novità normative emir ifrs 9 hedge accounting · products and services. require new systems,...

TRANSCRIPT

Novità normativeEMIRIFRS 9 Hedge Accounting

RiccardoBua OdettiPartner PwC Advisory

Membro EFRAG Financial Instrument Working GroupMembro OIC Financial Instrument Working GroupCorporate Treasury Technical Committee PwC

PwC

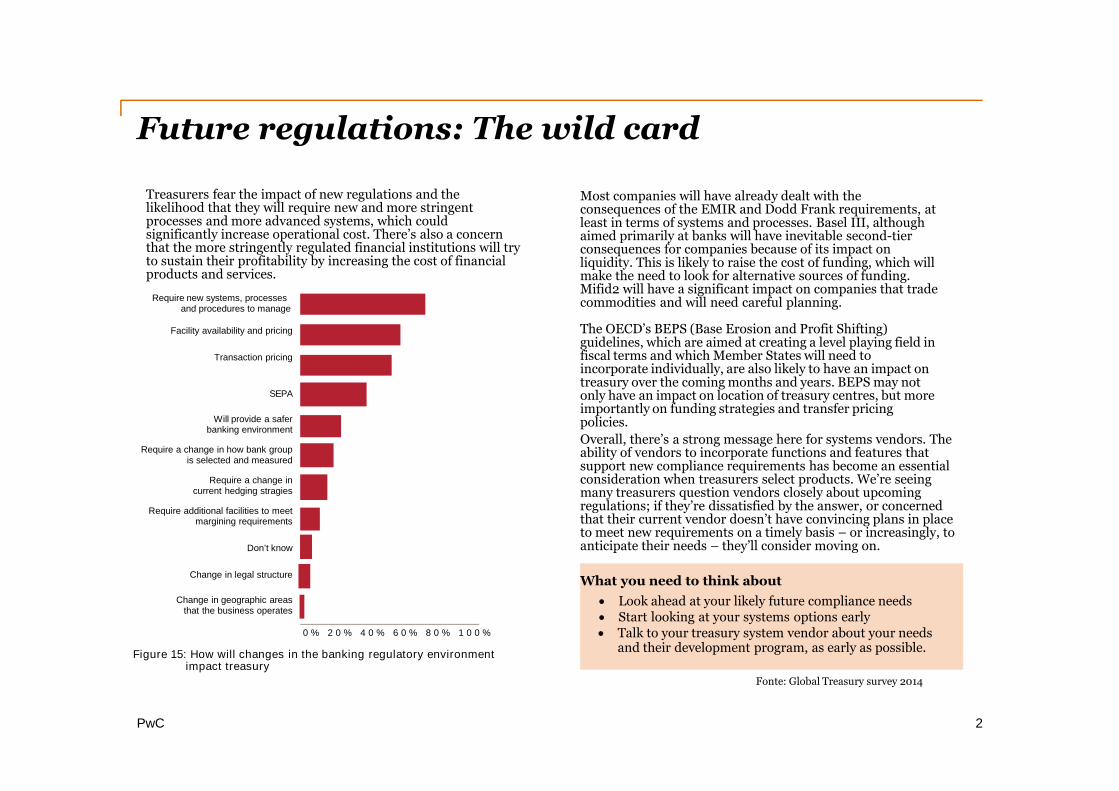

Future regulations: The wild card

2

Treasurers fear the impact of new regulations and thelikelihood that they will require new and more stringentprocesses and more advanced systems, which couldsignificantly increase operational cost. There’s also a concernthat the more stringently regulated financial institutions will tryto sustain their profitability by increasing the cost of financialproducts and services.

Require new systems, processesand procedures to manage

Facility availability and pricing

Transaction pricing

SEPA

Will provide a saferbanking environment

Require a change in how bank groupis selected and measured

Require a change incurrent hedging stragies

Require additional facilities to meetmargining requirements

Don’t know

Change in legal structure

Change in geographic areasthat the business operates

0 % 2 0 % 4 0 % 6 0 % 8 0 % 1 0 0 %

Figure 15: How will changes in the banking regulatory environmentimpact treasury

Most companies will have already dealt with theconsequences of the EMIR and Dodd Frank requirements, atleast in terms of systems and processes. Basel III, althoughaimed primarily at banks will have inevitable second-tierconsequences for companies because of its impact onliquidity. This is likely to raise the cost of funding, which willmake the need to look for alternative sources of funding.Mifid2 will have a significant impact on companies that tradecommodities and will need careful planning.

The OECD’s BEPS (Base Erosion and Profit Shifting)guidelines, which are aimed at creating a level playing field infiscal terms and which Member States will need toincorporate individually, are also likely to have an impact ontreasury over the coming months and years. BEPS may notonly have an impact on location of treasury centres, but moreimportantly on funding strategies and transfer pricingpolicies.

Overall, there’s a strong message here for systems vendors. Theability of vendors to incorporate functions and features thatsupport new compliance requirements has become an essentialconsideration when treasurers select products. We’re seeingmany treasurers question vendors closely about upcomingregulations; if they’re dissatisfied by the answer, or concernedthat their current vendor doesn’t have convincing plans in placeto meet new requirements on a timely basis – or increasingly, toanticipate their needs – they’ll consider moving on.

What you need to think about

Look ahead at your likely future compliance needs Start looking at your systems options early Talk to your treasury system vendor about your needs

and their development program, as early as possible.

Fonte: Global Treasury survey 2014

PwC

EMIR

3

PwC

Quadro normativo

• I contratti derivati “over the counter” : scarsa trasparenza e limitata rappresentazione dei livelli dirischio implicito

• Nel settembre 2009, i leader del G-20 riuniti a Pittsburgh hanno concordato quanto segue:

"Al massimo entro la fine del 2012 tutti i contratti derivati OTC standardizzatidovranno essere negoziati in borsa o, se del caso, su piattaforme elettroniche dinegoziazione e compensati mediante controparti centrali. I contratti derivati OTCdevono essere notificati ai repertori di dati sulle negoziazioni. I contratti noncompensati a livello centrale devono soddisfare requisiti patrimoniali più elevati“

• Il fine della regolamentazione EMIR è il miglioramento della trasparenza dei mercati dei derivati,l’attenuazione del rischio sistemico e la protezione dagli abusi di mercato

• Il Regolamento EMIR è entrato in vigore il 16 agosto 2012

4

PwC

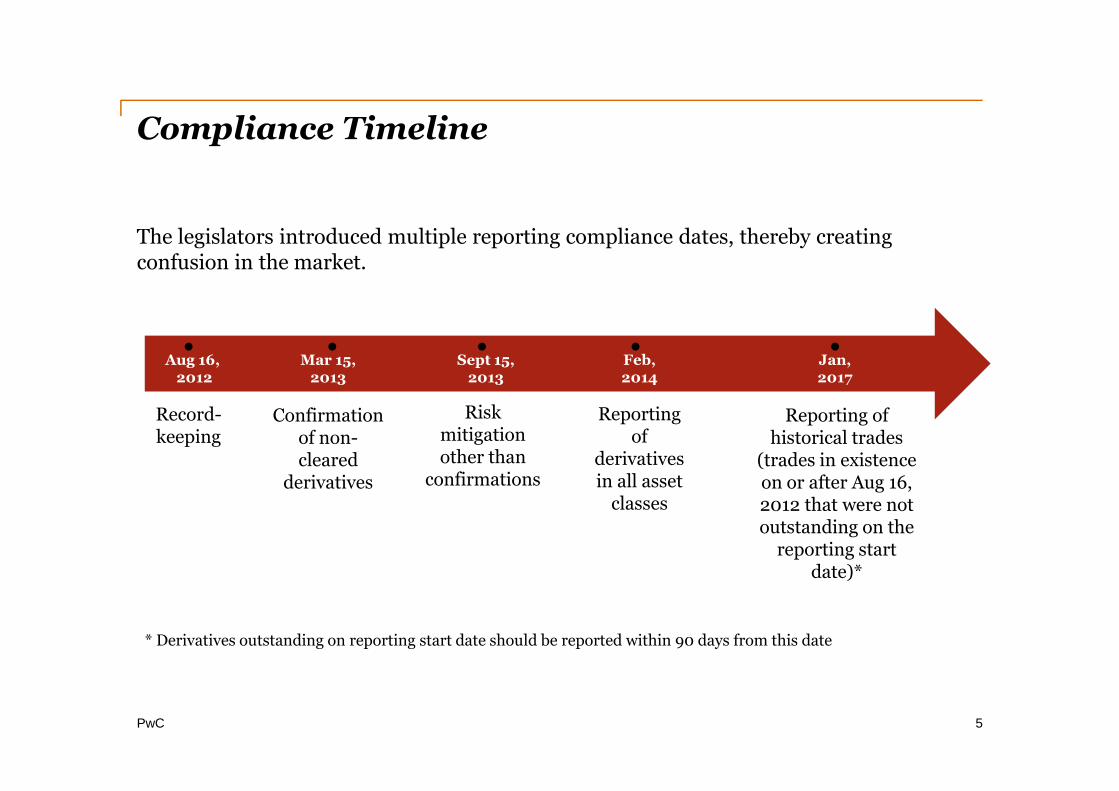

Compliance Timeline

The legislators introduced multiple reporting compliance dates, thereby creatingconfusion in the market.

Record-keeping

Aug 16,2012

Reportingof

derivativesin all asset

classes

Feb,2014

* Derivatives outstanding on reporting start date should be reported within 90 days from this date

5

Mar 15,2013

Confirmationof non-cleared

derivatives

Sept 15,2013

Riskmitigationother than

confirmations

Reporting ofhistorical trades

(trades in existenceon or after Aug 16,2012 that were notoutstanding on the

reporting startdate)*

Jan,2017

PwC

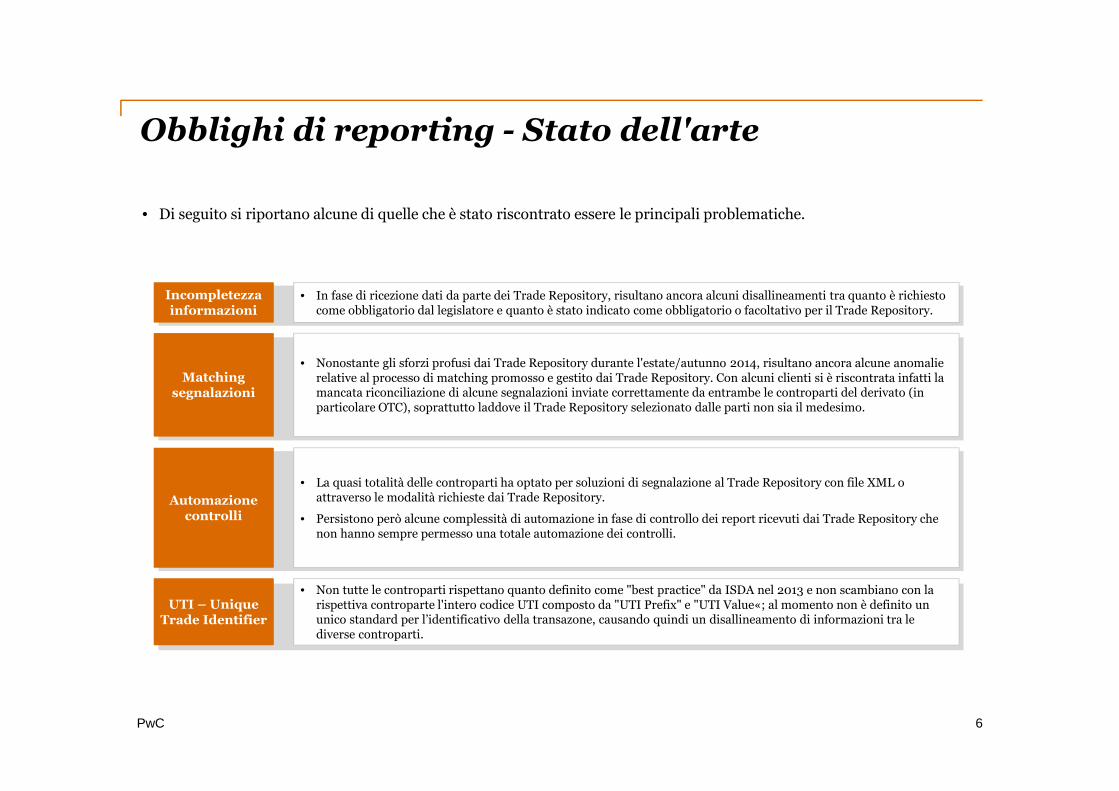

Obblighi di reporting - Stato dell'arte

• Di seguito si riportano alcune di quelle che è stato riscontrato essere le principali problematiche.

• In fase di ricezione dati da parte dei Trade Repository, risultano ancora alcuni disallineamenti tra quanto è richiestocome obbligatorio dal legislatore e quanto è stato indicato come obbligatorio o facoltativo per il Trade Repository.

Incompletezzainformazioni

Incompletezzainformazioni

• Nonostante gli sforzi profusi dai Trade Repository durante l'estate/autunno 2014, risultano ancora alcune anomalierelative al processo di matching promosso e gestito dai Trade Repository. Con alcuni clienti si è riscontrata infatti lamancata riconciliazione di alcune segnalazioni inviate correttamente da entrambe le controparti del derivato (inparticolare OTC), soprattutto laddove il Trade Repository selezionato dalle parti non sia il medesimo.

Matchingsegnalazioni

Matchingsegnalazioni

• La quasi totalità delle controparti ha optato per soluzioni di segnalazione al Trade Repository con file XML oattraverso le modalità richieste dai Trade Repository.

• Persistono però alcune complessità di automazione in fase di controllo dei report ricevuti dai Trade Repository chenon hanno sempre permesso una totale automazione dei controlli.

Automazionecontrolli

Automazionecontrolli

• Non tutte le controparti rispettano quanto definito come "best practice" da ISDA nel 2013 e non scambiano con larispettiva controparte l'intero codice UTI composto da "UTI Prefix" e "UTI Value«; al momento non è definito ununico standard per l’identificativo della transazone, causando quindi un disallineamento di informazioni tra lediverse controparti.

UTI – UniqueTrade Identifier

UTI – UniqueTrade Identifier

6

PwC 7

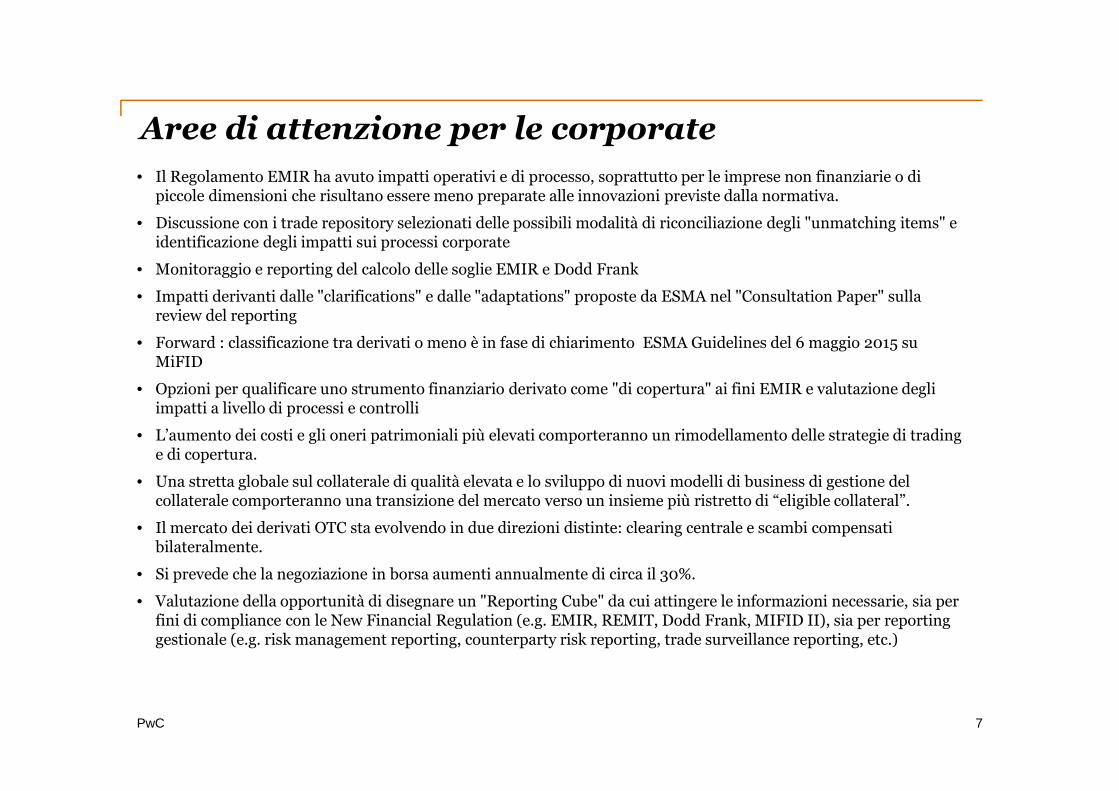

• Il Regolamento EMIR ha avuto impatti operativi e di processo, soprattutto per le imprese non finanziarie o dipiccole dimensioni che risultano essere meno preparate alle innovazioni previste dalla normativa.

• Discussione con i trade repository selezionati delle possibili modalità di riconciliazione degli "unmatching items" eidentificazione degli impatti sui processi corporate

• Monitoraggio e reporting del calcolo delle soglie EMIR e Dodd Frank

• Impatti derivanti dalle "clarifications" e dalle "adaptations" proposte da ESMA nel "Consultation Paper" sullareview del reporting

• Forward : classificazione tra derivati o meno è in fase di chiarimento ESMA Guidelines del 6 maggio 2015 suMiFID

• Opzioni per qualificare uno strumento finanziario derivato come "di copertura" ai fini EMIR e valutazione degliimpatti a livello di processi e controlli

• L’aumento dei costi e gli oneri patrimoniali più elevati comporteranno un rimodellamento delle strategie di tradinge di copertura.

• Una stretta globale sul collaterale di qualità elevata e lo sviluppo di nuovi modelli di business di gestione delcollaterale comporteranno una transizione del mercato verso un insieme più ristretto di “eligible collateral”.

• Il mercato dei derivati OTC sta evolvendo in due direzioni distinte: clearing centrale e scambi compensatibilateralmente.

• Si prevede che la negoziazione in borsa aumenti annualmente di circa il 30%.

• Valutazione della opportunità di disegnare un "Reporting Cube" da cui attingere le informazioni necessarie, sia perfini di compliance con le New Financial Regulation (e.g. EMIR, REMIT, Dodd Frank, MIFID II), sia per reportinggestionale (e.g. risk management reporting, counterparty risk reporting, trade surveillance reporting, etc.)

Aree di attenzione per le corporate

PwC

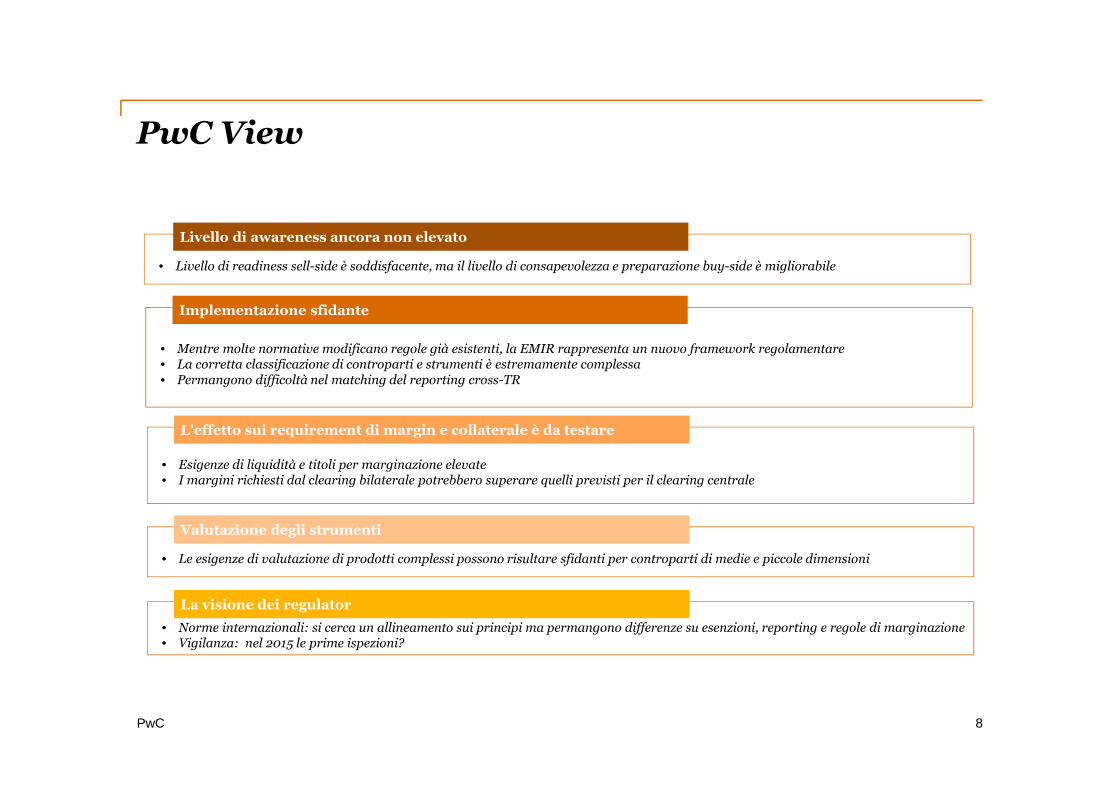

PwC View

• Livello di readiness sell-side è soddisfacente, ma il livello di consapevolezza e preparazione buy-side è migliorabile

Livello di awareness ancora non elevato

• Mentre molte normative modificano regole già esistenti, la EMIR rappresenta un nuovo framework regolamentare• La corretta classificazione di controparti e strumenti è estremamente complessa• Permangono difficoltà nel matching del reporting cross-TR

Implementazione sfidante

• Esigenze di liquidità e titoli per marginazione elevate• I margini richiesti dal clearing bilaterale potrebbero superare quelli previsti per il clearing centrale

L'effetto sui requirement di margin e collaterale è da testare

• Le esigenze di valutazione di prodotti complessi possono risultare sfidanti per controparti di medie e piccole dimensioni

Valutazione degli strumenti

• Norme internazionali: si cerca un allineamento sui principi ma permangono differenze su esenzioni, reporting e regole di marginazione• Vigilanza: nel 2015 le prime ispezioni?

La visione dei regulator

8

PwC

IFRS 9 hedge accounting

9

PwC

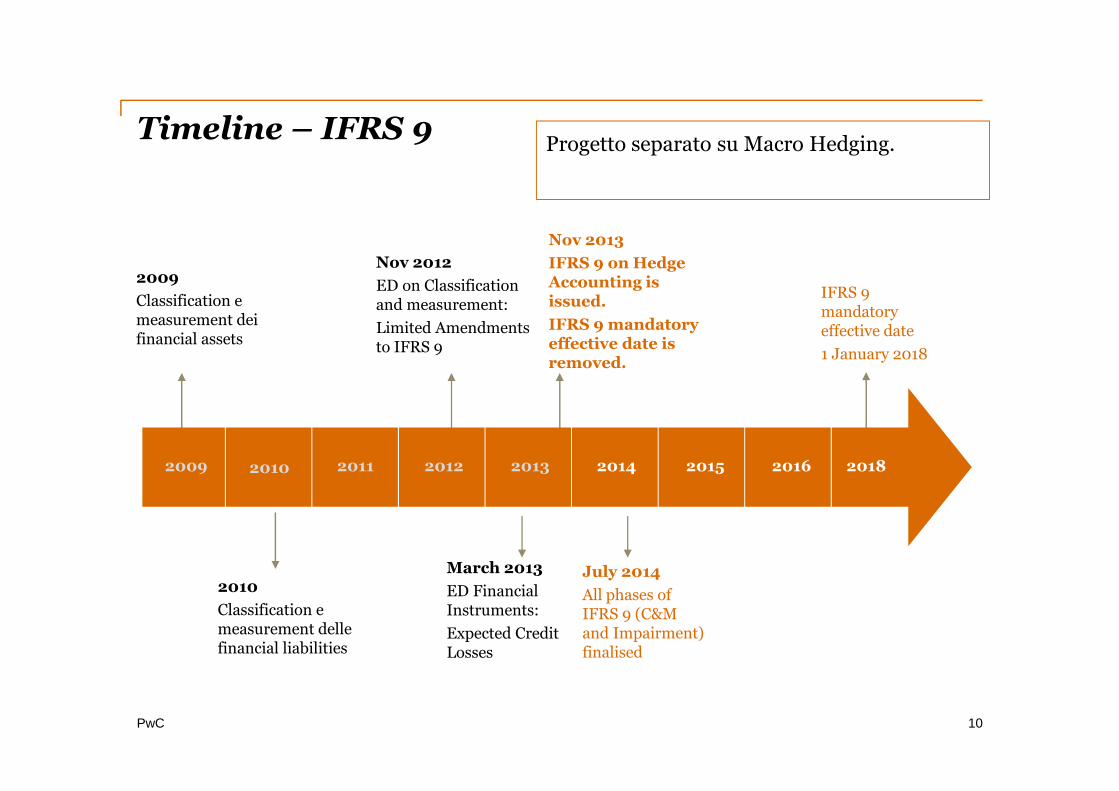

Timeline – IFRS 9

2009 2010 2011 2012 2014 2015 2016 2018

2009

Classification emeasurement deifinancial assets

Nov 2013

IFRS 9 on HedgeAccounting isissued.

IFRS 9 mandatoryeffective date isremoved.

IFRS 9mandatoryeffective date

1 January 2018

Nov 2012

ED on Classificationand measurement:

Limited Amendmentsto IFRS 9

2010

Classification emeasurement dellefinancial liabilities

July 2014

All phases ofIFRS 9 (C&Mand Impairment)finalised

March 2013

ED FinancialInstruments:

Expected CreditLosses

Progetto separato su Macro Hedging.

2013

10

PwC

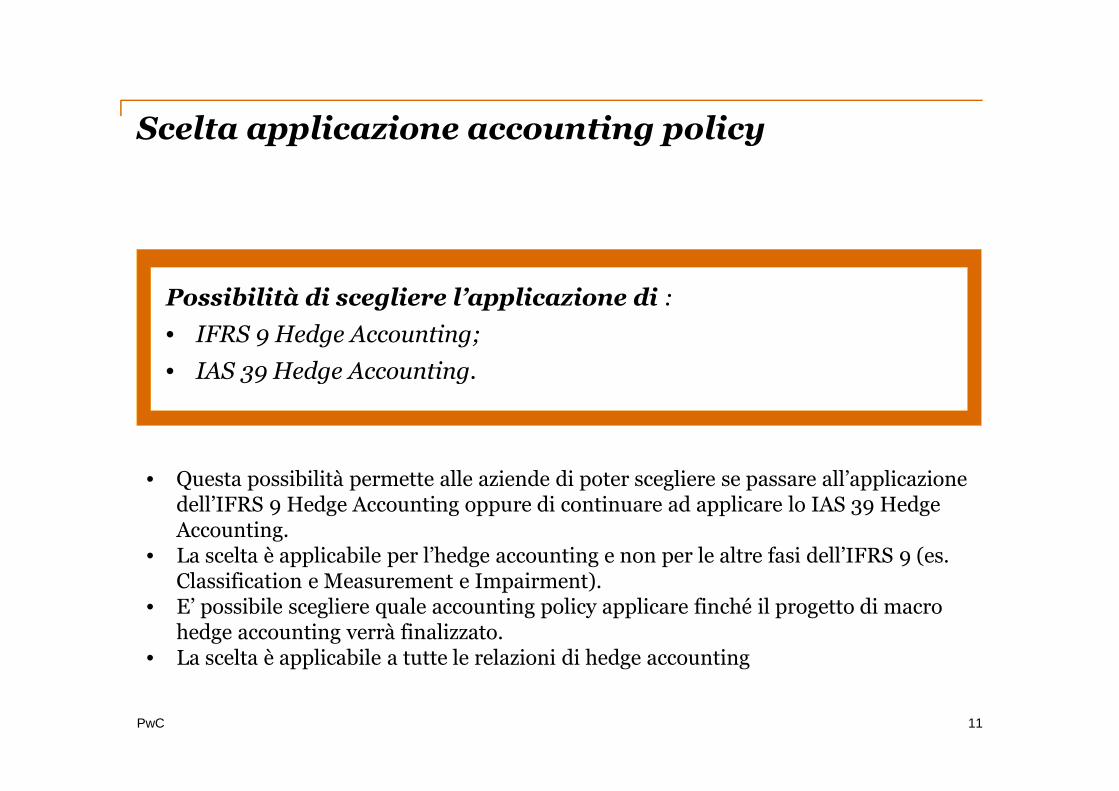

Scelta applicazione accounting policy

Possibilità di scegliere l’applicazione di :

• IFRS 9 Hedge Accounting;

• IAS 39 Hedge Accounting.

11

• Questa possibilità permette alle aziende di poter scegliere se passare all’applicazionedell’IFRS 9 Hedge Accounting oppure di continuare ad applicare lo IAS 39 HedgeAccounting.

• La scelta è applicabile per l’hedge accounting e non per le altre fasi dell’IFRS 9 (es.Classification e Measurement e Impairment).

• E’ possibile scegliere quale accounting policy applicare finché il progetto di macrohedge accounting verrà finalizzato.

• La scelta è applicabile a tutte le relazioni di hedge accounting

PwC

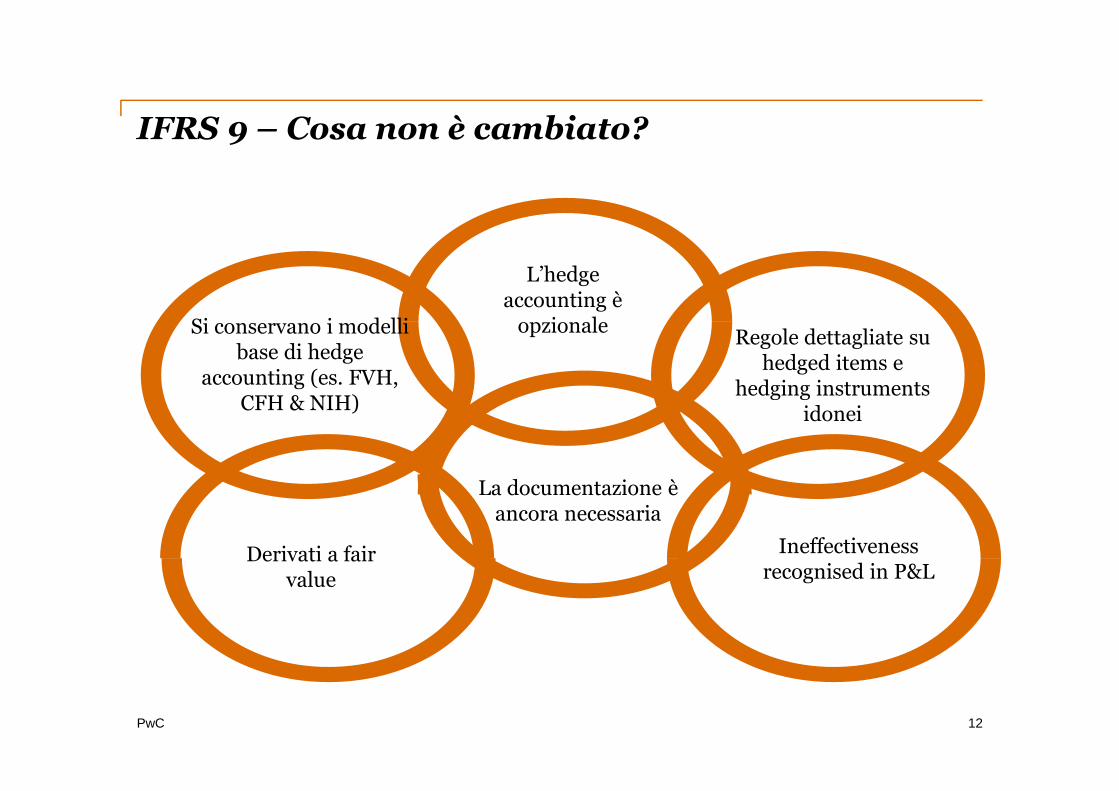

IFRS 9 – Cosa non è cambiato?

Si conservano i modellibase di hedge

accounting (es. FVH,CFH & NIH)

L’hedgeaccounting è

opzionaleRegole dettagliate su

hedged items ehedging instruments

idonei

12

La documentazione èancora necessaria

Derivati a fairvalue

Ineffectivenessrecognised in P&L

PwC

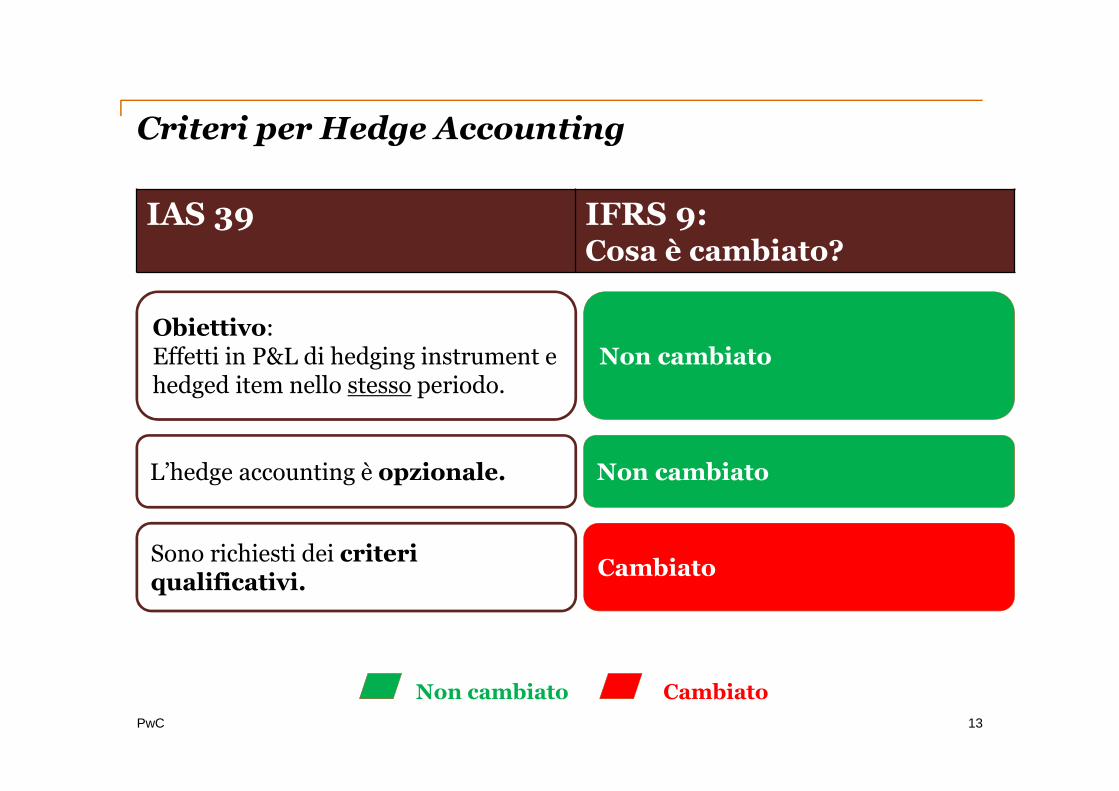

Criteri per Hedge Accounting

IAS 39 IFRS 9:Cosa è cambiato?

CambiatoNon cambiato

L’hedge accounting è opzionale.

Obiettivo:Effetti in P&L di hedging instrument ehedged item nello stesso periodo.

Sono richiesti dei criteriqualificativi.

Cambiato

Non cambiato

Non cambiato

13

PwC

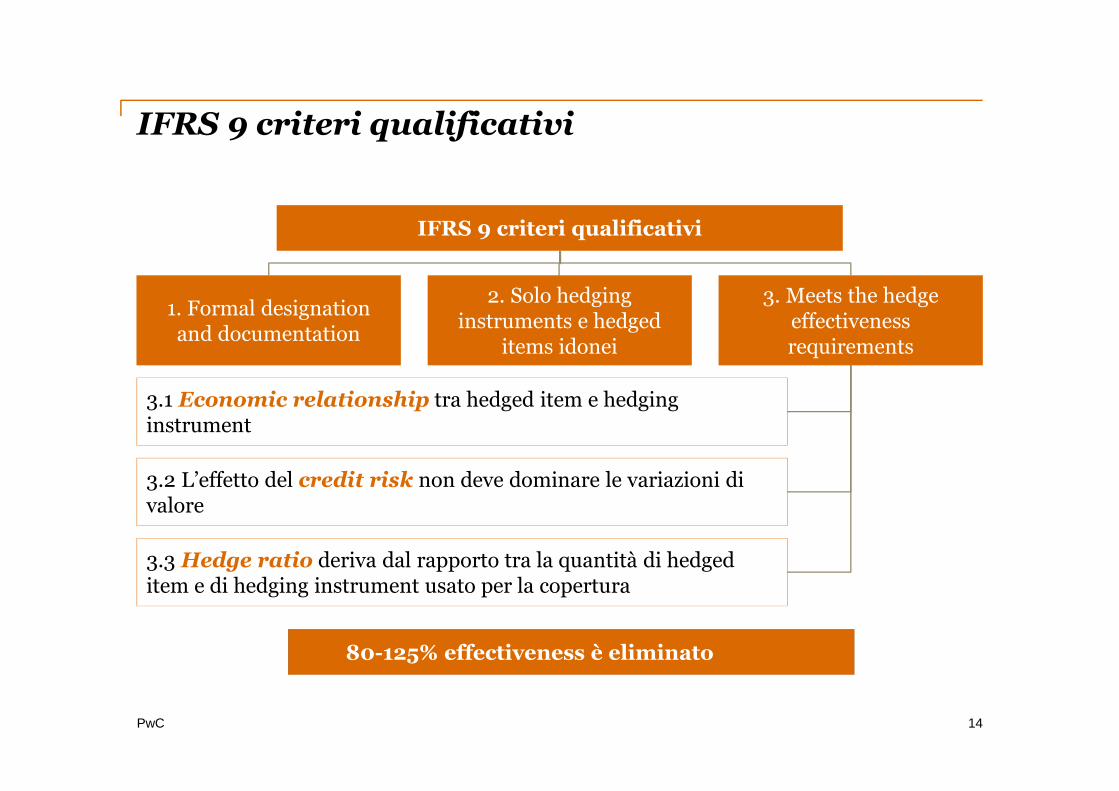

IFRS 9 criteri qualificativi

80-125% effectiveness è eliminato

IFRS 9 criteri qualificativi

1. Formal designationand documentation

2. Solo hedginginstruments e hedged

items idonei

3. Meets the hedgeeffectivenessrequirements

3.1 Economic relationship tra hedged item e hedginginstrument

3.2 L’effetto del credit risk non deve dominare le variazioni divalore

3.3 Hedge ratio deriva dal rapporto tra la quantità di hedgeditem e di hedging instrument usato per la copertura

14

PwC

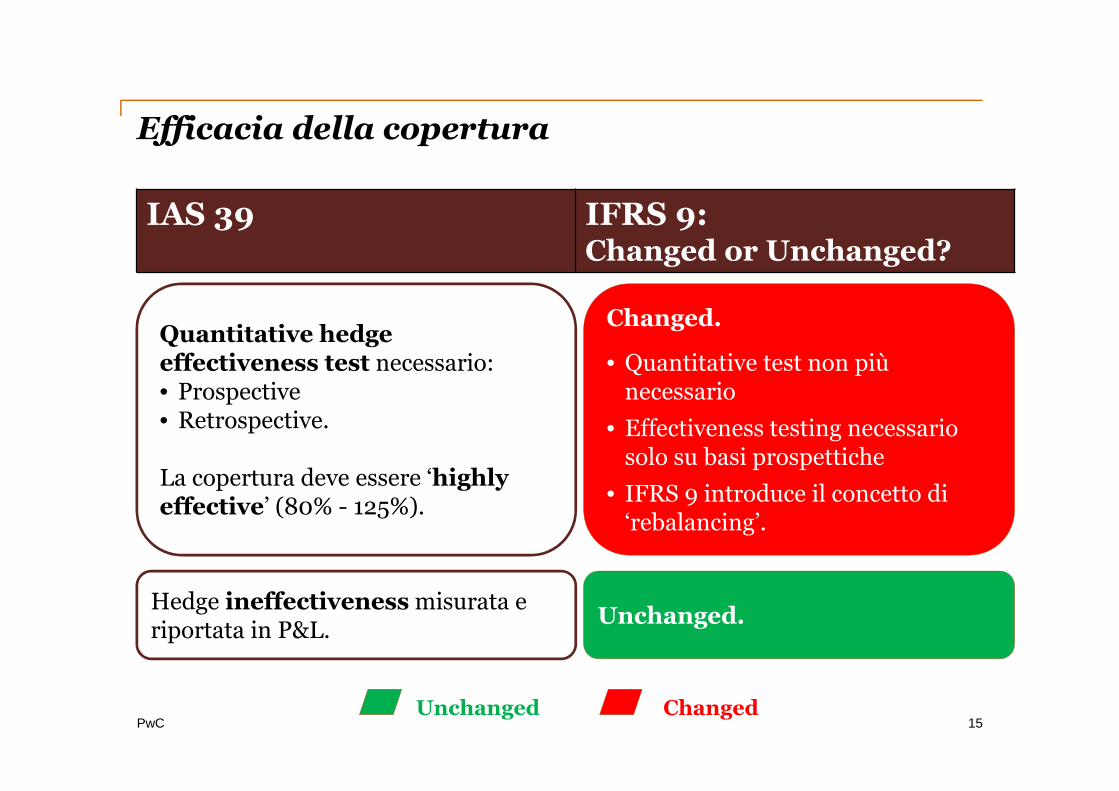

Efficacia della copertura

IAS 39 IFRS 9:Changed or Unchanged?

ChangedUnchanged

Quantitative hedgeeffectiveness test necessario:• Prospective• Retrospective.

La copertura deve essere ‘highlyeffective’ (80% - 125%).

Hedge ineffectiveness misurata eriportata in P&L.

Unchanged.

Changed.

• Quantitative test non piùnecessario

• Effectiveness testing necessariosolo su basi prospettiche

• IFRS 9 introduce il concetto di‘rebalancing’.

15

PwC

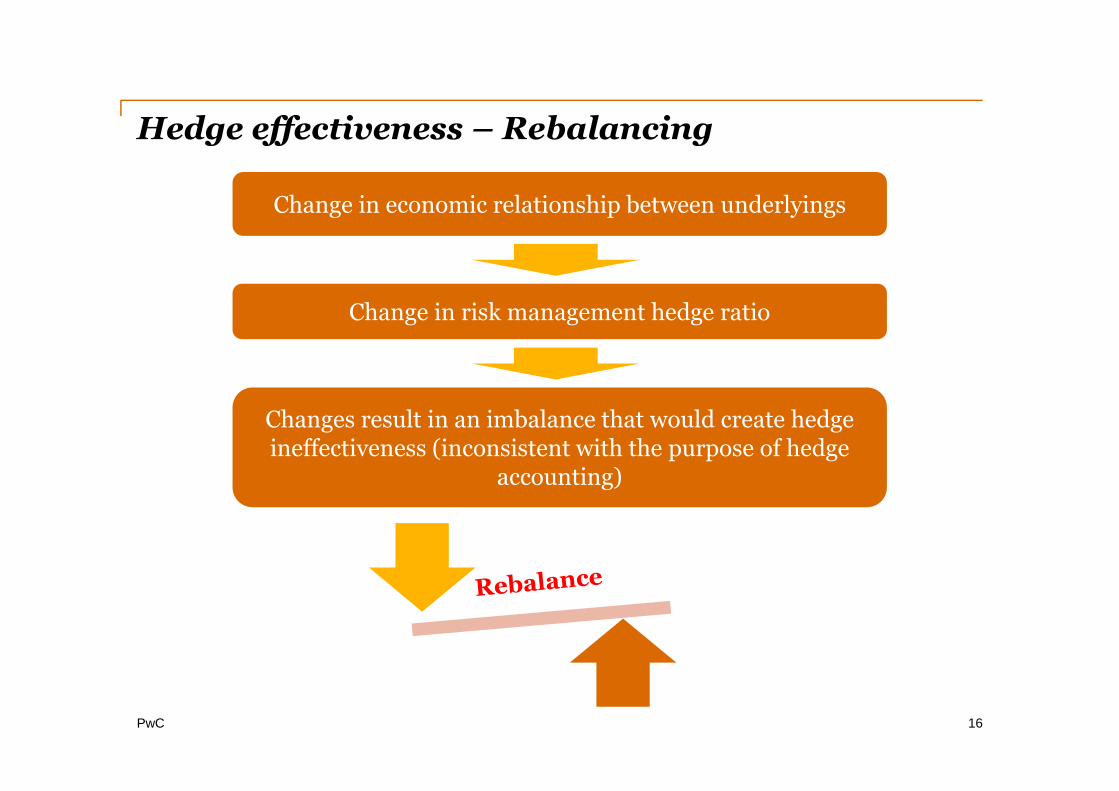

Hedge effectiveness – Rebalancing

Change in economic relationship between underlyings

Changes result in an imbalance that would create hedgeineffectiveness (inconsistent with the purpose of hedge

accounting)

Change in risk management hedge ratio

16

PwC

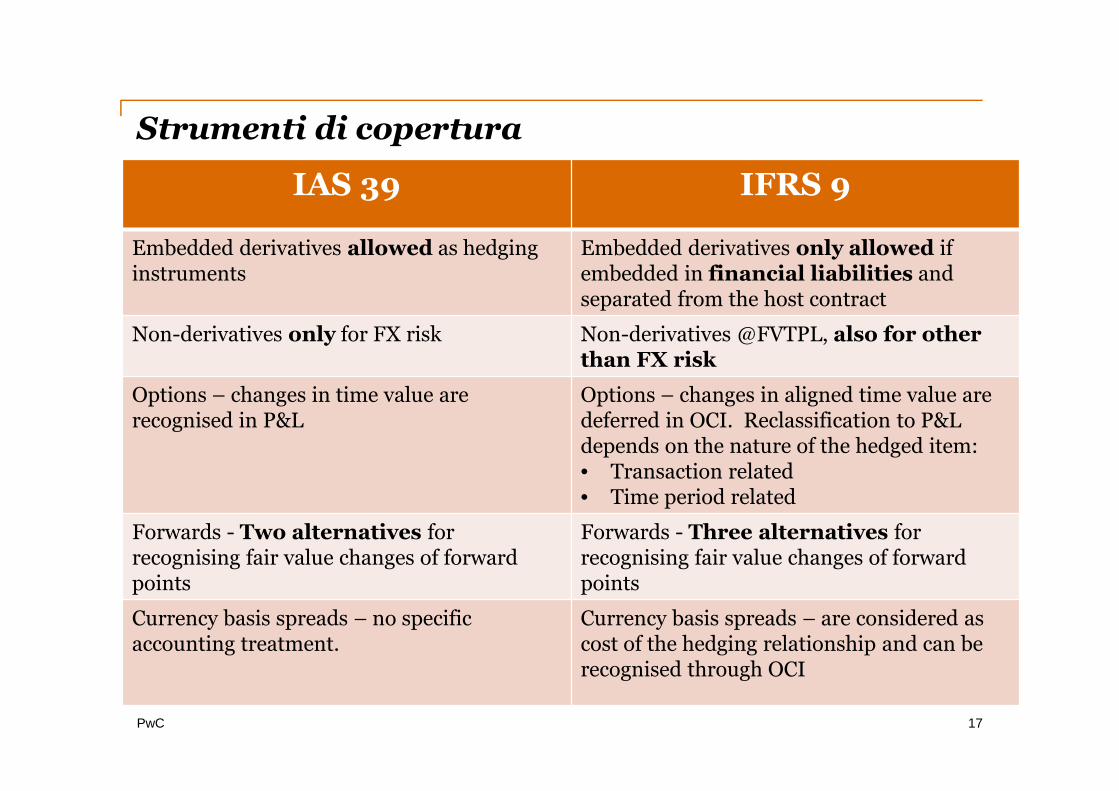

Strumenti di copertura

17

IAS 39 IFRS 9

Embedded derivatives allowed as hedginginstruments

Embedded derivatives only allowed ifembedded in financial liabilities andseparated from the host contract

Non-derivatives only for FX risk Non-derivatives @FVTPL, also for otherthan FX risk

Options – changes in time value arerecognised in P&L

Options – changes in aligned time value aredeferred in OCI. Reclassification to P&Ldepends on the nature of the hedged item:• Transaction related• Time period related

Forwards - Two alternatives forrecognising fair value changes of forwardpoints

Forwards - Three alternatives forrecognising fair value changes of forwardpoints

Currency basis spreads – no specificaccounting treatment.

Currency basis spreads – are considered ascost of the hedging relationship and can berecognised through OCI

PwC

Strumenti coperti

18

IAS 39 IFRS 9

Only possible to hedge risk components offinancial items

Possible to hedge risk components of bothfinancial and non-financial items

Derivatives not allowed as hedged items Aggregated positions allowed

Net positions not allowed Net positions (including net nil positions)allowed as hedged item, in certaincircumstances

Equity instruments through OCI cannot behedged item

Equity instruments through OCI can behedged items

Use of layers as hedged item relativelyrestricted. Layers only for cash flow hedges

Layers allowed for both cash flow hedges,fair value hedges and groups of items

PwC

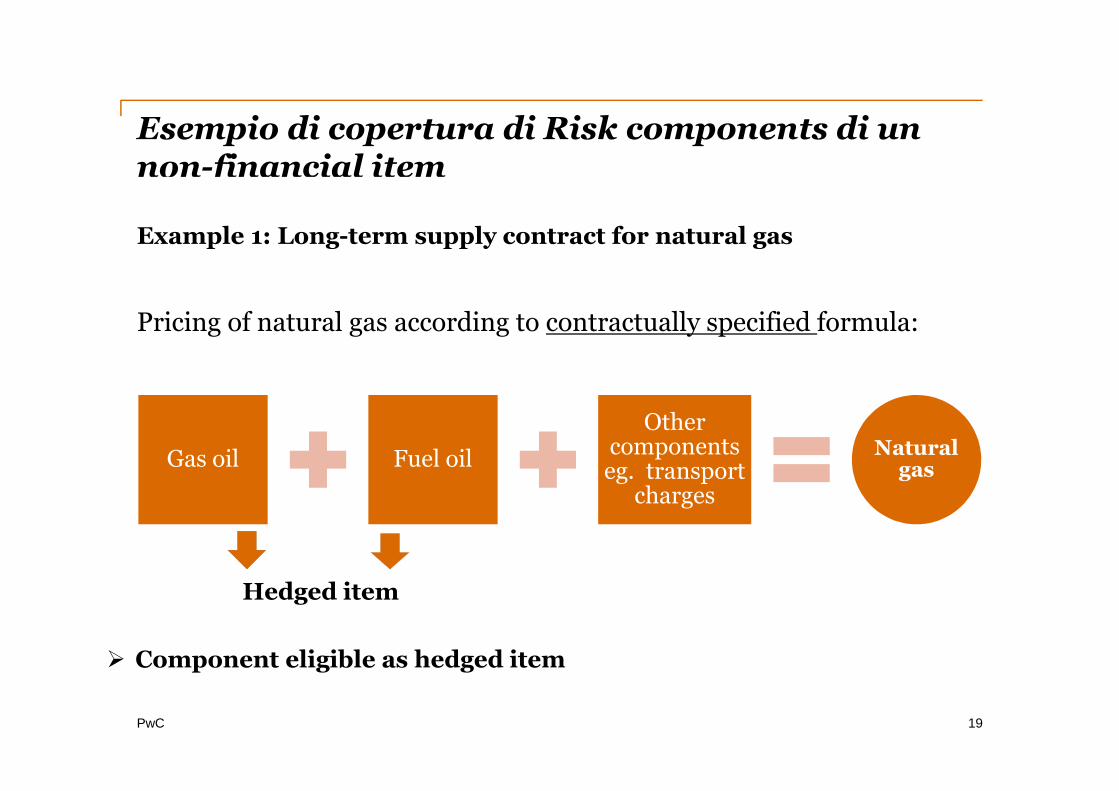

Esempio di copertura di Risk components di unnon-financial item

19

Example 1: Long-term supply contract for natural gas

Pricing of natural gas according to contractually specified formula:

Gas oil Fuel oil

Othercomponentseg. transport

charges

Naturalgas

Hedged item

Component eligible as hedged item

PwC

PurchasesTeam(EUR)

SalesDepartment

(EUR)

Bank

CentralTreasury

USD 100

USD 100

USD 90

USD 90

USD 10

EUR 72

EUR 8

EUR 80

IAS 39

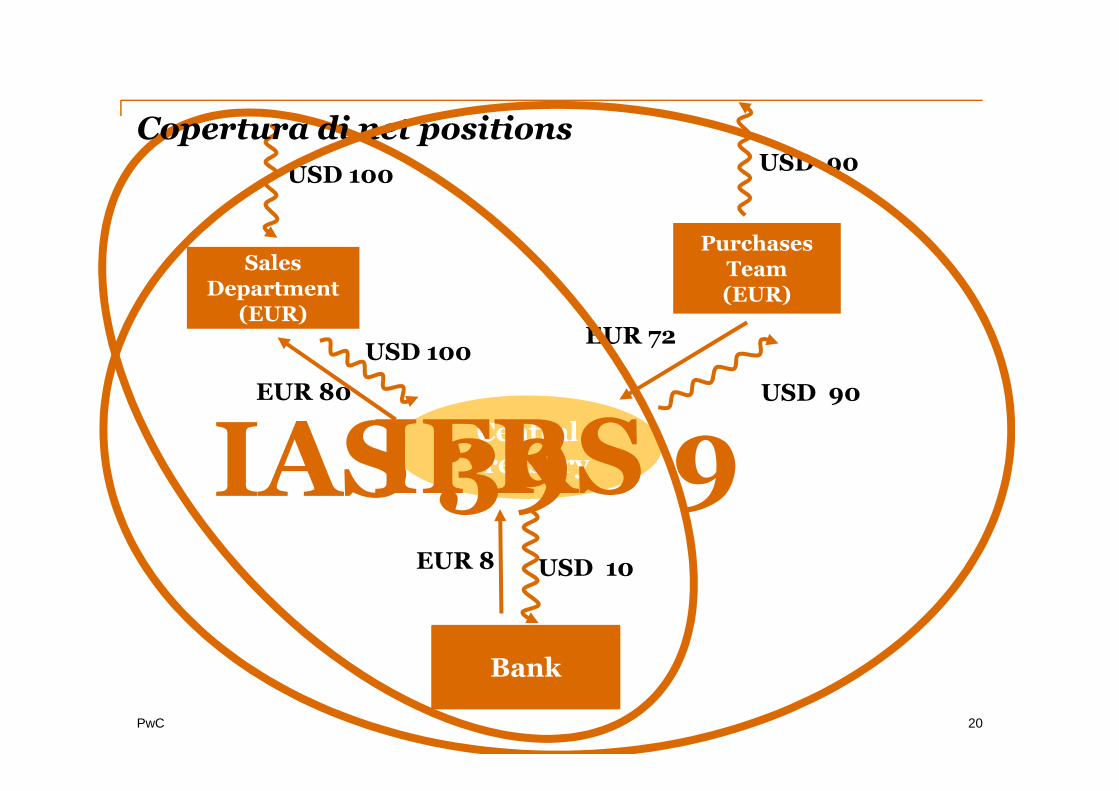

Copertura di net positions

IFRS 9

20

PwC

Opzione di designazione di una esposizione alrischio credito a fair value through P&L

Allows fair value through profit or loss accounting for a financialinstrument (or a proportion of it) when hedged with a creditderivative.

Certain criteria must be met.

Not irrevocable.

Disclosure requirements added.

21

PwC

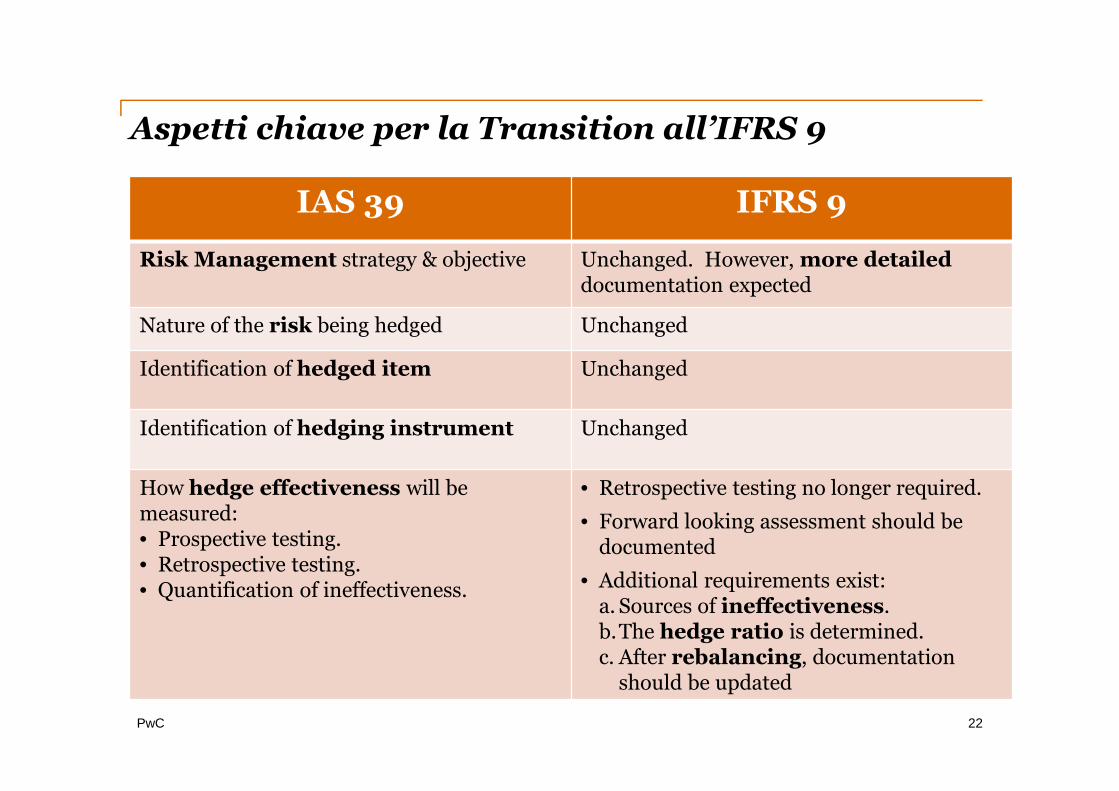

Aspetti chiave per la Transition all’IFRS 9

IAS 39 IFRS 9

Risk Management strategy & objective Unchanged. However, more detaileddocumentation expected

Nature of the risk being hedged Unchanged

Identification of hedged item Unchanged

Identification of hedging instrument Unchanged

How hedge effectiveness will bemeasured:• Prospective testing.• Retrospective testing.• Quantification of ineffectiveness.

• Retrospective testing no longer required.

• Forward looking assessment should bedocumented

• Additional requirements exist:a. Sources of ineffectiveness.b.The hedge ratio is determined.c. After rebalancing, documentation

should be updated

22

PwC23

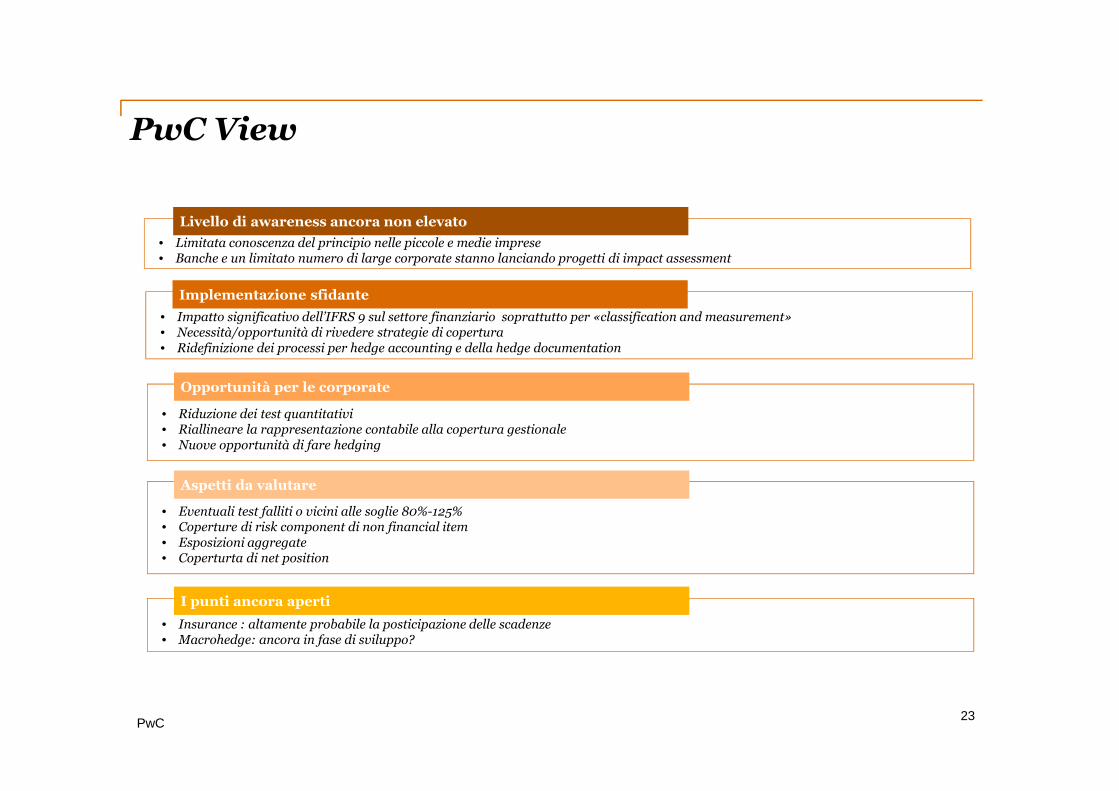

PwC View

• Limitata conoscenza del principio nelle piccole e medie imprese• Banche e un limitato numero di large corporate stanno lanciando progetti di impact assessment

Livello di awareness ancora non elevato

• Impatto significativo dell’IFRS 9 sul settore finanziario soprattutto per «classification and measurement»• Necessità/opportunità di rivedere strategie di copertura• Ridefinizione dei processi per hedge accounting e della hedge documentation

Implementazione sfidante

• Riduzione dei test quantitativi• Riallineare la rappresentazione contabile alla copertura gestionale• Nuove opportunità di fare hedging

Opportunità per le corporate

• Eventuali test falliti o vicini alle soglie 80%-125%• Coperture di risk component di non financial item• Esposizioni aggregate• Coperturta di net position

Aspetti da valutare

• Insurance : altamente probabile la posticipazione delle scadenze• Macrohedge: ancora in fase di sviluppo?

I punti ancora aperti

Thank you ...

This publication has been prepared for general guidance on matters of interest only, and doesnot constitute professional advice. You should not act upon the information contained in thispublication without obtaining specific professional advice. No representation or warranty(express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, itsmembers, employees and agents do not accept or assume any liability, responsibility or duty ofcare for any consequences of you or anyone else acting, or refraining to act, in reliance on theinformation contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, "PwC" refers tothe UK member firm, and may sometimes refer to the PwC network. Each member firm is aseparate legal entity. Please see www.pwc.com/structure for further details.

Riccardo Bua OdettiPartner

PricewaterhouseCoopers Advisory SpA

Via Monte Rosa, 91

20149 Milano

T: +39 02 66720536

M: +39 348 4428809

www.pwc.com/it