oil & gas - pwc · *connectedthinking pwc oil & gas in the fifth edition of oil & gas...

TRANSCRIPT

PwC*connectedthinking

Oil & Gas

In the fifth edition of Oil & Gas Group News you can learn

about managing in a downturn, including finding out more

about funding from capital markets, what effect the current

market conditions are having on the M&A market, discover

how to manage tax in a downturn and the hidden costs of

excise duties and possible exemptions.

We also provide a timely reminder of the VAT reclaim

opportunity available to all UK businesses and highlight how

our Commercial Assurance team have helped minimise

cash leakage and reduce costs on oil & gas contracts

There is also a round up of the best oil & gas publications

and events and our key PwC Oil & Gas experts who can

answer your questions.

Welcome

Group News*Issue 5

Welcome to the fifth edition of our regular PricewaterhouseCoopers Oil & Gas group newsletters. We have introduced a new electronic format for quick access to articles of interest. The newsletter presents a selection of articles from our industry experts, covering a range of topics within the assurance, tax and advisory arenas.

This edition is published in an environment which is seen as the most challenging in recent history. The record oil prices seen last summer seem a long distance away, with the global recession causing prices to plummet to a level less than a third of what was being achieved only 9 months ago. The capital markets have effectively frozen, with a record number of IPOs being withdrawn or postponed, and refinancing also proving difficult. Mid-tier companies in particular are being forced to find other means by which to ensure they have enough cash to continue operations. Some companies in the sector are having to consider whether acquisition by a larger player is the only means by which major projects will be completed.

Against this background, our newsletter considers some of the key issues which management teams should be aware of to not only to survive in the current marketplace but also prosper in the longer term. Our contributors consider areas where we have been successful in helping companies save costs, together with opportunities to reclaim costs from unexpected sources and how best to position companies to access new finance when the capital markets eventually thaw.

Our team of experts stand ready to assist you meet the current challenges and ensure that you are well-placed to come through the other side.

If you would like to discuss any of the issues please contact your local contact or myself in the first instance, but any of the team who are listed on the back page would be delighted to help you.

Mark KingUK Oil and Gas Group LeaderMarch 2009

WelcomeFunding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

Nick StevensonMid Tier Oil & Gas Leader+44 (0) 20 7804 [email protected]

Derek CarmichaelSenior Manager, Assurance+44 (0) 20 7804 [email protected]

Welcome

Editorial team

Funding from the capital marketsWith capital markets frozen, what strategies should companies adopt to maximise their access to new finance?

Sink, survive or succeedWhat effect are the current market conditions having on the M&A market?

Managing tax in a downturnThe key areas which should be at the front of your mind when managing tax in the current environment

Hidden costsExcise duties can be a major cost incurred by the company… but exemptions may be available

Spotlight on… Commercial AssuranceFind out how we have helped minimise cash leakage and reduce costs on major oil & gas contracts

Events & publicationsA round up of the best oil & gas events and thought leadership from PwC

Cash refund opportunitiesA reminder of the VAT reclaim opportunity to all UK businesses, and the 31 March 2009 deadline

Key contactsPwC’s wide range of oil & gas experts are on hand to answer your queries

In this edition

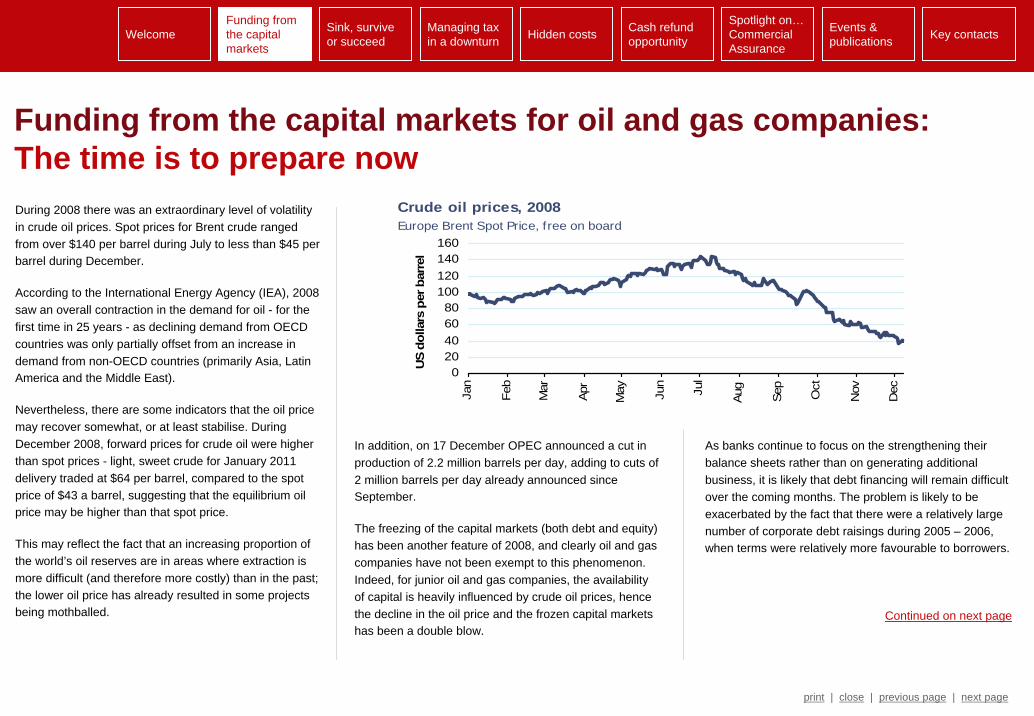

Funding from the capital markets for oil and gas companies:The time is to prepare nowDuring 2008 there was an extraordinary level of volatility in crude oil prices. Spot prices for Brent crude ranged from over $140 per barrel during July to less than $45 per barrel during December.

According to the International Energy Agency (IEA), 2008 saw an overall contraction in the demand for oil - for the first time in 25 years - as declining demand from OECD countries was only partially offset from an increase in demand from non-OECD countries (primarily Asia, Latin America and the Middle East).

Nevertheless, there are some indicators that the oil price may recover somewhat, or at least stabilise. During December 2008, forward prices for crude oil were higher than spot prices - light, sweet crude for January 2011 delivery traded at $64 per barrel, compared to the spot price of $43 a barrel, suggesting that the equilibrium oil price may be higher than that spot price.

This may reflect the fact that an increasing proportion of the world’s oil reserves are in areas where extraction is more difficult (and therefore more costly) than in the past; the lower oil price has already resulted in some projects being mothballed.

print | close | previous page | next page

WelcomeFunding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

Crude oil prices, 2008Europe Brent Spot Price, free on board

020406080

100120140160

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

US

dolla

rs p

er b

arre

l

In addition, on 17 December OPEC announced a cut in production of 2.2 million barrels per day, adding to cuts of 2 million barrels per day already announced since September.

The freezing of the capital markets (both debt and equity) has been another feature of 2008, and clearly oil and gas companies have not been exempt to this phenomenon. Indeed, for junior oil and gas companies, the availability of capital is heavily influenced by crude oil prices, hence the decline in the oil price and the frozen capital markets has been a double blow.

As banks continue to focus on the strengthening their balance sheets rather than on generating additional business, it is likely that debt financing will remain difficultover the coming months. The problem is likely to be exacerbated by the fact that there were a relatively large number of corporate debt raisings during 2005 – 2006, when terms were relatively more favourable to borrowers.

Continued on next page

Treasury management in the current economic environment should be a high priority, and should include a particular focus on reviewing and monitoring the adequacy of existing financing arrangements compared to expected future cash requirements, based on expected performance as well as realistic worst-case scenarios. This will also assist in providing regular and timely information to existing finance providers, which ultimately will build or cement relationships with them.

Managing the cost base is all the more important in a low oil price environment. Cost inefficiencies which may have been overlooked in the past will now need to be identified and eliminated. A targeted reduction of identified, specific costs is much more meaningful and realistic to investors than a generic aim of reducing costs by a specified amount across the board, and much less likely to damage the long-term health of the business.

The quality and timeliness of disclosures to the market is key; investors need to be kept informed about the business and performance, and will not appreciate last minute surprises.

print | close | previous page | next page

Many of these were 5-year deals and therefore fall due for refinancing over the next two to three years; given that most corporate refinancing is organised up to a year in advance, it is expected that 2009- 2010 will be a period of high corporate demand for debt refinancing combined with constraints in lending capacity from banks.

With regard to the equity markets, 2008 witnessed a record number of IPOs being withdrawn or postponed, and increased selling activity from institutional investors and hedge funds, driven in part by the need to meet redemption requirements. Most commentators predict that the prospects for fund raising in the equity markets will not pick up until Q3 2009 at the earliest.

Whatever the timing may be, it is clear that investors and debt providers will be significantly more risk-averse and discerning than has been the case in recent years. As such, companies will need to be able to effectively demonstrate and communicate a clear, realistic strategy in order to be successful in attracting further financing, be it debt or equity.

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

Richard [email protected]+44 (0) 020 7212 3887

Information regarding oil reserves is clearly a key element of information for investors. Disclosures in this area could be enhanced by including, for example, information regarding the basis of the investment decision in any particular field, which would have been based on factors beyond the “proved, possible, probable” categorisation of the field required by accounting and disclosure standards. Disclosure of the factors driving the investment decision, which would include sensitised best estimates of recovery, sales prices, capital costs and operating costs, would help investors to make more informed investment and valuation assessments for your company.

Ultimately, when the capital markets reopen it will be those companies that have demonstrated value through a viable strategy to operate in a difficult economic environment, and have kept the markets informed, that will succeed in attracting financing.

Funding from the capital markets for oil and gas companies:The time is to prepare now

Welcome

In February 2008 Brent Crude was trading at approximately $100 a barrel, subsequently trending upward over the following five months peaking at $147 a barrel in July 2008; there was even talk of crude prices reaching $200 a barrel and the question appeared to be more “when” rather than “if”. Today Brent Crude is trading nearer $40 a barrel and the world is appears to be in the deepest economic contraction since the great depression in the early 1930’s. So what are the short term implications for the oil and gas industry and what would this mean for Merger & Acquisition activity?

Sink, Survive or Succeed

Falling oil prices are putting a number of oil and gas company’s cash flows under pressure, particularly independents focussed on exploration and development without a strong base of production to support these activities or with a significant amount of debt to support. These companies are likely to find it difficult to raise fresh capital to finance on-going spend as traditional backers, such as banks, become more cautious and other forms of funding, such as asset sales or farm-outs, become more difficult to get away in the short term.

In addition to trying to understand the implications of the current economic downturn, stakeholders in the sector are grappling with uncertainty over the oil price and questioning the economic viability of assets when crude is trading at $40 a barrel and may even go lower. The combination of reduced funding (through debt, equity or disposals) and on-going capital commitments have started to result in players either reducing or postponing development programmes or, as in the case of Oilexco(the most active driller in the North Sea a year ago) resulting in the more extreme situation of going into administration.

However, these challenges present an opportunity for the mid-tier oil and gas companies that are cash rich or have a low gearing ratio that is not pressurised by their existing expenditure. In this environment of suppressed equity valuations and, in some cases, distressed sellers, companies with a strong balance sheet will have the ability to acquire good assets at relatively cheap prices. Recently, Dana Petroleum announced the acquisition of Bow Valley Energy for £123m and they confirmed that they are looking for opportunities via other distressed companies. “This is typical of the times we are in,” said Tom Cross, Dana chief executive, in a recent article in the Financial Times. “Things were going along well (for Bow Valley). They have a professional and conservative management team. But they were unable to extend their debt. And this will happen to others” he commented.

In the coming month we expect a number of other companies in the sector to be forced to consider their position as actual, or potential, covenants breaches occur or they identify inability to raise funds for contracted spend. In particular, this is likely to impact businesses that raised finance at the peak of the market between June 2007 and April 2008.

In addition, given the way in which assets in the sector are owned by multiple parties, any JV partners which themselves are struggling financially will have a knock-on effect on the other partner(s) who may be forced to increase their share of spend to compensate for this.

As recently reported in the press, the oil majors are putting pressure on service suppliers to reduce costs. This is understandable given that last time oil prices were at current levels the supplier cost base was significantly lower than where it is today. One key concern is that in previous periods of low oil prices, the oil majors have taken similar initiatives to reduce unit costs, but they haven't addressed the underlying efficiency of supply chain activities. As a result, as soon as oil prices rise again, the costs follow. This time the pressure is on the majors and service suppliers to collaborate in streamlining and simplifying process and asset activities as well as focus in on unit cost.

print | close | previous page | next page

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

Continued on next page

Welcome

The key to successfully managing through this downturn is for companies to recognise risks inherent in their business model and take actions quickly to address these. This will mean carefully considering a number of areas of risk, such as supplier solvency risk, JV partner financing risk, customer credit risk, an inability to meet contractual commitments and so on.

Coupled with the fact that traditional sources of finance for the sector are likely to be difficult to access in the short term, companies will need to assess what this means for their business and develop a plan to address this. This could include accelerating asset disposals or looking for solvent partners before companies become distressed sellers. And if banks are involved, initiating dialogue early with the support of appropriate professional advice to manage a process which many companies will not have had to be involved in previously.

PricewaterhouseCoopers has a range of services that may be of assistance to companies in the current economic climate, including the following:

print | close | previous page | next page

Brian [email protected]

+44 (0) 20 7804 4973

Neil [email protected]

+44 (0) 20 7804 3168

Sink, Survive or Succeed

• Cash Accelerator, designed to help companies to identify ways in which cash can be optimised. Our methodology considers cash optimisation in a more comprehensive way by putting it at the heart of the business and focusing on longer-term value enhancement rather than short term measures. It also benefits from PwC specialist service involvement such as treasury, operations, pension and performance improvement

• Independent Business Reviews, which can be undertaken on behalf of management prior to discussions with lending banks. Through experience we have seen that where companies have identified a potential risk of default or need to negotiate a funding extension, even in the short term, there is significant benefit in engaging with us in order to ensure that companies maintain control over any process undertaken with the banks

• Due Diligence (Buy and Sell Side) and Vendor Assistance. In the current market we expect to see a number of deals and it will be expected by shareholders that appropriate due diligence has been undertaken. We have undertaken due diligence for a number of companies in the sector, covering areas such as financial, taxation and pensions.

In addition, for companies that are considering a sale of part or all of their business, we can assist by preparing either a Vendor Due Diligence report or by undertaking Vendor Assistance to help companies to ensure that information provided to bidders is robust and comprehensive and addresses the key value areas from a financial perspective.

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contactsWelcome

print | close | previous page | next page

Managing tax in a downturn

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

At a time of economic downturn, businesses are under even more pressure than usual to focus on cost reductions. Tax is a significant cost for most businesses and there should be an emphasis on managing tax like any other cost.

A more UK-specific technique would be to reassess the calculations of quarterly instalment tax payments, using more timely and accurate financial information rather than using budgets or prior year results which do not accurately reflect the impact of the downturn.

Other techniques include ensuring that the effect of reliefs, allowances and losses are maximised in the current year. There are a number of different ways that these techniques can be achieved.

Managing indirect taxes can have a direct impact on both cash and the profit before tax line in the accounts. Certain types of business pay substantially more in indirect than direct taxes. Groups need to know what their indirect tax bills are and how they can manage them more effectively.

Managing financing in the credit crunch

In recent times, obtaining credit was easy. Traditional tax planning matched borrowings against operating profits arising in local jurisdictions. In times of economic downturn, when obtaining external finance is much harder, managing intra-group financing becomes crucial.

Considering refinancing options may be a necessary part of ensuring that financing arrangements are tax efficient, with the overall aim of maximising available tax deductions in high tax jurisdictions (without creating losses that cannot be used) and mitigating the tax impact of interest income.

• Restrictions on interest deductions: Several jurisdictions (for example, the US and Germany) have restrictions in place over how much of a company’s taxable profits can be sheltered by interest expense. The UK is proposing to bring in a similar rule (the “interest cap”). Financing structures should therefore be reviewed in detail to ensure they do not fall foul of any of these specific provisions.

• Transfer pricing: Given current capital market conditions, there is always a question as to whether tax authorities are going to change their approach to what constitutes arms length rates or require higher levels of equity, thereby restricting debt deductions.

• Anti-avoidance: Tax authorities have an increasingly wide range of tools at their disposal to counter actual, or perceived, tax avoidance. We would expect these tools to be freely used, and any tax planning implemented should therefore have underlying substance and be properly documented with careful on-going management and assessment to have the best chance of succeeding.

However, tax authorities are likely to scrutinise financing arrangements carefully and the following issues must always be considered:

At the same time, tax functions face pressure from legislative change and more aggressive and litigious approaches being taken by tax authorities which are eager to help governments balance their books.

The balance between managing tax costs and managing tax risks is therefore a difficult one. With the storm clouds brewing, tax directors are under pressure to address the myriad of issues affecting their global tax strategies in such an uncertain world. At a time of an economic downturn when there is a renewed focus on ’cash is king’, managing tax efficiency, both risks and opportunities, becomes essential.

The following are areas that should be at the front of peoples’ minds when managing tax in the current environment.

How to manage tax efficiency

With intense focus on the credit crunch, companies are starting to recognise the benefits of managing tax to obtain short term cash flow benefits from managing their tax payments. In hard times cash is king and as such opportunities to focus on actions that either produce an immediate saving or provide short term cash flow benefits are common.

For example, resolving long-standing tax investigations that have been provided against will result in a release of provisions that can improve profits or make available cash previously earmarked for settlement of the provision.

Continued on next page

Welcome

John [email protected]

+44 (0) 20 7804 3479

print | close | previous page | next page

Linda [email protected]

+44 (0) 20 7804 6760

Summary

The evolution of global business models and the current economic climate are making the job of managing tax harder.

The need for a global tax strategy that is integral to corporate strategy, and tax planning that is better aligned with operations while taking into account legislation and the attitude of tax authorities, is crucial to achieving and sustaining a lower worldwide effective accounts and cash tax rate especially in the potentially difficult times to come.

The challenge is how to give the tax number some transparency, particularly in a downturn, as it enables investors to better understand the tax profile of the company and better value their investments.

To provide transparency it is necessary for the business to understand the key drivers of the cash tax rate and the overall effective rate and to understand what, if any, the risk inherent in the tax figure is and whether it is properly reflected in the reported results. It is also important to note that the total tax cost not only comprises the more visible direct taxes suffered, but also a number of less visible taxes such as excise duties, payroll taxes, VAT, and business rates.

To improve the accuracy of reporting, several techniques or approaches can be followed. For example, resolving long standing enquiries that have been provided against, reviewing tax planning structures which are currently in place to assess the risk inherent in them and the quality of the procedures in place to maintain them helps provide comfort around the provisions required.

Ensuring that the filing position of the tax returns is accurate and up to date also gives more transparency to the overall tax profile of the group. All of these will help communication of the group’s tax rate profile and exposure, which potentially reduces the volatility of results and improves investors’ confidence.

Realign business plans to make them more tax efficient

In many cases, globalisation has led to business operations having overly-complex historic corporate structures. This has resulted in challenging decision making processes and corporate governance compliance which in turn has lead to high legal, processing and systems maintenance costs. These structures are now under pressure as organisations seek to simplify their businesses to improve efficiency in their markets.

There are two main drivers to business change - those driven by the business and those driven by opportunities to optimise tax. Due to the current environment, the alignment between these two drivers is increasing. Groups should ensure that operational change does not create tax exposure, risk or incremental cost and take the necessary steps to defend against possible tax authority enquiries. With careful implementation, the opportunity provided by business change can be used to optimise the tax position of that change and create long term benefits to the tax position of the group.

How to be more transparent in tax reporting

There continue to be increases in the complexity of tax laws and IFRS has required a mindset shift for tax reporting. This makes it increasingly difficult for companies and stakeholders to understand clearly all the components that make up the tax figure and what implications it has for the business.

Managing tax in a downturn

To view our recent webcast on foreign profits, please click here.

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contactsWelcome

Hidden costs

The Australian Government recently repealed an exemption it had applied since 1977 to the condensate (a light crude oil) obtained from gas wells in the North West Shelf Project Area. The excise charge is calculated as an ad valorem tax based on the value of crude oil produced from a petroleum field. The highest excise rate, levied on the largest producers, is set at 30% of the value of the crude.

The majority of excise revenue, though, is still levied on the finished, refined products, ensuring that Governments benefit from the whole chain of exploration, production and refining.

In the UK, over £24 billion was received in excise revenue from oils. However, there are a number of anomalies within the excise law, particularly in relation to the EC Energy Tax Directive that requires scrutiny to ensure that Governments and relevant fiscal authorities are complying with their own obligations. In a time of heavy regulation to all aspects of the oil industry, Governments must ensure that they are applying the law correctly.

Examples of this include mandatory exemptions within European law for oils used in certain processes. A number of Member States have been slow to transpose the Energy Tax Directive requirements (introduced in 2004) into local legislation.

print | close | previous page | next page

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

More recently, a new Excise Directive has been introduced to replace the general excise Directive that relates to the production, storage and distribution of excise goods in the EU. Energy products obtain certain concessions in relation to costs incurred and flexibility of operations and it is important that these concessions are placed in any new excise law that must be in force by 1 January 2010. The concessions include an exemption of financial guarantees for energy products moved by sea or pipeline and movement criteria in relation to the electronic movement document that will replace the paper Administrative Accompanying Document.

The variety of excise taxes across national boundaries, and complexity of those taxes, poses challenges for companies who operate in multiple locations, are new to territories or have small tax functions.

PwC tax specialists operate in 148 countries and, with their detailed knowledge of the regulations specific to their location, are able to assist companies in identifying tax saving opportunities while still ensuring full compliance with local laws and regulations. An example of savings available for a gas company was highlighted by PwC in Denmark. The company receives natural gas from the North Sea.

The gas is transmitted directly to the consumers or is stored if there is no immediate need for the gas. The gas pressure is increased using motor compressors driven by natural gas. The increase of the pressure creates extensive heat, which is used for heating purposes. When the gas is transmitted from the storage facilities into the transmission line, the gas pressure must be reduced. The reduction of the pressure involves extensive cooling. This is prevented by heating the natural gas before reducing the pressure.

Using the mandatory exemptions provided for in the Energy Tax Directive the use of gas in the above cases must be exempt from excise duty.

In conclusion, excise duty is often seen as a fixed cost that may be passed on to the consumer. However, excise duty may relate to a hidden cost that may be exempt from the duty charge. Excise legislation also impacts the manner in which you do business and simplified procedures and reductions in guarantees can greatly assist your business.

Excise duty is a major source of revenue to Government Treasury Departments across the globe. Both developed and developing countries rely heavily on the revenue received from excise goods to bolster Treasury funds. Although the vast majority of excise costs are borne by the downstream activities relating to oil and gas production and supply, upstream activities are also beginning to be viewed as yielding revenue opportunities for excise.

Philip [email protected]

+44 (0) 161 247 4518

Welcome

Significant cash refund opportunity

print | close | previous page | next page

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

Recent developments have created a VAT reclaim opportunity that is available to all businesses in the UK, and could generate significant repayments for businesses in the oil and gas sector.

The decision of the UK courts in the cases of Fleming and Conde Naste mean that business have a one off opportunity to revisit their VAT affairs prior to 1997 in order to assess whether they have claims to recover VAT that may have been under-recovered on costs or over-declared on revenues at the time.

A number of businesses have made successful reclaims already, and the VAT repaid plus interest accrued on these repayments has amounted to many millions of pounds in some circumstances.

The potential difficulty that businesses may face is the lack of availability of records prior to 1997. However, HMRC are taking a pragmatic approach to accepting evidence to support such claims, on the basis that this opportunity to revisit these time periods is a result of HMRC's failure to implement legislation correctly at that time.

Claims have been successfully made in respect of a number of areas including costs incurred as a result of share issues and other finance raising transactions, company car fleets, employee expenses and previous VAT claims that could not be applied prior to 1997.

Businesses are required to make claims by 31 March 2009, so it is important that they consider this as a matter of urgency.

Seamus [email protected]

+44 (0) 20 7213 2359

Welcome

The recent decline in the Oil price has been viewed as an opportunity to challenge costs on existing and planned projects as well as to re-visit the cost base. The mantra is “you can’t do much about the oil price but you can manage costs”.

Many IOCs have been on record to say that they will defer projects to provide themselves with leverage against their suppliers. The problem is that a combination of credit scarcity and pressure on prices could drive oil services companies to consolidation or administration. The subsequent upcycle is then likely to see an even steeper escalation of costs.

Since some projects take several years to completion, it is entirely possible that early negotiated price reductions are reversed and overall cost outcomes are no different from what was anticipated.

So what is the most effective way of taking advantage of current market conditions to build a sustainable cost advantage?

The first step is to understand the difference between price and cost. There is a often a confusion that the “work is done” when the price is negotiated – however this is only one element of a number of drivers that determine cost.

print | close | previous page | next page

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

These include risk management decisions, contractual pricing mechanisms, contingencies, communication and workflow, competency, scope and change management to name a few.

The second step is to evaluate which contracts are sensitive to factors outside price, a tool to make that assessment could be a subjectivity v complexity map as shown below.

Continued on next page

Spotlight on… Commercial AssuranceUnderstanding price and cost

Welcome

Spotlight on… Commercial AssuranceUnderstanding price and cost

cash leakage and highlighting opportunities to conserve cash or reduce costs.

Qadir works predominantly within the Oil & Gas industry, working with the Majors, independents, juniors and oilfield service providers both in the UK and overseas, within both the upstream and downstream areas.

Qadir has been with the firm for 10 years and has considerable experience providing advice relating to the commercial control of contractual arrangements. In particular, Qadir provides advice on supplier selection, contract charging mechanisms, alignment and management of contractor incentivisation (KPIs), demand management, planning & budgeting, contract operation and structure, post-award management and billing compliance.

print | close | previous page | next page

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

Qadir Marikar has recently been appointed as a Partner within the Risk Assurance Services practice and leads our Commercial Assurance practice in the UK. Qadir developed PwC’s proprietary approach to reviewing major commercial arrangements with a view to preventing

Recent projects have included:

Qadir [email protected]

+44 (0) 771 892 8344

The third step is to understand how cost is impacted by the various cost drivers and rank those drivers that have the greatest influence on cost.

In order to do this it would be necessary to trace the cash payments and allocate it to the different activities and interfaces that took place in the delivery of the service –this is usually carried out by a contract deep dive using experienced contract auditors.

Finally once the relationship between price and cost is understood and the operational levers identified, the next step is to develop a strategy for dealing with the contract. This could include changing the way you operate with the contractor, improving planning and information sharing as well as developing a commercial relationship that delivers value over the longer term.

The current economic environment is such that contractors are open to deliver long term improvement in exchange for guaranteed workloads. The challenge for IOCs is to utilise the present opportunity to secure a long term cost advantage rather than just a short term win.

• Advising a Major Oil & Gas Company on developing a deep dive approach to uncovering areas of cost leakage when engaging Capital Project and Service Contractors in their North Sea business unit, resulting in an 11% reduction in overall costs.

• Reviewing the integrity of the supply chain for an oilfield services provider focussing on identifying opportunities for cost reduction and cash management.

• Advising on developing a reporting and commercial framework for delivering project under a production sharing arrangement to maximise cost recovery.

About Qadir

Welcome

Events and publications

print | close | previous page | next page

Upcoming events

Mid-Tier BriefingsIntroducing a series of webcasts which discuss hot topics within the industry, and provide participants an opportunity to ask questions directly to our specialists.

Date Topic

May 2009 Deal or No Deal

If you are interested in participating in the webcasts, contact Louise Holland or your usual PwC contact.

Other publications

• The wealth of nations – How well do countries petroleum strategies align?

• Petroleum Accounting Principles, Procedures & Issues

• Financial Reporting in the oil and gas industry*

• Utilities global survey

For further information or hard copies of our publications, please contact Anna Crone in the Oil & Gas Marketing team or visit: www.pwc.com/oil&gas

Global energy capabilities statementThis global publication showcases our services and case studies that relate to the challenges the industry is facing. It contains our global and regional contacts, client list and a comprehensive overview of our thought leadership publications.

Oil & Gas Deals* 2008 - February 2009Oil & Gas Deals reviews deal activity in the oil and gas industry, examining both the rationale behind the overall trends and looking at key individual deals. The publication looks at both the year under review and ahead to the future direction of deal-making in the sector.

Cash Accelerator* - February 2009Access to cash is limited at a time when it’s most needed. Our new guide provides tips to companies on methods which can help accelerate the availability of cash within the existing structure of the business.

CFO Survival Guide - February 2009CFO's are struggling to meet the increasing and competing demands of their business, particularly in the current economic climate. The compliance burden has grown, the finance function is subject to increasing cost pressure, whilst the demand for more and better management information challenges the function to do more at lower cost.

prospects* Provides an insight into the aggregated performance of the junior oil & gas industry, as represented by 50 of the largest listed companies outside of the FTSE-100. Both oil & gas producers and oil equipment, services & distribution companies are included within our selection.

The IOCs in 2020 – Time for a change? - November 2008This report discusses how, given the recent events of unprecedented global financial crisis and turmoil, with the likely outcome of a global recession, now is probably an ideal opportunity for the IOCs to take a critical look at their mid to long term strategy and the organisational and operating attributes that will underpin this strategy.

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contactsWelcome

Key contacts

print | close | previous page | next page

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

Mark KingUK Oil and Gas Group Leader+44 (0) 20 7804 [email protected]

Michael HurleyPartner, Market & Value Advisory+44 (0) 20 7804 [email protected]

Tony SkryzpeckiPartner, Transaction Services+44 (0) 20 7804 [email protected]

Ian GreigPartner, Tax+44 (0) 1224 253 [email protected]

Ross HunterUK Energy, Utilities and Mining Leader+44 (0) 20 7804 [email protected]

Kevin ReynardPartner, Assurance+44 (0) 1224 253 [email protected]

Linda BealPartner, Tax+44 (0) 20 7804 [email protected]

Brian PufferPartner, Assurance+44 (0) 20 7804 [email protected]

Martin GrazierPartner, Market & Value & Advisory

+44 (0) 20 7804 [email protected]

Mike BeattieDirector, Tax+44 (0) 1224 253 [email protected]

Mark HigginsonPartner, Assurance+44 (0) 1224 253 [email protected]

Qadir MarikarCommercial Assurance Leader+44 (0) 189 552 [email protected]

Kate LeightonDirector, Tax+44 (0) 20 7213 [email protected]

Nick StevensonMid Tier Oil & Gas Leader+44 (0) 7804 [email protected]

Peter FieldDirector, Risk Assurance Services+44 (0) 20 7212 [email protected]

Tina TrickettDirector, Risk Assurance Services+44 (0) 20 7804 [email protected]

Stephanie PhizackerleyPartner, Personal Tax+44 (0) 20 804 [email protected]

Clare McCollDirector, Tax+44 (0) 141 245 [email protected]

Assurance Market & Value Advisory

Risk Assurance Services

Transaction services Tax

Commercial Assurance

Personal Tax Indirect Tax

Welcome

Alan BarrDirector, Transaction Services+44 (0) 1224 253 [email protected]

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2009 PricewaterhouseCoopers LLP. All rights reserved. ‘PricewaterhouseCoopers’ refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom), or, as the context requires, the PricewaterhouseCoopers global network or other member firms of the network, each of which is a separate and independent legal entity.

Design by PwC Online (03/09)

PwC

www.pwc.com/oil&gas

Funding from the capital markets

Sink, survive or succeed

Managing tax in a downturn

Spotlight on…Commercial Assurance

Events & publicationsHidden costs Cash refund

opportunity Key contacts

print | close | previous page | next page

Welcome