ots maribor - mark hambly

TRANSCRIPT

www.british-business-bank.co.uk

@britishbbank

British Business Bank UK Guarantee Programmes

AECM Operational Training Session

Maribor

16th & 17th April 2015

www.british-business-bank.co.uk

@britishbbank

Contents

• Introduction to BBB (Slides 3-5)

• Use of Guarantees in UK (Slides 6-10)

• Links to further information (Slide 11)

2

www.british-business-bank.co.uk

@britishbbank

British Business Bank

• Change the structure of the finance markets for smaller businesses, so they work more effectively and dynamically

• This will help business prosper and build economic activity in the UK

• PLC since 1st November 2014.

An Economic Development

Bank A plc – 100% owned by UK Government

Working with 80 partners – banks, fund managers, angel networks, micro-finance

institutions etc.

3

www.british-business-bank.co.uk

@britishbbank

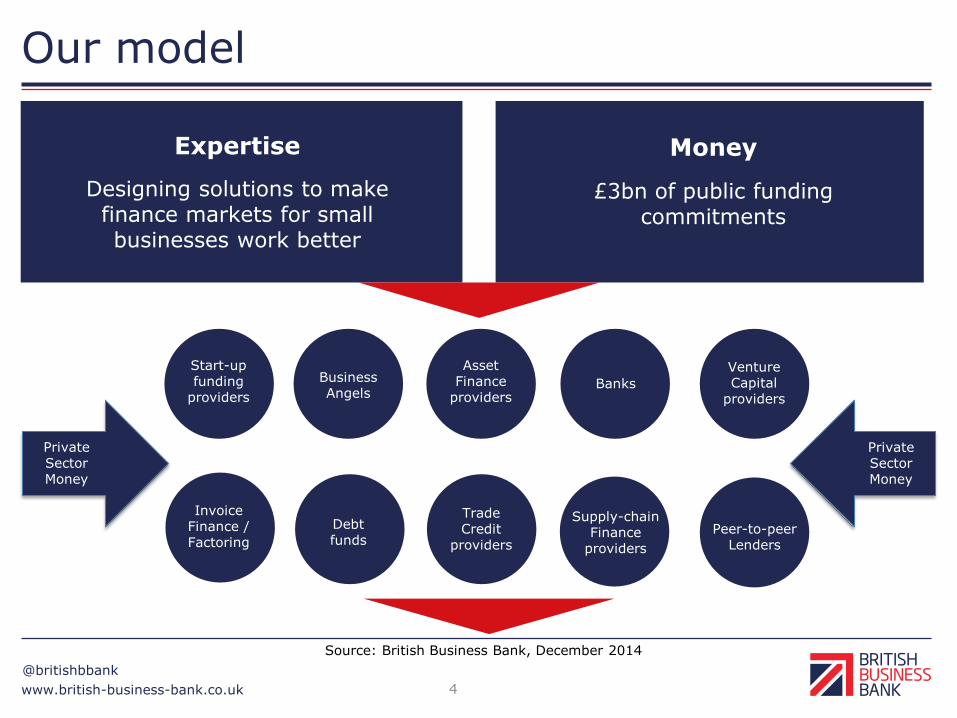

Our model

Start-up funding

providers

Business Angels

Asset Finance

providers Banks

Venture Capital

providers

Debt funds

Trade Credit

providers

Supply-chain Finance

providers

Peer-to-peer Lenders

Private Sector Money

Private Sector Money

Expertise

Designing solutions to make finance markets for small businesses work better

Money

£3bn of public funding commitments

Invoice

Finance / Factoring

4

Source: British Business Bank, December 2014

www.british-business-bank.co.uk

@britishbbank

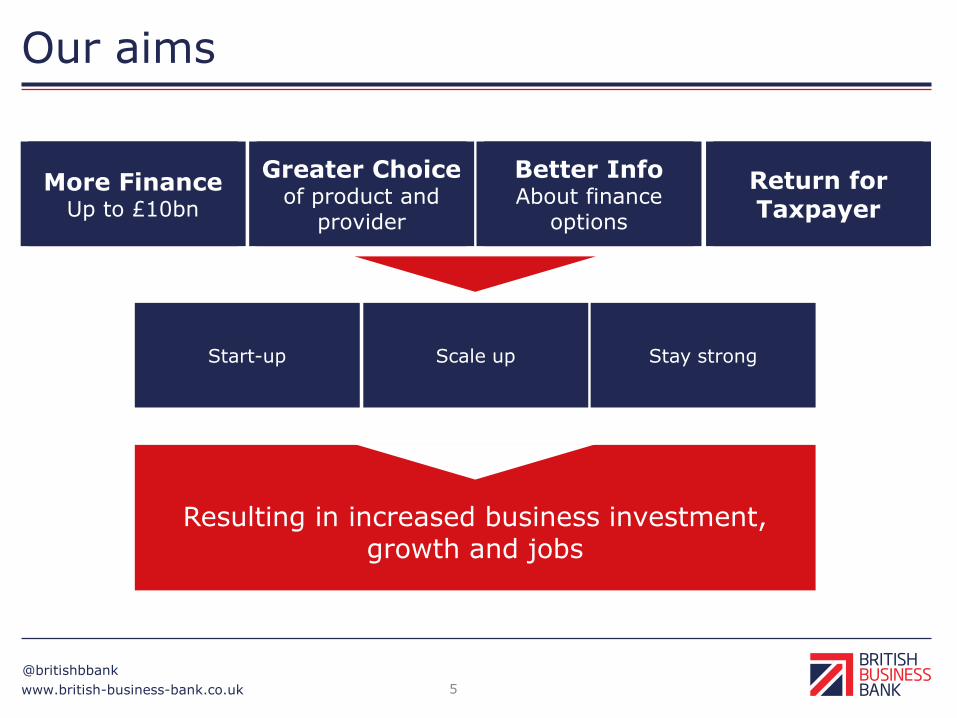

Our aims

More Finance

Up to £10bn

Greater Choice of product and

provider

Better Info About finance

options

Return for Taxpayer

Start-up Scale up Stay strong

Resulting in increased business investment, growth and jobs

5

www.british-business-bank.co.uk

@britishbbank

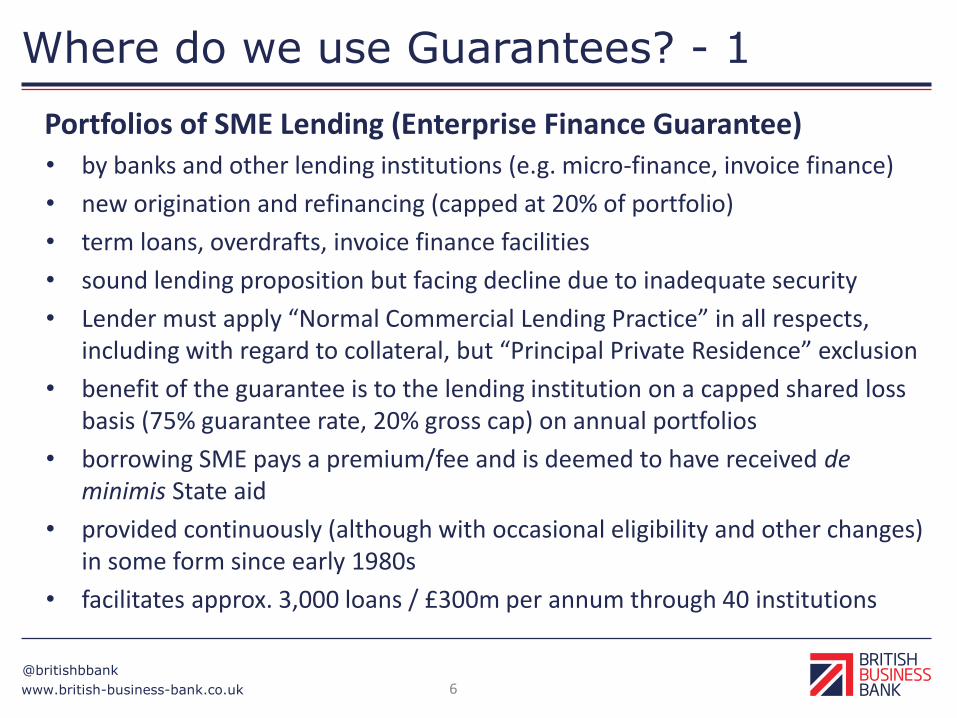

Where do we use Guarantees? - 1

Portfolios of SME Lending (Enterprise Finance Guarantee) • by banks and other lending institutions (e.g. micro-finance, invoice finance)

• new origination and refinancing (capped at 20% of portfolio)

• term loans, overdrafts, invoice finance facilities

• sound lending proposition but facing decline due to inadequate security

• Lender must apply “Normal Commercial Lending Practice” in all respects, including with regard to collateral, but “Principal Private Residence” exclusion

• benefit of the guarantee is to the lending institution on a capped shared loss basis (75% guarantee rate, 20% gross cap) on annual portfolios

• borrowing SME pays a premium/fee and is deemed to have received de minimis State aid

• provided continuously (although with occasional eligibility and other changes) in some form since early 1980s

• facilitates approx. 3,000 loans / £300m per annum through 40 institutions

6

www.british-business-bank.co.uk

@britishbbank

More on the Enterprise Finance Guarantee

7

• Sovereign Guarantee

• provided by Secretary of State for Business, Innovation & Skills

• to Lending Institution, not Borrower

• financial benefit of the guarantee is to the lending institution on a capped shared loss basis (75% guarantee rate, 20% gross cap) on annual portfolios

• single indivisible transaction – not separate “guaranteed” and “commercial” portions

• transactional decision-making devolved to Lending Institution but reported to BBB on-line and guarantee confirmed immediately

• borrowing SME aware of Guarantee BUT NOT a party to it

• Government as Guarantor is aware of Lending institution’s valuation but has no direct rights to security held by Lending Institution

• a guarantee, not a form of insurance

• Each Lender determines own treatment for regulatory capital purposes

www.british-business-bank.co.uk

@britishbbank

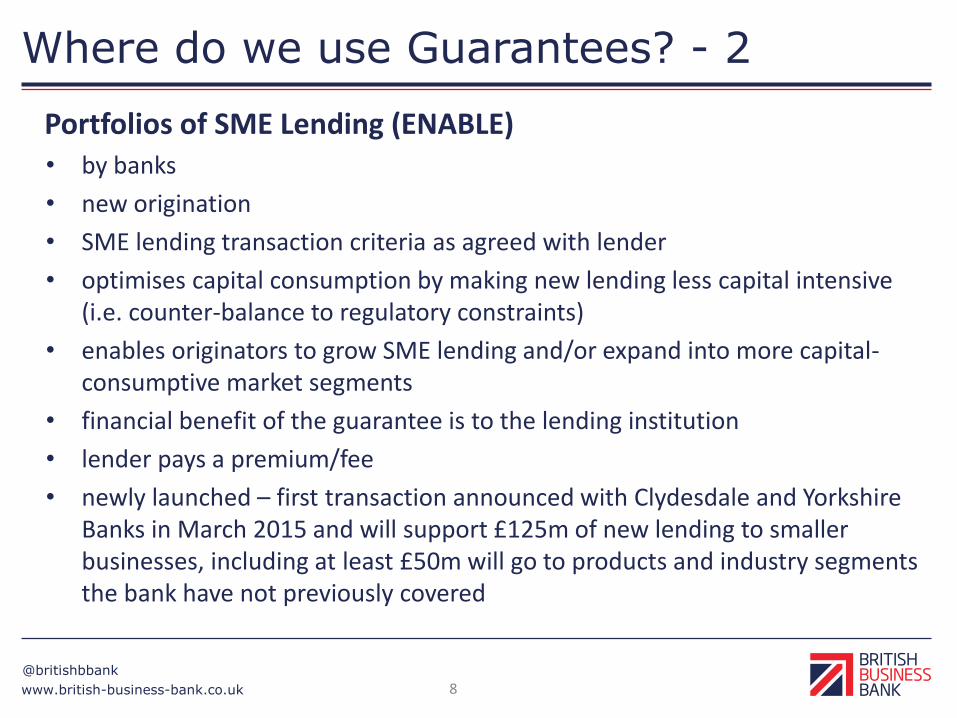

Where do we use Guarantees? - 2

Portfolios of SME Lending (ENABLE) • by banks

• new origination

• SME lending transaction criteria as agreed with lender

• optimises capital consumption by making new lending less capital intensive (i.e. counter-balance to regulatory constraints)

• enables originators to grow SME lending and/or expand into more capital-consumptive market segments

• financial benefit of the guarantee is to the lending institution

• lender pays a premium/fee

• newly launched – first transaction announced with Clydesdale and Yorkshire Banks in March 2015 and will support £125m of new lending to smaller businesses, including at least £50m will go to products and industry segments the bank have not previously covered

8

www.british-business-bank.co.uk

@britishbbank

Where do we use Guarantees? - 3

Portfolios of SME Lending (Growth Loans) • by banks and other lending institutions (e.g. debt funds)

• principally new origination

• term loans, including possibility of deferred repayments and possible up-side participation (i.e. mezzanine structures)

• focus on sound propositions (£500k-£2m) which are not currently within lender appetite, generally because of the high cost of due diligence for smaller deals and the lack of track record for the asset class

• financial benefit of the guarantee is to the lending institution on a capped shared loss basis

• payment of premium/fee and State aid treatment determined according to structure of individual lender proposals

• Request for Proposals issued 18th March 2015

9

www.british-business-bank.co.uk

@britishbbank

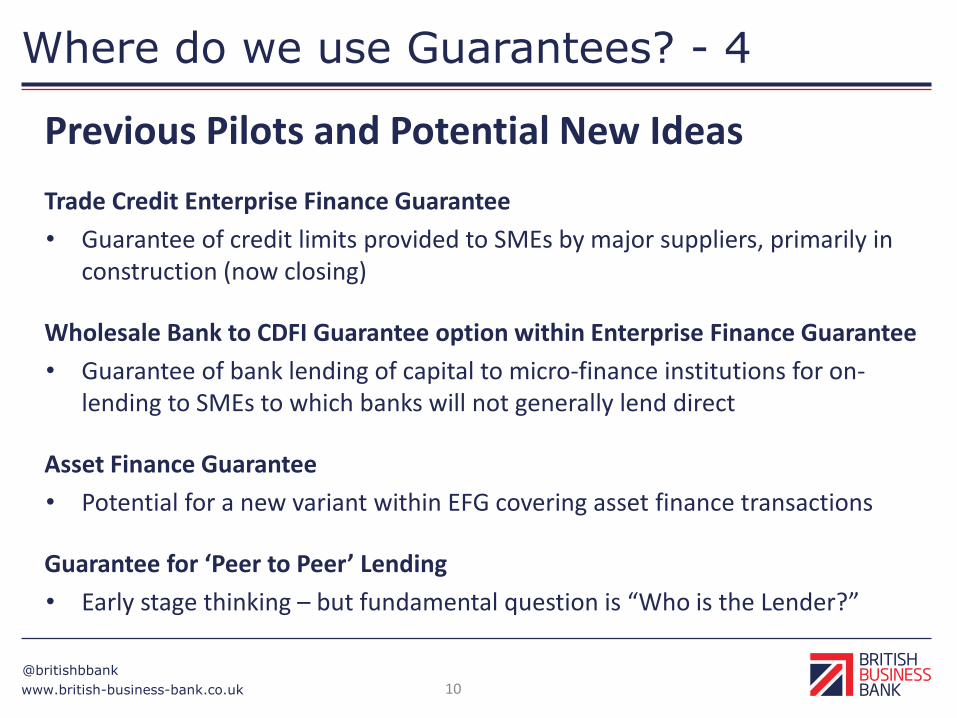

Where do we use Guarantees? - 4

Previous Pilots and Potential New Ideas

Trade Credit Enterprise Finance Guarantee

• Guarantee of credit limits provided to SMEs by major suppliers, primarily in construction (now closing)

Wholesale Bank to CDFI Guarantee option within Enterprise Finance Guarantee

• Guarantee of bank lending of capital to micro-finance institutions for on-lending to SMEs to which banks will not generally lend direct

Asset Finance Guarantee

• Potential for a new variant within EFG covering asset finance transactions

Guarantee for ‘Peer to Peer’ Lending

• Early stage thinking – but fundamental question is “Who is the Lender?”

10

www.british-business-bank.co.uk

@britishbbank

Links to other BBB Documents

Enterprise Finance Guarantee (EFG) Programme

http://british-business-bank.co.uk/market-failures-and-how-we-address-them/enterprise-finance-guarantee/

Evaluation of Trade Credit Enterprise Finance Guarantee Pilot

http://british-business-bank.co.uk/performance/evaluations-of-british-business-bank-programmes/trade-credit-enterprise-finance-guarantee-evaluation-and-response/

Growth Loans Pilot Programme

http://british-business-bank.co.uk/market-failures-and-how-we-address-them/growth-loans/

‘ENABLE’ Wholesale Guarantee

http://british-business-bank.co.uk/market-failures-and-how-we-address-them/wholesale-solutions/

11

British Business Bank plc is a public limited company registered in England and

Wales registration number 08616013, registered office at Foundry House, 3

Millsands, Sheffield, S3 8NH. As the holding company of the group operating under

the trading name of British Business Bank, it is a development bank wholly owned by

HM Government and is not authorised or regulated by the Prudential Regulation

Authority (PRA) or the Financial Conduct Authority (FCA). British Business Bank

operates under its own trading name through a number of subsidiaries, one of which

is authorised and regulated by the FCA.

British Business Finance Ltd (registration number 09091928), British Business Bank

Investments Ltd (registration number 09091930) and British Business Financial

Services Ltd (registration number 09174621) are wholly owned subsidiaries of British

Business Bank plc. These companies are all registered in England and Wales, with

their registered office at Foundry House, 3 Millsands, Sheffield, S3 8NH. They are not

authorised or regulated by the PRA or FCA.

Capital for Enterprise Fund Managers Limited is a wholly owned subsidiary of British

Business Bank plc, registered in England and Wales, registration number 06826072,

registered office at Foundry House, 3 Millsands, Sheffield, S3 8NH. It is authorised

and regulated by the FCA (FRN: 496977).

British Business Bank plc and its subsidiary entities are not banking institutions

and do not operate as such.

A complete legal structure chart for British Business Bank plc and its

subsidiaries can be found at www.british-business-bank.co.uk.

BBB 011214 22

www.british-business-bank.co.uk

@britishbbank