opportunites in the food markets of india€¦ · opportunities in the food markets of india for...

TRANSCRIPT

OPPORTUNITIES IN THE FOOD MARKETS OF

INDIA

For further information about this report contact:

Dennis Pervis, Senior Markets AnalystMarketing and Trade TeamAgriculture and Agri-Food CanadaBritish Columbia Regional Office#420 - 4321 Still Creek DriveBurnaby, B.C.V5C 6S7Email: [email protected]

Last Updated: February, 2012

Although every effort is made to ensure that the information is correct. Agriculture and Agri-

Food Canada assumes no responsibility for its accuracy, reliability, or for any decisions arising

from the information contained herein.

ii

OPPORTUNITIES IN THE FOOD MARKETS OF INDIA

TABLE OF CONTENTS

EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

I. PURPOSE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

II. BUSINESS PARADIGMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1A. The Competitive Environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1B. Pure Export . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2C. Export with Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2D. Multi-National Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

III. PROFILE OF INDIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3A. Geography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1. The Himalayan Mountains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32. The Gangetic Plain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33. Peninsular India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

B. Demography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4C. Culture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1. History . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52. Food . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

a) Traditional . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5b) Recent Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

i) Shopping Habits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7ii) Health and Wellness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

3. Religions and Philosophies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12D. Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1. Data Sources and Valuations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132. Currencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143. Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144. Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

E. International Transportation - Canada to India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161. Ocean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162. Air Freight . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

F. Economic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171. Historical Development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172. Recent Conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173. Determinants of Food Demand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 194. Consumer Expenditures on Food and Non-Alcoholic Beverages, by Political Division

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

iii

5. Determinants of Food Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22G. The Regions of India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

1. East & Northeast India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242. North India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253. South India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 254. West India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

IV. RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25A. Internal Political/Economic Conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25B. External Political/Economic Conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26C. Handling Risks of International Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

V. PRODUCT ANALYSIS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27A. Selected Products Imported by India From Canada . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27B. Selected Products Imported by India But Currently Not From Canada . . . . . . . . . . . . . . 30

VI. GRID ANALYSIS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35A. All Agricultural, Agri-food & Seafood Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35B. Agricultural Agri-food & Seafood Imports of India From Canada vs From the Whole

World . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

VII. PRICE WORK-UPS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39A. The Research Price Work-up . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40B. Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

VIII. IDENTIFICATION OF CONTESTABLE MARKETS . . . . . . . . . . . . . . . . . . . . . . . . . 41A. Dairy Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42B. Opportunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42C. Product Groups with an Index of Indicators of 1.00 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48D. Product Groups with an Index of Indicators from 0.75 to 0.99 . . . . . . . . . . . . . . . . . . . . 51E. Product Groups with an Index of Indicators from 0.50 to 0.74 . . . . . . . . . . . . . . . . . . . . 51F. Product Groups with an Index of Indicators from 0.25 to 0.49 . . . . . . . . . . . . . . . . . . . . 53G. Product Groups with an Index of Indicators from 0.00 to 0.24 . . . . . . . . . . . . . . . . . . . . 54

IX. CONCLUSIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

X. CONTACTS IN INDIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

XI. CONTACTS IN CANADA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

APPENDIX 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

APPENDIX 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

iv

Canada - New Zealand/US - Measures Affecting the Importation of Milk and the Exportationof Dairy Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

A. The WTO Rulings Regarding Dairy Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85B. The Mutually Agreed Solutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

ENDNOTES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

v

LIST OF TABLES

Table 1. Selected Traditional Cuisines of India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Table 2. Estimated Consumption of Packaged and Processed Food Products. India. 2006 and

2011. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Table 3. Value of Sales of Health and Wellness Classifications. India . . . . . . . . . . . . . . . . . . 11Table 4. Religions and Philosophies of India - Food Preferences. . . . . . . . . . . . . . . . . . . . . . 12Table 5. Average Tariff Rates Applied on Agricultural, Agri-food, Fish and Seafood Products,

2008. India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Table 6. Determinants of Changes in the Effective Demand for Food. 2005 to 2011. . . . . . . 19Table 7. Expenditure on Food and Non-alcoholic Beverages in Selected Political Divisions of

India. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Table 8. Production and Annual Increases of Selected Crops, India . . . . . . . . . . . . . . . . . . . . 22Table 9. Tariff Rates on Selected Imported Products. India. 2008. . . . . . . . . . . . . . . . . . . . . . 23Table 10. Ratios of Indian CIF Import Prices from Canada to Indian CIF Import Prices from the

World. Selected Products. 2010. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Table 11. Summary of Indicators of Contestability of Selected Markets. India. . . . . . . . . . . . . 43Table 12. Area, Population and NSDP of States and Union Territories of India. 2011. . . . . . . 60Table 13. Population and GDP. India. 1992 - 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Table 14. GDP by Origin, 2011. India. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63Table 15. Percent of Employment by Sector. India. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64Table 16. Distribution of Households by Disposable Income. India . . . . . . . . . . . . . . . . . . . . . 65Table 17. Value and Volume of Retail Sales of Packaged Food. India. 2005 and 2010. . . . . . 65Table 18. Compound Annual Rates of Change of Production and Consumption (Supply) of

Selected Products. India. 1997 - 2007. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68Table 19. Indicative CIF Prices of Imports to India from Canada, the World and Major

Competitors. 2010. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69Table 20. Canada's WTO Dairy Export Subsidy Commitment Levels . . . . . . . . . . . . . . . . . . . 86

vi

LIST OF FIGURES

Figure 1. Population Pyramid. India. 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Figure 2. Distribution of Households by Disposable Income Classes. India. . . . . . . . . . . . . . . . 7Figure 3. Proportion of Packaged Food Sales by Distribution Format. India. . . . . . . . . . . . . . . 8Figure 4. Value of the INR Expressed in CADs (CAD per INR). January 1993 to February

2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Figure 5. Percentage Changes in Selected Indian Agricultural, Agri-food & Seafood Imports -

From Canada vs From the World. 2005 - 2010. Part 1. . . . . . . . . . . . . . . . . . . . . . . . 38Figure 6. Percentage Changes in Selected Indian Agricultural, Agri-food & Seafood Imports -

From Canada vs From the World. 2005 - 2010. Part 2. . . . . . . . . . . . . . . . . . . . . . . . 39Figure 7. Political Map of India. 2001. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

vii

EXECUTIVE SUMMARY

INDIA:

• is the second most populous country in the world after China; with 1.21 billionpeople increasing at an annual rate of 1.64%. - A positive influence on the demandfor food;

• experienced a 7.80% annual increase in GDP per person between 1999 and 2010.- A positive influence on the effective demand for food;

• has 20 political regions out of 35 with NSDP per person above the national average(Andaman & Nicobar Islands, Mizoram, Nagaland, Sikkim, Chandigarh, Delhi,Haryana, Himachal Pradesh, Punjab, Uttarakhand, Andhra Pradesh, Karnataka,Kerala, Lakshedweep, Pondicherry, Tamil Nadu, Dadra & Nagar Haveli, Goa,Gujarat and Maharashtra).- Canadian exporters should initially target one or more of these geographic areas;

• experienced a -3.99% annual decrease in the value of the Indian Rupee relative tothe Canadian Dollar, between January 1995 and February 2012. - A small butnegative influence on imports from Canada;

• is experiencing growing inequities in per capita income as measured by a gini ratioof 39.9 in 2011 and estimated NSDP per capita ranging from CAD 436 in BiharState to CAD 4,355 in Goa. - A negative influence on political stability;

• sourced 24.70% of its food imports from 32 American countries, in 2010. The topfive American countries were: Argentina, Brazil, the USA, Canada and Chile. - Canada faces considerable competition from emerging economies in SouthAmerica and from the USA;

• imported CAD 13,767 million worth of agricultural, agri-food & seafood products in2010, of which CAD 568 million worth (4.1%) was from Canada. As a supplier offood to India, Canada has moved from 9th place in 2005 to 7th place in 2010 - Canada must continue this progress;

• represents several risks for Canadian exporters. - The facilities of ExportDevelopment Canada and the Canadian Trade Commissioner service may be usefulin managing these risks.

Based on the analysis in this paper, Canadian food exporters may find new orcontinuing opportunities in the following Indian markets:

• Fish, Nesoi, With Bones, Fresh Or Chilled;

viii

• Milk & Cream, Concentrated, Sweetened, Powder, Granules / Other Solids, Not over1.5% Fat;

• Milk & Cream, Concentrated, Sweetened, Powder, Granules / Other Solids, Over1.5% Fat;

• Fats And Oils Derived From Milk, Nesoi;

• Peas, Dried Shelled, Including Seed;

• Kidney Beans & White Pea Beans, Dried Shelled, Including Seed;

• Beans Nesoi, Dried Shelled, Including Seed;

• Leguminous Vegetables Nesoi, Dried Shell, Including Seed;

• Nuts Nesoi, Fresh Or Dried, Shelled Or Not;

• Pears And Quinces, Fresh;

• Ginger;

• Poppy Seeds, Whether Or Not Broken;

• Natural Gums, Gum Resins, Resins And Balsams Nesoi;

• Cocoa Paste, Not Defatted;

• Cocoa Powder, Not Sweetened;

• Nonalcoholic Beverages, Nesoi;

• Ethyl Alcohol & Other Spirits Denatured Any Strength;

• Wool, Not Carded Or Combed, Greasy, Nesoi;

• Wool Not Carded / Combed Degreased Not Carbonized, Shorn.

1

OPPORTUNITIES IN THE FOOD MARKETS OFINDIA

I. PURPOSEThe purpose of this paper is to provide Canadian food exporters with indications of

opportunities or “contestable markets” in India. The analysis uses several indicators ofcontestability and ranks product groups according to the number of positive indicators associatedwith each.

The paper provides indications only. Individual companies should follow up on opportunitiesof interest with: further market research, including the determination of quality and packaging ofcompeting products; acquisition of information on sanitary/phyto-sanitary and labelling requirements; the development of a research price work-up; other barriers to trade and;eventually a specific price work-up.

The indicators of contestability used in this paper are based on historical statistics andtherefore assume Indian tastes and preferences are fixed. It also assumes that the images thatIndian consumers have of Canada and Canadian products are fixed and not always positiverelative to the images of competing products. The Branding Strategy for the CanadianAgriculture and Food Sector1 is designed to improve knowledge of Canadian products and foodsystems, to differentiate Canada from its competitors and establish a reputation for high quality.This program can have a major positive influence on Indian acceptance of Canadian foodproducts and increase the probabilities of finding opportunities in Indian markets.

II. BUSINESS PARADIGMSThere are several ways in which Canadian companies can participate in the food markets of

India. Some understanding of the competitive nature of the Indian food markets is necessary forCanadian companies to decide on the appropriate paradigm for them.

A. The Competitive EnvironmentIn 2010, the packaged food market was dominated by multinational companies local

manufacturers and government cooperatives. There was also a thriving unorganised sectorconsisting of many small entities. The market was highly competitive and fragmented. Even thelarge multinationals had to fight hard to maintain market positions. However, over the period2005 to 2010, the market has become slightly more concentrated. The top 10 food companiesproducing impulse and indulgence products accounted 68 percent of the market in 2005 and 73percent in 2009. Similarly, the top 10 food companies producing nutrition products / staplesaccounted for 38 percent of the market in 2005 and 41 percent in 2009. To compete in thisenvironment companies continuously reviewed product innovations as well as marketing andcommunication strategies. As the rural areas became increasingly important, companies engaged

2

in various promotional offers. Smaller packs at low prices were key to growth in sales of suchproducts as bakery products, soup, noodles, and confectionery products.

B. Pure ExportThe paradigm assumed in this paper is characterised by production in Canada by Canadian

companies with sea or air transport to India by any available carrier. Canadian companiesnormally cease to be interested in a shipment when it is loaded onto a ship or plane and paymentis received. Wholesaling, distributing and retailing is done by Indian companies at their risk.With this paradigm the emphasis is on identifying products that Canadian companies canprofitably export and Indian companies can profitably import from Canada and finding thoseIndian buyers.

C. Export with AgreementsThis paradigm is much the same as pure export except that Canadian companies enter into

various kinds of agreements with Indian companies to perform any one or more marketingfunctions such as wholesaling, storage, distributing, advertising and/or retailing.

D. Multi-National OperationsThis paradigm includes a mix of local (in India) production and imports. It might also

includes the performance of marketing functions throughout the marketing channel. Multi-nationals operate as if there were no borders, placing production plants in the most economicposition in relation to sources of inputs and the markets to be served. Tariffs and other tradebarriers are costs of doing business and influence the placement of production plants based onlyon economic and financial considerations. With barriers to trade falling, these companies are inthe best position to adjust and benefit from the comparative advantages of many countries.

Some multi-national companies active in India were 2:

Cadbury India Ltd. is a part of Kraft Foods of the USA. The company is involve in theproduction of chocolate confectionery, beverages, biscuits, gum and candy.

Frito-Lay India is a owned by PepsiCo Inc. of the USA. The company produces confectioneryproducts, specifically potato chips.

Perfetti Van Melle India Pvt Ltd is based in Europe. In India the company is involved in theproduction of gums, candies and chewies.

Nestle India Ltd is a subsidiary of Nestle SA of Switzerland. The company is involved in theproduction of milk products & nutrition, beverages, prepared dishes & cooking aids andchocolate & confectionery.

3

GlaxoSmithKline Consumer Healthcare Ltd is an associate of GlaxoSmithKline plc of theUK. It manufactures and distributes hot drinks and OTC healthcare products.

III. PROFILE OF INDIAA. GeographyIndia is located in Southern Asia with the Arabian sea to the west, the Bay of Bengal to the

east and the Indian Ocean to the south. On the north-west it is bordered by Pakistan, on the northby China, Nepal, and Bhutan. On the northeast, it is bordered by Bangladesh and Myanmar. Withan area of 3,287,590 Km2 3, it is almost one-third the size of Canada.

India can be divided into three main regions: the Himalayan Mountains, the Gangetic Plain,and Peninsular India.

1. The Himalayan MountainsThe Himalayan mountain system is 160 to 320 km wide and extends 2,400 km along the

northern and eastern borders of India. It includes the mountains surrounding the Vale of Kashmirin the Karakoram Range, and the central and eastern Himalayas. Ancient geological forcesmoulded the Himalayas as the Indian plate of the Earth’s crust subducted under the Eurasianlandmass, creating an uplift that continues to push this northernmost boundary of India everhigher.

The Himalayan Range is the highest mountain system in the world. Among its summits,wholly or partly within India or within territory claimed by India and administered by Pakistan,are K2 (8,611 m) and Kanchenjunga (8,598 m), which are the second and third highest peaks inthe world, after Mount Everest. Other prominent Indian peaks include Nanga Parbat (8,125 m),Nanda Devi (7,817 m), Rakaposhi (7,788 m), and Kamet peak (7,756 m). The Himalayan region,including the foothills, is sparsely settled. Agriculture and animal herding are the main economicactivities.

2. The Gangetic PlainSouth of, and parallel to, the Himalayas, lies the Gangetic Plain, a belt of flat, alluvial

lowlands 280 to 400 km wide. This area includes some of the most agriculturally productive landin India. The Indian portion of the broad Gangetic Plain encompasses several river systems, andstretches from Punjab state in the west to the Assam Valley in the east. Marking the western endof the Gangetic Plain are the Indus River and its tributaries, including the Sutlej and Chenabrivers, which flow through Punjab in India’s northwest corner. The Gangetic Plain is formed bythe Ganges River and its tributaries, which drain the southern slopes of the Himalayas. TheAssam Valley is separated from the Gangetic Plain by a narrow corridor of land near the city ofDarjeeling. The valley is watered by the Brahmaputra River, which rises in Tibet and crosses intoIndia at its northeast corner, then flows north of the Khasi Hills into Bangladesh. The Thar

4

Desert, a huge, dry, sandy region extending into Pakistan, lies at the southwestern end of theGangetic Plain.

3. Peninsular IndiaSouth of the plains region lies Peninsular India. The northern peninsula features a series of

mountain ranges and plateaus. The Aravalli Range runs in a north-south direction on the easternedge of the Thar Desert, and low hills cut by valleys lie along the border between the states ofUttar Pradesh and Madhya Pradesh in central India. The Narmada River flows southwestbetween the Vindhya Range and an associated plateau on the north, and the Satpura Range on thesouth. The plains of the Chota Nagpur Plateau in the eastern states of Chhattisgarh and Jharkhandalso lie within this region. The rocky and uneven lands of the northern peninsula are sparselypopulated. Herding is a major occupation in the west, and farming of coarse grains such as milletis common in the central part.

In the southern part of peninsular India lies the vast Deccan Plateau, a tableland lying withina triangle formed by the Satpura Range, the steep mountain slopes of the Western Ghats, and thegentler slopes of the Eastern Ghats. Elevations in the plateau region average 600 m, althoughoutcroppings as high as 1,200 m occur. At their northern end, the Western Ghats vary in heightfrom 900 to 1,200 m, but the Nilgiri Hills of the extreme south reach a height of 2,637 m at DodaBetta, their highest peak. The Eastern Ghats lie along the eastern flank of the Deccan Plateau,interrupted by the Krishna and Godavari river basins. Elevations of the Eastern Ghats are muchlower, averaging 600 m. The plateau itself, even rockier than the northern extension of peninsularIndia, supports a sparse agricultural population and is also home to industrial enterprises.

The Indian Peninsula is bordered by a mostly fertile seashore. The west coast, including theextensive Gujarat Plain in the north, the thin Konkan shore in Maharashtra state, and the MalabarCoast in the south, support substantial populations of farmers and fishermen. Ancient traderoutes to the west helped make the cities and towns of this region into market centers for textilesand spices. The east coast’s broad alluvial plains, stretching from the Kaveri River delta in thesouth to the Mahanadi River delta in the north, are intensely farmed.4

B. Demography The population of India was estimated to be 1,205,074,000 (2012). A compound trend line

fitted to the population data from 1992 to 2012 indicates an annual rate of increase of 1.64%. SeeTable 13.

The age/gender distribution of the population is presented in the population pyramid ofFigure 1. The largest age groups were between 0 and 19 years of age. The younger age groupswere almost the same size, indicating a reduction in the rate of growth of the population (from1.72% between 1999/2000 to 1.34% between 2011/2012).

5

Figure 1. Population Pyramid. India. 2012.

Source: Data from US B ureau of Census.

International Data Base.

C. Culture1. History

Many cultures have come together toinfluence the India of today. Indian historycan be traced back to 3000 - 2500 BC. Areader interested in the details of Indianhistory can access the website:http://www.sscnet.ucla.edu/southasia/History/mainhist.html 5. More recent events will bediscussed in section “F” Economic.

2. Fooda) Traditional

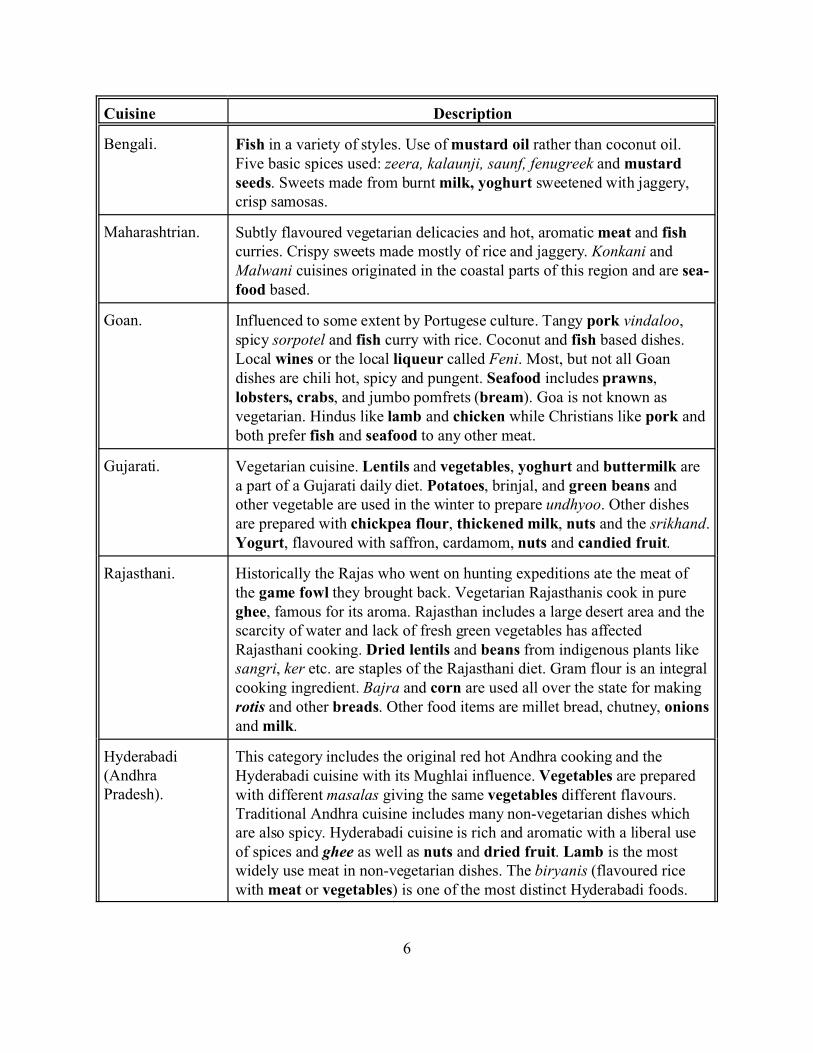

There is no single traditional cuisine ofIndia. The many cultures that have come toIndia over the centuries have contributed theirflavours and recipes using the basic productsavailable locally. A sampling of traditionalIndian cuisines and the products that might bysupplied by Canada is presented in Table 1.

Table 1. Selected Traditional Cuisines of India.

Cuisine Description

Kashmiri. Largely meat based, particularly lamb, goat and chicken flavoured withsaffron and chillies. Other products include walnuts, dried dates andapricots used in puddings, curries and snacks. Cottage cheese is popularwith meats and vegetables. Fresh water fish is also a delicacy. Populardesserts consist of fresh fruits such as strawberries, plums, cherries andapples.

Punjabi. Marinated chicken, fish, paneer, rotis and naans of many types arecooked in earthen ovens half buried in the ground. In the winter, makki kiroti (maize flour bread) is popular along with sarson ka saag (mustardleaf gravy). Fresh curd and white butter are consumed in large quantities.A popular drink is lassi (a sweet or salted drink made with curd). Otherpopular dishes are ma ki dal, rajma (kidney beans) and stuffed parathas.

Mughlai (Delhi). Rich sauces, butter-based curries, ginger flavoured roast meats anddelicious sweets.

Cuisine Description

6

Bengali. Fish in a variety of styles. Use of mustard oil rather than coconut oil.Five basic spices used: zeera, kalaunji, saunf, fenugreek and mustardseeds. Sweets made from burnt milk, yoghurt sweetened with jaggery,crisp samosas.

Maharashtrian. Subtly flavoured vegetarian delicacies and hot, aromatic meat and fishcurries. Crispy sweets made mostly of rice and jaggery. Konkani andMalwani cuisines originated in the coastal parts of this region and are sea-food based.

Goan. Influenced to some extent by Portugese culture. Tangy pork vindaloo,spicy sorpotel and fish curry with rice. Coconut and fish based dishes.Local wines or the local liqueur called Feni. Most, but not all Goandishes are chili hot, spicy and pungent. Seafood includes prawns,lobsters, crabs, and jumbo pomfrets (bream). Goa is not known asvegetarian. Hindus like lamb and chicken while Christians like pork andboth prefer fish and seafood to any other meat.

Gujarati. Vegetarian cuisine. Lentils and vegetables, yoghurt and buttermilk area part of a Gujarati daily diet. Potatoes, brinjal, and green beans andother vegetable are used in the winter to prepare undhyoo. Other dishesare prepared with chickpea flour, thickened milk, nuts and the srikhand.Yogurt, flavoured with saffron, cardamom, nuts and candied fruit.

Rajasthani. Historically the Rajas who went on hunting expeditions ate the meat ofthe game fowl they brought back. Vegetarian Rajasthanis cook in pureghee, famous for its aroma. Rajasthan includes a large desert area and thescarcity of water and lack of fresh green vegetables has affectedRajasthani cooking. Dried lentils and beans from indigenous plants likesangri, ker etc. are staples of the Rajasthani diet. Gram flour is an integralcooking ingredient. Bajra and corn are used all over the state for makingrotis and other breads. Other food items are millet bread, chutney, onionsand milk.

Hyderabadi(AndhraPradesh).

This category includes the original red hot Andhra cooking and theHyderabadi cuisine with its Mughlai influence. Vegetables are preparedwith different masalas giving the same vegetables different flavours.Traditional Andhra cuisine includes many non-vegetarian dishes whichare also spicy. Hyderabadi cuisine is rich and aromatic with a liberal useof spices and ghee as well as nuts and dried fruit. Lamb is the mostwidely use meat in non-vegetarian dishes. The biryanis (flavoured ricewith meat or vegetables) is one of the most distinct Hyderabadi foods.

Cuisine Description

7

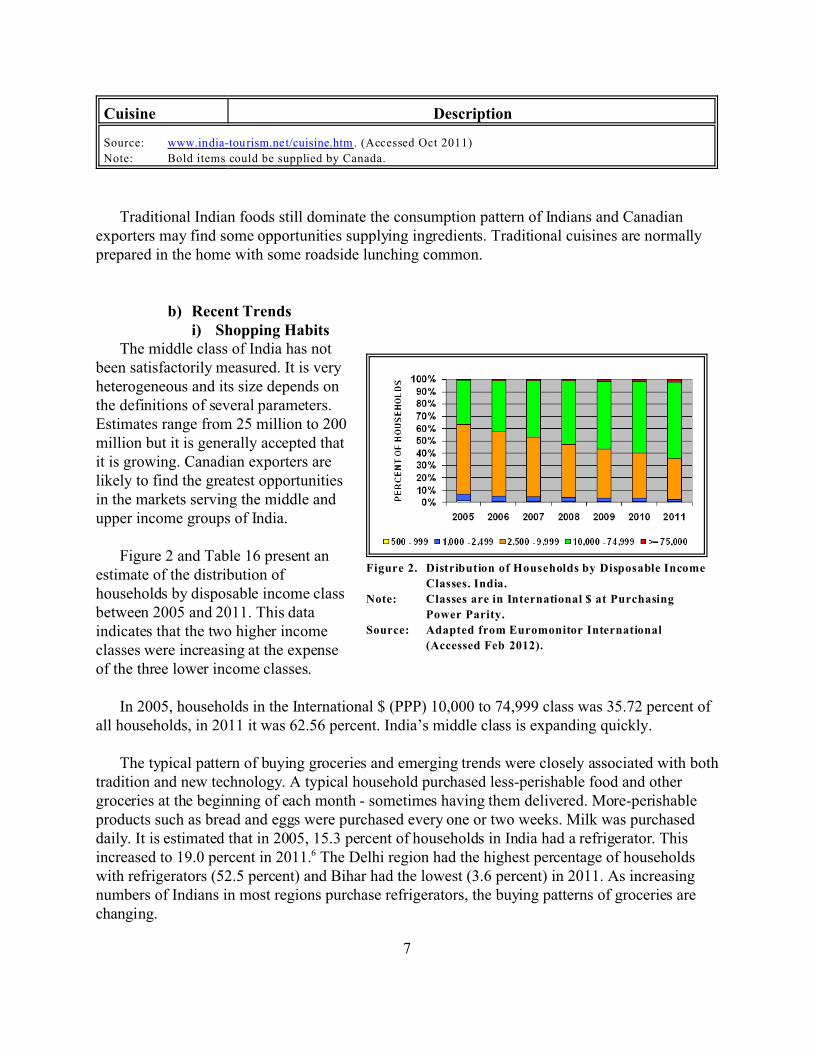

Figure 2. Distribution of Households by Disposable Income

Classes. India.

Note: Classes are in International $ at Purchasing

Power Parity.

Source: Adapted from Euromonitor International

(Accessed Feb 2012).

Source: www.india-tourism.net/cuisine.htm. (Accessed Oct 2011)

Note: Bold items could be supplied by Canada.

Traditional Indian foods still dominate the consumption pattern of Indians and Canadianexporters may find some opportunities supplying ingredients. Traditional cuisines are normallyprepared in the home with some roadside lunching common.

b) Recent Trendsi) Shopping Habits

The middle class of India has notbeen satisfactorily measured. It is veryheterogeneous and its size depends onthe definitions of several parameters.Estimates range from 25 million to 200million but it is generally accepted thatit is growing. Canadian exporters arelikely to find the greatest opportunitiesin the markets serving the middle andupper income groups of India.

Figure 2 and Table 16 present anestimate of the distribution ofhouseholds by disposable income classbetween 2005 and 2011. This dataindicates that the two higher incomeclasses were increasing at the expenseof the three lower income classes.

In 2005, households in the International $ (PPP) 10,000 to 74,999 class was 35.72 percent ofall households, in 2011 it was 62.56 percent. India’s middle class is expanding quickly.

The typical pattern of buying groceries and emerging trends were closely associated with bothtradition and new technology. A typical household purchased less-perishable food and othergroceries at the beginning of each month - sometimes having them delivered. More-perishableproducts such as bread and eggs were purchased every one or two weeks. Milk was purchaseddaily. It is estimated that in 2005, 15.3 percent of households in India had a refrigerator. Thisincreased to 19.0 percent in 2011.6 The Delhi region had the highest percentage of householdswith refrigerators (52.5 percent) and Bihar had the lowest (3.6 percent) in 2011. As increasingnumbers of Indians in most regions purchase refrigerators, the buying patterns of groceries arechanging.

8

Figure 3. Proportion of Packaged Food Sales by

Distribution Format. India.

Source: Adapted from Euromonitor International

(Accessed Oct 2011).

Small grocery stores were thedominant single food outlets but fruit andvegetables were bought from unorganizedvendors. Some grocery chains wereexpanding into the supermarket orhypermarket category offering a widerange of products; however, the purchaseof fruit and vegetables in this format wasnot yet fully accepted. Even so,supermarkets and hypermarkets wereputting pressure on the traditional grocerystore. Visits to a supermarket encouragedmore impulse buying than did visits to atraditional grocery store or phoneshopping.

Small grocery stores dominated thesales of packaged food but were being pressured by supermarkets and hypermarkets, particularlyin urban areas. In 2005, 57.4 percent of packaged food was sold through small grocery stores; in2010 the proportion was down to 51.7 percent. During the same period, sales throughsupermarkets/hypermarkets increased from 6.9 percent to 11.4 percent. See Figure 3.

Eating out was a very popular activity while attending other functions. It is estimated thatIndians spent INR 350 billion (approx. CAD 10.5 billion) eating out annually. Of this, organizedestablishments accounted for only INR 20 billion (CAD 0.6 billion). International fast foodchains such as Subway, McDonald’s and Pizza Hut were found in shopping malls and nearcinema theatres.

The “well-off” in urban areas were increasingly eating out in coffee shops, malls or retailstores. Lounge bars were the latest trend in urban areas and were frequented by youngprofessionals, successful executives and single women in their late 20's. This trend began inMumbai, Bangalore, Delhi and Kolkata and will no doubt spread to other urban areas.

Among the “affluent”, clubs were becoming popular. In addition to many recreationalfacilities they were upgrading their food facilities and were competing with some of the finestrestaurants or hotels of India. The “affluent” also had an interest in the performing arts. A play inMumbai could cost about INR 1,000 (approx. CAD 23) which was beyond the reach of mostIndians.

9

Middle to upper income families were increasingly two income, younger families. A smallproportion of Indian families were moving to quick ready-to-eat foods and frozen foods.However 90% of the population still prefered fresh foods and considered processed foods to benot fresh and containing harmful preservatives.

Table 2 presents estimates of the consumption of both regular and“health and wellness” packaged and processed food and beverages. In 2011, baked goods was the regular food categorywith the highest level of consumption (1,994.1 gm per person). Still bottled water was thebeverage category with the highest level of consumption (4,291.4 ml per person). Between 2006and 2011 chips / crisps and breakfast cereals were the fastest growing food categories.Consumption increased at a rate of 25.4 percent per year reaching 73.2 gm per person of chips /crisps and 24.7 gm per person of breakfast cereals, in 2011.

India has one of the fastest growing economies in the world. Rising incomes and a morehectic lifestyle have increased the incidence of the health problems of the affluent (obesity,diabetes, hypertension and heart trouble). This has increased consumer interest in “health andwellness” products. In 2011, “health and wellness” bakery products had the highest level ofconsumption ( 479 gm per person). The fastest growing “health and wellness” category wassnack bars. Consumption increased at a rate of 53.3 percent per year reaching a still small levelof 1.5 gm per person.

Table 2. Estimated Consumption of Packaged and Processed FoodProducts. India. 2006 and 2011.

Product 2006 2011 Change2006 to 2010(% / Year)

REGULAR PR ODUCTS

100% Juice (ml./person). 10.6 29.7 22.1

Baked G oods (gms./person). 1,801.2 1,994.1 2.2

Biscuits (gms./person). 818 .2 1,344.7 10.3

Breakfast Cereals

(gms./person).

8.2 24.7 25.4

Butter (gms./person). 34.8 40.1 2.6

Canned Meat and Meat

Products (gms./person).

0.2 0.3 11.0

Canned Vegetables

(gms./person).

0.9 1.3 7.3

Chips /Crisps (gms./person). 24.2 73.2 25.4

Product 2006 2011 Change2006 to 2010(% / Year)

10

Chocolate Confectionery

(gms./person).

35.4 79.3 17.2

Dehydrated Soup

(gms./person).

1.3 3.0 18.3

Dried Baby Food

(gms./person).

16.9 19.3 2.6

Dried Pasta (gms./person). 0.9 1.6 12.3

Extruded Snacks (gms./person). 24.1 59.4 19.4

Frozen Processed Fish/Seafood

(gms./person).

0.6 0.9 8.7

Honey (gms./person). 6.0 9.1 8.8

Instant Noodles (gms./person). 64.5 168 .5 21.3

Juice Drinks (up to 24% Juice)

(ml./person).

188 .9 478 .5 21.0

Ketchup (gms./person). 16.7 33.5 14.8

Nectars (25-99% Juice)

(ml./person).

41.9 110 .7 20.8

Nuts (gms./person). 3.1 4.0 5.1

Other Sweet and Savoury

Snacks (gms./person).

46.7 135 .0 24.3

Still Bottled Water

(ml./person).

1,632.2 4,291.4 21.0

Sugar Confectionery

(gms./person).

96.2 142 .6 8.2

Take-Home Ice Cream

(ml./person).

28.9 64.6 17.2

Vegetable and Seed Oils

(gms./person).

1,042.9 1,565.2 8.6

HEALTH AND WELLNESS PRODUCTS

Bakery Products (gms./person). 363 .9 479 .8 5.3

Noodles (gms./person). 3.1 12.2 31.5

Product 2006 2011 Change2006 to 2010(% / Year)

11

Sauces, Dressings and

Condiments (gms./person).

1.1 2.7 20.4

Snack Bars (gms./person). 0.2 1.5 53.3

Soft Drinks (ml./person). 40.9 76.1 13.4

Source: Euromonitor International from trade sources / national statistics. (Accessed Jan

2012)

ii) Health and WellnessHealth and wellness products are identified and classified as: organic, fortified/functional

(FF), better for you (BFY), naturally healthy (NH) and food intolerance. The largestclassification, by value of sales was BFY. Between 2005 and 2010, the value of sales of BFYproducts was increasing at a rate of 115.67 percent per year reaching CAD 4,235.1 million in2010. See Table 3.

Table 3. Value of Sales of Health and Wellness Classifications. India.

YearCAD per INR

Organic

(Million

CAD)

Fortified

/ Functional

(Million

CAD)

Better for

You

(Million

CAD)

Naturally

Healthy

(Million

CAD)

Food

Intolerance

(Million

CAD)

Total

(Million

CAD)

2005 0.027516 16.3 1,601.3 2,064.6 328 .9 3.2 4,014.3

2006 0.025117 18.0 1,611.8 2,347.7 349 .3 3.2 4,330.0

2007 0.026042 22.1 1,851.8 3,062.7 423 .1 3.6 5,363.4

2008 0.024576 24.8 1,996.6 3,356.7 471 .7 3.6 5,853.5

2009 0.023591 29.0 2,100.9 3,758.0 536 .3 3.7 6,428.1

2010 0.022556 35.7 2,258.0 4,235.1 605 .3 4.0 7,138.1

Annual

Change

-3.48% 16.94% 7.68% 15.67% 13.54% 4.74% 12.59%

Sources: Adapted from Euromonitor International, “Health and Wellness - India”. Nov 2011. (Accessed Jan

2012).

Pacific Exchange Rate Service.

In Regard to Health and Wellness Products:• Sales were expanding due to increasing number of products and targeting of lower-

income groups;• Sales were based on consumer demand for products with additional benefits and nutrients

12

such as proteins, vitamins and minerals and more recently omega-3 oil. Also the demandfor naturally healthy foods such as green tea and 100% juices;

• Production was dominated by small domestic companies serving small local nichemarkets. There were also a number of larger domestic companies specializing inparticular subsectors for example Hindustan Lever Ltd. lead in reduced fat soup, NestleIndia lead in high fibre noodles and GlaxoSmithKline Consumer Healthcare specializedin fortified/functional hot drinks;

• They were marketed through supermarkets and as these outlets become increasinglypopular so do health and wellness products.

3. Religions and PhilosophiesTable 4 presents a list of the major religions and philosophies of India and a brief indication

of their food preferences. Vegetarianism is often strongly associated with India and severalreligions do include it as one if their requirements. However, many Indians eat meat of some kindaccording to what their religion allows and others do not adhere strictly to food rules. There aremarkets in India for meat products.

Table 4. Religions and Philosophies of India - Food Preferences.

Religion /Philosophy

Percent ofPopulation

(%)

Brief Indication of Food Preferences

Hindu. 80.4 Do not eat beef of any kind but will eat other meats.

Devout H indus are vegetarians and do not eat meat at all.

This derives from the concept of Ahimsa or non-violence

to anything.

Islam. 13.4 Do not eat pork or drink alcohol. Strict Islamists will eat

only according to the rules of Halal and Haram. See:

http://www.eat-halal.com/halal.shtml (Apr 2006. Under

reconstruction Jan 2012) and

http://www.eat-halal.com/haram.shtml (Apr 2006. Under

reconstruction Jan 2012).

Christian. 2.2 Few or no food restrictions based on religion. Strict Roman

Catholics may eat fish on Fridays. Individuals may have

personal aversions to some foods.

Sikh. 1.9 Few food restrictions. There are some restrictions

regarding preparation. A strict Sikh will not drink alcohol.

Buddhist. 1.1 Food rules vary considerably. Some are vegetarian. The

eater of meat must believe that the animal was not killed

specifically to be eaten.

Religion /Philosophy

Percent ofPopulation

(%)

Brief Indication of Food Preferences

13

Jain. 0.4 Strictly vegetarian and some vegetables are forbidden. In

recent years the rules have not been strictly adhered to.

Other.* 0.5

Source: http://www.nationmaster.com/encyclopedia/demographics-of-India. (Accessed Oct

2011).

Punjab for Health-Care Workers. See

http://www.hospitalconnect.com/healthcareworkforce/content/PunjabiforHealthCare

Workers.pdf (Accessed Oct 2011).

* Jews, Parsis, Bahais, tribal animists and non-religous.

D. Trade1. Data Sources and Valuations

In this and following sections, trade data is presented and analysed. Unless otherwiseindicated, all trade data has been obtained from the Global Trade Atlas, a product of:

Global Trade Information Services, Inc. -GTI-2218 Devine StreetColumbia, SC 29205USATel: (803) 765-1860Fax: (803) 799-5589E-Mail: [email protected].

The data reported for India is supplied to GTI by the Indian Ministry of Commerce and isevaluated CIF for imports and FOB for exports. At the time of the analysis, data for 2010 is thelatest full year available.

CIF (Cost, Insurance and Freight): The landed value of merchandise at the firstport of arrival in the importing country. It is computed by adding “ImportCharges” to the “Customs Value” and therefore excludes import duties.

FOB (Free On Board): The value of exports as they are moved onto the ship at theport of export. The buyer bears all costs and risks of loss of or damage to thegoods from that point. The FOB term requires the seller to clear the goods forexport. This term is used only for sea or inland waterway transport. For othermodes of transport the FCA (Free Carrier) term should be used.

14

2. CurrenciesCurrency designations used in this paper are the ISO 4217 codes. Specifically:

Canadian Dollar . . . . CAD;Indian Rupee . . . . . . . INR;United States Dollar . USD.

For a complete list of the ISO currency codes see the website: www.xe.com/iso4217.htm. (Nov2011).

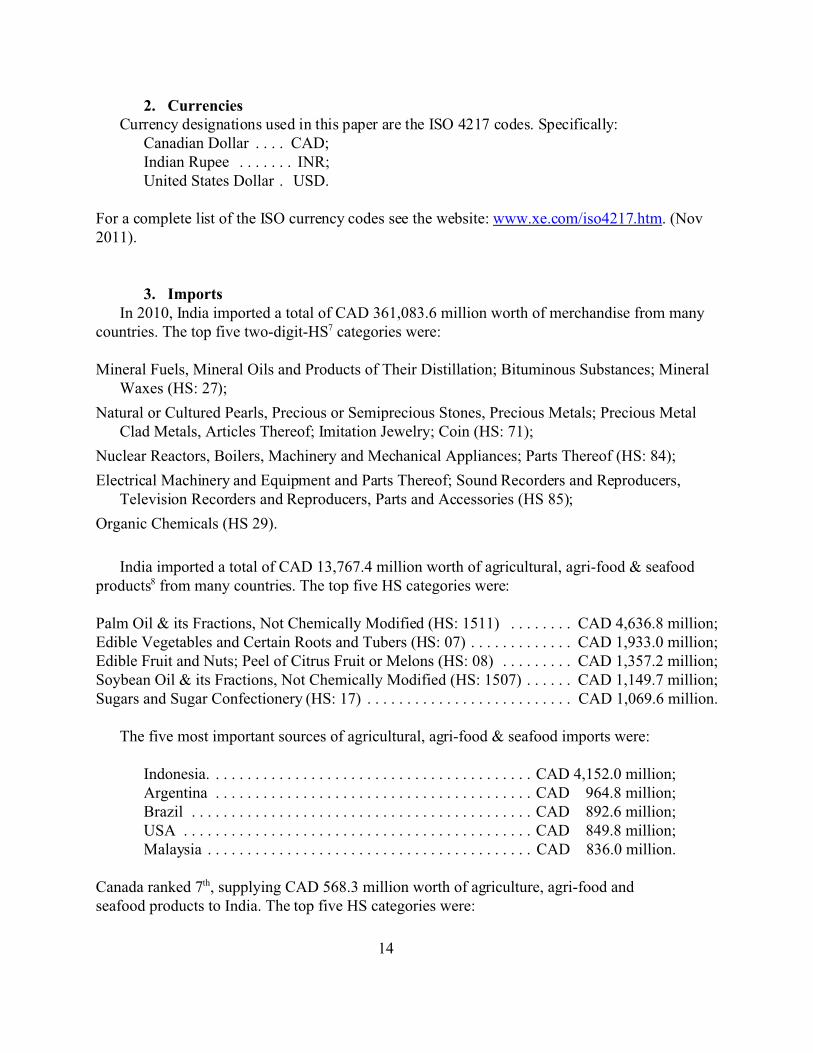

3. Imports In 2010, India imported a total of CAD 361,083.6 million worth of merchandise from many

countries. The top five two-digit-HS7 categories were:

Mineral Fuels, Mineral Oils and Products of Their Distillation; Bituminous Substances; MineralWaxes (HS: 27);

Natural or Cultured Pearls, Precious or Semiprecious Stones, Precious Metals; Precious MetalClad Metals, Articles Thereof; Imitation Jewelry; Coin (HS: 71);

Nuclear Reactors, Boilers, Machinery and Mechanical Appliances; Parts Thereof (HS: 84);

Electrical Machinery and Equipment and Parts Thereof; Sound Recorders and Reproducers,Television Recorders and Reproducers, Parts and Accessories (HS 85);

Organic Chemicals (HS 29).

India imported a total of CAD 13,767.4 million worth of agricultural, agri-food & seafoodproducts8 from many countries. The top five HS categories were:

Palm Oil & its Fractions, Not Chemically Modified (HS: 1511) . . . . . . . . CAD 4,636.8 million;Edible Vegetables and Certain Roots and Tubers (HS: 07) . . . . . . . . . . . . . CAD 1,933.0 million;Edible Fruit and Nuts; Peel of Citrus Fruit or Melons (HS: 08) . . . . . . . . . CAD 1,357.2 million;Soybean Oil & its Fractions, Not Chemically Modified (HS: 1507) . . . . . . CAD 1,149.7 million;Sugars and Sugar Confectionery (HS: 17) . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 1,069.6 million.

The five most important sources of agricultural, agri-food & seafood imports were:

Indonesia. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 4,152.0 million;Argentina . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 964.8 million;Brazil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 892.6 million;USA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 849.8 million;Malaysia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 836.0 million.

Canada ranked 7th, supplying CAD 568.3 million worth of agriculture, agri-food andseafood products to India. The top five HS categories were:

15

Edible Vegetables and Certain Roots and Tubers (HS: 07) . . . . . . . . . CAD 557.2 million;Sugars and Sugar Confectionery (HS: 17) . . . . . . . . . . . . . . . . . . . . . . CAD 2.7 million;Residues and Waste from the Food Industries; Prepared Animal

Feed (Fodder) (HS: 23) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 2.7 million;Miscellaneous Edible Preparations (HS: 21) . . . . . . . . . . . . . . . . . . . . CAD 1.3 million;Cocoa and Cocoa Preparations (HS: 18) . . . . . . . . . . . . . . . . . . . . . . . . CAD 751,000.

4. Exports In 2010, India exported a total of CAD 229,277.5 million worth of merchandise to

many countries. The top five two-digit-HS categories were:

Mineral Fuels, Mineral Oils and Products of Their Distillation; Bituminous Substances;Mineral Waxes (HS: 27);

Natural or Cultured Pearls, Precious or Semiprecious Stones, Precious Metals; PreciousMetal Clad Metals, Articles Thereof; Imitation Jewelry; Coin (HS: 71);

Vehicles, Other than Railway or Tramway Rolling Stock, and Parts and Accessories Thereof (HS: 87);

Electrical Machinery and Equipment and Parts Thereof; Sound Recorders andReproducers, Television Recorders and Reproducers, Parts and Accessories (HS: 85);

Organic Chemicals (HS: 29).

India exported a total of CAD 23,208.1 million worth of agricultural, agri-food &seafood products. The top five HS categories were:

Cotton, not Carded or Combed (HS: 5201) . . . . . . . . . . . . . . . . . . . . CAD 3,059.4 million;Cereals (HS: 10) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 3,012.5 million;Fish and Crustaceans, Molluscs and Other Aquatic Invertebrates

(HS: 03) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 2,231.4 million;Residues and Waste from the Food Industries; Prepared Animal

Feed (HS: 23) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 2,130.1 million;Coffee, Tea, Mate and Spices (HS: 09). . . . . . . . . . . . . . . . . . . . . . . CAD 2,064.8 million.

The five most important markets for India’s agricultural, agri-food & seafood exportswere:

China . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 2,704.1 million;USA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 1,656.5 million;United Arab Emirates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 1,621.7 million;Pakistan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 1,258.9 million;

16

Vietnam . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 1,211.7 million.

Canada ranked 32nd, taking CAD 167.8 million worth of India’s agri-food and seafood exports.The top five HS categories were:

Fish and Crustaceans, Molluscs and Other Aquatic Invertebrates (HS: 03) . . . CAD 44.8 million;Coffee, Tea, Mate and Spices. (HS: 09) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 25.1 million;Cereals (HS: 10) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . CAD 18.1 million;Preparations of Vegetables, Fruit, Nuts or Other Parts of Plants (HS: 20) . . . . CAD 15.2 million;Oil Seeds and Oleaginous Fruits; Miscellaneous Grains, Seeds, and Fruit;

Industrial or Medicinal Plants; Straw and Fodder (HS: 12) . . . . . . . . . . . . . CAD 11.4 million.

E. International Transportation - Canada to India1. Ocean

A number of shipping companies provide container services from Vancouver BC and HalifaxNS to India, either direct or with transshipments. Exporters may contact a freight forwarder toarrange shipping and transshipping. Coordinates of freight forwarders may be found in thetelephone directories of most cities and at the following website: www.superpages.ca (Nov 2011).

A list of shipping companies serving Vancouver is available at the website:http://portmetrovancouver.com/en/users/landoperations/terminalsandfacilities/container/containercarriersandberthschedule.aspx. (Nov 2011).

Cosco shipping line serves the Port of Prince Rupert, B.C. See website:http://www.cosco-usa.com/fpdb/Services/schedules.aspx. (Nov 2011). From Prince Rupert, Coscoships primarily to China but transshipments are possible - contact a freight forwarder.

A list of international shipping companies serving Montreal is available at the website:http://www.port-montreal.com/site/3_0/3_2.jsp?lang=en. (Nov 2011).

A list of shipping companies serving Halifax is available at the website:http://www.portofhalifax.ca/english/cargo/sailing-schedule/index.html. (Nov 2011).

2. Air FreightMany airlines serve Canadian airports with international cargo services. For example,

Vancouver International Airport is served by more than 45 air carriers, that accept cargo.

A list of air carriers serving Vancouver International Airport is available at the followingwebsite: http://www.yvr.ca/en/business-at-YVR/cargo/Cargo-Village/Carriers.aspx. (Nov 2011)

A list of freight forwarders serving Vancouver International Airport is available at the

17

following website:http://www.yvr.ca/en/business-at-YVR/cargo/Cargo-Village/Freight-Forwarders.aspx. (Jun 2011).

A list of air carriers and air freight forwarders serving Calgary International Airport isavailable at the following website: http://www.calgaryairport.com/Default.aspx?cid=682&lang=1(Nov 2011).

A list of air carriers and freight forwarders serving Winnipeg International Airport is availableat the following website: http://www.waa.ca/business/cargo/airlines (Nov 2011).

A list of air carriers serving Toronto International Airport is available at the followingwebsite: http://www.torontopearson.com/PearsonContent.aspx?id=903 (Nov 2011).

A list of air carriers serving the airports of Montreal is available at the following website:http://www.admtl.com/Business/Cargo/CarriersAndIntegrators.aspx (Feb 2012).

A list of air carriers and freight forwarders serving Halifax International Airport is available atthe following website: http://www.hiaa.ca/default.asp?mn=70.1.261.286#AirCarriersCargo (Feb2012).

F. Economic1. Historical Development

The Indus Valley civilization dates back at least 5,000 years. Aryan tribes from the northwestinvaded about 1500 BC; their merger with the earlier Dravidian inhabitants created the classicalIndian culture. Arab incursions starting in the 8th century and Turkish in the 12th were followedby those of European traders, beginning in the late 15th century. By the 19th century, Britain hadassumed political control of virtually all Indian lands. Indian armed forces in the British armyplayed a vital role in both World Wars. Nonviolent resistance to British colonialism broughtindependence in 1947. The subcontinent was divided into the secular state of India and the smallerMuslim state of Pakistan - split into East Pakistan and West Pakistan. Wars between India andPakistan resulted in East Pakistan becoming the separate nation of Bangladesh. Despiteimpressive gains in economic investment and output, India faces pressing political and economicproblems such as the ongoing dispute with Pakistan over Kashmir, overpopulation, environmentaldegradation, extensive poverty, and ethnic and religious strife.9

2. Recent ConditionsIndia's diverse economy includes traditional village farming, modern agriculture, handicrafts,

a wide range of modern industries, and a multitude of services. Between Q3 2010 and Q3 2011,India’s GDP increased 6.9 percent (The Economist Jan 21-27, 2012). In 2011, almost 18 percentof the country’s GDP originated in the Agriculture, Hunting and Forestry sectors. See Table 14.

In 2011, 52.9 percent of the population between the ages of 15 and 64 was employed. Of

18

these, 52.8 percent were in the Agriculture, Hunting, Forestry and Fishing sectors, down from56.5 percent in 2006. See Table 15.

Government controls on foreign trade and investment have been reduced for some products,but high tariffs for agricultural and agri-food products remain (averaging 36.04 percent for alldutiable items from all countries). Tariff rates on agricultural and agri-food products that areimported from Canada averages 35.11 percent. The average tariff rates on these products weightedby the value of actual imports was 10.30 percent. See Table 5.

Privatization of government-owned industries has proceeded slowly, and continues to generatepolitical debate. Continued social, political, and economic rigidities hold back needed initiatives.

Table 5. Average Tariff Rates Applied onAgricultural, Agri-food, Fish andSeafood Products, 2008. India.

Source Country/ Region

SimpleAverageTariff by

Tariff Line(%) a

WeightedTariff Rate

(%) b

All Sources 36.04 23.38

NAFTA 36.04 15.34

Canada 35.11 10.30

Australia 12.67

EU 30.05

USA 24.75

China 30.48

Myanmar 10.00

Malaysia 27.37

Ukraine 10.00

Russia 10.38

Source Country/ Region

SimpleAverageTariff by

Tariff Line(%) a

WeightedTariff Rate

(%) b

19

Source: Tariff Analysis Facility of the WTO.

https://tariffanalysis.wto.org/welcome.aspx?Return

Url=%2f (Accessed Nov 2011).

Notes: a Simple Average = Sum of Duties / Number of

Tariff Lines.

b Weighted Average = (Sum of (Tariff Rate *

Import Value)) / Sum of Import Values.

The tariff on all fish and seafood products from all

sources is 30 %.

India is capitalizing on its large number of well-educated people skilled in the Englishlanguage to become a major exporter of software services and software workers. Despite stronggrowth, the World Bank and others worry about the combined state and federal budget deficit.The public debt was 64.2 percent of GDP in 2010 and expected to be 61.9 percent in 2011. Thebudget deficit in 2011 is expected to be 5.4 percent of GDP. The huge and growing population isthe fundamental social, economic, and environmental problem.

3. Determinants of Food DemandQuantitatively, the rate of increase in the effective demand for agricultural, agri-food &

seafood products is influenced by the rates of change of: population, product prices, income perperson / household and income distribution.

Qualitatively, the types of products demanded by consumers are determined by their tastes andpreferences which are in turn influenced by the cultures that make up today’s India and theirknowledge and acceptance of foreign cuisines. Income level also has an important influence onthe level of quality demanded.

Table 6. Determinants of Changes inthe Effective Demand forFood. 2005 to 2011.

Item Value(%)

Population, Annual Change. 1.45

Consumer Price Index, Annual

Change.9.02

Item Value(%)

20

Food and Non- Alcoholic Beverage

Price Index, Annual Change.9.37

Disposable Income per Household

Annual, Change. * 14.40

Number of Households in the

Disposable Income Range Int’l $

(PPP) 10,000 to 74,999, Annual

Change.

11.47

Source: Euromonitor International.

Note: Measured in INRs.

PopulationBetween 2005 and 2011, the Indian population was increasing at a rate of 1.45% per year,

reaching an estimated 1.21 billion people. The rate of increase was moderately rapid compared tosome other countries. This rate of increase and the size were very positive factors in the potentialdemand for food products.

PricesBetween 2005 and 2011, the price index of consumer goods generally were increasing rapidly

at 9.02 percent per year and the price index of food and non-alcoholic beverages was increasingeven faster at 9.37 percent per year. Generally this was a negative factor affecting the effectivedemand for food but may be offset by increases in income

IncomeBetween 2005 and 2011, disposable income per household was increasing at 14.40 percent per

year reaching INR 324,867 per year. This rate of increase was very positive and offset theincreases in prices.

Income DistributionBetween 2005 and 2011, the middle income household group (Int’l $ 10,000 to 74,999), was

increasing at a rate of 11.47 percent per year reaching 143.4 million households in 2011.

The overall national distribution of income was becoming slightly less equitable as the lowerincome groups still make up about 35 percent of households. The level of income inequality isindicated by the Gini ratio10. In 2005 it was calculated as 37.8; by 2011 it had reached 39.9(compared to Canada’s ratio of 38.5 in 2011).

Of all the Indian states/union territories, Bihar had the lowest average Net State Domestic Product(NSDP) per person at CAD 436 in 2011. Goa had the highest NSDP per person at CAD 4,355.

21

4. Consumer Expenditures on Food and Non-Alcoholic Beverages, by PoliticalDivision

Total expenditure on food and non-alcoholic beverages in a political division is influenced bypopulation, income and to some extent the preferences of consumers for food.

Household expenditure on food and non-alcoholic beverages is an average and is not affected bythe size of the population but is influenced by income and preferences.

The proportion of total expenditures allocated to food and non-alcoholic beverages generallydecreases as income increases. This effect may be somewhat softened as consumers withincreasing income demand higher quality, and higher priced, food.

Table 7. Expenditure on Food and Non-alcoholic Beverages in Selected PoliticalDivisions of India.

Political Division

Total Expenditure

on Food & Non-

Alcoholic Beverages

2011

Expenditure per

Household on Food &

Non-Alcoholic Beverages

(CAD)

Proportion of Total

Expenditure Allocated to Food

& Non-Alcoholic Beverages

(%)

CAD

(Million)% 2006 2011 2006 2011

India. 295 ,311 .0 100.00% 955.7 1,287.1 32.52% 26.30%

Andhra Pradesh. 20,686.1 7.00% 843.6 1,071.4 31.72% 26.29%

Bihar. 19,874.3 6.73% 942.8 1,199.5 45.97% 35.03%

Delhi. 6,474.8 2.19% 1,309.4 1,734.9 23.80% 17.74%

Goa. 892 .6 0.30% 2,130.6 2,280.7 24.89% 23.86%

Jammu & Kashmir. 4,123.4 1.40% 1,400.7 1,942.4 34.08% 28.91%

Maharashtra. 30,548.7 10.34% 982.0 1,334.8 27.98% 21.61%

Mizoram. 440 .7 0.15% 1,539.8 2,028.1 33.57% 21.96%

Orissa. 8,558.8 2.90% 761.1 966 .9 41.11% 33.93%

Punjab. 8,405.7 2.85% 1,300.5 1,675.6 27.59% 22.00%

Sikkim. 180 .8 0.06% 1,040.0 1,388.8 34.43% 28.09%

Uttar Pradesh. 42,761.3 14.48% 999.3 1,341.1 34.47% 28.13%

West Bengal. 23,569.7 7.98% 946.7 1,277.3 35.47% 30.99%

Source: Based on data from Euromonitor International (Accessed Jan 2012).

22

5. Determinants of Food ImportsMany factors influence the amount of food imported into a country including: total food

demand, productive capacity, exchange rate movements, transportation costs, tariffs and variousnon-tariff trade barriers. The capacity of a country to produce food is in turn influenced by theagricultural and fishery resources it possesses, the levels of technology and the number ofmanagers with modern management skills.

Food DemandBetween 2006 and 2011, the expenditure on food and non-alcoholic beverages, measured in

current INR prices was increasing at a rate of 11.60 percent per year. Measured in CADs it isincreasing at a rate of 7.50 percent per year, reaching CAD 300,752 million in 2011.

Measured at fixed 2011 prices, Indian expenditure on food was increasing at a rate of 1.77percent per year.

On a per household basis, Indian households were increasing expenditure (measured in currentINRs) on food and non-alcoholic beverages at a rate of 9.74 percent per year. In CADs, householdexpenditures on food and non-alcoholic beverages was increasing at a rate of 5.72 percent peryear, reaching CAD 1,311 in 2011.

Productive CapacityTable 8 presents the production data for selected crops. The FAO food balance sheet for India

indicates that in 2007, India was almost self sufficient in wheat and “other pulses” and fully selfsufficient in rice, millet, sorghum and rapeseed & mustardseed. It was not self sufficient in beans,peas and soybean oil. In February 2012, FAO food balance sheets for 2010 were not available

Table 8. Production and AnnualIncreases of Selected Crops,India.

Crop 2004-2010Change(% perYear)

2010Production

(t)

Rice, Paddy. -0.3 120,620,000

Wheat. 2.8 80,710,000

Pulses. 3.3 17,110,000

Millet. -0.8 10,940,000

Sorghum. 0.6 6,980,000

Crop 2004-2010Change(% perYear)

2010Production

(t)

23

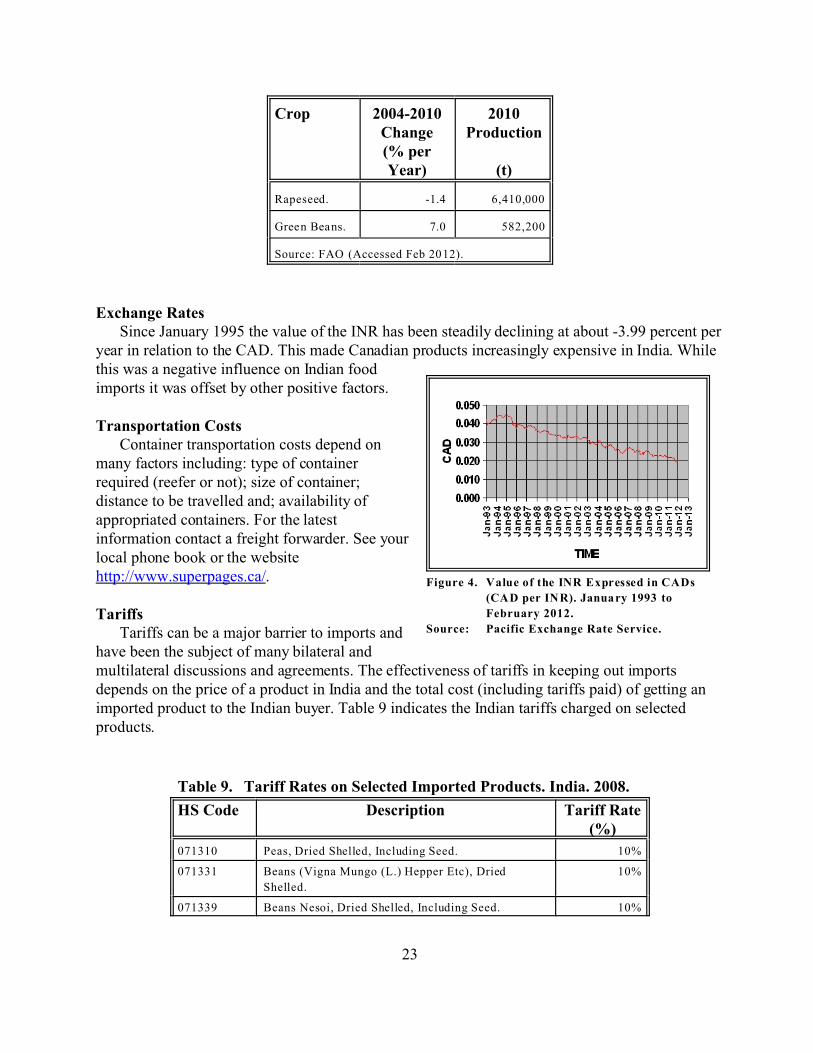

Figure 4. Value of the INR Expressed in CADs

(CAD per INR). January 1993 to

February 2012.

Source: Pacific Exchange Rate Service.

Rapeseed. -1.4 6,410,000

Green Beans. 7.0 582,200

Source: FAO (Accessed Feb 2012).

Exchange RatesSince January 1995 the value of the INR has been steadily declining at about -3.99 percent per

year in relation to the CAD. This made Canadian products increasingly expensive in India. Whilethis was a negative influence on Indian foodimports it was offset by other positive factors.

Transportation CostsContainer transportation costs depend on

many factors including: type of containerrequired (reefer or not); size of container;distance to be travelled and; availability ofappropriated containers. For the latestinformation contact a freight forwarder. See yourlocal phone book or the websitehttp://www.superpages.ca/.

TariffsTariffs can be a major barrier to imports and

have been the subject of many bilateral andmultilateral discussions and agreements. The effectiveness of tariffs in keeping out importsdepends on the price of a product in India and the total cost (including tariffs paid) of getting animported product to the Indian buyer. Table 9 indicates the Indian tariffs charged on selectedproducts.

Table 9. Tariff Rates on Selected Imported Products. India. 2008.

HS Code Description Tariff Rate(%)

071310 Peas, Dried Shelled, Including Seed. 10%

071331 Beans (Vigna Mungo (L.) Hepper Etc), Dried

Shelled.

10%

071339 Beans Nesoi, Dried Shelled, Including Seed. 10%

HS Code Description Tariff Rate(%)

24

071340 Lentils, Dried Shelled, Including Seed. 10%

071390 Leguminous Vegetables Nesoi, Dried Shell,

Including Seed.

10%

080810 Apples, Fresh. 50%

100110 Durum W heat. 50%

150710 Soybean Oil & Fractions, Crude, Whether or Not

Degummed.

0%

151211 Sunflower-seed or Safflower Oil, Crude, and

Fractions Thereof, Etc.

0%

2106901900

2106909900

Food Preparations Nesoi. 90%

2106901901

2106909901

Food Preparations Nesoi Other, Compound

Alcoholic Preparations (Other than Those Based on

Odoriferous Substances) of a Kind Used for

Manufacture of Beverages, of Alcoholic Strength by

Volume Exceeding 0 .5% Volume.

150%

2106901902

2106909902

Food Preparations Nesoi Other [Excluding

Compound Alcoholic Preparations (Other than

Those Based on Odoriferous Substances) of a Kind

Used for M anufacture of B everages, of Alcoholic

Strength by Volume Exceeding 0.5% V olume].

30%

230990 Animal Feed Preparations Except Dog or Cat Food,

Put up for Retail Sale.

30%

510119 Wool, Not Carded or Combed, Greasy, Nesoi. 5%

Source: Tariff Analysis Facility of the WTO.

https://tariffanalysis.wto.org/welcome.aspx?ReturnUrl=%2f (Accessed Nov

2011).

G. The Regions of India1. East & Northeast India

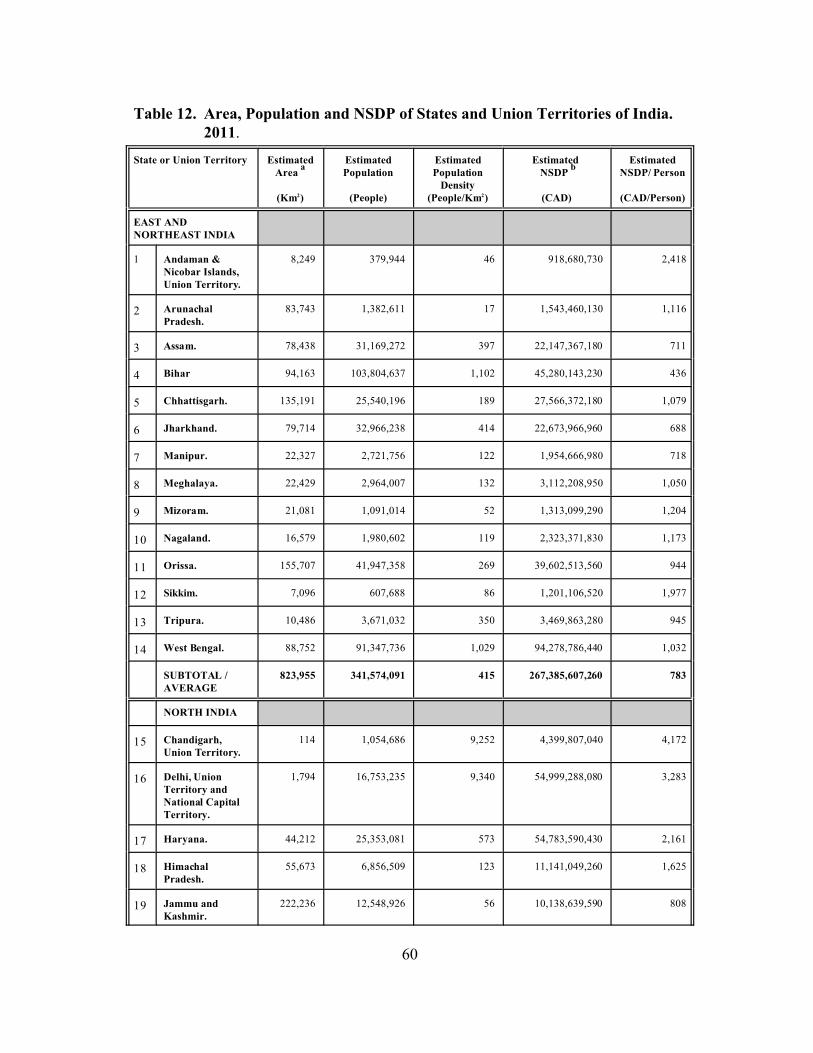

The East & Northeast Region consists of: Andaman & Nicobar Islands; Arunachal Pradesh;Assam; Bihar; Chhattisgarh; Jharkhand; Manipur; Meghalaya; Mizoram; Nagaland; Orissa;Sikkim; Tripura and; West Bengal. In 2011 the region had a population of 341.6 million and anNSDP per person of CAD 783. Four jurisdictions had values of NSDP per person higher than thecountry average. See Table 12.

The Andaman & Nicobar Islands Union Territory had the highest 2011 NSDP per person(CAD 2,418) in the region but a population at only 379,944. Sikkim is also an important marketwith an NSDP of CAD 1,977 per person and a population of 607,688.

25

2. North IndiaThe North India Region consists of: Chandigarh; Delhi; Haryana; Himachal Pradesh; Jammu

& Kashmir; Punjab; Rajasthan; Uttar Pradesh and; Uttaranchal. In 2011 the region had apopulation of 368.6 million and an NSDP per person of CAD 1,054. Six of the jurisdictions hadvalues of NSDP per person higher than the country average. See Table 12.

The most attractive market in this region is Chandigarh Union Territory which had the highest2011 NSDP per person (CAD 4,172) in the region and 1.1 million people. Delhi Union Territoryand Capital Territory is also an important market with an NSDP of CAD 3,283 per person and apopulation of 16.8 million.

3. South IndiaThe South India Region consists of: Andhra Pradesh; Karnataka; Kerala; Lakshedweep Union

Territory; Pondicherry Union Territory and; Tamil Nadu. In 2011 the region had a population of252.6 million and an NSDP per person of CAD 1,510. All six jurisdictions had NSDPs per persongreater than the national average. See Table 12.

The most attractive market in this region is Pondicherry which has the highest 2011 NSDP perperson (CAD 2,208) in the region and a population of 1.2 million. Kerala is also an importantmarket with an NSDP per person of CAD 1,707 and a population of 33.4 million.

4. West IndiaThe West India Region consists of: Dadra & Nagar Haveli Union Territory; Daman & Diu

Union Territory; Goa; Gujarat; Madhya Pradesh and; Maharashtra. In 2011 the region had apopulation of 247.4 million and an NSDP per person of CAD 1,533. Four of the jurisdictions hadNSDPs per person above the national average. See Table 12.

The most attractive market in this region is Goa which had the highest 2011 NSDP per person(CAD 4,355) in the region and a population of 1.5 million. Maharashtra is also an importantmarket with an NSDP per person of CAD 1,947 and a population of 112.4 million.

IV. RISK FACTORSA. Internal Political/Economic Conditions

• Increasing economic disparities among consumers and regions are emerging as apolitical risk capable of provoking serious socio-political tensions that could lead tolocalized violence from time to time. The states likely to be advancing economicallyare: Gujarat, Haryana, Kerala, Maharashtra, Punjab and Tamil Nadu. Those likely tobe lagging economically are: Assam, Bihar, Madhya Pradesh, Orissa, Rajasthan andUttar Pradesh. Although this is essentially an internal situation it can, at times,interrupt the flow of imports and negatively affect the solvency of Indian importers.

• An ongoing Maoist insurgency is becoming increasingly violent. The insurgentsoperate in several rural states and have targeted security forces, government

26

infrastructure and extractive companies.• Corruption remains a problem. Several scandals came to light in late 2010 and early

2011, particularly in the organisation of the Commonwealth Games and the granting ofmobile telephony licences. Corruption in general can increase the cost of doingbusiness in India.

• Inadequate infrastructure is a problem in India. Unreliable electric power and lack ofroad maintenance are examples of this problem which is rooted in the constraints ofpublic sector finances.

B. External Political/Economic ConditionsIndia has major disputes with Pakistan and China.

• India disputes Pakistan’s claim to Kashmir and questions its claim to have stoppedsponsoring terrorism in Kashmir.

• Relations with China are strained by its claim to Arunachal Pradesh and a portion of landadjacent to Jammu and Kashmir.

• India has recently been the victim of terrorism and occasionally, attacks disrupt businessactivities.

Any outbreak of hostilities between India and its neighbours could disrupt trade.

C. Handling Risks of International Trade Some risks are normally covered by commercial cargo insurance in accordance with

minimum cover of the Institute Cargo Clauses (Institute of London Underwriters) or some similarclause. This insurance normally covers the standard risks involved in transporting goods, such asaccidents and weather.

If a Canadian exporter expects to incur costs, or receive payment in INRs, consideration maybe given to hedging against currency risks by participating in the futures market. This strategy isnot appropriate in all situations and the exporter should obtain advice from a bank or other trustedexpert.

Additional risks might be covered by Accounts Receivable Insurance and other productssimilar to those offered by Export Development Canada (EDC). The availability, terms and costsof this insurance will depend on conditions in the importing country, the reputation of theimporter and EDC policy. The risks covered are:

• Accounts Receivable Insurance covers your receivables up to 90 per cent of lossesresulting from commercial or political risks;

• Single Buyer Insurance covers unlimited sales to one customer for 180 days;• Contract Frustration Insurance covers up to 90 per cent of your losses for one export

contract;

27

• Political Risk Insurance protects your overseas assets, including equipment andmanufacturing facilities;

• Performance Security Insurance covers up to 95 per cent of your losses if yourcustomer demands payment of a bond issued by your bank without valid reason.

For more detailed information see the website www.edc.ca.

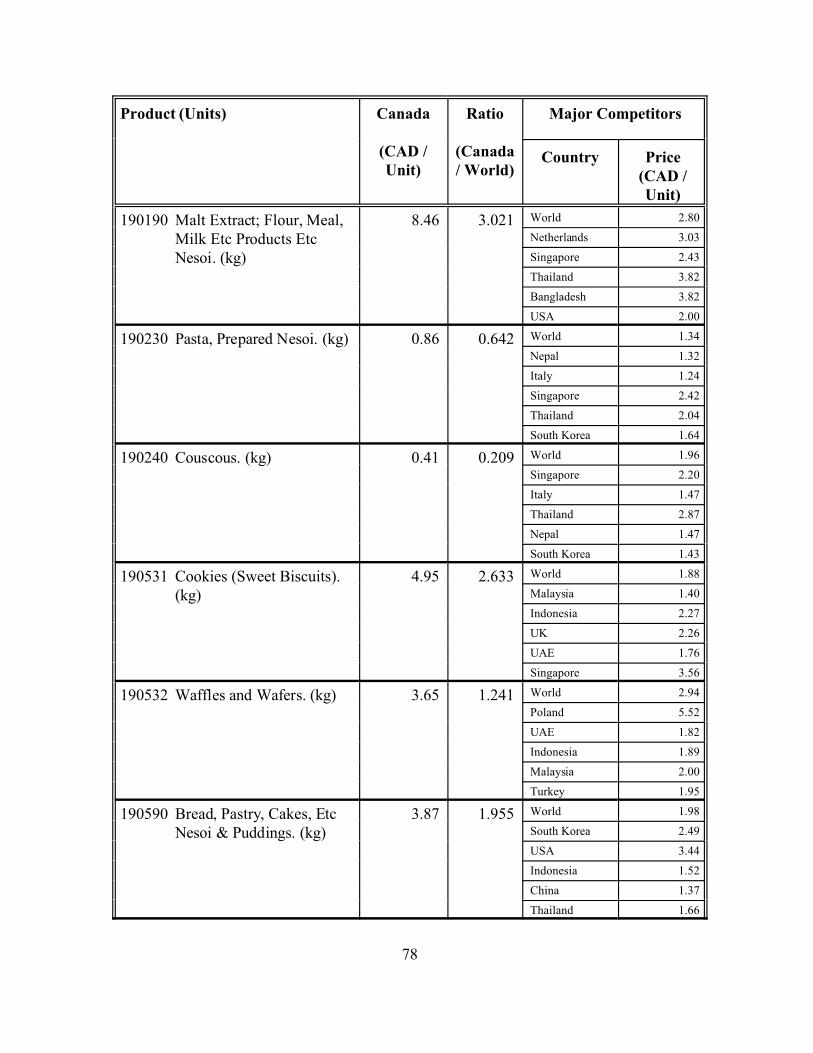

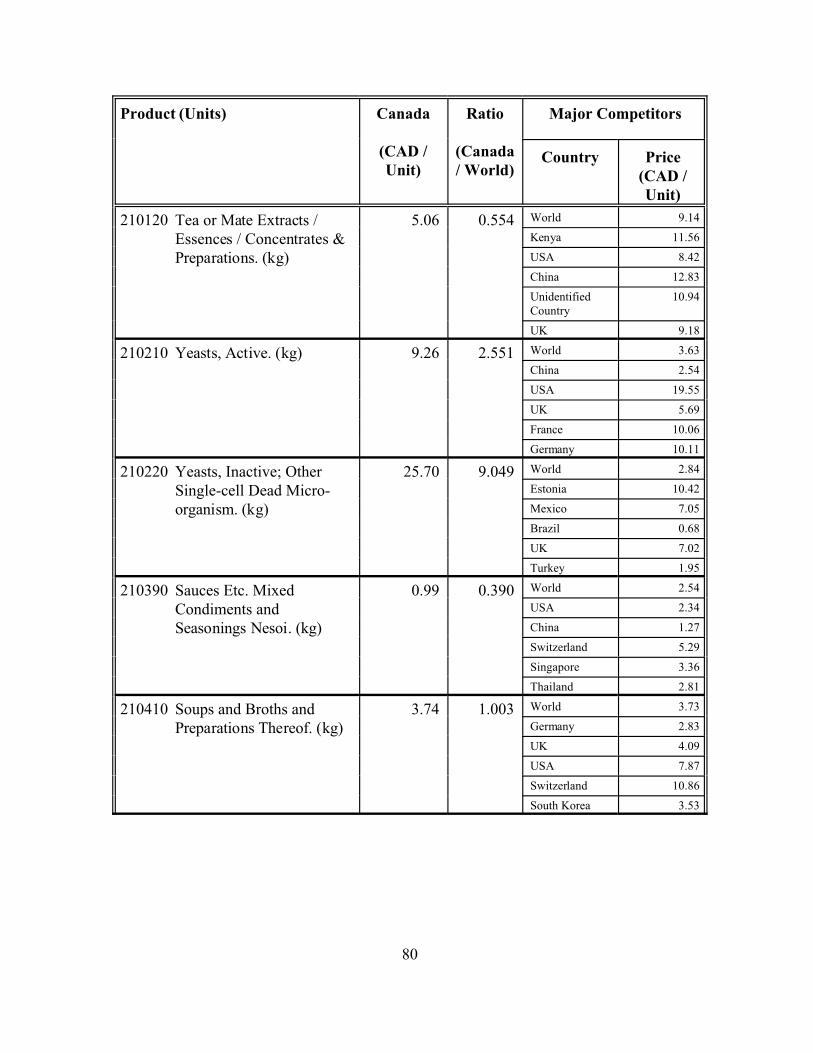

V. PRODUCT ANALYSIS11

A. Selected Products Imported by India From CanadaFollowing are descriptions of selected food products imported by India from many countries

including Canada. Unless otherwise specified, the average annual value of imports refer to the sixyears 2005 to 2010.

030613 Shrimps and Prawns, Including in Shell, FrozenThe average annual value of imports was CAD 6.0 million. In 2010, India imported

CAD 4.3 million worth from: Thailand (CAD 1.3 million); Unidentified Country (CAD 1.0million); Pakistan (CAD 782,000); the UK (CAD 501,000); the USA (CAD 169,000) and; Canada(86,000). Seven other countries supplied CAD 372,000 worth.

040410 Whey & Modified Whey Whether or Not Concentrated Containing AddedSweetenersThe average annual value of imports was CAD 5.0 million. In 2010, India imported

CAD 11.6 million worth from: the UK (CAD 2.4 million); France (CAD 2.2 million); the USA(CAD 2.0 million); New Zealand (CAD 1.6 million); Denmark (CAD 1.6 million) and; Canada(CAD 493,000). Ten other countries supplied CAD 1.2 million worth.

051000 Ambergris, Castoreum Etc; Glands Etc. for PharmacyThe average annual value of imports was CAD 717,000. In 2010, India imported CAD

1.7 million worth from: the USA (CAD 1.0 million); Canada (CAD 478,000); New Zealand(CAD 96,000); Italy (CAD 46,000) and; Pakistan (CAD 21,000). Three other countries suppliedCAD 20,000 worth.

071310 Peas, Dried Shelled, Including SeedThe average annual value of imports was CAD 515.9 million. In 2010, India imported

CAD 516.7 million worth from: Canada (CAD 396.6 million); the USA (CAD 74.0 million);Australia (CAD 21.7 million); Russia (CAD 8.6 million) and; the Ukraine (CAD 7.6 million).Sixteen other countries supplied CAD 8.3 million worth.

071320 Chickpeas (Garbanzos), Dried Shelled, Including SeedThe average annual value of imports was CAD 111.1 million. In 2010, India imported

CAD 89.0 million worth from: Australia (CAD 66.0 million); the USA (CAD 10.4 million);Tanzania (CAD 7.5 million); Canada (CAD 2.5 million) and; Mexico (CAD 1.4 million). Twelveother countries supplied CAD 1.2 million worth.

28

071340 Lentils, Dried Shelled, Including SeedThe average annual value of imports was CAD 97.9 million. In 2010, India imported

CAD 215.4 million worth from: Canada (CAD 158.1 million); the USA (CAD 46.5 million);Australia (CAD 7.1 million); Russia (CAD 3.3 million) and; Brazil (CAD 185,000). Five othercountries supplied CAD 379,000 worth.

080131 Cashew Nuts, Fresh or Dried, in ShellThe average annual value of imports was CAD 560.7 million. In 2010, India imported

CAD 590.3 million worth from: Cote d’ Ivoire (CAD 169.2 million); Tanzania (CAD 125.7million); Benin (CAD 81.1 million); Guinea-Bissau (CAD 61.0 million); Ghana (CAD 47.4million) and; Canada (CAD 112,000). Twenty-two other countries supplied 105.6 million worth.

080211 Almonds, Fresh or Dried, in ShellThe average annual value of imports was CAD 198.0 million. In 2010, India imported

CAD 252.8 million worth from: the USA (CAD 221.0 million); Australia (CAD 24.1 million);China (CAD 3.7 million); Afghanistan (CAD 1.3 million); the United Arab Emirates (CAD469,000) and; Canada (CAD 138,000). Fifteen other countries supplied CAD 2.0 million worth.

090940 Seeds of CarawayThe average annual value of imports was CAD 3.7 million. In 2010, India imported

CAD 4.7 million worth from: Afghanistan (CAD 3.4 million); Finland (CAD 458,000); Egypt(CAD 444,000); Canada (CAD 130,000) and; Syria (CAD 106,000). Three other countriessupplied CAD 170,000 worth.

120750 Mustard Seeds, Whether or Not BrokenThe average annual value of imports was CAD 1.3 million. In 2010, India imported

CAD 222,000 worth from Canada.

151419 Rapeseed / Colza Oil & Fractions, Low Erucic Acid, NesoiThe average annual value of imports was CAD 39,000. In 2010, India imported CAD

227,000 worth from: Canada (CAD 227,000) and; Japan (less than CAD 1,000).

151499 Rapeseed, Colza, Mustard Oil & Fractions Thereof, NesoiThe average annual value of imports was CAD 59,000. In 2010, India imported CAD

168,000 worth from: Canada (CAD 145,000); Italy (CAD 16,000) and; Singapore (CAD 7,000).

170199 Cane / Beet Sugar Chemically Pure Sucrose Refined NesoiThe average annual value of imports was CAD 73.7 million. In 2010, India imported

CAD 232.1 million worth from: Brazil (CAD 109.7 million); Thailand (CAD 71.5 million); theUnited Arab Emirates (CAD 18.4 million); Spain (CAD 10.2 million); Malaysia (CAD 6.4million) and; Canada (CAD 98,000). Twenty-one other countries supplied CAD 15.7 millionworth.

170211 Lactose & Lactose Syrup Containing 99% or More Lactose by Weight

29