oil markets outlook - latest oil, energy & metals news, … · · 2013-09-24oil prices rise...

TRANSCRIPT

© 2013 Platts, McGraw Hill Financial. All rights reserved.

Oil Markets Outlook

Esa Ramasamy Editorial Director Singapore, September 18 2013

Crude – Range-bound or back to volatility?

2 Source: ICE

Making sense of the fundamentals…

• The US is awash with crude oil and refined products

• US oil demand is almost flat year on year and declining in some sectors

• Europe oil use continues to decline

• China, India consumption growth moderating

• OPEC is pumping above its 30 mil b/d ceiling

So why are oil prices high?

3

Market Drivers

4

MAIN DRIVERS

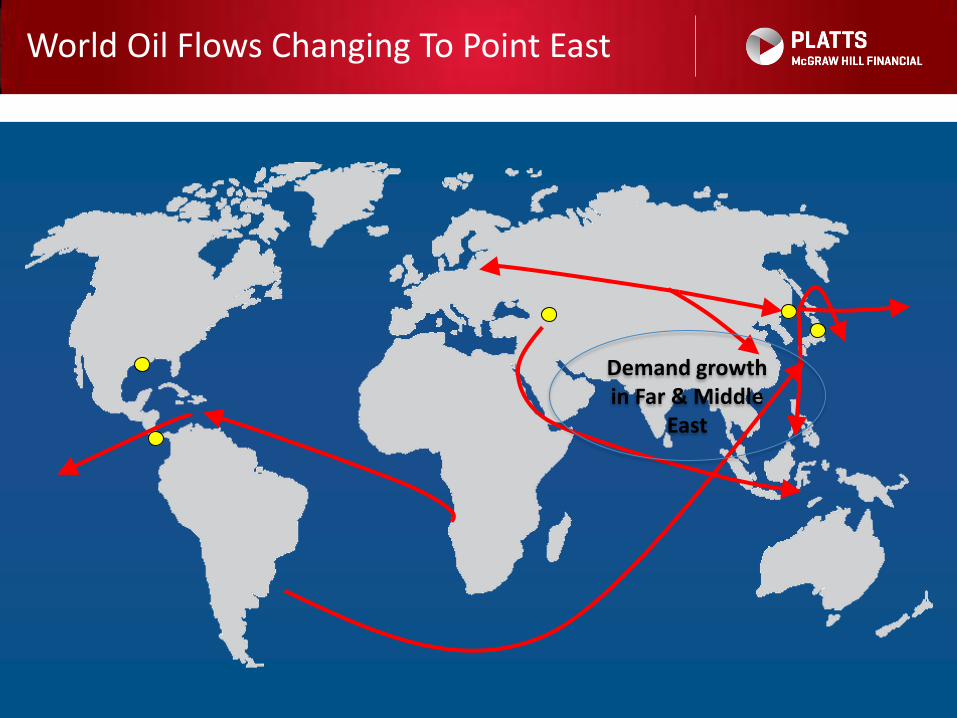

World Oil Flows Changing To Point East

Demand growth in Far & Middle

East

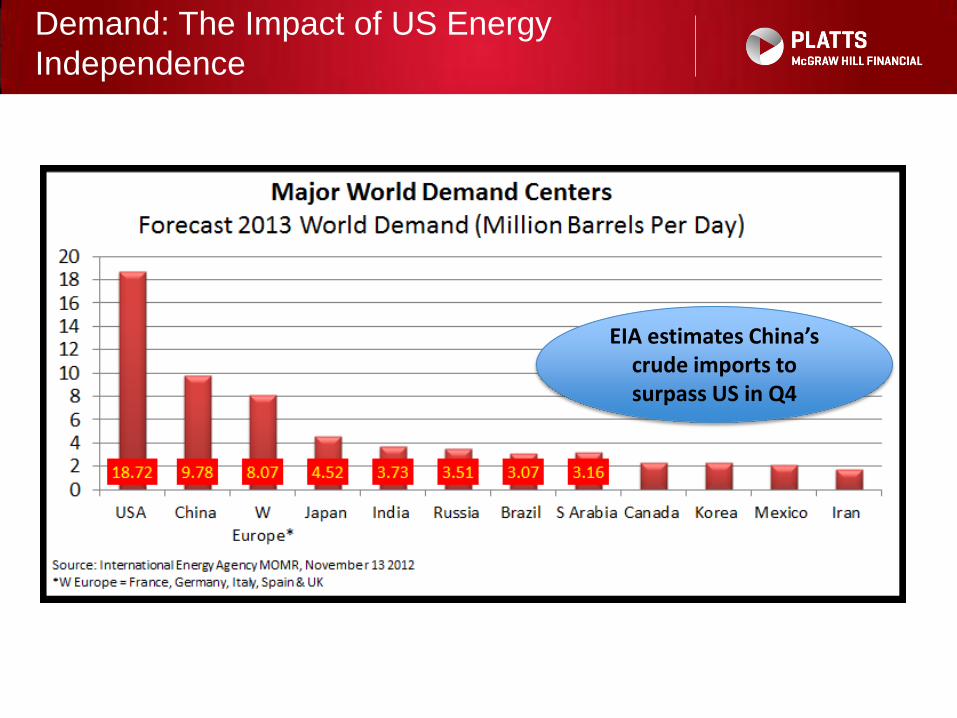

Demand: The Impact of US Energy

Independence

EIA estimates China’s crude imports to surpass US in Q4

Consumption Growth From Asia Pacific

7 Source: World Oil Outlook, OPEC

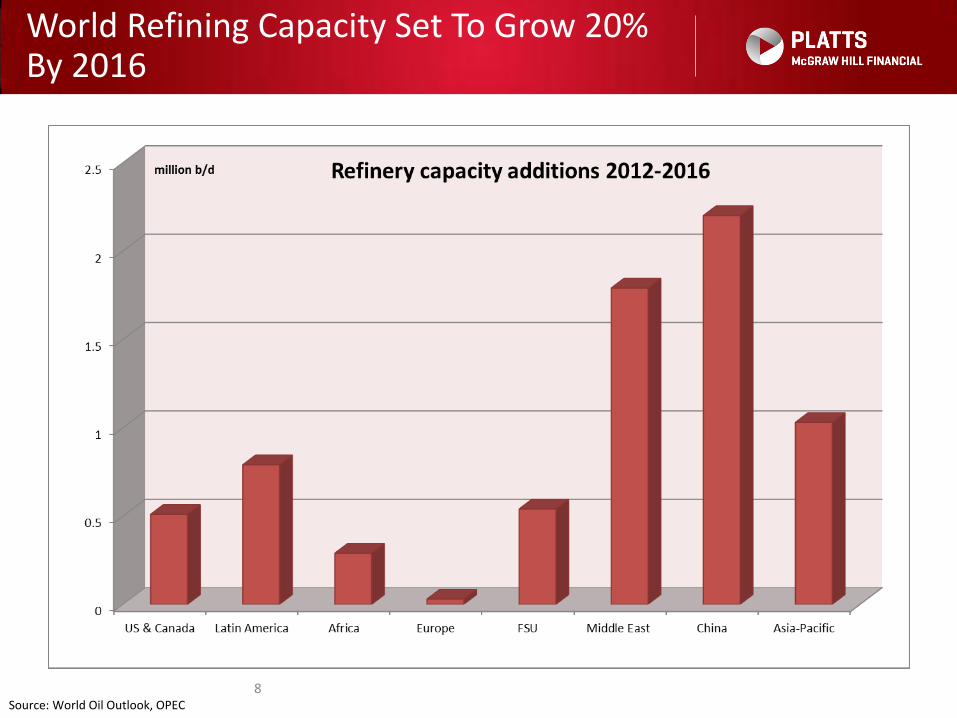

• Asia Pacific to see largest demand growth, but also largest refinery capacity increase

• Europe and Africa both facing steady diesel demand growth, coupled with limited capacity growth, or even reversal

World Refining Capacity Set To Grow 20% By 2016

8 Source: World Oil Outlook, OPEC

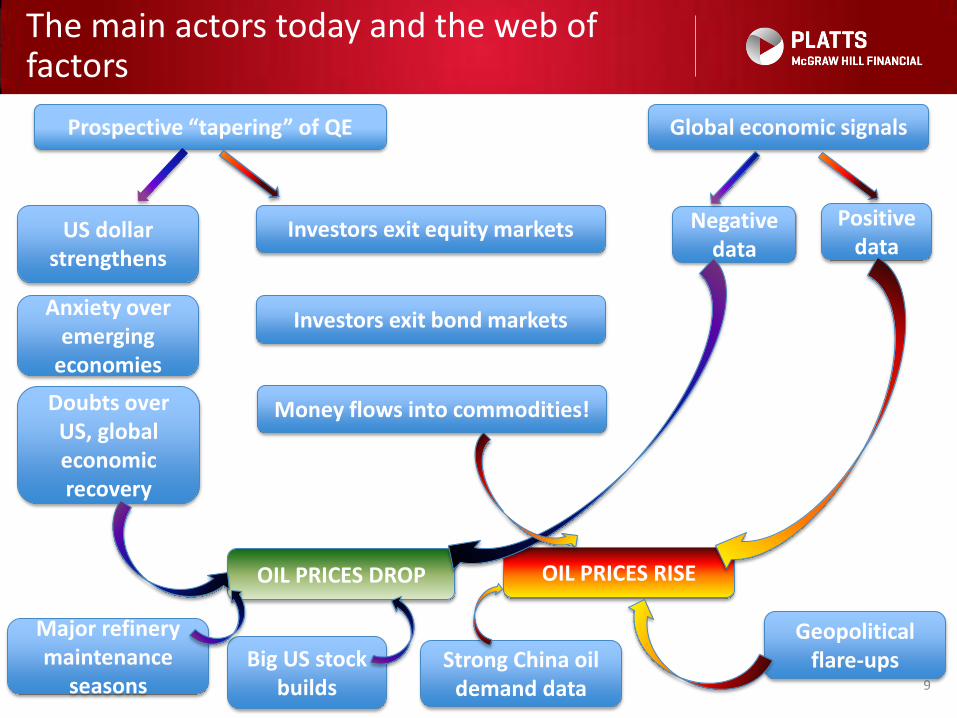

The main actors today and the web of factors

9

Prospective “tapering” of QE

US dollar strengthens

OIL PRICES DROP

Anxiety over emerging

economies

Doubts over US, global economic recovery

Investors exit equity markets

Money flows into commodities!

OIL PRICES RISE

Investors exit bond markets

Global economic signals

Negative data

Positive data

Geopolitical flare-ups Strong China oil

demand data

Major refinery maintenance

seasons Big US stock

builds

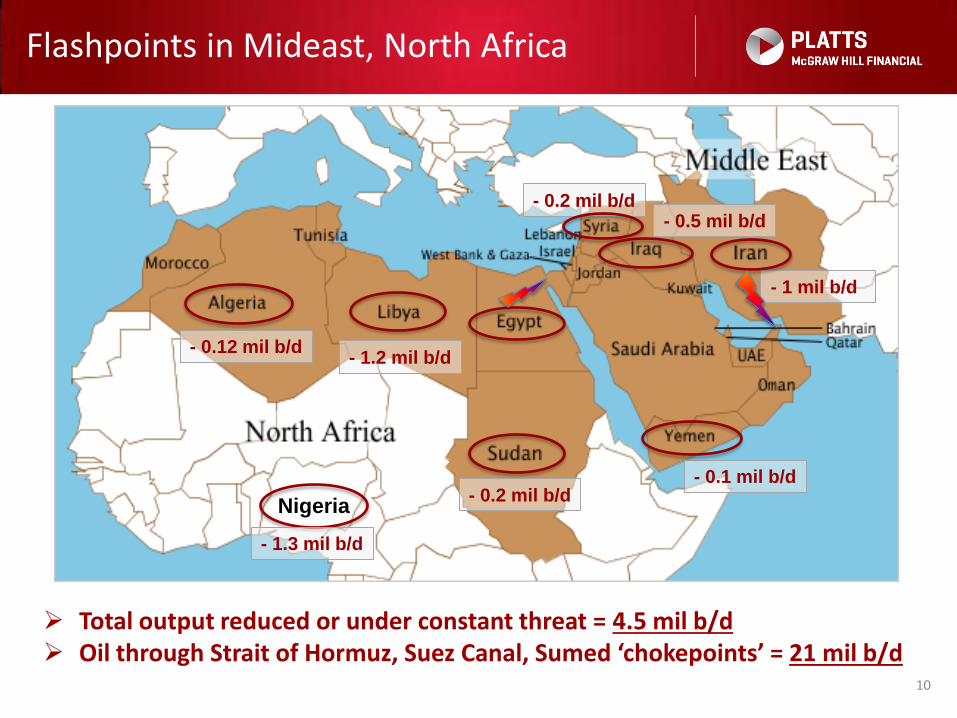

Flashpoints in Mideast, North Africa

10

- 1.2 mil b/d

- 1 mil b/d

- 0.5 mil b/d

- 0.2 mil b/d - 0.1 mil b/d

- 0.2 mil b/d

- 0.12 mil b/d

Nigeria

- 1.3 mil b/d

Total output reduced or under constant threat = 4.5 mil b/d Oil through Strait of Hormuz, Suez Canal, Sumed ‘chokepoints’ = 21 mil b/d

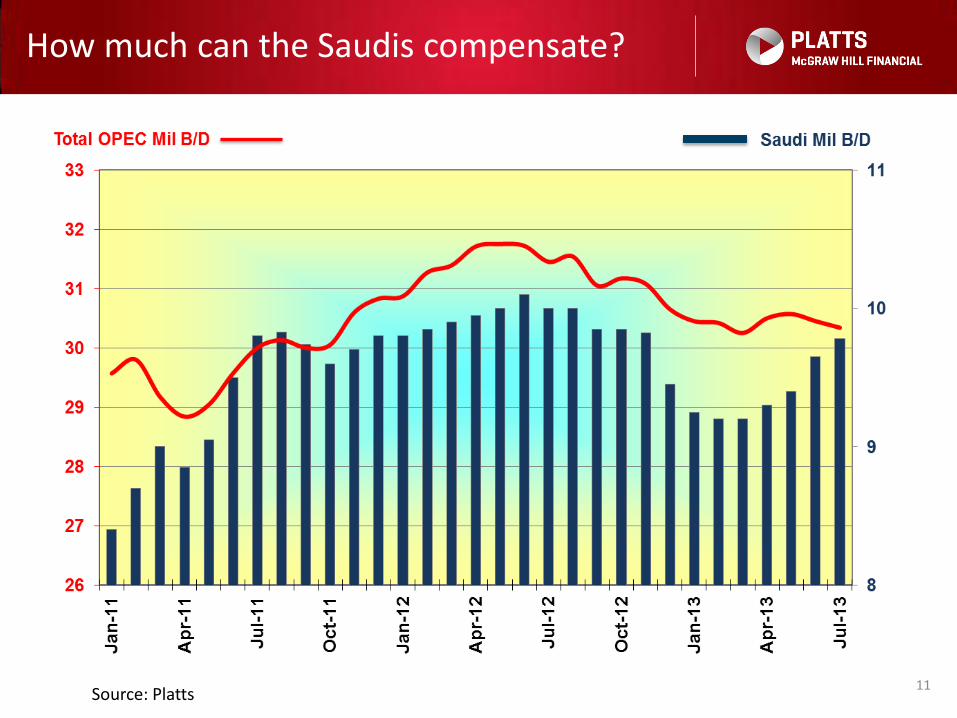

How much can the Saudis compensate?

11 Source: Platts

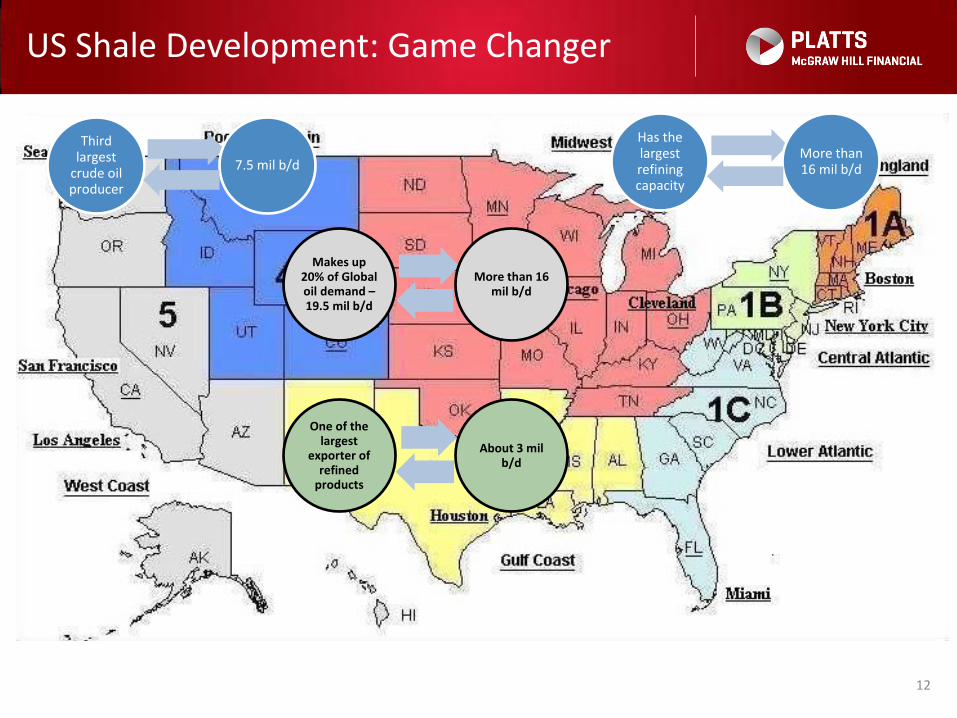

US Shale Development: Game Changer

12

Third largest

crude oil producer

7.5 mil b/d

Has the largest refining capacity

More than 16 mil b/d

Makes up 20% of Global oil demand – 19.5 mil b/d

More than 16 mil b/d

One of the largest

exporter of refined

products

About 3 mil b/d

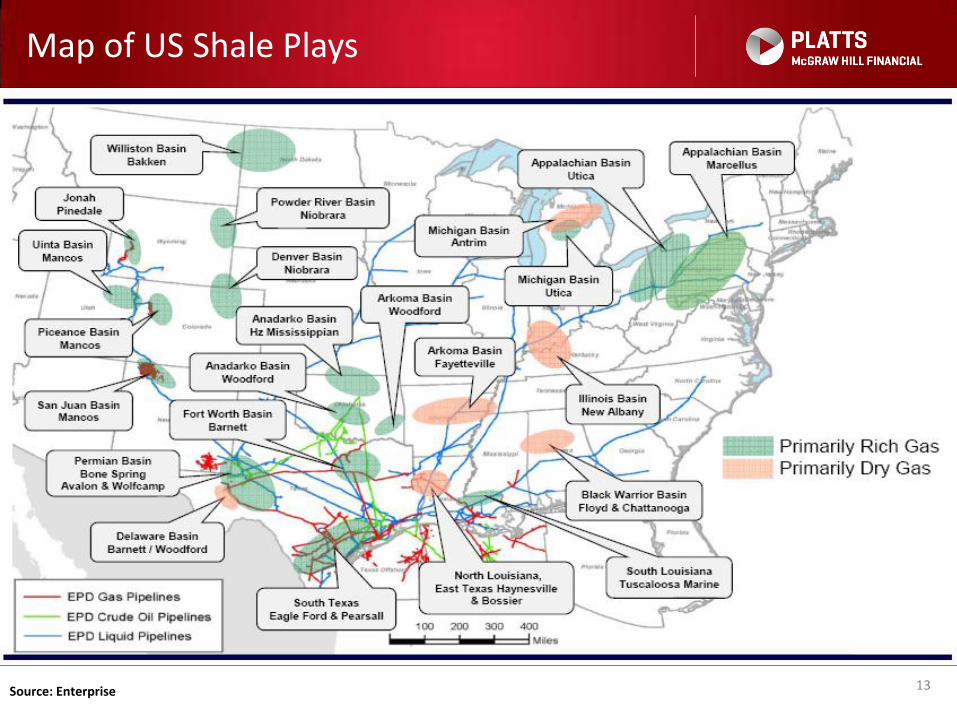

Map of US Shale Plays

13 Source: Enterprise

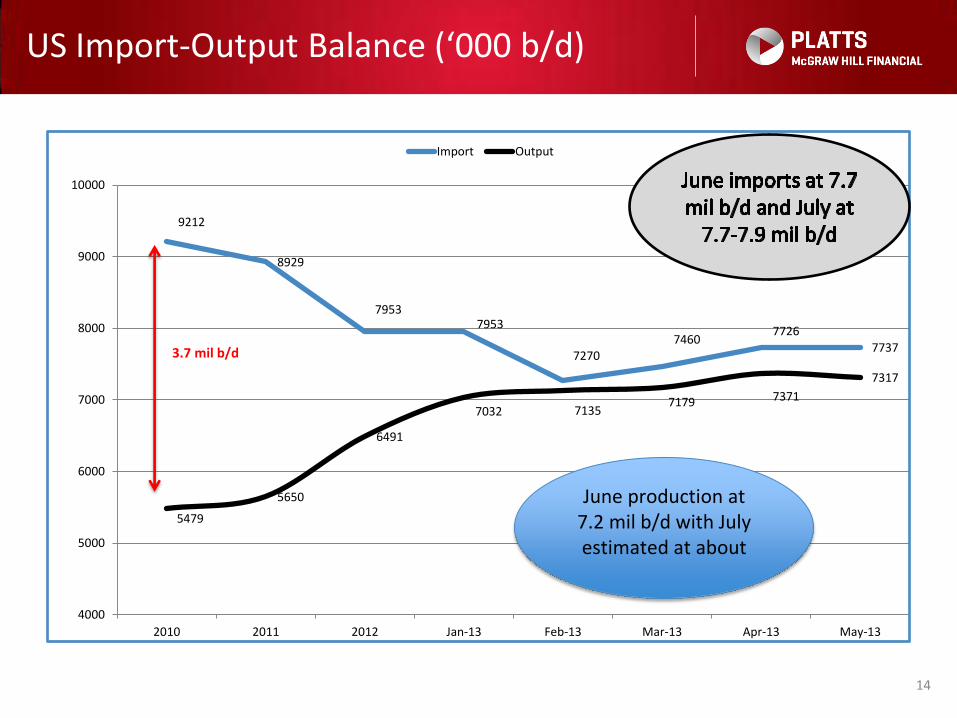

US Import-Output Balance (‘000 b/d)

14

9212

8929

7953 7953

7270 7460

7726 7737

5479

5650

6491

7032 7135 7179 7371

7317

4000

5000

6000

7000

8000

9000

10000

2010 2011 2012 Jan-13 Feb-13 Mar-13 Apr-13 May-13

Import Output

3.7 mil b/d

June production at 7.2 mil b/d with July estimated at about

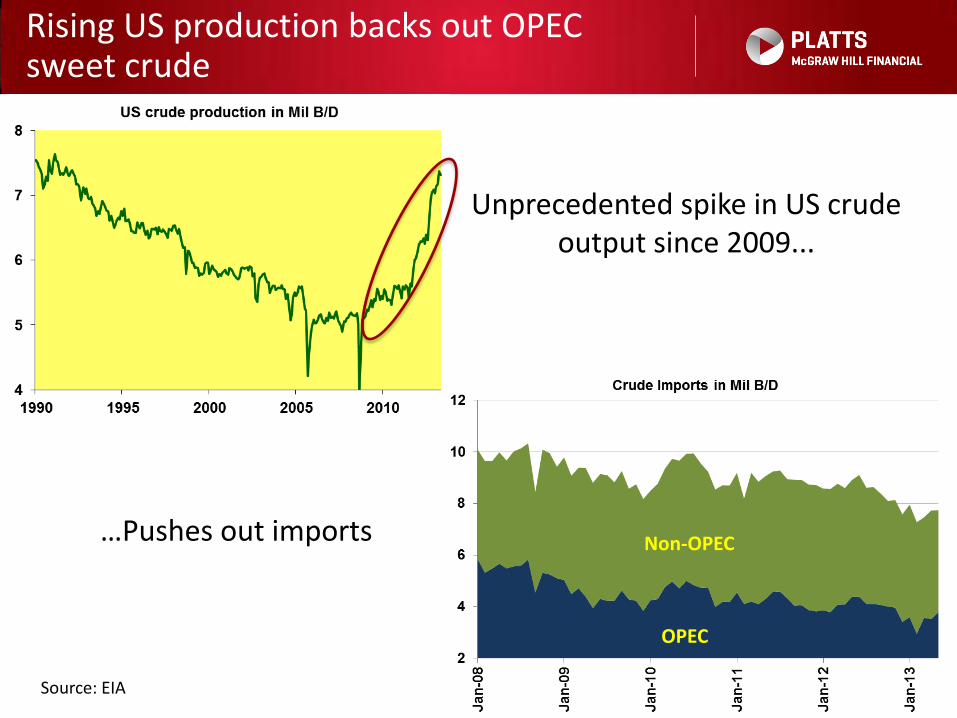

Rising US production backs out OPEC sweet crude

15

Unprecedented spike in US crude output since 2009...

…Pushes out imports

OPEC

Non-OPEC

Source: EIA

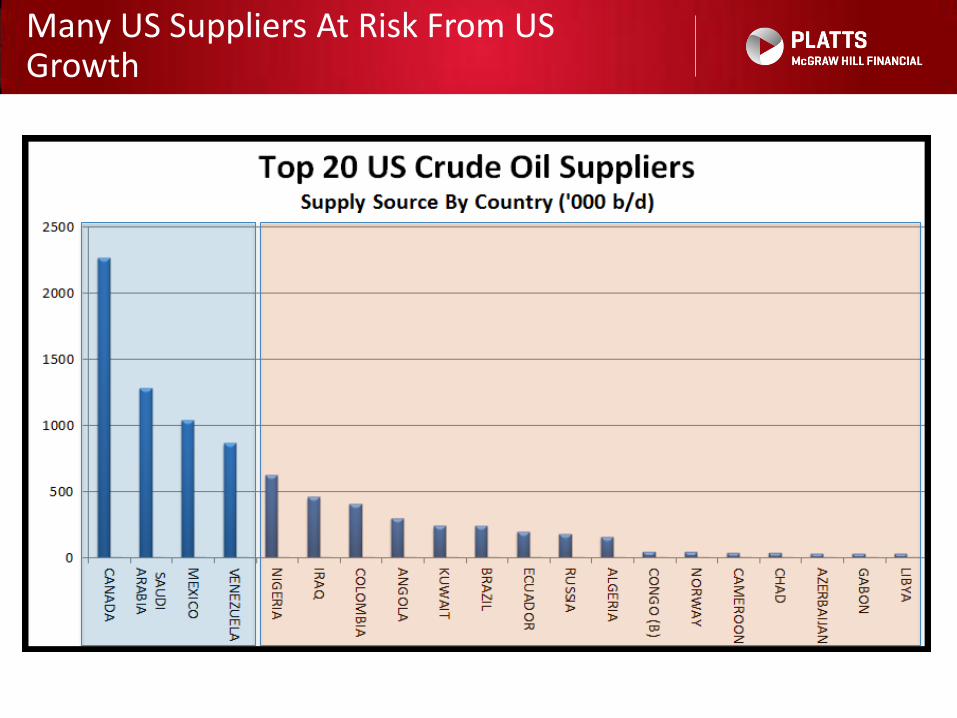

Many US Suppliers At Risk From US Growth

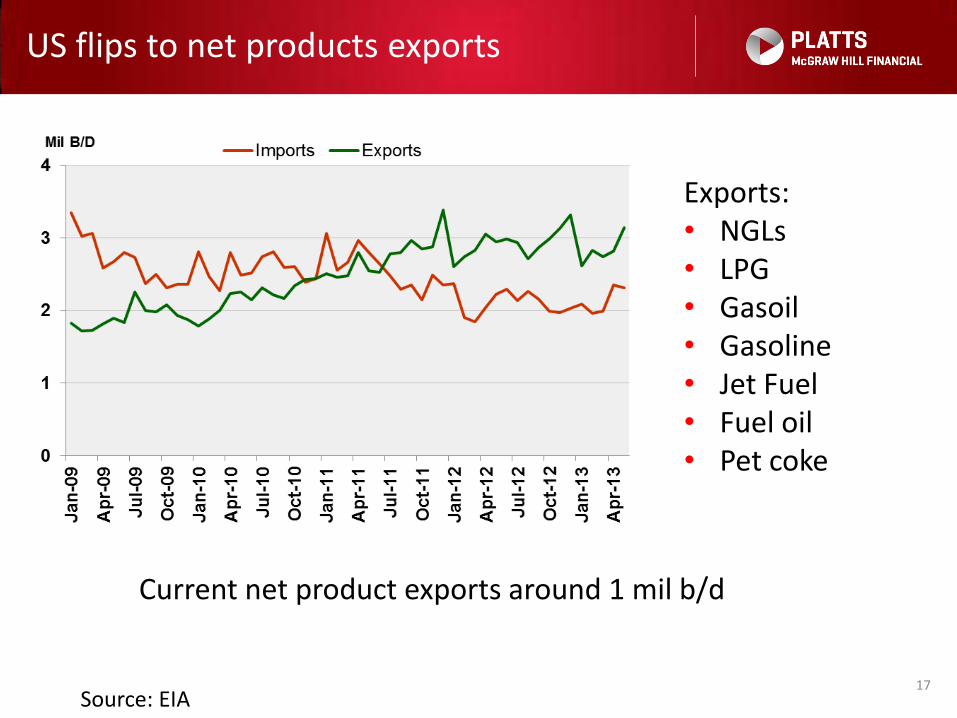

US flips to net products exports

17

Current net product exports around 1 mil b/d

Exports: • NGLs • LPG • Gasoil • Gasoline • Jet Fuel • Fuel oil • Pet coke

Source: EIA

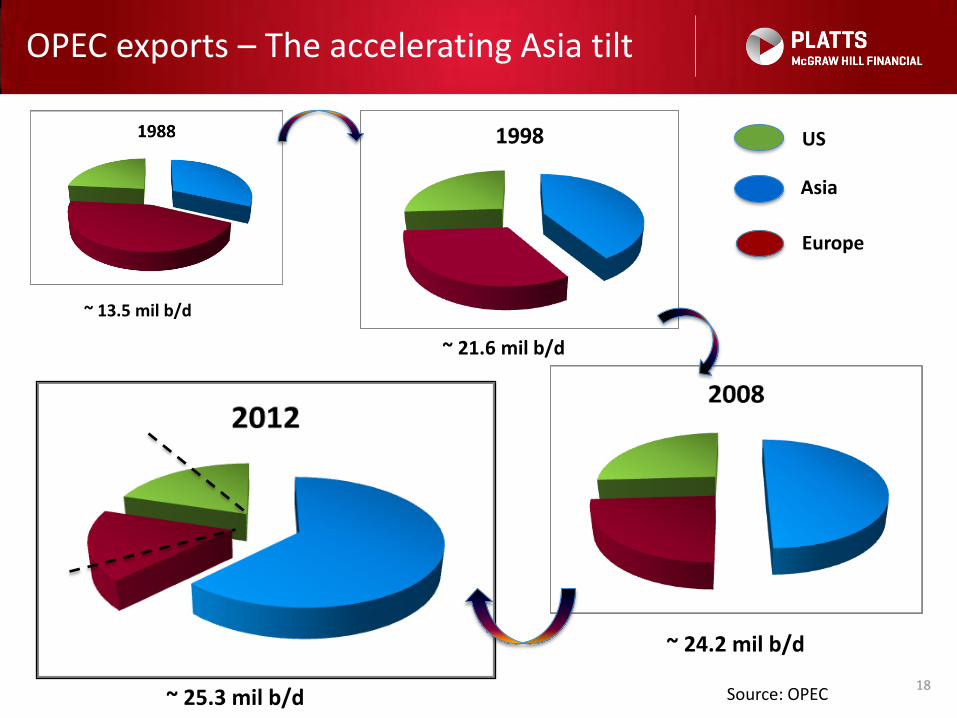

OPEC exports – The accelerating Asia tilt

18

US

Asia

Europe

~ 13.5 mil b/d

~ 21.6 mil b/d

~ 24.2 mil b/d

~ 25.3 mil b/d Source: OPEC

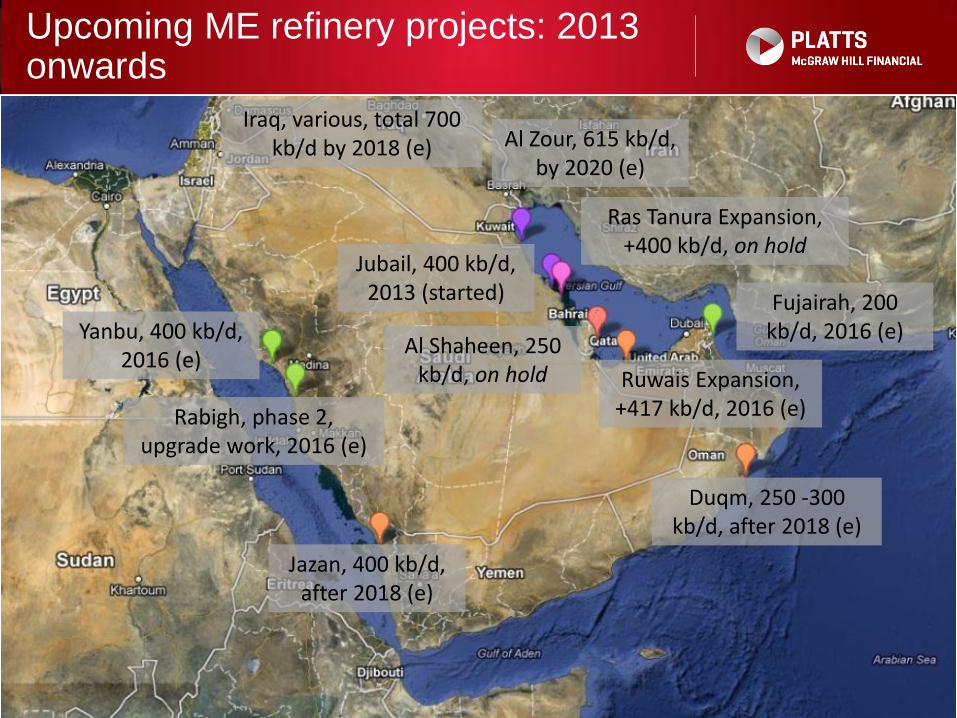

Upcoming ME refinery projects: 2013 onwards

19

19

Yanbu, 400 kb/d, 2016 (e)

Rabigh, phase 2, upgrade work, 2016 (e)

Jazan, 400 kb/d, after 2018 (e)

Duqm, 250 -300 kb/d, after 2018 (e)

Fujairah, 200 kb/d, 2016 (e)

Ruwais Expansion, +417 kb/d, 2016 (e)

Al Shaheen, 250 kb/d, on hold

Jubail, 400 kb/d, 2013 (started)

Ras Tanura Expansion, +400 kb/d, on hold

Al Zour, 615 kb/d, by 2020 (e)

Iraq, various, total 700 kb/d by 2018 (e)

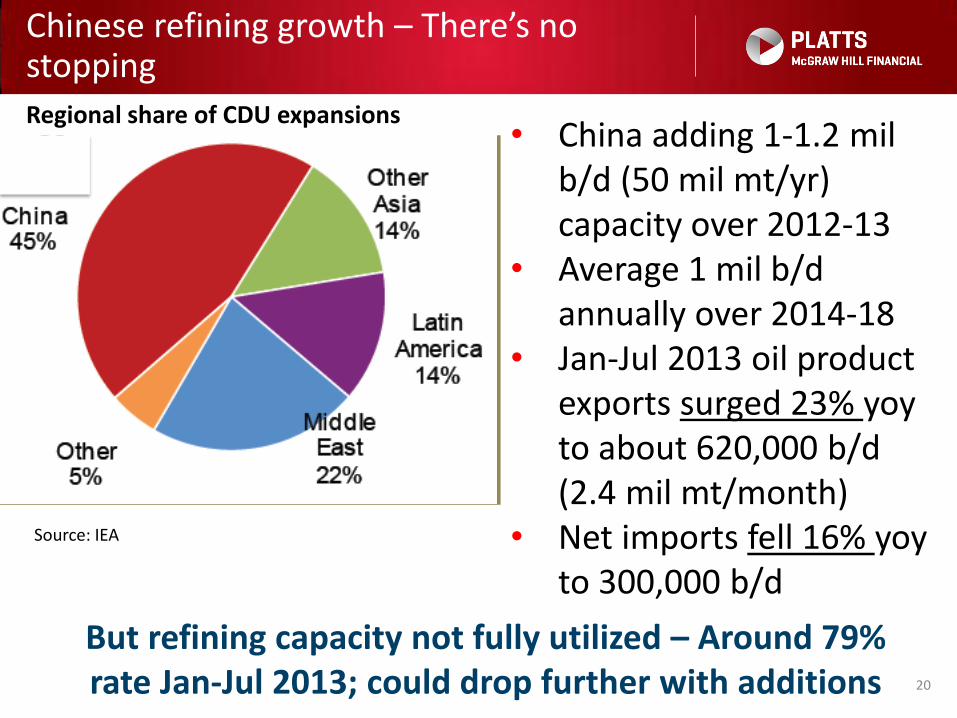

Chinese refining growth – There’s no stopping

20

Regional share of CDU expansions • China adding 1-1.2 mil

b/d (50 mil mt/yr) capacity over 2012-13

• Average 1 mil b/d annually over 2014-18

• Jan-Jul 2013 oil product exports surged 23% yoy to about 620,000 b/d (2.4 mil mt/month)

• Net imports fell 16% yoy to 300,000 b/d

But refining capacity not fully utilized – Around 79% rate Jan-Jul 2013; could drop further with additions

Source: IEA

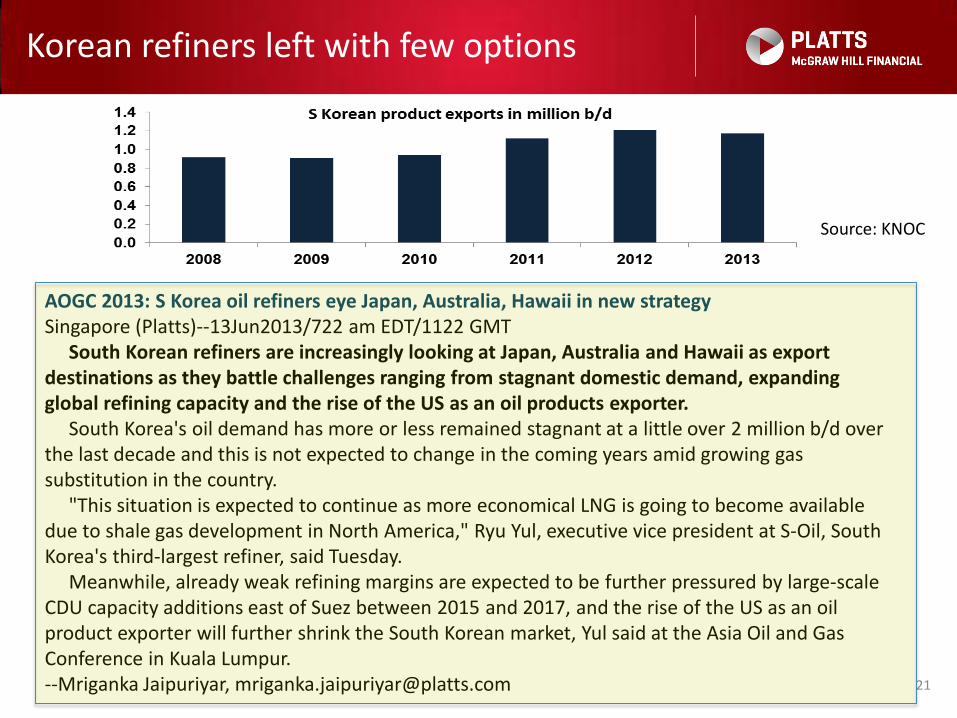

Korean refiners left with few options

21

AOGC 2013: S Korea oil refiners eye Japan, Australia, Hawaii in new strategy Singapore (Platts)--13Jun2013/722 am EDT/1122 GMT South Korean refiners are increasingly looking at Japan, Australia and Hawaii as export destinations as they battle challenges ranging from stagnant domestic demand, expanding global refining capacity and the rise of the US as an oil products exporter. South Korea's oil demand has more or less remained stagnant at a little over 2 million b/d over the last decade and this is not expected to change in the coming years amid growing gas substitution in the country. "This situation is expected to continue as more economical LNG is going to become available due to shale gas development in North America," Ryu Yul, executive vice president at S-Oil, South Korea's third-largest refiner, said Tuesday. Meanwhile, already weak refining margins are expected to be further pressured by large-scale CDU capacity additions east of Suez between 2015 and 2017, and the rise of the US as an oil product exporter will further shrink the South Korean market, Yul said at the Asia Oil and Gas Conference in Kuala Lumpur. --Mriganka Jaipuriyar, [email protected]

Source: KNOC

Indian refined product exports steady – so far

• Indian private sector oil product exports averaged just over 4 mil mt/month (about 1 mil b/d) Jan-Jul 2013, flat from 2012 despite rise in Essar capacity – Exports comprise nearly 60% diesel, 15% gasoline

• Another 1.3-1.5 mil mt/month from PSU refiners – Predominantly naphtha and fuel oil

• Around 27.5 mil mt/year (553,000 b/d) capacity addition over 2011-2013

• Plans and projects to add another 36.7 mil mt/year (734,000 b/d) over 2014-2016

22

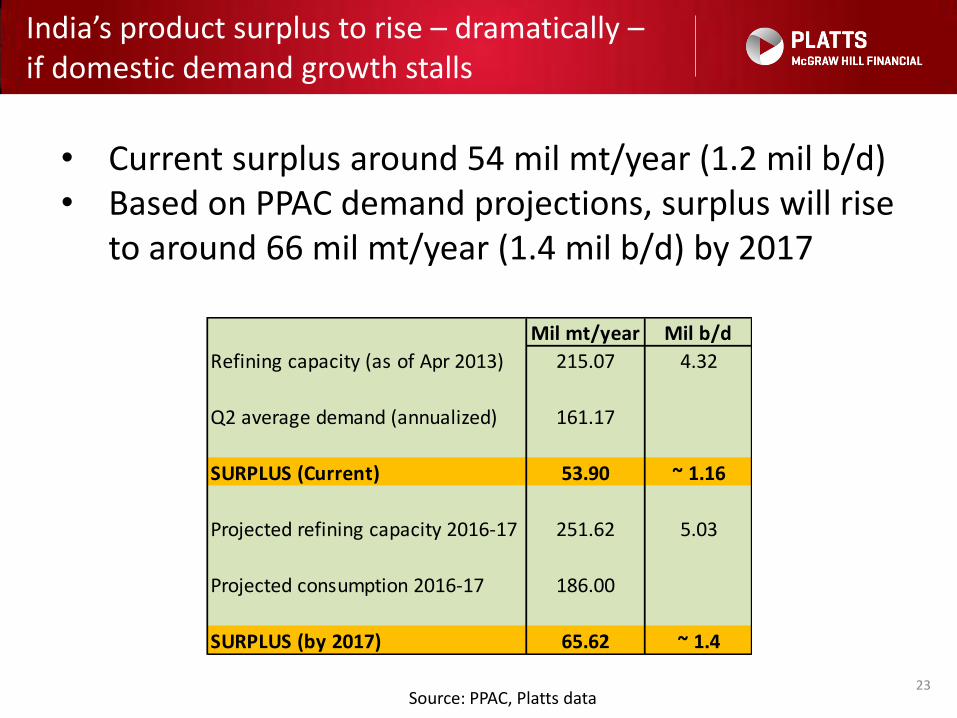

India’s product surplus to rise – dramatically – if domestic demand growth stalls

23

• Current surplus around 54 mil mt/year (1.2 mil b/d) • Based on PPAC demand projections, surplus will rise

to around 66 mil mt/year (1.4 mil b/d) by 2017

Source: PPAC, Platts data

Mil mt/year Mil b/d

Refining capacity (as of Apr 2013) 215.07 4.32

Q2 average demand (annualized) 161.17

SURPLUS (Current) 53.90 ~ 1.16

Projected refining capacity 2016-17 251.62 5.03

Projected consumption 2016-17 186.00

SURPLUS (by 2017) 65.62 ~ 1.4

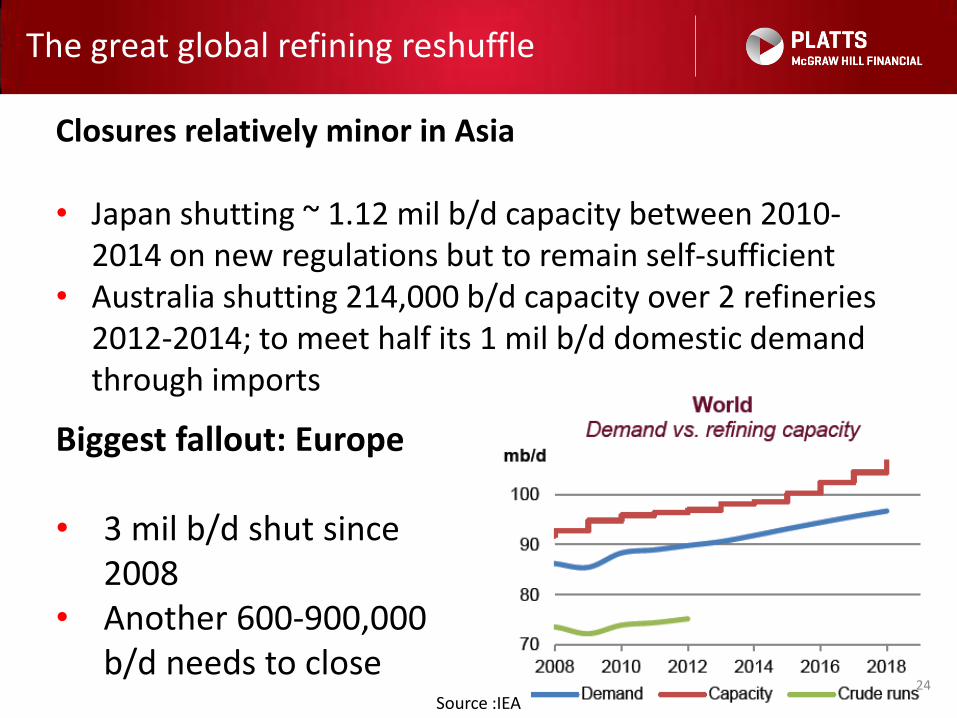

The great global refining reshuffle

24

Closures relatively minor in Asia • Japan shutting ~ 1.12 mil b/d capacity between 2010-

2014 on new regulations but to remain self-sufficient • Australia shutting 214,000 b/d capacity over 2 refineries

2012-2014; to meet half its 1 mil b/d domestic demand through imports

Biggest fallout: Europe • 3 mil b/d shut since

2008 • Another 600-900,000

b/d needs to close Source :IEA

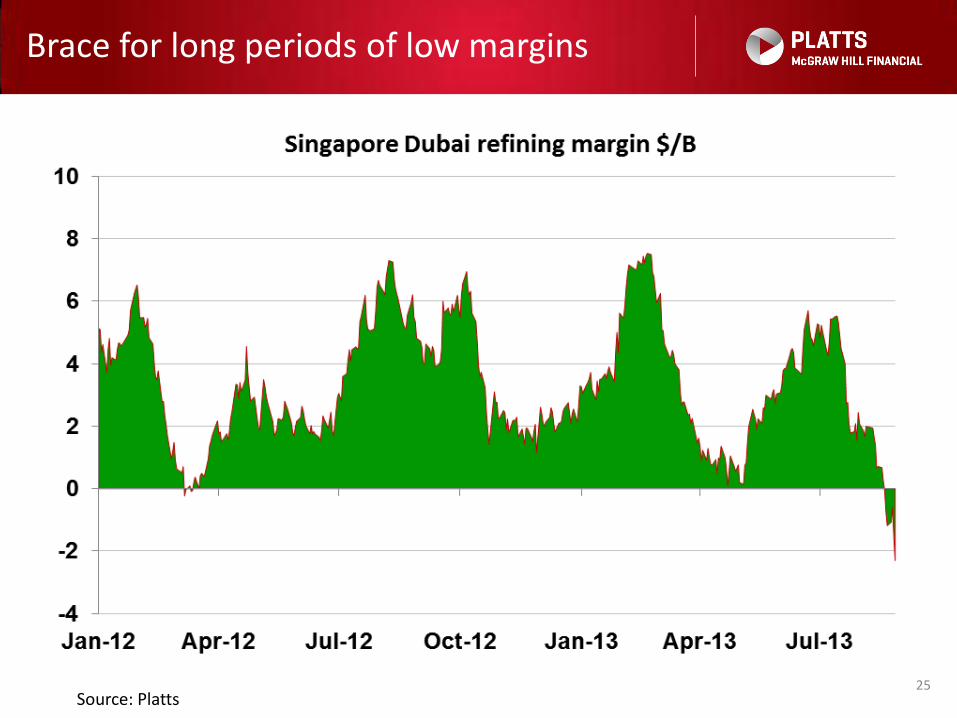

Brace for long periods of low margins

25 Source: Platts

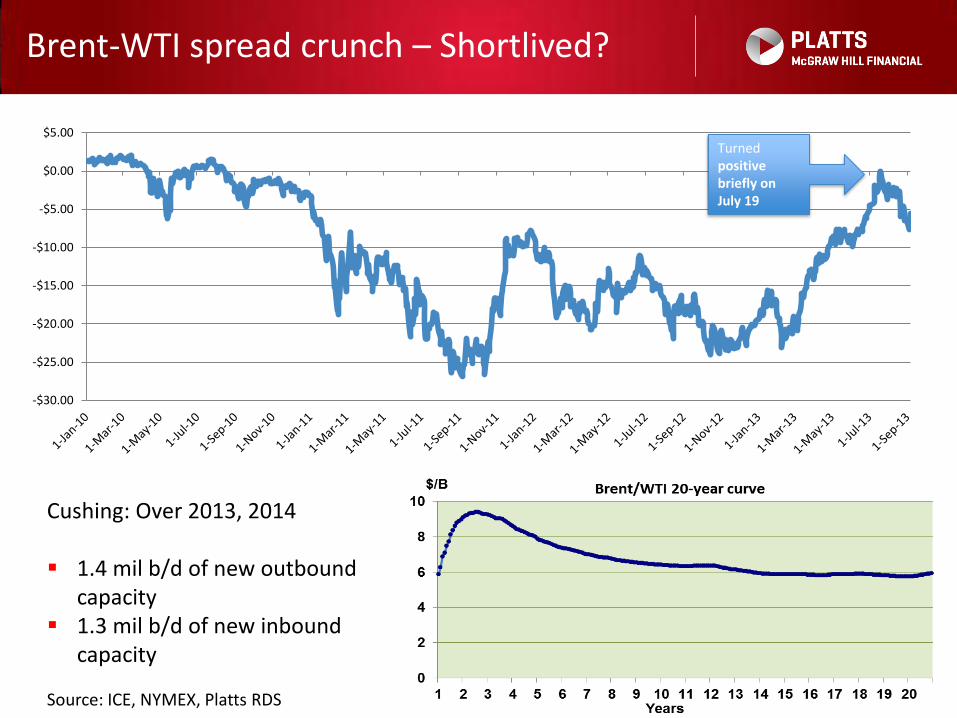

Brent-WTI spread crunch – Shortlived?

26 Source: ICE, NYMEX, Platts RDS

Cushing: Over 2013, 2014 1.4 mil b/d of new outbound

capacity 1.3 mil b/d of new inbound

capacity

-$30.00

-$25.00

-$20.00

-$15.00

-$10.00

-$5.00

$0.00

$5.00Turned positive briefly on July 19

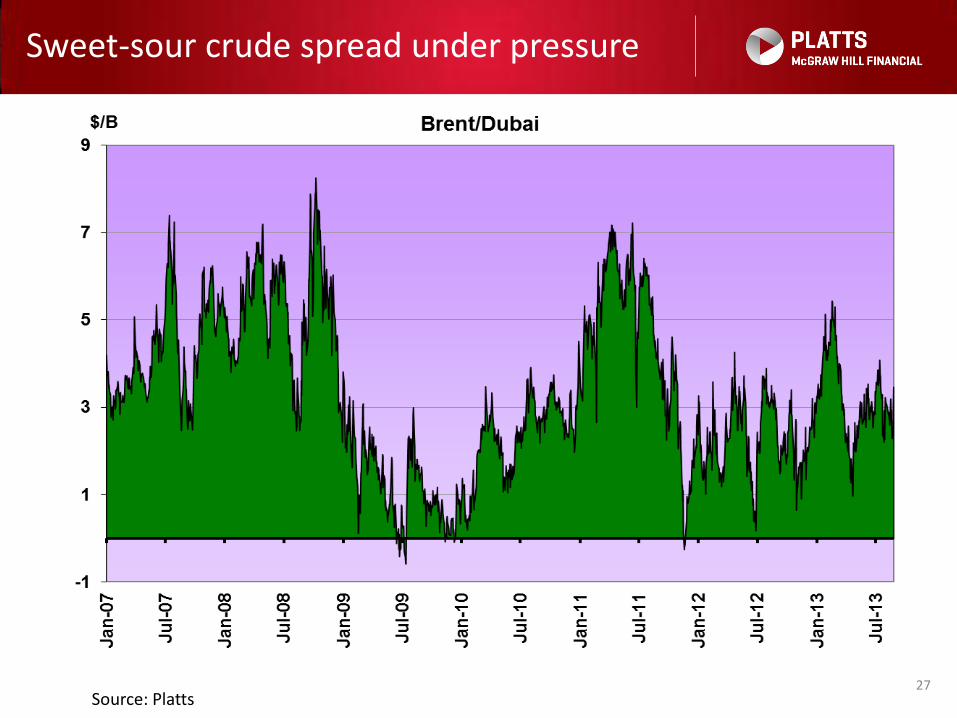

Sweet-sour crude spread under pressure

27 Source: Platts