new york breakfast series - files.arnoldporter.com · fdic, “statement of ... administrative...

TRANSCRIPT

Private Capital Investments in Financial Institutions: An Update on Key Developments and Regulatory Issues Associated with Investments in Banks, Thrifts, and Their Holding Companies

October 29, 2009

New York n Brussels n Denver n London n Los Angeles n Northern Virginia n San Francisco n Washington, DC

New York Breakfast Series

Private Capital Investments in Financial Institutions: An Update on Key Developments and Regulatory Issues Associated with Investments in Banks, Thrifts, and Their Holding Companies

Table of ContentsAgenda and Presentation Slides ........................................................................................................................ Tab 1

Speaker Biographies: A. Patrick Doyle, David F. Freeman, Jr., Alan W. Avery, and David S. Berg ........................................................................................................................................................ Tab 2

Arnold & Porter LLP’s Financial Services Practice Group Overview ………………. ...................................... Tab 3

Arnold & Porter LLP’s Corporate and Securities Practice Group Overview ..………. ................................... Tab 4

Supporting Documents

Arnold & Porter LLP Advisory, “The Federal Reserve Board Policy Statement on Equity Investments Relaxes Restrictions on Minority Investments in Banks and Bank Holding Companies,” September 2008………………………………………………………………. ....................... Tab 5

Federal Reserve Board, “Policy Statement on Equity Investments in Banks and Bank Holding Companies,“ 12 C.F.R. § 225.144, September 22, 2008 ………………………………….. .......... Tab 6

Arnold & Porter LLP Advisory, “FDIC Final Statement of Policy on Qualifications for Failed Bank Acquisitions,” September 2009 …………………………………………………................................. Tab 7

FDIC, “Statement of Policy on the Acquisition of Failed Insured Depository Institutions,” 74 Federal Register 45440, September 2, 2009 ................................................................................................ Tab 8

FDIC, “Statement of Policy on Applications for Deposit Insurance,” July 7, 1998 ...................................... Tab 9

FDIC, Financial Institutions Letter FIL-50-2009, “Enhanced Supervisory Procedures for Newly Insured FDIC-Supervised Depository Institutions,” August 28, 2009 ............................................. Tab 10

Recent Form of Federal Reserve Passivity Commitments (Redacted) ………………. ................................. Tab 11

OTS Regulation, 12 C.F.R. § 574.4 ..................................................................................................................... Tab 12

OTS Form of Rebuttal of Rebuttable Determination of Control Under 12 C.F.R. Part 574 ......................... Tab 13

Selected Federal Banking Agency Documents .............................................................................................. Tab 14

– OTS Approval of OneWest Bank (Indy Mac Acquisition)

– OTS Approval of BankUnited Acquisition

– Redacted FDIC Passivity Agreement

Tab 1: Agenda and Presentation Slides

Private Capital Investments in Financial Institutions: An Update on Key Developments and Regulatory Issues Associated with Investments in Banks, Thrifts, and Their Holding Companies

Agenda

8:00–8:30 a.m. Breakfast

8:30–8:40 a.m. Welcome and Overview

A. Patrick Doyle, Partner, Co-Chair, Financial Services Practice

8:40–9:45 a.m. Presentations and Discussion

A. Patrick Doyle, Partner, Co-Chair, Financial Services Practice

David F. Freeman, Jr., Partner, Financial Services Practice

Alan W. Avery, Partner, Financial Services Practice

David S. Berg, Counsel, Corporate and Securities Practice

Overview of What’s New I.

Structures For Investment II.

Acquisition of Institutions III.

Process For Bidding on Receiverships IV.

Control Considerations V.

Other Regulatory Issues VI.

Other Private Equity Deal ConsiderationsVII.

9:45–10:00 a.m. Questions and Answers

New York Breakfast Series

Private Capital Investments in FinancialInstitutions: An UpdateInstitutions: An Update

Arnold & Porter Panel Members

A. Patrick Doyle, Co-Head, Financial Services Practice (NY)

David F. Freeman, Jr., Partner, Financial Services Practice (NY)

Alan W. Avery, Partner, Financial Services Practice (NY)

David S. Berg, Counsel, Corporate and Securities Practice (NY)

2Financial Markets Regulatory Roundtable

October 29, 2009

Overview of What’s New

FDIC August 2009 Policy Statement

FDIC October 2009 Out of MoneyAcknowledgement

FDIC responsiveness FDIC responsiveness

Target-rich environment

3Financial Markets Regulatory Roundtable

October 29, 2009

Structures For Investment

Direct investment by private equity fund– BHC Act/SLHC Act restrictions on control or other

Investments

– Below 25%/passive investments– Below 25%/passive investments

– Investments in loans, REO, and other assets spun out ofbanks

Silo fund (Federal Reserve and FDIC do not permit)

Club deals– Issues on other relationships among investors/action in

concert

4Financial Markets Regulatory Roundtable

October 29, 2009

Structures For Investment (cont’d)

Management-led acquisition (current regulatoryfavorite)

Strategic investors– Existing– Existing

– Create your own

5Financial Markets Regulatory Roundtable

October 29, 2009

Acquisition of Institution

De novo– FDIC policy statement on De novo institutions

– Difficulty in getting insurance approval from FDIC

Acquiring healthy institutions Acquiring healthy institutions– Change-in-Control Act

– BHC Act or S&L Holding Company Act

– Limitations on growth

– Inflatable charter (out); expansion of mid-size charter (in)

6Financial Markets Regulatory Roundtable

October 29, 2009

Acquisition of Institution (cont’d)

Acquiring from FDIC as receiver/new FDIC policystatement– Applicability

– Capital commitment

– Cross support

– Transactions with affiliates

– Secrecy law jurisdictions

– Continuity of ownership

– Prohibited structures

– Special owner bid limitation

– Disclosure

7Financial Markets Regulatory Roundtable

October 29, 2009

Process For Bidding on Receiverships

Pre-qualification/pre-clearance/shelf charter process

Applications

Bid packages

Bidding/award Bidding/award

Final approvals and closing

8Financial Markets Regulatory Roundtable

October 29, 2009

Control Considerations

Percentage of ownership– Voting

– Total equity

– Options/warrants/conversion rights

Aggregation of investors, action in concert, andagreements and relationships among investors

Board seats, interlocks, and governance

9Financial Markets Regulatory Roundtable

October 29, 2009

Control Considerations (cont’d)

Other business done between investor and bank– Reg O

– Sections 23A/B

– Passivity commitments

• Federal Reserve

• FDIC

• OTS

10Financial Markets Regulatory Roundtable

October 29, 2009

Other Regulatory Issues

Business plan

Management team

Geographic choice

Cross-guarantees Cross-guarantees

Heightened capital requirements

Source of strength/capital maintenance obligations

Restrictions on transfer of interests

Background investigation, disclosures of ownership,management

11Financial Markets Regulatory Roundtable

October 29, 2009

Other Regulatory Issues (cont’d)

Administrative enforcement jurisdiction/institution-affiliated parties

Veto rights

Prior involvement with troubled institution Prior involvement with troubled institution

12Financial Markets Regulatory Roundtable

October 29, 2009

Other Private Equity Deal Considerations

13

Other Private Equity Deal Considerations

Financial Markets Regulatory RoundtableOctober 29, 2009

Q&AQ&A

14Financial Markets Regulatory Roundtable

October 29, 2009

Contact Information

Washington+1 202.942.5000+1 202.942.5999 Fax

555 Twelfth Street, NW

New York+1 212.715.1000+1 212.715.1399 Fax

399 Park AvenueNew York, NY 10022-4690

555 Twelfth Street, NWWashington, DC 20004-1206

Financial Markets Regulatory RoundtableOctober 29, 2009

15

New York, NY 10022-4690

Tab 2: Speaker Biographies

arnoldporter.com

A. Patrick DoylePartner

Patrick Doyle has a broad background in financial institution regulation and has headed the firm’s financial services practice group since 1993.

Mr. Doyle regularly counsels bank holding companies, foreign banks, savings institutions, insurance companies, and securities firms on a wide variety of matters, including strategic planning, complex regulatory issues, enforcement proceedings and legislation. In addition, he has represented firm clients on numerous mergers and acquisitions including such recent acquisitions as BB&T’s acquisition of First Virginia Bank and M&T Bancorp’s acquisition of Allfirst Financial. In another notable matter, Mr. Doyle represented State Farm Insurance in the formation of State Farm Bank, FSB. Mr. Doyle is recognized for his ability to devise creative solutions to complex regulatory issues.

Prior to joining Arnold & Porter LLP in 1983, Mr. Doyle served as Deputy General Counsel and Acting General Counsel of the Federal Home Loan Bank Board and earlier served in a variety of legal positions at the Office of the Comptroller of the Currency, including Counsel to the Multinational Banking Group. Mr. Doyle served on the adjunct faculty of the Morin Center for Banking Law Studies at Boston University School of Law from 1985 to 1993, and currently serves on the Board of Advisors of the University of North Carolina School of Law’s Banking Law Institute.

Mr. Doyle is a frequent lecturer on topics related to the regulation of the financial services industry.

Rankings

Chambers USA: America's Leading Lawyers for Business 2009 for Financial Services Regulation: Banking & Securities (Regulatory Compliance)

The Best Lawyers in America 2009 for Banking Law

International Who’s Who of Business Lawyers 2008 for Banking

Contact Information [email protected] tel: +1 212.715.1770 fax: +1 212.715.1399

399 Park Avenue New York, NY 10022-4690

Practice Areas Financial Services (practice chair) Litigation Subprime Lending Regulation, Enforcement & Litigation

Education JD, Syracuse University College of Law, 1975 BA, State University of New York at Oswego, 1970

Admissions District of Columbia New York

A. Patrick DoyleArnold & Porter LLP 2

Articles

A. Patrick Doyle, David F. Freeman, Jr. and Beth S. DeSimone. "Private Equity Investment in US Financial Institutions: Promises and Challenges" World Law Reports Spring 2009.

A. Patrick Doyle, David F. Freeman, Jr. and Beth S. DeSimone. "Private Equity Investment: Navigating The Mine Fields" Financial Services Law360 October 2008.

A. Patrick Doyle and Robert E. Mannion. "Opportunities and Challenges for Financial Institutions in the US" Global Banking and Financial Policy Review Dec. 2000.

A. Patrick Doyle and Beth S. DeSimone. "Unitary Thrift Holding Company Worry is Overdrawn" The National Law Journal, Volume 21, Number 37, May 10, 1999.

A. Patrick Doyle and Robert E. Mannion. "Client Memo: Banking Legislation Still Pending in the House and Senate" Arnold & Porter Bulletin Apr. 1998.

A. Patrick Doyle and Beth S. DeSimone. "Client Memo: Financial Institutions Practice" January 11, 1996.

Presentations

A. Patrick Doyle. "Financial Services Reform: What the Regulatory Overhaul Means for Clients" Telephone Seminar / Audio Webcast, American Law Institute / American Bar Association (ALI-ABA), September 22, 2009.

Alan Avery, Kevin F. Barnard, A. Patrick Doyle and Kathleen Scott. "Treasury's Financial Stability Plan and Framework for Financial Regulatory Reform: An Overview and Update on Key Programs" Arnold & Porter LLP, Financial Services Regulatory Roundtable, New York, NY, April 23, 2009.

David S. Berg, Alan Avery, Kevin F. Barnard and A. Patrick Doyle. "Emergency Economic Stabilization Act: Statutory Structure, the Implementing Regulations and Procedures, and Practice Implications of TARP" Arnold & Porter LLP, Financial Services Regulatory Roundtable, New York, NY, October 28, 2008.

Advisories

"FDIC Proposed Guidance on Private Equity Investments in Failed Depository Institutions." Jul. 2009.

"Proposal to Reform Financial Regulation Contemplates Significant Changes." Jun. 2009.

"Treasury's Public-Private Investment Program for Legacy Loans and Securities." Apr. 2009.

"Summary of Treasury's Capital Assistance Program." Mar. 2009.

"What's Coming for Financial Institutions, Issuers, and Market Participants?." Mar. 2009.

"Stimulus Bill Amends Restrictions on Executive Compensation Under TARP." Feb. 2009.

"Treasury Announces the Financial Stability Plan." Feb. 2009.

"Treasury Announces New Restrictions on Executive Compensation." Feb. 2009.

A. Patrick DoyleArnold & Porter LLP 3

"Continued Participation In or Opt Out of the FDIC Debt Guarantee Program." Dec. 2008.

"US Treasury Announces Details and Guidelines for Capital Purchase Program." Oct. 2008.

"Bank Acquisitions--Congress May Review Recent Treasury Notices." Oct. 2008.

"US Treasury Announces Capital Purchase Program for Qualifying Financial Institutions." Oct. 2008.

"Implementation Begins on US Emergency Financial Relief Program." Oct. 2008.

"The Federal Reserve Board Policy Statement on Equity Investments Relaxes Restrictions on Minority Investments in Banks and Bank Holding Companies." Sep. 2008.

arnoldporter.com

David F. Freeman , Jr.Partner

David Freeman represents financial institutions, investment managers, and broker-dealers on a variety of matters including banking and securities regulatory issues, legislation, mergers and acquisitions, private investment funds, and

new product development. He has represented clients in numerous transactions, including acquisition or creation of bank holding companies, banks, trust companies, federal savings banks, joint ventures, broker-dealers, investment advisers, and insurance agencies. Mr. Freeman has also represented financial institutions in litigation involving various federal regulatory issues.

Rankings

Chambers USA: America's Leading Lawyers for Business 2009 for Financial Services Regulation: Banking & Securities (Regulatory Compliance)

Books

David F. Freeman, Jr.. "Duty to Supervise, Supervision of Registered Representatives' Outside Business Activities, and Bank Exemptions from Broker-Dealer Regulation" three chapters in PLI, Broker-Dealer Regulation, (C. Kirsch ed., 2004, 2005, 2006, 2007 revisions).

Martha L. Cochran and David F. Freeman, Jr.. "Functional Regulation (Chapter 21)" The Financial Services Revolution, C. Kirsch ed. (Irwin 1997).

David F. Freeman, Jr.. "Mutual Fund Activities of Banks" Aspen Law & Business, 1994.

Articles

David F. Freeman, Jr.. "Administration Proposes Financial Regulation Reform" The Investment Lawyer August 2009.

John D. Hawke, Jr. and David F. Freeman, Jr.. "Money Market Funds Have No Place on Banking Sheets" American Banker Apr. 2009.

Contact Information [email protected] tel: +1 202.942.5745 fax: +1 202.942.5999

555 Twelfth Street, NW Washington, DC 20004-1206

Practice Areas Financial Services Corporate and Securities Subprime Lending Regulation, Enforcement & Litigation

Education JD, University of Virginia School of Law, 1987 MBA, University of Virginia, 1987 BA, University of Virginia, 1981

Admissions District of Columbia Virginia Supreme Court of the United States

David F. Freeman , Jr.Arnold & Porter LLP 2

A. Patrick Doyle, David F. Freeman, Jr. and Beth S. DeSimone. "Private Equity Investment in US Financial Institutions: Promises and Challenges" World Law Reports Spring 2009.

A. Patrick Doyle, David F. Freeman, Jr. and Beth S. DeSimone. "Private Equity Investment: Navigating The Mine Fields" Financial Services Law360 October 2008.

David F. Freeman, Jr. and Andrew Joseph Shipe. "The Range and Impact of Ratings Reform in the US Securities Markets" The Investment Lawyer October 2008.

David F. Freeman, Jr.. "Broker Dealer Supervision" in The ABC's of Broker-Dealer Regulation, (PLI course materials, May 2006 and 2007).

David F. Freeman, Jr.. "Investment Lawyer" Regular contributor of series of articles and columns on financial services regulatory issues (1999-current).

David F. Freeman, Jr.. "Broker-Dealer Compliance Programs" SEC/NASD Compliance (ALI-ABA course materials), June 2005.

David F. Freeman, Jr. and Eunice Y. Kang. "Analyzing Bank Securities Activities: Are You Really a Finder or Trader?" Investment Lawyer Jun. 2004.

David F. Freeman, Jr.. "The Fair Valuation Mess" The Journal of Investment Compliance, (Summer 2003).

David F. Freeman, Jr. and John D. Hawke, Jr.. "The Authority of National Banks to Invest Trust Assets in Bank-Advised Mutual Funds" In 10 Ann. Rev. Banking Law (1991).

Advisories

"SEC Seeks Comments on Alternative Short Sale Rule." Aug. 2009.

"SEC Proposes Rules to Curtail Pay to Play Practices." Aug. 2009.

"SEC Announces Additional Steps to Prevent Abusive Short Sales and Increase Market Transparency." Jul. 2009.

"FDIC Proposed Guidance on Private Equity Investments in Failed Depository Institutions." Jul. 2009.

"Proposal to Reform Financial Regulation Contemplates Significant Changes." Jun. 2009.

"SEC Proposes Modifications to Custody Practices for Registered Investment Advisers." May. 2009.

"SEC Proposes and Seeks Comments on New Short Selling Regulations." Apr. 2009.

"SEC Adopts Rules Governing Short Sales and Reporting of Short Sales and Short Positions." Oct. 2008.

"US Treasury Announces Capital Purchase Program for Qualifying Financial Institutions." Oct. 2008.

"The SEC Extends Emergency Report Sale Orders." Oct. 2008.

"The Federal Reserve Board Policy Statement on Equity Investments Relaxes Restrictions on Minority Investments in Banks and Bank Holding Companies." Sep. 2008.

David F. Freeman , Jr.Arnold & Porter LLP 3

"Prohibition on Short Selling of Financial Firm Securities and New Disclosure Requirements." Sep. 2008.

"SEC Proposed New Rules to Affect Hedge Funds." Jan. 2007.

"SEC Provides No-Action Relief for Registered Investment Advisers." Aug. 2006.

arnoldporter.com

Alan AveryPartner

Alan Avery is a member of the firm’s financial services practice and concentrates his practice in federal and state regulation of banking organizations, advising domestic and foreign banking institutions concerning the impact of US

Federal and state banking laws on their global operations. Additionally, he advises domestic and foreign banks on regulatory issues, including Bank Secrecy Act (BSA) and anti-money laundering issues and investigatory matters, as well as related corporate and litigation matters.

Mr. Avery regularly counsels bank clients on a wide variety of matters, including permissible activities and investments, forms of organization, internal reorganizations, internal compliance and controls programs, product and geographical expansion, margin regulations, capital adequacy requirements, electronic banking issues, anti-tying rules, privacy regulation, Federal and state consumer lending compliance issues, affiliate transaction regulation, Bank Holding Company Act issues, corporate governance issues, state law fiduciary qualification and regulation issues, USA PATRIOT Act compliance, the BSA and related anti-money laundering regulations, payment systems issues, and pending legislation relevant to their US operations.

Mr. Avery has represented a number of US and non-US financial institutions in regards to Federal and state regulatory approval requirements for bank formations, office establishment and licensing, internal reorganizations, and mergers and acquisitions. He also advises transactional practice groups worldwide on US bank regulations. Additionally, Mr. Avery has represented sovereign wealth funds and private equity funds with respect to investments in US financial institutions.

Articles

Alan Avery and Michael B. Mierzewski. "Regulation and the Financial Crisis" Executive Counsel, May/June 2009.

Carl L. Liederman and Alan Avery. "Talk of the TALF" The European Lawyer May 2009.

Presentations

Contact Information [email protected] tel: +1 212.715.1056 fax: +1 212.715.1399

399 Park Avenue New York, NY 10022-4690

Practice Areas Financial Services

Education JD, summa cum laude, Pace Law School, Pace University, 1998 BS, with honors, United States Military Academy, 1983

Admissions New York

Alan AveryArnold & Porter LLP 2

Alan Avery, Kevin F. Barnard and D. Grant Vingoe. "Financial Regulatory Reform" Osgoode Professional Development, Toronto, ON, October 19, 2009.

Alan Avery, Kevin F. Barnard, A. Patrick Doyle and Kathleen Scott. "Treasury's Financial Stability Plan and Framework for Financial Regulatory Reform: An Overview and Update on Key Programs" Arnold & Porter LLP, Financial Services Regulatory Roundtable, New York, NY, April 23, 2009.

David S. Berg, Alan Avery, Kevin F. Barnard and A. Patrick Doyle. "Emergency Economic Stabilization Act: Statutory Structure, the Implementing Regulations and Procedures, and Practice Implications of TARP" Arnold & Porter LLP, Financial Services Regulatory Roundtable, New York, NY, October 28, 2008.

Advisories

"FDIC Proposed Guidance on Private Equity Investments in Failed Depository Institutions." Jul. 2009.

"Proposal to Reform Financial Regulation Contemplates Significant Changes." Jun. 2009.

"Treasury's Public-Private Investment Program for Legacy Loans and Securities." Apr. 2009.

"Federal Reserve's TALF Lending Program Gets Under Way and Gets Expanded Twice." Apr. 2009.

"Stimulus Bill Amends Restrictions on Executive Compensation Under TARP." Feb. 2009.

"Treasury Announces the Financial Stability Plan." Feb. 2009.

"US Treasury Announces Capital Purchase Program for Qualifying Financial Institutions." Oct. 2008.

"The Federal Reserve Board Policy Statement on Equity Investments Relaxes Restrictions on Minority Investments in Banks and Bank Holding Companies." Sep. 2008.

arnoldporter.com

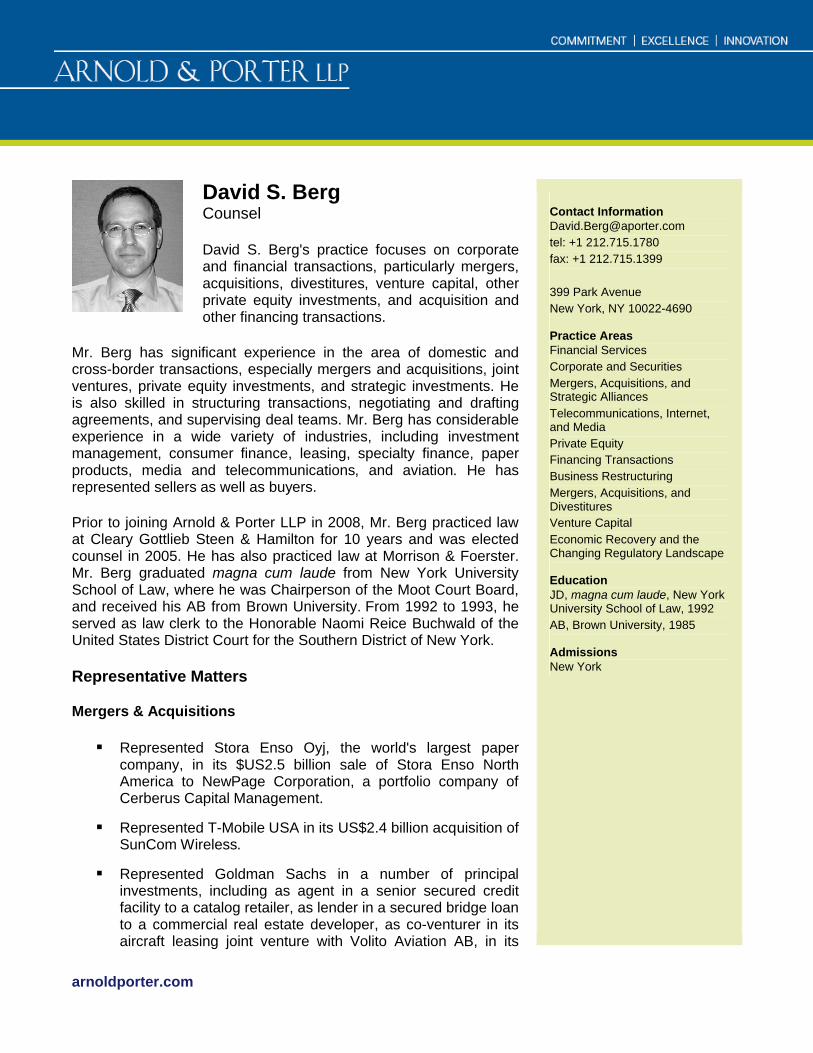

David S. BergCounsel

David S. Berg's practice focuses on corporate and financial transactions, particularly mergers, acquisitions, divestitures, venture capital, other private equity investments, and acquisition and other financing transactions.

Mr. Berg has significant experience in the area of domestic and cross-border transactions, especially mergers and acquisitions, joint ventures, private equity investments, and strategic investments. He is also skilled in structuring transactions, negotiating and drafting agreements, and supervising deal teams. Mr. Berg has considerable experience in a wide variety of industries, including investment management, consumer finance, leasing, specialty finance, paper products, media and telecommunications, and aviation. He has represented sellers as well as buyers.

Prior to joining Arnold & Porter LLP in 2008, Mr. Berg practiced law at Cleary Gottlieb Steen & Hamilton for 10 years and was elected counsel in 2005. He has also practiced law at Morrison & Foerster. Mr. Berg graduated magna cum laude from New York University School of Law, where he was Chairperson of the Moot Court Board, and received his AB from Brown University. From 1992 to 1993, he served as law clerk to the Honorable Naomi Reice Buchwald of the United States District Court for the Southern District of New York.

Representative Matters

Mergers & Acquisitions

Represented Stora Enso Oyj, the world's largest paper company, in its $US2.5 billion sale of Stora Enso North America to NewPage Corporation, a portfolio company of Cerberus Capital Management.

Represented T-Mobile USA in its US$2.4 billion acquisition of SunCom Wireless.

Represented Goldman Sachs in a number of principal investments, including as agent in a senior secured credit facility to a catalog retailer, as lender in a secured bridge loan to a commercial real estate developer, as co-venturer in its aircraft leasing joint venture with Volito Aviation AB, in its

Contact Information [email protected] tel: +1 212.715.1780 fax: +1 212.715.1399

399 Park Avenue New York, NY 10022-4690

Practice Areas Financial Services Corporate and Securities Mergers, Acquisitions, and Strategic Alliances Telecommunications, Internet, and Media Private Equity Financing Transactions Business Restructuring Mergers, Acquisitions, and Divestitures Venture Capital Economic Recovery and the Changing Regulatory Landscape

Education JD, magna cum laude, New York University School of Law, 1992 AB, Brown University, 1985

Admissions New York

David S. BergArnold & Porter LLP 2

investment in a real estate and retail appraisal and liquidation firm, in its acquisition of CIT Group's micro-ticket leasing business, in its acquisition, and subsequent disposition, of Transamerica Corporation's European trailer leasing business, and numerous other minority and control investments and secured financings.

Represented Hellman & Friedman in a management buyout of Lincoln Financial Group's Delaware International Advisers, a UK-based investment management firm.

Represented Crédit Agricole Structured Asset Management in its acquisition of Ursa Capital LLC, a sponsor of funds of hedge funds and managed accounts, and Crédit Agricole Indosuez (now Calyon) in its sale of a hedge fund business to Neuberger Berman.

Represented Jackson National Life Insurance Company and Jackson Federal Bank in the sale of Jackson Federal to Union Bank of California.

Represented Instinet Corporation in its acquisitions of Pro Trader Group and Lynch, Jones & Ryan.

Represented Deutsche Telekom in its simultaneous acquisition of VoiceStream Wireless (now T-Mobile USA) and Powertel.

Financing Transactions Experience

Represented Goldman Sachs as agent in a senior secured credit facility to a catalog retailer, commercial real estate developer, and as agent in a debtor-in-possession financing for DVI, Inc.

Represented Hellman & Friedman in acquisition financing for the management buyout of Delaware International Advisors.

Professional and Community Activities

Member, Bar of New York

Presentations

David S. Berg, Alan Avery, Kevin F. Barnard and A. Patrick Doyle. "Emergency Economic Stabilization Act: Statutory Structure, the Implementing Regulations and Procedures, and Practice Implications of TARP" Arnold & Porter LLP, Financial Services Regulatory Roundtable, New York, NY, October 28, 2008.

Tab 3: Arnold & Porter LLP’s Financial Services Practice Group Overview

arnoldporter.com

FINANCIAL SERVICES

Widely acknowledged as one of the nation's premier financial services practices, the Arnold & Porter LLP team of over 30 lawyers provides US and international financial institution clients with comprehensive regulatory, litigation, and transactional services. The practice group handles complex regulatory and transactional issues and litigates cases involving the financial services industry at the administrative level and in the state and federal courts, including the US Supreme Court.

The practice group is recognized for developing innovative structures and novel solutions to regulatory issues, which allow clients to optimize their business strategy. Clients include a broad cross-section of bank holding companies, thrift institutions, foreign banks, insurance companies, securities firms, investment managers, electronic commerce businesses, and foreign governments.

Located primarily in Washington, DC, and New York, the practice group offers extensive experience in dealing with financial institutions and securities regulatory agencies, both federal and state. Several members of the practice group have served in senior positions at the key federal regulatory agencies. The team is supported by the full interdisciplinary resources of Arnold & Porter, including the corporate and securities, antitrust, tax, ERISA, trusts, environmental, and intellectual property practice groups.

Anti-Money Laundering and USA Patriot Act DefenseWe have been active in a variety of Patriot Act, anti-money laundering, and computer security matters for our financial services clients, including internal investigations, defense of enforcement actions and civil and criminal litigation, development and documentation of compliance programs, public policy issues, and regulatory counseling. Our information privacy and security team includes former federal prosecutors as well as former senior officials from the US Department of Justice, the Federal Trade Commission, the Central Intelligence Agency, the National Security Administration, the Department of Defense, and the US federal banking agencies.

Antitrust and CompetitionBank mergers are unique in the antitrust world. Both the process and standard of review are different from those followed in the antitrust review of mergers in other industries. We assist clients in analyzing potential transactions and shepherd them through the multiple agency review process. Historically, we have had one of the leading bank mergers and acquisition practices in the US. In this regard, for the last two decades, our team has been involved in shaping some of the most complex divestiture proposals ever designed to cure competitive concerns. Our lawyers were instrumental in preparing the Bank Mergers and Acquisitions Handbook, a leading reference manual devoted to this area of law. In addition, as a full-service firm, we are also able to draw upon the resources of our consistently top-ranked antitrust and competition practice in such instances as when a non-bank is being acquired and FTC issues are raised.

Charter Assessment

Financial ServicesArnold & Porter LLP 2

We regularly assist clients in assessing which is the optimal charter to operate under to best meet their business goals. We have extensive experience in advising clients on the advantages and disadvantages of the various types of charters—state bank charter, national bank charter, federal savings bank charter, or a specialized or limited purpose charter—and the implications of a charter choice on the parent holding company. As one of the few national firms with a separate, sophisticated thrift practice, we have been at the forefront in developing novel uses for thrift charters, especially by securities and insurance companies, in addition to advising our bank holding company clients on such matters. In the last several years, we have represented several of the nation's largest insurance and securities companies in forming federal savings banks in order to offer banking services to their customers.

Corporate Control Contests and Corporate GovernanceWe help financial institutions develop takeover defenses, handle unsolicited takeover attempts, and prepare shareholders' rights plans, and we advise on corporate governance and shareholder relations issues. We also represent acquirors in takeovers, offering special value in resolving regulatory and antitrust issues raised by proposed transactions.

Enforcement Counseling and DefenseWe assist individuals and institutions—and their boards of directors and holding companies—with the negotiation of consent agreements, memoranda of understanding and other written settlements, the development of compliance programs, and the defense of enforcement actions in administrative and judicial proceedings, and in addressing financial reporting and disclosure issues presented by agency enforcement initiatives. We also represent officers and directors, accountants, and other professionals in actions by receivers of insolvent financial institutions and in shareholder suits.

We are experienced in such currently high-profile issues as subprime lending, vendor management, privacy, nontraditional lending products and practices, money laundering, bank secrecy, and various activities considered inconsistent with safe and sound practices. In addition, we have substantial experience representing individuals and entities who are alleged to have the control provisions of the Change in Bank Control Act, the Bank Holding Company Act and the Savings and Loan Holding Company Act. Many of our attorneys have served as senior enforcement officials or on the enforcement staffs of the federal banking agencies, adding depth and insight to our representation of clients in enforcement matters.

Financial Products and ServicesHelping financial institutions enter new lines of business and structure new products and services is a major focus of our financial services practice. We represent clients in establishing, acquiring, and operating lines of business, including securities underwriting and dealing; brokerage; investment advising; mutual and hedge funds; pension servicing; credit, debit, and other card operations; funds and other money transmission; fiduciary and investment management activities; insurance; and leasing.

Broker-Dealer and Investment Advisers. We represent broker-dealers and investment advisers on regulatory matters related to their creation, expansion, services, and operations.

Private Investment and Private Banking. We represent numerous clients in the creation, operation, and offering of private investment funds, in establishing and structuring the management companies that operate private equity and venture capital funds, and in connection with portfolio investment transactions by the funds. We advise clients on new fund

Financial ServicesArnold & Porter LLP 3

development and structuring, required documentation, and compliance with state and federal securities and banking laws. We are also familiar with issues relating to specialized investment funds, such as SBICs, business development companies, collective investment funds, and employee securities companies. Drawing on the resources of our trust and estates, ERISA, and tax attorneys, our financial services team also represents clients in the bank regulatory and fiduciary law aspects of running a trust department.

Special Purpose Institutions. Our lawyers have helped create special purpose institutions designed to take advantage of favorable regulatory treatment and exploit niche markets. For example, we assist clients in establishing non-depository banks and thrifts created to offer trust services on a nationwide basis, as well as credit card and other limited purpose institutions.

Credit Card/Debit Card/Stored Value and Payments Systems. We assist clients in the card area with litigation, product development, and regulatory policy, and in negotiations of their processing, co-branding, and other agreements. Our clients include representatives of all parts of the credit and debit card industry, including one of the major credit card associations, card issuers, diversified financial services companies offering card products, merchant processors, merchants, and ATM and POS operators. We represent clients that operate other types of payment systems, as well. Clients in this area include funds and other money transmitting companies, a major government-sponsored enterprise, and merchants in a variety of online businesses. Our work for these organizations has included product development, assistance with mergers and acquisitions, advice on compliance with a variety of regulations, development and documentation of internal policies and procedures, documentation of system rules and policies for users, and various commercial, litigation, and regulatory matters.

Financial Services Consumer ProtectionWe advise clients, including regulated financial institutions, mortgage lenders, and other specialty consumer and commercial lending companies on various consumer credit issues. For example, we counsel clients on exporting interest rates and fees on loans and on the practical implications and limitations of this exportation power; we review client compliance with federal and state consumer credit laws, including the Real Estate Settlement Practices Act, the Truth in Lending Act, the Equal Credit Opportunity Act, the Home Mortgage Disclosure Act, and the Fair Credit Reporting Act, and undertake risk assessments of these areas; we structure lending programs to be compliant with the consumer lending laws; we defend clients that are sued for alleged violations of the consumer credit and consumer protection laws; and we advise clients regarding the agencies' published standards and statements of policy relating to lending practices in the consumer credit area.

In the fair lending area, we regularly assist clients in successfully resolving allegations of violations of the fair lending laws brought by the federal agencies in the earliest stages of the process, thereby avoiding costly and onerous settlements. We also advise clients on the rapidly changing area of subprime and “predatory” lending, and in providing affordable lending products consistent with the fair lending laws. We work with clients whose novel activities do not fit within the traditional banking model to develop innovative strategic plans to satisfy their Community Reinvestment Act (CRA) responsibilities and have advised investors in and organizers of community development-focused banks and CDCs. We are also experienced in addressing CRA protests raised against clients by parties challenging merger and acquisition transactions.

Financial Services LitigationFinancial services clients benefit from our extensive firmwide litigation resources and experience. Professionals in each of our offices regularly handle disputes on behalf of financial services clients,

Financial ServicesArnold & Porter LLP 4

whether arising in a civil litigation/class action context, mediation and arbitration, or in a civil enforcement context. Our clients include financial services companies, banks, thrifts, officers and directors, law firms, accounting firms, other experts and consultants, and parties having dealings with failed institutions. Our representations have included litigation involving issues of federal preemption of state laws; litigation against the federal government for losses caused by changes in legislation that made so-called "supervisory goodwill" ineligible for treatment as regulatory capital; litigation defending financial services companies against alleged violations of consumer protection laws; litigation concerning grants and denials of permission to engage in nonbanking activities and in administrative enforcement proceedings; litigation over commercial transactions, employment issues, and fiduciary relationships of financial services firms; and litigation defending a card association in various antitrust suits filed by merchants and rival card associations.

Our firm’s experience includes client representation in lawsuits and investigations stemming from consumer mortgage lending. The firm also has experience in lender liability litigation arising from, among other things, loan commitments and modifications, alleged untimely or improper disbursements of loan proceeds, alleged erroneous valuation of collateral and of borrower’s ability to pay, as well as usury and bad faith claims. We have substantial experience in litigations with respect to securitization issues in state, federal, and bankruptcy courts involving prime, non-prime, and subprime assets ranging from consumer loan assets to audio-video equipment, which raised a number of significant Uniform Commercial Code (UCC) and secured lending issues. The firm has also represented clients in disputes with respect to investor suitability issues and purported unfair and deceptive business practices arising in the consumer and commercial lending arenas.

Our litigators also have considerable experience in complex securities litigation, demonstrated by the lead role we played in the recent landmark case, Stoneridge Investment Partners, LLC v. Scientific-Atlanta, Inc. 128 S. Ct. 761 (2008), in which the Supreme Court rejected the theory of “scheme liability”and held that a secondary actor cannot be liable unless it has made deceptive statements on which investors have relied.

We regularly handle SEC investigations and enforcement actions, and have represented major financial institutions in SEC investigations arising out of significant corporate governance and related party issues. We also defend financial services companies in class actions alleging securities fraud and related securities law violations.

Financial Services Preemption LitigationWe have played a prominent role in much of the most significant federal banking litigation of the past three decades. For a number of years, Arnold & Porter LLP has been actively involved in challenging, on grounds of federal preemption, state and local efforts to supervise and regulate activities of federally chartered financial institutions. The firm in recent years has developed considerable experience in representing national banks and federal savings banks in a series of cases involving preemption of state law by the National Bank Act (NBA) and the Home Owners' Loan Act (HOLA). In a series of cases, the Arnold & Porter team, including lawyers from the firm's Washington, DC, New York, and Los Angeles offices, has achieved major victories for national banks, savings and loan institutions, and credit unions threatened with overreaching state and local actions. With a growing number of states and localities seeking to control financial institutions' activities, these issues have become increasingly important to financial institutions nationwide.

Financial ServicesArnold & Porter LLP 5

Examples of the cases in which we have recently achieved federal banking law preemption victories include:

State Farm Bank, F.S.B. v. Reardon, 539 F.3d 336 (6th Cir. 2008) (obtained declaratory and injunctive relief from enforcement of Ohio's mortgage-broker licensing laws against agents of federal savings bank)

Rose v. Chase Bank USA, N.A., 513 F. 3d 1032 (9th Cir. 2008), aff'g 396 F. Supp. 2d 1116 (C.D. Cal. 2005) (obtained dismissal of class action complaint alleging violation of state statutory disclosure requirements for access checks and unfair and deceptive practices)

Consumers Against Unfair Business Practices (Miller) v. Bank of Am., N.A. (USA), 170 Cal. App. 4th 980 (2009) (obtained dismissal of class action complaint alleging national bank's collection of finance charges and late fees when credit card payment date fell on weekend or holiday violated state "holiday" statutes and constituted unlawful, unfair and deceptive practices)

Augustine v. FIA Card Servs., N.A., 485 F. Supp. 2d (E.D. Cal. 2007), appeal docketed (9th Cir. No. 07-16751) (obtained dismissal of class action complaint alleging violation state unfair and deceptive practices in that national bank failed to give notice to borrower before raising credit card interest rate due to borrower default)

Montgomery v. Bank of America Corp., 515 F. Supp. 2d 1106 (C.D. Cal. 2007) (obtained dismissal of class action complaint alleging unfair and deceptive trade practices based upon the amount of a national bank's insufficient funds fees and the manner in which the fee amount was disclosed to customers)

State Farm Bank, F.S.B. v. Burke, 445 F. Supp. 2d 207 (D. Conn. 2006) (obtained injunctive and declaratory relief from enforcement of state mortgage broker licensing laws against agents of a federal savings bank)

Silvas v. E*Trade Mortgage Corp., 421 F. Supp. 2d 1315 (S.D. Cal. 2006) (obtained dismissal of complaint alleging violations of Truth in Lending Act and state unfair and deceptive practices laws), aff'd 514 F.3d 1001 (9th Cir. 2008)

Bank of Am., N.A. v. McCann, 444 F. Supp. 2d 1227 (N.D. Fla. 2006) (obtained injunctive relief under the visitorial powers provision of the National Bank Act preventing state court lawsuit by qui tam plaintiffs alleging violation of state escheat laws)

Am. Bankers Ass'n v. Lockyer, 239 F. Supp. 2d 1000 (E.D. Cal. 2002) (obtained summary judgment declaring that state disclosure statute requiring minimum payment disclosures was preempted)

Parks v. MBNA America Bank, N.A., et al., Orange Superior Court, Case No. 04CC00598 (June 17, 2008) (obtained judgment on the pleadings for national bank in class action alleging violation of state disclosure statute), appeal docketed (Fourth App. Dist., Div. Three, No. G040798)

Bank One Del., N.A. v. Wilens, 2003 WL 21703629 (C.D. Cal. July 7, 2003) (obtained injunctive relief barring state court suit alleging violations of state disclosure and unfair and deceptive practices laws)

Armanini v. Bank One, Del., N.A., Orange County Super. Ct., No. 03 CC 00255 (Feb. 3, 2005) (obtained summary judgment for national bank in class action alleging violation of state access check disclosure requirements and unlawful, unfair, and deceptive practices). We also recently

Financial ServicesArnold & Porter LLP 6

achieved a grant of review by the New York Court of Appeals of Spitzer v. Applied Card Systems, 7 A.D.3d 104 (NY 2005), in order that we may appeal our Truth in Lending Act preemption defenses.

In addition, we have filed amicus briefs on behalf of the banking industry arguing federal banking law preemption in numerous cases, including:

Watters v. Wachovia Bank, N.A., 127 S. Ct. 1559 (2007) (NBA preemption)

The Clearing House Assn., L.L.C. v. Spitzer, 510 F.3d 105 (2d Cir. 2007) (visitorial powers),aff'g in part, 394 F. Supp. 2d 620 (S.D.N.Y. 2005), and Office of the Comptroller of the Currencyv. Spitzer, 396 F. Supp. 2d 383 (S.D.N.Y 2005), cert. granted (January 16, 2009 No. 08-453).

Pacific Capital Bank, N.A. v. Connecticut, 542 F.3d 341 (2d Cir. 2008) (NBA preemption), aff'g2006 WL 2331075 (D. Conn. 2006).

Miller v. Bank of Am. N.T. & S.A., 51 Cal. Rptr. 3d 223 (Cal. Ct. App. 2006) (NBA preemption),review granted (March 21, 2007 No. S149178).

Am. Fin. Servs. Ass'n v. City of Oakland, 34 Cal. 4th 1239 (2005) (NBA and HOLA preemption)

Am. Bankers Assn. v. Gould , 412 F.3d 1081 (9th Cir. 2005) (Fair Credit Reporting Act preemption

Financing Transactions and Capital MarketsWe advise both domestic and international financial institutions on a wide variety of financing opportunities, including securities offerings, leveraged buyouts, lending activities, and debt restructuring. Our attorneys are skilled at structuring securities offerings to ensure favorable regulatory capital treatment. We represent both issuers and underwriters of hybrid capital instruments and other capital markets transactions.

Hedge Fund and Private Equity Investment in Financial InstitutionsWe have considerable breadth and depth of experience in counseling hedge and private equity funds and their investment advisors in working through the implications of the rules and policies that apply to both controlling and non-controlling investments in financial institutions and their holding companies, including the recent policy statements from the FDIC and Federal Reserve on private capital investments in banks and bank holding companies. Our experience includes structuring investment vehicles to make such investments and the forms in which such investments will be made, negotiating the relevant documentation, and working with the funds and the regulators in either obtaining the appropriate regulatory approvals for such investments, or in addressing any presumption of control by negotiating "custom tailored" passivity agreements or rebuttal of control agreements that may be required to ensure that such investment remain passive.

International and Foreign BankingWe actively advise foreign banks on entry into the US and the activity of their US offices, as well as regulatory requirements, including comprehensive consolidated supervision determinations, new products (in securities, asset management, derivatives, insurance, and venture capital areas), capital issuances and other expansion opportunities. We also assist US financial services firms in expanding banking activities internationally through the establishment of foreign branches, the acquisition of subsidiary banks, and the expansion of foreign investments in established and emerging markets. In addition to commercial clients, we advise foreign governments and agencies on regulatory issues

Financial ServicesArnold & Porter LLP 7

involving the US. With attorneys from our international practice, we advise foreign governments with respect to their dealings with the Federal Reserve and other regulators and international organizations located in Washington, DC, as well as their commercial dealings with banks and securities firms.

Legislation and Public PolicyWe also represent individual institutions and trade associations on matters relating to federal financial regulatory legislation and policy. We develop legal positions for clients on many of the major public policy issues affecting financial institutions. Working with our legislative and public policy colleagues, we monitor legislative developments that concern the financial services industry, draft legislative proposals, provide legal and technical support for institutions commenting on proposed legislation, and work closely with congressional and federal agency staffs.

Mergers, Acquisitions, and Strategic AlliancesOur firm historically has had one of the leading bank mergers and acquisitions practices in the US. Our attorneys are experienced with sophisticated merger techniques and skilled in developing related tax, antitrust, and regulatory strategies. Our work includes structuring and negotiating acquisitions of all types within the financial services industry, including cross-industry acquisitions, and strategic alliances among financial services companies and other entities. We also perform targeted due diligence to assist potential acquirors in regulatory risk assessment.

Privacy and Data SecurityWhat financial services firms know about their customers has become a heavily regulated aspect of doing business. We have been active for two decades in representing our financial services clients on matters relating to customer privacy.

In this regard, we counsel financial institutions on the rapidly growing body of federal and state privacy laws affecting their operations, including developing privacy notices, negotiating data protection agreements with business partners, and setting up internal databases to ensure appropriate safeguards on access to, and disclosure of, personal information. We also work with clients on the privacy rules adopted pursuant to the HIPAA and on international privacy requirements, including the restrictions imposed by the Data Protection Directive of the EU. Our privacy experience includes protection of financial information, including electronic data. As a complement to this advice, we work closely with clients on the security aspects of information privacy, which involve technical considerations that are integral to any program of privacy compliance.

Regulatory and Strategic CounselingWe counsel clients on complicated issues arising under the statutes, regulations, and proposed regulations governing the financial services industry. We also counsel clients on the application of agency guidance documents and statements of policy on a wide range of issues, particularly in the areas of evolving regulatory scrutiny, in order to assist clients in identifying significant legal, supervisory, and reputational risks, and implementing systems and controls tailored to address those risks.

Based on our extensive experience, we often propose changes to agency regulations and request interpretations of existing or proposed agency rules. These efforts have led to novel legal interpretations that have enabled our clients to offer new products and services, and to expand the scope of their operations.

Tab 4: Arnold & Porter LLP’s Corporate and Securities Practice Group Overview

arnoldporter.com

CORPORATE AND SECURITIES

With diverse experience in the US and abroad, Arnold & Porter LLP’s corporate and securities team provides premier services to a wide variety of corporate clients, handling matters from complex, high-profile mergers and acquisitions involving multinational FORTUNE 500 companies to vital business transactions for rising mid-market companies, start-ups, and entrepreneurs. We also have one of the world’s most sophisticated and respected sovereign finance practices, handling multibillion dollar transactions throughout South America, Asia, and the Middle East.

Our corporate and securities group, based in our US and London offices, helps clients meet their goals by effectively executing both routine corporate matters and high-stakes transactions that require innovative thinking and novel structures, representing issuers, underwriters, acquirers, targets, financial institutions, borrowers, governments, governmental entities, private equity and venture capital firms, and investment funds, among others. In international transactions, our team provides a bridge between diverse legal and business cultures and efficiently completes transactions involving international legal systems.

Our clients often look to us to provide legal counsel with respect to a multitude of legislative, regulatory, and governance issues that draw on our corporate experience. With one of the nation’s leading regulatory practices, we offer clients in highly regulated industries a valuable combination of regulatory and corporate resources centered in the nation’s capital. In addition, we offer a full range of complementary resources, including respected experience in areas such as tax, financial institutions, antitrust, telecommunications, intellectual property, real estate, employee benefits, government contracts, food and drug law, environmental law, and bankruptcy.

Business RestructuringOur restructuring work includes M&A, divestitures, debt and equity issuances and exchanges, refinancings, legacy costs reductions, and commercial contract renegotiations. We represent clients in negotiating plans of reorganization in complex Chapter 11 cases, in buying or selling assets and businesses through “Section 363 sales” outside of a Chapter 11 plan, and in cross-border insolvencies. Our US and international clients include large corporate debtors, private equity firms, hedge funds, lenders, creditors, and other entities seeking opportunities in Chapter 11 cases, across a diverse range of industries, including airlines, energy production and distribution, manufacturing, real estate, financial institutions, communications, consumer goods, technology, insurance, and publishing.

Our finance, bankruptcy, and restructuring teams stand ready to advise clients dealing with financially distressed businesses. We represent creditors and debtors in bankruptcy and insolvency proceedings, as well as in connection with workouts and out-of-court debt restructurings. Our attorneys use a multidisciplinary approach, which draws upon the experience of attorneys in other practice areas, to offer creative, practical, and efficient solutions to problems faced by our clients. Our attorneys have

Corporate and SecuritiesArnold & Porter LLP 2

negotiated and documented forbearance agreements, debtor-in-possession financings, restructuring agreements, and alternative collateral arrangements to support problem loans.

Although we prefer a collaborative approach to the restructuring process, we are comfortable initiating and defending litigation when necessary to achieve our clients’ business objectives.

Capital Markets TransactionsOur team represents issuers, underwriters, security holders, and indenture trustees in the full range of public offerings and private placements of debt, equity, and hybrid securities. Our work includes initial public offerings, SEC-registered and global offerings, Rule 144A and Regulation S debt and equity offerings, commercial paper programs, Eurobond and other foreign offerings, municipal bond financings, medium-term note programs, and asset-backed securities offerings.

Our lawyers serve as counsel in capital-raising and financing transactions for, among others, financial institutions, international banks, telecommunications companies, computer software and systems companies, biotechnology firms, real estate investment trusts, specialty finance companies, and other businesses. We represent both large and small institutions in the US in their capacity as underwriters in public offerings and as initial purchasers or placement agents in private placements.

Our capital markets transactional capacity includes the ability to offer regulatory, corporate, securities, and tax law experience in structuring new securities products, as well as in advising on regulatory compliance and marketing issues from the perspective of underwriters or placement agents, broker-dealers, and issuers. We have extensive experience in advising clients with respect to the SEC registration statement filing and review process and the listing of securities and depositary receipts on major securities exchanges in the US, London, Luxembourg, and elsewhere.

Corporate Governance, SEC Reporting and ComplianceWe have extensive experience in a wide variety of corporate governance matters, frequently serving as counsel to boards of directors, independent directors, and special committees in connection with matters such as financial reporting issues, internal corporate investigations, change of control issues, and similar matters. We counsel clients on a variety of topics, including board fiduciary duties; board and committee composition, structure, and process; Sarbanes-Oxley Act compliance; executive compensation disclosure and strategy; stockholder communications; and proxy contests and other contested and uncontested changes of control.

As principal outside counsel for several FORTUNE 500 companies, we handle corporate compliance, corporate governance, risk management, business ethics, and corporate social responsibility matters. We also help our clients in developing, implementing, and enhancing corporate compliance programs based on the standards established in the US Federal Sentencing Guidelines and in drafting the codes of conduct, various substantive law practice guides, training programs, and charters. In addition, we help clients develop Regulation FD and communications policies and often advise on sensitive disclosure matters. When required, we represent clients in investigations by the Securities and Exchange Commission and the Department of Justice and special investigations by corporations with respect to corporate practices regarding the granting and exercise of stock options. We counsel clients regarding issues implicated by options and other equity grants, including accounting issues, corporate governance issues, civil and criminal enforcement issues, disclosure issues, and emerging best practices.

Corporate and SecuritiesArnold & Porter LLP 3

Financing TransactionsWe represent US and international lenders and borrowers in structuring, negotiating, and documenting all types of secured and unsecured financing transactions, including public and private offerings of debt securities, commercial lending transactions, leasing transactions, and restructuring transactions. We advise major insurance companies, banks, private equity funds, and other institutional lenders, as well as US and international companies in a variety of industries, including computers, communications, construction, financial services, real estate, airlines, energy, mining, healthcare, biotechnology, pharmaceuticals, resorts, printing, newspapers, and consumer products.

Our team prepares and negotiates commercial loan documentation on behalf of lenders and borrowers in connection with all types of commercial lending structures, including participated and syndicated facilities, single- and multiple-borrower facilities, domestic and cross-border loans, debtor-in-possession financings, and asset-based lending transactions. Our commercial lending work covers senior, mezzanine, and subordinated facilities, and we routinely advise borrowers and lenders on inter-creditor arrangements, guarantees, letters of credit, and liens on all types of collateral, including intellectual property, aircraft, equipment, inventory, accounts receivable, certificated and uncertificated securities and investment property, insurance policies, and government contracts. Our commercial lending practice also extends to specialized lending arrangements, including conduit loan programs, warehouse lines of credit, and factoring loans. We work closely with attorneys in our private equity and venture capital practice to develop financing solutions for leveraged buyouts and other acquisition transactions on behalf of private equity and other investment fund clients, as well as their portfolio companies.

We advise our corporate clients with respect to lease financing transactions of equipment and other capital assets. Our work in the lease financing area covers true leases, finance leases, synthetic leasing arrangements, and leveraged leases. In addition, our project finance attorneys offer significant experience with project finance transactions, both US and international. Our project finance experience includes representation of private developers, commercial lenders, export credit agencies, multilateral development banks, and contractors, as well as transactions conducted with foreign government representatives and other participants in a variety of industries.

Hedge Funds and DerivativesOur hedge funds team is highly skilled in the structuring and syndication of US and non-US alternative investment funds, and has significant experience in establishing a broad range of alternative investment funds encompassing extensive investment strategies and styles, including hedge funds and funds of funds, as well as privately and publicly offered commodity pools.

Representation includes advice regarding selection of jurisdiction; structuring and distribution issues; allocations of assets to outside advisors and funds; and the establishment of prime broker, ISDA, and other over-the-counter counterparty trading relationships. We also have experience in the creation of structured notes, over-the-counter derivatives, and other off-exchange products. In addition, we have significant experience in strategic corporate transactions, such as acquisitions and divestitures of equity interests in hedge fund managers.

Our clients include US and non-US banks, brokerage firms, investment advisers, commodity trading advisors, commodity pool operators, and other market participants.

Our attorneys have regularly interfaced with officials and staff at the Securities and Exchange Commission (SEC), the Financial Industry Regulatory Authority (FINRA), the Commodity Futures

Corporate and SecuritiesArnold & Porter LLP 4

Trading Commission (CFTC), and the National Futures Association (NFA). We have designed and implemented compliance and supervisory policies and procedures; addressed issues arising out of broker-dealer and investment adviser registration and regulation in hedge fund offerings; facilitated the acquisition and utilization of exchange memberships; and assisted in the creation and registration of derivative, exchange-listed, and off-exchange products.

Complementing our core hedge funds team and providing a full client-service team approach, our tax and ERISA teams support our hedge funds attorneys with respect to tax and ERISA planning and structuring for collective investment vehicles and their participants, and deferred compensation arrangements for fund managers and other matters. Hedge fund clients also benefit from our firm's extensive litigation resources and experience, where our litigation attorneys have significant experience representing hedge fund managers, brokerage firms, investment advisers, commodity trading advisors and pool operators, and other market participants in regulatory investigations before the SEC, FINRA, and CFTC, in arbitrations before the NFA and other tribunals, and in US federal and state courts.

Mergers, Acquisitions, and DivestituresOur team advises US and international companies and private equity and venture capital funds in complex domestic and cross-border merger, acquisition, and divestiture transactions, including public company mergers, strategic acquisitions and divestitures of private companies, and leveraged buyout transactions. With offices in the US and abroad, we advised clients on several of the largest and most complex transactions of the last several years, including Finmeccanica S.p.A.’s acquisition of DRS Technologies, Inc., CSX’s sale of its global port assets to Dubai Ports International, US Airways’merger with America West, Boston Scientific’s acquisition of Guidant, and BAE’s acquisitions of Armor Holdings and United Defense Industries. At the same time, the majority of the transactions we have closed are in the middle market, where we provide a cost-effective alternative to our clients who are looking for practical, solution-oriented counsel.

Our corporate attorneys have particularly deep experience in transactions in regulated industries, where the breadth of our regulatory practices complements our core merger and acquisition experience to provide a strategic advantage to our clients. Because of our firm’s extensive regulatory practice, our corporate merger and acquisition attorneys are familiar with a myriad of regulatory issues that can arise in merger and acquisition transactions and work efficiently to address those issues with our regulatory colleagues while remaining attentive to our client’s business objectives. We have completed numerous transactions in a number of regulated industries including financial services and banking; government and defense contracting, including acquisitions of US government contractors by international companies; telecommunications; biotechnology and life sciences; and transportation.

Our transactional teams assist clients in all phases of their acquisitions, from letters of intent, to due diligence, to the negotiation and drafting of transaction documents, through the various regulatory approval processes, and in the planning and implementation of post-closing integration activities. While the core of our merger and acquisition work is based in our corporate practice, our transactional teams include our colleagues throughout many of our practice areas, including intellectual property, employee benefits and executive compensation, employment, tax, government contracts and national security, financial services, environmental, real estate, antitrust and competition, food and drug and healthcare, and litigation. Our corporate attorneys work closely with our attorneys in other practice areas to ensure a coordinated, integrated approach to accomplish our clients’ legal and business goals.

Corporate and SecuritiesArnold & Porter LLP 5

Private EquityOur international private equity practice focuses on representing private equity funds in leveraged acquisitions and subsequent dispositions of portfolio companies, as well as representation of portfolio companies in general corporate and transactional matters. We also have an active fund formation practice and regularly counsel funds on regulatory compliance, tax, and fund management issues. Five of the top 10 private equity funds and business development companies based in the Washington, DC region use Arnold & Porter as principal outside counsel, as well as funds throughout the US, Europe, and Japan. Our private equity team has extensive experience in handling transactions in numerous industries. As a full service firm headquartered in Washington, DC, we have developed special experience in providing due diligence and corporate transactional services to private equity funds investing in regulated industries, such as government contracting, telecommunications, financial services, and energy.

Sovereign FinanceOur firm has a long and distinguished history of advising international governments in financial transactions and related issues and undertakings. We have been active in representing the ministries of finance and central banks of many sovereign governments since before the original debt crisis of the 1980s and have helped our clients design and implement novel and complex financing structures to overcome their liquidity and debt problems. We have represented and advised a number of the world’s most prominent multilateral financial institutions, including the World Bank, the Inter-American Development Bank, the International Finance Corporation, OPIC, the European Bank for Reconstruction and Development, and the Bank for International Settlements, in significant financial transactions and other novel legal assignments.

We assist and advise our sovereign clients in numerous financial transactions, including offerings of debt and equity securities, complex exchange offers for securities and cash tender offers for securities, derivative transactions, and project and syndicated financing. We have also had extensive experience in dealing with multilateral and bilateral lenders on behalf of sovereign and private sector borrowers, as well as representation of multilateral lenders and institutions in connection with such types of transactions. We also assist governments in a variety of privatization transactions, specifically in telecommunications, banking, chemicals, airport services, and other sectors.

Venture CapitalOur venture capital practice includes representation of both investors and early stage companies that are venture-backed or seeking venture capital investment. Our clients include very early stage companies that are seeking their seed round of venture capital investment and later stage companies that are seeking expansion capital in advance of an initial public offering or transformational transaction. In addition to our corporate capabilities, we have a leading intellectual property practice that provides expert advice to our early stage clients on how best to protect and license their patents and other intellectual property as they grow their business. We have experience in all of the major industry sectors attracting venture capital, including software products and services, equipment manufacturing, biotechnology, nanotechnology, and telecommunications.

Tab 5: Arnold & Porter LLP Advisory,

“The Federal Reserve Board Policy Statement on Equity Investments Relaxes Restrictions on Minority Investments in Banks and BankHolding Companies,” September 2008

SEPTEMBER 2008

Washington, DC+1 202.942.5000

New York+1 212.715.1000

London+44 (0)20 7786 6100

Brussels+32 (0)2 517 6600

Los Angeles+1 213.243.4000

San Francisco+1 415.356.3000

Northern Virginia+1 703.720.7000

Denver+1 303.863.1000

This summary is intended to be a general summary of the law and does not constitute legal advice. You should consult with competent counsel to determine applicable legal requirements in a specific fact situation.

arnoldporter.com

ARNOLD PORTER LLP

C L I E N T A DV I S O RY

Commitment | exCellenCe | innovation

ThE FEDERAL RESERVE BoARD PoLiCY STATEMENT oN EquiTY iNVESTMENTS RELAxES RESTRiCTioNS oN MiNoRiTY iNVESTMENTS iN BANkS AND BANk hoLDiNg CoMPANiESOn September 22, 2008, the Federal Reserve Board issued its long-awaited Policy Statement on minority equity investments in banks and bank holding companies.1 It was anticipated that this Policy Statement would loosen certain of the Federal Reserve’s policies with respect to these investments in order to encourage private equity investment in banks and bank holding companies struggling with losses in the current economic environment. And indeed, the Policy Statement relaxes certain long-standing Federal Reserve policies on non-controlling investments, including allowing investors:

to make minority investments of up to 33% of the target’s total equity without ��being considered in control, if certain conditions are met;

to have one board seat on the target’s board, and up to two board seats on the ��target’s board under certain conditions;

to obtain updates from the target’s management on key issues and to participate ��in discussion of these issues with the target’s management and board of directors; and

to have additional business relationships with the target than previously allowed, ��if the investment is closer to 10% than to 25% of the total voting securities of the target.

However, the Policy Statement does not address control issues present in so-called “club” deals, where several private equity firms invest together, each taking a non-controlling interest in the target institution. It also does not address attribution and other issues arising under any of the controlling investments being proposed by private equity funds through alternative investment vehicles or so-called “silo” fund structures. Many private equity funds had hoped for liberalization of control standards to allow investments using these structures. While the lack of guidance in these areas may result in continued reluctance on the part of private equity firms from making control investments in the banking sector, the revised standards expressed in the Policy Statement are likely useful to those investors interested

1 http://www.federalreserve.gov/newsevents/press/bcreg/bcreg20080922b1.pdf

ARNOLD PORTER LLP

2The Federal Reserve Board Policy Statement on Equity Investments Relaxes Restrictions on Minority Investments in Banks and Bank Holding Companies

Commitment | exCellenCe | innovation

in making non-controlling investments in banks and bank holding companies.

LEgAL FRAMEWoRkUnder the Bank Holding Company Act, an entity is considered to be in control of a bank or a bank holding company if the entity, among other things:

acquires direct or indirect control of 25% or more of any 1. class of voting securities of the bank or bank holding company;

controls the election of a majority of the board of director 2. of the bank or bank holding company; or

has the power to directly or indirectly exercise a 3. controlling influence over the management or policies of the bank or bank holding company.

The Policy Statement focuses on the ability of an investor to “exercise a controlling influence over the management or policies of the bank or bank holding company.” In the past, the Board has drawn fairly strict limits on what could be considered exercising such a controlling influence if an investor acquired between 10% and 24.9% of the voting shares of a bank or bank holding company and wanted to remain passive. These strict limits were set forth in a 1982 policy statement on non-voting equity investments, as well as in certain passivity commitments (popularly known as “Crownx” commitments) that the Board required of investors making such non-controlling equity investments. Generally, these limits included:

Limiting total investment in a bank or bank holding ��company to no more than 24.9% of the total equity of the target;

Prohibiting board representation once the investment ��reached 15% of the voting securities of the target, and limiting an investor to one board member for investments below that level;

Limiting an investor’s ability to influence any policy or ��operation of the target by prohibiting the investor from having any input into any business decisions, or from not using their investment stake to influence decisions

by, for example, threatening to sell the stake or soliciting proxies from other shareholders; and

Limiting business relationships with the target to small ��and routine business such as maintaining a deposit account of US$500,000, and having vendor contracts (although existing relationships generally were grandfathered).

The Policy Statement relaxes each of these limitations, and in doing so, reflects a willingness on the part of the Board to accommodate a wider range of investment structures than has been permitted in the past.

Specifically, the Policy Statement:

Allows total passive investments in banks and 1. bank holding companies of up to 33% of total equity. Under the Policy Statement, the Board has indicated that it would permit an investor to acquire a combination of voting and nonvoting shares, that when aggregated, would represent less than one-third of the total equity of the target bank or bank holding company, provided that the investor does not acquire 15% or more of any class of voting securities, and the investor would hold less than one-third of any class of voting securities even assuming all convertible nonvoting shares held by the investor were converted. As in previous cases, the Policy Statement notes that the Board expects that any non-voting convertible shares held by a passive investor would remain non-voting in the hands of that investor and may only be transferred (i) to an affiliate of the investor or to the target; (ii) in a widespread public offering; (iii) in transfers in which no transferee (or group) would receive 2% or more of any class of voting securities; or (iv) to a transferee that already controls more than 50% of the voting securities of the target. Of course, any passive investor would continue to be restricted to acquiring only up to 24.9% of any class of voting securities without being considered in control of the target bank or bank holding company. Allows a private equity investor to have up to 2. two directors on a target’s board. Under the Policy Statement, a minority investor may name a director

ARNOLD PORTER LLP

3The Federal Reserve Board Policy Statement on Equity Investments Relaxes Restrictions on Minority Investments in Banks and Bank Holding Companies

Commitment | exCellenCe | innovation