nai black’s nai black market...nai black’s roots have been in spokane for over 50 years. we’re...

TRANSCRIPT

NAI Black’s roots have been in Spokane

for over 50 years. We’re committed to

being an active partner in the Inland

Northwest’s great history and its vibrant

future. NAI Black is proud to manage,

lease and market for sale commercial

real estate properties throughout Spokane

and the region. We look forward to our

continued role in building a dynamic and

vital Inland Northwest.

2

Serving the Inland Northwest’s Commercial Real Estate Needs

• Asset Management • Sales Investments• Association Management • Real Estate Development• Tenant & Buyer Representation • Consulting • Facilities Management • Business Opportunities

n Letter From Our CEO 4

n Retail 6

n Office / Medical Office 8

n Business Opportunities 11

n Industrial 12

n Downtown 14

n Apartments 16

n Troubled Assets 18

n Principals / Agents 19

3

A L E T T E R F R O M O U R C E O

am very pleased to report that 2012 was an incredible year for all of us at NAI Black. We have three major companies within our firm, and we hit on all cylinders for record revenue! Black Realty Management, Inc., our property management group, led by President John Bennett, recorded several large new clients and many new accounts, making 2012 the busiest year ever in our company’s 55-year history. We acquired a portfolio of 20 apartment management accounts with 1,200 units from McVicars and Associates. We also added 32 grocery anchored shopping centers totaling one million square feet of GLA throughout the Inland Northwest to our growing portfolio of commercial and retail space under management. We continue to add trophy accounts such as Rock Pointe Corporate Center, Wells Fargo Center, the Integrated Medical Plaza acquired by a health care REIT, and many others. We also remodeled our entire sixth floor at the James S. Black building and are very happy with our new space. The new property managers and staff that we added in connection with the McVicars accounts are fantastic additions to our team.

Black Commercial, Inc., our commercial brokerage group, under President Jeff Johnson, had a record year up 70%, and truly led the way in eliminating the negativity that still may be lingering in our minds over the Great Recession. Not that all of the markets have fully recovered, it just seems that companies and people are finally doing things and deciding that they cannot put their firms’ commercial real estate needs on hold forever. Our commercial brokers each had a much better year in 2012 than they did the previous three or four years.

Highlights of our year included: selling the Wells Fargo Center (we sold the note to INHS from Sterling, then INHS completed the foreclosure); finishing the Lowe’s ground lease on North Division; completing the Hobby Lobby lease at Lincoln Road and Division; selling the Coeur d’Alene Town Center shopping center; taking over the leasing of the US Bank Building; selling the former Eastern Washington University building downtown; and many large office lease renewals such as Pitney Bowes, US Bank, and the Washington State Department of Social & Health Services at Rock Pointe Corporate Center.

I am very excited about what 2013 will hold. We continue to work with financial institutions to resolve their bad loan issues, and our development and investment efforts are picking up steam. Investors are excited because interest rates are at a historic low, and capitalization rates, especially in this Inland Northwest region, are relatively high. This creates positive leverage that is unprecedented. For example, a 10% free and clear return (cap rate) when leveraged with a mortgage constant of 6% will yield a 22% cash on cash first-year return! A great yield and a sound place to put your money. This is especially true given low returns on cash equivalent investments and the risks in today’s stock market. Real estate seems to be safer as the federal government deals with the debt ceiling, budget deficits, and other major fiscal issues.

I

4

A L E T T E R F R O M O U R C E O

We continue to be involved in industry, civic and charitable organizations. We have board members and volunteers throughout our company in many different and important capacities, such as the GSI Board of Trustees, Downtown Spokane Partnership Board, Washington Policy Center Eastern Washington Advisory Board, and Boy Scouts of America.

I want to personally take this opportunity to thank all of our great clients, business friends, and those that have associated with us in the last 55 years of doing business. We have come a long way since my father, James S. Black, Sr., founded the company in the holiday season of 1957; the year I was born. He had purchased the oldest real estate company in Spokane, Arthur D. Jones Company, which was founded in 1887. This technically makes us the oldest real estate company in our region, and we are the largest. I am entering my 32nd year of the real estate business and my 29th year of running the company. I am a lucky man to work around so many great people and to have a first- hand view of what is going on in our region. It’s never boring! Someone once said, “Find a job you love, and you will never have to work a day in your life”. This is how I feel when I come to work every day, and I trust those that work with us feel the same way.

Thank you for your continued business!

David R. BlackNAI BlackChief Executive Officer

5

David R. Black CCIM, SIOR

6

R E T A I L

Retail Opportunities Expected In 2013

he demand for retail space on the South Hill and North Spokane increased in 2012. This resulted in lower vacancy rates and in some cases increased rental rates. The South Hill retail market is currently enjoying a 4% vacancy rate, which has resulted in multiple tenants vying for the few remaining spaces. This improvement is primarily due to quality retailers like Trader Joe’s and Ross Stores leasing refurbished legacy center space and attracting other tenants who want to profit from the traffic generated by those stores. The Valley market experienced increased vacancy and decreased average rental rates. This provides attractive opportunities for tenants seeking space in 2013. The downtown CBD retail market held steady with national retailers continuing to consider space options in the best locations. A vibrant coalition of downtown organizations has worked hard to maintain downtown Spokane as an energetic and profitable location for national retailers.

A positive contributor to the North Spokane retail market is the opening of a portion of the North Spokane Corridor, which will eventually connect the Highway 395 Wandermere area to I-90 in 10.5 miles of multi-modal highway. This corridor will provide an evolving stimulus to the outlying consumer market giving easier access to North Spokane retailers.

During 2012, a number of well-positioned iconic shopping centers such as Lincoln Heights and Manito engaged consultants to update their store front appearances and merchandise mix to increase retail traffic. In a transitional retail market, an architectural upgrade has been a proven formula for tenant success and increased sales. Of note, the lower Perry Street Historic District has seen resurgence in quality neighborhood retail interest, keeping pace with the young urban professionals re-establishing their lifestyles in older transitional neighborhoods.

The Washington State Liquor Control Board state–owned stores (Initiative 1183 that became effective in June 1, 2012) that were de-commissioned, paved the way for larger foot print private sector wine and spirits operators to enter the market. Of note was the opening of a 25,000 square foot Total Wine store in the Northpointe Plaza Shopping Center on Spokane’s North side. Correspondingly, the majority of the local grocery, drug stores and large format stores such as Costco took advantage of I-1183, by adding hard liquor to their product lines. This shift and expansion of the wine and spirit venues is likely to continue at an aggressive rate through 2013.

This year, a number of national retailers are evaluating the Spokane market for new concepts, especially discount retailers and grocery operators who are back-filling vacated big box spaces. National retail trends suggest an 11% growth of new store openings, and a growing trend to open “stores within a store.” Target has opened Apple Displays; JC Penney operates Mango and Sephora units; and Finish Line plans to open 450 stores inside Macy’s. The evolving store downsizing (square footage) of many national brands

T

has provided a creative vehicle to place their presence in a market that was previously not considered. Portland and Seattle retailers have been aggressively eyeing Eastern Washington opportunities. During 2012, the Valley, anchored by the Spokane Valley Mall, saw the opening of Dick’s Sporting Goods; and H & M, a Swedish multinational retailer. The fifth Spokane area Wal-Mart superstore opened its doors on Sprague Avenue near Costco. Hobby Lobby and a re-positioned Lowes Home Improvement made a strategic impact on North Division. North Town Mall opened a Marshall’s, replacing the exiting Nordstrom Rack, which relocated to the Valley. The confidence exhibited by these large format stores has reenergized the demand for outparcel development. Quick serve restaurant brands are expanding in Spokane, with Jimmy John’s, Subway, Bruchi’s CheeseSteaks and Subs, and Chipotle taking advantage of key locations that were open in the market.

We expect the retail market to improve at a slow and steady pace during 2013 as retailers adapt to a new post-recession economy. National fiscal policy will likely have a muting effect in the short term, but the efficiencies of the market place, coupled with improving fundamentals of job growth, rebounding residential housing, continuing low inflation, and increasing consumer confidence should serve to sustain steady retail growth in the long run.

Our retail specialists bring a wide range of experience in acquisitions, dispositions, community centers, and regional mall tenant representation. We have been involved in leasing, property management or development of almost every major shopping center in the region. NAI Black is extensively involved with the International Council of Shopping Centers, and is a retail market leader in all of Eastern Washing- ton and Northern Idaho. The NAI Global network of independently owned companies continues to provide a great source of networking, leads, education and technology.7

Stephen B. Pohl David B. Wright CPM®

© Auble, Jolicoeur & Gentry, Inc., 2012

8

Tenants Are King

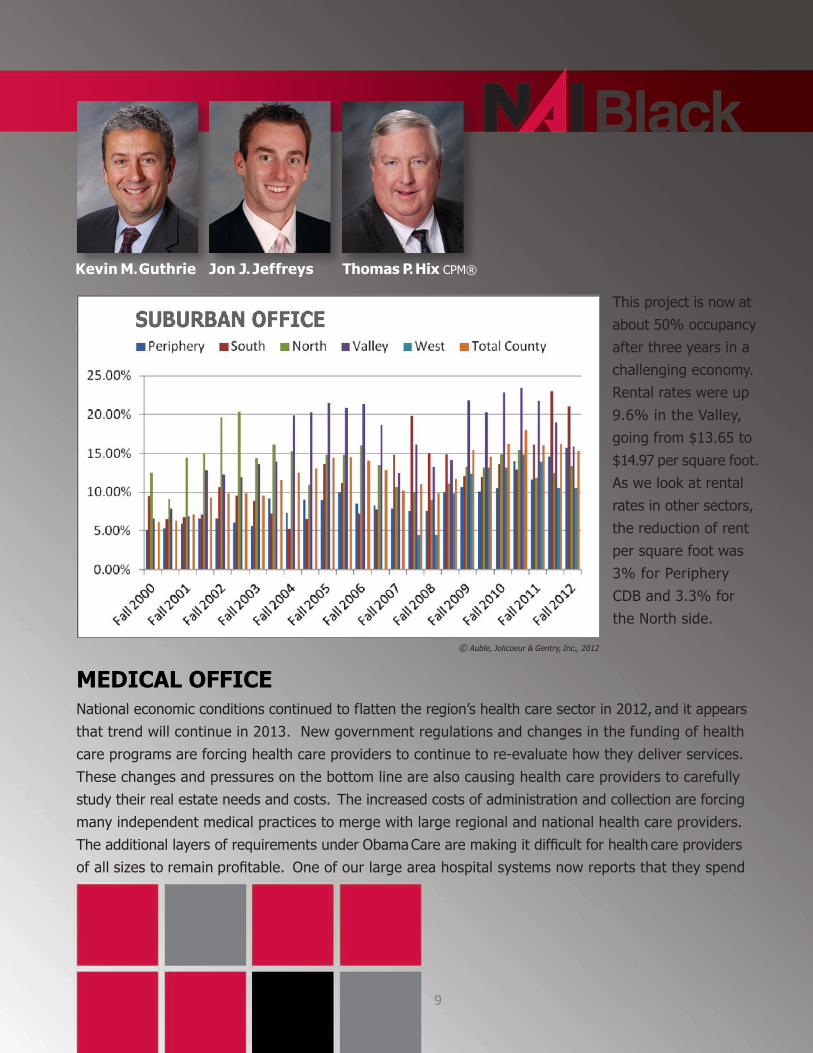

he best characterization of the Spokane office market in 2012 is to say that it was a good year for tenants to get some great deals on office space, both for renewals and relocations. Leasing activity was flat with very few new tenants coming into the market over the last year. The majority of the leasing activity was musical chairs with existing tenants taking advantage of a soft market to relocate to better space for equal or less rent. Many tenants with leases rolling over in 2012 tested the market with RFPs, but the majority renewed their leases in their existing spaces due to aggressive landlord retention efforts. The overall vacancy rate for all classes of office space decreased slightly from 15.85% in February 2012 to 14.25% at the end of October 2012. Landlords are reporting that to retain their existing tenants, they found it necessary to reduce rents down to current market rates and provide their tenants with generous refurbishment allowances for carpet, paint and other improvements. Tenants have enjoyed reductions in rent; in some cases, from $21 per square foot down to $17 per square foot on a full service lease for Class A space. The majority of the leasing activity during the year took place with smaller tenants leasing or relocating to spaces from 1,000 square feet to 3,000 square feet. Deals for larger office tenants over 5,000 square feet were limited. The tenants who were out in the market place in the last year took full advantage of the soft market conditions to make some very attractive deals. Only landlords who were highly motivated and willing to adjust to the lower rents and greater incentives were leasing space and renewing leases. The CBD Class A office market is comprised of nine surveyed office buildings with 1.1 million square feet of office space. In October 2012, approximately 98,500 square feet (or 8.89%) of the CBD Class A office market was vacant. The surveyed average rental rates for these buildings worked out to $21.71 per square foot, though based on the individual transactions that occurred over the last year, it would appear that this number is high. The largest pockets of vacancy are in Wells Fargo Center and the Chase Financial Center with approximately 60,500 square feet of the available space in those two buildings.

In the CBD periphery, the market is comprised of 120 buildings and nearly three million square feet of office space. Approximately 470,000 square feet of space was vacant in October 2012, representing 15.67% of the total. Over one-quarter of that total vacant space is situated in the four-building Rock Pointe Corporate Center complex. Leasing activity in that project has produced a number of new tenants from 1,000 to 5,000 square feet over the last year. With very few large floor plate spaces available in the CBD (space over 10,000 square feet) Rock Pointe holds a major, strategic advantage in attracting large space users looking for 10,000 to 30,000 square feet.

In review of all the submarkets, there was a slight reduction in vacancy from 16.2% in February 2012 to 15.35% at the end of October 2012. The Valley market was the best performing sector with office space vacancy going down from 21.76% in October 2011 to 15.83% at the end of October 2012. This reduction can be attributed to the slow but steady leasing activity at the Riverview Corporate Center office building along I-90 at Sullivan Road.

O F F I C E & M E D I C A L O F F I C E

T

9

This project is now at about 50% occupancy after three years in a challenging economy. Rental rates were up 9.6% in the Valley, going from $13.65 to $14.97 per square foot. As we look at rental rates in other sectors, the reduction of rent per square foot was 3% for Periphery CDB and 3.3% for the North side.

MEDICAL OFFICE National economic conditions continued to flatten the region’s health care sector in 2012, and it appears that trend will continue in 2013. New government regulations and changes in the funding of health care programs are forcing health care providers to continue to re-evaluate how they deliver services. These changes and pressures on the bottom line are also causing health care providers to carefully study their real estate needs and costs. The increased costs of administration and collection are forcing many independent medical practices to merge with large regional and national health care providers. The additional layers of requirements under Obama Care are making it difficult for health care providers of all sizes to remain profitable. One of our large area hospital systems now reports that they spend

Kevin M. Guthrie Jon J. Jeffreys Thomas P. Hix CPM®

© Auble, Jolicoeur & Gentry, Inc., 2012

10

approximately 12% of every dollar they generate on the billing and collection process necessary to meet state and federal regulations. The health care community continues to be a key contributor to Spokane’s economic vitality. In 2012 we saw a number of local medical practices absorbed by our major health care providers. These major health care providers are expanding their medical office facilities to accommodate the practices being absorbed. Providence Health & Services has broken ground on 140,000 square feet of medical space along I-90 in the Spokane Valley, and Cancer Care Northwest has also broken ground with a new 20,000 square foot center in the Valley where they will move the administrative office and Valley Clinic. The State of Washington has funded a $78 million WSU biomedical and health science building on the Riverpoint campus. This 110,000 square foot structure is under construction and will be a great addition to the University District. In addition to these large projects, local dentists and specialty health care providers continue to construct and occupy small stand-alone medical buildings for their own use. This trend has continued through the recession as one of the bright spots in the office development market. The October 2012 survey for medical office space showed a vacancy rate of 10.34%, which is lower than vacancy in the October 2011 report of 10.93%. The average rental rate went down nominally from $22 per square foot in October 2011 to $21.16 per square foot in October 2012; a 3.8% reduction. The outlook for the future of medical office space in Spokane is bright. The mandated health care and growing federal regulations related to Obama Care will most likely drive the need for additional administrative office space in the years ahead. With record low interest rates, small local specialty medical service providers will continue to purchase or develop office buildings for their own use. We anticipate that the medical office market will remain stable in 2013 with the potential for additional growth in the years ahead.

M E D I C A L O F F I C E ( c o n t i n u e d )

© Auble, Jolicoeur & Gentry, Inc., 2012

11

ccording to survey results released November 28, 2012, by BizBuySell.com, the internet’s largest marketplace for buying or selling small businesses, business brokers reported an increase in business-for-sale transactions in 2012 and predict even more businesses sales in 2013. Of the nearly 5,000 business brokers surveyed across the nation, 61.1% of respondents believed the business-for-sale market improved in 2012 compared to 2011, and 28.6% of those that saw improvement cited an increasing number of interested buyers being the leading factor assisting in more closed transactions. Another 21.1% stated an increase in the amount of owners selling their business, and 17% indicated sellers’ more realistic sale price expectations as the driving force. “The brokers’ positive sentiment toward 2012 reflects a general trend we’ve seen in the business-for-sale marketplace since hitting bottom in 2009,” said Curtis Kroeker, General Manager of BizBuySell.com. “Overall, there has been a slow, but steady, improvement as buyers and sellers continue to find ways to get more deals done, despite challenging operating and financing environments.”

In 2012, business sales activity in the Spokane area market coincided with national trends. With consumer confidence on the rise, most area business brokers saw that more buyers entered into the business- for- sale market in 2012, compared to 2011 and previous years. The general consensus is that business sales in the Spokane area will increase in 2013. With more buyers entering the market, an increase in business sales is expected, but is more likely to happen if the businesses on the market are priced aggressively and seller financing is available. The SBA loan process and other traditional forms of lending are still constricted in funding small business acquisitions, so the majority of buyers in the market to purchase a business right now are cash buyers looking for extraordinary deals. In order to appeal to these buyers, sellers need to price accordingly and offer seller financing.

John T. Powers, III

An Increased Number Of Interested Buyers

B U S I N E S S O P P O R T U N I T I E S

A

12

I N D U S T R I A L

Industrial Market Ready For Rebound

AI Black and its market survey partners surveyed 27,300,128 square feet of industrial space in 1,206 buildings in our Fall 2012 survey. Overall, the composite vacancy rate for the West, CBD, North, East, Valley, and Liberty Lake industrial markets was 8.61% in October, with 2.35 million square feet vacant. The vacancy rate has declined from 10.9% reported in October 2011; an indication of material improvement. Over that last year, the level of industrial space absorption or increased vacancy varied by submarket. In the Spokane Valley market, where over 53% of the leasable space is located, the vacancy rate dropped from 12.49% in 2011 to 8.45% in 2012. This substantial improvement in occupancy was the result of a few major lease transactions. One of those transactions was the lease with PepsiCo for over 80,000 square feet at the Central Business Park, located at 11016 East Montgomery. Another transaction was the lease to Aramark Uniform of 17,000 square feet at 11511 East Indiana. Spokane Industrial Park (S.I.P.), owned and managed by Crown West Realty, completed six transactions over 20,000 square feet in 2012, which contributed to that vacancy reduction. Those S.I.P. lease transactions had an average term of seven years and an average rental rate of $.028 square feet NNN. The next largest market, West Spokane, saw a decrease from 7.59% to 6.5%. Other submarkets showingimprovement were the CBD (14.69% to 8.81%) and North submarket (9.04% to 8.0%). Only the East market (8.55% to 10.46%) showed an increase in vacancy. The Liberty Lake market showed no significant change.The chart on the next page illustrates a material drop in recent and average rental rates year-over-year for industrial office space. Industrial property owners have been more aggressive in lowering their expectations on office rents to attract industrial tenants whose needs tend to be more warehouse oriented. This reduction of rent on the office space in warehouse buildings has reduced the overall warehouse rental rates as shown in the fall survey on Page 13. The West Spokane submarket saw the biggest drop in rental rates as property owners attempted to attract tenants previously focused more on the Valley industrial market.

There is a major owner-occupant component to the inventory of small and medium sized industrial buildings in Spokane. These owner-users influence the majority of industrial sales activity in Spokane each year from a number of sales standpoints. Investor sales are fewer in number but can be higher in sales volume as investors are usually purchasing properties priced over $1,000,000. In 2010, there were 35 sales of industrial properties; 28 in 2011; and only 17 in 2012. Deal volume decreased from $21,360,000 in 2010 to $11,900,000 in 2012. Despite the decrease in both the number of sales and the overall sales volume, the average sales price per square foot for industrial buildings increased slightly from $45 per square foot in 2011 to $49 per square foot in 2012. Buildings from 3,000 to 20,000 square feet sold from $40 to $68 per square foot and larger buildings up to 100,000 square feet sold for as low as $24 per square foot. NAI Black brokered the sale of a 91,000 square foot warehouse building located at 715 East Sprague in the CBD industrial market to a local investor group. The sale price per square foot for that property was slightly over $26, and the

N

13

building had a mix of office and warehouse tenants. Industrial land prices held steady or decreased slightly in major industrial corridors but declined due to lack of demand in secondary and outlying industrial areas. Land sales in the far East Valley were at a low of $.50 per square foot. Northeast Spokane land sellers reduced prices as low as $2.00 per square foot to attract purchasers. Land sales between downtown and Sullivan Road resulted in sales between $2.25 and $3.00 per square foot. The overall industrial market appears to have bottomed out, and we anticipate overall improvement in 2013. The number of industrial property sales should increase from the 17 properties sold in 2012. Land sales should increase to users as financing rates for new construction are at all time lows. Increased market absorption of vacant rental space should be influenced by the lack of spec industrial development. There will need to be a significant increase in rental rates before developers come back into the market. So overall, we see a slow but steady improvement in the industrial market in 2013. Our industrial brokerage team forecasts leasing activity to be moderately better in 2013 than in 2012, as the regional and national economies continue to recover.

Darren Slackman Heidi A. Irvine

© Auble, Jolicoeur & Gentry, Inc., 2012

14

D O W N T O W N

Downtown Renaissance Continues

pokane is fortunate to enjoy a very vibrant downtown with great shopping, dining, and entertainment adjacent to the Spokane River and Riverfront Park. These attractions make Downtown Spokane a great place to both live and work. Since 1999, over $3.7 billion in public and private capital has been invested in some 800 construction, renovation, redevelopment, and infrastructure projects in Downtown Spokane. This Downtown Spokane Renaissance continues even though the pace of activity has been slowed down by the recession. Despite this slowdown, there were still deals taking place in Downtown Spokane throughout 2012.

There is a continued interest by both investors and end-users in purchasing and upgrading Downtown Spokane’s older historic buildings. Some of the sellers of these properties have been local banks who have been forced to take back failed projects. These properties have been priced to fit the new economics of today’s commercial real estate market. That new pricing, coupled with willing cash buyers, has resulted in a rising number of sales. Cash has been king this year with most buyers in the market making purchases without bank financing. The few purchasers in the market with the ability to pay cash have resulted in reduced prices and more aggressive negotiations.

Very few buyers requiring a high degree of leverage have been able to obtain financing and complete transactions during 2012. The lenders have narrowed their sights to only making loans to purchasers with the ability to make a large down payment or providing a very liquid financial statement. End-users can still obtain SBA financing, but the investment market requires a buyer to have a significant amount of skin in the game. There have been some owner-user purchases, but these buyers are required to have a strong balance sheet for their business, as well as a strong personal financial statement. An example of an owner-user sale would be the purchase and rehabilitation of the Forester Building at 35 West Pacific Avenue, which had laid vacant for nearly a decade. It is now the home of Emvy and Bridge Press Wineries.

Near the latter part of 2012, American West Bank, Cathay Bank, and Washington Trust Bank sold their entireHavermale block portfolio to two separate developers at bargain basement prices. The block consisted of approximately 63,000 square feet of improvements and a 27,000 square foot parking lot, for a combined purchase price of approximately $2.7 million. Also sold in 2012 was an old downtown warehouse buildingat 130 West Pacific, which was purchased by an investor-user at year-end for $360,000.

Also in 2012, two notable lease transactions in Downtown Spokane were the Spokane College of English Language (leasing 8,072 square feet of space at 718 West Riverside), and Columbia State Bank (leasing 11,019 square feet of space in the Fernwell Building). The Downtown Spokane office market remained flat in 2012 with a limited number of tenants relocating and landlords working hard to hang on to their existing tenants.

S

15

As 2012 came to an end, the Downtown market saw an increase in commercial real estate sales activity. Some of this activity was the result of sellers pushing to close sales and take full advantage of the current capital gains tax rates that are expected to increase in 2013. Overall, this increase in activity signals the recession finally turning around in Spokane. We anticipate a stronger Downtown Spokane commercial real estate market in 2013.

Mark C. McLees Kevin M. Guthrie

16

A P A R T M E N T S

Apartment Market Showed Continuing Improvement In 2012

he year 2012 was a good time to be an apartment owner, with vacancy continuing to drop from its 2009 peak and rental rates continuing to rise! In terms of trends anticipated for 2013, however, following an onslaught of new construction, we foresee Spokane County apartment vacancies ticking upwards as the market absorbs new construction above historical production levels, while Kootenai County is likely to stay relatively strong with upwards pressure on rents continuing.

Spokane County

Within the last 12 months, we have seen stabilization in the market place and the upward trending in rents, including the “burning off” of rental concessions. Property owners and developers took this as a green light to build more apartments, and lenders climbed on board. Average rents for all unit types in March 2011 for the Spokane area were $676; March of 2012 average rents rose 3% to $697. Average overall vacancy rates in March 2011 were 5.1% and slightly decreased to an overall vacancy rate of 5% in March 2012; viewed by many as a point of equilibrium. The Washington Center for Real Estate Research’s most recent survey (September 2012) shows Spokane County with an overall vacancy rate of 4.3%. Lowest vacancies are seen in the studio units at 1.3% and two-bedroom vacancies are averaged at 4.9%. Rental rates showed a decrease as of September 2012 averaging at $678 per month. Two-bedroom units in March 2012 had the highest reported vacancy rates at 6.6%, with one-bedroom units at 4.1% vacancy. Two-bedroom units in September 2012 reported 5.8% vacancy and three-bedroom units September 2012 led the market with the highest vacancy rate of 6.9%. The year-end 2012 Spokane County average vacancy rate was estimated to close at 5.1%.

Kootenai County

On March 15, 2012, Kootenai County had an average apartment vacancy rate of 3.8%. In June, this rate rose to 5.3%. In September, the overall vacancy rate dropped markedly to a remarkable 1.5%. The highest vacancy in September was seen in the three-bedroom one-bath units with vacancy rates at 2.7%. This is largely due to the availability of duplexes, single family homes, and townhomes in the same price range or lower. An estimated 263 new apartment units were brought online to market in 2012, with another 121 units being available in early 2013. As of July 2012, another four apartment projects totaling 175 units were approved. The majority of new apartment construction in Kootenai County has been in the affordable, low-income housing sector.

2013 Forecast

The 2013 forecast for Metropolitan Spokane is for material softening of occupancy rates, with 1,203 units coming online between now and within the next six months, and another 943 units starting and/or proposed construction in 2013. We anticipate rental rates to be flat or softening in the submarkets where the majority of new construction is to occur, including, but not limited to, the Spokane Valley. As is typical in these cycles,

T

17

there will likely be trickle down impacts upon Class A, B, and C markets as rent-up ensues on the newly created inventory. There is no corresponding uptrend in population, employment, or job growth forecasted for the Spokane area in 2013 at the rate of construction of new multifamily housing. We can likely expect rental rates to start stalling out and possibly trending downwards by third or fourth quarter 2013. Rental concessions with the new construction projects are highly likely. Spokane Valley will be the hardest hit area with 821 units at or near completion at year-end 2012, and another 279 units to start construction in early 2013. Kootenai County can expect vacancy rates to climb moderately with the influx of new construction impacting both Post Falls and Coeur d’Alene.

The Apartment Resale Market

Mitch Swenson maintains a proprietary data base of apartment investment transactions in Spokane County. Financing, though advantageous, remains difficult to procure; thus, sales of multifamily properties in the Spokane Region fell off from $58,000,000 in 2011 to $16,500,000 in 2012. This denotes a decrease of over 400%. Cap rates remain very strong on the transactions that were recorded in 2012 at an average of 7%. Apartments as an asset class remain on the top of most investors’ list, but the overall uncertainty in the national and local economies, as well as the amount of new projects being brought online, will continue to put apprehension in the market. That being said, many investors appear to be looking at secondary markets due to the huge run up of values in larger cities; so, 2013 could hold great promise for the multifamily market.

Mitch D. Swenson CCIM Kim Sample Jason J. Jackson ARM

© Auble, Jolicoeur & Gentry, Inc., 2012

18

ixed rate CMBS loan maturities have steadily increased 2009-2012, but are expected to moderately decline in 2013 before beginning a steep climb through 2017. At the IMN’s 9th Annual Winter Forum on Real Estate and Private Fund Investing in 2012, one expert opined that about 65% of the $1.7 trillion of commercial mortgage-backed securities maturing between 2012 and 2016 will not qualify for refinancing at maturity. Most of this debt was originated when values and rents were at historical highs but values declined materially below market peaks.

Delinquency rates for commercial real estate lenders remain disparate by lender type. CMBS, life company, Fannie Mae, Freddie Mac, and banks and thrifts hold approximately 80% of the commercial real estate debt outstanding. In the third quarter of 2012, a published Mortgage Bankers Association Report reflected 8.86% of CMBS as delinquent, compared with 0.12% of life company loans; 0.28% of Fannie Mae loans; 0.27% of Freddie Mac loans; and 2.93% of bank and thrift loans. Subsequent reports pegged CMBS delinquency at 9.38%. It was further projected that CMBS delinquencies will decline to 9.0% by year-end 2013. A positive trend is a conclusion that newly delinquent loans have been declining steadily. We have observed in the Spokane market that several of the major CRE delinquencies have been in default since 2010 and are still working through the resolution process. As the Spokane CRE market continues to emerge from the recession, some borrowers and lenders will face ongoing challenges with maturing loans that do not meet conforming underwriting standards for refinancing due to a combi- nation of tighter criteria, compression in commercial rents, and/or changes in occupancy levels. NAI Black continues to be a local market leader in receiver- ships, REO management and leasing, and troubled assets liquidation.

T R O U B L E D A S S E T S

FJohn M. Bennett CPM® Christopher D. Bell

Commercial Real Estate Loan Maturity & Delinquency Trends

David R. Black CCIM, SIOR Jeff K. Johnson CCIM, SIOR Mark G. Pinch CCIM, SIOR Gloria A. Ries CPA John M. Bennett CPM® Thomas P. Hix CPM®Chief Executive Officer President Chief Financial Officer President Senior Vice President

C. Brian Anderson Christopher D. Bell James S. Black, III CCIM Earl L. Engle CCIM Kevin M. Guthrie Jamie R. Hutchison

Heidi A. Irvine Jason J. Jackson ARM Don B. Jamieson Jon J. Jeffreys Mike P. King Jeff A. McGougan

Mark C. McLees Jim A. Orcutt J. Grant Person Stephen B. Pohl John T. Powers, III Aaron J. Reugh

Kim Sample Darren Slackman Jeffrey A. Swanson Mitch D. Swenson CCIM Scott Thaler Ryan Towner

Commercial Management

Commercial Real Estate Services, Worldwide.

Black Commercial, Inc.Black Realty Management, Inc.

509.623.1000 Bryan A. Walker David B. Wright CPM®

P R I N C I P A L S & A G E N T S

19

Member of InternationalCouncil of Shopping Centers

Commercial Real Estate Services, Worldwide.

107 South Howard Street, Spokane, WA 99201509.623.1000 • www.naiblack.com

Photograph by Alan Bisson Photography

Designed and produced by: Printed by: