spouse, or the filer’s immediate family, and its location;

editor’s of the filer, the filer’s spouse, or the filer’s immediate family

o are owed more than a specified amount. The policy should specify the

lar amount required to be reported; and, Sources of gifts over a

ecified amount, which should be stated in the policy, to the filer, the

r’s spouse, or the filer’s immediate family, except for gifts from family

mbers.

40-41 X 90%

The policy should further require an affirmative statement by the filer

t he or she has no interest that would cause a conflict with his or her

icial duties.

41 X 90%

Sanction for noncompliance with the filing requirements also should

detailed in the policy.41 100%

To ensure compliance with the code of ethics adopted, MSD should

velop and implement policies, procedures, and responsibilities

garding reporting, investigation, and resolution of allegations of ethical

sconduct as detailed in the recommendations of Finding 1 regarding a

istleblower policy.

41 X 80%

These recommendations have been incorporated into the Board and

Management Ethics Policy adopted January 23, 2012. Refer to the res

provided in Finding 4, Recommendation 40.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 10/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

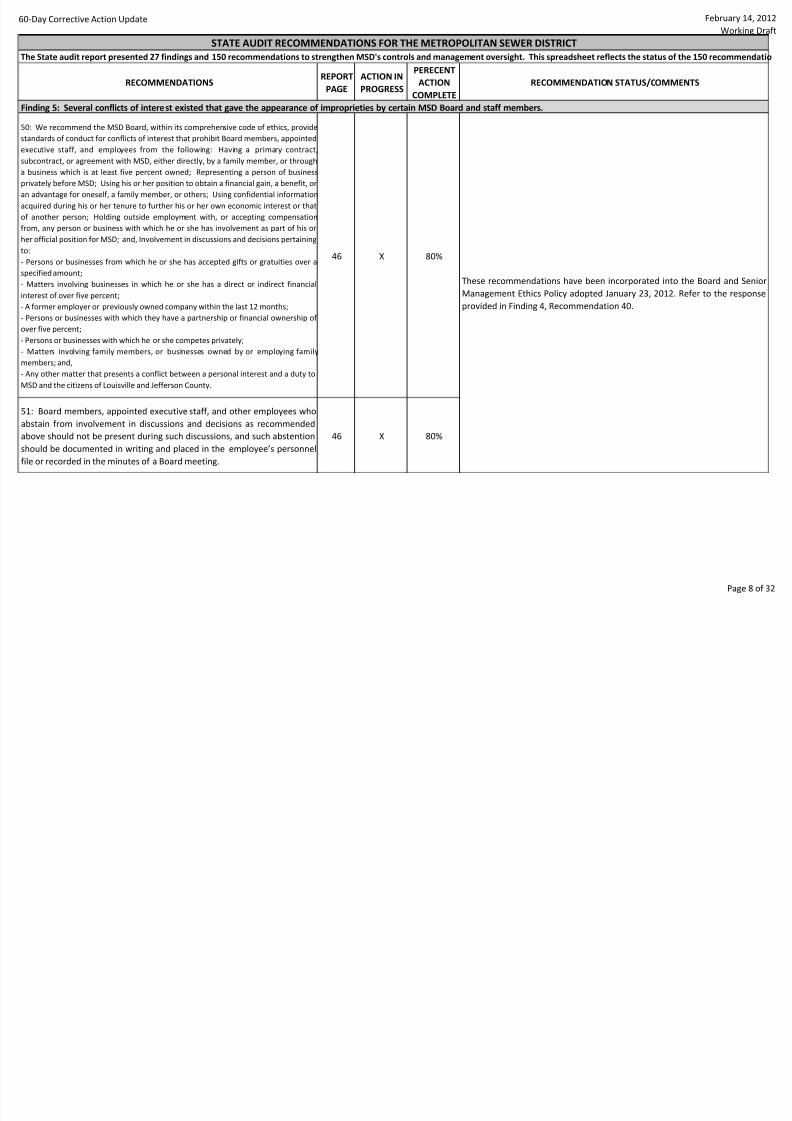

We recommend the MSD Board, within its comprehensive code of ethics, provide

ndards of conduct for conflicts of interest that prohibit Board members, appointed

cutive staff, and employees from the following: Having a primary contract,

contract, or agreement with MSD, either directly, by a family member, or through

usiness which is at least five percent owned; Representing a person of business

vately before MSD; Using his or her position to obtain a financial gain, a benefit, or

advantage for oneself, a family member, or others; Using confidential informationuired during his or her tenure to further his or her own economic interest or that

another person; Holding outside employment with, or accepting compensation

m, any person or business with which he or she has involvement as part of his or

official position for MSD; and, Involvement in discussions and decisions pertaining

ersons or businesses from which he or she has accepted gifts or gratuities over a

cified amount;

atters involving businesses in which he or she has a direct or indirect financial

erest of over five percent;

former employer or previously owned company within the last 12 months;

ersons or businesses with which they have a partnership or financial ownership of

r five percent;

rsons or businesses with which he or she competes privately;

Matters involving family members, or businesses owned by or employing family

mbers; and,

ny other matter that presents a conflict between a personal interest and a duty to

D and the citizens of Louisville and Jefferson County.

46 X 80%

Board members, appointed executive staff, and other employees who

stain from involvement in discussions and decisions as recommended

ove should not be present during such discussions, and such abstention

ould be documented in writing and placed in the employee’s personnel

or recorded in the minutes of a Board meeting.

46 X 80%

These recommendations have been incorporated into the Board and

Management Ethics Policy adopted January 23, 2012. Refer to the res

provided in Finding 4, Recommendation 40.

ding 5: Several conflicts of interest existed that gave the appearance of improprieties by certain MSD Board and staff members.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 11/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

To ensure compliance with the conflict of interest policies adopted,

SD should develop and implement policies, procedures and

ponsibilities found in Finding 1 regarding reporting and resolution of

mplaints. Finally, we reiterate MSD’s Policy and Benefits Manuals that

te: “As public servants, employees must display a high standard of

hical behavior that ensures the public that employees do not use their

sitions to provide special privileges to themselves, to other individuals

organizations.”

46 X 80%

This recommendation has been incorporated into the Board and

Management Ethics Policy adopted January 23, 2012. Refer to the res

provided in Finding 4, Recommendation 40.

Pag

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 12/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend that MSD designate this contract as an applicable

ofessional services contract that should be periodically advertised and

mpetitively negotiated to ensure MSD’s best interests are met.

48 100%

Due to the multiple types of legal services that can be assigned to this

m and attorney, the contract should be separated based on the type of

al services needed.

48 X 90%

An analysis should be performed to determine the need for outsideal services.

48 X 80%

Based on the results of the analysis, a separate request for proposals

ould be developed for advertising each type of service and an evaluation

mmittee should be created to evaluate the responses using specific

teria.

48 X 80%

The evaluation committee should consist of staff members that are

ormed and knowledgeable regarding the services needed by MSD.48 X 80%

We recommend the Board consider whether Board Legal Counsel

ould be independent of all other legal services.48 100%

Effective January 9, 2012, MSD’s primary legal services contrac

designated by the MSD Board as a professional services contract that

be periodically advertised and competitively negotiated, and sta

authorized to and has begun drafting a Request for Qualifications (R

procure legal services. The RFQ separates legal services into multiple p

areas for purposes of procuring qualified attorneys under separate cofor each area, (including the areas of special board and bond coun

being reviewed by a procurement evaluation team and is expected

advertised by April 15, 2012. The team will also participate in the eva

of statements of qualifications and further recommendations concern

procurement. On February 13, 2012 the Board directed the Legal Dire

review the internal legal staff resources, consider the need for add

staff and the ability to perform legal services in-house to minimize

expenses. The Board has also directed the Legal Director to issue an R

Board Legal Counsel, separate from all other legal services in order to

independent advice to the Board where appropriate. In the interim,

internal Legal Director is serving as the Board's General Counsel.

ding 6: MSD's primary legal services contract has been with the same attorney's firm since 1984 while never being competitively negotiated or advertised.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 13/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend the MSD Board rescind the 1984 resolution that

quires a review and approval of all matters by the Board Legal Counsel

or to presentation to the Board.

50 100%

Secondary reviews by Board Legal Counsel of issues or documents

esented to the Board should be performed only upon request by the

ard, Executive Director, or Legal Director and only for the specific

idence of the request.

50 100%

We recommend the Board not make a blanket request of the Board

gal Counsel to review all documents or issues of a certain type.50 100%

Effective January 9, 2012, the MSD Board rescinded the 1984 resolutio

requires Board Legal Counsel approval and oversight of Board matte

addresses each of these recommendations. See Attachment B.

ding 7: Board Legal Counsel given approval authority in MSD Board Process.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 14/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

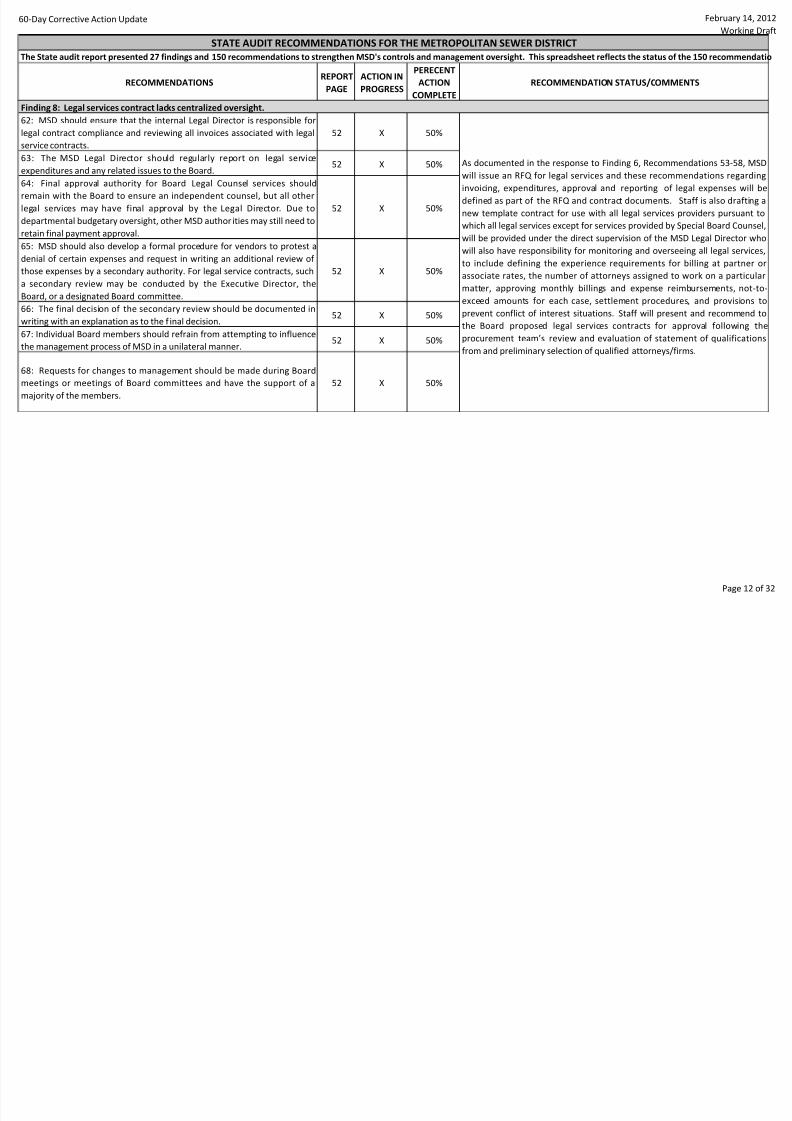

MSD should ensure that the internal Legal Director is responsible for

al contract compliance and reviewing all invoices associated with legal

vice contracts.

52 X 50%

The MSD Legal Director should regularly report on legal service

penditures and any related issues to the Board.52 X 50%

Final approval authority for Board Legal Counsel services should

main with the Board to ensure an independent counsel, but all otheral services may have final approval by the Legal Director. Due to

partmental budgetary oversight, other MSD author ities may still need to

ain final payment approval.

52 X 50%

MSD should also develop a formal procedure for vendors to protest a

nial of certain expenses and request in writing an additional review of

ose expenses by a secondary authority. For legal service contracts, such

econdary review may be conducted by the Executive Director, the

ard, or a designated Board committee.

52 X 50%

The final decision of the secondary review should be documented in

ting with an explanation as to the f inal decision.52 X 50%

Individual Board members should refrain from attempting to influence

e management process of MSD in a unilateral manner.52 X 50%

Requests for changes to management should be made during Board

etings or meetings of Board committees and have the support of a

jority of the members.

52 X 50%

ding 8: Legal services contract lacks centralized oversight.

As documented in the response to Finding 6, Recommendations 53-58

will issue an RFQ for legal services and these recommendations reg

invoicing, expenditures, approval and reporting of legal expenses w

defined as part of the RFQ and contract documents. Staff is also dra

new template contract for use with all legal services providers pursu

which all legal services except for services provided by Special Board Co

will be provided under the direct supervision of the MSD Legal Directo

will also have responsibility for monitoring and overseeing all legal se

to include defining the experience requirements for billing at part

associate rates, the number of attorneys assigned to work on a par

matter, approving monthly billings and expense reimbursements, n

exceed amounts for each case, settlement procedures, and provis

prevent conflict of interest situations. Staff will present and recomm

the Board proposed legal services contracts for approval followi

procurement team’s review and evaluation of statement of qualific

from and preliminary selection of qualified attorneys/firms.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 15/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend that MSD amend its contract for legal services to ensure that

D adequately controls the costs and responsibilities of the outside legal firm.

visions should address the following areas: Specifically, define the experience

uirements for billing at the partner or associate rates. The contract should

uire a justification if the partner rate is used by more than one attorney on the

e. For optimal monitoring by MSD, the contract should require a written

ermination for each assigned case as to the expected number of attorney

tners, associates, and paralegals, etc. This determination should also include a

-to-exceed amount to be paid to the Firm for the assigned case. The Firm must

ain written prior approval to exceed the maximum amount specified.

parate the types of legal work into individual contracts to improve monitoring

orts. Designate the MSD Legal Director to assign contracted legal work as

eded. Require prior approval of any costs other than for time spent on a case

a Firm attorney from the Legal Director. This includes any costs related to

vel, meals, expert witnesses, mock juries, and other costs incurred not related

he Firm’s time costs. Include a term that specifies the settlement process that

uld be followed by the Firm.

ude a term that requires the Firm to disclose any actual or potential conflict of

erest between MSD and any of the Firm’s other clients.

54 X 50%

Concurrent with the issuance of a RFQ for legal services, as explai

greater detail in response to recommendations under Finding 6, staff

drafting a new template contract for use with all legal services propursuant to which all legal services, except for services provided by S

Board Counsel, will be provided under the direct supervision of th

Legal Director/Legal Counsel who will also have responsibility for mon

and overseeing all legal services, to include defining, among other t

settlement procedures, and provisions to prevent conflict of i

situations. Staff will present and recommend to the Board propose

services contracts for approval following the procurement team’s revie

evaluation of statement of qualifications from and preliminary select

qualified attorneys/firms.

ding 9: MSD's legal services contract terms are not well defined and are silent as to settlement procedures and conflict of interest disclosures.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 16/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend the MSD Board formally adopt a policy to select bond

nsel and a financial advisor through a competitive selection process using

her a RFP or RFQ. This competitive process should assist in determining those

st qualified to perform the services, while also provide an opportunity to

trol the costs of issuing bonds.

61 X 40%

If co-bond counsel is desired, justification for co-bond counsel should be

vided to the Board for its review and approval.

61 X 40%

The RFP or RFQ should state the services desired, the length of the

gagement, the evaluation method, the selection process, and a cost proposal to

vide services.

61 X 40%

If co-bond counsel is being engaged the RFP, RFQ, or engagement letter

uld specify the roles and responsibilities and tasks assigned to each firm to

nimize potential duplication of work and costs.

61 X 40%

MSD should ensure proper oversight of legal counsel to ensure work is

gressing and coordinated as required by the RFP, RFQ, or engagement letter.61 X 40%

We further recommend the MSD Board be fully apprised of the RFP, RFQ, and

gagement letter for procuring services, the method used to select bond counsel

d financial advisor, the tasks to be performed by counsel and financial advisor,

ir fees and other bond issue costs.

62 X 40%

ding 10: MSD spent $2.1 million for co-bond counsel services with no documented justification.

MSD staff is preparing an RFQ for legal services that will include servi

Bond Counsel (see Response to Finding 6, Recommendations 53-58). A

for Financial Advisor is being developed and will be issued by June 15,

MSD has amended the contract with its existing Financial Advisor for se

on a month-by-month basis until a new Financial Advisor is selected

Board will be kept up-to-date on responses and selections for

professional services. Any use of Co-Bond Counsel will be justifie

approved by the Board and the Board will approve the Bond Counsel.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 17/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

MSD should develop a policy or process by which policies are to be

tiated and developed and subsequently brought before the Board. This

ould include who has the authority to initiate policy development and

o has the authority to authorize the expense of Board Legal Counsel to

ist in the process.

63 X 10%

When making an initial request for a new or revised policy, use of

ernal staff should be considered first, when possible, to ensure the mostst effective methods of policy development are used.

63 X 80%

A determination for the need of outside legal expertise should be

de in consultation with the internal legal staff.63 X 80%

ding 11: The lack of a policy development process results in duplication of work and potentially unnecessary legal fees.

Staff will prepare and present to the MSD Board Policy Committ

recommendation to the full Board, a resolution pursuant to which the

designates certain MSD policies as policies to be drafted, revised, mo

and monitored by MSD staff as directed and approved by the MSD

The resolution, which will be presented to the Board Policy Commit

June 15, 2012, will also serve to designate those policies to be perioreviewed by the Board. Staff will use internal resources where appropr

develop policies and only use external resources where appropriate. St

benchmark with other local and state agencies as well as the Institu

Internal Auditors and other professional organizations to assist in deve

best practices for policies.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 18/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend the Louisville Green Board amend its bylaws to

move specific names of individuals. The Louisville Green bylaws should

free of any redundant or unnecessary terms that may complicate the

vernance of this corporation.

64 X 0%

Further, we recommend the Louisville Green Board select a legal

unsel through a transparent, competitive process as similarly

ommended in Finding 6.

64 X 0%

ding 12: The Louisville Green Corporation bylaws specify by name the President and the special legal counsel.

The bylaws of the Louisville Green Corporation stipulate that the bylaw

be amended at any regular or special meeting of the Board by an affir

vote of six (6) members; however, the Corporation’s Board currently h

five (5) members. As soon as the Board’s membership is increased to

members, the bylaws will be amended to remove the names of the Pre

and special legal counsel. Also, effective January 9, 2012, MSD’s p

legal services contract was designated by the MSD Board as a profe

services contract that should be periodically advertised and compe

negotiated, and staff was authorized to and has begun drafting a R

procure legal services. The RFQ separates legal services into multiple p

areas for purposes of procuring qualified attorneys under separate co

for each area, (including the areas of special board counsel and

counsel), is being reviewed by a procurement evaluation team

expected to be advertised within 30 days. The team will also partici

the evaluation of statements of qualifications and further recommend

concerning the procurement.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 19/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

MSD should, at a minimum, follow current Investment Policy and

ovide the Board with detailed semi-annual reports as to the holdings of

e investment program, investment activities, risk levels of the program,

d program strategies.

69 X 90%

However, we recommend the policies be updated and investment

ports be provided to the Board, or to a Board investment committee as

ommended in Finding 16, on a monthly basis.

69 X 90%

Board members should request such information if not provided by

ff.69 X 90%

MSD should follow the requirements of the current Investment Policy

d annually solicit Request for Proposals for investment services that

ntain all required details of the investment management firm and the

vices being provided.

69 X 90%

Following MSD's Procurement Regulations for professional services, RF

Investment Management Services will be issued for annual contracts

the option to renew annually up to four additional years.

In the interests of transparency, MSD should not enter into a

oprietary investment program that does not disclose all details of the

ogram to the Board members.

69 X 90%

At the direction of the Board, all investments in the Yield Enhanc

Program have been withdrawn and invested in government

securities. A new investment policy is being drafted for review and ap

by the Board. All details of MSD investment programs will be disclosed

Budget Committee and MSD Board.

ding 13: MSD Board provides inadequate investment oversight and lacks sufficient information.

Staff is providing the MSD Board with quarterly reports that inclu

investments by category and amount, and any change in market va

those investments and investment earnings. MSD's current Inve

Policy is being reviewed for any necessary updates, including re

requirements to MSD Board.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 20/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

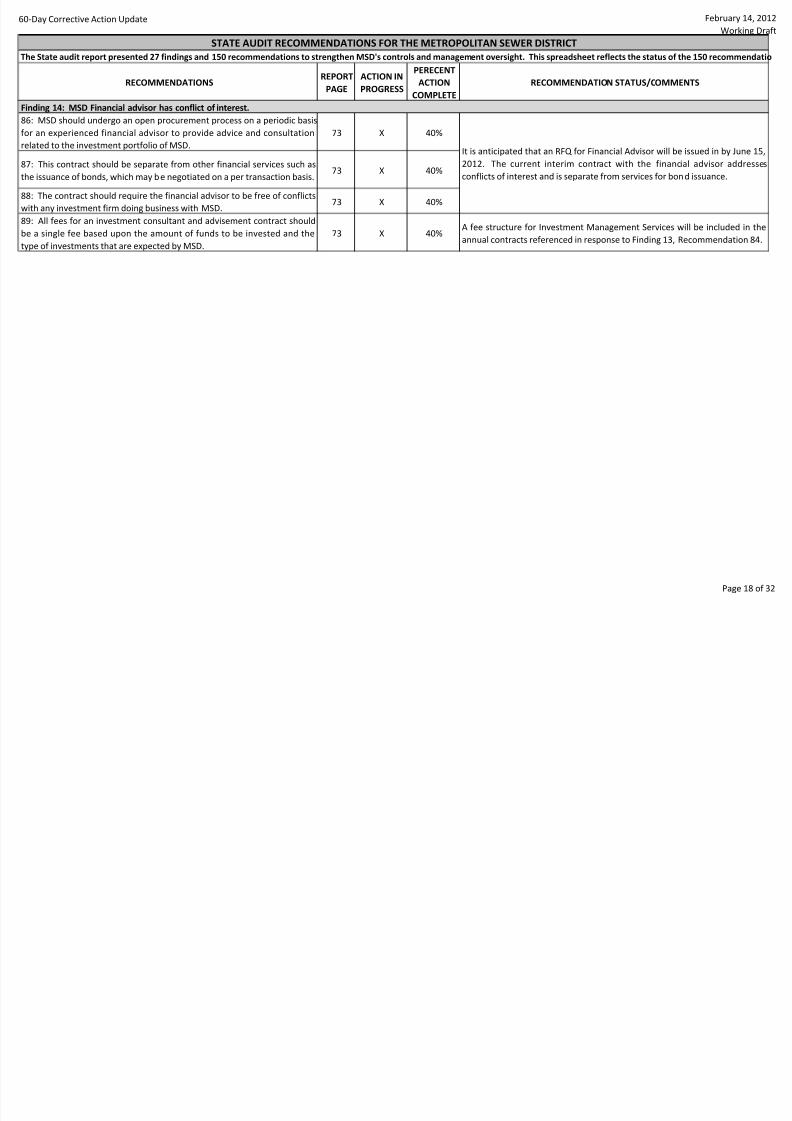

MSD should undergo an open procurement process on a periodic basis

an experienced financial advisor to provide advice and consultation

ated to the investment portfolio of MSD.

73 X 40%

This contract should be separate from other financial services such as

e issuance of bonds, which may be negotiated on a per transaction basis.73 X 40%

The contract should require the financial advisor to be free of conflictsh any investment firm doing business with MSD.

73 X 40%

All fees for an investment consultant and advisement contract should

a single fee based upon the amount of funds to be invested and the

e of investments that are expected by MSD.

73 X 40%A fee structure for Investment Management Services will be included

annual contracts referenced in response to Finding 13, Recommendatio

ding 14: MSD Financial advisor has conflict of interest.

It is anticipated that an RFQ for Financial Advisor will be issued in by Ju

2012. The current interim contract with the financial advisor add

conflicts of interest and is separate from services for bond issuance.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 21/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

We recommend that MSD ensure that the finance staff include a

rson or persons with strong financial and investment knowledge and

perience to enable investment and financial strategies to be based on

e knowledge and understanding of such activities by MSD staff and not

ely on the advice of third party advisors.

75 X 80%MSD posted the Budget and Finance Director position and is cu

reviewing candidates. The position is expected to be filled within 60 day

We further recommend that MSD Board membership include at least

e professional who is particularly knowledgeable in investment andancial management activities commensurate with the types of activities

which MSD may engage.

75 X 50%

The Mayor of Louisville Metro Government is currently reviewing cand

for MSD Board positions in compliance with KRS 76.030. The plan is tat least one of the four vacant positions to be filled with a professiona

investment and financial experience.

In addition, we recommend the MSD Board create an investment

mmittee whose members are responsible for the oversight of

estment activity and programs.

75 X 10%

The committee should include, at a minimum, one professional who is

rticularly knowledgeable in investment and financial management

ivities.

75 X 10%

We recommend the investment committee receive detailed reporting

MSD’s investment portfolio, all investment activities, programs, trends,

d strategies.

76 X 10%

The investment committee should have a thorough understanding of

sting investment policy, and propose additional policies as deemed

cessary.

76 X 10%

The committee should question staff and financial advisors regarding

estment activity and programs to evaluate compliance with investment

icies.

76 X 10%

ding 15: MSD does not have financial staff or Board members with background or specific experience in the types of investments and other related financial activities undertaken at M

The Mayor of Louisville Metro Government is currently reviewing cand

for MSD Board positions in compliance with KRS 76.030. The plan is t

at least one of the four vacant positions to be filled with a professiona

investment and financial experience. It is expected that the MSD Boa

create an investment committee, or the duties of an investment com

will be delegated to an existing committee of the Board. These dut

include oversight of investment activity and financial management pro

reviewing detailed reporting of MSD's investment portfolio, all inves

activities, trends, and strategies; and questioning staff and financial a

regarding investment activity and programs to evaluate complianc

investment policies.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 22/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

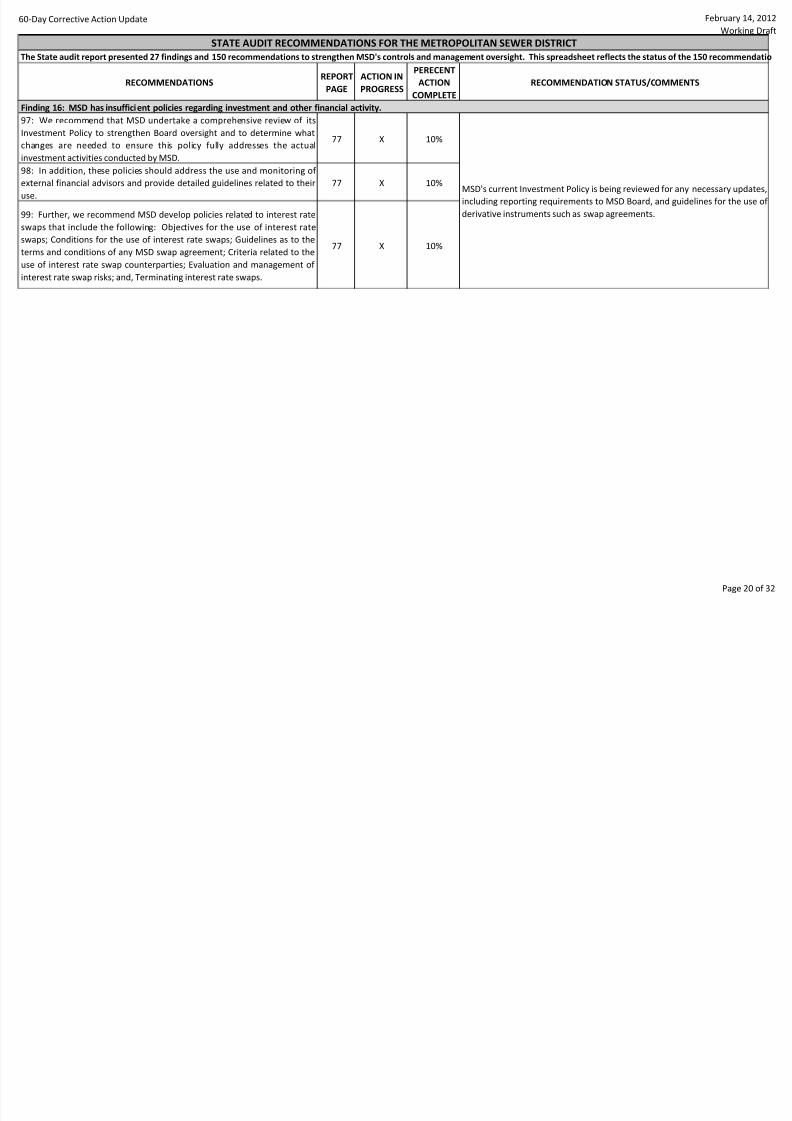

We recommend that MSD undertake a comprehensive review of its

estment Policy to strengthen Board oversight and to determine what

anges are needed to ensure this policy fully addresses the actual

estment activities conducted by MSD.

77 X 10%

In addition, these policies should address the use and monitoring of

ernal financial advisors and provide detailed guidelines related to their

e.

77 X 10%

Further, we recommend MSD develop policies related to interest rate

aps that include the following: Objectives for the use of interest rate

aps; Conditions for the use of interest rate swaps; Guidelines as to the

ms and conditions of any MSD swap agreement; Criteria related to the

e of interest rate swap counterparties; Evaluation and management of

erest rate swap risks; and, Terminating interest rate swaps.

77 X 10%

ding 16: MSD has insufficient policies regarding investment and other financial activity.

MSD's current Investment Policy is being reviewed for any necessary up

including reporting requirements to MSD Board, and guidelines for the

derivative instruments such as swap agreements.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 23/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

0: We recommend the MSD Audit Committee develop and approve

ocedures for the internal audit function.78 100%

1: The adopted procedures should state the process for the Internal

ditor to follow in initiating an audit, including the process for the Audit

mmittee to be informed of and approve or authorize any audit requests

t already on the annual audit plan made by management or other

rties.

78 100%

2: The adopted procedures should also state the acceptable time period

the Internal Auditor to allow management to respond to a draft audit

port.

78 100%

3: The adopted procedures should specify that the Auditor is to inform

e Audit Committee if management fails to respond to the draft report

thin the specified time period and the process to follow to release an

dit report when management fails to respond.

78 100%

4: The procedures should require the Internal Auditor to inform the

mmittee when a draft audit is completed for the Audit Committee to

view and approve the draft report prior to forwarding the report to

nagement for response.

78 X 90%

MSD is currently seeking further guidance from the State Auditor's Offi

Institute of Internal Auditors and other agency practices regardi

procedures for communicating preliminary draft audit reports to the

Audit Committee prior to management review.

5: Finally, procedures should require the Audit Committee, after

viewing and approving internal audit reports, to ensure internal audit

ports are presented to the full MSD Board for ratification.

78 100%

This recommendation has been incorporated into the Audit Committ

Internal Audit Charters adopted by the MSD Board on February 13,

Refer to the response provided in Finding 17, Recommendation 100.

ding 17: MSD lacks a formal process for initiating, performing, reporting and distribution of its internal audits.

Updates to the Audit Committee and Internal Audit Charters were ad

by the MSD Board on February 13, 2012. These updates include proc

for initiating internal audits, approval of audit requests by the

Committee, responses to audit findings by management, and appro

internal audit reports by the MSD Board. Also included were statem

responsibility for the Audit Committee to assist in performing the a

evaluation of the Internal Auditor, approve and recommend to the

Board an annual budget for the Internal Auditor, review and approval

annual work plan for internal audit, and to hold at least four me

annually, on a quarterly basis, to receive routine status updates fro

Internal Auditor. The adopted Internal Audit Charter states that the I

Auditor reports functionally to the Audit Committee and administrativ

the Executive Director. The MSD organizational chart was imme

revised to reflect the reporting structure of the Internal Auditor.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 24/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

6: We recommend the MSD Audit Committee perform the annual

aluation of the Internal Auditor.81 100%

7: We recommend the MSD Audit Committee approve and recommend

the full Board an annual budget for the Internal Auditor based on the

proved internal audit work plan.

81 100%

8: The Internal Auditor should request directly to the Audit Committee

e amount of funds estimated as necessary to conduct those audits. 81 100%

9: Once approved by the Audit Committee, the annual budget for the

ernal Auditor should be ratified by the full Board to be included in the

SD budget by the Finance Director.

81 100%

0: We also recommend the MSD Board revise the Audit Committee

arter to include within the Committee’s responsibilities the

rformance of the annual evaluation of the Internal Auditor and the

dgeting for the expenses of the Internal Auditor.

81 100%

1: We recommend the MSD Board revise the organizational chart of

SD to include a direct reporting line from the Internal Auditor to the

dit Committee of the Board.

81 100%

2: We recommend the MSD Audit Committee consistently approve the

nual MSD internal audit work plan as required under the Internal Audit

arter.

81 100%

3: Further, the Board should revise the Audit Committee Charter

guage to agree with the language in the Internal Audit Charter as the

rent Committee Charter only states the Committee is responsible for

iewing the work plan.

81 100%

4: Additionally, we recommend the MSD Internal Auditor provide

utine status updates on audits to the Audit Committee. This will foster

ntinued communication between the Internal Auditor and Audit

mmittee members. It will allow the Internal Auditor to discuss any

oblems that may be encountering on an audit with the Committee in a

ore timely manner and will allow the Committee an opportunity to

cuss any concerns they may have with the thoroughness of a particular

dit or regarding other areas of the organization that they may wish to

k her to investigate.

82 100%

These recommendations have been incorporated into the Audit Com

and Internal Audit Charters adopted by the MSD Board on February 13

Refer to the response provided in Finding 17, Recommendation 100.

ding 18: Oversight of MSD internal audit function primarily performed by executive management; MSD Audit Committee is not sufficiently engaged with Internal Audit.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 25/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

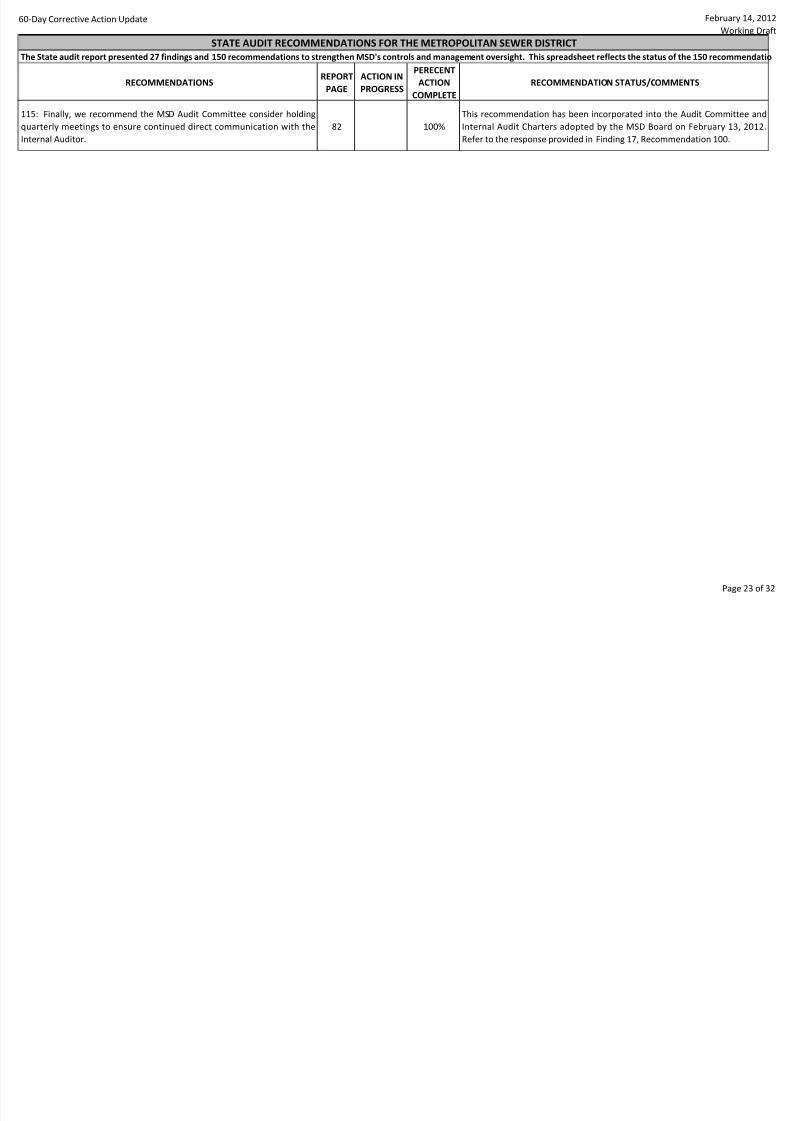

5: Finally, we recommend the MSD Audit Committee consider holding

arterly meetings to ensure continued direct communication with the

ernal Auditor.

82 100%

This recommendation has been incorporated into the Audit Committ

Internal Audit Charters adopted by the MSD Board on February 13,

Refer to the response provided in Finding 17, Recommendation 100.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 26/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

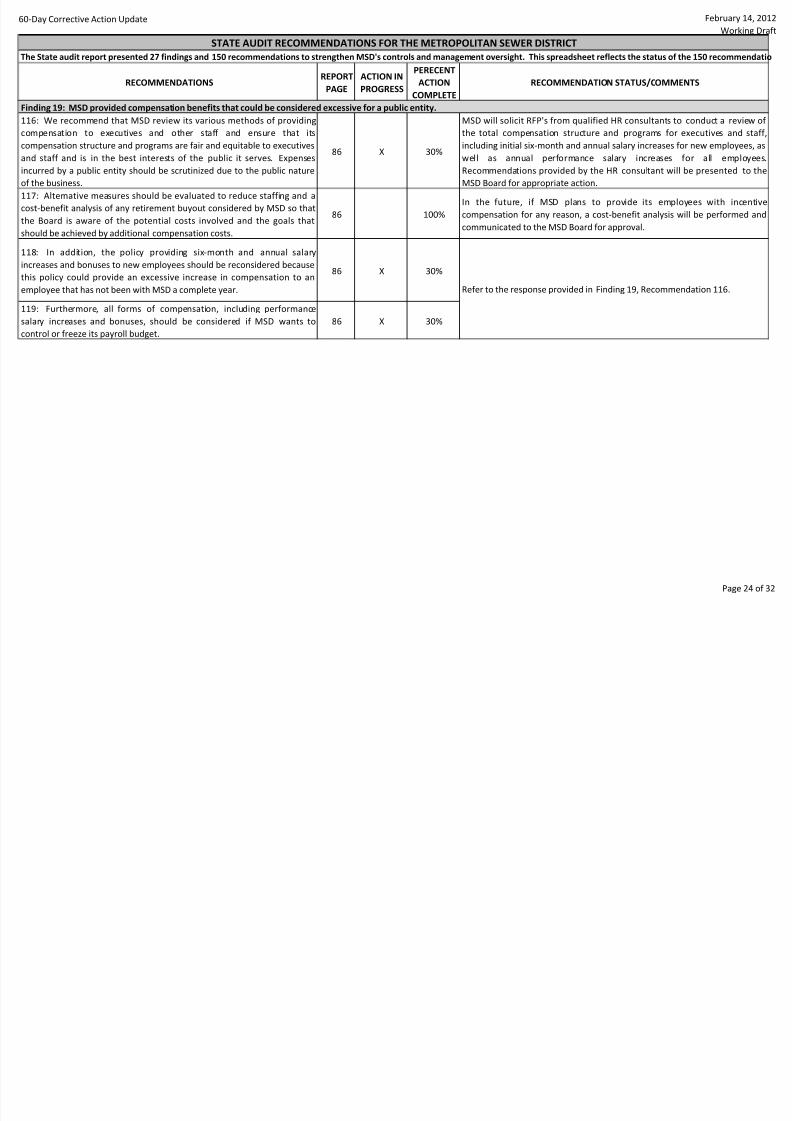

6: We recommend that MSD review its various methods of providing

mpensation to executives and other staff and ensure that its

mpensation structure and programs are fair and equitable to executives

d staff and is in the best interests of the public it serves. Expenses

urred by a public entity should be scrutinized due to the public nature

the business.

86 X 30%

MSD will solicit RFP's from qualified HR consultants to conduct a rev

the total compensation structure and programs for executives and

including initial six-month and annual salary increases for new employe

well as annual performance salary increases for all emp

Recommendations provided by the HR consultant will be presented

MSD Board for appropriate action.

7: Alternative measures should be evaluated to reduce staffing and ast-benefit analysis of any retirement buyout considered by MSD so that

e Board is aware of the potential costs involved and the goals that

ould be achieved by additional compensation costs.

86 100%

In the future, if MSD plans to provide its employees with in

compensation for any reason, a cost-benefit analysis will be performe

communicated to the MSD Board for approval.

8: In addition, the policy providing six-month and annual salary

reases and bonuses to new employees should be reconsidered because

s policy could provide an excessive increase in compensation to an

ployee that has not been with MSD a complete year.

86 X 30%

9: Furthermore, all forms of compensation, including performance

ary increases and bonuses, should be considered if MSD wants to

ntrol or freeze its payroll budget.

86 X 30%

Refer to the response provided in Finding 19, Recommendation 116.

ding 19: MSD provided compensation benefits that could be considered excessive for a public entity.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 27/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

0: We recommend MSD implement procedures to ensure compliance

h all procurement policies, particularly those pertaining to professional

vices. Employees responsible for procurement should be sufficiently

ined on those policies.

91 X 10%

Refer to the response provided in Finding 3, Recommendation 32. S

provisions will be provided for procurement of professional servic

training will be provided to employees in the procurement depar

employees

1: Further, we recommend MSD adopt the provisions in the Model

ocurement Code in KRS 45A.740, 45A.745, and 45A.750 pertaining to the

ocurement of architectural and engineering services.

91 X 90%

MSD has adopted the local public agency provisions of the Kentucky

Procurement Code (KRS 45A.345 through KRS 45A.460), and staff be

that the foregoing provisions allow for procedures similar to those auth

under KRS 45A.740, KRS 45A.745, and KRS 45A.750 and therefore enab

to award a contract for architectural or engineering related services

best firm qualified to perform the required work on the ba

demonstrated competence and qualification for the type of profe

services required and at fair and reasonable prices.

2: We recommend: Procurement Method Determination Forms be

mpleted in a timely manner in accordance with procurement policies

d used to document the method by which the agency intends to procure

ervice. It is a checkpoint to ensure the agency is utilizing the correct

ocurement method and should not be overlooked or completed after

e contract is signed or services are provided; MSD centrally maintain all

ocurement records; and, MSD only approve payments that have a signed

rchase Order.

92 X 10%

Refer to the response provided in Finding 3, Recommendation 32. In ad

will evaluate a central procurement process for engineering, constructi

goods and services to improve the controls, documentation, recor

payments to contractors and vendors.

3: We recommend that MSD’s policy of allowing the Board to waive any

all requirements related to the procurement of professional services bepealed.

92 X 0%

MSD staff is currently reviewing Procurement Regulations to determi

appropriateness of the Board's authority regarding procuremeprofessional services.

ding 20: MSD did not comply with procurement guidelines when procuring certain professional services.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 28/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

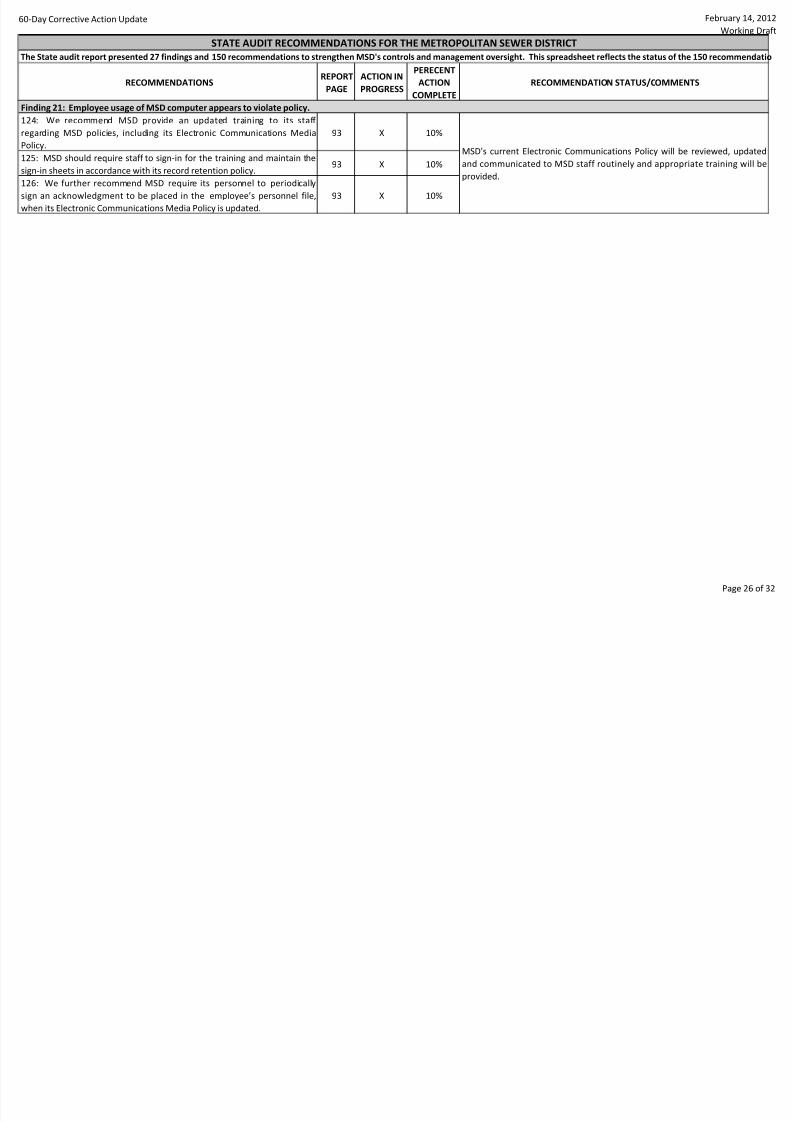

4: We recommend MSD provide an updated training to its staff

garding MSD policies, including its Electronic Communications Media

icy.

93 X 10%

5: MSD should require staff to sign-in for the training and maintain the

n-in sheets in accordance with its record retention policy.93 X 10%

6: We further recommend MSD require its personnel to periodically

n an acknowledgment to be placed in the employee’s personnel file,en its Electronic Communications Media Policy is updated.

93 X 10%

ding 21: Employee usage of MSD computer appears to violate policy.

MSD's current Electronic Communications Policy will be reviewed, u

and communicated to MSD staff routinely and appropriate training

provided.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 29/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

7: To ensure MSD retention schedules and related systems and

ocesses are being effectively carried out, we recommend MSD formally

opt records retention policies to be included in the Policies and Benefits

nuals for employees. Such policies should detail employee

ponsibilities over retaining required books, papers, maps, photographs,

cs, software, e-mails, databases, and other electronically generated

ords.

94 X 0%

8: We further recommend an archival policy and system be drafted and

opted specifically regarding proper e-mail retainage. Policies should also

lude training requirements.

94 X 0%

9: We recommend that all employees be formally trained on all records

ention requirements, including the proper retention of e-mail

mmunications.

94 X 0%

0: Upon employment, all new employees should be trained on records

ention responsibilities to assure proper retainage of records. MSD also

y want to consider having employees sign an acknowledgement that

ey have read and understand the records management policies.

94 X 0%

ding 22: MSD had no formal records retention policies or records retention training for its employees.

MSD has created a Records Retention Policy team to develop a

retention policy. The policy will detail employee responsibilitieretaining required books, papers, maps, photographs, discs, softw

mails, databases, and other electronically generated records. All c

employees and new hires will be trained of records retention require

including proper e-mail retention. A comprehensive policy is needed a

take up to 10 months to develop and implement. Plan is to compl

December 15, 2012.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 30/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS

STATE AUDIT RECOMMENDATIONS FOR THE METROPOLITAN SEWER DISTRICT

e State audit report presented 27 findings and 150 recommendations to strengthen MSD's controls and management oversight. This spreadsheet reflects the status of the 150 recomm

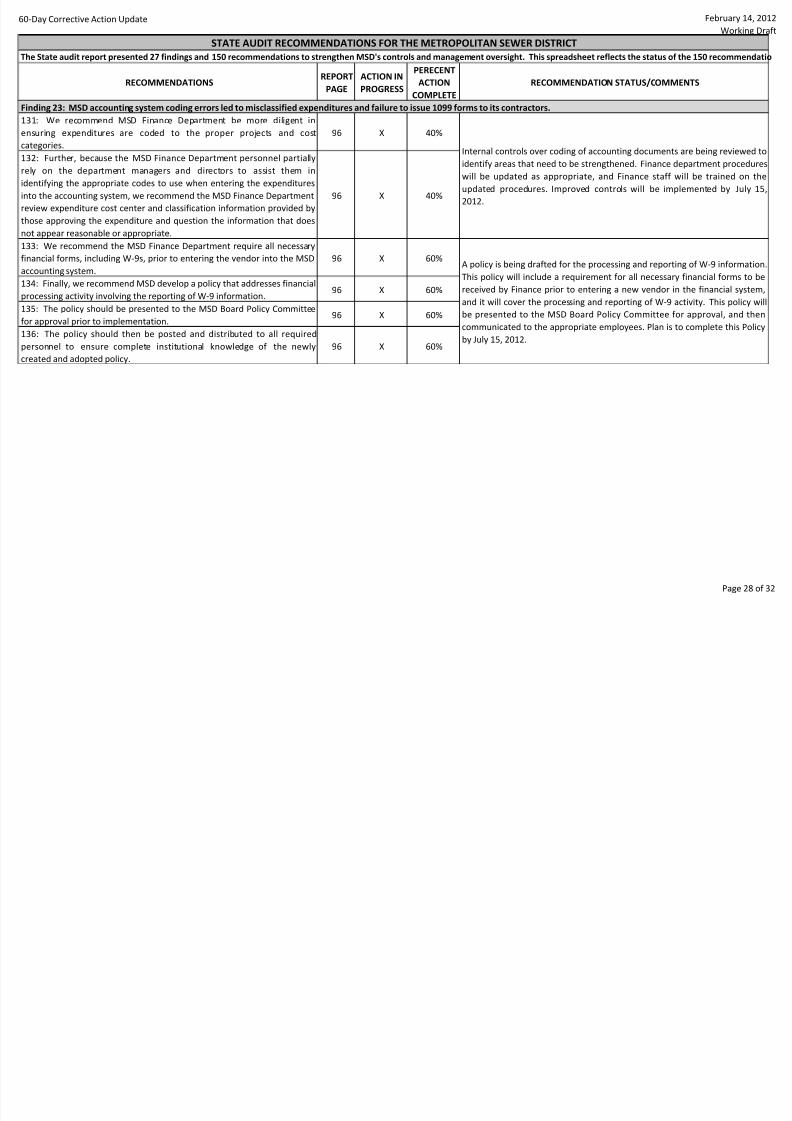

1: We recommend MSD Finance Department be more diligent in

suring expenditures are coded to the proper projects and cost

egories.

96 X 40%

2: Further, because the MSD Finance Department personnel partially

y on the department managers and directors to assist them in

ntifying the appropriate codes to use when entering the expenditures

o the accounting system, we recommend the MSD Finance Departmentiew expenditure cost center and classification information provided by

ose approving the expenditure and question the information that does

t appear reasonable or appropriate.

96 X 40%

3: We recommend the MSD Finance Department require all necessary

ancial forms, including W-9s, prior to entering the vendor into the MSD

counting system.

96 X 60%

4: Finally, we recommend MSD develop a policy that addresses financial

ocessing activity involving the reporting of W-9 information.96 X 60%

5: The policy should be presented to the MSD Board Policy Committee

approval prior to implementation.96 X 60%

6: The policy should then be posted and distributed to all required

rsonnel to ensure complete institutional knowledge of the newly

ated and adopted policy.

96 X 60%

ding 23: MSD accounting system coding errors led to misclassified expenditures and failure to issue 1099 forms to its contractors.

Internal controls over coding of accounting documents are being review

identify areas that need to be strengthened. Finance department proc

will be updated as appropriate, and Finance staff will be trained

updated procedures. Improved controls will be implemented by J

2012.

A policy is being drafted for the processing and reporting of W-9 inform

This policy will include a requirement for all necessary financial forms

received by Finance prior to entering a new vendor in the financial sy

and it will cover the processing and reporting of W-9 activity. This pol

be presented to the MSD Board Policy Committee for approval, and

communicated to the appropriate employees. Plan is to complete this

by July 15, 2012.

Page

8/3/2019 MSD 60-day response to state auditor 2-14-2012

http://slidepdf.com/reader/full/msd-60-day-response-to-state-auditor-2-14-2012 31/59

Day Corrective Action Update February

Work

RECOMMENDATIONSREPORT

PAGE

ACTION IN

PROGRESS

PERECENT

ACTION

COMPLETE

RECOMMENDATION STATUS/COMMENTS