ontario tourism market assessment research study - ministry of

TRANSCRIPT

Ontario Tourism Market Assessment Research Study

Final Report

Presented to:

Ontario Ministry of Tourism Competitiveness Study

February 2009

2

© Queen’s Printer for Ontario, 2009

Although copyright in the research papers is held by the Queen's Printer for Ontario, the papers were prepared by external companies and their conclusions do not necessarily represent the views of the

Government of Ontario.

ISBN 978-1-4249-8933-1 (PDF)

3

Table of Contents

At TNS, we know that being successful in today’s dynamic business environment requires more understanding, clearer direction and greater certainty than ever before. While accurate information is the foundation of our business, we focus our expertise, services and resources to give you greater insight into your customers’ behavior and needs.

Our integrated, consultative approach exploits our depth of coverage across all the research, analysis, marketing, and industry issues that will be required for this work. That is what sets TNS apart.

Thank you for allowing us to explore your business needs. The comprehensive program that follows is designed to help you achieve your goals. We hope you will trust TNS to provide the insight you need to sharpen your competitive edge.

Executive Summary ................................ 4

Strategic Overview and Recommendations .................................. 16

Detailed General Summary ..................... 22

Overview of Visitation and Spending - Domestic versus U.S. versus Overseas .. 23

Overview of Visitation and Spending - U.S. versus Overseas.............................. 26

North American Opportunity Markets....... 32

Overseas Opportunity Markets ................ 37

Domestic Markets.................................... 44

Quebec Market........................................ 46

United States........................................... 57

Detroit...................................................... 69

New York................................................. 71

Massachusetts ........................................ 82

Illinois ...................................................... 93

New Jersey/Connecticut........................... 104

Florida ............................. 115

Texas .............................. 126

California ......................... 137

Overseas Markets ........... 148

Europe............................. 150

The U.K. .......................... 152

France ............................. 163

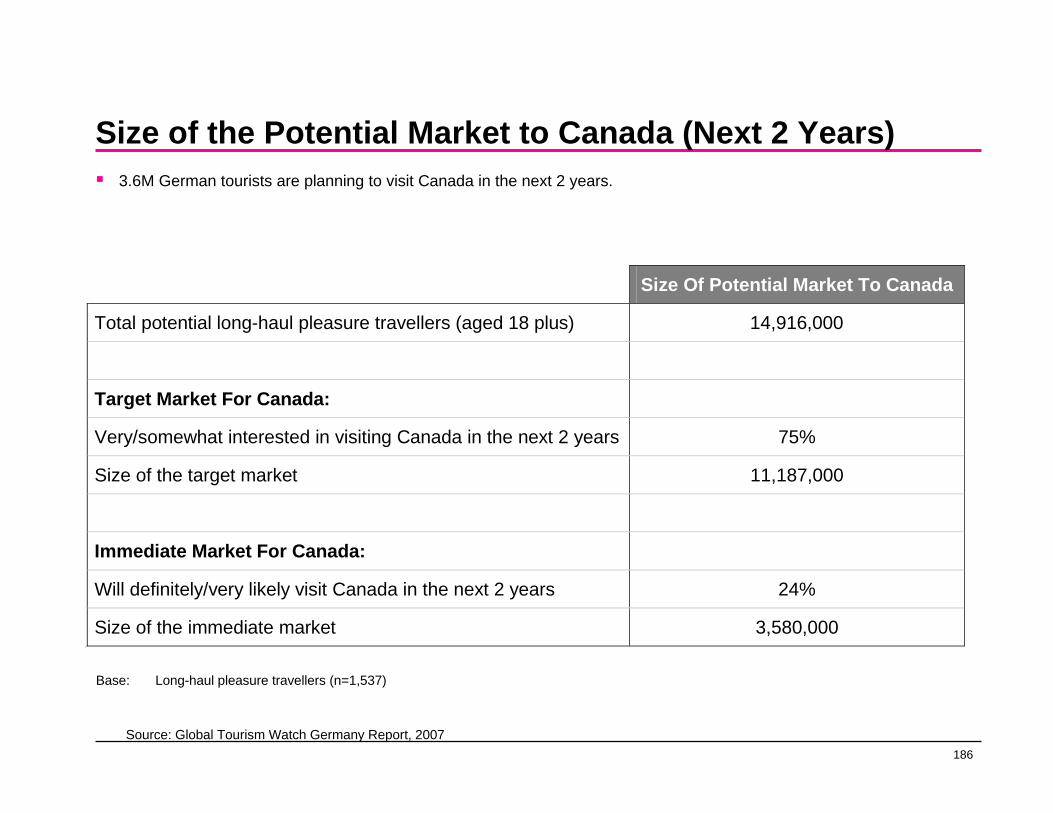

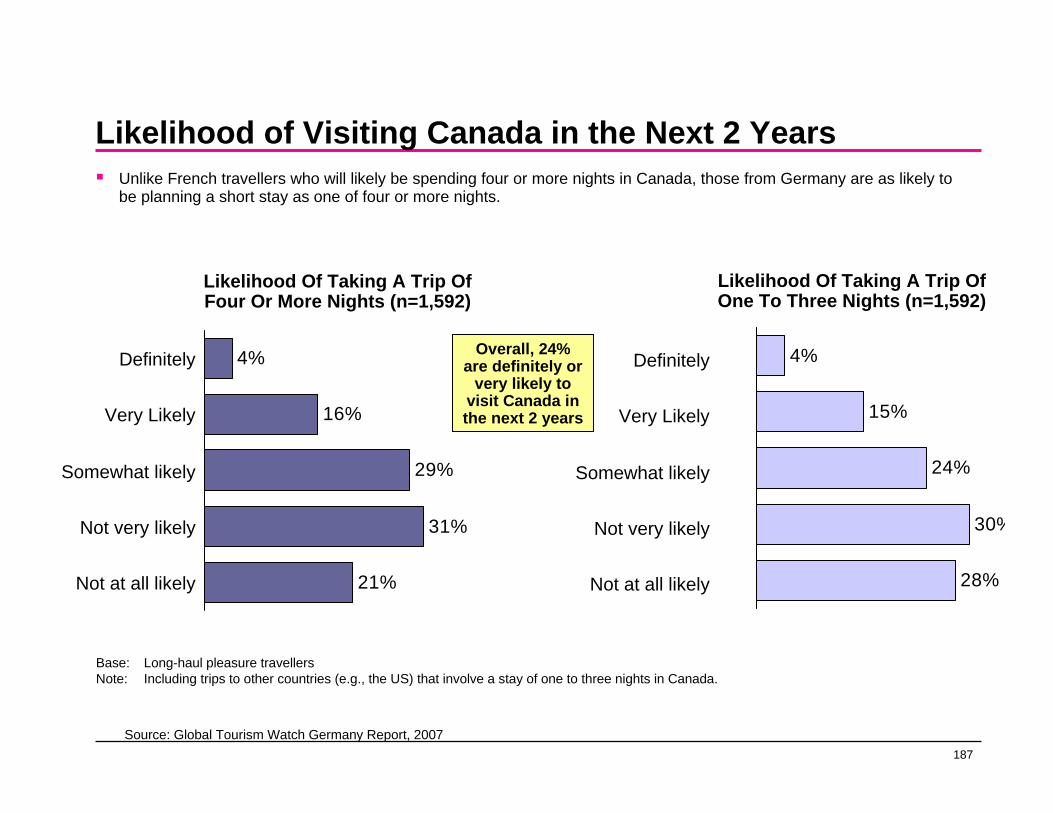

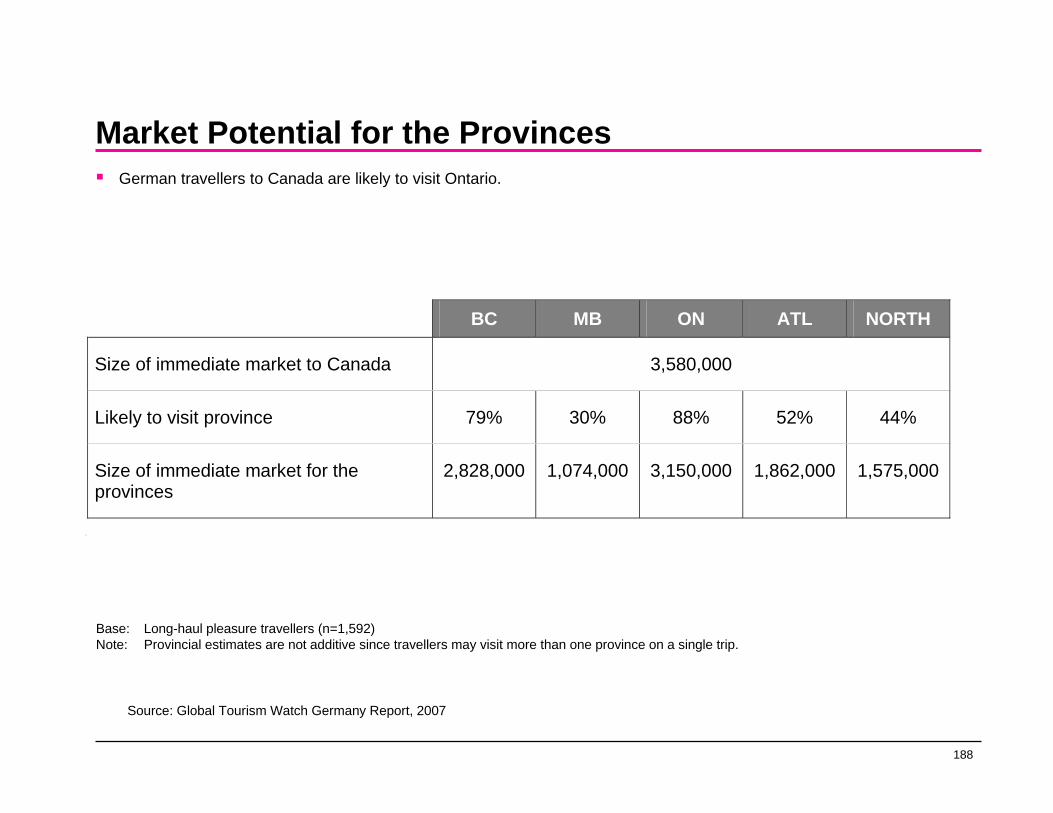

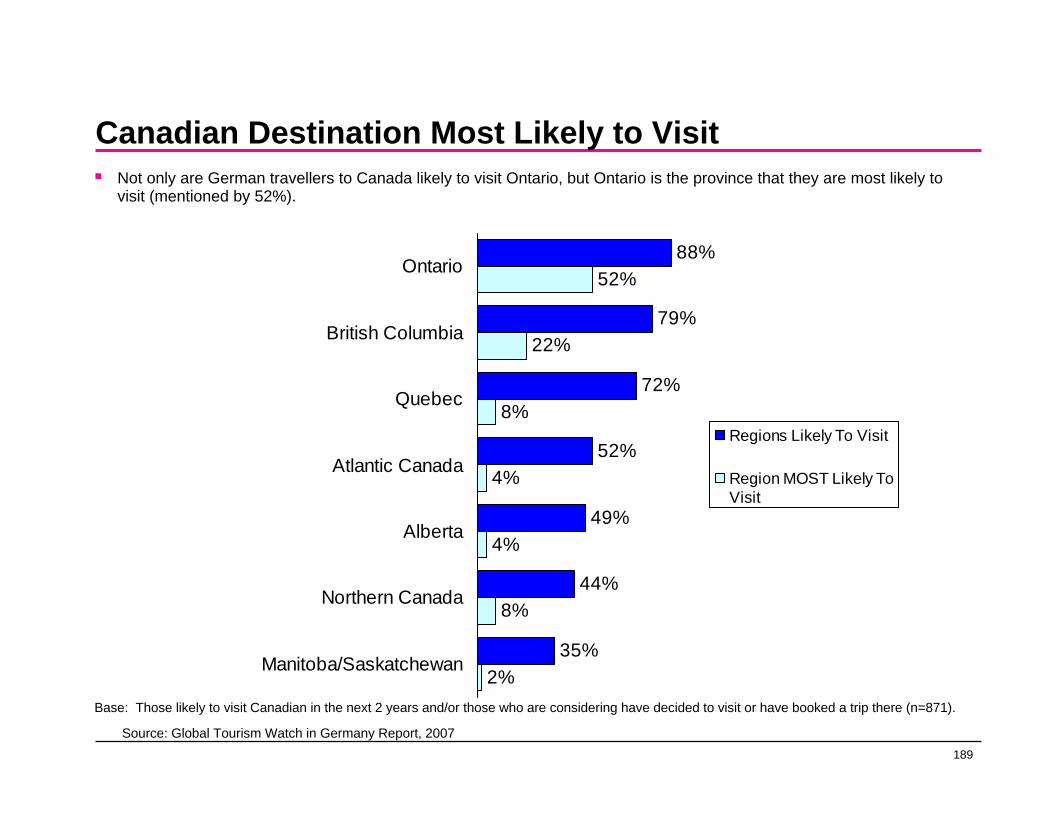

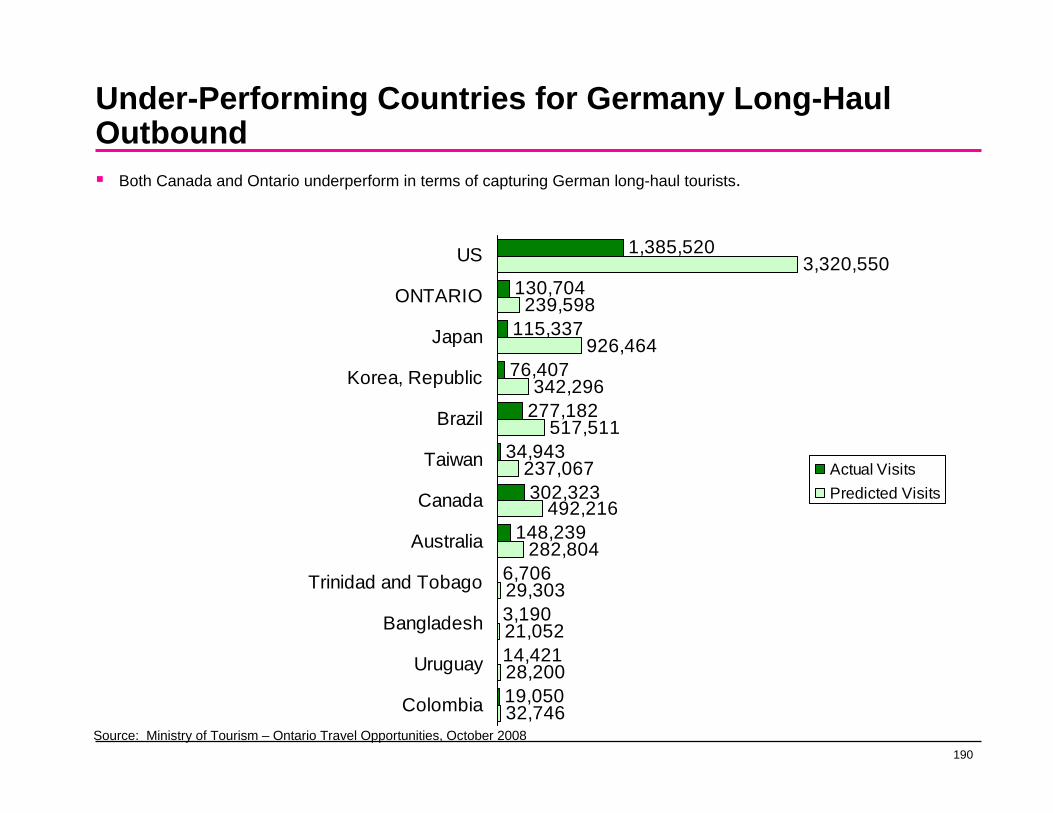

Germany ......................... 178

South America................. 193

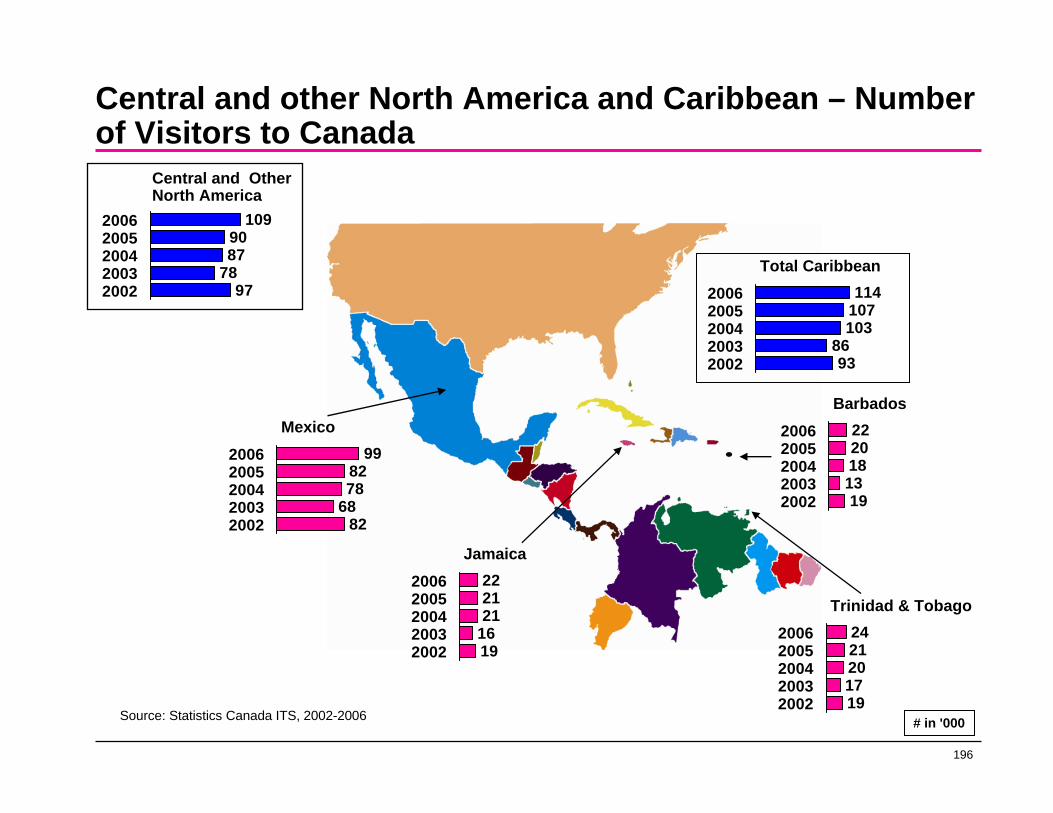

Central America............... 195

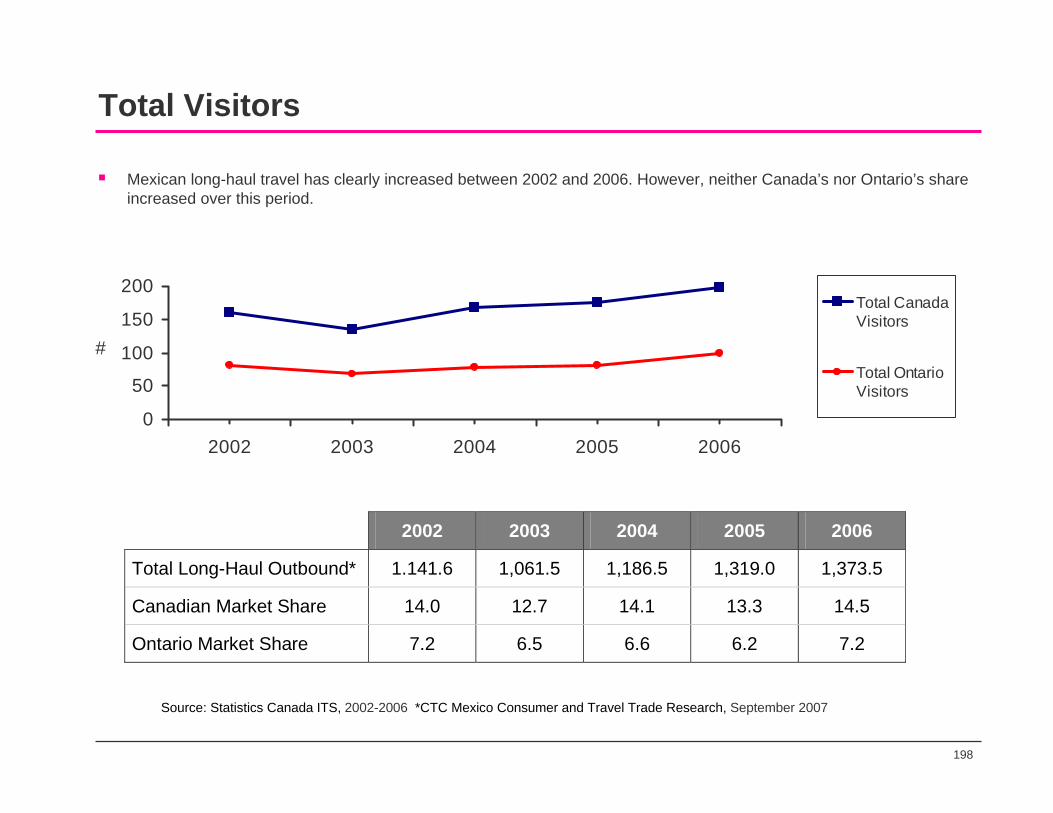

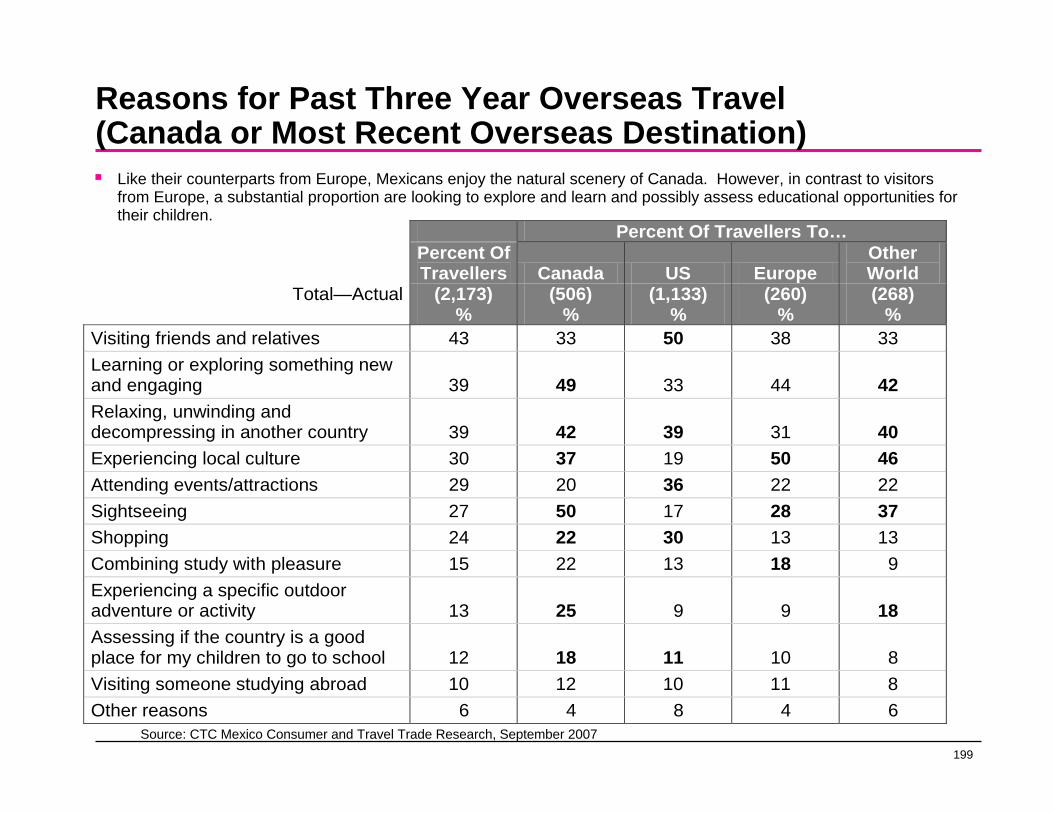

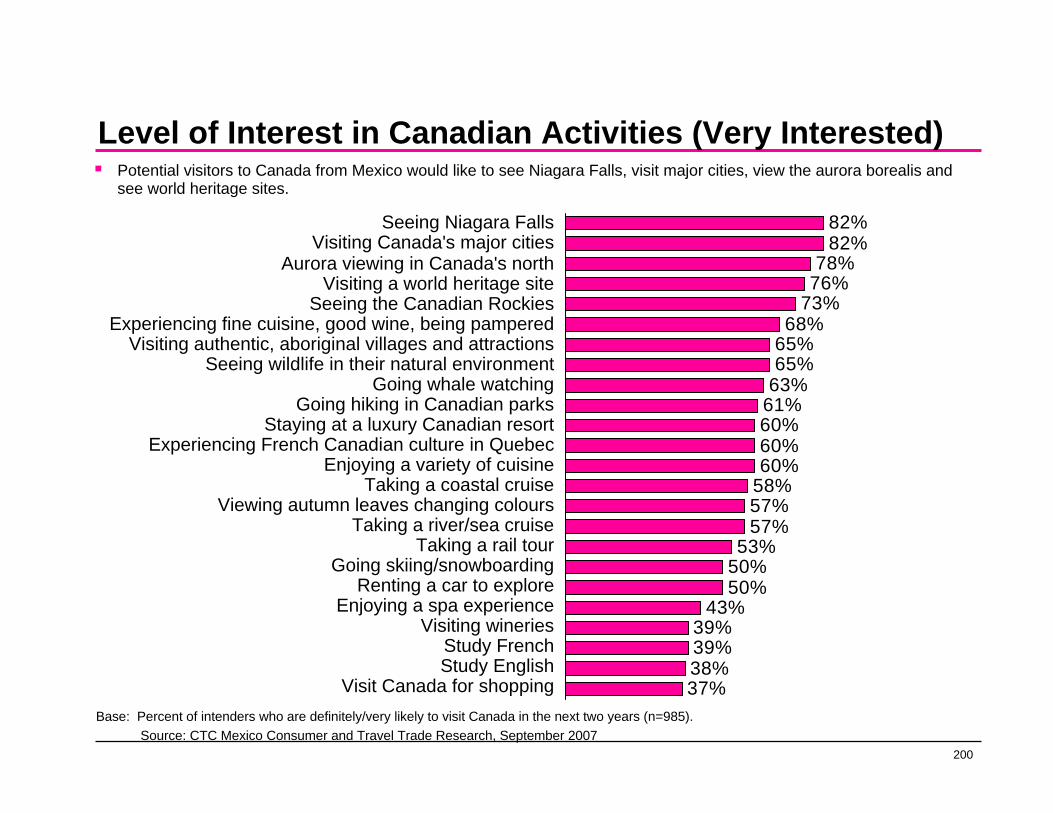

Mexico............................. 197

Asia ................................. 210

Korea............................... 212

Japan .............................. 224

China............................... 236

India ................................ 248

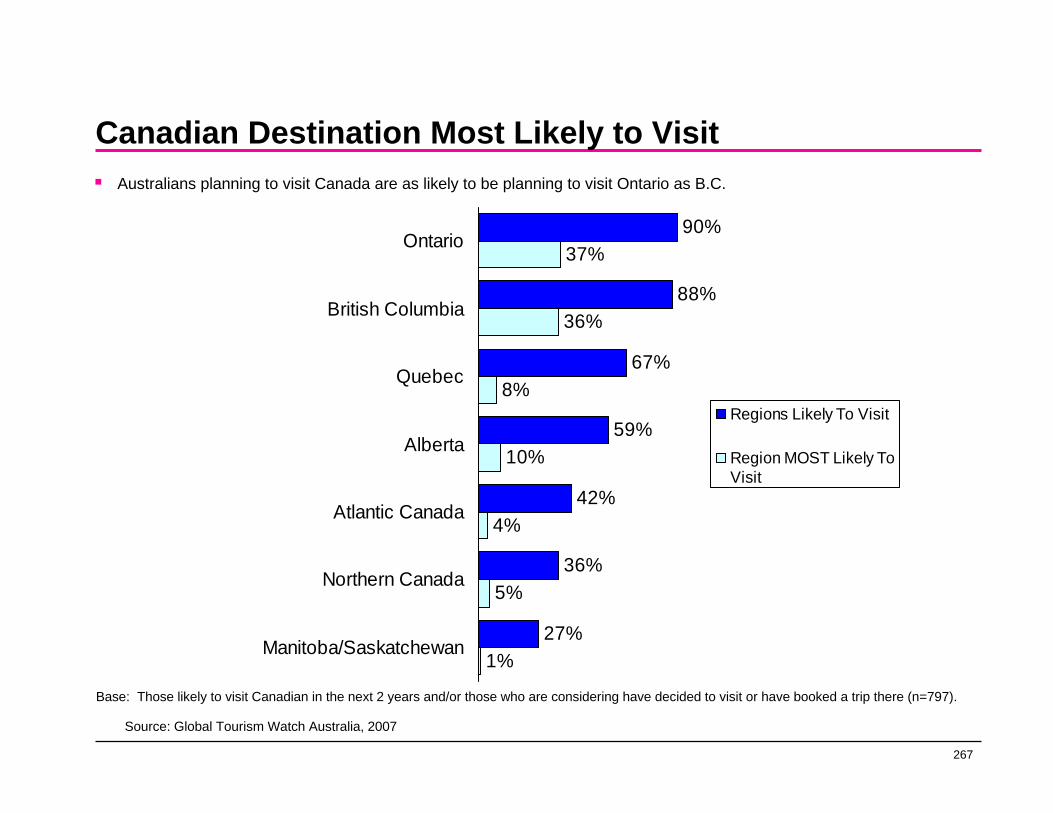

Australia .......................... 257

4

Executive Summary

5

Study Overview

Although the global tourism market is growing, Ontario is competing with more destinations than ever before:

The global tourism industry is characterized by newly popular destinations;

Intensified competition; and

Growing disposable incomes worldwide.

For Ontario to be competitive, it needs to strategically pursue markets with the highest potential for growth over the next 10 years or so, in terms of total tourist expenditures, while nurturing its current base of source markets.

This Study provides recommendations for the Province on:

Best prospect markets (Canadian provinces, U.S. states and Overseas markets) which present Ontario with the highest potential for growth over the next several years in terms of total tourist expenditures by targeting:

Populations that are interested in Ontario; and Populations offering the best prospects for translating interest in Ontario to a behavioural response and increased tourism volume.

6

MethodologyThis Study undertook research in the following markets:

Domestic Markets including Quebec and Western Canada.Tier One/Near U.S. markets to provide recommendations on the potential of various consumer groups within these border regions.Tier Three and Tier Four U.S. potential markets.High potential Overseas growth markets.

Attention was given to:

Size

Nature of these markets

Needs and interests of the target populations

Based on available data, this study produced expenditure projections for various potential markets.Within the identified markets, consumer segments were identified that represent Ontario’s most likely consumers.

7

Overview Key Findings

Domestic Markets - Ontario’s domestic market continues to be the anchor for the province’s tourism industry and its main source of volume:

Ontario’s domestic market is 4.5 times larger than the U.S. market in terms of numbers of visitors (person visits) and 3.5 times larger than the U.S. market in terms of total dollars spent.Ontario’s proximity to major U.S. population centres and relatively ease of access to many overseas destinations via Toronto’s transportation hub is a double-edged sword. It presents opportunities to attract large numbers of visitors from the U.S. and overseas but also facilitates the outbound movement of domestic travellers. Although recent currency exchange rates may have moderated the outbound effects, the potential for this sort of “leakage”is always present.

While Canada’s western provinces (B.C., Alberta, Saskatchewan) and Quebec hold the largest untapped pools of potential visitors to Ontario, Quebec is a better prospect than the West. In fact, U.S. Tier One markets are a better opportunity than the western provinces and should be pursued ahead of Western Canada.

U.S. - The U.S. market is eight times larger than the overseas market in terms of visitors (person visits) and U.S. overnight visitors spend more per person, per night in Ontario than do overnight travellers from other overseas markets:

U.S. Tier One is Ontario’s key U.S. market: Eastern Michigan (including Detroit); Northern Ohio and Western New York; Tier Three U.S. markets hold considerable potential: New York City, Chicago, New Jersey, Philadelphia and Washington D.C.; and Tier Four U.S. markets hold some potential (principally, California, Texas, Florida, Arizona, Georgia and North Carolina). However, potential visitors are scattered across these states making them less attractive than the aforementioned Tier Three U.S. markets. There is, however, potential to strategically target large population centres in this Tier such as Los Angeles, San Francisco-Oakland, Phoenix and Dallas-Fort Worth.

Overseas - While the UK will remain the top overseas market through 2012, it is clear that China will be overtaking the traditional markets of Germany and France in terms of total visitor spending in Ontario in the next year or two. Mexican tourism expenditures are also expected to overtake those of Germany and France. Indian tourism expenditures may overtake those of Germany by 2012. Although a lower priority, monitor Brazil and South Korea.

8

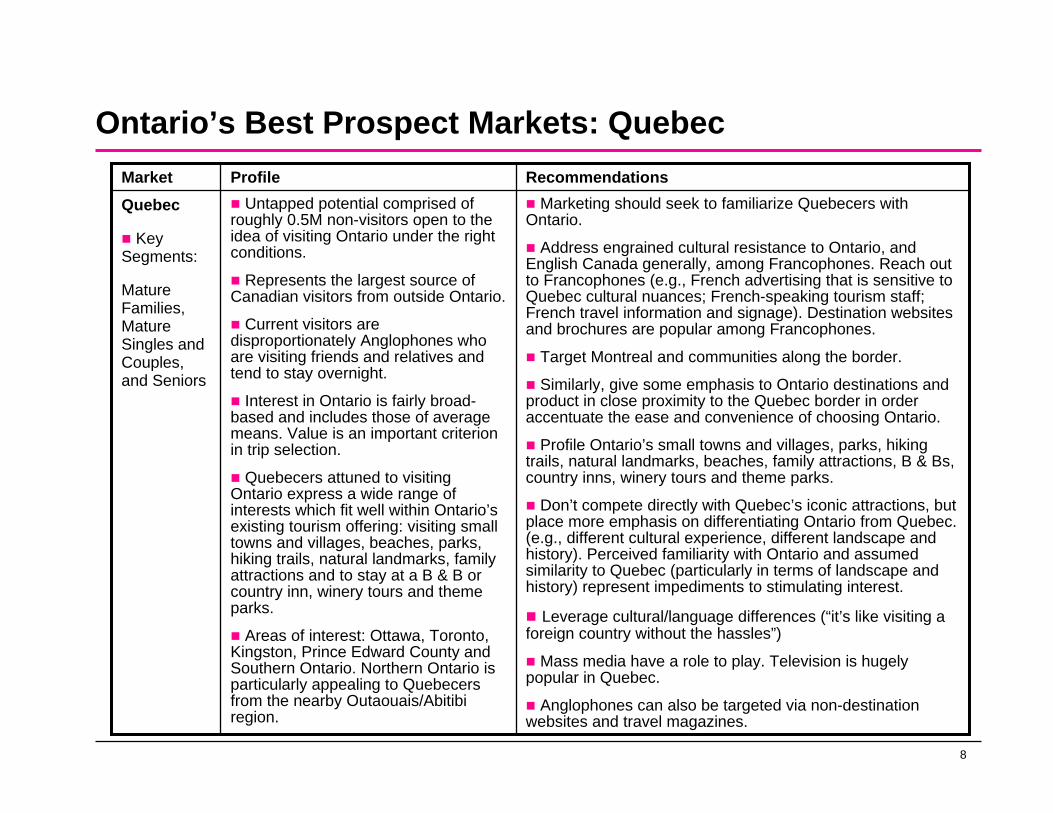

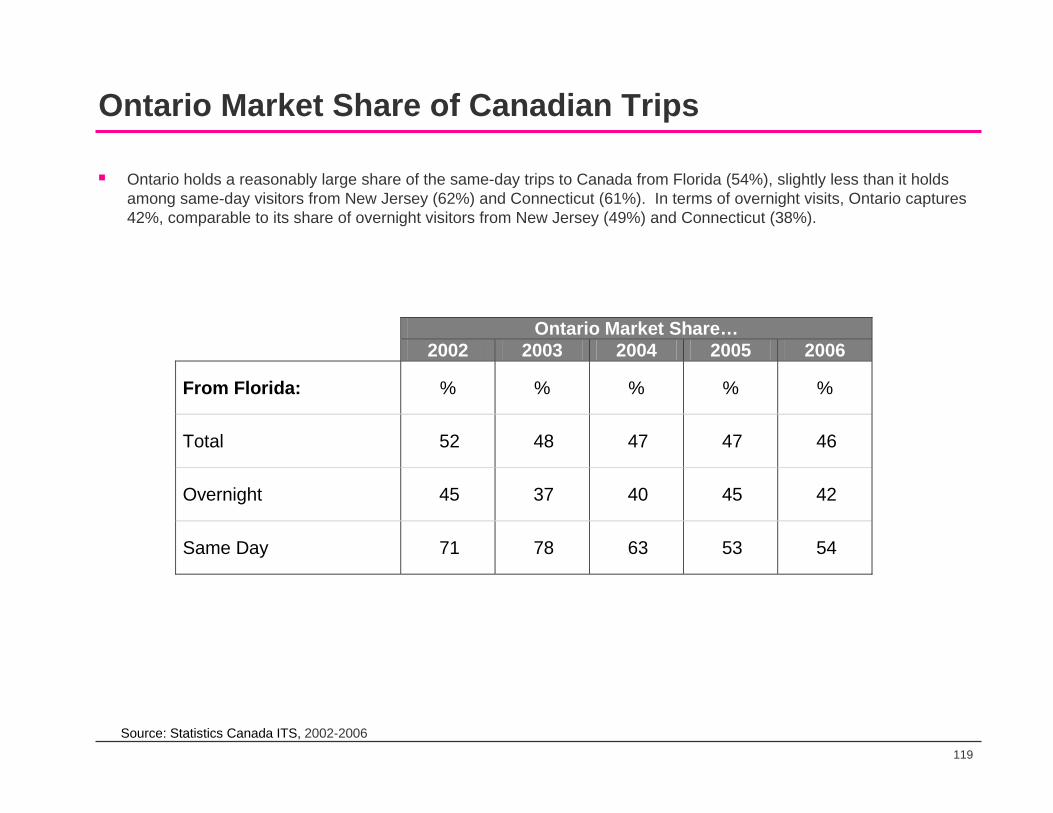

Ontario’s Best Prospect Markets: Quebec

Quebec

Key Segments:

Mature Families, Mature Singles and Couples, and Seniors

Market RecommendationsProfileMarketing should seek to familiarize Quebecers with

Ontario.

Address engrained cultural resistance to Ontario, and English Canada generally, among Francophones. Reach out to Francophones (e.g., French advertising that is sensitive to Quebec cultural nuances; French-speaking tourism staff; French travel information and signage). Destination websites and brochures are popular among Francophones.

Target Montreal and communities along the border.

Similarly, give some emphasis to Ontario destinations and product in close proximity to the Quebec border in order accentuate the ease and convenience of choosing Ontario.

Profile Ontario’s small towns and villages, parks, hiking trails, natural landmarks, beaches, family attractions, B & Bs, country inns, winery tours and theme parks.

Don’t compete directly with Quebec’s iconic attractions, but place more emphasis on differentiating Ontario from Quebec. (e.g., different cultural experience, different landscape and history). Perceived familiarity with Ontario and assumed similarity to Quebec (particularly in terms of landscape and history) represent impediments to stimulating interest.

Leverage cultural/language differences (“it’s like visiting a foreign country without the hassles”)

Mass media have a role to play. Television is hugely popular in Quebec.

Anglophones can also be targeted via non-destination websites and travel magazines.

Untapped potential comprised of roughly 0.5M non-visitors open to the idea of visiting Ontario under the right conditions.

Represents the largest source of Canadian visitors from outside Ontario.

Current visitors are disproportionately Anglophones who are visiting friends and relatives and tend to stay overnight.

Interest in Ontario is fairly broad-based and includes those of average means. Value is an important criterion in trip selection.

Quebecers attuned to visiting Ontario express a wide range of interests which fit well within Ontario’s existing tourism offering: visiting small towns and villages, beaches, parks, hiking trails, natural landmarks, family attractions and to stay at a B & B or country inn, winery tours and theme parks.

Areas of interest: Ottawa, Toronto, Kingston, Prince Edward County and Southern Ontario. Northern Ontario is particularly appealing to Quebecers from the nearby Outaouais/Abitibi region.

9

Ontario’s Best Prospect Markets: Tier 1 U.S. Markets

Tier One U.S. Markets: Eastern Michigan; Northern Ohio; Western New York urban markets

Consumer Segments:

Key Target: 45-64 age-range (older parents, working older couples and retired couples)

Secondary Target: 25-44 age-group comprised of a fragmented market with diverse life stages (older and younger families, young and middle-aged singles, and young couples without children)

Market RecommendationsProfile

Maintain focus on these core markets.

Build interest in a return visit to Ontario by broadening the range of products promoted and building bridges from popular, familiar ones.

Ontario should position itself as a “safe locale” without the “hassle” associated with foreign travel.

Promote the availability of quality, mid-range accommodation.

Promote how Ontario’s product meets the interests of both active and less-active travellers in communications.

In the short-term, leverage the lower Canadian dollar and work to reduce existing concerns about border crossing difficulties.

Apathy toward Ontario - “been there, done that”.

The pool of “open” non-visitors is small; the potential lies with previous visitors.

It is important to maintain support here, particularly with respect to fueling incoming short-stay and same-day revenues. However, growth potential is limited and therefore the marketing strategy, here, would be defensive.

Concerns include: economic uncertainty, safety of a destination, wants to avoid the hassle of foreign travel.

Urban and cultural pursuits are popular.

Have broad-ranging interests and are more active and outdoors-oriented than the typical U.S. pleasure traveller. Activities of interest: golfing, horseback riding, sailing and cycling.

10

Ontario’s Best Prospect Markets: Tier 3 U.S. Markets

Tier Three U.S. Markets:New York City, Chicago

Consumer Segments:

Key Target: 45-64 age-range (older parents, working older couples and retired couples)

Secondary Target: 25-44 age-group (younger, upwardly mobile individuals and couples)

Market RecommendationsProfile

There is a general need to build an awareness and image profile or ‘umbrella’ for the Ontario brand in these markets under which specific offerings and destinations can be positioned.

Continue to build on past efforts by promoting key components of the Ontario tourism product.

Promote Ontario’s urban environment and related activities to allure and enhance commitment to return.

Generate “buzz” around the urban experience offered by the GTA.

Given the growing interest in environmental matters, promote Ontario as “green/clean”.

Ontario should position itself as a “safe locale”.

Promote Ontario as an affordable destination e.g., availability of mid-range accommodation.

Promote Ontario’s historical offerings to Chicago market.

Currently maintain large populations of“open” non-visitors to Ontario.

Urban and cultural pursuits are popular. Some evidence that U.S. travellers to Ontario tend to have broad-ranging interests and are more active and outdoors-oriented than the typical U.S. pleasure traveller.

Ontario’s appeal more congruent with natural features (i.e., Niagara Falls) and the natural environment rather than with man-made entertainment offerings or “sun and sand”.

Concerned with economic uncertainty.

Toronto viewed as more green/clean than any U.S. urban centre.

Specific to New York City:

Toronto’s profile and image are virtually non-existent among New Yorkers.

Safety is highly desirable.

Specific to Chicago:

Interested in historic sites.

11

Ontario’s Best Prospect Markets: Tier 3 & 4 U.S. Markets

Tier Four Distant U.S. Markets: California, Florida, Georgia, Texas and Arizona

Undeveloped Tier Three U.S. Markets: New Jersey, Philadelphia, Washington, DC

Consumer Segments:

Key Target: 45-64 age-range (older parents, working older couples and retired couples)

Secondary Target: 25-44 age-group (younger, upwardly mobile individuals and couples)

Market RecommendationProfile

Monitor the numbers of potential Ontario visitors, possibly undertaking research if numbers of potential visitors appear to be growing.

The next step would involve identifying activity and life-stage/psychographic segments for targeting.

The initial approach should be tightly focused geographically to optimize ROI (e.g., Los Angeles, San Francisco, Dallas-Fort Worth, etc.).

Large numbers of open non-visitors.

Launch marketing efforts as budgets allow.

Target New Jersey much like a large urban centre (a campaign targeting New York City could potentially be expanded to include the state of New Jersey).

Promote Ontario as “green/clean”.

Promote Ontario as an affordable destination e.g., availability of high quality, mid-range accommodation (superior to NYC in this respect).

New Jersey ranks first among all states for household income.

Philadelphia and Washington DC each offer a large pool of potential visitors.

May prefer travel to New York and Boston, as closer to home than Toronto.

Drawn by urban and cultural interests, as well as more active/outdoor pursuits.

Growing interest in environmental matters. Toronto viewed as more green/clean than any U.S. urban centre.

Concerned with the economic uncertainty.

12

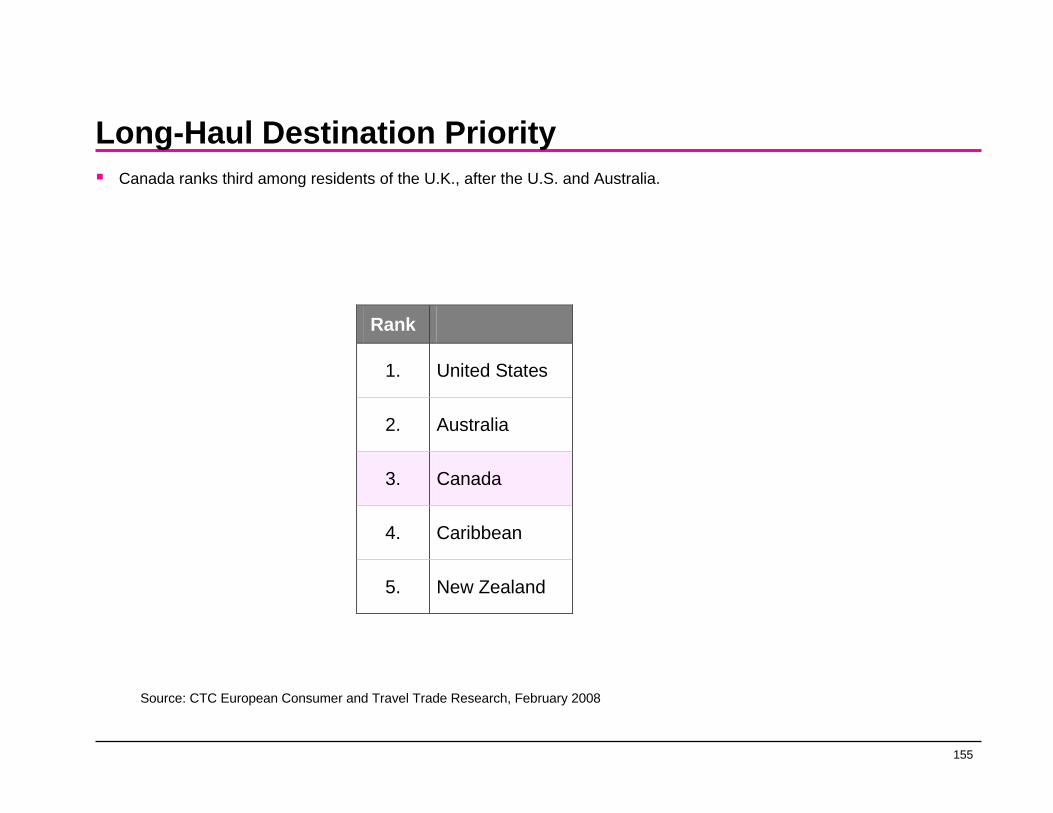

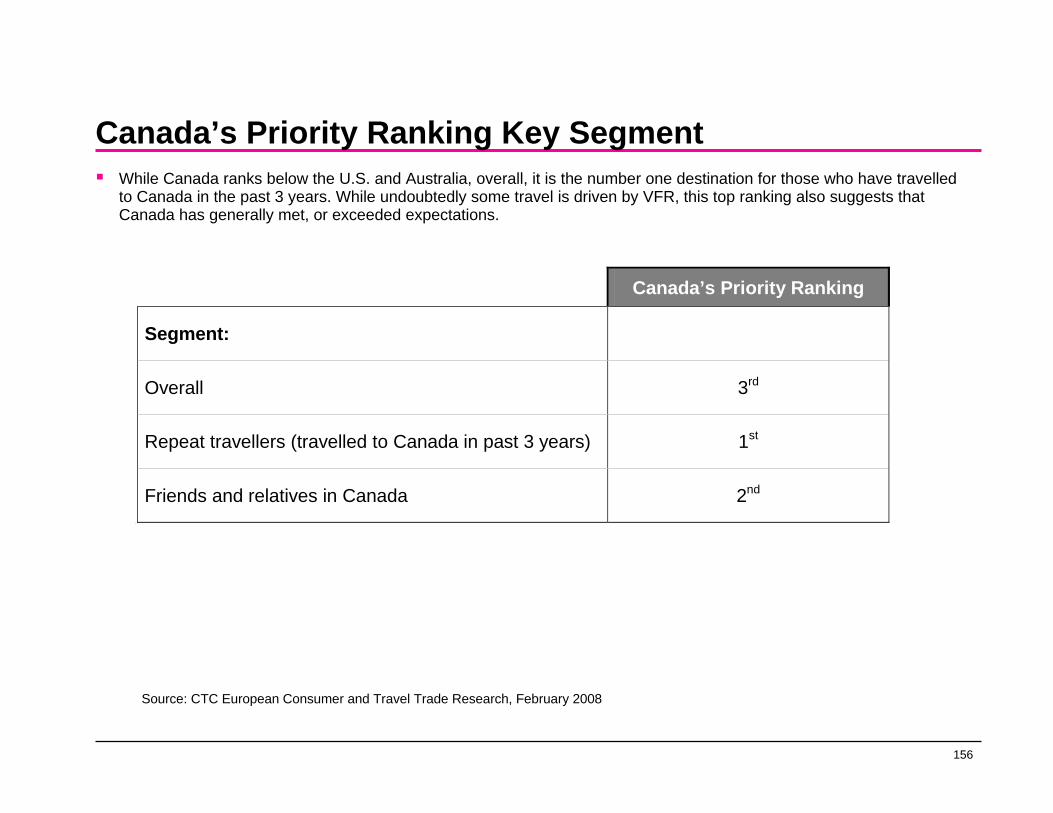

Ontario’s Best Prospect Markets: United Kingdom

United Kingdom

Average age of a British visitor to Canada has fallen from 51 (in 1997) to 44 years of age (in 2007

Market RecommendationProfileIncrease awareness of Ontario destinations within

Canada and Ontario’s unique regional product offer.

Promote the natural beauty of wilderness areas, rivers and lakes, as well as Ontario’s historical sites particularly in relation to British colonial history.

Promote Ontario’s diversity in terms of urban/rural product, and use this to continue to attract larger numbers of younger travellers on their first trip to Canada.

As with all overseas destinations, don’t shy away from the possibility of packaging Ontario with other Canadian provinces to enhance drawing power within a national (CTC) strategy.

Promote Ontario as an affordable destination.

Use clear and comprehensive personalized web services that offer clear travel plans and itineraries.

Testimonies and word-of-mouth (given that U.K. travellers who have visited Canada are typically satisfied and rate Canada ahead of the U.S. and Australia as a destination they want to visit).

TV commercials and travel shows which would highlight the various parts of Ontario should also be considered for U.K. television programming.

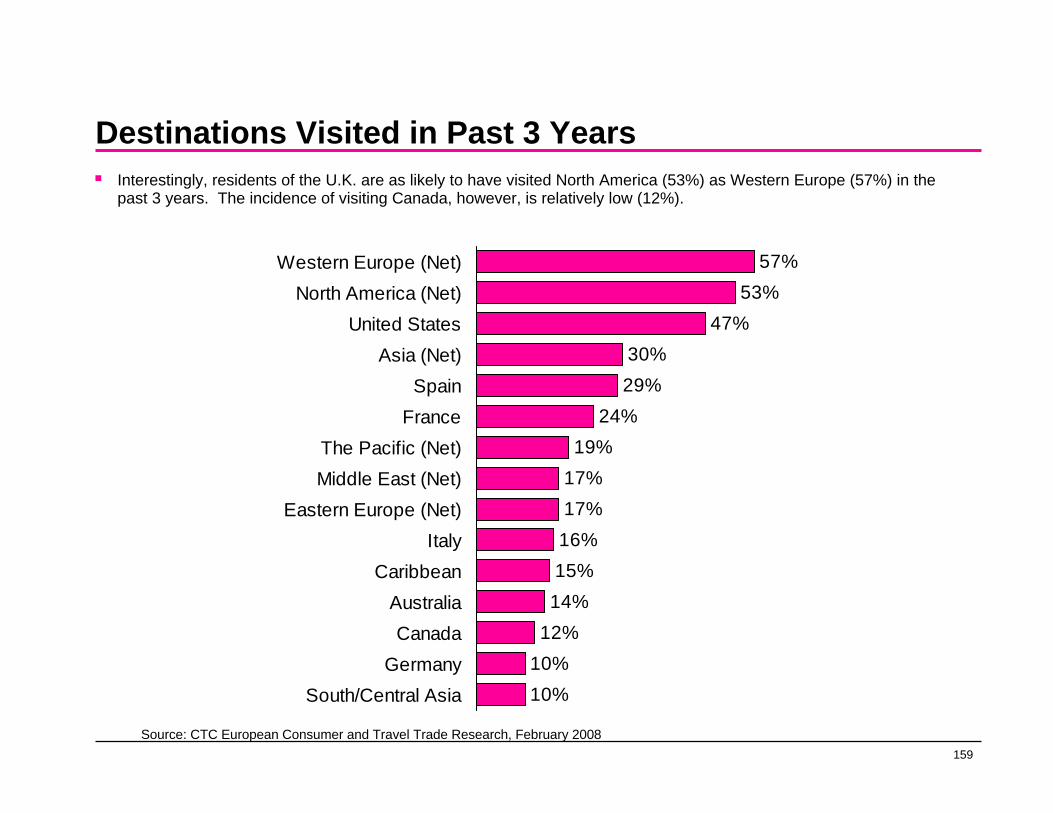

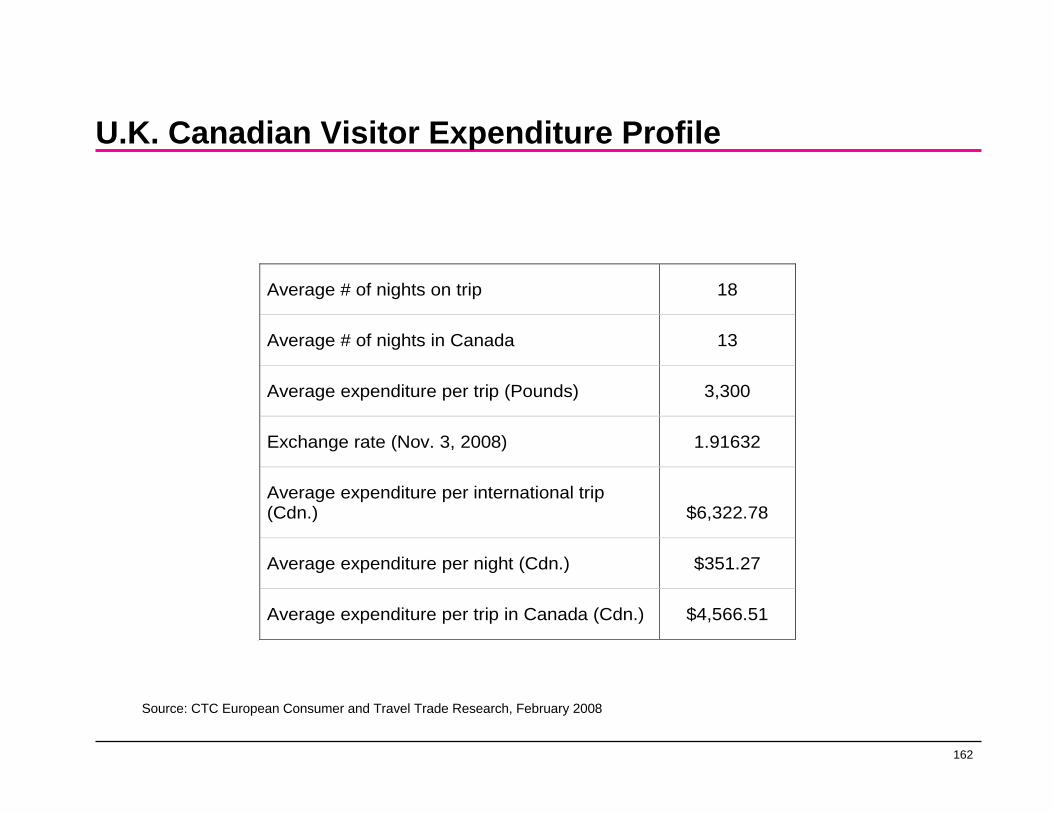

While travel to Canada and in particular to Ontario has been decreasing in recent years, the U.K. is Ontario’s largest overseas source of tourism revenue and will continue to be for at least the next 5 to 10 years.

As a commonwealth country, UK travellers feel a high level of comfort in visiting Canada. and view Canadians as warm and friendly.

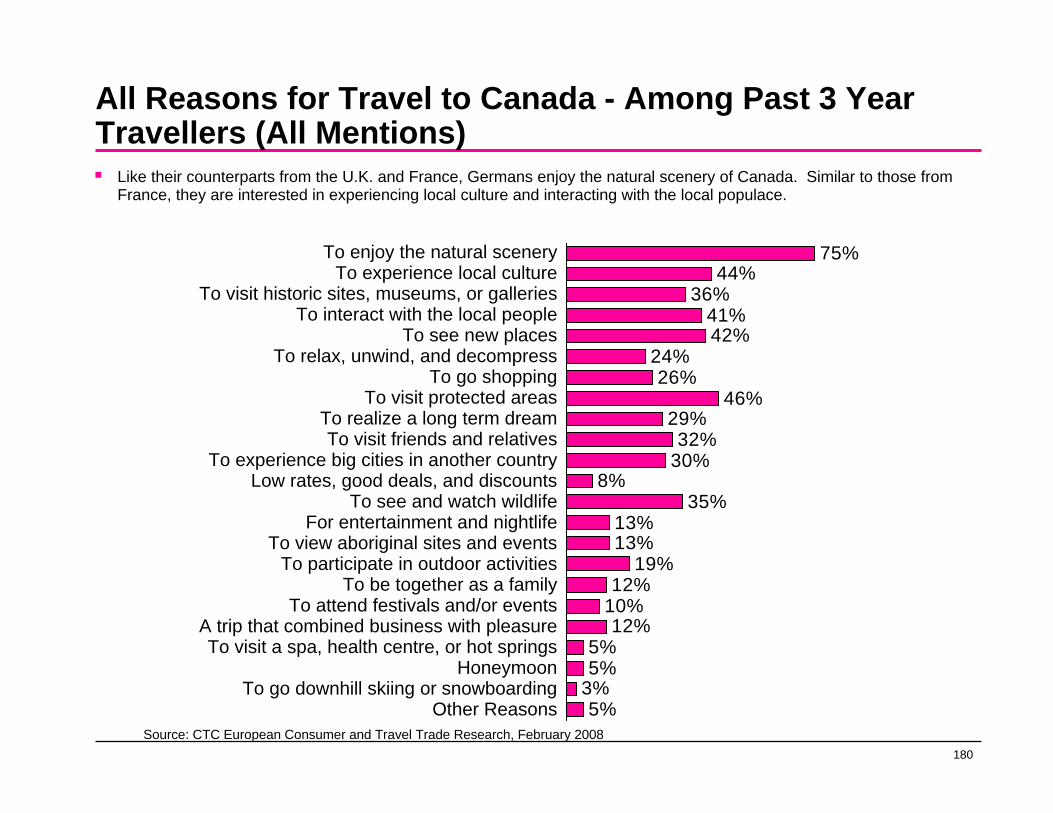

One of the key motivational factors for visiting Canada is the natural scenery which seems to intermingle with large cities and urban destinations.

Visiting friends and relatives (“VFR”) is a key reason for British travel to Canada.

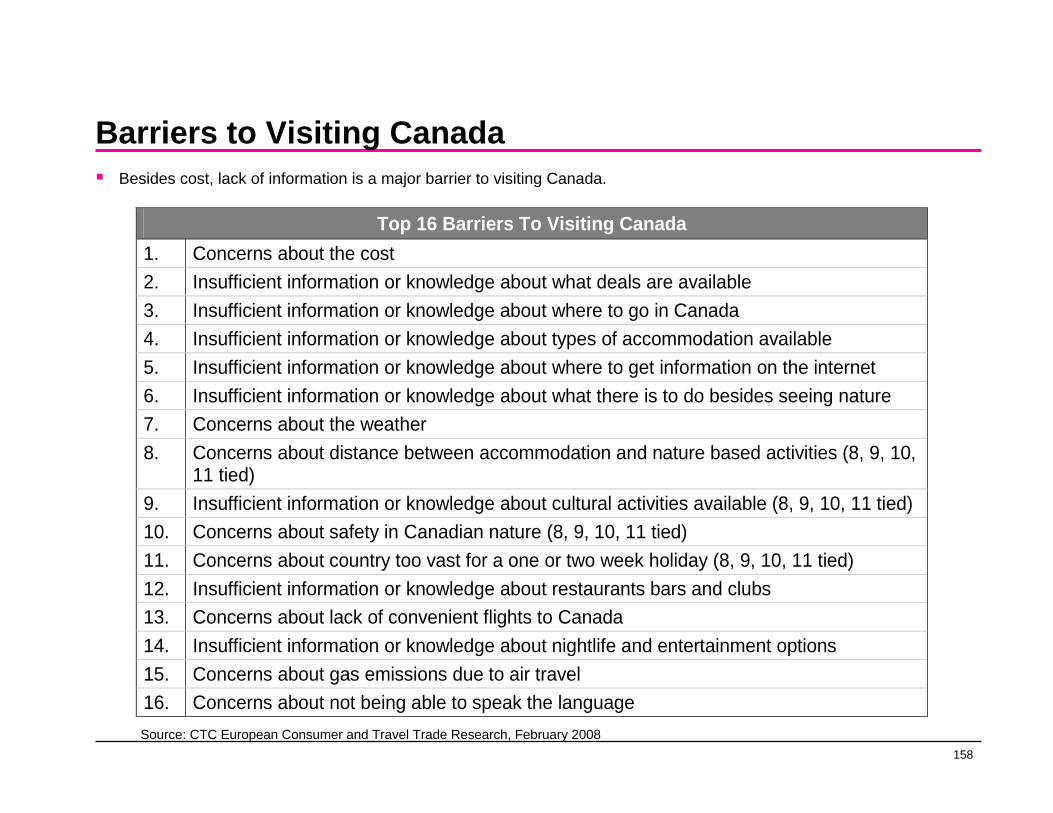

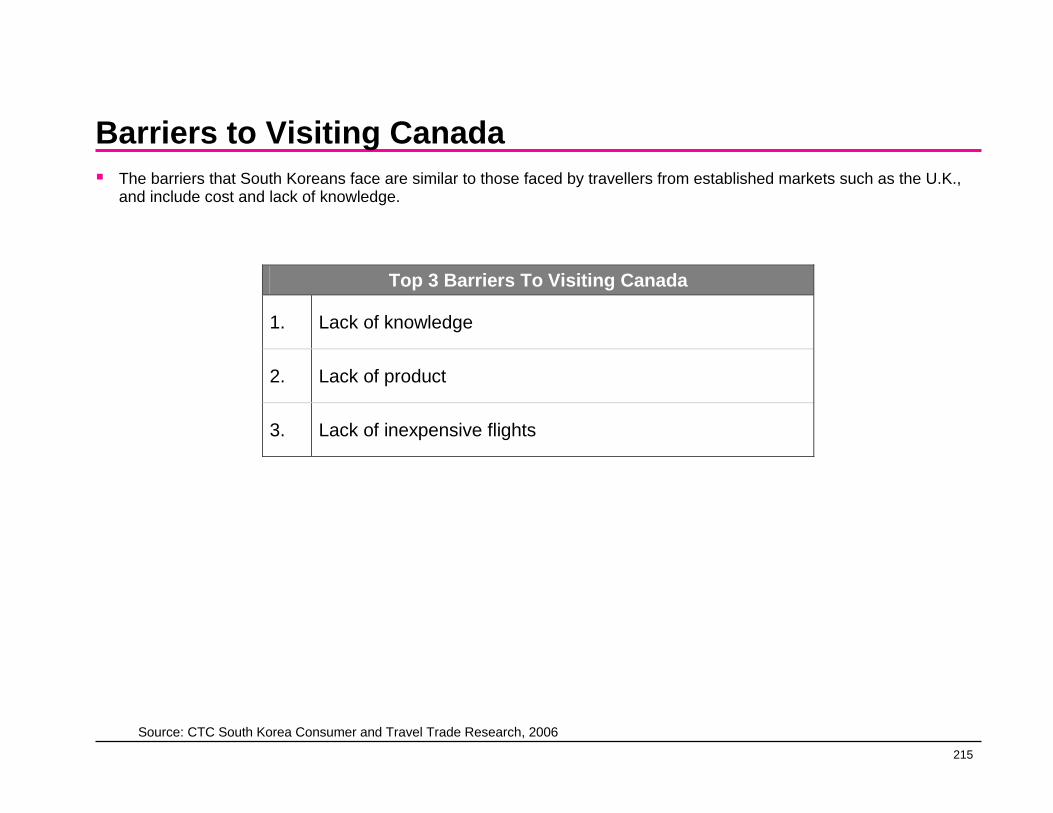

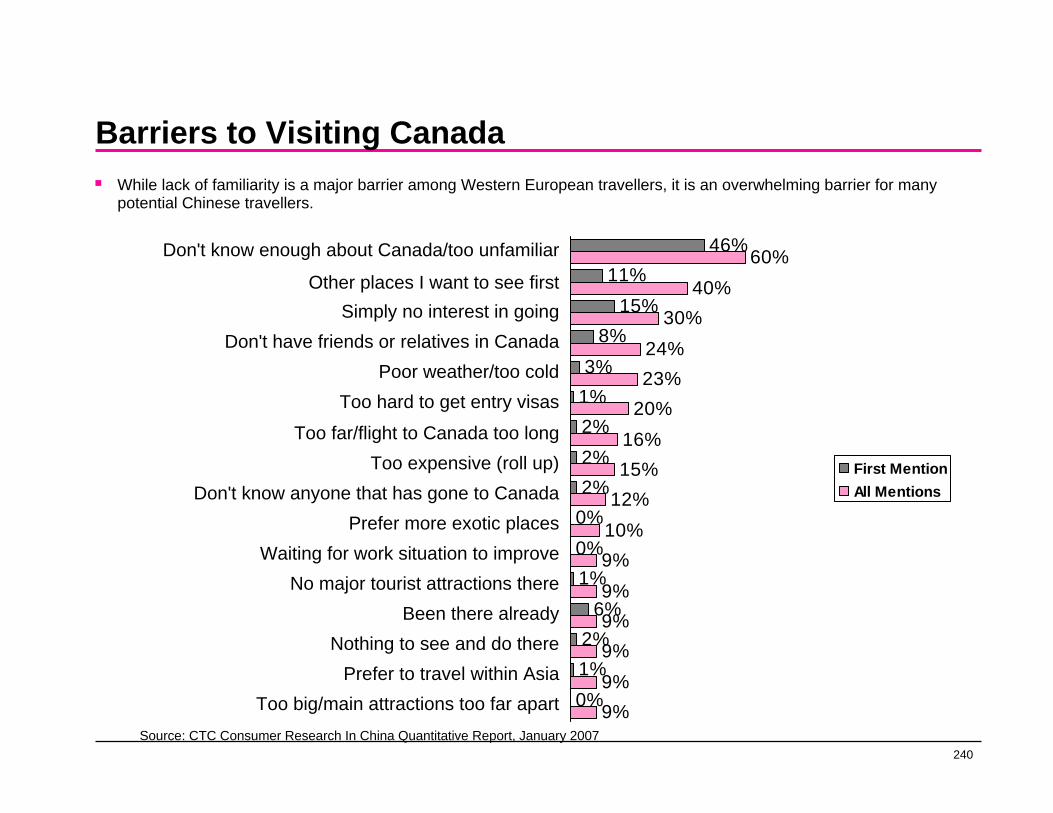

Lack of sufficient knowledge about Canada as a destination and the product available are the largest barriers to visiting. Canada is often viewed as too vast and can be intimidating to visitors who are used to travelling shorter distances.

British very commonly use the internet to book travel .

13

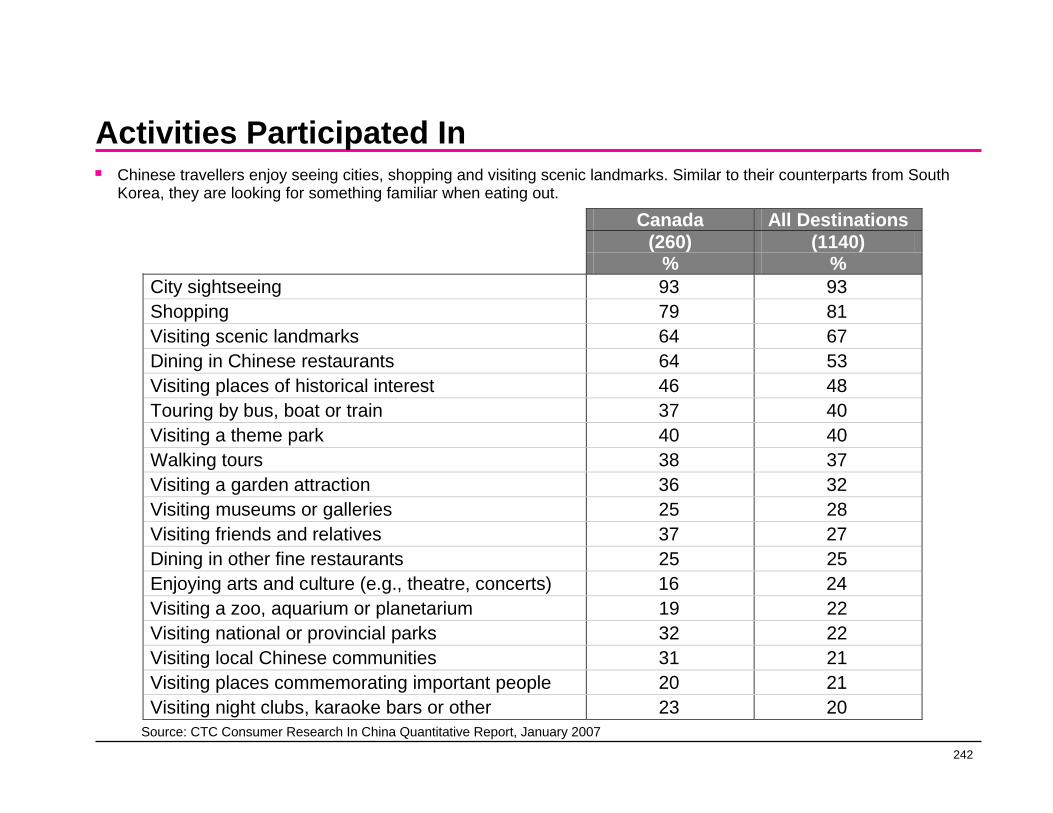

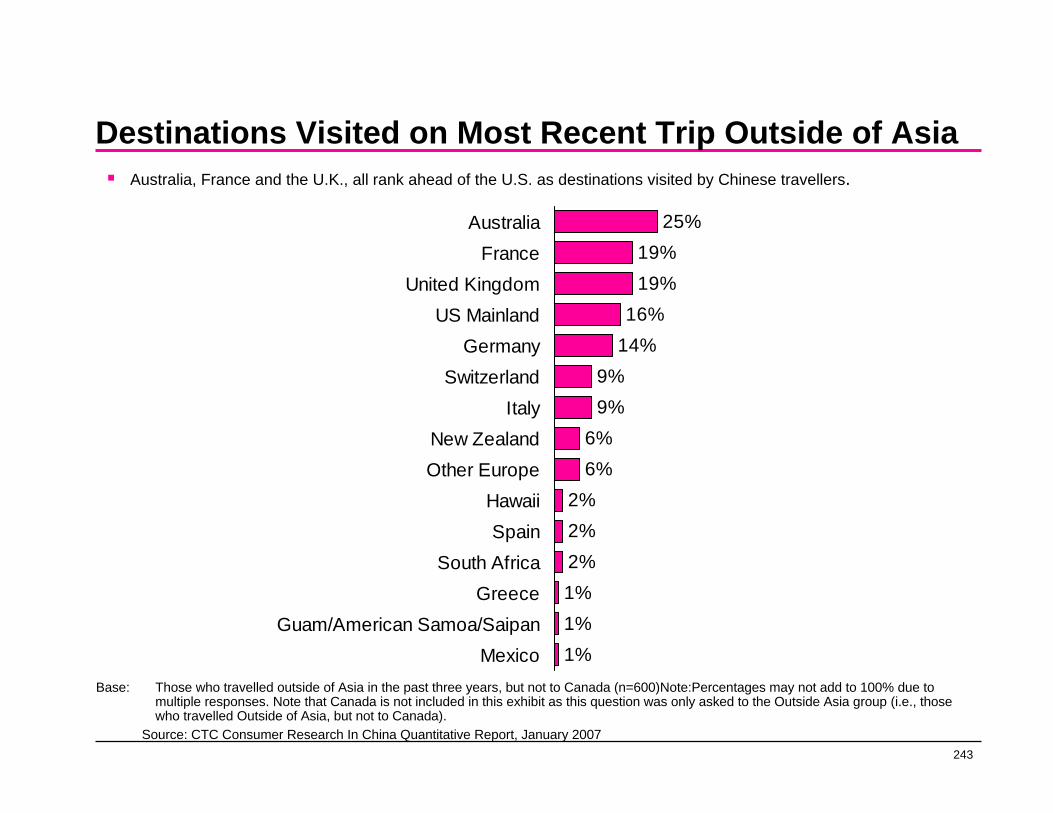

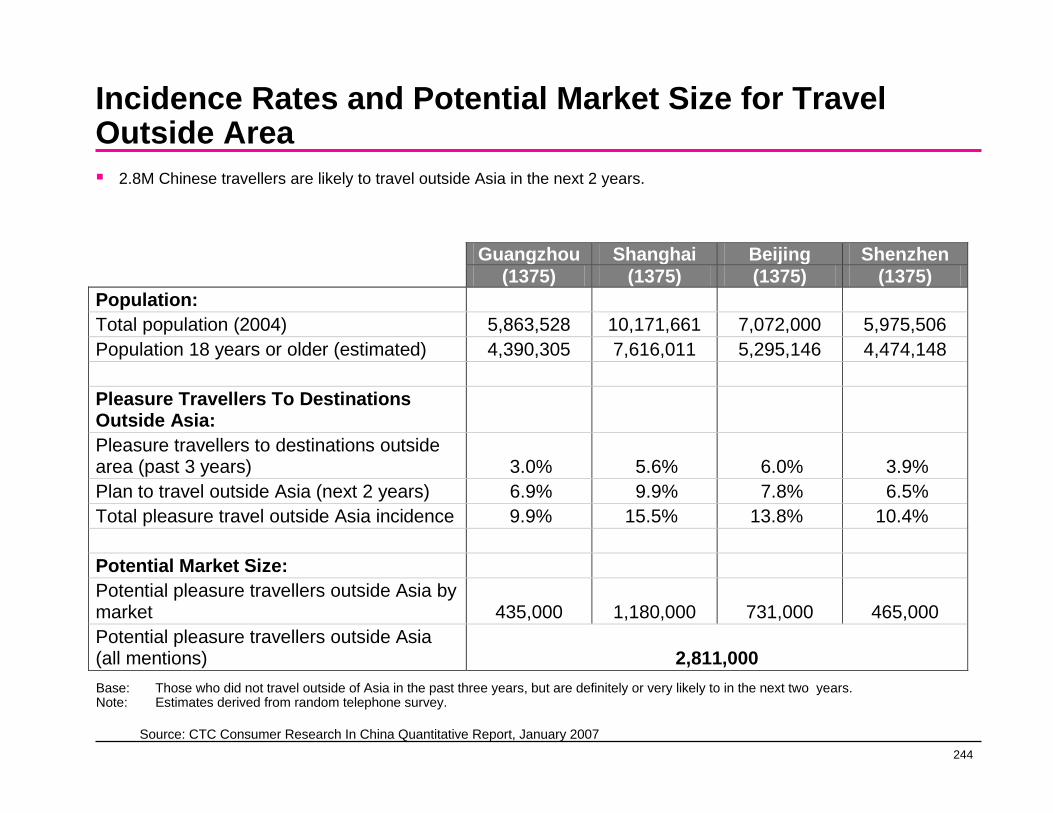

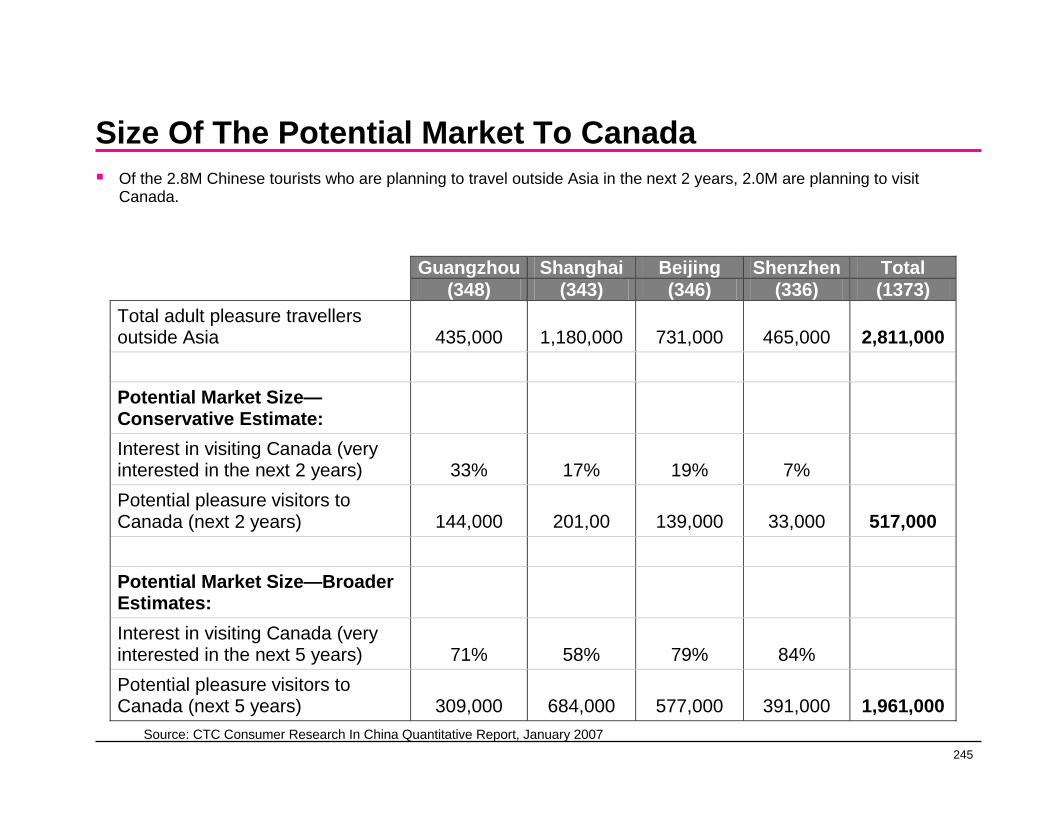

Ontario’s Best Prospect Markets: China

China

Well-established, middle-aged families with a visiting friends and relatives (“VFR”) connection.

Nouveau riche.

Managerial employees likely Joint Venture, foreign company.

35 - 54 years of age.

Canton province strongest market followed by Beijing.

Market RecommendationProfileConcentrate on increasing awareness for

future travel rather than short term gain.

Lack of familiarity with Canada (Ontario) needs to be addressed. Create a strong brand image that has cache value that will stand out against competitive destinations.

Use the web to promote all of Ontario’s product providing details on how to get the most out of a trip as this market wants to see as much as possible. Again, links to neighbouring provinces could increase overall drawing power.

Create a risk-free itinerary to make travel as easy as possible.

TV has strong influence on choice of travel destination (investigate the success of Dashan television show featuring Canada to determine if it would be useful to do a follow-up in the same format).

VFR from Canton province constitutes most immediate potential.

Try to leverage Vancouver 2010 games to benefit Ontario as a necessary destination if you visit Canada.

China’s growing middle class presents the best opportunity to increase visitation. But, without ADS there continue to be limitations.

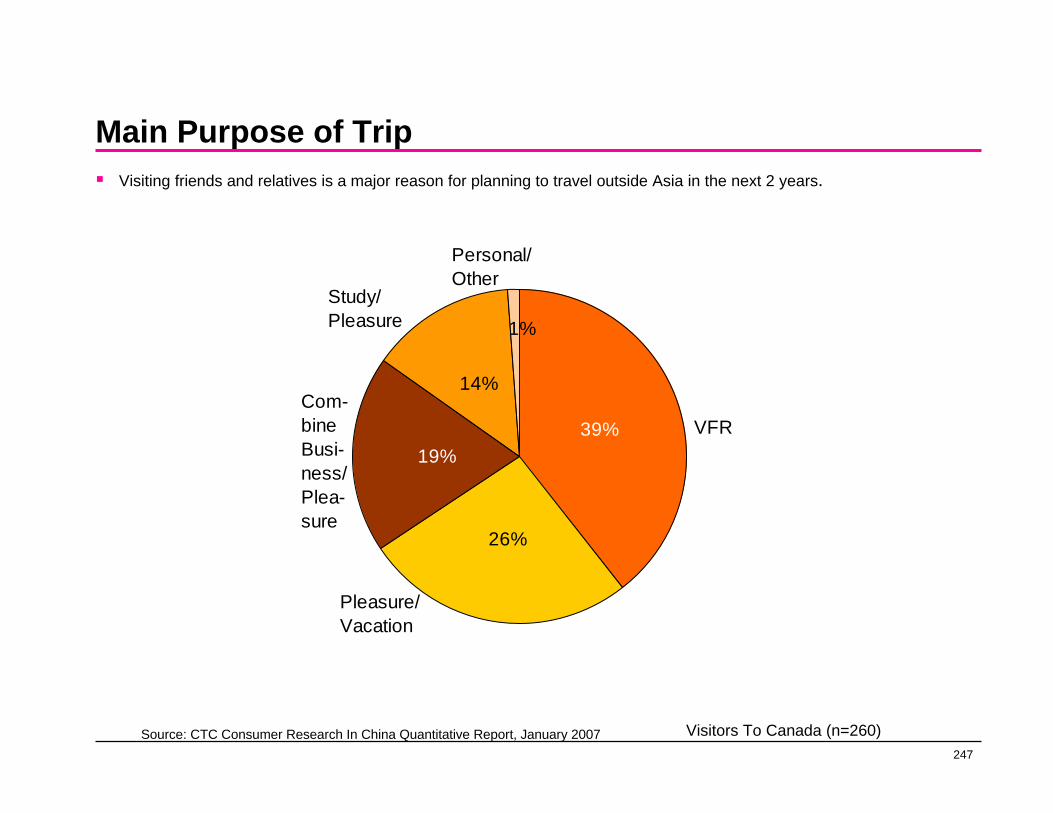

VFR tends to be the key reason for Chinese to visit Canada, particularly from Guangzhou/Canton province.

Canada is not perceived as a destination with lots to see or do.

Growth of consumerism in China could dissuade travel in near future as consumers purchase household conveniences.

The internet is a strong source of information for Chinese overseas travellers.

Great lack of awareness of Ontario, and its tourism offerings. Ontario/Canada seen as a destination for immigration or education but not necessarily for travel.

14

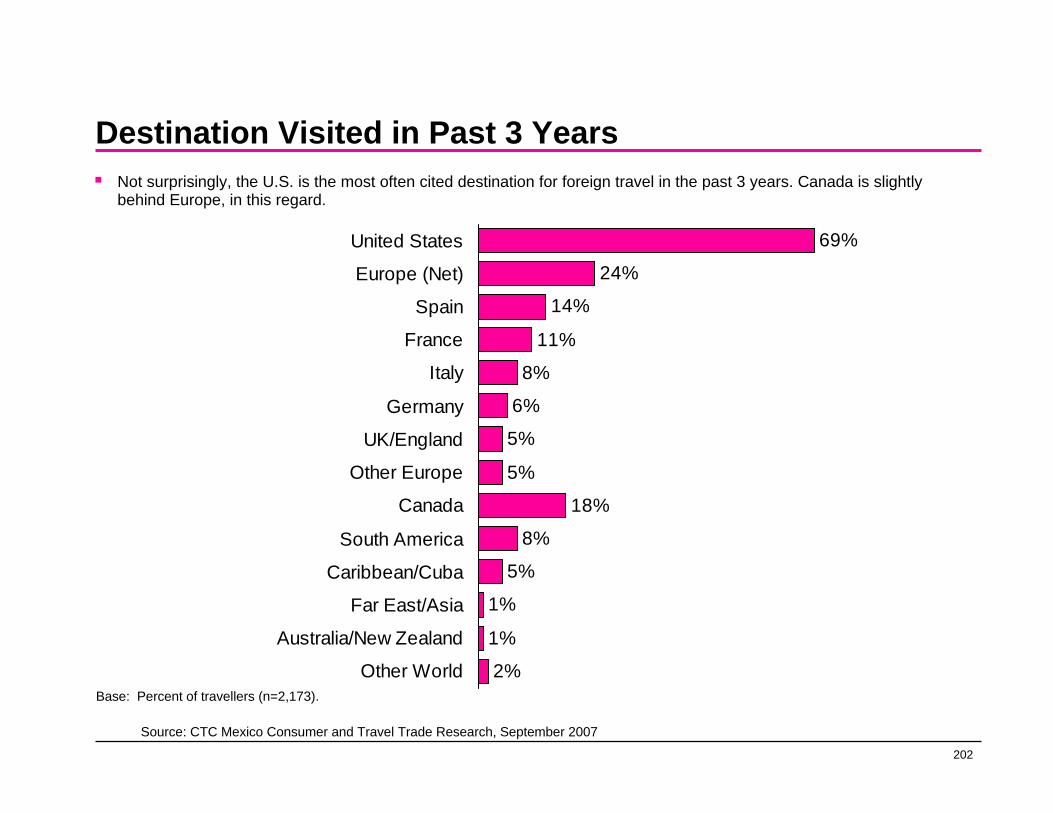

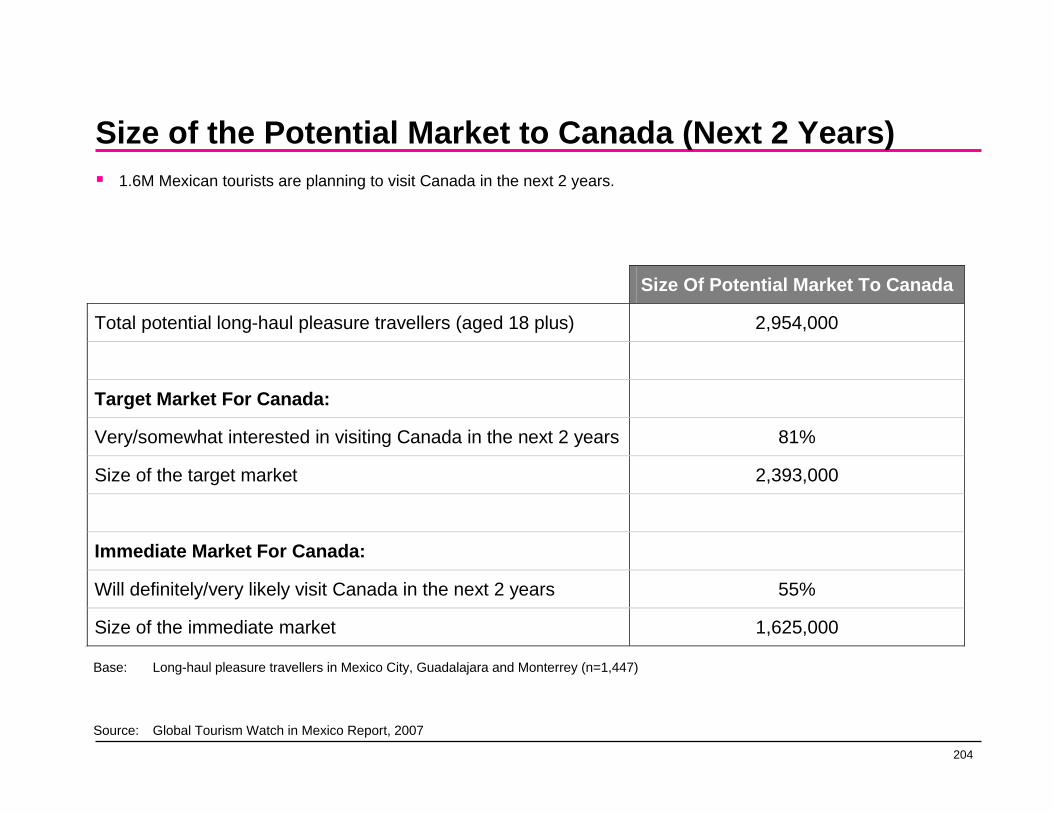

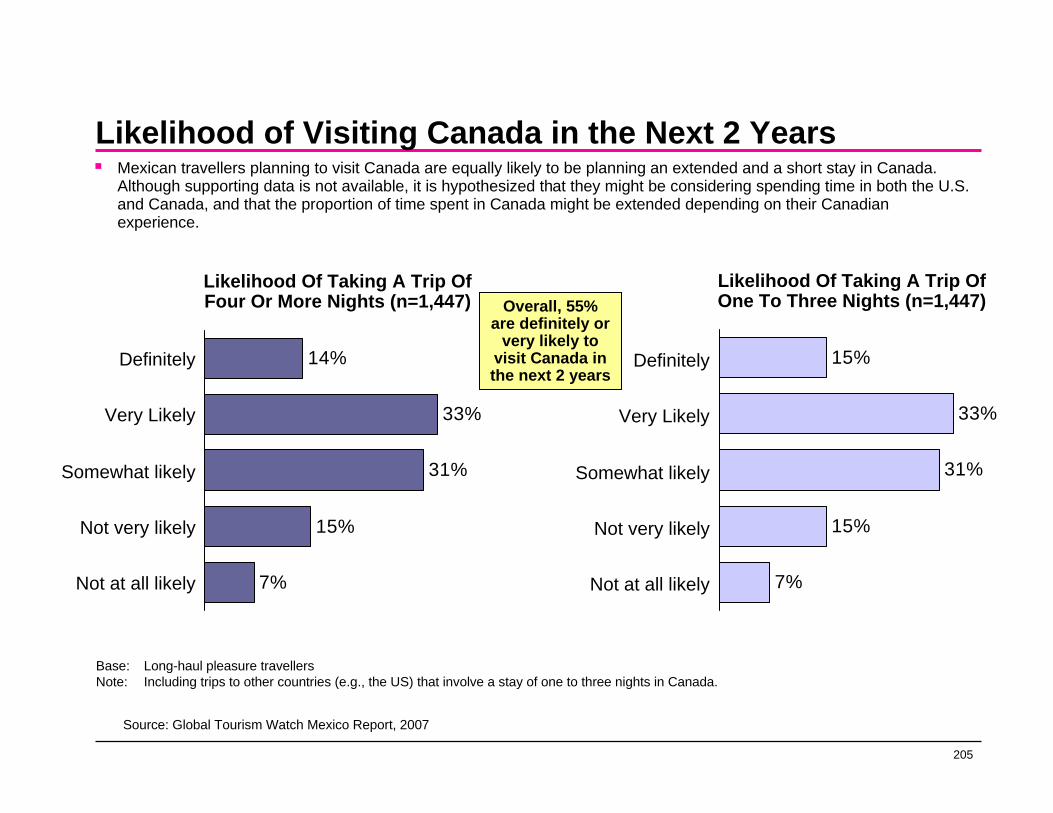

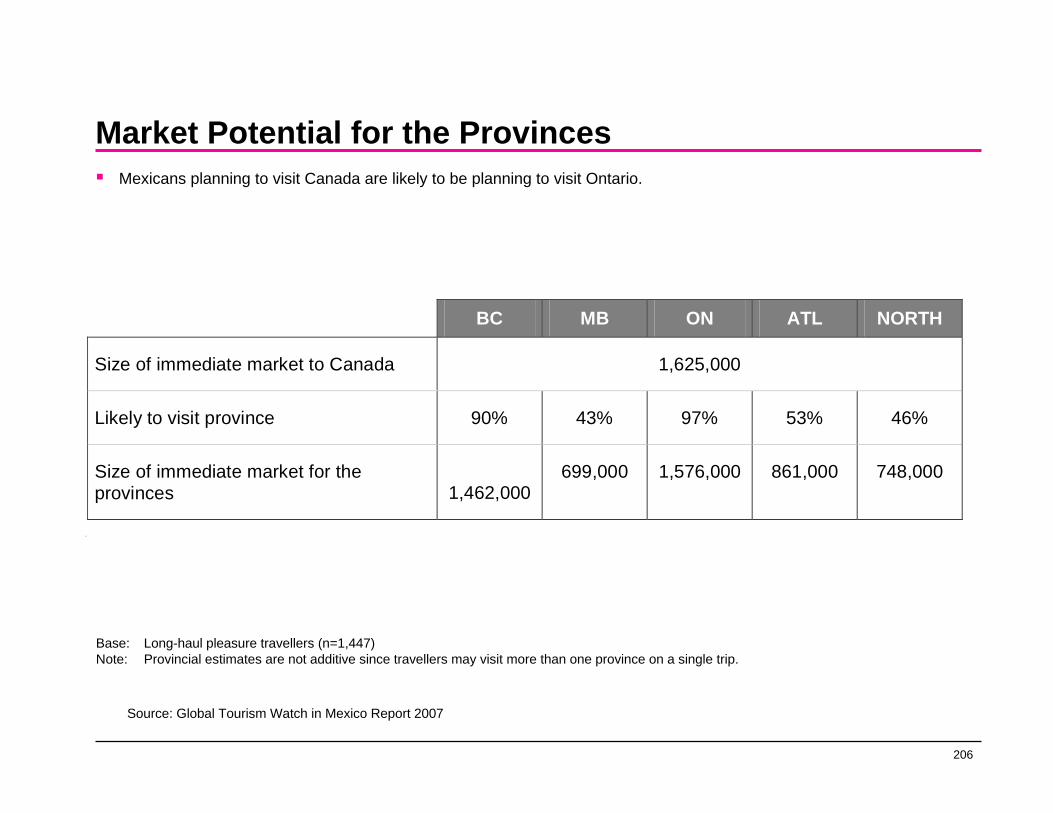

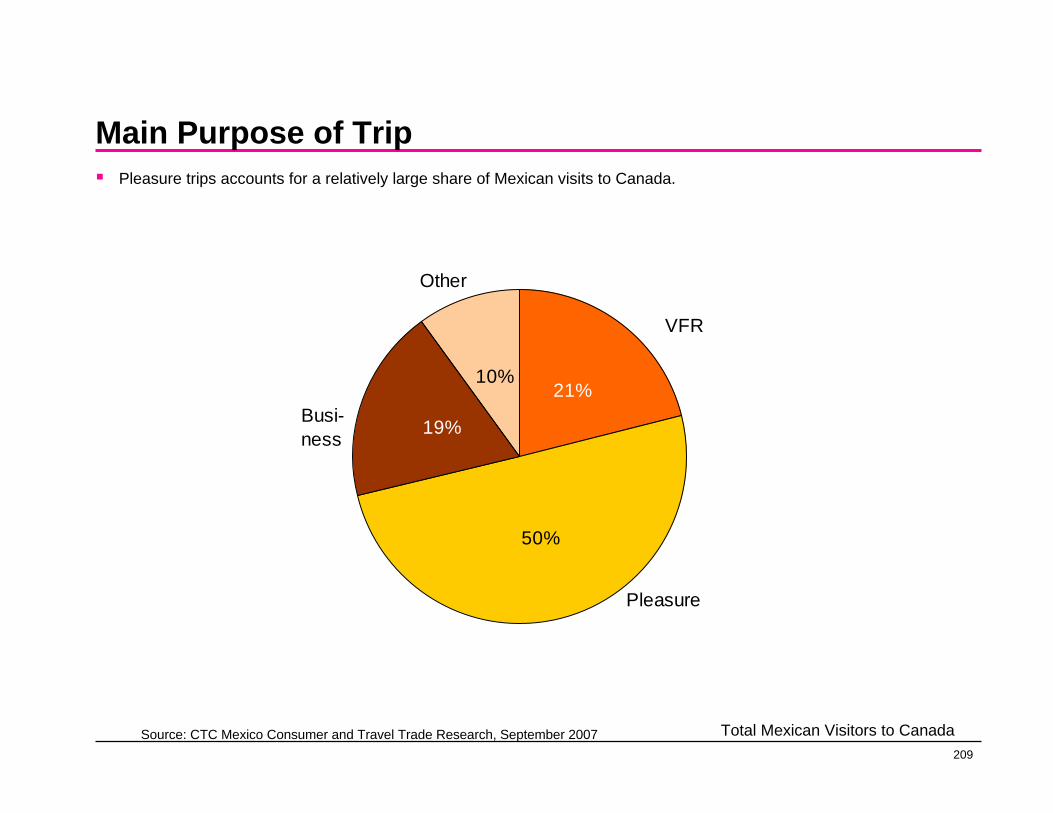

Ontario’s Best Prospect Markets: Mexico

Mexico

travellers tend to be middle-aged or older and well educated.

Strong brand recognition.

Educational travellers- look for education elements incorporated in their trips.

Shopping is very popular, even in comparison with other overseas visitors.

Market RecommendationProfileStrong internet penetration. Use web to

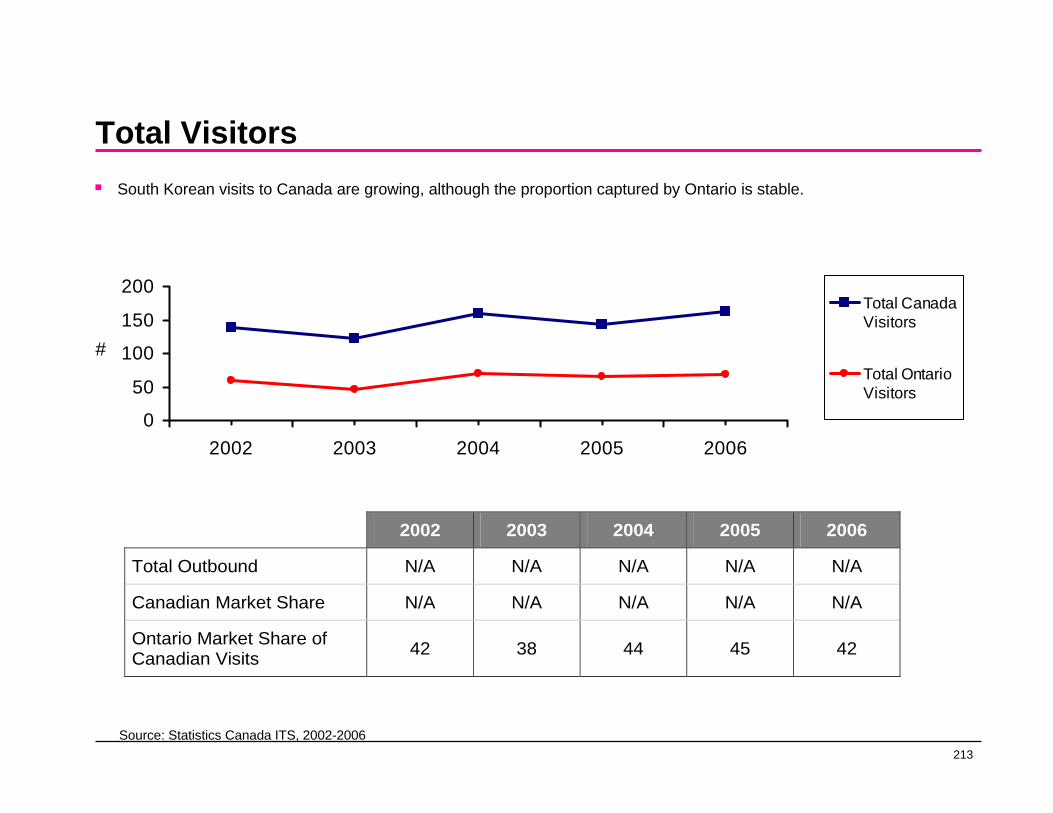

provide greater knowledge about Ontario’s product.

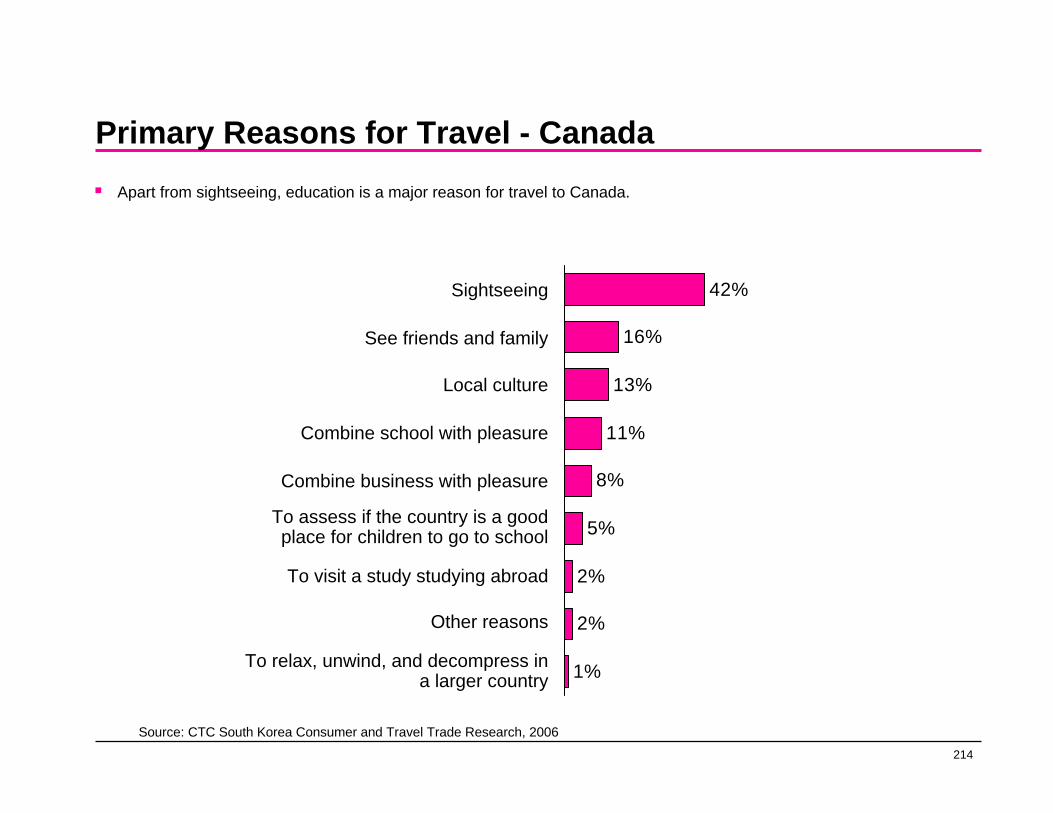

Focus on outdoor experiences and historic sites, potentially Northern experiences, such as wildlife viewing to compete with travel motivators more associated with B.C or other destinations (e.g., whale watching, Rockies).

Use travel media to target this group (e.g., articles, editorials, videos, etc.) to build the Ontario brand. Word of mouth is also important.

Incorporate urban learning experiences with rural outdoors experiences to respond to interests in education, shopping, and seeing wildlife and world heritage sites.

Highlight heritage sites (Niagara Falls, The Rideau Canal), the outdoors, as well as cultural elements within the outdoors, and shopping as key elements in presentation to Mexicans. The combination of these diverse elements in concert with education/historical underpinnings offer good potential to differentiate Ontario from other provinces in Canada.

Growing middle class that is likely to travel outside of the country.

Outdoors and major attractions seem to be key motivational activities for Mexican travellers

Educationally-orientated travellers.

Tend to be pleasure travellers who like to sightsee, shop, and participate in outdoor activities and local culture.

Ontario is the strongest Canadian market for Mexican tourists but is facing competition from B.C.

Strong desire to see places of historical importance such as world heritage sites, and as much as possible on one trip.

Lacking awareness of available product in Ontario.

Travel magazines, shows and guides are strong sources of information.

15

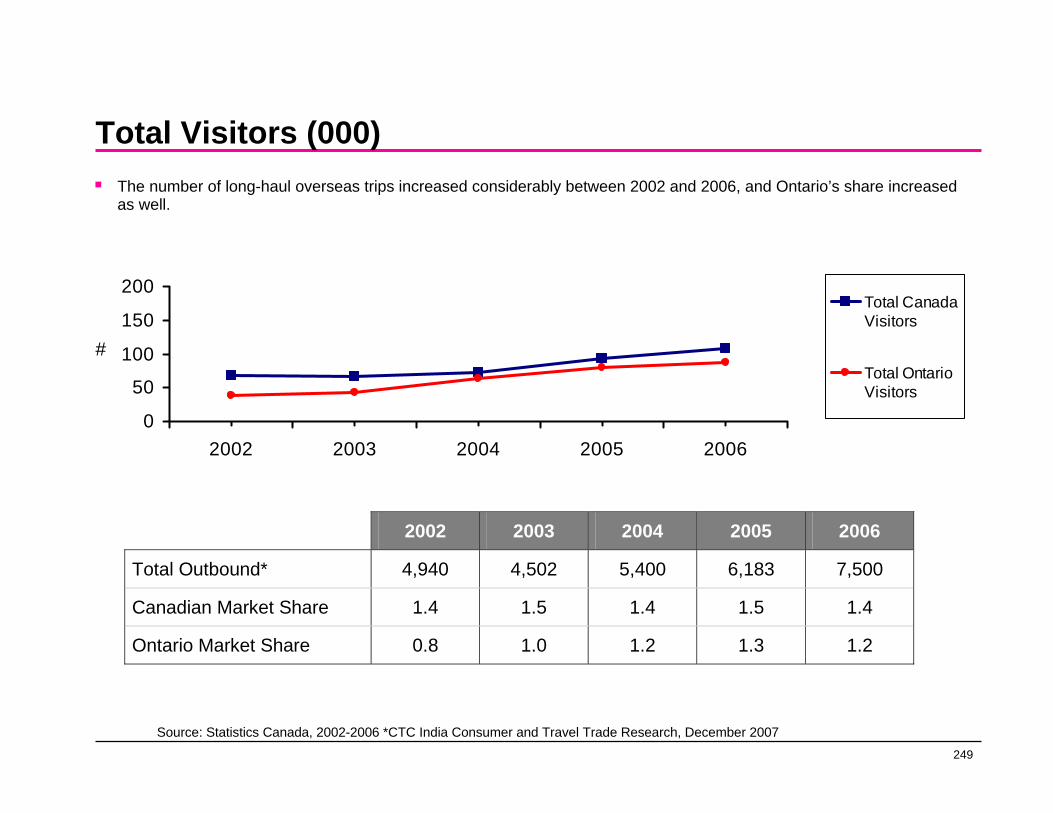

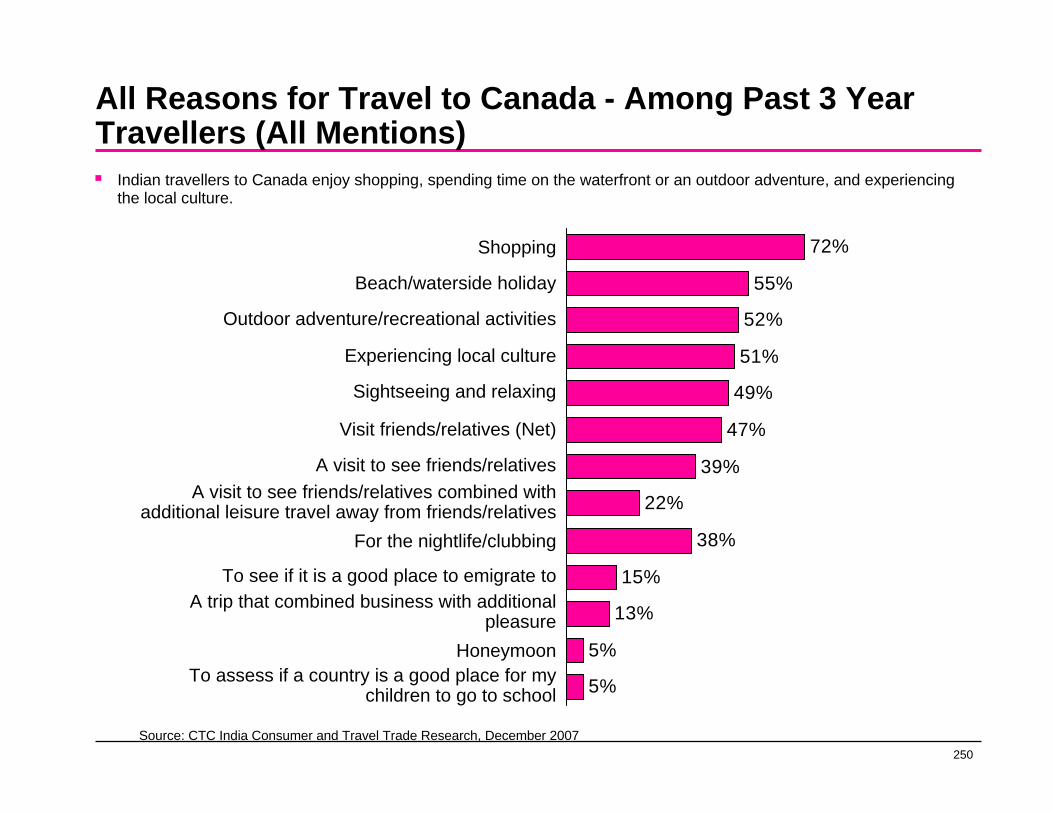

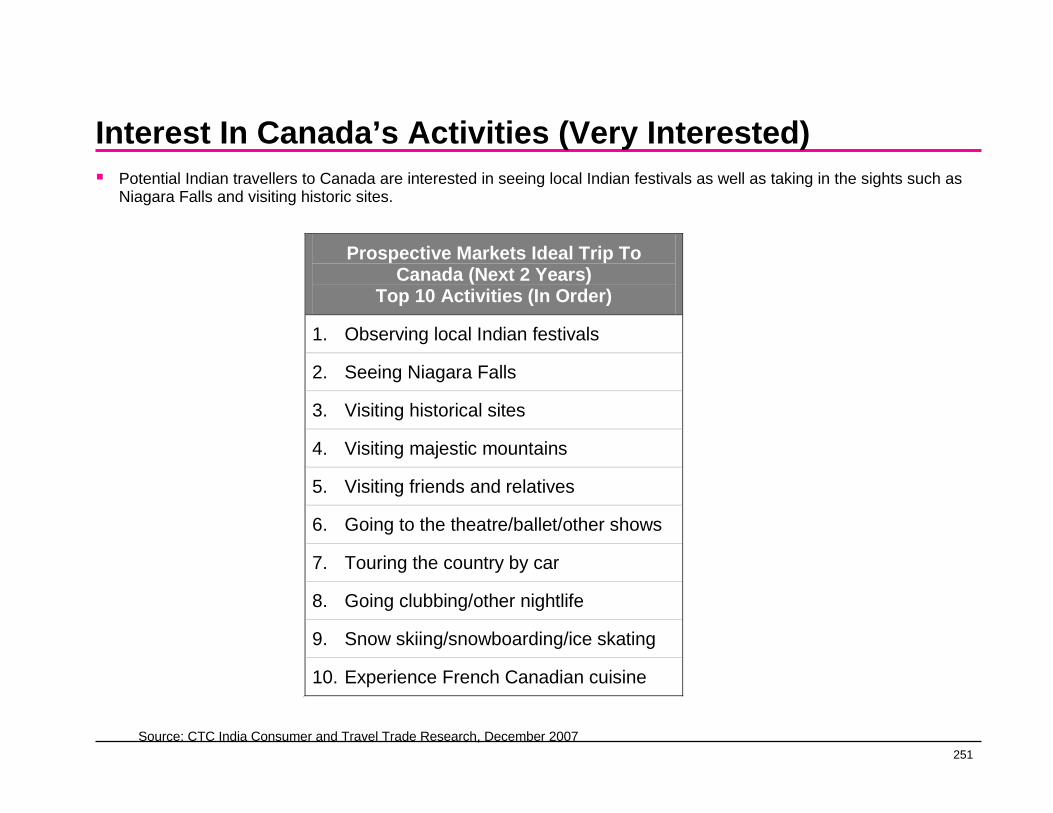

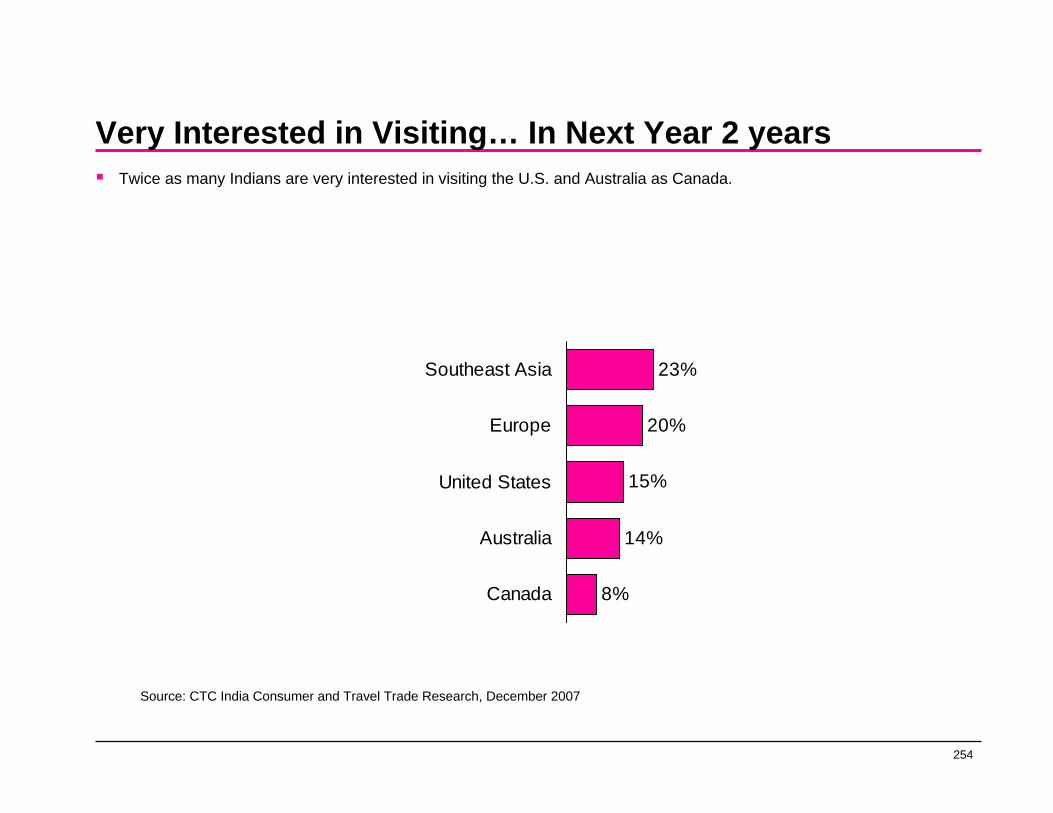

Ontario’s Best Prospect Markets: India

India

Higher socio-economic class (one-third of population).

VFR market is strong.

Tends to be younger 18-49 years of age.

Status Seekers.

Ontario captures most of the trips from India to Canada.

Market RecommendationProfilePromote Ontario as a must see status making

destination, particularly Niagara Falls. Build profile of other iconic, potentially status-worthy Ontario attractions and activities.

Consider building on VFR connections. Use Canadian hosts as ambassadors and conduits for extending the travel experience.

Aim to build word-of-mouth advertising as Indians tend to recount travel experiences to colleagues, friends and family.

Potential opportunity in winter months (honeymoon season) as the tendency is to travel to colder climates of the Himalayans but could create more status to visit Canada, particularly if linked to unique “must-do” activities (e.g., snowmobiling, dog-sledding, etc.)

Promote the nightlife and local culture available in Ontario as enticements to this market.

Promote the strong Indian cultural enclaves in Ontario as evidence of a welcoming non-threatening environment within a distinctively foreign land.

Television and radio are appropriate vehicles, focusing on major urban centres. The regional capital of Chandigarh should be included in any media plan given the large number of Ontarians originally from that region.

VFR tends to be a principal reason for travelling to Canada, but more as an afterthought to seeing the sights.

Higher socio-economic class, younger.

Social activities, such as nightlife, clubbing, and experience local culture.

Sightseeing and shopping top motivators.

Niagara Falls is a key attraction for most Indian visitors.

Status is a key travel motivator for Indian travellers.

Interest in Canada is limited compared to other more exotic destinations in Asia or Europe, which may be perceived as more enriching from both a cultural and status perspective.

16

Strategic Overview and Recommendations

17

Strategic Overview

Focus

Spend to Ontario’s strengths, i.e., where knowledge of Ontario and pools of convertible interest are greatest. This is especially important in the current economic climate. Indeed, even maintaining current volume may be a challenge.

A three-tier planning and investment strategy is recommended:

1. Regional Markets

Focus on markets where there is high potential for return on investment now. In a weaker economy, travellers may be restricting their destination options geographically allowing Ontario to tap into a relatively larger pool of potential visitorscloser to home. Key markets include, Ontario, U.S. near markets, select U.S. mid-markets and Quebec.

This does not imply accepting the status quo. To the contrary, these markets need to be approached with growing sophistication in terms of reaching relevant target groups with appropriate product and messages, and making use of emerging media to engage potential visitors with greater assurance. Packaging product will also become increasingly important as a means of simultaneously adding value and encouraging extended stays.

18

Strategic Overview

2. Traditional Overseas Markets

It is important for Ontario to maintain its standing in the traditional overseas markets, where the province already has a presence.

While these markets are not necessarily growing, they will continue to provide valuable revenue streams for the foreseeable future. In particular, the U.K. market is expected to remain the largest source of overseas visitors for at least the next five to ten years.

Work with the Canadian Tourism Commission (CTC) and independently to educate U.K. travellers and provide them with trip-planning information.

Online sources will be a cost-effective medium for communicating the desired message. Customize websites for other major overseas markets such as Germany and Japan.

3. New Overseas Markets

Plan longer-term to build new overseas markets. Monitor and consider assigning higher priority to budgets for Mexico, China and India. First steps should include online educational and promotional efforts, tailoring the site for each market. Co-ordinate and collaborate with the CTC to ensure that Ontario’s desired message and images are included in CTC

efforts.

19

Strategic Overview

Although a lower priority than the aforementioned three countries, South Korea and Brazil have also been identified as holding potential. In particular, Brazilian spending in Ontario currently surpasses that of Australians and is projected to grow to match that of visitors from France by 2012.

Significant budgets should not be devoted to developing these emerging markets immediately. Instead, emphasis should be placed on the exploration of opportunities and the eventual crafting of growth plans. Some fundamental questions still need to be answered, such as:

How should these markets be segmented and target groups defined in a manner that best serves Ontario’s interests?

What messages and product are relevant to these target groups?

How much will it cost to break into these markets, and which media and communications approaches will be most effective?

It is also likely necessary to come to terms with the CTC’s leading role in marketing Canadian destinations overseas and whether Ontario’s objectives can be accommodated effectively within the existing structure. Is it possible for Ontario to gain the leverage it needs within these emerging markets and, if not, what are the alternatives? It may very well be that Ontario’s objectives can be well accommodated within the overseas marketing program for the Canadian brand, and certainly this would be desirable. Regardless, it will be necessary to work closely with the CTC to ensure that strategic directions are congruent, that Ontario receives appropriate attention, and that budgets are sufficient and media mix optimized to achieve success.

20

Overview – Recommendations and Priorities

Canada

Don’t ignore Ontario as a source market. It is absolutely vital to the health of the domestic industry and open to competitive encroachment.Continue to develop the Quebec market, placing particular emphasis addressing Francophone sensibilities, emphasizing points of differentiation from Quebec and aligning product to interest (both in terms of geographical proximity and activities).The three western provinces (B.C., Alberta, Saskatchewan) do not represent high potential for Ontario at the present time.

United States

Maintain a presence in all Tier One markets as an important defensive/ maintenance measure.Pursue the Tier Three markets of New York City and also Chicago.Develop New Jersey, Philadelphia and Washington D.C. as budgets allow.Consider a targeted strategy for major Tier Four markets longer term.

21

Overview – Recommendations and Priorities

Overseas

Work with the CTC to ensure that Ontario’s desired presence and positioning is appropriately represented in overseas marketing for Canada (coordination of strategic direction).Maintain a presence in the traditional core European countries (Germany, France) and Japan.Focus on the U.K. as it will continue to be the overseas revenue leader.Develop China, followed by Mexico and India, as budgets allow. Due to proximity, Mexico represents a better immediate target than India. Mexicans travellers’ interests in nature and outdoor experiences, history and educational experiences fit well with the Ontario offering.Monitor the growth of the middle-class in India and develop communication and advertising programs as budgets allow. Determine whether a low-cost ‘host strategy’ targeted to major ethnic communities in Canada (Chinese, Indian) is viable as a means of generating greater tourism revenue from incoming VFR.Although a lower priority, monitor Brazil and South Korea

22

Detailed General Summary

23

Overview of Visitation and Spending - Domestic versus U.S. versus Overseas

24

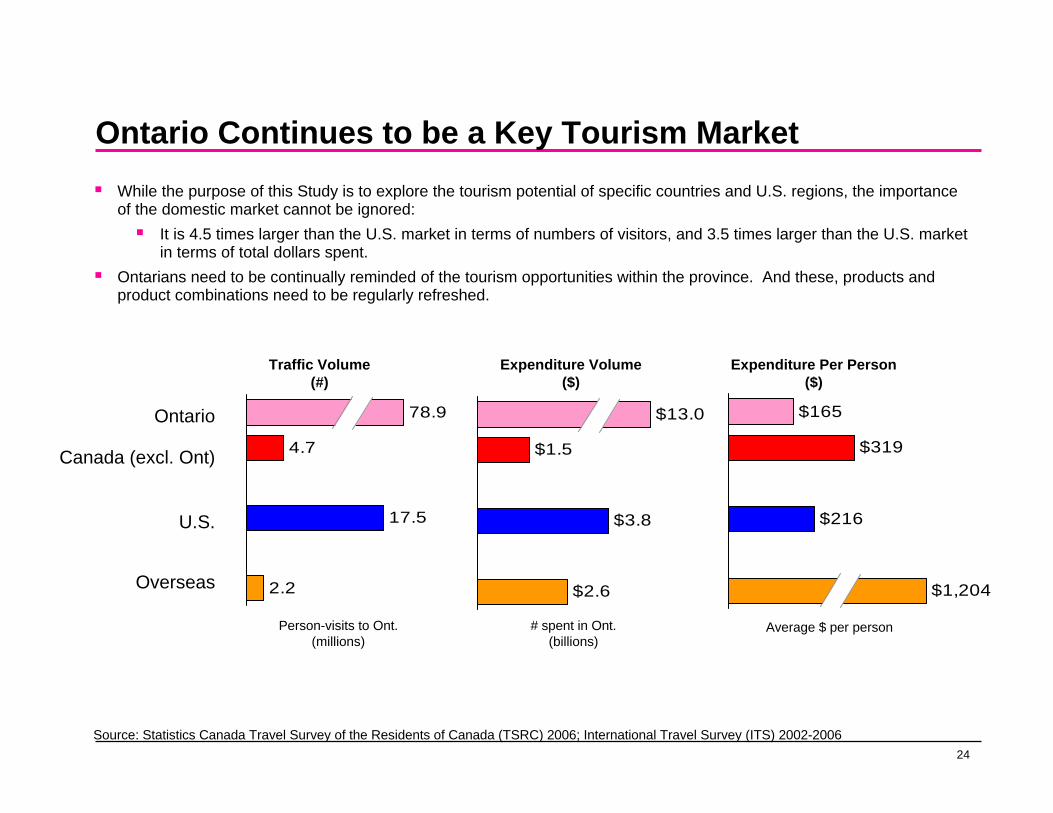

Ontario Continues to be a Key Tourism MarketWhile the purpose of this Study is to explore the tourism potential of specific countries and U.S. regions, the importance of the domestic market cannot be ignored:

It is 4.5 times larger than the U.S. market in terms of numbers of visitors, and 3.5 times larger than the U.S. market in terms of total dollars spent.

Ontarians need to be continually reminded of the tourism opportunities within the province. And these, products and product combinations need to be regularly refreshed.

4.7

17.5

2.2

78.9

$1.5

$3.8

$2.6

$13.0 $165

$319

$216

$1,204

Ontario

Canada (excl. Ont)

U.S.

Overseas

Traffic Volume(#)

Expenditure Volume($)

Expenditure Per Person($)

Person-visits to Ont.(millions)

# spent in Ont.(billions)

Average $ per person

Source: Statistics Canada Travel Survey of the Residents of Canada (TSRC) 2006; International Travel Survey (ITS) 2002-2006

25

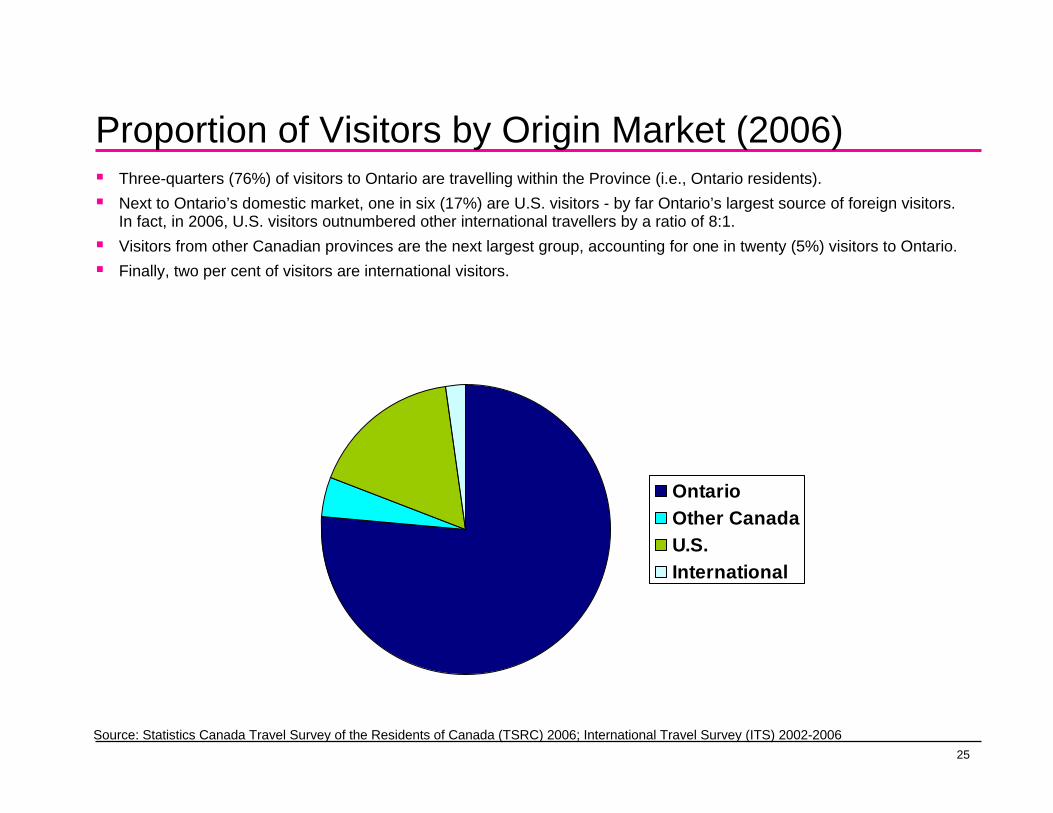

Proportion of Visitors by Origin Market (2006)Three-quarters (76%) of visitors to Ontario are travelling within the Province (i.e., Ontario residents).Next to Ontario’s domestic market, one in six (17%) are U.S. visitors - by far Ontario’s largest source of foreign visitors. In fact, in 2006, U.S. visitors outnumbered other international travellers by a ratio of 8:1.Visitors from other Canadian provinces are the next largest group, accounting for one in twenty (5%) visitors to Ontario.Finally, two per cent of visitors are international visitors.

OntarioOther CanadaU.S.International

Source: Statistics Canada Travel Survey of the Residents of Canada (TSRC) 2006; International Travel Survey (ITS) 2002-2006

26

Overview of Visitation and Spending - U.S. versus Overseas

27

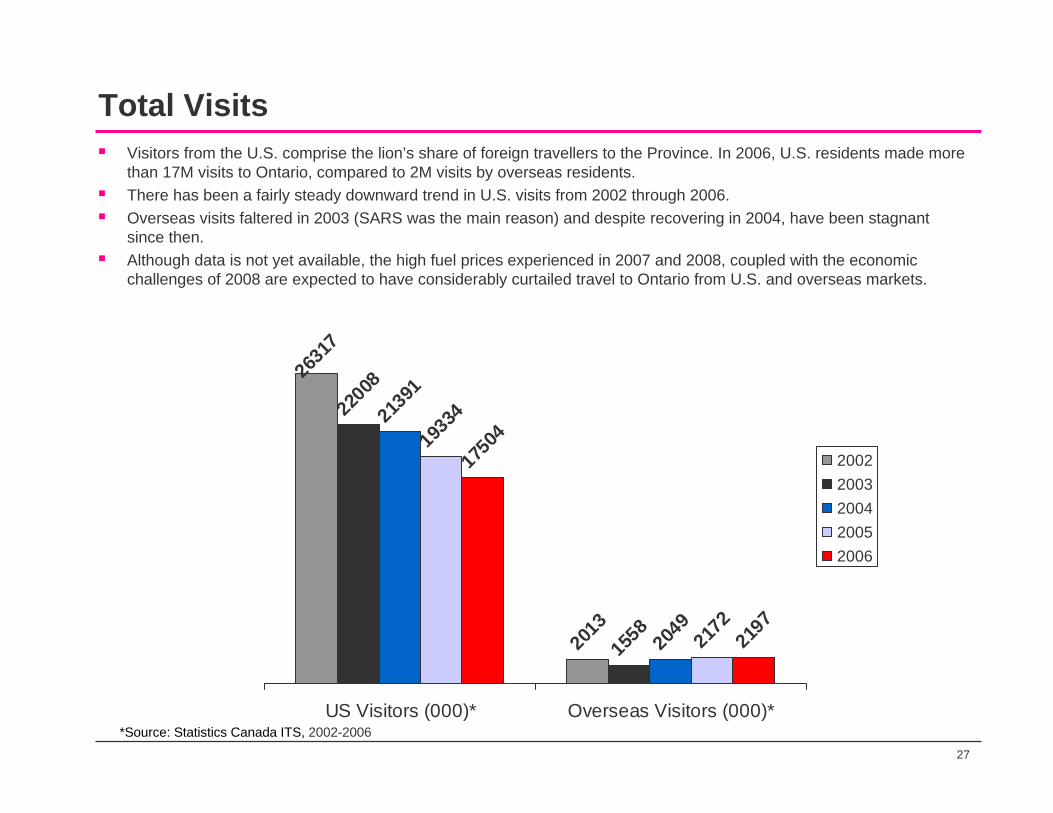

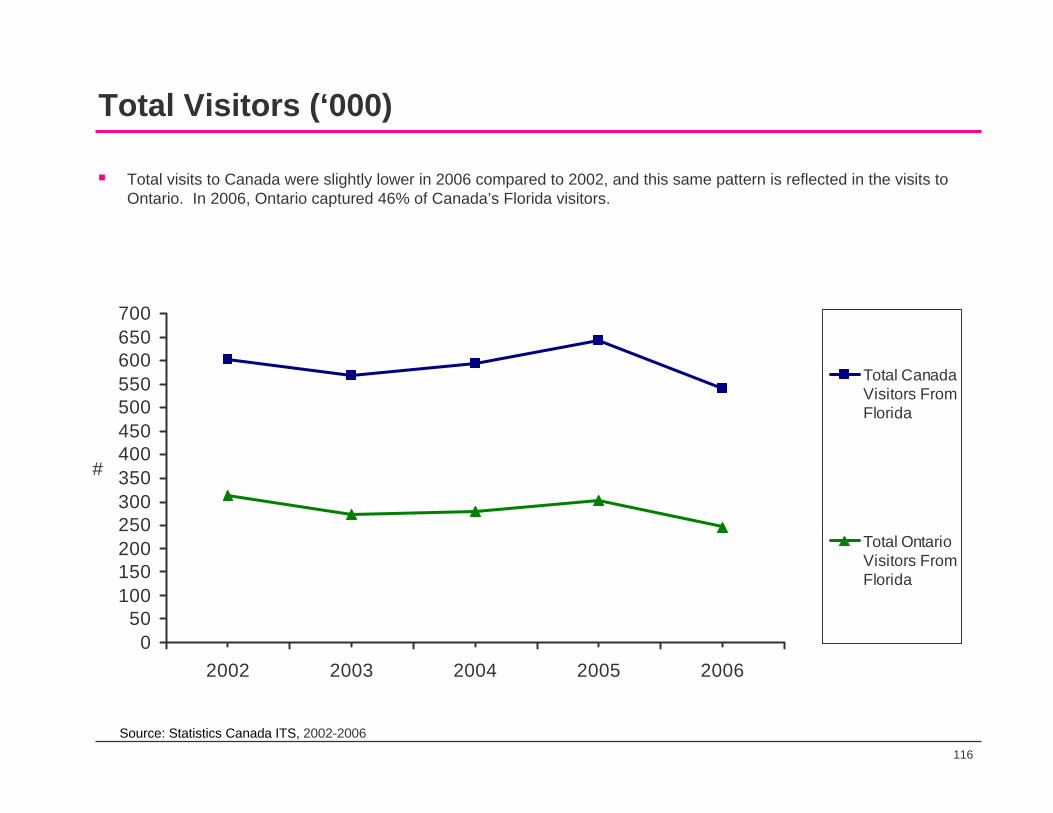

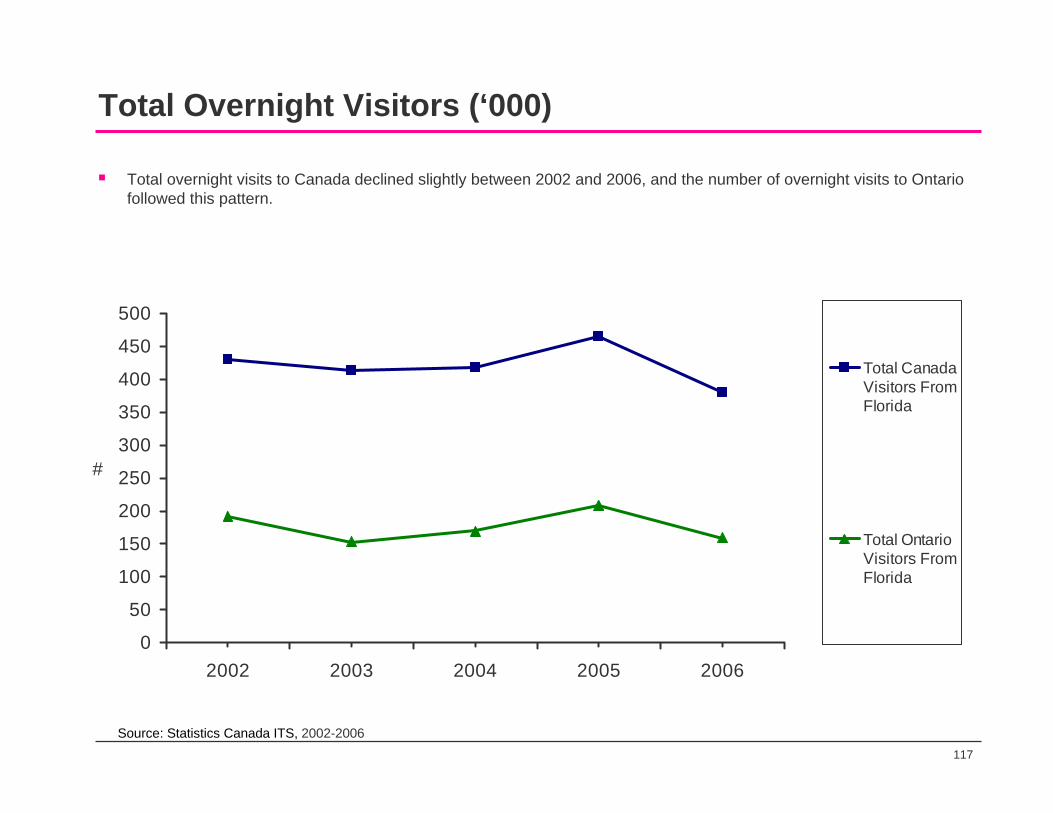

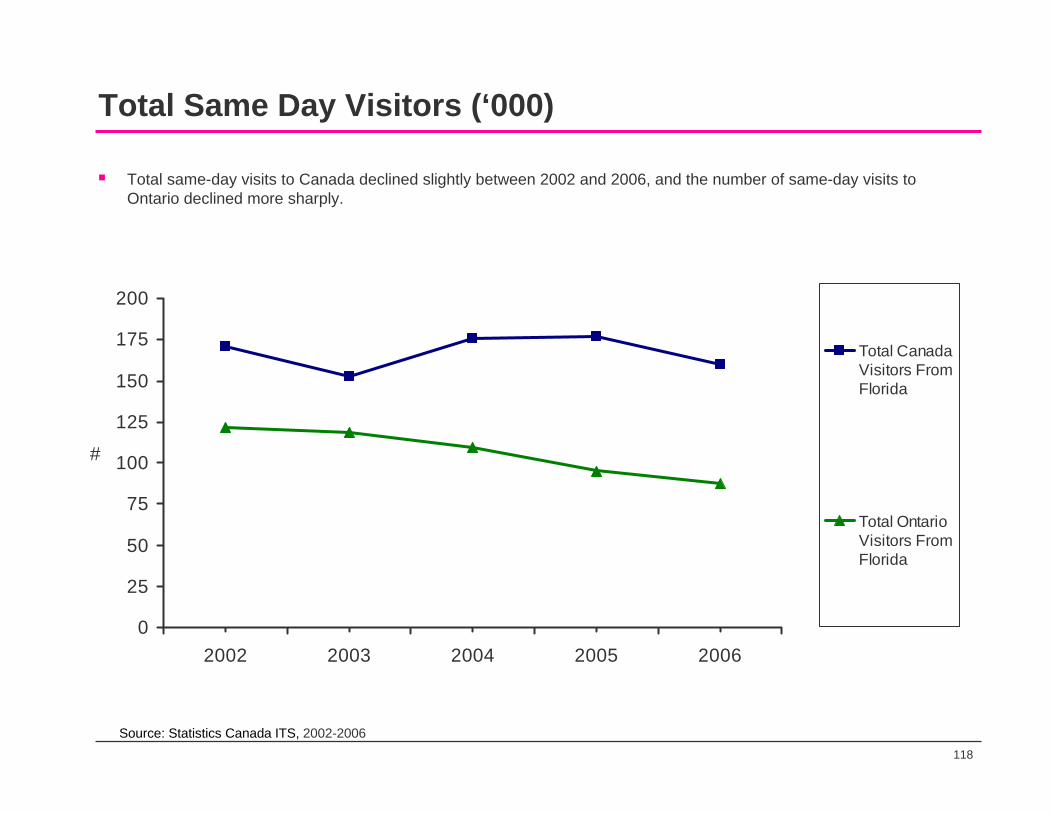

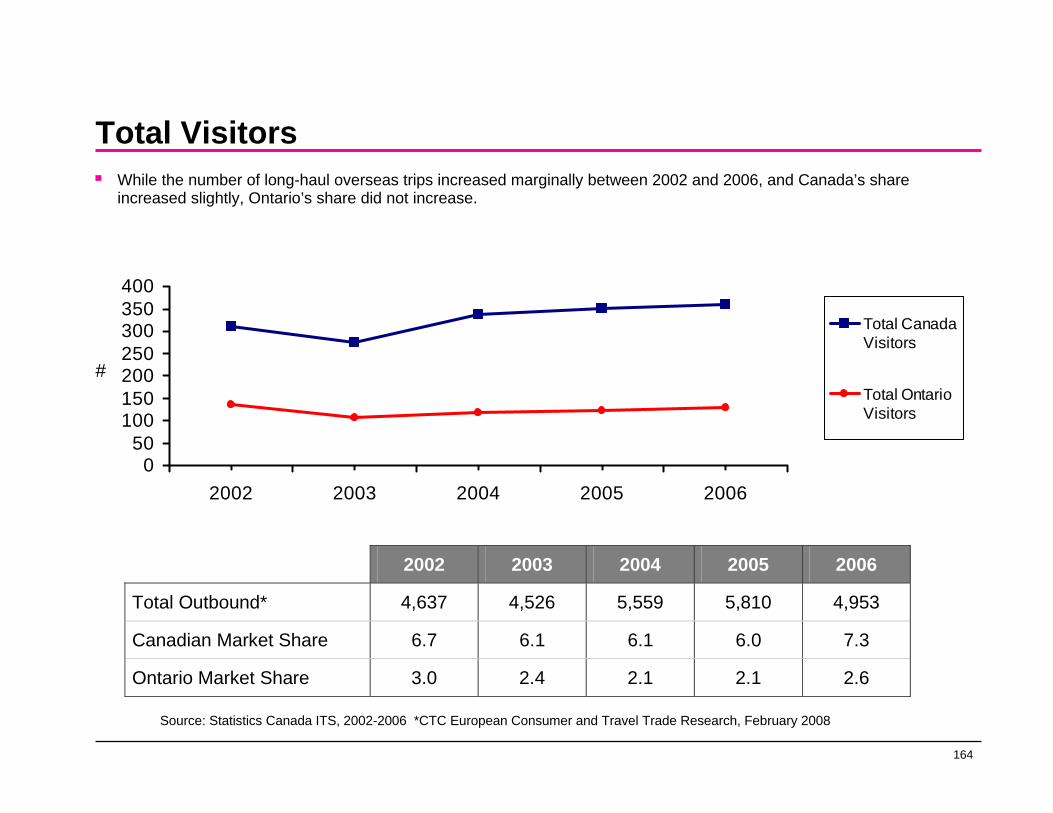

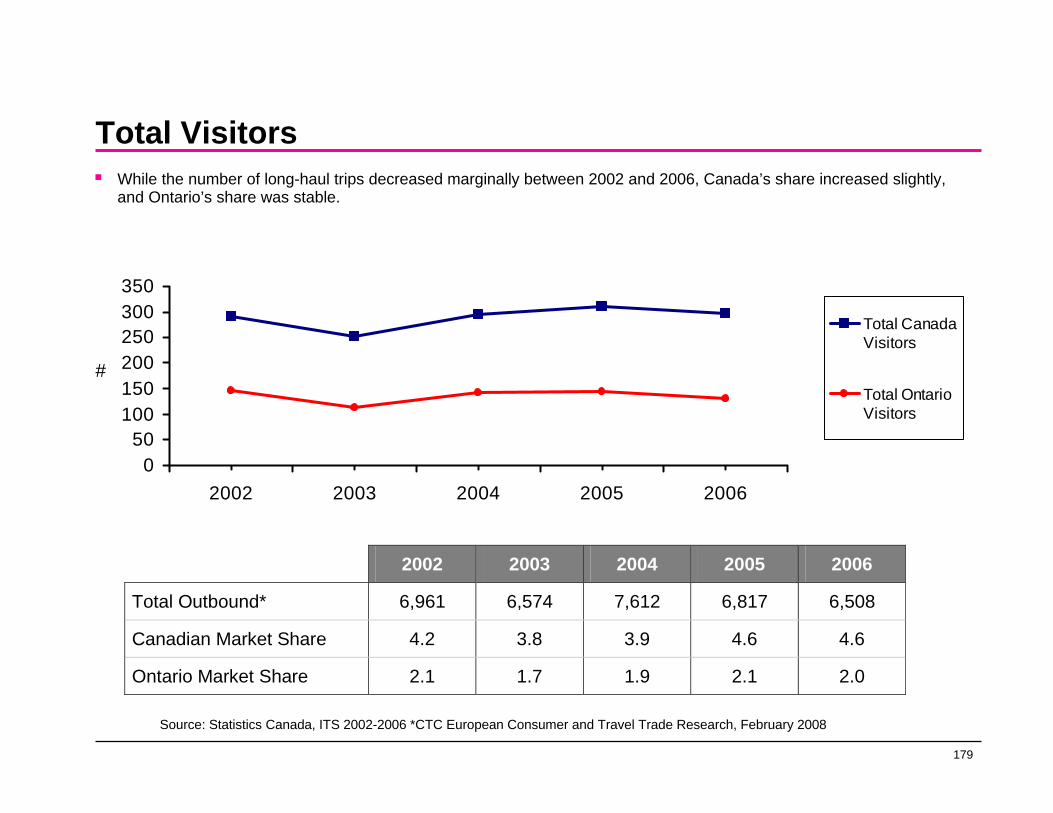

Total VisitsVisitors from the U.S. comprise the lion’s share of foreign travellers to the Province. In 2006, U.S. residents made more than 17M visits to Ontario, compared to 2M visits by overseas residents.There has been a fairly steady downward trend in U.S. visits from 2002 through 2006.Overseas visits faltered in 2003 (SARS was the main reason) and despite recovering in 2004, have been stagnant since then.Although data is not yet available, the high fuel prices experienced in 2007 and 2008, coupled with the economic challenges of 2008 are expected to have considerably curtailed travel to Ontario from U.S. and overseas markets.

2631

7

2013

2200

8

1558

2139

1

2049

1933

4

2172

1750

4

2197

US Visitors (000)* Overseas Visitors (000)*

20022003200420052006

*Source: Statistics Canada ITS, 2002-2006

28

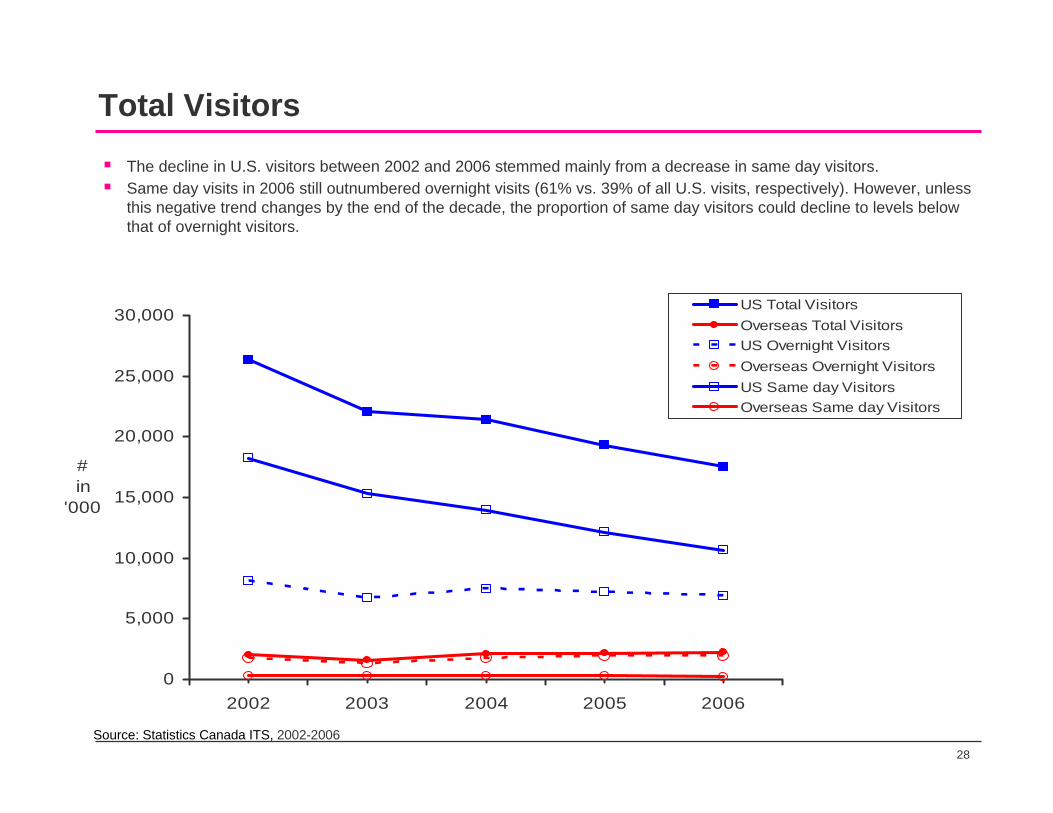

Total Visitors

The decline in U.S. visitors between 2002 and 2006 stemmed mainly from a decrease in same day visitors.Same day visits in 2006 still outnumbered overnight visits (61% vs. 39% of all U.S. visits, respectively). However, unless this negative trend changes by the end of the decade, the proportion of same day visitors could decline to levels below that of overnight visitors.

0

5,000

10,000

15,000

20,000

25,000

30,000

2002 2003 2004 2005 2006

#in

'000

US Total VisitorsOverseas Total VisitorsUS Overnight VisitorsOverseas Overnight VisitorsUS Same day VisitorsOverseas Same day Visitors

Source: Statistics Canada ITS, 2002-2006

29

Same Day Spending

1,385

1,1421,058

885771

191 136 143 118 127

0

500

1,000

1,500

2002 2003 2004 2005 2006

$in

million

USOverseas

Source: Statistics Canada ITS, 2002-2006

Same-day visitors’ spending patterns generally reflect the same trends as same-day visits to the province, with a significant downward trend in spending among U.S. visitors.Overseas same-day visitors are more lucrative to Ontario than U.S. same-day visitors, as the former likely compress more tourist activities into a single day. While overseas visitors represent only 2% of the total same-day visitors in 2006, they account for a disproportionately large share (14%) of the total dollars spent by same-day visitors in Ontario.

30

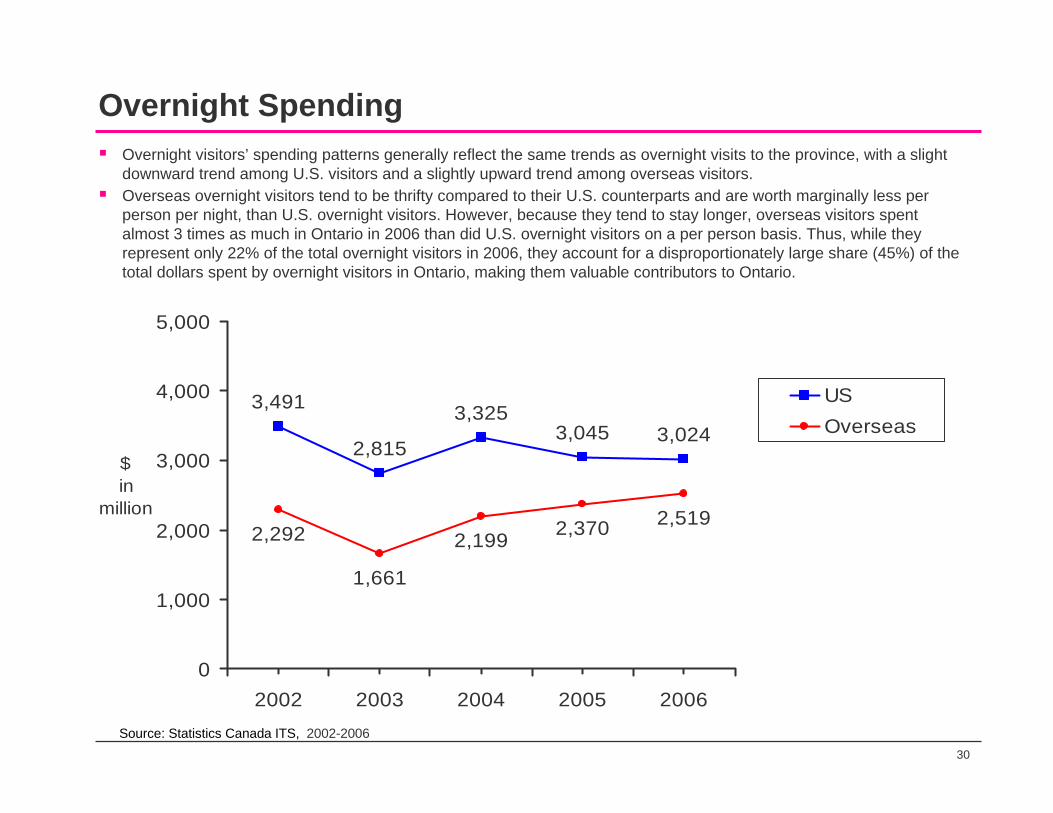

Overnight Spending

3,491

2,815

3,3253,045 3,024

2,292

1,661

2,199 2,370 2,519

0

1,000

2,000

3,000

4,000

5,000

2002 2003 2004 2005 2006

$in

million

USOverseas

Overnight visitors’ spending patterns generally reflect the same trends as overnight visits to the province, with a slight downward trend among U.S. visitors and a slightly upward trend among overseas visitors.Overseas overnight visitors tend to be thrifty compared to their U.S. counterparts and are worth marginally less per person per night, than U.S. overnight visitors. However, because they tend to stay longer, overseas visitors spent almost 3 times as much in Ontario in 2006 than did U.S. overnight visitors on a per person basis. Thus, while they represent only 22% of the total overnight visitors in 2006, they account for a disproportionately large share (45%) of the total dollars spent by overnight visitors in Ontario, making them valuable contributors to Ontario.

Source: Statistics Canada ITS, 2002-2006

31

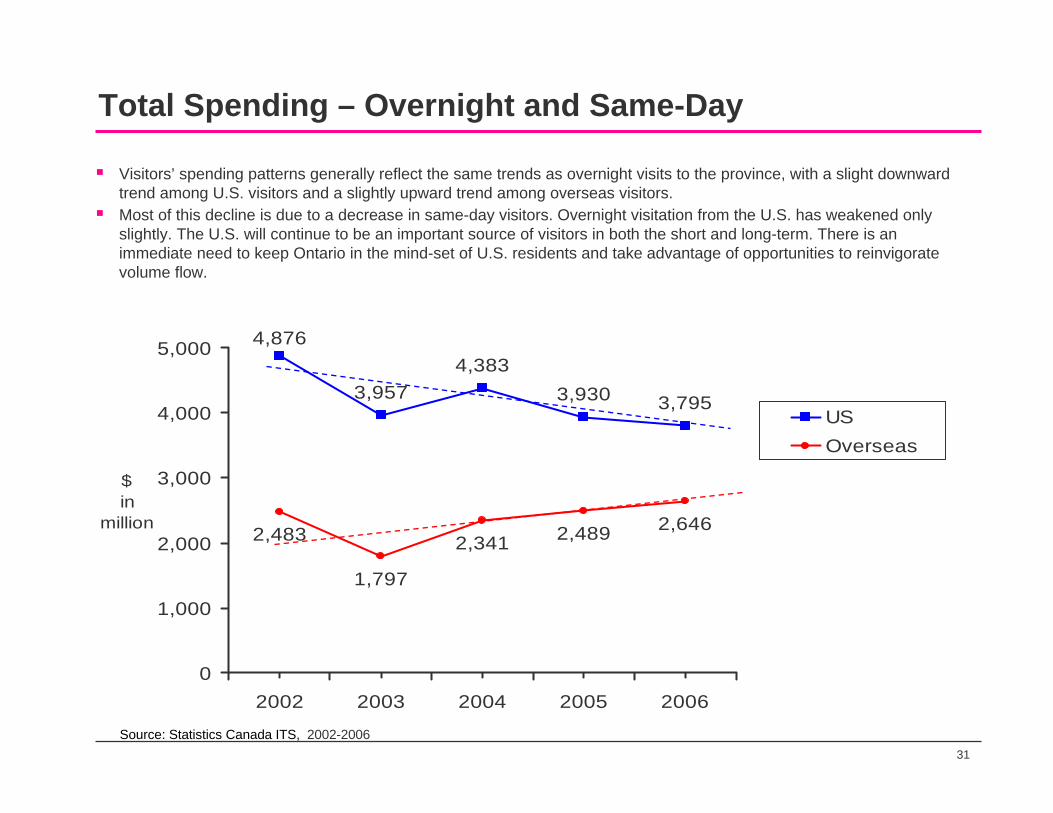

Total Spending – Overnight and Same-Day

4,876

3,9574,383

3,930 3,795

2,483

1,797

2,341 2,489 2,646

0

1,000

2,000

3,000

4,000

5,000

2002 2003 2004 2005 2006

$in

million

USOverseas

Visitors’ spending patterns generally reflect the same trends as overnight visits to the province, with a slight downward trend among U.S. visitors and a slightly upward trend among overseas visitors.Most of this decline is due to a decrease in same-day visitors. Overnight visitation from the U.S. has weakened only slightly. The U.S. will continue to be an important source of visitors in both the short and long-term. There is an immediate need to keep Ontario in the mind-set of U.S. residents and take advantage of opportunities to reinvigorate volume flow.

Source: Statistics Canada ITS, 2002-2006

32

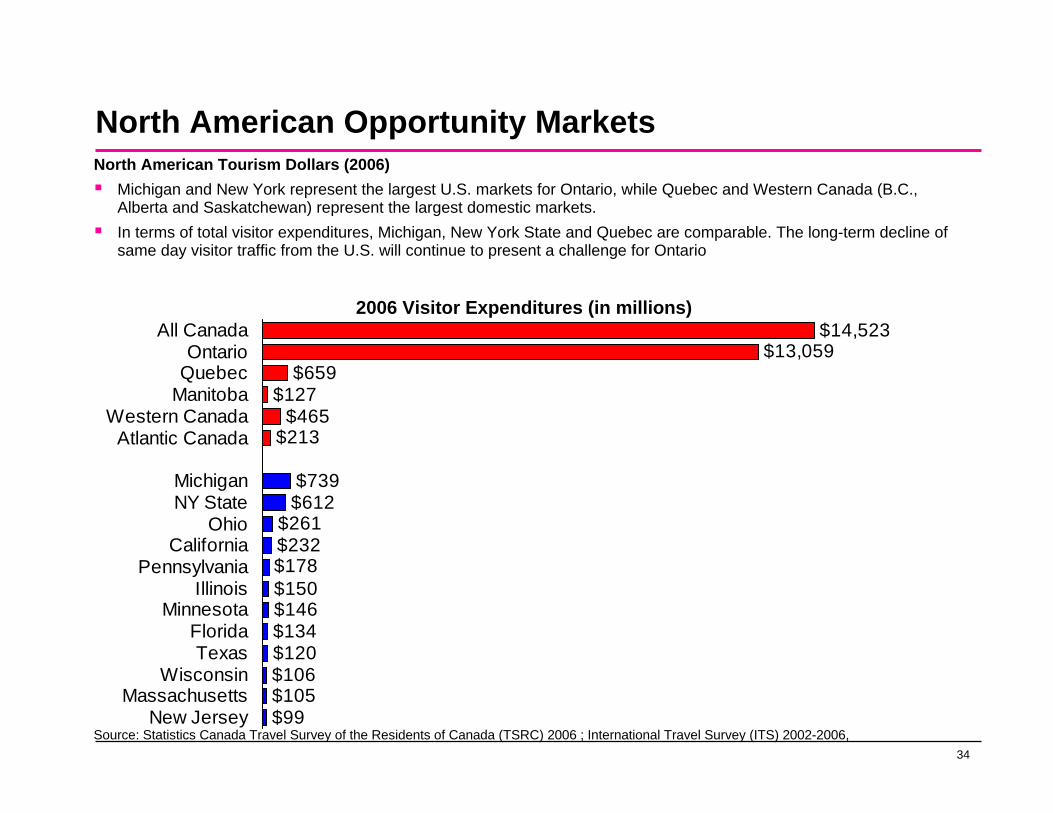

North American Opportunity Markets

33

Ontario’s Best Prospect Markets: North America

RecommendationMarket

Monitor the numbers of potential Ontario visitors, possibly undertaking research if numbers of potential visitors appear to be growing.

The next step would involve identifying activity and life-stage/psychographic segments for targeting within significant population clusters.

Distant U.S. markets with large numbers of open non-visitors such as California, Florida, Georgia, Texas and Arizona (Tier Four)

5.

Launch marketing efforts as budgets allow.New Jersey, Philadelphia, Washington DC (undeveloped Tier Three markets)

4.

Target Montreal and Quebec communities along the Ontario border.

Quebec3.

Continue to build on past efforts.New York City, Chicago (Tier Three)2.

Maintain focus on core markets.Eastern Michigan/Northern Ohio/ Western New York urban markets (Tier One)

1.

34

$99 $105 $106 $120 $134

$261

$739

$213 $465

$127 $659

$13,059 $14,523

$612

$232 $178 $150$146

All CanadaOntario

QuebecManitoba

Western CanadaAtlantic Canada

MichiganNY State

OhioCalifornia

PennsylvaniaIllinois

MinnesotaFloridaTexas

WisconsinMassachusetts

New Jersey

North American Opportunity Markets

Source: Statistics Canada Travel Survey of the Residents of Canada (TSRC) 2006 ; International Travel Survey (ITS) 2002-2006,

North American Tourism Dollars (2006)Michigan and New York represent the largest U.S. markets for Ontario, while Quebec and Western Canada (B.C., Alberta and Saskatchewan) represent the largest domestic markets.In terms of total visitor expenditures, Michigan, New York State and Quebec are comparable. The long-term decline of same day visitor traffic from the U.S. will continue to present a challenge for Ontario

2006 Visitor Expenditures (in millions)

35

North American Opportunity MarketsNorth America - Important Core Markets:

The U.S. market currently offers Ontario a much more attractive opportunity than individual overseas markets. The U.S. market is eight times larger than the overseas market in terms of visitors and U.S. overnight visitors spend more per person per night, in Ontario than do overnight overseas market visitors. Tier One markets will continue to be key. Within Tier One, there are several markets that carry particular weight: Eastern Michigan (including Detroit), Northern Ohio and Western New York are each home to more than 100,000 non-visitors who are open to the idea of travelling to Ontario if the right opportunity were to be presented to them. More importantly, there is strong support for Ontario among the 4.7M visitors from these states who might be encouraged to make a return visit.

North America - Potential Markets:

Tier Three markets hold considerable potential. The top two, in terms of numbers of potential visitors are New York City and Illinois (largely Chicago), each with more than 500,000 residents who are non-visitors to Ontario but who are quite open to choosing it for a future trip.Southeastern Pennsylvania (principally Philadelphia), New Jersey and Washington D.C. also hold considerable promise and should be included in future planning as budgets allow:

Southeastern Pennsylvania has 324,000 who are open to visiting Ontario (with 204,000 residing in Philadelphia).New Jersey has 457,000 who are open to visiting Ontario.Washington D.C. has 289,000 who are open to visiting Ontario.

36

North American Opportunity Markets

North America - Potential Markets:

Tier Four also holds some potential for Ontario but is less attractive than Tier Three (and not simply due to greater distance). While there are large numbers of people open to visiting Ontario living in the states of: California, Texas, Florida, Arizona, Georgia and North Carolina, these potential visitors are geographically scattered and therefore difficult to reach cost-effectively with sufficient weight and frequency to be persuasive. For example, while Texas has 614,000 potential visitors to Ontario, they are scattered across a large state, which poses a significant challenge with respect to marketing. In contrast, a Tier Three city such as Washington D.C. has 289,000 potential visitors within one MSA, which lends itself to more focused communication efforts (i.e., messaging and media).Tier Two markets hold some potential but are clearly less attractive than those in Tier One and Tier Three since Tier Two essentially represents more distant areas within the Border States with generally lower population concentrations. The Tier Two market potential is largely spread over Western Michigan, Central & Western Ohio and Eastern New York State. Efforts to target Tier One are also likely to have a positive impact on some of the Tier Two markets through advertising spillover.

Canada

Within Canada, the West and Quebec hold the largest untapped pools of potential visitors to Ontario (997,000 and 554,000, respectively). Quebec’s proximity presents Ontario with a relatively greater opportunity to attract potential visitors from this province than from among the more distant pools of potential visitors scattered throughout the three most western provinces.

37

Overseas Opportunity Markets

38

Ontario’s Best Prospect Markets: Overseas

Overseas

Somewhat lower priority than China; Launch marketing efforts as budgets allow, focusing on key urban markets. Place emphasis on the unique combination of urban life, natural experiences history and education that Ontario offers within Canada.

Mexico4.

RecommendationMarket

Monitor economic conditions and tourism statistics to see whether it may be worthwhile to launch marketing efforts.

Brazil6.

Launch marketing efforts as budgets allow, focusing on key urbanmarkets, including the Punjab. Place emphasis on differentiating, unique, status-worthy experiences that will fuel conversation ‘back home’.

India 5.

Increase marketing efforts in major urban centresChina3.

Maintain a presence in these core marketsGermany, France, Japan2.

Boost efforts to attract more U.K. residents (while the U.K. is a traditional market, it contains undeveloped potential which may require less effort to capture than new, emerging markets). There are significant opportunities among emerging overseas outbound travellersin the younger age cohorts.

U.K.1.

39

$24$48$66$69$92$104$113$116$151$154

$250$530

$612$739Michigan

NY State

UK Japan China

Germany Mexico France

India Brazil

South KoreaAustralia

NetherlandsSpain

Source: Statistics Canada ITS, 2002- 2006

Overseas Opportunity MarketsTo help set the overseas markets into context, U.S. visitors provide an extremely important revenue stream. Visitors from Michigan and New York State spend more in Ontario annually than do overseas visitors from the top six countries combined.The U.K. and to a lesser extent Japan are currently the two most attractive overseas sources of tourism spending in Ontario.

2006 Visitor Expenditures (in millions)

40

Overseas Opportunity MarketsThe Overseas Market:

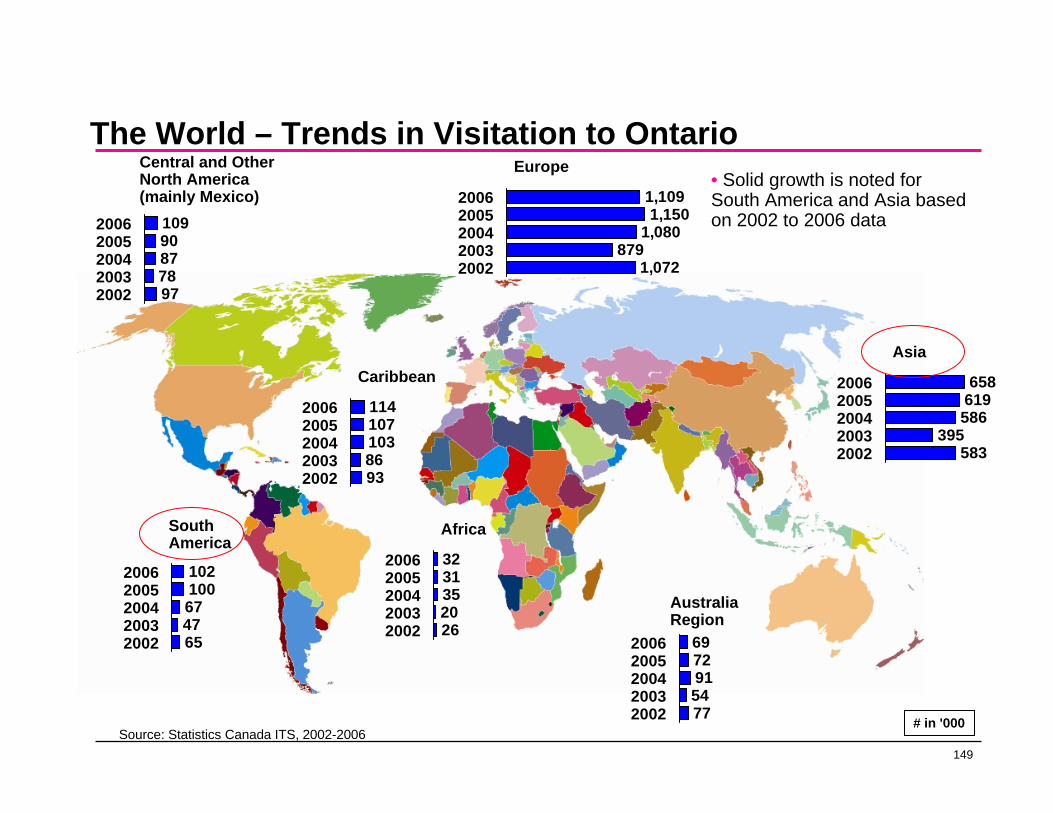

Regionally, Europe is by far the largest overseas market for Ontario generating 1.1M visitors in 2006. In distant second position, the region of Asia supplied 658,000 visitors to Ontario during the same year.In terms of growth, while the European outbound market has been expanding considerably in recent years, visits to Canada and to Ontario have not been growing. Asia and the much smaller region of South America however, are exhibiting steady growth in Ontario visitation.Despite this, at current growth rates, Asia will not overtake Europe in terms of numbers of visitors to Ontario for at least 10 years.Nevertheless, Asian expenditures in Canada and Ontario are strong and growing. In particular, spending by Chinese visitors to Ontario is expected to overtake that of Japanese visitors in the next couple of years. Similarly, spending by Indian visitors to Ontario is expected to overtake that of French visitors in the next few years.All of this implies that it is important for Ontario (via Canada) to maintain a strong presence in its traditional overseas markets over the next few years, but to also begin implementation of strategies to develop a presence and tap into the potential of newly emerging markets. This is a transitional phase that is likely to play itself out over a long period of time. It should be noted as well, that there is no intended implication here to abandon the traditional source markets long-term. It is anticipated that they will continue have a prominent place as drivers of external tourism volumes. However, they will ultimately become part of a larger and more diverse global mix of source markets.

41

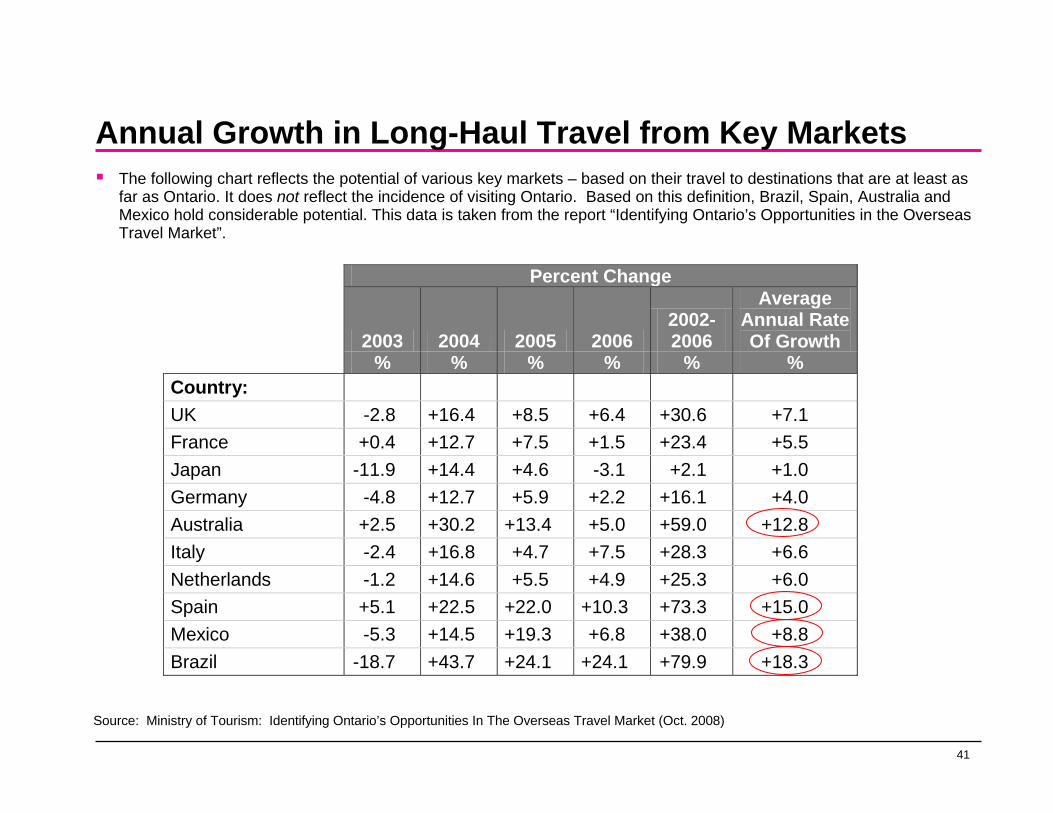

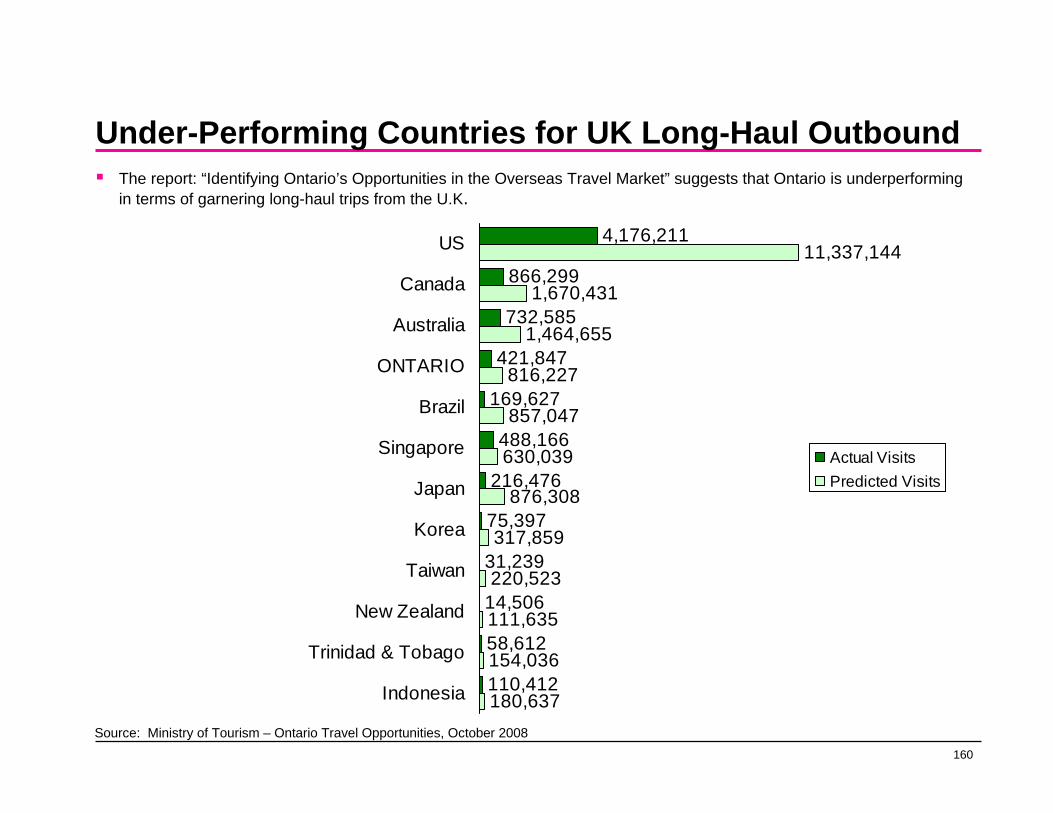

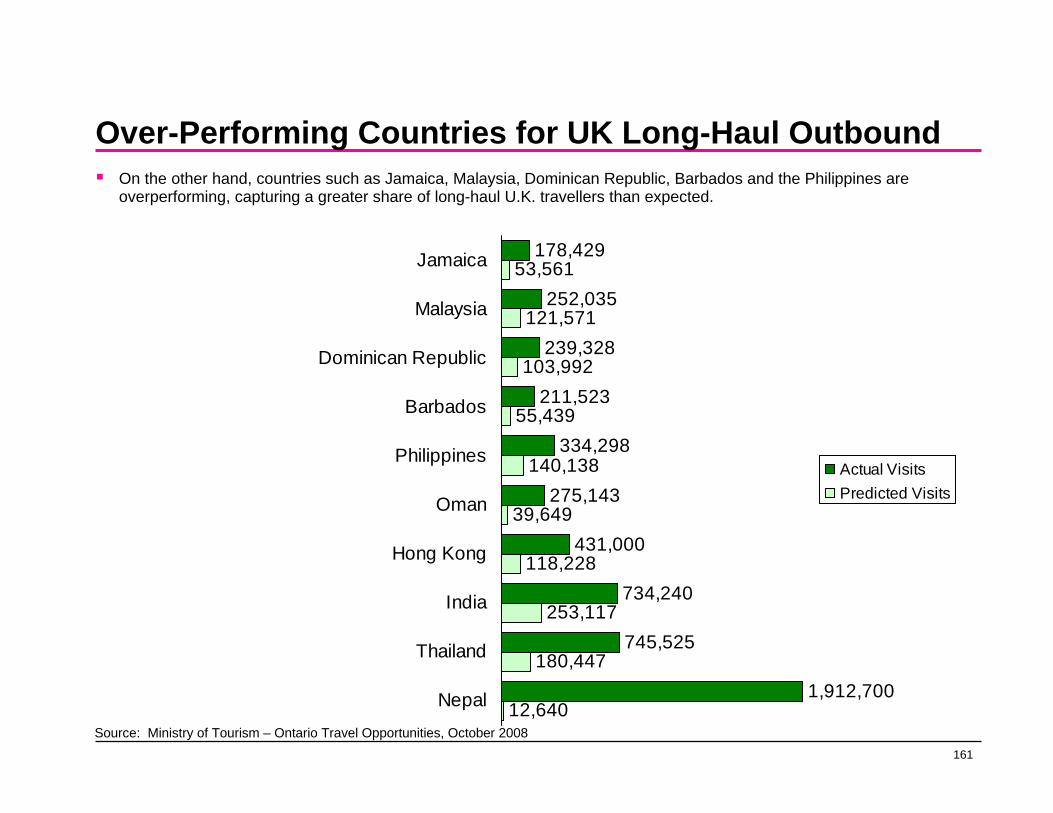

Annual Growth in Long-Haul Travel from Key MarketsThe following chart reflects the potential of various key markets – based on their travel to destinations that are at least as far as Ontario. It does not reflect the incidence of visiting Ontario. Based on this definition, Brazil, Spain, Australia and Mexico hold considerable potential. This data is taken from the report “Identifying Ontario’s Opportunities in the Overseas Travel Market”.

Percent Change

2003 2004 2005 2006 2002-2006

Average Annual Rate Of Growth

% % % % % % Country: UK -2.8 +16.4 +8.5 +6.4 +30.6 +7.1 France +0.4 +12.7 +7.5 +1.5 +23.4 +5.5 Japan -11.9 +14.4 +4.6 -3.1 +2.1 +1.0 Germany -4.8 +12.7 +5.9 +2.2 +16.1 +4.0 Australia +2.5 +30.2 +13.4 +5.0 +59.0 +12.8 Italy -2.4 +16.8 +4.7 +7.5 +28.3 +6.6 Netherlands -1.2 +14.6 +5.5 +4.9 +25.3 +6.0 Spain +5.1 +22.5 +22.0 +10.3 +73.3 +15.0 Mexico -5.3 +14.5 +19.3 +6.8 +38.0 +8.8 Brazil -18.7 +43.7 +24.1 +24.1 +79.9 +18.3

Source: Ministry of Tourism: Identifying Ontario’s Opportunities In The Overseas Travel Market (Oct. 2008)

42

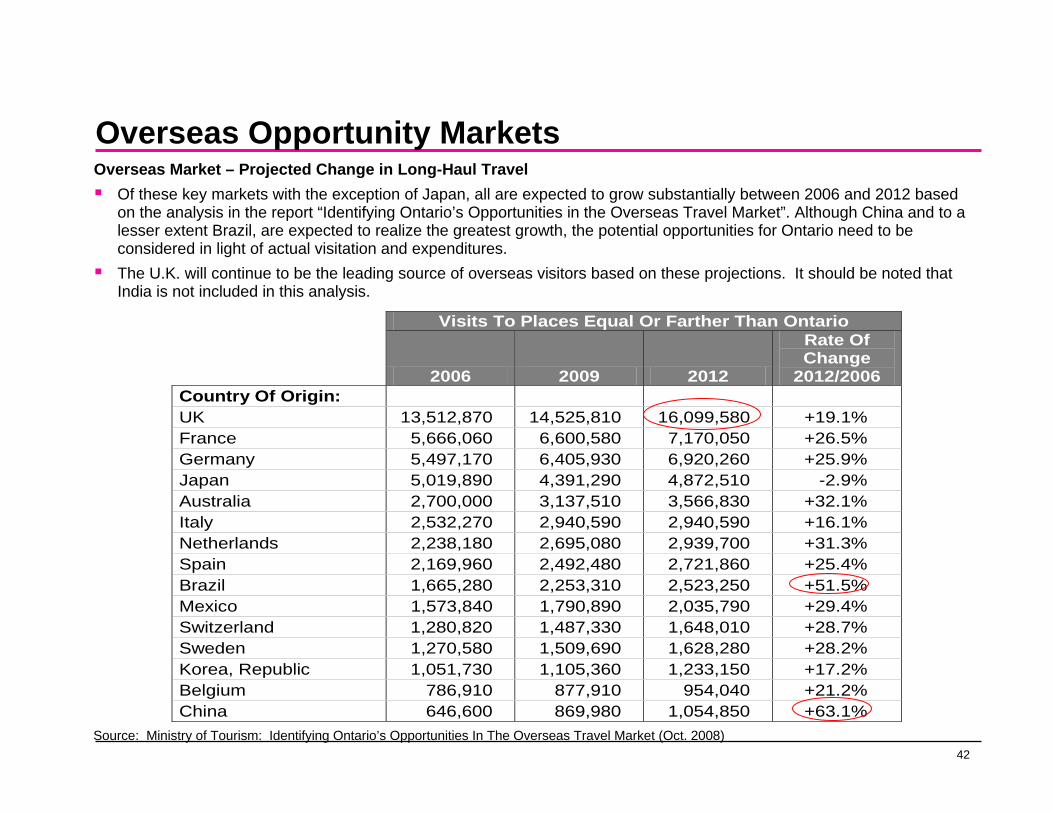

Overseas Opportunity MarketsOverseas Market – Projected Change in Long-Haul Travel

Of these key markets with the exception of Japan, all are expected to grow substantially between 2006 and 2012 based on the analysis in the report “Identifying Ontario’s Opportunities in the Overseas Travel Market”. Although China and to a lesser extent Brazil, are expected to realize the greatest growth, the potential opportunities for Ontario need to be considered in light of actual visitation and expenditures. The U.K. will continue to be the leading source of overseas visitors based on these projections. It should be noted that India is not included in this analysis.

Visits To Places Equal Or Farther Than Ontario

2006 2009 2012

Rate Of Change

2012/2006 Country Of Origin: UK 13,512,870 14,525,810 16,099,580 +19.1% France 5,666,060 6,600,580 7,170,050 +26.5% Germany 5,497,170 6,405,930 6,920,260 +25.9% Japan 5,019,890 4,391,290 4,872,510 -2.9% Australia 2,700,000 3,137,510 3,566,830 +32.1% Italy 2,532,270 2,940,590 2,940,590 +16.1% Netherlands 2,238,180 2,695,080 2,939,700 +31.3% Spain 2,169,960 2,492,480 2,721,860 +25.4% Brazil 1,665,280 2,253,310 2,523,250 +51.5% Mexico 1,573,840 1,790,890 2,035,790 +29.4% Switzerland 1,280,820 1,487,330 1,648,010 +28.7% Sweden 1,270,580 1,509,690 1,628,280 +28.2% Korea, Republic 1,051,730 1,105,360 1,233,150 +17.2% Belgium 786,910 877,910 954,040 +21.2% China 646,600 869,980 1,054,850 +63.1% Source: Ministry of Tourism: Identifying Ontario’s Opportunities In The Overseas Travel Market (Oct. 2008)

43

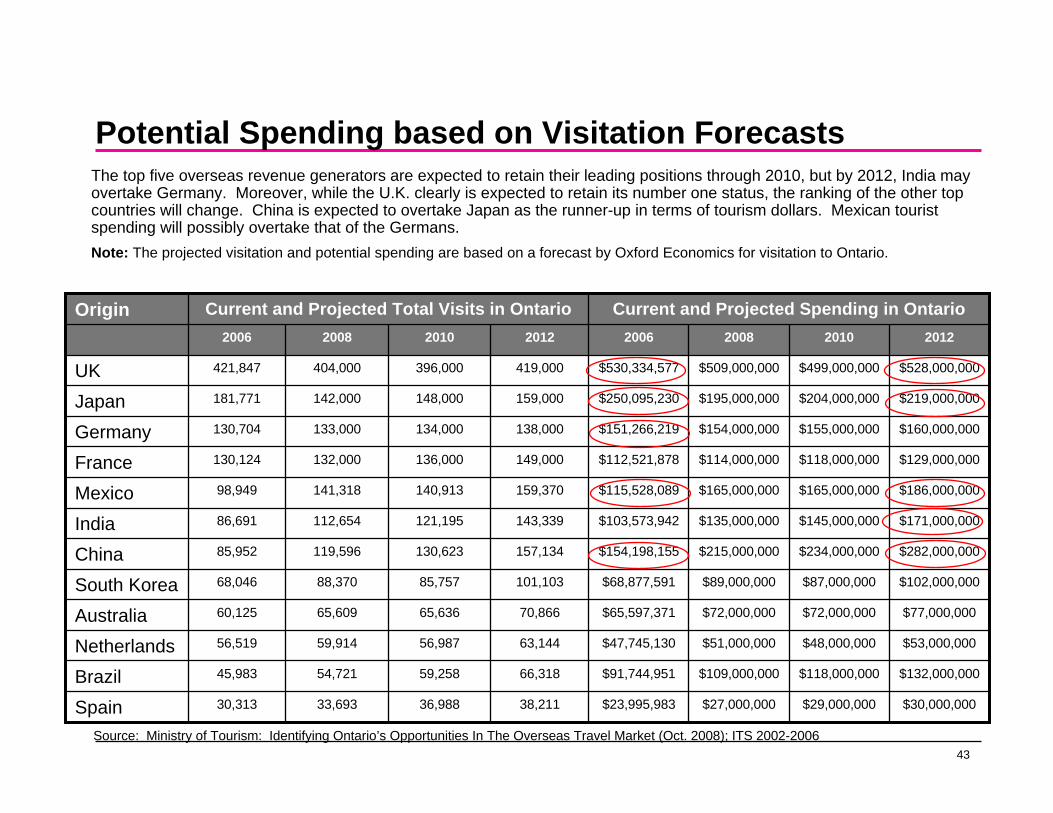

Potential Spending based on Visitation Forecasts

20122010200820062012201020082006

$30,000,000$29,000,000$27,000,000$23,995,98338,211 36,988 33,693 30,313 Spain

$132,000,000$118,000,000$109,000,000$91,744,95166,318 59,258 54,721 45,983 Brazil

$53,000,000$48,000,000$51,000,000$47,745,13063,144 56,987 59,914 56,519Netherlands

$77,000,000$72,000,000$72,000,000$65,597,37170,866 65,636 65,609 60,125 Australia

$102,000,000$87,000,000$89,000,000$68,877,591101,103 85,757 88,370 68,046 South Korea

$282,000,000$234,000,000$215,000,000$154,198,155157,134 130,623 119,596 85,952 China

$171,000,000$145,000,000$135,000,000$103,573,942143,339 121,195 112,654 86,691 India

$186,000,000$165,000,000$165,000,000$115,528,089159,370 140,913 141,318 98,949 Mexico

$129,000,000$118,000,000$114,000,000$112,521,878149,000136,000132,000130,124 France

$160,000,000$155,000,000$154,000,000$151,266,219138,000134,000133,000130,704 Germany

$219,000,000$204,000,000$195,000,000$250,095,230159,000148,000142,000181,771 Japan

$528,000,000$499,000,000$509,000,000$530,334,577419,000396,000404,000421,847 UK

Current and Projected Spending in OntarioCurrent and Projected Total Visits in OntarioOrigin

Source: Ministry of Tourism: Identifying Ontario’s Opportunities In The Overseas Travel Market (Oct. 2008); ITS 2002-2006

The top five overseas revenue generators are expected to retain their leading positions through 2010, but by 2012, India may overtake Germany. Moreover, while the U.K. clearly is expected to retain its number one status, the ranking of the other top countries will change. China is expected to overtake Japan as the runner-up in terms of tourism dollars. Mexican tourist spending will possibly overtake that of the Germans.Note: The projected visitation and potential spending are based on a forecast by Oxford Economics for visitation to Ontario.

44

Domestic Markets

45

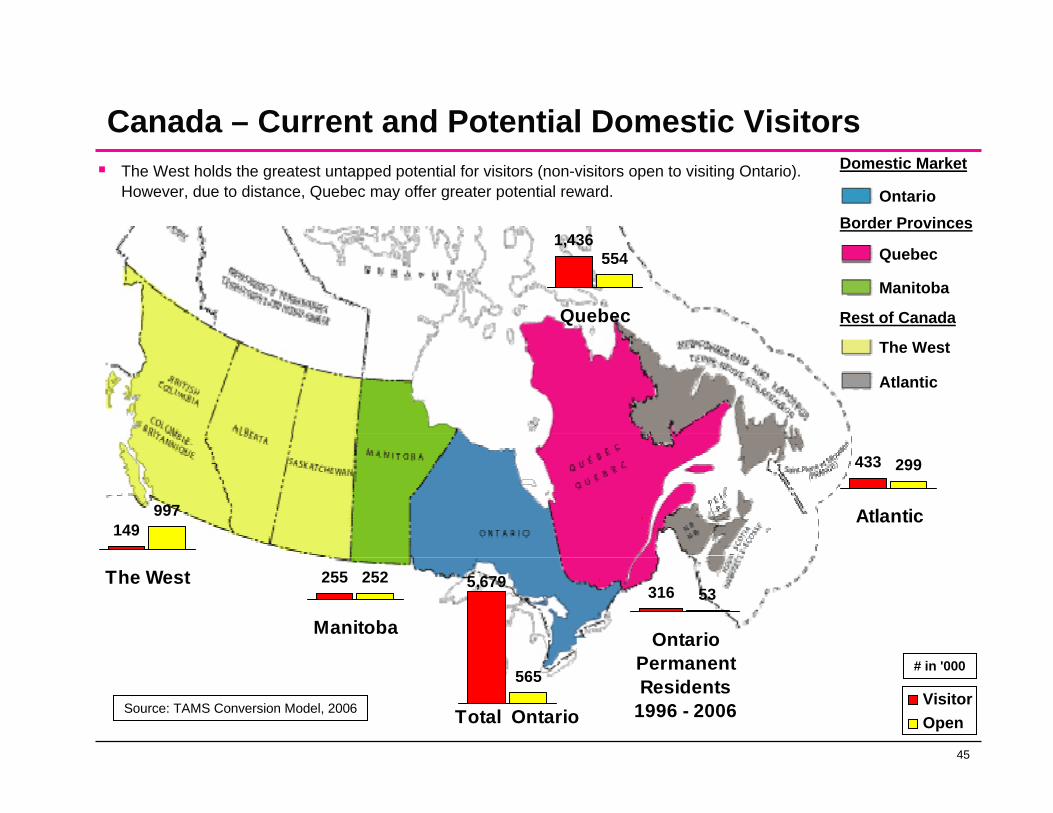

Canada – Current and Potential Domestic VisitorsDomestic Market

Border Provinces

Manitoba

The West

Atlantic

Ontario

Quebec

Rest of Canada

VisitorOpen

# in '000

433 299

Atlantic

1,436554

Quebec

316 53

OntarioPermanentResidents

1996 - 2006

5,679

565

Total Ontario

255 252

Manitoba

149997

The West

Source: TAMS Conversion Model, 2006

The West holds the greatest untapped potential for visitors (non-visitors open to visiting Ontario). However, due to distance, Quebec may offer greater potential reward.

46

Quebec Market

47

Quebec Summary

The Quebec market represents the largest source of Canadian visitors from outside Ontario. Overnight visitors constitute the majority of visitors from Quebec.However, these visitors are disproportionately Anglophone and visiting friends and relatives.Quebec also holds untapped potential, with roughly 0.5M non-visitors open to the idea of visiting Ontario under the right conditions.Quebecers who express any interest in visiting Ontario, express a wide range of interests which fit well with the existing tourism offering. In particular they mention that they would like to visit small towns and villages, parks, hiking trails, natural landmarks, family attractions and to stay at a B&B or country inn. Winery tours and theme parks are also high on the list of intended activities.Interest in Ontario is centered around the cities of Ottawa, Toronto and Kingston, but also extends to include southern Ontario. Northern Ontario is particularly appealing to those from the nearby Outaouais/Abitibi region.To make inroads into Quebec, Ontario needs to reach out to Francophone travellers as well as Anglophones. This requires French advertising that is sensitive to Quebec cultural nuances and does not appear to compromise. Travel information also needs to be provided in French. French signage will also create positive touch-points. The key to advertising and communications is to address the lack of familiarity with Ontario and perceptions of Ontarians as being unfriendly/unwelcoming people. There is also a need to focus on what is distinctive relative to Quebec itself. This is a challenge given similarities in geography, environment (the outdoors) and the strength of Montreal and other centres in Quebec as focal points for culture and entertainment.Strategies need to be developed to make Francophones feel welcome in Ontario. Having staff who can reach out to Francophones in their own language could be leveraged to make French Quebecers feel comfortable in Ontario.

48

Quebec Summary

Interest in Ontario is fairly broad-based, and includes those of average means. Value is an important criterion in trip selection.Mature Families, Mature Singles and Couples and Seniors are the best prospects.Given its population, the Greater Montreal area is a good target.However, all regions along the Quebec/Ontario border offer good prospects, particularly if an effort is made to attract Quebecers to specific local events and attractions in close proximity to their point of origin.Similarly, give some emphasis to Ontario destinations and product in close proximity to the Quebec border in order accentuate the ease and convenience of choosing Ontario.Profile Ontario’s small towns and villages, parks, hiking trails, natural landmarks, beaches, family attractions, B & Bs, country inns, winery tours and theme parks.Don’t compete directly with Quebec’s iconic attractions. Place more emphasis on differentiating Ontario from Quebec (e.g., different cultural experience, different landscape and history). Perceived familiarity with Ontario and assumed similarity to Quebec (particularly in terms of landscape and history) represent impediments to stimulating interest.Leverage cultural/language differences (“it’s like visiting a foreign country without the hassles”).Mass media have a role to play. In particular, television is hugely popular in Quebec.Destination websites and brochures are popular among Francophones and provide good means of delivering secondary support to broadcast and print.Other means of targeting Francophones include non-destination websites and government tourism offices.In addition to mass media and brochures, Anglophones can also be targeted via non-destination websites and travel magazines.

49

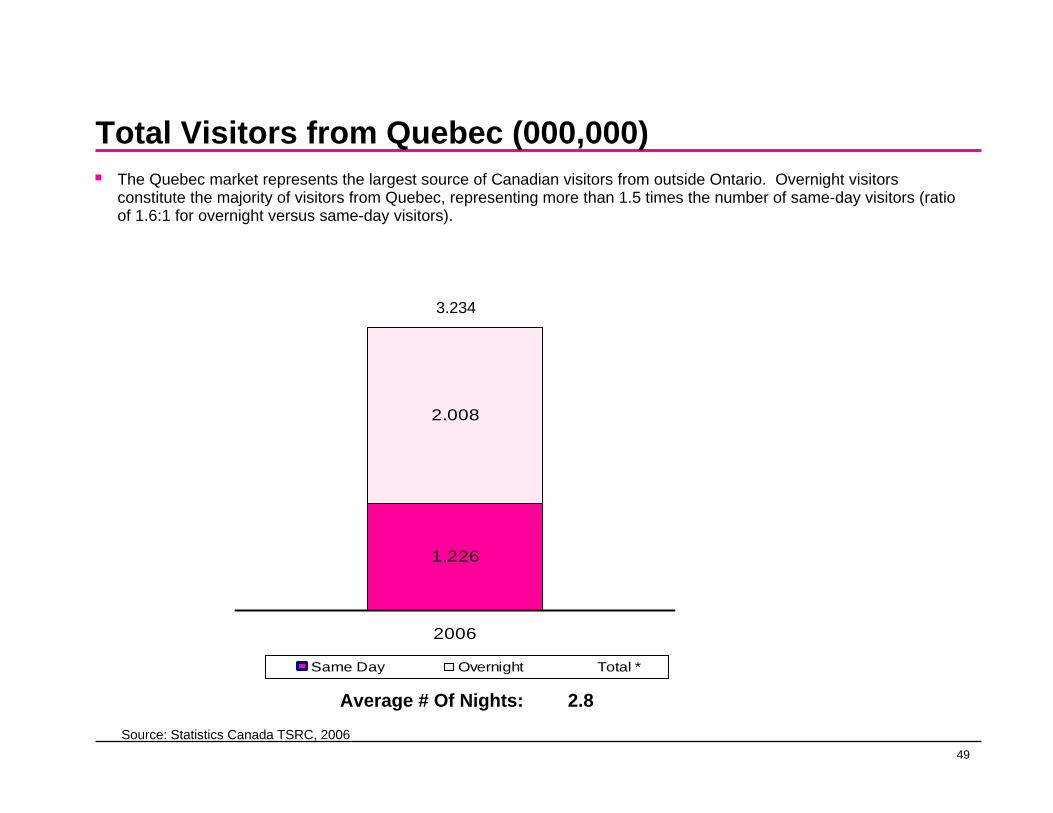

Total Visitors from Quebec (000,000)

1.226

2.008

2006

Same Day Overnight Total *

Average # Of Nights: 2.8

Source: Statistics Canada TSRC, 2006

3.234

The Quebec market represents the largest source of Canadian visitors from outside Ontario. Overnight visitors constitute the majority of visitors from Quebec, representing more than 1.5 times the number of same-day visitors (ratio of 1.6:1 for overnight versus same-day visitors).

50

Main Purpose of TripVisiting friends and relatives is the main reason for Quebecers to visit Ontario, accounting for one-half (49%) of all trips to Ontario.

5%

11%

35%

49% VFR

Pleasure

Other

Busi-ness

Sources Statistics Canada TSRC 2006 Base: All visitors from Quebec 3,234,000

51

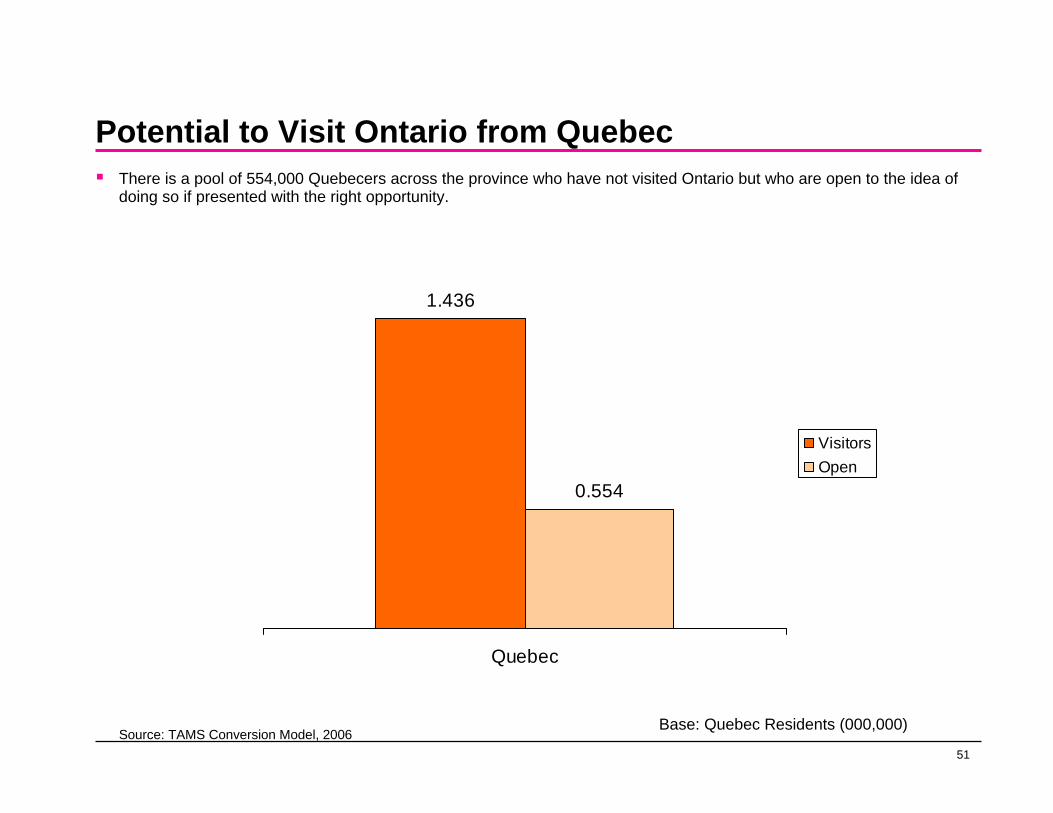

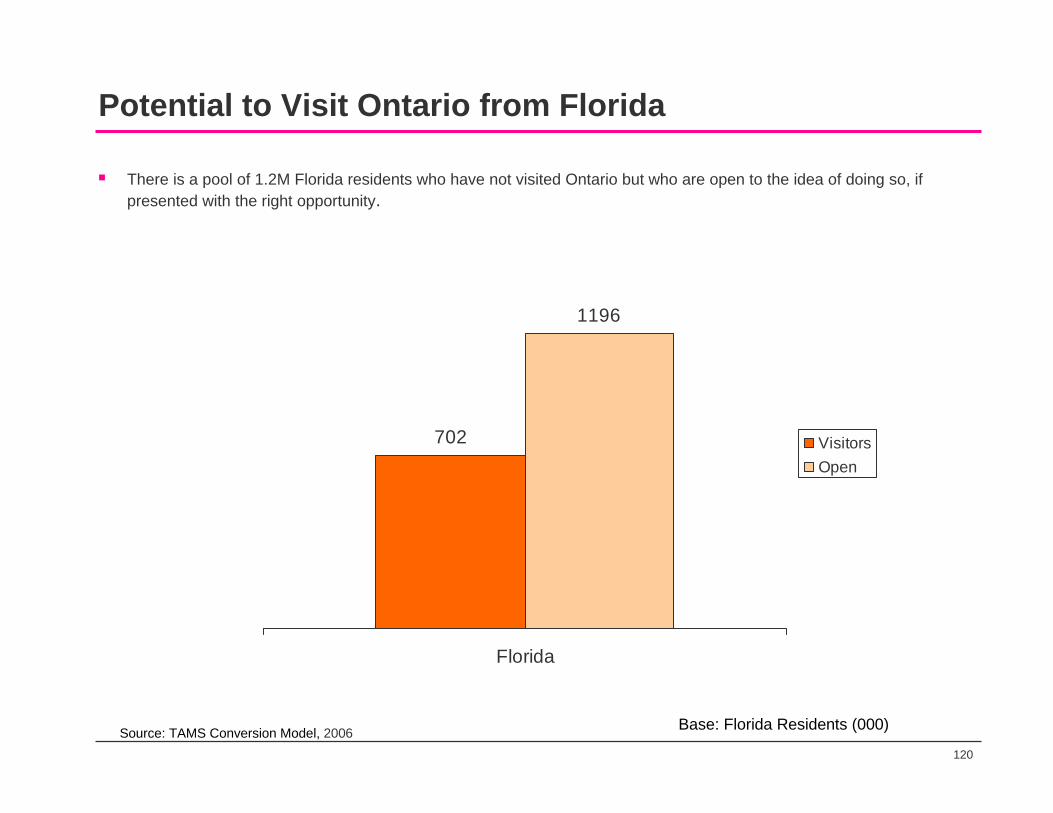

Potential to Visit Ontario from QuebecThere is a pool of 554,000 Quebecers across the province who have not visited Ontario but who are open to the idea of doing so if presented with the right opportunity.

1.436

0.554

Quebec

VisitorsOpen

Source: TAMS Conversion Model, 2006Base: Quebec Residents (000,000)

52

Travel Motivators

51%

56%

43%

31%

30%

17%

17%

13%

37%

31%

39%

36%

35%

26%

26%

25%

88%

87%

82%

67%

65%

43%

43%

38%

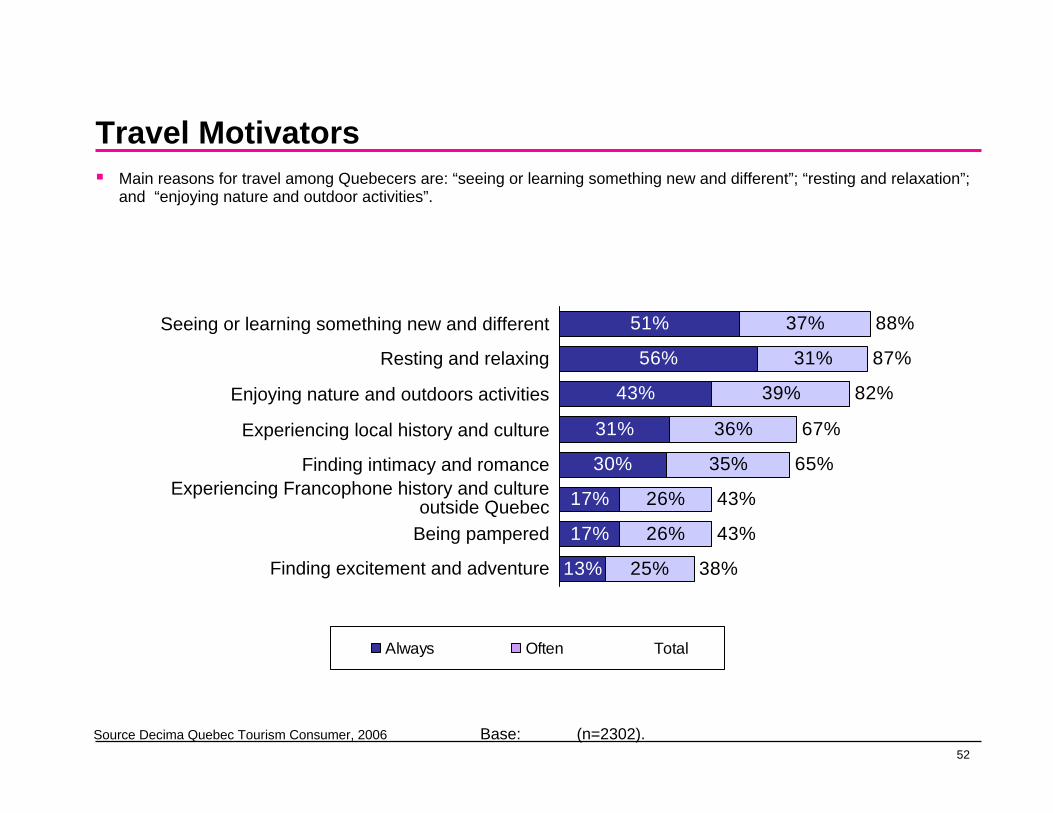

Main reasons for travel among Quebecers are: “seeing or learning something new and different”; “resting and relaxation”; and “enjoying nature and outdoor activities”.

Seeing or learning something new and different

Resting and relaxing

Enjoying nature and outdoors activities

Experiencing local history and culture

Finding intimacy and romanceExperiencing Francophone history and culture

outside QuebecBeing pampered

Finding excitement and adventure

Always Often Total

Source Decima Quebec Tourism Consumer, 2006 Base: (n=2302).

53

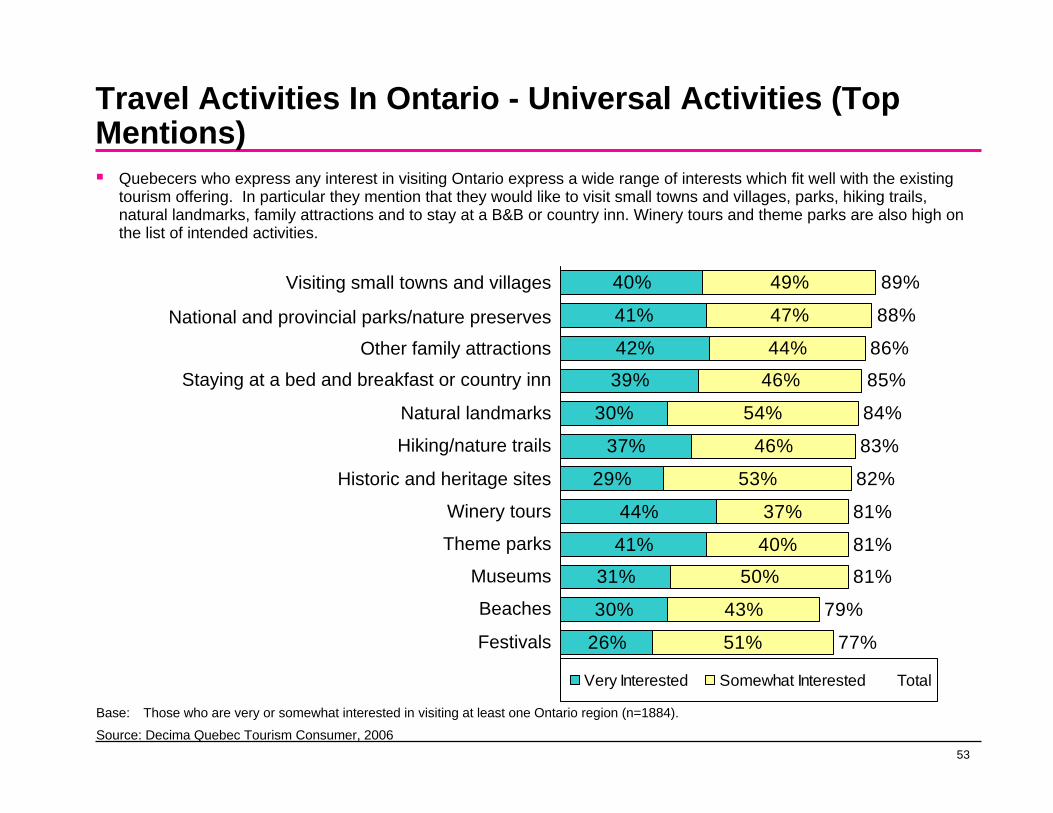

Travel Activities In Ontario - Universal Activities (Top Mentions)

Quebecers who express any interest in visiting Ontario express a wide range of interests which fit well with the existing tourism offering. In particular they mention that they would like to visit small towns and villages, parks, hiking trails, natural landmarks, family attractions and to stay at a B&B or country inn. Winery tours and theme parks are also high on the list of intended activities.

40%

41%

42%

39%

30%

37%

29%

44%

41%

31%

30%

26%

49%

47%

44%

46%

54%

46%

53%

37%

40%

50%

43%

51%

89%

88%

86%

85%

84%

83%

82%

81%

81%

81%

79%

77%

Visiting small towns and villages

National and provincial parks/nature preserves

Other family attractions

Staying at a bed and breakfast or country inn

Natural landmarks

Hiking/nature trails

Historic and heritage sites

Winery tours

Theme parks

Museums

Beaches

Festivals

Very Interested Somewhat Interested Total

Base: Those who are very or somewhat interested in visiting at least one Ontario region (n=1884).

Source: Decima Quebec Tourism Consumer, 2006

54

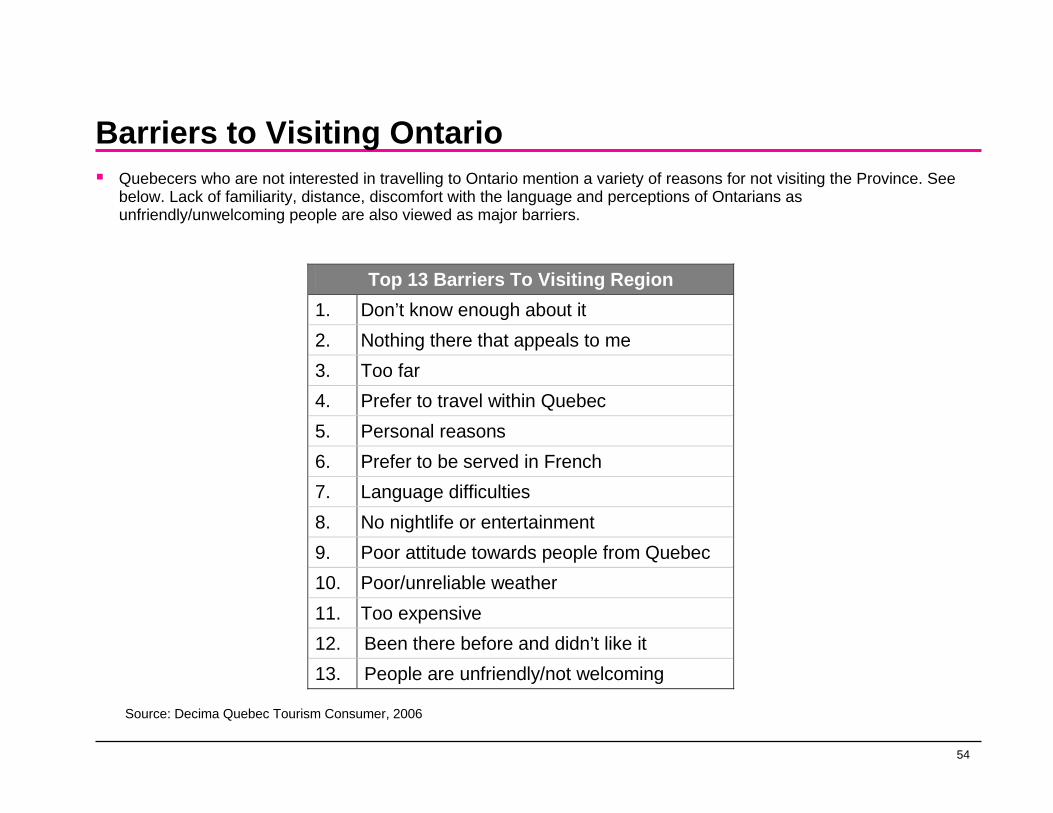

Barriers to Visiting OntarioQuebecers who are not interested in travelling to Ontario mention a variety of reasons for not visiting the Province. See below. Lack of familiarity, distance, discomfort with the language and perceptions of Ontarians as unfriendly/unwelcoming people are also viewed as major barriers.

Top 13 Barriers To Visiting Region 1. Don’t know enough about it 2. Nothing there that appeals to me 3. Too far 4. Prefer to travel within Quebec 5. Personal reasons 6. Prefer to be served in French 7. Language difficulties 8. No nightlife or entertainment 9. Poor attitude towards people from Quebec 10. Poor/unreliable weather 11. Too expensive 12. Been there before and didn’t like it 13. People are unfriendly/not welcoming

Source: Decima Quebec Tourism Consumer, 2006

55

Destinations Visited in the Last Year

70%

25%

10%

8%

24%

10%

8%

7%

Quebec

Ontario

Atlantic Canada

Other Canada

United States

Caribbean

Europe

Other International

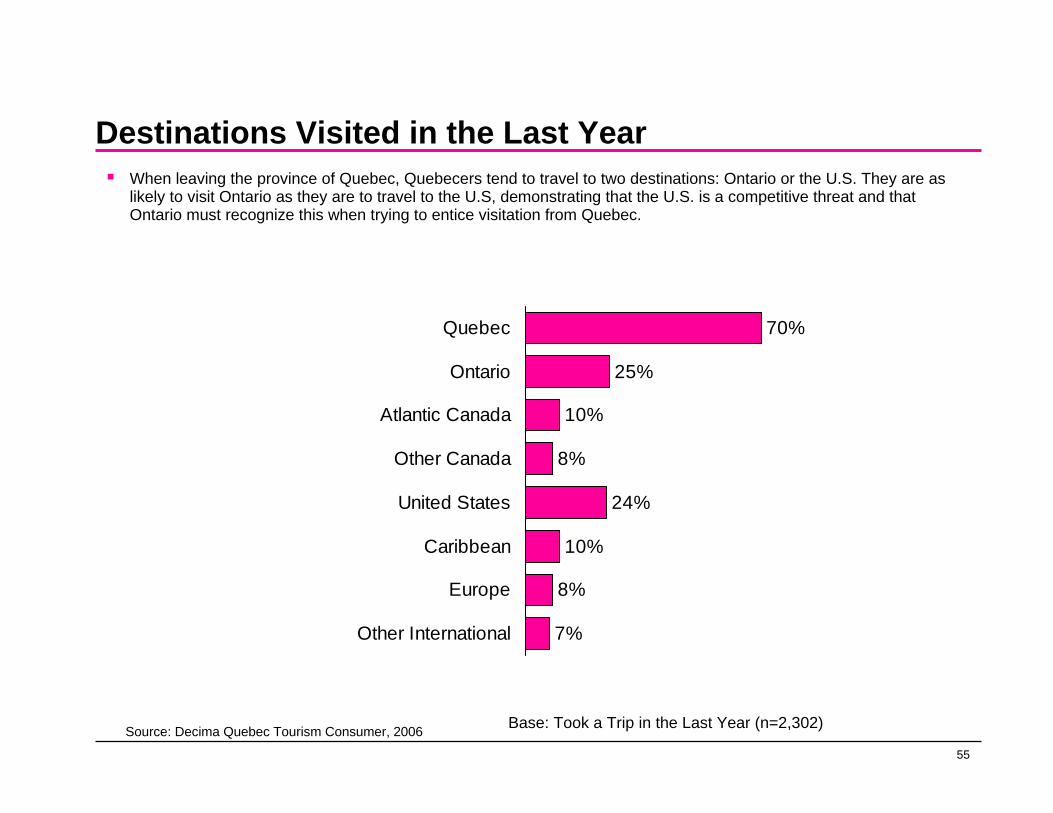

When leaving the province of Quebec, Quebecers tend to travel to two destinations: Ontario or the U.S. They are as likely to visit Ontario as they are to travel to the U.S, demonstrating that the U.S. is a competitive threat and that Ontario must recognize this when trying to entice visitation from Quebec.

Source: Decima Quebec Tourism Consumer, 2006 Base: Took a Trip in the Last Year (n=2,302)

56

70%

72%

79%

40%

43%

27%

83%

72%

English Montreal81%

70%

59%

57%

46%

34%

74%

71%

79%

66%

58%

64%

61%

46%

79%

69%

84%

67%

53%

65%

45%

71%

64%

86%

66%

51%

50%

Total Montreal

na

na

na

na

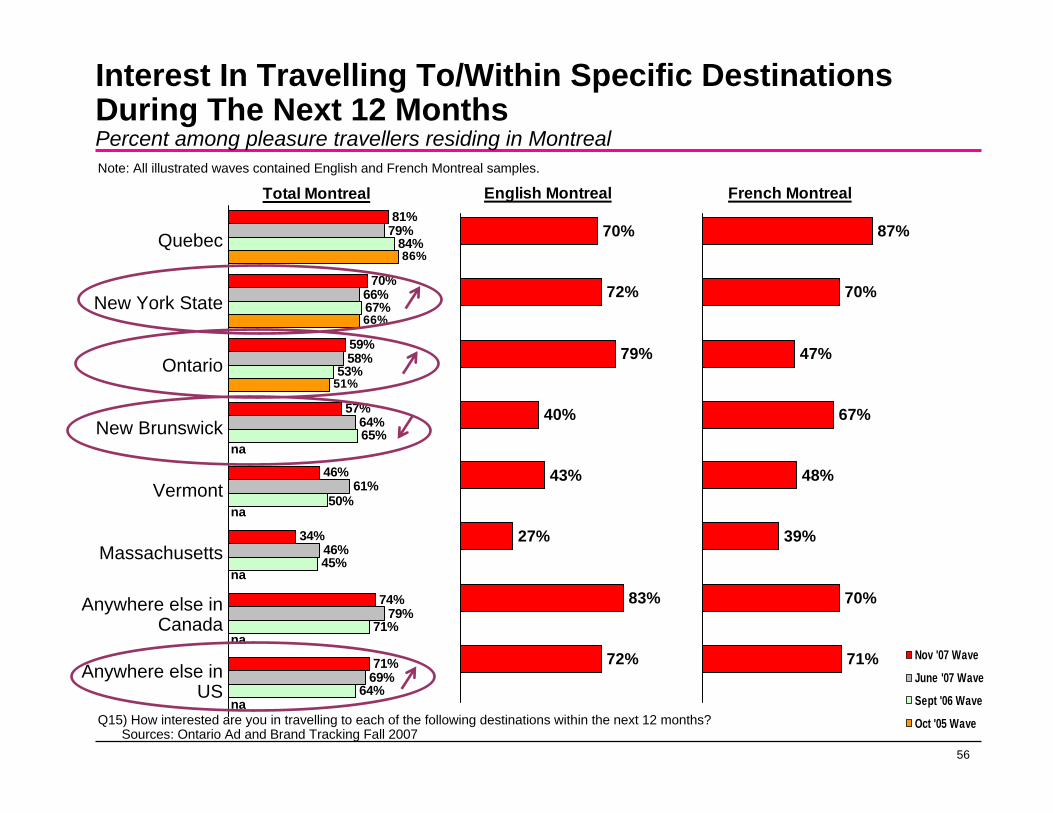

naQ15) How interested are you in travelling to each of the following destinations within the next 12 months?

Sources: Ontario Ad and Brand Tracking Fall 2007

Interest In Travelling To/Within Specific Destinations During The Next 12 MonthsPercent among pleasure travellers residing in Montreal

87%

70%

47%

67%

48%

39%

70%

71%

French MontrealNote: All illustrated waves contained English and French Montreal samples.

Quebec

New York State

Ontario

New Brunswick

Vermont

Massachusetts

Anywhere else in Canada

Anywhere else in US

Nov '07 Wave

June '07 Wave

Sept '06 Wave

Oct '05 Wave

57

United States

58

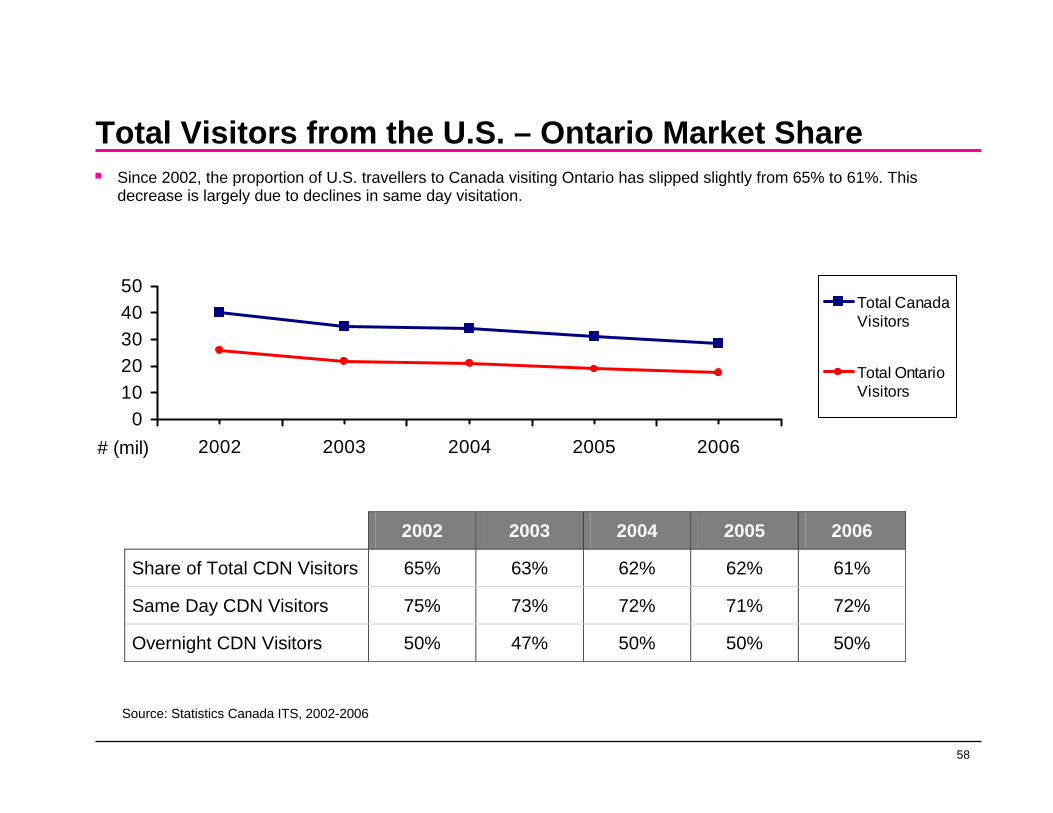

Total Visitors from the U.S. – Ontario Market Share

01020304050

2002 2003 2004 2005 2006# (mil)

Total Canada Visitors

Total OntarioVisitors

2002 2003 2004 2005 2006

Share of Total CDN Visitors 65% 63% 62% 62% 61%

Same Day CDN Visitors 75% 73% 72% 71% 72%

Overnight CDN Visitors 50% 47% 50% 50% 50%

Source: Statistics Canada ITS, 2002-2006

Since 2002, the proportion of U.S. travellers to Canada visiting Ontario has slipped slightly from 65% to 61%. This decrease is largely due to declines in same day visitation.

59

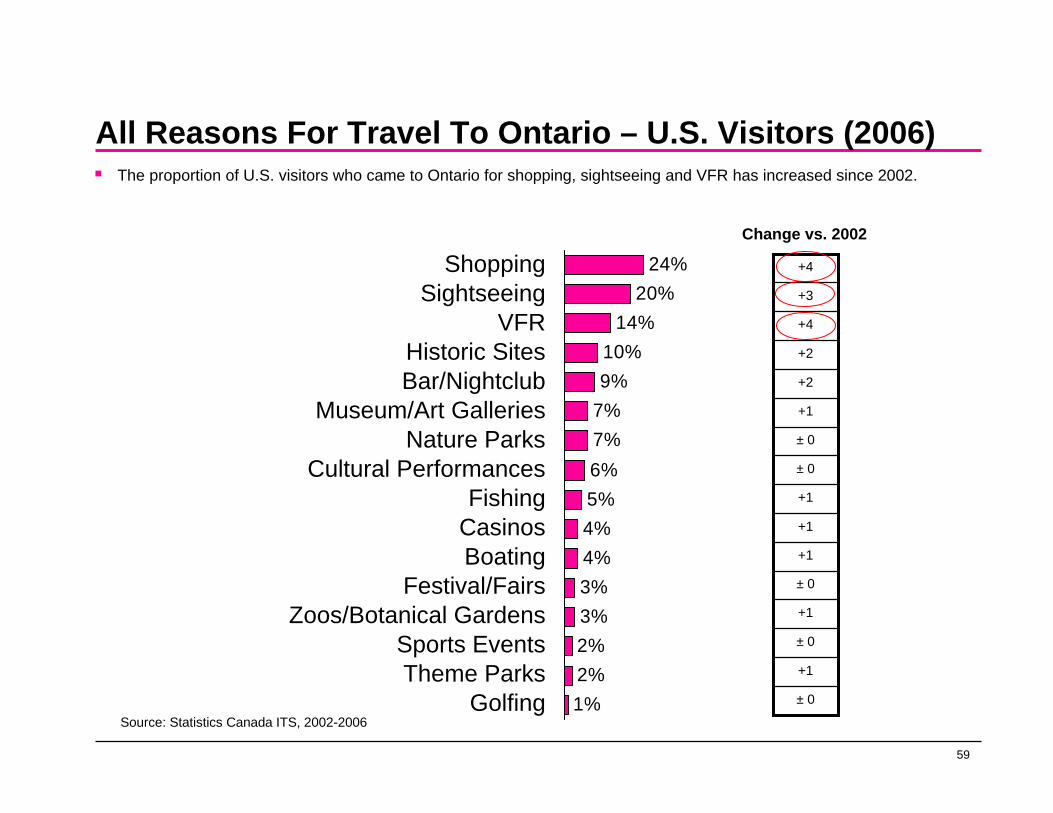

All Reasons For Travel To Ontario – U.S. Visitors (2006)

24%20%

14%10%9%

7%7%6%5%4%4%3%3%2%2%1%

ShoppingSightseeing

VFRHistoric SitesBar/Nightclub

Museum/Art GalleriesNature Parks

Cultural PerformancesFishing

CasinosBoating

Festival/FairsZoos/Botanical Gardens

Sports EventsTheme Parks

Golfing ± 0

+1

± 0

+1

± 0

+1

+1

+1

± 0

± 0

+1

+2

+2

+4

+3

+4

Change vs. 2002

Source: Statistics Canada ITS, 2002-2006

The proportion of U.S. visitors who came to Ontario for shopping, sightseeing and VFR has increased since 2002.

60

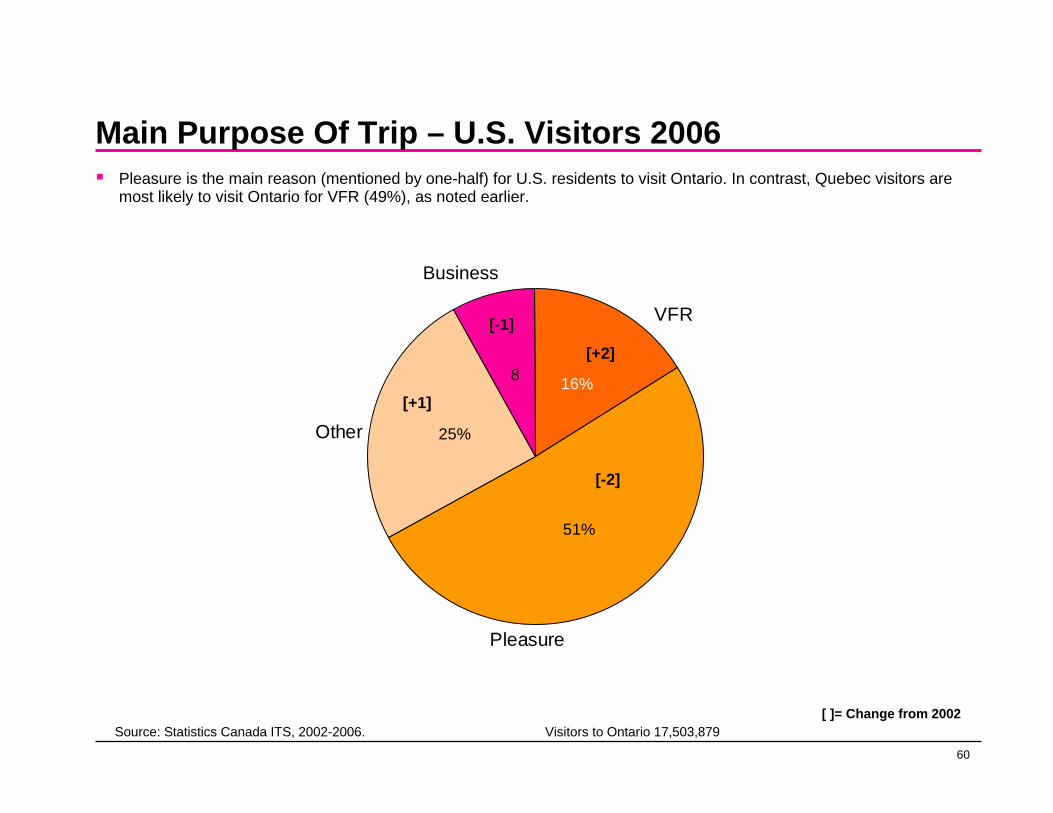

Main Purpose Of Trip – U.S. Visitors 2006Pleasure is the main reason (mentioned by one-half) for U.S. residents to visit Ontario. In contrast, Quebec visitors are most likely to visit Ontario for VFR (49%), as noted earlier.

16%

51%

25%

8

VFR

Pleasure

Other

Business

[+1]

[-2]

[-1]

[+2]

Source: Statistics Canada ITS, 2002-2006. Visitors to Ontario 17,503,879[ ]= Change from 2002

61

Destinations Visited In Past 3 Years – TravelsAmerica

15%

14%

14%

10%

5%

3%

3%

3%

2%

2%

2%

2%

60%

Mexico

Canada

Caribbean/Bermuda

Western Europe

Ontario

Asia

Eastern Europe

Central America

South America

Pacific

Middle East/Africa

Other

NoneSource: TravelsAmerica 2008 Q1/Q2

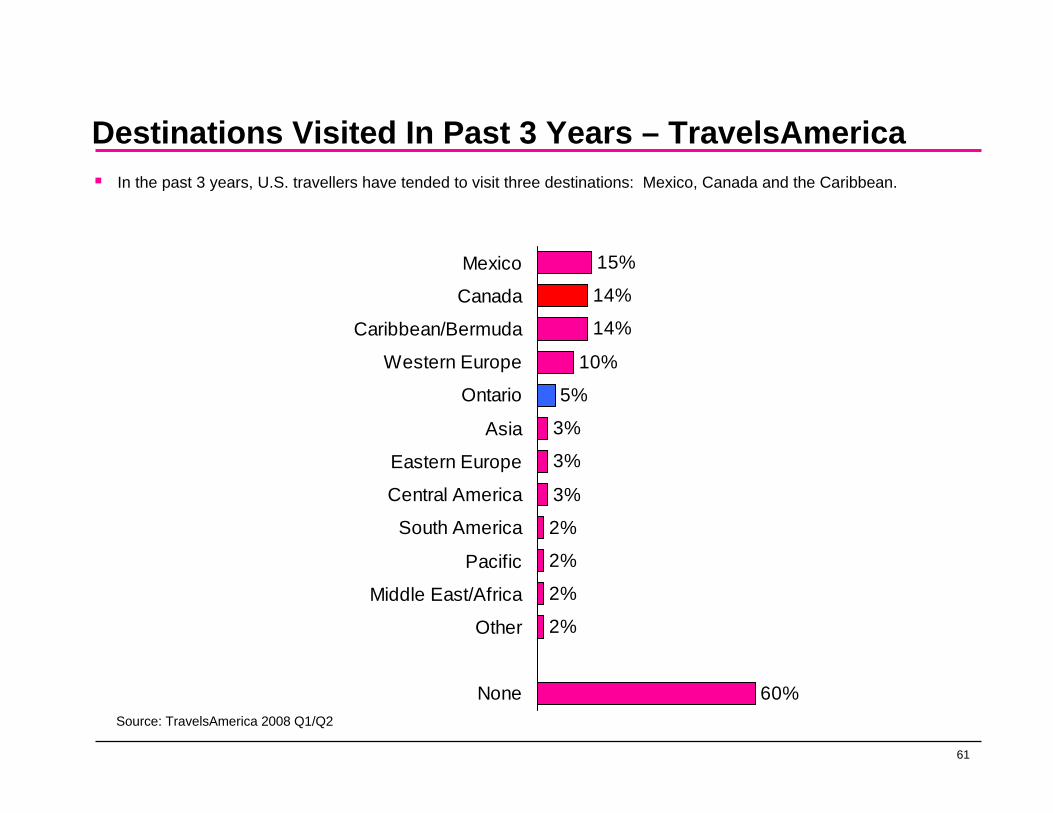

In the past 3 years, U.S. travellers have tended to visit three destinations: Mexico, Canada and the Caribbean.

62

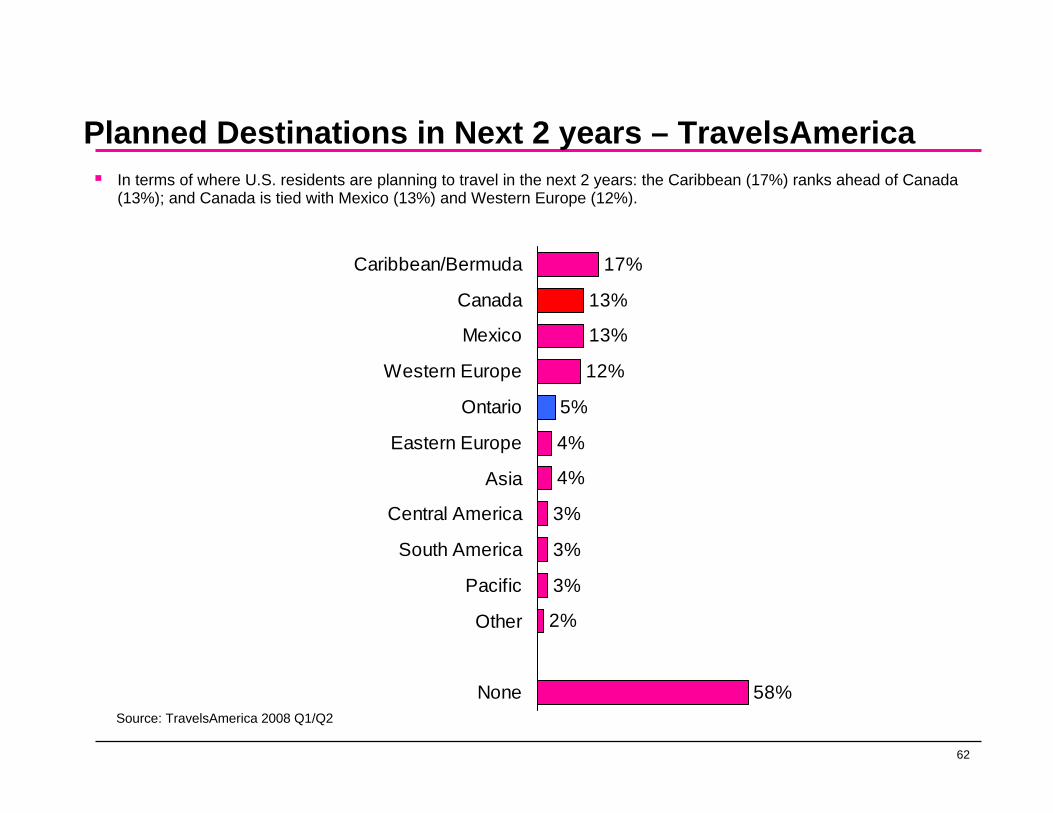

Planned Destinations in Next 2 years – TravelsAmerica

17%

13%

13%

12%

5%

4%

4%

3%

3%

3%

2%

58%

Caribbean/Bermuda

Canada

Mexico

Western Europe

Ontario

Eastern Europe

Asia

Central America

South America

Pacific

Other

NoneSource: TravelsAmerica 2008 Q1/Q2

In terms of where U.S. residents are planning to travel in the next 2 years: the Caribbean (17%) ranks ahead of Canada (13%); and Canada is tied with Mexico (13%) and Western Europe (12%).

63

U.S. – Current and Potential Visitors from the U.S.

2,306

4,041

West

VisitorOpen

5,047

2,093

Midwest

4,431

2,418

Northeast

1,016 553

NewEngland

1,9542,772

SouthAtlantic

478 506

East SouthCentral

620 945

West SouthCentral

# in '000Source: TAMS Conversion Model, 2006

64

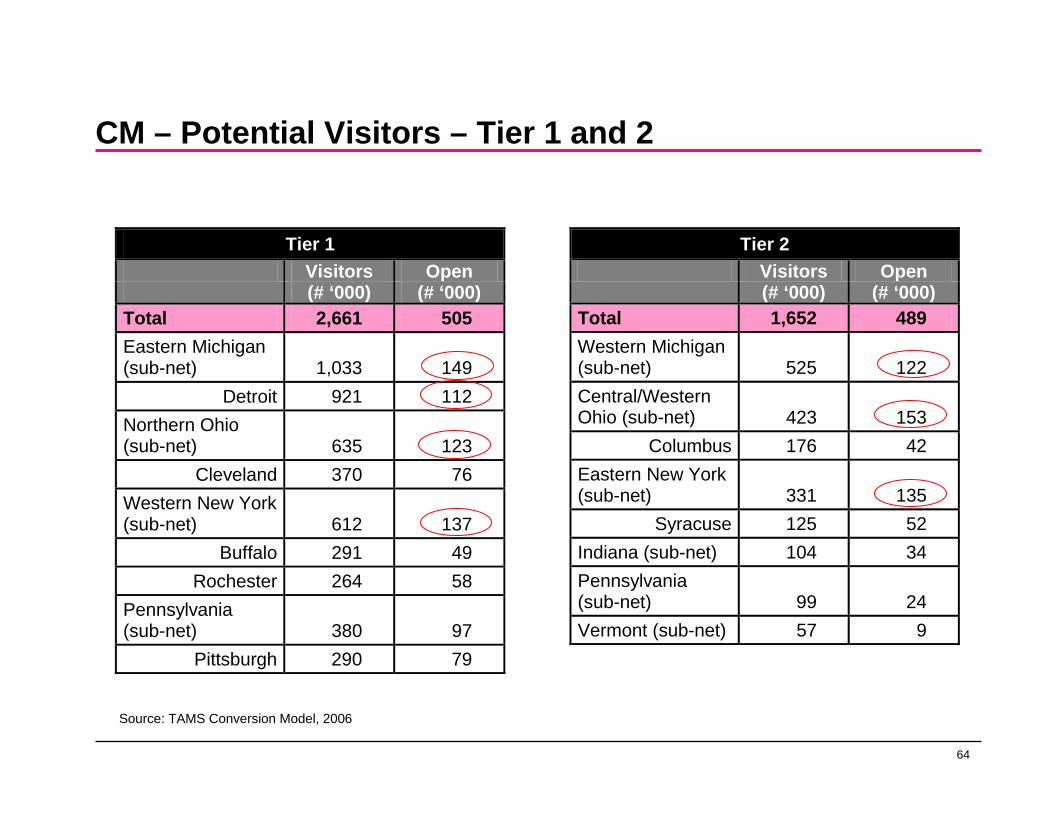

CM – Potential Visitors – Tier 1 and 2

Tier 1 Visitors Open (# ‘000) (# ‘000)

Total 2,661 505 Eastern Michigan (sub-net) 1,033 149

Detroit 921 112 Northern Ohio (sub-net) 635 123

Cleveland 370 76 Western New York (sub-net) 612 137

Buffalo 291 49 Rochester 264 58

Pennsylvania (sub-net) 380 97

Pittsburgh 290 79 11

Tier 2 Visitors Open (# ‘000) (# ‘000)

Total 1,652 489 Western Michigan (sub-net) 525 122 Central/Western Ohio (sub-net) 423 153

Columbus 176 42 Eastern New York (sub-net) 331 135

Syracuse 125 52 Indiana (sub-net) 104 34 Pennsylvania (sub-net) 99 24 Vermont (sub-net) 57 9

11

Source: TAMS Conversion Model, 2006

65

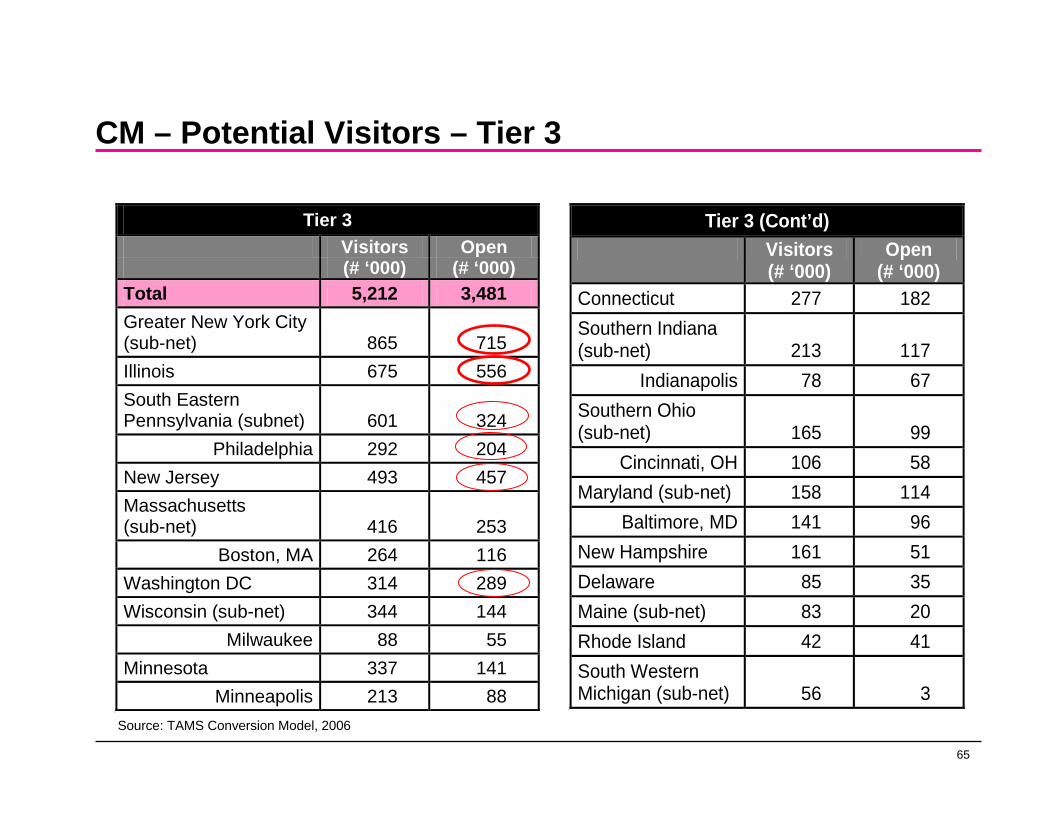

CM – Potential Visitors – Tier 3

Tier 3 Visitors Open (# ‘000) (# ‘000)

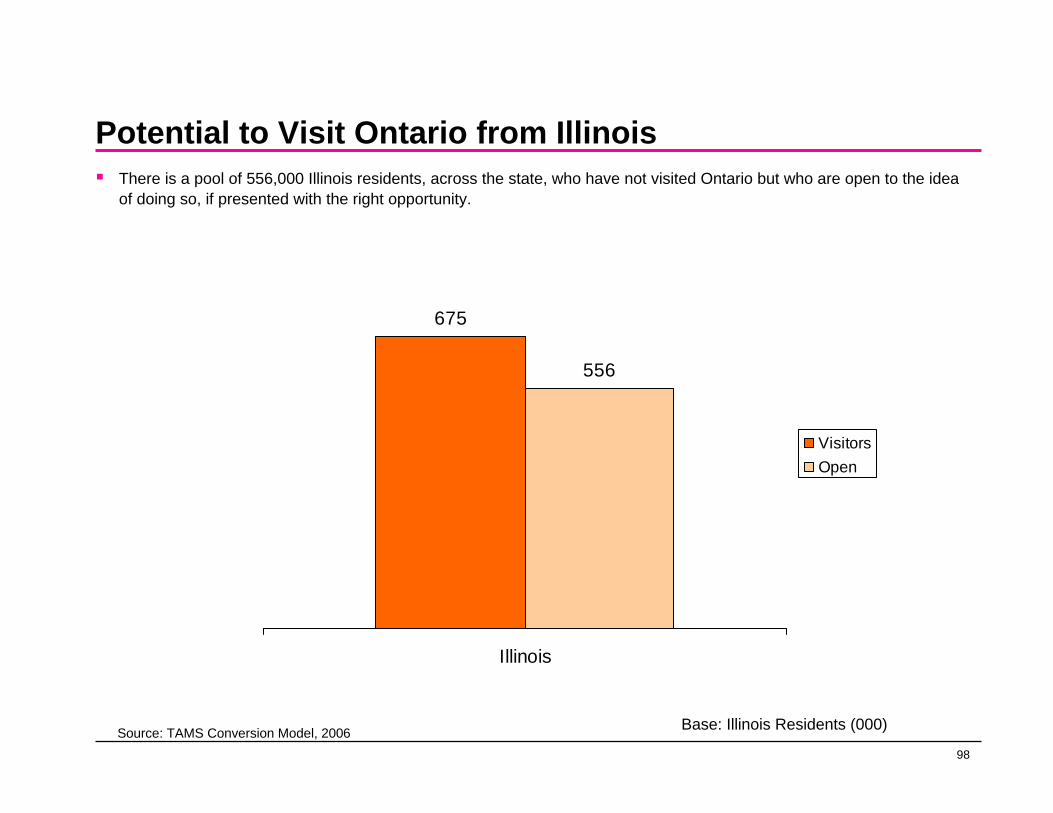

Total 5,212 3,481 Greater New York City (sub-net) 865 715 Illinois 675 556 South Eastern Pennsylvania (subnet) 601 324

Philadelphia 292 204 New Jersey 493 457 Massachusetts (sub-net) 416 253

Boston, MA 264 116 Washington DC 314 289 Wisconsin (sub-net) 344 144

Milwaukee 88 55 Minnesota 337 141

Minneapolis 213 88 11

Tier 3 (Cont’d) Visitors Open (# ‘000) (# ‘000)

Connecticut 277 182 Southern Indiana (sub-net) 213 117

Indianapolis 78 67 Southern Ohio (sub-net) 165 99

Cincinnati, OH 106 58 Maryland (sub-net) 158 114

Baltimore, MD 141 96 New Hampshire 161 51 Delaware 85 35 Maine (sub-net) 83 20 Rhode Island 42 41 South Western Michigan (sub-net) 56 3

11

Source: TAMS Conversion Model, 2006

66

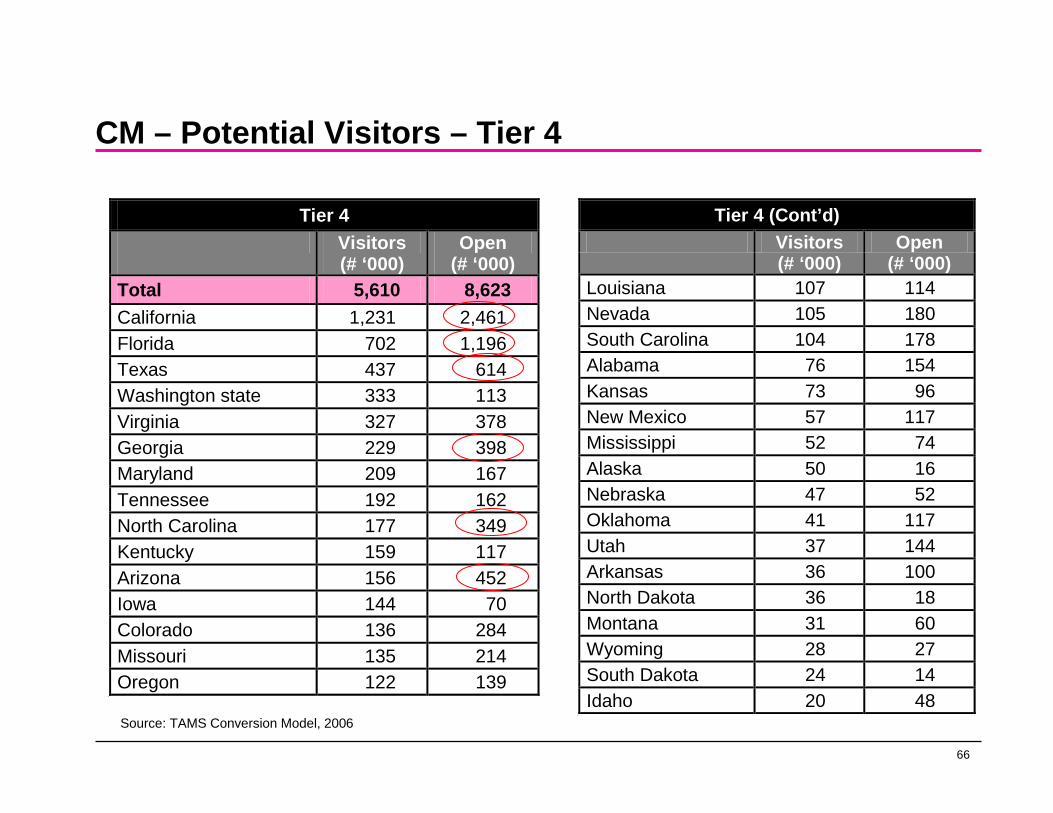

CM – Potential Visitors – Tier 4

Tier 4 Visitors Open (# ‘000) (# ‘000)

Total 5,610 8,623 California 1,231 2,461 Florida 702 1,196 Texas 437 614 Washington state 333 113 Virginia 327 378 Georgia 229 398 Maryland 209 167 Tennessee 192 162 North Carolina 177 349 Kentucky 159 117 Arizona 156 452 Iowa 144 70 Colorado 136 284 Missouri 135 214 Oregon 122 139

11

Tier 4 (Cont’d) Visitors Open (# ‘000) (# ‘000)

Louisiana 107 114 Nevada 105 180 South Carolina 104 178 Alabama 76 154 Kansas 73 96 New Mexico 57 117 Mississippi 52 74 Alaska 50 16 Nebraska 47 52 Oklahoma 41 117 Utah 37 144 Arkansas 36 100 North Dakota 36 18 Montana 31 60 Wyoming 28 27 South Dakota 24 14 Idaho 20 48

11

Source: TAMS Conversion Model, 2006

67

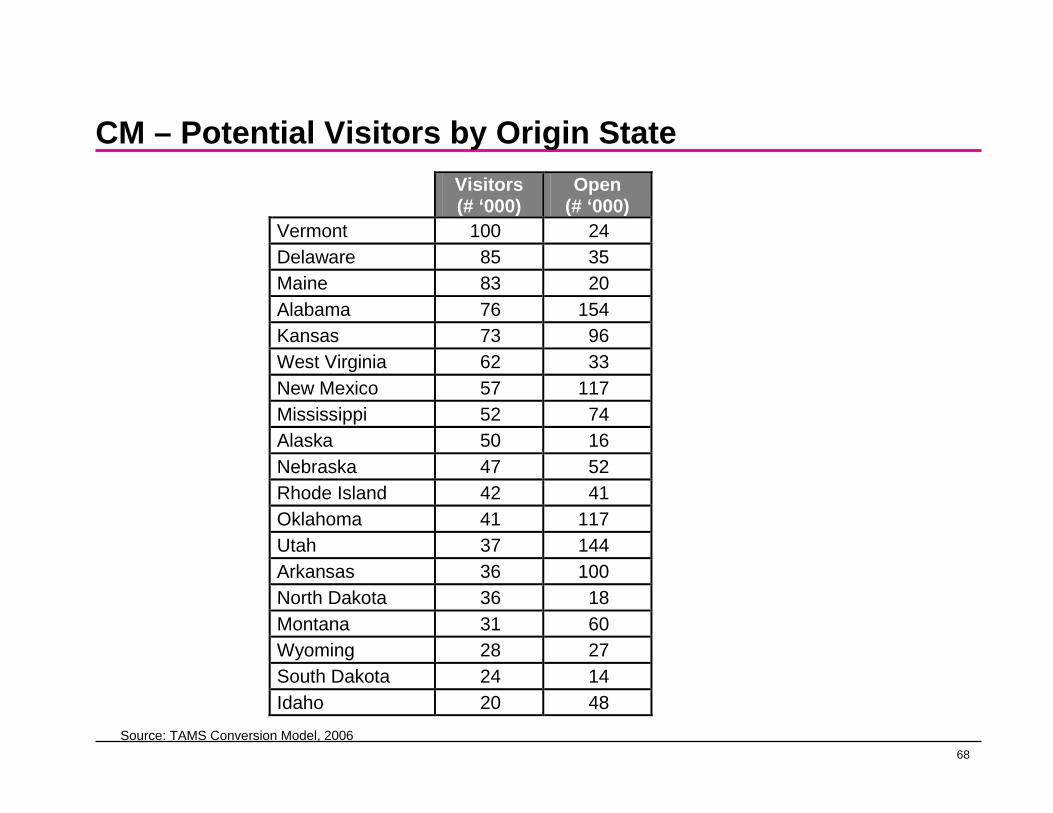

CM – Potential Visitors by Origin State Visitors Open (# ‘000) (# ‘000)

New York 1,903 1,022 New York City 597 514

Michigan 1,615 274 California 1,231 2,461 Ohio 1,187 350 Pennsylvania 1,019 386

Philadelphia 292 204Pittsburgh 290 79

Florida 702 1,196 Tampa 128 144Miami 96 203Orlando 82 117

Illinois 675 556 Chicago 487 430

New Jersey 493 457 Minnesota 444 150 Texas 437 614 Massachusetts 354 234

Boston 264 116 Wisconsin 349 146

11

Visitors Open (# ‘000) (# ‘000)

Washington 333 113 Virginia 327 378 Indiana 318 152 Washington, D.C 314 289 Connecticut 277 182 Georgia 229 398

Atlanta 148 231Maryland 209 167 Tennessee 192 162 North Carolina 177 349 New Hampshire 161 51 Kentucky 159 117 Arizona 156 452 Iowa 144 70 Colorado 136 284 Missouri 135 214 Oregon 122 139 Louisiana 107 114 Nevada 105 180 South Carolina 104 178

11

Source: TAMS Conversion Model, 2006

68

CM – Potential Visitors by Origin State Visitors Open (# ‘000) (# ‘000)

Vermont 100 24 Delaware 85 35 Maine 83 20 Alabama 76 154 Kansas 73 96 West Virginia 62 33 New Mexico 57 117 Mississippi 52 74 Alaska 50 16 Nebraska 47 52 Rhode Island 42 41 Oklahoma 41 117 Utah 37 144 Arkansas 36 100 North Dakota 36 18 Montana 31 60 Wyoming 28 27 South Dakota 24 14 Idaho 20 48

11

Source: TAMS Conversion Model, 2006

69

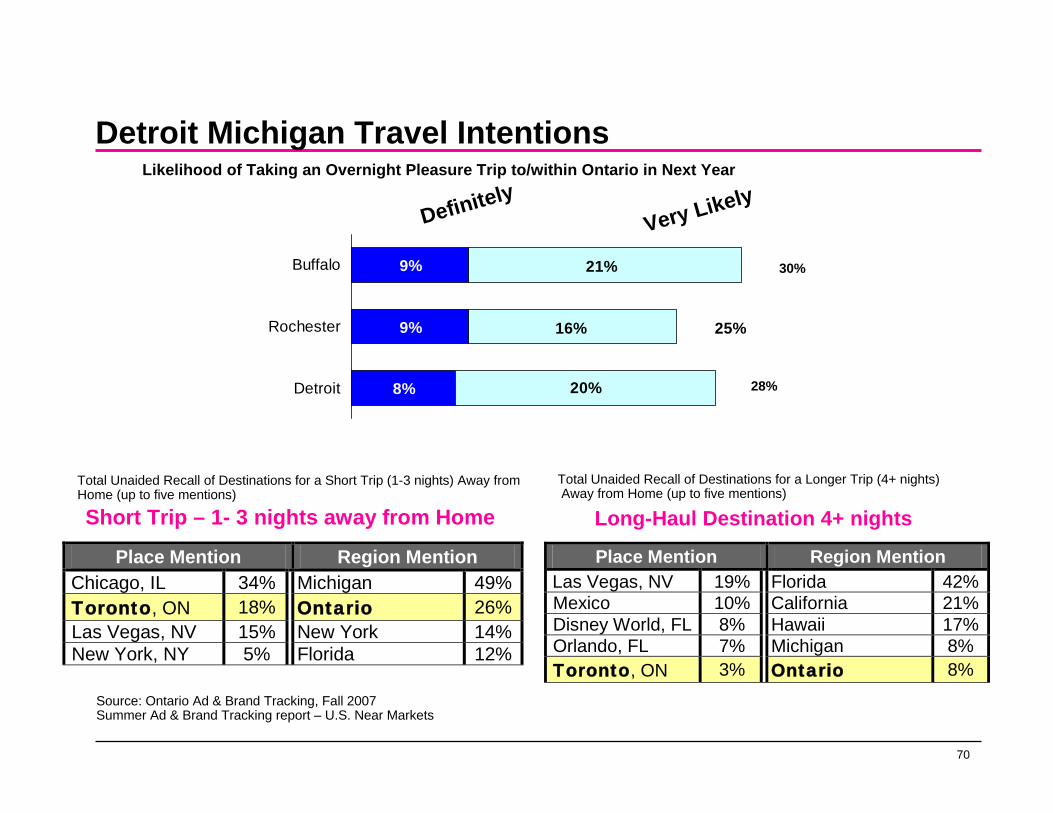

Detroit

70

Short Trip – 1- 3 nights away from Home

Place Mention Region Mention Chicago, IL 34% Michigan 49%Toronto, ON 18% Ontario 26%Las Vegas, NV 15% New York 14%New York, NY 5% Florida 12%

Long-Haul Destination 4+ nights

Place Mention Region Mention Las Vegas, NV 19% Florida 42%Mexico 10% California 21%Disney World, FL 8% Hawaii 17%Orlando, FL 7% Michigan 8% Toronto, ON 3% Ontario 8%

Very LikelyDefinitely

9%

9%

8%

21%

16%

20%

25%

Buffalo

Rochester

Detroit

Total Unaided Recall of Destinations for a Short Trip (1-3 nights) Away from Home (up to five mentions)

Likelihood of Taking an Overnight Pleasure Trip to/within Ontario in Next Year

Detroit Michigan Travel Intentions

Total Unaided Recall of Destinations for a Longer Trip (4+ nights)Away from Home (up to five mentions)

30%

28%

Source: Ontario Ad & Brand Tracking, Fall 2007Summer Ad & Brand Tracking report – U.S. Near Markets

71

New York

72

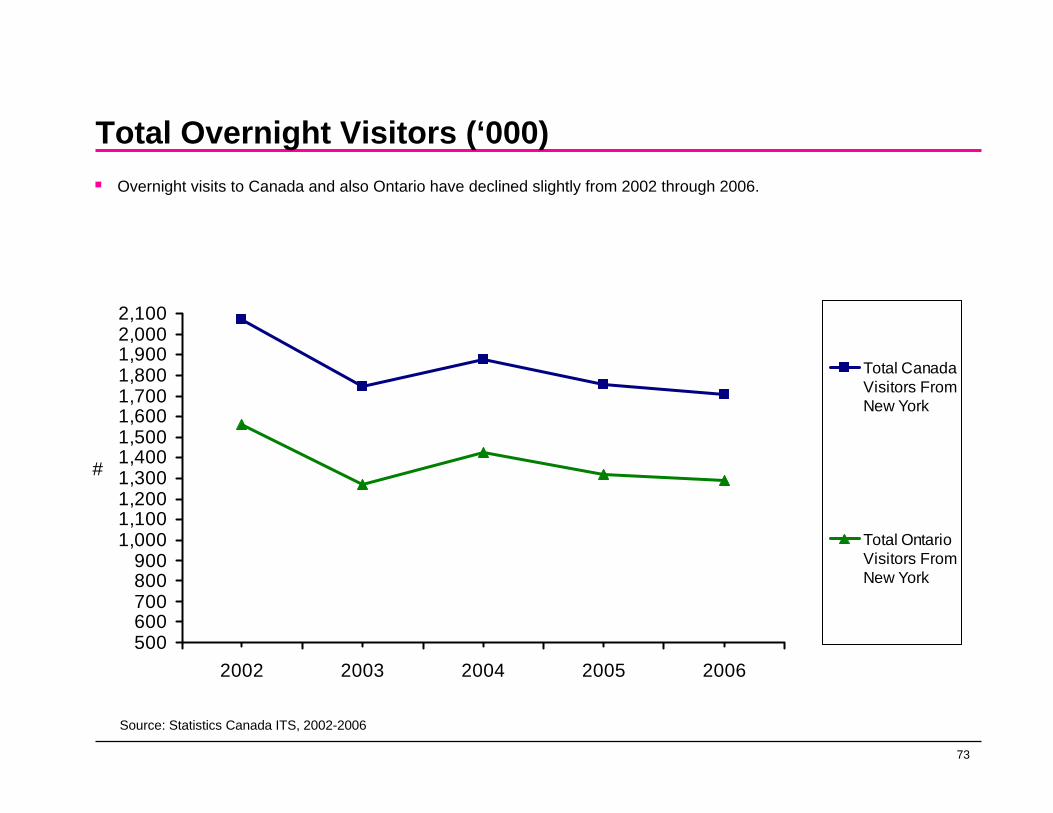

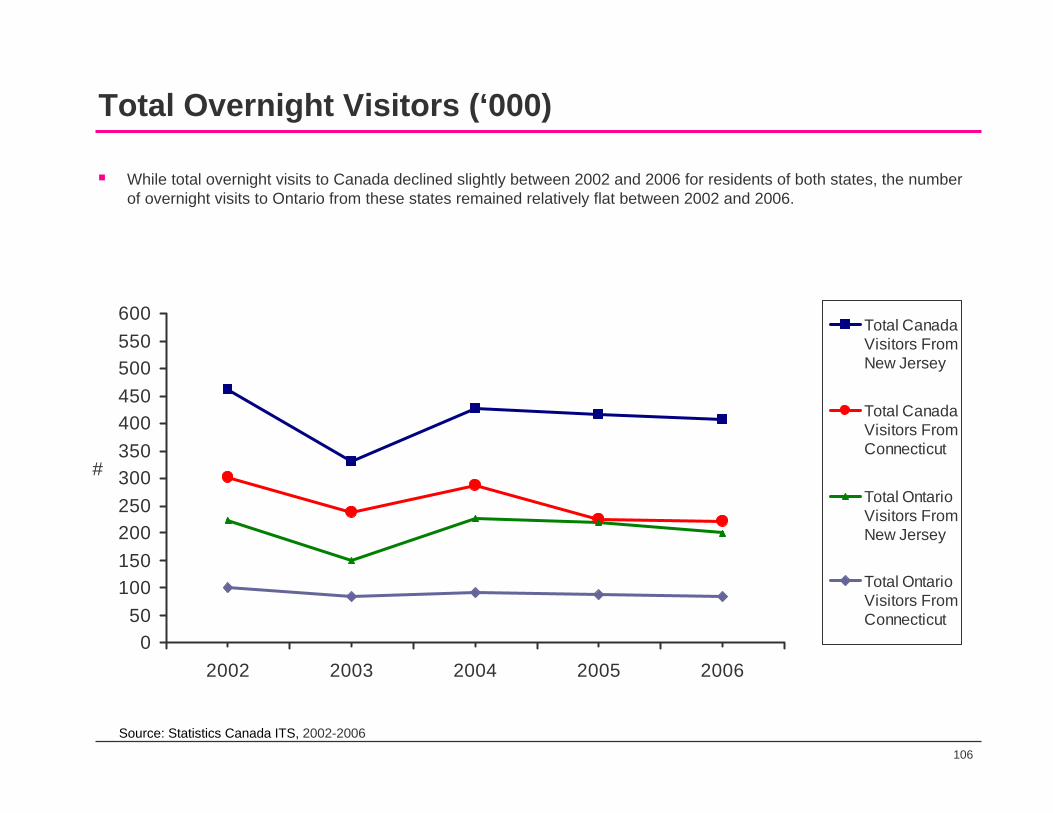

Total Visitors (‘000)

2,0002,5003,0003,5004,0004,5005,0005,5006,0006,5007,0007,5008,0008,5009,0009,500

2002 2003 2004 2005 2006

#

Total CanadaVisitors FromNew York

Total OntarioVisitors FromNew York

Source: Statistics Canada ITS, 2002-2006

As would be expected, Ontario continues to holds the lion’s share of Canadian visits from New York State residents. However, there has been a negative trend in Canadian visits since 2002, also negatively affecting visits to Ontario.

73

Total Overnight Visitors (‘000)

500600700800900

1,0001,1001,2001,3001,4001,5001,6001,7001,8001,9002,0002,100

2002 2003 2004 2005 2006

#

Total CanadaVisitors FromNew York

Total OntarioVisitors FromNew York

Source: Statistics Canada ITS, 2002-2006

Overnight visits to Canada and also Ontario have declined slightly from 2002 through 2006.

74

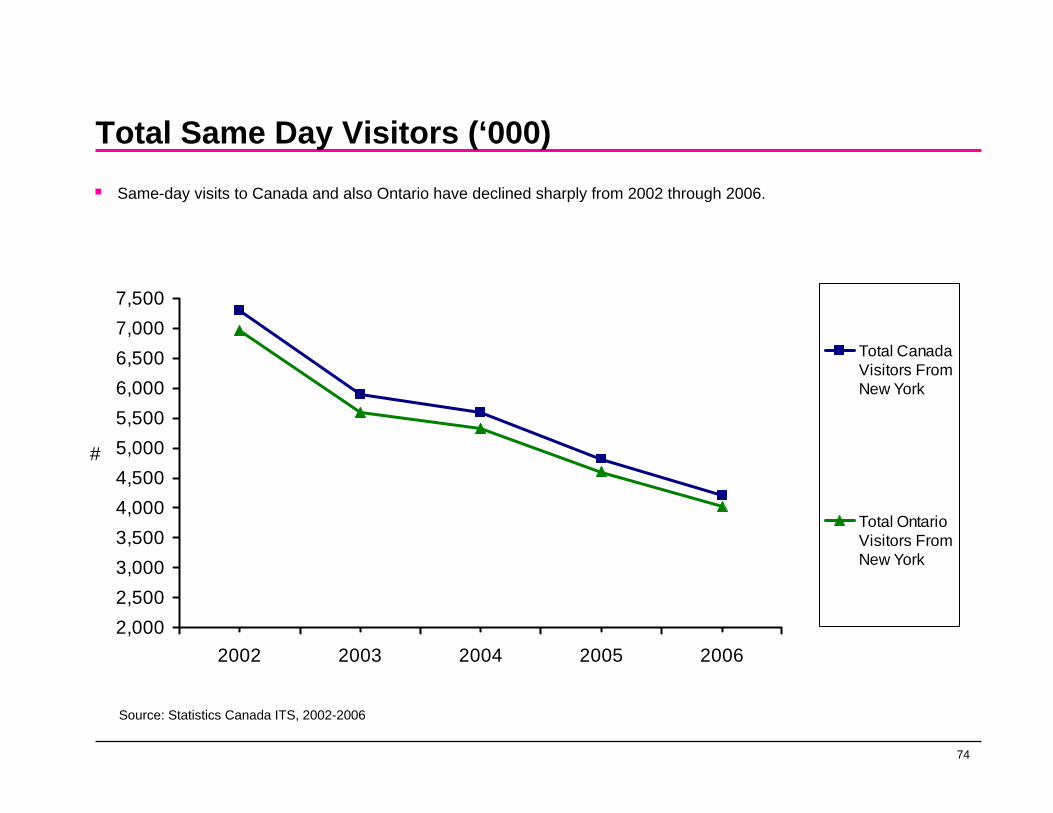

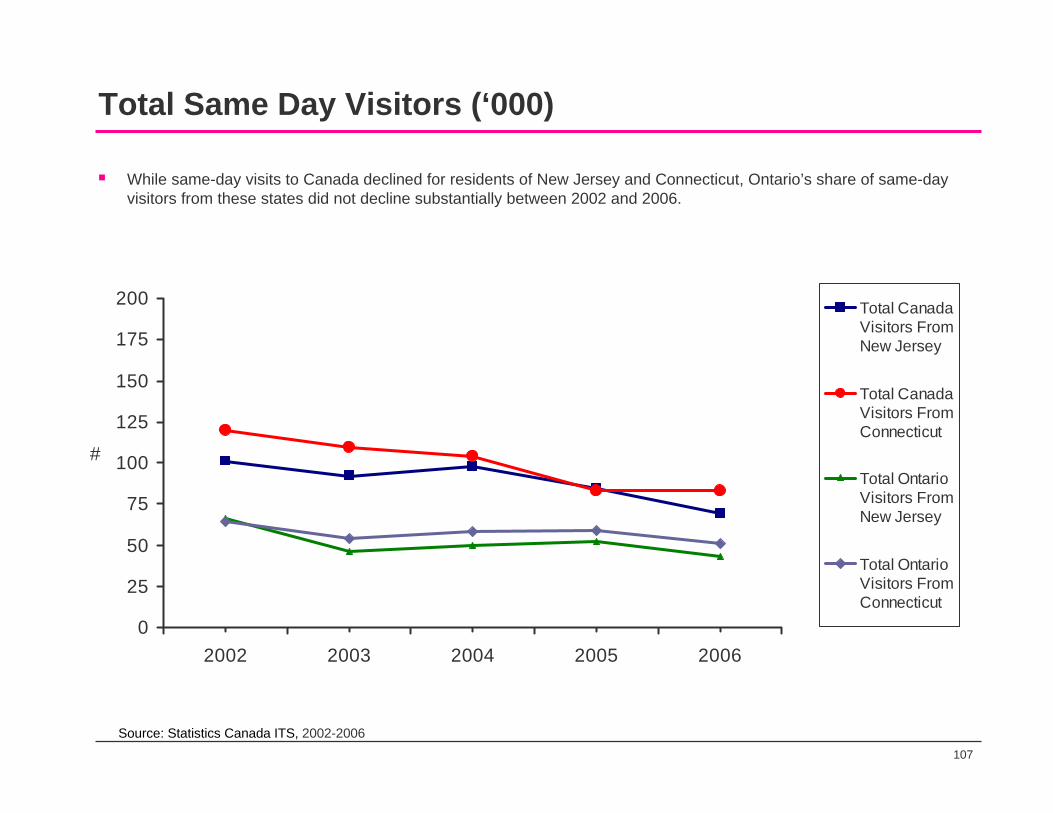

Total Same Day Visitors (‘000)

2,0002,5003,0003,5004,0004,5005,0005,5006,0006,5007,0007,500

2002 2003 2004 2005 2006

#

Total Canada Visitors FromNew York

Total OntarioVisitors FromNew York

Source: Statistics Canada ITS, 2002-2006

Same-day visits to Canada and also Ontario have declined sharply from 2002 through 2006.

75

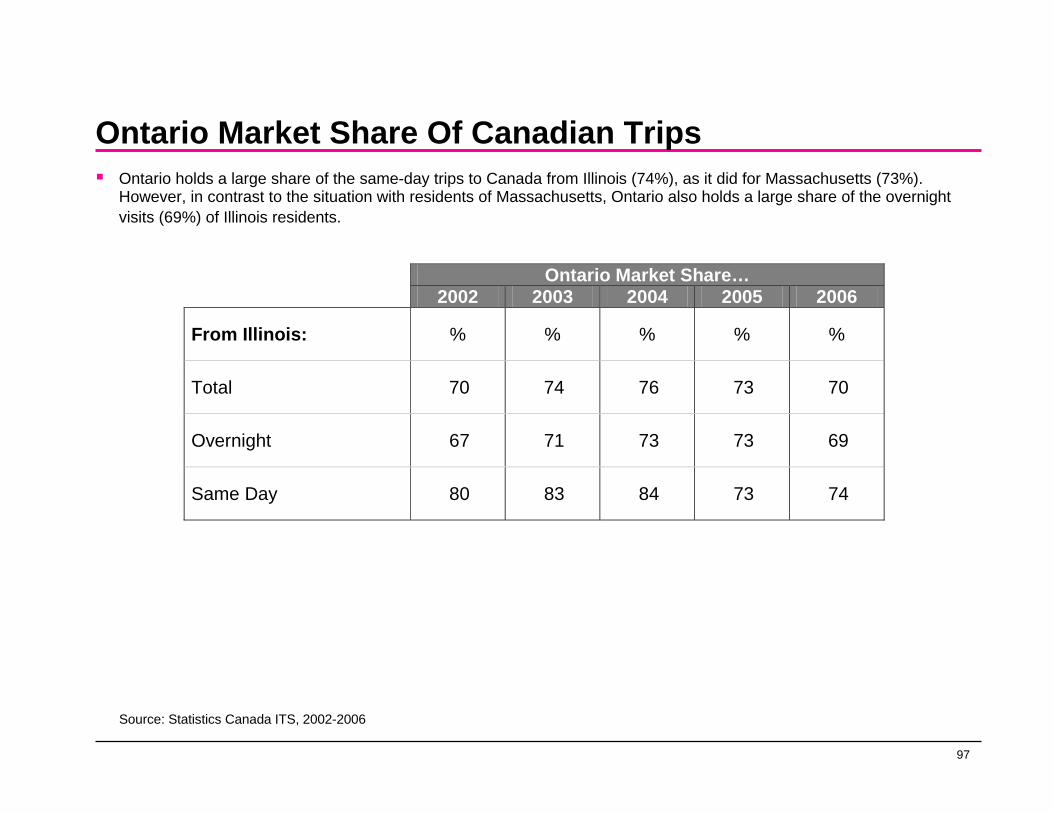

Ontario Market Share Of Canadian TripsOntario holds an extremely large share of the same-day trips to Canada from New York State (96%) and a large proportion (75%) of overnight visits to Canada.

Ontario Market Share… 2002 2003 2004 2005 2006

From New York: % % % % %

Total 91 90 90 90 90

Overnight 75 73 76 75 75

Same Day 95 95 95 96 96

Source: Statistics Canada ITS, 2002-2006

76

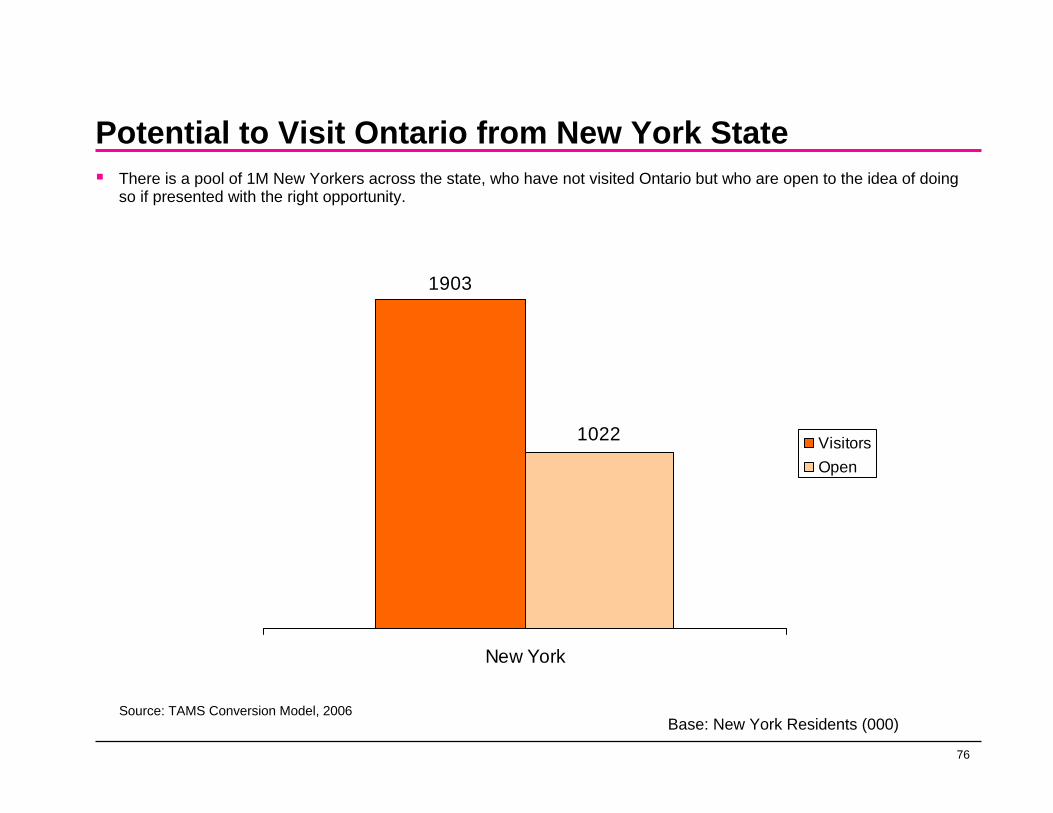

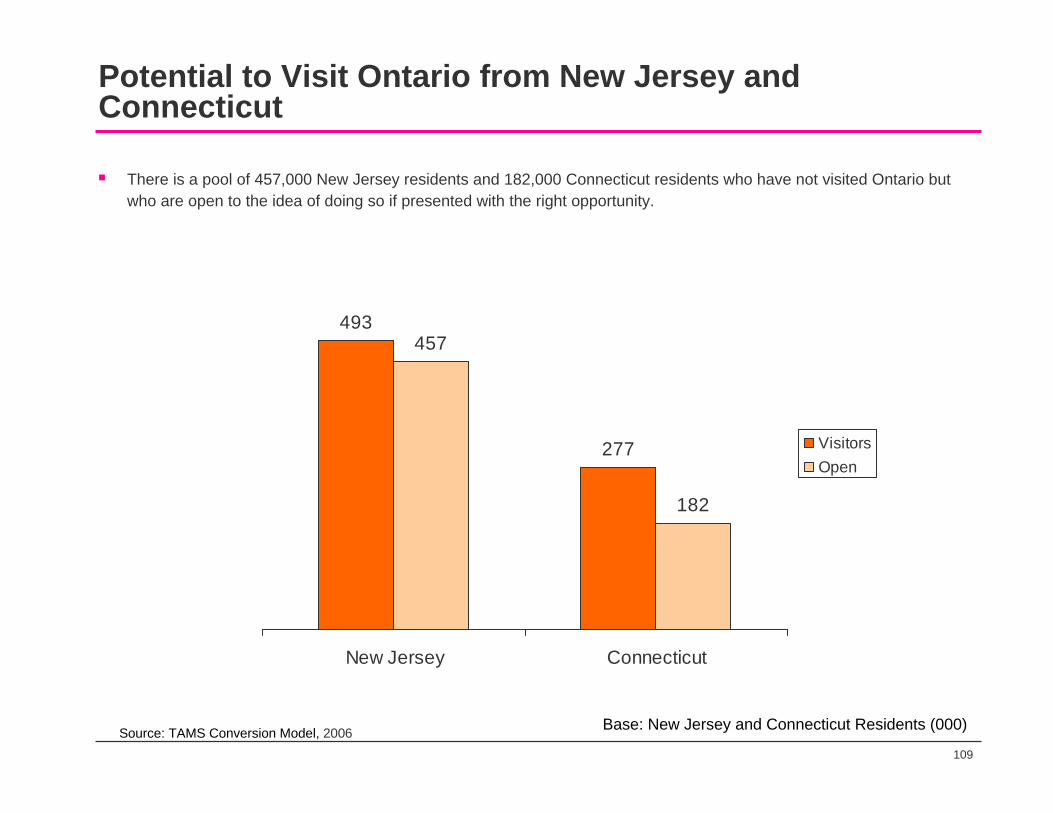

Potential to Visit Ontario from New York StateThere is a pool of 1M New Yorkers across the state, who have not visited Ontario but who are open to the idea of doing so if presented with the right opportunity.

1903

1022

New York

VisitorsOpen

Source: TAMS Conversion Model, 2006Base: New York Residents (000)

77

Main Purpose Of Trip - Leisure Travellers To Canada From New York

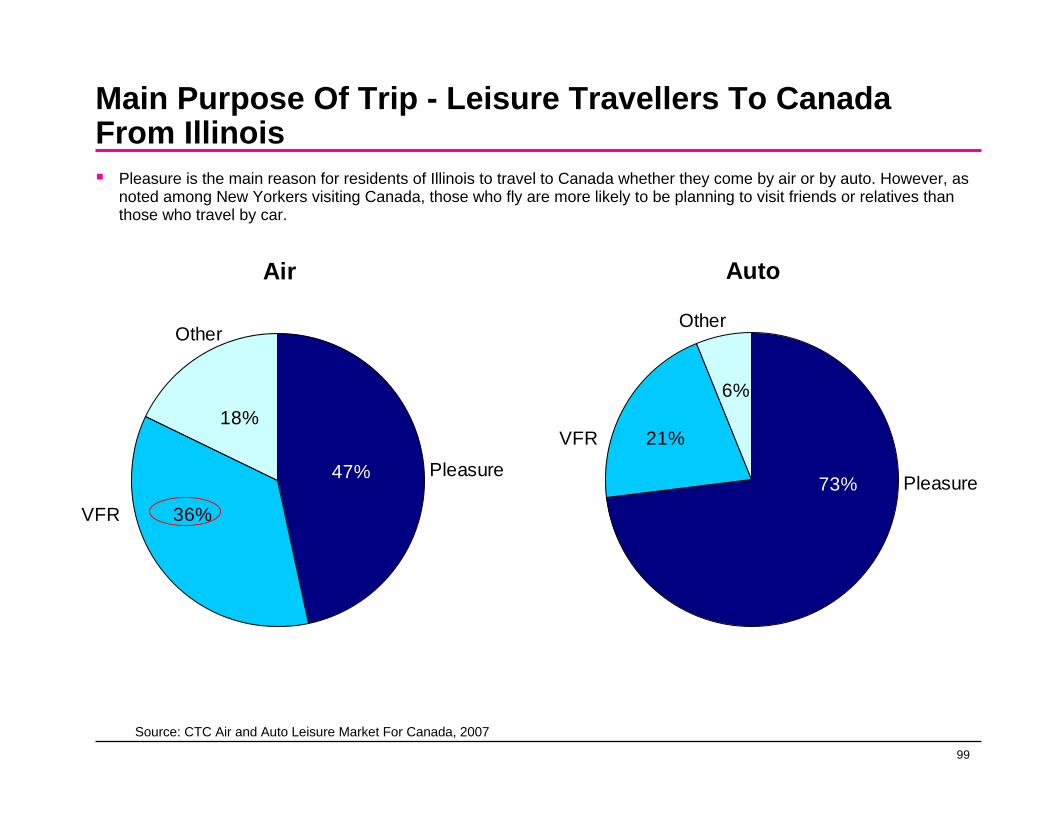

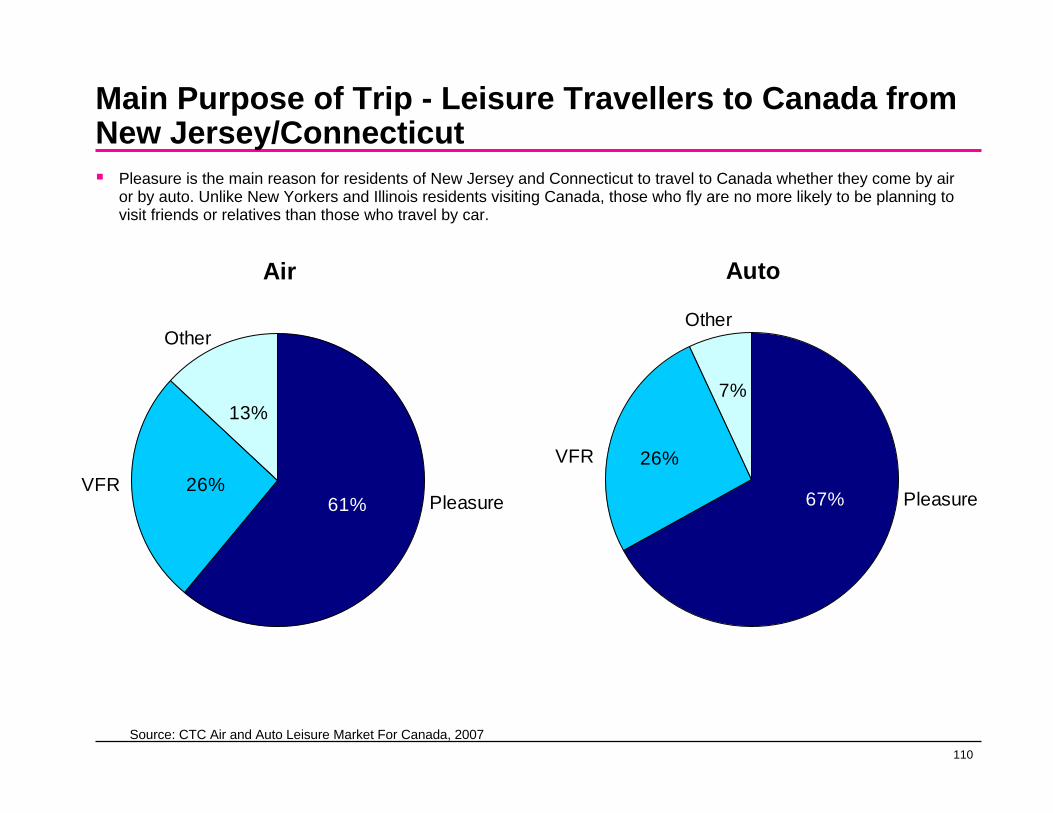

Pleasure is the main reason for New Yorkers to travel to Canada, whether they come by air or by auto. However, those who fly are more likely to be planning to visit friends or relatives than those who travel by car.

Air

14%

37%

49% Pleasure

VFR

Other

Auto

68%

19%

12%

Pleasure

VFR

Other

Source: CTC Air and Auto Leisure Market For Canada, 2007

78

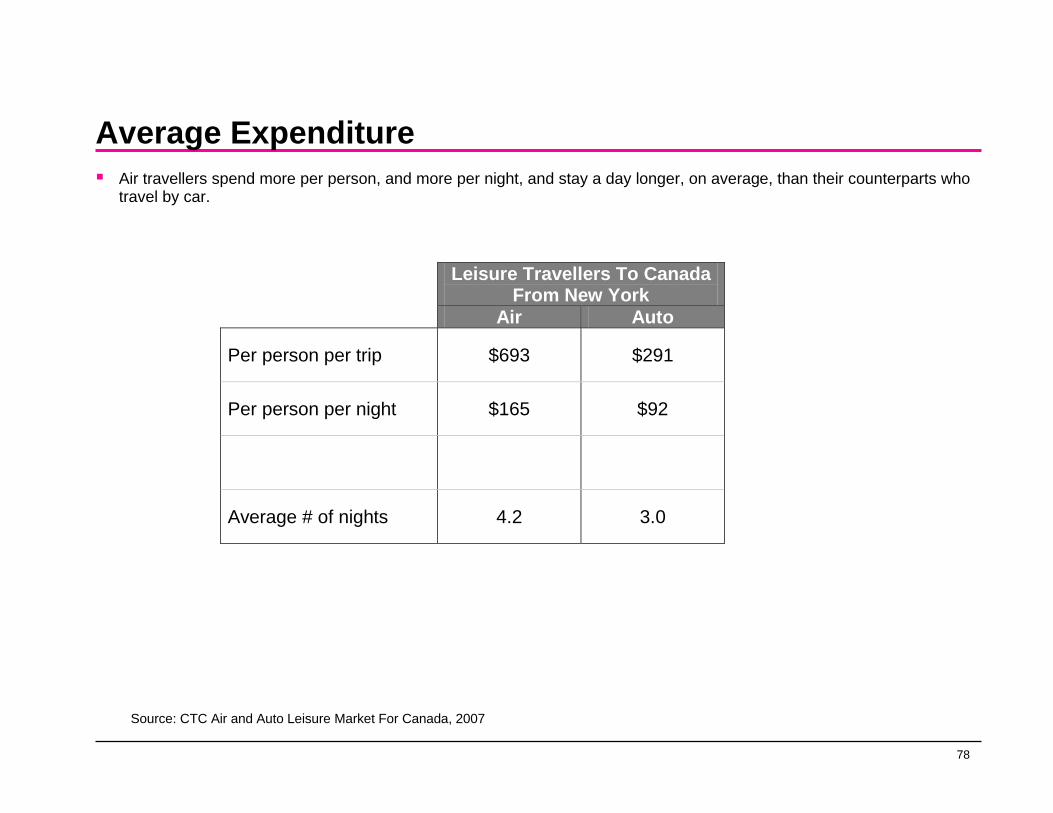

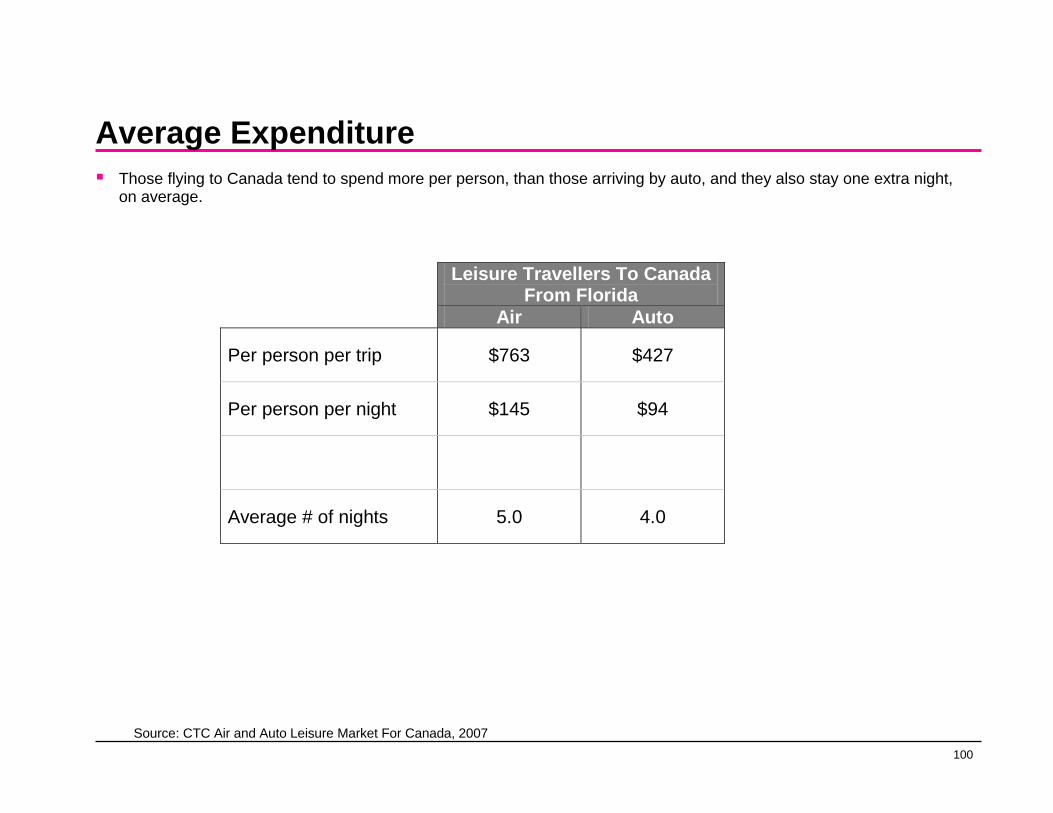

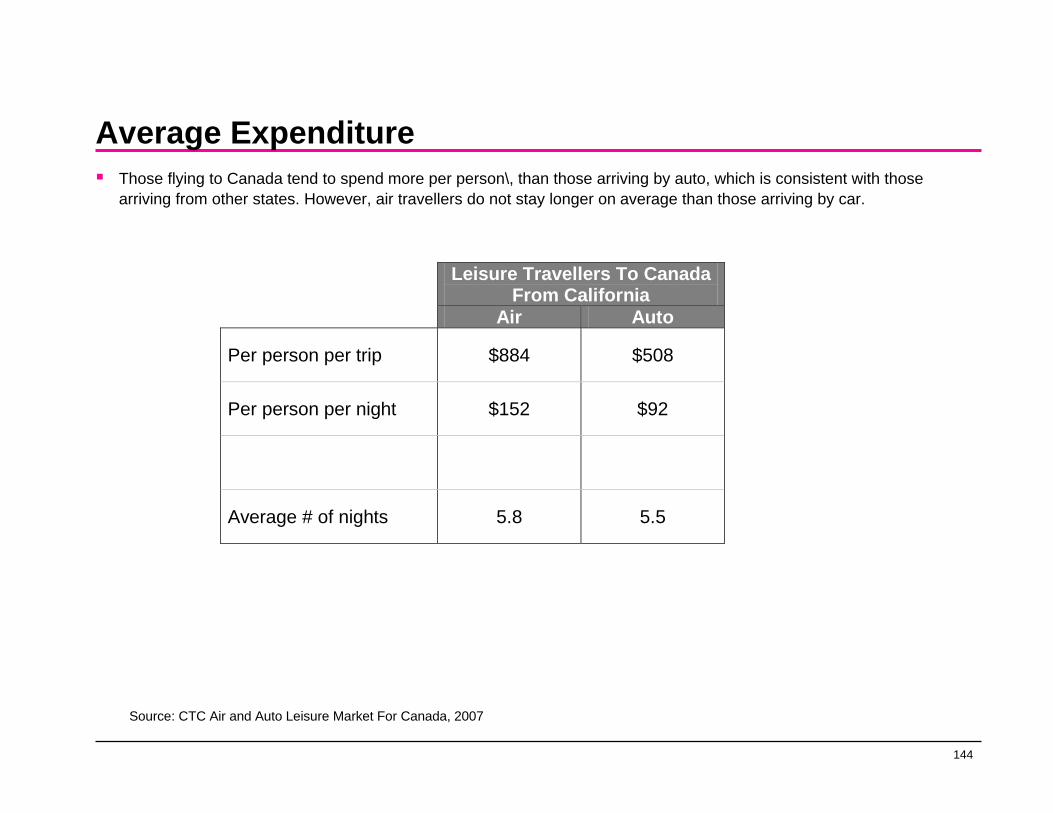

Average ExpenditureAir travellers spend more per person, and more per night, and stay a day longer, on average, than their counterparts who travel by car.

Leisure Travellers To Canada From New York

Air Auto

Per person per trip $693 $291

Per person per night $165 $92

Average # of nights 4.2 3.0

Source: CTC Air and Auto Leisure Market For Canada, 2007

79

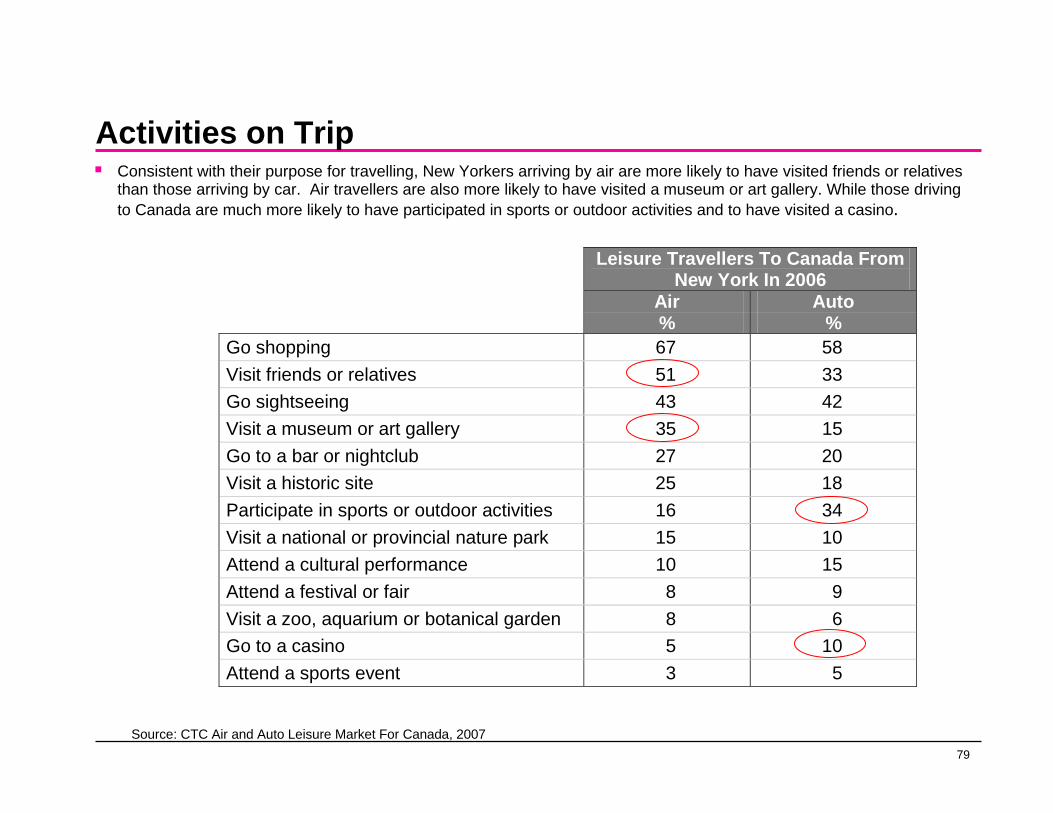

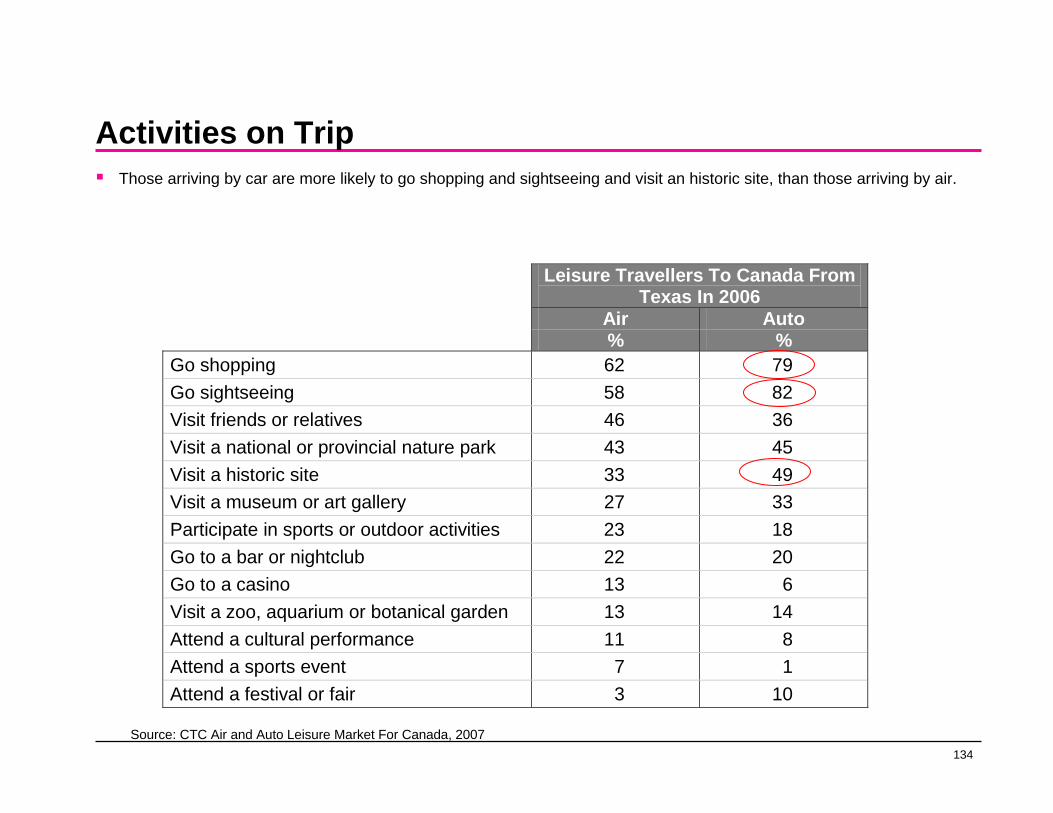

Activities on TripConsistent with their purpose for travelling, New Yorkers arriving by air are more likely to have visited friends or relatives than those arriving by car. Air travellers are also more likely to have visited a museum or art gallery. While those driving to Canada are much more likely to have participated in sports or outdoor activities and to have visited a casino.

Leisure Travellers To Canada From New York In 2006

Air Auto % % Go shopping 67 58 Visit friends or relatives 51 33 Go sightseeing 43 42 Visit a museum or art gallery 35 15 Go to a bar or nightclub 27 20 Visit a historic site 25 18 Participate in sports or outdoor activities 16 34 Visit a national or provincial nature park 15 10 Attend a cultural performance 10 15 Attend a festival or fair 8 9 Visit a zoo, aquarium or botanical garden 8 6 Go to a casino 5 10 Attend a sports event 3 5

Source: CTC Air and Auto Leisure Market For Canada, 2007

80

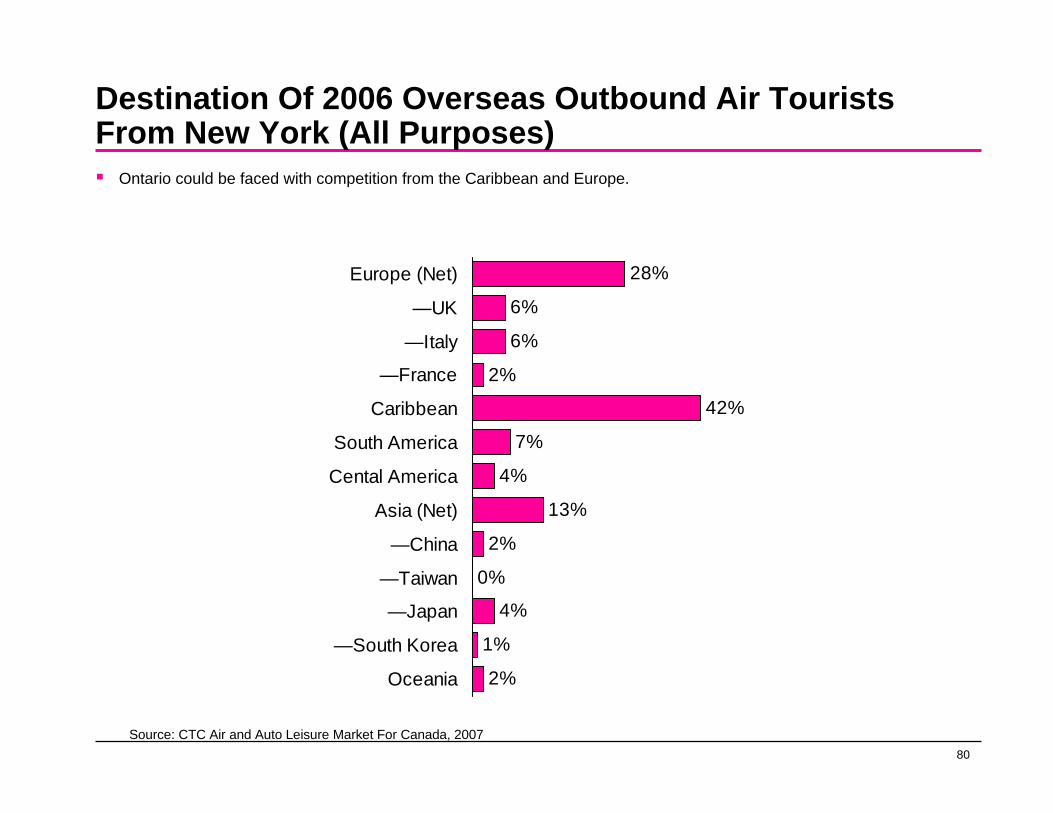

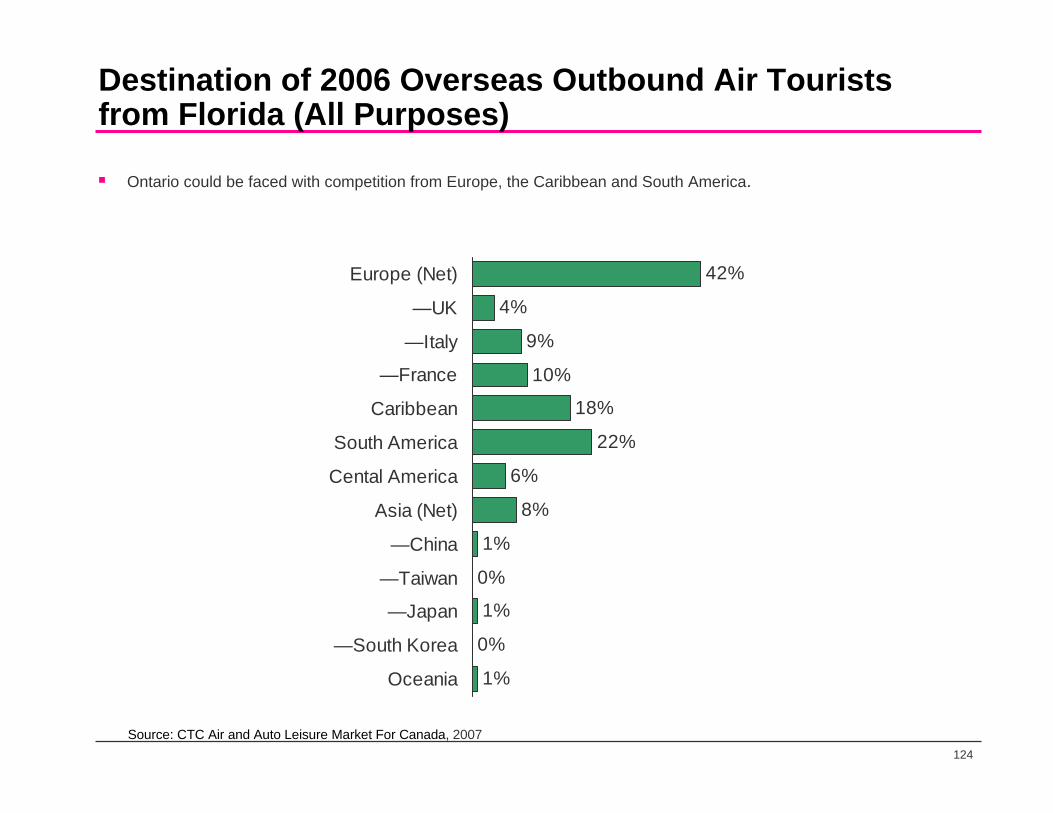

Destination Of 2006 Overseas Outbound Air Tourists From New York (All Purposes)

Ontario could be faced with competition from the Caribbean and Europe.

28%

6%

6%

2%

42%

7%

4%

13%

2%

0%

4%

1%

2%

Europe (Net)

—UK

—Italy

—France

Caribbean

South America

Cental America

Asia (Net)

—China

—Taiwan

—Japan

—South Korea

Oceania

Source: CTC Air and Auto Leisure Market For Canada, 2007

81

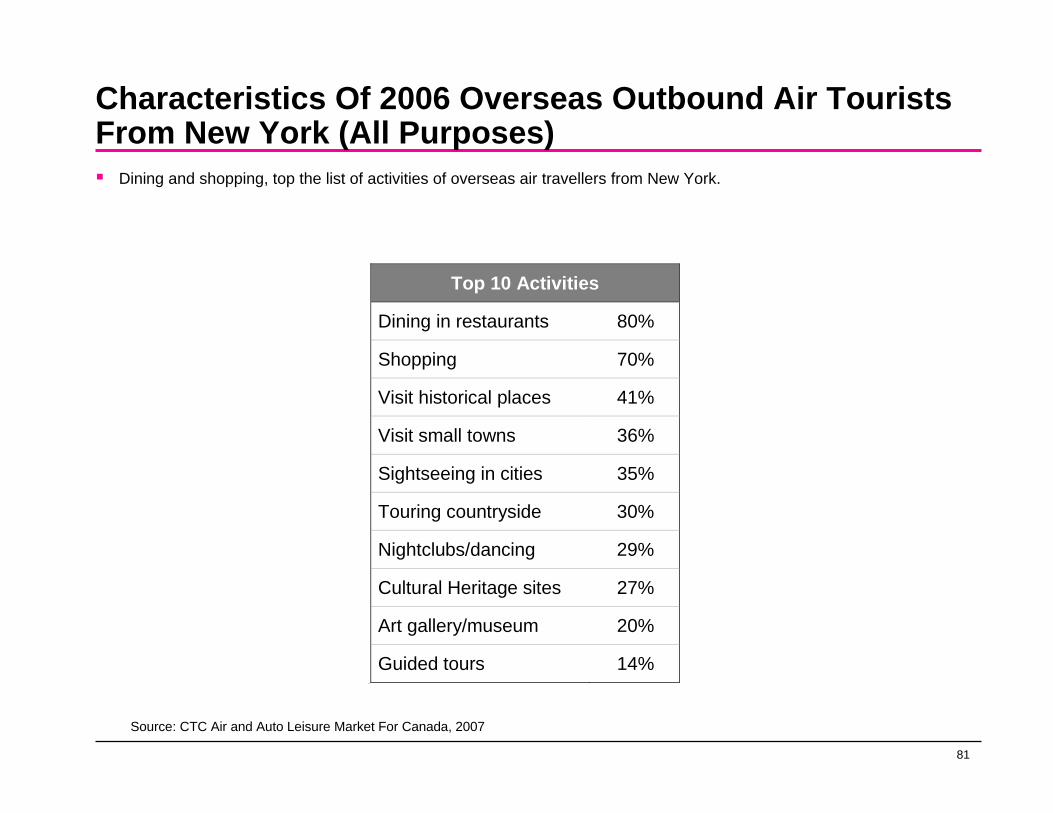

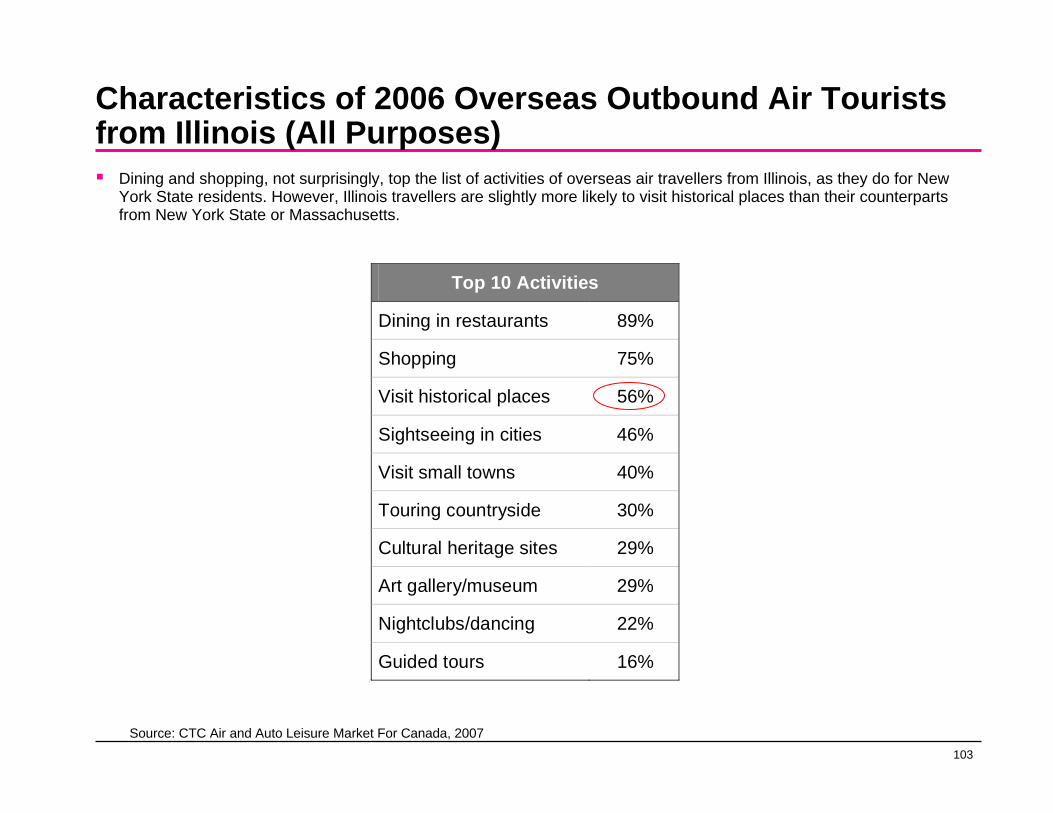

Characteristics Of 2006 Overseas Outbound Air Tourists From New York (All Purposes)

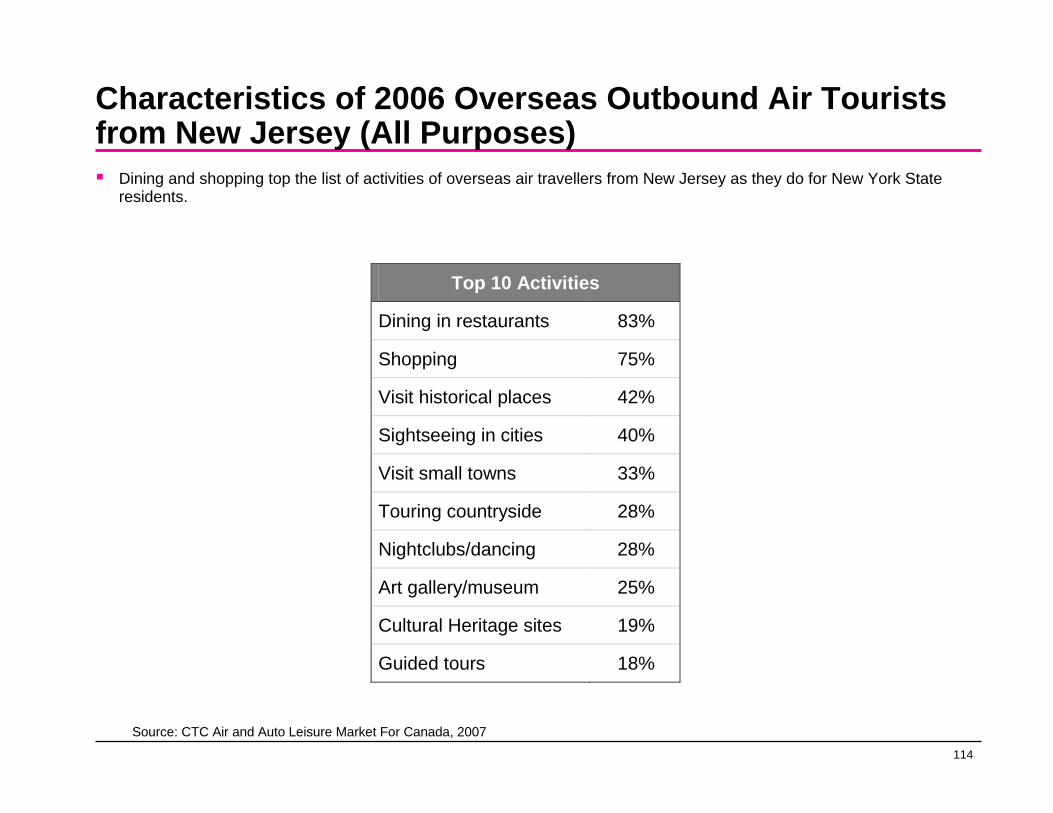

Dining and shopping, top the list of activities of overseas air travellers from New York.

Top 10 Activities

Dining in restaurants 80%

Shopping 70%

Visit historical places 41%

Visit small towns 36%

Sightseeing in cities 35%

Touring countryside 30%

Nightclubs/dancing 29%

Cultural Heritage sites 27%

Art gallery/museum 20%

Guided tours 14% 11

Source: CTC Air and Auto Leisure Market For Canada, 2007

82

Massachusetts

83

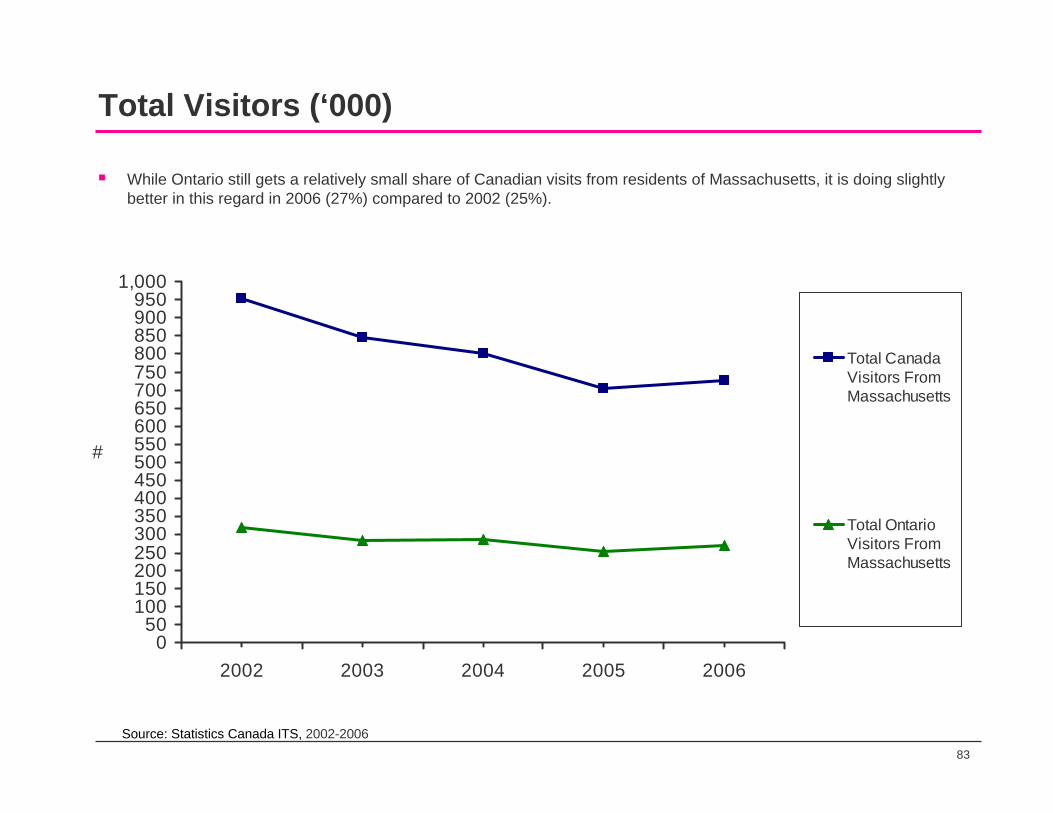

Total Visitors (‘000)

While Ontario still gets a relatively small share of Canadian visits from residents of Massachusetts, it is doing slightly better in this regard in 2006 (27%) compared to 2002 (25%).

050

100150200250300350400450500550600650700750800850900950

1,000

2002 2003 2004 2005 2006

#

Total CanadaVisitors FromMassachusetts

Total OntarioVisitors FromMassachusetts

Source: Statistics Canada ITS, 2002-2006

84

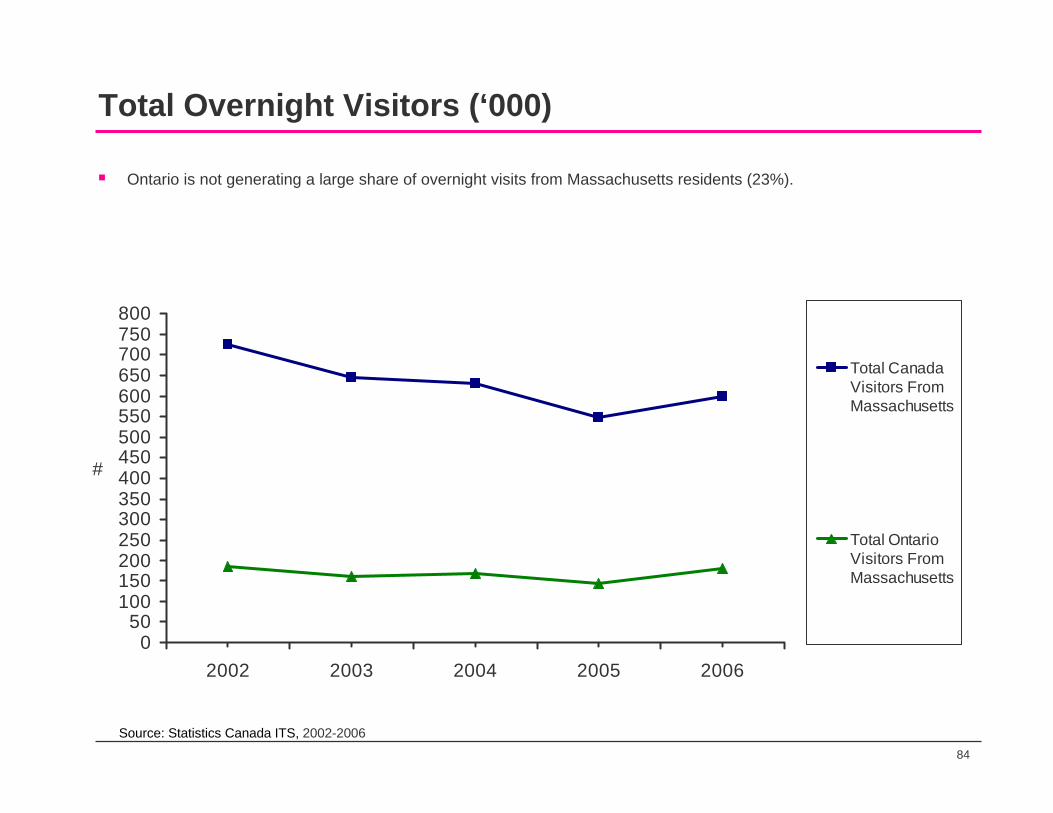

Total Overnight Visitors (‘000)

Ontario is not generating a large share of overnight visits from Massachusetts residents (23%).

050

100150200250300350400450500550600650700750800

2002 2003 2004 2005 2006

#

Total CanadaVisitors FromMassachusetts

Total OntarioVisitors FromMassachusetts

Source: Statistics Canada ITS, 2002-2006

85

Total Same Day Visitors (‘000)

However, Ontario is getting a large share of same-day visitors from Massachusetts to Canada.

0

25

50

75

100

125

150

175

200

225

250

2002 2003 2004 2005 2006

#

Total Canada Visitors FromMassachusetts

Total OntarioVisitors FromMassachusetts

Source: Statistics Canada ITS, 2002-2006

86

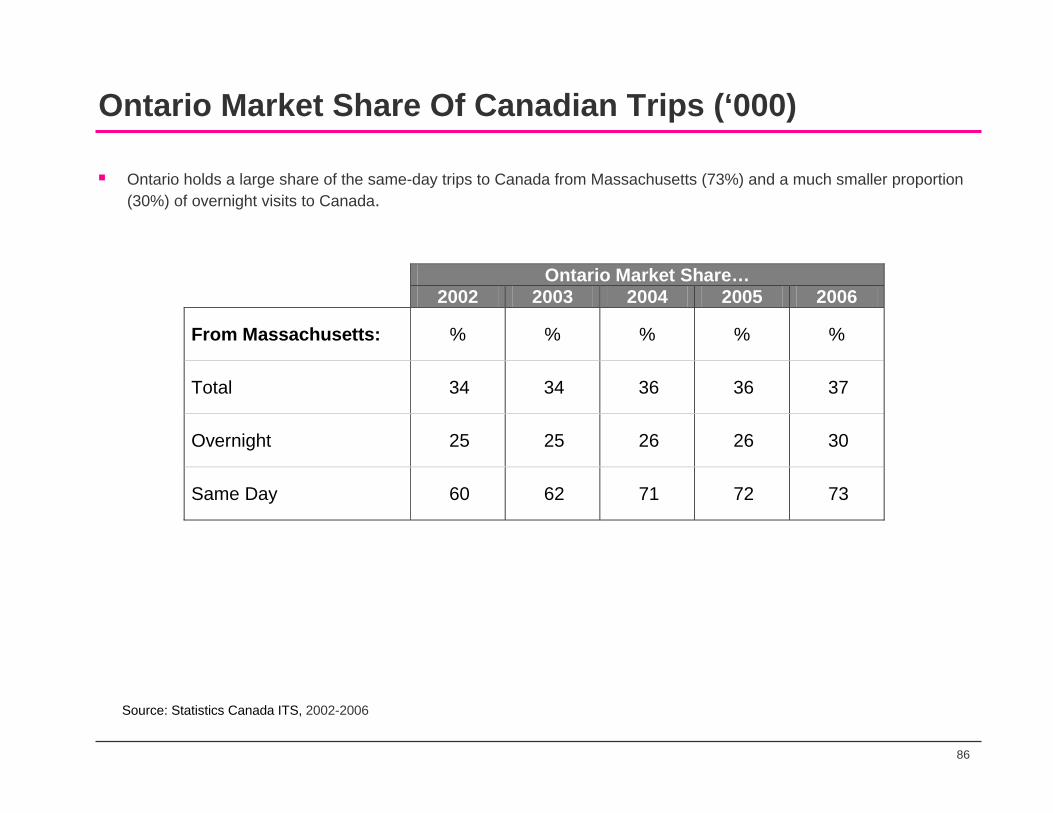

Ontario Market Share Of Canadian Trips (‘000)

Ontario holds a large share of the same-day trips to Canada from Massachusetts (73%) and a much smaller proportion (30%) of overnight visits to Canada.

Ontario Market Share… 2002 2003 2004 2005 2006

From Massachusetts: % % % % %

Total 34 34 36 36 37

Overnight 25 25 26 26 30

Same Day 60 62 71 72 73

Source: Statistics Canada ITS, 2002-2006

87

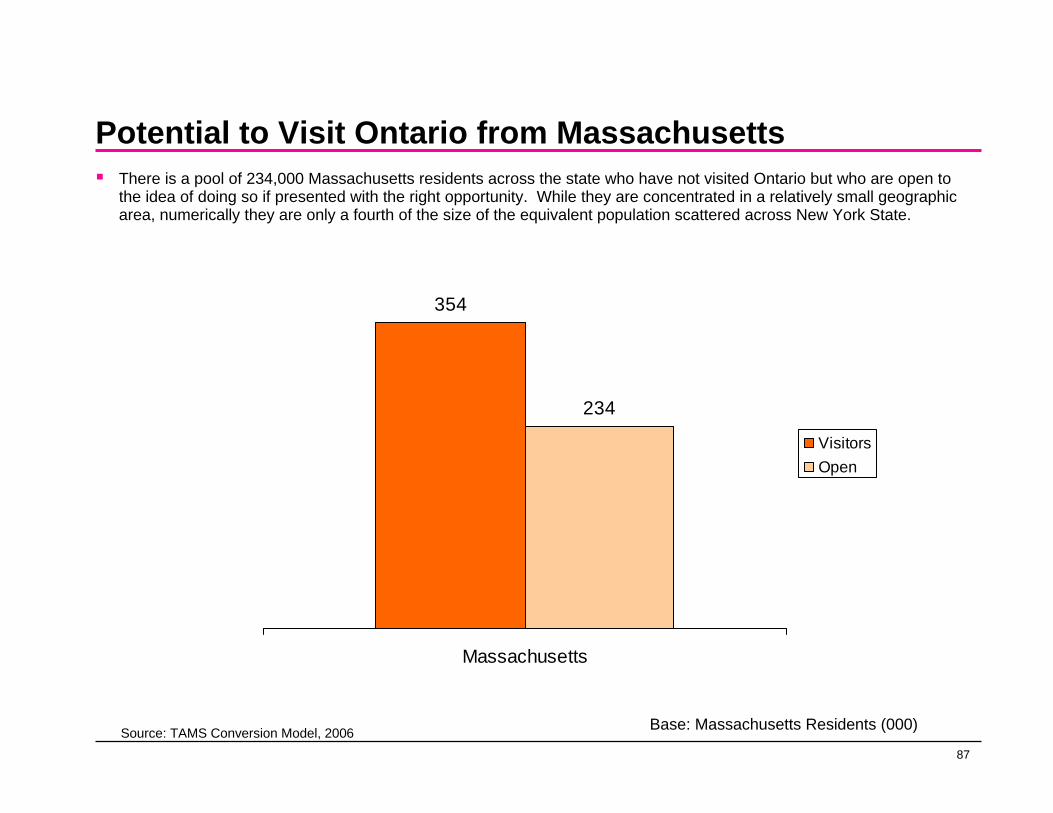

Potential to Visit Ontario from MassachusettsThere is a pool of 234,000 Massachusetts residents across the state who have not visited Ontario but who are open to the idea of doing so if presented with the right opportunity. While they are concentrated in a relatively small geographic area, numerically they are only a fourth of the size of the equivalent population scattered across New York State.

354

234

Massachusetts

VisitorsOpen

Source: TAMS Conversion Model, 2006 Base: Massachusetts Residents (000)

88

Main Purpose Of Trip - Leisure Travellers To Canada From Massachusetts

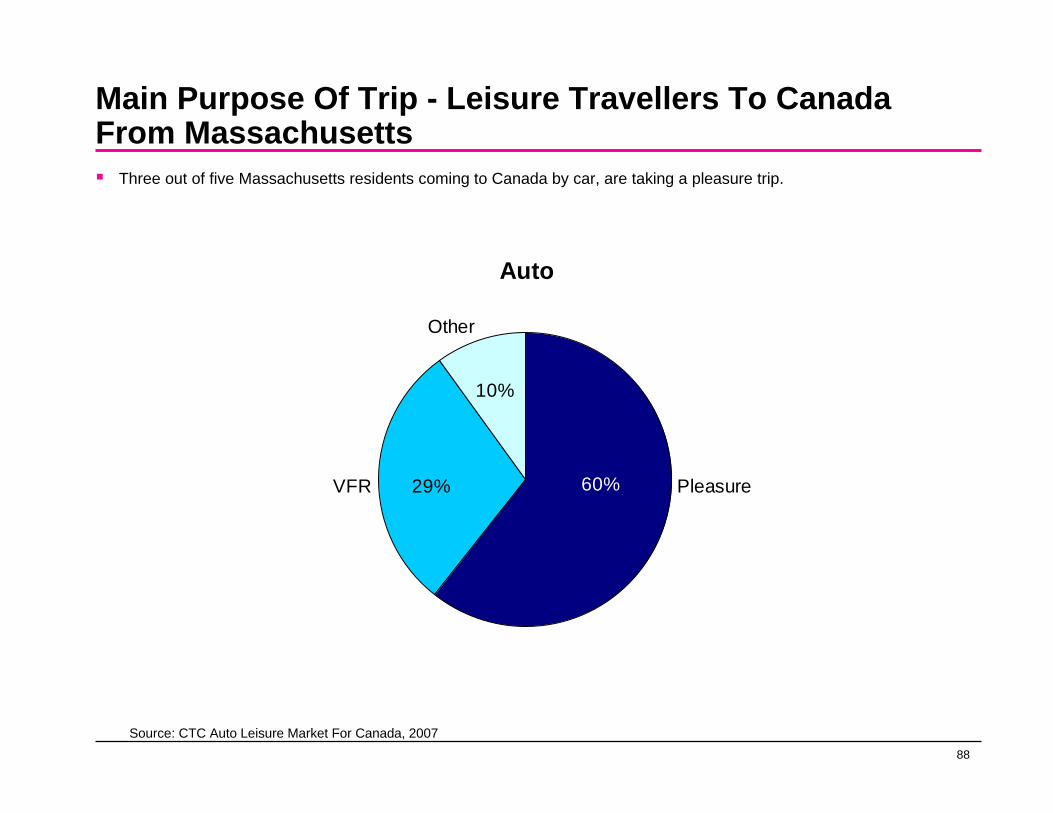

Three out of five Massachusetts residents coming to Canada by car, are taking a pleasure trip.

Auto

60%29%

10%

PleasureVFR

Other

Source: CTC Auto Leisure Market For Canada, 2007

89

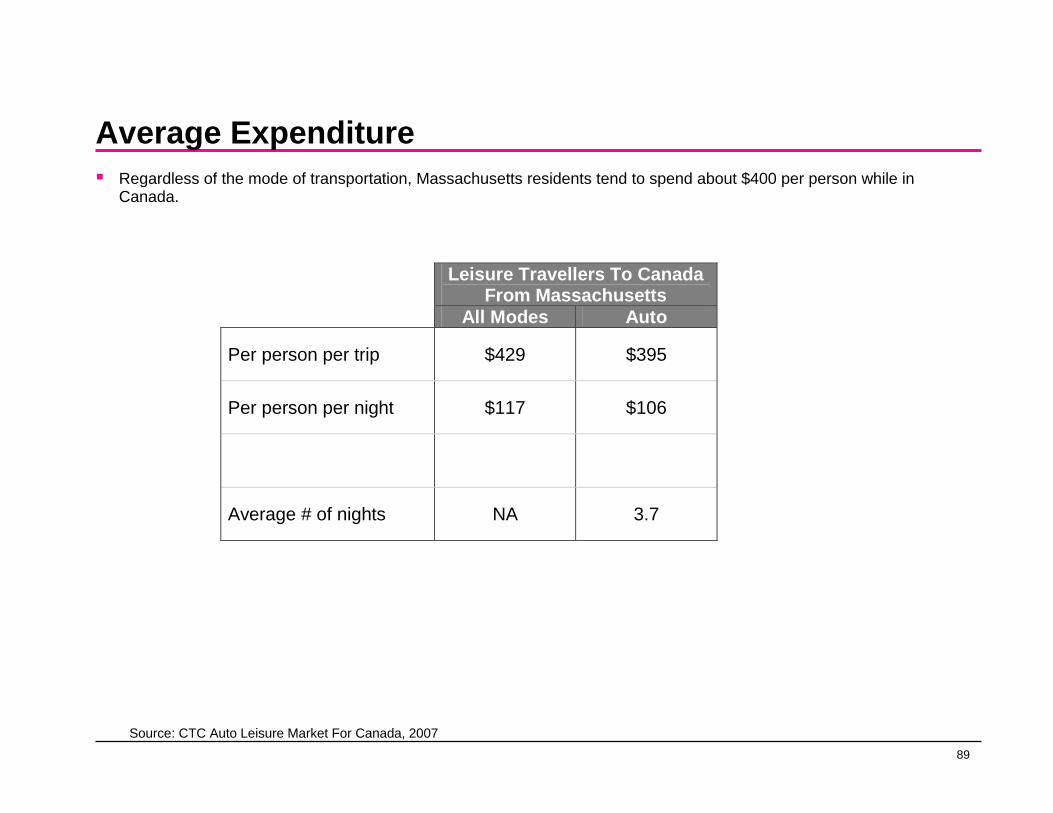

Average ExpenditureRegardless of the mode of transportation, Massachusetts residents tend to spend about $400 per person while in Canada.

Leisure Travellers To Canada From Massachusetts

All Modes Auto

Per person per trip $429 $395

Per person per night $117 $106

Average # of nights NA 3.7

Source: CTC Auto Leisure Market For Canada, 2007

90

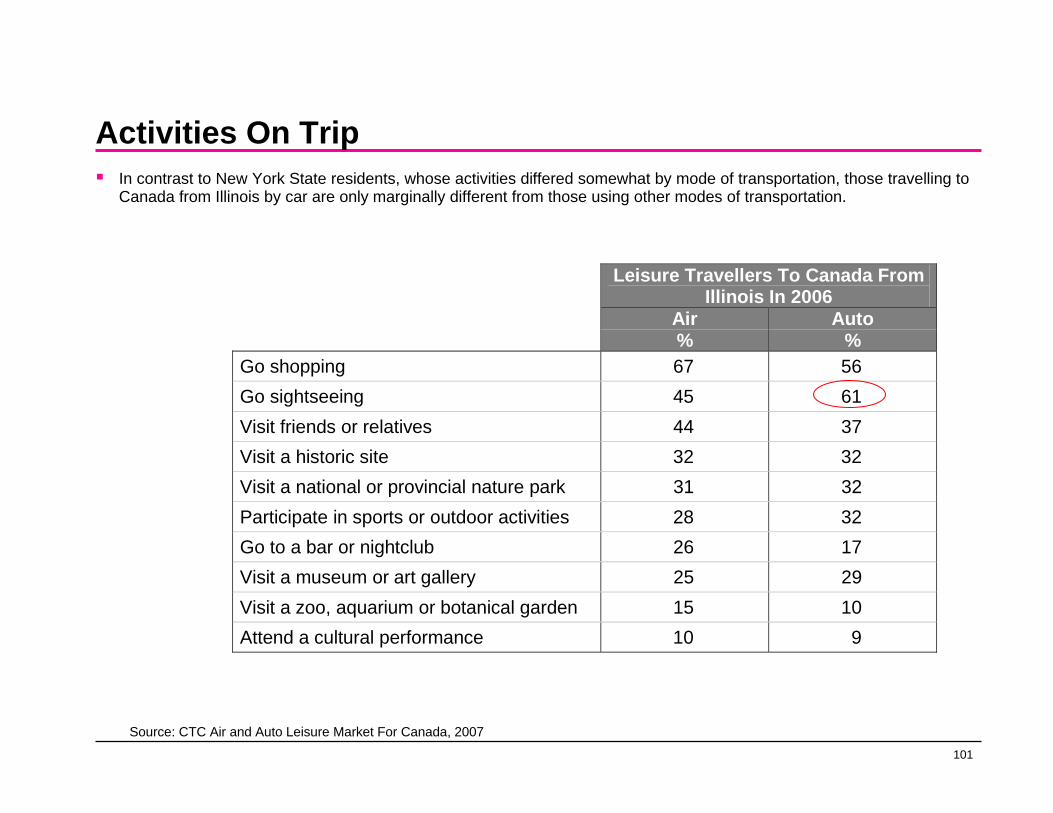

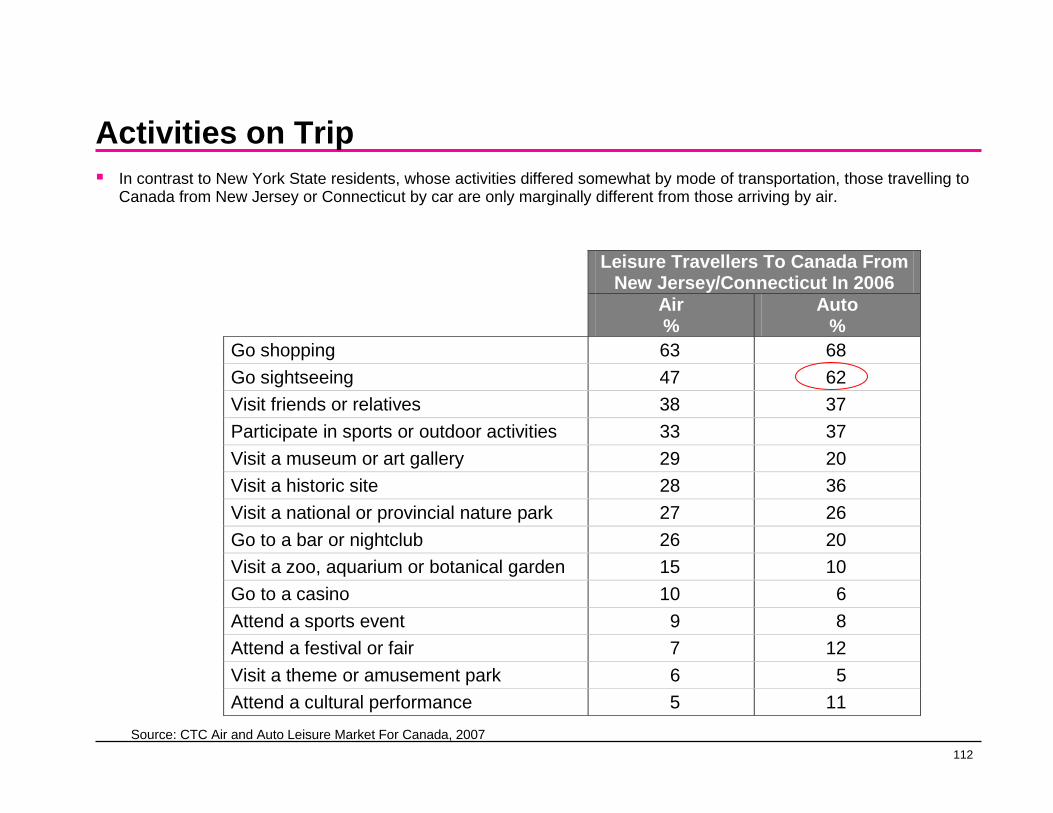

Activities On TripIn contrast to New York State residents whose activities differed somewhat by mode of transportation, those travelling to Canada from Massachusetts by car are not substantially different from those using other modes of transportation.

Leisure Travellers To Canada From Massachusetts In 2006

All Modes Auto % % Go shopping 62 65 Go sightseeing 57 59 Visit a historic site 36 36 Visit friends or relatives 34 43 Visit a museum or art gallery 28 26 Go to a bar or nightclub 26 30 Visit a national or provincial nature park 25 24 Attend a cultural performance 22 13 Participate in sports or outdoor activities 21 25 Visit a zoo, aquarium or botanical garden 13 11 Go to a casino 12 7 Attend a festival or fair 11 12 Attend a sports event 7 9

Source: CTC Auto Leisure Market For Canada, 2007

91

Destination Of 2006 Overseas Outbound Air Tourists From Massachusetts (All Purposes)

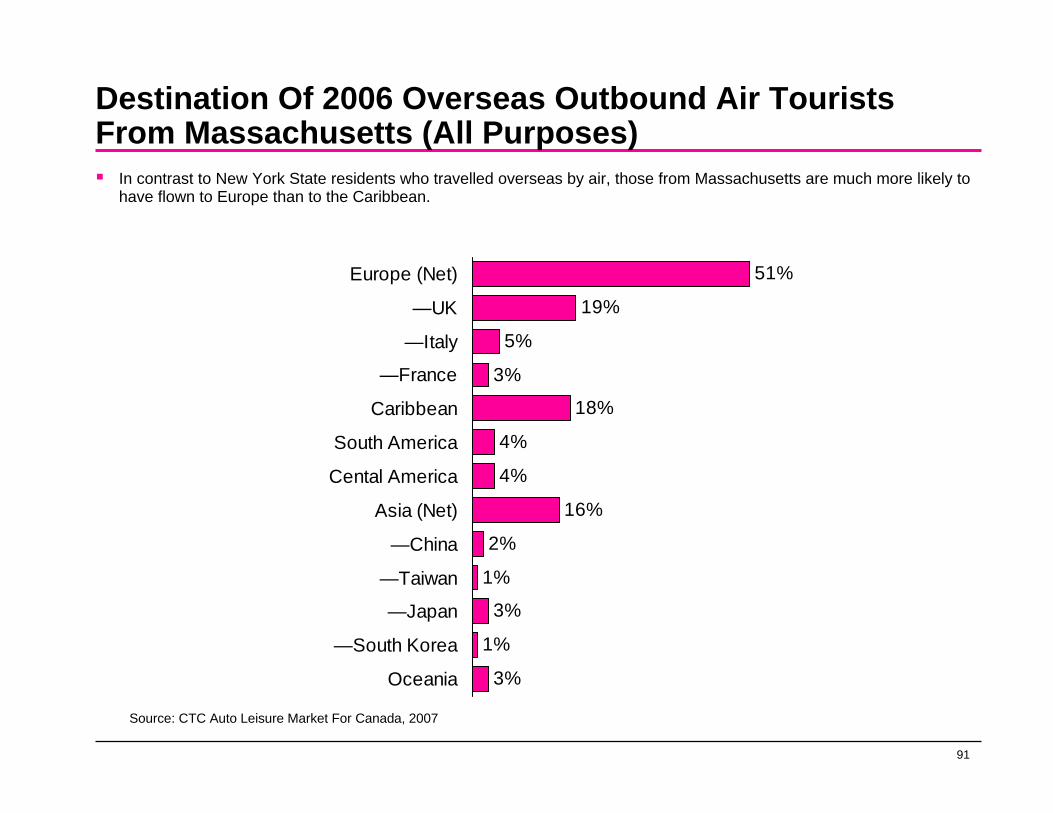

In contrast to New York State residents who travelled overseas by air, those from Massachusetts are much more likely to have flown to Europe than to the Caribbean.

51%

19%

5%

3%

18%

4%

4%

16%

2%

1%

3%

1%

3%

Europe (Net)

—UK

—Italy

—France

Caribbean

South America

Cental America

Asia (Net)

—China

—Taiwan

—Japan

—South Korea

Oceania

Source: CTC Auto Leisure Market For Canada, 2007

92

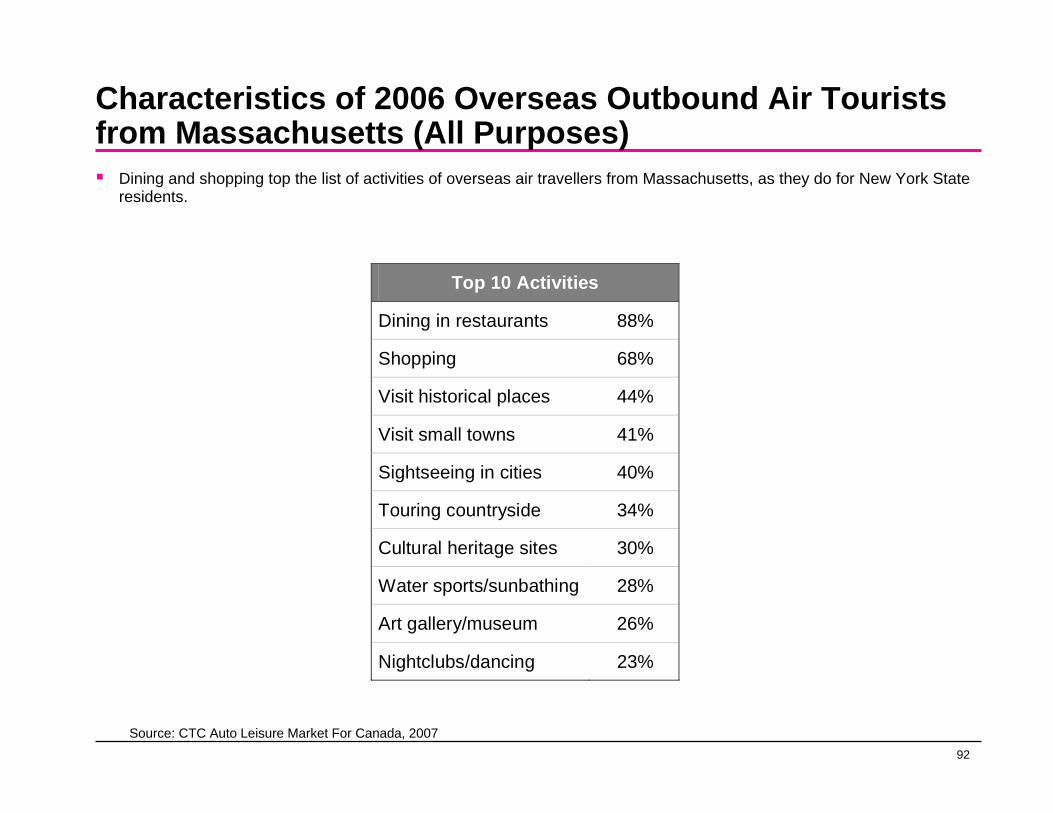

Characteristics of 2006 Overseas Outbound Air Tourists from Massachusetts (All Purposes)

Dining and shopping top the list of activities of overseas air travellers from Massachusetts, as they do for New York State residents.

Top 10 Activities

Dining in restaurants 88%

Shopping 68%

Visit historical places 44%

Visit small towns 41%

Sightseeing in cities 40%

Touring countryside 34%

Cultural heritage sites 30%

Water sports/sunbathing 28%

Art gallery/museum 26%

Nightclubs/dancing 23% 11

Source: CTC Auto Leisure Market For Canada, 2007

93

Illinois

94

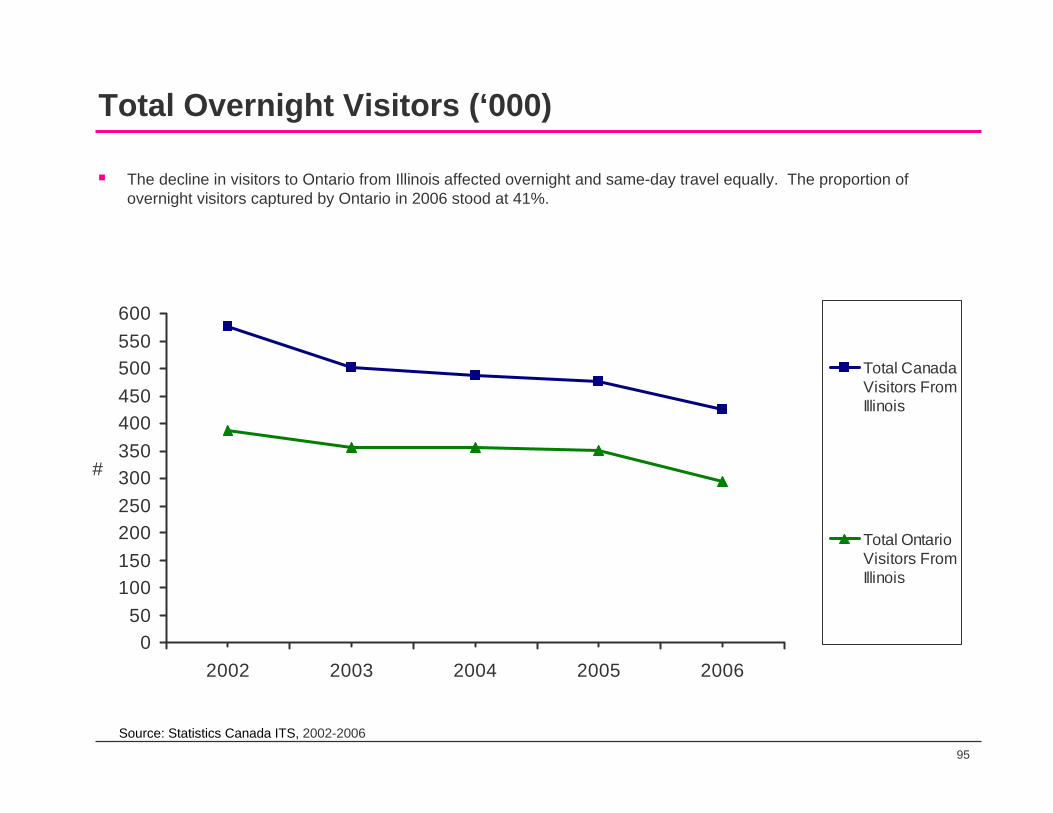

Total Visitors (‘000)

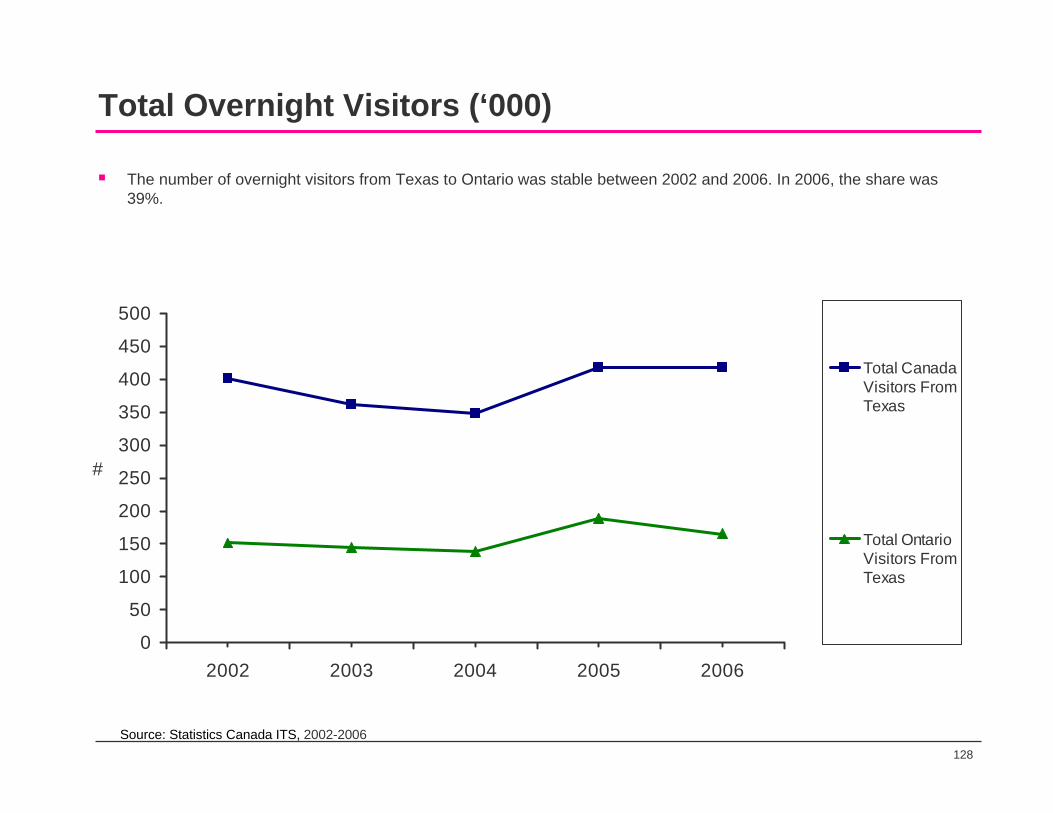

While visits to Canada from Illinois fell from 2002 through 2006, Ontario continued to get a reasonable share of Canadian visits from residents of Illinois. In 2006 Ontario’s share stood at 41%.

100150200250300350400450500550600650700750800

2002 2003 2004 2005 2006

#

Total CanadaVisitors FromIllinois

Total OntarioVisitors FromIllinois