ompany presentation santander 17th annual latin american ... · santander 17th annual latin...

TRANSCRIPT

COMPANY PRESENTATION

Santander 17th Annual Latin American CEO Conference

January 15-17, 2013

Company Overview

Agenda

Business Strategy

Financial Profile

Chilean Electricity Sector Overview

2

Recent developments Company Overview

3

HYDRO CONDITION

2012 3rd consecutive extremely dry year

SANTA MARIA I COAL PROJECT

1,853 GWh generated during 2012 (out of the estimated 2,500 GWh/year) Dec. 12’: Insurance settlement for USD 65 million (USD 40 million for ALOP)

COMMERCIAL BALANCE

Relevant input of coal (efficient thermal complement to hydro) Net seller in the spot market, despite reduced hydro

NATURAL GAS

Medium-term natural gas supply secured 2 CCGT with gas for Jan-Apr 2013

ANGOSTURA PROJECT

Over 80% of progress, scheduled for end of 2013.

CREDIT RATING

Fitch Ratings (12.17.2012): BBB rating reaffirmed S&P (12.28.2012): BBB- rating reaffirmed, maintaining negative outlook

8.829

5.566

10.687

5.462

~9.800

5.233

95 1.853 1.273

2.418

2.242 2.563 1.901

2.240

0

2.000

4.000

6.000

8.000

10.000

12.000

2010 2011 2012

GWh Generation vs. commitments

Contractual Sales Hydro Natural gas (LNG) Diesel Coal

Market Share (as a % of Installed Capacity) - SIC

Generation (GWh) and Installed Capacity (MW)

Source: CNE – December 2011

Source: Colbún 2011 Generation and 3Q12 closing Capacity

Thermal 55%

Hydro 45% 57

%

43%

Generation

Capacity

Business Power Generation & Trade

Size 2nd largest generator in Chile’s Central Grid (SIC), with over 20% market share (MW).

The SIC covers 90% of the population

Capacity 2,962 MW

43% hydro and 57% thermal

Generation 11,568 GWh in 2012

45% hydro and 55% thermal

Assets 15 hydro plants in 4 different basins 7 thermal plants in 4 different regions

People 961 employees as of September’12

Results EBITDA of USD 204.7 million in 2011

EBITDA of USD 242.6 million LTM Sep. 12’

Revenues of USD 1.3 billion in 2011

Revenues of USD 1.3 billion LTM Sep. 12’

Colbún at a glance Company Overview

4

Colbún 21%

Endesa 41%

AES Gener 18%

Others 20%

Nehuenco III Capacity: 108 MW

Nehuenco I Capacity: 368 MW

Nehuenco II Capacity: 398 MW

NEHUENCO COMPLEX: 874 MW DIESEL/GAS

Candelaria Capacity Unit I : 133 MW Capacity Unit II : 137 MW

CANDELARIA POWER PLANT: 270 MW DIESEL/GAS

Los Pinos Capacity: 100 MW

LOS PINOS POWER PLANT: 100 MW DIESEL

Antilhue Capacity Unit I : 51 MW Capacity Unit II : 52 MW

ANTILHUE POWER PLANT: 103 MW DIESEL

Chacabuquito Capacity: 29 MW

ACONCAGUA BASIN: 213 MW

Los Quilos Capacity: 39 MW

Hornitos Capacity: 55 MW

Blanco Capacity: 60 MW

Juncal Capacity: 29 MW

Juncalito Capacity: 1 MW

7 T

HER

MA

L P

OW

ER P

LAN

TS

Carena Capacity: 9 MW

CARENA POWER PLANT: 9 MW

Colbún Capacity: 474 MW

MAULE BASIN: 630 MW

San Ignacio Capacity: 37 MW

San Clemente Capacity: 5 MW

Machicura Capacity: 95 MW

Chiburgo Capacity: 19 MW

Rucúe Capacity: 178 MW

LAJA BASIN: 249 MW

Quilleco Capacity: 71 MW

Canutillar Capacity: 172 MW

CHAPO LAKE: 172 MW

15

HY

DR

O P

OW

ER P

LAN

TS A diversified asset base

Company Overview

5

Santa María I Capacity: 342 MW

SANTA MARIA I POWER PLANT: 342 MW COAL

737 KM Additional Transmission System

68 KM Sub Transmission System

TRANSMISSION LINES

47 KM Trunk Transmission System

Combined Cycle

Open Cycle

Run of the River

Reservoir

Coal-fired

CHILECTRA (2011- 2021/23/25)

SAESA (2010- 2019)

CGE-Río Maipo (2010- 2021)

CONAFE (Until 2020)

CGE-Distribución (2010- 2024)

CODELCO Andina

ANGLOAMERICAN Los Bronces

CMPC Puente Alto

CODELCO Ventanas

CODELCO Salvador

CODELCO Teniente

CMPC Procart

METRO AGUAS ANDINAS La Farfana

UN

-REG

ULA

TED C

USTO

MER

S R

EGU

LATE

D C

UST

OM

ERS

Company Overview

6

A diversified customer base

Santiago

0

50

100

150

200

250

300

350

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

0

500

1.000

1.500

2.000

2.500

3.000

3.500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

2,962 MW

1,070 MW CAGR: 8%

0

200

400

600

800

1.000

1.200

1.400

1.600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

US$ 1,333 million

US$ 129 million

CAGR: 21%

US$ 54 million

US$ 291 million

CAGR: 15%

Colbún has grown steadily over the past decade Company Overview

7

Capacity (MW) Total Operating Revenues (MMUSD)

Market Cap (MMUSD) 3-year Moving Average EBITDA (MMUSD)

0

1.000

2.000

3.000

4.000

5.000

6.000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US$ 4,830 million

US$ 435 million CAGR: 20%

Angelini Group 10%

Pension Funds 19%

Others 22%

Matte Group 49%

CONTROL

Controlled by the Matte Group (49%), one of the leading economic groups in Chile, with stakes in various sectors (forestry, financial, telecommunications, among others).

LARGE STAKEHOLDER

The second important stakeholder, the Angelini Group, is also a leading Chilean economic group and owns 9.6% of Colbún.

FLOAT

41% free float, with relevant local institutional investor presence.

GOVERNANCE

4 out of 9 are independent directors.

ACCOUNTING STANDARDS

Disclosure under IFRS standards Functional currency: US dollar

Solid and reliable controlling group with a strategic and long term vision

Company Overview

8

Ownership Structure

Source: Colbún, December 2012

Agenda

9

Company Overview

Business Strategy

Financial Profile

Chilean Electricity Sector Overview

10

Corporate Strategy Business Strategy

We are a Chilean company, leader in the generation of reliable, competitive and sustainable energy

Who are we?

What do we do?

We seek to generate long-term value by developing projects and managing power infrastructure to meet the

country’s energy demand.

11

Strategic Pillars Business Strategy

1. Consolidation

2. Diversification and Risk

Management

3. Growth

Consolidate our people, our operations, our projects, our financials…

Identify and develop project options to consolidate our market share. Commercial strategy that generates long-term returns consistent with our asset base.

Narrow our exposure to exogenous variables: diversified asset base (technology, fuel and location) and clients.

Active risk management policy.

Long-term value generation (Profitability/EBITDA)

Value Chain Business Strategy

Sustainability Value & Trust

Multidimensional challenge:

Technical

+ Environmental / Social

+ Financial

High standards:

Reliability

+ Security

+ Environmental

Risk / return profile combining:

Commercial policy

+ Financial strength

+ Risk management

Project Development

Operational

Excellence

Risk / Return

Profile

12

EMPLOYEES

COMMUNITY AND

SOCIETY

ENVIRONMENT

CONTRACTORS

Business Strategy

13

Colbún: a sustainable partner

INVESTORS

CLIENTS AND SUPPLIERS

COMMERCIAL GOALS

Supply secure and competitive energy to our customers Maximize returns from our current and future assets Manage volatility given large renewable component

1. CONTRACT LEVEL

Define optimal Contract Level

Hydro capacity (Output of a medium-dry year)

+ Efficient thermal

capacity (Output of coal-fueled plant)

2. SALE PRICE INDEXATION

Incorporate indexation formulas of sale prices

that reflect our cost structure

Structure tailor-made hedge programs

to protect from more adverse

1) Hydrologic conditions 2) Fuel prices

3. HEDGE PROGRAM

Business Strategy

14

Commercial policy

Hydro CPI

Efficient thermal Fossil Fuels

Transitional periods Flexible Price

109 128

156 170

211

446

19

236

337 331

205

0

50

100

150

200

250

300

350

400

450

500

0

2.000

4.000

6.000

8.000

10.000

12.000

GWh MMUSD

EBITDA (EBITDA Margin)

Ratio: Base Generation /

Commitments Base Generation1 / Commitments2 ≥ 90% B.G. / C ≤ 70% B.G. / C ≥ 85%

“Base” Generation

Contractual Commitments

1: Commitments represent Colbún’s committed sales (through contracts) excluding commitments which price is indexed to the spot price

2: Base Generation represents Colbún’s electricity production @ low variable cost (hydro generation + gas generation during Phase I and coal generation in Phase III)

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012e

Business Strategy

15

Evolution of Colbún’s Business Model

144% 125% 112% 97% 90% 92% 53% 70% 70% 87% 67% 74%

(58%) (60%) (60%) (48%) (45%) (59%) (1%) (18%) (29%) (32%) (15%)

43%

57%

51%

49%

3,428 MW

2,962 MW

Angostura 316 MW

Thermoelectric capacity

Hydroelectric capacity San Pedro 150 MW

Other Growth Opportunities Santa María II (350 MW) Environmental approval for the construction of a second unit Hydraulic Various water rights in different basins Geothermal Two concessions awarded for exploration, others under process

Wind Two wind measurement towers located in Maule Region

Business Strategy

16

Our expansion plan

ANGOSTURA HYDRO POWER PLANT: 316 MW Santa Barbara and Quilaco, Biobío Region

INVESTMENT POWER PLANT: 675 MMUSD

INVESTMENT TX LINE: 45 MMUSD

SPENT AS OF SEP. 2012: 480 MMUSD

ADVANCE SEP. 2012: 80%

ESTIMATE START OF OPERATION: 4Q2013

SAN PEDRO HYDRO POWER PLANT: 150 MW Riñihue Lake, Los Ríos Region

INVESTMENT: Under revision

SPENT AS OF SEP 2012: 112 MMUSD

ESTIMATE START OF OPERATION: Under revision

ANGOSTURA

SAN PEDRO

Business Strategy

17

Our projects under development

Agenda

18

Company Overview

Business Strategy

Financial Profile

Chilean Electricity Sector Overview

59%

2%

18%

29% 32%

15% 18%

0

200

400

600

800

1.000

1.200

1.400

1.600

2006 2007 2008 2009 2010 2011 LTM Sep.12'

Revenues EBITDA EBITDA margin (%)

MMUSD 2006 2007 2008 2009 2010 2011 LTM

Sep. 12’

Revenues 753 1,160 1,346 1,159 1,024 1,333 1,327

EBITDA 446 19 236 337 331 205 243

Depreciation (107) (118) (117) (122) (124) (125) (128)

Non-operational result (43) 75 106 (51) (103) (37) (52)

Exchange rate differences 12 (65) (120) 82 18 (14) 17

Income Tax (32) (1) (37) (7) (6) (24) (52)

Net Income 276 (90) 67 239 116 5 26

Revenues, EBITDA (MMUSD) & EBITDA Margin

Financial Profile

19

Income Statement

Average EBITDA 2006-2011: MMUSD 262

Non-operational result from past years affected by payments to early terminate old natural gas transport contracts

2012 Income Tax: one-time MMUSD 74 charge from increase in tax rate

Financial Profile

20

Capital Structure and Credit Metrics

Key Credit Metrics

2006 2007 2008 2009 2010 2011 LTM

Sep. 12’

Total debt to total capital (%)

18.8 26.0 25.0 27.0 31.0 30.0 29.7

Net debt to EBITDA (x)

0.4 36.6 2.3 2.3 3.1 5.9 6.1

EBITDA Interest coverage (x)

14.3 0.5 3.9 6.5 6.7 7.4 10.7

Cash, Debt & Net Debt (MMUSD)

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2.000

2006 2007 2008 2009 2010 2011 3Q12

Cash

Net debt

Total debt

Financial Profile

21

Free Cash Flow Analysis

Selected Sources & Uses of Funds (MMUSD)

0

100

200

300

400

500

600

700

2008 2009 2010 2011 LTM Sep.12'

K WK Capex EBITDA

Negative FCF in past years due to intensive capex program

Intensity of capex diminishes in 2013

Expected recovery of VAT Credit in coming years

(current stock of MMUSD 245)

Low dividend policy (30% of Net Income)

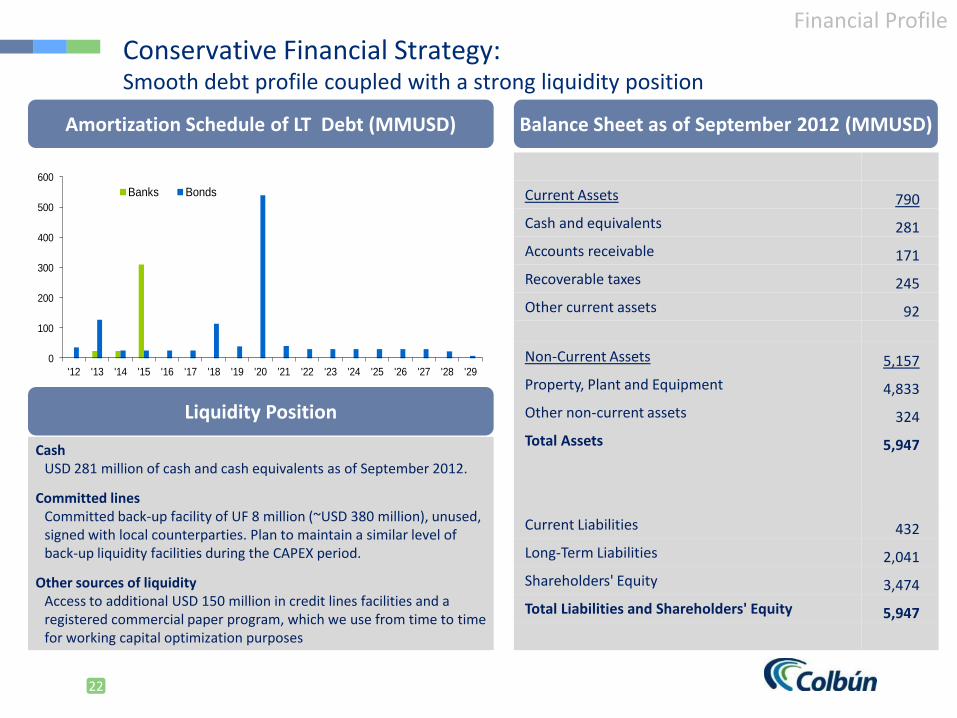

Current Assets 790

Cash and equivalents 281

Accounts receivable 171

Recoverable taxes 245

Other current assets 92

Non-Current Assets 5,157

Property, Plant and Equipment 4,833

Other non-current assets 324

Total Assets 5,947

Current Liabilities 432

Long-Term Liabilities 2,041

Shareholders' Equity 3,474

Total Liabilities and Shareholders' Equity 5,947

Cash USD 281 million of cash and cash equivalents as of September 2012.

Committed lines Committed back-up facility of UF 8 million (~USD 380 million), unused,

signed with local counterparties. Plan to maintain a similar level of back-up liquidity facilities during the CAPEX period.

Other sources of liquidity Access to additional USD 150 million in credit lines facilities and a

registered commercial paper program, which we use from time to time for working capital optimization purposes

Amortization Schedule of LT Debt (MMUSD) Balance Sheet as of September 2012 (MMUSD)

22

Conservative Financial Strategy: Smooth debt profile coupled with a strong liquidity position

Liquidity Position

Financial Profile

0

100

200

300

400

500

600

'12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25 '26 '27 '28 '29

Banks Bonds

315

335

362

320

361

332

315

1Q 2Q 3Q 4Q

Revenues 2011 Revenues 2012

5%

2%

29%

23%

8% 8%

37%

0%

10%

20%

30%

40%

50%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

0

500

1.000

1.500

2.000

2.500

3.000

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12e

Sales vs. Generation - quarterly (GWh) Revenues - quarterly (MMUSD)

17 8

106

74

27 25

116

1Q 2Q 3Q 4Q

EBITDA 2011 EBITDA 2012

EBITDA - quarterly (MMUSD) EBITDA margin - quarterly (%)

A quarterly look at Colbún’s results

23

Contractual Sales Hydro Natural gas (LNG) Diesel Coal

Financial Profile

Agenda

24

Company Overview

Business Strategy

Financial Profile

Chilean Electricity Sector Overview

Tal-Tal

Arica

Antofagasta

Santiago

Castro Chaitén

Cochrane

Pto. Natales

Pto. Williams

SING

SIC

SEA

SAM

GENERATION

Regulated

sectors

(concessions)

RELEVANT INSTITUTIONS

Ministry of Energy

Regulator: CNE

Supervisor: SEC

Coordinator: CDEC

3,964 MW - 25%

15.881 GWh - 25%

12,365 MW - 75%

46.052 GWh - 74%

52 MW - 0%

146 GWh - 0%

100 MW - 0%

276 GWh - 0%

3 SUB-SECTORS

Chilean Electricity Sector Overview

TRANSMISSION

DISTRIBUTION

4 SEPARATE GRIDS

Sector Segmentation

25 Source: CNE, December 2011

GENERATORS

REGULATED CUSTOMERS

DISTRIBUTION COMPANIES

Regulated Auction Tariffs

UNREGULATED CUSTOMERS

“FREE” CUSTOMERS

Unregulated Auction Tariffs

SPOT MARKET

CDEC

Marginal Cost /Spot Price

41%

21%

18%

2% 1%

17%

Endesa Colbún Gener Arauco CGE Others

>15 players

Market Structure

Electricity Market Structure Main Players in the Generation Sector-SIC

26

Source: “Capacidad Empresas Generadoras CDEC, December 2011

Chilean Electricity Sector Overview

0

5

10

15

20

25

30

35

40

45

50

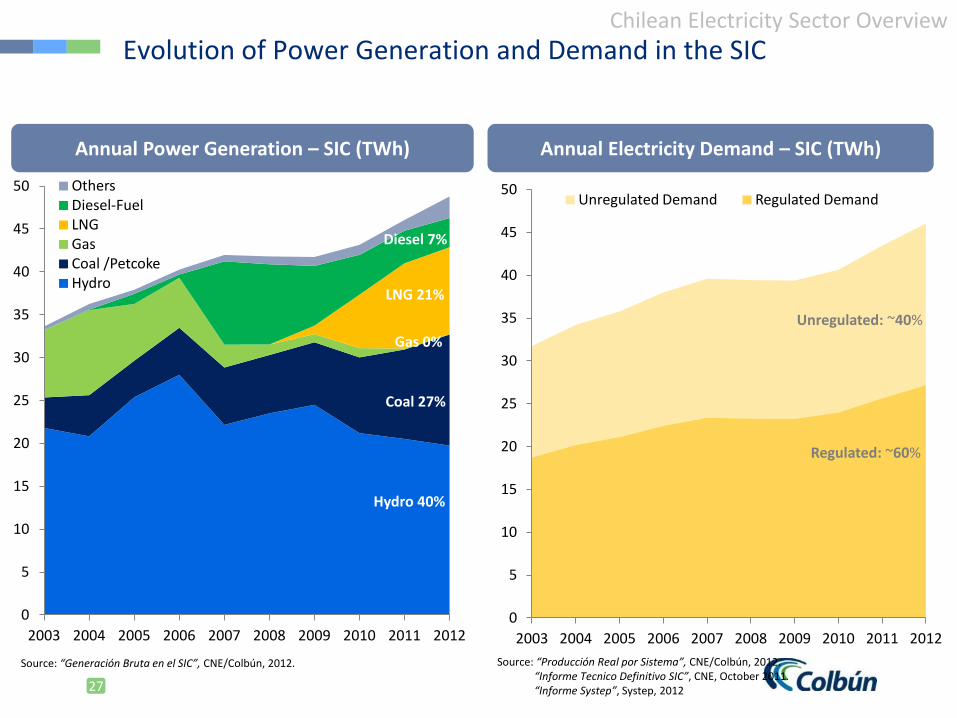

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Others Diesel-Fuel LNG Gas Coal /Petcoke Hydro

Diesel 7%

Coal 27%

Gas 0%

Hydro 40%

LNG 21%

0

5

10

15

20

25

30

35

40

45

50

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Unregulated Demand Regulated Demand

Unregulated: ~40%

Regulated: ~60%

Evolution of Power Generation and Demand in the SIC

Annual Power Generation – SIC (TWh) Annual Electricity Demand – SIC (TWh)

27

Source: “Producción Real por Sistema”, CNE/Colbún, 2012. “Informe Tecnico Definitivo SIC”, CNE, October 2011. “Informe Systep”, Systep, 2012

Source: “Generación Bruta en el SIC”, CNE/Colbún, 2012.

Chilean Electricity Sector Overview

OBJECTIVE Meet demand at the lowest cost possible

INSTITUTION Independent load dispatch center (CDEC) coordinates the efficient dispatch of electricity producers

MODEL CDEC dispatches plants in ascending order of variable production cost

Prices vary according to the type of customer:

REGULATED CUSTOMERS

1) Node Price: calculated by the CNE every 6 months

2) Auction Price: auctioned under the supervision of the Regulator for bilateral LT contracts

UNREGULATED CUSTOMERS

3) Market Price: free price settled by both parties for bilateral contracts

OTHER GENERATORS

4) Spot Market Price: the variable cost of the most expensive dispatched plant at each moment of the day

All facilities are also paid a capacity charge for being available

Hydro

OC-Diesel

Coal

Thermo-Diesel

Output from available plants (MWh)

Var

iab

le C

ost

of

the

Pla

nts

(U

SD/M

Wh

)

CC-Diesel

Dispatched Plants Back Up Plants

*Margin = [Spot Price - Var. Cost]

Plants receive revenues from Capacity charge

Plants earn a Margin*

CC-LNG

SPOT PRICE

Marginal Cost of the System

Demand Curve

Dispatch and pricing model: a technical guide

Dispatch Model Dispatch Scheme

Pricing Model

28

Chilean Electricity Sector Overview

Source: “Costos reales marginales mensuales Alto Jahuel”, CDEC/ Colbún; “Historia precios nudos”, CNE; “Informes Mensuales Systep”, www.systep.cl Note (*): The market Price is calculated by the Regulator upon information provided by all generation companies. This average price does not includes the capacity charge component.

Evolution of electricity prices

Electricity Prices-SIC (USD/MWh)

29

0

50

100

150

200

250

300

350

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1) Energy Node Price Alto Jahuel (USD/MWh)

2) Average Auction price (USD/MWh)

3) Average Market price (USD/MWh)*

4) Energy Spot Market Price Alto Jahuel (USD/MWh)

Chilean Electricity Sector Overview

0

10

20

30

40

50

60

70

2011 2012 2013 2014 2015 2016

Source: “Informe Técnico Definitivo Fijación Precio Nudo SIC” ,CNE/Colbún, April 2012

Demand and Supply: what to expect in the coming years

Electricity Demand - SIC (TWh) Available Power by type - SIC (MW)

30

Source: “Informe Técnico Definitivo Fijación Precio Nudo SIC” ,CNE/Colbún, April 2012

(1) Considering normal hydro conditions

(2) Real gas output depends on fuel availability

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

2011 2012 2013 2014 2015 2016

Hydro (1) Wind Coal Gas (2) Diesel Max demand Min demand Average demand

Additional installed capacity: 562 MW Hydro 214 MW Wind 927 MW Coal

0 MW Gas and Diesel

Chilean Electricity Sector Overview