overview of format and topiceoplugin.commpartners.com/hsmai/130730/130730_slides.pdfchain scale...

TRANSCRIPT

7/30/2013

1

If you need technical assistance with thewebcast, contact us at [email protected]

and we will assist you immediately.

Revenue Management Webinar Series

Testing v. Shooting in the DarkJuly 30, 2013

This webinar series is brought to you by HSMAI University, HotelNewsNow, and STR

Overview of Format and Topic

Fran BrasseuxExecutive Vice President, HSMAI

7/30/2013

2

POLL QUESTION #1How many people are participating

in this webinar at your location today?

� 1� 2� 3� 4� 5� 6� 7� 8 or more

3

Panel Moderator:

Jeff Higley, VP, Digital Media & CommunicationsHotelNewsNow/STR/STR Global

4

7/30/2013

3

Today’s Presenters: Panel Moderator: Jeff Higley, VP, Digital Media and Communications, HotelNewsNow.com/STR/STR Global

Panelists:

Lauren Faulkner

Business Development

Executive

STR

5

Kim Tranter

Associate Professor/Dir of

Resort, Lodging & Tourism

Mgmt Programming

Johnson & Wales

University-Denver

Dev Koushik

Vice President

Global Revenue

Optimization

InterContinental

Hotels Group

Janelle Cornett

Regional Director of

Revenue Management

TPG Hospitality

U.S. Hotel Industry Overview

HSMAI Webinar SeriesJuly 30, 2013

7/30/2013

4

Presentation is available for download.

To view this presentation, go to the “Data” drop-down menu on

www.HotelNewsNow.com and click “Data Presentations”.

Total U.S. Review

7/30/2013

5

June YTD 2013: Highest RevPAR Ever (First 6 Months)

% Change

Room Supply* 880 mm 0.8%

Room Demand* 544 mm 2.3%

Occupancy 61.8% 1.5%

ADR* $109 4.0%

RevPAR* $68 5.6%

Room Revenue* $60 bn 6.4%

Total U.S. Results – YTD June 2013

* All Time High

June 2013:

Highest Monthly Room Revenue

EVER

($11.5 Billion)

7/30/2013

6

-8

-4

0

4

8

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Supply Demand

.7%

Favorable Supply / Demand Fundamentals for 2013

-7.1%

-0.9%

- 4.7%

Total U.S. – Supply & Demand % Change

12 MMA 1/1990 – 6/2013

7.7%

2.3%

-10

-5

0

5

1990 2000 2010

Demand ADR

7.7%

2.3%

ADR Growth Stalls

-4.5%

7.5%6.8%

-8.9%

4.0%

Total U.S. – ADR & Demand % Change

12 MMA 1/1990 – 6/2013

7/30/2013

7

-20

-15

-10

-5

0

5

10

1990 2000 2010

Positive RevPAR Growth For The Foreseeable Future

-16.8%

-2.6%

-10.1%

9%8.6%

Total U.S. – RevPAR % Change

12 MMA 1/1990 – 6/2013

65 Months 34 Mo.112 Months

Chain Scale Review

Luxury – Fairmont, Four Seasons, Ritz Carlton, JW Marriott

Upper Upscale – Sheraton, Embassy Suites, Hyatt, Marriott

Upscale – Radisson, Hilton Garden Inn, Courtyard, Best Western Premier

Upper Midscale – Holiday Inn, Clarion, Hampton Inn, Best Western US

Midscale – Best Western, Candlewood Suites, Quality Inn

Economy – Extended Stay America, Red Roof Inn, Days Inn, Value Place

7/30/2013

8

Strong Demand Growth, Supply Not An Issue

-0.1

0.1

3.1

0.9

1.7

-1.2

2.1

1.5

4.3

1.9

3.5

0.2

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy

Supply Demand

Chain Scales – Supply / Demand % Change

YTD June 2013

ADR Growth > OCC Growth

2.1

1.31.1 1.1

1.81.5

5.5

4.34.5

3.2

2.6

3.6

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy

Occupancy ADR

Chain Scales – Occ / ADR % Change

YTD June 2013

7/30/2013

9

RevPAR (Slowly) Catches Up To Prior Record Highs

$213

$113

$84

$62

$44$31

$219

$117

$87

$63

$41$29

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy

2007 YTD June 2013

Chain Scales – RevPAR $

YE 2007 & YTD June 2013

Segmentation

Group – rooms booked in blocks of 10 or more

Transient – third party, rack rate, government rate. Will include single

business traveler and leisure traveler

7/30/2013

10

Transient Drives Recovery

-0.3%-2.4%

6.7%

12.9%

18.3%

23.2%

-0.5%

-17.7%

-10.5%

-5.5%-2.6% -2.7%

2008 2009 2010 2011 2012 2013

Transient

Group

NOTE: Data is for upper tier hotels only (luxury chains, upper upscale chains, and upper tier independent hotels).

Segmentation Demand % Change

YTD June 2008 through 2013 vs. YTD June 2007

Pricing Opportunities Ahead

3.6%

-12.7% -12.7%

-7.7%

-3.4%

0.5%

5.4%

0.9%

-4.7%

-2.4%

0.4%

3.8%

2008 2009 2010 2011 2012 2013

Transient

Group

Segmentation ADR % Change

YTD June 2008 through 2013 vs. YTD June 2007

NOTE: Data is for upper tier hotels only (luxury chains, upper upscale chains, and upper tier independent hotels).

7/30/2013

11

YTD June ADR $ :

Transient Rooms Increase Premium

$180

$152 $151

$160

$168

$174

$161

$154

$146

$149

$153

$159

2008 2009 2010 2011 2012 2013

Transient $

Group $

*Segmentation ADR $, YTD June 2008 - 2013

Top Markets Review

7/30/2013

12

RevPAR Recovery by Tracts

% of Peak RevPAR

Still Mixed RevPAR Recovery Among U.S. Tracts

37 mos

41

42

44

47

48

55

56

57

59

60

60

61

67

68

69

69

72

72

74

76

82

83+

94

96+

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

San Francisco

Miami

Oahu

Boston

Nashville

Los Angeles

Denver

Detroit

Houston

Anaheim

Seattle

Dallas

St. Louis

Minneapolis

New Orleans

Chicago

Tampa

New York

Orlando

Philadelphia

Atlanta

San Diego

DC

Norfolk

Phoenix

a

Actual

Estimated

RevPAR Peak-Trough-Recovery Timeframe

7/30/2013

13

Pipeline & Forecasts

In Construction: Ground has been broken

Final Planning: Construction will begin within 12 months

Planning: Construction will begin within 13-24 months

Pre-Planning: Construction will begin in more than 24 months

Construction Accelerates

Phase June 2013 June 2012 Difference % Change

In Construction 76,581 59,803 16,778 28.1%

Final Planning 125,874 121,788 4,086 3.4%

Planning 124,838 114,742 10,096 8.8%

Active Pipeline 327,293 296,333 30,960 10.4%

Pre-Planning 71,576 87,529 -15,953 -18.2%

Total 398,869 383,862 15,007 3.9%

Total U.S. – Pipeline by Phase, ‘000s Rooms

June 2013 and 2012

7/30/2013

14

Under Construction Rooms Mostly In Middle Segments

5.06.8

27.5

21.6

3.41.3

10.9

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Luxury Upper

Upscale

Upscale Upper

Midscale

Midscale Economy Unaffiliated

Total U.S. – Pipeline by Chain Scale, Rooms Under Construction (‘000s Rooms)

June 2013

Total U.S. – Markets with Most Rooms In Construction

June 2013

Market Rooms % of Existing Supply

New York 11,143 10.5

Orlando 2,958 2.5

Washington, D.C. 2,948 2.8

LA-Long Beach, CA 2,132 2.2

Nashville, TN 1,963 5.4

Houston 1,699 2.3

Chicago, IL 1,678 1.5

Denver 1,675 4.1

Miami-Hialeah, FL 1,246 2.6

Some Markets are Still “Hot”

7/30/2013

15

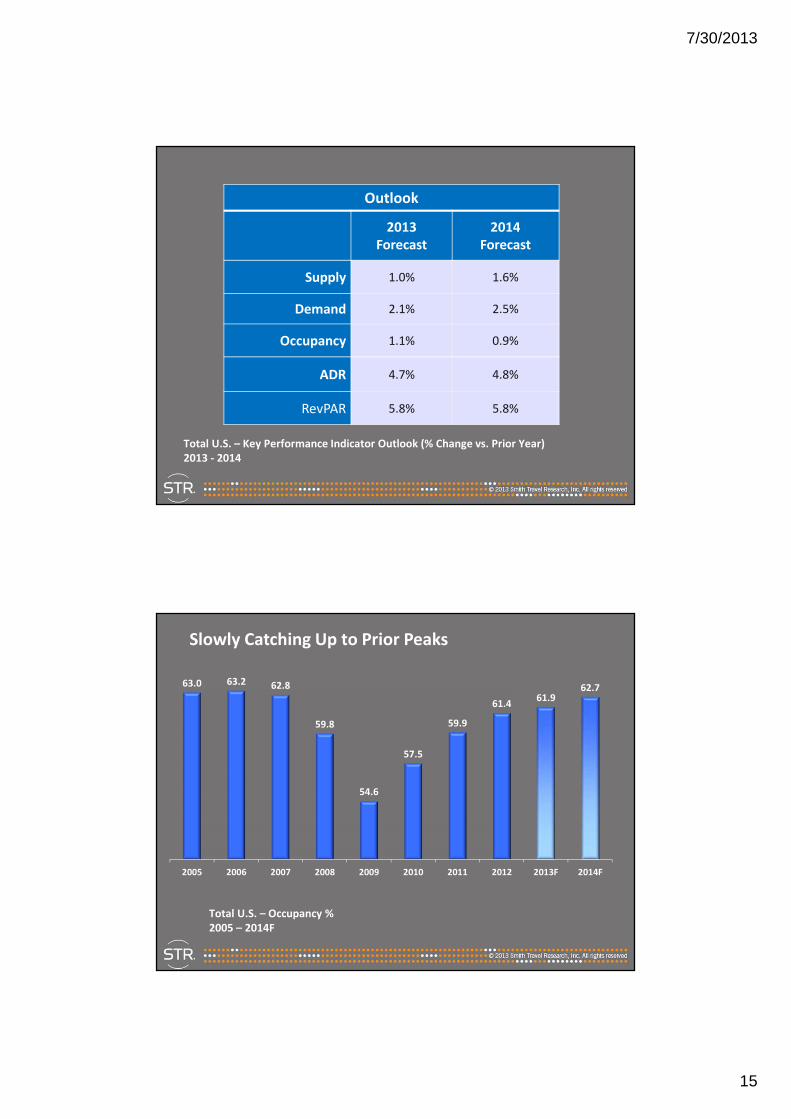

Total U.S. – Key Performance Indicator Outlook (% Change vs. Prior Year)

2013 - 2014

Outlook

2013

Forecast

2014

Forecast

Supply 1.0% 1.6%

Demand 2.1% 2.5%

Occupancy 1.1% 0.9%

ADR 4.7% 4.8%

RevPAR 5.8% 5.8%

Total U.S. – Occupancy %

2005 – 2014F

63.0 63.2 62.8

59.8

54.6

57.5

59.9

61.461.9

62.7

2005 2006 2007 2008 2009 2010 2011 2012 2013F 2014F

Slowly Catching Up to Prior Peaks

7/30/2013

16

$85$104 $107

$85

$102

Nominal ADR

2000/2008 ADR Grown by CPI

2000 ADR Grown by CPI

2008 ADR Grown by CPI

$107

Total U.S. – Room Rates

Actual vs. Inflation Adjusted 2000 – 2014F Note: 2012 & 2013 CPI forecast from Blue Chip Economic Indicators

$119

$116

Inflation Adjusted ADRs Well Out Of Reach

$111

$116

Takeaways

• Supply Growth – Slowly but Surely

• Healthy Demand Growth Despite “Everything”

• ADR Growth Drives RevPAR

• Steady Outlook

7/30/2013

17

34

Janelle Cornett

Regional Director of Revenue Management

TPG Hospitality

7/30/2013

18

35

Testing and Measuring Case

Study

TPG Hospitality Case Study

Make the Hypothesis

• Over high weekday transient demand periods (based on

2012 data), with either internal or external

compression it would be beneficial from both a revenue

and STAR standpoint to not allow 4 night on Sunday and

3 night on Monday arrivals hotel wide. This is done to

limit the number of lower rated BT occupied rooms

that could be replaced by higher rated retail or other

accounts.

36

7/30/2013

19

Timing

• There were several special events for 2013 identified

by the city event calendar including city wide group.

But also our own internal group and compression where

we saw high demand due to brand loyalty and internal

compression. Using tools to measure included

forecasted demand, denials, BT room night

displacement based on LOS restrictions.

37

Metrics – What to measure

against

• We used the following to measure our results

• STLY – or same period with high compression

• Period with similar demand levels YOY

• Reviewing LOS patterns YOY and measuring the change

in market segment mix of business over these dates

• STAR results

38

7/30/2013

20

Measure the Results

39

Measure the Results

40

7/30/2013

21

Measuring Results

• LOS 1-2 night down -3.6% YOY and 3 night up 5% / 4 night up 1%

YOY

• Booking window also has changed 20% of CNR booked 21+ day vs

10% year prior. LNR 28% booked 21+ days out vs 8% year prior –

result in putting the restricition on prior to opening inventory

• YTD through June = RevPAR up 4.8% vs comp set -3.1% = Index up

8.2% YOY

41

Conclusion

• To get a better/different outcome you need to test and

measure

• Understand what you are looking to change – make a

Hypothesis – so you understand what you are trying to do

• Determine how long and what you will measure. Then

determine the basis of the measurement

• Define the metrics or measurement

• Measure the results – they may not always be positive

42

7/30/2013

22

43

Kim Tranter

Associate Professor/Director of Resort, Lodging

& Tourism Mgmt Programming

Johnson & Wales University-Denver

Application of Strategic

Development, Execution, and

Evaluation in the Collegiate

Environment

7/30/2013

23

A Hands-On, High Tech Approach

• Obtain on internet based revenue simulation program.

• Make it a team-based competition.

• Best with teams of 2 to 3 people.

• Start with a simulation orientation.

• Each team is given the same scenario for the property

and the market.

Strategy Development For A Practice

Round and An Official Round

• Each team must make rate, channel, and marketing spending decisions for each month.

• Participate in a 12 month Practice Round and a 12 month Official Round.

• Teams develop and submit a set of strategies per month for the upcoming 12 months.

• Provide an incentive for winning.

• Since this in an internet based simulation, each team’s decisions impact the others.

7/30/2013

24

Executing, Modifying and Evaluating

Strategic Decisions

• Teams are permitted to modify their strategies as the

rounds proceed.

• They see all teams’ results monthly.

• Teams submit an analysis of their performance,

addressing what they would have or should have done

differently.

• Changes their thinking to become

much more strategic.

Forecasting and Strategic

Development Exercise• A low-tech method to integrate forecasting and strategic thinking.

• Create a series of monthly blank calendars.

• Fill in holidays, hot dates, city-wides from Convention Center and

CVB websites.

• Create monthly forecasts. Compare to actuals.

• KEY: DISCUSS what strategies could have been employed to drive in more demand per day? Achieve higher rates? Action plans???

7/30/2013

25

Where We Are Headed Next

• Creating two different simulation scenarios: city center and resort

to show differences.

• Plan would be to incorporate annual STR data.

• Using the STR data, what do the numbers really tell them? Big

picture.

• What adjustments should they make to improve performance?

• Also moving to case analysis in RM course similar to the Strategic

Management course.

50

Dev Koushik

Vice President, Global Revenue Optimization

InterContinental Hotels Group

7/30/2013

26

51

BENEFITS MEASUREMENT METHODOLOGIES

TEST PRE-REQUISITES

� Define the Metric to measure

� Choose Test Periods and Test hotels carefully

� Plan and Build Tracking Mechanisms

� Agree on the Process with stakeholders

� Plan for failures

� Implement and Scale successes

7/30/2013

27

$1.2

$1.1

$0.9

$0.8

$0.7

JAN FEB MAR APR MAY

Met

ric

Mea

sure

d

TreatmentApplied

Control Period

TreatmentPeriod

Expected Impact

Treatment Impact

The measurement model assumes that the METRIC trend continues to follow measurable seasonal trends and that any shift upwards or downwards is a result of the treatment.

STRATEGY TESTING USING CONTROL PERIOD APPROACH – METHOD 1

STRATEGY TESTING USING CONTROL PERIOD APPROACH – METHOD 2

Objective• Find the most appropriate control properties for each BETA property to use in the test

– Address key drivers: Seasonality / Group Mix / Market Factors

Process1. Select the eligible control properties using objective criteria:

TreatmentInitialization

Test Period:Time on Treatment

Baseline Period:Immediately prior period (equal number of days by DOW)

Control Property Eligibility Criteria:1.Same or similar: Brand / Size / Group Mix / Type (airport vs. non)2.Similar seasonality3.Control properties must be on similar systems4.No change in Quality Scores

Control Property Eligibility Criteria:1.Same or similar: Brand / Size / Group Mix / Type (airport vs. non)2.Similar seasonality3.Control properties must be on similar systems4.No change in Quality Scores

7/30/2013

28

55

STRATEGY TESTING USING CONTROL PERIOD APPROACH – METHOD 2

Control Hotels1%

Control Hotels1%

BETA Hotels5%

BETA Hotels5%

Test Results

Ch

ang

e in

Met

ric

Total Uplift: 4%

Statistical Significance

How confident are we that the test results are not by chance?

STRATEGY TESTING USING SIMULATION – METHOD 3

Analysis

– Calculated “optimal” and “baseline” revenue scenarios to compare against actual revenue results and isolate the benefit from the test

– Optimal revenue scenario used a hindsight optimal rate based on actual demand observed

– Compared baseline, actual and optimal scenarios to measure total opportunity and percentopportunity captured

7/30/2013

29

Questions? Panel Moderator: Jeff Higley, VP, Digital Media and Communications, HotelNewsNow.com/STR/STR Global

Panelists:

Lauren Faulkner

Business Development

Executive

STR

57

Kim Tranter

Associate Professor/Dir of

Resort, Lodging & Tourism

Mgmt Programming

Johnson & Wales

University-Denver

Dev Koushik

Vice President

Global Revenue

Optimization

InterContinental

Hotels Group

Janelle Cornett

Regional Director of

Revenue Management

TPG Hospitality

Upcoming Webinars:

Next Revenue Management Webinar:

#6: Outlet and Function Space Revenue Management is Here

August 27, 2013 ♦ 2:00-3:30 pm EDT

Next Digital Marketing Webinar:

#4: eBusiness Planning for 2014

September 10, 2013 ♦ 2:00 - 3:00 pm EDT

7/30/2013

30

59

Don’t miss -

HSMAI’s MEET

Reserve your booth space today!

Visit www.hsmaimeet.com for more

information.

7/30/2013

31

61

Get Informed - Get Ahead – Get Certified!

Certified Revenue Management Executive (CRME)

Certified Hospitality Digital Marketer (CHDM)

Certified Hospitality Sales Executive (CHSE)

Certified in Hospitality Business Acumen (CHBA)

Go to www.hsmaicertifications.org

For more information and downloadable applications!

Evaluation

� Please take a moment now to click on the Evaluation link

in the LINKS box and complete the evaluation.

� Be sure to click on “Submit” when you have completed

the evaluation to send us your responses.

� Your comments & suggestions are very important to us,

and they help us to provide you with quality programming.

Today’s webinar is copyright 2013 by the Hospitality Sales & Marketing Association International with All Rights Reserved.

62