npd presentation

TRANSCRIPT

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Copyright 2014. The NPD Group, Inc. All Rights Reserved. This presentation is Proprietary and Confidential and may not be disclosed in any manner, in whole or in part, to any third party without the express written consent of NPD.

Copyright 2014. The NPD Group, Inc. All Rights Reserved. This presentation is Proprietary and Confidential and may not be disclosed in any manner, in whole or in part, to any third party without the express written consent of NPD.

State of the Plate:

Fruit & Vegetable Consumption Trends

March 2015

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Trends in Fruits & Vegetables

Consumption

2

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Is Fruit & Vegetable Consumption Growing?

3

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

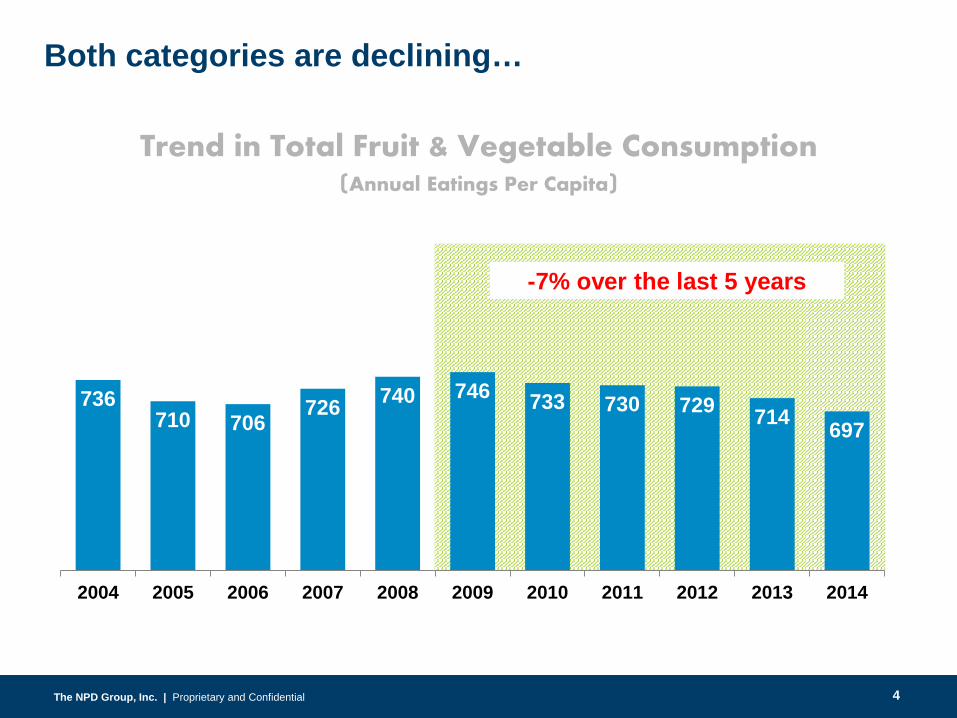

736710 706

726 740 746 733 730 729 714 697

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Trend in Total Fruit & Vegetable Consumption(Annual Eatings Per Capita)

-7% over the last 5 years

Both categories are declining…

4

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

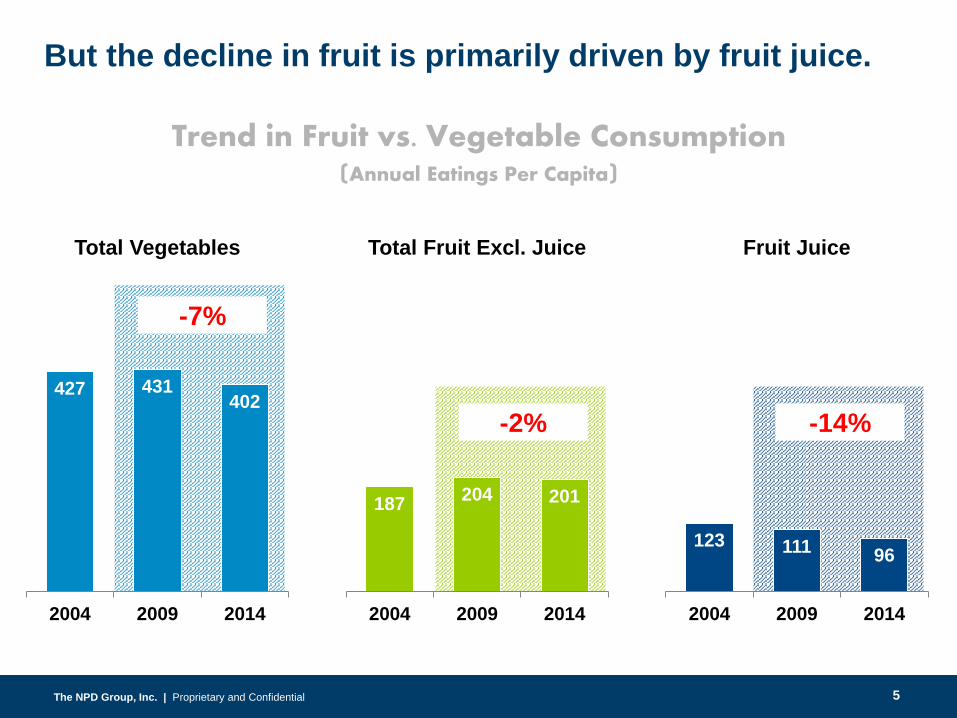

427 431402

2004 2009 2014

Total Vegetables

187 204 201

2004 2009 2014

Total Fruit Excl. Juice

123 111 96

2004 2009 2014

Fruit Juice

But the decline in fruit is primarily driven by fruit juice.

-2% -14%

-7%

Trend in Fruit vs. Vegetable Consumption(Annual Eatings Per Capita)

5

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

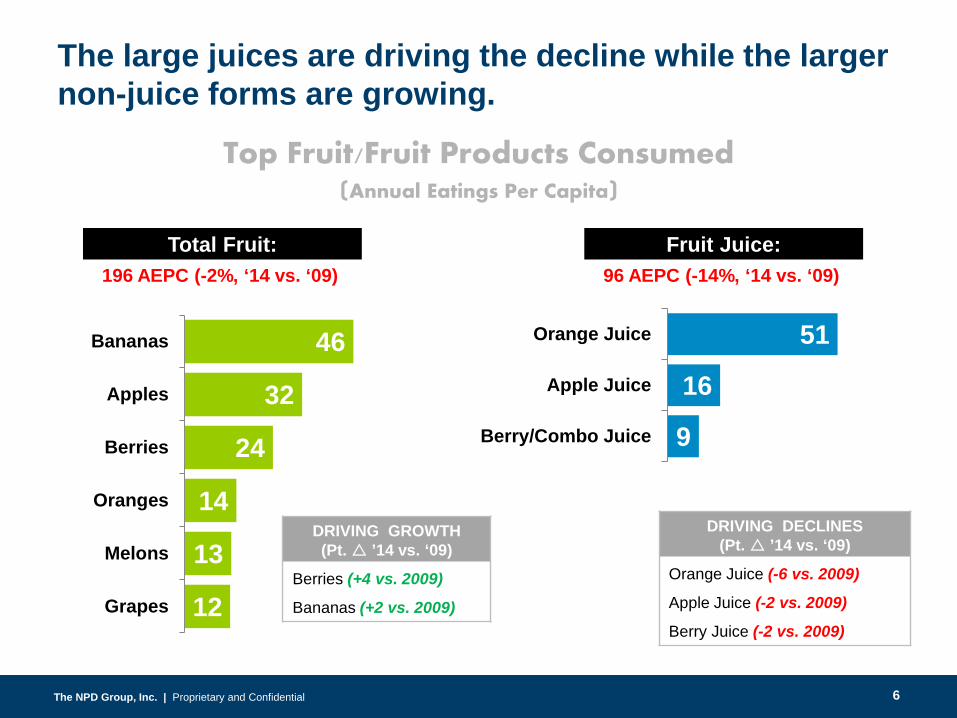

9

16

51

Berry/Combo Juice

Apple Juice

Orange Juice

Fruit Juice:

12

13

14

24

32

46

Grapes

Melons

Oranges

Berries

Apples

Bananas

Total Fruit:

Top Fruit/Fruit Products Consumed(Annual Eatings Per Capita)

The large juices are driving the decline while the larger non-juice forms are growing.

DRIVING GROWTH (Pt. ’14 vs. ‘09)

Berries (+4 vs. 2009)

Bananas (+2 vs. 2009)

DRIVING DECLINES (Pt. ’14 vs. ‘09)

Orange Juice (-6 vs. 2009)

Apple Juice (-2 vs. 2009)

Berry Juice (-2 vs. 2009)

96 AEPC (-14%, ‘14 vs. ‘09) 196 AEPC (-2%, ‘14 vs. ‘09)

6

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

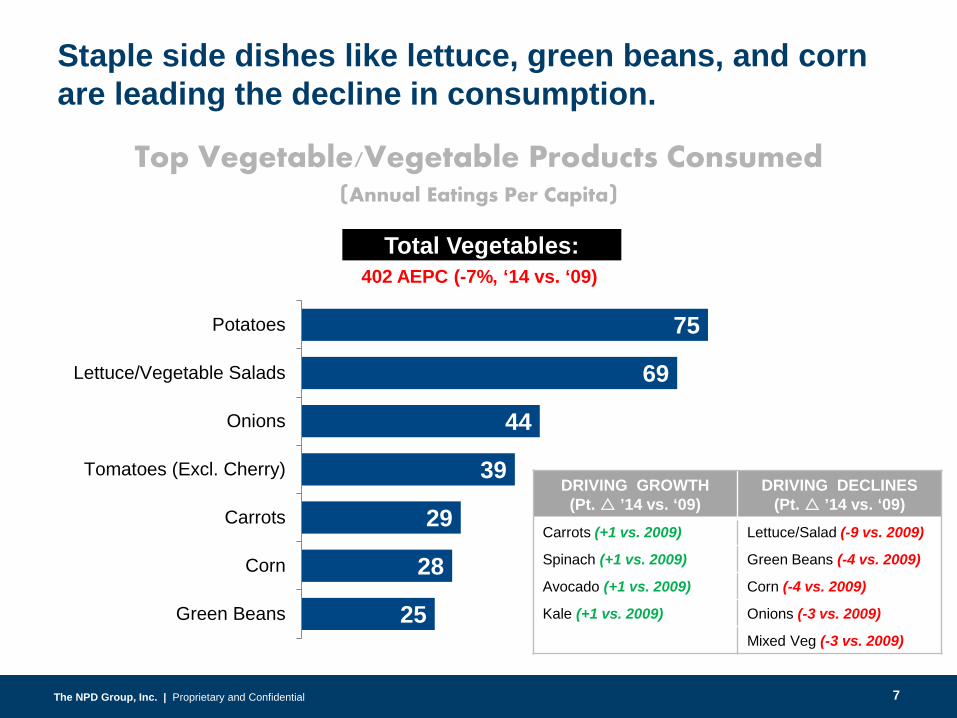

Staple side dishes like lettuce, green beans, and corn are leading the decline in consumption.

25

28

29

39

44

69

75

Green Beans

Corn

Carrots

Tomatoes (Excl. Cherry)

Onions

Lettuce/Vegetable Salads

Potatoes

Top Vegetable/Vegetable Products Consumed(Annual Eatings Per Capita)

DRIVING GROWTH (Pt. ’14 vs. ‘09)

DRIVING DECLINES (Pt. ’14 vs. ‘09)

Carrots (+1 vs. 2009) Lettuce/Salad (-9 vs. 2009)

Spinach (+1 vs. 2009) Green Beans (-4 vs. 2009)

Avocado (+1 vs. 2009) Corn (-4 vs. 2009)

Kale (+1 vs. 2009) Onions (-3 vs. 2009)

Mixed Veg (-3 vs. 2009)

Total Vegetables:402 AEPC (-7%, ‘14 vs. ‘09)

7

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

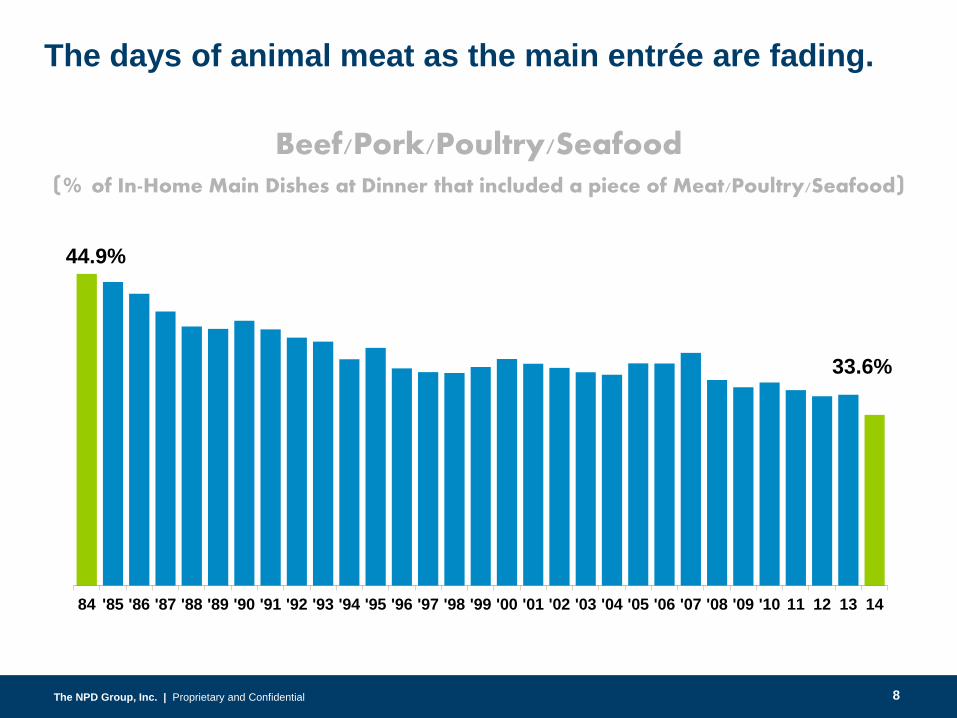

44.9%

33.6%

84 '85 '86 '87 '88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 11 12 13 14

Beef/Pork/Poultry/Seafood(% of In-Home Main Dishes at Dinner that included a piece of Meat/Poultry/Seafood)

The days of animal meat as the main entrée are fading.

8

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

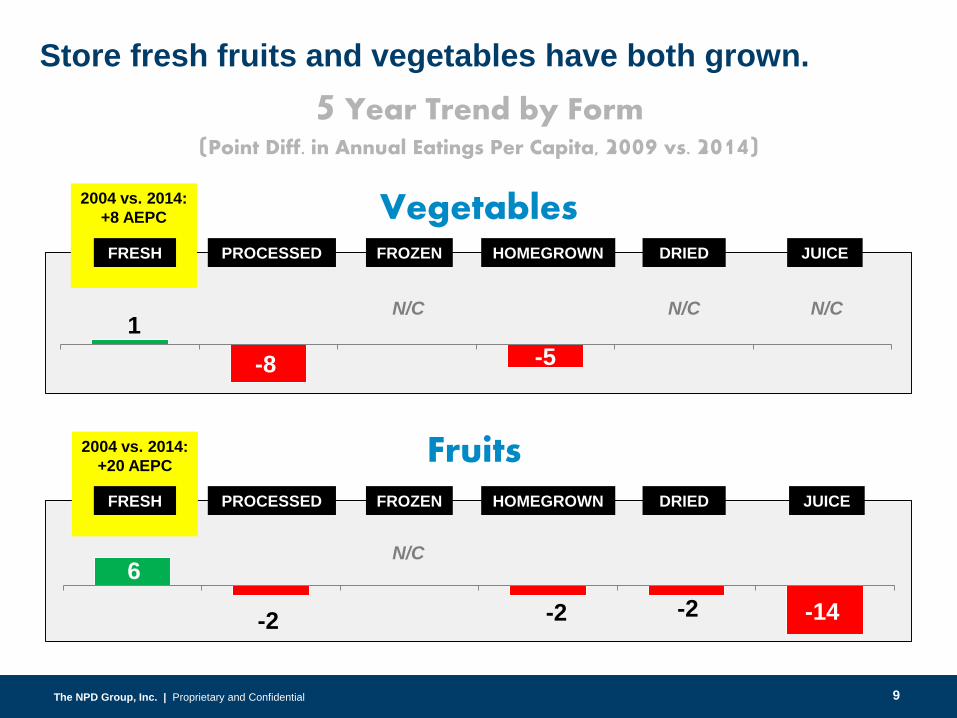

1-8 -5

2004 vs. 2014: +20 AEPC

2004 vs. 2014: +8 AEPC Vegetables

Fruits

FRESH PROCESSED FROZEN HOMEGROWN DRIED

5 Year Trend by Form(Point Diff. in Annual Eatings Per Capita, 2009 vs. 2014)

Store fresh fruits and vegetables have both grown.

JUICE

6

-2 -2 -2 -14

N/C N/C N/C

N/C

PROCESSED FROZEN HOMEGROWN DRIED JUICEFRESH

9

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

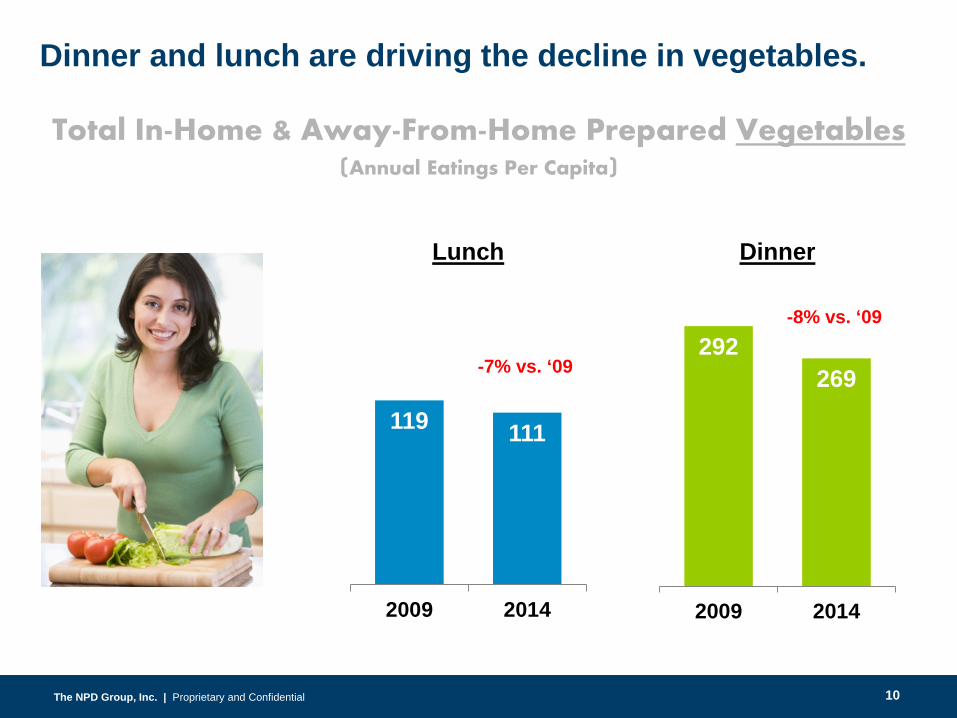

119 111

2009 2014

Lunch

Total In-Home & Away-From-Home Prepared Vegetables(Annual Eatings Per Capita)

292269

2009 2014

Dinner

-8% vs. ‘09

-7% vs. ‘09

Dinner and lunch are driving the decline in vegetables.

10

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

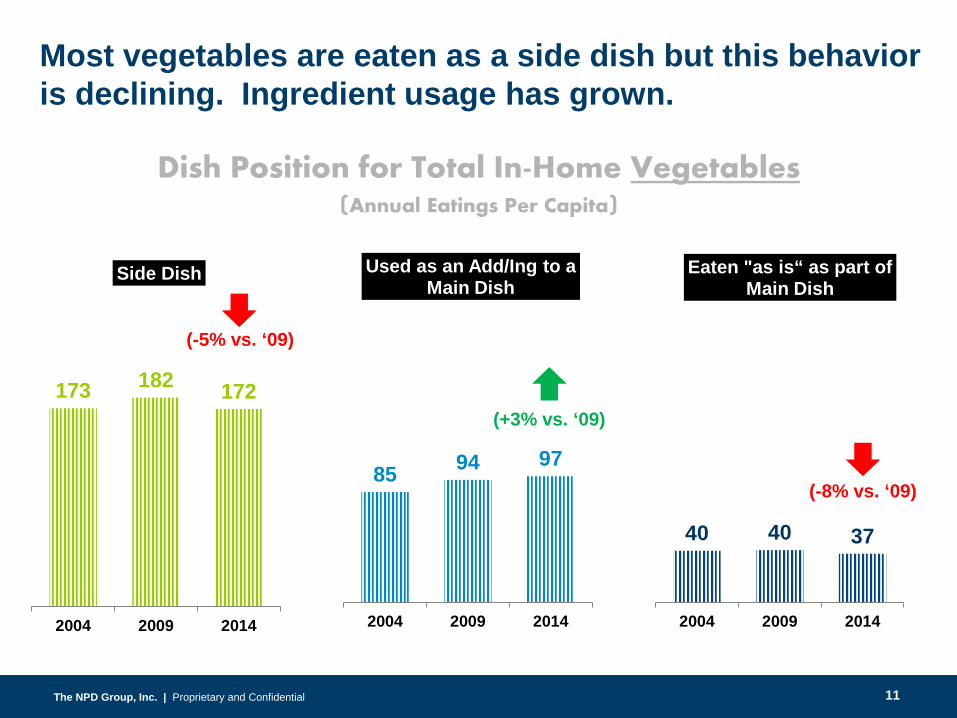

Dish Position for Total In-Home Vegetables(Annual Eatings Per Capita)

173 182 172

2004 2009 2014

Side Dish

(-5% vs. ‘09)

85 94 97

2004 2009 2014

Used as an Add/Ing to a Main Dish

40 40 37

2004 2009 2014

Eaten "as is“ as part of Main Dish

(+3% vs. ‘09)

(-8% vs. ‘09)

Most vegetables are eaten as a side dish but this behavior is declining. Ingredient usage has grown.

11

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

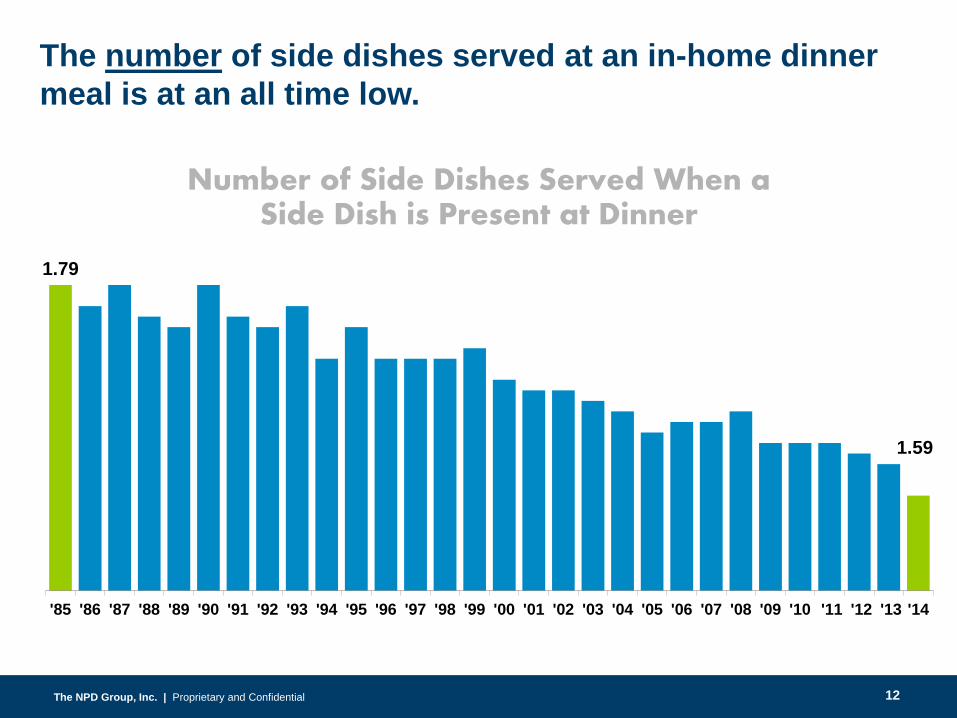

1.79

1.59

'85 '86 '87 '88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Number of Side Dishes Served When a Side Dish is Present at Dinner

The number of side dishes served at an in-home dinner meal is at an all time low.

12

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

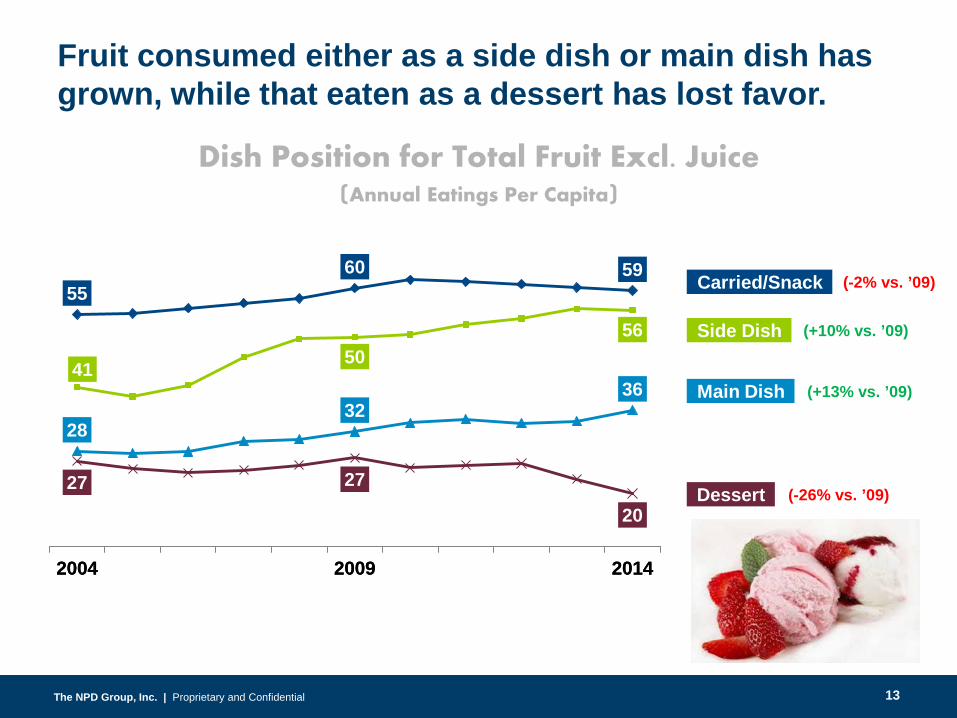

5560 59

27 27

20

2004 2009 2014

(-2% vs. ’09)Carried/Snack

(-26% vs. ’09)Dessert

Fruit consumed either as a side dish or main dish has grown, while that eaten as a dessert has lost favor.

41 5056

2832

36

2004 2009 2014

(+10% vs. ’09)Side Dish

(+13% vs. ’09)Main Dish

Dish Position for Total Fruit Excl. Juice(Annual Eatings Per Capita)

13

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

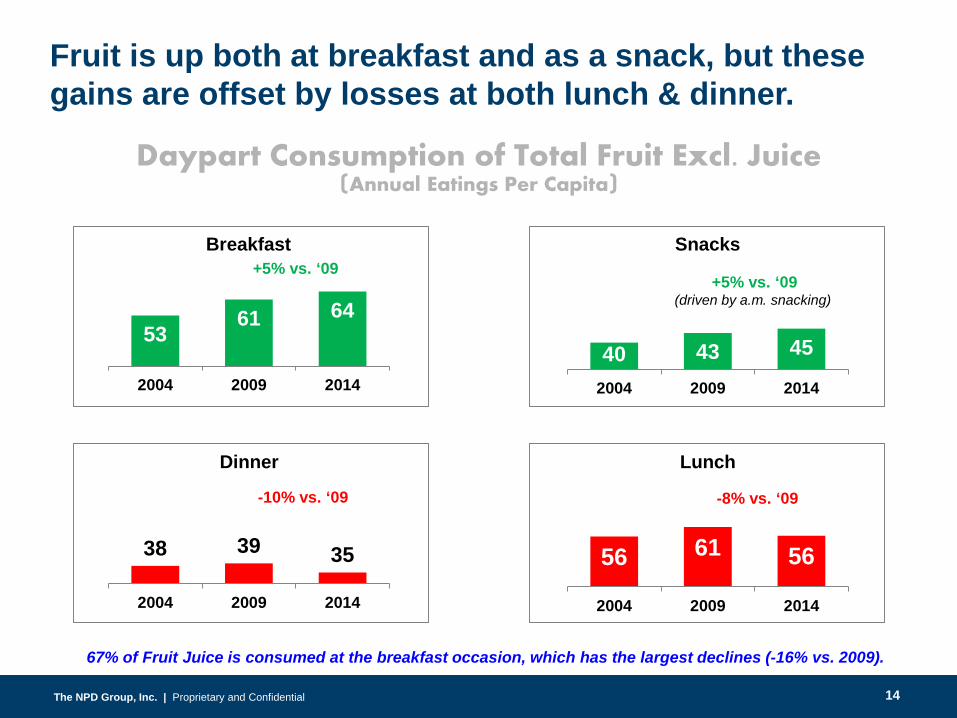

67% of Fruit Juice is consumed at the breakfast occasion, which has the largest declines (-16% vs. 2009).

Daypart Consumption of Total Fruit Excl. Juice (Annual Eatings Per Capita)

Fruit is up both at breakfast and as a snack, but these gains are offset by losses at both lunch & dinner.

-8% vs. ‘09-10% vs. ‘09

56 61 56

2004 2009 2014

Lunch

38 39 35

2004 2009 2014

Dinner

+5% vs. ‘09

5361 64

2004 2009 2014

Breakfast

+5% vs. ‘09(driven by a.m. snacking)

40 43 45

2004 2009 2014

Snacks

14

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

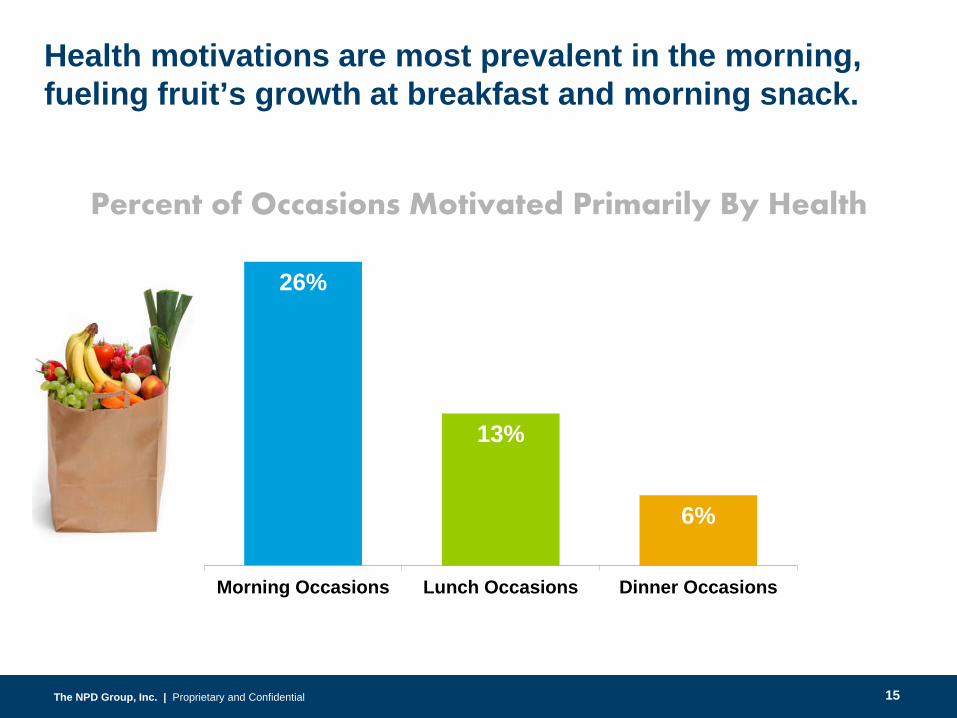

26%

13%

6%

Morning Occasions Lunch Occasions Dinner Occasions

Percent of Occasions Motivated Primarily By Health

Health motivations are most prevalent in the morning, fueling fruit’s growth at breakfast and morning snack.

15

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

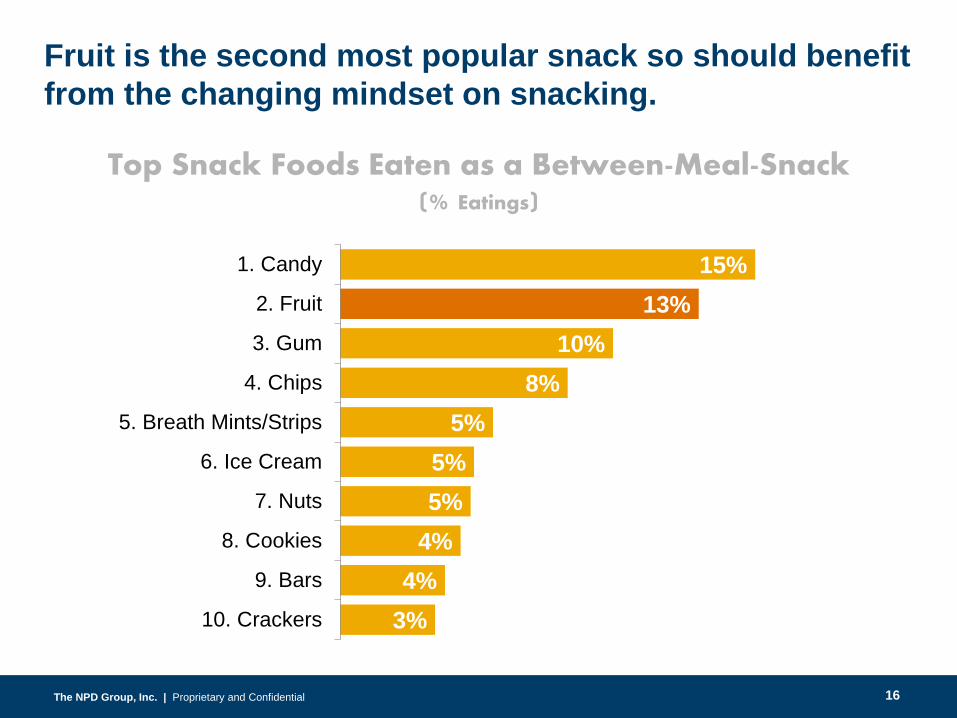

15%13%

10%8%

5%5%5%

4%4%

3%

1. Candy

2. Fruit

3. Gum

4. Chips

5. Breath Mints/Strips

6. Ice Cream

7. Nuts

8. Cookies

9. Bars

10. Crackers

Top Snack Foods Eaten as a Between-Meal-Snack(% Eatings)

Fruit is the second most popular snack so should benefit from the changing mindset on snacking.

16

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

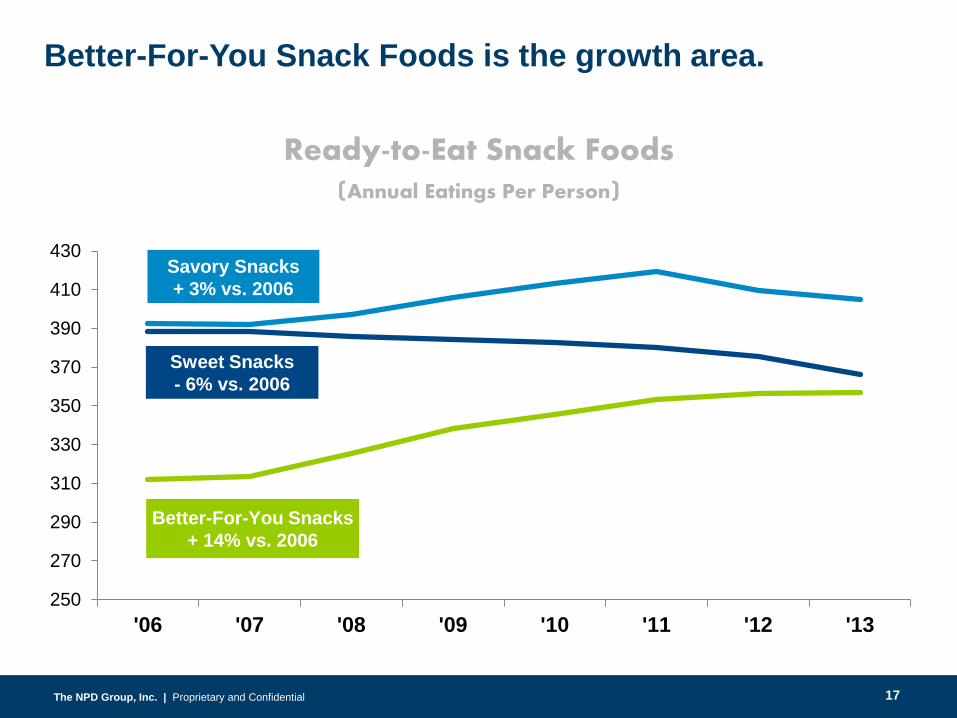

250

270

290

310

330

350

370

390

410

430

'06 '07 '08 '09 '10 '11 '12 '13

Better-For-You Snacks+ 14% vs. 2006

Sweet Snacks- 6% vs. 2006

Savory Snacks+ 3% vs. 2006

Better-For-You Snack Foods is the growth area.

Ready-to-Eat Snack Foods(Annual Eatings Per Person)

17

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

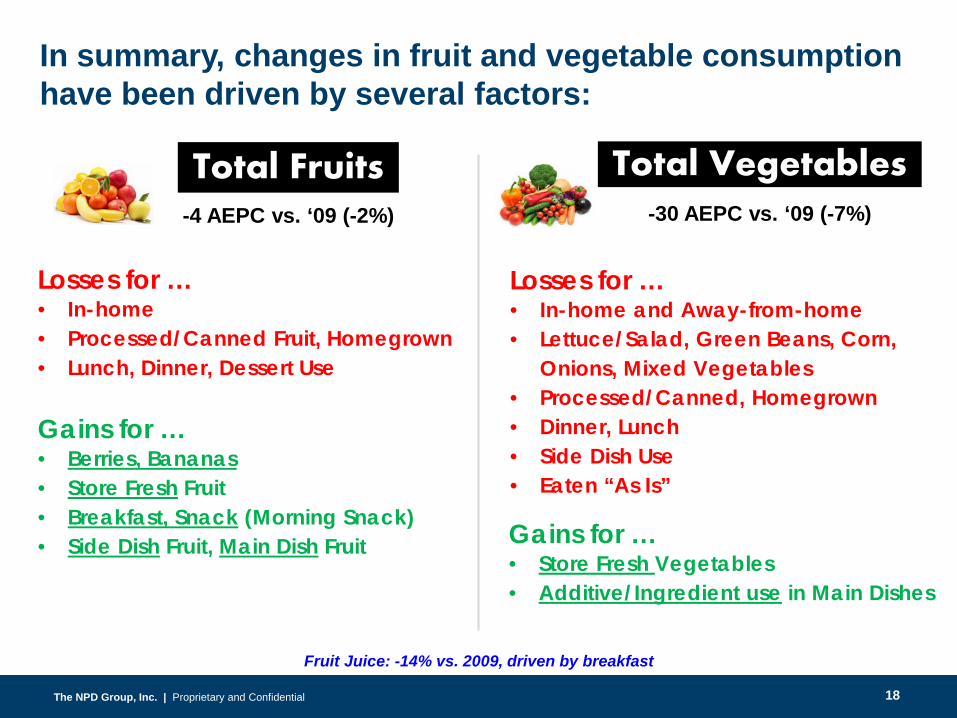

In summary, changes in fruit and vegetable consumption have been driven by several factors:

Losses for …• In-home • Processed/Canned Fruit, Homegrown• Lunch, Dinner, Dessert Use

Fruit Juice: -14% vs. 2009, driven by breakfast

-30 AEPC vs. ‘09 (-7%)-4 AEPC vs. ‘09 (-2%)

Losses for …• In-home and Away-from-home• Lettuce/Salad, Green Beans, Corn,

Onions, Mixed Vegetables• Processed/Canned, Homegrown• Dinner, Lunch• Side Dish Use• Eaten “As Is”

Total Fruits Total Vegetables

Gains for …• Berries, Bananas• Store Fresh Fruit• Breakfast, Snack (Morning Snack)• Side Dish Fruit, Main Dish Fruit Gains for …

• Store Fresh Vegetables• Additive/Ingredient use in Main Dishes

18

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

ConsumerDemographics

19

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

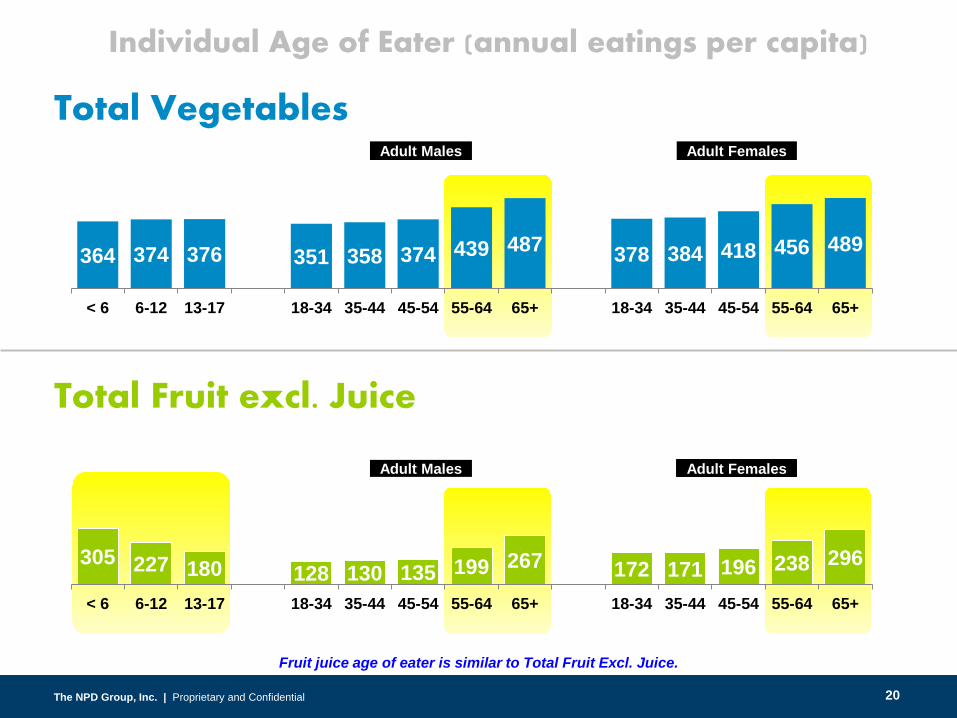

364 374 376 351 358 374 439 487 378 384 418 456 489

< 6 6-12 13-17 18-34 35-44 45-54 55-64 65+ 18-34 35-44 45-54 55-64 65+

Total Fruit excl. Juice

Total Vegetables

305 227 180 128 130 135 199 267 172 171 196 238 296

< 6 6-12 13-17 18-34 35-44 45-54 55-64 65+ 18-34 35-44 45-54 55-64 65+

Adult Males Adult Females

Adult Males Adult Females

Individual Age of Eater (annual eatings per capita)

Fruit juice age of eater is similar to Total Fruit Excl. Juice.

20

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

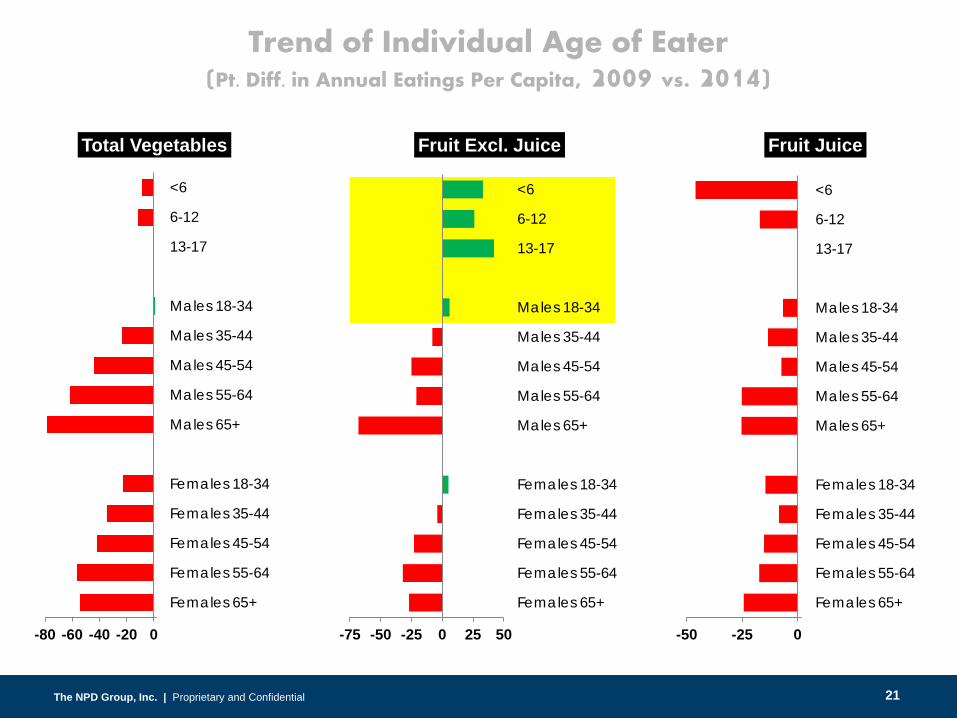

-80 -60 -40 -20 0

Females 65+

Females 55-64

Females 45-54

Females 35-44

Females 18-34

Males 65+

Males 55-64

Males 45-54

Males 35-44

Males 18-34

13-17

6-12

<6

Total Vegetables

-75 -50 -25 0 25 50

Females 65+

Females 55-64

Females 45-54

Females 35-44

Females 18-34

Males 65+

Males 55-64

Males 45-54

Males 35-44

Males 18-34

13-17

6-12

<6

Fruit Excl. Juice

-50 -25 0

Females 65+

Females 55-64

Females 45-54

Females 35-44

Females 18-34

Males 65+

Males 55-64

Males 45-54

Males 35-44

Males 18-34

13-17

6-12

<6

Fruit Juice

Trend of Individual Age of Eater(Pt. Diff. in Annual Eatings Per Capita, 2009 vs. 2014)

21

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

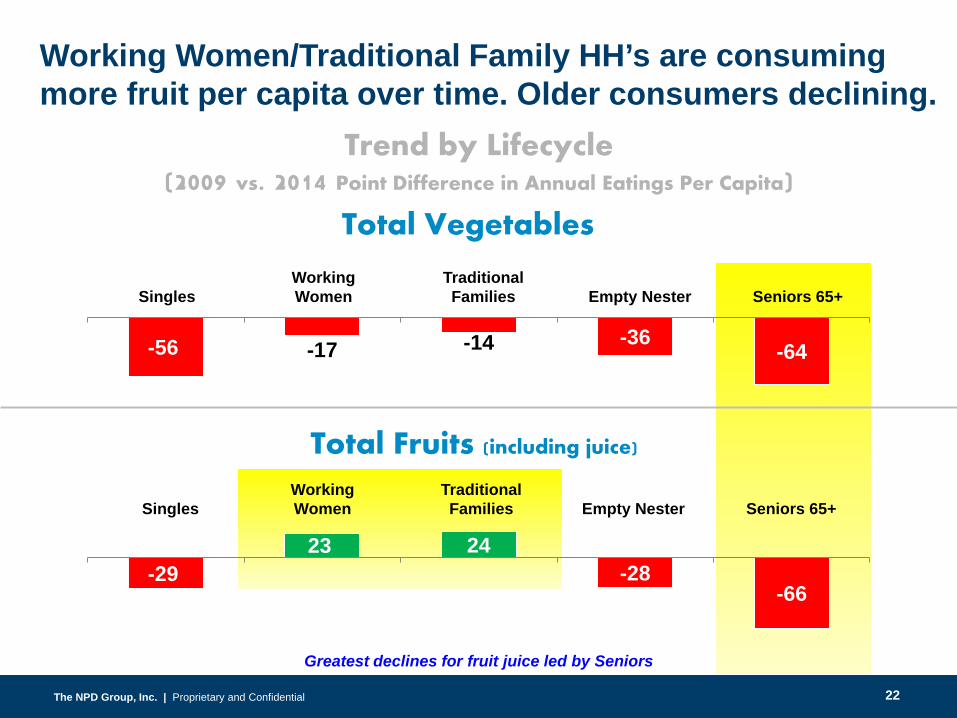

Total Fruits (including juice)

-56 -17 -14 -36 -64

SinglesWorking Women

Traditional Families Empty Nester Seniors 65+

Total Vegetables

SinglesWorking Women

Traditional Families Empty Nester Seniors 65+

-2923 24

-28-66

Trend by Lifecycle(2009 vs. 2014 Point Difference in Annual Eatings Per Capita)

Working Women/Traditional Family HH’s are consuming more fruit per capita over time. Older consumers declining.

Greatest declines for fruit juice led by Seniors

22

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

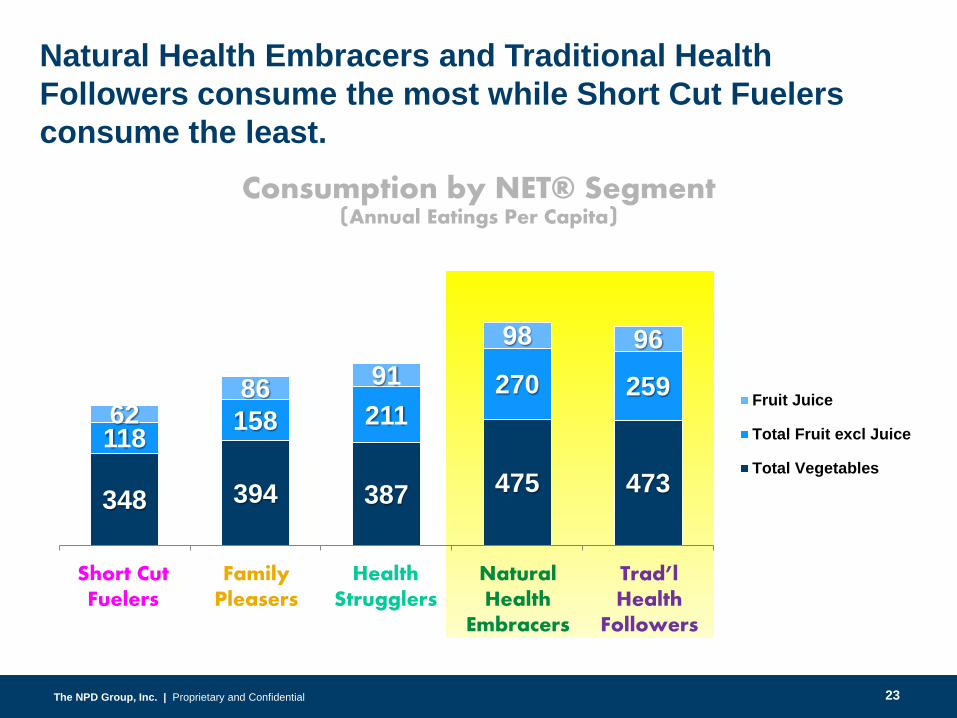

348 394 387 475 473118 158 211

270 25962

86 9198 96

Fruit Juice

Total Fruit excl Juice

Total Vegetables

Consumption by NET® Segment(Annual Eatings Per Capita)

Natural Health Embracers and Traditional Health Followers consume the most while Short Cut Fuelers consume the least.

Health Strugglers

Natural Health

Embracers

Trad’l Health

Followers

Family Pleasers

Short Cut Fuelers

23

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

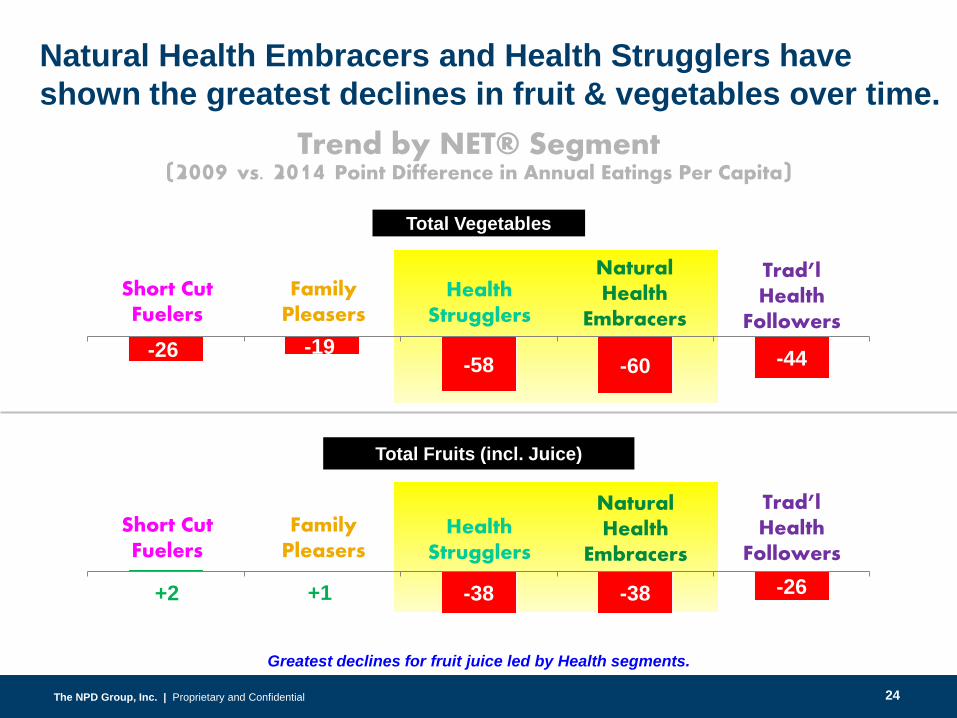

-26 -19-58 -60 -44

Total Vegetables

2 1 -38 -38 -26

Trend by NET® Segment(2009 vs. 2014 Point Difference in Annual Eatings Per Capita)

Natural Health Embracers and Health Strugglers have shown the greatest declines in fruit & vegetables over time.

Greatest declines for fruit juice led by Health segments.

Health Strugglers

Natural Health

Embracers

Trad’l Health

Followers

Family Pleasers

Short Cut Fuelers

Total Fruits (incl. Juice)

Health Strugglers

Natural Health

Embracers

Trad’l Health

FollowersFamily

PleasersShort Cut Fuelers

+2 +1

24

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

The Future of Fruits & Vegetables

25

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

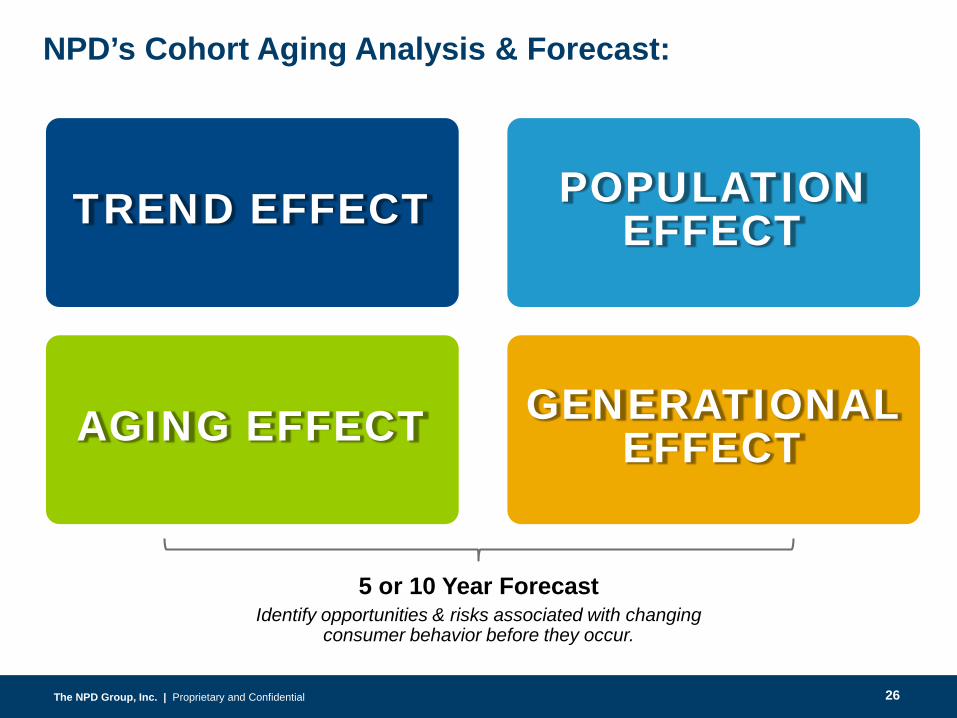

TREND EFFECT

NPD’s Cohort Aging Analysis & Forecast:

POPULATION EFFECT

AGING EFFECT GENERATIONAL EFFECT

5 or 10 Year ForecastIdentify opportunities & risks associated with changing

consumer behavior before they occur.

26

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

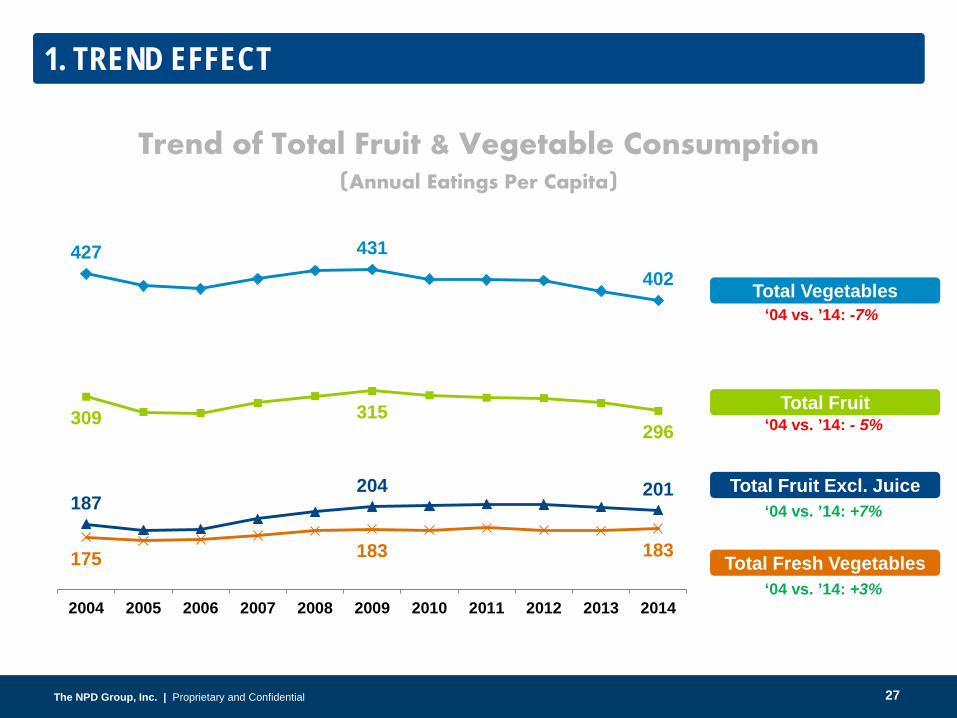

1. TREND EFFECT

427 431402

309 315296

187204 201

175 183 183

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Trend of Total Fruit & Vegetable Consumption(Annual Eatings Per Capita)

‘04 vs. ’14: -7%

‘04 vs. ’14: - 5%

‘04 vs. ’14: +7%

‘04 vs. ’14: +3%

Total Vegetables

Total Fruit

Total Fruit Excl. Juice

Total Fresh Vegetables

27

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

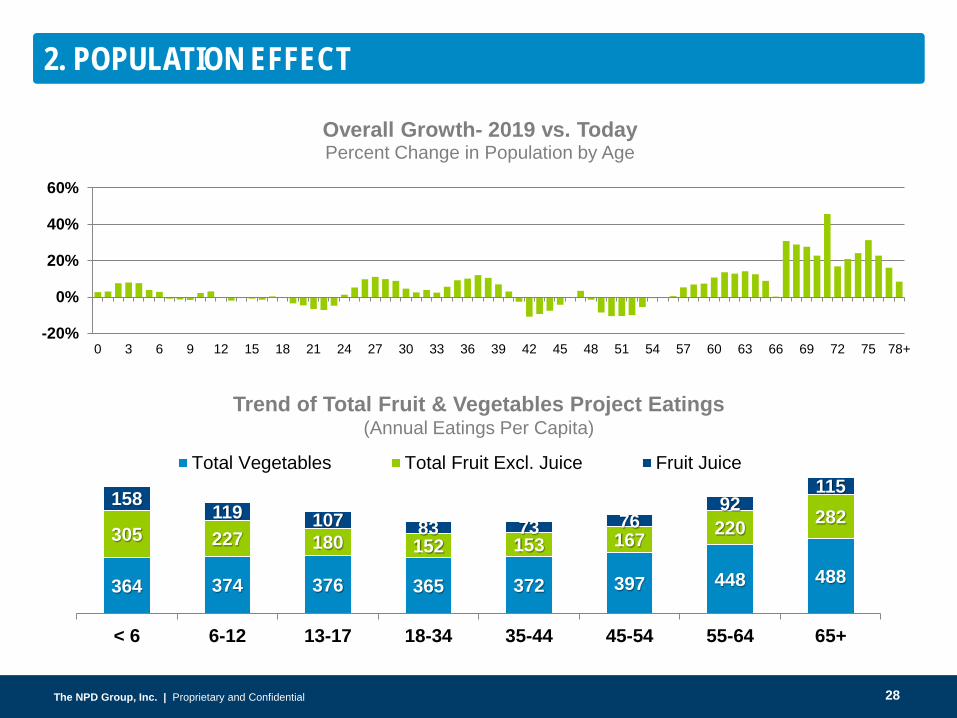

2. POPULATION EFFECT

364 374 376 365 372 397 448 488

305 227 180 152 153 167 220 282158 119 107 83 73 76

92115

< 6 6-12 13-17 18-34 35-44 45-54 55-64 65+

Total Vegetables Total Fruit Excl. Juice Fruit Juice

-20%

0%

20%

40%

60%

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78+

Overall Growth- 2019 vs. TodayPercent Change in Population by Age

Trend of Total Fruit & Vegetables Project Eatings(Annual Eatings Per Capita)

28

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

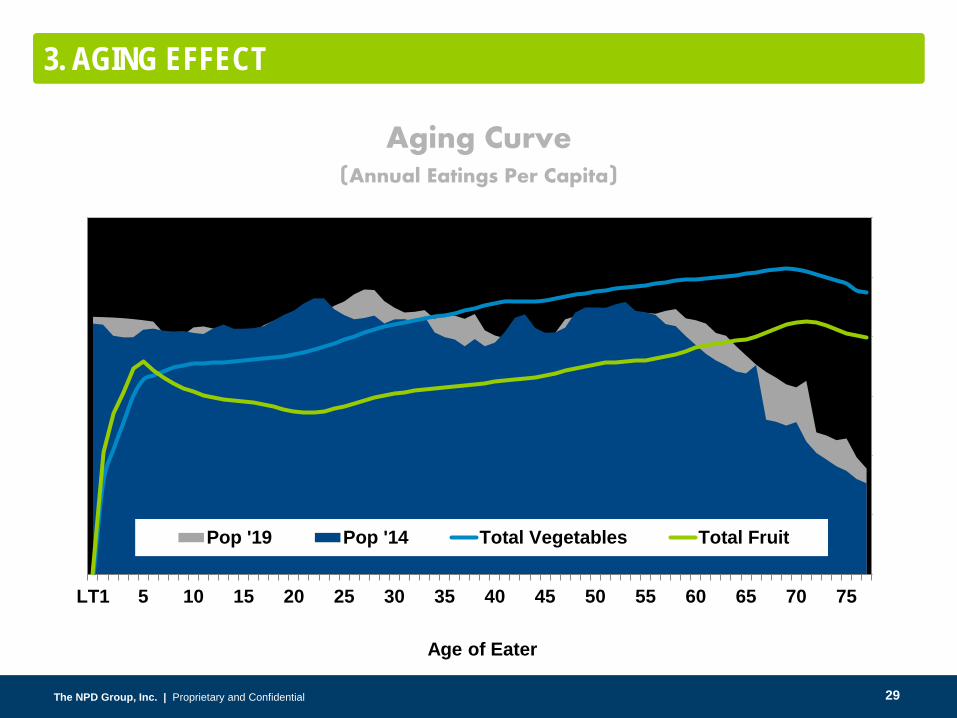

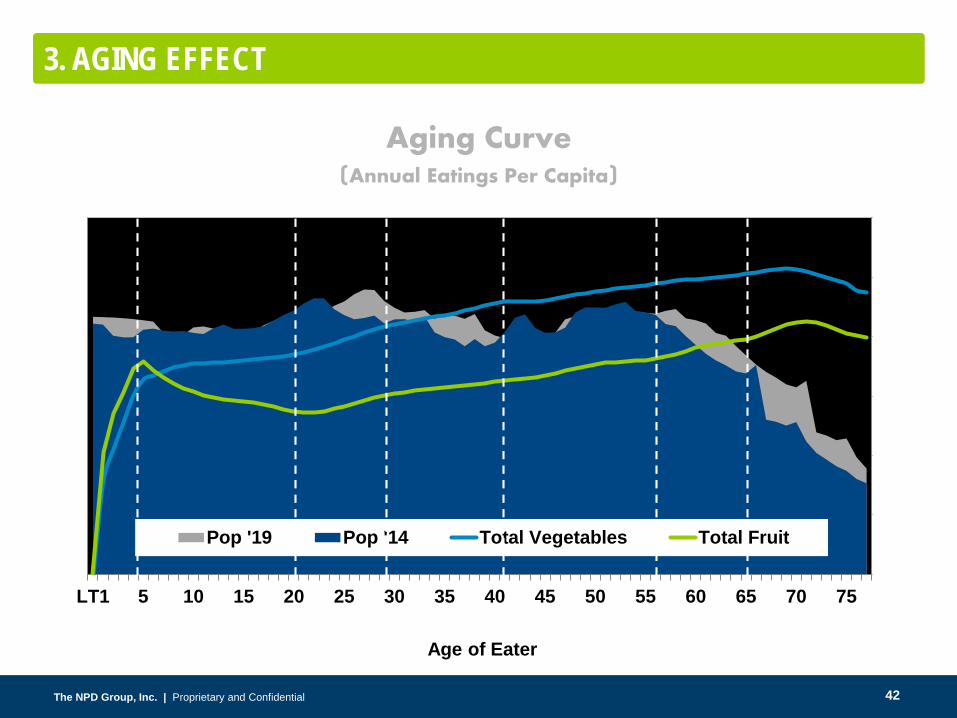

3. AGING EFFECT

Aging Curve(Annual Eatings Per Capita)

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

LT1 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 -

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Age of Eater

Pop '19 Pop '14 Total Vegetables Total Fruit

29

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

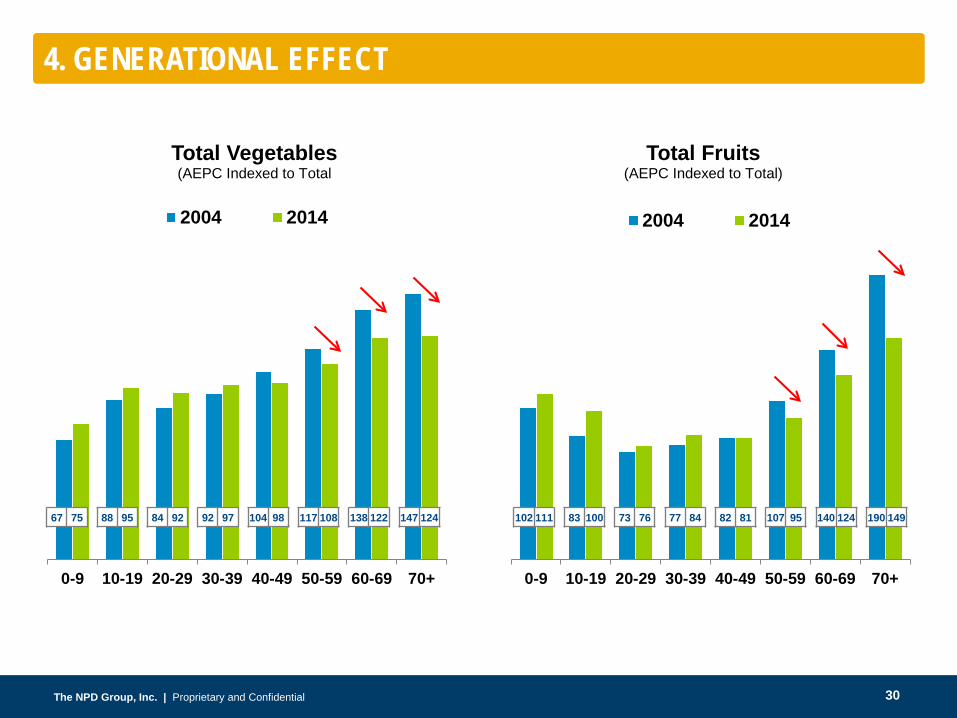

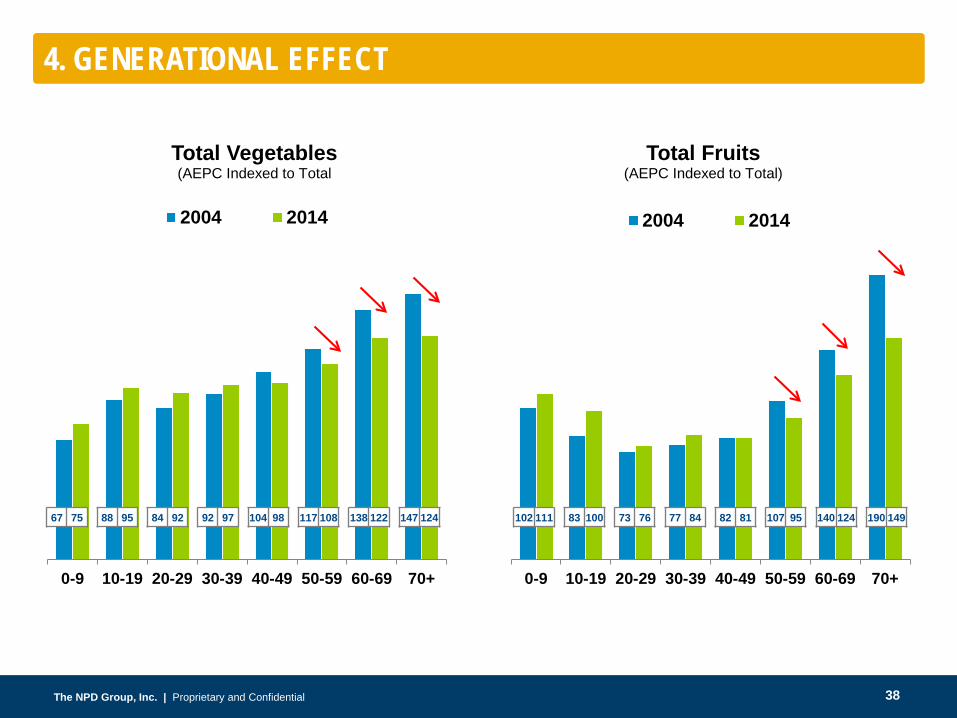

0-9 10-19 20-29 30-39 40-49 50-59 60-69 70+

Total Fruits(AEPC Indexed to Total)

2004 2014

102 111 83 100 73 76 77 84 82 81 107 95 140 124 190 149

0-9 10-19 20-29 30-39 40-49 50-59 60-69 70+

Total Vegetables(AEPC Indexed to Total

2004 2014

67 75 88 95 84 92 92 97 104 98 117 108 138 122 147 124

4. GENERATIONAL EFFECT

30

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

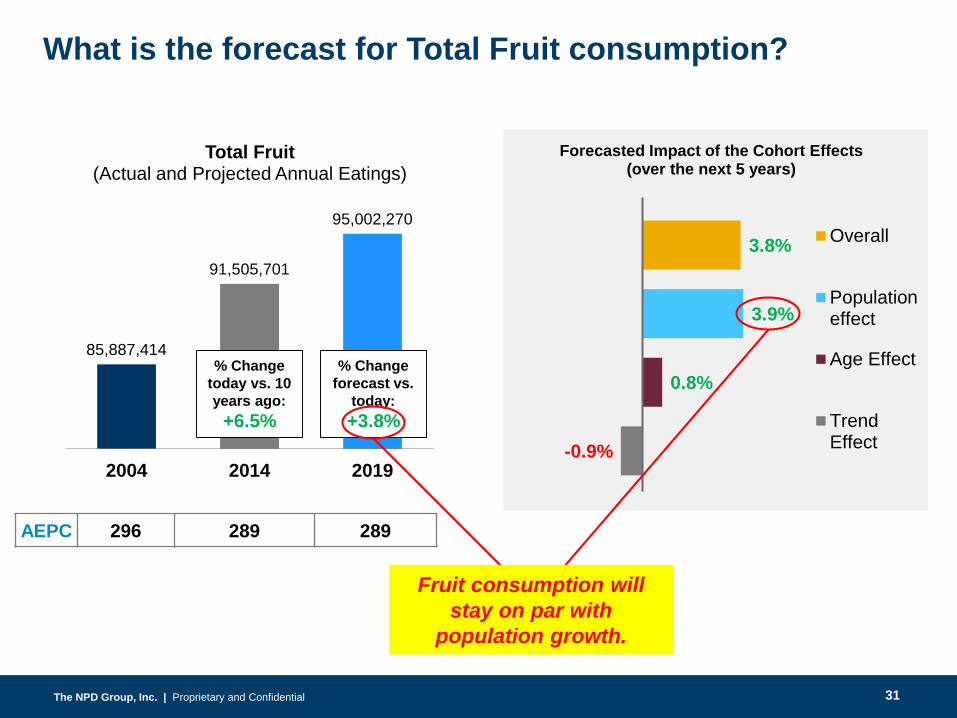

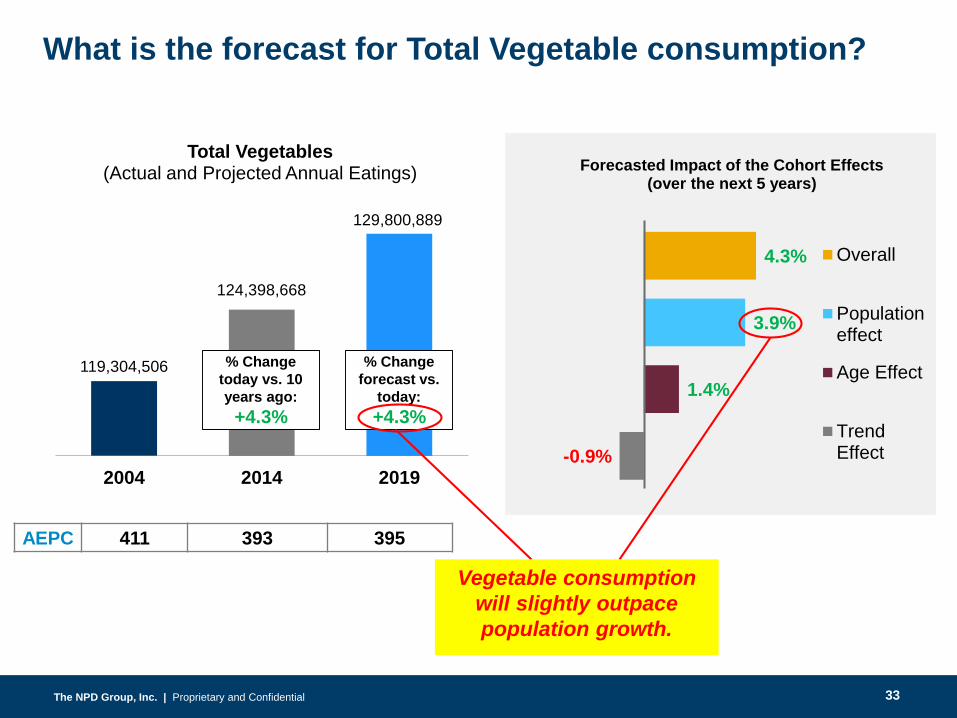

3.8%

3.9%

0.8%

-0.9%

Forecasted Impact of the Cohort Effects (over the next 5 years)

Overall

Populationeffect

Age Effect

TrendEffect

What is the forecast for Total Fruit consumption?

AEPC 296 289 289

85,887,414

91,505,701

95,002,270

2004 2014 2019

Total Fruit(Actual and Projected Annual Eatings)

% Change today vs. 10 years ago: +6.5%

% Change forecast vs.

today:+3.8%

Fruit consumption will stay on par with

population growth.

31

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

85,887,414

91,505,701

95,002,270

2004 2014 2019

Total Fruit(Actual and Projected Annual Eatings)

AEPC 296 289 289

% Change today vs. 10 years ago: +6.5%

% Change forecast vs.

today:+3.8%

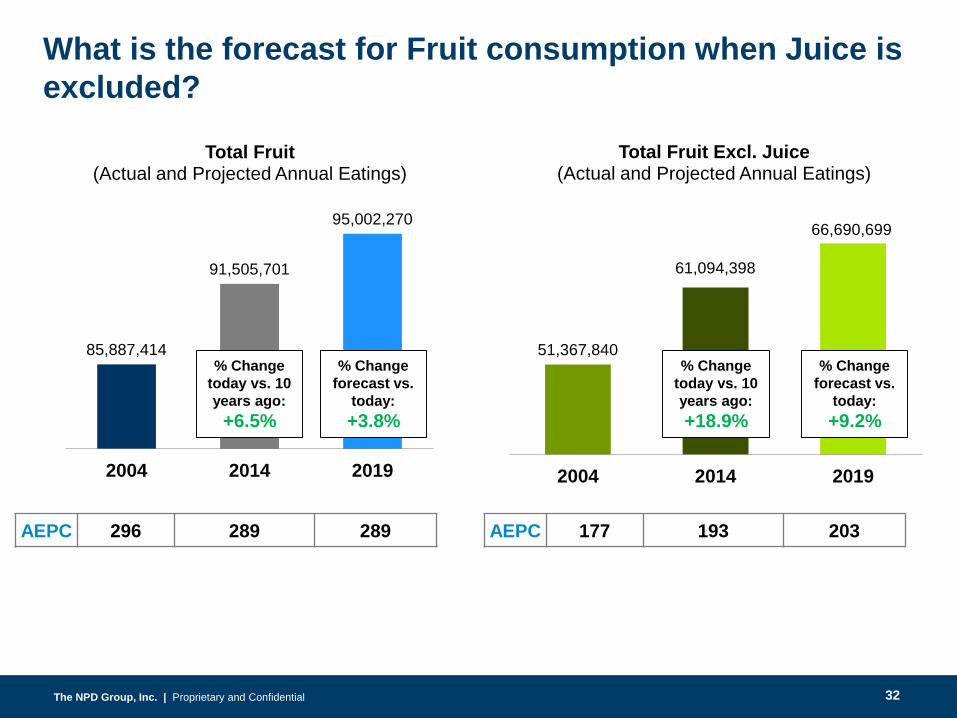

What is the forecast for Fruit consumption when Juice is excluded?

51,367,840

61,094,398

66,690,699

2004 2014 2019

Total Fruit Excl. Juice(Actual and Projected Annual Eatings)

% Change today vs. 10 years ago: +18.9%

% Change forecast vs.

today:+9.2%

AEPC 177 193 203

32

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

4.3%

3.9%

1.4%

-0.9%

Forecasted Impact of the Cohort Effects (over the next 5 years)

Overall

Populationeffect

Age Effect

TrendEffect

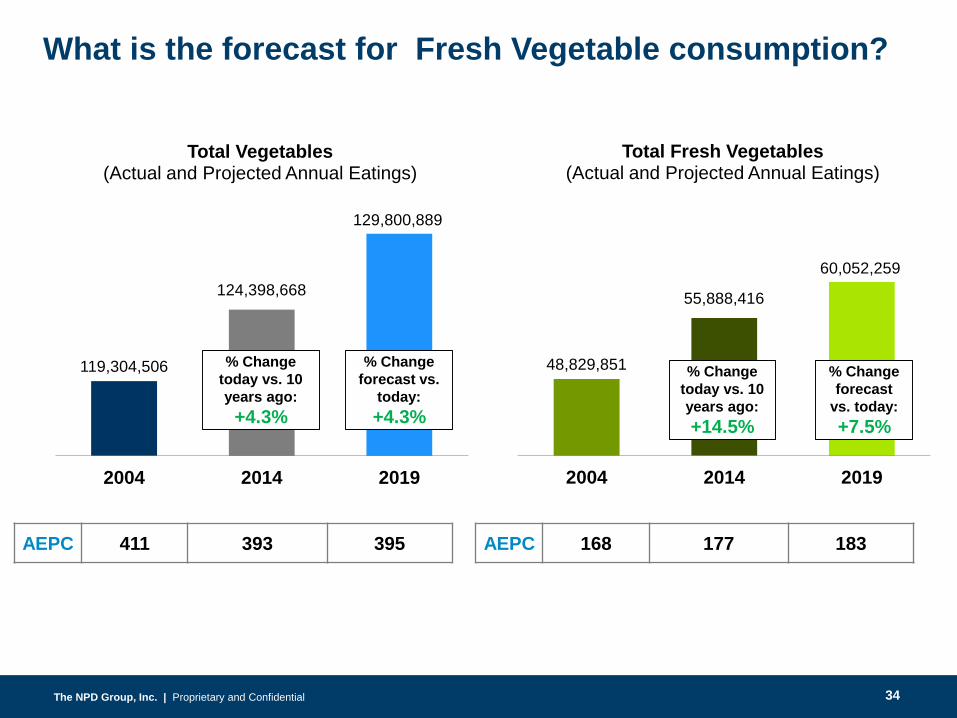

What is the forecast for Total Vegetable consumption?

AEPC 411 393 395

119,304,506

124,398,668

129,800,889

2004 2014 2019

Total Vegetables(Actual and Projected Annual Eatings)

% Change today vs. 10 years ago: +4.3%

% Change forecast vs.

today:+4.3%

Vegetable consumption will slightly outpace population growth.

33

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

AEPC 411 393 395

119,304,506

124,398,668

129,800,889

2004 2014 2019

Total Vegetables(Actual and Projected Annual Eatings)

% Change today vs. 10 years ago: +4.3%

% Change forecast vs.

today:+4.3%

What is the forecast for Fresh Vegetable consumption?

48,829,851

55,888,416

60,052,259

2004 2014 2019

Total Fresh Vegetables(Actual and Projected Annual Eatings)

% Change today vs. 10 years ago: +14.5%

% Change forecast

vs. today:+7.5%

AEPC 168 177 183

34

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

What to Focus on Next

35

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

What to focus on next:

1. Reposition Fruits & Vegetables

2. Extend Partnerships

3. Remember Pricing Strengths

4. Advance Away-From-Home Opportunities

36

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Reposition Fruits and Vegetables

Your core essence regarding health

has lost meaning in the world of health.

1.

37

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

0-9 10-19 20-29 30-39 40-49 50-59 60-69 70+

Total Fruits(AEPC Indexed to Total)

2004 2014

102 111 83 100 73 76 77 84 82 81 107 95 140 124 190 149

0-9 10-19 20-29 30-39 40-49 50-59 60-69 70+

Total Vegetables(AEPC Indexed to Total

2004 2014

67 75 88 95 84 92 92 97 104 98 117 108 138 122 147 124

4. GENERATIONAL EFFECT

38

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

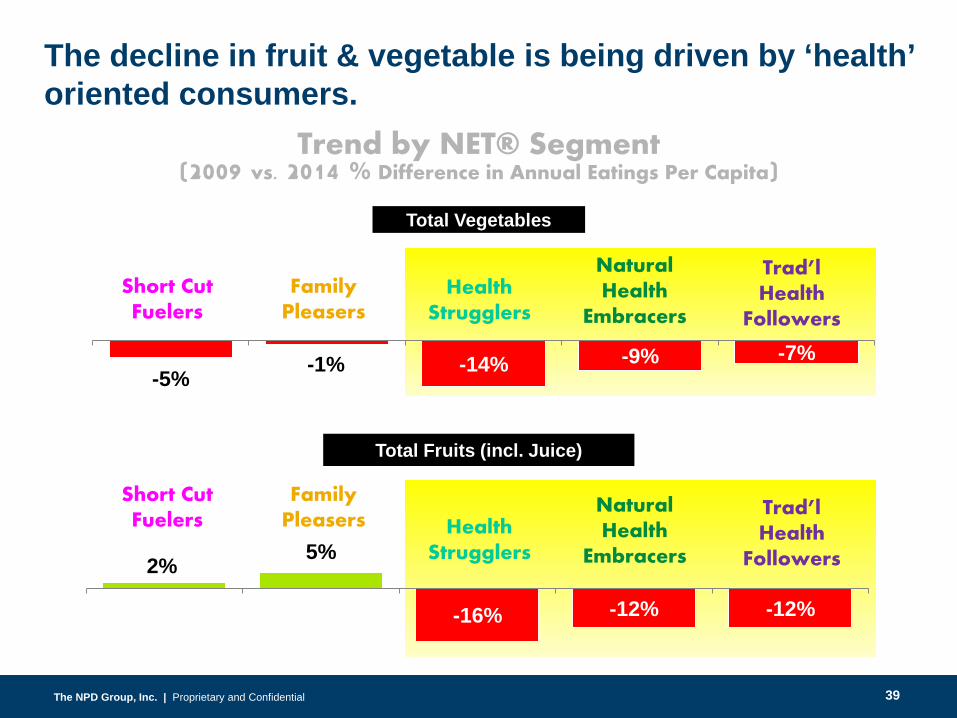

The decline in fruit & vegetable is being driven by ‘health’ oriented consumers.

2% 5%

-16% -12% -12%

-5% -1% -14% -9% -7%

Trend by NET® Segment(2009 vs. 2014 % Difference in Annual Eatings Per Capita)

Health Strugglers

Natural Health

Embracers

Trad’l Health

Followers

Family Pleasers

Short Cut Fuelers

Health Strugglers

Natural Health

Embracers

Trad’l Health

Followers

Family Pleasers

Short Cut Fuelers

Total Vegetables

Total Fruits (incl. Juice)

39

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

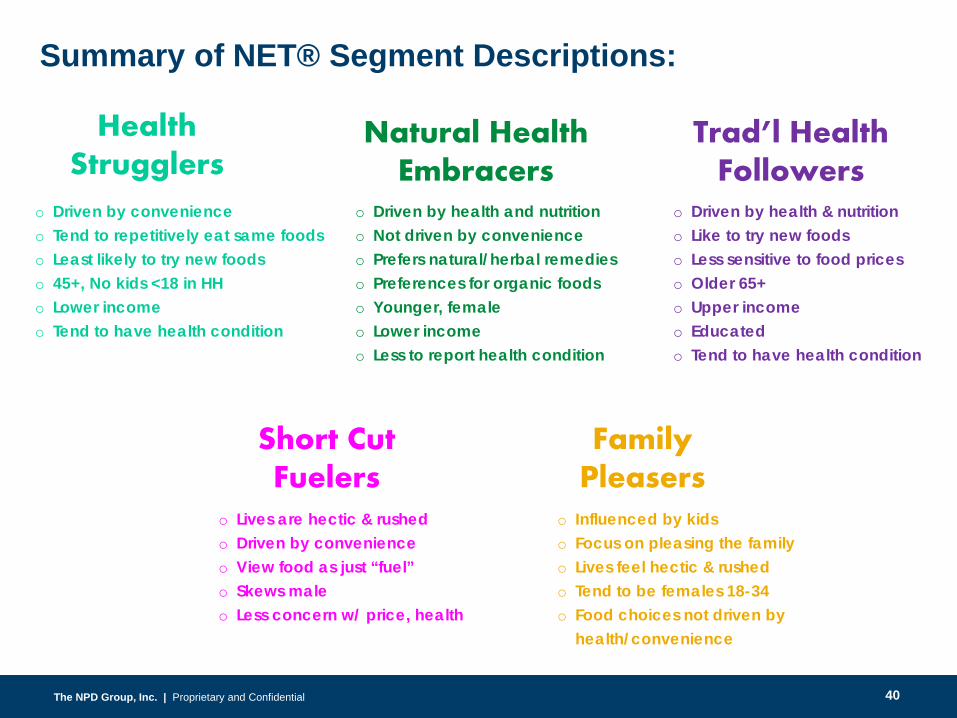

Summary of NET® Segment Descriptions:

o Driven by convenienceo Tend to repetitively eat same foodso Least likely to try new foodso 45+, No kids <18 in HHo Lower incomeo Tend to have health condition

Health Strugglers

o Driven by health and nutritiono Not driven by convenienceo Prefers natural/herbal remedieso Preferences for organic foodso Younger, femaleo Lower incomeo Less to report health condition

Natural Health Embracers

o Driven by health & nutritiono Like to try new foodso Less sensitive to food priceso Older 65+o Upper incomeo Educated o Tend to have health condition

Trad’l Health Followers

Short Cut Fuelers

o Lives are hectic & rushedo Driven by convenienceo View food as just “fuel”o Skews maleo Less concern w/ price, health

Family Pleasers

o Influenced by kidso Focus on pleasing the familyo Lives feel hectic & rushedo Tend to be females 18-34o Food choices not driven by

health/convenience

40

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

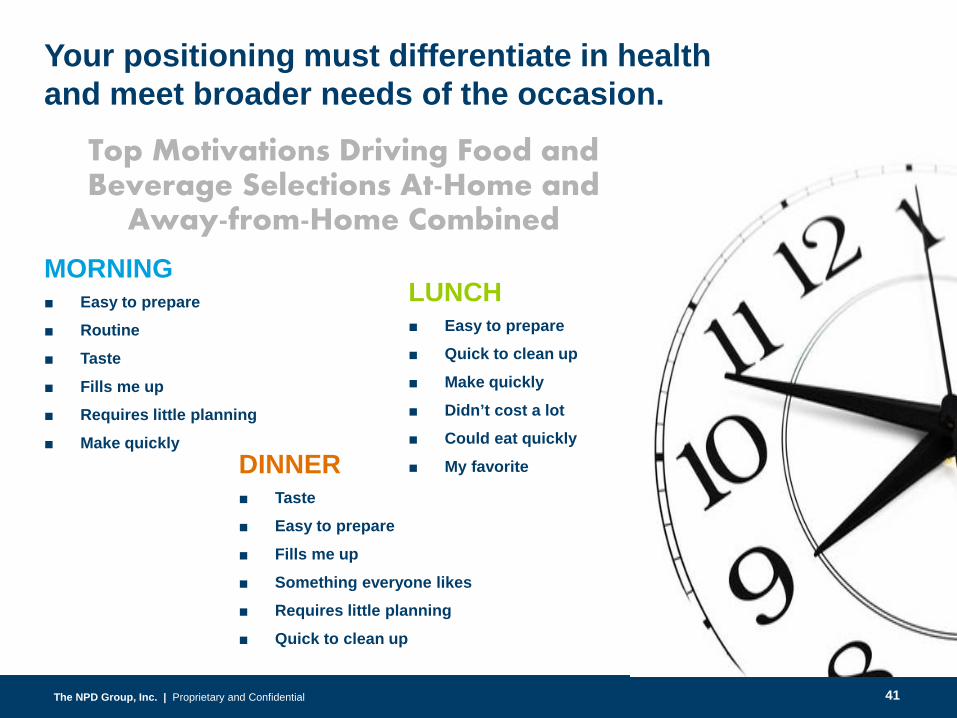

LUNCH■ Easy to prepare ■ Quick to clean up■ Make quickly■ Didn’t cost a lot■ Could eat quickly■ My favoriteDINNER

■ Taste■ Easy to prepare■ Fills me up■ Something everyone likes■ Requires little planning■ Quick to clean up

MORNING■ Easy to prepare■ Routine■ Taste■ Fills me up■ Requires little planning■ Make quickly

Top Motivations Driving Food and Beverage Selections At-Home and

Away-from-Home Combined

Your positioning must differentiate in health and meet broader needs of the occasion.

41

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

3. AGING EFFECT

Aging Curve(Annual Eatings Per Capita)

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

LT1 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 -

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Age of Eater

Pop '19 Pop '14 Total Vegetables Total Fruit

42

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

DRIVER BARRIERTRUTH

I wish…I hate...

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Extend Partnerships

Continue to work with core partners who

can use your help… but also look to new

partnerships.

2.

44

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

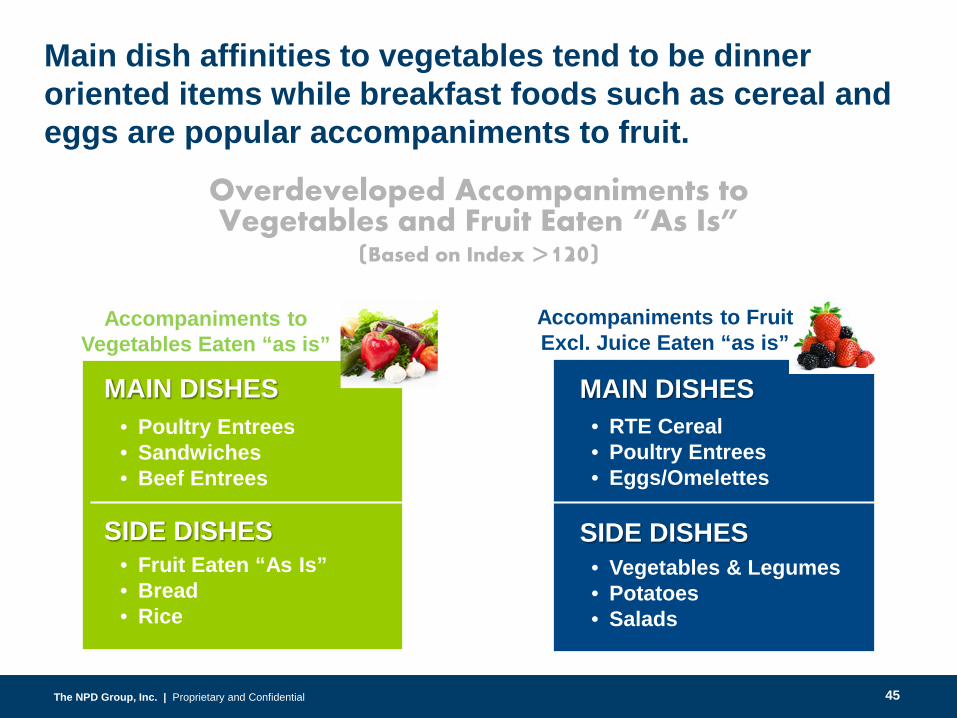

• Poultry Entrees• Sandwiches• Beef Entrees

• Fruit Eaten “As Is”• Bread• Rice

• RTE Cereal• Poultry Entrees• Eggs/Omelettes

• Vegetables & Legumes• Potatoes• Salads

MAIN DISHES

SIDE DISHES

MAIN DISHES

SIDE DISHES

Accompaniments to Vegetables Eaten “as is”

Accompaniments to Fruit Excl. Juice Eaten “as is”

Overdeveloped Accompaniments to Vegetables and Fruit Eaten “As Is”

(Based on Index >120)

Main dish affinities to vegetables tend to be dinner oriented items while breakfast foods such as cereal and eggs are popular accompaniments to fruit.

45

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

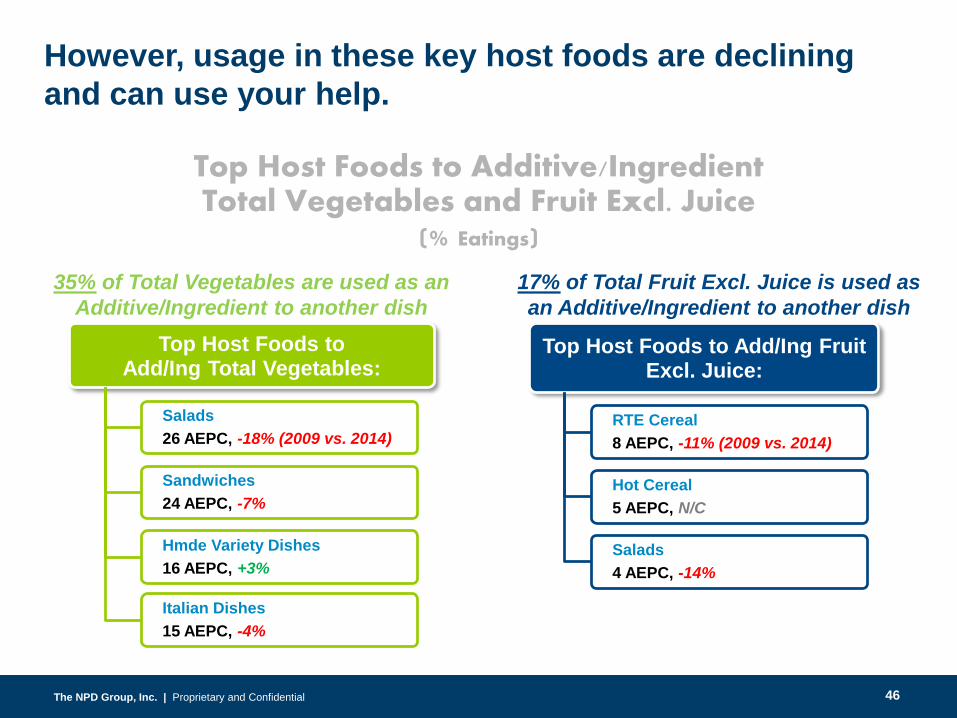

Top Host Foods to Add/Ing Total Vegetables:

Salads26 AEPC, -18% (2009 vs. 2014)

Sandwiches24 AEPC, -7%

Hmde Variety Dishes16 AEPC, +3%

Italian Dishes15 AEPC, -4%

Top Host Foods to Add/Ing Fruit Excl. Juice:

RTE Cereal8 AEPC, -11% (2009 vs. 2014)

Hot Cereal5 AEPC, N/C

Salads4 AEPC, -14%

Top Host Foods to Additive/Ingredient Total Vegetables and Fruit Excl. Juice

(% Eatings)35% of Total Vegetables are used as an

Additive/Ingredient to another dish17% of Total Fruit Excl. Juice is used as an Additive/Ingredient to another dish

However, usage in these key host foods are declining and can use your help.

46

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

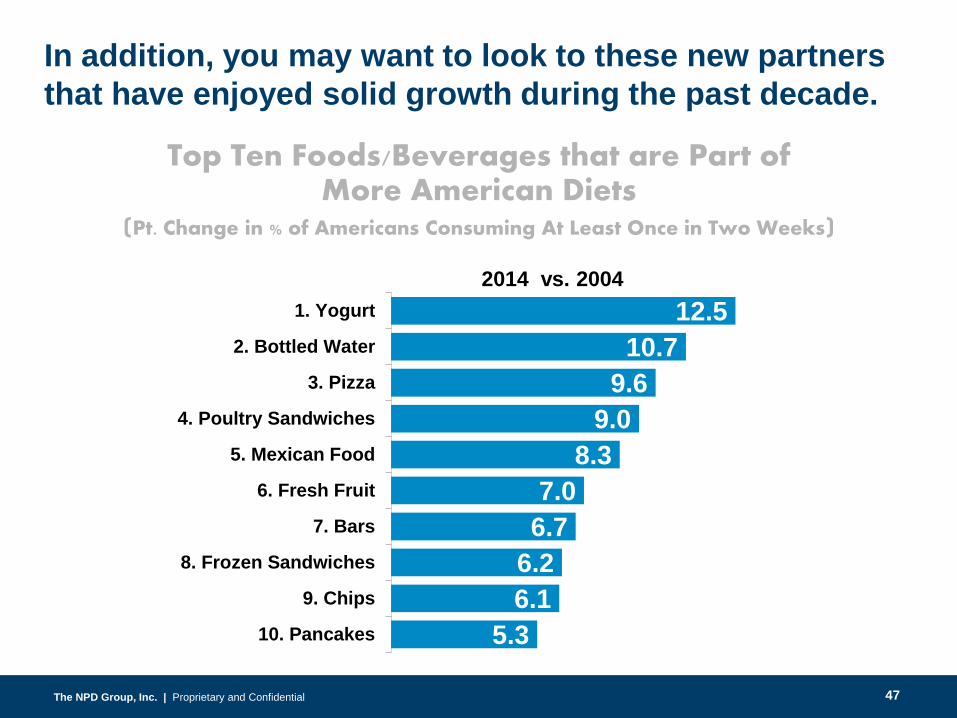

12.510.7

9.69.0

8.37.0

6.76.26.1

5.3

1. Yogurt

2. Bottled Water

3. Pizza

4. Poultry Sandwiches

5. Mexican Food

6. Fresh Fruit

7. Bars

8. Frozen Sandwiches

9. Chips

10. Pancakes

Top Ten Foods/Beverages that are Part ofMore American Diets

(Pt. Change in % of Americans Consuming At Least Once in Two Weeks)

And while our diet changes slowly, there are shifts happening.In addition, you may want to look to these new partners that have enjoyed solid growth during the past decade.

2014 vs. 2004

47

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Remember Your Pricing Strengths

Think broader about your pricing

decisions.

3.

48

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

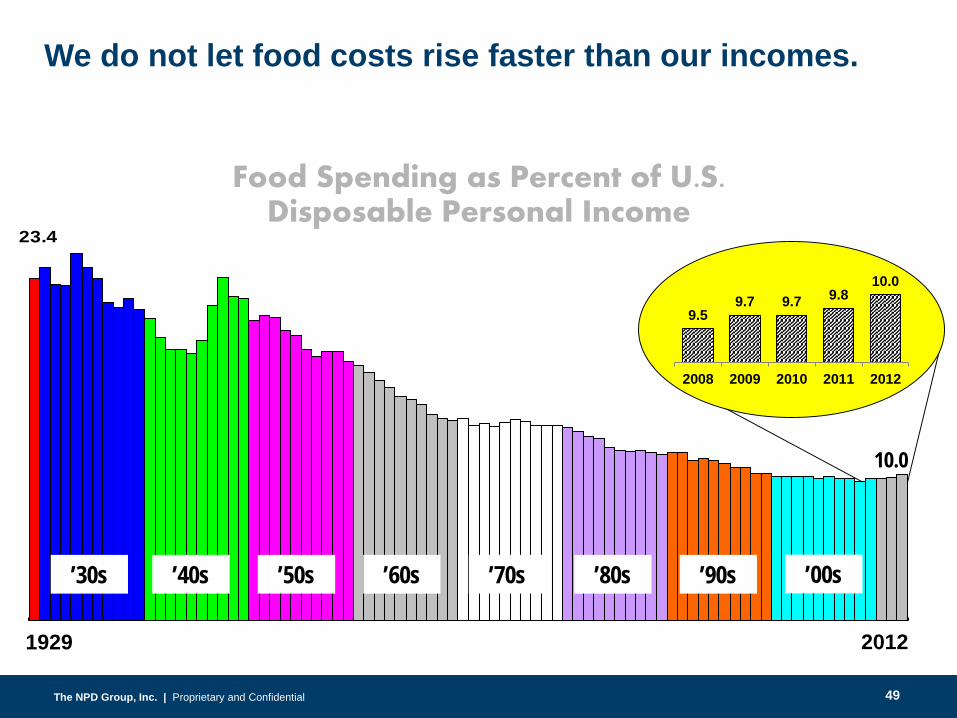

23.4

’30s ’40s ’50s ’60s ’70s ’80s ’90s

1929 2012

Food Spending as Percent of U.S. Disposable Personal Income

’00s

10.0

We do not let food costs rise faster than our incomes.

9.59.7 9.7 9.8

10.0

2008 2009 2010 2011 2012

49

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

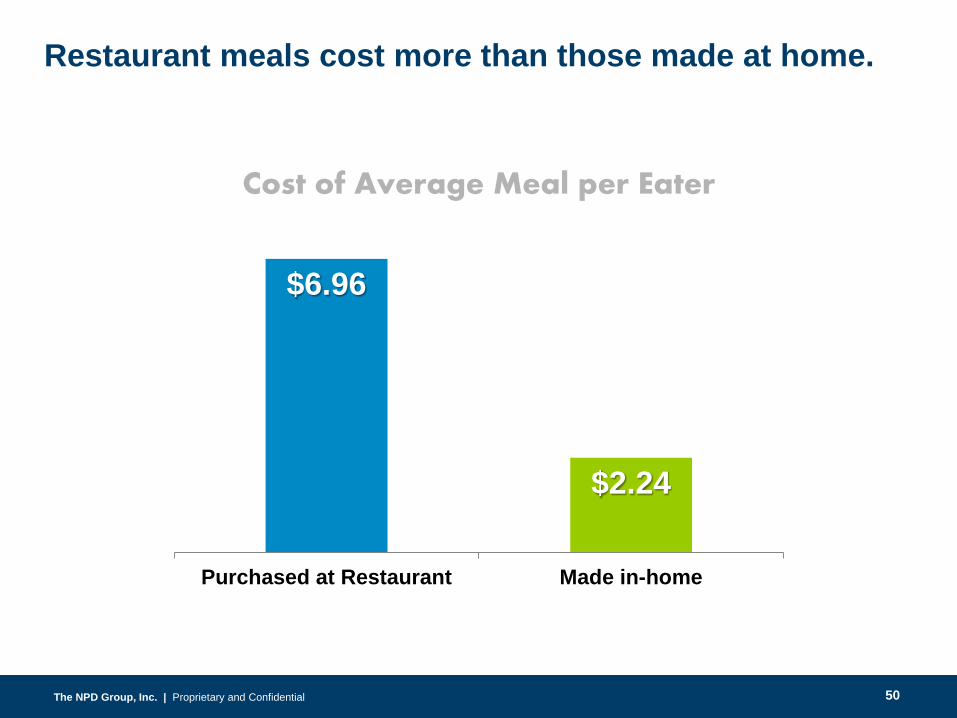

Cost of Average Meal per Eater

Restaurant meals cost more than those made at home.

$6.96

$2.24

Purchased at Restaurant Made in-home

50

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

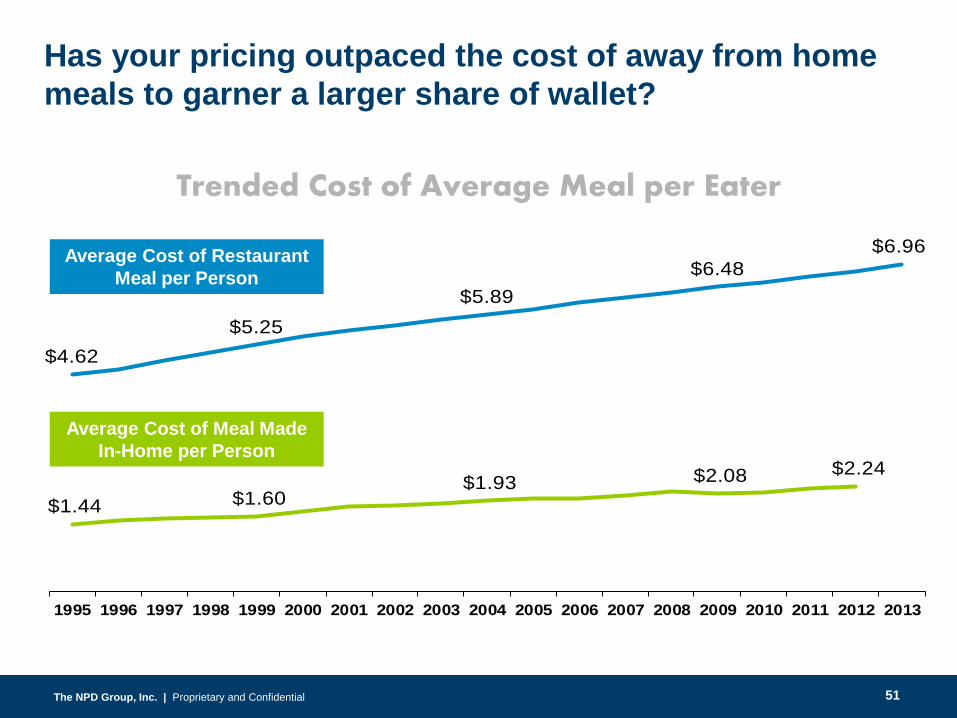

$4.62$5.25

$5.89$6.48

$6.96

$1.44 $1.60 $1.93 $2.08 $2.24

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Average Cost of Restaurant Meal per Person

Average Cost of Meal Made In-Home per Person

Trended Cost of Average Meal per Eater

Has your pricing outpaced the cost of away from home meals to garner a larger share of wallet?

51

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Advance Away-From-Home

Opportunities

Focus primarily on home but efforts

to increase presence at Foodservice are

still needed.

4.

52

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

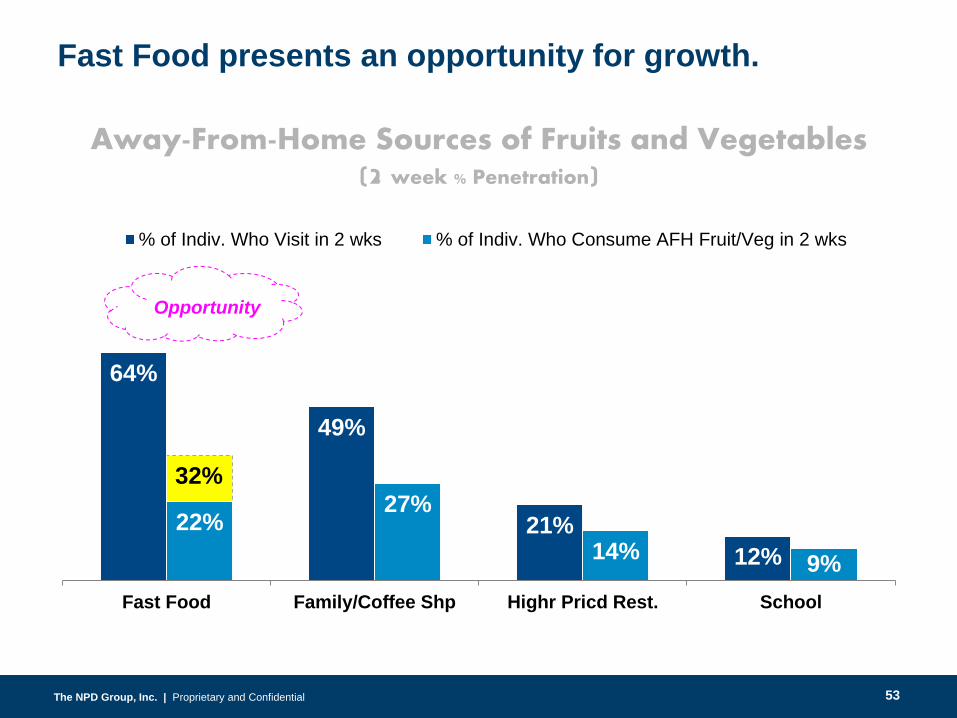

32%

64%

49%

21%12%

22%27%

14% 9%Fast Food Family/Coffee Shp Highr Pricd Rest. School

% of Indiv. Who Visit in 2 wks % of Indiv. Who Consume AFH Fruit/Veg in 2 wks

Away-From-Home Sources of Fruits and Vegetables(2 week % Penetration)

Fast Food presents an opportunity for growth.

Opportunity

53

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

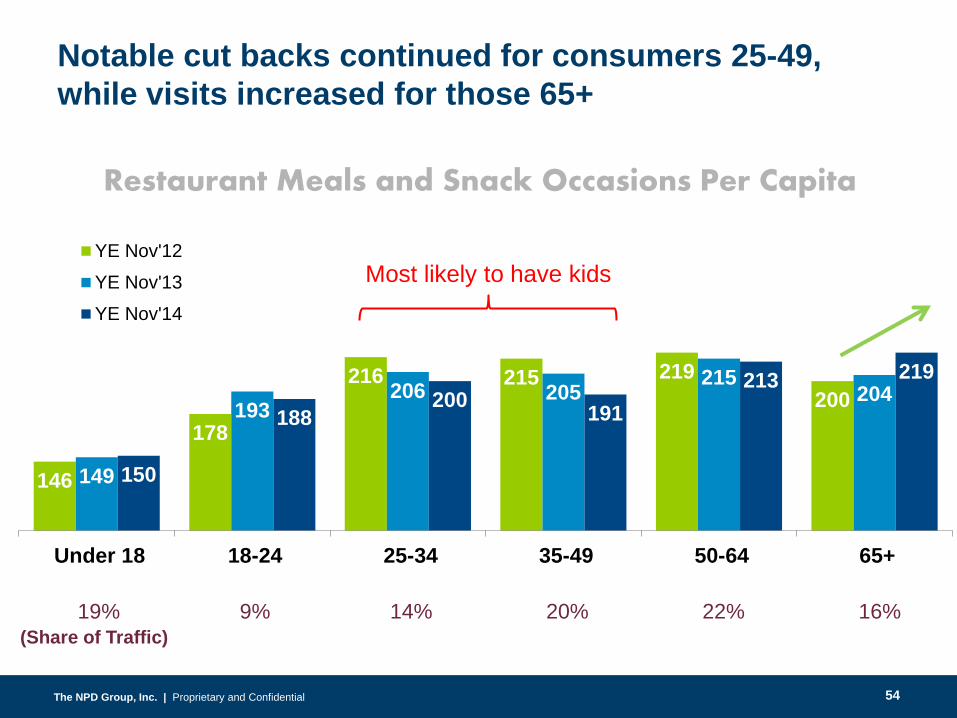

(Share of Traffic)19% 9% 14% 20% 22% 16%

Most likely to have kids

Notable cut backs continued for consumers 25-49, while visits increased for those 65+

146

178

216 215 219200

149

193206 205 215

204

150

188200 191

213 219

Under 18 18-24 25-34 35-49 50-64 65+

YE Nov'12YE Nov'13YE Nov'14

Restaurant Meals and Snack Occasions Per Capita

54

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

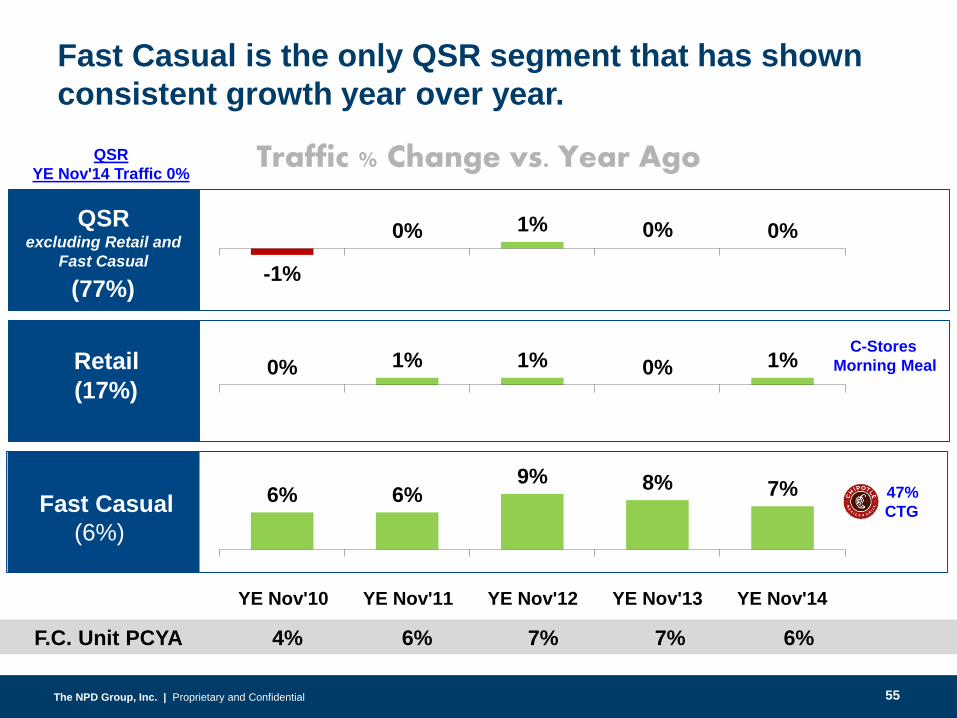

6% 6%9% 8% 7%

QSRYE Nov'14 Traffic 0%

YE Nov'10 YE Nov'11 YE Nov'12 YE Nov'13 YE Nov'14

0% 1% 1% 0% 1%

-1%

0% 1% 0% 0%

F.C. Unit PCYA 4% 6% 7% 7% 6%

Fast Casual is the only QSR segment that has shown consistent growth year over year.

QSR excluding Retail and

Fast Casual

(77%)

Retail(17%)

C-StoresMorning Meal

Fast Casual(6%)

47%CTG

Traffic % Change vs. Year Ago

55

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

In summary, there has never been a better time to be in the fruit and vegetable business:

The demographics are favorable

There is a consumer need

Though fighting inertia…advanced innovation and marketing can pay big dividends

56

The NPD Group, Inc. | Proprietary and ConfidentialThe NPD Group, Inc. | Proprietary and Confidential

Sometimes it’s hard to see!