nigeria agenda 2050: draft final report on …

TRANSCRIPT

8/21/2020

NIGERIA AGENDA 2050: DRAFT FINAL REPORT ON DEVELOPMENT OF A MACROECONOMIC FRAMEWORK USING A SYSTEM DYNAMICS MODEL INSPIRED BY THE iSDG MODEL

REPORT OF iSDG TEAM OF THE MODELLING GROUP

NSF DEVELOPMENTS LTD DEVELOPMENT PLANNING, MANAGEMENT AND TRAINING CONSULTANTS

21 August 2020

Contributors: 1. Barth T. Feese – Team Lead/Lead Consultant 2. Prof. Jean-Paul Cleron – Chief Modeller/Analyst 3. Dr. Charles Nche – Modeller/Analyst

1

EXECUTIVE SUMMARY

Nigeria is leading the way in Africa’s return to the era of development planning. This is evident

in both previous efforts since 2000 and present strides towards having successor plans for the

Economic Recovery and Growth Plan (ERGP) 2017-2020, and the Nigeria Vison 20:2020,

both of which come to an end in 2020. To this end the country has decided to use the Input-

Output model and the econometric model in developing a macroeconomic framework to guide

the preparation of the Medium Term National Development Plan (MTNDP), 2021-2025; while

the Computable General Equilibrium model and the System Dynamics based model inspired

by the integrated Sustainable Development Goals (iSDG) model are being used for a

perspective plan – the Agenda 2050, Nigeria’s 30-year Long Term National Development Pan

(LTNDP). This report highlights the background, approach, methodology and tools used in

developing the macroeconomic framework for the Agenda 2050. It examines the modelling

steps undertaken, the model structures that determine the long-term behaviour of the complex

system, which is Nigeria, and the interactions of different parts within the system. Finally, the

report presents an analysis of the preliminary results of simulations for two scenarios – i)

continuation of the present situation (base scenario) and ii) projections of a better future for

Nigeria (best scenario) over the next 30 years; and the assumptions underlying the simulations.

It must be emphasized that the purpose of long-term models cannot be to generate accurate

predictions. The uncertainties are far too many and the range of possibilities much too wide.

Rather, long-term models are useful to indicate trends or directions of change, shapes being

more important than the actual data which constitute them. To invent a better future for Nigeria,

eight assumptions were changed from the base case, one at a time, to simulate the best-case

scenario. These include: i) propensity to save increases over time, ii) government consumption

(the cost of governance) as a proportion of revenue falls over time, iii) government investment

(capital expenditure) as a proportion of revenue increases over time, iv) a higher initial, then

growing share of public domestic debt, v) interest rate on domestic debt falls, vi) subsidies on

petroleum products and electricity are completely removed by 2026, vii), productive capital is

better managed and better maintained, viii) net oil price and exports improve. Below is a

summary of the eight assumptions underlying the base case and best-case scenarios:

Assumption 2021 2026 2031 2036 2041 2046 2051

Propensity to save Base 14.0% 14.0% 14.0% 14.0% 14.0% 14.0% 14.0%

Dmnl 1st intermediate

simulation.

Propensity to save assumed to

increase over time Best

14.0% 14.5% 15.0% 16.0% 18.0% 21.0% 25.0%

1.Government

propensity to consume

Base 70.0% 68.0% 65.0% 60.0% 55.0% 49.0% 40.0%

Dmnl 2nd intermediate

simulation.

Government consumption falls

overtime Best

70.0% 68.0% 63.0% 56.0% 44.0% 33.0% 25.0%

2.Government

propensity to invest

Base 30.0% 30.0% 30.0% 30.0% 30.0% 30.0% 30.0%

Dmnl 3rd intermediate

simulation.

Government investment

increases over time

Best 30.0% 31.0% 34.0% 38.0% 44.0% 53.0% 63.0%

3.Share of domestic debt

Base 50.0% 50.0% 50.0% 50.0% 50.0% 50.0% 50.0%

Dmnl 4th intermediate

simulation. Higher share of domestic

debt Best 65.0% 66.0% 68.0% 71.0% 74.0% 80.0% 85.0%

4.Interest rate on domestic debt Base

7.8% 7.8% 7.8% 7.8% 7.8% 7.8% 7.8% 1/year 5th intermediate

simulation. Lower

2

Best 7.8% 7.5% 7.2% 6.8% 6.4% 5.2% 3.0%

interest rate on domestic debt

5.Average US$

subsidy per litre

Base 0.0526 0.0480 0.0440 0.0380 0.0290 0.0170 0.0000

US$/l

6th intermediate simulation. No more subsidies

after 2025

Best 0.0526 0.000 0.000 0.000 0.000 0.000 0.000

Average US$ subsidy per kWh

Base 0.0395 0.0360 0.0335 0.0290 0.0240 0.0140 0.0000

US$/kWh

Best 0.0395 0.000 0.000 0.000 0.000 0.000 0.000

6.Average capital lifetime Base

25 Year 7th intermediate

simulation. Capital better managed,

last longer Best 30

7.Net oil price Base 15 20 25 25 22 18 15

US$/bbl 8th and last

simulation: best case. Changing

hydrocarbon market conditions

Best 5 35 35 35 30 25 20

8.Net oil export Base 400 700 700 700 650 550 450 Mbbl/year Best 400 700 700 600 500 450 450

One of the most important findings from the results of the simulations indicate that Nigeria

will be placed on the path of sustained economic growth, if a consistent and deliberate long-

term (30-year) implementation of policy intervention packages is done as outlined in the best-

case scenario shown above. From the graph below, economic growth approaches 7% by 2050.

ECONOMIC GROWTH (%)

Fractional change in productive capital

.07

.0525

.035

.0175

0

2021 2025 2029 2033 2037 2041 2045 2049

Time (Year)

1/Y

ear

Fractional change in productive capital : AGENDA 2050 BASE

Fractional change in productive capital : AGENDA 2050 BEST

3

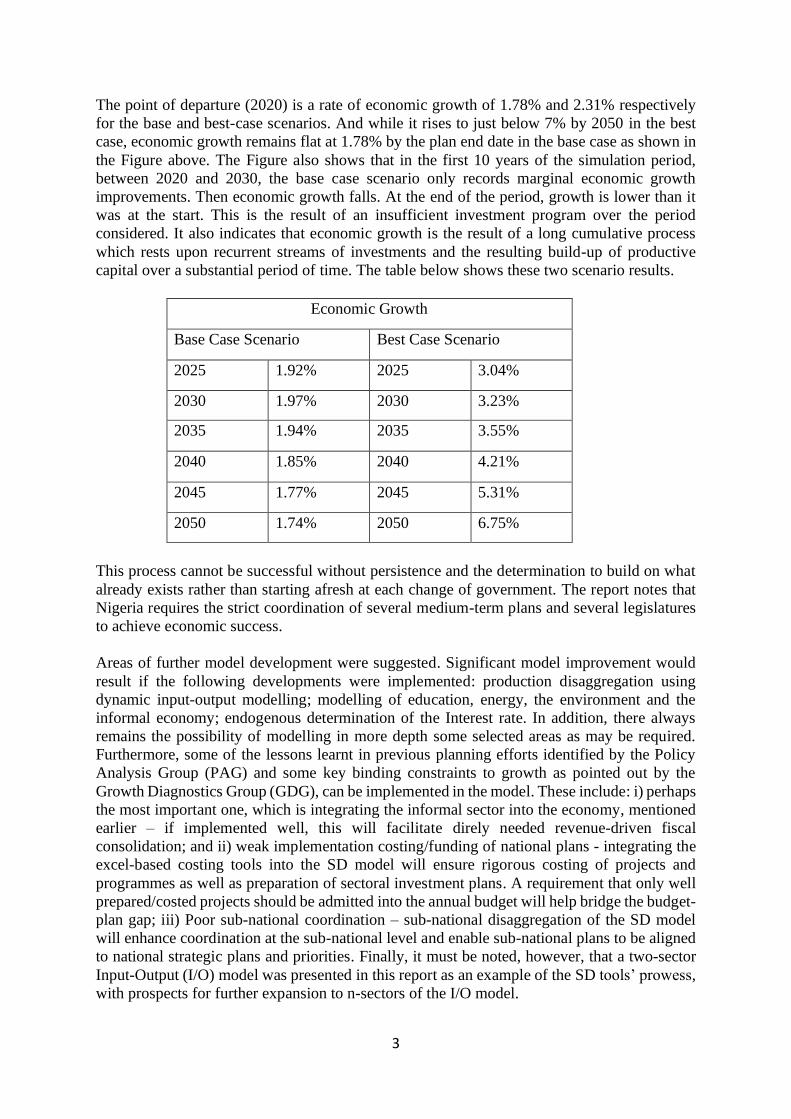

The point of departure (2020) is a rate of economic growth of 1.78% and 2.31% respectively

for the base and best-case scenarios. And while it rises to just below 7% by 2050 in the best

case, economic growth remains flat at 1.78% by the plan end date in the base case as shown in

the Figure above. The Figure also shows that in the first 10 years of the simulation period,

between 2020 and 2030, the base case scenario only records marginal economic growth

improvements. Then economic growth falls. At the end of the period, growth is lower than it

was at the start. This is the result of an insufficient investment program over the period

considered. It also indicates that economic growth is the result of a long cumulative process

which rests upon recurrent streams of investments and the resulting build-up of productive

capital over a substantial period of time. The table below shows these two scenario results.

Economic Growth

Base Case Scenario Best Case Scenario

2025 1.92% 2025 3.04%

2030 1.97% 2030 3.23%

2035 1.94% 2035 3.55%

2040 1.85% 2040 4.21%

2045 1.77% 2045 5.31%

2050 1.74% 2050 6.75%

This process cannot be successful without persistence and the determination to build on what

already exists rather than starting afresh at each change of government. The report notes that

Nigeria requires the strict coordination of several medium-term plans and several legislatures

to achieve economic success.

Areas of further model development were suggested. Significant model improvement would

result if the following developments were implemented: production disaggregation using

dynamic input-output modelling; modelling of education, energy, the environment and the

informal economy; endogenous determination of the Interest rate. In addition, there always

remains the possibility of modelling in more depth some selected areas as may be required.

Furthermore, some of the lessons learnt in previous planning efforts identified by the Policy

Analysis Group (PAG) and some key binding constraints to growth as pointed out by the

Growth Diagnostics Group (GDG), can be implemented in the model. These include: i) perhaps

the most important one, which is integrating the informal sector into the economy, mentioned

earlier – if implemented well, this will facilitate direly needed revenue-driven fiscal

consolidation; and ii) weak implementation costing/funding of national plans - integrating the

excel-based costing tools into the SD model will ensure rigorous costing of projects and

programmes as well as preparation of sectoral investment plans. A requirement that only well

prepared/costed projects should be admitted into the annual budget will help bridge the budget-

plan gap; iii) Poor sub-national coordination – sub-national disaggregation of the SD model

will enhance coordination at the sub-national level and enable sub-national plans to be aligned

to national strategic plans and priorities. Finally, it must be noted, however, that a two-sector

Input-Output (I/O) model was presented in this report as an example of the SD tools’ prowess,

with prospects for further expansion to n-sectors of the I/O model.

4

Table of Contents

EXECUTIVE SUMMARY ...................................................................................................... 1

CHAPTER 1: INTRODUCTION & BACKGROUND ................................................................... 6

a. Draft Final Report ..................................................................................................... 6

CHAPTER 2: REVIEW OF MACROECONOMIC DEVELOPMENTS IN NIGERIA........................... 7

a. Brief Overview of previous planning efforts ................................................................................................. 7

ii. Lessons learned from planning efforts of the last 20 years: ................................................................... 9

iii. Government Priorities, Global Megatrends and Growth Diagnostics .......................................................... 10

iv. Policy Implications: ....................................................................................................................................... 10

v. Policy recommendations on the basis of the GD analysis include the following: ........................................ 11

vi. Integration of key concepts and inputs from the Policy Analysis and the Growth Diagnostic Groups into the SD-based Model for Agenda 2050 Macro Framework: ................................................................................... 11

b. Macroeconomic developments in the last 20 years ................................................................................... 12

CHAPTER 3: APPROACH AND METHODOLOGY ................................................................. 14

a. Overview of approach, methods and tools: ................................................................................................ 14

b. Steps of System Dynamics Modelling. ........................................................................................................ 15

CHAPTER 4: SYSTEM DYNAMICS MODEL .......................................................................... 18

a. Key Concepts and Model Structures............................................................................................................ 18

b. The key feedback loops of the Nigerian socio-economy ............................................ 18

c. Model sketch, constants and parameters ................................................................. 25

d. Assumptions, Scenarios and Simulations .................................................................. 33

CHAPER 5: ANALYSIS OF PRELIMINARY RESULTS .............................................................. 34

Figure 25. Scenario comparison. Debt to GDP ratio.......................................................... 35

Figure 26. Population and national income ..................................................................... 36

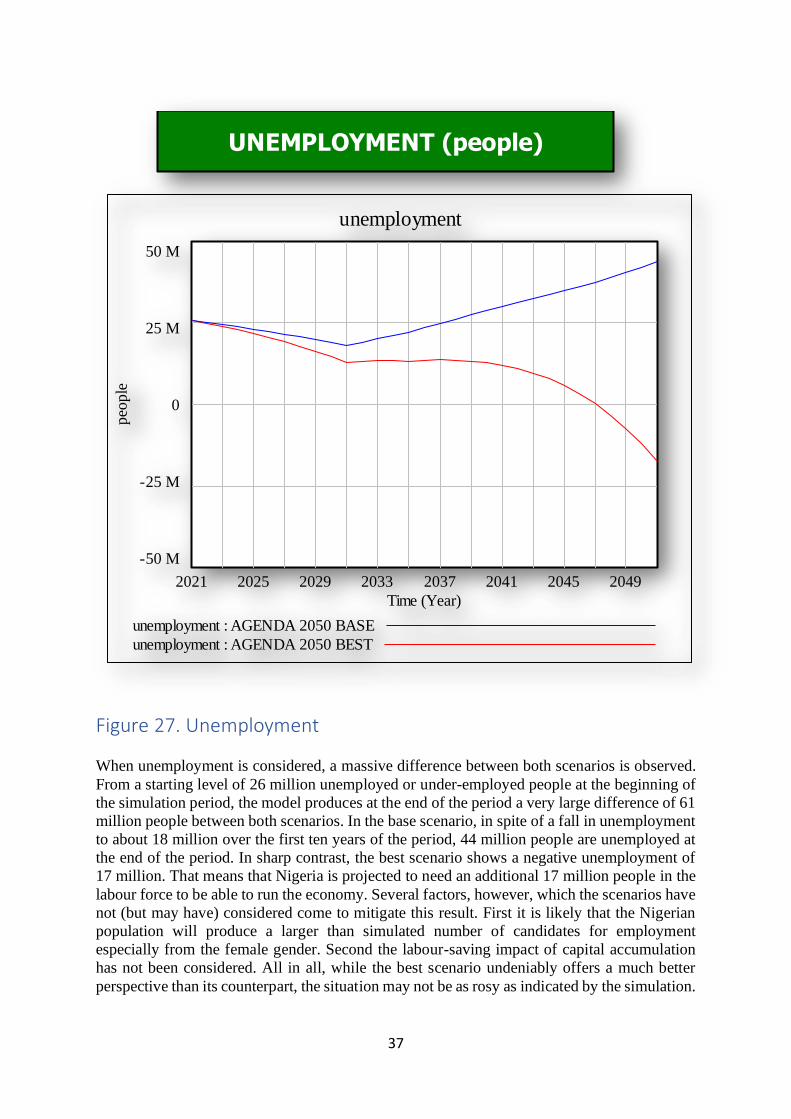

Figure 27. Unemployment ............................................................................................... 37

Figure 28. National income per head ............................................................................... 38

Figure 29. Productive capital ........................................................................................... 39

Figure 30. Economic growth ............................................................................................ 40

Figure 32. Best scenario: economic growth...................................................................... 41

Figure 33. Government revenues & expenditures ............................................................ 41

5

Figure 34. Government surplus / deficit ........................................................................... 42

Figure 35. Government debts .......................................................................................... 43

Figure 36. Debt servicing................................................................................................. 44

Figure 37. International trade ......................................................................................... 45

Figure 38. Forex reserves ................................................................................................ 46

Figure 39. The naira exchange rate ................................................................................. 47

Figure 40. Extract from the data entry worksheet. Relationship forex stock – exchange rate ...................................................................................................................................... 48

Figure 41. The exchange rate multiplier .......................................................................... 49

CHAPTER 6: FURTHER MODEL DEVELOPMENT - DYNAMIC INPUT-OUTPUT MODEL .......... 49

Figure 42. System dynamics sketch of the orders – inventory causal connection ............... 50

Figure 43. Stock and production adjustment ................................................................... 50

Figure 44. Labour force dynamics .................................................................................... 51

Figure 45. Material input procurement ........................................................................... 51

Figure 46. Complete causal structure of a single sector .................................................... 52

APPENDIX 1: MODEL EQUATIONS ................................................................................... 52

APPENDIX 2: SOME BIBLIOGRAPHICAL REFERENCES ........................................................ 61

6

CHAPTER 1: INTRODUCTION & BACKGROUND a. Draft Final Report: This Draft Final Report is submitted by NSF Developments Ltd,

a development management, planning and training consultancy, based in Abuja, in respect

to the consultancy assignment by the Federal Ministry of Finance, Budget and National

Planning (FMFBNP) - to prepare a macroeconomic framework for Nigeria Agenda 2050

using the Computable General Equilibrium (CGE) model and the System Dynamics-based

Model referenced to the integrated Sustainable Development Goals (iSDG) model.

b. Background: Nigeria is in the process of developing successor plans to the Economic

Recovery and Growth Plan (ERGP, 2017-2020) and the Nigeria Vision 20: 2020, both of

which are ending by December 2020. Consequently, the Government of Nigeria has taken

steps to ensure the preparation of a Medium-Term National Development Plan (2021-

2025), or MTNDP to replace the ERGP (2017-2020) and a Long-Term National

Development Plan (LTNDP), the Nigeria Agenda 2050 Perspective Plan to take the place

of the Nigeria Vision 20:2020, using globally acceptable economic development and

planning models.

c. Planning Models: In order to accomplish this task, a number of models have been

identified for use by the supervising authority, the FMFBNP, for use in developing the

macroeconomic framework for the preparation of the two plans. Thus, for the MTNDP the

macro econometric model is to be used, together with the input-output model; while for the

LTNDP the Computable General Equilibrium (CGE) model is to be used in conjunction

with the system dynamics-based model derived with reference to the integrated Sustainable

Development Goals (iSDG) model. Modelling consultants were therefore engaged to

design, implement and train users of the four models in the Ministry, according to the Terms

of Reference.

d. Terms of Reference: The overall objective of the consultancy services is to develop a

dynamic CGE model and a system dynamics-based model of the Nigerian economy for use

by the FMFBNP in policy impact analysis. The output of the models would be used for the

preparation of the Macroeconomic Framework for the Perspective Plan called “Nigeria

Agenda 2050”. The two models are expected to be complementary in terms of operation

and consistency in the use of economic variables; while the output of one model may be

used as an input for the other model, the results of one may also be used to validate the

result of the other. Specific terms of reference include:

i. Review the existing DCGE/CGE models and iSDG model, with a view to presenting

options and solutions to problems in the Nigerian economy;

ii. Develop a theoretical and methodological framework for the DCGE and iSDG models

in Nigeria;

iii. Prepare a possible set of indicators for the models and determine their frequency,

accessibility and sources; and gather data on relevant indicators in excel format;

iv. Update a DCGE Model/SAM for Nigeria and iSDG Model that can be calibrated to

analyse the impact of changes in policy variables and/or economic shocks using

appropriate statistical software;

v. Provide in excel format the output of the model including draft forecasts and

assessment model simulation results

vi. Generate user manuals that contains the theoretical framework of the DCGE and iSDG

models, containing the equations, variables used to include their sources, and the

procedure for conducting simulations or sensitivity analysis, updating the parameter,

and error diagnostics, etc. and;

7

vii. Conduct consultative workshop among the technical staff of FMFBNP, CBN, DMO,

BOF, SEC, NNPC, DPR, NCS, OAGF, FIRS, NBS, NISER, NASS, PEAC and key

sectors to solicit comments suggestions to enhance the initial DCGE and iSDG models;

viii. Enhance capacity of FMFBNP technical staff in updating the DCGE and iSDG Models

for Nigeria and conducting policy analysis using the model through hands-on trainings

and exercises and ensure technological transfer in updating, re-estimating and

calibrating the model.

CHAPTER 2: REVIEW OF MACROECONOMIC DEVELOPMENTS IN NIGERIA a. Brief Overview of previous planning efforts

i. Historical Evolution

The historical evolution of previous planning efforts in Nigeria in the post-colonial era can

be categorized into three phases as described below:

a) The development planning phase (1962-1985). There were four National Development

Plans launched between 1962 and 1985. These were the plans for 1962-1968, 1970-1974,

1975-1980 and 1981-1985. Government intervention was dominant, coordination among

regions was lacking, with modest growth and macroeconomic imbalances.

b) The Structural Adjustment Programme (SAP) and policy-oriented planning era (1985-

1999). This phase was characterized by SAP (1985-1989) and 3-year Rolling Plans, 1990-

1992, 1993-1995, 1996-1999. With an International Financial Institutions led development

agenda, promoting private sector participation through deregulation, liberalization and

privatization, and macroeconomic stabilization leading to macro-economic imbalances and

mixed outcomes;

c) The high growth and development phase (2000-present): The return to development

planning witnessed ambitious home-grown initiatives, with high economic growth rates

but no job or social development gains.

Below is a schematic diagram of the historical evolution of previous planning efforts in

Nigeria.

8

Figure 2: Historical evolution of development planning-policy framework, institutional

configuration and outcomes – in Nigeria:

Source: Adapted from UN ECA (2016)

1.Development Planning 2.Government led interventions 3.Poor policy coordination

Development Outcomes

Macroeconomic and

Development Policy

Framework

Institutional Configuration

1.Modest economic growth rates 2. Structural change -some sectoral shifts 3. Macro imbalances developed over time

1.Little coalition between government and private agents 2.Government-dominant in command but week in capacity 3. Private agents-weak

1.Policy-oriented Planning 2.Liberalisation-deraegulation-privatisation 3. Macroeconomic stability

1.Lower or negative per capital growth 2. Productivity-reducing structural change 3. Macro imbalances developed over time

1.Aid donors dominated 2. Little coalition between government and private agents 3.Government-weak and dwindling resources 3.Private agents-disfranchised and fragmented

1.Home grown development

initiatives 2.Return to development planning 3.Ambitious goals

1.High economic growth rates 2.Growth didn’t trigger structural transformation despite stronger planning 3.Social development gains were achieved but not at a scale

1.Renewed faith in development planning, better policy formulation/implementation and better fiscal/monetary management

Development Planning phase,

1962-1985

Structural Adjustment

Programme, Policy oriented planning

1985-1999

High Growth & Development Phase,

2000-Present

9

ii. Lessons learned from planning efforts of the last 20 years: A few of the Plans reviewed by the Policy Analysis Group (PAG) over the last 20 years include:

• The National Economic Empowerment and Development Strategy (NEEDS), which built

on the Interim Poverty Reduction Strategy Paper (IPRSP) between 2001 and 2003, and

incorporated the State Economic Empowerment and Development Strategies (SEEDS) and

Local Economic Empowerment and Development Strategies (LEEDS)

• Nigeria Vision 20:2020 (NV 20:2020) and the 1st medium-term national implementation

plans (NIPs)

• The Transformation Agenda (2011 – 2015)

• The Economic Recovery and Growth Plan (ERGP, 2017-2020)

Upon analyzing these various strategic documents that have guided Nigeria’s national

development policy over the past 20 years and even before, the group has deducted and

recommended that the country should avoid potential pitfalls both in the planning phase and

the implementation stage that have characterized national planning in the past. Table 1 below

exhibits some of the lessons learned from implementation of previous National Development

Plans in Nigeria.

Table 1: Lessons learned from previous National Development Plans

Weak link between

the plan and annual

budget

Key components of development plans are skipped or provided with less fund during

the preparation of the government annual budget.

Less emphasis on

inter-sectors

collaboration

There is little focus on building inter sectoral synergies for economic development.

Heavy reliance on

foreign funding

Relying on foreign funding is a major throwback for the implementation of several

plans. Most plans were also silent on implementation cost/funding.

Absence of

coordinating

institution(s) for

plan

implementation

This resulted in limited implementation capacities as well as issues of continuity and

coordination of programmes.

Less on addressing

key domestic

growth constraints

Several of the development plans skipped addressing key domestic growth and

productivity constraints. As a result, these issues became huge impediments to the

attainment of set targets.

Impact of oil prices Fluctuations in oil prices can have negative impact on Nigeria’s foreign exchange and

government revenue earnings culminating in severe macroeconomic shocks and

instability

Effect of political

changes

Plan implementation often affected by political and policy changes

Public vs private

investment

Public investment was promoted at the expense of private investment

Internal and

external pressures

Government often failed to keep scheduling and targets because of internal and external

pressures

10

iii. Government Priorities, Global Megatrends and Growth Diagnostics The simulations of the SD model are informed by findings of other sub-groups that

analyzed and reviewed previous plans, government priorities, megatrends in the global

economy and growth diagnostics. Presidential Priorities consist of the following objectives:

Stabilization of the economy

Achieving Agricultural and Food Security

Ensuring Energy Sufficiency in Power and Petroleum Products

Improving Transportation and Other Infrastructures

Driving Industrialization

Improving Health, Education, and Productivity of Nigerians

Enhancing Social Security and Reducing Poverty

Fighting Corruption and Improving Governance, and

Improving Security for all Citizens.

A few of the mega trends that will be expected to affect the planning process in Nigeria

include:

Economic Globalization: e.g., gradual shift in the global economic power relations

from the current industrialized countries to the rising and emerging markets;

increasingly connected global economy and economic integration…

Technology and the Digital Revolution: e.g., Artificial intelligence; 4th Industrial

Revolution (Industry 4.0); Internet of Things…

Demographics and Mobility: e.g., Hyper-urbanization; Rise of the middle class in

Asia and Africa; Demographic dividend…

Energy and Environment: e.g., Resource Constraints, Climate Change; Changing

Energy Mix…

Innovation Acceleration: e.g., Knowledge and Information Society…

Health and Wellness: Involving consumption; Demand for better health care

Global Security Risks: e.g., Pandemics; Natural Catastrophe; Cyber Attacks;

Terrorism…

iv. Policy Implications: The policy recommendations of the Policy analysis Group and Growth Diagnostics Group

are as follow:

• In budgetary provisions, the proportion of capital expenditure should be increased,

and implementation of capital budgets should be scaled up.

• The cost of governance should be reduced by at least 30%.

• Emphasizing movement away from dependence on crude oil

• Closing the fiscal gap to about 3% of GDP

• Stimulating the economy and business development

• Increasing post COVID-19 investment to 9% of GDP

• Diversifying the product space – whether agricultural or non-agricultural products,

particularly products that could earn foreign exchange for the country other than the

oil sector

• Adopt transformative trade policies

• Prioritize self-reliance and home-grown solutions, including import-substitution

• Reduce post-harvest losses in agriculture to stabilize prices

• Measures to diversify revenue and increase tax to GDP ratio by improving tax

administration, including the informal sector and widening the tax base.

• Enhance non-oil forex earnings by attracting FDI, improving diaspora remittances

and promoting non-oil exports.

11

• Prioritization and implementation of critical and strategic infrastructure projects

that will directly boost production and productivity in the SME, agriculture,

manufacturing and service sectors, in line with rapid growth, revenue and forex

diversification objectives.

v. Policy recommendations on the basis of the GD analysis include the following: Minimize macroeconomic volatility by strengthening domestic financial

institutions

Improve access to finance and credit to the private sector by removing existing

regulatory impediments

Strengthen legal and judicial reforms commensurate with economic reforms so as

to establish a stable policy environment in order to boost private investments

Ensure sufficient energy provision, particularly electricity, to enhance private

production

Focus policy on microfinance banking activities, which remain too minimal in

Nigeria and at times even financed by foreign firms, including improving access to

funding and intermediation.

vi. Integration of key concepts and inputs from the Policy Analysis and the Growth Diagnostic Groups into the SD-based Model for Agenda 2050 Macro Framework:

The SD-based Model for Agenda 2050 has the capability to incorporate many of the

lessons learnt from previous planning efforts and the recommendations of the other

Groups – PAG and GDG, a few examples of which include the following, some of which

have already been implemented in the model:

• Relaxing some of the growth constraints identified by the GDG – Feedback loops

in the SD model identify the leverage points where policy action can bring about

the desired development outcomes and impacts.

• Addressing the weak budget-plan link and poor implementation costing/funding of

projects and programmes – the SD model can incorporate the excel-based costing

tools to enable policy analysts in the MFBNP and line Ministries prepare investment

plans and detailed costing of interventions that can be used in programming

expenditures in the budget.

• To address diversification of revenue sources, increase the tax/GDP ratio, integrate

the informal sector and widen the tax base using the SD-based modelling approach.

• Strengthening the Sub-national coordination function of the MFBNP – By carrying

out the sub-national disaggregation of the analysis at the national level using the SD

Model the MFBNP will have a strong tool to deploy in the coordination of planning

at the sub-national level.

• The recommendation that government consumption (recurrent costs in the budget)

should be reduced by 30% while government investment (capital expenditure in the

budget) be increased has already been implemented in the SD Model for Agenda

2050.

• To facilitate the seamless integration of some of the many planning models/tools

and ensure complementarity for medium- and long-term planning, we have done an

SD version of a simple input/output model for demonstration to the Ministry. This

basic SD version of the I/O Model can be developed further if required.

12

b. Macroeconomic developments in the last 20 years In May 1999, after nearly two decades of military dictatorship, Nigeria ushered in a new

administration. The new government’s target was to accelerate economic growth to alleviate

Nigeria’s widespread poverty. In year 2000, the proportion of Nigerians living below the

poverty line of one dollar a day was 56 per cent. This proportion had increased dramatically

during the preceding two decades.

But growing poverty is not the only challenge Nigeria has been facing in the last 20 years. A

fast-growing population, mounting unemployment, particularly youth unemployment,

persistent corruption, a continued heavy reliance on hydrocarbons and the heavy cost of

governance are serious additional difficulties.

Viewed as a global socio-economy, Nigeria was not making significant progress. In 2000,

both per capita income and per capita private consumption were lower than in the early 1970s.

The first decade of the 21st century confirmed the strong influence of oil price variations on

Nigeria’s growth performance. Between 2000 and 2014, Nigeria’s GDP grew at an average

rate of 7% per year. An annual rate of 7.3% was even reached in 2011/12. But growth did

not translate into a strong diversified economy. Oil, gas, and agricultural output continued to

dominate wealth generation, contributing around 70% of total output. Oil alone accounted

for more than a third of GDP. Oil had risen from 58% of exports in 1970 to more than 90%

in the 2000s. It is during this period that Nigeria discovered a new economic evil: non-

inclusive growth.

In 2010, extreme poverty, the share of population living on less than $1.25 a day, not only

persisted but significantly increased to about 68% of the population in 2010. More recently,

the instability in the North and the resulting displacement of people have contributed to the

high incidence of poverty in the North East.

Following the oil price collapse in 2014-2016, combined with negative production shocks,

Nigeria’s GDP growth dropped to 2.7% in 2015. In 2016 during its first recession in 25 years,

the economy contracted by 1.6%. Domestic demand remained constrained by stagnating

private consumption in the context of high inflation: 11% in the first half of 2019. On the

production side, growth in 2019 was primarily driven by services, particularly telecoms.

Agricultural growth remained below potential due to continued insurgency in the Northeast

and ongoing farmer-herdsmen conflicts. Industrial performance was mixed. Oil GDP growth

was stable, while manufacturing production slowed down in 2019 due to a weaker power

sector performance. Food and beverages output increased in response to import restrictions.

Construction continued to perform positively, supported by ongoing megaprojects, higher

public investment and import restrictions.

The Nigerian economy does not grow fast enough, and the Nigerian population grows too

fast to lift the bottom half of the population out of poverty. Prospects for the rural poor are

grim due to the weakness of the agriculture sector, and the livelihoods of the urban poor are

adversely affected by high food prices.

Employment is another major concern. Formal employment is low while Nigeria’s informal

sector accounts for between 65% and 70% of total employment. Rising unemployment has

become a permanent feature of the Nigerian economy: 4% in 1986, 13% in 2007 and 23-25%

in 2018 with another 20% of the labour force underemployed. Youth unemployment is an

even bigger challenge estimated at 38-40% in the last years of the 2010s. Nigeria’s

13

employment problem is a simple arithmetic operation: employment creation remains

insufficient to absorb a much faster growing labour force.

Today, Nigeria’s external reserves stand at US$37 billion. External reserves rose from $4

billion in 1999 to $46 billion in 2010 after paying $12 billion in 2005 to liquidate the external

debt. The highest level of foreign reserves was observed in 2007/8 with a stock reaching

US$52/54 billion. Worth noting, it is also in the period 2006/8 that the naira exchange rate

appreciated. An empirical observation which gives some validity to our model structure. The

naira exchange rate passed the 100 mark for the first time in 2000 with ₦102 per US$. It then

increased to ₦306 per US$ in 2018. Today, the official rate is ₦380 for an American dollar

but the parallel market trades US dollar at ₦470.

Nigeria’s overall global competitiveness remains weak. This is due to the quantity and quality

of health, primary education and infrastructure.

One of Nigeria’s core strategies is a public-private partnership in investments, especially in

such core infrastructure projects as power, railways, roads and ports to generate employment

opportunities. But the private sector in general remains relatively weak. A large part of it is

the oil economy which has been unable to create linkages to the rest of the economy to

significantly contribute to structural change and transformation.

Nigeria is faced with problems both in implementation and in choice. It is not the right

approach to try and fix all problems simultaneously. It spreads thin resources too thin and

does not achieve much. One of the first lessons that economics students learn is that an

economy is a highly connected dynamic system. As a result of economic linkages, fixing one

important problem may result in fixing a number of others. It may also result in creating new

challenges.

Even with significant structural policy reforms, and considering climate change, the likely

fate of the international oil market and the likely appearance of Covid-type new challenges,

it will take a long time for Nigeria’s economic growth to go back to the performance of ten

years ago. For some time, the economy might even grow more slowly than the population,

leading to worsening living standards. Among the many factors that constrain economic

growth, rising public debt, inflation, multiple exchange rate windows and subsidies play a

role. But perhaps the most important is the lack of revenue-driven fiscal consolidation.

Nigeria is faced with the huge task of institutionalizing a large informal economy which

operates on a day to day basis outside of any formal financial and economic structures.

Another major challenge is to support the sustained growth of the non-oil economy. Reforms

in this direction would help raise living standards of low-income groups, reduce the size of

the informal economy and create job opportunities. It is indeed the lack of job opportunities

which is at the core of the high poverty levels, of regional inequality, and of social and

political unrest in the country.

14

CHAPTER 3: APPROACH AND METHODOLOGY a. Overview of approach, methods and tools: System dynamics is one of the

approaches selected to develop a macro framework for Nigeria Agenda 2050. System

Dynamics is the brainchild of late Professor Jay W. Forrester of the Massachusetts

Institute of Technology (MIT). System Dynamics is neither a theory nor a solution. It

is a method, that is, a vision of how the world works and it is a tool, that is, a means to

an end.

System dynamics rests on four foundations:

• The theory of information feedback systems;

• A knowledge of decision‐making processes;

• The experimental model approach to complex systems;

• The digital computer as a means to simulate realistic mathematical models.

The purpose of system dynamics practitioners is to build models capable of deriving

dynamic behaviours solely from variables and interactions belonging to and within the

system. The dynamics of systems does not depend upon any exogenous forces but is

endogenously generated by their structure.

System dynamics models are built on four pillars:

• Stocks & flows

• Feedback loops

• Non-linearity

• Time & delays

i. Stocks and flows are key system dynamics variables. Stocks are accumulators. Flows

feed and/or drain stocks. Examples of stocks and flows abound. Population is a stock

fed by births and drained by deaths; your bank account is a stock fed by your deposits

and drained by your withdrawals; a trader’s inventory is a stock fed by goods

produced and drained by goods shipped; your reputation is a stock fed by all the good

things you do and drained by all the bad things you accomplish; a price is a stock fed

by inflation and drained by deflation.

ii. Feedback loops are closed chains of multiple, causal interconnections linking stocks

and flows. They also often include time delays and non-linear interactions. It is the

interplay of these loops which determines system’s behaviour. Feedback loops are

major structural elements in system dynamics models. They are of two types:

reinforcing and balancing. Reinforcing loops generate exponential growth or

exponential decline. These are popularly known as virtuous and vicious circles. If

unchecked reinforcing loops explode or collapse leading to unmanageable situations.

In contrast, balancing loops counteract system growth or system decline. They thrive

to create equilibrium, that is, system stability. One of the favourite examples cited by

system dynamics textbooks is the dynamics of population. Population is a stock

driven by two major flows: births and deaths which both depend on population size.

But births and deaths also affect population size. There exists therefore a dynamic

system driven by two feedback loops of opposing polarity. The interactions between

births and population create a reinforcing loop which feeds upon itself. The

interactions between deaths and population create a balancing loop which counteracts

the effect of births and thrives to balance the system. For economists, the virtue is in

reinforcing loops because economic growth remains the gospel of the profession. For

physicists and natural scientists, however, the virtue is in balancing loops because

15

equilibrium means system stability. This fundamental difference of perspective

explains why it is so difficult to reach a compromise between economic growth and

the preservation of nature.

iii. Non-linearity is a characteristic of many natural and made-made systems. It is a

reaction to stimulus in a manner non-proportional to the action that caused the

response. System dynamics models do incorporate non-linear relationships either as

equations or as user-defined functional tables. Examples of functional tables include

a multiplier of importation which is assumed to be influenced by the exchange rate

or the effect of the income per head on the population’s fertility. These assumed

functional relationships may be modified but the direction of the effect (direct or

inverse) should be preserved. For example, fertility is supposed to decrease and not

increase when the economy creates more wealth.

iv. Time is the most important variable in a system dynamics model. It is time together

with the stocks included in the model which generate its dynamics. This is because

the future value of each stock partly depends upon its present value:

STOCKT+TIME STEP = STOCKT + TIME STEP * (FLOW INT – FLOW OUTT)

In the above equation, T is the index of current time and TIME STEP is the Δ time

also known as DT. TIME STEP is a parameter of the integration process driving its

accuracy. It is not a parameter of the model. System dynamics models most

frequently use Euler as their integration method. Flows are calculated from values of

stocks, other flows and/or from auxiliary variables. Auxiliary variables are

components of flows. They are made explicit to clarify how complex flows are

calculated.

v. Delays: very few relationships, if any, are instantaneous. System dynamics include a

number of delay functions to take account of this reality. Delays are fixed or

exponential, material or information, and of order 1, 3 or n.

It is our conviction that system dynamics is the right perspective to address the

dynamic complexity of such large adaptive systems as states, regions or whole

countries. System dynamics is a valuable approach for high level issues such as

corporate strategy and government policy. It is and has been widely used to look at a

variety of issues such as industry structure, urban dynamics, population, public health,

engineering prototyping, risk assessment and such global concerns as economic

development and environmental protection.

b. Steps of System Dynamics Modelling. Not every system dynamics model constructed

is substantial. But when it is there should be six steps in its construction. Interestingly

enough these six steps are in a feedback loop:

• Conceptualization – group model building

• Sketch

• Identification of feedback loops

• Equations & units

• Simulations & calibration

• Back to sketch or perhaps even to conceptualization for potential model

improvement

16

i. Conceptualization. The first step in system dynamics modelling is group model

building to get the concept right and accepted by all. Models built with system

dynamics address a large variety of issues. But system dynamics modelers cannot

be experts in all the fields they model especially when multidisciplinarity is a key

model requirement. The corollary of such an approach is that such models, which

call for multidisciplinarity, are never build by one person. If they were, they would

fail. The specific skill of system dynamics modelers is to capture experts’ expertise

– to extract experts’ mental model and to transform it into a formalized and explicit

computable structure which exploits this expertise to uncover interventions and

policy decisions favorable to the system under study. Much if not all of the

knowledge and information required to build a substantial system dynamics model

reside in the mental models of those that are part of the system under study.

Participating in model construction also enhances the learning process of those to

whom the model is destined. Modelling a problem always results in considerable

learning for those participating in the modelling process. Finally, model validity

and model implementation - the trust model recipients put on the model greatly

benefit from group model building. Even the most brilliantly built model includes

debatable structures and debatable assumptions. Multidisciplinarity is therefore not

the only requirement. It is also required to reconcile different visions of the same

problem to reach consensus on how to solve a problem or to reach a goal. This is

certainly the case for a model of the very long term such as the present macro

framework model. To some extent, the approach adopted by Government in the

preparation of Nigeria Agenda 2050 resembles group model building although

there is room for perfecting it.

ii. Sketch. System dynamics model are built graphically on a workbench called view.

As an example, the equation presented in 3a under non-linearity is represented by

the following sketch:

Figure 1. Stock & flow sketch in system dynamics

Stocks are balance sheet elements with no time dimension which accumulate money,

material, people or information. The double arrows represent the movement of stuff in

and out of the stock. Causality, which is not correlation, is represented by a single arrow

starting from the cause and pointing to the effect.

STOCKFlow in Flow out

Initial stock

17

Figure 2. Sketch representation of causality in system dynamics

System dynamics therefore represents causality as X Y while the traditional

mathematical notation is Y = f(X).

Complex models do require several views. Views are connected through shadow

variables. A shadow variable is a variable the cause of which is shown on a view while

its impact appears on another.

A model is computable only if all its variables are quantified. It is also required that the

polarity of each relationship the model includes is determined with certainty: whether

a directional change in the cause creates the same directional change in the effect (direct

connection) or an opposite change (inverse connection).

iii. Identification of feedback loops

Except for very large models for which the task might be too demanding, it is always

useful to identify a model’s key feedback loops and to determine their polarity. The

operation can give useful insights on why the model produces the results it produces.

Feedback loop identification starts with the identification of the polarity of each causal

connection in the loop. If the number of direct connections in the loop is odd, the loop

is balancing; if it is even the loop is reinforcing. Feedback loop identification is also a

graphical exercise, but it differs from sketching especially with large models built on

several views. The multiplication of views makes it difficult if not impossible to

identify feedback connections.

iv. Equations & units.

The completion of a model’s sketch reveals the entire causal structure of the system

being modelled. What remains to be done is to enter the model equations, that is, to

define the rules connecting the causal elements. An important aspect of this segment of

model construction is to define the units of each model parameters (variables and

constants) and to ensure their coherence. The unit on the left of the equal sign must be

the same as the unit on the right. Ensuring unit coherence is important. Even though

Vensim allows models with unit errors to simulate. Such unit errors may hide more

fundamental structural errors. It is therefore important that modellers take time to check

the units of their models.

v. Simulations & calibration

Models will only simulate if all equations are correctly written and all required

numerical data, including time parameters, entered. But that does not guarantee success.

Complex models simulating over a long period – a large number of time units might

diverge quickly and stop simulating well before the final time is reached. What is then

required is to calibrate the model: identify assumptions which are such that small

changes made to them have a large impact on model behavior. Calibration may take

time. Yet, it is an indispensable step for the success of a modelling project.

CAUSE

EFFECT

18

A set of numerical data that leads to a successful simulation is a scenario. System

dynamics models can produce a large number of scenarios in a very short time. It is

important to change one assumption at a time and to take time to understand why the

model produces the results it produces.

vi. Back to sketch

It may happen that simulation results produce inconsistencies or impossibilities or

reveal structural deficiencies or point to missing structures in the model or that any

combination of the above is observed. It is then necessary to rethink the concept and to

go back to the design of the model. Complex models are better built on a step by step

basis so that complexity is always under control. The building of system dynamics

models is therefore a feedback loop.

CHAPTER 4: SYSTEM DYNAMICS MODEL a. Key Concepts and Model Structures

In its present state, which we do not consider as the final state, the model depicts the

interactions of two major social structures: population and the global economy. The

economy is not disaggregated, and the environment is not modelled. Those are two

critical and required additions. It would not pose any major problem to disaggregate the

economy and build the environment in the model. It might even be useful to review the

existing model structure with the purpose of improving it. For this to be done, more time,

additional expertise and the implementation of group model building are required.

b. The key feedback loops of the Nigerian socio-economy are represented

in 11 diagrams. The diagram on Figure 3 shows the four reinforcing loops which drive

population growth through fertility rate and income per head. The sketch also shows a

potential connection between the economy and the population that would be created if a

policy existed to link investment volumes to the level of unemployment. This causal link,

however, has not been built in the model as it is not the purpose of models to substitute

for decision makers.

Figure 3. Population and the economy

VERY YOUNG(0-4)

Yearly births

SCHOOLAGE (5-14)

Growing toschool age

YOUNG ADULT(15-24)

ADULT(25-64)

Maturing toyoung adult Maturing to

adult

Laboursupply to

theeconomy

Unemployment

Labour requiredby the economy

PRODUCTIVECAPITAL

Fertilityrate

Indicated impact ofincome per head on

fertility rate

Income perhead index

Populationtotal

Income perhead

GDPfc

GDPmp

Nationalincome Investment

LINKAGES POPULATION - ECONOMY

Labouravailable

R

R

R

R

B

B

19

The two loops that would be created if the model had built in a formal policy to link investment

to unemployment are both balancing. This is because an increase (decrease) in the labour force

that population supplies to the economy creates more (less) investment and a higher (lower)

GDP which tends to reduce (increase) the fertility rate.

Evidently, this relationship is not instantaneous. The reaction of the population to the stimulus

generated by changes in the income per head is assumed to occur continuously and

progressively over a period of 5 years. This is indicated by a constant called delay impacting

on fertility.

Figure 4 displays the model’s major causal connections. Although this model is relatively

simple – with the exclusion of the population segment it has only five interconnected

differential equations, it is clear that this structure already constitutes a rather complex system

which only a computer can process. Understanding it requires further clarifying. This is the

purpose of the next nine diagrams.

Figure 4. Model major causal structures

The capital accumulation loop shown on Figure 5 represents the core of the economic growth

process. Each period, a proportion of the wealth created is reinvested in the stock of capital

which increases and produces more wealth. It is clearly a reinforcing process that feeds upon

itself.

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

20

Figure 5. The reinforcing capital accumulation loop

Two parameters are important here: the propensity to consume and the depreciation fraction of

the capital stock. The model also includes a third parameter called investment effectiveness. It

is a simple multiplier varying between 0 and 1. Lowering the value of investment effectiveness

is equivalent to assuming an imperfect flow of domestic saving to capital which may reflect

either capital flight or corruption or both. This parameter was not activated. It was kept neutral

(with the value 1) in the model simulations presented in this report.

By nature, a reinforcing loop is unstable and tends to make systems unmanageable except if

one or several balancing loops mitigate the exploding exponential growth or decay. One of

these loops is shown on Figure 6.

Figure 6. The first balancing tax loop

The income tax loop shows the stabilizing impact of taxation on the economy. More (less) tax

reduces (increases) disposable income, saving, investment and the stock of capital and

Deficit financingdomestic

PUBLICDOMESTIC DEBT

Interest paid ondomestic debt

Debt servicingdomestic

Debt servicingtotal

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomestic revenues

Government taxrevenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficit financingforeign

PUBLICFOREIGN DEBT

Interest paid onforeign debt

Debt servicingforeign

Productivecapital index

Capital multiplier ofnon-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange rate

RATE OFEXCHANGE

Forex in

Exchange rateindex

Forex out

Import

Exchange ratemultiplier of import

Exchange ratemultiplier of non-oil

export

R

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

B

21

dynamically results in less (more) tax revenue. While a reinforcing loop is such that an increase

(or a decrease) in any of its variables results in more increase (or decrease) in that same

variable, a balancing loop is such that an increase (or a decrease) in any of its variables results

in a decrease (or an increase) in that same variable. Applying this reasoning to taxation

demonstrates that it may end up being a good policy to reduce taxes to ultimately increase tax

revenue.

Figure 7 shows the two reinforcing government investment loops. Just like the private sector,

government uses part of its revenue to invest and contribute to the growth of the economy.

Both this structure and that shown on Figure 5 combine to produce the growth of the entire

economic system as they both aim at increasing the country’s stock of productive capital and

therefore GDP.

Figure 7. Two reinforcing government investment loops

The critical parameters in these feedback loops are the government propensity to consume and

invest. A high cost of governance may not necessarily reduce the contribution of government

to the country’s investment and growth but, if government does not run a budget surplus, it will

create more indebtedness and higher debt servicing obligations.

The model is constructed in such a way that no constraint is placed either on the size of deficit

financing, on public debts or on debt servicing both at home and abroad. Figure 8 displays the

reinforcing domestic debt loop and the deficit financing process as far as public domestic debt

is concerned.

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

R

R

22

Figure 8. The reinforcing domestic indebtedness loop

More (less) domestic debt means more (less) interest to pay which translates into more (less)

government expenditures, a larger (lower) deficit or a lower (larger) surplus, a larger (lower)

demand for deficit financing and further (less) debt deterioration.

As no indebtedness constraints are built in the model, the results the model generates entirely

depend upon the assumptions that model users make. The model might very well diverge or

produce unrealistic results as a result of the assumptions made. Calibration is then required. It

must occur for the assumptions leading to rejected results to be amended until acceptable

results are generated. This is one of the most difficult segments in system dynamics modelling

especially when working with complex models. It is also a very useful procedure as it allows

model users to understand the relative sensitivities of the parameters that drive the model and

the points of leverage. Where in the model a small variation of assumption generates a large

change in system behaviour.

Figure 9. The reinforcing foreign indebtedness loop

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

R

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

R

23

Exactly the same deficit financing process is at play when foreign domestic debts are

concerned. This is shown on Figure 9. It is, however, clear and obvious that such reinforcing

loops cannot continue forever if only because of the willingness of fund lenders to oblige.

Figure 10. The three balancing foreign reserves loops

The exchange rate is the naira price of a particular foreign currency: In Nigeria’s case and in

this model, the American dollar. Prices are stocks. When they are connected to a physical

inventory, they are determined by the size of this inventory compared to its desired size. In this

model, the inventory to which the exchange rate is connected is the reserve of foreign exchange,

basically the reserves of US dollars. The process that is taking place is a dynamic adjustment

of the price (the exchange rate) as a function of the fluctuations of the inventory. The model

assumes that the desired stock of foreign exchange is equal to the volume of US dollars required

to meet the country’s US dollar commitments plus a given precautionary margin. The model

also assumes that the ratio between desired and actual foreign reserves drives a price multiplier

of the actual exchange rate which both determine its desired level. The adjustment then takes

place over a given time delay indicated by constant time adjusting exchange rate.

The three balancing loops shown on Figure 10 depict this simple price adjustment mechanism

based on the dynamics of the stock of foreign reserves. This is precisely the reason why the

loops are balancing: the model generates inflows and outflows of US dollars which drive the

stock of foreign reserves and simultaneously searches for the equilibrium price (the exchange

rate) which corresponds to this inventory level.

The fluctuations in government revenue do not only affect domestic and foreign indebtedness,

they also affect disposable income in a reinforcing manner.

Domestic debt service adds purchasing power to the economy and therefore boosts

consumption and investment. The two additional balancing tax loops shown on Figure 11 add

to the first balancing tax loop shown on Figure 6. The causality described on Figure 11

illustrates the impact of a rising (falling).

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

BB

B

24

Domestic debt on national and disposable income through debt servicing. More (less)

disposable income generates more (less) GDP and more (less) tax and non-tax revenue which

themselves decrease (increase) government deficit and the need to borrow.

Figure 11. A second group of two balancing tax loops

Figure 12 displays the reinforcing impact of the foreign debt on the exchange rate. An increase

(decrease) in foreign debt servicing drains more (less) foreign reserves and leads to a further

depreciation (appreciation) of the exchange rate which, in turn, makes foreign debt servicing

more (less) expensive.

Figure 12. Interactions foreign indebtedness - exchange rate

Figure 13 displays the last component of the model structure which rests on a model assumption

that budget surpluses feed the stock of foreign reserves. If it is assumed that government budget

surpluses are kept in foreign currencies as foreign reserves, an additional reinforcing loop is

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

B

B

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

R

25

created, similar to the loop shown on Figure 12 but with opposite effect. The effect of an

increase (decrease) in foreign debt service is to increase (decrease) the drainage of foreign

exchange from the economy.

The effect of an increase (decrease) in government surplus is to add to (remove from) the stock

of foreign exchange. The controlling stock in the loop (foreign exchange reserves) is increased

rather than depleted.

Figure 13. Management of government surplus

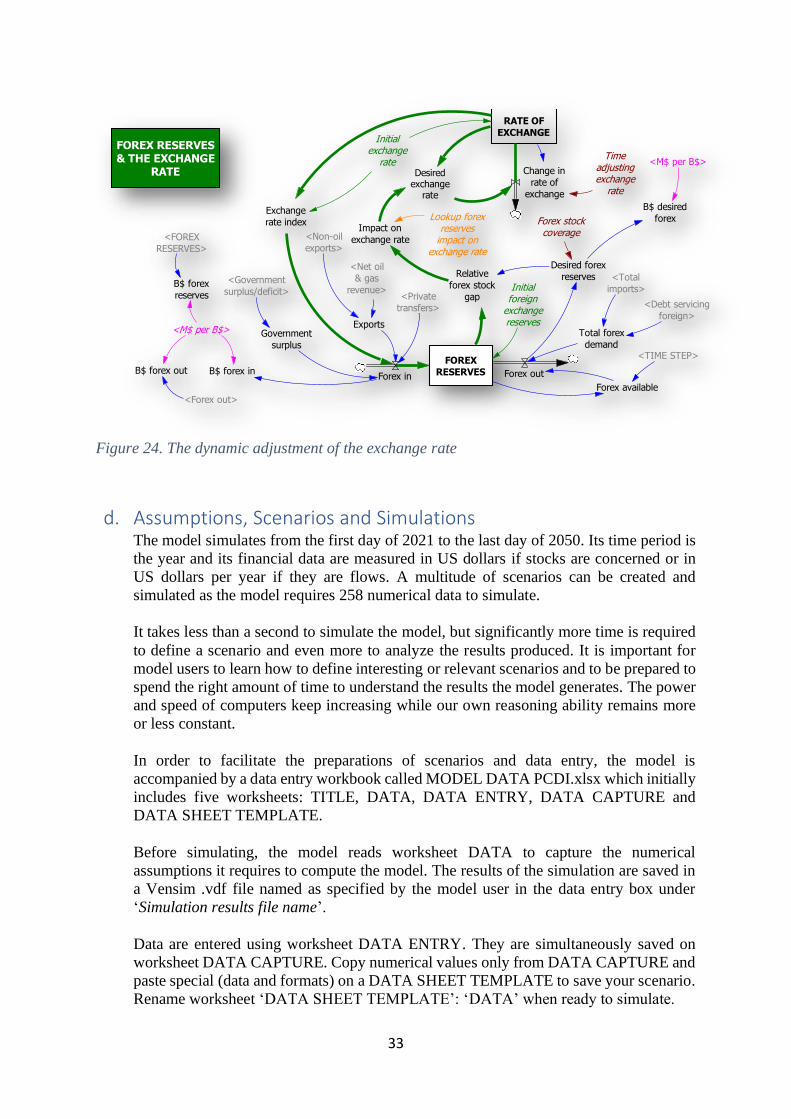

c. Model sketch, constants and parameters. Whether a feedback loop is

reinforcing or balancing, its impact on the dynamic system under study depends upon the

value of the coefficients or parameters that drive it. A structure is driven by data which

can become structures when more complexity is built into the model. The structural

components discussed in section a. above do not explicitly display the parameters and

coefficients which drive feedback loops. This would make the causal diagrams shown

above too bulky and more difficult to read. Parameters and coefficients, however, are

clearly shown on the different views of the model sketch which, together with the

database, are the sole input to the model’s computation process. The model sketch is

made of in nine views connected by shadow variables. In order to make views easier to

read, the following colour conventions are used:

• Green: initial values. All stocks in a model must be initialized. These are the model’s

opening balance sheet values. Initial values may be either assumed or calculated.

• Pink: constants that are fixed once and for all. For example, conversion factors: there

are 1,000 million in a billion or it takes 4 years to be 4 years old

• Dark red: parameters the model reads from the Excel database

• Orange: lookup or functional tables

The first view of the model is the population view. There are five stocks representing the aging

process.

Deficitfinancingdomestic

PUBLICDOMESTIC

DEBT

Interest paid ondomestic debt

Debtservicingdomestic

Debtservicing

total

Governmentexpenditures

Governmentsurplus/deficit

Governmentdomesticrevenues

Governmenttax revenue

Governmentnon-tax revenue

GDPfc index GDPfcPRODUCTIVE

CAPITAL

InvestmentGovernmentinvestment

Privateinvestment

Savings

Disposableincome

Nationalincome

GDPmp

Deficitfinancingforeign

PUBLICFOREIGN

DEBT

Interest paid onforeign debt

Debtservicingforeign

Productivecapital index

Capitalmultiplier of

non-oil export

Non-oilexport

Export

FOREIGNRESERVES

Desiredexchange

rateRATE OF

EXCHANGE

Forex in

Exchangerateindex

Forex out

Import

Exchangerate

multiplierof import

Exchange ratemultiplier of

non-oil export

R

26

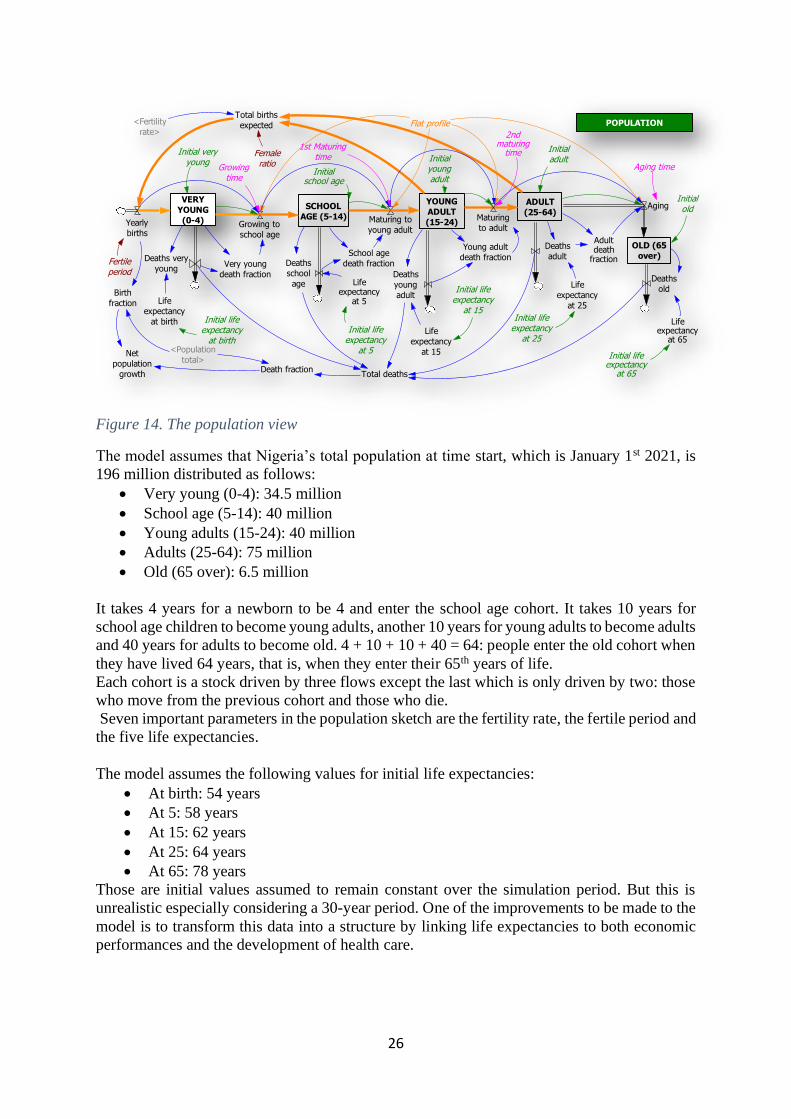

Figure 14. The population view

The model assumes that Nigeria’s total population at time start, which is January 1st 2021, is

196 million distributed as follows:

• Very young (0-4): 34.5 million

• School age (5-14): 40 million

• Young adults (15-24): 40 million

• Adults (25-64): 75 million

• Old (65 over): 6.5 million

It takes 4 years for a newborn to be 4 and enter the school age cohort. It takes 10 years for

school age children to become young adults, another 10 years for young adults to become adults

and 40 years for adults to become old. 4 + 10 + 10 + 40 = 64: people enter the old cohort when

they have lived 64 years, that is, when they enter their 65th years of life.

Each cohort is a stock driven by three flows except the last which is only driven by two: those

who move from the previous cohort and those who die.

Seven important parameters in the population sketch are the fertility rate, the fertile period and

the five life expectancies.

The model assumes the following values for initial life expectancies:

• At birth: 54 years

• At 5: 58 years

• At 15: 62 years

• At 25: 64 years

• At 65: 78 years

Those are initial values assumed to remain constant over the simulation period. But this is

unrealistic especially considering a 30-year period. One of the improvements to be made to the

model is to transform this data into a structure by linking life expectancies to both economic

performances and the development of health care.

VERY

YOUNG

(0-4)Yearly

births

Femaleratio

Growing to

school age

ADULT

(25-64)

Growingtime

OLD (65

over)

Aging

Aging time

Deaths

old

Deaths very

youngVery young

death fraction

Deaths

adult

Adultdeath

fraction

Initialold

Initialadult

Initial veryyoung

Fertileperiod

Birth

fraction

Net

population

growth Total deaths

Flat profile

SCHOOL

AGE (5-14)

School age

death fractionDeaths

school

age

Maturing to

young adult

1st Maturingtime

Initialschool age

Death fraction

Lifeexpectancy

at 65

Life

expectancy

at 25

Lifeexpectancy

at 5Life

expectancy

at birth

Total births

expected

YOUNG

ADULT

(15-24)

Deaths

young

adult

Initialyoungadult

Maturing

to adult

Young adult

death fraction

Life

expectancy

at 15

2ndmaturing

time

POPULATION

<Population

total>Initial life

expectancyat 65

Initial lifeexpectancy

at 25

Initial lifeexpectancy

at 15

Initial lifeexpectancy

at 5

Initial lifeexpectancy

at birth

<Fertility

rate>

27

The fertility rate is the number of children that, on average, a fertile woman will engender over

her fertile period. What makes the fertility rate important is its connection with the

performances of economies. There is a clear world level relationship between GDP per head

and fertility rate.

Fertility rates are very high at very low GDP level (below US$1,000) but a very large fall in

fertility occurs as soon as GDP per head rises to about US$3,000 to 4,000. This is shown on

Figure 15.

Figure 15. Correlation between fertility and GDP per head

This relationship may be one of the keys to Nigeria’s population problem. This is the reason

why it must be part of the model. The assumed relationship between fertility and income per

head included in the model is shown on Figure 16. It is a relatively mild assumption which has

been kept the same in both simulated scenarios.

Figure 16. Assumed effect of income per head on fertility

A second important connection between population and the economy is shown on the left-hand

side of Figure 17. The key coefficient in the relationship is the fraction participating, that is,

the proportion of the adult population able and willing to work.

0.00

0.20

0.40

0.60

0.80

1.00

1.20