online banking tools of standard chartered bank and its ... · standard chartered bank as primary...

TRANSCRIPT

1

Online Banking Tools of Standard Chartered Bank and its Impact on Building and Maintaining

Customer Relationships

XpertSolver.com

2

Table of Contents Abstract ........................................................................................................................................... 5

Chapter One: Introduction .............................................................................................................. 6

Background ................................................................................................................................. 6

Purpose or Rationale ................................................................................................................... 6

Research Aims ............................................................................................................................. 6

Research Objectives .................................................................................................................... 6

Research Questions ..................................................................................................................... 7

Hypothesis ................................................................................................................................... 7

Chapter Two: Literature Review .................................................................................................... 9

Demand of SCB’s Online Banking Tools ................................................................................... 9

Future Demand of Online Banking Tools ................................................................................. 10

Customer Relationship Management and Online Banking Tools ............................................. 11

SCB’s online Banking Tools ..................................................................................................... 11

Advantages ............................................................................................................................ 12

Internet Banking Tools and Customer’s Satisfaction ................................................................ 12

Cost Perspectives of Online Banking ........................................................................................ 15

Customer’s Perception on usage of Online Banking Tools ...................................................... 15

Determinants of Customer’s Satisfaction with Online Banking ............................................... 17

Determinants of Consumers Behavior ................................................................................... 18

Measurement of Service Quality ............................................................................................... 18

Perceived Soft Quality of Service ......................................................................................... 19

Measurement of Client Factors.............................................................................................. 19

Customer’s Satisfaction towards Online Banking Services ...................................................... 20

Consumers Satisfaction ......................................................................................................... 20

Corporate Image .................................................................................................................... 21

Consumer Retention .............................................................................................................. 21

Switching Barriers ................................................................................................................. 21

Service Quality, Customer Trust, Customer Satisfaction and Loyalty in Online Banking ....... 23

Service Quality Dimension of Customers Satisfaction in Online Banking .............................. 25

Tangibles ............................................................................................................................... 26

XpertSolver.com

3

Reliability .............................................................................................................................. 27

Responsiveness ...................................................................................................................... 27

Empathy ................................................................................................................................. 28

Assurance............................................................................................................................... 28

Chapter Three: Research Methodology ........................................................................................ 31

Research Approach ................................................................................................................... 31

Research Strategy and Design ................................................................................................... 32

Qualitative Method ................................................................................................................ 32

Quantitative Method .............................................................................................................. 33

Primary Data Collection ........................................................................................................ 34

Sampling Selection .................................................................................................................... 36

Data Analysis ............................................................................................................................ 37

Ethical Issues ............................................................................................................................. 37

Accessibility Issues ................................................................................................................... 37

Research Limitations ................................................................................................................. 38

Chapter Four: Results & Analysis ................................................................................................ 39

Users of Internet Banking ......................................................................................................... 39

Reason for Using Internet Banking ........................................................................................... 40

Frequency of Using Online Banking Tools ............................................................................... 41

Online Banking Service Attribute ............................................................................................. 42

Additional Attributes of Online Banking Tools ........................................................................ 43

Customer Level of Satisfaction ................................................................................................. 44

Bill Payment .......................................................................................................................... 45

Online Cheque Book Ordering System ................................................................................. 45

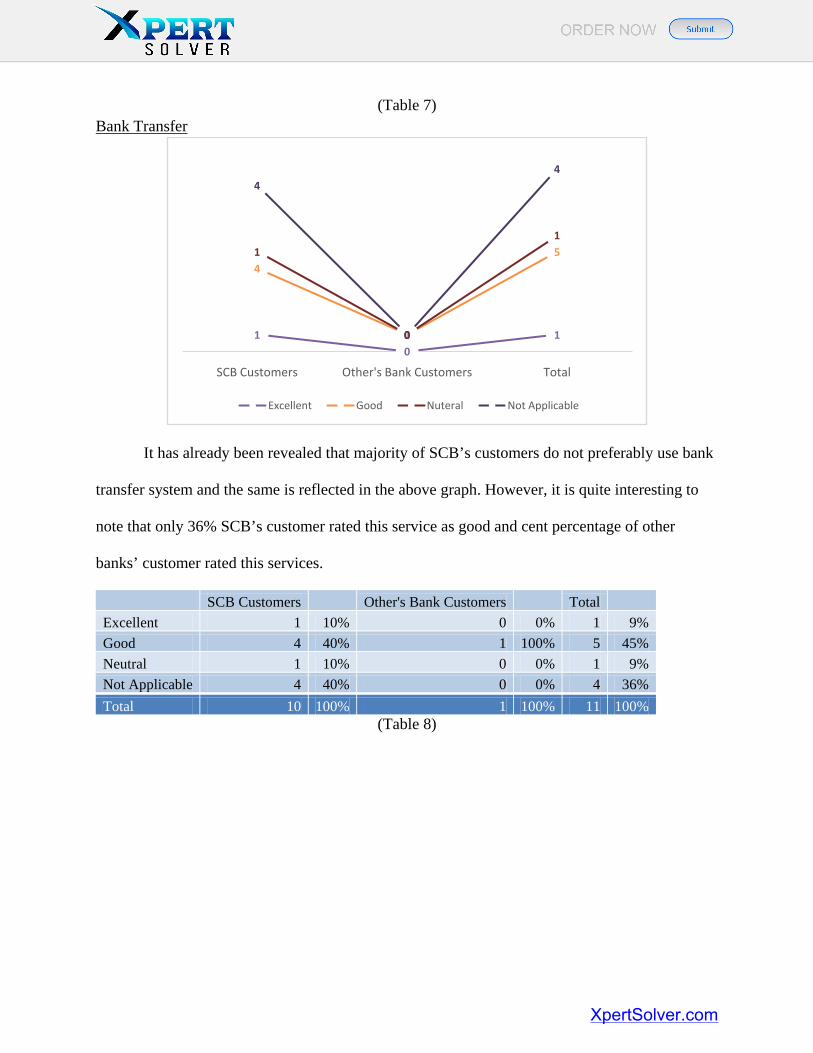

(Table 7) ................................................................................................................................ 47

Bank Transfer ........................................................................................................................ 47

Stop Payment ......................................................................................................................... 48

Balance Inquiry...................................................................................................................... 49

Accessing Bank Statement .................................................................................................... 50

Additional Service Attributes of Online Banking Tools ........................................................... 50

Preferences of Online Banking Tools ....................................................................................... 52

XpertSolver.com

4

Awareness of the Services and its Benefits ........................................................................... 52

Ease of Use or User Friendliness ........................................................................................... 53

Safety and Security of Transacting Over the Internet ........................................................... 54

The Cost of Using Internet Banking ......................................................................................... 54

Security and Privacy of Online Banking ................................................................................... 55

Importance of Interaction in Online Banking ........................................................................... 57

Customer Satisfaction Level of Online Banking ....................................................................... 58

Hypothesis Result .......................................................................................................................... 58

Focus Group Discussion............................................................................................................ 64

Chapter Five: Discussion .............................................................................................................. 66

Chapter Six: Conclusion/Recommendations ................................................................................ 68

XpertSolver.com

5

Abstract In current dynamic corporate environment, online banking tools are most commonly used by

Standard Chartered Bank as primary resource to satisfy its customer. Online transactions and

online banking will further increase in future years because online banking tools used by

Standard Chartered Bank provides strong base for e-commerce. Furthermore recent trend of

having online trading and e-commerce division along with physical existence of business caused

by increase in requirement of processing fast transactions. It is justified to express that online

banking tools have became promising field to facilitate the business of 21st Century. Further to

Asia, Eastern Europe and African markets have also potential for online banking tools used by

Standard Chartered Bank.

XpertSolver.com

6

Chapter One: Introduction Background

Not only in banking industry, information technology acted as major and primary driver

of changing the operating styles of almost every industry. More specifically among information

technology tools, internet or online technology had played substantial role in changing the

operational styles or methodology by improving efficiency of organization and reducing cost

which further strengthens the efficiency of an organization (Riquelme, Mekkaoui& Rios, pp. 1-6,

2009).

Purpose or Rationale

Along with the introduction of e-commerce methodology where overall business

operation is conducted through using online technology; this also includes placing or processing

customer orders online (Ho & Lin, pp.5 – 24, 2010). In order to support the payment function of

online orders of customers, SCB have to start its operating activities online in order to provide

fast, easy and quality services along with satisfying the new emerging need of its customers.

Research Aims This research is aimed to analyze the current online banking tools used by Standard

Chartered Bank (SCB) in order to meet the newly emerged need of its customers. Further to this,

in order to include the future or potential impact of online banking tools, this research is also

aimed to explore the potential of improvement in online banking with the help of current online

banking tools used by SCB.

Research Objectives • To analyze how online banking tools satisfy the customers.

XpertSolver.com

7

• To examine the current level of customer satisfaction in terms of online banking tools at

standard chartered bank

• To gain understanding of quality dimensions that impact level of satisfaction while using

internet banking tools.

• To make recommendation to SCB about potential improvement in online banking tools

after considering the online banking needs.

Research Questions • What are the specific customer needs or expectations regarding online banking services

offered by SCB?

• Are online banking tools currently used by SCB adequate enough to satisfy its customers

need?

• What is the potential demand of online banking tools currently used by SCB? Should

SCB invest further in its online banking tools?

• What are the competitive and Customer enhancements associated with online banking

tools of SCB?

• What are the primary benefits of online banking tools to the customers of SCB?

Hypothesis H0: Customer’s level of satisfaction in terms of online banking services offered by SCB is

positively related to service attributes.

Ha: Customer’s level of satisfaction in terms of online banking services offered by SCB is not

positively related to online service attributes.

XpertSolver.com

9

Chapter Two: Literature Review

All over the 20th Century, there is much remarkable advancement in terms of

technological updates. However, among the all, internet is the one of major technological

advancement occurred in the second last decade of 20th Century. Specifically, online tools have

impacted service, trading and banking activities and they all are conducted through internet

technology (Yap, Wong, Loh&Bak, p. 8-14, 2010). Different phases of business starting through

purchasing raw materials to management of supply chain including payments, sales and all

financing activities have been evolved due to adoption of online tools in business activity.

Furthermore recent trend of having online trading and e-commerce division along with

physical existence caused by increase in urgency of processing fast transactions, payments,

transfers, deposits, etc. (Sharma, p. 29-36, 2011), along with increase in growth of internet users

and considering the importance of banking role in all trading and transition activities, it is

justified to express that online banking tools have became promising field to facilitate the

business of 21st Century (Riquelme, Mekkaoui& Rios, pp. 1-6, 2009).

Demand of SCB’s Online Banking Tools In current dynamic corporate environment, online banking tools are most commonly used

by SCB as primary resource to satisfy its customer. With the help of online banking tools, all

communication can be processed immediately along with length and distance of communication

decreases the cost (Phan& Vogel, pp.58 – 72, 2010). There is a tremendous growth of online

baking tools for SCB in future because of growth of internet population all over the world.

Specifically Asia is the most dominant region where online banking customers are consistently

increasing (ECL, pp. 26-31, 2007).

XpertSolver.com

10

Future Demand of Online Banking Tools Online transactions and online banking will further increase in future years because

online banking tools used by SCB are the strong base for e-commerce. This means for trade that

are actually taken place over internet using online technology, where buyer visits the seller’s

website and processes its transactions there (Ngaia, Xiub&Chaua, pp. 56-62, 2009). Such way of

doing business is consistently increasing and will increase in future. Considering the fact that

these methodology of business can only be adopted by using online banking tools offered by

SCB, the demand of such tools will also increase in future. Further to this, online banking of

SCB not only satisfy the needs of large corporate users, but it also serves further type of

businesses either service, small, large, B2C, B2B and production (Zhengwei, pp. 1601-1608,

2012).

Comparative to current demand of online banking tools, there is a slow pace of

introducing new online banking tools or using existing online banking tools by SCB because of

lacking in using a reliable communication and networking infrastructure along with inadequate

control and planning techniques (Guttmann, pp. 14-19, 2002). However, SCB is (IPM) adopting

interpersonal main), EFTOPS (Electronic funds transfer at point of sale) and another supporting

technological tools to strengthen the level of confidence and reliance of its customers over online

banking channels and tools offered by SCB (Baskar, p. 45 – 51, 2010).

After implementation of such tools by SCB and other industries it will then increase the

use of online banking tools specifically after wireless systems and technology will become

uniform all over the industry and all over the world. Demand of online banking tools offered by

SCB will further grow and when the transaction all over the world could be carried out through

online banking channel, exchange rate problem that business faces will be resolved to significant

XpertSolver.com

11

extent (Yu-Qian& Chen, p. 482-498, 2012). Because all transactions would be carried out in real

time so they will be having sufficient applicable information about the exchange rates.

Customer Relationship Management and Online Banking Tools The first response of SCB’s customer towards after offering online banking tools was like

“show me my money.” It was the instinctive reaction of SCB’s customers when they realized

that their personal finances can be represented on any anonymous computer (Lee, pp. 27-35,

2007). It was the significant transformation of banking from high streets to cyberspace. When the

online banking tools allowed the customers of SCB to access their account at anywhere, at any

time either day or night despite of visiting their local branch or branch where they have opened

account (Yu-Qian& Chen, p. 482-498, 2012).

Further to this, online banking tools also helped SCB to keep record and track of

customer’s valuable information. Specifically, online banking tools enable SCB to individualize

the offer and customer services (Riquelme, Mekkaoui& Rios, pp. 1-6, 2009). Information

gathering about its customers and their preferences enabled SCB to personalize its products in

accordance with every expectation of its customers.

SCB’s online Banking Tools Between the accounts money transfer, paying utility bills and purchasing mobile credits

were the straight forward online banking tools initially offered by SCB. Round the clock,

accessing, controlling and managing account or money became easier for customers (Riquelme,

Mekkaoui& Rios, pp. 1-6, 2009). Further customer appreciated the online banking tools when

their cost of operating their accounts reduced, because customer of SCB can easily avoid

unnecessary several bank charges by using online banking tools of SCB.

XpertSolver.com

12

Advantages First and foremost advantage for SCB of using online banking tools is the low cost of

operating and selling its products and services to its customers (Lachowski, pp. 125-132, n.a).

Traditionally, serving cost of customers was very high, because SCB have to bear security,

supporting staff salaries, technical equipment, building maintenance and other types of fixed

costs. SCB has to invest substantial amount of money to bear its total fixed costs which

materially reduces the financial profits of bank. Or increasing the product and service prices

were the only option available to Standard Chartered in order to improve its financial profits

(Fjermestad& Romano, pp. 11-16, 2006)

Internet Banking Tools and Customer’s Satisfaction

Possibility of availing banking activities online with the help of online banking tools has

significantly improved the customer’s satisfaction level. One of the main satisfying factors is the

availability of banking activities 24/7, because official banking hours of Standard Chartered

collides with working hours of many customers (Zhengwei, pp. 1601-1608, 2012). Thus they

were unable to use banking activities, beside this; online banking tools of SCB resolved their

primary problem efficiently and effectively. Online banking tools of SCB provides quick and

efficient banking services as comparative to traditional banking tools.

Additionally, to facilitate its customers and capture more market, SCB has to establish its

branches in small towns where there were low potential of customers (Gardner, pp. 15-21, 2011).

However, after the introduction of online banking tools, Standard Chartered became in position

to facilitate those customers living in small towns where establishment of bank branches were

not financially sound (Yu-Qian& Chen, p. 482-498, 2012). Further to this, online banking tools

XpertSolver.com

13

does not brought expansion opportunity to local market level, but it also expended opportunity at

global market level

Implementation of information technology and advance communication tools changed

the way of doing business and increased the consumer needs, expectations, and demand. The use

of information technology and communication has created many new products, services, and

opportunities (Phan& Vogel, pp.58 – 72, 2010). Further, it created many new business oriented

ways and helping organizational staff in managing organizational core operations like planning,

controlling and co-ordination.

In order to support or facilitate the newly established ways of e-commerce, banks meets

customer’s new and changing expectations along with their new demand. Banking industry has

also introduced information and communication technology in order to make banking channel be

more competitive, reduce transaction cost, improve quality of services, fast response, creating

opportunities, facilitation of consumers and improve communication system between consumers

and bank management (Pikkarainen, Karjaluoto&Pahnila, pp.158 – 172, 2006).

SCB has competitive advantage in providing online banking services to its customers.

Further to SCB, other banks are also consistently making considerable investment in order to

utilize online banking tools to increase customer’s satisfaction. In 2008, by using information

technology some banks including SCB promote their banking servicing application software

(Ngaia, Xiub&Chaua, pp. 56-62, 2009). In order to increasing the role of information technology

in banking service, SCB introduce online banking and allowed consumers to team up with bank.

SCB is providing wide range of online banking products and services to its consumer.

SCB facilitates its consumers through online banking tools which allows them to receivemonthly

bank statements through e-mail, checked account status by online checking, using of online cash

XpertSolver.com

14

system, online funds transfer locally or internationally etc. (Mavri&Ioannou, pp. 552–560,

2006). All these SCB online services are creating competitive pressure to SCB competitors.

Here, one of the biggest think that, it is true in financial environment consumers has full freedom

to choose their satisfaction in their financial need. In considering these factors SCB is directing

their planning to increase consumer satisfaction and consumers loyalty by improving quality of

service (Mavri&Ioannou, pp. 552–560, 2006).

Quality of service is one the main issue for businesses and banking sector because,

through providing of good service quality banks are able to get consumers satisfaction. Because

consumer satisfaction is determine success or failure of business. SCB consider their consumers

first, in order to get consumers satisfaction SCB providing quality of online banking services to

its consumers and getting satisfaction from consumers because SCB known that consumers

satisfaction is require to becoming aggressive in working place (Pikkarainen,

Karjaluoto&Pahnila, pp.158 – 172, 2006).

In order to be competitive in working and consumers satisfaction SCB have adopted

online banking for its consumers. For the betterment of consumers satisfaction and service

quality SCB has offered online banking for communication with consumers concerning bank

statements. SCB has also been using online banking tools to give permit to its consumers to enter

their bank account anytime, anywhere and done local and international banking transactions

(Mavri&Ioannou, pp. 552–560, 2006). SCB is focusing many factors and also providing many

online banking services to maintaining consumer satisfaction. These services include sending

monthly bank statement through internet, allow checking cash in account through online cash

system and easily transfer of funds to local or international accounts through online transaction

XpertSolver.com

15

etc. All these online banking services provided by SCB is essential for banking success and

economic retune than competitors of SCB (Mannan&Oorschot, pp. 129-136, 2008).

Cost Perspectives of Online Banking Online banking service is becoming most important after the introduction of internet with

human. Another important perspective of online banking service is cost saving of banking

transactions and other banking activities (Kiang, Raghu, Shang &Huei-Min, pp 383-393, 2000).

Offering quality service to consumers and getting satisfaction form it at low cost, is the

prospective of aggressive benefit on online banking services.

SCB is considering the perspective of online banking services and has effectively reduced

in service, commission and organizational costs. With the help of online banking services SCB is

saving its cost and offering its consumer to use services at lowest cost and also offer highest

interest return to interest bearing consumers than other banks.

Customer’s Perception on usage of Online Banking Tools The amazing kind of modernization in technology and forceful combination of banking

with information technology made a standard shift in the banking sector. Technology creates its

world itself in the mind of users. Early nineties (1990) is considered as a time of involvement of

internet in banking sector (Lachowski, pp. 125-132, n.a). This start of internet banking is

established a unique system for banking sector. Internet banking is a type of system that permit

to financial consumers, individual or different businesses, to enter in account and get information

about funds, managing of business and gathering information about financial product or services

from internet.

XpertSolver.com

16

For the purpose of providing legal identification form online transaction, government of

United Kingdom is introduced Information Technology Act. After introducing the act of

information technology many banks of United Kingdom including SCB attempt internet banking

system to make available online banking solution (Lee, pp. 27-35, 2007). In recent scenario UK

consumers are going towards online banking service.

It is necessary to understand how consumers are appraised in online banking and creating

loyalty. Quality of service is main factor of determining the failure or success of online banking.

Consumer perception and their preferences of services quality have a considerable force on

banks success (Lachowski, pp. 125-132, n.a). Study about online banking helps in understanding

consumer perception against quality of service, consumer’s satisfaction, trust and loyalty and

also help in understanding about future of consumers behavior to evaluation of online banking.

In order tounderstand consumer’s attitude against recent banking service is able to

influence consumer decision to use online banking service or not. SCB believe consumers get

more and more educated, is able to getting insight in modern online banking (Lee, pp. 27-35,

2007). Now online banking is becoming leading concerning area for all upcoming banks in

United Kingdom.

Some studies indicate that the administration of bank is better understands consumers

perception about product and service offered by bank. Consumer perception is always influences

by consumer values. Consumers are considering valuable for every industry or businesses

because if consumers does not show their interest in company’s product or in servicing activities,

so all effort of organization consider meaningless (Mannan&Oorschot, pp. 129-136, 2008). Like

all industries or businesses, banking sector also require consumers acceptances or interest in their

activities. All banking sector require to fulfilling the consumers need and getting closer to firm

XpertSolver.com

17

because consumers have many alternative choices to get satisfaction. According to SCB,

consumers purchases based on values, SCB observed that consumers think neutrally and

positively about the result of product and situation during the use of product (Mavri&Ioannou,

pp. 552–560, 2006).

For the changing of consumer perception in favor of online banking service SCB hired

higher educated employees because employees were consider bank instrument and them services

create links between bank and consumer (Ngaia, Xiub&Chaua, pp. 56-62, 2009). Through

communicating with consumers and solving their problems, employees have ability to change

consumer trend and perception about online banking services.

SCB knows all influencing factors of consumer, consumers need quality of service, low

fees, high rate of return, and significant charges. For the fulfillment of consumers satisfaction

SCB providing excellent office services to its consumers, deposit based services, services to

consider consumers values, and also providing modern product and services to assure the

consumer needs, that is essential for consumers to pick online banking services offered by SCB

(Pikkarainen, Karjaluoto&Pahnila, pp.158 – 172, 2006).

All these promotional effect of SCB including providing significant information to

consumers by online banking in main areas, SCB is becoming able to change consumer

perception, level of satisfaction and level of loyalty.

Determinants of Customer’s Satisfaction with Online Banking Information about those factors is considerably important for financial sector to help in

getting consumer’s satisfaction, consumer’s loyalty and engaging to reused bank or organization

service (Lachowski, pp. 125-132, n.a). However, consumer satisfaction is closely related with

financial sector survival. Study conducted by Ian (2009) shows positive relationship between

XpertSolver.com

18

consumer’s satisfaction and consumer’s loyalty and online banking tools by which bank and

financial sector is getting income (Ian, pp. 61-69, 2009). Consumers need to get satisfaction at

lower cost offer by banks and financial sector.Financial sector knows the cost of attracting new

consumers higher than keeping existing consumer’s satisfaction and loyalty for higher earnings.

Financial banking sector focusing on consumer’s satisfaction, to giving satisfaction and loyalty

to make assure consumers exist with banks or financial sector (Ho & Lin, pp.5 – 24, 2010). All

these professional effort done by financial sector only for avoidance to consumer dissatisfaction.

Consumers require satisfaction and loyalty with the quality of service provider in one way or

another. However, if banks provide uninterested quality services product or services to it

consumers, so consumers have many ways to choose alternative services in option to switch off

from recent organization (Fjermestad& Romano, pp. 11-16, 2006).

Determinants of Consumers Behavior According to some studies there has been some misunderstanding over relationship

between quality of service and consumer satisfaction. Studies identify that satisfaction and

services quality determine original perception and therefore are the same (Guttmann, pp. 14-19,

2002). However, some studies identify that satisfaction with online transaction lead to overall

perception about firm’s perceived quality. As a common psychological perception that

satisfaction is initial step of consumer’s experience about quality of service (Gardner, pp. 15-21,

2011). So it is expected that high level of quality create higher level of consumer’s satisfaction.

Measurement of Service Quality In this regard we have some dimensions to measure service quality.

XpertSolver.com

19

Perceived Soft Quality of Service Perceived soft quality of service for financial sector indicate punctuality and power to

make agreements, contract and finalized budgets. Perceived soft quality of services also indicate

to done all work with speed and complete as early as possible (Greenbaum, pp. 103–104, 2012).

Perceived soft quality of service includes ability to understanding of consumers needs and

creates relationship between financial sector, cooperate and consumers with confidentiality.

Measurement of Client Factors Client factors identify the perceived advantage in financial institution by using time,

skills and finance in good way throughout the whole process from planning and implementation

steps.According to studies about United Kingdom consumer’s satisfaction was exists throughout

three measurement.

i. Overall Consumers level of satisfaction

ii. The level of which performance level up from expectation.

iii. Rating of performance related to provider of good services.

That is three measurements in which perceived value was operational and checked

quality and service relative to prices and prices related with quality of services (Ho & Lin, pp.5 –

24, 2010).

After considering those aspects, understanding soft process of service quality is less

important in service quality perception. This identify that SCB should need to focus on the hard

service quality area in order to influence consumers satisfaction (Ian, pp. 61-69, 2009). So it is

possible that, by the use of both hard and soft service quality SCB will be able to becoming

under in position on influences consumers behavior about quality of service of online banking

XpertSolver.com

20

service. Consumer satisfaction about the quality of service gives consumer loyalty and these

loyalty influence consumers to exits with SCB online service and continuously use those services

offered and provided by SCB.

Customer’s Satisfaction towards Online Banking Services After the valuable use of information technology all industry is becoming competitive,

not only banks but also other financial sectors are competing with each other (Kolodinsky,

Hogarth &Hilgert, pp.238 – 259, 2004). Mostly banks scarified their qualities of service in

competitive environment and focusing only one strategy to implement all possible factors to

remain competitive in banking industry.

Consumers Satisfaction It is require for organizations to understand consumers behavior because consumers

behavior identify consumers level of satisfaction and identify that consumers leave or stay with

an organization (Kolodinsky, Hogarth &Hilgert, pp.238 – 259, 2004). Organization is required to

understand how to maintain level of consumer satisfaction. Satisfied consumers do not looked

others because they that they never receive that services with satisfaction from to another place.

But unsatisfied consumers looked other organization to get better satisfaction. Different studies

indicate that approximately 40% of consumers leave their banks because they considered is to be

poor quality of services they have (Fjermestad& Romano, pp. 11-16, 2006). The only way to

keep consumers in hand, it is necessary for organization to provide better quality of services to

its consumer by which they get satisfaction.

XpertSolver.com

21

Corporate Image In recent days consumers have many options to fulfill their financial needs. Information

technology and globalization and high competition changed consumes expectation dramatically.

For keeping consumers in hand, one of the new factors used by organization and banking sector

is corporate image. Due to the improvement of corporate image many firms is using branding

techniques to being separate themselves (Guttmann, pp. 14-19, 2002).But here is a critical issue

for banking sector that all banks are offering same type of product to consumers. By using

branding, banks need to build and maintain their image through identifying the differences

between in all products which is also offered by its competitors (Fjermestad& Romano, pp. 11-

16, 2006).

Consumer Retention Consumer retention is important for organization to increase profitability by reducing of

cost for creating new consumers. A basic role of retention strategy consider as “zero cost of

getting profitable consumer” (ECL, pp. 26-31, 2007). Satisfaction with services and products

offer to it consumers by bank is important for generating consumers loyalty and that is absent in

retention situation. Here is different between loyalty and retention. Loyalty identifies consumer

repurchase behavior but situation is totally changed in consumer retention.

Switching Barriers Switching has been considered as a marketing strategy to make possible getting customer

satisfaction in low cost by switching to another organization. Use of switching barriers includes

different types of if consumer is thinks to leave (Duffee& Zhou, pp. 25-54, 2001). But negative

signs for organization that if they fail to satisfy consumers, so consumer will switch to other

XpertSolver.com

22

organization. In the way to avoid switching barriers firms need to fulfill consumer needs with

quality of services.

According to United Kingdom Commission study on people perceptions about online

banking service, study indicate consumer lack of trust on online banking and these lack of trust is

continuously discouraging consumer’s interest on e-banking (Claessens, Dem, De Cock, et. al.,

pp. 253-265, 2002). Understanding the difference between online banking and traditional

banking by SCB; SCB consider online banking system as a substitute of traditional banking

system, evidence of these consideration provide by SCB through offering modernized financial

services, more and more consumers adopting SCB modernized online banking services than

traditional banking system because technology is influenced to uses itself (Alsajjan& Dennis, p.

33-39, 2006).

Information technology is introducing new ways of businesses and also playing

significant role in increasing the level of banking sector. Initially SCB encourage their core

capabilities, products, services and advise to its consumers. After these SCB entered in online

banking and offer its online services and products (Fjermestad& Romano, pp. 11-16, 2006).

Future of banking sector is totally based on branchless system where consumers are able to enter

in banking system through remote. SCB believed that perception of consumers easy to change by

giving awareness about online banking. SCB needs to define online banking advantages to its

consumers like less charges, more profitable, friendly usage and secure system etc.

SCB thinks about consumers that they have two types of consumers one those consumers

who knows the internet use and able to enter in their online account easily, near SCB those

consumers who use internet easily to convinces and motivate about use of online banking and

also easy to change their perception and facilitate with moderated services (Bruce Ho & Dash

XpertSolver.com

23

Wu, p. 1835-1842, 2009). Second those consumers who does not use internet that consumers

becoming issue to SCB. It is a thing that SCB is concerning and thinking about the requirement

of awareness to those consumers to use internet and get benefit of online banking. SCB is

performing their best to enter those consumers in online banking toward traditionally or manual

banking (Baskar, p. 45 – 51, 2010).

Online banking service benefits like affordable charges, profitability, friendly usage and

secure system facilitates making payment on internet by using online transaction, transfer of

funds locally or international, applying of loans, making payments of loans, facilitate to perform

home business by using mobile or internet etc, and in more services like these SCB facilitates its

consumers effectively and efficiently (Greenbaum, pp. 103–104, 2012). These services offered

by SCB able to influences the individual perception about online banking use. Environment of

United Kingdom decision making of individual behavior surrounds in public (Guttmann, pp. 14-

19, 2002). So when people will see their friends, relatives and other people to performing online

transaction through online banking they may automatically influenced to use and get satisfaction

from online banking services.

Service Quality, Customer Trust, Customer Satisfaction and Loyalty in Online Banking

The important thing of accomplishment, survival and creating solid relationship with

consumers, it is necessary for financial institution to make sure consumers satisfaction, trust and

loyalty by focusing on service quality of online banking.

Different levels of studies show that trust of consumers totally based on quality of service

and quality of service increase level of consumers satisfaction and consumers satisfaction

increase loyalty of consumer (Aldás-Manzano, Lassala-Navarré, Ruiz-Mafé, et. al., pp.53 – 75,

XpertSolver.com

24

2009). These perceptive show that high level of consumers satisfaction cast high level of

consumer loyalty and loyalty influence to consumers to use product or services again and again

and show positive reaction in words for organization. On the bases of above lines we consider

that satisfaction and loyalty have strong positive relationship and also understand that

satisfaction is a leading determinant of consumer loyalty (Claessens, Dem, De Cock, et. al., pp.

253-265, 2002).

Now in recent days, online banking service is becoming important in international

business because of technology centric and based on information. In online operations banks and

financial sector is developing and providing best service quality to its consumers and improve

their service quality consistently (Acharya, Kagan & Lingam, pp.418 – 439, 2008). By giving

best service quality financial sectors have ability to affect consumer behaviors to online banking.

It is suggested in difference studies by delivering quality of service is influence consumer to use

services and get satisfaction with trust and would result in increasing consumer loyalty.

The relationship between consumer and service provider is the key to flourishing

business operation to maintaining business spirit and also helps in giving loyalty to consumer.

The result of relationship between consumer and service provider show that loyalty is influenced

by consumer satisfaction and consumers trust on online banking (Acharya, Kagan & Lingam,

pp.418 – 439, 2008). Studies suggest that online banking service providers improve their online

service quality to creating better relationship with their consumers to getting consumer

satisfaction and trust on online banking. And studies also suggest that poor online service quality

leads to reduce consumer satisfaction. For satisfaction of consumers financial institution needs to

provide better service with new trend of online banking and establish an environment where

XpertSolver.com

25

consumers will feel assurance, safety and familiarity (Bruce Ho & Dash Wu, p. 1835-1842,

2009). Banks needs to build beneficial relationship to establishing consumers trust.

On behalf of these phenomena SCB consider their existing consumers first though online

banking service (Chong, Ooi, Lin & Tan, p. 12-23. SCB gives best fulfillment of consumers need

because satisfied consumers more possible to reused SCB services and its opinion about SCB

will gather more consumers to SCB (Claessens, Dem, De Cock, et. al., pp. 253-265, 2002). By

providing good online banking services SCB performing their best to increase consumer level of

faith, assurance and feelings and convincing to use online banking services because SCB knows

bank image important for consumers to pick online banking services positively.

Service Quality Dimension of Customers Satisfaction in Online Banking Nowadays, onlinebanking services use is becoming important and use of internet in

businesses is becoming common part of our environment, importantly in communicating and

massaging technology (Bruce Ho & Dash Wu, p. 1835-1842, 2009). Online banking has

introduce many ways of banking for example, Television based banking, Personal Computer

banking, Telephone based banking, Internet banking etc all these banking activities require

internet to deliver online banking (Ho & Lin, pp.5 – 24, 2010). Experience of online banking

offered by SCB is continuously establishing by consumers satisfaction and service quality.

Consumer satisfaction is one of the essential for success of online banking. Consumers believe

that they are always right and consider them as a king. High level of consumer satisfaction

directly linked with high level of service quality (Greenbaum, pp. 103–104, 2012). In other

means, the return of high level of services quality influence consumers to use online banking

services.

XpertSolver.com

26

The usage of online banking offered by SCB to many financial organizations getting is

full of benefits. The main advantage of online banking is cost saving, secure privacy, getting

work done effectively and efficiently in shortest processing period. Through improving of

flexibility of business transaction and providing high speed of transaction SCB is getting

consumer satisfaction (Bruce Ho & Dash Wu, p. 1835-1842, 2009). All these are factors of

success for online banking to increasing consumer satisfaction. By the use of Online banking

services financial organizations and businesses unable to providing excellent services to its

consumers. So it is becoming important for organizations and businesses to make possible the

use of online banking system (Mannan&Oorschot, pp. 129-136, 2008). Online banking services

allow consumers to use their account from any place and any time in minimum cost. In recent

development by using smart phone online banking services growing extremely and many

consumers of traditional banking system is transferring to online banking system.

Understanding the relationship between consumers satisfaction and online banking

service quality. The studies indicate some dimensions of service quality as follows.

- Tangibles

- Reliability

- Responsiveness

- Empathy

- Assurance

Description of all dimensions identify in early step as below.

Tangibles Tangibles are means to providing physical service of bank premises; latest and up to date

setup of bank and manifestation of the bank’s human resources (Phan& Vogel, pp.58 – 72,

XpertSolver.com

27

2010). Generally consumers are always looked bank’s tangible signals about quality of services

which can be provided by SCB. Because of these tangibles consider most important factor on

behalf of consumer satisfaction (Phan& Vogel, pp.58 – 72, 2010). But here one of the important

factors is need to understand that, tangibles are not important to get consumers satisfaction in

online banking service.

Reliability It is essential for every business or organization to provide better technology and function

to its consumers with the accuracy and promises about services to get reliability of consumers

(Vatanasombut, Igbaria, Stylianou, et. al., 419-428, 2008). Reliability identify consumers feel

about services that they have paid for. Reliability considers the delivery of bank services toward

promises and expectation of consumers and accuracy. Studies about reliability shows, those

consumers are using online banking service consider essential determinant for reliability depth.

Further some studies concluded that consumers are more possible to use online banking services,

if they feel that their online transaction is more and more secure (Lee, pp. 27-35, 2007). Means

that consumer satisfaction is based on consumer reliability on online banking service is delivered

by SCB, if consumers relay on service quality of online banking they will automatically

influence to use online banking services.

Responsiveness Responsiveness shows quick response, service and power to resolve any issue or problem

if any issue or problem is found. Responsiveness also referred the ability of bank to provide their

punctual services to fulfill the consumer’s needs and get their satisfaction (Ngaia, Xiub&Chaua,

pp. 56-62, 2009). The users of online banking services feel that the online banking service is able

XpertSolver.com

28

to fulfill their needs faster than traditional banking system. Identification of important factors of

online banking services, fast transactions and easy access on accounts is considering main

elements for consumer satisfaction (Greenbaum, pp. 103–104, 2012). So due to faster service

and early response, responsiveness is considering important element of online banking service

for consumer satisfaction.

Empathy Empathy identifies the importance of concerning about individual behavior. Give

attention to individual consumer is important to getting consumers satisfaction. Communication

between bank staff and consumer are essential for identifying empathy depth. If consumers feel

that bank is giving significant importance to him individually (Mannan&Oorschot, pp. 129-136,

2008), so level of consumer satisfaction will automatically improve. In the lights of above

statement SCB is providing call center service to its consumers under online banking service,

through call center bank staff interacted with consumers and resolved consumers problems and

increase their level of satisfaction (Ho & Lin, pp.5 – 24, 2010). All these services of giving

importance to consumers, it is implementation on empathy by SCB.

Assurance Assurance is relate with believe of consumers on quality of service, degree of trust,

confidence, courtesy, knowledge and feeling of consumers about services (Bruce Ho & Dash

Wu, p. 1835-1842, 2009). Consumer assurance is one of the important factors of online banking

service. Consumers need assurance about online banking, if banks provide assurance about

quality of services, benefits, confidence, privacy, security, speed of working etc, all these factors

XpertSolver.com

29

of online service is able to influence or assure consumers positivity to use or utilize online

banking services.

This entire dimension like Tangibles, Reliability, Responsiveness, Empathy and

Assurance is playing important role to influencing consumer behavior to used online banking

services and in receiving of better satisfaction against traditionally banking system (Riquelme,

Mekkaoui& Rios, pp. 1-6, 2009). Though tangibles SCB is providing physical services by

upgraded bank setup to influence consumer behavior. By use of reliability SCB providing better

technological, functional services and accuracy to consumers for getting reliability of consumers

on online banking service. Responsiveness consider as quick response by organization

(Zhengwei, pp. 1601-1608, 2012). SCB always consider their consumers first in all places and

giving quick response to its consumer by using online banking, if consumers need SCB help.

Empathy is indicating to give importance to consumers individually.

In response of implementation on empathy, SCB is using call center services and also

hire educated person as employees and train him to interact with consumers in good behavior

and resolved consumers problems in friendly mode (Sharma, p. 29-36, 2011). Assurance

indicated consumers trust on services. SCB providing good services of online banking with fast

process, quality of services, accuracy, save and secure, privacy and many others benefit to

consumers for getting its assurance and satisfaction. Though statistical analysis we observed that

the relationship between online banking dimension and consumers satisfaction (Yu-Qian& Chen,

p. 482-498, 2012). By studies it is indicate that the consumer satisfaction directly influenced with

online banking dimensions and online banking dimensions able to change consumer behavior or

perception about the use of online banking services.

XpertSolver.com

31

Chapter Three: Research Methodology

The following chapter includes information about the research design. This chapter

highlights the means and ways utilized to conduct the underlying research. Specifically, this

chapter discuss about research approach, research methods, sampling technique and research

ethics. It will further discuss about qualitative method and quantitative methods along with

secondary and primary data, its reliability and validity.

Research Approach There are two most commonly utilized research approaches, which are inductive

approach and another is called deductive approach. These two are the primary stream of research

approaches. For the underlying research, deductive approach is utilized. This is also called top

bottom approach. Before conducting the research or data collection, broader theoretical concept

have been established and on the basis of those theoretical background, further theories are

narrowed down to reach in the depth of specific matters. This system is more systematic as

comparative to other research approaches.

However, on the other hand, inductive approach is just opposite of deductive research

approach. In deductive research approach, the direction of research is from top to bottom, but in

inductive research approach, the direction of research is from bottom to top. In this approach,

first data is collected. And after drawing desired sample size, it is then linked with the theoretical

concept. Basically, in this research approach theoretical background is tested on the basis of

sample size drawn from population of data collection.

Deductive research approach is utilized for this research as it is based upon identification

of underlying patterns and themes before data collection. In the second chapter of this research,

XpertSolver.com

32

theoretical literature regarding online banking, internet banking, customer satisfaction and

different relevant aspects of internet banking is reviewed. After then overall theoretical

framework is applied on online banking tools offered by Standard Chartered Bank.

Research Strategy and Design Further to research approach, explanatory, exploratory and descriptive are the three

specific research strategies to design the overall research strategy. Explanatory research strategy

is based on investigation of behaviour of variable associated with particular phenomena in

relation with the behaivour of other variables.

Descriptive research strategy is utilized for research issues which are previously

researched. It is just the presentation of information collected from different sources in

accordance with new point of views (Servon&Kaestner, p. 23-29, 2008). Exploratory research

is done on those variables that have never researched. Primary aim of exploratory research is to

find out findings for the first time. This research is not based on any theoretical concept. Instead

it creates theoretical backgrounds for other subsequent descriptive researches.

This research is based upon characteristics of explanatory research because it includes

obtaining information about the relationship between results and its causes among different

variables. And accordingly, in order to develop theoretical background, qualitative research

method is utilised. And for finding the behaviour of different variables, quantitative research

method is utilised.

Qualitative Method Qualitative research method is based upon theoretical data, it plays discussion role in

over all research. Qualitative method is used to discuss or express properties of variables that

XpertSolver.com

33

could not be expressed in numeric form (Servon&Kaestner, p. 23-29, 2008). Along with

different limitations, there are several advantages of using qualitative method. Firstly, it is based

on textual and narrative form which is more user friendly as comparative to quantitative research

method. Qualitative research method expresses the end result and outcome. It is considered as

direct channel of communication between researcher and the audience of research

(Sarel&Marmorstein, pp. 231-243, 2004). For this research, interviews, observations and focus

group discussion are the primarily used techniques to gather qualitative research. Further to these

qualitative data collection techniques, books and research articles were also played significant

role in overall establishment of literature review. On the other side, reliability of information is

the primary limitation of conducting research on the basis of qualitative data. Further to this, cost

and required time to conduct qualitative research are additional limitation to collect qualitative

data for the research.

Quantitative Method Quantitative research method is based on analysis of numeric data. Majorly, quantitative

data is collected through questionnaire and the same method is utilized to collect the quantitative

data for this research (Riquelme, Mekkaoui& Rios, pp. 1-6, 2009). Consent of respondents is

specifically considered during this activity and all respondents were provided by friendly

environment in order to gather unbiased and independent information. However, after gathering

response from all respondents sample responses are selected. It is assumed that the selected

sample perfectly represents the whole population and the overall population is normally

distributed.

Considering the advantages of both research methods, mix research method is used for

this research, that is quantitative and qualitative research method. Considering the fact that

XpertSolver.com

34

everything has its own advantages and disadvantages or limitations, combination or hybrid

approach is used to limit the inherent disadvantages of both research methods.

Primary Data Collection Investigation type of this research is twofold; it includes investigation of explanatory and

hypothesis testing study based quantitative as well as qualitative information (Zhengwei, pp.

1601-1608, 2012). More specifically, quantitative analysis would be based upon primary

research which will include collection of with the help of questionnaire.Further to this,

qualitative investigation would be based upon both primary and secondary information collected.

Questionnaire

Questionnaire comprised of 15 questions have sent to number of respondents who are

currently either customers of SCB and customer of any other bank, to collect the comparative

data.

Focus Group Interview

Focus group interview is conducted to collect wide range information regarding the

research questions through primary source. Participants in focus group interview were also

comprised of customers of SCB and other banks. However, it is specifically ensured that

respondents utilized in questionnaire activity do not participate in focus group interview, in order

to access wide range of information.

Secondary Data Collection

XpertSolver.com

35

Secondary data is called research on previously available data it could be both

quantitative and qualitative. For this research, journal articles, websites and books are manly

used to collect secondary data. However, the selection criteria are effectively implemented to

avoid selection of poor quality information source. Validity, availability and reliability are the

three main filter points to select secondary source of information. Accordingly, journals are the

most easily filtered secondary data sources as they usually represent current and relevant

information. On the contrary, book took long time to compile, edit, and printing, binding and

then publishing. Normally it takes at least a year to make it available for readers. Considering

this fact, current information could not be readily accessed through books. That is the primary

reason of using books in limited capacity to access secondary source of information.

Collection of unique data or collection of data for some specific purpose that is never

used before is called primary data (Yap, Wong, Loh, et. al. p. 8-14, 2010). As it includes

collection of unique data it requires cost and time to conduct such activity. For this research,

observation and questionnaire are the primary tools that are used to collect primary data.Further

to primary data collection, this data type also includes two main qualitative and quantitative data.

For this research, both qualitative and quantitative primary data is utilized. Main advantage of

using primary data is the control factor.

The whole research or data collection plan can be customized in accordance with the

research aim, objectives and purposes. By efficiently selecting the respondents, the reliability,

authenticity, validity and accuracy of data can be easily improved.

Further to this, customization of data property is easily modified in over developing the

framework for research. However, on the other side, data collection through primary sources

consumes time and it requires several re-testing of data in order to establish relationship between

XpertSolver.com

36

or among variables.Another main limitation of primary data collection is the time availability of

respondents. Often, respondents do not invest their time in our research without having any

benefit from our research. More specifically, no any type of benefit is provided to the

respondents of this research and accordingly response rate was less than 40%. However, it

constitutes that only serious respondents have participated in the primary data collection. So the

reliability, authenticity, validity and accuracy of data are inherently high.

There are two phases of research strategy. First phase of data collection includes data

collection from primary sources of information for both quantitative and qualitative

investigation. Moreover, quantitative data collection will be collected through conducting

questionnaire activity over selected sample class of people. However, data collection from

secondary sources for qualitative investigation will be from focus group interviews with SCB’s

employees and customers along with employees and customers of other banks in order to make

rational comparison among their satisfaction level.

Second phase of research strategy includes research from secondary sources for

qualitative investigation. It mainly includes data collection from previously conducted research

over online banking tools for customer relationship management in terms of customer

satisfaction. Among data collection from secondary sources, website of SCB will be widely used

to specifically gather data about specific online banking tools currently SCB to facilitate online

banking requirements of its customers. Further to this, peer reviewed journal articles and

different books are utilized to gather data from secondary sources.

Sampling Selection Overall population is divided in to two categories, customers of SCB and customers of

other banks. So, in order to ensure the selection of sample from every type of category, stratified

XpertSolver.com

37

sampling method is used for data sampling (Phan& Vogel, pp.58 – 72, 2010). And that is the

primary reason of using stratified random sampling considering the diversity of participants in

overall population. Overall population was65, and sample size is 50.

Data Analysis Data analysis plan is mainly divided in to threesections in accordance with the type of

investigation. Qualitative data is critically analyzed through focus group discussion in context

with other research over online banking tools for customer relationship management. However,

quantitative data is analyzed through two primary techniques; one is the percentage analysis and

another is testing of hypothesis against alternative hypothesis to meet the research objectives and

questions.

Ethical Issues Ethical issues always arise when researcher conducts data collection from primary

sources. Primary ethical issue is to protect the confidential information of participants especially

of those participants who are associated with SCB and other banks as employees. This ethical

issue is resolved by making personal information of participants confidential.

Accessibility Issues Accessibility issues is not experienced in data collection from previously conducted

researches or from secondary sources, because the selected sources are easily accessed through

online libraries or data bases like EBSCO Host, ERIC etc. and website of SCB is also easily

accessed. Further to this, there were some accessibility issues in data collection from primary

sources. As the data is collected from direct or online interaction with customers of SCB and

XpertSolver.com

38

other banks. Lack of time and low response rate was the primary accessibility issue for primary

data collection. However it has been easily managed by making proper coordination and

ensuring the commitment level of participants.

Research Limitations Information gathering from relevant and recent sources will be primary limitation at both

phases of research. However, such limitations are easily minimized by ensuring the reliability of

information source. Further to this, authenticity, sufficiency and adequacy of information were

another aspect of research limitation.

XpertSolver.com

39

Chapter Four: Results&Analysis

This research, conducted on online banking tools offered by Standard Chartered Bank

comprises of two sections. Section one represents the result of questionnaire by using percentage

analysis technique and hypothesis testing technique. Howeversection two represents focused

group discussion. The response rate of questionnaire was 80% which is far better than

expected.Overall, questionnaires were sent to 65 respondents belonging to SCB customer and

other bank’s customers. However, via random selection around 37 selected respondents were

SCB customers and 13 respondents were customers of other banks.

Users of Internet Banking

The table given below represents the user of internet banking within the selected sample.

From the data, irrespective of particular bank’s customer, it is clearly shown that most of the

people around 85% are the user of internet banking facility. However, only minimal percentage

around 14% of both categories is non users of internet banking that their respective bank offers.

It clearly illustrates that there is huge potential in offering banking tools to compete in the

industry.

SCB Customers

Other's Bank Customers

Total

Yes86%

No14%

XpertSolver.com

40

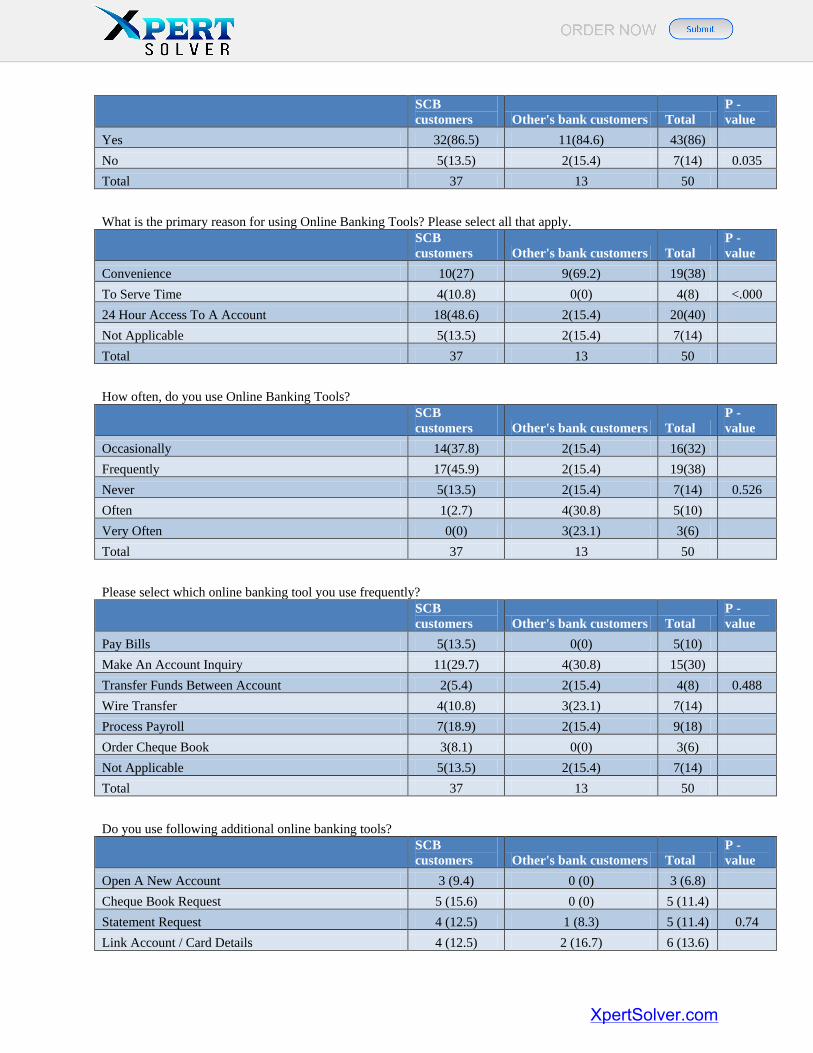

Yes 32 86% 11 85% 43 86% No 5 14% 2 15% 7 14% Total 37 100% 13 100% 50 100%

(Table 1)

Reason for Using Internet Banking

Graph clearly reveals the primary reason of using online banking tools in terms of

convenience, serving time, and 24 hour access by SCB and other bank’s customers. Results

represented in response of this question clearly reveal that majority of both SCB and other

bank’s customers use online banking due to 24 hour access to their account. Further to this,

convenience represents almost half percentage of primary reason. However, respondents who

were not the user of online banking of their respective banks market not applicable in the options

given.

Majority of online banking users of SCB uses online banking tools due to 24 hours access

to their account. It represents that there is a huge potential to also offer those banking services in

online banking tools that are currently not yet offered by SCB.

SCB Customer

Other's Bank Customer

Total

0 5 10 15 20 25

SCB Customer

Other's Bank Customer

Total

Not Applicable 24 Hour Access To Account To Serve Time Convenience

XpertSolver.com

41

Convenience 10 27% 9 69% 19 38% To Serve Time 4 11% 0 0% 4 8% 24 Hour Access To Account 18 49% 2 15% 20 40% Not Applicable 5 14% 2 15% 7 14% Total 37 100% 13 100% 50 100%

(Table 2)

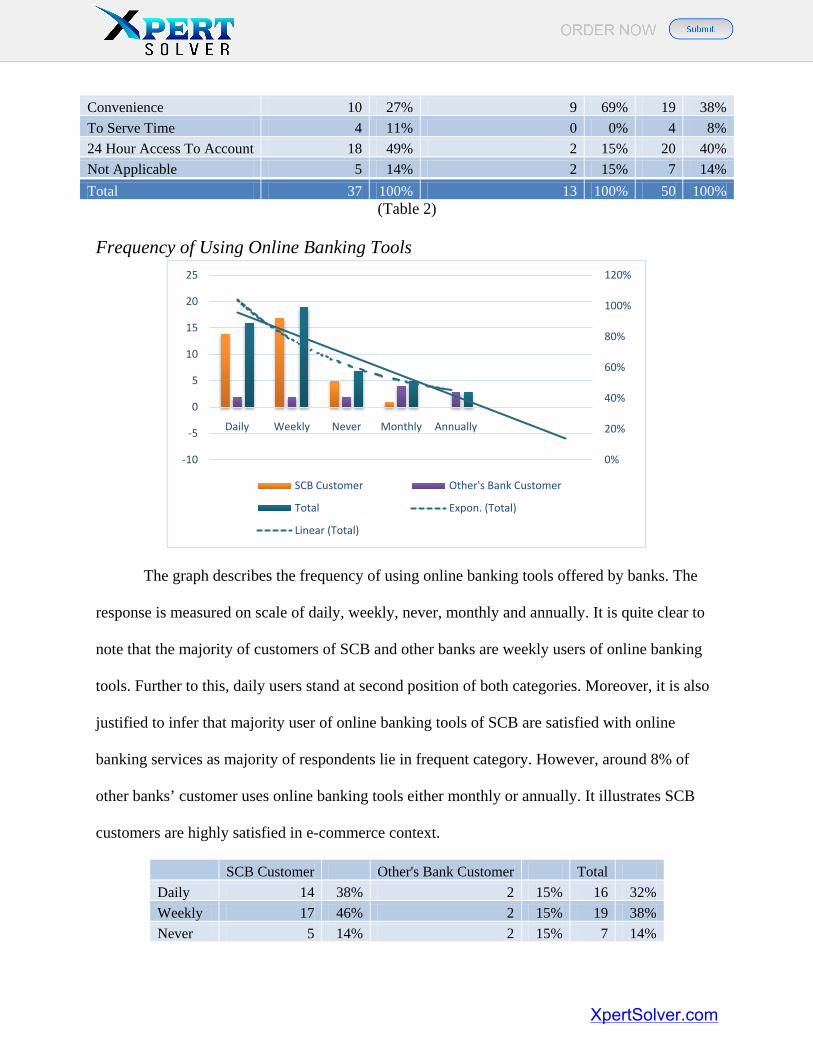

Frequency of Using Online Banking Tools

The graph describes the frequency of using online banking tools offered by banks. The

response is measured on scale of daily, weekly, never, monthly and annually. It is quite clear to

note that the majority of customers of SCB and other banks are weekly users of online banking

tools. Further to this, daily users stand at second position of both categories. Moreover, it is also

justified to infer that majority user of online banking tools of SCB are satisfied with online

banking services as majority of respondents lie in frequent category. However, around 8% of

other banks’ customer uses online banking tools either monthly or annually. It illustrates SCB

customers are highly satisfied in e-commerce context.

SCB Customer Other's Bank Customer Total

Daily 14 38% 2 15% 16 32% Weekly 17 46% 2 15% 19 38% Never 5 14% 2 15% 7 14%

0%

20%

40%

60%

80%

100%

120%

-10

-5

0

5

10

15

20

25

Daily Weekly Never Monthly Annually

SCB Customer Other's Bank Customer

Total Expon. (Total)

Linear (Total)

XpertSolver.com

42

Monthly 1 3% 4 31% 5 10% Annually 0 0% 3 23% 3 6% Total 37 100% 13 100% 50 100%

(Table 3)

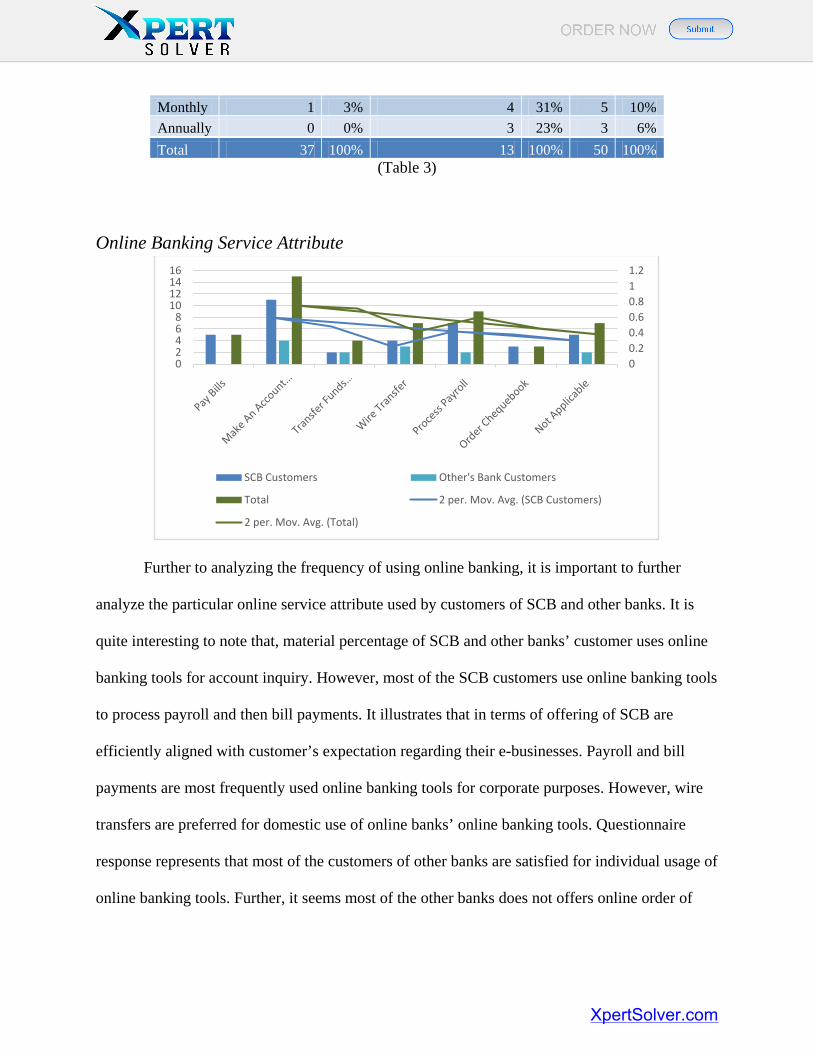

Online Banking Service Attribute

Further to analyzing the frequency of using online banking, it is important to further

analyze the particular online service attribute used by customers of SCB and other banks. It is

quite interesting to note that, material percentage of SCB and other banks’ customer uses online

banking tools for account inquiry. However, most of the SCB customers use online banking tools

to process payroll and then bill payments. It illustrates that in terms of offering of SCB are

efficiently aligned with customer’s expectation regarding their e-businesses. Payroll and bill

payments are most frequently used online banking tools for corporate purposes. However, wire

transfers are preferred for domestic use of online banks’ online banking tools. Questionnaire

response represents that most of the customers of other banks are satisfied for individual usage of

online banking tools. Further, it seems most of the other banks does not offers online order of

00.20.40.60.811.2

02468

10121416

SCB Customers Other's Bank Customers

Total 2 per. Mov. Avg. (SCB Customers)

2 per. Mov. Avg. (Total)

XpertSolver.com

43

cheque books but 8% of SCB customer uses this attribute which ultimately provides competitive

advantage to SCB over competitive banks.

SCB Customers

Other's Bank Customers

Total

Pay Bills 5 14% 0 0% 5 10% Make An Account Inquiry 11 30% 4 31% 15 30% Transfer Funds Between Account 2 5% 2 15% 4 8% Wire Transfer 4 11% 3 23% 7 14% Process Payroll 7 19% 2 15% 9 18% Order Chequebook 3 8% 0 0% 3 6% Not Applicable 5 14% 2 15% 7 14%

Total 37 100

% 13 100

% 50 100

% (Table 4)

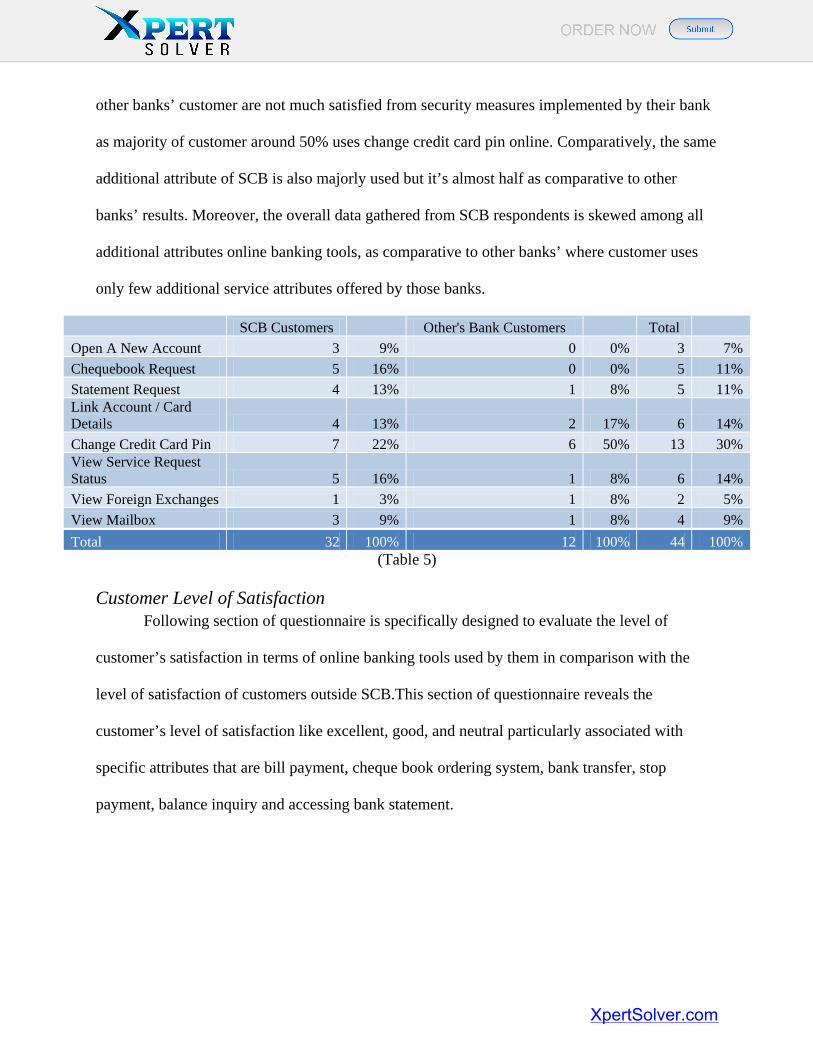

Additional Attributes of Online Banking Tools

Above graph clearly illustrates usage of additional online banking tools (like open new

account, cheque book request, statement request, link account/card, change credit card pin, view

service request status, view foreign exchanges and view mail box) by customers of SCB and

customers of other banks. As far as security of online banking channel is concerned, it seems

02468

101214

SCB Customers Other's Bank Customers Total

XpertSolver.com

44

other banks’ customer are not much satisfied from security measures implemented by their bank

as majority of customer around 50% uses change credit card pin online. Comparatively, the same

additional attribute of SCB is also majorly used but it’s almost half as comparative to other

banks’ results. Moreover, the overall data gathered from SCB respondents is skewed among all

additional attributes online banking tools, as comparative to other banks’ where customer uses

only few additional service attributes offered by those banks.

SCB Customers

Other's Bank Customers

Total

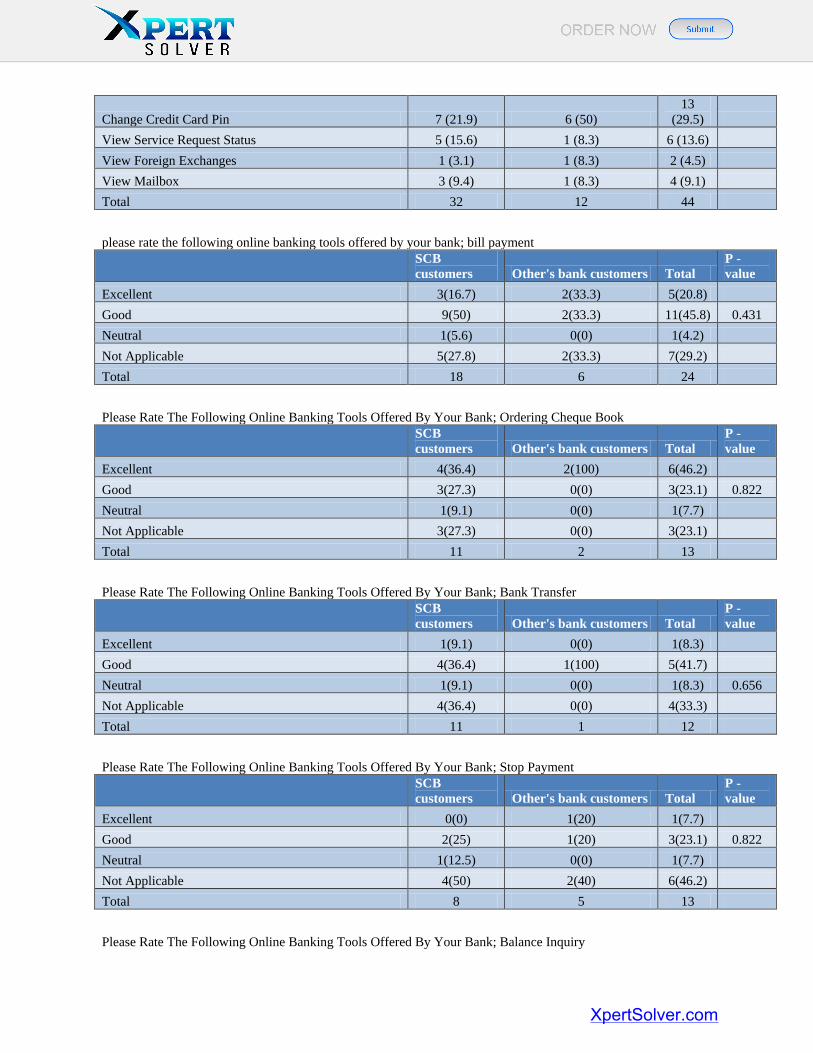

Open A New Account 3 9% 0 0% 3 7% Chequebook Request 5 16% 0 0% 5 11% Statement Request 4 13% 1 8% 5 11% Link Account / Card Details 4 13% 2 17% 6 14% Change Credit Card Pin 7 22% 6 50% 13 30% View Service Request Status 5 16% 1 8% 6 14% View Foreign Exchanges 1 3% 1 8% 2 5% View Mailbox 3 9% 1 8% 4 9% Total 32 100% 12 100% 44 100%

(Table 5)

Customer Level of Satisfaction Following section of questionnaire is specifically designed to evaluate the level of

customer’s satisfaction in terms of online banking tools used by them in comparison with the

level of satisfaction of customers outside SCB.This section of questionnaire reveals the

customer’s level of satisfaction like excellent, good, and neutral particularly associated with

specific attributes that are bill payment, cheque book ordering system, bank transfer, stop

payment, balance inquiry and accessing bank statement.

XpertSolver.com

45

Bill Payment

As far as payment of bill is concerned, it seems that around equal percentage of

customers of both categories does not use bill payment or not preferred to disclose. However, it

is quite interesting to note that the pattern of customer’s level of satisfaction of SCB and other

banks’ is same. High percentage of people rated their satisfaction level as good which is further

followed by 17% response in excellent category. Thus the level of satisfaction of customer is

considerably satisfactory.

SCB Customers

Other's Bank Customers

Total

Excellent 3 17% 2 33% 5 21% Good 9 50% 2 33% 11 46% Neutral 1 6% 0 0% 1 4% Not Applicable 5 28% 2 33% 7 29% Total 18 100% 6 100% 24 100%

(Table 6)

Online Cheque Book Ordering System

SCB Customers Other's Bank Customers Total

Not Applicable 5 2 7

Nuteral 1 0 1

Good 9 2 11

Excellent 3 2 5

0

5

10

15

20

25

30

Excellent Good Nuteral Not Applicable

XpertSolver.com

46

As for cheque book ordering system, customers of other banks’ are excellently satisfied

from their services which is far good as comparative to only 36% satisfied customers in terms of

cheque book ordering system. SCB should improve its cheque book ordering system and

promote specifically for this attribute because 27% of its customers do not uses online cheque

book ordering system.

SCB Customers

Other's Bank Customers

Total

Excellent 4 36% 2 100% 6 46% Good 3 27% 0 0% 3 23% Neutral 1 9% 0 0% 1 8% Not Applicable 3 27% 0 0% 3 23% Total 11 100% 2 100% 13 100%

4

2

6

3

0

3

1

0

1

3

0

3

S C B C U S T O M E R S O T H E R ' S B A N K C U S T O M E R S T O T A L

Excellent Good Nuteral Not Applicable

Excellent Good Neutral Not Applicable

XpertSolver.com

47

(Table 7) Bank Transfer

It has already been revealed that majority of SCB’s customers do not preferably use bank