nrf17008 data centre unboxed_v2 full.indd

TRANSCRIPT

Financial institutionsEnergyInfrastructure, mining and commoditiesTransportTechnology and innovationLife sciences and healthcare

Data centres unboxed A guide to legal issues, trends and risks

Attorney advertising

Data centres unboxed A guide to legal issues, trends and risks

A Norton Rose Fulbright guide 2013

Contents

1 Preface 05

2 Introduction 07

3 Planning and locating a data centre 09

4 Building and opening a data centre 17

5 Environment and corporate governance 25

6 Outsourcing and offshoring 33

7 Shared services 41

8 Data privacy 49

9 Hot topics and regional trends 55

10 Concepts and glossary 63

11 Contacts 67

6 Norton Rose Fulbright – 2013

Data centres unboxed

1Preface

Norton Rose Fulbright – 2013 07

Preface

Preface

Mike RebeiroGlobal head of technology and innovationNorton Rose Fulbright LLP

We are pleased to present the second edition of Data centres unboxed.

The world is reliant on data and the internet in our technological era. With increases in corporate data storage requirements and generally in data-heavy applications and solutions, the facilities and processes used to store such data are being more intensely scrutinised in areas such as security, availability and adherence to standards; and as shown in this guide, there is a degree of commonality of issues across international borders.

With that in mind we have prepared this guide with the aim of explaining some of the key considerations affecting data centres. The guide includes chapters on building a data centre; selecting an appropriate location; environmental and corporate governance issues; outsourcing, offshoring and shared services; data privacy; and a look at some of the hot topics and regional trends in this space around the world.

This publication is likely to be of particular interest to data centre operators, IT service providers, banks and other institutions funding data centre projects, and any other person with a vested interest in storing and handling large amounts of data.

Technology and innovation is a key area of strength for Norton Rose Fulbright. Knowing how our clients’ businesses work and understanding what drives their industries is fundamental to us. This is particularly true in the fast paced areas of technology and information management. Our lawyers share industry knowledge and sector experience across borders, enabling us to support our clients anywhere in the world. Our technology and innovation team comprises lawyers across many different practice areas, including sourcing and technology, construction, real estate, corporate finance, banking and dispute resolution. This reflects the complex nature of transactions and issues in this sector.

We trust that you will find our guide useful and insightful. If we can be of any further assistance please do contact us.

08 Norton Rose Fulbright – 2013

Data centres unboxed

2Introduction

Norton Rose Fulbright – 2013 09

Introduction

Introduction

There has been an explosion in the consumption and processing of data in recent years; as increasing volumes of data need to be stored, the overwhelming reliance on data centres is proportionately becoming greater and greater. As data centres become more prevalent and the need for them continues to increase, it can only be expected that the legal regime surrounding their construction and use (in particular environmental and data security laws) will be adapted and developed.

In practical terms, the size of a data centre can be greater than three large supermarkets. The costs of building a large data centre are said to be up to US $500 million and in some cases up to US $1 billion. With that in mind, anyone contemplating constructing a data centre will inevitably have many issues to consider, and will have to make sure that the cost of the project and the associated risks are appropriate, compared with the intended rewards.

There are obvious practical questions, such as how big should the data centre be, how much energy will it require and who will build it. In this guide, we have focused on some of the legal and commercial considerations that will apply once these decisions have been made. The planning and locating a data centre and the building and opening a data centre chapters are relevant to someone considering building or setting up a data centre, but the criteria for considering location of a data centre could also apply to someone considering, for example, the use of a shared services solution – e.g. sharing services in a data centre based in a zone that is at risk of flooding, storms or other hazardous elements could risk loss of the data stored there.

Before embarking on a project of building a new data centre, it may be useful to re-confirm that construction of a new data

centre is the most efficient way of dealing with the data storage needs concerned. There may in fact be a more suitable alternative solution, such as utilising services provided by an independent data centre provider or re-assessing the efficiency of any existing data centres. We have also considered in the shared services chapter other alternatives such as whether, in fact, the efficiency of any existing data centre could be improved (rather than incurring the costs of building a new data centre) or even whether parties can share services.

Regardless of whether the data is stored in a new data centre built for purpose or an existing one, there are a number of other matters that need to be considered simply to operate a data centre. The list is considerably larger than can be included in detail within this guide, but includes data privacy and continuing energy efficiency. As also mentioned in more detail in the environment and corporate governance chapter, the public demand for cleaner and greener IT may result, in due course, in requirements to report publicly on the “green” status of data centres or to comply with an industry-based standard of efficiency. This has already been discussed in a number of jurisdictions. Other possibilities are tax and investment incentives for data centres that will be powered using green energy sources.

We have also considered a number of “Hot Topics” across different regions (Africa, South America, Europe, Asia and the Pacific, the Middle East, the United States and Canada). Each of these demonstrates how data centres are becoming of greater significance worldwide and indicate a key trend or issue for that region at the time of writing.

10 Norton Rose Fulbright – 2013

Data centres unboxed

3Planning and locating

a data centre

Norton Rose Fulbright – 2013 11

Planning and locating a data centre

are set to rise, as are energy costs. Environmental issues and related factors that may also affect the selection of a data centre location are described in Chapter 5 on environment and corporate governance. Further real estate matters such as ownership of the chosen land and construction considerations are discussed further in Chapter 4 on building and opening a data centre.

The location will be largely determined on the basis of the end-needs of the functioning data centre. The factors described in this Chapter and Chapters 4 and 5 will be balanced and prioritised according to the purpose of the data centre – that is whose needs it will meet.

Factors in determining the location of a facility will be influenced by whether the data centre is to be an in-house facility, also known as an owner/occupier facility (which often leads to proximity being a major factor) as compared to a facility owned and operated by a third party provider (who may also be referred to as a “developer”) where the service is outsourced.

If the developer is a private developer, whose main source of business is not providing data centres (and therefore the data centre is a support function to protect the security and data of the existing “main” business), such developer may want to locate the data centre near to the main head office in order to utilise existing staff and to check on performance and security.

However, if the private developer builds the data centre and then appoints an agent who is fully responsible for its efficiency and operation, the developer may be comfortable locating the data centre away from its head office. In either case disaster recovery planning may take the decision away and impose the need for a remote facility.

The decision criteria as to whether an owner/occupier should seek to externalise the service include the need for internal management (perhaps for regulatory purposes), the lack of capital to build facilities/acquire new space, business needs (for example where additional facilities are required to service short to medium term demands from clients) and the lack of in-house skills. Choosing a third party to provide data centre services is clearly a major decision, and is considered further in Chapter 6 on outsourcing and offshoring.

Planning and locating a data centre

In this Chapter we will describe some of the major legal and commercial considerations in determining the location of a data centre. Whilst the recent economic climate has led to greater efficiencies of existing data centre footprint space, recent market surveys have confirmed that the need to expand facilities is increasingly a commercial imperative. It should be noted that a variety of finance and logistics models exist which granulise the site selection process in considerably more detail than is allowed in this paper. For example, sophisticated models may factor into data centre location the flight paths of commercial aircraft, the routes taken and changes predicted to flight landing paths, with the stated purpose of assessing the risk of aircraft collision with the data centre.

The importance of site selection

For global operators, clearly a growing sector given the inexorable growth of the cloud, an assessment must be made of the jurisdiction of the proposed data centre site. Data centre down time is costly and potentially catastrophic to a business, yet technological advantages have divorced the need for physical proximity of the data centre to the end user. Comparative analysis can often demonstrate a significant saving in operating costs by offshoring, but cost saving alone is rarely the definitive factor in deciding the location of a new facility.

Macro factors include political stability, international bandwidth, the risk of natural disasters, levels of regulatory control, energy infrastructure and levels of taxation. As assessment of these risks, together with the application of a weighting factor for each (imposed in order to reflect specific operator requirements) need to be considered carefully as a part of the site selection process.

The need to locate the data centre “offshore” due to the perceived reduction in costs (for example of land, labour, construction, telecommunications, and electricity) is considered further in Chapter 6 on outsourcing and offshoring.

Sustainability is increasingly a major consideration. It is claimed that data centres account for between 2 per cent and 5 per cent of global carbon emissions, a figure which draws significant attention. Carbon taxes

12 Norton Rose Fulbright – 2013

Data centres unboxed

• the seismic risk profile; it is noted that the data centre operations in Japan have proved to be remarkably robust despite recent major earthquakes;

• the ground can withstand the foundations or the floor loading can accommodate the levels of equipment installed; retro-fitting an existing building for data centre usage can prove to be problematic.

TemperatureData centres need to be kept cool in order to prevent any of the internal systems from overheating. Optimising air flow within a data centre is crucial to maintaining the correct temperature. A key requirement is to prevent hot air and cold air mixing, hence the design of many data centres include the provision of hot aisles and cold aisles.

Whilst it is possible to use energy resources to ensure that the data centre is kept cool, this can be costly both in terms of electricity costs and also in terms of potential carbon credits. Accordingly there has been a recent trend towards locating data centres in colder locations such as Iceland and Ireland, to reduce the cooling costs. In other words, the data centre benefits from “free” cooling from the ambient temperature rather than the developer paying for chillers and the energy such chillers consume. These cooler ambient temperatures are often complemented by an abundance of cold water, another resource used for temperature regulation.

Suitability and security of the actual land siteSecurity and protection of the data held within data centres is one of the biggest concerns to any data centre owner; this is considered further at Chapter 8 on data privacy. In order to protect the data, the energy supply should run all year round and the building has to be protected from extreme environmental factors. The risks (such as a breach of data security, or simply in losing the value of a multi-million dollar building) are far greater to anyone seeking to develop a data centre in an environment subject to inclement weather, extreme physical conditions such as earthquakes and volcanoes, or security threats/civil unrest.

Numerous industry surveys have sought to rank the importance of the factors used to determine the location of a data centre. Whilst results vary, the two standout and interrelated factors in choosing a data centre are the availability of power and the actual location of the data centre. Perhaps, and counter-intuitively, the availability of a skilled workforce ranks much lower down the list of requirements when choosing a site for a data centre.

Regardless of the risks and factors relevant in assessing the merits of choosing a certain location for a data centre, the commercial considerations are often those paramount in making the decision. As a result, the legal analysis in this guide will focus on mitigating the legal and commercial risks associated with the relevant jurisdiction and the ownership/operating model to be adopted.

Supply and demand

As with any project, location of a data centre may depend (to some extent) upon the demand for data centre services. For example, as seen in Chapter 9 on hot topics and regional trends, there is currently a demand for data centres in the Middle East to serve the burgeoning data supply within the region. Equally, China and India are rapidly increasing the number of data centres in their countries. On the other hand, the trend for increased mergers and acquisitions in the sector has been perceived by some users as running the risk of reducing the choice of providers.

The physical nature of the underlying land

It has to be determined whether it is physically possible to build and operate a data centre in the proposed location. Issues to consider include:

• whether a data centre can be built on the land concerned;

• local weather profiles, for example flood, tsunami and typhoon risk and the impact of these upon the site for the data centre;

Norton Rose Fulbright – 2013 13

Planning and locating a data centre

TelecommunicationsEvery data centre has to be able to send and receive the information it is storing. If a server crashes, the consequences for the end-users can be far-reaching. The availability of a reliable telecommunications supply may also affect the insurance premiums.

Data centres should ordinarily therefore be located in a position where they can receive a consistent and effective telecommunications supply, and which is linked to a network that passes on to customers over a fast connection. On the other hand, some countries may not be a desirable location for a data centre because of their lack of infrastructure. Reference is made to “peering point”, as a desirable location with an abundance of fibre network.

In a similar vein, “latency” (effectively the small delay caused in signals due to the physical remoteness of a site) can be a material factor where a data centre is expected to provide a near instantaneous back-up of data. As the fibre optic network improves and gigabit capacity increases, latency, as measured in milliseconds, continues to reduce.

Efficient energy supply Getting access to efficient and reliable energy is always a factor in data centre construction and operation. Where uninterruptible power supply is needed, access both to mains power and a temporary power supply is required. Indeed, many data centre users measure their requirement in terms of critical power usage rather than “space” as measured in square meters or number of racks.

There are major variances in the resilience of energy transmission systems across jurisdictions. Even where power is available, fees may be payable to ensure that adequate power supplies are available to meet future demand. Certain jurisdictions and locations benefit from nature’s renewable resources such as hydro-power and geothermal energy. Such locations tend to lend themselves to longevity and reliability of supply.

Even if the relevant jurisdiction has adequate mains power supply available to the intended location of the data centre, not all locations have access to temporary power. In some countries the mobile/telecommunications network has

Access to services and supplies

Anyone considering building a data centre should also consider, prior to embarking on the project, whether the data centre will be able to function efficiently after completion of the construction of the external building. For example the data centre should have access to the necessary networks/information grids, efficient energy supplies, goods and services, and skilled employees.

Two further and associated points are worth highlighting, based on recent experience:

• “reserving” power is important, particularly when planning a data centre facility, to ensure that the facility can be energised when required. This is even more important when a phased facility is planned or a commitment to deliver expanded facilities is given by a developer; and

• the power grid infrastructure should be considered. Future supply risks (including energy supply costs) can be managed through long term energy contracts. The Uptime Institute provide useful statistics in order to measure historic costs for comparison purposes and which assist in predicting future costs.

Physical access to the property itselfAs part of considering the location of a data centre, the ability to access the land is a crucial consideration. If there is no access via a public road and the only way to access it is via neighbouring land held by independent parties, the data centre will be land-locked. A similar position is arrived at if the facility forms part of a campus or larger complex where there is a failure to deliver the expected services and infrastructure. The possible effect is that either no one can access the land to build, use or check the security of the data centre. In some cases, neighbouring landowners could seek to hold the land owner to ransom – i.e. require payments to be made in exchange for the grant of the necessary land rights.

These risks can be managed through ring fencing a facility in order to allow the data centre to be self-sufficient wherever possible.

14 Norton Rose Fulbright – 2013

Data centres unboxed

Time for provision of goods and servicesGoods and services necessary for the construction or operation of a data centre are often on long lead times and the timescale for obtaining such products will need to be factored into the planning process. Many items used in the construction of data centres may not be manufactured locally. For example, it is likely that the necessary diesel or rotary UPS has been manufactured in Europe and data centres being located outside of Europe should tailor delivery times into their critical path analysis. Procurement process is a factor in the construction of almost every data centre and experienced consultants and suppliers should be involved during the design and planning phases ahead of construction.

Availability of key personnel Some staff may be able to work remotely from the data centre. However these remote staff will have to be supplemented by key personnel who can attend the site and deal with any issues that must be addressed on the ground. These are likely to include engineers, nearing close proximity to the premises to deal with problems in a matter of minutes. The remote staff will need to have suitable access to the “on-the-ground” staff. Working together with project managers and other consultants is also essential which raises the issue of dealing with the liability apportionment for key consultants during use.

There may be a requirement under local laws to employ local staff (or at least to employ a certain proportion of employees who are local staff).

expanded beyond the geographical boundaries of the electricity network. Anyone seeking to place a data centre in such jurisdiction should consider relying on on-site generators, with a greater risk that the data centre would not have suitable, constant or reliable power.

A metric often used to measure the cost of energy to a data centre is simply to determine the cost of the provision of electricity expressed in units of local currency (or US Dollar equivalent) in kw/h. Similarly users will be able to estimate their average power drawn from data centre facilities, measured in kw/sq m (i.e. the cost of the supply of electricity/size of facility). Combining the cost of supply against average use provides an indication of the energy costs, which in most instances is the most significant operating cost of a data centre.

Temporary back up power can either be stored on site (assuming the site has capacity to hold a generator) or it could be sourced from an external supplier. The contractual position can become quite complex when there are different sources of energy (and especially when there are different suppliers involved). Given that the temporary power is an emergency back-up, it must be a reliable source of power and it should be considered whether any failure to obtain such back-up power could affect the validity or cost of insuring the data centre.

One of the latest factors to enter any deliberation of location of a data centre is whether the energy supply is renewable. There are even suggestions of building data centres that can be powered by biogas, so that the data centre should be located near to a biogas supply.

Rights of wayIn order to receive the power from the main grid or temporary provider and to send and receive information by and through the telecommunications networks, it must be established whether cables are required to be laid over or through neighbouring land. If this is the case then the land on which the data centre is located should have sufficient rights of way over such neighbouring properties.

Norton Rose Fulbright – 2013 15

Planning and locating a data centre

Jurisdictional case study: AustraliaThere are varying strategies in place across Australia to encourage and promote “greener” construction and operating practices. Typically, the regulation of general planning and construction issues is undertaken at the State level and not at the national level, leading to inconsistent outcomes. Examples of Australia’s State-based regulation that can impact on the construction and development of data centres include:

• in New South Wales, contractors seeking to work on major projects worth AUS $10 million or more (or projects that are environmentally sensitive) are required to have a corporate Environment Management System accredited by a government construction agency. This system must either comply with the New South Wales Environmental Management System Guidelines, or comply with the Australian Standard AS/NZS ISO 14001:1996 relating to Environmental Management Systems;

• in Western Australia, the Environment Protection Agency (Agency) undertaking environmental impact assessments of proposals and schemes referred to under the relevant legislation. Where a development proposal is likely to have a significant effect on the environment,the project may be referred to the Agency for a decision on whether an impact assessment must be undertaken. However, an assessment of whether a project needs approval will usually depend on the environmental values of the area affected by the construction and the extent and likely impact of the change on the environment; and

• in Queensland, certain environmentally relevant activities are required to have development approval or to implement a code of compliance before the activity can be commenced.

Jurisdiction

Planning consentsThe developer should ensure that it is permitted to build and operate the data centre in the proposed location. If planning permission is not obtained prior to acquiring a site and ultimately is not available for the project, the site could become redundant.

In most jurisdictions, planning permission/consent is required prior to carrying out any development. Planning consent is usually obtained from a local planning authority or government department, although other entities may also need to approve the development, depending on the size of the development and the effect on the environment and any other applicable local laws.

The intended use of the land concerned may be set out in a “plan” and it can be extremely difficult to seek to place a data centre on land that has been determined by the authority to be used for purposes other than a data centre such as residential or retail purposes.

In some situations, the planning authority may require the developer to mitigate any negative effects on the local area. For example if the existing road infrastructure is inadequate to deal with the construction traffic, the authority may seek payments towards the road network or for the developer to build new roads.

There may also be authorities that will have specific requirements on the design and this will largely depend on the extent to which the jurisdiction concerned has experience in and houses existing data centres.

Obtaining planning permission can be a costly and lengthy process and it is recommended that planning consultants are appointed.

16 Norton Rose Fulbright – 2013

Data centres unboxed

Political and legislative interventionThought must be given to the political stability of the jurisdiction of the data centre. Protectionist legislation and protective markets can hinder development and political instability can endanger long term confidence in a project.

Design considerations

For new data centres being constructed, there are some additional design options that should be considered.

One option available for new data centre developments is to utilise external ambient air to cool the data centre, which is particularly effective where the data centre is located in colder environments.

Greenfield data centres can also take into account location-specific benefits when deciding on the site of a new data centre. For example, sea or lake water may be used as a thermal sink or heat exchange, or the data centre may be located near sources of renewable wind, solar or hydro power where available. However, these locations may conflict with other requirements such as ease of access to telecommunications infrastructure, geo-stability of the location and flood zone considerations.

Another option is the deployment of self-contained modular data centres that can be built to scale up capacity on demand or which can even be re-located to meet needs in another area.

Finally, for new data centres located near other buildings, waste heat from the data centre may be used to heat nearby office buildings.

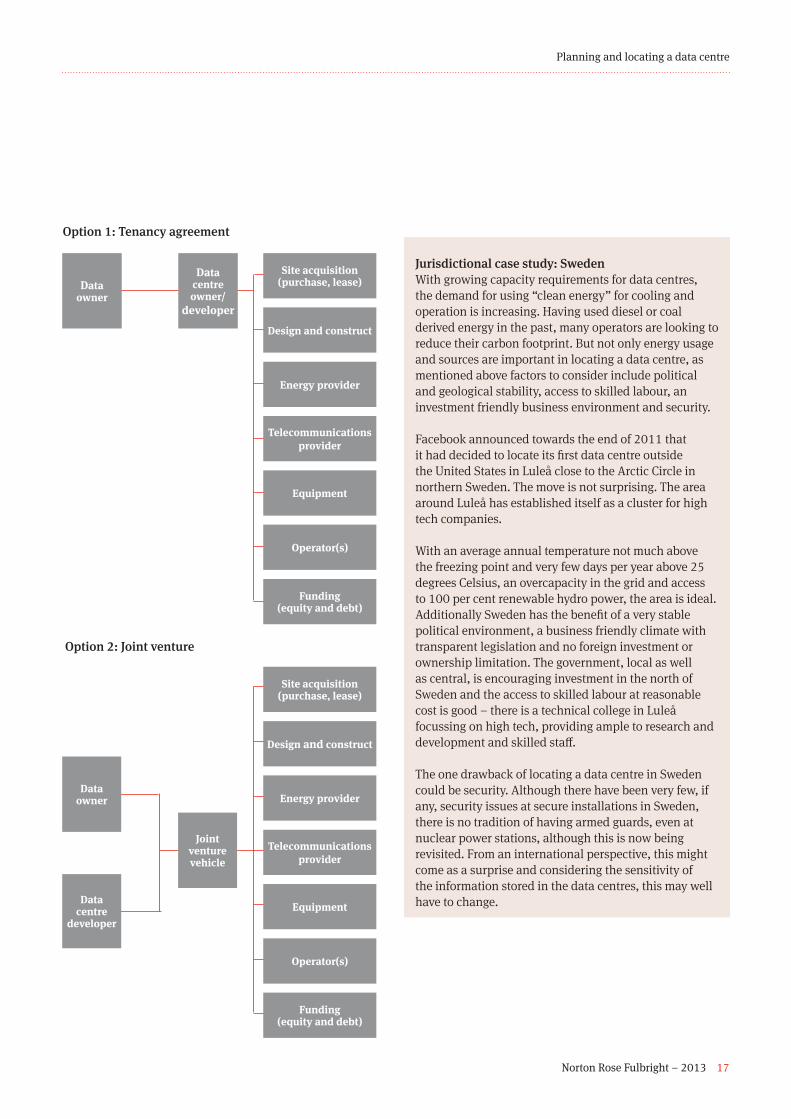

Ownership structures

Different structures also exist in terms of the actual ownership of the data centre facility. Two common ownership structures used by data centre owners are the tenancy agreement model and the joint venture model, which are described in diagrammatic form opposite.

Incentives to locate data centres in the regionThere are a number of jurisdictions that actively encourage data centre development, with the intended consequence of enhancing development in the area and improving employment and economic factors. In the US, incentives are offered in some markets to “enterprise” users (businesses operating commercial software and data) in order to create a business friendly environment.

Such jurisdictions may offer incentives to locate data centres there, advertise their power rates, or offer land for free, in return for the developer locating the data centre in the specified area.

Another positive factor in such jurisdictions is that planning consents are likely to be more readily obtainable for the proposed project site.

There has been an emergence of “clustering” whereby one well known provider develops a data centre and other providers subsequently place their data centres in the same geographical area. Many data centres have therefore emerged around business centres, which are likely to have established real estate laws and are also likely to attract employees.

For example, in Australia, several business parks have emerged as data centre clusters, such as the DC Creek Facility in New South Wales. In America, a number of clusters have arisen, such as at Quincy in Washington, where Yahoo! set up its data centre and others followed.

Whilst a private developer will be able to utilise the benefits of a data centre cluster, a host developer may be uncomfortable locating in an area where competing services already exist. However the host developer considering development in a location without any data centre experience may find that the hurdles in dealing with authorities and setting up outweigh the benefits from lack of competition.

Norton Rose Fulbright – 2013 17

Planning and locating a data centre

Option 2: Joint venture

Data owner

Data centre owner/

developer

Site acquisition (purchase, lease)

Energy provider

Equipment

Design and construct

Telecommunications provider

Operator(s)

Funding(equity and debt)

Joint venture vehicle

Data owner

Data centre

developer

Energy provider

Equipment

Design and construct

Telecommunications provider

Operator(s)

Funding(equity and debt)

Jurisdictional case study: SwedenWith growing capacity requirements for data centres, the demand for using “clean energy” for cooling and operation is increasing. Having used diesel or coal derived energy in the past, many operators are looking to reduce their carbon footprint. But not only energy usage and sources are important in locating a data centre, as mentioned above factors to consider include political and geological stability, access to skilled labour, an investment friendly business environment and security.

Facebook announced towards the end of 2011 that it had decided to locate its first data centre outside the United States in Luleå close to the Arctic Circle in northern Sweden. The move is not surprising. The area around Luleå has established itself as a cluster for high tech companies.

With an average annual temperature not much above the freezing point and very few days per year above 25 degrees Celsius, an overcapacity in the grid and access to 100 per cent renewable hydro power, the area is ideal. Additionally Sweden has the benefit of a very stable political environment, a business friendly climate with transparent legislation and no foreign investment or ownership limitation. The government, local as well as central, is encouraging investment in the north of Sweden and the access to skilled labour at reasonable cost is good – there is a technical college in Luleå focussing on high tech, providing ample to research and development and skilled staff.

The one drawback of locating a data centre in Sweden could be security. Although there have been very few, if any, security issues at secure installations in Sweden, there is no tradition of having armed guards, even at nuclear power stations, although this is now being revisited. From an international perspective, this might come as a surprise and considering the sensitivity of the information stored in the data centres, this may well have to change.

Site acquisition (purchase, lease)

Option 1: Tenancy agreement

18 Norton Rose Fulbright – 2013

Data centres unboxed

4Building and opening

a data centre

Norton Rose Fulbright – 2013 19

Building and opening a data centre

In some countries it is not possible to hold freehold title to land. It may therefore be the case that the developer is only able to obtain a lease and then build the data centre on the basis of such rights.

If the developer does not hold and cannot acquire freehold title to the underlying land, it is fundamental that the developer will have sufficient legal and contractual rights to build on the land concerned and to have exclusive use of the constructed data centre for the desired period of time. (In some countries there are also limitations on the length of leasehold type interests – for example there may be a maximum duration of 50 years, with a possible renewal thereafter.)

Due diligence If the land is to be acquired on a freehold basis, the developer should complete a full due diligence of the title to the property. Matters to be considered include:

• whether there are any encumbrances (third party rights) over the property such as an existing mortgage or a lease;

• whether there are sufficient rights to access the property (which are mentioned in Chapter 3 on planning and locating a data centre); and

• whether any third parties have rights to purchase the land or other priority interests that could prejudice the developer’s ownership and use of the land concerned.

Building and opening a data centre

In this Chapter we consider a number of factors that can fundamentally impede or affect the speed and ability to build a data centre. These are some of the salient issues, however they will still vary on a case by case basis. The issues can be separated into real estate matters and contractual matters. Many of the issues regarding building a data centre apply to both host and private developers, regardless of the end purpose. However we have made some references to issues that will likely only apply to either a private developer or a host developer.

Building a data centre: real estate factors

Ownership of the land concerned In most jurisdictions land is commonly owned by either:

• freehold estate/title, which gives the holder absolute title over the land (subject to any encumbrances (interests) that may legally affect the land); or

• leasehold estate/title, which gives the holder an interest in the land for a specific timeframe (or potentially for a rolling period), and on expiry of such term or other termination of the lease, all interest in the land reverts to the landlord. A leasehold estate may be subject to payment of rent and other restrictions and obligations. Assuming the intention is to build, the leasehold structure must enable construction upon the relevant site, which in some jurisdictions may be permitted by a mechanism such as a musataha.

It is increasingly common in certain jurisdictions for freehold and leasehold estates (usually long leasehold estates) to be held in the context of a “strata” or community title, where there has been a sub-division of land and/or a building. An application of this to a data centre project might be where a data centre is housed in the basement of a bigger building or other facility. This guide does not consider this and other types of land holding structures and only refers to freehold and leasehold estates.

A major consideration will therefore be whether the developer will hold leasehold or freehold title to the land on which the data centre will be built.

Acquisition of an existing data centreAs an alternative to constructing a data centre, a data centre provider may wish to acquire an existing data centre or at least accommodation which is readily adaptable for use as such. A few brief issues to consider are set out below.

If the developer is purchasing a completed data centre due diligence will be required on, for example, the ownership of the property and the equipment housed within the building.

It should not be assumed that ownership of both should rest in the same party.

20 Norton Rose Fulbright – 2013

Data centres unboxed

A building surveyor should check the structure, a valuer should confirm the value and other specialists should be called upon to look at more technical elements of the premises, for example the plant and equipment. If the “defects liability period”, or the period within which the parties involved in the initial construction of the facility have liabilities has not expired, then the developer may require the existing owner to assign to it the rights under the contractors’ appointments or by other means extend the duty of care owed to the developer by other key sub contractors and consultants engaged in the construction project. A similar analysis should be conducted in respect of key items of equipment in the data centre.

Many of the other issues in this Chapter will also apply to any such acquisition. Additionally, points on location, data privacy and environmental considerations will apply regardless of whether the data centre is being constructed or acquired as a completed (and possibly operating) structure.

However, other issues may apply when acquiring a data centre and a checklist will be akin to those to be considered when acquiring a business. For example some countries have laws regarding the automatic transfer of employees if there is a transfer of a business and indeed impose a regime that cannot be contracted out of; purchase taxes take different forms and are imposed at different rates depending on the jurisdiction; contractual arrangements may not be freely assignable or consent may be needed.

A key consideration in determining the form of the lease is the stage at which the tenant/developer engages with the land owner. At an early stage the land owner and intended tenant can work in unison to build a facility to meet the requirements of the tenant (commonly referred to as a “pre-let” agreement). The bespoke nature of the project should be reflected in the terms of the lease. A land owner may choose to build a facility in the expectation that a tenant can be found in due course. This type of development, often referred to as a “speculative development”, relies on the land owner being sufficiently confident that there is demand for his product. A facility procured on this basis is typically offered as a “powered shell” product (i.e. providing the external shell/structure of the building and an adequate power supply). A lease granted in this situation will include provisions to reflect the circumstances at the time, for example in order to address the often difficult issue of ownership and responsibility for fitting out the building for data centre usage. Retro fitting a premises as a data centre or granting a lease at different times in the lifecycle of a building, impose special demands to be factored into a lease.

Regardless the developer should consider:

• is the term/length of the lease long enough?;

• is there a right to break the lease early?;

• does the landlord have a right to terminate early which could prejudice the completion or use of the data centre?;

• is the rent a premium, or is it payable on an annual basis or a “turnover” basis?;

• are provisions regarding rent review appropriate? Does any increased rent over the course of the lease reflect projected revenue increases? (Negotiations on the meaning of “open market rent” can often be intense. For example in the UK data centre market the uncertainty in the open market value has resulted in many leases moving away to an alternative basis of review, such as fixed increment increases or review by reference to a market index, such as the retail prices index);

• what additional costs will be incurred by virtue of the lease, such as business rates and other local land taxes?;

LeaseIf leasehold property is being considered the major concern for the developer (as potential tenant) and its financier will be to ensure that the premises that are the subject of the lease are clear by reference to a plan, and that the lease cannot be broken early.

We would expect in most cases to see a “fully repairing insuring” lease, where the costs of all repairs and insurance are borne by the tenant (developer). The developer (especially any host developer) would likely wish to obtain the insurance itself and then provide evidence to the landlord, in order to ensure that the insurance is a viable and effective policy.

Norton Rose Fulbright – 2013 21

Building and opening a data centre

The developer will need to be certain that any contractor carrying out such building works complies with applicable planning and building consents and any other laws and regulations.

Registration and taxDepending on the jurisdiction in which the land concerned is located, there may be formalities applicable to either the acquisition of land on either a freehold or leasehold basis. For example it may be necessary to register:

• a purchase of freehold title; or

• entry into a lease – registration would likely be against the landlord’s (or superior landlord’s) freehold title.

Furthermore, transfer tax and duty may be payable on any acquisition of freehold land or entry into a lease and value added tax may be due on the rent payable under or the grant of the lease.

Financing the construction or acquisition of a data centre Any lenders will have separate concerns that need to be addressed.

Lenders will likely require a mortgage over the land. Usually lenders require their own independent legal advisers to complete a due diligence over the underlying land that will be mortgaged, to ensure that the mortgage will be valid and effective.

Financing documents can take a long time to prepare and usually contain the following:

• protections for the lenders – warranties and indemnities by the developer;

• costs of financing;

• construction standards and timelines (if applicable);

• operation standards which potentially will include environmental criteria to reflect the relevant lender’s corporate social responsibility requirements;

• events of default and consequences thereof, including an ability to call upon the security/mortgage; and

• what service charges are payable? If the user leases a “powered shell”, the service charge will be much lower as compared with a fully serviced facility where the scope of services often seen in a stand alone master services agreement are incorporated into the lease;

• are there sufficient rights to make alterations?;

• is there a mechanism to expand the facilities, for example to install additional UPS and/or standby facilities?;

• what are the powers to sell/ transfer the leasehold interest or enter into sub-leases? If the developer does not wish to operate the data centre and has to appoint a third party to do so on a leasehold basis this can be a deal breaker; and

• is there a right to obtain security over the leasehold interest (i.e. as a consequence of any mortgage)?

Some of the issues mentioned earlier in this Chapter regarding encumbrances may also apply to a lease.

It should also be considered whether a superior landlord’s consent is required.

In response to the user demands for flexible space a different approach is under review from the traditional lease. An alternative is to pay for data centre space by reference to power consumption (to reflect the major cost element for a data centre) or by number of rack spaces used. The scaleability of demand and useage can be matched by prices which tracks this metric directly.

Consents and permits We have referred to the ability to obtain planning permission in Chapter 3 on planning and locating a data centre. In most countries it is a requirement to obtain permission prior to commencing the development. The planning permission will likely contain conditions and require the development to be in accordance with the approved plans.

Additionally, prior to commencing building works, the developer will likely need to obtain a “building permit” or other equivalent consent. This usually entails submission of various plans and information to the applicable local authority. Such consents frequently contain conditions and ordinarily require the development to be completed in accordance with the approved plans.

22 Norton Rose Fulbright – 2013

Data centres unboxed

• requirements on the developer to provide information, such as regular reports on the construction progress and payments to contractors, and finance statements once the data centre is operational.

This list is not exhaustive as often the documentation will depend on the size and nature of the project concerned and also the relationship between the parties. As with any financing, the timescales and issues involved can be greater if dealing with a consortium of lenders.

Construction issues

The developer should need to appoint an array of consultants to ensure that the end data centre:

• fulfils the needs of the developers and if applicable, if the developer will be a host developer, the needs of the clients who will use the data centre services;

• complies with the requirements of any lenders;

• complies with any planning permissions, building consents and all other relevant laws affecting the construction and use of the data centre; and

• meets desired energy efficiency levels whether imposed by legislation or otherwise.

In the case of a turnkey product, it can become increasingly difficult to find a single team of consultants to deliver all the skills and services needed for the project.

Accordingly, (other than a legal team) the developer may need to consider the appointment of an architect/designer, a planning expert, a contractor/builder, a project manager and other specialist contractors.

The contracts of appointment for any of these consultants should be considered carefully. The allocation of responsibilities for completion of the end product needs to be established early in the appointment discussions and clearly set out in the appointment documentation.

Contracts of appointment should also at the very least require that the consultant concerned:

• maintains a specified standard of care;

• holds the necessary insurance throughout the course of the development;

• complies with all laws;

• if necessary holds a permit to carry out the relevant services; and

• meets targets and timetables (potentially a consultant could be offered greater pay for better efficiency in the data centre).

The appointments will also need to clearly set out when costs are payable and whether there should be a retention of payment until any “snagging” or defects have been rectified. The developer will likely also want the ability to assign its rights under the appointments to any purchasers and rights for its lenders to also rely on the consultant (collateral warranties). In addition, separate warranties and guarantees might be issued directly to the user to ensure that the integrity of the developer’s suite of warranties need not be broken up.

Specific contract issues will include site access and availability of particular parts of the building during different times of construction and then upgrades to the plant and equipment therein.

Plant and equipment: depreciation and upgradesWhether buying plant and equipment for a new data centre or as part of an existing data centre, the ownership and then depreciation of such plant and equipment should be considered.

Many items of plant and equipment will over the course of time be redundant from subsequent technological advancements. It therefore needs to be considered whether it is possible to efficiently upgrade such plant.

Norton Rose Fulbright – 2013 23

Building and opening a data centre

novated to the builder (or else directs the builder to adopt the nominated design team). We have set out the D&C model in diagrammatic form below:

Structures for appointment of building contractors This section examines at a high level some typical structures for the design and construction of a data centre project. It examines the conventional method of structuring the procurement by way of “construct only” and “D&C” models. It then discusses a unique solution to the challenges faced by data centre procurement – the “split model”.

Model 1: Construct only modelUnder this model the developer uses and retains a designer throughout the project, and accepts all design risk, while the builder (also known as the contractor) accepts only construction risk. The consultancy agreement between the developer and the designer remains in place throughout the design development stage, which takes the design to 100 per cent complete, prior to engagement of the builder. We have set out the construct only model in diagrammatic form below:

The owner

Builder

DesignerConsultancy agreement

Construct only contract

The owner

Builder Novation deed

Designer

Design and construct contract

Consultancy agreement

Model 2: Design and construct procurement structure (also known as a design and build structure)This model (the D&C model) commonly uses a novated design and construct structure, or else imposes an obligation to direct the contractor to use a nominated design team (which achieves a similar result). Under such a structure the developer would engage a designer to carry out initial design work and then separately engage a builder to carry out both the design and the construction of the data centre.

The D&C model will require that the builder accept the risk of carrying out the design, in circumstances where a significant portion (if not all) of the design has in fact been carried out by the designer while engaged by the developer. To enable the builder to accept this risk, the consultancy agreement under which the developer engages the designer will be

Model 3: Split modelThe split model combines the advantages of both the construct only model and D&C models.

Under the split model, it is anticipated that the developer will enter into two main contracts:

• a design contract with the relevant designer (for the preparation of a fully detailed design specification); and

• a modified “construct only” contract with a builder (who will be required to build the facility strictly in accordance with the detailed design).

The designer will take all design responsibility for the data centre project, and the builder will take all construction risk for the project.

24 Norton Rose Fulbright – 2013

Data centres unboxed

that in handing over greater responsibility to the builder, the builder could value manage down the quality of the facility; and

• timing – sometimes the developer is not clear on which packages of work will be undertaken and the timing for those packages, so it requires the ability to direct precisely what is built and when. By using the split model, the developer can tender and award the work as multiple packages as and when needed, which will minimise variations and keep the price to a minimum.

Disadvantages include:

• no single point of responsibility – by adopting a split model, there is a risk that if defects are found in the facility, this may lead to disputes as to whether the defect was caused by defective design or defective construction works. Under the D&C model, regardless of whether the defect is design or construction related (or a mix of both), the responsibility will rest with the builder. This may be particularly important if the data centre must achieve certain operational outcomes (for example cooling control, and ample power supply and availability). However, to mitigate this risk associated with the split model, the developer, designer and builder could jointly engage an independent certifier. Any disputes between the parties as to whether a defect in the facility is due to design or construction would then be dealt with by the independent certifier and the parties will be bound by this determination (subject to any agreed exceptions);

• designer insolvency – by separately engaging the designer, the developer places more dependency on the designer than it would do if the D&C model was adopted. In addition, the designer is likely to have lower levels of professional indemnity insurance and a smaller cap on liability than the builder. However, a developer can mitigate this risk by ensuring any designer it engages is of sound financial backing with prominence in the market, and the professional indemnity insurance level and limit of liability can be negotiated; and

• design management skills – under the D&C model, the developer would have the ability to tap into the in-house design management skill that large design and construct contractors have, which usually results in the design and construction process being better co-ordinated. However, often the design is largely complete by the time the construction commences, which minimises this risk.

The developer will also enter into a simple consultancy agreement with an independent certifier who will be responsible for testing the design of the facility (prior to being accepted by the developer) and for managing disputes regarding defects. The split model is set out in diagrammatic form below:

The owner

Builder DesignerIndependent certifier

Construct only contract

Independent certifier

agreement

Design agreement

There are both advantages and disadvantages of procuring a data centre using the split model.

Advantages include:

• price – by engaging separate entities for the design and construction elements of the project, the developer will avoid paying the premium that a single entity would impose for taking on both design and construction risk. This is advantageous considering the developer is likely to have a fixed budget for a project;

• design control – by directly engaging the designer for the duration of the project, the developer will retain control over the design for the entire project. If the developer does not have significant in-house design expertise for the specific type of project, this will enable the developer to have access to the designer to provide advice throughout all stages of the project when dealing with the builder;

• quality control – where the designer is separately engaged by the developer for the duration of the project, there is no incentive for the designer to compromise on quality. Where the D&C model is used, there is a risk

Norton Rose Fulbright – 2013 25

Building and opening a data centre

Summary of structure alternativesConventional models such as the construct only model and the D&C model remain the simplest way to approach procuring a new data centre. However, such conventional models are often not appropriate having regard to the commercial and technical requirements normally put forward by the developer’s commercial and technical representatives. In particular the following factors often mitigate against use of a conventional model and favour the use of the split model:

• the increased costs that will be incurred by the developer if the construct only model or the D&C model are used; and

• the timing issues which flow out of the requirement that the developer has direct control over both the design (through a direct design contract) and the facility that is actually constructed (through a construct only contract).

Under the split model, the developer will be required to play a more significant role in project management and, in particular, instructing and co-ordinating the roles of the designer and the contractor. While this is often a preference for the developer’s technical and commercial representatives, it is also an added responsibility and therefore a further risk.

Contractual matters

The developer will also enter into a number of contracts such as:

• contracts for equipping and maintaining the data centre with servers and infrastructure;

• contracts to procure staff or contracts with third parties responsible for managing the data centre; and

• contracts with telecommunications providers, electricity providers and security providers.

Insurance contracts Different types of insurance are required at different stages:

• insurance by both developer and consultant during construction of the project. The responsibility for procuring may be transferred to the principle contractor or retained by the developer. Regardless of the arrangements, continuity of insurance is a key requirement for risk management;

• insurance during ownership and use of the data centre, which could include:

— services interruption insurance (e.g. covering a failure of the utility company to provide electricity which prohibitively affects the business);

— property insurance;

— business interruption insurance (or “loss of revenue insurance”);

— accounts receivable insurance; and

— valuable documents insurance.

Developers should review any insurance policy and consider:

• does it cover replacement value or some depreciated value;

• what are the caveats; and

• managing user expectations. Economic loss as a consequence of an interruption in service is usually not an insurable risk. Developers are often advised to encourage users to make their own insurance arrangements for their business operations.

Case study – prevention is better than cureMany US data centres incorporate anti-hurricane measures to ensure additional layers of protection are available to preserve continuity of service. This has proved to be the case during the annual US East Coast hurricane season. In a similar vein, although in very difficult conditions, the anti-earthquake measures incorporated in Japanese data centres proved to be robust and effective in early 2011. Insurance risk reflected in the insurance premium and so proper design and management should result in an immediate and ongoing saving in insurance premiums.

26 Norton Rose Fulbright – 2013

Data centres unboxed

5Environment and

corporate governance

Norton Rose Fulbright – 2013 27

Environment and corporate governance

Environment and corporate governance

Carbon footprint of data centresIt is estimated that the ICT sector contributes similar global emissions attributable to the airline industry.

Of the global CO2 emissions currently attributed to the ICT sector, it is estimated that data centres are responsible for approximately a quarter of those emissions. Furthermore, the rapid growth in the number and size of data centres makes them an increasing contributor of CO2 emissions going forward.

Power consumption of data centres as an operating costThe energy consumption and efficiency of a data centre are also significant commercial issues for operators and users of data centres, as the cost of powering a data centre is a significant portion of its overall running cost. The power consumption of a data centre can be broadly grouped into two categories:

• user consumption – the power consumption of the computer equipment hosted in the data centre; and

• operator consumption – the power consumption of the data centre infrastructure (such as cooling and environmental controls, security systems, fire control systems, monitoring systems and redundancies).

User consumption is typically within the control of the user of the data centre, while operator consumption is within the control of the operator (and builder of the data centre). In a typical data centre hosting agreement, costs relating to user consumption are generally passed through directly from the data centre operator to the user, while the costs relating to operator consumption are generally amortised across all users of the data centre. This amortisation is usually performed as part of the fees for the “data centre services”, which are generally calculated on a fee per kW power basis or a fee per space or cabinet allocated basis. It has been estimated that the cooling requirements often consume up to 50 per cent of the electricity usage of a data centre. Accordingly, a data centre that provides more efficient cooling is likely to be more competitive in the long term (as it can offer a lower per kW or per space fee).

In this Chapter we examine some of the potential corporate governance and environmental issues relating to the operation and use of data centres. Due to the complexity and scope of the issues mentioned, it is not possible to concisely summarise the legal requirements described below on a cross-jurisdictional basis. However, we have provided case study examples of energy efficiency measures implemented in Australia and the UK.

Legal issues relevant to data centres and the environment

There is a range of conflicting and inconsistent national laws and regulations around the world relating to energy use, emissions reporting and other similar requirements. However, it is possible to draw out some general themes. Existing legislative or regulatory regimes may include either or both of the following areas:

• energy efficiency labelling or disclosure requirements for specified items, ranging from individual items of hardware or equipment to an overall rating for an entire building; and/or

• reporting requirements for energy use or carbon emissions, typically above a certain specified threshold.

These issues may be addressed through legislation, set out in mandatory standards or simply covered in voluntary codes. In addition, any existing regime typically has a broad application and does not apply solely to organisations in the information and communication technology (ICT) sector.

Energy issues relating to data centres

Data centres present a number of potential issues in the context of energy usage. As there is an increasing global focus on environmental issues, the high power demands of data centres present challenges for data centre operators due to the associated carbon emissions. Similarly, power consumption is a significant contributor to the operating costs of data centres.

28 Norton Rose Fulbright – 2013

Data centres unboxed

The efficiency of the data centre will also play a big part in the overall cost to a data centre user. The energy efficiency of a data centre is generally measured by its PUE, which is defined as the total power usage of the data centre divided by the total power usage of servers hosted at that data centre. For example, a PUE of 2.0 means that half the energy costs are used by the data centre’s own infrastructure and not by the hosted equipment. A well operated data centre is expected to have a PUE of less than 2.0. State of the art data centre designs have allowed PUE levels of 1.1 to 1.3 to be achieved.

Another common commercial factor that influences the efficiency of a data centre relates to the power density of the data centre. A higher power density data centre allows more ICT equipment to be located in the same amount of space, which decreases the physical footprint of the data centre (or increases the capacity of the data centre, at the same footprint). However, a high density data centre will require different cooling designs to ensure sufficient cooling of the hosted equipment.

In addition to power usage, the water consumption of a data centre is another significant commercial consideration. As potable water is generally used in the chillers that are typically used to cool data centres, the water consumption of a data centre is also directly related to power consumption of the data centre.

Corporate governance issues relating to data centres

Effective corporate governance is a key strategy for addressing the energy-related challenges posed by data centres. The monitoring of power usage, the adoption of energy efficiency standards and the implementation of power reduction strategies will assist in reducing both the environmental impact of data centres and the operational costs associated with such facilities.

Corporate governance and “green IT”The implementation of energy-efficient initiatives is not something that can be left to the Chief Information Officer as part of their responsibility for the organisation’s information technology needs. The board or executive management of an organisation needs to be involved and to support the implementation of such policies. A top down approach is often necessary in order to change attitudes towards energy efficiency and to drive improvements across the organisation.

In the context of data centres, senior management should be making enquiries in relation to:

• the energy efficiency of any data centres used or owned by the organisation;

• whether the data centres used or owned by the organisation already have, or could obtain, any independent certification relating to energy efficiency; and

• whether there are any power reduction strategies that could be implemented, both to drive down operating costs and to reduce the environmental impact of the organisation.

Energy efficiency standards Increasingly, ICT projects (including data centre design and construction) are seeking certification from independent national bodies on a voluntary basis. Examples of some of these national certification standards include:

• the LEED certification system – developed by the US Green Building Council. This is one of the most widely-used energy and environmental rating systems in the world. There is over 9 billion square feet of building space participating in the rating system and 1.6 million square feet being certified every day around the world. The LEED certification system provides independent, third-party verification that a building was designed and built using strategies aimed at achieving high performance in key areas of human and environmental health. In order to achieve LEED certification, a building must be eligible (this includes data centres) and must obtain a certain number of “points” in order to achieve a certification level; and

Norton Rose Fulbright – 2013 29

Environment and corporate governance

Accordingly, implementing power reduction strategies can have both environmental and practical commercial benefits. For the operators of data centres, energy efficiency can also be a key selling point for their services, particularly where large customers are interested in learning about the environmental credentials of their suppliers as part of the procurement process.

There are a number of different strategies available to reduce power consumption in a data centre. While these strategies are necessarily technical in nature, and may not be applicable in all situations, they can potentially have a significant effect on the commercial negotiations between the user and the operator.

While the user is in control over the consumption of their own equipment, the power reductions achieved by the user can have follow-on benefits and savings to the operator consumption (particularly by reducing the cooling capacity). Accordingly, a sole tenant or a substantial tenant of a data centre may be able to leverage any implementation of its own power reduction strategies to extract a lower fee from the data centre operator.

A data centre user may also impose contractual requirements on the operator to improve the power usage efficiency during the term of the contract. However, the cost savings may be difficult to quantify, given that most of the strategies will require substantial capital investment.

Options available to users of data centresAs users are not typically able to control the upgrade and configuration of the data centre, the two main power reduction strategies available to users are:

• relocating the hosted ICT equipment to a more power efficient data centre; and

• reducing the power usage of the hosted ICT equipment.

The main benefit of relocating hosted equipment to a more power efficient data centre is that power (and cost) savings are future looking in nature, and the savings will automatically extend to any new ICT equipment hosted in the new data centre. The main disadvantage is that relocation of ICT equipment is generally an expensive exercise requiring significant technical support. This is

• the Green Star certification system – administered by the Green Building Council of Australia. This is a comprehensive, national and voluntary environmental rating system that evaluates the environmental design and construction of buildings. Organisations may obtain a Green Star certification for a building if it meets all four of the Green Star Eligibility Criteria. Once a project has obtained an official Green Star rating, the relevant company may publicly claim and promote the star rating of its building(s).

Other benefits of being greenThe adoption of energy efficient strategies can have intangible benefits for organisations. Environmentally-aware organisations may wish to be seen to be “green” or at least to be “good corporate citizens” who do not use or procure environmentally-unfriendly services.

It may be a relevant factor for a data centre user (as part of its procurement requirements when choosing a data centre) that the data centre has been independently accredited under energy efficiency standards similar to those set out above.

A high level of environmental awareness and corporate social responsibility can in fact be a selling point for organisations, particularly if their competitors have not implemented environmentally-friendly policies.

As a result organisations should consider implementing energy efficiency policies (including utilising available power reduction strategies) as part of their corporate governance regime.

Power reduction strategies for data centres

The use of power reduction strategies has a dual benefit in relation to data centres, namely:

• fewer carbon emissions being produced as a result of meeting the electricity requirements of data centres, which indirectly reduces the environmental impact; and

• reduced operating costs for data centre operators and users as a result of lower power bills.

30 Norton Rose Fulbright – 2013

Data centres unboxed

particularly the case for older “24x7” equipment which may not have been powered off for an extended period of time. In addition, if the ICT equipment hosts mission critical production servers, then the migration will likely need to be conducted out of hours or in stages to minimise or eliminate downtimes, which will further increase the complexity and cost of the exercise. As a result, the engagement of a service provider to assist in the relocation will likely require a separate procurement exercise.

Users can generally reduce the power usage of their ICT equipment by upgrading older components to more power efficient components. For example, it may be possible to replace older power supplies with more modern power supplies with higher power efficiency ratings, as well as replacing hard disk drives with solid state drives and using more power efficient processors.

A significant benefit is that these upgrades can be conducted incrementally as part of an organisation’s hardware upgrade roadmap. The use of upgraded equipment may also enable significant server consolidation through virtualisation, which further reduces the total number of computer servers required.

Options available to operators of existing data centresThe operators of existing data centres can employ a range of power reduction strategies to improve the power efficiency of their data centre and reduce operating costs.

First, data centre operators can reduce power usage by upgrading older components with more efficient versions (such as more efficient chillers). For higher tier data centres, the cost and energy savings can be substantial, as higher tier data centres will generally have significant “standby” equipment to provide redundancy. This approach will allow such replacements to be carried out in a manner that is transparent to data centre users, as the changes generally do not require the cessation of operations.

More recently, significant research has been conducted in cooling designs for data centres. Practices such as the hot-aisle/cold-aisle rack arrangements are generally employed in most data centres to improve cooling efficiencies. However, newer technologies and computational fluid dynamics may

assist in identifying areas for further improvements, such as by reducing hot spots, reducing the mixing of hot and cold air and utilising variable capacity cooling units.

A more efficient cooling design may also allow the data centre operator to increase the air temperature of the cold-aisle or the chilled water without impacting the hosted equipment, which will reduce the power usage of cooling equipment and result in further operational savings. More recently, some hardware suppliers have suggested that their equipment is able to operate at much higher ambient temperatures without limiting its service life.

There are also some additional design options that should be considered for new data centres. These are considered further in Chapter 3 on planning and locating a data centre.

Tying it all together

Based on the above discussion, implementing environmentally-friendly green IT policies can be part of an overall corporate governance strategy. Energy-efficient strategies can have a positive effect on a company’s image, as well as on its bottom line. Pro-active management is essential in driving an energy-efficient approach to the way in which an organisation does business and how it implements any power reduction strategies.

In the specific context of data centres, incremental improvements implemented as part of an overall environmentally-friendly approach to corporate governance can be achieved in a number of ways as set out above. In light of the potential tangible and intangible benefits, organisations should consider implementing policies relating to energy efficiency and power consumption reduction, or reviewing and updating any existing policies covering these areas.

Norton Rose Fulbright – 2013 31

Environment and corporate governance

Although the carbon price covers a broad range of industry sectors, it is important to note that only facilities directly responsible for emitting carbon pollution will have a liability under the Mechanism. As the ICT sector contributes to emissions indirectly, through its acquisition of materials, resources and services (for example electronic equipment, electricity, transport and waste disposal), the sector itself is unlikely to have any direct obligations under the Mechanism. However, the Mechanism is likely to result in increased costs (due to higher electricity prices) being passed through from direct emitters suppling the ICT sector.

Various forms of financial assistance will be provided to industry as the Mechanism is phased in. However, as an indirect contributor to carbon emissions, the ICT industry is not directly eligible for any of these forms of assistance. It may be of relevance to the ICT industry that the power industry will receive some assistance as it may decrease the carbon liabilities for the power industry and consequently reduce the costs passed through to the ICT sector.

Those operating in the ICT sector, in particular data centre operators, may wish to ensure that the relevant clauses in supply contracts deal appropriately with liability for both direct and indirect costs arising from the Mechanism. The legal ability of suppliers to contractually pass on the carbon credit cost to customers, including data centre operators, will depend on the terms of the contract in question. Generally speaking, a tax recovery clause will not allow a supplier to pass on the carbon credit cost, as this cost is not a “tax”. The cost is more properly classified as a “charge”. However, “change in law” clauses should generally allow suppliers to pass on this charge, as it is legislatively mandated.

Other Australian-specific guidelinesThere is an existing Australian Standard for Corporate Governance of Information Technology (AS/NZS ISO/IEC 38500:2010). This standard encourages the adoption of practices and behaviours throughout an organisation to promote the efficient and effective use of IT (it does not cover green IT, energy use or carbon emissions).

Jurisdictional case study: AustraliaEnergy reportingAustralia has an existing energy efficiency and carbon emissions reporting regime. Energy efficiency and emissions reporting are particularly relevant topics in light of the Australian government’s recent introduction of a carbon emissions trading regime.

The Australian legal framework for energy use and carbon emission reporting is outlined in the National Greenhouse and Energy Reporting Act 2007 (Cth). Corporations that meet a “threshold” emissions/use level must register with the Clean Energy Regulator. Registered corporations must report annually in respect of, for example, their greenhouse gas emissions, energy production and energy consumption.

There are also additional registration and reporting requirements under the Energy Efficiency Opportunity Act 2007 (Cth) for corporations which use more than 0.5 petajoules of energy per year. However, an organisation in the ICT sector would have to be running tens of thousands of servers at peak load before such registration and reporting requirements were applicable.