*north s&p pds part a - confidently meet your goalspart_a).pdf ·...

TRANSCRIPT

Issue Number ₈, ₃₀September ₂₀₁₇

North®Super and PensionProduct Disclosure Statement

® Registered trademark of NMMT Limted ABN 42 058 835 573 AFS Licence No. 234653

This is a supplementary product disclosure statement (SPDS) to theNorth®Super andPensionproduct disclosure statement(PDS), issue number 8, dated 30 September 2017 and should be read together with that document.

PDS page reference: 3PDS title reference: Throughout this PDSInstructions: Insert the following rows into the table.

To be read as:References to:

The product disclosure statement for MyNorth Managed Portfolios ARSN 624 544 136, a registeredmanaged investment scheme of which NMMT Limited is the responsible entity, and which is anaccessible investment available through North Super and Pension. The MyNorth Managed PortfoliosPDS is issued by NMMT Limited.

MyNorthManagedPortfolios PDS

Anotional portfolio of assetsmanaged inaccordancewithaparticular investment strategy, as describedin the MyNorth Managed Portfolios PDS.

Managed portfolio

Your interest andassetholdings inMyNorthManagedPortfolios that ismanaged in linewithamanagedportfolio youhave selected. A separate interest andSchemePortfolio is held in respect of eachmanagedportfolio in relation to which you choose to invest.

Scheme Portfolio

PDS page reference: 3PDS title reference: Read all relevant documentsInstructions: Insert the followingparagraphafter theparagraph titledNorth Super andPension–Additional informationbooklet.

MyNorth Managed Portfolios PDSProvides specific information regarding MyNorth Managed Portfolios and the available managed portfolios.

PDS page reference: 11PDS title reference: Fast PaymentInstructions: Replace the section with the following.

Fast paymentThe fast payment of funds is available for partial withdrawals only, up to a maximum of 80% of your account balance. Wereserve the right to reduce the percentage. Wemay advance the payment of your funds without awaiting sale proceedsfrom underlying investments. During this period your cash account balance may fall below zero. Refer to ‘Negative cashaccount balance’ on page 15 for more information on the effect of your cash account balance becoming negative.

Issue date: 13 March 2018

® Registered trademark of NMMT Limited ABN 42 058 835 573 AFS License No. 234653. This document is issued by N.M.Superannuation Proprietary Limited (N.M. Super) ABN 31 008 428 322 AFS Licence No. 234654. N.M. Super is a member ofthe AMP group. The information provided in this product disclosure statement is general information only and does nottake into account your personal financial situation or needs. You should obtain financial advice tailored to your personalcircumstances.

1

North® Super and PensionSupplementary product disclosure statement

Fast Track withdrawalThe Fast Track withdrawal is available for a full cash withdrawal request of your account. You will receive 80% of your fundswithin two business days of your request being completed (including all requirements) by the North Service Centre. Theremainder of the fundswill be released after all other assets have been sold and the proceeds have been confirmed to cash.

Telegraphic TransferA Telegraphic Transfer (TT) is a fast electronic transfer to a nominated bank account. A $9 charge applies per TT. The fundsmay be cleared in the recipient’s bank account within two hours of the payment being made.

PDS page reference: 14PDS title reference: Your cash accountInstructions: Replace the second, third and fourth paragraphs with the following.

To help youmanage your cash account you have the flexibility to nominate a Target cash balance by specifying aMinimumcash balance (dollar amount) and/or a Target cash percentage (a percentage of your total account balance) to be held inyour cash account.

A default Target cash percentage of 5% and $0 Minimum cash balance will apply where no selection is made. Both theMinimum cash balance and Target cash percentage can be adjusted at any time.

Your Target cash balance is calculated as follows:

(Account balance x Target cash percentage) + Minimum cash balance = Target cash balance.

For example; where the Account balance is $100,000, the Minimum cash balance is $0 (default) and the Target cashpercentage is 5% (default), then the Target cash balance is calculated as:

($100,000 x 5%) + $0 = $5,000

If you increase your Minimum cash balance from $0 to $1,000 then the Target cash balance is calculated as:

($100,000 x 5%) + $1,000 = $6,000.

PDS page reference: 14PDS title reference: Cash account sweepsInstructions: Replace the section titled Cash account sweepswith the following.

Cash account sweepsWhen the balance of your cash account exceeds your Target cash balance by $500, the excess cash will be invested as peryour investment instructions. In order for the cash account sweep to take place, the excess cashmustmeet the transactiontrade minimums as defined in the 'At a glance section' of this PDS.

If the balance of your cash account falls below your Minimum cash balance, we will sell your assets as per your investmentinstructions to bring your cash account back to your Target cash balance. In order for the cash account sweep to take place,transaction trademinimumsmust bemet.Where you have not provided uswith adequate investment instructionswewillsell your managed funds proportionately.

Where you hold listed securities, the sweepmust result in a trade amount of at least your specified shares trademinimum,per listed security, for the sweep tooccur. Thedefault shares trademinimum is $650per listed security.Where thisminimumis not met, we will not sell your assets and your cash account balance will remain below your Minimum cash balance.

Term Deposits will not be sold to bring your cash account balance back to your target cash balance.

2

PDS page reference: 14PDS title reference: Your cash accountInstructions: Insert a new section after the section titled Earnings on your cash account.

Your cash account and MyNorth Managed PortfoliosYour cash accountwill be used for the purposes of settling all transactions in relation to your Scheme Portfolio(s), including:– settling transactions relating to the assets held as part of your Scheme Portfolio when it is rebalanced. This includes:

receiving net proceeds from a disposal of assets (disposal proceeds), and reinvesting those amounts to acquireother assets as part of your Scheme Portfolio; and

–

– making additional investments in circumstances where a rebalance involves a disposal of certain assets and acorresponding acquisition of substitute assets at the same time, andmarket movements result in the proceedsfromtheasset disposal being less than the costs of theasset acquisition (theamountof theadditional investmentfrom your cash account in these circumstances will be equal to the difference between the relevant disposalproceeds and acquisition costs);

– receiving income fromunderlying assets, and reinvesting these amounts (except in relation to thosemanagedportfolioswhere such amounts are not reinvested into your Scheme Portfolio the MyNorth Managed Portfolio PDS for details);

– pay any fees, expenses, taxes and or charges in relation to your investment in MyNorth Managed Portfolios.

You provide us with standing instructions to facilitate your investment in MyNorth Managed Portfolios and use your cashaccount in this way. The standing instructions you give to us are set out in the account details authorisation form that youwill complete prior to opening an account.

Refer to theMyNorthManagedPortfolios PDS for further information relating to theuse of your cash accountwhilst investedin MyNorth Managed Portfolios.

PDS page reference: 16PDS title reference: Investment optionsInstructions: The following replaces the first paragraph.

Investment optionsNorth offers you a wide range of investment options to choose from:– over 440 managed funds, including both Australian and international investments across a variety of asset classes– a range of listed securities including; companies in the S&P/ASX300, selected exchange traded funds (ETFs), exchange

traded commodities (ETCs), listed investment companies (LICs), listed investment trusts (LITs), andAustralian real estateinvestment trusts (AREITs),

– Managed Portfolios, and– term deposits with a range of providers and varying terms

3

PDS page reference: 19PDS title reference: Investment optionsInstructions: Insert the following new section immediately after the Does the Trustee invest in derivatives? section.

MyNorth Managed PortfoliosMyNorth Managed Portfolios is a non-unitised registered managed investment scheme, offering access to a range ofmanaged portfolios. NMMT Limited issues interests in, and is the responsible entity for, MyNorth Managed Portfolios.

NMMT Limited's role as responsible entity is separate to its role as service provider to NM Super in connection with NorthSuper and Pension.

Managed portfolios are designed to deliver a flexible and efficient means of gaining exposure to different asset classes.

You can instruct us to invest in MyNorth Managed Portfolios via your North Super and Pension account.

When you invest in MyNorth Managed Portfolios through North Super and Pension, we will make an application to theresponsible entity to establish an interest in the scheme, which we will hold in your account in relation to each particularmanaged portfolio that you select.

The responsible entitywill thenuse the funds invested fromyourNorth Super andPensionaccount to construct your SchemePortfolio by acquiring assets that are consistent with the managed portfolio you select. This will be done in proportionsthat match (as closely as practicable) the set asset allocation of the managed portfolio.

Your Scheme Portfolio will be managed by the responsible entity in line with the investment strategy applicable to themanaged portfolio you have selected. See the MyNorth Managed Portfolios PDS for details of the available managedportfolios and applicable investment strategies.

The interest inMyNorthManagedPortfolios is held for youbyus, under the termsofNorth Super andPension. All underlyingassets held in your Scheme Portfolio are held for the responsible entity by the custodian.

You direct us to use your cash account for the purposes of settling all transactions in relation to your Scheme Portfolio.Please refer to the 'Your cash account and MyNorth Managed Portfolios' section for further information.

A copy of theMyNorthManaged Portfolios PDS is available atnorthonline.com.au or by contacting theNorth Service Centreon 1800 667 841. You should consider theMyNorthManaged Portfolios PDS in deciding whether to acquire, or continue tohold, an interest in MyNorth Managed Portfolios through North Super and Pension.

4

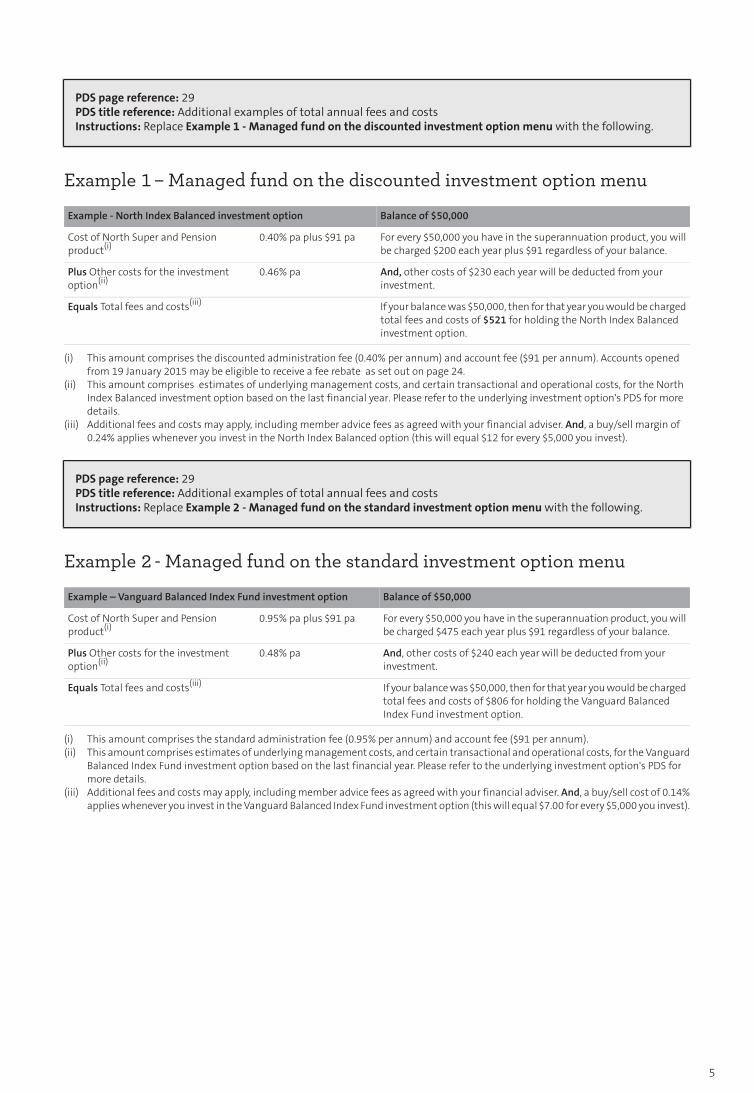

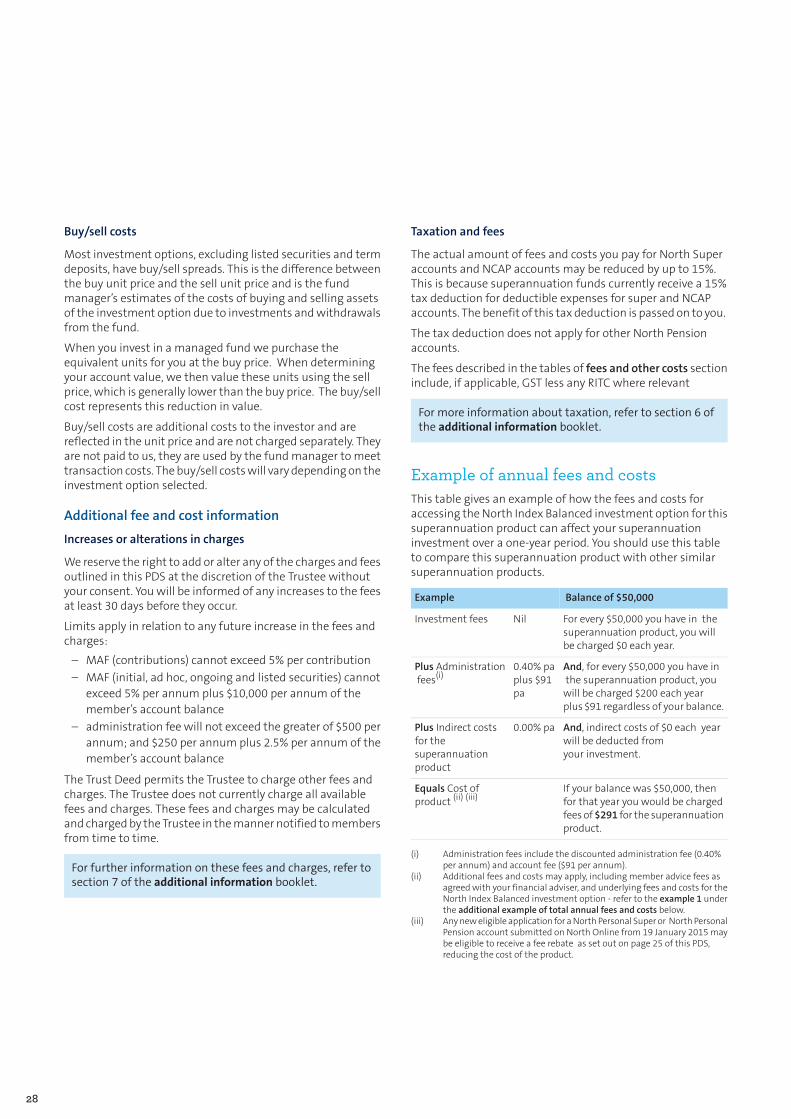

PDS page reference: 29PDS title reference: Additional examples of total annual fees and costsInstructions: Replace Example 1 - Managed fund on the discounted investment option menuwith the following.

Example ₁– Managed fund on the discounted investment option menu

Balance of $50,000Example - North Index Balanced investment option

For every $50,000 you have in the superannuation product, you willbe charged $200 each year plus $91 regardless of your balance.

0.40% pa plus $91 paCost of North Super and Pensionproduct(i)

And, other costs of $230 each year will be deducted from yourinvestment.

0.46% paPlus Other costs for the investmentoption(ii)

If your balancewas $50,000, then for that year youwould be chargedtotal fees and costs of $521 for holding the North Index Balancedinvestment option.

Equals Total fees and costs(iii)

This amount comprises the discounted administration fee (0.40% per annum) and account fee ($91 per annum). Accounts openedfrom 19 January 2015 may be eligible to receive a fee rebate as set out on page 24.

(i)

This amount comprises estimates of underlying management costs, and certain transactional and operational costs, for the NorthIndex Balanced investment option based on the last financial year. Please refer to the underlying investment option's PDS for moredetails.

(ii)

Additional fees and costs may apply, including member advice fees as agreed with your financial adviser. And, a buy/sell margin of0.24% applies whenever you invest in the North Index Balanced option (this will equal $12 for every $5,000 you invest).

(iii)

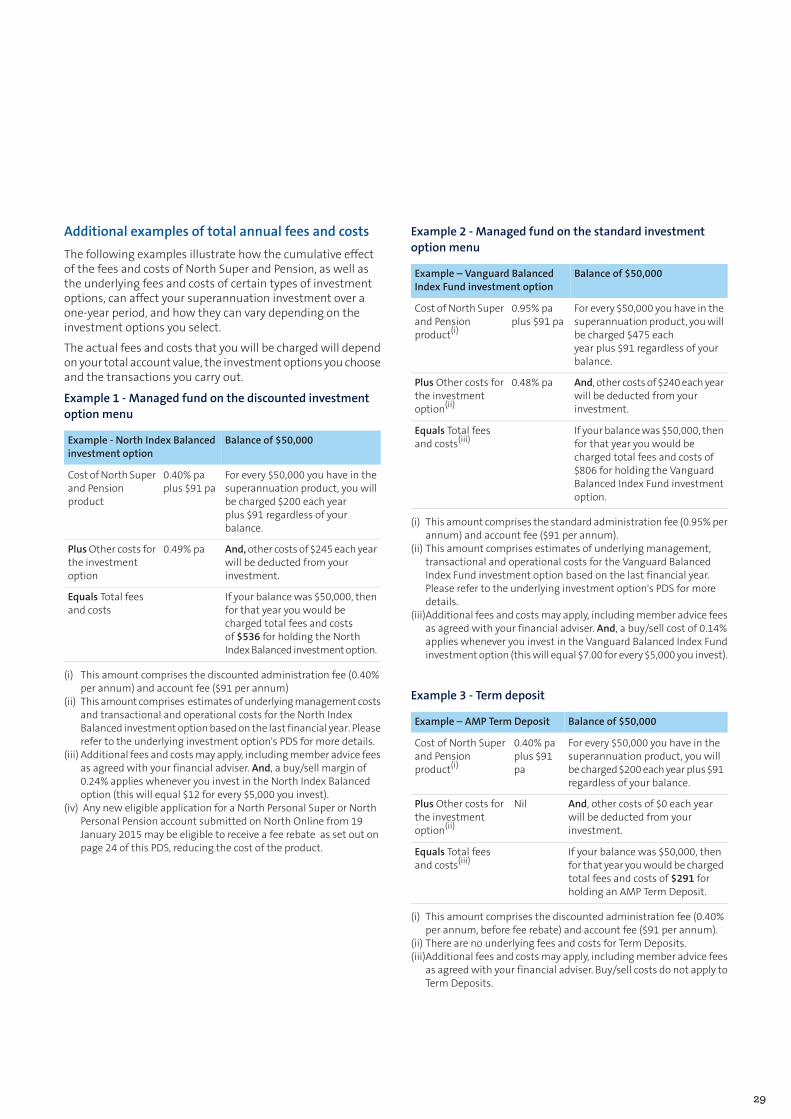

PDS page reference: 29PDS title reference: Additional examples of total annual fees and costsInstructions: Replace Example 2 - Managed fund on the standard investment option menuwith the following.

Example ₂ - Managed fund on the standard investment option menu

Balance of $50,000Example – Vanguard Balanced Index Fund investment option

For every $50,000 you have in the superannuation product, youwillbe charged $475 each year plus $91 regardless of your balance.

0.95% pa plus $91 paCost of North Super and Pensionproduct(i)

And, other costs of $240 each year will be deducted from yourinvestment.

0.48% paPlus Other costs for the investmentoption(ii)

If your balancewas $50,000, then for that year youwouldbe chargedtotal fees and costs of $806 for holding the Vanguard BalancedIndex Fund investment option.

Equals Total fees and costs(iii)

This amount comprises the standard administration fee (0.95% per annum) and account fee ($91 per annum).(i)This amount comprises estimates of underlyingmanagement costs, and certain transactional and operational costs, for the VanguardBalanced Index Fund investment option based on the last financial year. Please refer to the underlying investment option's PDS formore details.

(ii)

Additional fees and costsmay apply, includingmember advice fees as agreedwith your financial adviser. And, a buy/sell cost of 0.14%applieswhenever you invest in theVanguardBalanced Index Fund investment option (thiswill equal $7.00 for every $5,000 you invest).

(iii)

5

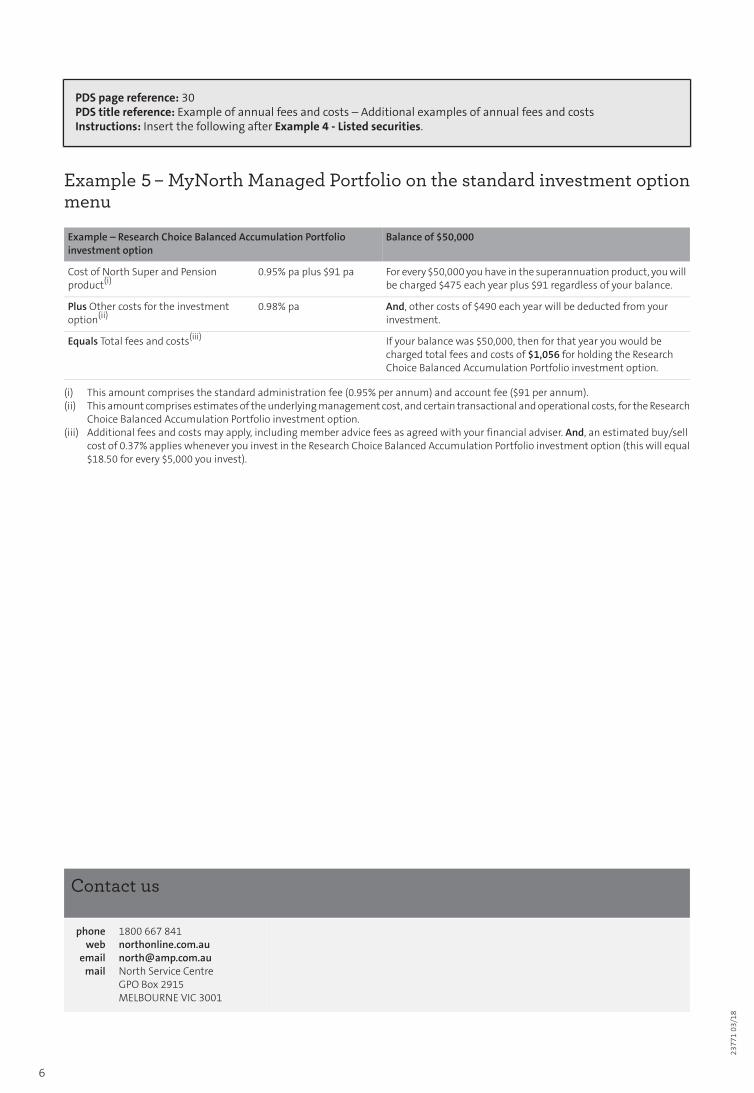

PDS page reference: 30PDS title reference: Example of annual fees and costs – Additional examples of annual fees and costsInstructions: Insert the following after Example 4 - Listed securities.

Example ₅– MyNorth Managed Portfolio on the standard investment optionmenu

Balance of $50,000Example – Research Choice Balanced Accumulation Portfolioinvestment option

For every $50,000 youhave in the superannuation product, youwillbe charged $475 each year plus $91 regardless of your balance.

0.95% pa plus $91 paCost of North Super and Pensionproduct(i)

And, other costs of $490 each year will be deducted from yourinvestment.

0.98% paPlus Other costs for the investmentoption(ii)

If your balance was $50,000, then for that year you would becharged total fees and costs of $1,056 for holding the ResearchChoice Balanced Accumulation Portfolio investment option.

Equals Total fees and costs(iii)

This amount comprises the standard administration fee (0.95% per annum) and account fee ($91 per annum).(i)This amount comprises estimates of theunderlyingmanagement cost, and certain transactional andoperational costs, for theResearchChoice Balanced Accumulation Portfolio investment option.

(ii)

Additional fees and costs may apply, including member advice fees as agreed with your financial adviser. And, an estimated buy/sellcost of 0.37% applies whenever you invest in the Research Choice Balanced Accumulation Portfolio investment option (this will equal$18.50 for every $5,000 you invest).

(iii)

Contact us

1800 667 [email protected] Service CentreGPO Box 2915MELBOURNE VIC 3001

phoneweb

emailmail

6

2377103/18

North Super and Pension are plans offered as a part of theWealthPersonal SuperannuationandPensionFund (the Fund).The Trustee of the Fund and issuer of this Product DisclosureStatement (PDS) is N.M. Superannuation Proprietary Limited(NM Super) ABN 31 008 428 322, a member of the AMP groupof companies.

North Super is not a MySuper authorised product.

The Trustee is an RSE Licensee under the SuperannuationIndustry (Supervision) Act 1993 (SIS), which means that wehave satisfied licensing conditions set by the AustralianPrudential Regulation Authority (APRA). The Trustee isresponsible for the monitoring and management of the Fundfor thebenefit of allmembers in accordancewith thegoverningrules of the Fund and relevant legislation.

Product Disclosure Statement

Information regardingNorthSuper (USI 92381911598002) andPension (USI 92381911598001) is contained in the ProductDisclosure Statement (PDS) and other documents being, theAdditional Information Booklet and the North investmentoptions document.

Important: North Personal Superannuation and PersonalPension is closed to newmembers of the Wealth PersonalSuperannuation and Pension Fund (the Fund) effective 12March 2016. No applications for newmembers to the Fundwill be accepted from this date. If you hold an existing NorthPersonal Super account, North Personal Pension account,Summit® Personal Super account, Summit Personal Pensionaccount, Generations® Personal Super account, GenerationsPersonal Pensionaccount, ipac iAccess®Personal Super accountor ipac iAccess Allocated Pension account as at 12March 2016,you can still apply for a North Super and Pension account

Optional insurance cover is available to members of NorthSuper and Pension through insurance arranged with AMP LifeLimited ABN 84 079 300 378 AFSL No 233 671. Please refer tothe AMP Elevate insurance PDS.

The information in this document is of a general nature onlyand is not basedon your personal objectives, financial situationor needs. You should consider whether the information in thisdocument is appropriate for you in accordance with yourobjectives, financial situation and needs. You should read thePDS and the other documents before making any decisionabout whether to acquire or continue to hold your account.

Changes to the PDS

Information in the PDS and the other documents may changefrom time to time. Wemay have updated information whichis not materially adverse by issuing a PDS Update. You canobtain a PDS Update free of charge by:– visiting northonline.com.au– contacting the North Service Centre to request a paper

copy of the PDS Update at [email protected] or 1800667 841

– asking your financial adviser.

NM Super and other providers

NMSuper is theTrusteeof theWealthPersonal Superannuationand Pension Fund and is referred to as NM Super, Trustee,weor us in this PDS.

Noother company in theAMPgroupof companies (AMPgroup)or any of the investmentmanagers of the investment options:– is responsible for any statements or representationsmade

in this PDS– guarantees the performance of NM Super’s obligations to

members nor assumes any liability to members inconnection with North Super and Pension.

Except as expressly disclosed in the PDS or the Northinvestment options document, investments in the investmentoptions are not deposits or liabilities of NM Super, AMP BankLimited ABN 15 081 596 009 AFSL No 234 517 (AMP Bank), anyother member of the AMP group or any of the investmentmanagers. NM Super is not a bank. AMP Bank does not standbehind NM Super. The investment options are subject toinvestment risks, which could include delays in repayment andloss of income and capital invested.

AMP companies receive fees and charges in relation to NorthSuper and Pension outlined in the PDS. AMP employees anddirectors receive salaries and benefits from the AMP group.

This offer is available only to persons receiving (includingelectronically) the PDSwithinAustralia.We cannot accept cashor applications signed and mailed from outside Australia.Monies must always be paid in Australian dollars. Wemayaccept or refuse (without reason) any application.

We reserve the right to change the features ofNorth Super andPensionwith, case of an increase in fees, at least 30days’ notice,otherwise notice of material changes will be provided beforeor as soon as practicable after the change occurs.

Issued by NM Superannuation Proprietary Limited ABN 31 008 428 322 AFSL No 234 654, the trustee of the Wealth Personal Superannuation and Pension Fund ABN92 381 911 598.

2

Important information

AustralianBusinessNumber (ABN)49079 354 519

AMP Limited

ABN 22 003 257 225Australian Financial Services (AFS)Licence No. 234655

ipac asset managementlimited (ipac)

ABN 88 079 804 676 LimitedAMP Group Holdings Limited

ABN 31 008 428 322AFS Licence No. 234654

N.M. SuperannuationProprietary Limited (NMSuper)

ABN 42 058 835 573AFS Licence No. 234653

NMMT Limited (NMMT)

Super Product Identification Number(SPIN) NMS0001AU

North PersonalSuperannuationandPersonalPension Unique Superannuation Identifier

(USI)Super: 92381911598002Pension: 92381911598001

ABN 84 079 300 379AFS Licence No. 233671

AMP Life Limited (AMP Life)

ABN 92 381 911 598Wealth PersonalSuperannuation and PensionFund

Throughout this PDSTo be read as:References to:

AMP Limited and its subsidiaries, including AMPLife, NMMT and NM Super

AMP

Wealth Personal Superannuation and PensionFund

Fund

AMP Group Holdings LimitedAMP GH

AMP Elevate Insurance Product DisclosureStatement

Insurance PDS

Amember of North Personal Superannuationand Personal Pension

Member of you

AMP Life Limited - issuer of Elevate insuranceAMP Life

NMMTLimited –provider of investment servicesto the Trustee

NMMT

North Personal Superannuation and PersonalPension plans

North, NorthSuper andPension

A list of investment options availablewithNorthSuper and Pension

North InvestmentOptions

N.M. Superannuation Proprietary LimitedTrustee, our, we orus

northonline.com.auNorth, NorthOnline

Read all relevant documentsVisit northonline.com.au to download a copy of the followingdocuments. Alternatively, a printed copy can be obtained freeof charge by contacting the North Service Centre [email protected] or on 1800 667 841.

North Super and Pension – Additionalinformation bookletThis Additional information booklet summarises the keyfeatures and benefits of North Super and Pension.

Further information on the topics in this PDS is provided in theAdditional information booklet.

North investment optionsProvides a list of investment options available through NorthSuper and Pension.

You can obtain free of charge the underlying investmentoptions' PDS by:

- visiting northonline.com.au

- contacting the North Service Centre on 1800 667 841 or

- visiting the Fund managers website.

Also considerAMP Elevate insurance PDS

Explains the insurance benefits available on AMP Elevate,including:– life Insurance– Additional optional insurancebenefits (includingTotal and

Permanent Disability (TPD))– income Insurance.

3

Contents

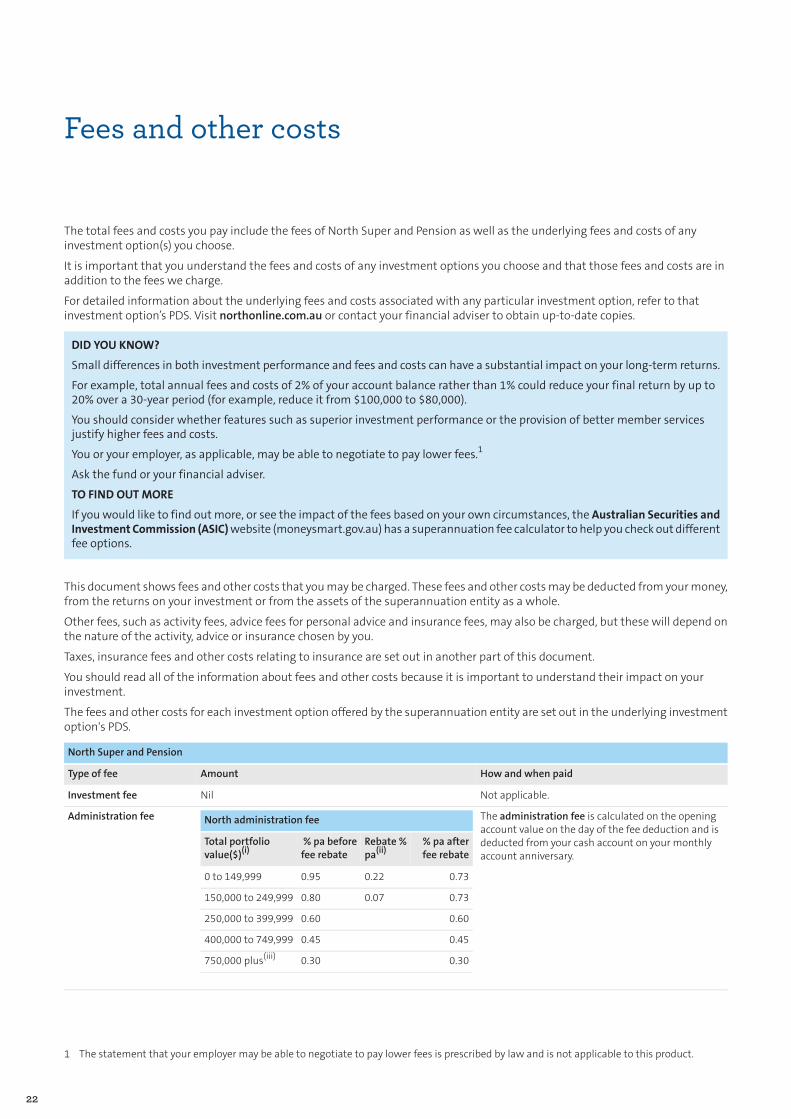

5At a glance

8Welcome to North Super and Pension

10North Super

12North Pension

14What is the cash account?

16Investing in North Super and Pension

20What risks apply to investing?

22Fees and other costs

32AMP Elevate insurance

33Howwill the benefit be paid upon death?

34What else do you need to know?

4

Minimum transactions

$2,000Minimum initial contribution,rollover or transfer to commenceyour account(i)

Nominimum(ii)Minimum ad hoc contribution orrollover or transfer(i)

$10 per fortnight, month, quarter, half-year or yearMinimum regular savings plan

NominimumMinimum ad hoc withdrawal

$100(iii)Minimum switch

$1,000(iii)Minimum rebalance

Automatic Buy: $500(iii)Minimum cash account sweep

Automatic Sell: $500(iii)

Product features

Non-concessional contributions can be made to your super account via direct debit from your bank accountfortnightly, monthly, quarterly, half-yearly or yearly.

Regular savings plan

A flexible working cash account that allows you to specify the minimum and target amounts to be held inyour cash account.

Cash account

Income distributions, dividends and interest for each investment option where applicable will be credited toyour cash account. Exceptions may apply. A dividend reinvesment plan (where available) may be nominatedfor listed securities. Refer to the income section on page 19 for full details.

Income

You can switch all or part of your portfolio between the full range of investment options available at anytime. There is no limit on the number of switches you can make each year.

Investment switching

You can arrange automatic buying and selling of investment options via your cash account. You can alsospecify instructions to rebalance your investments.

Investment instructions

To assist with your estate planning you may nominate beneficiaries through a:Payment of benefits on death– binding death benefit nomination– non-lapsing binding death benefit nomination– non-binding death benefit nomination– reversionary pension

Your financial adviser can help you to choose the best method for your particular circumstances.

Non-concessional contributions can be made to your super account using direct debit via North Online.You can also use an EFT or BPAY facility provided by your bank.

BPAY®, EFT and ad hoc direct debit

Allows you to invest a set dollar amount into the market at regular intervals. Available only on North Super.Dollar cost averaging

Wemay advance payment of partial withdrawal up to 80% of your account value without awaiting saleproceeds from the investment options. Restrictions may apply.

Fast payment

You may elect to split your super contributions with your spouse.Contribution splitting

® Registered to BPAY Pty Ltd ABN 69 079 137 518

5

At a glance

Investment options

.North offers you the option to choose your investment form:Investmentoptions 1. Discounted investment options -range of active and index funds, diversifiedmulti-manager investment options

offering access to specialist fund managers in each asset class and term deposits.2. Standard investment options - offers an extensive list of multi-manager and single manager funds, listedsecurities, selected Australian real estate investment trusts (AREIT), exchange traded funds (ETF), exchange tradedcommodities (ETC), listed investment companies (LICs), listed investment trusts (LITs) and term deposits.Refer to theNorth InvestmentOptions document for full details,which canbeobtained fromyour financial adviser,northonline.com.au/north or you can obtain a free copy by contacting the North Service Centre on 1800 667 841.

AMP Elevate insurance North Super and NCAP Personal Pension

Life InsuranceLife insuranceAvailable coverLife and TPD insuranceIncome insurance

Note:The insuranceoptions are issuedbyAMPLife via a separate PDS. The currentAMPElevate insurance PDS shouldbe consideredwhendecidingwhether to acquire that product. The current AMP Elevate insurance PDS is available from your financial adviser, northonline.com.au/north orby contacting the North Service Centre on 1800 667 841.

Fees and costs(iv)(v)

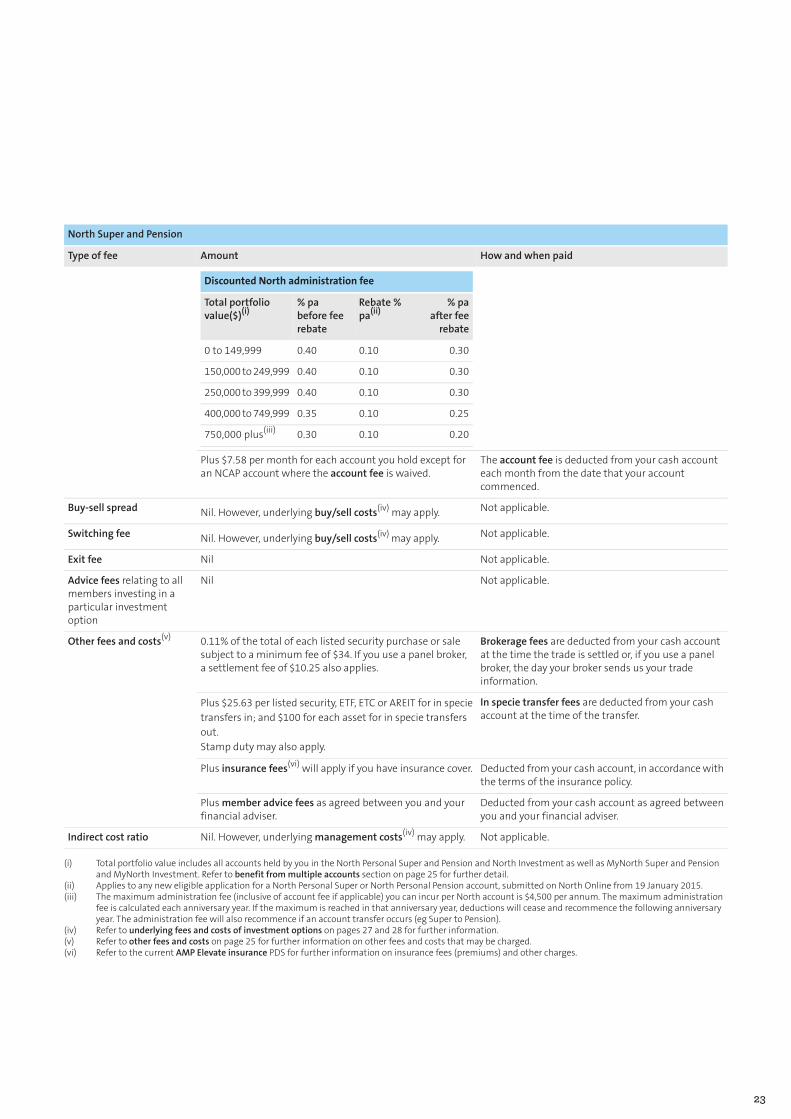

$0 for North Super and Pension accounts with an NCAP.Account fee$91 pa for North Super and North Pension accounts.

0.00% to0.95%paof your accountbalance, dependingonyour total portfolio value and your choice of investmentoptions. Themaximum administration fee (inclusive of account fee if applicable) you can incur across all NorthSuper, North Pension and North Investment accounts held by you is $4,500 pa.

Administration fee

The fees associated with purchasing or selling listed securities.Brokerage feesCharged at 0.11% of the total of each listed security purchase or sale subject to a minimum fee of $34.If you use a panel broker (third party broker) a settlement fee of $10.25 applies in addition to any brokeragefees. For a list of approved panel brokers and their terms and conditions, refer to North Online.

$25.63 per listed security, ETF, ETC or AREIT for transfers in; andIn specie transfer fee$100 for each asset transferred out.

These fees and costs apply to the investment options selected by you and your financial adviser. You can findan up-to-date list of the underlying investment option fees and costs reflecting the underlying investmentoption's PDSdisclosure onNorthOnlineor in theNorth InvestmentOptionsdocument. For detailed informationabout the underlying fees and costs associated with any particular investment option you should refer to therelevant PDS for that investment option.

Underlying fees and costs forinvestment options

6

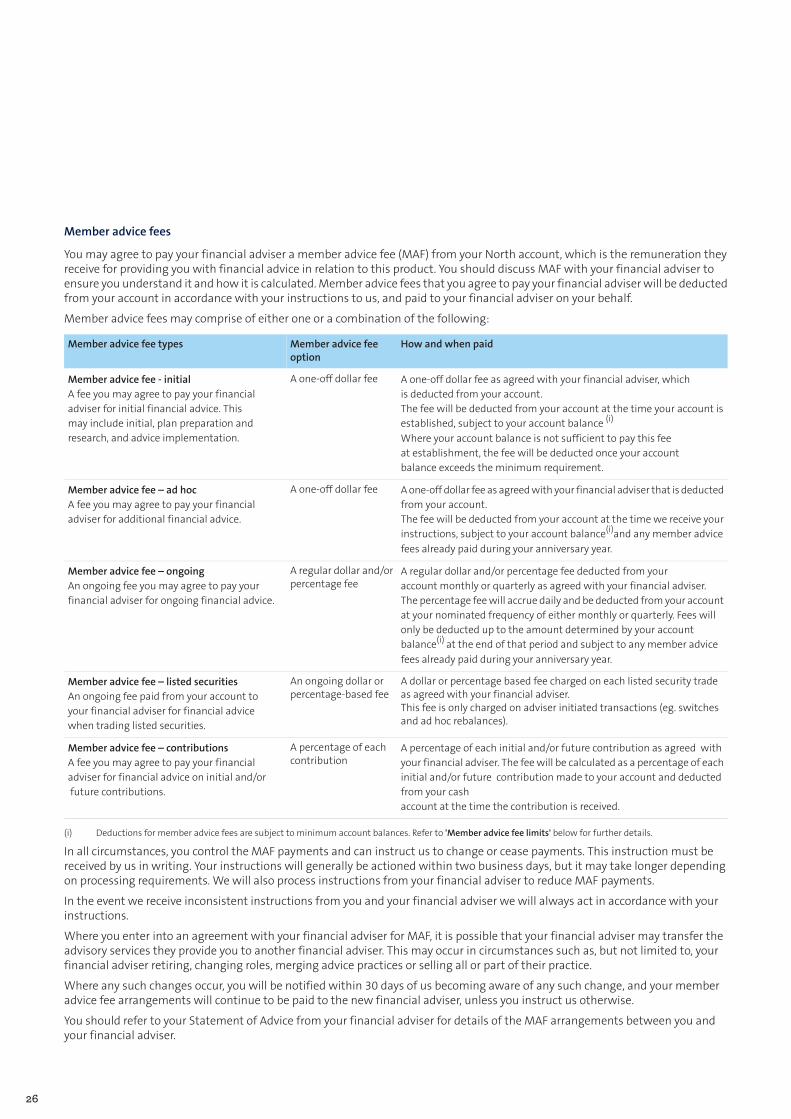

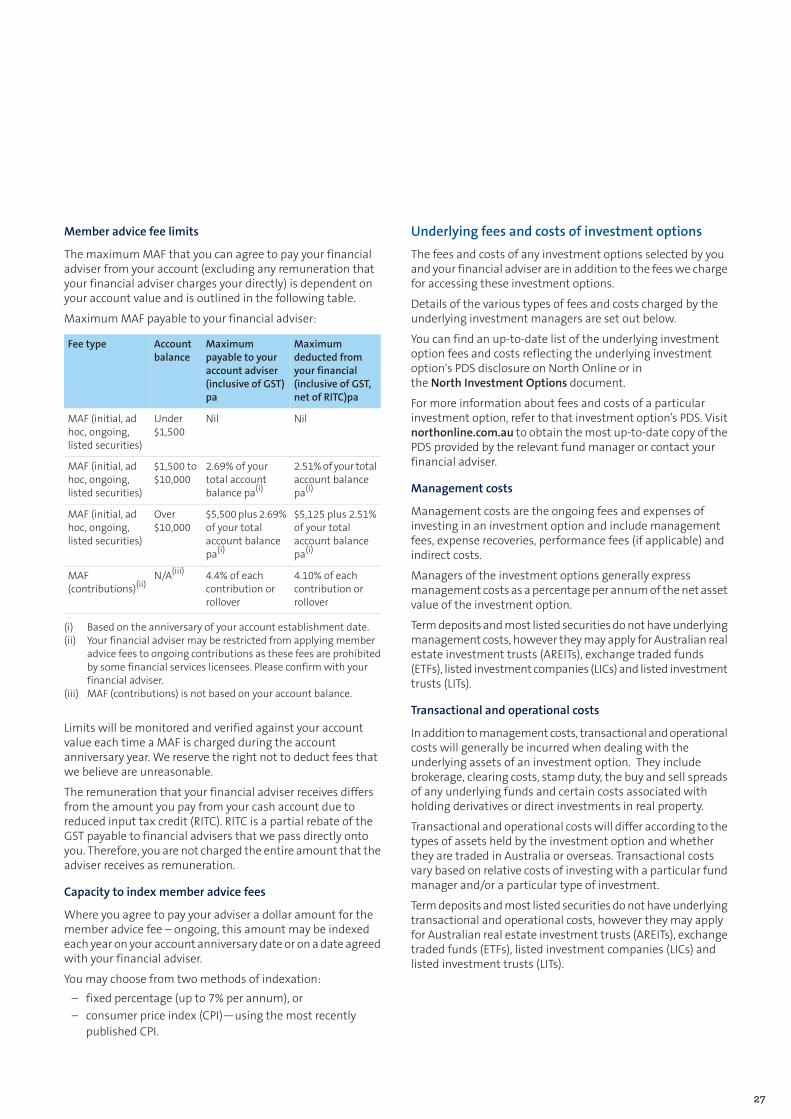

Member advice fees(iv)(vi)

Fees you can agree to pay your financial adviser for financial advice

Up to $5,125 pa plus 2.51%pa subject to your portfoliobalance

A fee paid from your account to your financial adviser for initial financialadvice. This may include initial, plan preparation and research, and adviceimplementation.

Member advice fee – initial

A feepaid fromyour account to your financial adviser for additional financialadvice.

Member advice fee – ad hoc

Anongoing fee paid fromyour account to your financial adviser for ongoingfinancial advice.

Member advice fee – ongoing

An ongoing dollar or percentage-based fee paid from your account to yourfinancial adviser for financial advice for trading listed securities.

Member advice fee – listed securities

Up to 4.10% of eachcontribution or rollover

A fee paid from your account to your financial adviser for financial adviceon initial and/or future contributions or rollovers.

Member advice fee – contributions

Reporting

All communications are issued via North Online and can be accessed in your personal filing cabinet.Online access

The Trustee annual report for the Fundwith information current as at 30 Juneof that yearwill be availableonline at northonline.com.au/north from 31 December.

Trustee annual report

Pension members can only make rollovers or transfers into their account.(i)A maximum contribution or rollover of $10 million applies for North Super and Pension accounts. The government has introduced a newtransfer balance cap of $1.6 million (indexed in line with CPI in $100,000 increments) effective from 1 July 2017. Please speak to your financialadviser to understand how it may impact your income in retirement.

(ii)

These transactions above are subject to a trade minimum of $650 per listed security held.(iii)All fees are inclusive of GST, less any reduced input tax credits where relevant.(iv)For details of all fees and costs refer to pages 22 to 30.(v)For all details of member advice fees refer to pages 26 and 27.(vi)

7

North Super

North Super helps you to save and grow your super so that youcan retire right. It offers a diverse range of investment options,favourable tax treatment on contributions and earnings, feeaggregation a regular savings plan facility and much more.

When you’re ready to retire, you can transfer your savings toa North Pension account.

Superannuation is a long-term investment designed forretirement.

North Pension

North Pension turns your super savings into regular pensionpayments. It offers you a tax effectiveway to spend your super,with taxoffsets and tax-free earnings. You can choose to investinanallocatedpensionor anon-commutable allocatedpension(NCAP).

Allocated pension

An allocated pension can be purchased with unrestrictednon-preserved superannuation benefits and it pays you aregular income stream to help you meet your financial needsin retirement. Depending on your individual circumstances,allocatedpensions allowyou to enjoy themany tax advantagesof superannuation and the possible benefits of social security.

It also includes an innovative retirement solution that canhelpyou maximise what you can spend in retirement.

Non-commutable allocated pension (NCAP)

An NCAP allows you to commence a pension with preservedand unrestricted non-preserved superannuation benefits. Youcan access a regular income streamwhile seeking to transitioninto retirement.

It provides a flexibleway for you to access your superannuationbenefits from preservation age, without having to choosebetween full-timeemployment and full-time retirement. If youchoose an NCAP you are not ‘locked-in’ to your choice shouldyour circumstances change.

Why invest in super, an allocated pension or an NCAP?

Super provides tax advantages when compared to some otherforms of saving for your retirement. An allocated pension is atax-effectiveway of drawing an income in your retirement andan NCAPmay assist you to transition fromwork to retirementin a tax-effective manner.

Bringing your strategy to lifeTogether with your financial adviser, you will agree on afinancial strategy to achieve your retirement goals.North Superand Pension seeks to bring that strategy to life by providing asingle access point for a range of investment options acrossmajor asset classes, drawingon the specialist expertise of someof the world’s leading investment managers.

North OnlineYour North account is operated through North Online atnorthonline.com.au. NorthOnlineallowsyouandyour financialadviser to review, transact and report on your North account.

You can log onto North Online at any time to see how yourinvestments are performing and perform a wide range oftransactions.

All communications fromuswill be sent to youviaNorthOnlineand stored in your online filing cabinet, or communicated via‘News & announcements’.

North is an online product so it's important that you haveinternet access to use the services offered and receiveinformation about your accounts.

You will require internet access to use and maintain youraccount.

Once you become a member of North Super and Pension, youwill be sent awelcome letter containing a guide tousingNorthOnline as well as your user ID. This will be followed by aseparate letter with your temporary password. The first timeyou log in to North Online you will be required to accept theterms and conditions and change your password.

8

Welcome to North Super and Pension

Transacting on your account

Financial adviser accessTransactions on your North Super and Pension account arecompleted by your financial adviser using North Online.

Your financial adviser should obtain your authorisation(consent) for each transaction they perform on your account.This authorisation will be obtained by your financial adviserduring the advice process and is retained by them as evidencethat you have authorised each transaction they perform.We'llact upon any instruction (except changes to bank accountdetails) received from your financial adviser in relation to youraccount.

Changes to bank account details are excluded for securitypurposes.

Your financial adviser can use North Online to:– open new accounts on your behalf– add additional or new investments– switch investments– complete transfers– submit withdrawal requests– trade shares– produceadhoc reports tomonitor theperformanceof your

account– view communications and statements online.

Any transactions made on your account will be confirmed toyou through North Online.

In certain circumstances you may enter into an arrangementwith your financial adviser allowing them to transact on youraccount on your behalf without the need for each transactionto be authorised by you. This is known as a ManagedDiscretionary Account (MDA). To offer an MDA arrangementyour financial advisermust beappropriately licensed tooperateanMDA. For further information about how to set up anMDA,please contact your financial adviser.

Member accessYou're are able to log on toNorthOnline at any time to see howyour investments are performing.

You can use North Online to:– view your account details and transactions– access your online filing cabinet– monitor the performance of your investments– check the progress of your transactions– update your personal details (including banking details).

NorthOnlinealsoprovides theoption for your financial adviserto change your North Online access to allow you to completea broader range of transactions. You should discuss this optionwith your financial adviser.

My AMPIn addition to accessing your account onNorthOnline, you canview your AMP consolidated details at My AMP.

My AMP gives you fast, easy and secure online access to yourbanking, super, insurance and investments. Keep an eye onyour account and review your AMP investments whenever youwant andgenerate aPortfolio Report fromthe commencementof your North Super and Pension account. You can also includeany external accounts and assets for reporting purposes.

Register for your online account at amp.com.au.

The AMP appIt’s the first app inAustraliawhere you canaccess your banking,insurance, investmentsandsuperaccounts—all fromoneplace.

The AMP app helps you get things done, like accessing yourAMP Bank accounts tomake payments or getting help to startconsolidating your super.

Get started in three easy steps:1. Have your MyAMP (super/insurance/investments) login

details handy.2. Download the app from the App Store or Google Play.3. Follow the set-up instructions and you're good to go.

Available from the Apple1 App Store and Google Play2

now.

Keeping track of your invesments

Annual StatementEvery year on or around your account anniversary we'll sendyou an annual statement via your filing cabinet on NorthOnline, which will include:

- your current account balance

- a statement of transactions, and

- an account performance summary.

Trustee Annual ReportThe Trustee annual report for the Fund with informationcurrent as at 30 June will be available on northonline.com.au.You can also request a printed copy by contacting the NorthService Centre on 1800 667 841.

1 Apple is a trademark of Apple Inc.2 Google Play is a trademark of Google Inc.

9

Contributing to North SuperNorth accept all contributions, rollovers and transfers allowedby legislation, as long as transaction minimums are reached.

You canmake a non-concessional contribution (eg personal orspouse) at any time on North Online by direct debit.Alternatively, you can use your bank’s online banking facilitiesto EFT or BPAY your contribution.

You can alsomake a non-concessional contribution by cheque.All cheques should be attached to a deposit advice created onNorth Online and made out to ‘North’.

Forward the cheque along with the deposit advice to:North Service CentreGPO Box 2915MELBOURNE VIC 3001

For further information on the types of contributions youcan be made to a super account and how to use EFT andBPAY tomake contributions, please refer to section 1 of theadditional information booklet..

Rollovers from other superannuation providersYou can roll over funds from other superannuation providersby completing rollover forms provided by:– us, through North Online– the other superannuation provider– the Australian Taxation Office (ATO).

If you transfer your whole balance, any insurance cover willcease on the date of transfer.

Regular savings planA regular savings plan is an easy and convenient way tocontribute to your retirement savings.

You can establish a regular savings plan for non-concessionalcontributions (eg personal or spouse) via direct debit from anominatedbankor financial institution account. You can selectfrom a fortnightly, monthly, quarterly, half-yearly or yearlyfrequency. The minimum amount per contribution for allfrequencies is $10.

Youmay nominate the date onwhich amounts arewithdrawnfrom your nominated bank account, between the 1st and the28thof themonthor the last day of themonth. Regular savingsplan investments will generally be receipted into your cashaccount that day.

If a regular savings plan payment falls on a weekend orMelbourne public holiday, we will initiate the payment on thefollowing business day.

Regular savings plan contributions will continue until wereceive any changes or a cancellation of the facility. You canmake changes or cancel your regular savings plan at any timevia North Online.

Automatically increasing your regular savings planOver time, inflation reduces the real value of your investments.

To help you keep pace with inflation you can choose to haveyour regular savings plan amount automatically increased orindexed each year.

You can choose between:– a fixedpercentage (up to 7%pa)—applied on your account

anniversary each year, or– Consumer Price Index (CPI)—applied on your account

anniversary each year using the most recently publishedCPI figure.

You may change or cancel the option at any time via NorthOnline.

Contribution splittingAs a member of the Fund, you may elect to split contributionswith your spouse. Themaximumamountof contributions thatcan be split is the lesser of 85% of your concessionalcontributions (which includes SuperannuationGuarantee andsalary sacrifice contributions) and the concessionalcontributions cap.

For further information on contribution splitting, pleaserefer to section 1 of the additional information booklet.

WithdrawalsWithdrawals (partial and full) can bemade at any time subjectto relevant superannuation legislation (where applicable) andtrust deed requirements. You can make a partial withdrawalfrom yourNorth Super account (subject to trademinimums asdescribed on page 5), provided youmaintain an account valueof at least $2,000.

You can select fromwhich individual investment options youwould like to sell down from or alternatively you can select tosell downyour investmentoptions according to your automaticsell instructions. Where you have not provided us with sellinstructions, we will sell your investments proportionately.

Your benefits are generally paid as a lump sum, but can alsobe:– rolled over in full or in part to North Pension (if you have

met a condition of release), or– rolled over to another complying superannuationprovider.

To make a withdrawal, your financial adviser will need tosubmit your withdrawal request on North Online, afterobtaining your authorisation.

10

North Super

Withdrawals fromyour account are normally processedwithin30 days of us receiving all of the necessary information. Thereis an exception to this requirement where particularinvestments have redemption restrictions imposed by theunderlying fundmanager that prevent us from paying the fullbenefit within this period.

However, time frames may vary depending on the time takenby fundmanagers to complete processing of sale transactions.A withdrawal may also be delayed if an existing buy or sellinstruction has not been confirmed. Refer to the underlyinginvestment options' PDS for further information relating towithdrawal conditions associated with the underlyinginvestment options.

If you nominate to sell part of your holdings in any managedinvestment fund or listed security (via a partial withdrawal oras part of a sell instruction) and the withdrawal amountexceeds 90% of the current asset value, the sale will beconverted from a dollar-based to a unit-based sale using thelatestmarket unit price held at the timeof sale. Thismay resultin a different withdrawal amount from your original requestdue to variations in unit prices. Withdrawal periods varybetween fund managers and can be found in the underlyinginvestment options' PDS.

For example, if you held 1,000 units in an investment optionvalued at $2 per unit (1,000 x $2 = $2,000) and you nominatedto sell $1,900, we would automatically convert the sale to aunit based sale of 950 units (950 units x $2 = $1,900).

For further information on conditions of release andwithdrawing from super, please refer to section 2 ofthe additional information booklet.

Fast payment

The fast payment of funds is available for partial withdrawalsonly, up to a maximum of 80% of your portfolio balance. Wereserve the right to reduce the percentage. Wemay advancethe payment of your funds without awaiting sale proceedsfrom underlying investments. During this period your cashaccount balance may fall below zero. Refer to ‘Negative cashaccount balance’ onpage15 formore informationon the effectof your cash account balance becoming negative

11

North offers two types of pensions, an allocated pension anda non-commutable allocated pension (NCAP).

An allocated pension can be purchased with unrestrictednon-preserved superannuation benefits.

A non-commutable allocated pension can be purchased withpreserved superannuation benefits provided youhave reachedpreservation age (refer to the table below):

Preservation ageDate of birth

55Before 1 July 1960

56From 1 July 1960 to 30 June 1961

57From 1 July 1961 to 30 June 1962

58From 1 July 1962 to 30 June 1963

59From 1 July 1963 to 30 June 1964

60On 1 July 1964 or after

Pensions commencing with multiplerolloversA pension can be commenced with more than one rollover;however, each rollover must be received prior to the pensioncommencing. It is not possible to contribute a further rolloveror anyother amount to apension thathas already commenced.Youmayhowever commence additional pensionswith eligiblerollovers. There is a transfer balance cap of $1.6million, pleasespeak toyour financial adviser tounderstandhow itmay impactyou.

If you are commencing your pension with more than onerollover, your financial adviser will need to indicate this whencompleting your application online. Each rollover received willbedeposited inNorthSuperaccountand invested inaccordancewith your investment instructions.Whenall specified rollovershavebeen received, theywill immediatelybeused to commenceyour pension, including any investment earnings received inthe interim. The earnings credited to yourNorth Super accountbefore your pension commences will be taxed at a rate of upto 15%.

It’s important to note that if any specified rollover is notreceived within 75 days of the submission of your application,the pension will automatically start with the total receiptedrollovers at that time. If rollovers are received after 75 days,your financial adviser will be contacted to confirm yourinstructions.

Pension paymentsWhen you hold an allocated pension you must receive aminimum income payment each financial year, based on yourage and account value. The minimum income amount for thepart-year up to 30 June is calculated at the time your pensioncommences. The minimum is then recalculated on 1 July insubsequent years using your age and account value on thatdate.

If you have not received the full minimum income amountafter your last income payment for the financial year, we willautomatically pay you an additional income payment for thedifference before the end of financial year to ensure that theminimum is met. Note that any relevant PAYG tax will bepayable. Your financial adviser can help you calculate yourstarting minimum pension payment level.

You can vary the pension payments at any time within theprescribed limits.

The maximum payment amount for NCAPs is 10% of youraccount value at the time your NCAP commences. Thismaximum is recalculated each year using your account valueat 1 July. In the first year of your NCAP, your minimum pensionpayment is prorated; however, the maximum remains at 10%.

For further information on NCAPs, how pension paymentsare calculated and how to make a withdrawal from yourpension, please refer to section 3 of the additionalinformation booklet.

Automatically increasing your pensionOver time, the purchasing power of your money is reducedthrough inflation.

To help keep pace with inflation you can choose to increaseyour pension payment automatically each year.

You can choose from twomethods:– A fixed percentage (up to 7% pa)—applied on 1 July, or– CPI—applied on 1 July each year using the most recently

published CPI figure.

To activate this facility, simply make this selection uponapplication. Youmay change or cancel this facility at any time.

12

North Pension

Withdrawals

If your pension is an allocated pension you can makewithdrawals (which exclude regular pension payments) fromyour account any time. Withdrawals can be made as either:– partial or full commutations, which may be subject to

lump-sum tax, or– ad hoc pension payments, whichmay be taxed at a higher

rate than regular pension payments.

For further information on taxation of withdrawals, pleaserefer to section 6 of the additional information booklet

If your pension is a non-commutable allocated pension,withdrawals can only bemade in the following circumstances:– where benefits are unrestricted non-preserved– to pay a super surcharge liability– to effect a super split under family law– where a condition of release (e.g. retirement or reaching

age 65) has been met after the NCAP commenced– to roll back to super (e.g. if the income stream from the

NCAP is no longer required)– to roll over to another non-commutable income stream– to pay for non-concessional contributions tax liability

For further informationon conditions of release, please referto section 2 of the additional information booklet

Tomakeawithdrawal fromyourpensionaccount your financialadviser will need to submit your withdrawal request on NorthOnline, after obtaining your authorisation.

Withdrawals fromyour account are normally processedwithin30 days of us receiving all of the necessary information. Thereis an exception to this requirement where particularinvestments have redemption restrictions imposed by theunderlying fund manager that prevent us from paying thebenefit within this period.

However, time frames may vary depending on the time takenby fund managers to complete the processing of saletransactions. A withdrawal may also be delayed if an existingbuy or sell has not been confirmed. Refer to the underlyinginvestment options' PDS for further information relating towithdrawal conditions associated with the underlyinginvestment options.

If you nominate to sell part of your holdings in any managedinvestment fund or listed security (via a partial withdrawal oras part of a sell instruction) and the withdrawal amountexceeds 90% of the current asset value, the sale will beconverted from a dollar-based to a unit-based sale using thelatestmarket unit price held at the timeof sale. Thismay resultin a different withdrawal amount from your original requestdue to variations in unit prices. Withdrawal periods varybetween fund managers and can be found in the underlyinginvestment options' PDS.

If you make a full withdrawal (commutation), we are requiredto first pay your minimum pension amount for the relevantportion of that financial year. If youhave already receivedmorethan this amount, no additional pension payment is required.If yournon-concessional contributions fromyour super accounthave exceeded the non-concessional cap prior to commencinga pension, youmay incur an excess tax liability. In this case youmust obtain a release authority from the ATO to withdraw anamount equal to your tax liability from your pension fund.

Fast payment

The fast payment of funds is available for partial withdrawalsonly, up to a maximum of 80% of your portfolio balance. Wereserve the right to reduce the percentage. Wemay advancethe payment of your funds without awaiting sale proceedsfrom underlying investments. During this period your cashaccount balance may fall below zero. Refer to ‘Negative cashaccount balance’ onpage15 formore informationon the effectof your cash account balance becoming negative.

For further information on non-concessional contributionscap, please refer to section 6 of the additional informationbooklet.

13

Your cash accountNorth Super and Pension uses a cash account that operates asa hub through which all of your transactions will pass. Yourcontributions, rollovers and transfers (unless these aretransferred in specie), as well as all of your pension paymentsandany otherwithdrawals,will bemade via your cash account.

To help youmanage your cash account you have the flexibilityto nominate a target cash balance by specifying a minimumcash balance (dollar amount) and/or a nominated target cashpercentage (a percentage of your total portfolio balance) to beheld in your cash account.

A default target cash amount of 5% and a default minimumcash balance of $0 will apply where no selection is made. Boththe Minimum cash balance and Nominated target cashpercentage can be adjusted at any time.

The target cash balance is calculated as follows:

(Account balance x Nominated target cash percentage) +Minimum cash balance = Target cash balance.

For example, where the Account balance is $100,000, theMinimum cash balance specified is $0 (default) and theNominated target cash percentage is 5% (default) then theTarget cash balance is calculated as:

($100,000 x 5%) + $0 = $5,000

If the Minimum cash balance is increased from $0 to $1,000then the Target cash balance is calculated as:

($100,000 x 5%) + $1,000 = $6,000

The cash account is used for essential functions, someofwhichare illustrated below.

Cash account sweepsWhen the balance of your cash account exceeds your targetcash balance by $500, the excess cash will be invested as peryour investment instructions. In order for the cash accountsweep to takeplace, the excess cashmustmeet the transactiontrade minimums as defined on page 5.

If the balance of your cash account falls below your target cashbalance we will sell your assets as per your investmentinstructions tobring your cashaccount back to your target cashbalance, provided the transaction trade minimums are met(refer to page 5 for transaction trade minimums). Where youhave not provided us with a sell profile, we will sell yourinvestments proportionately.

Where you hold listed securities and the trade minimum of$650 per listed security is not met, we will not sell your assetsand your cash account balance will remain below your targetcash balance.

Term Deposits will not be terminated early to bring your cashaccount balance back to your target cash balance.

Earnings on your cash accountFunds held in your cash account are pooled with the cashbalance of other members and will be invested in:– a tradingbankaccountwithWestpacBankingCorporation;

and– a trading bank account with AMP Bank Limited.

We reserve the right to change or to alter the investmentstrategy of the cash account at any time without prior notice.

Any balance held in your cash account will accrue interestcalculated daily. Interest accrued will be allocated to the cashaccount effective the first day following the endof eachmonthor, if you close your account before the end of a month, priorto payment being made.

14

What is the cash account?

Negative cash account balanceShould your cash account balance become negative at anytime, interest will be charged on the negative amount at thesame rate as the interest paid on positive cash accountbalances.

Events that may cause your cash account balance to becomenegative include payments such as fees, insurance premiums,withdrawals or if you are switching between investmentoptions.

When your cash account balance goes into negative, we willsell your investments as per your sell profile to bring your cashaccount balance back to your Target amount. Where you havenotprovideduswitha sell profile,wewill sell your investmentsproportionately. However, if you only hold illiquid investmentoptions, listed securities and/or term deposits, these assetswill not be sold down proportionately and your cash accountwill remain negative.

Formore information on investing inNorth Super and Pension,refer to page 16.

When will your money be invested?Your contribution will generally be credited to your cashaccount on the business day it is received. Any balance held inyour cash account will accrue interest at the current cashaccount crediting rate on thedaily balance from that date untilyour funds are invested according to your investmentinstructions.

Your investment instructions are forwarded to the underlyingfundmanager, termdeposit provider andAustralian SecuritiesExchange (ASX) on a daily basis. The effective date of yourinvestment will be the date applied by each individual fundmanager or termdeposit provider. Ad hoc instructions to tradelisted securities will normally be forwarded to the ASX whenthey are received.

15

Investment optionsNorth offers a range of investment options to choose from,with access to:– over 440 managed funds, including both Australian and

international investments across a variety of asset classes– a range of listed securities (including companies in the

S&P/ASX300, selected exchange traded funds (ETFs),exchange traded commodities (ETCs), listed investmentcompanies (LICs), listed investment trusts (LITs), Australianreal estate investment trusts (AREITs), and

– termdepositswith a range of providers and varying terms.

AMPhas implementedacomprehensive strategy formonitoringand selecting underlying investment options. This strategyincludes oversight by an Investment committee. NMMT is notresponsible for the performance of underlying investmentoptions.

For more information on the investment options available,refer to the North Investment Option document onnorthonline.com.au or contact the North Service Centre on1800 667 841 for a copy.

Investment instructionsWhenyour financial adviser completes your application toopena North Super and/or Pension account, you are required toprovide your automatic buy instructions. You can also arrangeto provide ongoing investment instructions, including:– Buy profile– Sell profile– Rebalance profile– Dollar cost averaging.

Restrictionsmayapply to the investmentoptions chosen. RefertoRemovingor closing investmentoptionsonpage17 formoreinformation.

Buy profileContributionsand rollovers that take your cashaccountbalanceabove your target amount will be invested according to yourbuy profile. Your buy profile can include managed funds andlisted securities and must be specified as percentages.

If any of your investment options are sold in full and you donot update your buyprofile, fundsmay continue to be investedinto that option.

Accounts without a buy profile will remain invested in yourcash account.

Sell profilePayments of taxes, fees, insurance premiums, pensionpayments and withdrawals may cause your cash accountbalance to fall belowyournominatedminimumamount. If thishappens we will sell down your investments according to thesell profile you have nominated. Your sell profile can includemanaged funds and listed securities and must be specified aspercentages.

As an alternative to specifying a sell profile in percentages youcan:– nominate an order by which investment options are sold,

or– nominate that managed funds be sold proportionately.

If there are insufficient funds in an investment option to sellusing your sell profile, then the required amount will be soldproportionally across your remaining investmentoptions. Sellsare processed as a dollar amount to match your specifiedpercentage. If the percentage amount for any investmentoption that is required to be sold is greater than 90%, the salewill be converted fromadollar-based to aunit-based sale usingthe latest unit pricewe hold. Thismay result in the percentagesold being different to the percentage you specified.

If you do not have a sell profile, your investments will be solddown proportionally.

Listed securities and term deposits will not be soldproportionally and may cause your cash account to becomenegative.

Rebalance profileOver time, the value of your underlying investments willfluctuate. If you invest inmore tan one underlying investmentoption, this variation is likely to cause your percentage ofholdings to vary from your initial investment profile. Theauto-rebalance facility rebalances your investment optionsback to your rebalanceprofile, in accordancewith your standinginstructions.

You can nominate a rebalance profile when you set up youraccount and modify it through North Online. Your profile caninclude managed funds and listed securities and must bespecified in percentages.

The auto-rebalancing feature gives you the option to rebalancequarterly, half-yearly or yearly on a selected date. Therebalancing will only occur on your nominated rebalance dateif the total of the buy transaction or sell transaction torebalance back to your profile meets the trade minimums asdescribed on page 5. In addition, any pending buy and selltransactions must be completed prior to the account beingrebalanced.

16

Investing in North Super and Pension

Dollar cost averagingDollar cost averaging (DCA) is the process of investing a setdollar amount into the market over regular intervals. The aimof this approach is to reduce the risks associated with tryingto choose the right time to buy. DCA is subject to a minimuminstalment of $500.

The benefits of DCA vary depending on the type of investmentand market conditions. You should seek advice from yourfinancial adviser on how DCAmay suit your individualcircumstances.

For further information on DCA, please refer to section 7 ofthe additional information booklet.

Switching between investment optionsSwitching involves the selling of an investment option and thepurchaseof another. Both thepurchaseandsale are conductedat the same time, which may result in your cash accountbecoming negative for a short period of time. Importantly, youare still invested for the day(s) your cash account is negative.

Your instructions for a switch are specified in dollars (subjectto trade minimums as described on page 5).

If the dollar amount of an investment to be sold is greater than90%of yourholding, the sell instructionswill be converted fromdollar-based to unit-based using the latest unit price we hold.Thismay result in the dollar amount purchasedbeingdifferentto the dollar amount sold.

Listed securitiesNorth allows you to invest in the S&P/ASX 300 securities listedon theAustralianSecurities Exchange (ASX) andother securitiesas listed in the North investment options document availableat northonline.com.au.

To invest in listed securities through North, your financialadviser will need to request a Holder Identification Number(HIN) through North Online, which is unique to your account.

If the listed security is no longer on the S&P/ASX 300 noadditional units can be purchased.

Corporate actionsFrom time to time there may be corporate actions associatedwith listed securities. Examples of corporate actions include,but are not limited to, rights issues, share splits and buy-backs.

As you will be assigned a unique HIN, you can participate inany corporate actions that are notified to us. We will notifyyour financial adviser of the corporate actions and ask themto contact you, to provide instructions on your behalf. We willact on those instructions as provided to us by your financialadviser. If your financial adviser has provided you withtransaction access for trading securities youwill be able to giveus your instructions directly.

For corporate actions, where the action results in you holdingassets outside the S&P/ASX 300, wemay, at our discretion, selldowntheseassets andcredit theproceeds to your cashaccount.

Removing or closing investment optionsWemay from time to time, remove or close certain investmentoptions Wemay from time to time, remove or close certaininvestment options (for example, where the underlyinginvestment is either terminating or being closed by the fundmanager).Where this occurs,wewill normally provide youwithat least 30 days’ prior notice. If the option is terminating, youwill need to select an alternative investment option.Wherewecannot provide you with at least 30 days’ prior notice (due tocircumstances outside of our control), wewill provide youwithnotice as soon as practicable.

Where we cannot provide you with adequate notice or wherewehave not received alternative investment instructions fromyou, we will take the below actions:1. If the investmentoption is terminatedor closed toadditional

investments and it forms part of your investmentinstructions:

– the investment option will be replaced with the AMPWholesale CashManagement Trust (NML0018AU) in yourbuy profile

– your dollar cost averaging purchase instruction will becancelled

– your existing sell profile will remain unchanged if theinvestment option is closed

– your rebalance instruction will be cancelled and yourrebalanceprofilewill bedeleted. Theauto-rebalance facilitywill no longer be available whilst you hold units in thatinvestment option.

2. If the investment option is closed to new investments youcan continue to invest in the closed investment optionprovided that you currently have aholding in the investmentoption. If it forms part of your investment instructions andyoudonot currentlyhaveaholding in the investmentoption:

– the investment option will be replaced with the AMPWholesale CashManagement Trust (NML0018AU) in yourbuy profile

– your dollar cost averaging purchase instruction will becancelled

– your rebalance profile will be deleted– your existing sell profile will remain unchanged.

3. If the investment option is suspended (frozen) and formspart of your investment instructions:

– the investment option will be replaced with the AMPWholesale CashManagement Trust (NML0018AU) in yourbuy profile

17

– your dollar cost averaging purchase instruction will becancelled

– your rebalance instruction will be cancelled and yourrebalanceprofilewill bedeleted. Theauto-rebalance facilitywill no longer be available whilst you hold units in thatinvestment option.

If it forms part of your sell profile and you have instructed usto:– ‘divest as per the sell down profile’, the entire sell profile

will be deleted and your instructions changed to sell down‘pro rata across all managed funds only’

– ‘divest as per the sell down order’, we will delete theinvestment option from the sell down order

– ‘pro rata across managed funds only’, we will continue tosell pro rata across your remaining managed funds.

Where you are invested in an investment option that isterminating, your holdings in the optionwill be sold subject toany suspension/withdrawal restrictions. Proceeds from thesale will be allocated to your cash account. Additionally, whereyou hold an investment option that is suspended (frozen),terminated or closed, the auto-rebalance facility is no longeravailable whilst you hold units in that option. However, youmay wish to complete a ‘One-off rebalance’ by excluding thesuspended, terminatedor closed investmentoption. For furtherinformation on the withdrawal restrictions that may apply,refer to the liquidity risk section of this PDS.

The PDS for the AMP Capital Wholesale Cash ManagementTrust (NML0018AU) is available from North Online. You canmake a switch out of this investment option at any time.

Obtaining up-to-date informationThe available investment options may change from time totime. Full details of the available investment options can befound in the North Investment Options document, availableat northonline.com.au or by contacting your financial adviseror the North Service Centre on 1800 667 841.

Fundmanagerswill notify us of anymaterially adverse changesor significant events that affect an investment option youhaveselected.Wewill notify youof these changesor events throughNorth Online as soon aswe can after we have been notified bythe fund managers. Copies of these documents are availablefree of charge upon request by contacting the North ServiceCentre via email at [email protected] or by calling 1800 667841.

We will not be responsible for any delays in notifying you ofthese changes or events, where the delay has been caused bya fund manager.

Fund manager paymentsNMMTmay receive payments of up to 0.55% pa from fundmanagers based on the amount invested in particularinvestment options made available to you. Payments receivedare based on amounts invested with the fund manager andthe management cost of the investment option. Thesepayments and their method of calculation may change fromtime to time and are not an additional cost to you. All fundmanager payments are agreed on arm's length terms.

Assets transfers (in specie)An asset transfer (in specie) is the process of transferringmanaged funds and listed securities from one product holderto another, without the need to sell and repurchase the assets.This helps reduceanyoutofmarket risks associatedwith sellingand repurchasing the assets.

In specie transfers do not have buy/sell costs for managedfunds or brokerage fees for listed securities.

Therewill be a realisation of any capital gains or losses as therewill be a changeofbeneficial ownership. Stampduty andothercosts may apply.

Some transfers can take in excess of threemonths to completedependingon the typeof asset being transferred. Asset parcelsare transferred out on a “first in first out” basis, meaning olderasset parcels will be transferred out before newer ones.

In specie inSome assets you hold outside of your North Super or Pensionaccountmaybe transferred in specie into your account if certainconditions are met, including:– The assets must be available in the North investment

options document, including listed securities.– The other holder (fund manager or platform) allows in

specie transfer out.

An in specie transfer fee will apply for any listed securities yourequest to transfer in. There are no fees for managed funds.Formore information on the in specie transfer fee, please referto page 25 of this PDS.

In specie outTheassets youhold in your accountmaybe transferred in specieto another holder, in place of a rollover or cash withdrawal, solong as certain conditions are met and the other holder iswilling to accept the particular assets being transferred.

An in specie transfer fee will apply to each managed fund orlisted security you request to transfer out. Formore informationon the in specie transfer fee please refer to page 25 of this PDS.

The other holder may also charge a fee for accepting in specietransfers in.

18

Partial in specie transfers out

You can request a partial transfer of your account balance bytransferring all or part of any managed fund or listed security.If you elect a partial transfer, your account will remain openand you can continue to transact on your account. However,you will not be able to transact on the remaining holdings inthe investment options you have elected to partially transferuntil all completed forms have been received and the requesthas been authorised by us. If you receive dividends paid as partof your Dividend Re-investment Plan (DRP) after you submitthe transfer, these will appear as additional units in yourexisting listed security holdings.

Full in specie transfers out

Where the transfer request results in a full withdrawal youwillneed to ensure you have sufficient cash available in your cashaccount to pay for the provisions detailed below, including thein specie fees. If you do not have sufficient funds in your cashaccount, you will need to sell part or all of your holdings in aninvestment option. If this occurs, you will need to provideinstructions onwhich investment option youwish to sell down.

If listed securities are sold, brokerage fees will apply. Once theasset transfer request has been submitted youwill not be ableto transact on your account and your account will be closedwhen the asset transfer has been completed.

The maximum amount you can transfer in specie will becalculated based on your total account value less outstandingfees and provisions. The maximum transfer value will becalculated at the time the request is submitted. If you receivedividends paid as part of your DRP after you submit yourtransfer, these units will be sold to cash as part of the cashwithdrawal and account closure.

Someasset transfersmay takeup to threemonths to complete,consequently we will provision for the following:– three months of scheduled pension payments (pension

only)– three months of administration fees– three months of insurance premiums (where applicable)

and– three months of advice fees.

Income

Dividends from listed securitiesYou have the option of receiving your dividends as a paymentmade into your cash account or choosing a dividendreinvestment plan (where available), that will reinvest anydividends automatically to purchase further shares.

Term deposit interestInterest earned from term deposits will be paid into your cashaccount upon maturity or at specified intervals as supportedby the term deposit provider. Refer to North Online for moredetails.

Distributions frommanaged fundsManaged funds will generally earn income and also generatecapital gains. Income is paid in the formof distributions,whichwill then be paid into your cash account.1

Where you hold a North Personal Pension account, you alsohave the option to have distribution payments paid from thecash account as a pension payment or added as part of anominated pension payment amount. When this option hasbeen selected, distributions received frommanaged funds andthe cashaccount thathaveaccumulated since your last pensionpayment will be paid. PAYG tax will apply (if applicable) on aper-payment basis.

Are labour standards, environmental, socialor ethical considerations taken intoaccount?The Trustee does not take labour standards, environmental,social or ethical considerations into account in the selection orretention of the Fund’s investment options.

Does the Trustee invest in derivatives?The Trustee does not invest directly in derivatives. However,underlying investment managers may do so. Derivatives aresecurities that derive their value from other assets or indices.Examples of derivatives include futures and options.

1 Unless otherwise indicated in the North Investment Options document or underlying investment options' PDS.

19

Risks apply to investing in super andpensionInvestments in super and pensions are subject to legislativerequirements. Changes to legislation aremade frequently andmay affect who can invest, what tax is to be paid and whenand howmoney can be withdrawn. Super and pension fundsare governed by a Trust Deed. The Trustee is able to amend therules in the Fund’s Trust Deed that affect how the Fundoperates, although the Trustee is prevented by law and theTrust Deed from amending the Trust Deed in a manner that isadverse tomembers’ entitlementswithout their consent.Otherrisks relate to increases in fees, a change in investmentmanagers and the performance of investment managers. TheTrustee uses adherence to the law and the Fund’s Trust Deedand ongoing monitoring of the performance of investmentmanagers to reduce these risks.

An investment in North Super and Pension is subject toinvestment risk, including possible delays in repayment andloss of incomeand capital invested. This risk can includemarketrisk, company risk, currency risk, interest rate risk and inflationrisk.

Neither the Trustee, nor any other member of AMP or theinvestment managers, guarantees the payment of income orthe performance of the investment options.

DiversificationDiversification is a basic strategy used to reduce some of therisks associatedwith investing. By spreading your investmentsacross a number of assets, you are not reliant on theperformance of, and are not exposed to the risks of, a singleinvestment. Investing in only one or a few specific assets ordirect securities can increase your risk. It is very important thatyou understand and are aware of the risks and mitigatingstrategies, such as diversification, that are available to you. Formore information on what risks apply to investing speak toyour financial adviser.

Risk and returnYour investment strategy will be highly dependent on yourattitude towards risk. All investments carry a risk component.Risk in an investment context refers to the possibility that theinvestment will not return its original capital or expectedincome and that the level of return will be volatile over anygiven time period. This risk can include market risk, companyrisk, currency risk, interest rate and inflation risk. Investmentswith a low risk profile will usually provide lower, thoughmoreconsistent, returns than those with a higher risk profile. Forexample, investing cash into bank accounts is considered lowrisk/low return,while the sharemarkethashistorically providedhigher returns over the longer term with higher volatility.

Liquidity riskLiquidity risk is the risk that your investment cannot be bought,sold, cashed, transferred or rolled over as quickly as youmightwish. Different investments have different transactionprocessing times, and thus different levels of liquidity risk.

Investment transactions, withdrawals, rollovers and transfersfrom your superannuation account are normally processedwithin 30 days of us receiving all the necessary information.Some investments, referred to as illiquid assets, require a longerperiod to be redeemed. This longer redemption period isimposedby theunderlying investmentmanager because someor all of the assets within the investment are illiquid. Accountfees will continue to be charged while invested in illiquidinvestment options.

For further informationon the risks of investing, please referto section 4 of the additional information booklet.

20

What risks apply to investing?

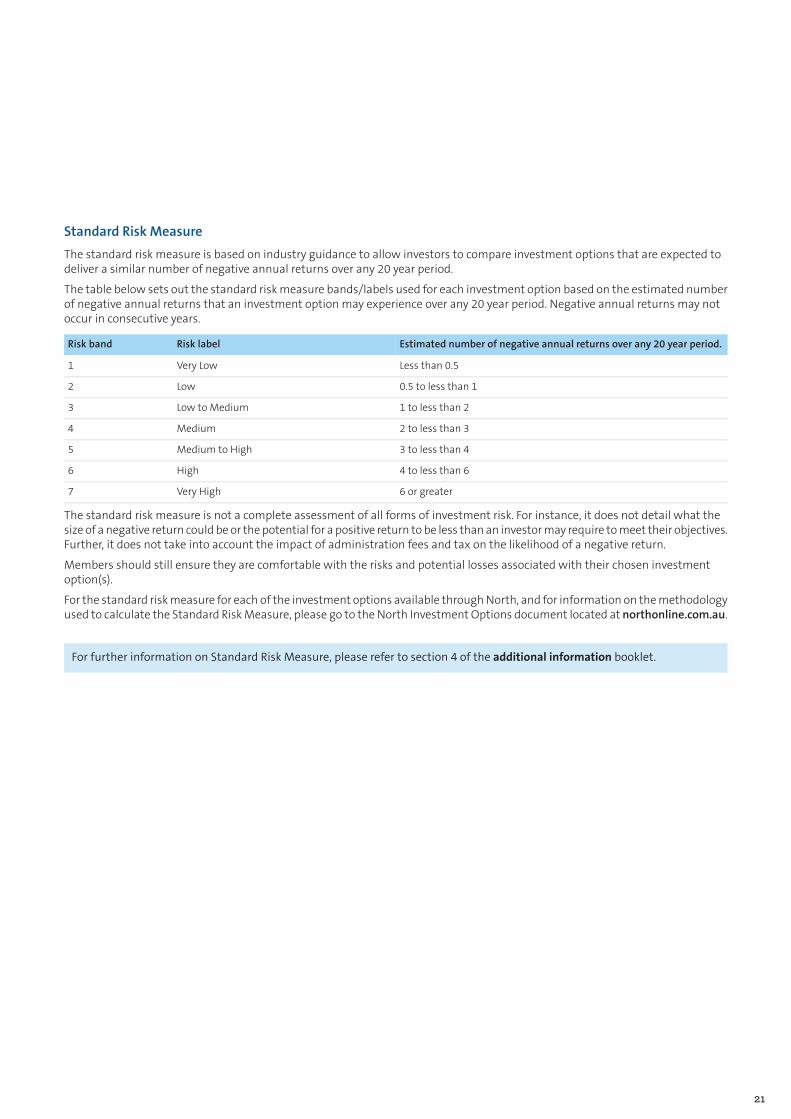

Standard Risk MeasureThe standard risk measure is based on industry guidance to allow investors to compare investment options that are expected todeliver a similar number of negative annual returns over any 20 year period.

The table below sets out the standard riskmeasure bands/labels used for each investment option based on the estimated numberof negative annual returns that an investment option may experience over any 20 year period. Negative annual returns may notoccur in consecutive years.

Estimated number of negative annual returns over any 20 year period.Risk labelRisk band

Less than 0.5Very Low1

0.5 to less than 1Low2

1 to less than 2Low to Medium3

2 to less than 3Medium4

3 to less than 4Medium to High5