on the look-out for distressed assets? some tips and...

TRANSCRIPT

On the Look-Out for Distressed Assets? Some Tips and Considerations Navigating

Today’s Market

June 29, 2016

Phillina Lai, BP America Production CompanyJohn Melko, Gardere Wynne Sewell LLPEunice Song, Gardere Wynne Sewell LLP

GARDERE WYNNE SEWELL LLP AUSTIN | DALLAS | DENVER | HOUSTON | MEXICO CITY | gardere.com

Current State of the Market

2

Overall Theme: Mixed Signals• Since January 2016, the price of oil has ranged from a low

of $27 to a high of $50, which would be highest level seen in almost 11 months. [http://www.cnbc.com/2016/06/13/reuters-america-corrected-update-1-opec-sees-oil-glut-shrinking-in-second-half-of-year.html]

• What’s behind the increase?

– Global output disruptions, especially in Nigeria (averaging more than 3.6M/day, highest since January 2011). [http://www.wsj.com/articles/oil-prices-rise-supply-outages-in-focus-1462871742]

– Drop in U.S. rig count (although as of the second week of June, numbers are slowly creeping back up)

– OPEC (announcing more balanced supply/demand in 2nd

half of 2016)

– General investment interest in commodities[https://www.morningstar.com/news/dow-jones/energy/TDJNDN_2016060911/crude-oil-prices-stay-above-50.html]

Current State of the Market – Cont’d

3

• Impact of rally? Risk of encouraging more production too soon? According to U.S. Energy Information Administration, U.S. crude stockpiles fell by 3.2 million barrels in early June, but total crude output increased by 10,000 bbls. [http://www.marketwatch.com/story/crude-oil-prices-extend-gains-above-50-2016-06-09]

• Current Rig Count – Total for North America: 497 (as of June 24, 2016) (Compared to 1 year ago when it was 984) [http://www.wtrg.com/rotaryrigs.html]

• 2016 Deloitte Report – Nearly 35% of publicly traded E&P companies (~175 companies) are considered “high-risk” based on their combination of high-leverage and low-debt service coverage ratios. [“The crude downturn for exploration & production companies – One situation, diverse responses” – Deloitte Report 2016, Deloitte Center for Energy Solutions]

Current State of the Market – Cont’dRecent E&P Bankruptcy Filings (2016 only)

4

• Aurora Operating, LLC • MOG Producing, LP • Antero Energy Partners, LLC • Emkey Resources, LLC • Osage Exploration and Development,

Inc. • Ginger Oil Company • Primrose La Sara, LLC • Argent Energy Trust • Argent Energy (U.S.) Holdings, Inc. • D.J. Simmons, Inc. • RMR Operating, LLC • New Source Energy Partners, LP • Venoco, Inc. • Emerald Oil, Inc. • Whistler Energy II, LLC • 7711 Operating Company, LLC • Postrock Energy Corporation • Bluff Creek Production, LLC • Aztec Oil & Gas, Inc.

• Energy XXI Ltd. • Goodrich Petroleum Corporation • Trinity River Resources, LP • Paladin Energy Corporation • Ultra Petroleum Corp. • Pacific Exploration & Production Corp. • Midstates Petroleum Company, Inc. • Calera Gas, LLC • Aurora Gas LLC • Chaparral Energy, Inc. • Linn Energy, LLC • Berry Petroleum Company, LLC • Penn Virginia Corporation • Breitburn Operating LP • Sandridge Energy, Inc. • Connacher Oil and Gas Limited • Ricochet Energy, Inc. • Intervention Energy Holdings, LLC • Linc USA GP • Hydrocarb Energy Corporation

Current State of the Market – Cont’dRecent Distressed/Downturn Triggered

Transactions

5

- Global M&A activity dropped in 2015 by 11% but given the current state, that trend appears to be reversing for increased activity in 2016. [www.rigzone.com/news/article_pf.asp?a_id=143261]

– Marathon Oil Corp.’s acquisition of PayRock Energy Holdings LLC (announced June 20, 2016) [Oklahoma-based assets]

– BP’s (Lower 48) acquisition of San Juan basin assets (NM/CO) from Devon Energy Corp. (announced December 18, 2015)

– Pioneer Natural Resources’ acquisition of Midland basin assets from Devon Energy Corp. (announced June 16, 2016)

– Newfield Exploration Co.’s acquisition of Oklahoma assets from Chesapeake Energy Corp. (announced May 5, 2016)

– Energen sale of its non-core Delaware and San Juan basin assets to undisclosed buyers (announced June 21, 2016)

– QEP Resources, Inc.’s acquisition of Permian Basin assets from undisclosed individuals and entities (announced June 21, 2016)

Current State of the Market – Cont’d

6

• Given the current state, as just illustrated, many companies are looking to shed non-core assets to stay afloat. Others will need to sell all assets. Consequently, there are a lot of distressed assets for the taking. If you’re on the look-out to acquire, what should you be familiar with and/or consider?

Today, we’ll cover the following topics:

- Acquiring Distressed Assets In Bankruptcy

- Acquiring Distressed Assets Outside of Bankruptcy

- Specific concerns and considerations when dealing with Oil & Gas Distressed Assets

7

Acquiring Distressed Assets In Bankruptcy

Acquiring Distressed Assets in Bankruptcy – Cont’d

8

• If you’re considering a transaction with a distressed seller, consider insisting on a bankruptcy filing and sale free & clear of liens, claims and encumbrances under section 363 of the Bankruptcy Code for sale of all or a portion of distressed seller’s assets.

• Benefits:- Insulation from later fraudulent conveyance/avoidable

transfer claims- Relative ease of clearing title to assets, provided proper notice has been given

– Findings that buyer is not a “successor in interest” to debtor

– Note: Sale is “free and clear” only if: • Consent from entity with interest in property, or• If no consent, if the interest is lien, price paid for

property is greater than aggregate value of all liens

9

• Usual paths to 363 bankruptcy sale:

– Path 1 - pre-negotiated sale

• Debtor and proposed buyer work out agreement and terms of sale, often before the bankruptcy filing, then the debtor files a motions to sell.

• Frequently, in a fire bankruptcy, Debtor will have hired an IB to run a process which would have yielded an offer.

– Path 2 - Debtor files motion and markets assets openly or to identified potential bidders

• IB or broker distributes a teaser• Collects non-binding expressions of interest • Sets up data room• Requires NDAs• Selects “Stalking Horse” buyer• Diligence/Solicitation process – 60 to 120 days range

Acquiring Distressed Assets in Bankruptcy – Cont’d

Acquiring Distressed Assets in Bankruptcy – Cont’d

10

• The Bankruptcy Code has processes intended to increase value asset sales bring into the Debtor’s bankruptcy estate. For example:– Nearly all bankruptcy sales are subject to “higher and

better” offers to maximize value for the estate.– Buyers being frozen out or ignored by Debtor can assert

pressure through secured lender or Creditors’ Committee.– Secured lenders’ participation in sale process is made

clear:• Will lender “credit bid”? • Does lender have veto power?• Has the Court limited credit bids?

11

Acquiring Distressed Assets in Bankruptcy – Cont’d

Milestones of a 363 Asset Sale

• 363 Sale Timelines: Time from initial motion for approval of sale can vary drastically for both legal and business reasons, but Bankruptcy Rules and Local Rules generally require a 21 day to 35 day period in non-emergency circumstances after the marketing period (60-120 days).

• Bid Procedures Motion– Luca: September 18, 2015

• Bid Procedures Order– Luca: October 27, 2015

• Notice of Sale• Due Diligence and Collecting Bids• Auction (if more than one qualified bid received)• Sale hearing and Sale Order

Acquiring Distressed Assets in Bankruptcy – Cont’d

Components of a Bid Procedures Motion

12

• Substantive basis for proposed sale– “sound business justification” (i.e., lack of capital, operational

loss, lender fatigue)• Proposed sale procedure. May include:

– Notice procedures;– Marketing and solicitation procedures;– Due diligence procedures and proposed form NDA;– Stalking horse procedures and terms of stalking horse

agreement;– Bidding procedures and proposed form of qualified bid; – Auction procedures.

• Proposed Orders– Almost always need to submit proposed order approving

sale/bid procedures;– Some jurisdictions require submission of proposed order

approving sale itself with initial bid procedures motion, as well.

Acquiring Distressed Assets in Bankruptcy – Cont’d Asset Sales Outside of the Ordinary Course

13

• § 363(b)(1) of the Bankruptcy Code allows trustee to use, sell, or lease property outside the ordinary course of business BUT:

– Adequate and reasonable notice required– Court approval required

• Proponent must demonstrate “sound business justification.”– Common justifications: (1) avoid unnecessary

administrative costs; (2) time is of the essence; (3) preserve going concern value; (4) no ongoing operations alternative.

Acquiring Distressed Assets in Bankruptcy – Cont’dIf Seller is already in bankruptcy, why be the

“Stalking Horse”?

14

• Stalking Horse structure designed to draw other bidders into the bidding arena. Stalking Horse may be out-bid, but advantages to being Stalking Horse are:

– Stalking Horse gets to structure the deal through initial negotiations with sell;

– Competing bidders generally have to bid on your terms;– If outbid, the Stalking Horse gets a break up fee to

compensate for its time and risk—generally in the range of 2–3% of the purchase price (smaller deal can be higher);

– Legal and diligence fees negotiated on top of the break up fee, but not always.

• The Debtor also wants to be compensated for its time, and generally builds that in to the “upset bid”.

Acquiring Distressed Assets in Bankruptcy – Cont’dThe Minimum Upset Bid

15

• Thus, the minimum bid to “top” or upset the existing bid must equal or exceed:

Buyer’s Purchase Price +Breakup fee+Expense reimbursement+Debtor’s incrementMinimum Upset Bid

Acquiring Distressed Assets in Bankruptcy – Cont’d Bidding and Auction

16

• If there is no Upset Bidder, then the Buyer closes the deal.• If there is a competing bid, then it goes to open auction among “Qualified Bidders”. • General requirements for Qualified Bidder:

– Demonstrate financial wherewithal to close; – Post required earnest money; – Deliver conforming APA; – Agree to be the “standby bidder” in case selected buyer

fails to close.• At auction, the Stalking Horse Bidder gets a “bidding credit” equal to the breakup fee and any expense reimbursement.

17

Acquiring Distressed Assets Outside of Bankruptcy

Acquiring Distressed Assets Outside of Bankruptcy –

Structured Distressed Sale

18

• What is entailed?

– Seller conveys property to Buyer and enters into separate agreement with Seller’s creditors to satisfy associated debt.

– Purchase and Sale Agreement:

1) Seller agrees to convey property (escrowed until creditors claims are resolved) in exchange for Buyer’s agreement to satisfy Seller’s debt related to property.

2) Buyer’s due diligence phase (contract review, current lien search, accounting and land files, title search, oilfield mechanics and materialmen liens (keep in mind, these can be filed up to 180 days after date of service or materials provided))

3) Pref Rights (unclear treatment - some courts may allow money satisfaction for such interest; pref right may still be enforceable even after debtor has rejected based on executory contract reasoning)

– Creditors’ Agreement:

1) Between Buyer and Seller’s creditors; details Buyer’s plan to pay off debts.

2) Closing occurs when certain percentage of secured and unsecured creditors accept. (Junior creditors may be more incentivized to agree given potential for more favorable treatment under this approach.)

3) Delayed payments to creditors possible.

Acquiring Distressed Assets Outside of Bankruptcy – Structured Distressed

Sale Cont’d

19

Why Consider this Approach:- May take less time. - You may end up paying more under a 363 sale/auction. - Easier to maintain confidentiality.

Associated Risks:

1) Speedy/Limited amount of due diligence

- Mitigate risk through reps/warranties, but likely illusory. - Consider M&A insurance as further protection.

2) Fraudulent conveyance claims.- Need to prove reasonable equivalent value.- Independent fairness opinion from investment bank.- Keep in mind, exposure exists for applicable statute of

limitations.

20

Specific concerns and considerations when dealing with Oil & Gas

Distressed Assets

Considerations for Distressed Oil & Gas Assets – Executory ContractsWithin 363 Asset Sale Context

21

• Treatment of Executory Contracts– Contract in which “the obligation of both the bankrupt and

the other party to the contract are so far unperformed that the failure of either to complete performance would constitute a material breach excusing the performance of the other.” [Countryman, Executory Contracts in Bankruptcy: Part I, 57 Minn. L. R. 439, 460 (1973].

– In the bankruptcy context, executory contracts can be rejected, assumed or assumed and assigned by debtor under Section 365 of the Code. [based on debtor’s business judgment standard (i.e., reasonable, good faith)]

Considerations for Distressed Oil & Gas Assets –

Within 363 Asset Sale Context – Cont’d

22

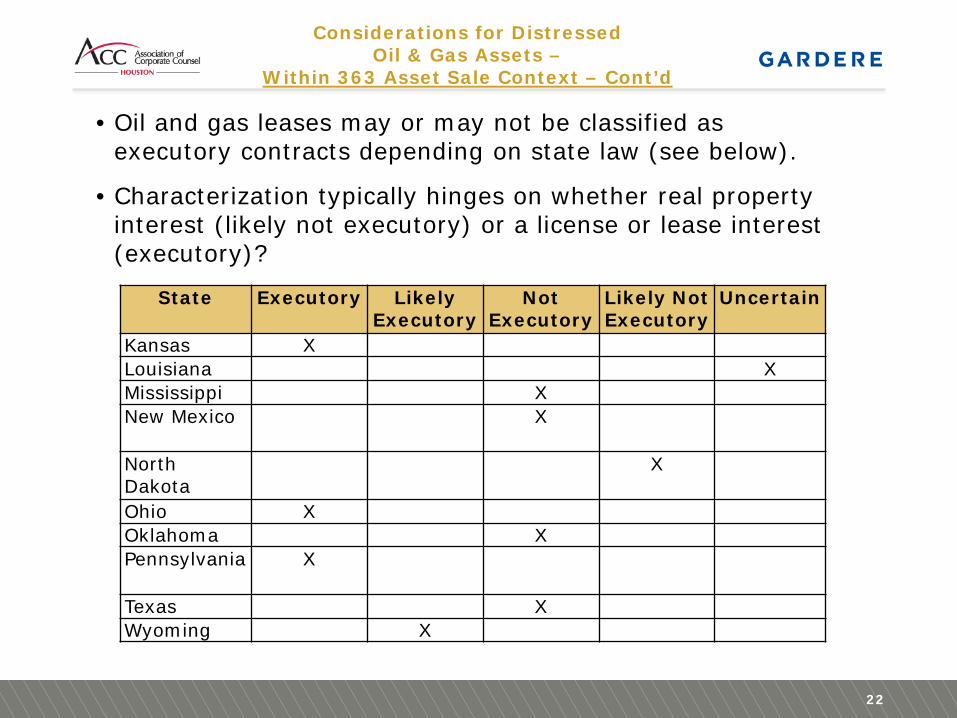

• Oil and gas leases may or may not be classified as executory contracts depending on state law (see below).

• Characterization typically hinges on whether real property interest (likely not executory) or a license or lease interest (executory)?

State Executory Likely Executory

Not Executory

Likely Not Executory

Uncertain

Kansas XLouisiana XMississippi XNew Mexico X

North Dakota

X

Ohio XOklahoma XPennsylvania X

Texas XWyoming X

Considerations for Distressed Oil & Gas Assets –

Within 363 Asset Sale Context – Cont’d

23

• Joint operating agreements and farmout agreements are typically viewed to be executory contracts.

• Department of Interior occasionally takes position that OCS leases are not “mineral interests” but lease or license rights executory.

Considerations for Distressed Oil & Gas Assets –

Within 363 Asset Sale Context – Cont’d

24

• As potential buyer, need to figure out what contracts are desired based on your due diligence.

• Avoid blanket assignments (too risky). Instead, develop specific listing of desired contracts or conversely, list of rejected ones.

• If debtor decides to assume and assign a particular contract, trustee may assign only if third party assignee demonstrates adequate assurance of future performance of such contract, whether or not there has been default.

Considerations for Distressed Oil & Gas Assets –

Within 363 Asset Sale Context – Cont’d

25

• How do Consent to Assignment Requirements Play Out?

• If a contract is an executory contract, requirement to obtain consent to assignment can be avoided under safe harbor provisions of the Bankruptcy Code 365(f)(1).

• However, for non-executory contracts, further analysis is required – is the consent requirement a personal covenant of debtor/leaseholder or is it a covenant running with the land?

• If a personal covenant, it is not tied to the land so 365(f)(1) will apply and the debtor should be free to assign without obtaining consent.

• Exceptions: personal services or government contract; loan agreements.

Considerations for Distressed Oil & Gas Assets –

Within 363 Asset Sale Context

26

• Consider state and federal obligations that might have impact –

– Plugging requirements and surety bonds (Tex. Nat. Res. Code Ann. §89.011 and 30 CFR §256.52). Be concerned that distressed sellers may not be in full compliance as they will inevitably be looking to cut corners. APA should address who shall remain liable for plugging and abandonment obligations. Side note: Outside of Bankruptcy context, non-major industry players may be required to post private bonds as part of the deal.

– To ease potential burden from buyer’s perspective, strongly consider escrows, holdbacks (but given competitive bidding scenario, not likely)

• Look out for statutory liens that may not be immediately apparent.

• Beware of environmental issues, such as water run off issues and wetland incursions, which can result from underfunded operations.

• Can’t rely on reps/warranties in APA, conduct direct investigation, especially on the environmental front.

Questions?

GARDERE WYNNE SEWELL LLP AUSTIN | DALLAS | HOUSTON | MEXICO CITY | gardere.com

Offices

28

Austin3000 One American Center600 Congress AvenueAustin, Texas 78701

Dallas3000 Thanksgiving Tower1601 Elm StreetDallas, Texas 75201

Denver200 Union Boulevard, Suite 200Lakewood, Colorado 80228

Houston2000 Wells Fargo Plaza1000 Louisiana StreetHouston, Texas 77002

Mexico CityTorre Esmeralda IIBlvd. Manuel A. Camacho No. 36-1802Lomas de ChapultepecMexico, D.F. 11000