non profit accounting and financial reporting update...non profit accounting and financial reporting...

TRANSCRIPT

John R. Null Audit Shareholder

Non profit Accounting and Financial Reporting Update

Financial Statements of Not-for-Profit Entities

Disclosure Framework

Simplification Initiative

Private Company Council (PCC)

Leases

Revenue Recognition

Government Assistance Disclosures

Agenda

2

Financial Statements of Not-for-Profit Entities

3

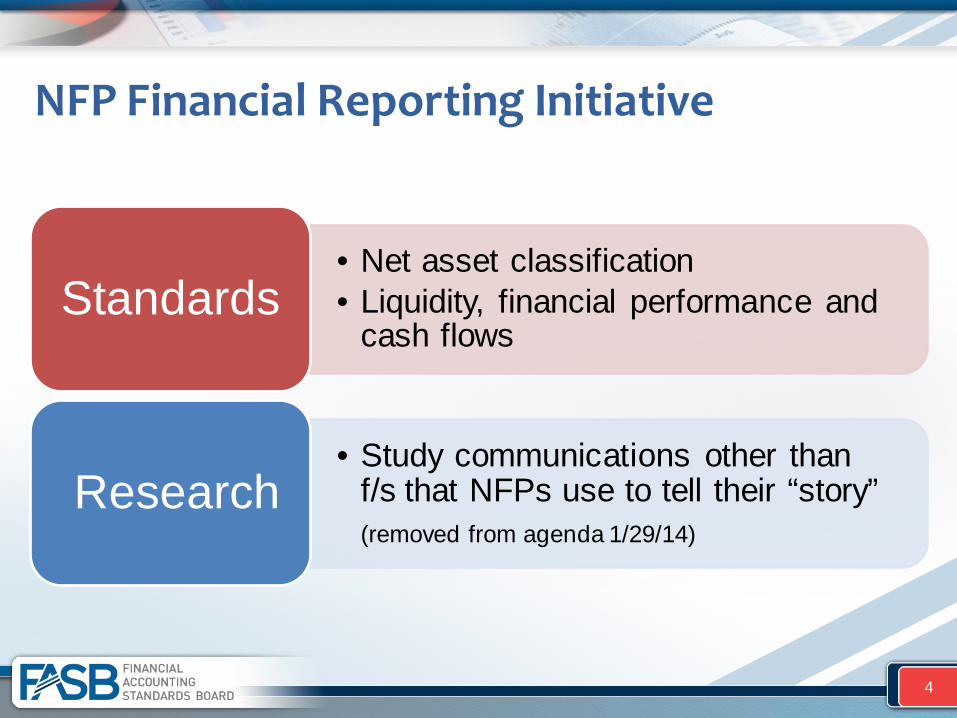

• Net asset classification • Liquidity, financial performance and

cash flows Standards

• Study communications other than f/s that NFPs use to tell their “story”

(removed from agenda 1/29/14) Research

NFP Financial Reporting Initiative

4

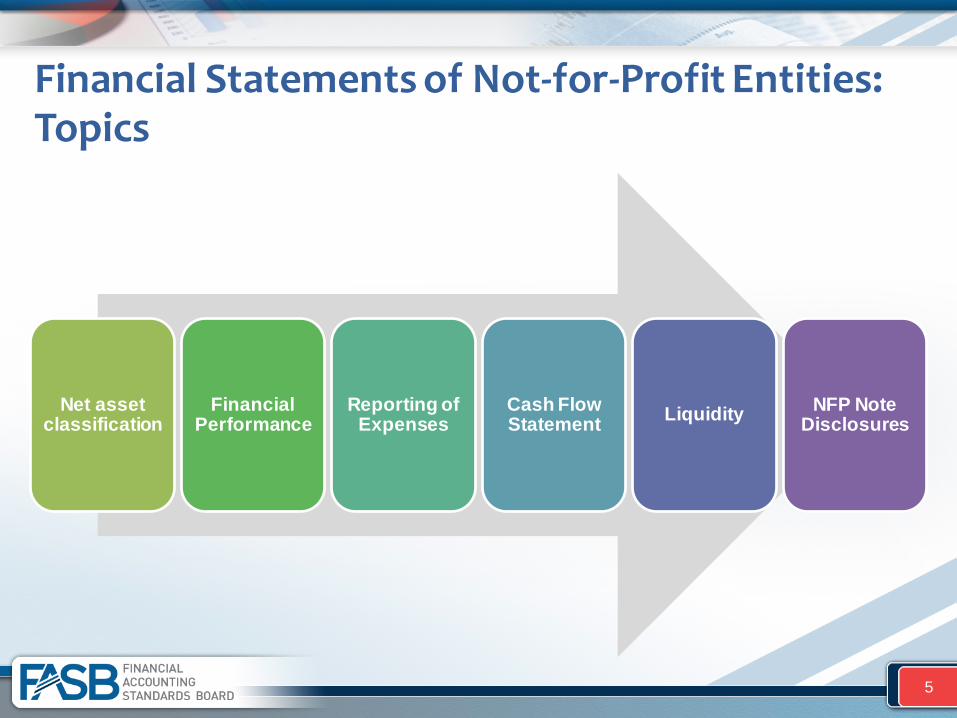

Net asset classification

Financial Performance

Reporting of Expenses

Cash Flow Statement Liquidity NFP Note

Disclosures

Financial Statements of Not-for-Profit Entities: Topics

5

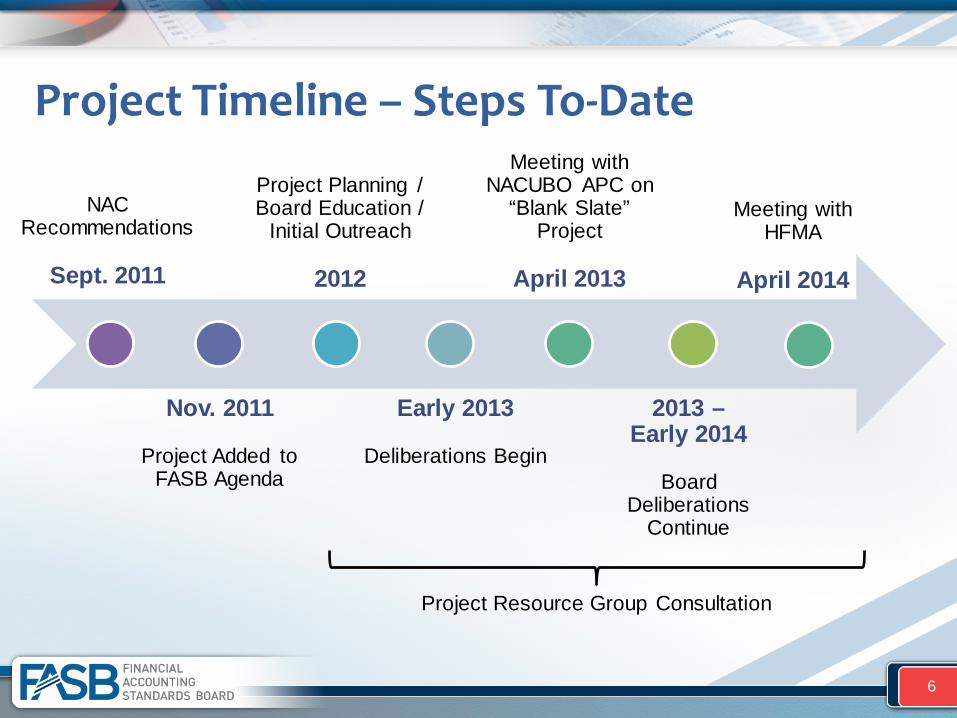

Project Timeline – Steps To-Date

NAC Recommendations

Sept. 2011

Nov. 2011

Project Added to FASB Agenda

Project Planning / Board Education /

Initial Outreach

2012

Early 2013

Deliberations Begin

Meeting with NACUBO APC on

“Blank Slate” Project

April 2013

2013 – Early 2014

Board

Deliberations Continue

Meeting with HFMA

April 2014

6

Project Resource Group Consultation

Net Assets - Issues UPMIFA and PRNA/TRNA distinction

- Ability to spend from donor-restricted endowments even if underwater

- Board action required to appropriate investment returns for spending

TRNA considered by many to be “Hodgepodge” - Need for better disclosure of the nature and availability (timing)

of donor restricted resources

URNA open to misinterpretation - Better disclosure surrounding availability/liquidity would be

helpful, including limits imposed by an entity’s governing board 7

Net Assets – Two Approaches

8

Approach 1 – Restrictions as primary cut

Without Restrictions

Operating Endowment Plant

Approach 2 – Purpose as primary cut

Operating Without

restrictions With restrictions

With Restrictions

Operating Endowment Plant

Endowment Without

restrictions With restrictions

Plant Without

restrictions With restrictions

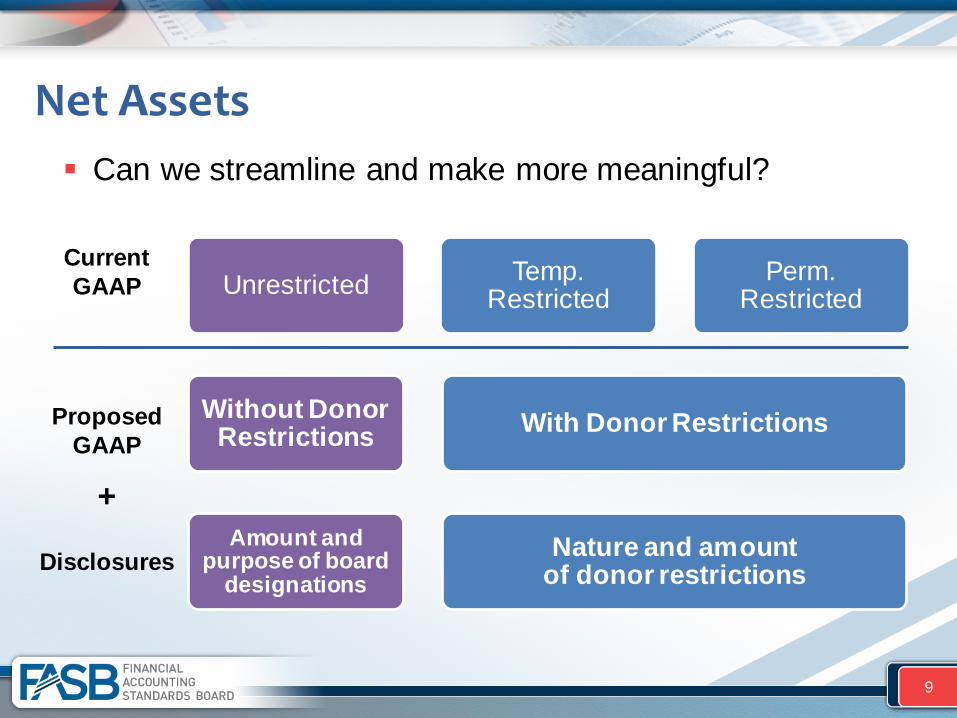

Net Assets Can we streamline and make more meaningful?

Unrestricted Temp. Restricted

Perm. Restricted

Without Donor Restrictions With Donor Restrictions

Amount and purpose of board

designations Nature and amount

of donor restrictions

Current GAAP

Proposed GAAP

Disclosures

+

9

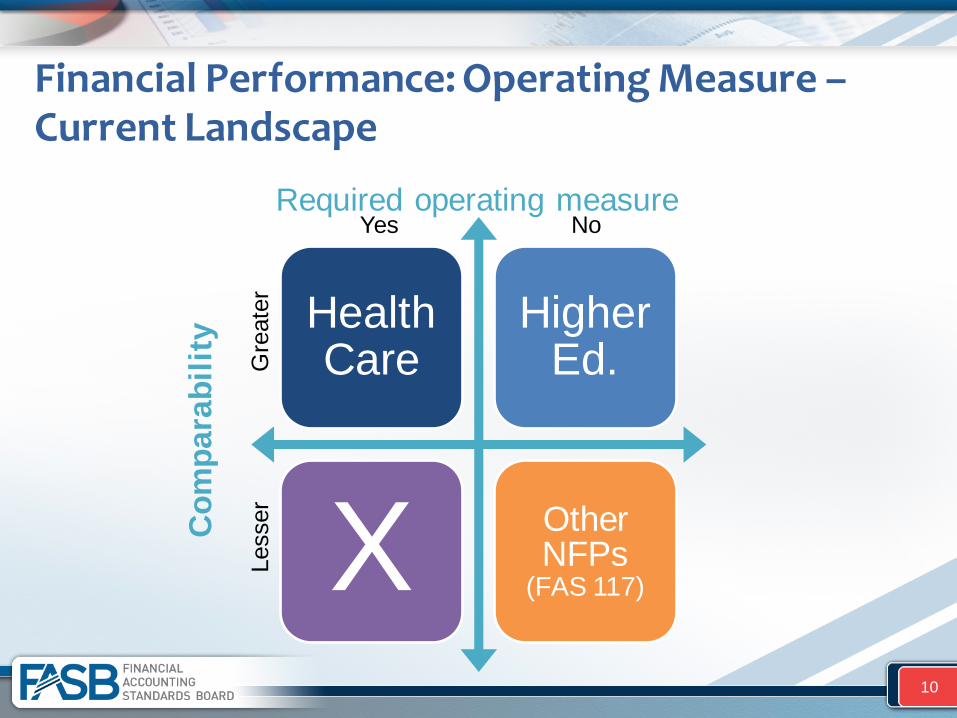

Financial Performance: Operating Measure – Current Landscape

Required operating measure

Health Care

Higher Ed.

X Other NFPs

(FAS 117)

Yes No C

ompa

rabi

lity

Gre

ater

Le

sser

10

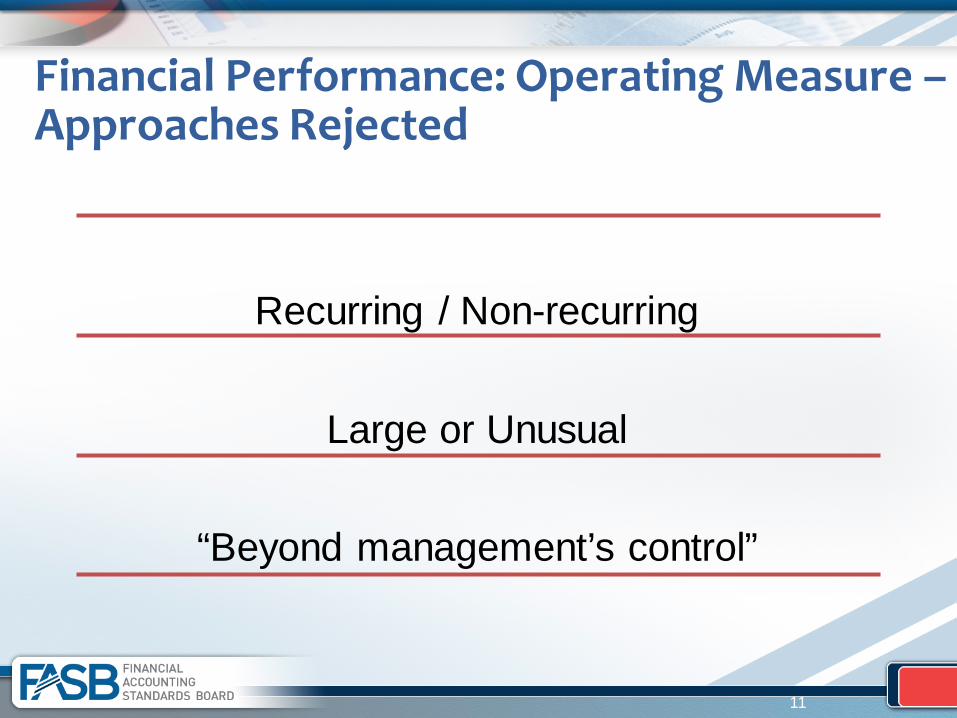

Financial Performance: Operating Measure – Approaches Rejected

Recurring / Non-recurring

Large or Unusual

“Beyond management’s control”

11

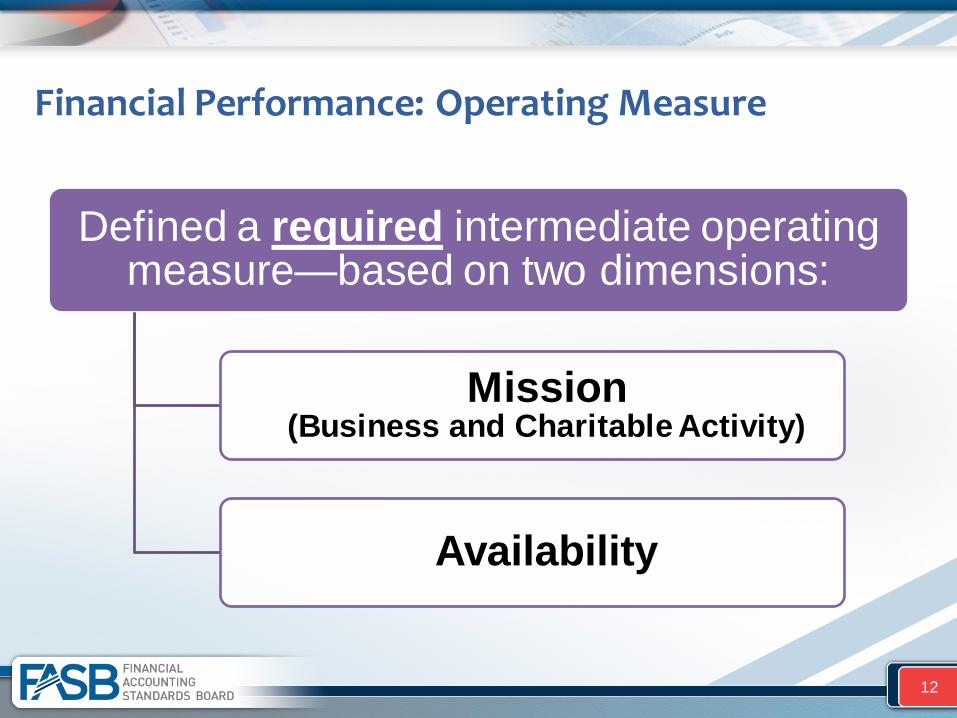

Financial Performance: Operating Measure

12

Defined a required intermediate operating measure—based on two dimensions:

Mission (Business and Charitable Activity)

Availability

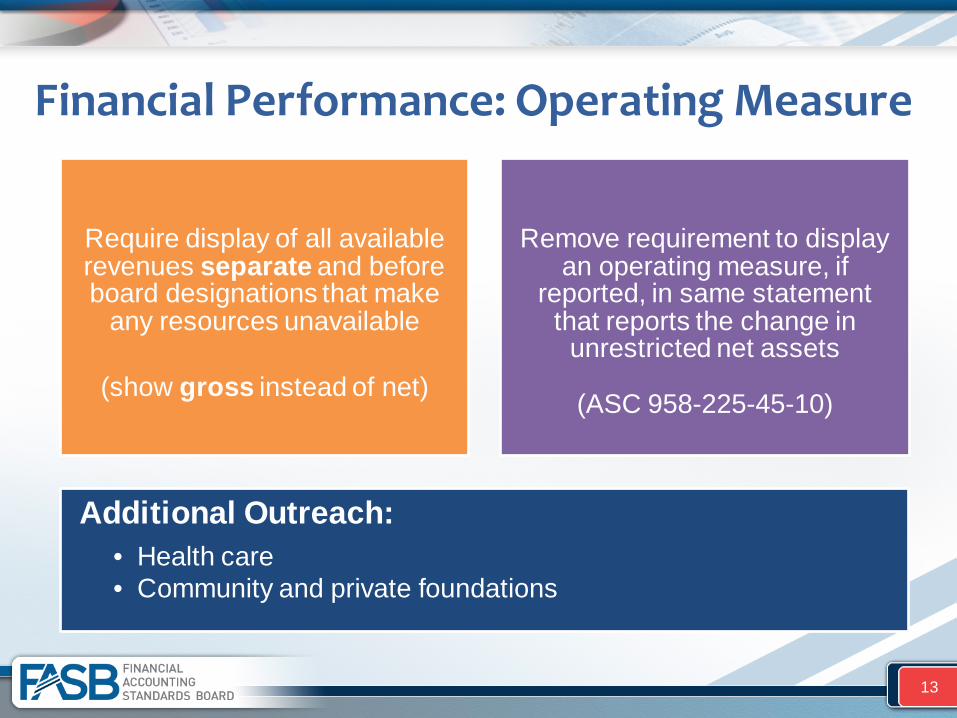

Require display of all available revenues separate and before board designations that make

any resources unavailable

(show gross instead of net)

Remove requirement to display an operating measure, if

reported, in same statement that reports the change in

unrestricted net assets

(ASC 958-225-45-10)

Additional Outreach: • Health care • Community and private foundations

Financial Performance: Operating Measure

13

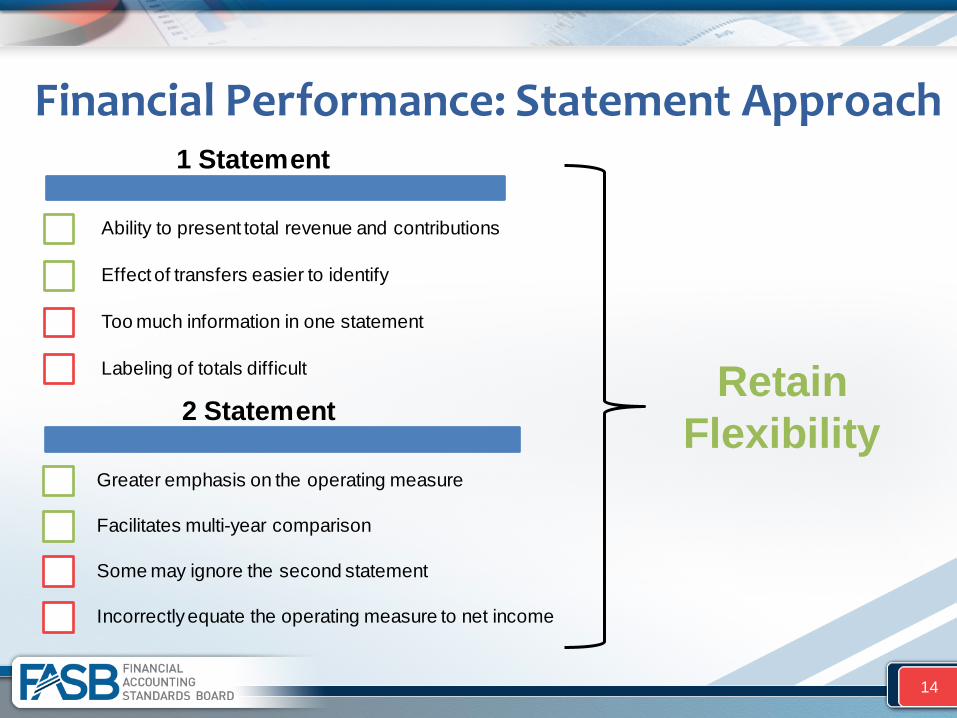

Financial Performance: Statement Approach

14

1 Statement

Ability to present total revenue and contributions

Effect of transfers easier to identify

Too much information in one statement

Labeling of totals difficult

2 Statement

Greater emphasis on the operating measure

Facilitates multi-year comparison

Some may ignore the second statement

Incorrectly equate the operating measure to net income

Retain Flexibility

Without Donor Restrictions

With Donor Restrictions

Total

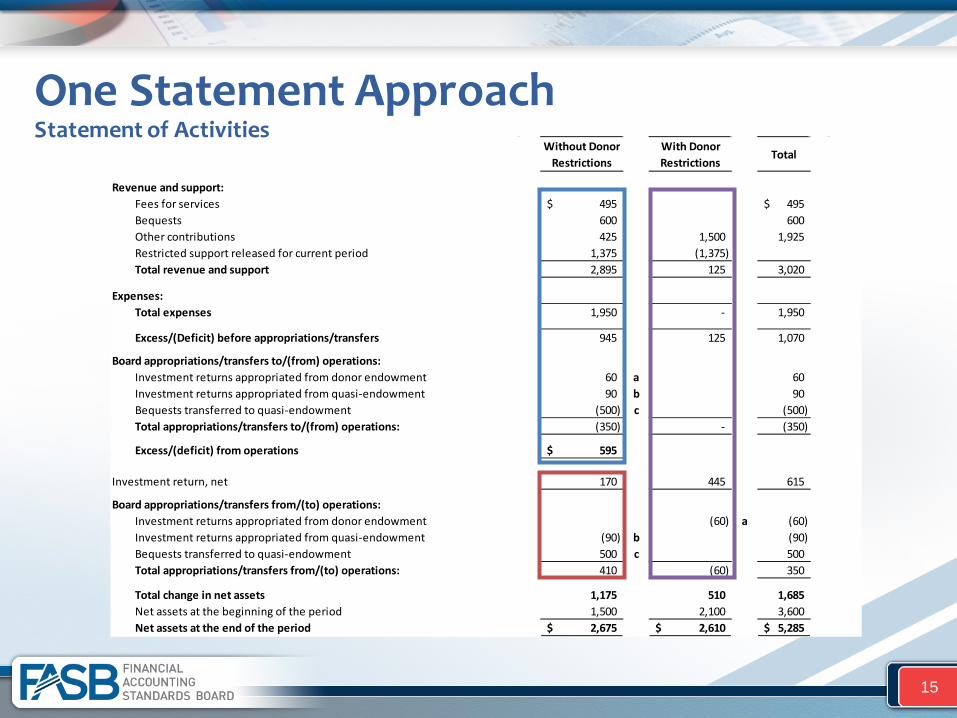

Revenue and support:Fees for services 495$ 495$ Bequests 600 600 Other contributions 425 1,500 1,925 Restricted support released for current period 1,375 (1,375) Total revenue and support 2,895 125 3,020

Expenses:Total expenses 1,950 - 1,950

Excess/(Deficit) before appropriations/transfers 945 125 1,070

Board appropriations/transfers to/(from) operations:Investment returns appropriated from donor endowment 60 a 60 Investment returns appropriated from quasi-endowment 90 b 90 Bequests transferred to quasi-endowment (500) c (500) Total appropriations/transfers to/(from) operations: (350) - (350)

Excess/(deficit) from operations 595$

Investment return, net 170 445 615

Board appropriations/transfers from/(to) operations:Investment returns appropriated from donor endowment (60) a (60) Investment returns appropriated from quasi-endowment (90) b (90) Bequests transferred to quasi-endowment 500 c 500 Total appropriations/transfers from/(to) operations: 410 (60) 350

Total change in net assets 1,175 510 1,685 Net assets at the beginning of the period 1,500 2,100 3,600 Net assets at the end of the period 2,675$ 2,610$ 5,285$

One Statement Approach Statement of Activities

15

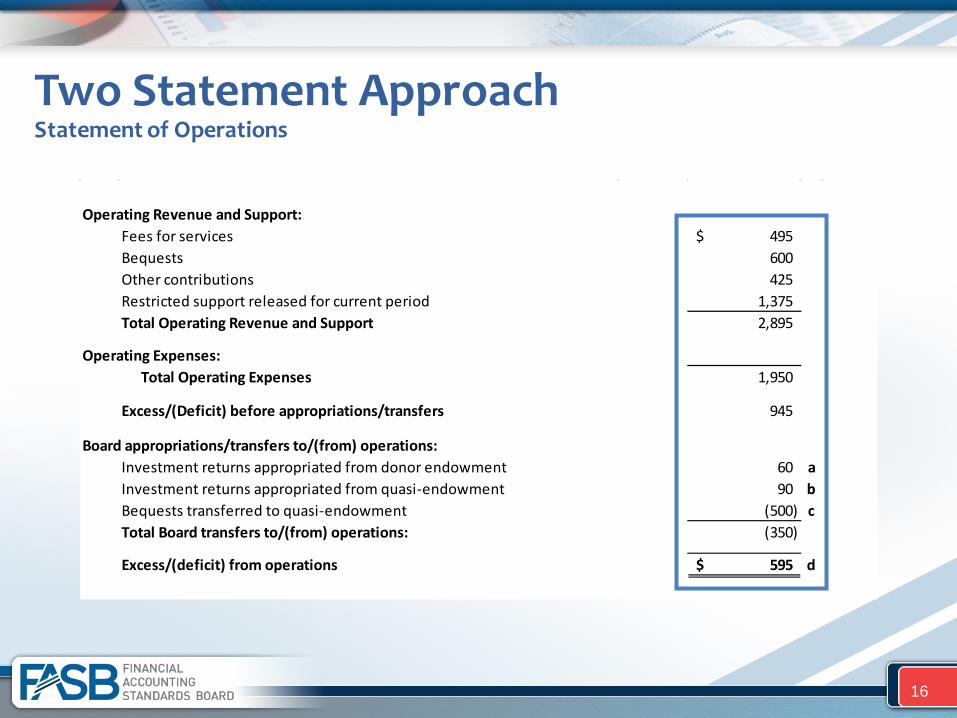

Operating Revenue and Support:Fees for services 495$ Bequests 600 Other contributions 425 Restricted support released for current period 1,375 Total Operating Revenue and Support 2,895

Operating Expenses:Total Operating Expenses 1,950

Excess/(Deficit) before appropriations/transfers 945

Board appropriations/transfers to/(from) operations:Investment returns appropriated from donor endowment 60 aInvestment returns appropriated from quasi-endowment 90 bBequests transferred to quasi-endowment (500) cTotal Board transfers to/(from) operations: (350)

Excess/(deficit) from operations 595$ d

Two Statement Approach Statement of Operations

16

Two Statement Approach (cont’d) Statement of Changes in Net Assets

17

Without Donor

Restrictions

With Donor Restrictions

Total

Excess/(deficit) from operations 595$ d $ 595$

Nonoperating activitiesContributions 1,500 1,500 Restricted support released for current period (1,375) (1,375) Investment return, net 170 445 615

Board designated transfers from/(to) operations:Investment returns appropriated to operations from donor endowment (60) a (60) Investment returns appropriated to operations from quasi-endowment (90) b (90) Bequests transferred to quasi-endowment 500 c 500

Changes in Net Assets 1,175 510 1,685

Net assets at the beginning of the period 1,500 2,100 3,600

Net assets at the end of the period 2,675$ 2,610$ 5,285$

Cash Flow Statement – Issues

18

#1 • Understandability / utility

#2 • Relation to Statement of Activities (and any operating measure therein)

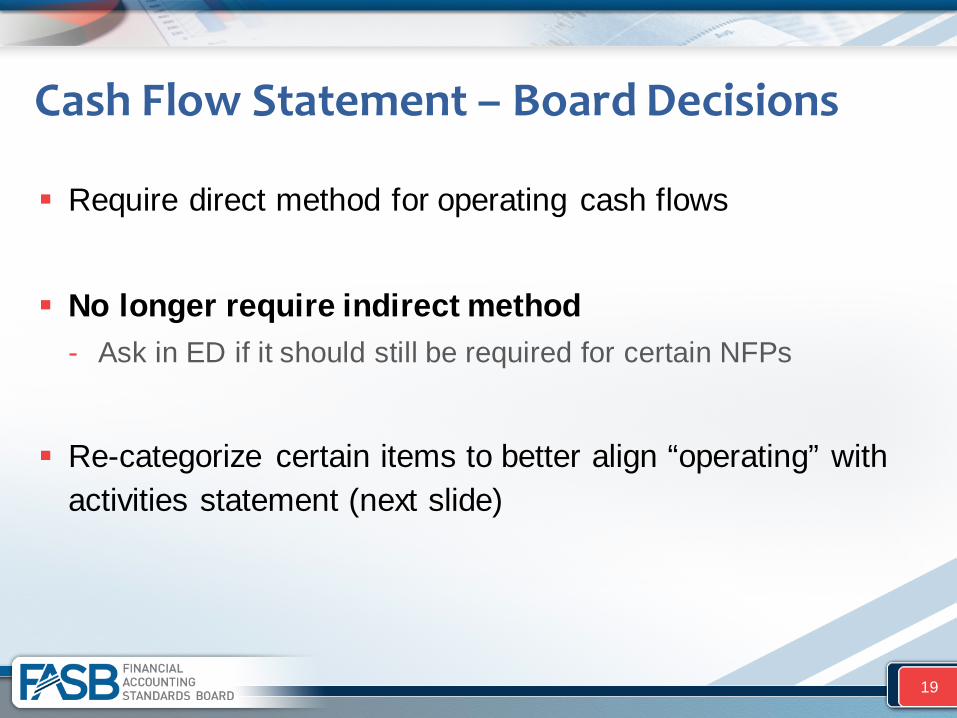

Cash Flow Statement – Board Decisions

Require direct method for operating cash flows

No longer require indirect method - Ask in ED if it should still be required for certain NFPs

Re-categorize certain items to better align “operating” with activities statement (next slide)

19

Cash Flow Statement

20

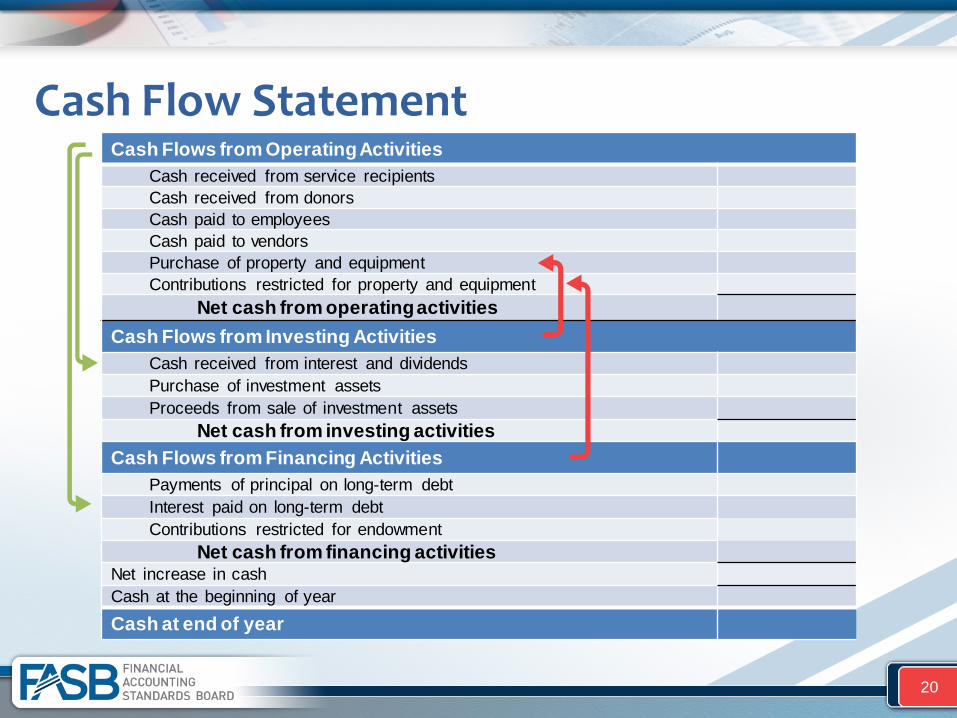

Cash Flows from Operating Activities Cash received from service recipients Cash received from donors Cash paid to employees Cash paid to vendors Purchase of property and equipment Contributions restricted for property and equipment

Net cash from operating activities Cash Flows from Investing Activities

Cash received from interest and dividends Purchase of investment assets Proceeds from sale of investment assets

Net cash from investing activities Cash Flows from Financing Activities

Payments of principal on long-term debt Interest paid on long-term debt Contributions restricted for endowment

Net cash from financing activities Net increase in cash Cash at the beginning of year Cash at end of year

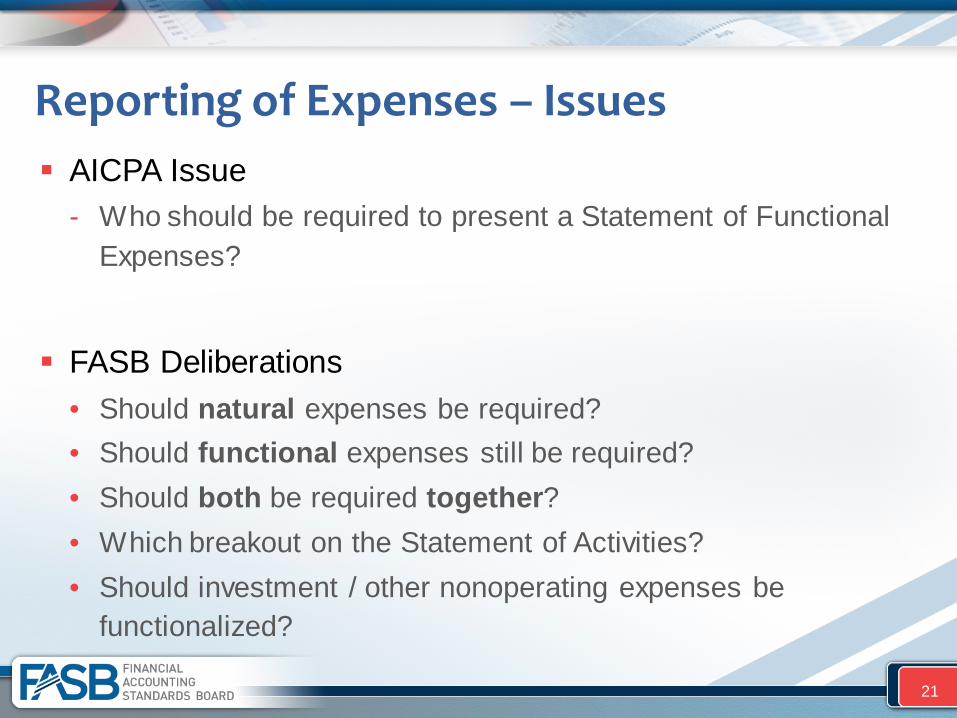

Reporting of Expenses – Issues AICPA Issue

- Who should be required to present a Statement of Functional Expenses?

FASB Deliberations • Should natural expenses be required? • Should functional expenses still be required? • Should both be required together? • Which breakout on the Statement of Activities? • Should investment / other nonoperating expenses be

functionalized? 21

Expense by nature and function one place in the F/S (statement of activities, separate statement, or schedule in notes)

Reporting of Expenses

22

Program Activities Supporting Activities Total

Operating Expenses

Non- Operating

Total Expenses Program A Program B M&G Fundraising

Salaries & Benefits Grants to Others Equipment Rental & Maintenance Occupancy Cost Depreciation Information Technology Professional Service Fees Supplies Travel Printing & Publication Interest Other

Total

F U N C T I O N

NATURE

*

*

*Either (or both) on face of Statement of Activities

Not-functionalized

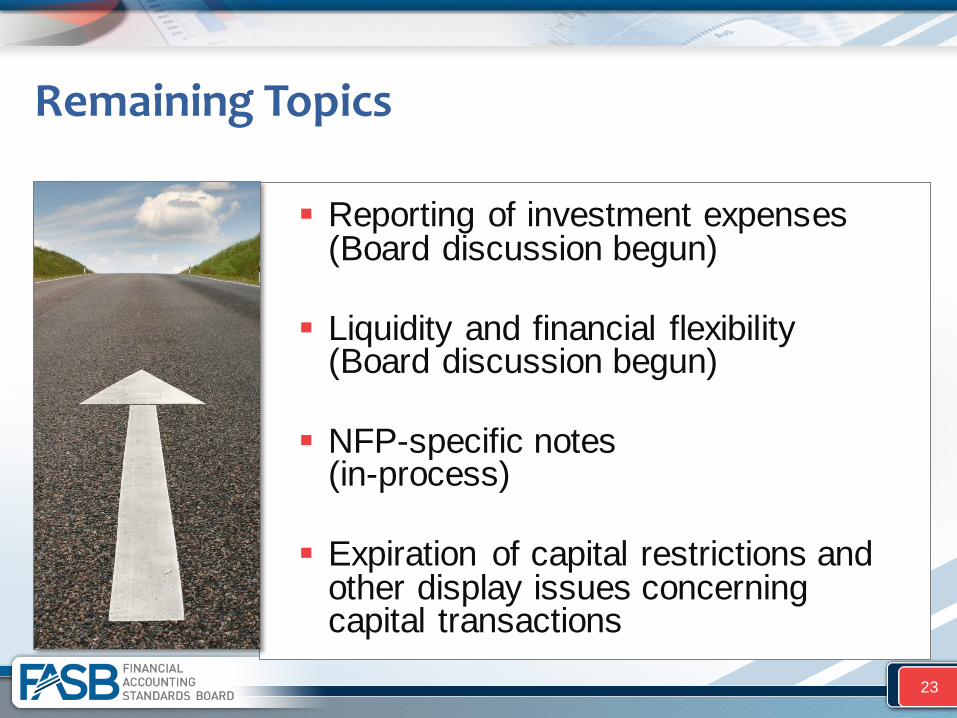

Reporting of investment expenses (Board discussion begun) Liquidity and financial flexibility

(Board discussion begun) NFP-specific notes

(in-process) Expiration of capital restrictions and

other display issues concerning capital transactions

Remaining Topics

23

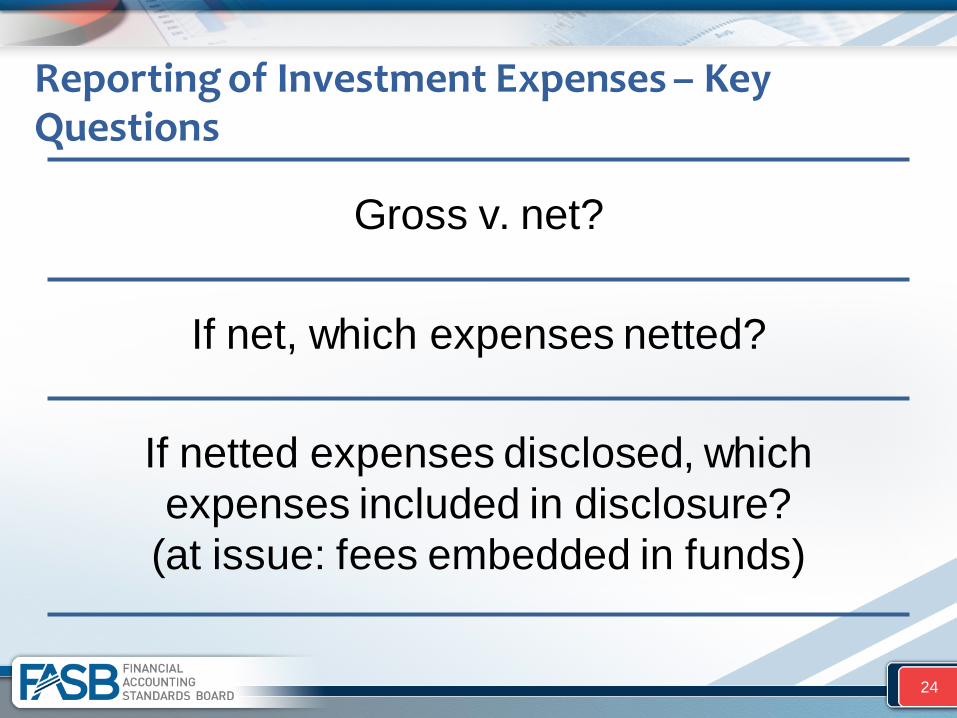

Gross v. net?

If net, which expenses netted?

If netted expenses disclosed, which expenses included in disclosure?

(at issue: fees embedded in funds)

Reporting of Investment Expenses – Key Questions

24

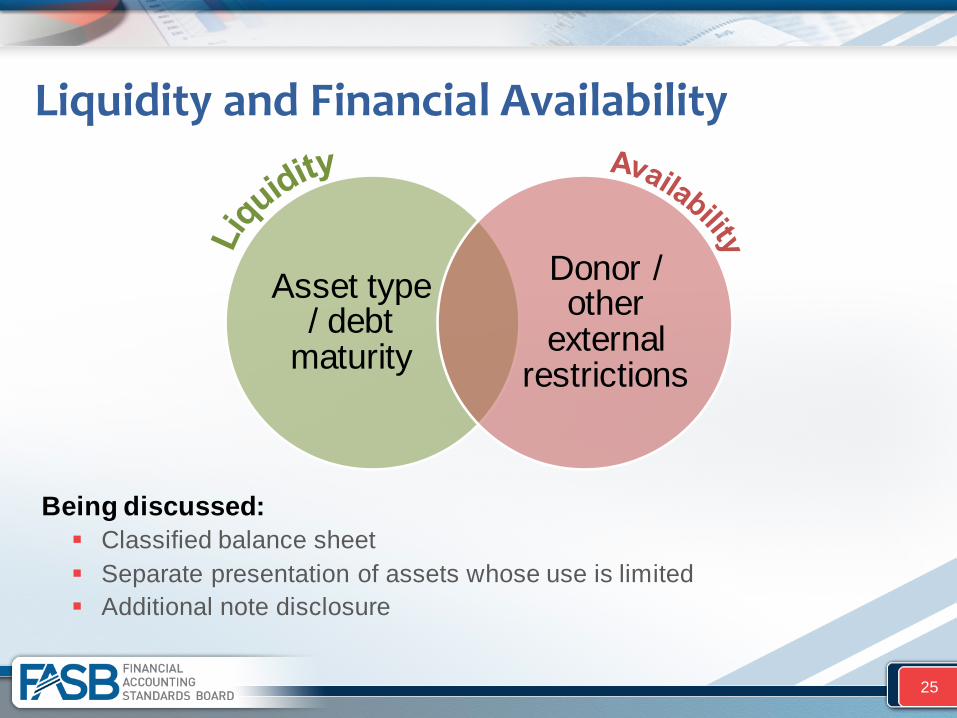

Liquidity and Financial Availability

Being discussed: Classified balance sheet Separate presentation of assets whose use is limited Additional note disclosure

25

Asset type / debt

maturity

Donor / other

external restrictions

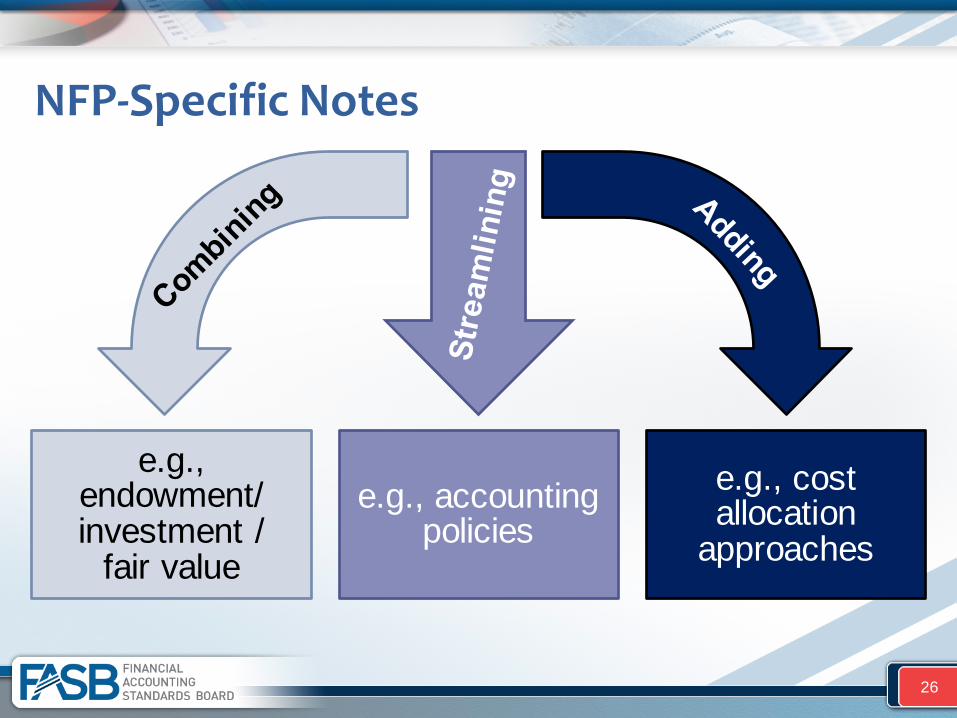

NFP-Specific Notes

e.g., endowment/ investment /

fair value

e.g., accounting policies

e.g., cost allocation

approaches

26

Capital

27

Display alternatives

• Separate line(s) within operating

• Subsection within operating

• Separate section

Expiration of capital restrictions

• Current U.S. GAAP (2 alternatives) 1) when placed in service 2) over time, to match depreciation

• For comparability, do we need to eliminate one of the U.S. GAAP alternatives?

Board Deliberations

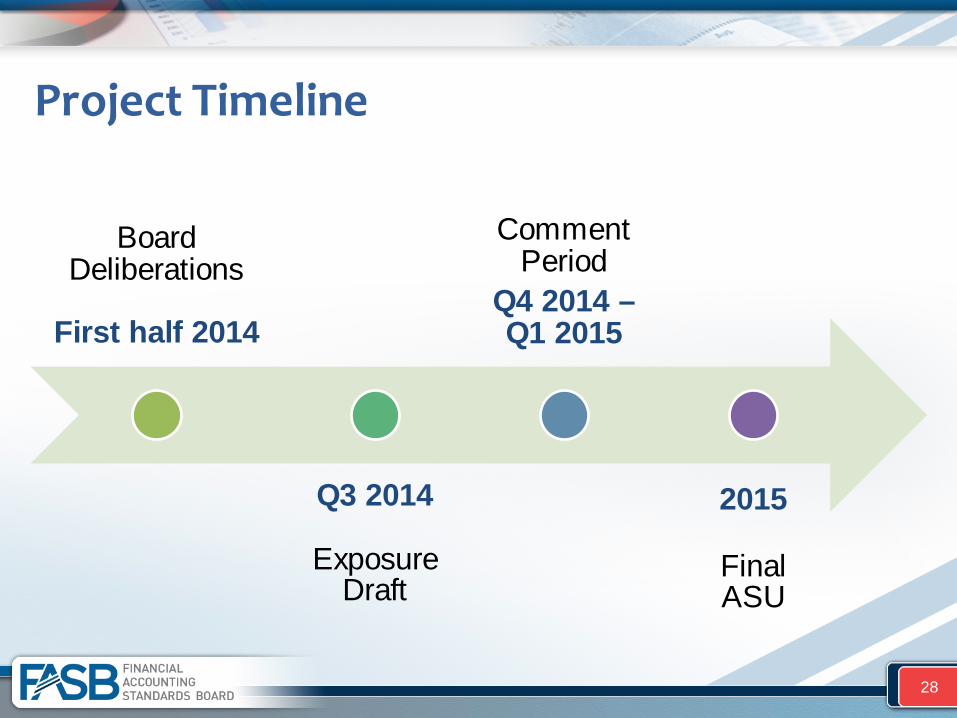

First half 2014

Q3 2014

Exposure Draft

Comment Period

Q4 2014 – Q1 2015

2015

Final ASU

Project Timeline

28

Disclosure Framework Project

29

Objective:

Improve the effectiveness of disclosures in notes to financial statements by clearly communicating the information most important to users of those statements.

Disclosure Framework Project

30

Are financial statements a vehicle for communications with investors? Or are

they more of a compliance exercise?

Field Study Results

31

More guidance around discretion facilitates more qualitative considerations

The word “materiality” has a strong quantitative connotation in practice

Preparers thought notes were generally more effective after applying their assigned discretion criterion

Obstacles in the financial reporting system discourage the application of discretion

Pensions

Fair Value Measurement

Income Taxes

Entity’s Decision Process Next Steps

32

Develop ways the Board can promote the appropriate use of discretion. This will include exploring section-specific disclosure modifications

Examine in the context of the Proposed Statement of Financial Accounting Concepts, Notes to Financial Statements.

Findings may become a basis for other Codification modifications

FASB Simplification Initiative

To reduce narrow sources of unnecessary complexity in current standards - To identify aspects of GAAP that might be streamlined for all

companies—both public and private—as well as for not-for-profit organizations

- To consider whether improvements can be made to simplify GAAP while maintaining or improving the relevance of reported financial information

Objective

34

Types of Complexity To Be Addressed

35

Complicated, dense standard obscures its meaning

Accounting treatment is clear, but applying it is lengthy, convoluted & expensive

Private Company Council (PCC)

36

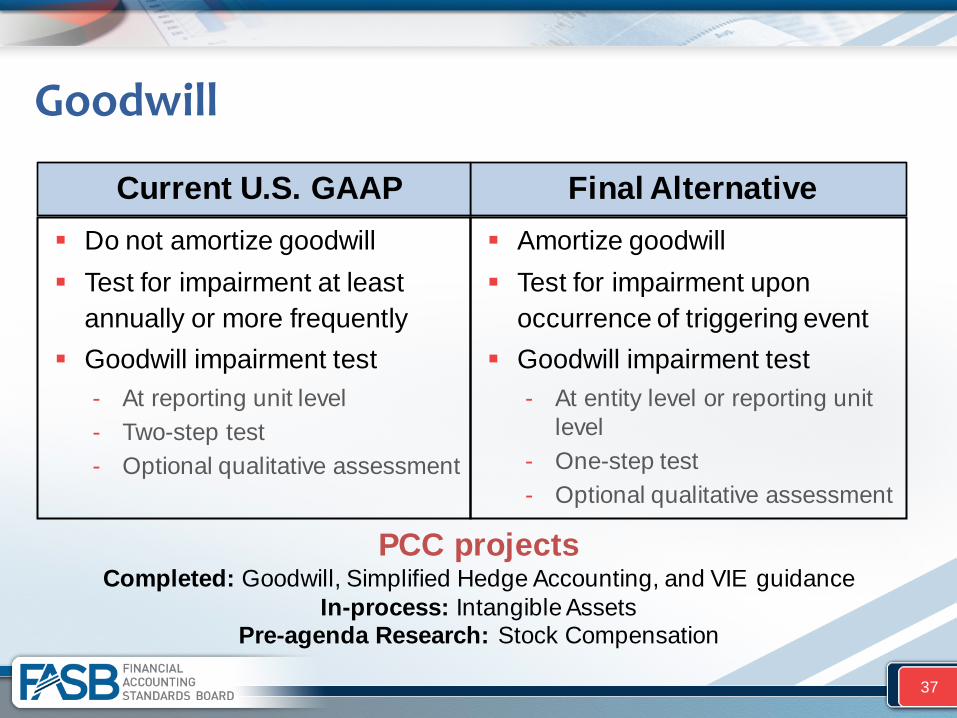

Goodwill

37

Do not amortize goodwill Test for impairment at least

annually or more frequently Goodwill impairment test

- At reporting unit level - Two-step test - Optional qualitative assessment

Amortize goodwill Test for impairment upon

occurrence of triggering event Goodwill impairment test

- At entity level or reporting unit level

- One-step test - Optional qualitative assessment

Final Alternative Current U.S. GAAP

PCC projects Completed: Goodwill, Simplified Hedge Accounting, and VIE guidance

In-process: Intangible Assets Pre-agenda Research: Stock Compensation

Leases

38

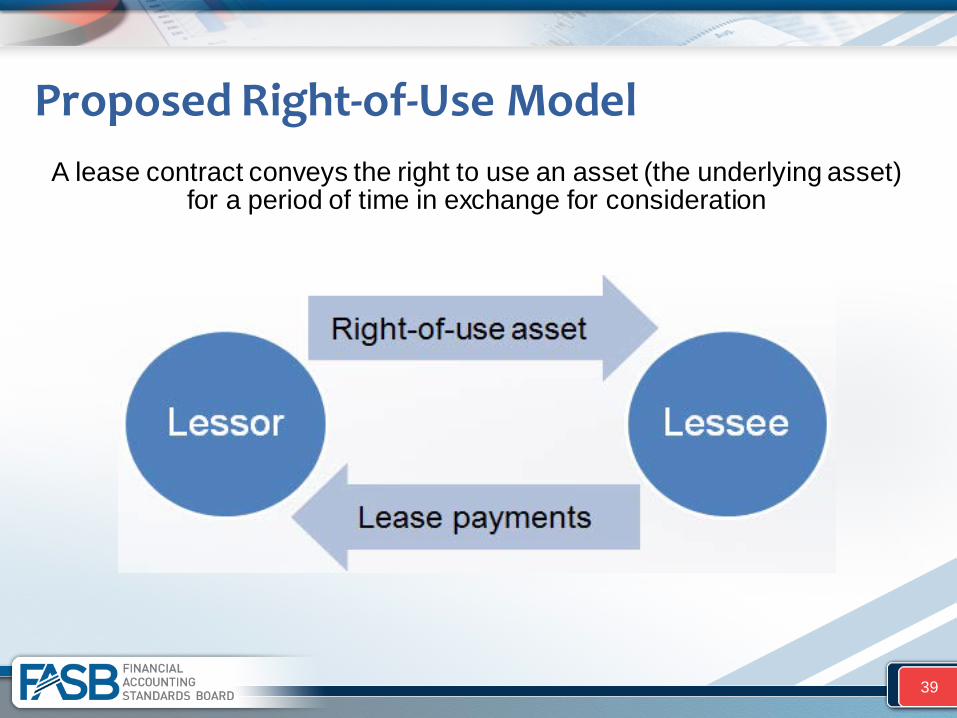

Proposed Right-of-Use Model

39

A lease contract conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration

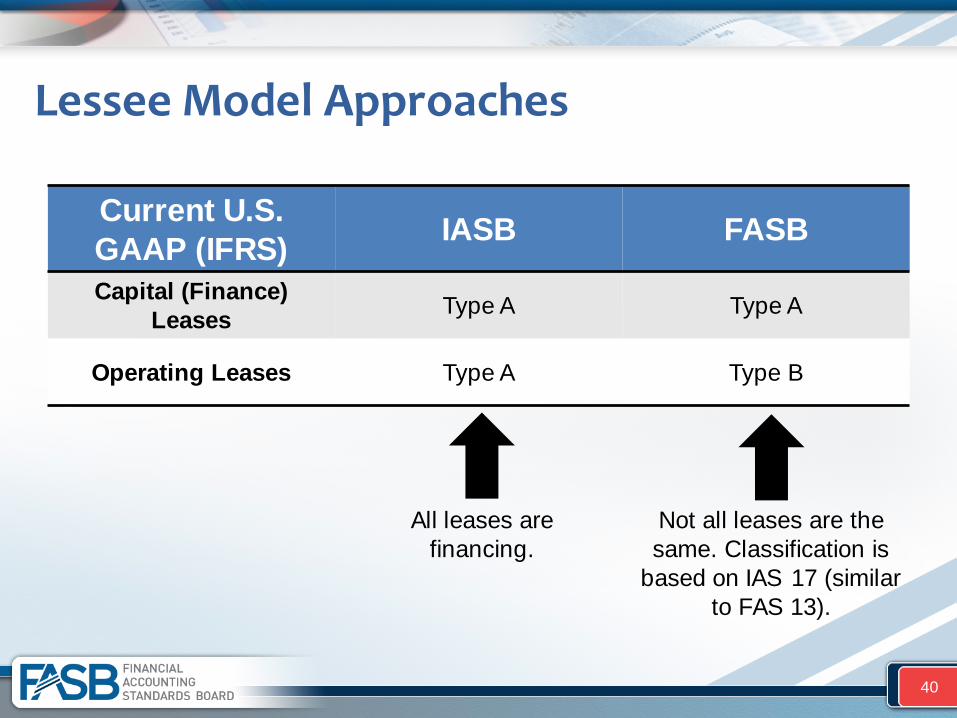

Lessee Model Approaches

40

Current U.S. GAAP (IFRS) IASB FASB

Capital (Finance) Leases Type A Type A

Operating Leases Type A Type B

All leases are financing.

Not all leases are the same. Classification is

based on IAS 17 (similar to FAS 13).

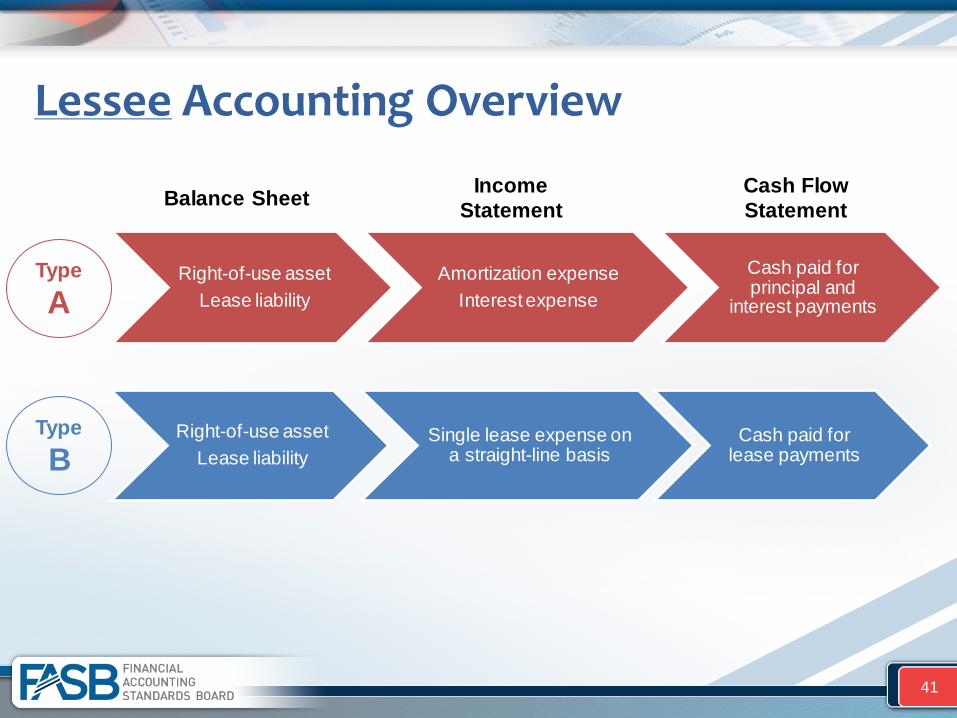

Lessee Accounting Overview

41

Type A

Type B

Right-of-use asset Lease liability

Amortization expense Interest expense

Cash paid for principal and

interest payments

Right-of-use asset Lease liability

Single lease expense on a straight-line basis

Cash paid for lease payments

Income Statement

Cash Flow Statement Balance Sheet

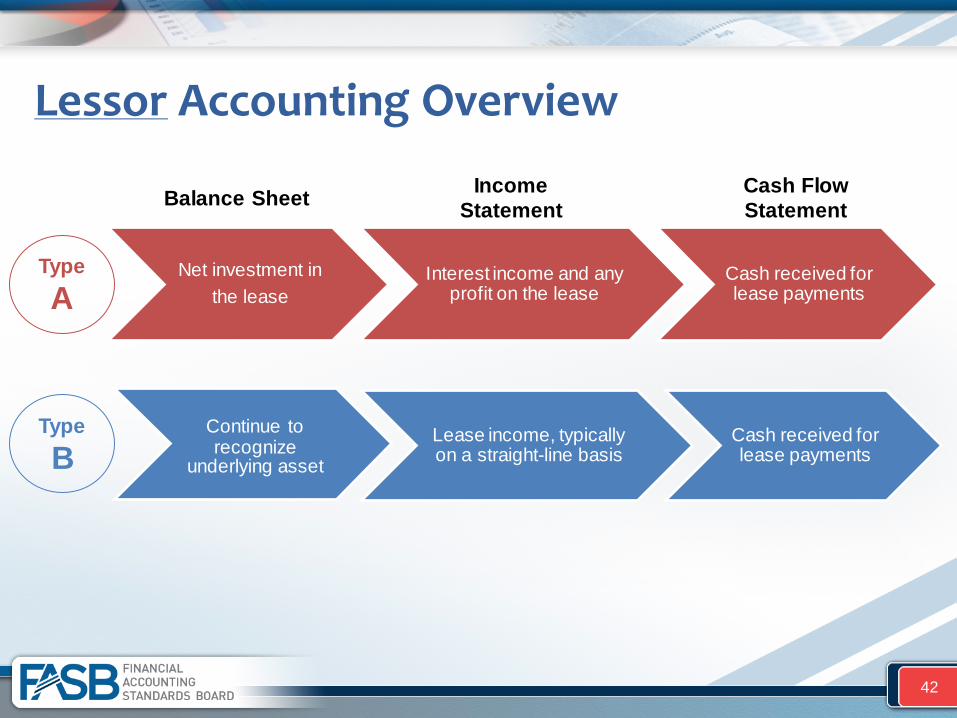

Lessor Accounting Overview

42

Type A

Type B

Net investment in the lease

Interest income and any profit on the lease

Cash received for lease payments

Continue to recognize

underlying asset Lease income, typically on a straight-line basis

Cash received for lease payments

Income Statement

Cash Flow Statement Balance Sheet

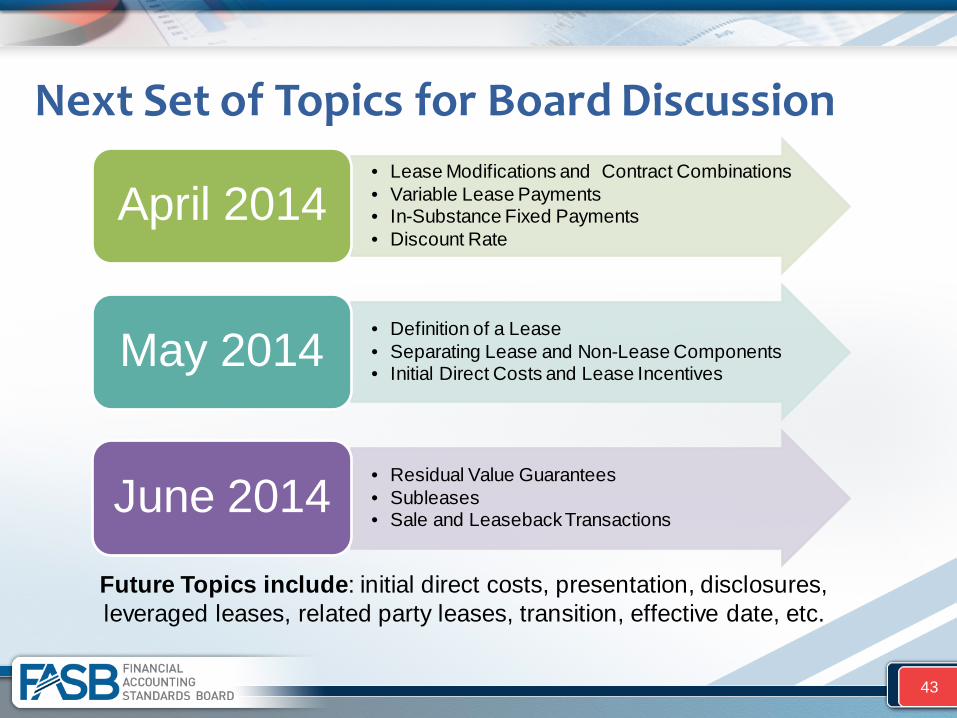

Next Set of Topics for Board Discussion

43

• Lease Modifications and Contract Combinations • Variable Lease Payments • In-Substance Fixed Payments • Discount Rate

April 2014

• Definition of a Lease • Separating Lease and Non-Lease Components • Initial Direct Costs and Lease Incentives

May 2014

• Residual Value Guarantees • Subleases • Sale and Leaseback Transactions

June 2014

Future Topics include: initial direct costs, presentation, disclosures, leveraged leases, related party leases, transition, effective date, etc.

Revenue Recognition

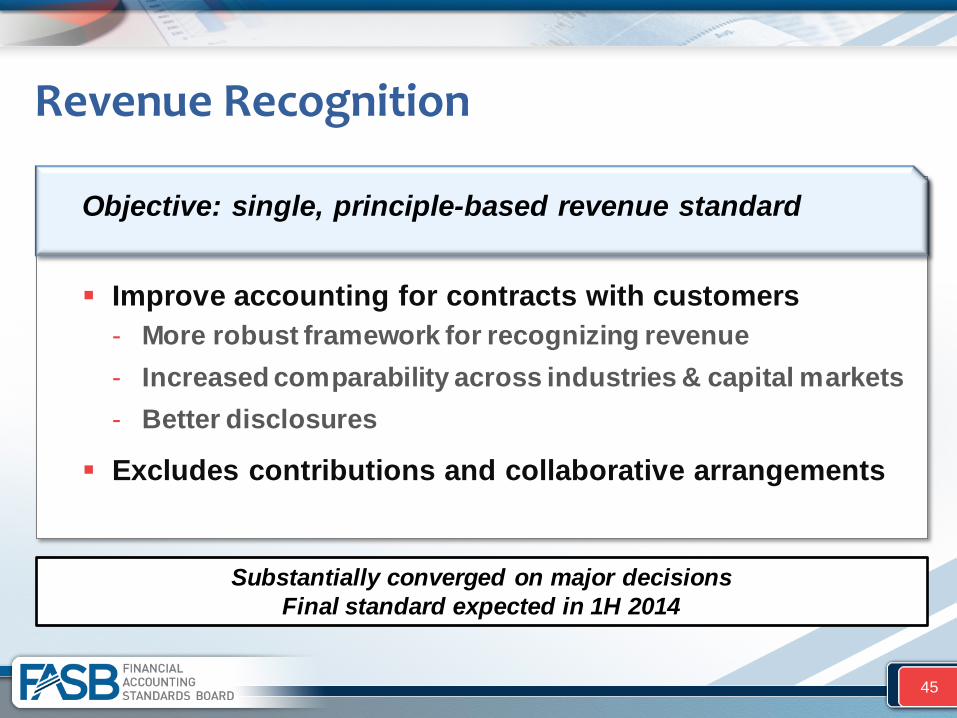

44

Objective: single, principle-based revenue standard Improve accounting for contracts with customers

- More robust framework for recognizing revenue - Increased comparability across industries & capital markets - Better disclosures

Excludes contributions and collaborative arrangements

Revenue Recognition

45

Substantially converged on major decisions Final standard expected in 1H 2014

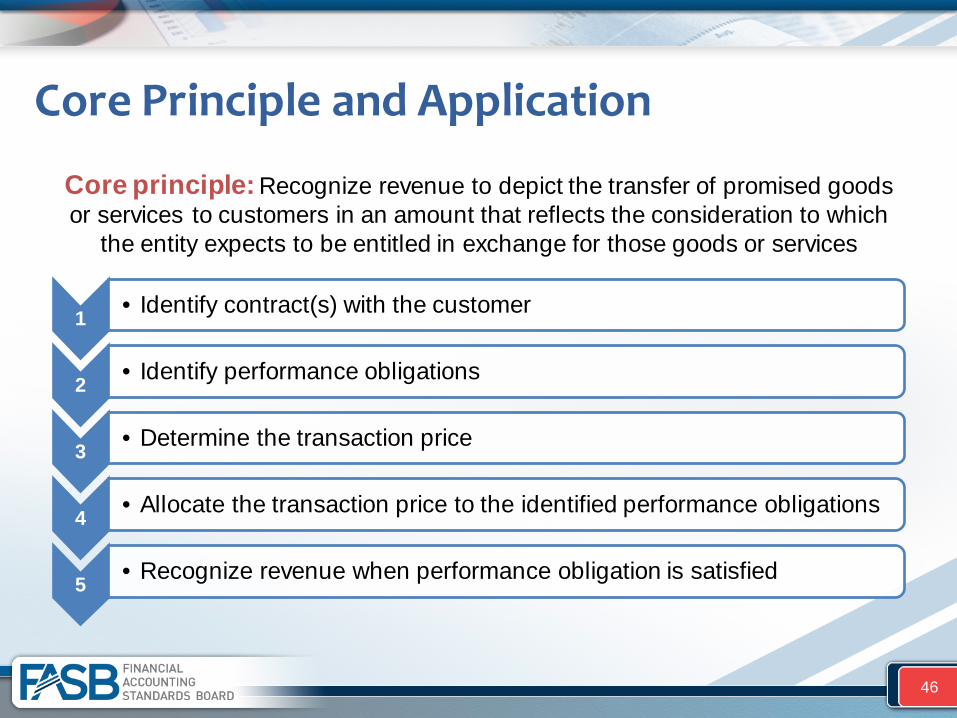

Core Principle and Application

46

1 • Identify contract(s) with the customer

2 • Identify performance obligations

3 • Determine the transaction price

4 • Allocate the transaction price to the identified performance obligations

5 • Recognize revenue when performance obligation is satisfied

Core principle: Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which

the entity expects to be entitled in exchange for those goods or services

Rev Rec—Issuance & Effective Dates: Timeline

47

Issue final standard 2Q 2014

Establish Transition

Resource Group 2Q 2014

Effective Date – Public Entity

Jan. 2017

Effective Date – Nonpublic

Entity Jan. 2018

A nonpublic entity has the option to early adopt (no earlier than a public entity)

An entity may apply the guidance retrospectively, either to

1) Each prior period presented 2) The current period with supplemental footnote disclosures

Government Assistance Disclosures

48

Government Assistance Disclosures

49

Disclosure-only project

Applies to all entities

Scope: TBD

Questions / Comments ?

50