outdoor power equipment orientation guide · 2019-04-25 · “what you need to know” about...

TRANSCRIPT

200-130-00 Rev May 2019

Outdoor Power Equipment Orientation GuideCredit extended by Synchrony • www.synchronybusiness.com

Outdoor Power Equipment Orientation Guide

We’re delighted to help you help your customers!

NOTE: This is for INTERNAL USE ONLY and is not to be shared with consumers for any reason.

Credit extended by Synchrony • www.synchronybusiness.com

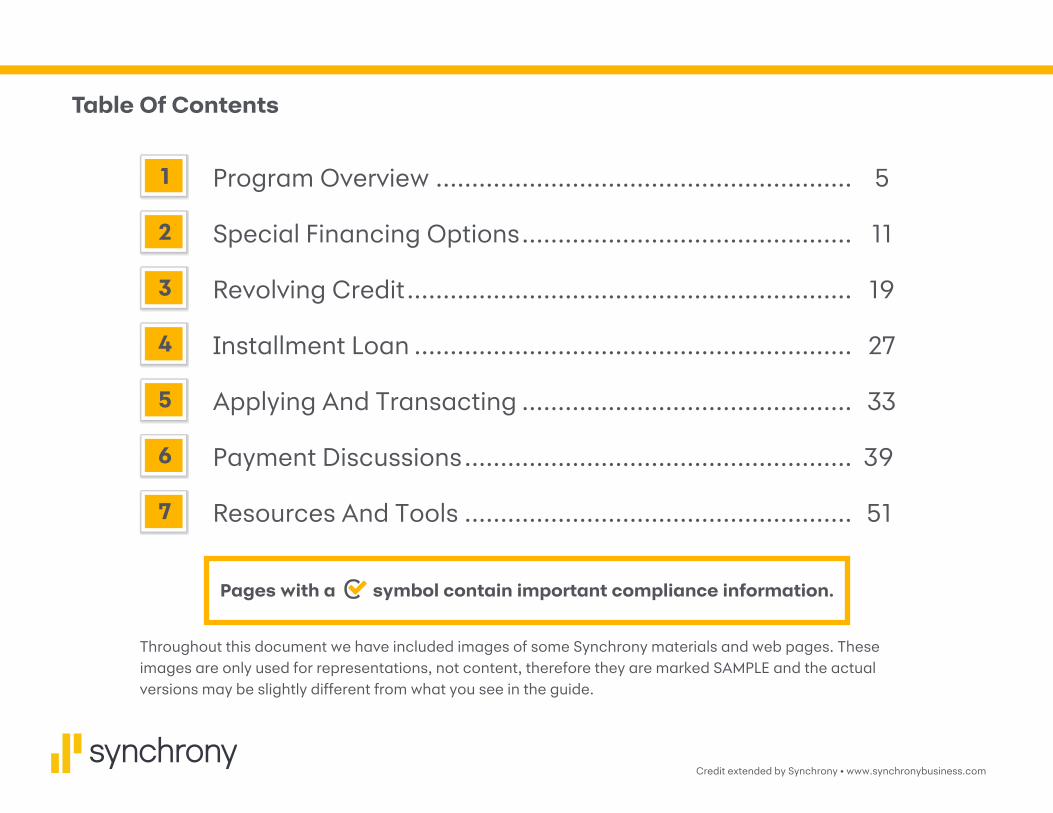

Table Of Contents

1 Program Overview .......................................................... 5

2 Special Financing Options .............................................. 11

3 Revolving Credit .............................................................. 19

4 Installment Loan ............................................................. 27

5 Applying And Transacting .............................................. 33

6 Payment Discussions ...................................................... 39

7 Resources And Tools ...................................................... 51

Pages with a symbol contain important compliance information.

Throughout this document we have included images of some Synchrony materials and web pages. These images are only used for representations, not content, therefore they are marked SAMPLE and the actual versions may be slightly different from what you see in the guide.

This page intentionally left blank.

Outdoor Power Equipment Orientation Guide – 51Credit extended by Synchrony • www.synchronybusiness.com

Program Overview

Let’s introduce ourselves!

Credit extended by Synchrony • www.synchronybusiness.com

– 61Outdoor Power Equipment Orientation Guide

What Are The Top Things You’d Like To Know Today?

_________________________________________________________________________________________________________

_________________________________________________________________________________________________________

_________________________________________________________________________________________________________

_________________________________________________________________________________________________________

Help Us Understand

Your Business

Action • Place a check next to the top 3 things you want to improve for your business.

q Increasing average ticket size

q Offering customers convenient special financing options

q Closing more sales

q Increasing customer satisfaction

q Attracting new customers

q Building customer loyalty

Credit extended by Synchrony • www.synchronybusiness.com

– 71Outdoor Power Equipment Orientation Guide

This Is The First Step To Offering Financing Options For Your Customers.

Today I will…

• Demonstrate how to achieve your business goals by offering a Synchrony credit card or installment loan (aka “financing”).

• Explain how your different financing options work.

• Show how financing can help your customers get what they really want or need. Review “What you need to know” about offering financing fairly and compliantly.

• Show how to comply with Federal and State regulations, such as UDAAP and Fair Lending. Get you set up and ready to introduce financing to your team and customers as part of your sales process.

We’re eager to understand your needs!

Credit extended by Synchrony • www.synchronybusiness.com

– 81Outdoor Power Equipment Orientation Guide

Who Benefits From Financing?*

Your Customers Can:

Buy what they want,when they want it,and pay how they want.

Your Business Can:

Get more sales,from more customers,with more loyalty.

PLUS…With your Synchrony financing program, you get payment in just 2 business days, and purchases are non-recourse**

Customers Benefit.You Benefit.

Everybody Wins.

Pause & Chat

• Have you ever bought anything using financing that you wouldn’t have purchased otherwise?

• Would there be any reason you wouldn’t offer it, along with other payment options, to every customer?

*Subject to credit approval.

**You must validate 2 forms of ID on the application for non-recourse. Subject to any chargeback rights in the Synchrony Merchant Agreement and compliance with Synchrony Operating Procedures. See your Operating Guide for additional information about fraud and chargebacks.

Credit extended by Synchrony • www.synchronybusiness.com

– 91Outdoor Power Equipment Orientation Guide

Financing Benefits All Consumers

Cash Management Upgrades Budgeting

“I like to take advantage of special financing offers and save my on-hand cash for other things”

Business Benefit:

Customer Loyalty

“I want to use financing to purchase a better product than I can get with on-hand cash”

Business Benefit:

Bigger Tickets

“I need to use financing to make a purchase at this time”

Business Benefit:

Close More Sales

This page intentionally left blank.

Outdoor Power Equipment Orientation Guide – 112Credit extended by Synchrony • www.synchronybusiness.com

Special Financing Options

Convenient, flexible options

Credit extended by Synchrony • www.synchronybusiness.com

– 122Outdoor Power Equipment Orientation Guide

Types Of Financing

Revolving Credit: • Allows customers to easily purchase again from you in the future

• Includes credit card

• Minimum purchase as low as $1, excludes promotional offers (see program rates)

• Customer lists for marketing to current customers, including available credit amounts

Installment Loan: • Provides funding for one-time purchases with no expected repeat business

• No credit card; customer must reapply to receive another loan

• $2,500 minimum purchase

Do you know your available promotions?

Credit extended by Synchrony • www.synchronybusiness.com

– 132Outdoor Power Equipment Orientation Guide

Financing Options Explained*

Deferred Interest:• Also known as “No Interest if Paid in Full”• Only available for Revolving credit; not Installment Loan• Minimum monthly payments are required, which may or may not pay off the promotional purchase by the end of the

promotional period. This means in order to pay the promotion in full before the end of the promotional period, the cardholder may need to pay more than the minimum monthly payments

• If monthly payments are made by their due dates and the purchase is paid in full within the promotional period, interest is not assessed on the promotional purchase

No Interest:• Often referred to as “Equal Pay,” “Zero Interest” or “0% for XX Months”• Available for both Revolving credit and Installment Loan• No interest is charged on the promotional purchase, regardless of the length of promotion • Monthly payments on promotional purchase are the same every month

Reduced Interest:• Often referred to as “Fixed Pay” for Revolving credit• Available for both Revolving credit and Installment Loan• A reduced interest rate is charged on the promotional purchase, regardless of the length of promotion• Monthly payments on promotional purchase are the same every month

Introductory Rate:• Often referred to as “Step Rate”• Only available for Installment Loan; not Revolving credit• A reduced interest rate is charged on the daily balance for an introductory period, then the interest rate is increased

to a higher fixed rate for the remainder of the loan• Monthly payments are the same every month during the introductory period, then increase to a higher fixed monthly

payment thereafter*Some promotions are not available in all markets.

Do you know your available promotions?

Credit extended by Synchrony • www.synchronybusiness.com

– 142Outdoor Power Equipment Orientation Guide

Flexible ways to manage paymentsDeferred Interest/No Interest If Paid In Full*

Repayment Scenarios For The Cardholder

Promotional Balance$0

No Interest Paid

$35 $815Minimum Payments + Payoff*

Promotional Balance$780 + $262.22Interest Owed

$35 $35Minimum Payments Only*

Equal Monthly Payments

Promotional Balance$0

No Interest Paid

$1,200 Twelve-Month Deferred Interest/No Interest if Paid in Full* Financing Option: 3 scenarios to show how the cardholders may choose to make monthly payments. Note that the outcomes below assume that there are no other balances on the cardholder’s account.

• Deferred Interest promotions only available for Revolving Credit; not Installment Loan

• In order to pay the promotion in full before the end of the promotional period, the cardholder may need to pay more than the required minimum monthly payments.

• Be sure that the cardholder understands the risks of not paying off the promotion before the end of the promotional term. Examples shown are for a 12 Month Deferred Interest promotion. Multiple promotional or other purchases on an account may change payment allocation.

• Minimum revolving monthly payments are calculated as the highest of $35 or 3.25% of new balance or $20 + Interest Charges + Late Payment Fees + Non-Sufficient Funds Fees

• Amount financed includes any applicable promotion fees

*The values used are for illustrative purposes only. Amounts may vary.

2

1

3

MONTHS 1-11 MONTH 12 OUTCOME

$100 $100

Interest Accruing

Interest Accruing

Interest Accruing

Credit extended by Synchrony • www.synchronybusiness.com

– 152Outdoor Power Equipment Orientation Guide

Things To Remember About Deferred Interest Promotions

• The customer must make at least minimum monthly payments. Note: making only minimum monthly payments may or may not pay off the promotional purchase by the end of the promotional period. This means in order to pay the promotion in full before the end of the promotional period, the cardholder may need to pay more than the minimum monthly payments.

• Interest accrues during the promotional period. To avoid paying the accrued interest, the entire promotional purchase balance must be paid in full by the end of the promotional period.

• If balance is not paid in full within the promotional period, the accrued interest is added to the account balance, and the balance will continue to bill interest at the account level Annual Percentage Rate until the balance is paid in full.

• Cardholder may be charged fees for late payments.

• Deferred Interest promotions are only available with Revolving Credit; not Installment Loan.

Credit extended by Synchrony • www.synchronybusiness.com

– 162Outdoor Power Equipment Orientation Guide

Used Unit Financing

To help you increase sales and profits, Synchrony also finances used equipment.

• Used units are typically not eligible for manufacturer-sponsored promotions, but may qualify for other financing offers.

• Actual available terms and interest rates may vary based on product and risk criteria.

• Log on to Business Center at bc.syf.com to review rate sheets and program details for more information on used unit financing, including interest rates and eligible models (and model years).

We finance used units!

Credit extended by Synchrony • www.synchronybusiness.com

– 172Outdoor Power Equipment Orientation Guide

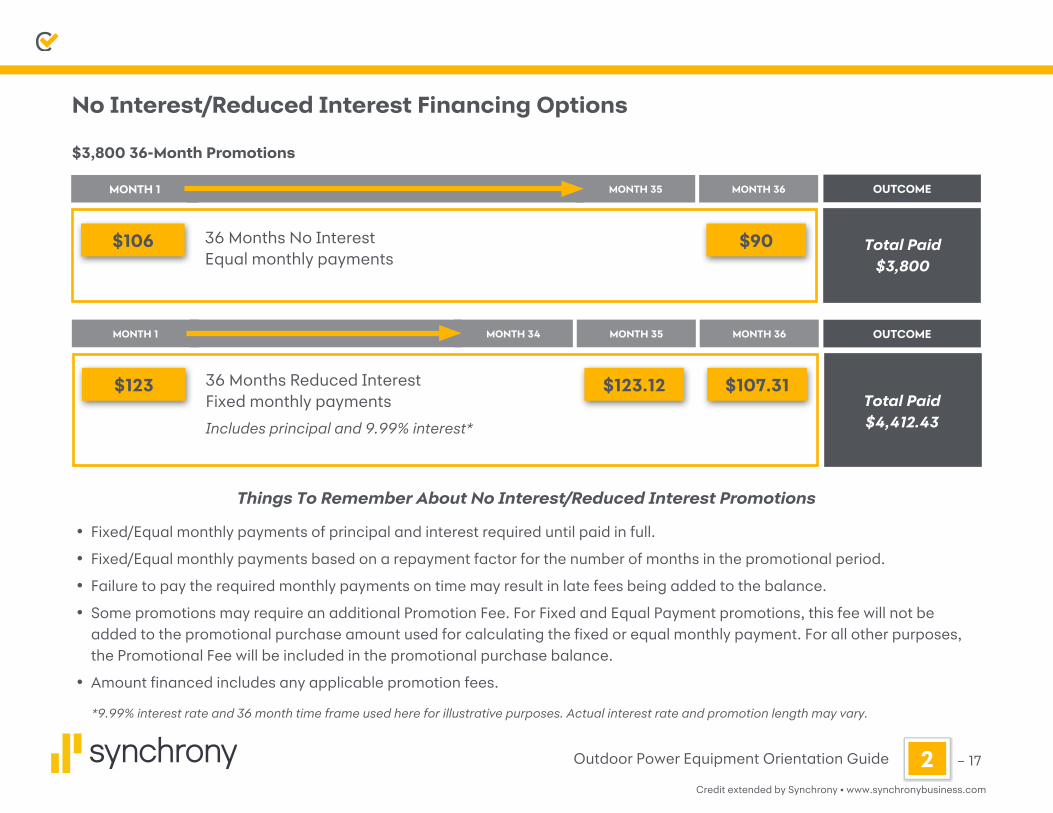

No Interest/Reduced Interest Financing Options

$3,800 36-Month Promotions

*9.99% interest rate and 36 month time frame used here for illustrative purposes. Actual interest rate and promotion length may vary.

Things To Remember About No Interest/Reduced Interest Promotions

• Fixed/Equal monthly payments of principal and interest required until paid in full.

• Fixed/Equal monthly payments based on a repayment factor for the number of months in the promotional period.

• Failure to pay the required monthly payments on time may result in late fees being added to the balance.

• Some promotions may require an additional Promotion Fee. For Fixed and Equal Payment promotions, this fee will not be added to the promotional purchase amount used for calculating the fixed or equal monthly payment. For all other purposes, the Promotional Fee will be included in the promotional purchase balance.

• Amount financed includes any applicable promotion fees.

Total Paid $4,412.43

$123

OUTCOME

36 Months Reduced InterestFixed monthly payments

Includes principal and 9.99% interest*

$123.12 $107.31

MONTH 1 MONTH 34 MONTH 35 MONTH 36

Total Paid $3,800

$106

MONTH 1 OUTCOME

36 Months No InterestEqual monthly payments

$90

MONTH 35 MONTH 36

This page intentionally left blank.

Outdoor Power Equipment Orientation Guide – 193Credit extended by Synchrony • www.synchronybusiness.com

Revolving Credit

How to apply and transact

Credit extended by Synchrony • www.synchronybusiness.com

– 203Outdoor Power Equipment Orientation Guide

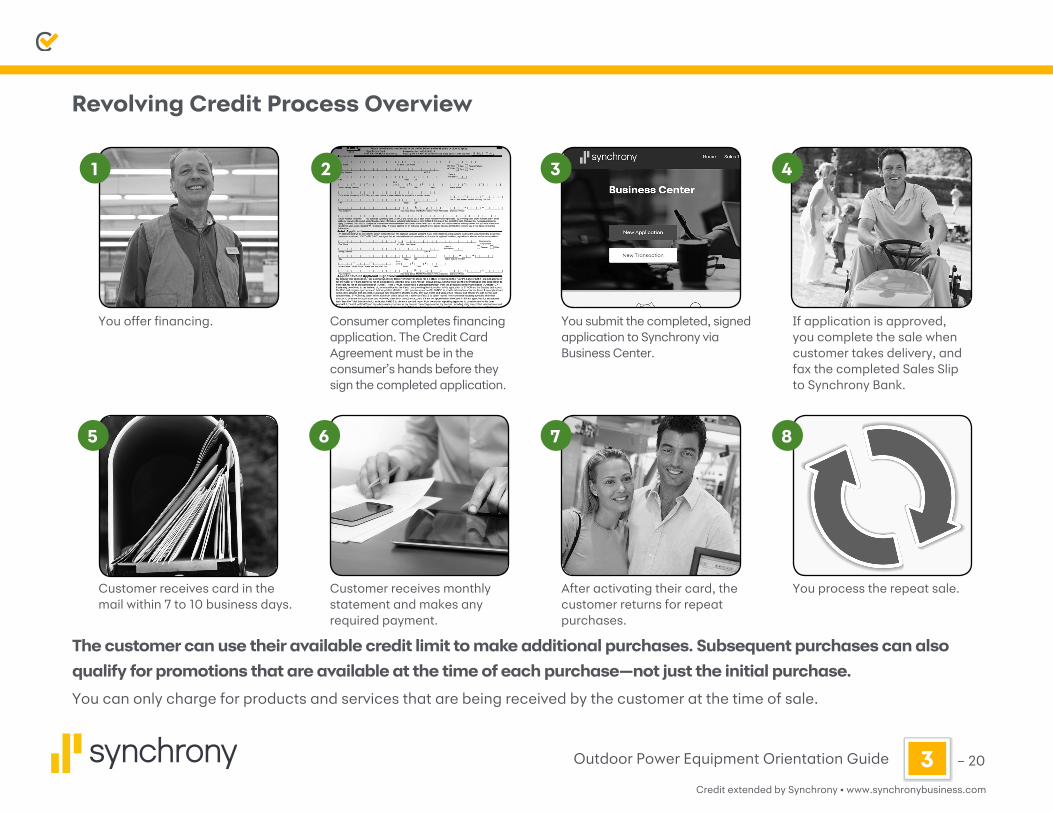

Revolving Credit Process Overview

You offer financing.

Customer receives card in the mail within 7 to 10 business days.

Consumer completes financing application. The Credit Card Agreement must be in the consumer’s hands before they sign the completed application.

Customer receives monthly statement and makes any required payment.

You submit the completed, signed application to Synchrony via Business Center.

After activating their card, the customer returns for repeat purchases.

You process the repeat sale.

If application is approved, you complete the sale when customer takes delivery, and fax the completed Sales Slip to Synchrony Bank.

1 2 3 4

5 6 7 8

The customer can use their available credit limit to make additional purchases. Subsequent purchases can also

qualify for promotions that are available at the time of each purchase—not just the initial purchase.

You can only charge for products and services that are being received by the customer at the time of sale.

Credit extended by Synchrony • www.synchronybusiness.com

– 213Outdoor Power Equipment Orientation Guide

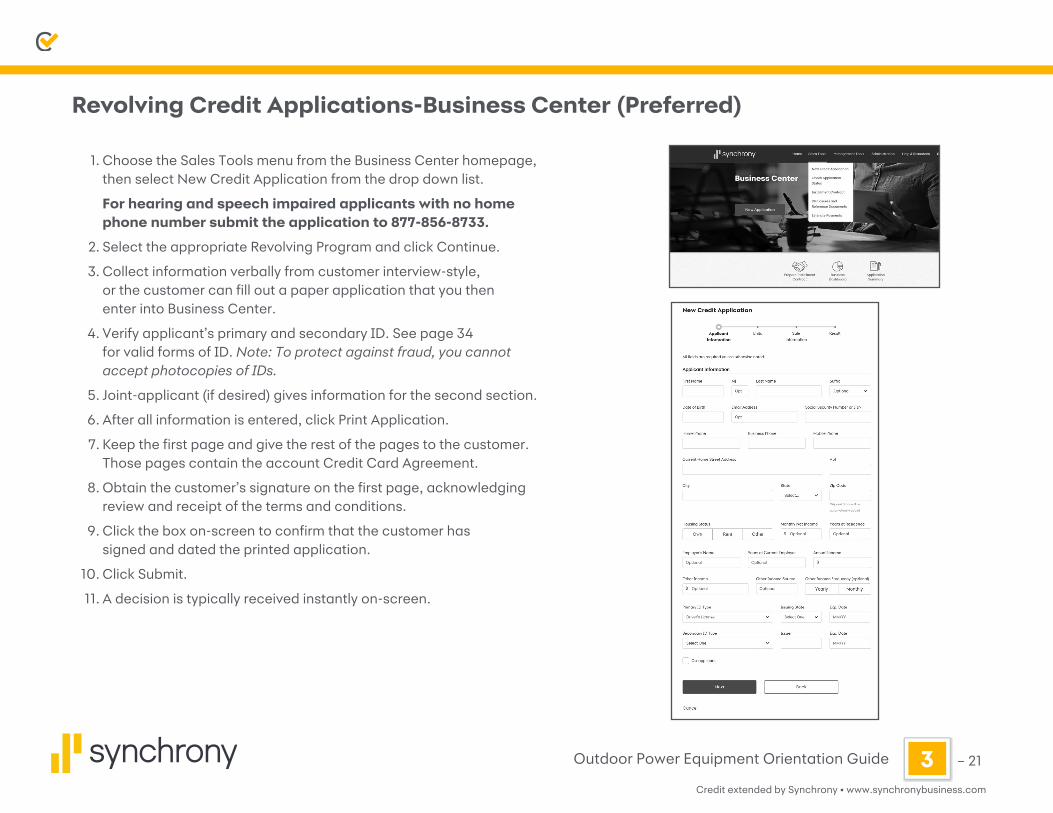

Revolving Credit Applications-Business Center (Preferred)

1. Choose the Sales Tools menu from the Business Center homepage, then select New Credit Application from the drop down list.

For hearing and speech impaired applicants with no home phone number submit the application to 877-856-8733.

2. Select the appropriate Revolving Program and click Continue.

3. Collect information verbally from customer interview-style, or the customer can fill out a paper application that you then enter into Business Center.

4. Verify applicant’s primary and secondary ID. See page 34 for valid forms of ID. Note: To protect against fraud, you cannot accept photocopies of IDs.

5. Joint-applicant (if desired) gives information for the second section.

6. After all information is entered, click Print Application.

7. Keep the first page and give the rest of the pages to the customer. Those pages contain the account Credit Card Agreement.

8. Obtain the customer’s signature on the first page, acknowledging review and receipt of the terms and conditions.

9. Click the box on-screen to confirm that the customer has signed and dated the printed application.

10. Click Submit.

11. A decision is typically received instantly on-screen.

Credit extended by Synchrony • www.synchronybusiness.com

– 223Outdoor Power Equipment Orientation Guide

Revolving Credit Applications-Paper

1. Customer fills out top section of application.

2. Joint applicant (if desired) completes the second section.

3. Make sure the customer has the opportunity to review the Credit Card Agreement of the application prior to signing.

4. If the customer doesn’t want to be considered for an Installment Loan in the event that they are declined for a Revolving Credit account, they should check the box above the applicant signature line.

5. Check to ensure all information is complete and the application is signed.

6. Verify applicant’s primary and secondary ID. See page 34 for valid forms of ID. Note: To protect against fraud, you cannot accept photocopies of IDs.

7. You complete the Store #, Store Fax # and Total Sale Amount sections at the bottom of the form.

8. Submit the application via fax to the number at the top of the form.

9. A decision will be faxed back within approximately 5 to 15 minutes. If the application is approved, enter the customer’s Account # from the approval notification at the bottom of the form.

Credit extended by Synchrony • www.synchronybusiness.com

– 233Outdoor Power Equipment Orientation Guide

After a customer is approved for Revolving Credit, they are ready to make a purchase. Here are the steps to complete that purchase in Business Center:

1. From the Business Center homepage, select Sales Tools, then choose Enter a Transaction from the drop-down menu.

2. Select the appropriate revolving program from the Program drop-down menu.

3. Select Purchase from the Transaction Type drop-down menu.

4. Enter the account number.

5. Enter the unit information, additional line items, tax, down payment, etc. and click Next.

6. Enter the Plan Number for the financing promotion being used for the purchase.

7. Verify all of the on-screen information is correct and click View Sales Slip.

8. Print the completed Sales Slip and hand it to the customer to sign. Be sure to explain to the customer that, depending on which promo they choose, a promotional fee will be added to their first statement by Synchrony Bank. Refer the customer to the language on the Sales Slip above the signature line.

9. Fax the Sales Slip to Synchrony for funding to the fax number shown at the top of the Sales Slip form.

Additional Notes: • If processing a return, please complete a ‘credit slip’ located in Business Center Sales Tools- Disclosures & Reference Documents

and fax to 800-924-3214. Questions? Call Dealer Services at 877-856-8733

• To look up a customer’s account number or available balance in Business Center, select Sales Tools-Look Up Account Information

Completing A Sale – Same Day Delivery

Credit extended by Synchrony • www.synchronybusiness.com

– 243Outdoor Power Equipment Orientation Guide

If the customer is making a purchase that will be delivered on a future date, follow these steps: From the Business Center homepage, select Sales Tools-Enter a Transaction.

1. Select the appropriate revolving program from the Program drop-down menu

2. Select Authorization Only from the Transaction Type menu

3. Enter the customer’s account number

4. Select if card is present (will automatically be set to “yes” if a card was swiped)

5. Click Next

6. Enter amount and cardholder name

7. Enter cardholder name and Tran/Promo Code if required

8. Click the Submit button to continue

9. Click Print Receipt

10. Obtain a customer signature on the Merchant Copy and file it in a secure location along with the customer’s financing application

11. Give the Customer Copy to the customer

When the product is delivered:

1. Complete the first step above, then select Purchase from the Transaction Type drop-down menu

2. Complete the fields on-screen, including the Authorization Code from the Merchant Copy of the receipt

3. Verify all of the on-screen information is correct and click View Sales Slip

4. Print the completed Sales Slip and fax it to Synchrony at the fax number shown at the top of the Sales Slip form

NOTE: Ensure that the amount of the sale and the promotion that the customer originally agreed to is what the customer receives on date of delivery. If not, the customer needs to receive the proper disclosures.

Completing A Sale – Future Delivery

Credit extended by Synchrony • www.synchronybusiness.com

– 253Outdoor Power Equipment Orientation Guide

How To Process A Credit Limit Increase Request

Note: You must have the customer’s consent to submit a credit limit increase request. A credit bureau may be performed just like a new credit application.

1. Click “Sales Tools” and choose “Request Credit Limit Increase” from the drop-down menu

2. Select a program from the drop down list

3. Enter Account Number, or App Key #, SSN and Zip Code, or Name and Phone Number and click “Search”

4. Click Continue

5. Verify customer with a valid ID

6. Enter Applicant Monthly Income, Housing Status and Requested Purchase Amount

7. Click the Submit button for approval and it will return a decision on the credit limit increase request

Credit extended by Synchrony • www.synchronybusiness.com

– 263Outdoor Power Equipment Orientation Guide

How to Process Fraud and Dispute Transactions

Efficiently process fraud dispute transactions using the Disputes Documentation Requests Tool. It also provides open, past due and pending fraud request.

To access the tool, location administrators must first grant access via the Users Permissions template. Select “Administration” then click “Manage Users.”

How to Register 1. Select “Management Tools” and click “Disputes Documentation

Requests.”

2. An Enrollment page will appear for unenrolled merchants

3. Fill in the required fields

4. Headquarter (HQ) Merchants-to update contact information for all child locations, check the box on topa decision on the credit limit increase request

a. All previously submitted information will be overwritten; upon first time login, child locations will be brought to the Dashboard page

Note: Child locations will not be able to update their contact information. All new dispute and dispositions of requests will go through the HQ Merchant

b. Child locations are responsible for enrolling and updating contact information if the HQ Merchant does not do it

c. To change preferences the HQ Merchant must call Merchant Services at 1-800-333-1082 for assistance

Outdoor Power Equipment Orientation Guide – 274Credit extended by Synchrony • www.synchronybusiness.com

Installment Loan

How to apply and transact

Credit extended by Synchrony • www.synchronybusiness.com

– 284Outdoor Power Equipment Orientation Guide

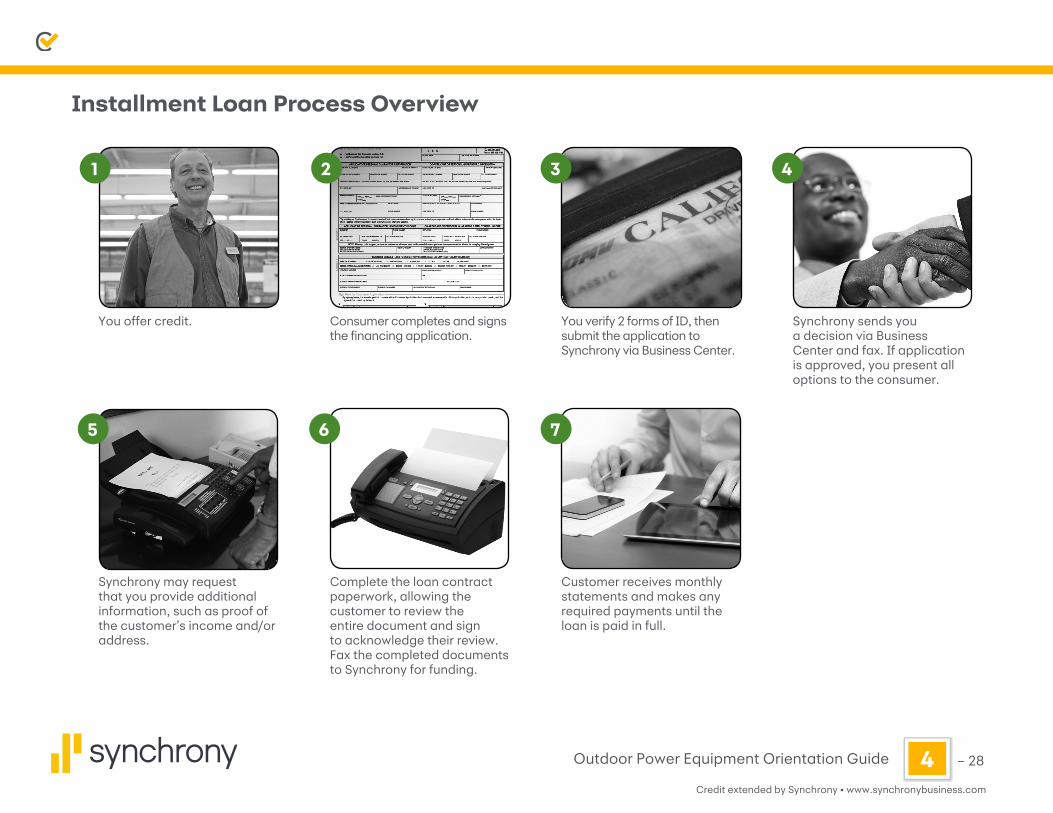

Installment Loan Process Overview

You offer credit.

Synchrony may request that you provide additional information, such as proof of the customer’s income and/or address.

Consumer completes and signs the financing application.

Complete the loan contract paperwork, allowing the customer to review the entire document and sign to acknowledge their review. Fax the completed documents to Synchrony for funding.

You verify 2 forms of ID, then submit the application to Synchrony via Business Center.

Customer receives monthly statements and makes any required payments until the loan is paid in full.

Synchrony sends you a decision via Business Center and fax. If application is approved, you present all options to the consumer.

1 2 3 4

5 6 7

Credit extended by Synchrony • www.synchronybusiness.com

– 294Outdoor Power Equipment Orientation Guide

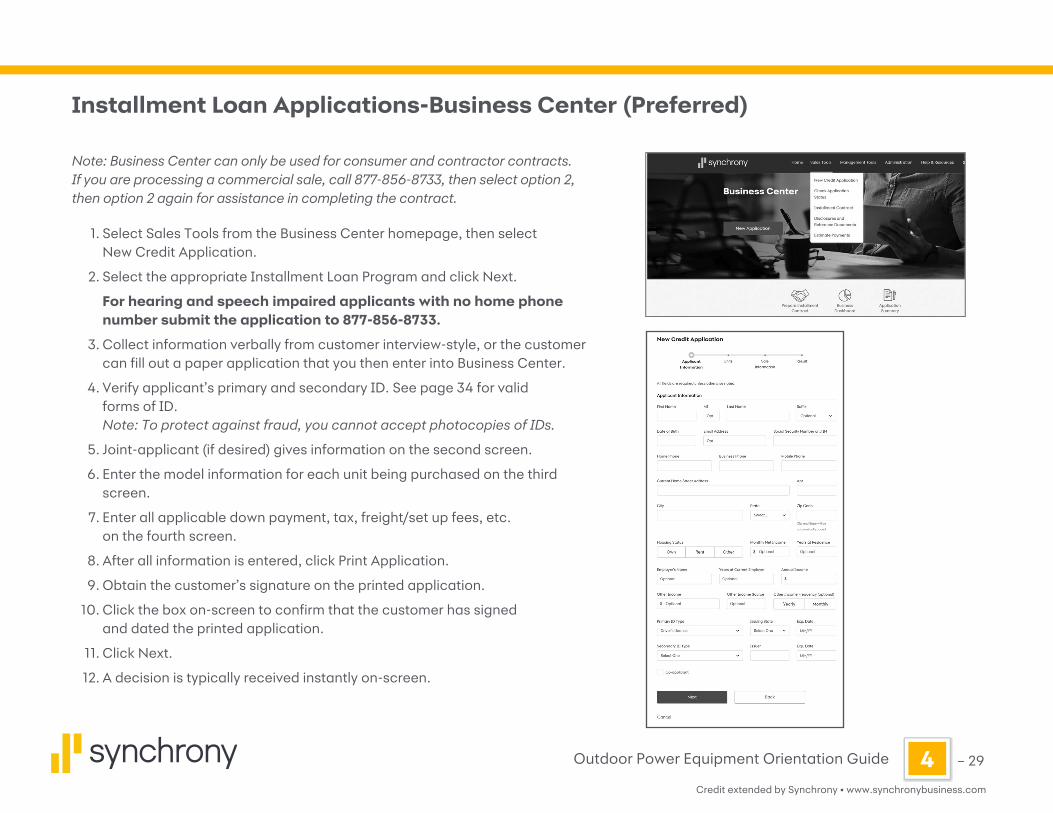

Installment Loan Applications-Business Center (Preferred)

Note: Business Center can only be used for consumer and contractor contracts. If you are processing a commercial sale, call 877-856-8733, then select option 2, then option 2 again for assistance in completing the contract.

1. Select Sales Tools from the Business Center homepage, then select New Credit Application.

2. Select the appropriate Installment Loan Program and click Next.

For hearing and speech impaired applicants with no home phone number submit the application to 877-856-8733.

3. Collect information verbally from customer interview-style, or the customer can fill out a paper application that you then enter into Business Center.

4. Verify applicant’s primary and secondary ID. See page 34 for valid forms of ID. Note: To protect against fraud, you cannot accept photocopies of IDs.

5. Joint-applicant (if desired) gives information on the second screen.

6. Enter the model information for each unit being purchased on the third screen.

7. Enter all applicable down payment, tax, freight/set up fees, etc. on the fourth screen.

8. After all information is entered, click Print Application.

9. Obtain the customer’s signature on the printed application.

10. Click the box on-screen to confirm that the customer has signed and dated the printed application.

11. Click Next.

12. A decision is typically received instantly on-screen.

Credit extended by Synchrony • www.synchronybusiness.com

– 304Outdoor Power Equipment Orientation Guide

201-828-00Rev. 04/201619672

Toro Installment Application

TORO INSTALLMENT APPLICATION

(1)

SEC

TIO

N 1

SEC

TIO

N 2

SEC

TIO

N 3

Synchrony BankFax: 866-405-9648 Phone: 877-856-8733

DEALER NAME DEALER PHONE NUMBER

DEALER #

2 - 6 - 6 - - - - - -

SALES INFORMATION (DEALER USE ONLY)CASH SALE PRICE LESS AMOUNT OWED ON TRADE-IN FREIGHT & SET UP

CASH DOWN PAYMENT SALES TAX TOTAL OTHER FEES

GROSS TRADE-IN ACCESSORIES AMOUNT FINANCED

Sign Here for Business, Personal GuarantyBy signing below, I acknowledge that I have read the Personal Guaranty disclosure on the reverse side of this application, which is incorporated herein, and that I agree to be bound by its terms.

X ________________________________________________________ Signature of Personal Guarantor #1 (Please do not Print) Date

X ______________________________________________________________ Signature of Personal Guarantor #2 (Please do not Print) Date

Sign Here for Consumer ApplicationBy signing below, I acknowledge that I have read the Consumer Application disclosure on the reverse side of this application, which is incorporated herein, and that I agree to be bound by its terms.

X ________________________________________________________ Applicant Signature Date

X ______________________________________________________________ Co-Applicant Signature Date

Signature of Company’s Authorized RepresentativeBy signing below, I acknowledge that I have read the Company’s Authorized Representative Application disclosure on the reverse side of this application, which is incorporated herein, and that I agree to be bound by its terms.

X ________________________________________________________________________________ X ____________________________________ Signer must be an officer, owner, or agent of business or entity and Title Date Print name must be authorized to enter into contracts on behalf of business or entity

COLLATERAL INFORMATION (DEALER USE ONLY)NEW/USED MODEL YEAR MAKE MODEL

q LAWN TRACTORS q GARDEN TRACTORS q ZERO TURN MOWERS q FRONT DECK MOWERS q WALK BEHIND MOWERSq ATTACHMENTS

NEW/USED MODEL YEAR MAKE MODEL

q LAWN TRACTORS q GARDEN TRACTORS q ZERO TURN MOWERS q FRONT DECK MOWERS q WALK BEHIND MOWERSq ATTACHMENTS

NEW/USED MODEL YEAR MAKE MODEL

q LAWN TRACTORS q GARDEN TRACTORS q ZERO TURN MOWERS q FRONT DECK MOWERS q WALK BEHIND MOWERSq ATTACHMENTS

PRIMARY ID TYPE ISSUING STATE EXPIRATION DATE PRIMARY ID TYPE ISSUING STATE EXPIRATION DATE

SECONDARY ID TYPE ISSUER EXPIRATION DATE SECONDARY ID TYPE ISSUER EXPIRATION DATE

q For Personal Use (Complete sections 1-2)

q For Business Use Using Personal Credit History (Complete sections 1-3)

q For Business Use Using Business Credit History (Complete section 3 only)

APPLICANT OR PERSONAL GUARANTOR 1 INFORMATION CO-APPLICANT OR PERSONAL GUARANTOR 2 INFORMATIONNAME: First, MI, Last (print) BIRTHDATE (MMDDYY) NAME: First, MI, Last (print) BIRTHDATE (MMDDYY)

SOCIAL SECURITY NUMBER HOME PHONE NUMBER CELL PHONE NUMBER SOCIAL SECURITY NUMBER HOME PHONE NUMBER CELL PHONE NUMBER

PRESENT STREET ADDRESS PRESENT STREET ADDRESS

CITY, STATE, ZIP MORTGAGE/RENT PAYMENT CITY, STATE, ZIP MORTGAGE/RENT PAYMENT

YEARS AT ADDRESS OWN____ RENT____

OTHER____

EMAIL ADDRESS (OPTIONAL)* YEARS AT ADDRESS OWN____ RENT____

OTHER____

EMAIL ADDRESS (OPTIONAL)*

*By providing an Email address, I consent to receive Email communications about my Account and authorize you to provide my Email address to the manufacturer sponsor and to the dealer where I applied so that I may receive such communications, offers and updates.

APPLICANT OR PERSONAL GUARANTOR 1 EMPLOYMENT/INCOME CO-APPLICANT OR PERSONAL GUARANTOR 2 EMPLOYMENT/INCOMEBUSINESS NAME BUSINESS/WORK PHONE NUMBER BUSINESS NAME BUSINESS/WORK PHONE NUMBER

SELF-EMPLOYED?

YES____ NO____

HOW LONG AT PRESENT JOB

YEARS: MONTHS:

NET MONTHLY INCOME SELF-EMPLOYED?

YES____ NO____

HOW LONG AT PRESENT JOB

YEARS: MONTHS:

NET MONTHLY INCOME

NOTE: Alimony, child support, or separate maintenance income need not be revealed unless you want them considered as a basis for repaying this obligation

SOURCE OF OTHER INCOME (SPOUSAL INCOME MAY ONLY BE INCLUDED FOR WISCONSIN RESIDENTS)

MONTHLY AMOUNT SOURCE OF OTHER INCOME (SPOUSAL INCOME MAY ONLY BE INCLUDED FOR WISCONSIN RESIDENTS)

MONTHLY AMOUNT

BUSINESS DETAILS (ONLY REQUIRED FOR COMMERCIAL OR CONTRACTOR APPLICATIONS)

TYPE OF BUSINESS: q SOLE PROPRIETOR q PARTNERSHIP q NONPROFIT q C-CORP q S-CORP q GOVERNMENT

GROSS ANNUAL SALES / REVENUES: q Less Than $50,000 q $50,000 - $100,000 q $100,001 - $250,000 q $250,001 - $500,000 q $500,001 - $3,000,000 q $3,000,000 +

NATURE OF BUSINESS YEARS IN BUSINESS SINCE NUMBER OF EMPLOYEES

YOUR COMPANY’S FULL LEGAL NAME DBA

BUSINESS MAILING STREET ADDRESS CITY, STATE, ZIP

BUSINESS PHONE NUMBER BUSINESS FAX NUMBER ACCOUNT CONTACT PERSON TAX ID NUMBER

Installment Loan Applications-Paper

1. If it is a consumer application, the customer fills out top left sections of application.

2. Joint applicant (if desired) completes the top right sections.

3. If the purchase is for a business, complete section 3.

4. Obtain signatures from applicant and joint-applicant (if applicable)

5. Check to ensure all information is complete and the application is signed.

6. Verify applicant’s primary and secondary ID and enter that information beneath the customer signature. See page 34 for valid forms of ID. Note: You should not make photocopies of the applicant’s primary and/or secondary IDs.

7. You enter your dealer number, store name and phone, and check the appropriate box for business or personal use at the top of the form.

8. You complete the Collateral Information and Sales Information sections at the bottom of the form.

9. Submit the application via fax to the number at the top of the form.

10. A decision will be faxed back within approximately 5 to 15 minutes.

Credit extended by Synchrony • www.synchronybusiness.com

– 314Outdoor Power Equipment Orientation Guide

Installment Loan Contract

Note: Business Center can only be used for consumer and contractor contracts. If you are processing a commercial sale, call 877-856-8733, then select option 2, then option 2 again for assistance in completing the contract.

1. Select Sales Tools from the Business Center homepage, then select Prepare a Contract.

2. Select your Program and enter the customer information to locate the approved application number. Click Search.

3. Enter the date the contract will be signed and select the unit (s) to be included in the contract. Click Next.

4. Select the financing promotion the customer chose. Click Next.

5. Update the loan terms and select first payment date as necessary. The due date must be between 30 and 45 days from the date of the contract. Only the 1st through the 25th of the month are allowed as due dates.

6. Review all dollar amounts on-screen and make changes as needed. Then click Continue.

7. Make sure the box is checked next to “Print application with contract.” Click Generate Contract.

8. Print the entire pdf that appears on-screen.

9. Review each page of the contract and any other printed disclosures with the customer, asking them to sign or initial in all of the appropriate fields on the dealer copy after their review is complete.

10. Fax (preferred) or mail the complete loan package to the fax number listed on the printout. If mailing, make a store copy of the package.

11. Retain original (or copy if mailing contract) in a secure location for the term of the loan.

Note: Pre-printed paper contracts are available upon request if needed. Call Dealer Services at 877-856-8733 for details.

This page intentionally left blank.

Outdoor Power Equipment Orientation Guide – 335Credit extended by Synchrony • www.synchronybusiness.com

Applying And Transacting

Things to Remember

Credit extended by Synchrony • www.synchronybusiness.com

– 345Outdoor Power Equipment Orientation Guide

At the time of application, the customer must verify two forms of identification. At least one of them must be “Primary.” See the right side of this page for definitions of primary and secondary identification. Synchrony does not require or advocate the photocopying of customer identification.

On occasion, an application may be chosen by Synchrony for a fraud review to protect both you and your customers. When needed, you may be asked to call Synchrony and put the customer on the phone, or the customer may be asked to respond to a passcode message on their home or mobile phone after the application is submitted.

Validating Customer’s Identity

Valid Identification for Financing Applications

• Primary - State or government issued non-expired IDs (Driver’s License, State ID, Passport, Military ID, or Resident/Alien Green Card) Note: When using a passport, use state of residence. When using a military ID, the expiration is the date on the top right.

• Secondary - Major credit and debit cards (VISA, MasterCard, American Express, Discover) department store cards, or gas cards with the customer’s name and an expiration date on them (non-expired).

Credit extended by Synchrony • www.synchronybusiness.com

– 355Outdoor Power Equipment Orientation Guide

Application Outcomes

Approved

“I’m happy to tell you that your application has been approved.”

Pending

“The application came back ‘Pending,’ which simply means they need to clarify some information. Let’s give them a call to see what they need.”

Note: You must call 877-856-8733 on a pending application within 24 hours or it will be automatically denied.

Declined

“Unfortunately, the bank wasn’t able to extend credit to you at this time. You will receive a letter within 30 days indicating the specific reasons for the decision. If you like, you may reapply with a joint-applicant.”

What to say aboutthe decision

• If approved for a Revolving Credit account, the applicant and joint applicant (if applicable) will receive a credit card in the mail in 7-10 days for future purchases, but the initial charge can be made immediately upon approval.

• Call 877-856-8733 for application processing, assistance with a transaction, or credit limit increase (Revolving Credit only).

• If your customer is going to apply online from home (if applicable), remind him/her to print out the approval page and bring it in with two forms of required ID. You will use the store section at the bottom of the form to notate IDs.

Credit extended by Synchrony • www.synchronybusiness.com

– 365Outdoor Power Equipment Orientation Guide

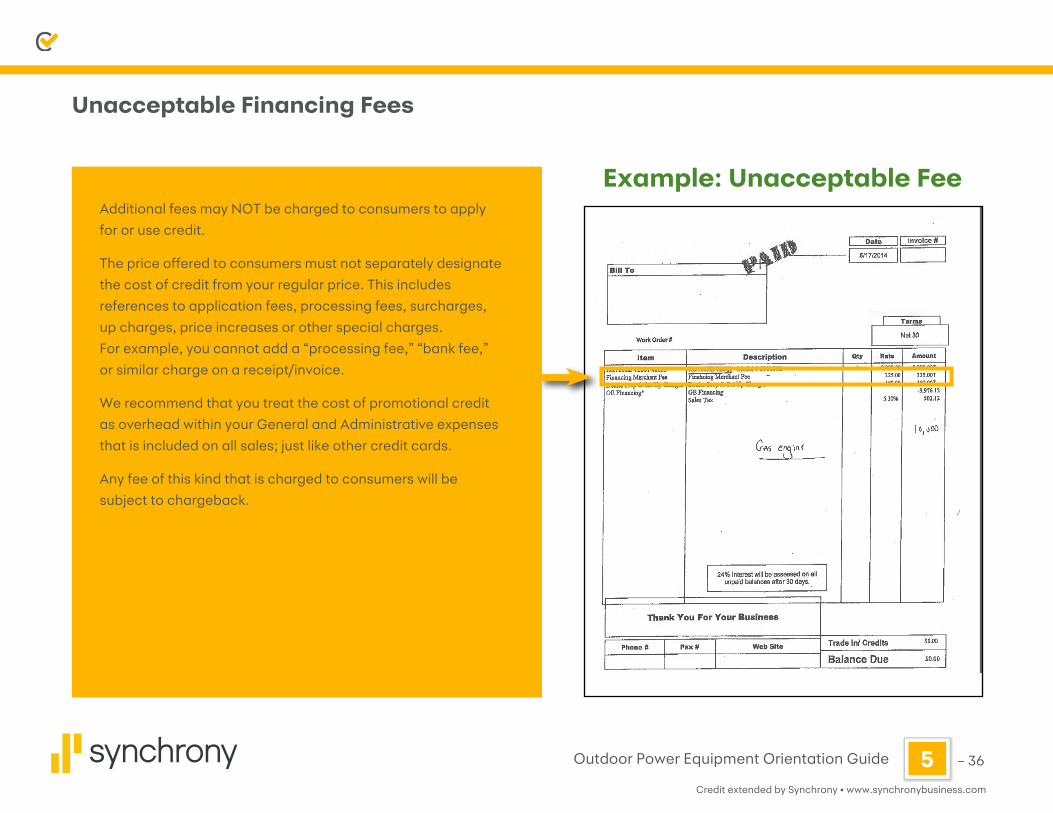

Unacceptable Financing Fees

Example: Unacceptable FeeAdditional fees may NOT be charged to consumers to apply

for or use credit.

The price offered to consumers must not separately designate

the cost of credit from your regular price. This includes

references to application fees, processing fees, surcharges,

up charges, price increases or other special charges.

For example, you cannot add a “processing fee,” “bank fee,”

or similar charge on a receipt/invoice.

We recommend that you treat the cost of promotional credit

as overhead within your General and Administrative expenses

that is included on all sales; just like other credit cards.

Any fee of this kind that is charged to consumers will be

subject to chargeback.

Credit extended by Synchrony • www.synchronybusiness.com

– 375Outdoor Power Equipment Orientation Guide

• Be sure to always use current versions of applications and other documents. Updated versions can be found on Business Center (bc.syf.com) under Sales Tools- Disclosures & Reference Documents. You can also order pre-printed forms free of charge in Business Center under Help & Resources – Order Supplies.

• Customer must be present for all transactions.

• Customer must sign a sales receipt and receive a copy for all transactions. Customer must be given promotional details prior to completing the sale.

• Two forms of ID, one primary and one secondary, must be presented by the customer at the time of application. Synchrony does not require or advocate the photocopying of customer identification.

• You can only charge for services that have been completed. Please obtain an authorization for any products or services that will not be delivered/completed the same day as the sale.

• Your business will receive funding for purchases from Synchrony within 2 business days.

• For Revolving Credit transactions, if the card is not present, check both of the customer’s ID to ensure that the purchaser is the cardholder to help avoid potential fraud and chargeback issues to your business.

• Regardless of which method you use for applying, a copy of a completed and signed application must be retained in a secure location for 25 months (Revolving, Installment, Approved and Declined). Approved and funded Installment Loan applications must be retained in a secure location for life of loan.

• Applications must not be solicited in a language other than English.

• Dealers are required by law to suppress - or hide - all but the last five digits of the customer’s account number on a printed receipt. For Revolving Credit, the expiration date must also be hidden.

Applying And Transacting Key Information

This page intentionally left blank.

Outdoor Power Equipment Orientation Guide – 396Credit extended by Synchrony • www.synchronybusiness.com

Payment Discussions

They’re easy with Synchrony Bank

Credit extended by Synchrony • www.synchronybusiness.com

– 406Outdoor Power Equipment Orientation Guide

Suggestions From Your Peers Here are some tips from current merchants who are using a Synchrony credit card program successfully to increase their sales.

1. Advertising: Include “Special Financing Available” or other mention of your financing program in your regular advertising.*

• TV, radio and print advertising

• Direct mail

• On your web page

• During on-hold telephone messaging

2. Merchandising: Place your signage in high traffic areas to act as your “silent sales force” when you aren’t with your customer or as a reference point. Also make sure to have signage near your big ticket items and at the checkout.*

3. Training: Train your staff to offer financing to EVERY customer EARLY in the sales process and discuss credit at staff meetings.

4. Pricing: Use financing to help close more sales at higher average ticket amounts.

• Financing is a cost of doing business just as payroll, rent, electric, etc. and any fees charged to you by Synchrony cannot be passed to your customers as an extra fee. See page 36 for samples of unacceptable fees.

5. Incentives: Offer reasonable employee and customer incentives.

• Encourage all employees to talk about financing with every customer. If offering an incentive, contest or spiff for submitting applications, talk to your Synchrony contact for ideas and incentive guidelines.

Synchrony requires that all incentives, contests and sweepstakes be submitted prior to launch for review and approval.

The Five Pillars Of Success

*Refer to disclosures in Advertising Guidelines.

Credit extended by Synchrony • www.synchronybusiness.com

– 416Outdoor Power Equipment Orientation Guide

Advertising Guidelines

Select the Advertising Guidelines file, located in Advertising Center under Resources at www.synchronybusiness.com.

View compliant headlines and disclosures to use in your advertisements in print,online and in other media.

Credit extended by Synchrony • www.synchronybusiness.com

– 426Outdoor Power Equipment Orientation Guide

Typical Customer Conversation Steps

In this section we will review…

• How to estimate customer payments and discuss options

• How to discuss cardholder payment options (with examples)

• Clear and accurate responses to customer questions and concerns

Customers WantOptions

Mention your financing promotions

and offerings as a “by the way”

message early in the sales conversation

1 2 3

Break purchases down into monthly

payments when the customer is selecting a product or service

Tell the customer about the benefits of financing when

they’re ready to pay for their purchase

Credit extended by Synchrony • www.synchronybusiness.com

– 436Outdoor Power Equipment Orientation Guide

Customer Discussion Examples

• Tell me about how and when you discuss price today?

• How will you incorporate financing into your price discussions moving forward to make sure all customers are aware of their options?

At the beginning of the sales conversation“Hi, welcome to our store. Just so you know, we’re offering a great 36 months special financing promotion right now*. What brings you in the store today?”

When the customer is selecting a product or service“As I mentioned before, we currently have a 36 months special financing promotion available to you*. Would you like to talk through your options and see how much your monthly payments would be, and other key details?”

When the customer is ready to check out“Do you already have a [store name] credit card? I can help you with a quick application, and if it is approved, you can use your account immediately so you can take advantage of paying it off over time. Would you like to go ahead and submit an application?”

Customers can purchase today and

pay over time*

*Subject to credit approval.

Credit extended by Synchrony • www.synchronybusiness.com

– 446Outdoor Power Equipment Orientation Guide

Responding To Customer Hesitations

I don’t want another credit card.“I understand. Other competing general utility bank cards may offer special promotions periodically; however, our card features special promotional financing on an ongoing basis for qualifying purchases. Additionally, having a dedicated credit card for special purchases leaves your other bank cards available for emergencies and day to day needs.”

Note: For purchases over $2,500, the purchase can be made using Installment Loan without a credit card.

My credit isn’t great.“I understand. I’ll be happy to process an application for you to see if it may be approved. We also offer the option of applying with a joint-applicant.”

I don’t have time to apply.“Our credit application process takes only a couple minutes, and we usually get an answer back within seconds.”

I’m worried about how my personal information might be used.“I can understand your concern about personal information; that is something that we take very seriously. If you like, we can provide a more private location to fill out the application. We process several applications every day and we make every effort to keep your information secure to keep you protected.”

Focus on the benefits of paying

over time

ActionLet’s practice to see if you

have any questions.

*Deferred Interest promotion is used in this example for illustration purposes.

Credit extended by Synchrony • www.synchronybusiness.com

– 456Outdoor Power Equipment Orientation Guide

Introducing Financing To Your Team Is Easy…

1. Introduce your Synchrony financing program at your next team meeting.

2. Review the benefits of the program for both your business and your customers.

3. Point out the ways to include financing into every sales discussion with your customers compliantly, as well as how to use signage and other visual tools to help your customers understand their financing options.

4. Review the videos, courses and printable tools on the Learning Center website at https://learn.synchronybusiness.com. Click the “Where to Start” link for a list of “core” courses your entire team should view.

It’s a “Team Thing”

Credit extended by Synchrony • www.synchronybusiness.com

– 466Outdoor Power Equipment Orientation Guide

Put It In Perspective

Think of financing as if it is a new product line you’re carrying. How can your sales team sell effectively if they don’t know that new product up and down? You expect everyone to spend a lot of time experiencing and researching the product.

Financing is no different. It’s going to move more product for your store and allow your customers to get the product or service they really want. Your customer will walk away with the best product for them, confident in their ability to pay it off over time instead of worrying about how to pay for the entire purchase upfront.

Any questions?

Credit extended by Synchrony • www.synchronybusiness.com

– 476Outdoor Power Equipment Orientation Guide

Transparency Principles: COMPLIANCE REQUIREMENTS

Synchrony promotes full transparency and disclosure to all applicants for its credit card program (the “Synchrony Financing Program”). To assure that applicants are aware of several key attributes of the Synchrony Financing Program, you hereby agree as follows:

1. You will ensure that training on how to offer, process and transact with the Synchrony Financing Program is integrated into your existing associate training program. Helpful training materials including videos, self-paced courses and pre-recorded webinars can be found online at Synchrony’s Learning Center: http://learn.synchronybusiness.com.

2. Your customers must receive the Credit Card Agreement in writing and have the opportunity to review it and other disclosures in the application brochure before signing an application (Revolving credit only).

3. You must retain each applicant’s application and sales receipt/contract for no less than 25 months from the date of the application for revolving credit; and for the life of loan for installment loans. Failure to keep and, upon request, produce the application and sales receipt/contract to Synchrony may expose your business to an automatic chargeback upon consumer dispute.

4. Any fees that might be charged to you for a promotion may not be passed on to the customer (See page 36). All are prohibited by your Card Acceptance Agreement with Synchrony and you will be responsible for refunding customers accordingly.

5. You or your staff must inform all Synchrony Financing Program applicants of the following:

• The Synchrony Financing Program is a credit card and is NOT an in-house credit program. The Synchrony Financing Program is NOT an interest-free credit card.

• Cardholders should be provided with information about the different special financing options available to them and how they work before requested to choose which one to use for their specific purchase. It is especially important that cardholders understand the basic features of No Interest, Reduced Interest and Deferred Interest /No Interest if Paid in Full options, if all these type of promotions are being offered. The key concepts include:

– The length of the promotion – Whether the promotion expires and if so what happens upon expiration – Required payments during the promotional term

• For Deferred Interest promotions, deferred interest accrues on the outstanding balance during the promotional period from the date of the transaction. Finance charges can be avoided ONLY IF the promotional balance is paid off prior to the end of the promotional period.

6. You must provide the promotional terms to the customer on the completed, signed Sales Slip.

7. Make sure that you include customer promotion fees in your discussion and point out where it is stated on the sales slip (above the customer’s signature).

8. You will advise customers of any policy regarding returns/refunds.

9. These program guidelines are designed to provide transparency for cardholders. Synchrony reserves the right to monitor your adherence to these and other Synchrony Financing Program policies subject to the consequences defined in your Card Acceptance Agreement.

Credit extended by Synchrony • www.synchronybusiness.com

– 486Outdoor Power Equipment Orientation Guide

Transparency Principles: COMPLIANCE REQUIREMENTS

Fair Lending Principles to KnowCredit must be offered to all applicants fairly and consistently. Failure to do so may result in allegations of discrimination, potential violations of federal or state fair lending laws, litigation or reputational risk. All customers should be encouraged to apply for credit without regard to race, color, religion, national origin, sex, marital status, familial status, age, disability, receipt of income (in whole or in part) from public assistance programs, or an applicant’s good faith exercise of a right under the Consumer Credit Protection Act. In addition, credit-related activities must be conducted in a way that is not considered unfair, deceptive, or abusive from the customer’s perspective. Unfair activities are those that may cause unavoidable “substantial injury” (typically financial harm) to customers. Deceptive activities could include statements or omissions that mislead customers or influence their decision to buy or use a product or service. Abusive practices interfere with the customers’ ability to understand the terms and conditions of a product or service; or which take advantage of the customer’s lack of understanding or inability to protect their interests.

Clear and Accurate CommunicationsYour advertising, signage, and conversations with customers should help them understand and make informed choices regarding your products and available financing options. Disclosures should clearly and accurately describe the terms, conditions, and any limitations associated with the purchase and the Synchrony relationship the customer is establishing.

Taking and Processing ApplicationsAll customers should be encouraged to complete and submit applications for credit. Do not discourage anyone from submitting an application, either through oral statements, body language, delays or discourtesy. Also, make certain that employees provide a consistent level of service in responding to questions from customers about the availability of credit and/or completing the application.

Completing the Credit ApplicationThe credit application must be completed and signed by the customer(s) before it is submitted to Synchrony for approval. For Revolving Credit accounts, the Credit Card Agreement must be provided to the customer before the application is completed and signed. It is the customer’s choice to have a joint applicant, but it is not required that a joint applicant be a spouse. Alimony, child support or separate maintenance payments do not need to be disclosed unless the customer wants this income to be considered.

Pricing and FeesNo fees related to the application process or Synchrony financing are allowed, and the pricing of credit approved for customers cannot be changed from what Synchrony approved and communicated, except in approved cases of “buy-down” rates. The availability of promotions must be consistently shared with customers when they apply for credit.

Credit extended by Synchrony • www.synchronybusiness.com

– 496Outdoor Power Equipment Orientation Guide

Today We Discussed…

• How financing can help you achieve your business’s priorities, while helping your customers get what they really want or need.

• How promotional financing works, including Deferred Interest, No Interest and Reduced Interest promotions.

• How and when to discuss financing with every customer clearly.

• How to get additional training for new and existing team members.

• Important rules for fair and compliant business practices when offering financing.

You made it!

Any questions?

This page intentionally left blank.

Outdoor Power Equipment Orientation Guide – 517Credit extended by Synchrony • www.synchronybusiness.com

Resources And Tools

The Mechanics

Credit extended by Synchrony • www.synchronybusiness.com

– 527Outdoor Power Equipment Orientation Guide

Business Center Processing Training

To take an interactive online course on how to use the Business Center, access Learning Center at https://learn.synchronybusiness.com.

Business Center strengthens three pillars of your business: • Sales: Fast, easy transactions • Marketing: Drive more traffic to your business • Operations: Greater control and efficiency

Credit extended by Synchrony • www.synchronybusiness.com

– 537Outdoor Power Equipment Orientation Guide

1. How Do I Get Started? • Register at bc.syf.com (You will need your merchant number and bank DDA number) • Person registering will be Location Administrator for Business Center and responsible for: - Providing an email address and other requested information - Adding all users for that location and setting permissions for each user - Adding Synchrony programs for that location

2. Get Familiar with Business Center • Access the Business Center training courses via Learning Center at: https://learn.synchronybusiness.com. • Practice in a safe online environment by clicking Help & Resources then select Product Demo from the drop down menu

3. Start Offering Credit • Offer to every customer • Offer early in the sales process

Use Business Center for all your processing, reporting and resources needs to begin enjoying the increased sales you can generate by offering credit today.

Business Center Registration

Credit extended by Synchrony • www.synchronybusiness.com

– 547Outdoor Power Equipment Orientation Guide

Help & Resources

There is an assortment of resources in Business Center available to help you manage your financing program.

Click the Help & Resources menu to access the various resources offered in the Business Center.

The following resources are available for revolving financing programs.

• Order Supplies

• Frequently Asked Questions

• Learning Center

• Product Demo

• Merchant Services

• Chat With an Agent

Credit extended by Synchrony • www.synchronybusiness.com

– 557Outdoor Power Equipment Orientation Guide

Reporting

Click the “Management Tools” menu to access the various reports offered.

The following reports are available for revolving financing programs:

• Application Summary - Provides a history of your consumer applications

• Authorizations Report - View all authorization-only transactions

• Business Dashboard - Summarizes application and credit limit approvals

• Credit Card Transaction Report - Supplies detailed data of transactions and can be used for reconciliation

• Daily Funding Report - Provides a daily update of funding

• Monthly Statement - Details your monthly transactions of sales, fees and deposits

• My Customer List - pull a list of your current customers available credit

and MORE...

Credit extended by Synchrony • www.synchronybusiness.com

– 567Outdoor Power Equipment Orientation Guide

Note: The Phone Express Processing (PEP) system uses only numeric characters. Do not leave spaces between any numbers.

You will be asked to confirm the entered data by Pressing #1 after some steps.

STEP Example

Call your standard credit processing number 1-877-856-8733

Press #1 if you are a Merchant then follow instructions to submit a new PEP application

Select # 1 for standard entry (repeats each entry) or #2 for express entry 2

Enter Your 16 digit Merchant Number

If you have multiple product codes on your account, you will be asked to select from a menu of available product codes

534812xxxxxxxxxx

Enter sales amount in whole dollars 1149 then #

Enter applicant’s 6 digit date of birth (MM/DD/YY see example) 010752

Enter applicant’s 9 digit Social Security Number or Individual Tax Identification Number (ITIN) 123456789

Enter applicant’s street number or box number and Press # 4848 then #

Enter applicant’s 5- digit zip code 51301

Enter applicant’s 10 digit home phone, starting with area code, then # 5555555555 then #

Enter applicant’s residential status

#1 = Own

#2 = Rent

#3 = Other

1

Enter monthly net income in whole dollars from all sources and Press # 1457 then #

Enter 10 digit business phone, starting with area code 5555555555

Press #1 if there is a joint-applicant (repeat process for joint-applicant) 1

Press #2 if no joint-applicant

At this point you will be given a key number for the application and asked to wait while the application is processed.

You will then be given the credit decision or if we need further verification, the call may be transferred to a Dealer

Services representative. If application is approved, process the sale in the normal manner.

Downtime Application Processing

Credit extended by Synchrony • www.synchronybusiness.com

– 577Outdoor Power Equipment Orientation Guide

When a customer’s credit application is approved on the Internet, they have two ways to make a purchase:

1. Print the Internet Response Page and take it to the merchant location for up to 10 days after applying.

2. Wait until they receive the card in the mail and go to the merchant location.

The customer must have either the Internet Response Page or the card to make a purchase after being approved on the Internet.

1. Internet Response Page Purchase

The account holder is attempting to make a purchase with the Internet Response Page. When the account holder presents the Internet Response Page, you must follow the procedures listed below: • Make sure that the Internet Response Page has not expired. • Verify and record the cardholder’s identification on the Internet Response Page. • Call the Sales Finance Help Desk to obtain the account number. If it has been more than 10 days since approval, you will be informed of this and the customer should be told that the Internet Response Page has expired and the card must be presented in order to make a purchase. • Retain the Internet Response Page for your records for 25 months.

2. Credit Card Purchase You will not be able to distinguish an Internet-originated card from any other card; therefore, you should process the sale as usual.

Failure to follow the above procedures may result in a chargeback!

(See next page for sample Internet Response.)

Customer Internet Response Page

Credit extended by Synchrony • www.synchronybusiness.com

– 587Outdoor Power Equipment Orientation Guide

Sample Internet Response Page

Validation Of Customer I.D. - Completion Of All Boxes Required Initials Merchant # Account # Amount of initial transaction 1st Type of ID / Number Exp. Date 2nd Type of ID / Credit Card Type and Issuer Exp. Date

Store Phone # Store Fax #

Please do the following: • Verify and record above the account holder identification the same as you would for a face – to – face applicant. • Call Synchrony to obtain the account number. • Process the sale as you normally would with no card present. • Retain this page for your records for 25 months.

Failure To Follow The Above Procedures May Result In A Chargeback!

STOP

Congratulations Cardholder ___________________ __________________! You are now a ______________________________ cardholder.

Thank you for applying. Soon you will receive your credit card in the mail . Your credit limit is : ____________________ Your reference number for this application is: ____________________ If you wish to use your new account before you receive your credit card, just go to the _________________________________________ nearest you and present this page.

We want to make it easy and convenient for you to shop with us. If you need further information regarding your account, please contact our Customer Service Department at _______________________________________. Thank you for applying, we look forward to serving you at any of our locations. Please print this page and save for future reference.

Expiration Date: _______________________

FOR MERCHANT USE ONLY

Client Name and Location

Cardholder First Name LastName

Client Name

Credit extended by Synchrony • www.synchronybusiness.com

– 59Outdoor Power Equipment Orientation Guide 7

You are part of a teamGetting Help

Dealer Support 877-856-8733

• Assistance with submitting applications

• Obtain names on an account

• Check available credit amount

• Request a credit limit increase

• Technical assistance with terminal or Business Center

Accountholder Support 800-250-5411

• Account Questions

• Credit Limit Increases

• Address updates

On-Demand Training

• Learning Center: https://learn.synchronybusiness.com

• Call 866-885-2637 Mon-Fri 8:00am to 8:00pm EST

Please Note: Accountholder Support representatives are authorized to speak only with accountholders about their account.

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.

200-130-00 Rev May 2019

Outdoor Power Equipment Orientation GuideCredit extended by Synchrony • www.synchronybusiness.com