navios maritime containers inc. · navios maritime containers inc. (1) based on total fleet...

TRANSCRIPT

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Navios Maritime Containers Inc.

Q4 2017 Earnings Presentation

January 29, 2018

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Forward Looking Statements

2

This presentation contains forward-looking statements concerning future events, including future contracted revenues and

rates, EBITDA, future available days, future financial performance of the fleet, timing of vessel deliveries, and Navios

Containers' growth strategy and measures to implement such strategy; including future vessel acquisitions and the ability to

secure or refinance related financing, the further growth of our containership fleet, and entering into further time charters.

Words such as “may,” “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such

words and similar expressions are intended to identify forward-looking statements. These forward-looking statements are

based on the information available to, and the expectations and assumptions deemed reasonable by Navios Containers at

the time these statements were made. Although Navios Containers believes that the expectations reflected in such forward-

looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct.

These statements involve known and unknown risks and are based upon a number of assumptions and estimates which are

inherently subject to significant uncertainties and contingencies, many of which are beyond the control of Navios Containers.

Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could

cause actual results to differ materially include, but are not limited to, risks relating to the future vessel acquisitions, the

quality of the fleet and the market for the fleet vessels, the uncertainty relating to global trade, including prices of seaborne

commodities and continuing issues related to seaborne volume and ton miles, our continued ability to enter into long-term

time charters, our ability to maximize the use of our vessels, expected demand in the container shipping sector in general,

fluctuations in charter rates for container carrier vessels, the aging of our fleet and resultant increases in operations costs,

the loss of any customer or charter or vessel, the financial condition of our customers, changes in the availability and costs

of funding due to conditions in the bank market, capital markets and other factors, increases in costs and expenses,

including but not limited to: crew wages, insurance, provisions, port expenses, lube oil, bunkers, repairs, maintenance, and

general and administrative expenses, the expected cost of, and our ability to comply with, governmental regulations and

maritime self-regulatory organization standards, as well as standard regulations imposed by our charterers applicable to our

business, general domestic and international political conditions, competitive factors in the market in which Navios

Containers operates, and risks associated with global operations. Navios Containers expressly disclaims any obligations or

undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any

change in Navios Containers' expectations with respect thereto or any change in events, conditions or circumstances on

which any statement is based. Navios Containers makes no prediction or statement about the performance of its common

stock.

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Global brand, industry relationships

and reputation

Economies of scale of ~ 200 vessel

fleet owned/managed

Ship management within the public

company – cost center vs profit

center

Track record of value creation

through the cycle

Access to deal flow

Professional management team

Alignment of interests

Fixed OpEx

NMCI Within the Navios Group

Why important for NMCI?

Scale, experience and relationships

3

Navios Maritime

Holdings Inc.

(NYSE: NM) 64 dry bulk vessels: 38 owned, 26 chartered-in

Navios Maritime

Containers Inc.

(N-OTC:NMCI)

21 containerships

Navios Maritime

Partners L.P.

(NYSE: NMM)

38 vessels: 13 Capes, 15

Panamaxes, 3 Ultra-Handymaxes, 7 containerships

Navios South American

Logistics Inc. Port Terminal facilities,

barging & cabotage Special Purpose Vehicles Navios

Europe I & II 24 vessels:

12 containerships, 5 Panamax, 2 Handymax,

5 Product Tankers

Navios Maritime

Midstream Partners L.P.

(NYSE: NAP)

6 VLCCs

Navios Maritime

Acquisition Corporation (NYSE: NNA)

36 vessels - 26 product

tankers, 8 VLCCs, 2 chemical tankers

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Ownership Structure

37.1% Interest 62.9% Interest

100% Interest

Navios Maritime

Containers Inc.

(OSLO N-OTC: NMCI)

Common Shareholders

Navios Group (33.7% NMM / 3.4% NM)

21 Containerships

4

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

NMCI: Company Highlights

5

Navios Group’s Containership Vehicle – Right of First Refusal for all Containerships

New Growth Vehicle

Focused on the

Containership Sector

New growth vehicle with attractive entry point and clean, low-cost structure

Attractive opportunities to buy containerships toward bottom of the cycle

Access to distressed deals from banks / operators - available only to select

managers

Leverage Existing

Operating Platform

Leverage an established large operating platform

Economies of scale = ~ 5% lower operating expenditures than the industry (1)

Charterers prefer to deal with large, safe and reliable owners

Well Positioned to

Grow in Container

Market Recovery

Sector poised for recovery: trade growth + high scrapping + lack of new orders

Focus on containerships with attractive deployment opportunities in higher

growth trades

Acquisitions provide free cash flow in current market with significant capital

appreciation and yield improvement as market recovers

Strong Sponsor with

Seasoned

Management

Strong & strategic relationships with banks and other key industry players

Management team has average industry experience of 20+ years per person

Demonstrated access of Navios Group to debt and equity capital markets

Long track record of financial reporting, compliance and investor accountability

(1) Drewry Shipping Consultants – Annual Report 2016/2017. Drewry only identifies opex and drydock amortizations, but does not include commercial

management or other costs. Based on the 2016 average for vessel operating costs for containership sizes between 3,000 and 6,000 TEU.

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Platform to Capitalize on Attractive Containership Opportunities

3 ships from Banks 14 ships from RMT

Note: Contracted EBITDA at the time of acquisition assumes $6,100 Opex for the vessels in the fleet

G&A assumed to be $685 per vessel per day. Based on 360 operating days and 365 cost days.

14 vessels / 57,100 TEU

11 x 4,250 TEU

3 x 3,450 TEU

Avg age: 10 years

Contracted EBITDA ~ $45m

Five vessels on TC with

staggered expirations ending

in Q1 2019

Price: $118.0m

3 vessels / 12,860 TEU

2 x 4,250 TEU

1 x 4,360 TEU

Avg age: 8 years

Price: $31.2m

Attractive Return Profile Through Scrap + Contracted EBITDA, with Significant Potential Upside

Vessels

in F

leet

Co

ntr

acte

d

Cash

Flo

w

4 ships from German Owner

4 vessels / 18,920 TEU

4 x 4,730 TEU

Avg age: 9.5 years

Contracted EBITDA ~ $70m

4 vessels on TC to

CMA/APL through Q2 2020

Price: $96.8m

6

NMCI continues to build critical mass

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Recent Developments

7

Navios Maritime Containers Inc.

Seven vessels purchased for a total of $128.0 million - All vessels delivered in Q4 2017

$96.8 million acquisition of four 4,730 TEU containerships - average age of 9.5 years

• All vessels chartered out at a net rate of $27,156 per day through Q2 2020

• $70.0 million expected contracted EBITDA ~ 72% of price

$19.75 million acquisition of two 2009-built 4,250 TEU containerships

$11.45 million acquisition of one 2010-built 4,360 TEU containership

$50.0 million equity issuance

Follow-on private placement November 2017 at $5.50 per share issuance price (10% increase compared

to the previous issuance)

$74.0 million debt financing

$50.0 million add-on loan, for acquisition of the four 4,730 TEU vessels

• Interest: L + 3.85%; $5.6 million quarterly amortization; maturing in November 2019

$24.0 million new loan for acquisition of up to four vessels

• $18.0 million already drawn for three vessels

• Interest: L + 3.00%; 7-year profile; maturing in December 2022

Extended maturity of existing $40.0 million and $21.0 million facilities to end of 2019

$121.0 million refinancing of existing $102.7 million facilities

Advanced discussions(1) for a new facility maturing 2023 to refinance existing facilities maturing in Q4

2019

Refinancing is expected to reduce debt service requirements for 2018 by 58%

(1) No assurances can be provided that the Company will successfully refinance these credit facilities

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

$5,069 $8,086

$20,202

2018 Breakeven per open day Current Rates 15 Year Average Rates

Expected Free Cash Flow Generation FY 2018

Cash Flow Analysis 2018E

($ Thousands) Current Rates 15 Year Average Rates

Contracted Revenues 87,344 87,344

Total Expenses (Opex, G&A and debt service) (103,523) (103,523)

Net cash from contracted revenue (16,179) (16,179)

Revenue from open days* 25,811 64,485

Free cash generation 9,632 48,306

Open Days 3,192 3,192

Breakeven per open day $5,069 $5,069

15-year average charter rates are expected to provide $48.3 million Free Cash Flow in 2018

8

Note: Current rate based on Clarksons Platou SIN December 2017 rates of $8,000 per day for 4,250 TEU vessels and $8,500 per day for 3,450 TEU vessels;

15 year average rates; 4,250 TEU $20,759; 3,450 TEU: $17,525 per day. Cash flow generation assumes normal operational performance of current fleet.

Rates shown in above tables are weighted to reflect vessel sizes for open days.

$9.6 million

$48.3 million

60%

150%

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

(1) Based on total fleet lightweight tons of 353,801 and an assumed scrap price @ $500 per lwt (2) Appraised value of 21 vessel fleet as of December 2017

Asset Coverage NMCI Debt

1.47x of facility covered by collateral vessel scrap value

2.8x coverage by collateral vessel value + contracted EBITDA

Strong Asset Coverage

$120.7 $176.9

$336.1

Total Debt Outstanding 12/31/2017 Scrap Value Market Value+ Contracted EBITDA

($ million)

1.47 x 2.8 x

(1) (2)

9

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

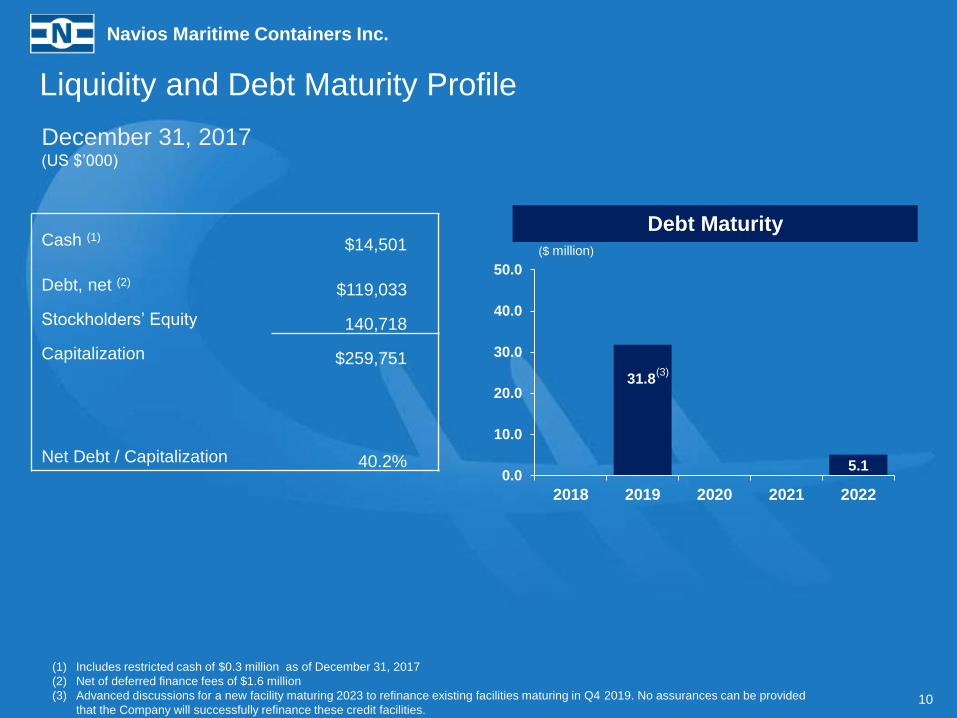

Liquidity and Debt Maturity Profile

December 31, 2017

(US $’000)

Cash (1) $14,501

Debt, net (2) $119,033

Stockholders’ Equity 140,718

Capitalization $259,751

Net Debt / Capitalization 40.2%

Debt Maturity

31.8

5.1 0.0

10.0

20.0

30.0

40.0

50.0

2018 2019 2020 2021 2022

($ million)

10

(1) Includes restricted cash of $0.3 million as of December 31, 2017

(2) Net of deferred finance fees of $1.6 million

(3) Advanced discussions for a new facility maturing 2023 to refinance existing facilities maturing in Q4 2019. No assurances can be provided

that the Company will successfully refinance these credit facilities.

(3)

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Summary of Containership Fleet

11

21 Vessels (89K TEU) Average age of combined fleet(1): 9.8 years

21 Container Vessels

4 Vessels

4,730 TEU

14 Vessels

4,250 TEU

3 Vessels

3,450 TEU

18,920 TEU 59,610 TEU 10,350 TEU

(1) Navios Containers average age based on a dwt basis

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

58.4%

Fixed days

Open days

Jan-18 Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19 Apr-19 Jun-19 Aug-19 Oct-19 Dec-19 Jan-20 Mar-20 May-20 Jul-20

APL Atlanta

APL Denver

APL L.A

APL Oakland

MOL Devotion

MOL Destiny

Navios Spring

Navios Indigo

MOL Delight

MOL Dedication

Navios Amaranth

Navios Lapis

Navios Verano

Navios Amarillo

Navios Felicitas

MOL Dominance

Navios Tempo

Navios Azure

Navios Summer

Navios Vermillion

Navios Verde

$26,850 April 2018

$26,850 July 2018

$26,850 September 2018

$26,850 November 2018

$26,850 February 2019

(1) Daily charter-out rate net of commissions, where applicable. See fleet appendix for further detail.

Fleet and Employment Summary

$8,010 March 2018

12

Charter Coverage FY2018

$7,093 July 2018

$8,006 February 2018

$8,133 October 2018

$8,037 February 2018

$9,144 May 2018

$8,444 November 2018

41.6%

$7,604 June 2018

$7,411 April 2018

$8,106 March 2018

$7,575 May 2018

$7,431 May 2018

$27,156 May 2020

$27,156 April 2020

$27,156 March 2020

$27,156 June 2020

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

13

NMCI Fleet Trading in the High Growth Trading Areas

Higher trade growth in Intra Asia and Africa N-S favoring NMCI Fleet

Trade Growth - NMCI Fleet Deployment (1)

Intra Asia

6.6%

(1) NMCI Fleet voyages for Nov 2017 – Jan 2018, trade growth estimate for 2018

Africa N-S

7.2%

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Navios Holdings generates economies of scale from a ~ 200 vessel diverse

fleet under management.

Economies of Scale

(1) Drewry Shipping Consultants – Annual Report 2016/2017. Drewry only identifies opex and drydock amortizations, but does not include commercial

management or other costs. Based on the 2016 average for vessel operating costs for containership sizes between 3,000 and 6,000 TEU. 14

Navios Holdings agreed to provide Navios Containers the following:

Commercial and Technical Management

10-year agreement

Opex - initial rates ~ 5% below the industry average (1)

• $6,100 per day for 4,250 TEU containerships, fixed for two years

• $6,100 per day for 3,450 TEU containerships, fixed for two years

Administrative Services

Reimbursement of allocated G&A costs

No other fees and expenses

NO additional technical or commercial management fees

NO commissions charged for commercial management

NO commissions or fees charged for any sale or purchase transaction

NO commissions or fees charged for originating any loan or other financing transactions

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

NMCI Q4 2017 Earnings Highlights

15

Earnings Highlights

Figures in $’000, except active vessels,

TCE and available days Three Months Ended

December 31, 2017

Period from April 28, 2017

(date of inception) to

December 31, 2017

Time charter revenue 21,329 39,188

EBITDA 9,917 18,709

Adjusted EBITDA (1) 9,917 19,156 (1)

Net Income 1,673 2,638

Adjusted Net Income (1) 1,673 3,085 (1)

EPS 0.07 0.14

Adjusted EPS (1) 0.07 0.17 (1)

Active Vessels at period end 21 21

Available Days 1,434 2,411

TCE $14,232 $15,730

(1) Adjusted EBITDA, Adjusted Net Income and Adjusted Earnings per Share for the period from April 28, 2017 (date of inception) to

December 31, 2017 exclude $0.4 million relating to the reactivation costs of four laid-up vessels.

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Balance Sheet

16

Selected Balance Sheet Data (in $’000)

December 31, 2017

Cash & cash equivalents (1) $14,501

Other current assets 6,870

Vessels, net 177,597

Total Assets $266,811

Other current liabilities $7,060

Current portion of long term debt, net 42,499

Long term debt, net of current portion and discount 76,534

Stockholders’ equity 140,718

Total Liabilities & Stockholders’ Equity $266,811

Net Debt / Book Capitalization 40.2%

(1) Includes restricted cash of $0.3 million as of December 31, 2017

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Industry Overview

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

5.3%

2.2%

4.1%

5.0% 5.0%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

120

140

160

180

200

220

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7 (

e)

201

8 (

f)

growth m TEU

Source : Clarkson Research Services, IMF Oct 2017

Trade Growth % World GDP Growth % (RHS)

1996 – 2017 CAGR = 6.9%

World Container Trade 1996-2018

World trade growth

2015 2.2%

2016 4.1%

2017 e 5.0%

2018 F 5.0%

18

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

904

1,147

1,686 1,667

1,070

538

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

As of Jan 1, 2017 As of Jan 1, 2018

Orderbook by year of delivery: Actual # vessels delivered: 2014 = 205; 2015 = 213; 2016 = 131; 2017 = 148

‘000 TEU

2016 2017 2018 2017 2018 2019

Before non-delivery

Before non-delivery

Actual non-

delivery

538,000

TEU

Actual

non-

delivery

437,000

TEU

Deliveries

2017 1.15 million TEU delivered; 1.69 million projected (32% non deliveries by TEU); 148 vessels delivered

2016 0.90 million TEU delivered; 1.34 million projected (33% non deliveries by TEU); 131 vessels delivered

2015 1.68 million TEU delivered; 1.89 million projected (11% non deliveries by TEU); 213 vessels delivered

2014 1.49 million TEU delivered; 1.62 million projected ( 8% non deliveries by TEU); 205 vessels delivered

2013 1.35 million TEU delivered; 1.84 million projected (27% non deliveries by TEU); 206 vessels delivered

2012 1.26 million TEU delivered; 1.58 million projected (20% non-deliveries by TEU); 212 vessels delivered

2011 1.21 million TEU delivered; 1.65 million projected (27% non-deliveries by TEU); 193 vessels delivered

2010 1.39 million TEU delivered; 2.24 million projected (38% non-deliveries by TEU); 267 vessels delivered

2018 orderbook = 1.7 million TEU

(before non deliveries)

2018 estimated deliveries:

1.2 million TEU assuming 30%

non delivery rate

0.4 million TEU estimated 2018

scrapping

Expected 2018 Net fleet

growth ~ 3.7%

Containership Sector Orderbook

Source: Clarksons 19

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

1.1%

3.6%

9.7%

0.0%

5.0%

10.0%

15.0%

20.0%

Fleet Age Profile (% TEU)

25+ yrs 20-24 yrs 15-19 yrs

Source: Clarksons; Unless noted, all data in TEU; YTD through 12/31/17

Containership Net Fleet, Age Profile + Historical Scrapping

Demolition

Year Total Demolition (‘000 TEU) % of Fleet 2000 15.5 0.35%

2001 36.2 0.73%

2002 68.1 1.23%

2003 25.7 0.42%

2004 8.0 0.12%

2005 2.3 0.03%

2006 23.8 0.29%

2007 20.9 0.22%

2008 101.2 0.93%

2009 378.4 3.07%

2010 132.6 1.02%

2011 77.9 0.55%

2012 334.7 2.17%

2013 444.2 2.72%

2014 372.6 2.16%

2015 193.3 1.05%

2016 654.4 3.30%

2017 397.9 1.98%

Deliveries Scrapping Net Fleet Growth

Year Actual Projected % Non-

Delivery Year TEU

% of

Fleet Year TEU % of Fleet

Fleet Period

End

2017 1,147 K 1,686 K 32% 2017 398 K 2.0% 2017(1) 747 K 3.7% 20,808 K

2016 906 K 1,341 K 32% 2016 654 K 3.3% 2016 246 K 1.2% 20,061 K

2015 1,658 K 1,889 K 12% 2015 193 K 1.1% 2015 1,460 K 8.0% 19,815 K

2014 1,513 K 1,624 K 7% 2014 373 K 2.2% 2014 1,138 K 6.6% 18,355 K

2013 1,346 K 1,840 K 27% 2013 444 K 2.7% 2013 888 K 5.4% 17,216 K

2012 1,263 K 1,578 K 20% 2012 335 K 2.2% 2012 914 K 5.9% 16,328 K

2011 1,224 K 1,652 K 26% 2011 78 K 0.5% 2011 1,129 K 7.9% 15,414 K

2010 1,381 K 2,242 K 38% 2010 133 K 1.0% 2010 1,232 K 9.4% 14,284 K

0.40 M = 141 Vessels Scrapped in 2017

2017 Net Fleet Growth 0.75 M =

1.15 M Delivered – 0.40 M Scrapped

Total Containership Fleet: 5,164

2018 Deliveries: 12 ships, 119K TEU to 1/18/18

3.00 M TEU

20 (1) Net Fleet Growth YTD reflects deliveries and scrapping through 12/31/17

For the whole fleet that is: 1.15M TEU delivered – 0.40M TEU scrapped

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Improving Fundamentals 2,000-5,100 TEU Sizes

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

22

Deployment 4,000 – 5,100 TEU Containerships: Depends on Specifications

Pre Panama Canal expansion, main trading route was Far East – US (through old Panama Canal locks)

Post Canal expansion, deployment in Far East – US East Coast declined by 81%: vessels redeployed to

different trades after being replaced by wider and larger vessels

Redeployment limited due to port restrictions in high growth trading areas (Africa and Intra Asia)

~260/270 LOA, Draft 12.5 m, Beam 32m

~290 LOA, Draft 13.5m, Max Beam 32m

Not all Panamaxes Are the Same

Shorter vessels with shallower draft found new

deployment in Africa and Intra Asia where limitations

in port infrastructure eliminate larger and deeper

vessels

Less deployment options for longer and deeper draft

vessels led to increased scrapping and idle capacity

Baby Panamax

Panamax Max

88% of the 4-5,100 TEU vessels scrapped

since 2015 were Panamax Maxes

(94 out of 107 ships) 13

94

0

20

40

60

80

100

Baby panamax Panamax Max

54,465 TEU

430,895 TEU

# of vessels

Vessels Scrapped

Source: Clarksons

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

20

30

40

50

60

70

80

90

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

3.6-3.8K TEU NB, nominal Avg 1996-2017, nominal

3.6-3.8K, infl adj Avg 1996-2017, infl adj

$ M

illi

on

s

0

5

10

15

20

25

30

35

NB 5 10 15 20 25

Scrap value NB parity 3.6-3.8K TEU Discount to NB parity

57%

59%

61%

$ M

illi

on

s

Discount to Newbuild Price Parity

23

Historical NB Price ($mm) Discount to NB Parity

Significant discount to NB parity, even with today`s NB prices around historically low levels

Source: Clarksons Platou Securities AS, Shipping Intelligence Network

Scrap value

Avg. ~$55.6m

Avg. ~$44.4m

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

6%

16%

10%

0% 1% 0%

19%

44%

13%

0%

10%

20%

30%

40%

50%

3% 3%

6%

5%

3%

2% 2%

7%

6%

8%

5%

3%

0%

2%

4%

6%

8%

10% 2017 2016

Strong Value Potential in Sub-Panamax Segment Orderbook-to-Fleet Ratio by Segment Scrapping in % of Fleet by Segment

Baby Panamaxes are versatile and found in numerous main trades

No orderbook

for 4,000-5,099

TEU segment

Source: Clarksons Platou Securities AS, Shipping Intelligence Network, Clarksons Research Services, Alphaliner

New Panama Canal in 2016 led to:

• Wide beam Panamax replacing Old Panamax vessels

• High scrapping incentivized by low TC-rates and high costs due to new

IMO regulations

• Cascading effect from larger modern tonnage, all the way down to

Panamax segment

• Baby Panamaxes have migrated to other trade routes

Domino Effect Through Cascading A Panamax is Not a Panamax Old Panamax vessels:

• Baby Panamax (LOA 260/270, Draft 12.5m, Beam 32m)

• Versatile ships found in numerous trade routes

• Panamax Max (LOA 290, Draft 13.5m, Beam 32m)

• Overpowered and single purpose built

Neo Panamax (wide beam) vessels:

• New Panamax (LOA 360, Draft 15m, Beam 49m)

24

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

2,000 to 5,100 TEU Trade: Intra-Asia Outpaces World

2-5,100 TEU Intra-Asia Deployment

Source: Clarksons Research

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

10

20

30

40

50

60

70

2013 2014 2015 2016 2017e 2018f

Intra-Asia (M TEU LHS) Intra-Asia (% growth RHS)

Global Trade (% growth RHS)

Intra-Asia Trade Growth 2013 to 2018

Intra-Asia trade lane has been one of the fastest growing, outpacing world container trade growth

every year since 2013

Currently accounts for 29% of total container trade

2,000 to 5,100 TEU vessels saw an increase of 89% since 2013 in deployment on the Intra-Asia

trade lane

168

317

0

50

100

150

200

250

300

350

Jan 2013 Jan 2018

# of vessels

89%

25

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Growing cargo volumes and capacity expansions boosts demand for 4,000 – 5,100 TEU vessels

Line operators in order to increase market share are starting new strings to service their customers

Line operators new services creates demand for additional ~40 vessels

New Services Boost Demand for 4,000 - 5,100 TEU Vessels

Partners Trade Starting date North Europe East Med Cosco, Evergreen, Yang Ming

China Indonesia Cosco

Korea, China South East Asia Cheng Lie, APL

Nov 2017

Dec 2017

China LatAm PIL

Nov 2017

Jan 2018

~40

Vessels China West India WHL, Cosco Jan 2018

China East India WHL, Cosco, IAL, OOCL, SeaCon Jan 2018

China Pakistan APL, OOCL Dec 2017

North Europe USEC Cosco, CMA CGM, Evergreen, OOCL Apr 2018

Source: Alphaliner 26

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

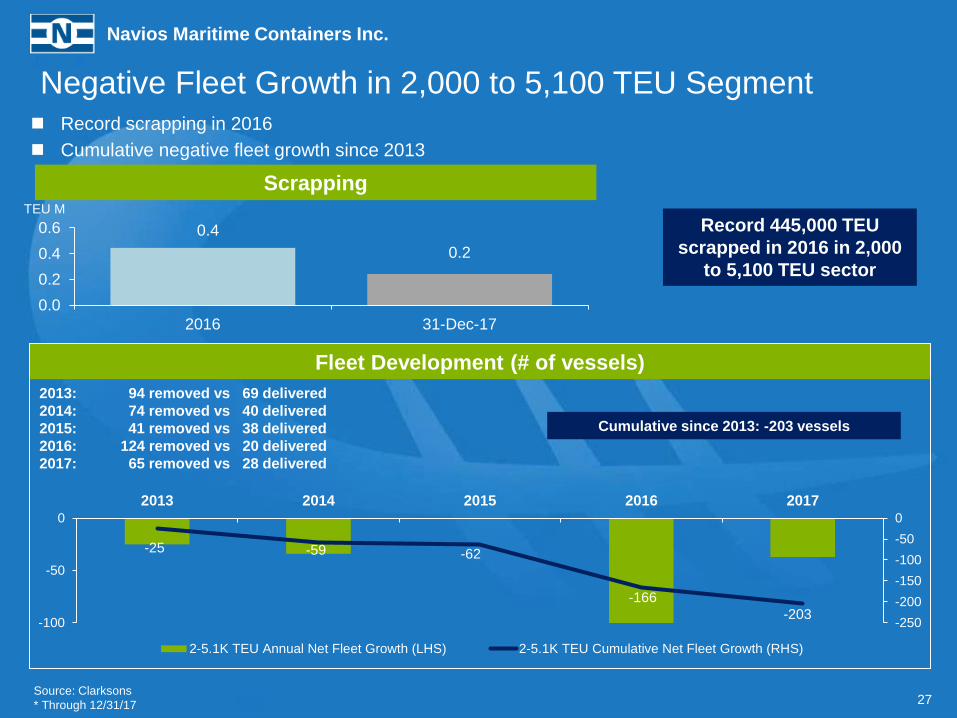

Fleet Development (# of vessels)

2013: 94 removed vs 69 delivered

2014: 74 removed vs 40 delivered

2015: 41 removed vs 38 delivered

2016: 124 removed vs 20 delivered

2017: 65 removed vs 28 delivered

Source: Clarksons

* Through 12/31/17

Negative Fleet Growth in 2,000 to 5,100 TEU Segment

Record 445,000 TEU

scrapped in 2016 in 2,000

to 5,100 TEU sector

27

Record scrapping in 2016

Cumulative negative fleet growth since 2013

0.4

0.2

0.0

0.2

0.4

0.6

2016 31-Dec-17

-25 -59 -62

-166

-203 -250

-200

-150

-100

-50

0

-100

-50

0

2013 2014 2015 2016 2017

2-5.1K TEU Annual Net Fleet Growth (LHS) 2-5.1K TEU Cumulative Net Fleet Growth (RHS)

Cumulative since 2013: -203 vessels

Scrapping TEU M

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

-

100,000

200,000

300,000

400,000

500,000

600,000

Jan 2017 Jan 2018

28

Improving Fundamentals for 2,000 to 5,100 TEU Fleet

Idle Capacity Fleet Deployment Fleet Size

95%

4,200

4,600

5,000

5,400

Jan 2017 Oct 2017 4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

5,800

Jan 2017 Jan 2018

3.1%

6.6%

Negative fleet growth YTD 2017 for 2,000 to 5,100 TEU Segment

‒ Fleet decreased 11.4% since 2013

Increase in Intra-Asia trade lifts deployment

‒ Overall deployment increased by 6.6% since January 2017

Idle capacity decreased by 95% since January 2017

Source: Clarksons

TEU ‘000 TEU ‘000 TEU

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Appendix

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

Navios Containers Fleet

30 (1) Daily charter-out rate net of commissions, where applicable.

Owned Vessels

Vessel Name TEU Built Expiration Date Charter Rate (1)

Navios Verano 3,450 2006 May-2018 $9,144

Navios Summer 3,450 2006 Mar-2018 $8,010

Navios Spring 3,450 2007 Nov-2018 $8,444

Navios Vermillion 4,250 2007 Feb-2018 $8,037

Navios Indigo 4,250 2007 Oct-2018 $8,133

Navios Amaranth 4,250 2007 Jul-2018 $7,093

Navios Amarillo 4,250 2007 May-2018 $7,575

Navios Verde 4,250 2007 Feb-2018 $8,006

Navios Azure 4,250 2007 Mar-2018 $8,106

MOL Dominance 4,250 2008 Apr-2018 $26,850

MOL Dedication 4,250 2008 Jul-2018 $26,850

MOL Delight 4,250 2008 Sep-2018 $26,850

MOL Destiny 4,250 2009 Nov-2018 $26,850

MOL Devotion 4,250 2009 Feb-2019 $26,850

Navios Lapis 4,250 2009 Jun-2018 $7,604

Navios Tempo 4,250 2009 Apr-2018 $7,411

Navios Felicitas 4,360 2010 May-2018 $7,431

APL Oakland 4,730 2008 Mar-2020 $27,156

APL Los Angeles 4,730 2008 Apr-2020 $27,156

APL Denver 4,730 2008 May-2020 $27,156

APL Atlanta 4,730 2008 June-2020 $27,156

Total – 21 vessels 88,880

Color

Scheme

255,255,255

51,51,153

221,242,250

0,153,153

128,128,128

153,204,0

255,255,255

0,0,0

Navios Maritime Containers Inc.

www.navios-containers.com