needs and challenges in the zambian (small scale) …

TRANSCRIPT

NEEDS AND CHALLENGES IN THE ZAMBIAN (SMALL SCALE) MINING SECTOR

Contents

Executive Summary � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 3

1� Overview of the sector � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 51.1. Brief history and current state of play in the sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.2. Mining value chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2�Methodology � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �8

3� Challenges in the mining sector � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 103.1. The dominance of foreign owned businesses in supply chains . . . . . . . . . . . . . . . 10

3.2. Challenges with financial capacity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

3.3. Quality and efficiency challenges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

3.4. Regulatory challenges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.5. Discriminatory practices and transparency gaps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3.6. Needs for digital tools and equipment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.7. Challenges in skills development and education . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

3.8. Environmental challenges and circular models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

3.9. Social challenges: safety and community relations . . . . . . . . . . . . . . . . . . . . . . . . . . .24

4� Opportunities and recommendations � � � � � � � � � � � � � � � � � � � � � � � � � � � �264.1. Product and service lines with opportunities for local suppliers . . . . . . . . . . . . . .26

4.2. Demand for affordable, modern tools and equipment . . . . . . . . . . . . . . . . . . . . . . .28

4.3. Circular business opportunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

4.4. Development of technical skills, business skills, and expertise

in modern equipment and digitalisation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

4.5. Needs and benefits of quality assurance and certifications . . . . . . . . . . . . . . . . . . .30

4.6. Networking and supply chain development to support

procurement processes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

4.7. Local content regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

4.8. Financing instruments and payment terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

4.9. Solutions for sustainable and inclusive business. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Executive Summary

Background and methodology

The Accelerated Growth for MSMEs in Zambia (AGS) Programme was commissioned to undertake a study on the needs and challenges within the mining industry in Zambia, as a starting point for the SDG Booster Zambia 2021. The objective was to identify some of the most pressing challenges experienced in the sector, covering but not limited to digitalisation, circular economy, education and training, and environmental sustainability. As the scope is rather broad, the study serves as a general overview rather than a deep dive into specific challenges.

In March 2021, sixteen interviews were conducted among businesses and stakeholders operating the mining value chain in the Copperbelt and North Western Provinces of Zambia. The interviews covered a variety of local suppliers, contractors, and service providers, a few of the largest mining companies in the country, one final product manufacturer, one university, and one local Chamber of Commerce. To complement the interviews, some secondary data has been sourced from relevant literature.

Chapter 1 provides a brief history and current state of the mining sector and chapter 2 states the methodology of the study. Chapter 3 outlines the findings and explains the primary needs and challenges in the sector. Although the focus of the study is on identifying challenges, chapter 4 discusses some ways that these can be turned into opportunities and recommendations.

Findings, challenges, and opportunities

Zambia’s rich mining history spans over 90 years, playing a key role in the country’s social and economic development. Zambia is the second largest producer of copper in Africa and the seventh in the world. The sector represents over three quarters the country’s total export value.

Local suppliers currently participate in a relatively small fraction of the USD 2.38 billion that mines spend on goods and services annually. Although over 80% of this is said to be sourced locally, only 10.6% of total procurement value can be classified as ‘true local procurement’, i.e. locally manufactured goods, and services provided by resident firms.

Strategic partnerships between Zambian and international actors could support the development of more inclusive supply chains benefitting the local economy.

There is movement towards development of a standalone Local Content Act – a statutory instrument compelling mining companies to prioritise local sourcing of goods and services. First full drafts and more research on targeted product and service categories are expected later in 2021. Improved local content regulation could present significant opportunities for Zambian suppliers and their international partners to tap into new markets.

Digitalisation is one of the key priorities to increase efficiency, productivity, and sustainability of mining. There are opportunities in automation of drilling, digging, blasting, and loading processes, and modernising machinery in local manufacturing workshops. Smaller local suppliers would benefit from basic digital tools such as Enterprise Resource Planning (ERP) software, and an improved digital presence to better market their services. The need for modern equipment goes hand-in-hand with a need to upgrade digital skills of

only

of total goods and services can be classified as ‘true local procurement’.

10�6%

workforce in the industry. There are a variety of opportunities in environmental management and circular models that can be pursued in the sector. Water treatment processes, waste disposal, and rehabilitation of mining areas are some of the highlighted challenge areas. The industry produces valuable waste streams that could be recycled and reused more effectively, such as truck tyres and plastic waste.

Gaps in working capital is one of the challenges faced by local suppliers. Joint financing solutions would enable Zambian-international partnerships to handle larger contract volumes together. Quality control is another identified challenge area. Local suppliers tend to lose bidding processes due to perceived – and sometimes real – quality deficiencies, lack of warranty offers, and sometimes poor pricing strategies. A modern workforce driven by advanced technologies will require an improved set of skills, including technical problem-solving skills (e.g. welding, boiler making, foundry skills, diagnosing breakdowns) and business skills (e.g. pricing of proposals). Needs exist in vocational skills training, management skill development, and university-industry collaboration. Local universities can be engaged by setting up on-campus showrooms, allowing students to learn

using modern technology. The Copperbelt University (CBU) is eager to engage in more research and development projects to support the mining industry. The need for training in quality assurance and quality certification of products is recommended for further investigation.

There is an array of opportunities for out-of-the-box thinking entrepreneurs in non-mining related products and services. Mines and the communities built around them consume large volumes of fast-moving consumables and specialized products and services. Expanding to non-mining activities would support surrounding communities with sustained livelihoods beyond the life of the mine.

In chapter 4, the study has outlined some of the products and services with potential for local manufacturing and supply. In addition, possible models are discussed to tap into opportunities relating to technology transfer and R&D for products and services on demand, circular economy as well as capacity development needs on use of modern equipment and quality processes. Networking and supply chain development are recommended to support local companies to be more successful in procurement processes. Collaboration to improve sustainability and inclusivity of business practices is further recommended.

Needs and challenges in the Zambian (small scale) mining sector 5

Mining has been the main economic stay of Zambia from as early as 1920’s, and predominantly private sector led. There was significant investment in the industry which included mine development and operation, processing facilities and infrastructure and included the building of new towns around the mines.

Between 1973-1990, the state gained ownership of much of the modern sector of the economy. The mining sector was among the sectors that the government took ownership of. The government decided to nationalise the copper industry, and this led to the formation of the Zambia Consolidated Copper Mines (ZCCM). They did so with the view to maximising returns to the Zambian people. The benefits were used to invest in the construction of new schools, hospitals, and roads.

In the early 1990s, a new government was ushered in on the promise of good governance and economic liberalisation. Due to pressure from donor countries, the World Bank and IMF, the government embarked on very extensive macroeconomic reforms and undertook a market liberalisation programme. As part of its economic recovery programme, the government privatised the state owned ZCCM. Due to the liberal market approach, companies such as Anglo-American and Binani (i.e. new mining investors who bought Nchanga, Konkola and Nkana Divisions; and Luanshya division respectively) were able to pull out completely in the early stages of privatisation without suffering any significant regulatory penalties. In addition, there were not many individual Zambians, or Zambian companies, with the resources to purchase a privatised mining company. Government, at the inception of the privatisation exercise, had this in mind when it established ZCCM Investment Holdings (ZCCM-IH) as an equity holding company on behalf of the government and people of Zambia. Since then, the government has re-acquired a percentage of shareholding in each mine until in recent times when they took over the ownership of Konkola Copper Mines (KCM) and Mopani Copper Mines (MCM).

Benefits of privatisation that were experienced by Zambian economic actors include an increase in tax revenue by the mining firms. The new investment also meant that the mining industry was revitalised and there was focus on mines to buy more goods locally from services providers, contractors, and suppliers. The introduction of new technologies also meant that the cost of production was lowered significantly. Local companies were able to

1� Overview of the sector

1�1� Brief history and current state of play in the sector

By the time Zambia was attaining independence from Britain in 1964, it was a major copper producer in the world accounting for 12% of global output.1 By 1969, Zambia was classified a middle-income country with one of the highest GDPs in Africa.2

Needs and challenges in the Zambian (small scale) mining sector6

1�2� Mining value chain

make linkages to manufacturing industries all set up to support mining services in processing, instrumentation, electrical and mechanical engineering as well as supply services.

According to the Chamber of Mines, Mining for Zambia Tax Report (2019) for the 2018/2019 period, the combination of royalty and profit-based tax results in regular flow of tax revenue for the government over the life of the mine. The report further states that the mineral royalty tax is a cost to the mine, this

should be deductible against profit tax – as is the globally recognised best practice. Zambia has experienced challenges with the adoption of the new tax regime by the government, with the sector lobbying for clarity around the ability to deduct mineral royalties against profit tax. The current state of affairs is that government is willing to dialogue and strike a balance by putting in place stable, predictable, consistent, and transparent tax regimes, which has been widely hailed as a positive move.

The objective of mining companies is to make profit by employing the different processes of extraction, processing and selling minerals from their mines. Given the time and capital constraints, mines have to optimize the process of mineral extraction, though it is also worth noting the uncertainty associated due to variable technical and human factors. Mining companies that manage their value chain end up establishing a competitive advantage and increased value creation. Mining value chains continue to evolve as commodity markets change, and new opportunities are arising due to increased environmental protections and new regulatory policies.

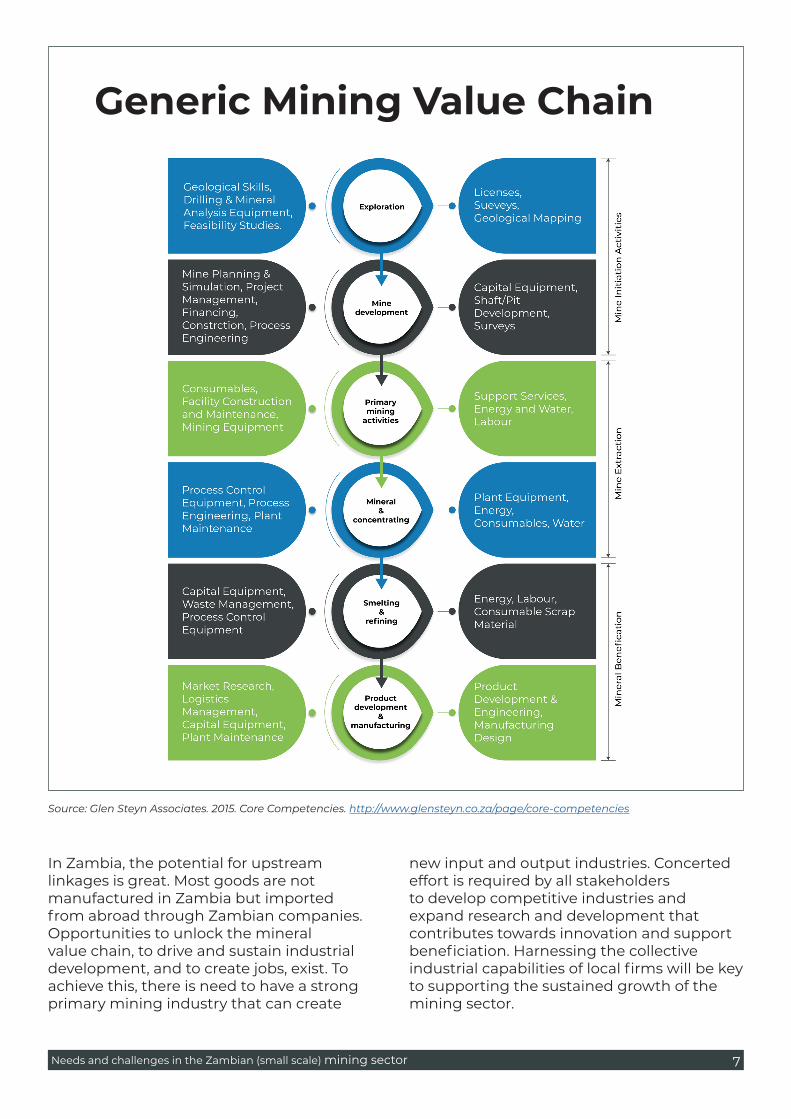

The figure below shows an overview of a typical mining value chain, from exploration activities to product development and manufacturing. The different processes are all dependent on each other. Each link must be complete for the units to function and to serve other units upstream or downstream. In this study, suppliers, contractors, and service providers providing goods and services to various parts of the value chain were identified and interviewed. The study aimed to cover the views, needs and challenges of businesses operating as many parts of the chain as possible.

Needs and challenges in the Zambian (small scale) mining sector 7

In Zambia, the potential for upstream linkages is great. Most goods are not manufactured in Zambia but imported from abroad through Zambian companies. Opportunities to unlock the mineral value chain, to drive and sustain industrial development, and to create jobs, exist. To achieve this, there is need to have a strong primary mining industry that can create

new input and output industries. Concerted effort is required by all stakeholders to develop competitive industries and expand research and development that contributes towards innovation and support beneficiation. Harnessing the collective industrial capabilities of local firms will be key to supporting the sustained growth of the mining sector.

Source: Glen Steyn Associates. 2015. Core Competencies. http://www.glensteyn.co.za/page/core-competencies

Generic Mining Value Chain

Needs and challenges in the Zambian (small scale) mining sector8

2� Methodology

This study has been conducted to provide a starting point for the SDG Booster series of workshops focusing on the Zambian mining sector. The purpose of this report is to serve as background for discussions between Zambian and Finnish businesses, NGOs, and academia during the workshops. It outlines some of the challenges and needs experienced by businesses in the mining value chain in Zambia.

The study draws primarily on field interviews with local suppliers, contractors, and service providers to the mining sector, as well as large mining companies. A total of 16 semi-structured interviews were conducted in early March 2021 in the Copperbelt and North Western Provinces of Zambia. It is important to note that the results are based on interviewees’ personal experiences and views as professionals in the sector. Secondary data has been sourced from relevant literature.

A set of interview questions was developed and used to cover some pre-determined focus areas: � General needs and challenges (allowing

the respondent to freely express the most pressing challenges without

guiding questions) � Relationship between large mining

companies and local suppliers � Digitalisation � Recycling and circular business models � Environmental sustainability � Education and training � Health and safety.

As the scope is rather broad, the study serves as a general overview rather than a deep dive into specific challenges. The SDG Booster welcomes a large variety of businesses connected to the mining sector as participants to the workshops. In line with this approach, this study is not limited to certain product lines, services, or parts of the value chain. To obtain more detailed results on challenges and opportunities in the sector, the study team recommends conducting further, product or service specific market studies.

Another limitation is the variety of interviewed stakeholders. To expand the study further, it would be recommended to interview Ministry representatives and other past and present initiatives supporting the mining sector in Zambia.

The study was carried out by the Accelerated Growth for MSMEs in Zambia (AGS) Programme in March-April 2021.

AGS is a private sector development programme funded by the Ministry for Foreign Affairs of Finland and implemented with the Ministry of Commerce Trade and Industry of Zambia.

The Programme intends to accelerate the growth of Zambian start-ups and micro, small, and medium sized enterprises, as contributors to well-being and inclusive job growth in the Zambian economy. AGS also supports business partnerships between Zambia and Finland. Mining services is one of AGS’ focus sectors.

Needs and challenges in the Zambian (small scale) mining sector 9

Type of business / actor Description Position in value chain

Suppliers*

Foundry Supplies castings in various metals, mostly as spare parts to the mines and other industries. Has a circular business model using scrap metal from the mining industry as the primary raw material.

Product development and manufacturing

Power solutions provider Provides power solutions including transformers, mini-substations, motors and engineering services to mining and other industries.

Adds value throughout the value chain, particularly in milling and smelting processes.

Rigging service provider Provides rigging services, including equipment and labour, for mining companies.

Mineral extraction

Engineering and manufacturing supplier Does structural steel fabrication and installation, machining, and manufacturing of mining accessories, building and civil works, and more.

Mainly operates in mine development and primary mining activities stages, and any stage that includes construction.

Environmental consultancy Environmental and geospatial consultancy to mines (and other sectors) including Environmental Impact Assessments (EIA), baseline monitoring (e.g. air quality assessments), socio-economic assessments, geospatial mapping, monitoring emissions and helping clients reach requirements.

Operates in various parts of the value chain, particularly mine initiation (EIA).

Security service provider Provides guards and other security services to large mining companies (one in particular)

Throughout the value chain.

Multi-purpose service provider, incl. waste management

Service provider with many specialty areas, including recycling, accommodation, health services, and pest control.

Throughout the value chain.

The below table outlines the type of businesses and actors that were interviewed.

Large mining companies (mostly copper)**

Large mining company 1: Engineering department

One of the largest mines in Zambia. Throughout the value chain.

Large mining company 2: CSR department One of the largest mines in Zambia, foreign owned. Mine operations cover all of the value chain. CSR work focuses on on-mining activities.

Large mining company 2: Senior manage-ment

One of the largest mines in Zambia, foreign owned. Throughout the value chain.

Large mining company 3: CSR department One of the largest mines in Zambia, foreign owned. Mine operations cover all of the value chain. CSR work focuses on on-mining activities.

Large mining company 3:Environmental department

One of the largest mines in Zambia, foreign owned. Throughout the value chain.

Product developers and manufacturers

Manufacturer of copper wire and cable Sources copper from Zambian mines, manufactures semi-finished products mostly for export markets.

Product development and manufacturing (end of value chain)

Expert organisations

Local university (School of Mines and Centre of Excellence)

One of the primary universities in the field of mining in Zambia. No particular focus in the value chain.

Local Chamber of Commerce Advocates, lobbies, builds linkages, and facilitates networking to support its members, 90% of which are in the mining industry, primarily in supply.

No particular focus in the value chain.

*In this study, we use the term “suppliers” to cover suppliers, contractors, and service providers to the mines. Businesses supplying goods, services, and labour are all coined under this term.

**In this study, we use the term ‘large mining company’ and ‘mine’ interchangeably.

‘Mines’ in this context refer only to large scale mines, as no small mining operations were interviewed (expect for one silica sand mine supplying silica sand to larger mines. This business is categorised as a supplier).

Needs and challenges in the Zambian (small scale) mining sector10

3� Challenges in the mining sector

3�1� The dominance of foreign owned businesses in supply chains

The interviews revealed an array of challenges in the Zambian mining sector. The findings were largely in line with other recent studies, notably the African Development Bank’s Analysis of input goods and services in Zambia’s mining industry, (2019). The difficulty of competing against international businesses is the single largest, overarching challenge experienced by Zambian suppliers and contractors in the mining sector. Challenges in financial capacity, quality of products, and efficiency

of operations contribute to this. Large mining companies are blamed for giving preference to international competitors, and there are gaps in the enforcement of regulations supporting local content. This chapter outlines some of these and other challenges, including specific needs for modern technologies and the primary skill gaps in the industry. Challenges relating to the protection of environmental and social sustainability are also discussed based on interview findings.

3�1�1� Procurement volumes from foreign and local suppliers

The total value of goods and services consumed by mines in Zambia was estimated to be over 2.38 billion USD in 2017. Although over 80% of this is said to be sourced locally, only 10.6% of total goods and services can be classified as ‘true local procurement’. The overwhelming volumes

of ‘locally procured’ goods and services are typically imported into the country by foreign owned firms with local presence. ‘True local procurement’ is defined as locally manufactured goods, irrespective of firm ownership, and services provided by resident firms, excluding multinational companies. Procurement from Zambian owned businesses only accounts for 2.5% of total procurement.3

2�5%Only of total

procurement is sourced from Zambian owned companies (with >50% Zambian shareholding).

Needs and challenges in the Zambian (small scale) mining sector 11

Category As % of TotalPurchases

As % ofLocal Purchases

As % of True LocalPurchases

% of Total Purchases from Zambia Firms

CORE MINING INPUTS AND CONSUMABLES

Rubber Products 0.1 0.1 0.8 0.0

Metallic 1.0 1.2 9.2 0.1

Electrical Components 0.5 0.6 4.4 0.0

Assembled Components 0.2 0.2 1.5 0.2

Chemicals and Reagents 0.6 0.7 5.7 0.0

Explosives 3.0 3.5 28.1 0.0

Others 1.3 1.5 11.9 0.0

CORE MINING 2.1 2.5 19.9 0.7

NON-CORE GOODS 0.5 0.5 4.3 0.5

NON-CORE SERVICES 1.5 1.8 14.2 0.9

TOTAL TRUE LOCAL PURCHASES 10�6 12�6 100�0 2�5

Table 1: Proportions of True Local Procurement of goods and services. Source: African Development Bank, 2019

The distribution of total consumption by mines is as follows:

53% Core mining goods and consumables:

Equipment, spares and consumables that are critical to production operations, including: � rubber products (tyres, conveyor belts,

rubber moulded products, etc); � metallic components comprising

fabricated products (tanks, chutes, thickeners, process piping, etc) and cast products (impellers, mill liners, crusher parts, etc);

� electrical components (motors, wires, transformers, etc);

� assembled products (pumps, drives and gear boxes, rock drills, off-highway trucks, etc);

� chemicals and reagents (collectors, frothers, flocculants, etc); and

� explosives.

40% Core mining services:

Services that are critical to production operations (e.g. drilling, mine development, shaft sinking, etc).

6%

1%

Non-coreservices:

Non-coregoods:

Services that are not essential to production (e.g. catering, gardening, security, transportation, etc).

Goods not essential to production (e.g, uniforms, food, medicines, stationary, etc).1

Needs and challenges in the Zambian (small scale) mining sector12

Core goods and consumables

Core services

Non-core goods

Non-core services

53%40%

6%1%

Figure 1: Distribution of goods and services in total mining procurement. Source: African Development Bank, 2019

As shown in the table above, nearly a third (28%) of true local procurement comes from explosives. After explosives, the largest categories for ‘true local suppliers’ are core mining services and non-core services – the latter consisting largely of transportation. Despite local facilities and capacity to manufacture e.g. metallic products (such as crusher plate wears, cables, switch gear or transformers) or explosives, the vast majority of products are still imported into the country.1

As the localisation of supply chains is discussed in this study, our primary focus is on ‘true local suppliers’, i.e. those manufacturing products locally, providing services locally (involving local labour), and/or businesses with majority (50% or more) local ownership. The AGS Programme and SDG Booster focus on businesses that add value and create jobs in the Zambian economy. From here onwards, the term ‘local suppliers’ is used to refer to ‘true local suppliers’.

3�1�2� Reasons behind poor local representation in supply chains

Representatives of both local suppliers (of goods, services, and labour), and large

mining companies were interviewed for this study. The gap between the two sides of procurement became apparent, and reasons provided to explain the situation differed significantly between the two. Based on the interviews, key factors affecting the situation include the following:

Most equipment needed in mining is not available locally.

This is the obvious reason for the huge percentage of procurement from non-local sources. The large (often internationally owned) mines operate with state-of-the-art machinery, sourced from international Original Equipment Manufacturers (OEMs) or their local or regional representatives. These constitute the largest values in procurement. OEMs tend to lock in their customers by packaging spare parts, maintenance services and even training in their deals. This leaves Zambian manufacturers and suppliers the chance to contribute mainly by providing small components and spares, chemicals, non-core products, and services – all of which are small in value compared to the large machinery procurements.

Needs and challenges in the Zambian (small scale) mining sector 13

Local suppliers’ weak financial muscle affects their ability to deliver, particularly for larger contracts.

Limited working capital and inability to keep stock affect their performance and attractiveness as suppliers negatively. This issue is discussed in more detail in Chapter 3.2. Financial Challenges.

Uncompetitive pricing of local offers. On average, local suppliers are significantly more expensive than foreign ones.

This is likely to be due to high costs of inputs and intermediaries, relatively high costs of doing business in Zambia, and partly due to poor pricing strategies. This is also discussed in Chapter 3.2.

Inadequate quality of goods and services is one of the primary excuses given by large mining companies. Some

suppliers admit having quality challenges

and, unsuccessfully, look towards the mines for support in reaching the desired quality. Warranty is another important reason for mines to source from OEMs. Quality and efficiency challenges are discussed in chapter 3.3.

Discrimination and lack of transparency in procurement. Poor information flow on mines’

local procurement plans makes it hard for local suppliers to plan their work. As a consequence, many suppliers go into general dealership instead of specialised services. Many suppliers believe foreign owned mines to have personal preferences towards suppliers from their own countries. This is discussed in more detail in Chapter 3.5.

Large numbers of identical local businesses wishing to supply overwhelms procurement officers at large

scale mines. Hundreds of local bids are submitted for each tender. Without prior track records and relationships with the buyers, it is challenging for a local business to stand out from the crowd. This, combined with inconsistent delivery from Zambian suppliers, leads to continued contracts with pre-existing international suppliers. According to several mine representatives, the best opportunities for local businesses lie in providing non-mining related products and services to the communities created around the mines, or supplying simple, fast-moving consumables to the mines.

Regulation protecting Zambian suppliers is poorly enforced and barely recognised in practice. Many

local suppliers deem changes in the regulatory scheme as the most promising way forward. Chapter 3.4. discusses the regulatory situation in more detail.

One truck tyre alone costs 75,000 USD. We have 52 trucks, each of which need 12 tyres per years. These are simply not available locally.”

“

- CSR manager in a mine

Needs and challenges in the Zambian (small scale) mining sector14

3�2� Challenges with financial capacity

3�2�1� Limitations due to insufficient working capital

Local suppliers’ weak financial capacity was mentioned as a challenge in nearly every interview. Particularly the lack of working capital was highlighted, as mines generally do not pay up-front. Suppliers are unable to cover expensive procurements from overseas. As a result, local SMEs are often limited to smaller sub-contracting deals only, despite ambitions for managing larger contracts. Past failures to deliver large order volumes affect the reputation of local suppliers in general.

Access to quick operational funding from banks is a challenge. Requirements for bank loans are stringent and interest rates can be as high as 28%. Getting a loan approved can take 14 days – leading to deals being lost. According to the AfDB study in 2019, many suppliers have lost their properties because they borrowed commercially but were unable to repay on time due to delayed

payments from mines.1 Some mines do consider this and provide fixed 30-day payment policies.

Weak financials equally limit the local suppliers’ capacity to expand and keep stock of products and spare parts, thereby making them less attractive suppliers. When equipment breaks down, mines usually turn to OEMs who can provide back-ups and spares quickly from their in-country warehouses.

3�2�2� High pricing of proposals

Large mines report that more often than not, local bids are more expensive than those by foreign suppliers.

This can be partly explained by currency fluctuations and high costs of production. High electricity costs are a limitation for businesses such as local foundries running furnaces. Partly, high prices are likely to be due to poor business skills and overly ambitious mark-ups. In most cases, having to import raw materials and parts shoots up local suppliers’ costs. For example, locally produced copper cables are reported to be more expensive than imports1.

To deliver a rigging contract, we are required to have working capital for 180 days, covering mobilisation of equipment and labour, procurement, and safety measures. Weak commercials are the biggest challenge among local companies in the sector.”

“

- A rigging service provider.

We gladly procure from Zambian suppliers whenever possible, but usually prices are too high, lead times are longer, and the risk of delivery failures is unacceptable.”

“

- Senior manager in alarge mine

Needs and challenges in the Zambian (small scale) mining sector 15

3�3� Quality and efficiency challenges

Many local suppliers struggle with quality control. A need for training in quality assurance was mentioned a few times, as was the wish to obtain an ISO certification. Typical complaints from mines include unreliability, inconsistency, and delays in supply of parts, products, and repair services. Logistics in a land-locked country can cause challenges to suppliers who are unable to keep stock and import items on an as-required-basis. To reach Zambia, goods need to pass through many borders.

With labour contractors, there is a problem with the stability of labour. As workers jump between jobs and work sites, quality suffers. Suppliers located in remote areas struggle with access to electricity, affecting their efficiency negatively.

According to some of the mines, many Zambian suppliers prefer to import and resell, rather than manufacture. From the mines’ perspective, the import-resell

structure is simply an unnecessary cost, as they have equally good access to the original foreign source themselves, without the help of middlemen. Furthermore, OEMs offer important insurances, warranties, and after-sale services that local suppliers fail to provide.

A clear message from the mines was for suppliers to specialise in certain goods or services instead of going into general dealing. Suppliers were encouraged to manage their risks by supplying something easily accessible, such as fast-moving goods (e.g. toilet paper).

Mines’ excuses are always about competence and quality without even knowing the company. One mining house came to visit us, they were surprised positively and started making orders. Quality could be improved further if the mines supported us!”

“

- Manager in an engineering and manufacturing company

When their core business does not bring in enough income, suppliers tend to multi-skill, which compromises quality.”

- Manager in a large mine

“

- Manager in a large mine

If an SME fails to deliver a highly expensive, technical product, the whole business will go down. It’s a huge risk for them, too.”

“

Needs and challenges in the Zambian (small scale) mining sector16

Mining managers also recommended local businesses to look beyond the mining value chain. For instance, in Kalumbila, many basic products and services such as lettuce, butcheries, mechanic services, tyre pumping stations, paintbrushes, nails, screws, or dishwashing powder are difficult to find.

An environmental consultancy company reported that poor practices among

their competitors affect the reputation of local consultants in general. Sometimes documents are written without site visits, and plagiarism is common. The best way toget business is through referrals or credible partners.

Quality issues are closely tied to gaps in digital tools, equipment, and skills, which are discussed further in chapters 3.6 and 3.7.

3�4� Regulatory challenges

Suppliers located in remote areas struggle with access to electricity, affecting their efficiency negatively.

3�4�1� Gaps in current local content legislation

Zambia has a clear gap in dedicated local content legislation protecting local suppliers in the mining sector, although the current Mines and Minerals Development Act (2015) does compel a mining right licence holder to give preference to: � Materials and products made in Zambia; � Contractors, suppliers and service

agencies located in Zambia and owned by citizens or citizen owned companies;

� Give preference in employment to citizens with relevant qualifications or skills; and

� Conduct training programmes for the transfer of technical and managerial skills to Zambians.1

However, in their assessment in November 2020, the Ministry of Mines and Mineral Development identify five key weaknesses in the current legislation: � Lack of definition for “local” � Lack of defined target values or

parameters for procurement of locally manufactured goods and sourced services

� Lack of mechanisms to monitor, enforce, and evaluate local procurement

� Only mines are bound by the legislation, leaving out large, typically foreign owned ‘Tier 1 contractors’ and OEMs

� Loophole for mines to implement low quality Local Business Development (LBD) programmes as Corporate Social Responsibility (CSR) initiatives resulting in failure to address the local suppliers’ real technical and financial barriers.4

The interviews showed that awareness on the existing policies and legislation was very low among professionals both in large mining companies and local suppliers. Most suppliers were in favour of stronger regulations, seeing legislative measures as the most promising path towards increasing local content in supply chains.

3�4�2� Proposed new local content legislation

There is movement towards creating a standalone Local Content Act, particularly for local manufacturing and supply of selected product and service categories. Enacting the law could change the playing field and offer fruitful opportunities for Zambian businesses – and those partnering with them.

Needs and challenges in the Zambian (small scale) mining sector 17

Type of product / service Target opportunities for localisation according to AfDB

Assembled components � Substitute imported steels in rock drills and drill steels � Manufacturing conveyor belt pulleys and idlers, pumps (casings)

and valves � Manufacturing rolled mild steel plate and sheet

Metallic components � Manufacturing hard wearing steel alloys for use in mill balls, mill rods, crusher wear parts, feeder wear parts, pump impellers etc, and manufacture of components themselves

� Manufacturing mild steel plate and sheet for bins, chutes and pipes and or the components themselves

� Manufacturing specialty steels for gear cutting and gear boxes � Manufacturing high tensile steel for winding, normal wire and steel

for nuts and bolts

Explosives � Explore boosting operations at Nitrogen Chemicals Zambia (NCZ, parastatal company) to meet domestic demand

Reagents and chemicals � Explore boosting operations at NCZ to meet domestic demand

Electrical components � Manufacturing winding wire for motors and transformers � Manufacturing special steels for motor and transformer

components � Manufacturing electric motors � Manufacturing ceramic insulators

Other inputs � Manufacturing refractory bricks � Transportation of oils and fuels

Core mining services � Explore possibilities of Zambians becoming junior partner to Tier 1 suppliers of core mining services

Non-core services � Limit transportation of copper to ports by foreign firms to provide space for Zambian companies.

Source: African Development Bank, 2019.1

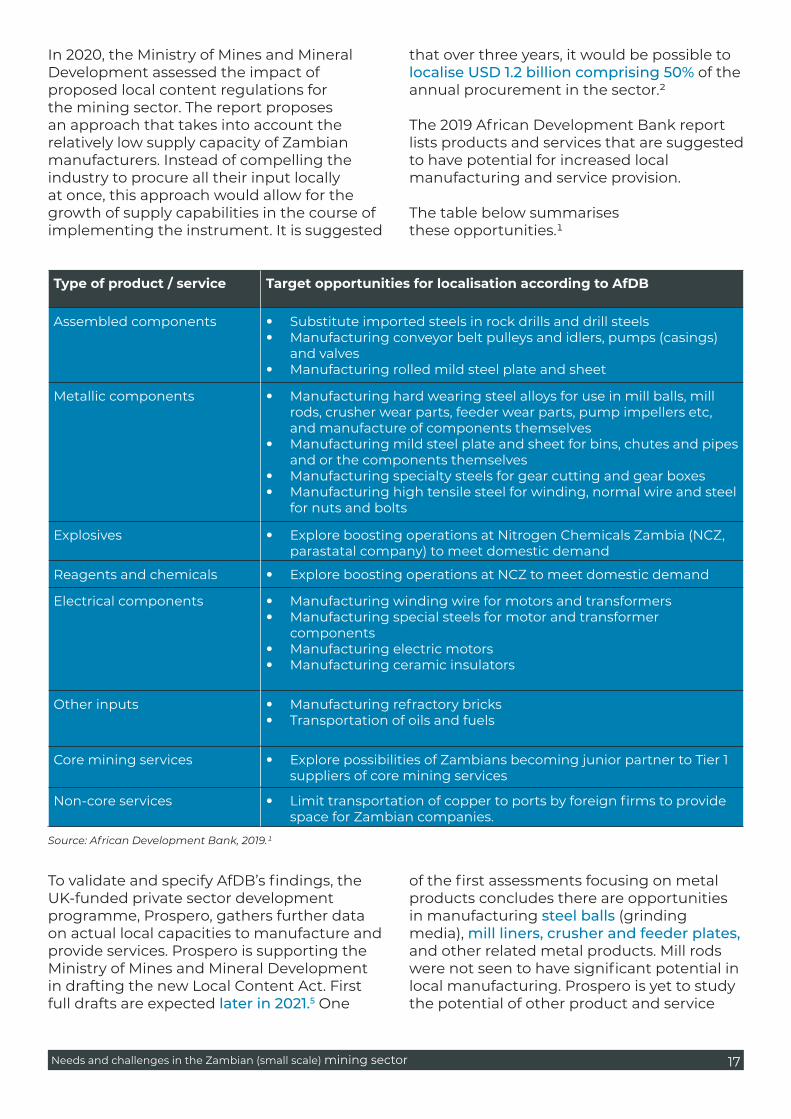

In 2020, the Ministry of Mines and Mineral Development assessed the impact of proposed local content regulations for the mining sector. The report proposes an approach that takes into account the relatively low supply capacity of Zambian manufacturers. Instead of compelling the industry to procure all their input locally at once, this approach would allow for the growth of supply capabilities in the course of implementing the instrument. It is suggested

that over three years, it would be possible to localise USD 1.2 billion comprising 50% of the annual procurement in the sector.2

The 2019 African Development Bank report lists products and services that are suggested to have potential for increased local manufacturing and service provision.

The table below summarises these opportunities.1

To validate and specify AfDB’s findings, the UK-funded private sector development programme, Prospero, gathers further data on actual local capacities to manufacture and provide services. Prospero is supporting the Ministry of Mines and Mineral Development in drafting the new Local Content Act. First full drafts are expected later in 2021.5 One

of the first assessments focusing on metal products concludes there are opportunities in manufacturing steel balls (grinding media), mill liners, crusher and feeder plates, and other related metal products. Mill rods were not seen to have significant potential in local manufacturing. Prospero is yet to study the potential of other product and service

Needs and challenges in the Zambian (small scale) mining sector18

groups. At least nuts, bolts, wire, nails and centrifugal pumps are in the pipeline for

further investigations.6

Some of the interviewed suppliers reported experiencing discrimination in procurement processes. According to the AfDB study, discrimination has affected at least local manufacturers of transformers, cables, explosives, and switch gear, as well as foundries. The study identified close relationships between mines and ‘Tier 1’ suppliers – dominant, typically foreign owned large suppliers. Chinese and South African companies crowded out local suppliers by sourcing all their inputs directly from their own countries.1

The suppliers interviewed by AfDB stated that mines provide favourable business terms to foreign ‘Tier 1’ contractors and their subcontractors, including duty free imports of inputs, advance payments on goods and services, guarantees for credit lines and sometimes even office space. According to the AfDB study findings, Zambian subcontractors pay duty on their imports and have overheads including statutory payments like NAPSA, Workers Compensation, Affiliation fees to EIZ and NCC, etc. Foreign companies are not subjected to these statutory payments.1 Zambian contractors are often forced into inferior junior partnerships with foreign ‘Tier 1’ service providers.

Transparency in tender processes was described as weak. According to a local Chamber of Commerce, the mines’ annual local procurement plans are not made available with enough detail for suppliers to plan their courses of action. Consequently, many suppliers become general dealers trying to prepare for everything – which, in turn, is not attractive to mines interested in specialised skills and services. After receiving negative responses to their bids, (aspiring) suppliers are left wondering what the weaknesses were, without a chance to learn or improve.

3�5� Discriminatory practices and transparency gaps

We mainly get junior sub-contracting jobs, even though we have the capacity to handle entire contracts.”

“- An engineering business manager

One mine stated that the locally produced mill balls are not compatible with their machinery – but they don’t disclose the information on the type of mill balls that are needed. How can a local manufacturer compete without knowing these trade secrets?”

“

- Representative of a local Chamber of Commerce

Needs and challenges in the Zambian (small scale) mining sector 19

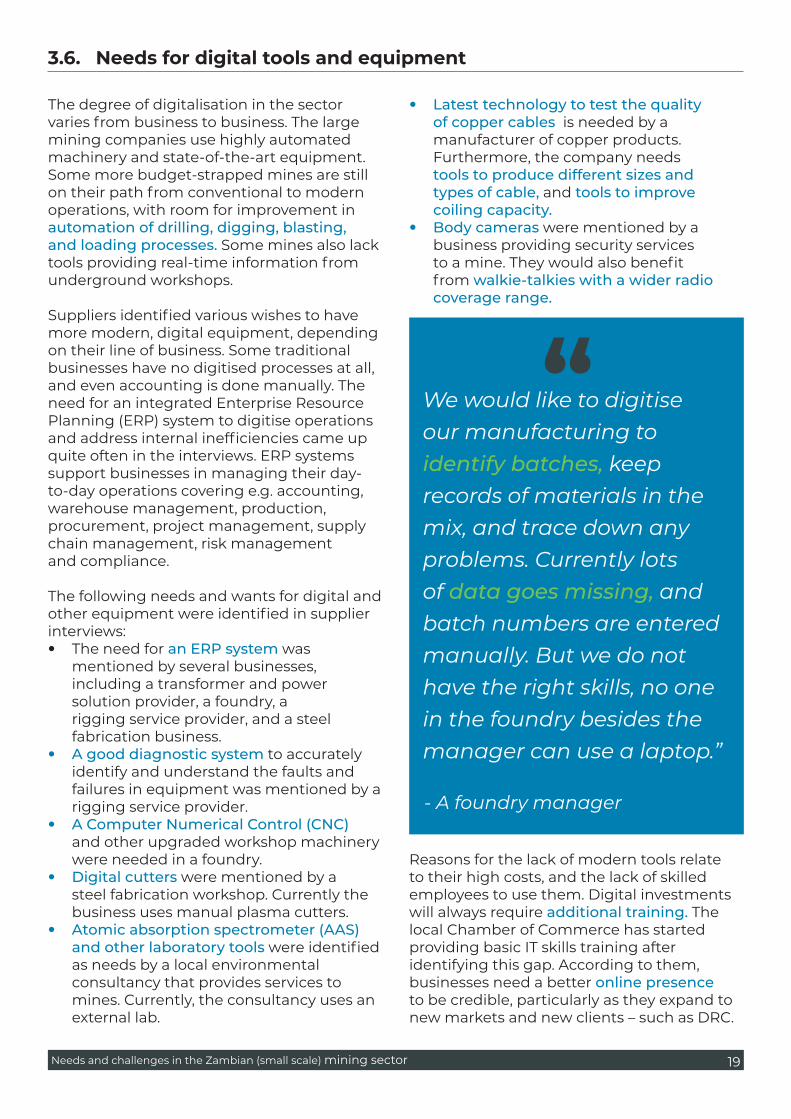

The degree of digitalisation in the sector varies from business to business. The large mining companies use highly automated machinery and state-of-the-art equipment. Some more budget-strapped mines are still on their path from conventional to modern operations, with room for improvement in automation of drilling, digging, blasting, and loading processes. Some mines also lack tools providing real-time information from underground workshops.

Suppliers identified various wishes to have more modern, digital equipment, depending on their line of business. Some traditional businesses have no digitised processes at all, and even accounting is done manually. The need for an integrated Enterprise Resource Planning (ERP) system to digitise operations and address internal inefficiencies came up quite often in the interviews. ERP systems support businesses in managing their day-to-day operations covering e.g. accounting, warehouse management, production, procurement, project management, supply chain management, risk management and compliance.

The following needs and wants for digital and other equipment were identified in supplier interviews: � The need for an ERP system was

mentioned by several businesses, including a transformer and power solution provider, a foundry, a rigging service provider, and a steel fabrication business.

� A good diagnostic system to accurately identify and understand the faults and failures in equipment was mentioned by a rigging service provider.

� A Computer Numerical Control (CNC) and other upgraded workshop machinery were needed in a foundry.

� Digital cutters were mentioned by a steel fabrication workshop. Currently the business uses manual plasma cutters.

� Atomic absorption spectrometer (AAS) and other laboratory tools were identified as needs by a local environmental consultancy that provides services to mines. Currently, the consultancy uses an external lab.

� Latest technology to test the quality of copper cables is needed by a manufacturer of copper products. Furthermore, the company needs tools to produce different sizes and types of cable, and tools to improve coiling capacity.

� Body cameras were mentioned by a business providing security services to a mine. They would also benefit from walkie-talkies with a wider radio coverage range.

Reasons for the lack of modern tools relate to their high costs, and the lack of skilled employees to use them. Digital investments will always require additional training. The local Chamber of Commerce has started providing basic IT skills training after identifying this gap. According to them, businesses need a better online presence to be credible, particularly as they expand to new markets and new clients – such as DRC.

3�6� Needs for digital tools and equipment

We would like to digitise our manufacturing to identify batches, keep records of materials in the mix, and trace down any problems. Currently lots of data goes missing, and batch numbers are entered manually. But we do not have the right skills, no one in the foundry besides the manager can use a laptop.”

“

- A foundry manager

Needs and challenges in the Zambian (small scale) mining sector20

The lack of modern mining technology was identified as a challenge in a local university. Students do not get enough exposure to

high-tech machinery and tools during their studies, making them less attractive for employment in the industry.

3�7� Challenges in skills development and education

3�7�1� Key skill gaps in the industry

The interviewed large mining companies have training facilities and on-the-job training processes for in-house staff. Some of them support the surrounding community with skills development in non-mining related fields as an attempt to decrease dependency on the mine. Some staff are supported to finish schooling or qualifications in vocational schools or universities.

One of the large mines reported contracting the vast majority of labour locally – but not without criticism. Reliable technical professionals with specialised skills, such as welders and boiler makers, are hard to find. Illiteracy continues to be an issue among the labour force.

Several businesses mentioned that technical problem-solving skills were scarce - for example, understanding why a transformer is overheating and how to fix it. Very few are able to diagnose breakdowns beyond what a diagnostic tool can tell. Some SMEs reported being reliant on one or two individuals with specific skills. One foundry business only has one skilled pattern maker and no back-up plan. Another business still relies on a retired furnace builder.

Management and supervision skills were mentioned a few times. A rigging business stated that supervisors tend to rather fix problems themselves than teach their subordinates. A local Chamber of Commerce explained that many employees are very dependent on their manager, unable to operate the business without them. According to the Chamber, SMEs in the sector generally lack financial skills – particularly managing working capital, human resource development skills and knowledge in statutory requirements. Many businesses fail to expand due to lack of business skills such as business plan development, pitching for investors or developing partnerships.

Some of the larger and more established SMEs offer structured training programmes for employees. Smaller businesses tended to follow the on-the-job training approach. A few SMEs mentioned wishing to complete ISO or other quality assurance training. Some of the SMEs that invest in skills development mentioned a “brain drain” problem. Ensuring that trained employees stay onboard instead of going to work in the mines is a challenge.

Technical skill gaps mentioned in interviews: � Diagnosing breakdowns � Welding � Making boilers � Basic foundry skills � Specialised foundry skills e.g. pattern making � Building furnaces � Winding and assembling transformers � Environmental research skills � Correct use of security tools such as tasers or

pepper spray � ISO / quality assurance training

Business skill gaps mentioned in interviews: � Management and supervision skills � Basic digital skills � Financial skills, particularly managing

working capital � Knowledge on statutory requirements � HR management skills � Business planning, obtaining investors and

partners � Self-driven and independent working skills

among employees

Needs and challenges in the Zambian (small scale) mining sector 21

3�7�2� Collaboration between industry and educational institutions

There is a certain level of misalignment between educational institutions’ curricula and the needs in the industry. University courses were criticised for being too academic, leaving students with little practical skills. The lack of modern equipment in schools contributes to the problem. Despite these issues, graduate uptake rates are good according to the interviewed university.

Vocational schools were cited as focusing too much on business courses, while compromising the quality of technical skills development. This was explained by business courses bringing in more enrolments and therefore more income for the schools.

There appears to be opportunity to increase interaction between educational institutions and SMEs in the mining industry. Some businesses send employees to vocational schools for upgrading of skills. Others have considered it but could not have employees gone for long periods. Training on the site would be preferred. Internships and student field trips to mines are less common than before due to funding gaps. Some of the SMEs accepted interns, but in most cases the collaboration was not formalised.

There are serious skill gaps in the environmental consulting industry. Academically educated professionals are unable to complete studies on topics such as quality, hydraulic, aquatic ecology, or fauna assessment. Reports are of poor quality and plagiarism is common.”

“

- Environmental consultant

Vocational school quality is not great – but they are very important! Unfortunately, they want to be more like universities and to focus on business. Real trade schools have been killed, but we need to go back to that.”

“

- A university professor

Needs and challenges in the Zambian (small scale) mining sector22

The interviewed local university showed great interest in engaging with the industry further – both in curriculum development and research and development (R&D). R&D collaboration is currently very uncommon, despite the university’s attempts to activate the mining houses. The university is interested in co-owning patents and developing new solutions in Zambia. The response from industry has been sluggish.

According to the university, mines tend to turn to foreign countries when new technology needs emerge. Their focus is on short-term production instead of investing in long-term research. Lobbying and partnerships are needed to raise the mines’ interest in R&D. There is also interest from the university to partner with OEMs in conducting local training.

3�8� Environmental challenges and circular models

3�8�1� Mines and the environment

The environmental law around mining is quite strong, but there are serious gaps in its implementation and enforcement. According to environmental experts interviewed for this study, most mines are non-compliant when it comes tothe environment.

Environmental management systems are missing, as are environmental officers, policies, and procedures.

The situation is different with larger mines, who do invest in environmental management. Some of them report very high environmental compliance rates. However, experts question the truthfulness of these numbers, stating that mines usually write the reports themselves. Auditors approve the reports without studying samples. Due to financial and human resource gaps, law enforcement and governmental monitoring of compliance is insufficient.

A facility called Environmental Protection Fund collects contributions from mines and aims to assure funds for the rehabilitation of mining areas when a mine fails to do so. One

of the interviewed experts states, however, that contributions to the fund are low, and many mines are years behind in remittances.

Water management, waste disposal and rehabilitation of mining areas were highlighted as some of the largest environmental challenges in the sector. Some mines and suppliers complained not being able to afford the environmentally sound, electronic equipment. Acids used in leaching processes were also mentioned as a problematic area.

On paper, we surely demand our suppliers to follow environmental regulations, but we can only control what we see. There is a gap in enforcement.”

“

- Manager in large mine

To get a mining license, mines must complete an initial Environmental Impact Assessment (EIA). For many of the smaller mines, commitment ends there.

Needs and challenges in the Zambian (small scale) mining sector 23

The more environmentally compliant mines grant their success to good planning in the mine initiation phase. Such players have come across challenges with the environmental literacy among stakeholders, including public officials and the surrounding community. One mine in particular reports that due to knowledge gaps, the community tends to blame the mine for any occurring environmental issue, even when it has no relation to the mine’s activities.

3�8�2� Suppliers and the environment

On the supplier side, environmental matters were considered to varying degrees. Some of the interviewees were not aware of mines having any environmental criteria towards suppliers. Others had some systems in place, but usually processes were nottoo formalised.

High use of electricity (in a foundry) or diesel (in a silica sand mine) were mentioned as some of the experienced environmental challenges.

3�8�3� Recycling and circular business models

Disposal of waste was mentioned as a challenge quite often, both by mines and

suppliers (e.g. by a rigging company and a transformer company). Some mentioned witnessing other industry players having poor practices, such as waste disposal into rivers. Larger companies tend to have waste recycling plants or established suppliers taking care of waste collection. In many cases, the problem stems from lack of awareness and know-how. One large mine reported having a waste segregation system in place but experiencing that employees and contracted staff still fail to place hazardous waste in the correct container.

Although the concept of a circular economy may not be familiar to everyone in the industry, many inherently circular models are in place. All scrap metal is recycled and used to produce e.g. castings or mill balls. Currently, a shortage of scrap metal is causing real challenges to the foundries, as scrap is being exported despite regulations against it. Markets exist for scrap copper, aluminium, transformer oil, and obsolete equipment. In some cases used engine oil is used to create explosives.

Some businesses recycle and reuse plastic in packaging or bedding processes. Others sell chemical bags and other plastics to businesses supplying PVC ceilings. More opportunities may potentially lie in compressing and reusing plastic in walls, pillars, paving blocks, roof tiles and other construction purposes. Local manufacturers of dustbins, piping, plastic sheeting or electrical are potential buyers of pellets made from recycled plastic.7

The industry generates large volumes of used tyres. This was mentioned frequently as a circular business opportunity. Black carbon extracted from tyres can be used as a reinforcing material or pigment in rubber products and other industrial applications. Tyres can be used for various noise and vibration reducing purposes in the mining and construction sectors. Shredded tyres can be mixed with tarmac to reduce material costs.5

- CSR manager in a copper product manufacturing company

In this industry, a dedicated expert in environmental matters is considered a luxury.”

“

Needs and challenges in the Zambian (small scale) mining sector24

3�9� Social challenges: safety and community relations

3�9�1� Health and safety practices

Most interviewees were of the view that health and safety measures are prioritised and well taken care of by mines. Similar procedures are expected of contractors and suppliers. Chinese mines were mentioned as an exception.

Despite having measures and training in place, some businesses reported problems with employees internalising the protocols. A large mine reported the biggest reason for safety dismissals being alcohol - reporting to work drunk. As a response, the company had started using breathalysers.

3�9�2� CSR and community relations

The larger mines have dedicated departments for corporate social responsibility (CSR). Two CSR managers in large mines were interviewed for this study. Notably, most of the CSR work focuses on

non-mining related activities. Their core work aims to build sustainable livelihoods outside of the mining sector, with an attempt to reduce dependence on the mine. Projects range from agribusiness support, entrepreneurship training, training on nutrition, support to jewellery manufacturing workshops, to projects reducing gender-based violence.

In mining towns, most economic activity revolves around the mine. Large mines have changed lifestyles by building infrastructure, services, and creating direct and indirect jobs. Developing a social sustainability strategy or preparing for mine closure was mentioned as one of the major challenges in CSR work. Managing expectations of the surrounding community is also a challenge when the mine is moving from the construction phase to the operations phase:

Human behaviour is the main attribute to safety incidents. Awareness needs to be raised on each individual’s responsibility towards their own safety.”

“

- CSR manager in alarge mine

We don’t support mining suppliers because there are hundreds of them. We would rather support other, more sustainable, income generating opportunities, such as conservation farming.”

“

- CSR manager in alarge mine

Needs and challenges in the Zambian (small scale) mining sector 25

When a mine is initially constructed, large volumes of labour are needed. This creates expectations in the community. In the operational phase, labour must be reduced, planting a permanent seed of bitterness in the community.”

“

- CSR manager in a large mine

Needs and challenges in the Zambian (small scale) mining sector26

4� Opportunities and recommendations

In this chapter the study aims to give recommendations on how to turn the challenges and needs into opportunities.

This chapter compiles the products and services that were identified as opportunity areas for local manufacturing and supply, based on the interviews. In addition, it discusses next steps and possible models to tackle expressed challenges relating to: � demand for affordable, modern tools

and equipment � technology transfer and R&D for products

and services on demand, � opportunities in the circular economy, � development of skills and expertise for

modern equipment and digitalisation, � networking and supply chain

development to support procurement processes,

� needs and benefits of quality processes, � audits and certifications, � local content regulations, and � sustainable and inclusive

business practices.

Expressed needs and challenges will be taken into consideration when planning AGS Programme activities, specifically training programmes (LEARN), the mining sector business accelerator (LEVEL UP), and innovation and co-creation activities (LEAP).

4�1� Product and service lines with opportunities for local suppliers

In several interviews, local suppliers received criticism for attempting unrealistic bidding opportunities competing against large numbers of similar competitors. As counter suggestions, some products and services were mentioned as ‘low-hanging fruits’: opportunity areas with potential for local manufacturing and service provision.

In general, it was recommended to move away from general supply towards specialised products or services. This would help to focus the offering and expertise, and to develop references and credibility.

The table below lists some products and services mentioned in the interviews and literature, with comments or recommendations attached. The list is not comprehensive, but it can provide some ideas for local businesses. Furthermore, collaboration opportunities can be explored between Zambian and Finnish companies around these products and services. The study recommends investigating whether there is suitable offering or know-how available in Finland, to look at options for technology transfer, and different forms of collaboration.

The study recommends investigating whether there is suitable offering or know-how available in Finland, to look at options for technology transfer, and different forms of collaboration.

Needs and challenges in the Zambian (small scale) mining sector 27

Type of business / actor Comments / points of further study

Manufacturing steel balls The bulk of steel balls are already manufactured in Zambia by foreign-owned (primari-ly Chinese) firms, but there is opportunity for more Zambian-owned businesses to tap into this market.4

Manufacturing mill liners Currently, 97% of mill liners are imported. There are opportunities for local manufacturing. However, it should be noted that: � the design and manufacturing process is somewhat complex � OEMs are currently dominating the market. There may be potential for OEMs

outsourcing or licencing to Zambian manufacturers. � Demand is irregular.4

Manufacturing crusher and feeder plates

There is potential for growth in local manufacturing, if competitive local hard steel intermediate products become available.4

Manufacturing other small equip-ment such as: � back-up generators � pumps � conveyer belts � bearings � pipes � electric motors

Points of further study: � Who are the current or potential manufacturers? � Are they competitive and compliant? � Are technologies and manufacturing skills available locally or can they be

trained?

Conveyer belts are currently being imported, but there is potential to manufacture locally.

Assembled components; Especially metallic parts i.e. steel plates, other steel parts, specialty steel for gear boxes, rock drills and drill steels.

Opportunity for local manufacturers providing parts to substitute imported parts. Mild rolled steel plates and sheets for manufacture of components. Look at opportunities on manufacturing of hard steel.

Electrical components Manufacturing of electric motors or components for motors and transformers, manu-facturing of ceramic insulators

Explosives Explosives are already the largest product group in local manufacturing. Further opportunities to be explored with manufacturing of reagents and chemicals as well as increasing manufacturing of explosives to meet the local demand.

Recycling and reusing used tyres. Black carbon extracted from tyres can be used as a reinforcing material or pigment in rubber products and other industrial applications. Tyres can be used for various noise and vibration reducing purposes in the mining and construction sectors. Shredded tyres can be mixed with tarmac to reduce material costs.

Points of further study: � Are there companies interested in this circular economy business? � Is the material i.e. used tyres and their recycling available regularly? � Could collection of used tyres offer business opportunity to some actor? � Are there regulations and support available? � Are recycled materials acceptable and interesting in Zambian context?

Core mining services Explore opportunities of becoming junior partner to larger suppliers.

Transportation service Explore opportunities to deliver oils and fuels to mines as well as copper to ports.

Supplying fast-moving consumables to mines

An opportunity for the non-mining sector. Points of further study: � What can be learned from the successes and failures of businesses already

doing this? � What are the procurement channels?

Serving communities built around the mines, some of which include affluent expats. Non-mining related business opportunities.

See above. Probably partly the same companies, partly different. Sales channels would be different.

Needs and challenges in the Zambian (small scale) mining sector28

4�2� Demand for affordable, modern tools and equipment

4�3� Circular business opportunities

Market opportunities around providing specific equipment and modern/digital tools to mining companies and actors in the value chains should be analysed further. Finnish offerings and opportunities for business partnerships should be explored. Digitalisation is one of the key priorities to increase efficiency, productivity, and sustainability in mining. There are opportunities in automation of drilling, digging, blasting, and loading processes, and modernising machinery in local manufacturing workshops. Smaller local suppliers would benefit from basic digital tools such as Enterprise Resource Planning (ERP) software, and an improved digital presence to better market their services. However, the need for digital tools goes hand-in-hand with a need to upgrade digital

skills of workforce in the industry.

Other needs for specific equipment included:

� Diagnostic system to accurately identify and understand the faults and failures in equipment

� Computer Numerical Control (CNC) machine

� Digital cutters � Atomic absorption spectrometer (AAS)

and other laboratory tools � Latest technology to test the quality of

copper cables � Tools to produce different sizes and types

of cable � Tools to improve coiling capacity. � Body cameras � Walkie-talkies with a wide radio

coverage range.

There is a variety of opportunities in environmental management and circular models that can be pursued in the sector. Water treatment processes, waste disposal, and rehabilitation of mining areas are some of the highlighted opportunity areas.Fresh water balance and quality management and monitoring is essential to guarantee proper water supply for mine plant and household use in the mining communities. Likewise effluent water processing is environmentally a key issue in mining regions. Finnish-Zambian cooperation opportunities for both of these should be explored in more detail.

Opportunities to reuse of old tyres were specifically mentioned several of the interviews (see table in chapter 4.1.) Although some solutions already exist, there may be further opportunities in recycling and reusing plastic, e.g. in walls, pillars, paving blocks, roof tiles and other construction purposes. Local manufacturers of dustbins, piping, plastic sheeting or electrical are potential buyers of pellets made from recycled plastic.

The study recommends exploring further opportunities related to recycling, reusing and remanufacturing goods from recycled materials.

Opportunities in vocational training and business skills training can be explored to address the basic technical and business skills that were deemed insufficient. AGS Programme plays a role in mending the gap

through its business development trainings and acceleration programmes. The text box below recaps the mentioned technical and business skill gaps.

4�4� Development of technical skills, business skills, and expertise in modern equipment and digitalisation�

Needs and challenges in the Zambian (small scale) mining sector 29

Technical skill gaps mentioned in interviews:

� Diagnosing breakdowns � Welding � Making boilers � Basic foundry skills � Specialised foundry skills e.g. pattern

making � Building furnaces � Winding and assembling transformers � Environmental research skills � Correct use of security tools such as

tasers or pepper spray � ISO / quality assurance training

Business skill gaps mentioned in interviews:

� Management and supervision skills � Basic digital skills � Financial skills, particularly managing

working capital � Knowledge on statutory requirements � HR management skills � Business planning, obtaining investors

and partners � Self-driven and independent working

skills among employees � Literacy skills among labourers

The lack of skills and expertise to use modern equipment and digital tools seems to be common, apart from the large international mining companies. There are successful industry-academia collaboration models from other countries and sectors, that can be used as benchmark in creating awareness and skills. Some examples are outlined below. AGCO Zambia Ltd operates a Martin Richenhagen Future Farm near Lusaka. The vision is to empower farmers by educating people on modern farming techniques to develop sustainable food production systems and to increase productivity. The farm started in 2015 and is providing online and classroom-based courses to promote latest solutions in agriculture and the understanding of successful farming techniques. AGCO Corporation is an agricultural machinery company designing, manufacturing, and distributing a wide variety of agricultural equipment.

These kinds of demonstration farms are a common model in the agricultural machinery sector to promote new technology and modern farming practices by demonstrating the use of novel machinery and providing training on how to use them. Operating models vary from pilots, longer term projects with external funding, to self-sustainable entities, possibly joint ventures or cooperatives. These model farms enable skills development, product testing, and

development, and serve also as companies’ showrooms. Typically, the machinery is large and expensive, hence buyers would want to see it before making the purchasing decision.

In another best practice model, within the Indian Institute of Management (IIM) of Ahmedabad, a course or series of lectures are organised in collaboration with industry. Company representatives act as lecturers and mentors, and companies provide the technology for the students to train with. For companies this is a good opportunity to create awareness of their technology among students, who in a few years will be working in their potential customer companies. Between courses this platform can also serve as the companies’ showroom to present, demonstrate, and pilot the equipment for potential customers.

The study recommends discussing whether these kinds of models could be adapted to the mining sector in the Zambian context. In our view, it would best fit to be organised in collaboration with the mining education programme at CBU. Specialised courses in collaboration with the industry could be added to the university curriculum to enhance skills and expertise to use modern equipment. This would increase the employability and skills of students, as well as develop the capacity, offering, and academia-industry collaboration of the university.

Needs and challenges in the Zambian (small scale) mining sector30

The need for training in quality assurance was mentioned in the interviews a few times. Quality assurance training and support to the development of companies’ quality systems and processes should be made locally available. Quality assurance and quality management should also be included in mining sector related curricula.

The relevance of quality certificates depends a lot on the product or service. Needs for certificates should be analysed as part of company specific development needs assessment to understand what kind of quality certificates would be required, if any. In some cases, lack of required certificates can be a barrier to trade, especially in export trade and procurement of international

mining companies. A quality certificate can be a differentiating factor in the procurement process, verifying adherence to certain quality standards.

It would be important to find out the locally relevant ISO and other certificates as well as the process to obtain these. Especially beacuse ISO certification is a laborious and fairly expensive process and should not be entered without conscious strategic decision.

This being said, it is good to note that typical complaints from mines include unreliability, inconsistency, and delays, which are often more related to the basic service process development than need for expensive certification.

4�5� Needs and benefits of quality assurance and certifications

Service process development and quality assurance are the key to solve most common quality issues. Need for certificates should be analysed carefully before entering the often expensive and laborious process.

4�6� Networking and supply chain development to support procurement processes

We recommend local suppliers to focus on networking, supply chain development and entering contracts as subcontractors to obtain references. Supply chain development will also be in focus within AGS mining sector business accelerator.It is common, though frustrating, that large international companies prefer to use foreign suppliers and OEM manufacturers whom they already have long-term contracts with. However, based on their statements in the interviews, mining companies would be open to further localise their supply chain, provided that sufficient products and services of required quality are available. This would also support their sustainable business practices

and community relations.

Networking, trust building, and references are key roles, especially when it comes to bidding competitions. Suppliers need to understand the requirements, decision making criteria, learn how to prepare their proposals, and be competitive.

Partnering with international businesses/investors was seen as an option to increase credibility and get foot through the door. This could also increase availability of working capital. Manufacturing locally would spill over to other economic areas too.

Needs and challenges in the Zambian (small scale) mining sector 31

Partnerships with Finnish companies, for example, could improve our prospects to compete against international suppliers.”

“- Foundry manager.

4�7� Local content regulations

4�8� Financing instruments and payment terms

Challenges, frustrations, and aspirations regarding local procurement were discussed in several, if not all interviews. The development of a new Local Content Act presents an opportunity to overcome some of these challenges. First full drafts of the Act are expected later in 2021.

It is recommended to closely follow the development of the new legislation, and studies proposing targeted product and service categories. Interested parties are encouraged to liaise with key institutions developing the Act, including the Ministry of Mines and Minerals, and Prospero. Changes in legislation could offer significant new opportunities for Zambian-owned businesses, as well as Finnish-Zambian

partnerships manufacturing or providing services locally. The nature – and beneficiaries – of the new opportunities will be largely affected by the definition of “local” taken in the new Act.

A need to raise awareness on the Local Content Act may present itself once the legislation is enacted. The involvement of stakeholders such as Chambers of Commerce and universities will be important in disseminating information to all businesses in the sector. It would be important to create dialogue and common understanding between the large mining companies and their potential local suppliers on the steps to be taken on new development of practices and procurement processes.

Challenges related to working capital and long payment terms were mentioned in several interviews. Needs for financing are obvious and commercial interest rates make it difficult, if not impossible, to build profitable business.