omnia at a glance financial overview

TRANSCRIPT

Agriculture overview Mining overview

Chemicals overview Prospects

Omnia at a glance

Financial overview

AGENDA

Page 2

OMNIA AT A GLANCE

Page 3

AGRICULTUREOmnia’s Agriculture division comprises Omnia Fertilizer and Omnia Specialities

MININGOmnia’s Mining division services the mining industry through BME and Protea Mining Chemicals

CHEMICALSThe Chemicals division’s main business is through ProteaChemicals

Vision‘Creating customer wealth by leveraging knowledge’

Strategy• Providing specialised solutions to the agriculture, mining and chemicals markets• Focusing on unique market offerings that create value and, in so doing, earn a premium• Diversifying geographically beyond South Africa, primarily focused on Africa with a growing

presence in other international countries• Identifying and implementing strategic acquisitions to build on the strengths of each division• Improving on cost competitiveness across all divisions, particularly in the Chemicals division• Continuously improving on health, safety and environmental practices by following the guiding principles

of Responsible Care®

• Building a culturally diverse business that respects and promotes the rights of its people• Building a learning organisation• Leverage our intellectual property, systems and technology to create value for customers and shareholders

OUR VISION AND STRATEGY

Page 4

• We differentiate ourselves from othercommodity chemical suppliers by applyingour intellectual capital and technologies toall key points along our supply andservice chains

• This enables Omnia to create valuethroughout by tailoring our products andservices to the specific and changingneeds of our customers

• Our business model has been tried andtested over many years, and continues tobe fine-tuned as our markets andcustomers evolve

OUR VALUE PROPOSITION

Page 5

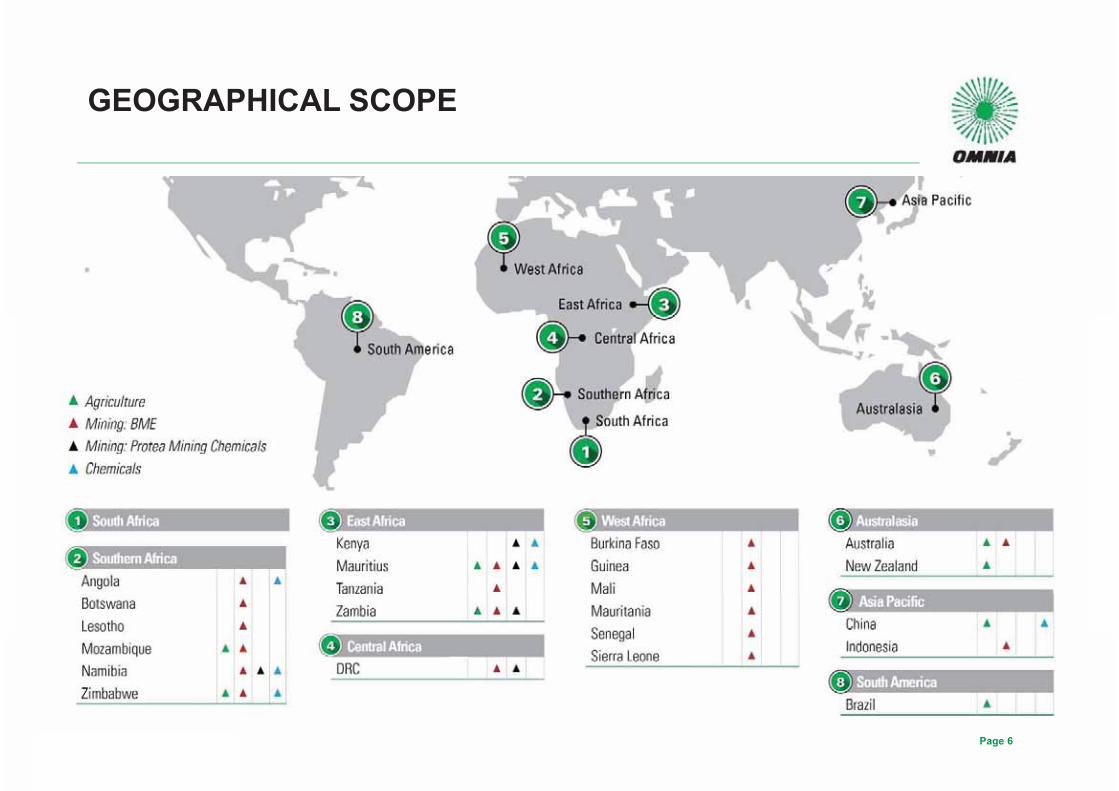

GEOGRAPHICAL SCOPE

Page 6

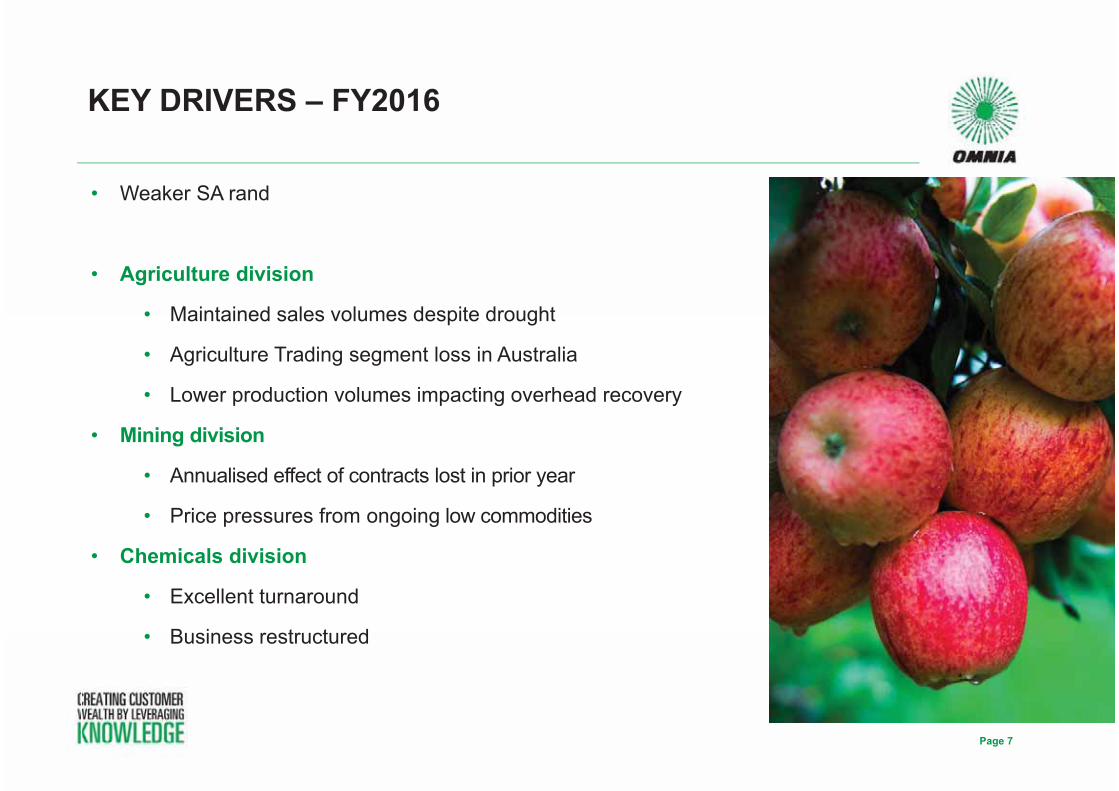

• Weaker SA rand

• Agriculture division

• Maintained sales volumes despite drought

• Agriculture Trading segment loss in Australia

• Lower production volumes impacting overhead recovery

• Mining division

• Annualised effect of contracts lost in prior year

• Price pressures from ongoing low commodities

• Chemicals division

• Excellent turnaround

• Business restructured

KEY DRIVERS – FY2016

Page 7

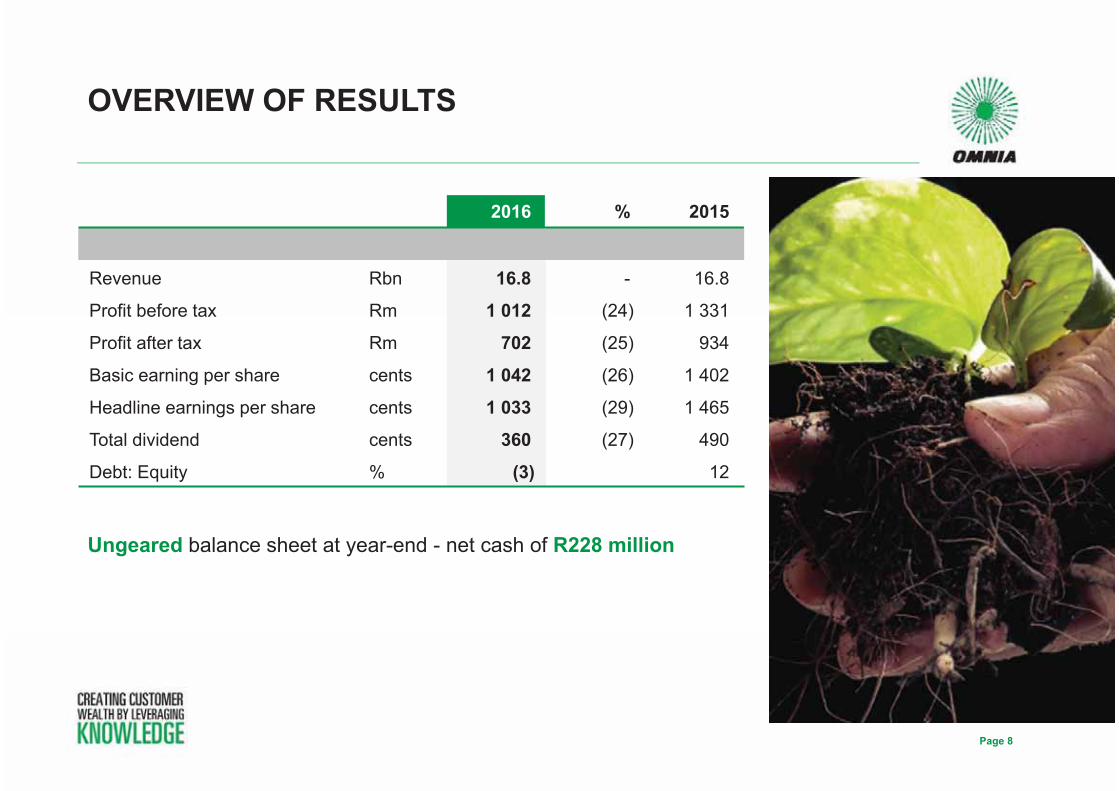

OVERVIEW OF RESULTS

Page 8

2016 % 2015

Revenue Rbn 16.8 - 16.8

Profit before tax Rm 1 012 (24) 1 331

Profit after tax Rm 702 (25) 934

Basic earning per share cents 1 042 (26) 1 402

Headline earnings per share cents 1 033 (29) 1 465

Total dividend cents 360 (27) 490

Debt: Equity % (3) 12

Ungeared balance sheet at year-end - net cash of R228 million

• Revenue remained flat at R16.8 billion

• Operating profit down 19% to R1 189 million

• Profit after tax of R702 million down 25%

• Cash generated from operations increased to R2.3 billion,up R1.3 billion year-on-year

• Headline earnings per share down 29% to 1 033 cents per share

• Credit rating affirmed in July 2015 as A- (long-term) and A1- (short-term), with a positive ratings outlook

• Safety - recordable case rate of 0.83 - below target of 1.0

OTHER KEY FEATURES

Page 9

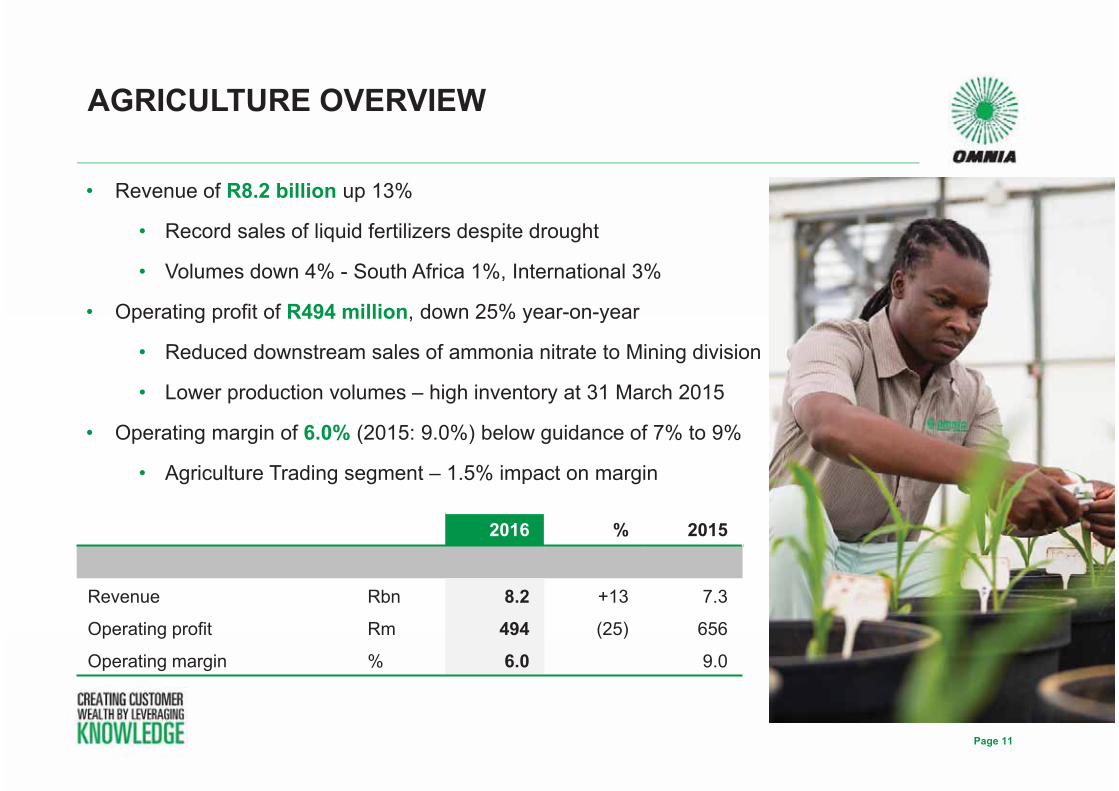

AGRICULTURE OVERVIEW

• Revenue of R8.2 billion up 13%

• Record sales of liquid fertilizers despite drought

• Volumes down 4% - South Africa 1%, International 3%

• Operating profit of R494 million, down 25% year-on-year

• Reduced downstream sales of ammonia nitrate to Mining division

• Lower production volumes – high inventory at 31 March 2015

• Operating margin of 6.0% (2015: 9.0%) below guidance of 7% to 9%

• Agriculture Trading segment – 1.5% impact on margin

AGRICULTURE OVERVIEW

Page 11

2016 % 2015

Revenue Rbn 8.2 +13 7.3

Operating profit Rm 494 (25) 656

Operating margin % 6.0 9.0

$ 0

$ 100

$ 200

$ 300

$ 400

$ 500

$ 600

$ 700

$ 0

$ 50

$ 100

$ 150

$ 200

$ 250

$ 300

$ 350

$ 400

Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015 Mar 2016

Soya

Mai

ze a

nd W

heat

Maize Wheat Soya

-5.7%-8.8%-5.7%

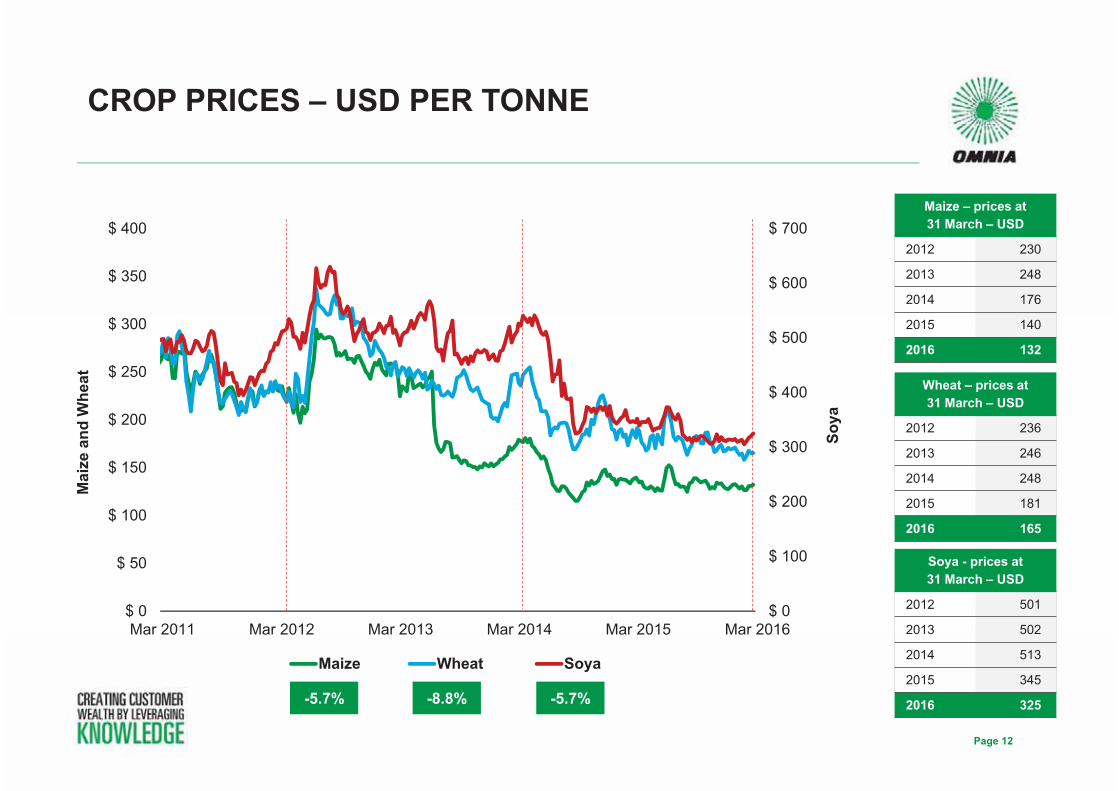

CROP PRICES – USD PER TONNE

Page 12

Maize – prices at 31 March – USD

2012 230

2013 248

2014 176

2015 140

2016 132

Wheat – prices at 31 March – USD

2012 236

2013 246

2014 248

2015 181

2016 165

Soya - prices at 31 March – USD

2012 501

2013 502

2014 513

2015 345

2016 325

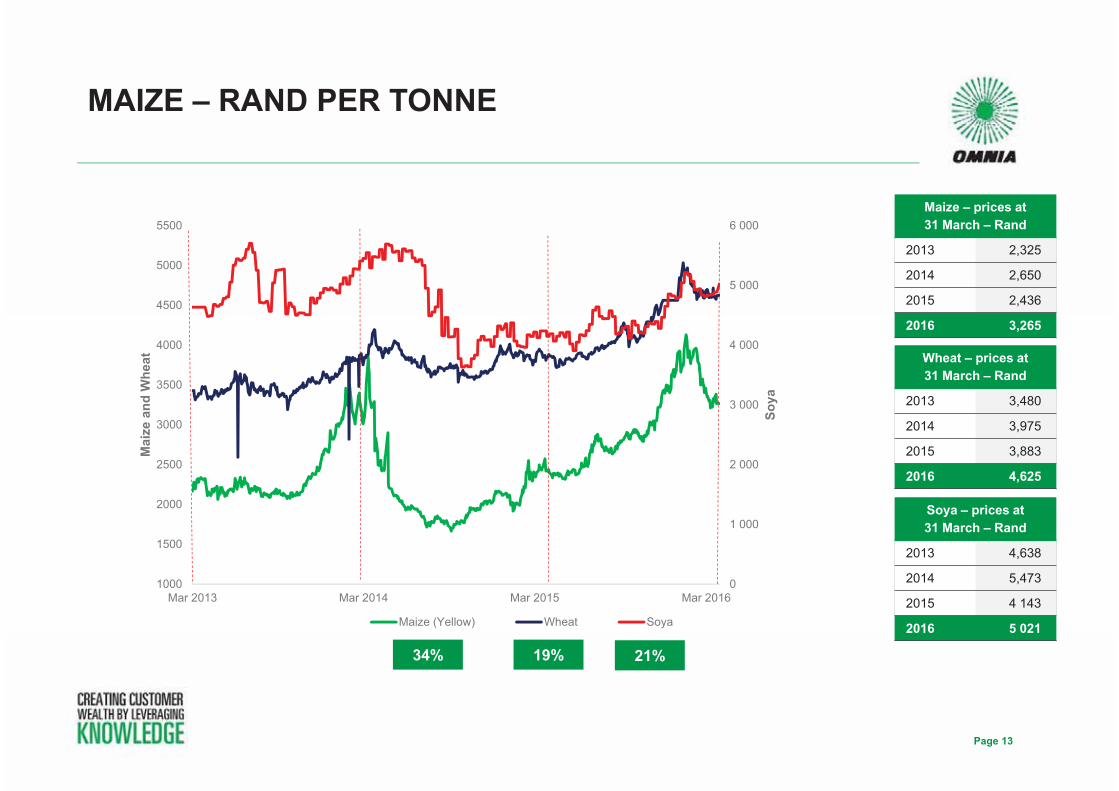

MAIZE – RAND PER TONNE

Page 13

19%

Maize – prices at 31 March – Rand

2013 2,325

2014 2,650

2015 2,436

2016 3,265

Wheat – prices at 31 March – Rand

2013 3,480

2014 3,975

2015 3,883

2016 4,625

Soya – prices at 31 March – Rand

2013 4,638

2014 5,473

2015 4 143

2016 5 021

21%34%

0

1 000

2 000

3 000

4 000

5 000

6 000

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

Mar 2013 Mar 2014 Mar 2015 Mar 2016

Soya

Mai

ze a

nd W

heat

Maize (Yellow) Wheat Soya

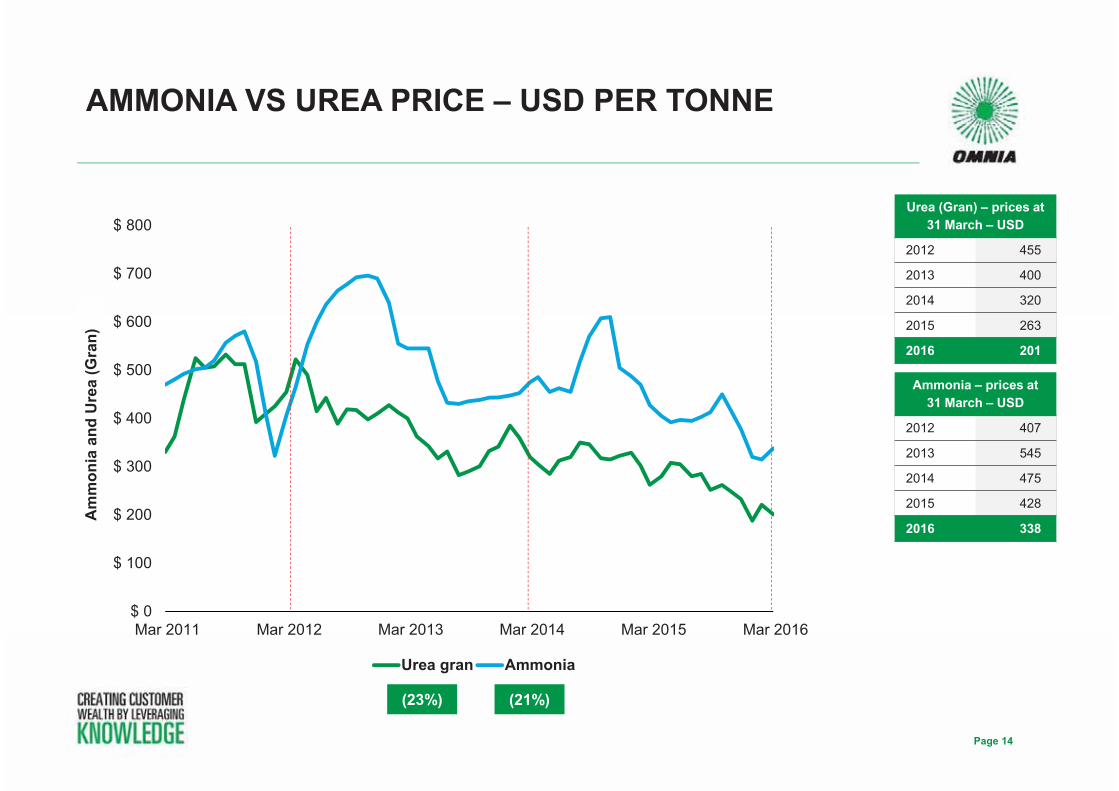

AMMONIA VS UREA PRICE – USD PER TONNE

Page 14

$ 0

$ 100

$ 200

$ 300

$ 400

$ 500

$ 600

$ 700

$ 800

Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015 Mar 2016

Urea gran Ammonia

Urea (Gran) – prices at 31 March – USD

2012 455

2013 400

2014 320

2015 263

2016 201

Ammonia – prices at 31 March – USD

2012 407

2013 545

2014 475

2015 428

2016 338

(23%) (21%)

Am

mon

ia a

nd U

rea

(Gra

n)

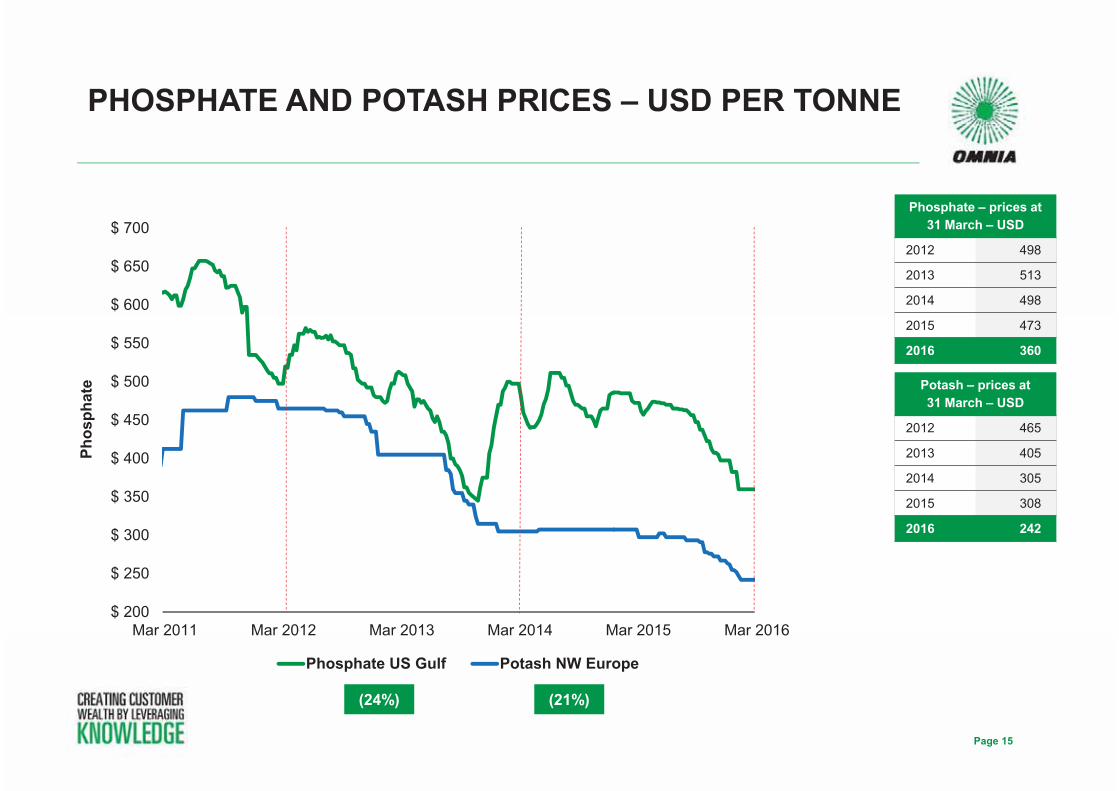

PHOSPHATE AND POTASH PRICES – USD PER TONNE

Page 15

$ 200

$ 250

$ 300

$ 350

$ 400

$ 450

$ 500

$ 550

$ 600

$ 650

$ 700

Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015 Mar 2016

Phos

phat

e

Phosphate US Gulf Potash NW Europe

(24%) (21%)

Phosphate – prices at 31 March – USD

2012 498

2013 513

2014 498

2015 473

2016 360

Potash – prices at 31 March – USD

2012 465

2013 405

2014 305

2015 308

2016 242

SOUTH AFRICA RAINFALL

Page 16

Approximate mm rainfall per year

2009 620

2010 620

2011 660

2012 590

2013 580

2014 570

2015 403

SOUTH AFRICA RAINFALL: 403 MM IN 2015

Page 17

Annual total rain <500 mm per annum

Year mm

2015 403

1945 437

1992 440

2003 446

1935 451

1919 451

1965 452

1926 468

1916 476

1927 488

1912 493

1982 496

1941 496

13 years when the total rainfall for South Africa was less than 500 mm per annum

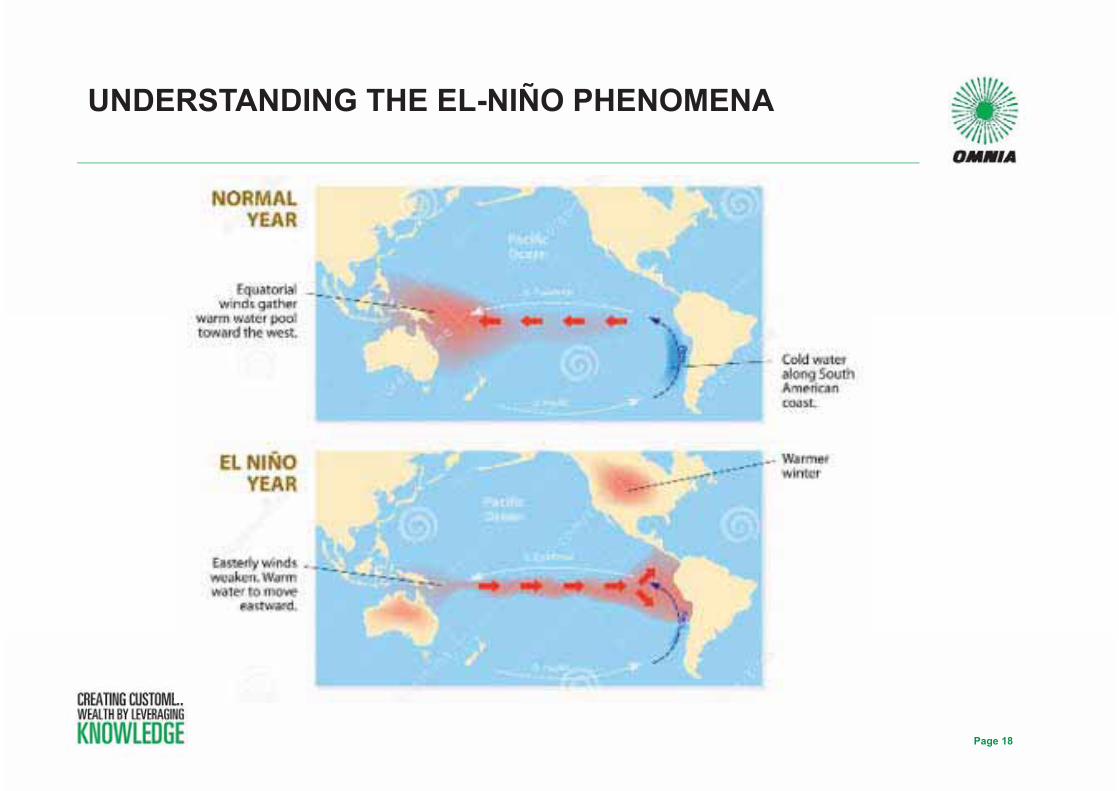

UNDERSTANDING THE EL-NIÑO PHENOMENA

Page 18

RSA - COMMERCIAL MAIZE PRODUCTION

Page 19

0

2

4

6

8

10

12

14

16

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

�200

0/01

�200

1/02

�200

2/03

�200

3/04

�200

4/05

�200

5/06

�200

6/07

�200

7/08

�200

8/09

�200

9/10

�201

0/11

�201

1/12

�201

2/13

�201

3/14

�201

4/15

2015

/16

Tons�produ

ced�(m

illions)

Production�year

El�Niño Neutral La�Niña

• El-Niño has a variable effect on crop production – currently dissipating• Start of La-Niña conditions predicted for 2016/2017

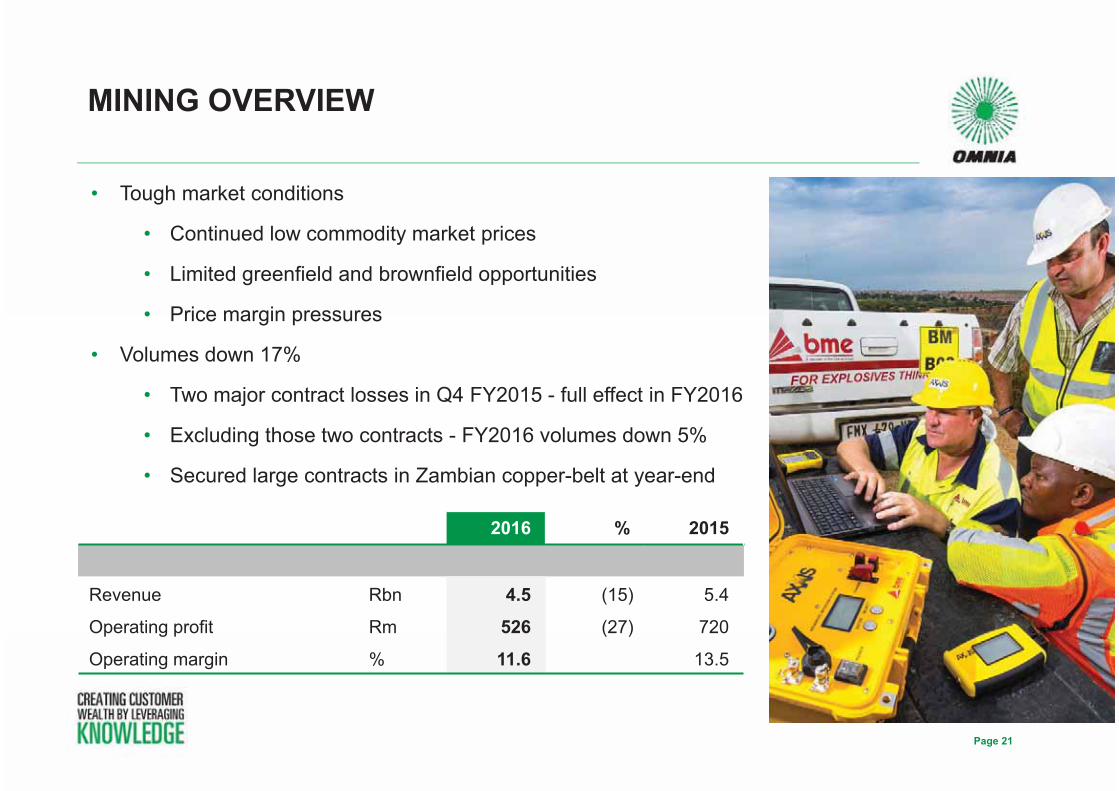

MINING OVERVIEW

• Tough market conditions

• Continued low commodity market prices

• Limited greenfield and brownfield opportunities

• Price margin pressures

• Volumes down 17%

• Two major contract losses in Q4 FY2015 - full effect in FY2016

• Excluding those two contracts - FY2016 volumes down 5%

• Secured large contracts in Zambian copper-belt at year-end

MINING OVERVIEW

Page 21

2016 % 2015

Revenue Rbn 4.5 (15) 5.4

Operating profit Rm 526 (27) 720

Operating margin % 11.6 13.5

• BME – Axxis ®

• World record blast in Australia - 5 665 electronic delay detonators

• New markets – high tech precision blasting in built-up area (Singapore mass rapid transport rail system)

• BME – Emulsion application systems• Gaining acceptance in underground markets• Alternative delivery options under development

• Protea Mining Chemicals• Introduction of new mining chemicals products in southern

African markets• Implementation of a long distance Sulphuric acid logistic

solution in Namibia

MINING OVERVIEW

Page 22

Page 23

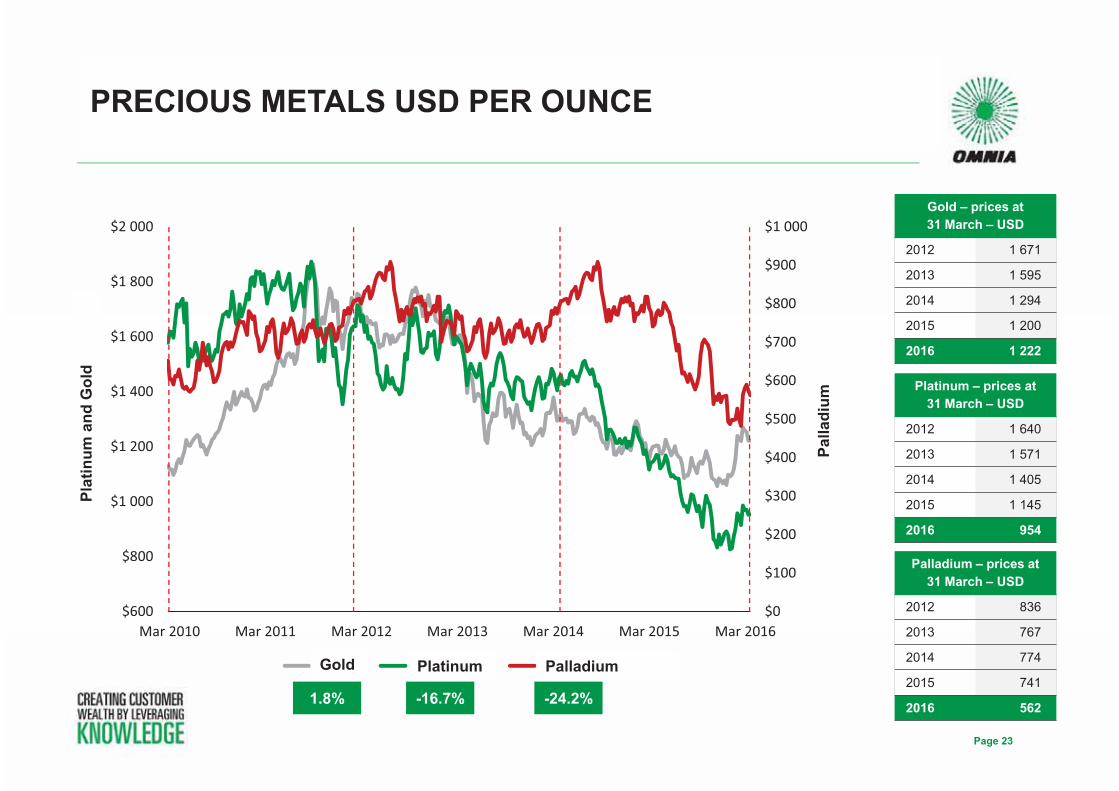

PRECIOUS METALS USD PER OUNCE

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1�000

$600

$800

$1�000

$1�200

$1�400

$1�600

$1�800

$2�000

�Mar�2010 �Mar�2011 �Mar�2012 �Mar�2013 �Mar�2014 �Mar�2015 �Mar�2016

Palladium

Platinum

�and

�Gold

GOLD PLATINUM PALLADIUM

Gold – prices at 31 March – USD

2012 1 671

2013 1 595

2014 1 294

2015 1 200

2016 1 222

Platinum – prices at 31 March – USD

2012 1 640

2013 1 571

2014 1 405

2015 1 145

2016 954

Palladium – prices at 31 March – USD

2012 836

2013 767

2014 774

2015 741

2016 5621.8% -16.7% -24.2%

PalladiumPlatinumGold

Plat

inum

and

Gol

d

Palla

dium

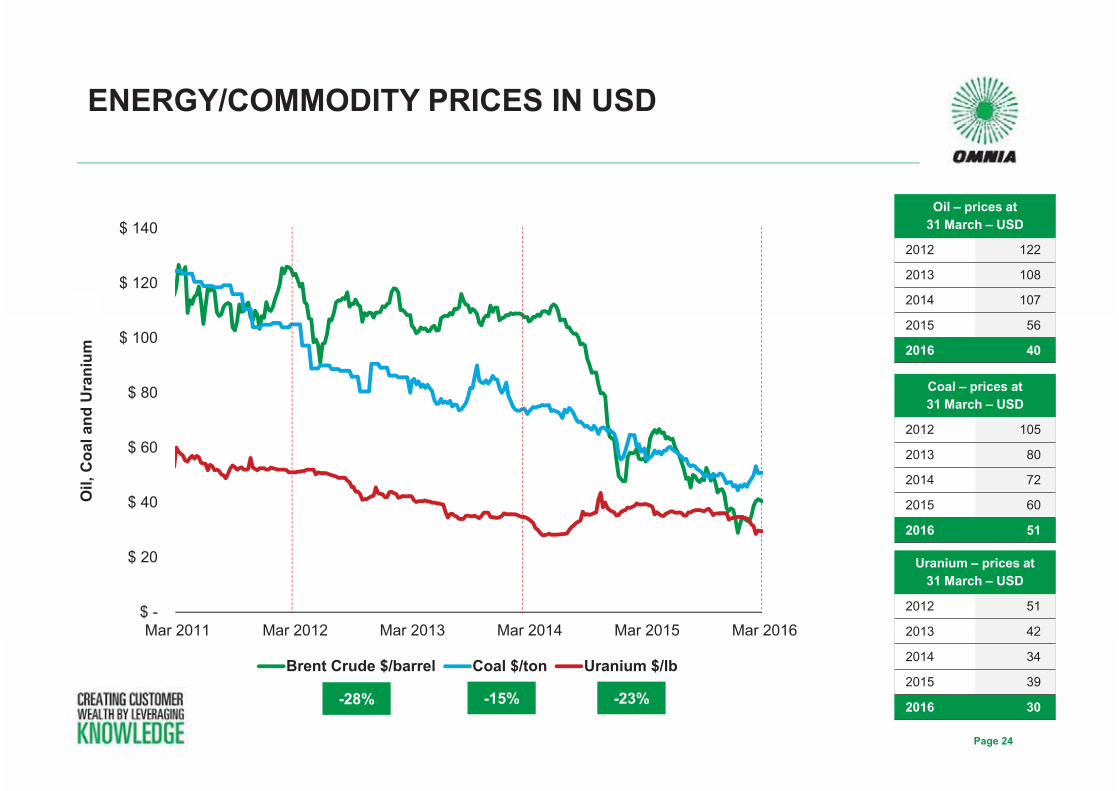

ENERGY/COMMODITY PRICES IN USD

Page 24

$ -

$ 20

$ 40

$ 60

$ 80

$ 100

$ 120

$ 140

Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015 Mar 2016

Brent Crude $/barrel Coal $/ton Uranium $/lb

-23%

Oil – prices at 31 March – USD

2012 122

2013 108

2014 107

2015 56

2016 40

Coal – prices at 31 March – USD

2012 105

2013 80

2014 72

2015 60

2016 51

Uranium – prices at 31 March – USD

2012 51

2013 42

2014 34

2015 39

2016 30-28% -15%

Oil,

Coa

l and

Ura

nium

Page 25

METAL COMMODITY PRICES IN USD PER TONNE

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

$0

$2�000

$4�000

$6�000

$8�000

$10�000

$12�000

Mar�2010 Mar�2011 Mar�2012 Mar�2013 Mar�2014 Mar�2015 Mar�2016

Iron�ore

Copp

er

COPPER IRON�ORE�CHINA

Copper – prices at 31 March – USD

2012 8 480

2013 7 469

2014 6 730

2015 6 105

2016 4 754

Iron ore – prices at 31 March – USD

2012 145

2013 140

2014 112

2015 57

2016 53

-22% -7%

Copper Iron ore China

Cop

per

Iron

ore

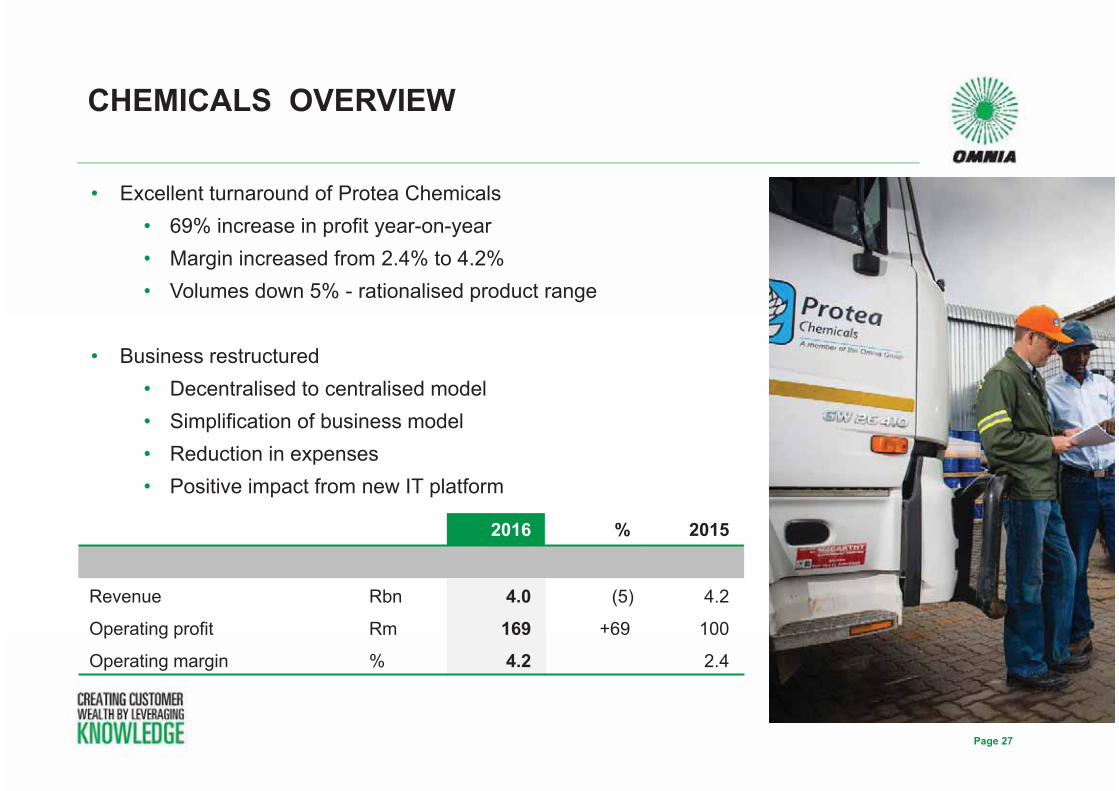

CHEMICALS OVERVIEW

• Excellent turnaround of Protea Chemicals• 69% increase in profit year-on-year• Margin increased from 2.4% to 4.2% • Volumes down 5% - rationalised product range

• Business restructured • Decentralised to centralised model• Simplification of business model • Reduction in expenses• Positive impact from new IT platform

CHEMICALS OVERVIEW

Page 27

2016 % 2015

Revenue Rbn 4.0 (5) 4.2

Operating profit Rm 169 +69 100

Operating margin % 4.2 2.4

Page 28

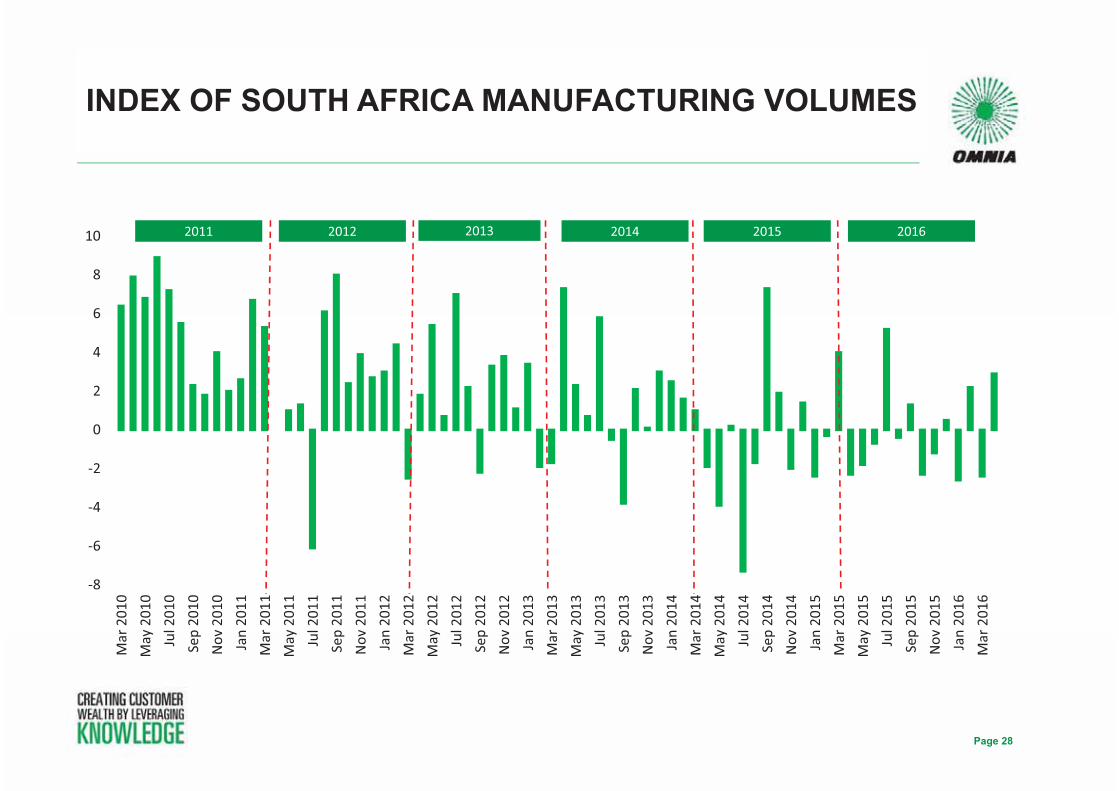

INDEX OF SOUTH AFRICA MANUFACTURING VOLUMES

�8

�6

�4

�2

0

2

4

6

8

10

Mar�201

0May�201

0Jul�201

0Sep�20

10Nov�201

0Jan�20

11Mar�201

1May�201

1Jul�201

1Sep�20

11Nov�201

1Jan�20

12Mar�201

2May�201

2Jul�201

2Sep�20

12Nov�201

2Jan�20

13Mar�201

3May�201

3Jul�201

3Sep�20

13Nov�201

3Jan�20

14Mar�201

4May�201

4Jul�201

4Sep�20

14Nov�201

4Jan�20

15Mar�201

5May�201

5Jul�201

5Sep�20

15Nov�201

5Jan�20

16Mar�201

6

2012 2013 2014 2015 20162011

• Low international commodity USD prices - especially oil-derived chemical prices

• SA rand prices remained flat – weakening of rand/dollar exchange rate offset lower USD prices

• Customer centric focus - improvements in product offering and service levels

• Improved logistics - rationalised warehouse and distribution expenses

CHEMICALS

Page 29

FINANCIAL OVERVIEW

• Exchange rates

• Weakening SA rand:US dollar

• Currency hedge – translation of earnings from foreign operations

• Commodity prices and volumes

• Lower across all three divisions

• Ammonia:urea ratio

• Unfavourable throughout the year

KEY DRIVERS OF REVENUE AND PROFITS

Page 31

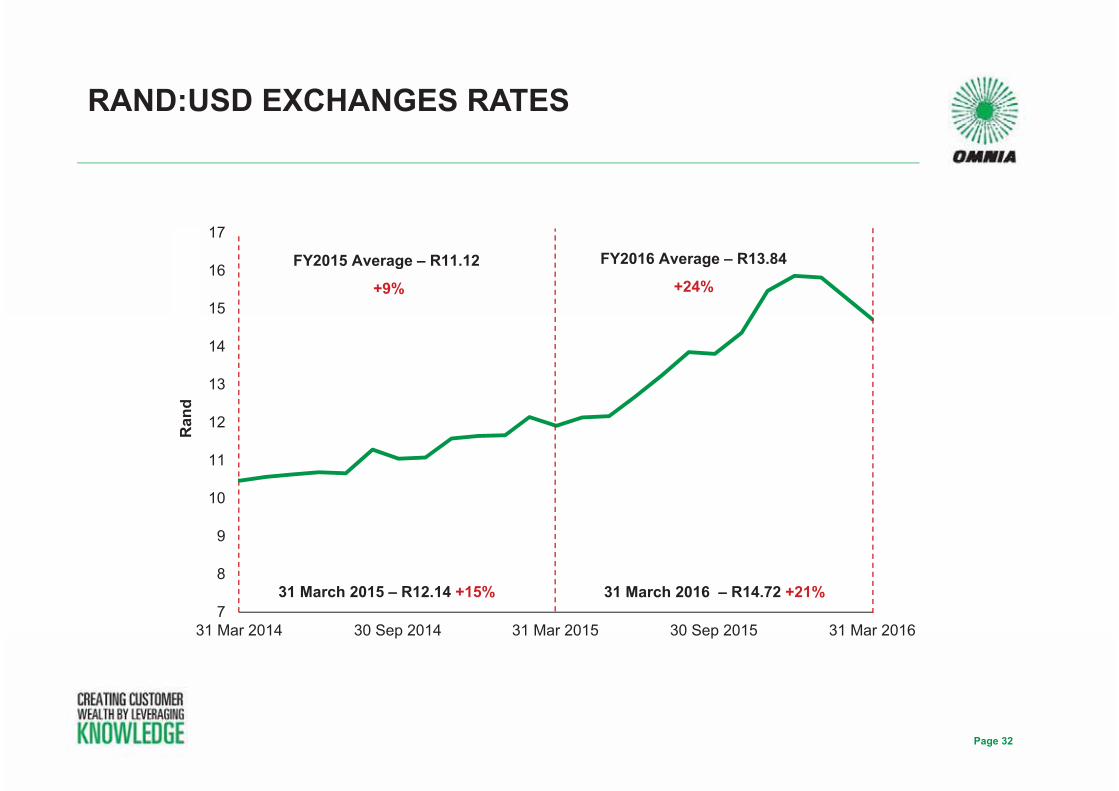

RAND:USD EXCHANGES RATES

Page 32

7

8

9

10

11

12

13

14

15

16

17

31 Mar 2014 30 Sep 2014 31 Mar 2015 30 Sep 2015 31 Mar 2016

FY2016 Average – R13.84

+24%FY2015 Average – R11.12

+9%

31 March 2015 – R12.14 +15% 31 March 2016 – R14.72 +21%

Ran

d

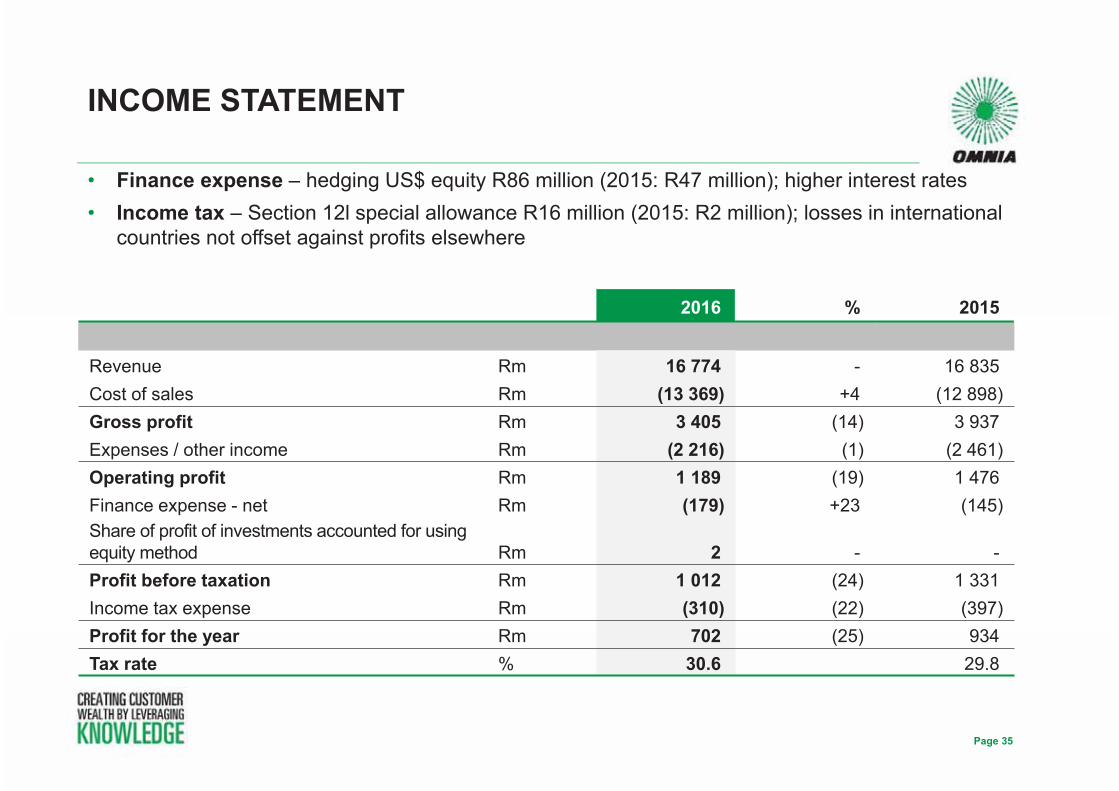

• Gross profit – Decrease in volumes, lower unit selling price and weakening exchange rate

• Distribution expenses – Decreased due to sales volumes resulting in lower distribution expenses

• Administrative expenses – Weaker rand: US dollar which affected costs of operations outside SA

• Other operating expenses – Foreign exchange loss of R53 million (2015: R59 million)

INCOME STATEMENT

Page 33

2016 % 2015

Revenue Rm 16 774 - 16 835Cost of sales Rm (13 369) +4 (12 898)Gross profit Rm 3 405 (14) 3 937Distribution expenses Rm (1 400) (8) (1 524)Administrative expenses Rm (802) (12) (907)Other operating expenses Rm (93) +3 (90)Other operating income Rm 79 +32 60Operating profit Rm 1 189 (19) 1 476Gross margin % 20.3 23.4Operating margin % 7.1 8.8

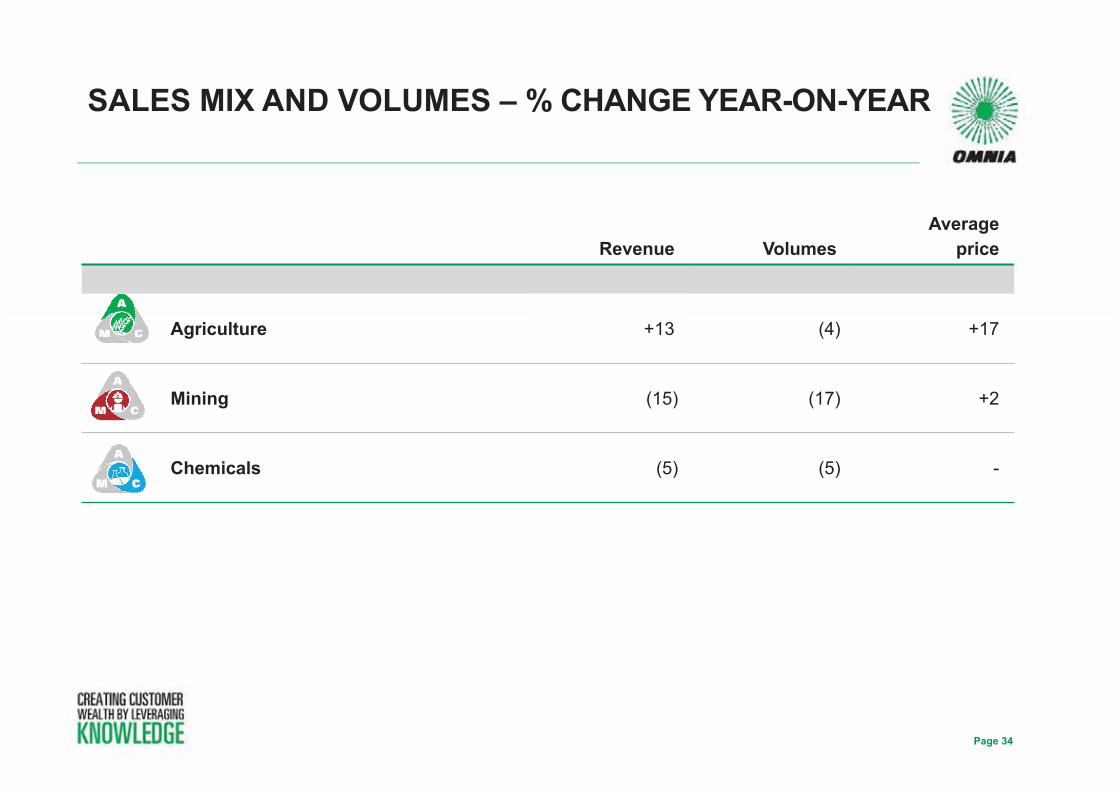

SALES MIX AND VOLUMES – % CHANGE YEAR-ON-YEAR

Page 34

Revenue VolumesAverage

price

Agriculture +13 (4) +17

Mining (15) (17) +2

Chemicals (5) (5) -

• Finance expense – hedging US$ equity R86 million (2015: R47 million); higher interest rates • Income tax – Section 12l special allowance R16 million (2015: R2 million); losses in international

countries not offset against profits elsewhere

INCOME STATEMENT

Page 35

2016 % 2015

Revenue Rm 16 774 - 16 835Cost of sales Rm (13 369) +4 (12 898)Gross profit Rm 3 405 (14) 3 937Expenses / other income Rm (2 216) (1) (2 461)Operating profit Rm 1 189 (19) 1 476Finance expense - net Rm (179) +23 (145)Share of profit of investments accounted for using equity method Rm 2 - -Profit before taxation Rm 1 012 (24) 1 331Income tax expense Rm (310) (22) (397)Profit for the year Rm 702 (25) 934Tax rate % 30.6 29.8

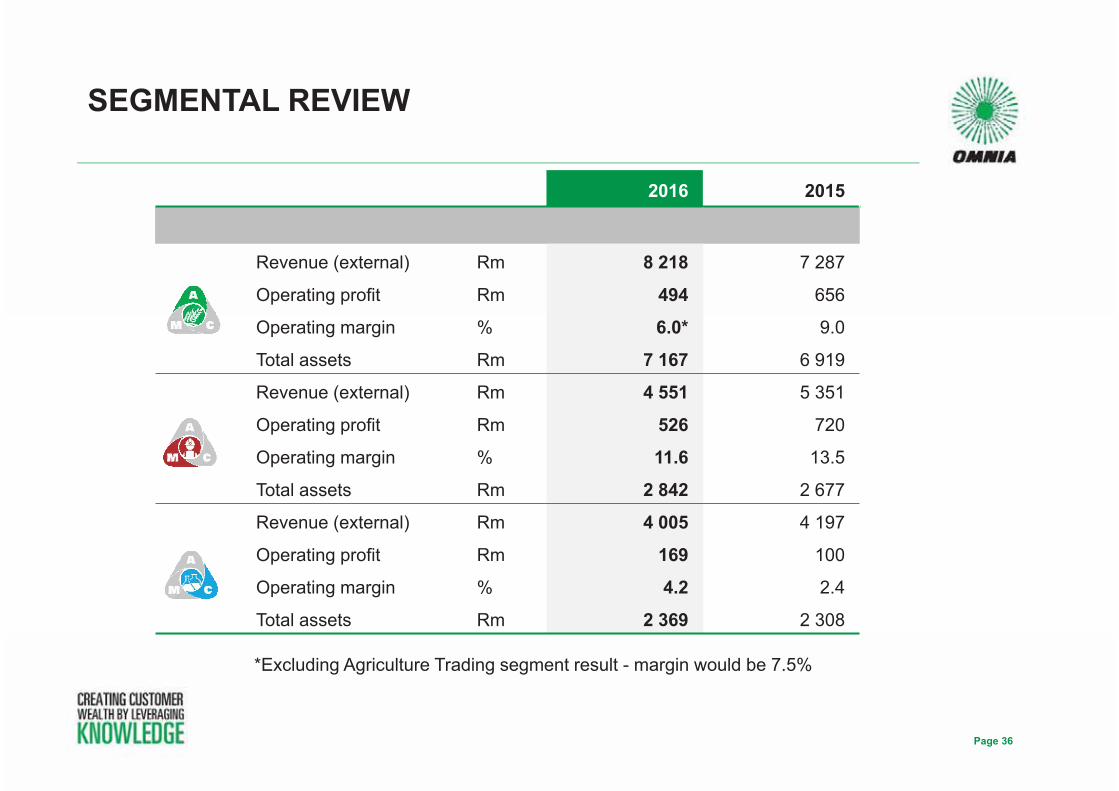

SEGMENTAL REVIEW

Page 36

2016 2015

Revenue (external) Rm 8 218 7 287

Operating profit Rm 494 656

Operating margin % 6.0* 9.0

Total assets Rm 7 167 6 919

Revenue (external) Rm 4 551 5 351

Operating profit Rm 526 720

Operating margin % 11.6 13.5

Total assets Rm 2 842 2 677

Revenue (external) Rm 4 005 4 197

Operating profit Rm 169 100

Operating margin % 4.2 2.4

Total assets Rm 2 369 2 308

*Excluding Agriculture Trading segment result - margin would be 7.5%

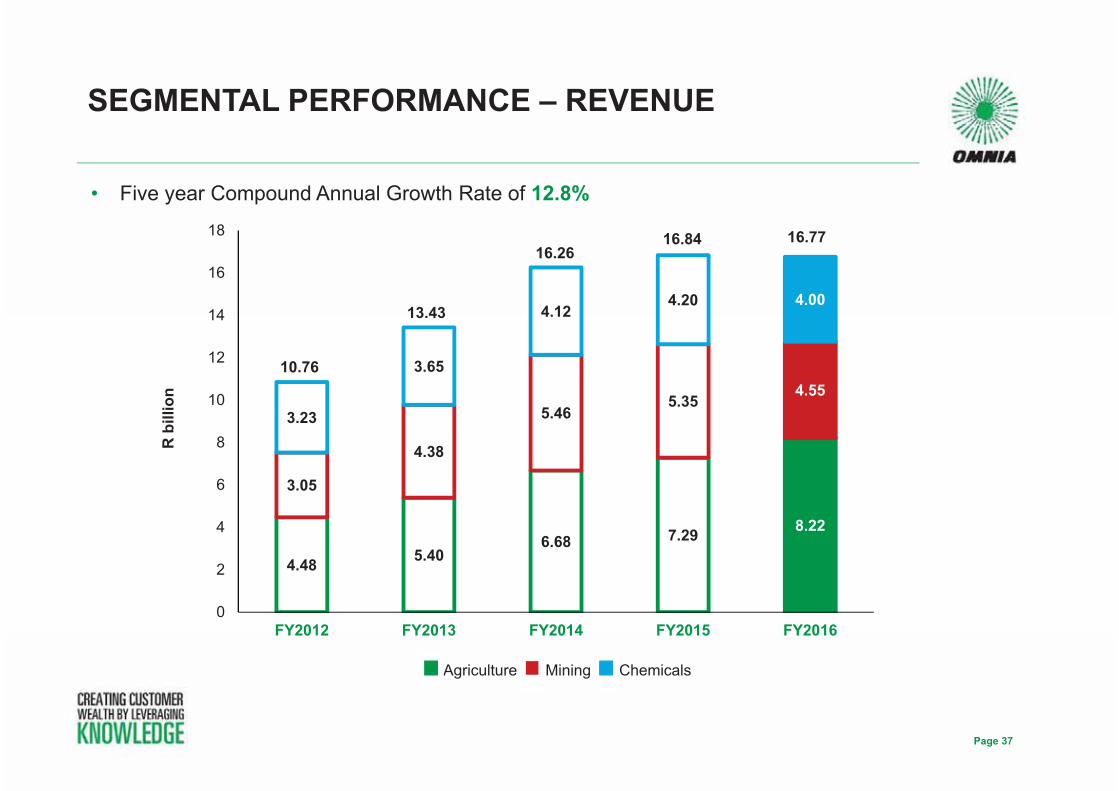

• Five year Compound Annual Growth Rate of 12.8%

SEGMENTAL PERFORMANCE – REVENUE

Page 37

4.48 5.406.68 7.29 8.22

3.05

4.38

5.465.35

4.55

3.23

3.65

4.124.20 4.00

0

2

4

6

8

10

12

14

16

18

FY2012 FY2013 FY2014 FY2015 FY2016

R b

illio

n

Agriculture Mining Chemicals

10.76

13.43

16.2616.84 16.77

• Five year Compound Annual Growth Rate of 11.6%

SEGMENTAL PERFORMANCE – OPERATING PROFIT

Page 38

323443 431

656494

476

735 829

720

52682

53

156100

169

0

200

400

600

800

1 000

1 200

1 400

1 600

FY2012 FY2013 FY2014 FY2015 FY2016

R m

illio

n

Agriculture Mining Chemicals

881

1 231

1 4161 476

1 189

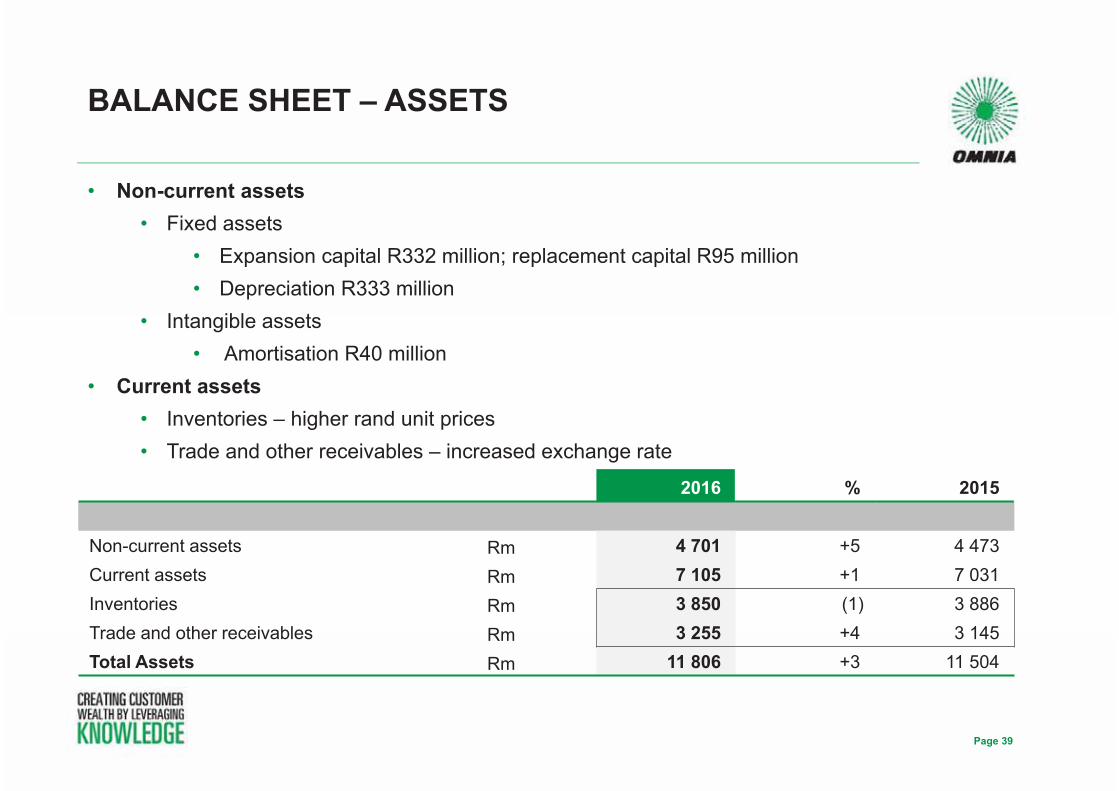

• Non-current assets• Fixed assets

• Expansion capital R332 million; replacement capital R95 million• Depreciation R333 million

• Intangible assets• Amortisation R40 million

• Current assets • Inventories – higher rand unit prices• Trade and other receivables – increased exchange rate

BALANCE SHEET – ASSETS

Page 39

2016 % 2015

Non-current assets Rm 4 701 +5 4 473Current assets Rm 7 105 +1 7 031Inventories Rm 3 850 (1) 3 886Trade and other receivables Rm 3 255 +4 3 145Total Assets Rm 11 806 +3 11 504

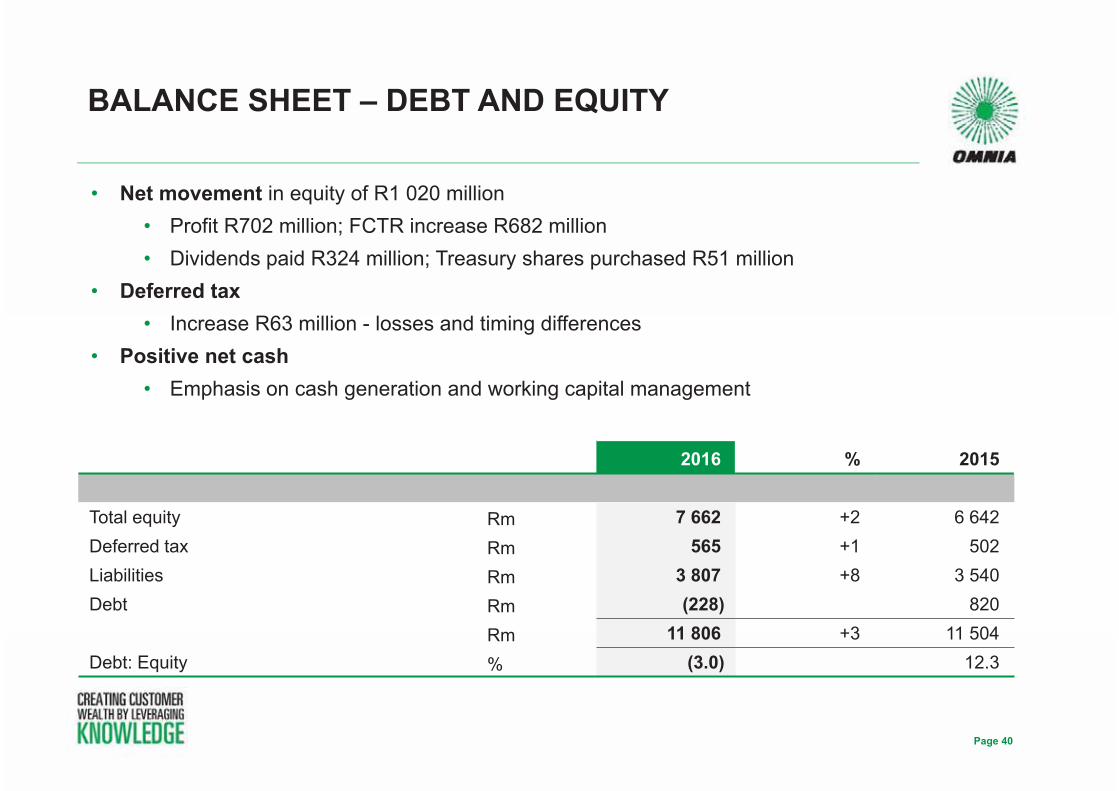

• Net movement in equity of R1 020 million• Profit R702 million; FCTR increase R682 million• Dividends paid R324 million; Treasury shares purchased R51 million

• Deferred tax • Increase R63 million - losses and timing differences

• Positive net cash • Emphasis on cash generation and working capital management

BALANCE SHEET – DEBT AND EQUITY

Page 40

2016 % 2015

Total equity Rm 7 662 +2 6 642 Deferred tax Rm 565 +1 502Liabilities Rm 3 807 +8 3 540Debt Rm (228) 820

Rm 11 806 +3 11 504Debt: Equity % (3.0) 12.3

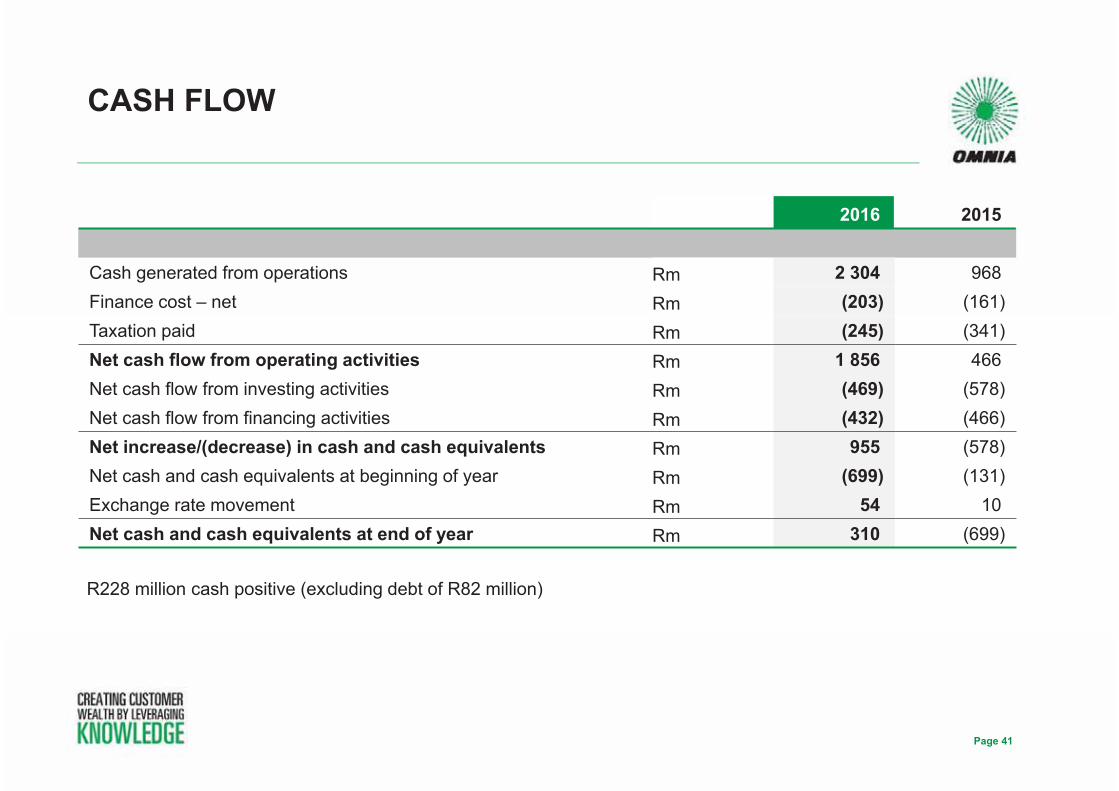

CASH FLOW

Page 41

2016 2015

Cash generated from operations Rm 2 304 968Finance cost – net Rm (203) (161)Taxation paid Rm (245) (341)Net cash flow from operating activities Rm 1 856 466Net cash flow from investing activities Rm (469) (578)Net cash flow from financing activities Rm (432) (466)Net increase/(decrease) in cash and cash equivalents Rm 955 (578)Net cash and cash equivalents at beginning of year Rm (699) (131)Exchange rate movement Rm 54 10Net cash and cash equivalents at end of year Rm 310 (699)

R228 million cash positive (excluding debt of R82 million)

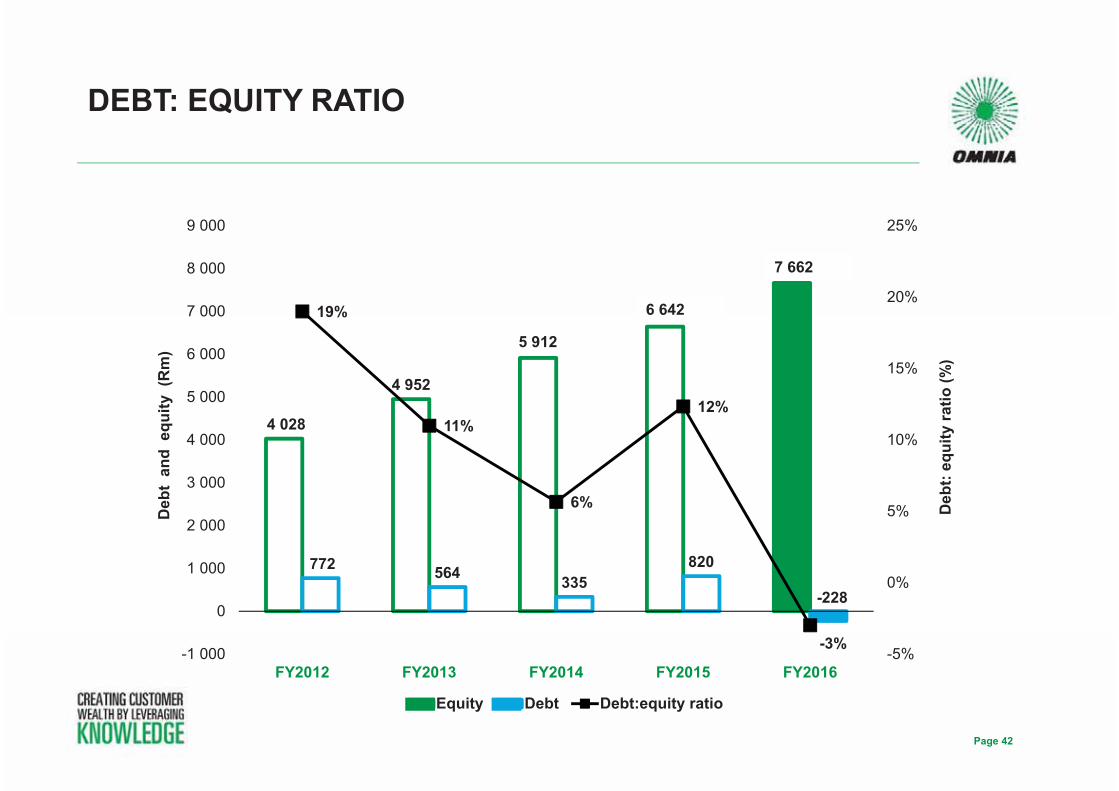

DEBT: EQUITY RATIO

Page 42

4 028

4 952

5912

6642

7662

772 564 335820

-228

19%

11%

6%

12%

-3%-5%

0%

5%

10%

15%

20%

25%

-1 000

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

FY2012 FY2013 FY2014 FY2015 FY2016

Deb

t: eq

uity

ratio

(%)

Deb

t an

d e

quity

(R

m)

Equity Debt Debt:equity ratio

5 912

6 642

7 662

PROSPECTS

• SA rand:USD weakness benefits all three divisions

• Strong balance sheet

• Growth opportunities – continue to identify and evaluate

• Turnaround of Protea Chemicals continues building momentum

• Upgrading of IT platforms adding value

• Strong management team and business model

• Continue to expand markets beyond Africa

GROUP OUTLOOK

Page 44

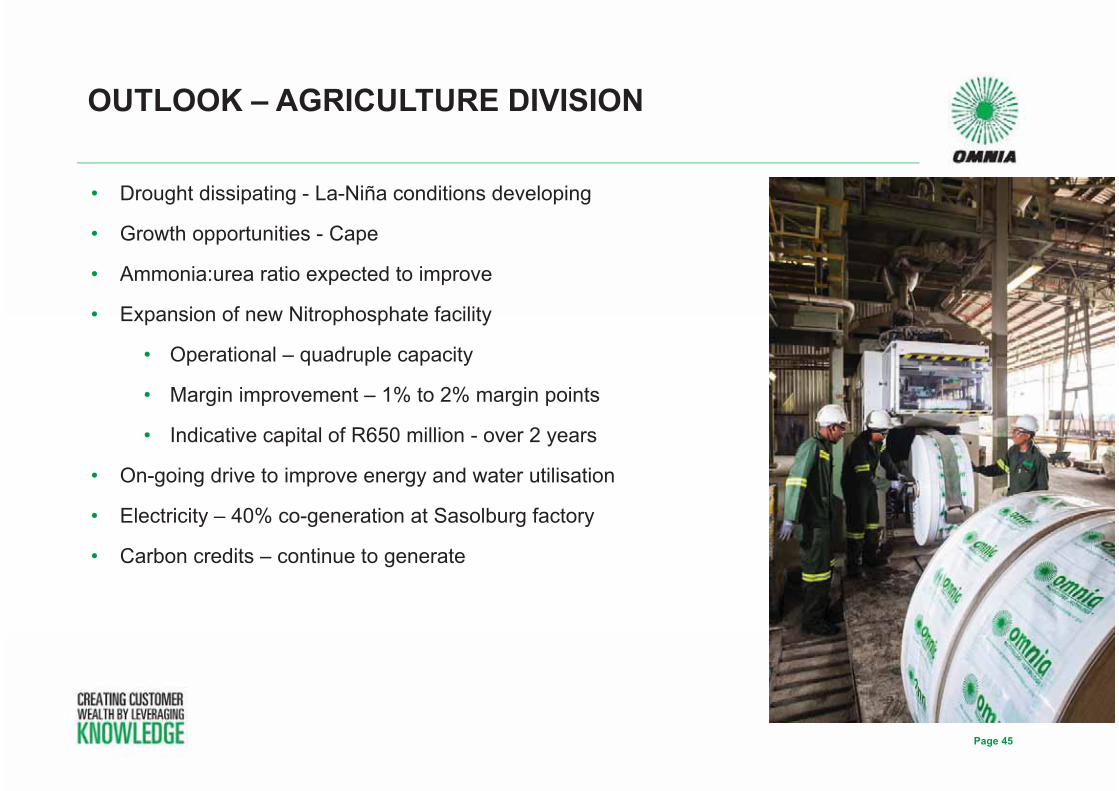

• Drought dissipating - La-Niña conditions developing

• Growth opportunities - Cape

• Ammonia:urea ratio expected to improve

• Expansion of new Nitrophosphate facility

• Operational – quadruple capacity

• Margin improvement – 1% to 2% margin points

• Indicative capital of R650 million - over 2 years

• On-going drive to improve energy and water utilisation

• Electricity – 40% co-generation at Sasolburg factory

• Carbon credits – continue to generate

OUTLOOK – AGRICULTURE DIVISION

Page 45

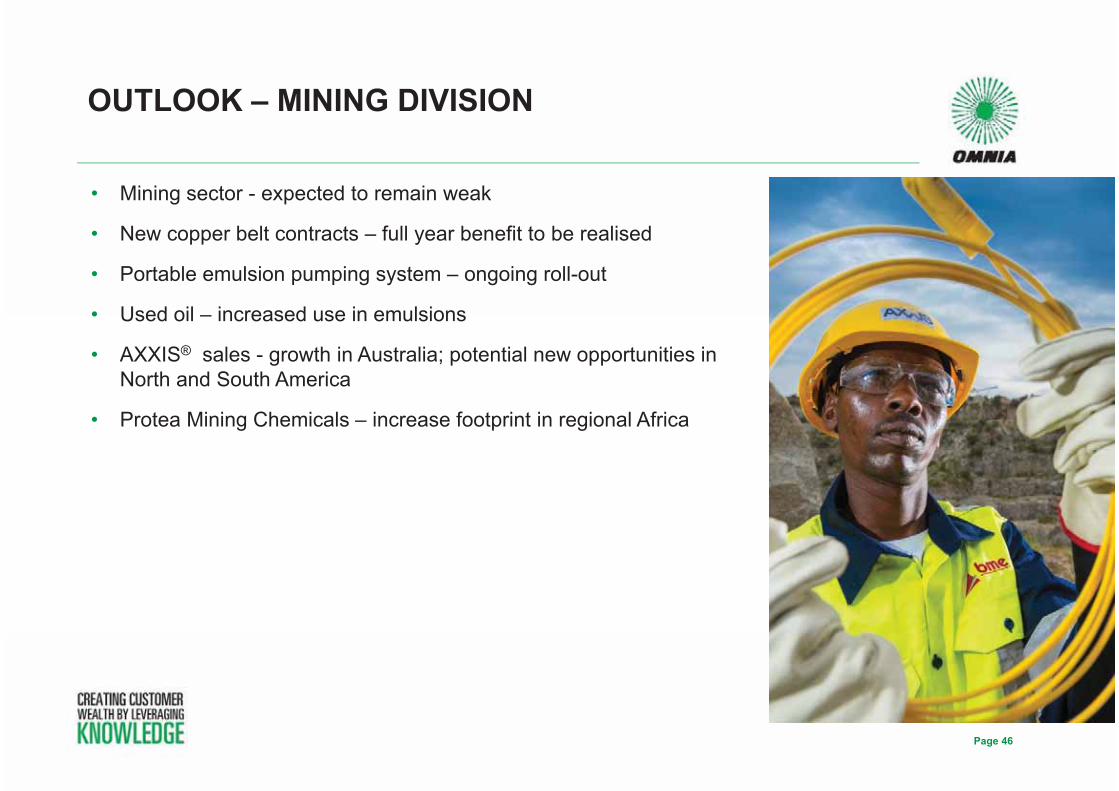

• Mining sector - expected to remain weak

• New copper belt contracts – full year benefit to be realised

• Portable emulsion pumping system – ongoing roll-out

• Used oil – increased use in emulsions

• AXXIS® sales - growth in Australia; potential new opportunities in North and South America

• Protea Mining Chemicals – increase footprint in regional Africa

OUTLOOK – MINING DIVISION

Page 46

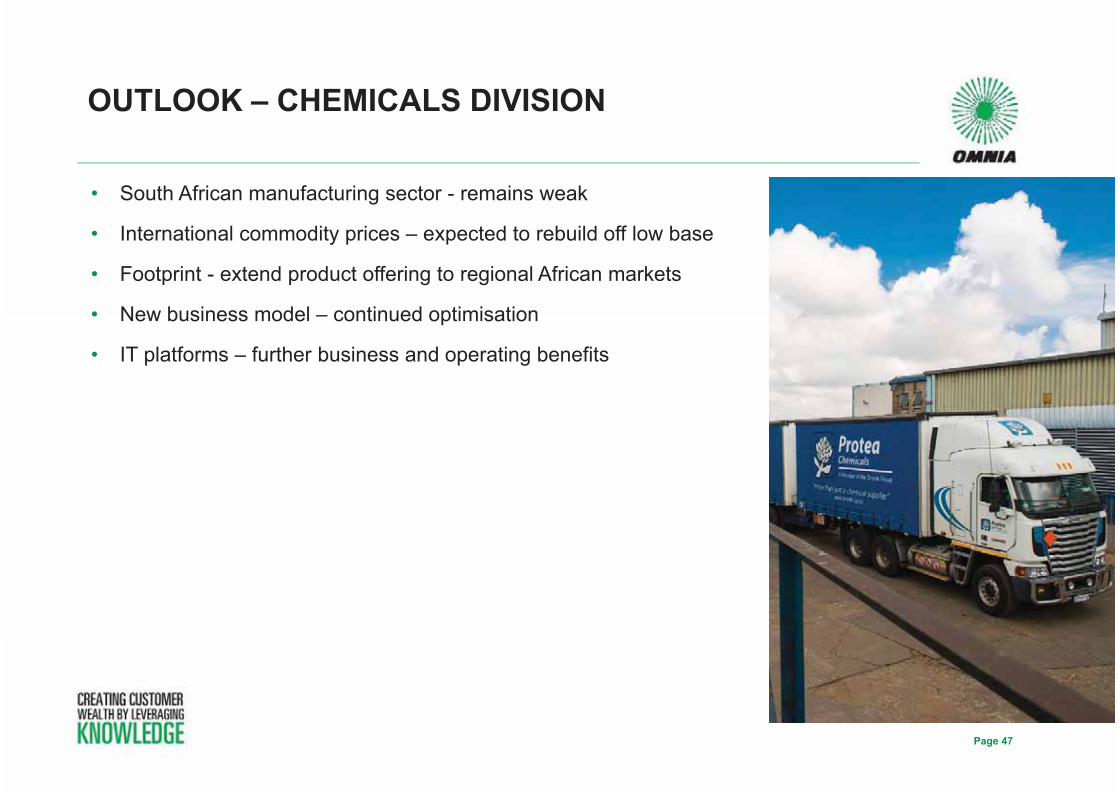

• South African manufacturing sector - remains weak

• International commodity prices – expected to rebuild off low base

• Footprint - extend product offering to regional African markets

• New business model – continued optimisation

• IT platforms – further business and operating benefits

OUTLOOK – CHEMICALS DIVISION

Page 47

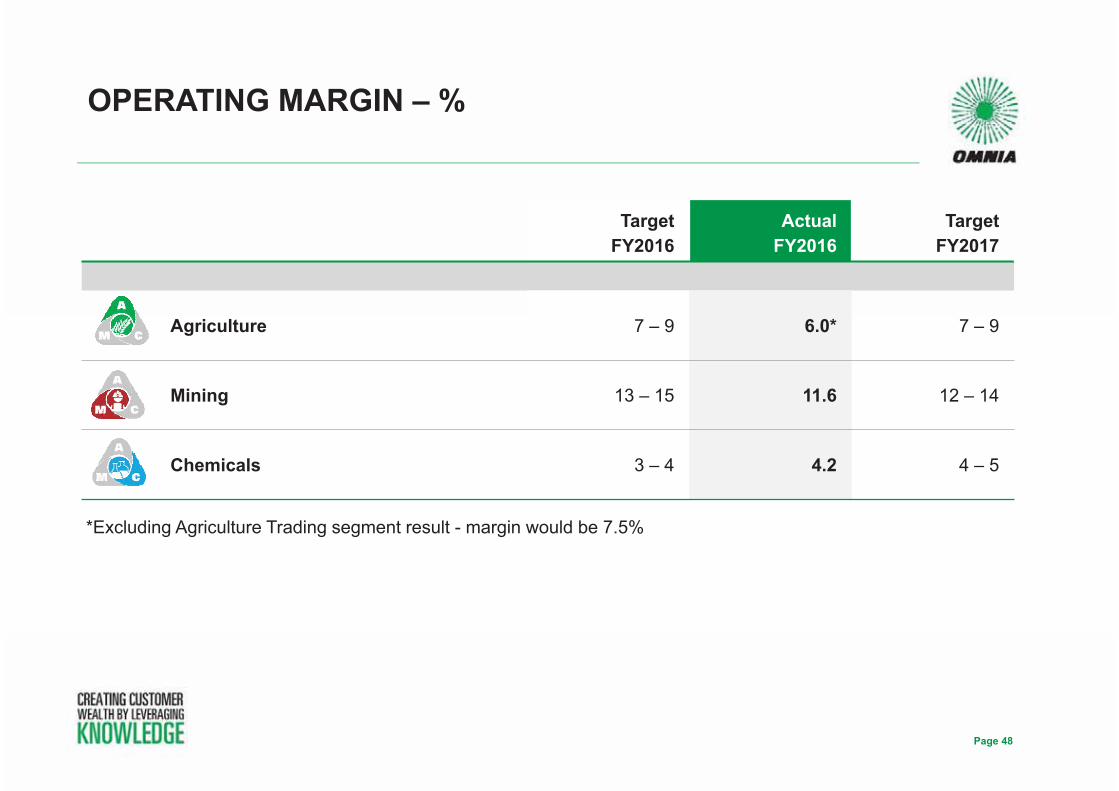

OPERATING MARGIN – %

Page 48

TargetFY2016

ActualFY2016

TargetFY2017

Agriculture 7 – 9 6.0* 7 – 9

Mining 13 – 15 11.6 12 – 14

Chemicals 3 – 4 4.2 4 – 5

*Excluding Agriculture Trading segment result - margin would be 7.5%