oracle financial services software pte ltdoracle financial services software pte. ltd. page 2...

TRANSCRIPT

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD.

(Incorporated in the Republic of Singapore) (Registration Number: 200107453K)

AND ITS SUBSIDIARY

FINANCIAL STATEMENTS YEAR ENDED

31 MARCH 2016

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

Directors Venkatachalam Krishnakumar Wong Gen Kown Secretary Kong Yuh Ling Doreen Registered Office 27 International Business Park #02-01, iQuest@IBP Singapore 609924 Auditors Rohan • Mah & Partners LLP Banker

Citibank, N. A. Contents Page Directors’ Statement 1 - 2 Independent Auditors' Report 3 - 4 Consolidated Statement of Financial Position 5 - 6 Consolidated Statements of Comprehensive Income 7 Consolidated Statements of Changes in Equity 8 Consolidated Statements of Cash Flows 9 Notes to the Financial Statements 10 - 52

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 1 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

DIRECTORS’ STATEMENT

The directors are pleased to present their statement to the members together with the audited consolidated financial statements of Oracle Financial Services Software Pte. Ltd. (“the Company”) and its subsidiary (“the Group”) for the financial year ended 31 March 2016.

1 OPINION OF THE DIRECTORS

In the opinion of the directors,

(a) the financial statements of the Company are drawn up so as to give a true and fair view of the financial position of the Company as at 31 March 2016 and the financial performance, changes in equity and cash flows of the Company for the year then ended; and

(b) at the date of this statement, there are reasonable grounds to believe that the Company will be

able to pay its debt as and when they fall due.

2 DIRECTORS

The directors of the company in office at the date of this statement are: Venkatachalam Krishnakumar Wong Gen Kown

3 ARRANGEMENTS FOR DIRECTORS TO ACQUIRE SHARES OR DEBENTURES

Neither at the end of nor at any time during the financial year was the Company a party to any arrangement whose objects are, or one of whose objects is, to enable the directors of the Company to acquire benefits by means of the acquisition of shares in, or debentures of the Company or any other body corporate.

4 DIRECTORS' INTEREST IN SHARES OR DEBENTURES

The directors holding office at the end of the financial year and their interests in the shares of the Company and related corporation as recorded in the register kept by the Company for the purposes of Section 164 of the Companies Act, Cap. 50 were as follows:

Holding in the name of the Directors

Shares of Rs 5 each Name of Directors At At

Immediate Holding Corporation beginning end - Oracle Financial Services Software Limited of year of year

Venkatachalam Krishnakumar 1,500 5,500

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 2 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

DIRECTORS’ STATEMENT

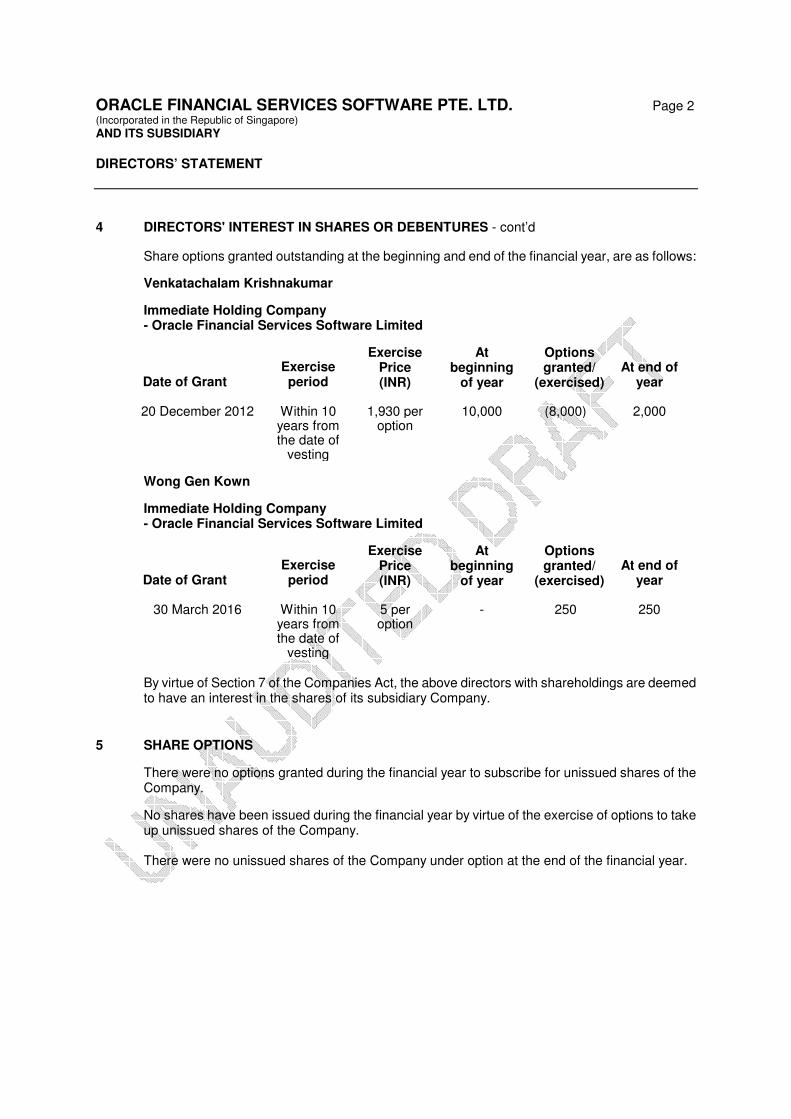

4 DIRECTORS' INTEREST IN SHARES OR DEBENTURES - cont’d

Share options granted outstanding at the beginning and end of the financial year, are as follows:

Venkatachalam Krishnakumar

Immediate Holding Company - Oracle Financial Services Software Limited

Date of Grant

Exercise period

Exercise Price (INR)

At beginning

of year

Options granted/

(exercised)

At end of year

20 December 2012 Within 10 years from the date of

vesting

1,930 per option

10,000 (8,000) 2,000

Wong Gen Kown

Immediate Holding Company - Oracle Financial Services Software Limited

Date of Grant

Exercise period

Exercise Price (INR)

At beginning

of year

Options granted/

(exercised)

At end of year

30 March 2016 Within 10 years from the date of

vesting

5 per option

- 250 250

By virtue of Section 7 of the Companies Act, the above directors with shareholdings are deemed to have an interest in the shares of its subsidiary Company.

5 SHARE OPTIONS

There were no options granted during the financial year to subscribe for unissued shares of the Company.

No shares have been issued during the financial year by virtue of the exercise of options to take up unissued shares of the Company. There were no unissued shares of the Company under option at the end of the financial year.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 3 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

DIRECTORS’ STATEMENT

6 AUDITORS

The auditors, Messrs. Rohan • Mah & Partners LLP have expressed their willingness to accept re-appointment.

ON BEHALF OF THE BOARD .....................................………… Venkatachalam Krishnakumar Director .....................................………... Wong Gen Kown Director Singapore, XX

Page 5 INDEPENDENT AUDITORS’ REPORT

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

Report on the Consolidated Financial Statements

We have audited the accompanying financial statements of Oracle Financial Services Software Pte. Ltd. (“the Company”) and its subsidiary (“the Group”), which comprise the statement of financial position of the Group and the Company as at 31 March 2016, and consolidated statement of comprehensive income, consolidated statement of changes in equity and consolidated statement of cash flows of the Group for the year then ended, and a summary of significant accounting policies and other explanatory information. Management’s Responsibility for the Financial Statements

Management is responsible for the preparation of financial statements that give a true and fair view in accordance with the provisions of the Singapore Companies Act, Cap 50 (“the Act”) and Singapore Financial Reporting Standards, and for devising and maintaining a system of internal accounting controls sufficient to provide a reasonable assurance that assets are safeguarded against loss from unauthorised use or disposition; and transactions are properly authorised and that they are recorded as necessary to permit the preparation of true and fair profit and loss accounts and balance sheets and to maintain accountability of assets. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Singapore Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control.

An audit also includes evaluating the appropriateness of accounting policies

used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Page 6 INDEPENDENT AUDITORS’ REPORT

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

Opinion In our opinion, the consolidated financial statements of the Group and the balance sheet of the Company are properly drawn up in accordance with the provisions of the Act and Singapore Financial Reporting Standards so as to give a true and fair view of the state of affairs of the Group and of the Company as at 31 March 2016 and the results, changes in equity and cash flows of the Group for the year ended on that date. Report on Other Legal and Regulatory Requirements In our opinion, the accounting and other records required by the Act to be kept by the Company and by the subsidiary incorporated in Singapore of which we are the auditors have been properly kept in accordance with the provisions of the Act. ROHAN •••• MAH & PARTNERS LLP Public Accountants and Chartered Accountants Singapore (RK/MA/FM/WL/CS/as)

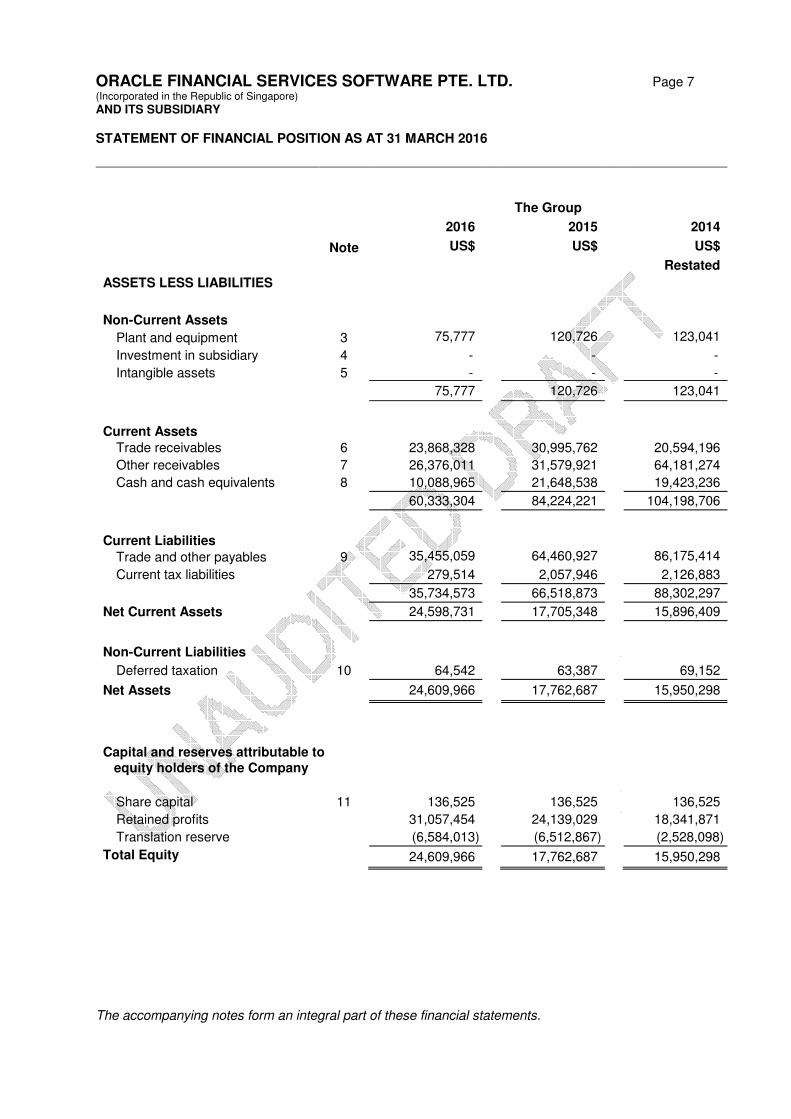

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 7 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

The accompanying notes form an integral part of these financial statements.

STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2016

The Group

2016

2015

2014

Note US$

US$

US$

Restated

ASSETS LESS LIABILITIES

Non-Current Assets

Plant and equipment 3 75,777

120,726 123,041

Investment in subsidiary 4 - - -

Intangible assets 5 - - -

75,777 120,726 123,041

Current Assets Trade receivables 6 23,868,328

30,995,762 20,594,196

Other receivables 7 26,376,011

31,579,921 64,181,274

Cash and cash equivalents 8 10,088,965

21,648,538 19,423,236

60,333,304

84,224,221 104,198,706

Current Liabilities Trade and other payables 9 35,455,059 64,460,927 86,175,414

Current tax liabilities 279,514 2,057,946 2,126,883

35,734,573 66,518,873 88,302,297

Net Current Assets 24,598,731 17,705,348 15,896,409

Non-Current Liabilities

Deferred taxation 10 64,542

63,387 69,152

Net Assets 24,609,966 17,762,687 15,950,298

Capital and reserves attributable to equity holders of the Company

Share capital 11 136,525

136,525 136,525

Retained profits

31,057,454

24,139,029 18,341,871

Translation reserve

(6,584,013)

(6,512,867) (2,528,098)

Total Equity 24,609,966

17,762,687 15,950,298

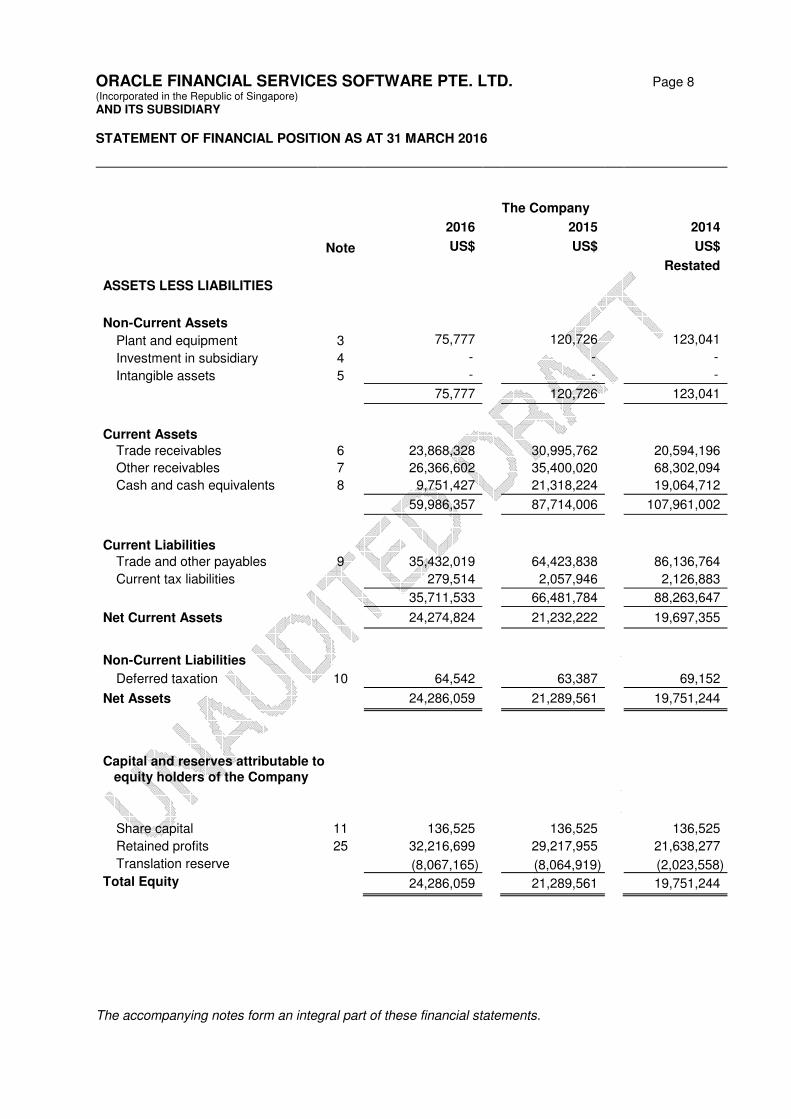

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 8 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

The accompanying notes form an integral part of these financial statements.

STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2016

The Company

2016

2015

2014

Note US$

US$

US$

Restated

ASSETS LESS LIABILITIES

Non-Current Assets

Plant and equipment 3 75,777

120,726 123,041

Investment in subsidiary 4 -

- -

Intangible assets 5 -

- -

75,777 120,726 123,041

Current Assets Trade receivables 6 23,868,328

30,995,762 20,594,196

Other receivables 7 26,366,602 35,400,020 68,302,094

Cash and cash equivalents 8 9,751,427

21,318,224 19,064,712

59,986,357

87,714,006 107,961,002

Current Liabilities Trade and other payables 9 35,432,019

64,423,838 86,136,764

Current tax liabilities 279,514 2,057,946 2,126,883

35,711,533 66,481,784 88,263,647

Net Current Assets

24,274,824

21,232,222 19,697,355

Non-Current Liabilities

Deferred taxation 10 64,542 63,387 69,152

Net Assets 24,286,059

21,289,561 19,751,244

Capital and reserves attributable to equity holders of the Company

Share capital 11 136,525

136,525 136,525

Retained profits 25 32,216,699

29,217,955 21,638,277

Translation reserve (8,067,165) (8,064,919) (2,023,558)

Total Equity 24,286,059

21,289,561 19,751,244

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 9 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

The accompanying notes form an integral part of these financial statements.

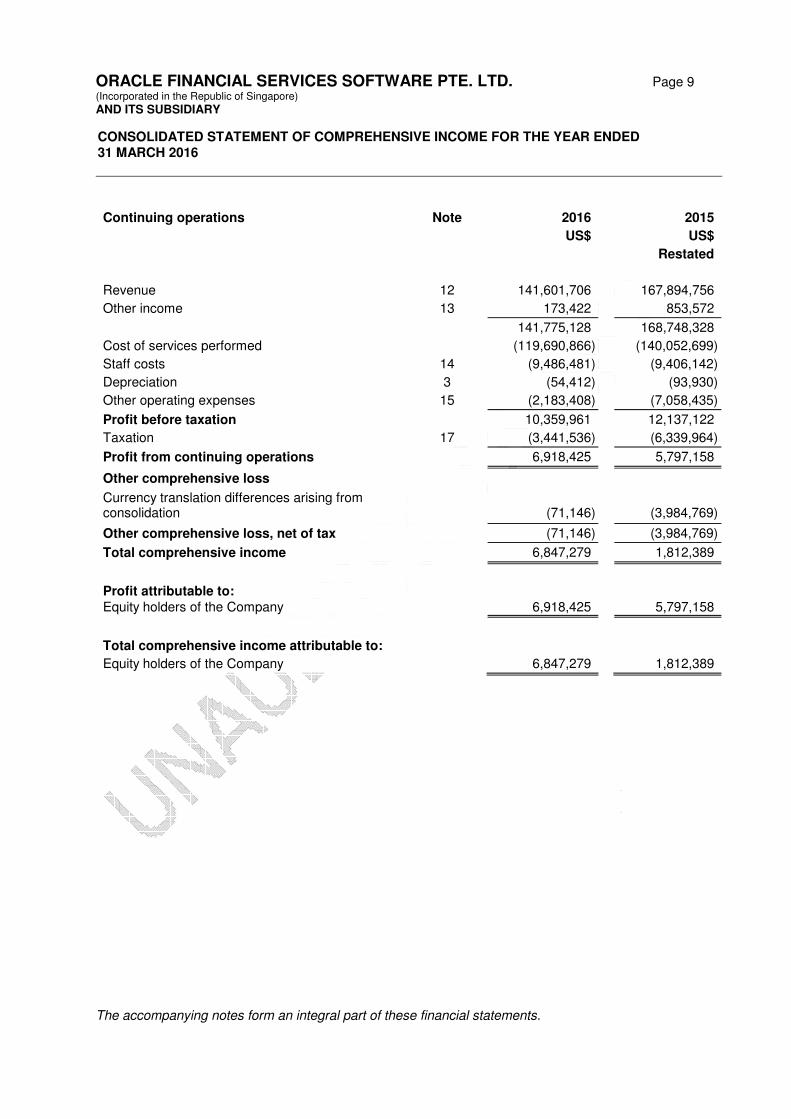

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 MARCH 2016

Continuing operations Note 2016 2015

US$ US$

Restated

Revenue 12 141,601,706 167,894,756

Other income 13 173,422 853,572

141,775,128 168,748,328

Cost of services performed (119,690,866) (140,052,699)

Staff costs 14 (9,486,481) (9,406,142)

Depreciation 3 (54,412) (93,930)

Other operating expenses 15 (2,183,408) (7,058,435)

Profit before taxation 10,359,961 12,137,122

Taxation 17 (3,441,536) (6,339,964)

Profit from continuing operations 6,918,425 5,797,158

Other comprehensive loss

Currency translation differences arising from consolidation

(71,146)

(3,984,769)

Other comprehensive loss, net of tax (71,146) (3,984,769)

Total comprehensive income 6,847,279 1,812,389

Profit attributable to: Equity holders of the Company 6,918,425 5,797,158

Total comprehensive income attributable to:

Equity holders of the Company 6,847,279 1,812,389

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 10 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

The accompanying notes form an integral part of these financial statements.

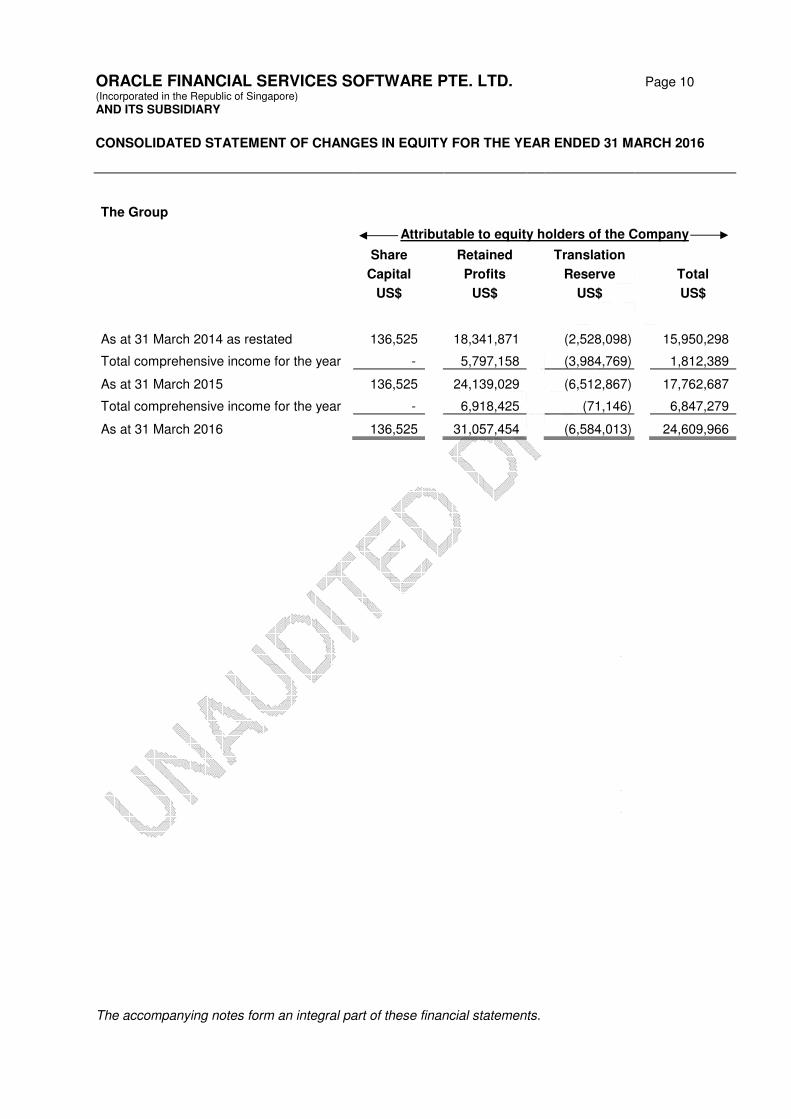

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 MARCH 2016

The Group

Attributable to equity holders of the Company

Share Retained Translation

Capital Profits Reserve Total

US$ US$ US$ US$

As at 31 March 2014 as restated 136,525 18,341,871 (2,528,098) 15,950,298

Total comprehensive income for the year - 5,797,158 (3,984,769) 1,812,389

As at 31 March 2015 136,525 24,139,029 (6,512,867) 17,762,687

Total comprehensive income for the year - 6,918,425 (71,146) 6,847,279

As at 31 March 2016 136,525 31,057,454 (6,584,013) 24,609,966

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 11 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

The accompanying notes form an integral part of these financial statements.

CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 MARCH 2016

2016 2015

CASH FLOWS FROM OPERATING ACTIVITIES US$ US$ Restated

Profit before taxation 6,918,425 12,137,122

Adjustments for: Allowance for doubtful debts 85,280 1,508,764 Foreign exchange difference in plant and equipment 179 138 Reversal for doubtful debts (774,758) - Depreciation of plant and equipment 54,412 93,930 Interest income (130,132) (196,708) Operating profit before working capital changes 6,153,406 13,543,246 Working capital changes, excluding changes related to cash: Trade receivables 7,816,912 (11,910,330) Other receivables 10,942,494 11,849,497 Trade and other payables (29,005,868) (21,714,487)

Cash (used in)/generated from operations (4,093,056) (8,232,074) Interest received 130,132 196,708 Income taxes paid (net) (1,777,277) (6,414,666)

Net cash (used in)/generated from operating activities (5,740,201) (14,450,032)

CASH FLOWS FROM INVESTING ACTIVITIES

Amount due from immediate holding company – non-trade (3,690,866) 20,693,039 Amount due from related companies – non-trade (2,047,718) 58,817 Acquisition of plant and equipment (9,642) (91,753)

Net cash generated from/(used in) investing activities (5,748,226) 20,660,103

Net increase/(decrease) in cash and cash equivalents (11,488,427) 6,210,071

Effect of exchange rate fluctuation on cash and cash equivalent

(71,146)

(3,984,769)

Cash and cash equivalents at beginning of financial year 21,648,538 19,423,236

Cash and cash equivalents at the end of the financial year (Note 8) 10,088,965 21,648,538

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 12 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

These notes form an integral part of and should be read in conjunction with the accompanying financial statements. 1 CORPORATE INFORMATION

Oracle Financial Services Software Pte. Ltd. is a limited liability company incorporated in Singapore with its registered office and its principal place of business at 27 International Business Park #02-01, iQuest@IBP, Singapore 609924.

The financial statements of the Company for the year ended 31 March 2015 relate to the Company and its subsidiary (collectively referred to as the “Group”).

The principal activities of the Company in the course of the financial year are those relating to providing information technology solutions, consulting services and development of software to the financial service industry. The principal activities of its subsidiary company are set out in Note 4 to the financial statements. There have been no significant changes in the nature of these activities during the financial year.

The Company is a wholly-owned subsidiary of Oracle Financial Services Software Limited, a company incorporated in India. The Company’s ultimate holding company is Oracle Corporation, a company incorporated in the United States of America.

The financial statements of the Company for the year ended 31 March 2015 were authorised for issue in accordance with a resolution of the Directors on __________________.

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

2.1 Basis of Preparation

The financial statements are prepared in accordance with Singapore Financial Reporting Standards (“FRS”). The financial statements, expressed in United States Dollar (USD or US$) are prepared on the historical cost convention, except as disclosed in the accounting policies below.

The preparation of financial statements in conformity with FRS requires management to exercise its judgement in the process of applying the Group’s accounting policies. It also requires the use of accounting estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the financial year. Although these estimates are based on management’s best knowledge of current events and actions, actual results may ultimately differ from those estimates. Critical accounting estimates and assumptions used that are significant to the financial statements, and areas involving a higher degree of judgement or complexity, are disclosed in Note 21.

In the current financial year, the Group has adopted all the new and revised FRSs and Interpretations of FRS (“INT FRS”) that are relevant to its operations and effective for annual years beginning on or after 1 April 2014. The adoption of these new/revised FRSs and INT FRSs does not result in changes to the Group’s accounting policies except as disclosed in Note 21 and has no material effect on the amounts reported for the current or prior years.

The Group has not applied any new standard or interpretation that has been issued but is not yet effective. The new standards that have been issued and not yet effective do not have any impact on the result of current or prior years.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 13 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.2 Group Accounting 2.2.1 Subsidiaries

(i) Consolidation

Subsidiaries are entities (including special purpose entities) over which the Group has power to govern the financial and operating policies so as to obtain benefits from its activities, generally accompanied by a shareholding giving rise to a majority of the voting rights. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether the Group controls another entity. Subsidiaries are consolidated from the date on which control is transferred to the Group. They are de-consolidated from the date on which control ceases. In preparing the consolidated financial statements, transactions, balances and unrealised gains on transactions between group entities are eliminated. Unrealised losses are also eliminated but are considered an impairment indicator of the asset transferred. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the policies adopted by the Group. Non-controlling interests are that part of the net results of operations and of net assets of a subsidiary attributable to the interests which are not owned directly or indirectly by the equity holders of the Company. They are shown separately in the consolidated statement of comprehensive income, statement of changes in equity and balance sheet. Total comprehensive income is attributed to the non-controlling interests based on their respective interests in a subsidiary, even if this results in the non-controlling interests having a deficit balance.

(ii) Acquisitions

The acquisition method of accounting is used to account for business combinations by the Group. The consideration transferred for the acquisition of a subsidiary or business comprises the fair value of the assets transferred, the liabilities incurred and the equity interests issued by the Group. The consideration transferred also includes the fair value of any contingent consideration arrangement and the fair value of any pre-existing equity interest in the subsidiary. Acquisition-related costs are expensed as incurred. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are, with limited exceptions, measured initially at their fair values at the acquisition date.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 14 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d 2.2 Group Accounting - cont’d

2.2.1 Subsidiaries - cont’d

(ii) Acquisitions - cont’d

On an acquisition-by-acquisition basis, the Group recognises any noncontrolling interest in the acquiree at the date of acquisition either at fair value or at the non-controlling interest’s proportionate share of the acquiree’s net identifiable assets. The excess of (i) the consideration transferred, the amount of any noncontrolling interest in the acquiree and the acquisition-date fair value of any previous equity interest in the acquiree over the (ii) fair value of the net identifiable assets acquired is recorded as goodwill. Please refer to note 2.5.1 for the accounting policy on goodwill.

(iii) Disposals

When a change in the Group ownership interest in a subsidiary results in a loss of control over the subsidiary, the assets and liabilities of the subsidiary including any goodwill are derecognised. Amounts previously recognised in other comprehensive income in respect of that entity are also reclassified to profit or loss or transferred directly to retained earnings if required by a specific Standard. Any retained equity interest in the entity is remeasured at fair value. The difference between the carrying amount of the retained interest at the date when control is lost and its fair value is recognised in profit or loss. Please refer to note 2.4 for the accounting policy on investment in subsidiary.

2.2.2 Transactions with non-controlling interests

Changes in the Group’s ownership interest in a subsidiary that do not result in a loss of control over the subsidiary are accounted for as transactions with equity owners of the Company. Any difference between the change in the carrying amounts of the non-controlling interest and the fair value of the consideration paid or received is recognised within equity attributable to the equity holders of the Company.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 15 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.3 Plant and Equipment 2.3.1 Measurement

All items of plant and equipment are initially recorded at cost and subsequently carried at cost less accumulated depreciation and accumulated impairment losses.

2.3.2 Components of costs The cost of plant and equipment includes expenditure that is directly attributable to the acquisition of the items. Dismantlement, removal or restoration costs are included as part of the cost of plant and equipment if the obligation for dismantlement, removal or restoration is incurred as a consequence of acquiring or using the asset.

2.3.3 Depreciation

Depreciation on plant and equipment is calculated using the straight line method to allocate their depreciable amounts over their estimated useful lives as follows:

Years

Furniture and fittings 2 - 7 Computers 2 - 3

Office equipment 5 - 7

The useful lives of plant and equipment are reviewed and adjusted as appropriate at each balance sheet date. Fully depreciated assets are retained in the financial statements until they are no longer in use.

2.3.4 Subsequent Expenditure

Subsequent expenditure relating to plant and equipment that has already been recognised is added to the carrying amount of the asset only when it is probable that future economic benefits will flow to the Group and the cost can be reliably measured. Other subsequent expenditure is recognised as an expense during the financial year in which it is incurred.

2.3.5 Disposal

On disposal of an item of plant and equipment, the difference between the net disposal proceeds and its carrying amount is taken to the statement of comprehensive income. Any amount in revaluation reserve relating to that asset is transferred to retained earnings.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 16 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.4 Investments in Subsidiary

Investments in subsidiaries are carried at cost less accumulated impairment losses in the Group’s balance sheet. On disposal of investments in subsidiaries, the difference between disposal proceeds and the carrying amounts of the investments are recognised in profit or loss.

2.5 Intangible Assets

2.5.1 Goodwill

Goodwill on acquisitions of subsidiaries and businesses on or after 1 January 2012 represents the excess of (i) the consideration transferred, the amount of any non-controlling interest in the acquiree and the acquisition-date fair value of any previous equity interest in the acquiree over (ii) the fair value of the net identifiable assets acquired.

Goodwill on acquisition of subsidiaries and businesses prior to 1 January 2012 and on acquisition of joint ventures and associated companies represents the excess of the cost of the acquisition over the fair value of the Group’s share of the net identifiable assets acquired.

Goodwill on subsidiaries and joint ventures is recognised separately as intangible assets and carried at cost less accumulated impairment losses.

Goodwill on associated companies is included in the carrying amount of the investments.

Gains and losses on the disposal of subsidiaries, joint ventures and associated companies include the carrying amount of goodwill relating to the entity sold, except for goodwill arising from acquisitions prior to 1 January 2001. Such goodwill was adjusted against retained profits in the year of acquisition and is not recognised in profit or loss on disposal.

2.5.2 Customer Contracts

Customer contracts acquired as part of business combinations are initially recognised at their fair values at the acquisition date and are subsequently carried at cost (i.e. the fair values at initial recognition) less accumulated amortisation and accumulated impairment losses. These costs are amortised to the statement of comprehensive income using the straight-line method over 12 months, which is the shorter of their estimated useful lives and periods of contractual rights.

2.5.3 Customer Relationship

Customer relationship acquired as part of business combinations are initially recognised at their fair values at the acquisition date and are subsequently carried at cost (i.e. the fair values at initial recognition) less accumulated amortisation and accumulated impairment losses. These costs are amortised to the statement of comprehensive income using the straight-line method over 5 years, which is the shorter of their estimated useful lives and periods of contractual rights.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 17 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.5 Intangible Assets - cont’d

2.5.3 Customer Relationship - cont’d The amortisation period and amortisation method of intangible assets other than goodwill are reviewed at least at each balance sheet date. The effects of any revision of the amortisation period or amortisation method are included in the statement of comprehensive income for the financial year in which the changes arise.

2.6 Impairment of Non-Financial Assets

2.6.1 Goodwill

Goodwill is tested annually for impairment, as well as when there is any indication that the goodwill may be impaired. For the purpose of impairment testing of goodwill, goodwill is allocated to each of the Group’s cash-generating-units (CGU) expected to benefit from synergies of the business combination. An impairment loss is recognised in the statement of comprehensive income when the carrying amount of CGU, including the goodwill, exceeds the recoverable amount of the CGU. Recoverable amount of the CGU is the higher of the CGU’s fair value less cost to sell and value in use.

The total impairment loss is allocated first to reduce the carrying amount of goodwill allocated to the CGU and then to the other assets of the CGU pro-rata on the basis of the carrying amount of each asset in the CGU.

Impairment loss on goodwill is not reversed in a subsequent period.

2.6.2 Intangible assets Plant and Equipment Investments in subsidiary

Intangible assets, plant and equipment, investments in subsidiary are reviewed for impairment whenever there is any indication that these assets may be impaired. If any such indication exists, the recoverable amount (i.e. the higher of the fair value less cost to sell and value in use) of the asset is estimated to determine the amount of impairment loss.

For the purpose of impairment testing of these assets, recoverable amount is determined on an individual asset basis unless the asset does not generate cash flows that are largely independent of those from other assets. If this is the case, recoverable amount is determined for the CGU to which the asset belongs to. If the recoverable amount of the asset (or CGU) is estimated to be less than its carrying amount, the carrying amount of the asset (or CGU) is reduced to its recoverable amount. The impairment loss is recognised in the statement of comprehensive income unless the asset is carried at revalued amount, in which case, such impairment loss is treated as a revaluation decrease.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 18 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.6 Impairment of Non-Financial Assets - cont’d

2.6.2 Intangible assets Plant and Equipment

Investments in subsidiary - cont’d An impairment loss for an asset other than goodwill is reversed if, and only if, there has been a change in the estimates used to determine the assets’ recoverable amount since the last impairment loss was recognised. The carrying amount of an asset is increased to its revised recoverable amount, provided that this amount does not exceed the carrying amount that would have been determined (net of amortisation or depreciation) had no impairment loss been recognised for the asset in prior years. A reversal of impairment loss for an asset is recognised in the statement of comprehensive income, unless the asset is carried at revalued amount, in which case, such reversal is treated as a revaluation increase.

2.7 Financial Assets

2.7.1 Initial Recognition and Measurement

Financial assets are recognised on the balance sheet when, and only when, the Group becomes a party to the contractual provisions of the financial instrument. The Group determines the classification of its financial assets at initial recognition. When financial assets are recognised initially, they are measured as fair value, plus, in the case of financial assets not at fair value through profit or loss, directly attributable transaction costs.

2.7.2 Subsequent Measurement

The subsequent measurement of financial assets depends on their classification as follows: (i) Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss include financial assets held for trading and financial assets designated upon initial recognition at fair value through profit or loss. Financial assets are classified as held for trading if they are acquired for the purpose of selling or repurchasing in the near term. This category includes derivative financial instruments entered into by the Group that are not designated as hedging instruments in hedge relationships as defined by FRS 39. Derivatives, including separated embedded derivatives are also classified as held for trading unless they are designated as effective hedging instruments.

The Group has not designated any financial assets upon initial recognition at fair value through profit or loss.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 19 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.7 Financial Assets - cont’d

2.7.2 Subsequent Measurement - cont’d

(i) Financial assets at fair value through profit or loss - cont’d Subsequent to initial recognition, financial assets at fair value through profit or loss are measured at fair value. Any gains or losses arising from changes in fair value of the financial assets are recognised in profit or loss. Net gains or net losses on financial assets at fair value through profit or loss include exchange differences, interest and dividend income. Derivatives embedded in host contracts are accounted for as separate derivatives and recorded at fair value if their economic characteristics and risks are not closely related to those of the host contracts and the host contracts are not held for trading or designated at fair value through profit or loss. These embedded derivatives are measured at fair value with changes in fair value recognised in profit or loss. Reassessment only occurs if there is a change in the terms of the contract that significantly modifies the cash flows that would otherwise be required.

(ii) Loans and receivables Non-derivative financial assets with fixed or determinable payments that are not quoted in an active market are classified as loans and receivables. Subsequent to initial recognition, loans and receivables are measured at amortised cost using the effective interest method, less impairment. Gains and losses are recognised in profit or loss when the loans and receivables are derecognised or impaired, and through the amortisation process.

(iii) Held-to-maturity investments Non-derivative financial assets with fixed or determinable payments and fixed maturity are classified as held-to-maturity when the Group has the positive intention and ability to hold the investment to maturity. Subsequent to initial recognition, held-to-maturity investments are measured at amortised cost using the effective interest method, less impairment. Gains and losses are recognised in profit or loss when the held-to-maturity investments are derecognised or impaired, and through the amortisation process.

(iv) Available-for-sale financial assets Available for-sale financial assets include equity and debts securities. Equity investments classified as available-for-sale are those, which are neither classified as held for trading nor designated at fair value through profit or loss. Debt securities in this category are those which are intended to be held for an indefinite period of time and which may be sold in response to needs for liquidity or in response to changes in the market conditions.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 20 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.7 Financial Assets - cont’d

2.7.2 Subsequent Measurement - cont’d

(iv) Available-for-sale financial assets - cont’d After initial recognition, available-for-sale financial assets are subsequently measured at fair value. Any gains or losses from changes in fair value of the financial asset are recognised in other comprehensive income, except that impairment losses, foreign exchange gains and losses on monetary instruments and interest calculated using the effective interest method are recognised in profit or loss. The cumulative gain or loss previously recognised in other comprehensive income is reclassified from equity to profit or loss as a reclassification adjustment when the financial asset is derecognised. Investments in equity instruments whose fair value cannot be reliably measured are measured at cost less impairment loss.

2.7.3 Derecognition A financial asset is derecognised where the contractual right to receive cash flows from the asset has expired. On derecognition of a financial asset in its entirety, the difference between the carrying amount and the sum of the consideration received and any cumulative gain or loss that had been recognised in other comprehensive income is recognised in profit or loss. All regular way purchases and sales of financial assets are recognised or derecognised on the trade date i.e., the date that the Group commits to purchase or sell the asset. Regular way purchases or sales are purchases or sales of financial assets that require delivery of assets within the period generally established by regulation or convention in the marketplace concerned.

2.8 Impairment of Financial Assets The Group assesses at each end of the reporting period whether there is any objective evidence that a financial asset is impaired.

2.8.1 Financial Assets Carried at Amortised Cost For financial assets carried at amortised cost, the Group first assesses individually whether objective evidence of impairment exists individually for financial assets that are individually significant, or collectively for financial assets that are not individually significant. If the Group determines that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be recognised are not included in a collective assessment of impairment.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 21 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.8 Impairment of Financial Assets - cont’d

2.8.1 Financial Assets Carried at Amortised Cost - cont’d If there is objective evidence that an impairment loss on financial assets carried at amortised cost has incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the financial asset’s original effective interest rate. If a loan has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate. The carrying amount of the asset is reduced through the use of an allowance account. The impairment loss is recognised in profit or loss. When the asset becomes uncollectible, the carrying amount of impaired financial assets is reduced directly or if an amount was charged to the allowance account, the amounts charged to the allowance account are written off against the carrying value of the financial asset. To determine whether there is objective evidence that an impairment loss on financial assets has incurred, the Group considers factors such as the probability of insolvency or significant financial difficulties of the debtor and default or significant delay in payments. If in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed to the extent that the carrying amount of the asset does not exceed its amortised cost at the reversal date. The amount of reversal is recognised in profit or loss.

2.8.2 Financial Assets Carried at Cost

If there is objective evidence (such as significant adverse changes in the business environment where the issuer operates, probability of insolvency or significant financial difficulties of the issuer) that an impairment loss on financial assets carried at cost has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the current market rate of return for a similar financial asset. Such impairment losses are not reversed in subsequent periods.

2.8.3 Available-For-Sale Financial Assets

In the case of equity investments classified as available-for-sale, objective evidence of impairment include (i) significant financial difficulty of the issuer or obligor,

(ii) information about significant changes with an adverse effect that have taken place in the technological, market, economic or legal environment in which the issuer operates, and indicates that the cost of the investment in equity instrument may not be recovered; and

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 22 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.8 Impairment of Financial Assets - cont’d

2.8.3 Available-For-Sale Financial Assets - cont’d

(iii) a significant or prolonged decline in the fair value of the investment below its costs. ‘Significant’ is to be evaluated against the original cost of the investment and ‘prolonged’ against the period in which the fair value has been below its original cost.

If an available-for-sale financial asset is impaired, an amount comprising the difference between its acquisition cost (net of any principal repayment and amortisation) and its current fair value, less any impairment loss previously recognised in profit or loss is transferred from other comprehensive income and recognised in profit or loss. Reversals of impairment losses in respect of equity instruments are not recognised in profit or loss; increase in their fair value after impairment are recognised directly in other comprehensive income.

In the case of debt instruments classified as available-for-sale, impairment is assessed based on the same criteria as financial assets carried at amortised cost. However, the amount recorded for impairment is the cumulative loss measured as the difference between the amortised cost and the current fair value, less any impairment loss on that investment previously recognised in profit or loss. Future interest income continues to be accrued based on the reduced carrying amount of the asset and is accrued using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss. The interest income is recorded as part of finance income. If, in a subsequent year, the fair value of a debt instrument increases and the increases can be objectively related to an event occurring after the impairment loss was recognised in profit or loss, the impairment loss is reversed in profit or loss.

2.9 Financial Liabilities

2.9.1 Initial Recognition and Measurement Financial liabilities are recognised on the balance sheet when, and only when, the Group becomes a party to the contractual provisions of the financial instrument. The Company determines the classification of its financial liabilities at initial recognition. All financial liabilities are recognised initially at fair value and in the case of other financial liabilities, plus directly attributable transaction costs.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 23 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.9 Financial Liabilities - cont’d

2.9.2 Subsequent Measurement The measurement of financial liabilities depends on their classification as follows: (i) Financial liabilities at fair value through profit or loss

Financial liabilities at fair value through profit or loss includes financial liabilities held for trading and financial liabilities designated upon initial recognition as at fair value. Financial liabilities are classified as held for trading if they are acquired for the purpose of selling in the near term. This category includes derivative financial instruments entered into by the Group that are not designated as hedging instruments in hedge relationships. Separated embedded derivatives are also classified as held for trading unless they are designated as effective hedging instruments. Subsequent to initial recognition, financial liabilities at fair value through profit or loss are measured at fair value. Any gains or losses arising from changes in fair value of the financial liabilities are recognised in profit or loss. The Group has not designated any financial liabilities upon initial recognition at fair value through profit or loss.

(ii) Other financial liabilities After initial recognition, other financial liabilities are subsequently measured at amortised cost using the effective interest rate method. Gains and losses are recognised in profit or loss when the liabilities are derecognised, and through the amortization process.

2.9.3 Derecognition A financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognised in profit or loss.

2.10 Fair Value Estimation The fair values of financial instruments traded in active markets are based on quoted market prices at the balance sheet date. The quoted market prices used for financial assets held by the Group are the current bid prices; the appropriate quoted market prices for financial liabilities are the current ask prices.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 24 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.10 Fair Value Estimation - cont’d

The fair values of financial instruments that are not traded in an active market are determined by using valuation techniques. The Group uses a variety of methods and makes assumptions that are based on market conditions existing at each balance sheet date. Quoted market prices or dealer quotes for similar instruments are used where appropriate. Other techniques, such as estimated discounted cash flows, are also used to determine the fair values of the financial instruments.

The carrying amounts of current receivables and payables are assumed to approximate their fair values. The fair values of non-current receivables for disclosure purposes are estimated by discounting the future contractual cash flows at the current market interest rates that are available to the Group for similar financial instruments.

2.11 Cash and Cash Equivalents

Cash and cash equivalents comprise cash in hand, bank deposits and short-term, highly liquid investments which are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value. For the purpose of the statement of cash flows, cash and cash equivalents are presented net of bank overdrafts which are repayable on demand and which form an integral part of the Group’s cash management.

2.12 Share Capital

Ordinary shares are classified as equity. Incremental costs directly attributable to the issuance of new ordinary shares are deducted against the share capital account.

2.13 Revenue Recognition Revenue is recognized as follows 2.13.1 Product licenses and related revenue

License fees are recognised, on delivery and subsequent milestone schedule as per the terms of the contract with the end user.

Implementation services are recognised as services are provided, when arrangements are on a time and material basis. Revenue for fixed price contracts is recognised using the proportionate completion method. Balance revenue is recognised at the time of receipt of customer acceptance. Proportionate completion is measured based upon the efforts incurred to date in relation to the total estimated efforts to complete the contract. The Group monitors estimates of total contract revenue and cost on a routine basis throughout the delivery period. The cumulative impact of any change in estimates of the contract revenue or costs is reflected in the period in which the changes become known. In the event that a loss is anticipated on a particular contract, provision is made for the estimated loss.

Customization services are recognised based on the acceptance received from the customer for the milestone achieved.

Product maintenance revenue is recognised, over the period of the maintenance contract.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 25 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.13 Revenue Recognition - cont’d 2.13.2 IT solutions and consulting services

Revenue from IT solutions and consulting services are recognised as services are provided, when arrangements are on a time and material basis. Revenue from fixed price contracts is recognised using the proportionate completion method till contracts reach 90% completion. Balance revenue is recognised at the time of receipt of customer acceptance. Proportionate completion is measured based upon the efforts incurred to date in relation to the total estimated efforts to complete the contract. The Group monitors estimates of total contract revenue and cost on a routine basis throughout the delivery period. The cumulative impact of any change in estimates of the contract revenue or costs is reflected in the period in which the changes become known. In the event that a loss is anticipated on a particular contract, provision is made for the estimated loss. Cost and revenue in excess of billing is classified as unbilled revenue while billing in excess of revenue is classified as deferred revenue. Reimbursable expenses for projects are invoiced separately to customers and although reflected as sundry debtors to the extent outstanding as at year end, are not included as revenue or expense.

2.13.3 Interest income

Interest income is measured using the effective interest method.

2.14 Currency Translation 2.14.1 Functional and Presentation Currency

The functional currency of the Group is United States Dollar (USD or US$). As sales and purchases are denominated primarily in USD and receipts from operations are usually retained in USD, the directors are of the opinion that the USD reflects the economic substance of the underlying events and circumstances relevant to the Group.

2.14.2 Translation of Foreign Currency Transactions and Balances Transactions in a currency other than the functional currency (“foreign currency”) are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Currency translation gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the statement of comprehensive income.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 26 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.14 Currency Translation - cont’d

2.14.3 Translation of Group Entities’ Financial Statements

The results and financial position of group entities (none of which has the currency of a hyperinflationary economy) that have a functional currency different from the presentation currency are translated into the presentation currency as follows:

(i) Assets and liabilities for each balance sheet presented are translated at the

closing rate at the date of that balance sheet; (ii) Income and expenses for each statement of comprehensive income are

translated at average exchange rates (unless this average is not reasonable approximation of the cumulative effect of the rates prevailing on the translation dates, in which case income and expenses are translated at the dates of the transactions); and

(iii) All resulting exchange differences are taken to the foreign currency translation

reserve within equity.

Goodwill and fair value adjustments arising on acquisition of a foreign entity on or after 1 January 2005 are treated as assets and liabilities of the foreign entity and translated at the closing rate.

2.15 Leases

2.15.1 Operating Leases

Leases of assets in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases (net of any incentives received from the lessor) are taken to the statement of comprehensive income on a straight-line basis over the period of the lease. When an operating lease is terminated before the lease period has expired, any payment required to be made to the lessor by way of penalty is recognised as an expense in the period in which termination takes place.

2.15.2 Finance Leases

Leases of assets in which the Group assumes substantially the risks and rewards of ownership are classified as finance leases. Finance leases are capitalised at the inception of the lease at the lower of the fair value of the leased property and the present value of the minimum lease payments. Each lease payment is allocated between the liability and finance charges so as to achieve a constant rate on the finance balance outstanding. The corresponding rental obligations, net of finance charges, are included in borrowings. The interest element of the finance cost is taken to the statement of comprehensive income over the lease period so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 27 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.16 Related Parties

A related party is defined as follows:

(a) A person or a close member of that person’s family is related to the Group and Company if that person:

(i) Has control or joint control over the Company; (ii) Has significant influence over the Company; or (iii) Is a member of the key management personnel of the Group or Company

or of a parent of the Company.

(b) An entity is related to the Group and the Company if any of the following conditions applies:

(i) The entity and the Company are members of the same group (which means that each parent, subsidiary and fellow subsidiary is related to the others).

(ii) One entity is an associate or joint venture of the other entity (or and associate or joint venture of a member of a group of which the other entity is a member).

(iii) Both entities are joint ventures of the same third party. (iv) One entity is a joint venture of a third entity and the other entity is an

associate of the third entity. (v) The entity is a post-employment benefit plan for the benefit of employees of

either the Company or an entity related to the Company. If the Company is itself such a plan, the sponsoring employers are also related to the Company;

(vi) The entity is controlled or jointly controlled by a person identified in (a); (vii) A person identified in (a)(i) has significant influence over the entity or is a

member of the key management personnel of the entity (or of a parent of the entity).

2.17 Provisions

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event, it is more likely than not that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate can be made of the amount of the obligation.

Where the Group expects some or all of a provision to be reimbursed, the reimbursement is recognised as a separate asset but only when the reimbursement is virtually certain. The expense relating to any provision is presented in the statement of comprehensive income net of any reimbursement.

If the effect of the time value of money is material, provisions are discounted using a current pre-tax rate that reflects, where appropriate, the risks specific to the liability. Where discounting is used, the increase in the provision due to the passage of time is recognised as finance costs.

Provisions are reviewed at each balance sheet date and adjusted to reflect the current best estimates. If it is no longer probable that an outflow of resources embodying economic benefits will be required to settle the obligation, the provision is reversed.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 28 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d 2.18 Income Taxes

Current income tax liabilities (and assets) for the current and prior periods are recognised at the amounts expected to be paid to (or recovered from) the tax authorities. The tax rates and tax laws used to compute the amounts are those that are enacted or substantively enacted by the balance sheet date.

Deferred income tax assets/liabilities are recognised for all deductible taxable temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the financial statements except when the deferred income tax assets/liabilities arise from the initial recognition of an asset or liability in a transaction that is not a business combination and at the time of the transaction, affects neither accounting nor taxable profit or loss.

Deferred income tax liability is recognised on temporary differences arising on investments in subsidiaries, except where the Group is able to control the timing of the reversal of the temporary difference and it is probable that the temporary difference will not reverse in the foreseeable future. Deferred income tax asset is recognised to the extent that it is probable that future taxable profit will be available against which the temporary differences can be utilised.

Deferred income tax assets and liabilities are measured at:

(i) the tax rates that are expected to apply when the related deferred income tax asset is realised or the deferred income tax liability is settled, based on tax rates (and tax laws) that have been enacted or substantially enacted by the balance sheet date; and

(ii) the tax consequence that would follow from the manner in which the Group expects, at the balance sheet date, to recover or settle the carrying amounts of its assets and liabilities.

Current and deferred income taxes are recognised as income or expenses in the statement of comprehensive income for the period, except to the extent that the tax arises from a business combination or a transaction which is recognised directly in equity. Deferred tax on temporary differences arising from the revaluation gains and losses on land and buildings, fair value gains and losses on available-for-sale financial assets and cash flow hedges, and the liability component of convertible debts are charged or credited directly to equity in the same period the temporary differences arise. Deferred tax arising from a business combination is adjusted against goodwill on acquisition.

2.19 Employee Benefits

2.19.1 Defined Contribution Pension Costs

Defined contribution plans are post-employment benefit plans under which the Group pays fixed contributions into separate entities such as the Central Provident Fund, and will have no legal or constructive obligation to pay further contributions if any of the funds do not hold sufficient assets to pay all employee benefits relating to employee services in the current and preceding financial years. The Group’s contribution to defined contribution plans are recognised in the financial year to which they relate.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 29 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - cont’d

2.19 Employee Benefits - cont’d

2.19.2 Employee Leave Entitlement

Employee entitlements to annual leave are recognised when they accrue to employees. A provision is made for the estimated liability for leave as a result of services rendered by employees up to balance sheet date.

2.20 Government Grants

Grants from the government are recognised as a receivable at their fair value when there is reasonable assurance that the grant will be received and the Company will comply with all the attached conditions.

Government grants receivable are recognised as income over the periods necessary to match them with the related costs which they are intended to compensate, on a systematic basis. Government grants relating to expenses are shown separately as other income.

Where the grant relates to an asset, the fair value is recognized as deferred government grant on the balance sheet and is amortised as income on a systematic and rational basis over the useful life of the asset.

Alternatively, government grant relating to an asset may be presented in the balance sheet by deducting the grant at the carrying amount of the assets. The grant is recognised as income over the life of a depreciable asset by way of a reduced depreciation charge.

Jobs credit grants, which are government grants given to match staff and business costs, are recognised in the month of payment only as certain conditions have to be fulfilled before payment.

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 30 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

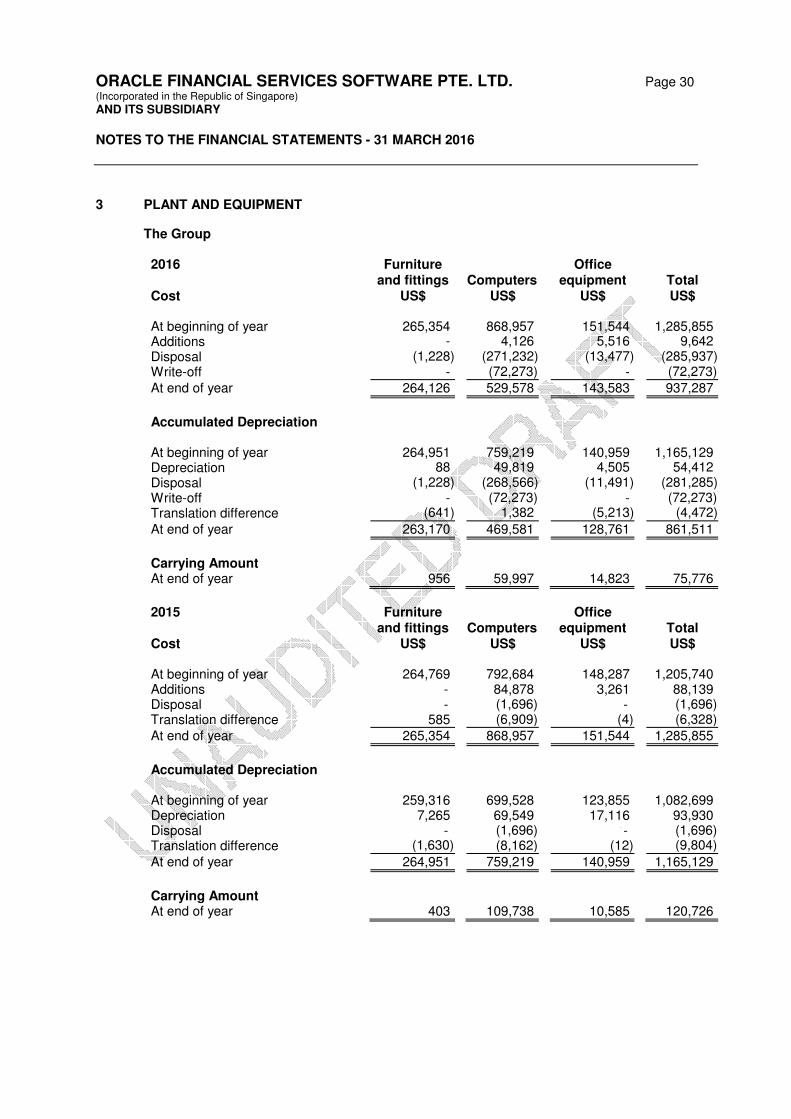

3 PLANT AND EQUIPMENT The Group

2016

Furniture and fittings

Computers

Office equipment

Total

Cost US$ US$ US$ US$ At beginning of year 265,354 868,957 151,544 1,285,855 Additions - 4,126 5,516 9,642 Disposal (1,228) (271,232) (13,477) (285,937) Write-off - (72,273) - (72,273)

At end of year 264,126 529,578 143,583 937,287

Accumulated Depreciation At beginning of year 264,951 759,219 140,959 1,165,129 Depreciation 88 49,819 4,505 54,412 Disposal (1,228) (268,566) (11,491) (281,285) Write-off - (72,273) - (72,273) Translation difference (641) 1,382 (5,213) (4,472)

At end of year 263,170 469,581 128,761 861,511

Carrying Amount At end of year 956 59,997 14,823 75,776

2015

Furniture and fittings

Computers

Office equipment

Total

Cost US$ US$ US$ US$ At beginning of year 264,769 792,684 148,287 1,205,740 Additions - 84,878 3,261 88,139 Disposal - (1,696) - (1,696) Translation difference 585 (6,909) (4) (6,328)

At end of year 265,354 868,957 151,544 1,285,855

Accumulated Depreciation At beginning of year 259,316 699,528 123,855 1,082,699 Depreciation 7,265 69,549 17,116 93,930 Disposal - (1,696) - (1,696) Translation difference (1,630) (8,162) (12) (9,804)

At end of year 264,951 759,219 140,959 1,165,129

Carrying Amount At end of year 403 109,738 10,585 120,726

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 31 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

3 PLANT AND EQUIPMENT The Company

2016

Furniture and fittings

Computers

Office equipment

Total

Cost US$ US$ US$ US$ At beginning of year 265,354 796,684 151,544 1,213,582 Additions - 4,126 5,516 9,642 Disposals (1,228) (271,232) (13,477) (285,937)

At end of year 264,126 529,578 143,583 937,287

Accumulated Depreciation and Impairment At beginning of year 264,951 686,946 140,959 1,092,856 Depreciation 88 49,819 4,505 54,412 Disposals (1,228) (268,566) (11,490) (281,285) Adjustments (641) 1,382 (5,213) (4,472)

At end of year 263,170 469,581 128,761 861,511

Carrying Amount At end of year 956 59,997 14,822 75,776

2015

Furniture and fittings

Computers

Office equipment

Total

Cost US$ US$ US$ US$ At beginning of year 264,769 711,702 148,287 1,124,758 Additions - 84,878 3,261 88,139 Translation difference 585 104 (4) 685 At end of year 265,354 796,684 151,544 1,213,582

Accumulated Depreciation and Impairment At beginning of year 259,316 618,546 123,855 1,001,717 Depreciation 7,265 69,549 17,116 93,930 Translation difference (1,630) (1,149) (12) (2,791)

At end of year 264,951 686,946 140,959 1,092,856

Carrying Amount At end of year 403 109,738 10,585 120,726

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 32 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

4 INVESTMENT IN SUBSIDIARY

The Company

2016 US$

2015 US$

Unquoted investment, at cost 1,150,184 1,150,184 Impairment loss (1,150,184) (1,150,184)

- -

Details of the subsidiary is as follows: Name of company

Principal activities

Country of incorporation and business

Effective equity held by the Company

2016 %

2015 %

Oracle Financial Services Consulting Pte Ltd*

Provision of computer software and technology services

Republic of Singapore 100 100

* Audited by Rohan • Mah & Partners, Singapore LLP

* In financial year 2013, the Management recognised an impairment loss of US$1,150,184 as the subsidiary has been operating at a loss and was in a negative equity position as at balance sheet date.

5 INTANGIBLE ASSETS

The Group 2016 2015 US$ US$

At fair values Customer contracts 556,364 556,364 Customer relationships 416,851 416,851 Less: Amortisation

973,215 (973,215)

973,215

(973,215) - -

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 33 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

6 TRADE RECEIVABLES

The Group The Company

2016 2015 2016 2015 US$ US$ US$ US$

Outside parties 5,571,874 6,605,607 5,571,874 6,605,607 Less: Impairment Balance at beginning of year 1,508,764 1,048,906 1,508,764 1,048,906 Allowance made during the year 85,280 1,508,764 85,280 1,508,764 Written off during the year Written back during the year

(192,989) (774,758)

- (1,048,906)

(192,989) (774,758)

- (1,048,906)

Balance at end of year 626,297 1,508,764 626,297 1,508,764 4,945,577 5,096,843 4,945,577 5,096,843 Related parties 18,922,751 25,898,919 18,922,751 25,898,919 Total 23,868,328 30,995,762 23,868,328 30,995,762

The Group and the Company does not have concentration of credit risk in respect of a customer or a group of customers.

The aging of trade receivables at the reporting date is:

The Group

The maximum exposure of credit risk for trade receivables at the reporting date is US$23,868,328 (2015: US$30,995,762).

Gross Impairment

losses

Gross Impairment

losses 2016 2016 2015 2015 US$ US$ US$ US$

Not past due 13,147,774 - 10,434,405 - Past due 31 - 120 days 5,573,139 - 16,317,112 655,068 Past due 121 - 365 days 3,883,088 130,869 5,108,668 226,240 More than one year 1,890,624 495,428 644,341 627,456 24,494,625 626,297 32,504,526 1,508,764

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 34 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

6 TRADE RECEIVABLES - cont’d

The Company The maximum exposure of credit risk for trade receivables at the reporting date is US$23,570,485 (2015: US$30,995,762).

Gross Impairment

losses

Gross Impairment

losses 2016 2016 2015 2015 US$ US$ US$ US$

Not past due 13,147,774 - 10,434,405 - Past due 31 - 120 days 5,573,139 - 16,317,112 655,068 Past due 121 - 365 days 3,883,088 130,869 5,108,668 226,240 More than one year 1,890,624 495,428 644,341 627,456 24,494,625 626,297 32,504,526 1,508,764

Based on historical default rates, the Group and the Company believes that no impairment allowance is necessary in respect of trade receivables not past due and past due up to 365 days. These receivables are mainly arising by customers that have good record with the Company. The carrying amounts of trade receivables approximate their fair values and are denominated in the following currencies: The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Australian Dollar 7,935,529 14,703,306 7,935,529 14,703,306

Singapore Dollar 1,997,097 607,151 1,997,097 607,151

United States Dollar 11,734,280 13,347,454 11,734,280 13,347,454

Others 2,201,422 2,337,851 2,201,422 2,337,851

23,868,328 30,995,762 23,868,328 30,995,762

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 35 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

7 OTHER RECEIVABLES

The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Advance costs (Note 16) 2,384,711 12,998,555 2,384,711 12,998,555 Amount due from immediate holding company - non-trade

21,127,874

17,437,008

21,118,065

17,420,430

Amount due from related companies - non-trade

2,334,178

286,460

2,334,178

286,460

Amount due from subsidiary - non-trade

-

-

-

3,836,677

Deposit 70,725 89,539 70,725 89,539 Prepayments 306,479 551,683 306,479 551,683 Other debtors 152,044 216,676 152,444 216,676 26,376,011 31,579,921 26,366,602 35,400,020

The amounts due from ultimate holding, immediate holding, related companies and subsidiary company are unsecured, interest free and repayable on demand.

The advance costs relate to the costs rendered by the immediate holding company for projects, which will be charged to the statement of comprehensive income in the future periods. The carrying amounts of other receivables approximate their fair values and are denominated in the following currencies:

The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Australian Dollar 14,880,029 18,996,701 14,880,029 19,022,307 Singapore Dollar 3,576,194 5,565,841 3,566,785 9,293,283 United States Dollar 5,717,648 3,693,299 5,717,648 3,771,378 Others 2,202,140 3,324,080 2,202,140 3,313,052

26,376,011 31,579,921 26,366,602 35,400,020

8 CASH AND CASH EQUIVALENTS

The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Cash and bank balances 10,088,965 21,648,538 9,751,427 21,318,224

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 36 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

8 CASH AND CASH EQUIVALENTS - cont’d

The carrying amounts of cash and cash equivalents approximate their fair values and are denominated in the following currencies:

The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Australian Dollar 3,192,918 2,157,842 3,192,918 2,157,842 Singapore Dollar 4,560,524 5,571,385 4,254,810 5,272,342 United States Dollar 943,900 1,678,490 912,077 1,647,219 Others 1,391,623 12,240,821 1,391,622 12,240,821 10,088,965 21,648,538 9,751,427 21,318,224

9 TRADE AND OTHER PAYABLES

The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Trade creditors 1,496,022 1,392,461 1,478,142 1,374,633 Advance billings 7,991,187 15,669,520 7,991,187 15,669,520 Amount due to immediate holding company - trade

21,470,741

38,213,796

21,470,741

38,213,796

Amount due to related company – trade

1,411,293

5,932,310

1,411,293

5,932,310

Accrued operating expenses* 2,983,901 2,717,542 2,978,741 2,698,357 Other creditors 101,915 535,298 101,915 535,222 35,455,059 64,460,927 35,432,019 64,423,838

* Included in accrued operating expense is a provision for leave encashment to compensate which pertains to defined benefit plan on compensated absences given to employees. (Note 23)

The carrying amounts of trade and other payables approximate their fair values and are denominated in the followings currencies:

The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Australian Dollar 9,793,760 20,786,180 9,793,760 20,786,180 Singapore Dollar 3,764,495 3,017,169 3,764,495 2,997,907

United States Dollar 17,398,524 32,531,058 17,398,524 32,531,058

Others 4,498,280 8,126,520 4,475,240 8,108,693 35,455,059 64,460,927 35,432,019 64,423,838

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 37 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

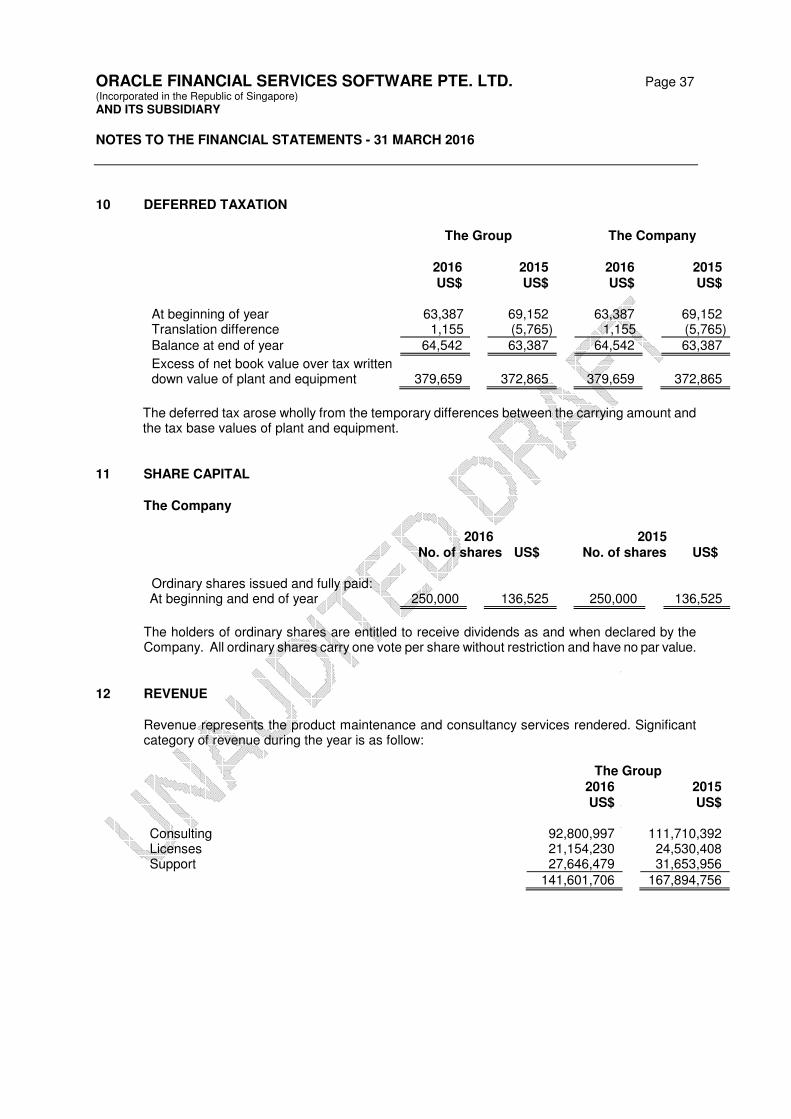

10 DEFERRED TAXATION

The Group The Company

2016

US$ 2015

US$ 2016

US$ 2015

US$ At beginning of year 63,387 69,152 63,387 69,152 Translation difference 1,155 (5,765) 1,155 (5,765) Balance at end of year 64,542 63,387 64,542 63,387

Excess of net book value over tax written down value of plant and equipment 379,659 372,865 379,659 372,865

The deferred tax arose wholly from the temporary differences between the carrying amount and the tax base values of plant and equipment.

11 SHARE CAPITAL The Company

2016 No. of shares US$

2015 No. of shares US$

Ordinary shares issued and fully paid: At beginning and end of year 250,000 136,525 250,000 136,525

The holders of ordinary shares are entitled to receive dividends as and when declared by the Company. All ordinary shares carry one vote per share without restriction and have no par value.

12 REVENUE Revenue represents the product maintenance and consultancy services rendered. Significant

category of revenue during the year is as follow:

The Group

2016 US$

2015 US$

Consulting 92,800,997 111,710,392 Licenses 21,154,230 24,530,408 Support 27,646,479 31,653,956 141,601,706 167,894,756

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 38 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

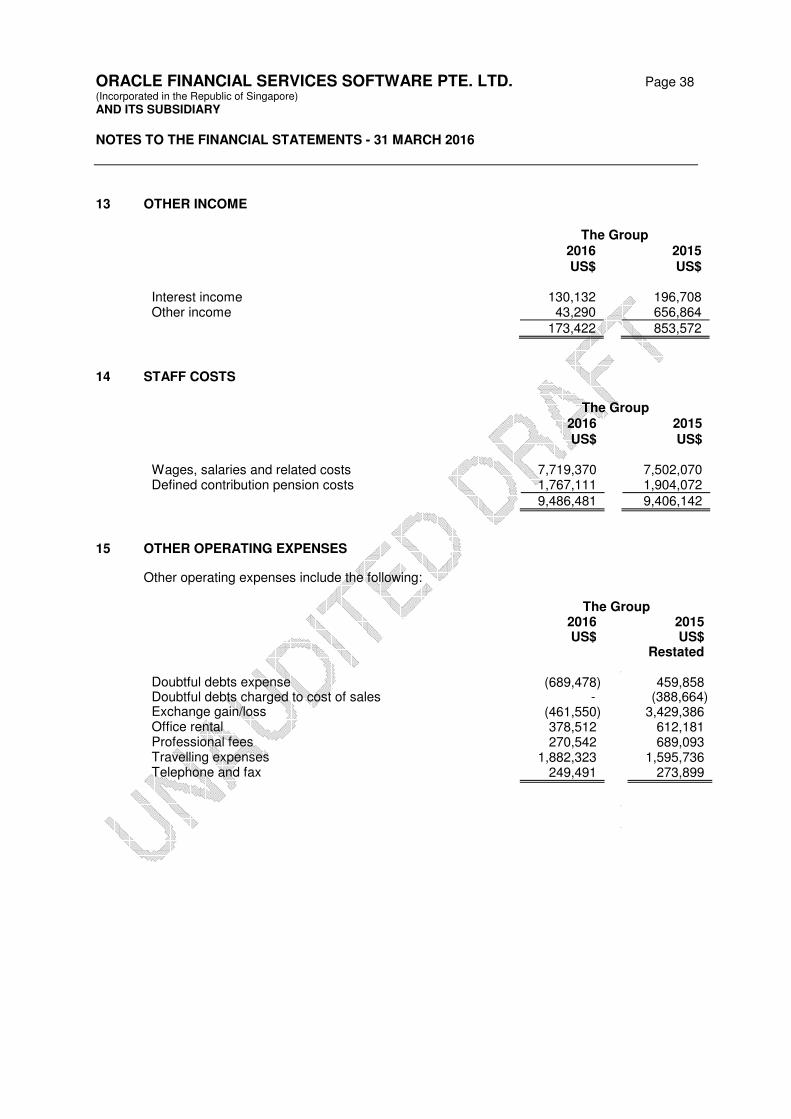

13 OTHER INCOME

The Group

2016 US$

2015 US$

Interest income 130,132 196,708 Other income 43,290 656,864 173,422 853,572

14 STAFF COSTS

The Group

2016 US$

2015 US$

Wages, salaries and related costs 7,719,370 7,502,070 Defined contribution pension costs 1,767,111 1,904,072 9,486,481 9,406,142

15 OTHER OPERATING EXPENSES

Other operating expenses include the following:

The Group

2016 US$

2015 US$

Restated

Doubtful debts expense (689,478) 459,858 Doubtful debts charged to cost of sales - (388,664) Exchange gain/loss (461,550) 3,429,386 Office rental 378,512 612,181 Professional fees 270,542 689,093 Travelling expenses 1,882,323 1,595,736 Telephone and fax 249,491 273,899

ORACLE FINANCIAL SERVICES SOFTWARE PTE. LTD. Page 39 (Incorporated in the Republic of Singapore)

AND ITS SUBSIDIARY

NOTES TO THE FINANCIAL STATEMENTS - 31 MARCH 2016

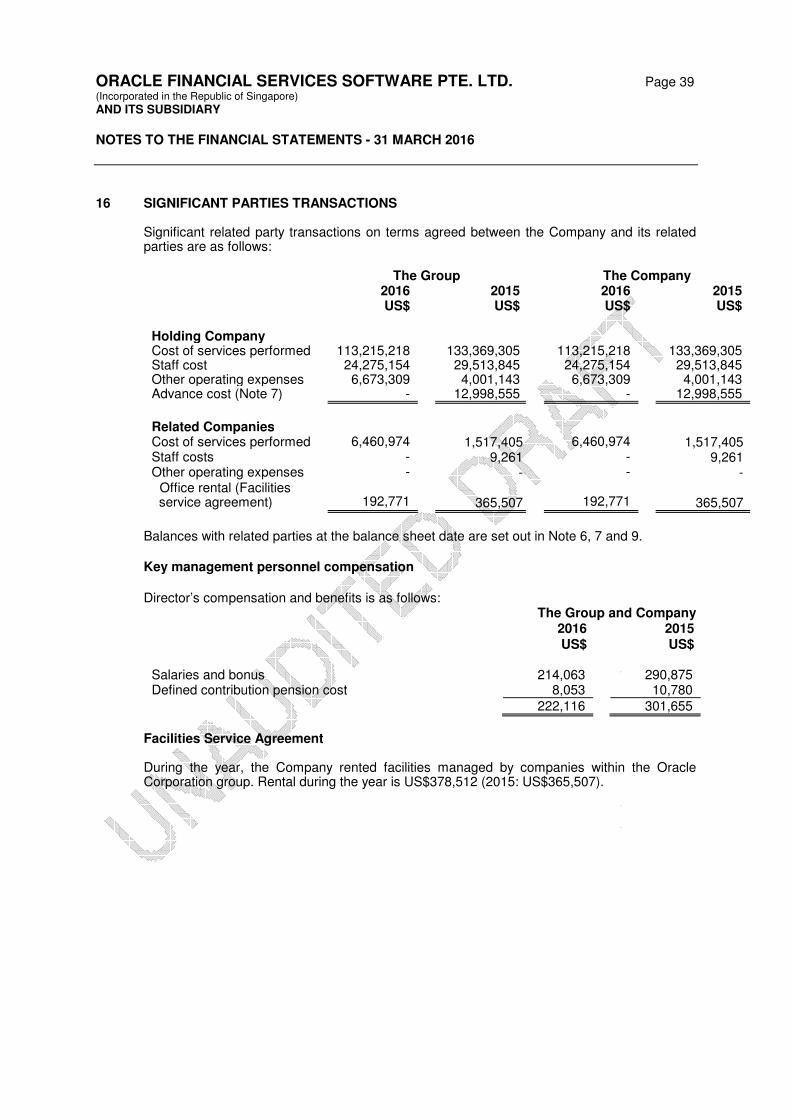

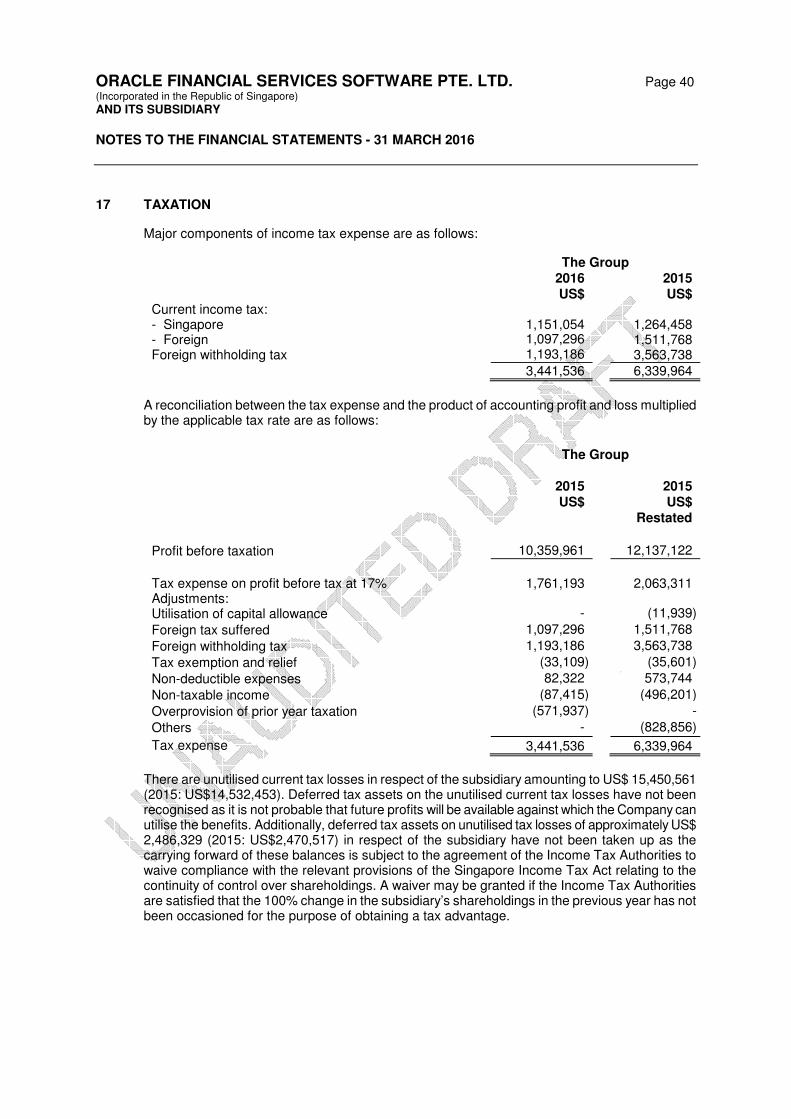

16 SIGNIFICANT PARTIES TRANSACTIONS

Significant related party transactions on terms agreed between the Company and its related parties are as follows:

The Group The Company

2016 US$

2015 US$

2016 US$

2015 US$

Holding Company Cost of services performed 113,215,218 133,369,305 113,215,218 133,369,305 Staff cost 24,275,154 29,513,845 24,275,154 29,513,845 Other operating expenses 6,673,309 4,001,143 6,673,309 4,001,143 Advance cost (Note 7) - 12,998,555 - 12,998,555

Related Companies Cost of services performed 6,460,974 1,517,405 6,460,974 1,517,405 Staff costs - 9,261 - 9,261 Other operating expenses - - - -

Office rental (Facilities service agreement)

192,771

365,507

192,771

365,507

Balances with related parties at the balance sheet date are set out in Note 6, 7 and 9.

Key management personnel compensation

Director’s compensation and benefits is as follows: The Group and Company

2016 US$

2015 US$

Salaries and bonus 214,063 290,875 Defined contribution pension cost 8,053 10,780 222,116 301,655

Facilities Service Agreement