paradigm shift in domestic natural gas resources, supplies and costs

TRANSCRIPT

JAF028113.PPT1 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Paradigm Shift in Domestic Paradigm Shift in Domestic Natural Gas Resources, Supplies and CostsNatural Gas Resources, Supplies and Costs

Prepared For: EFI Gas-to-Market & Energy Conversion Forum

Prepared By:Vello Kuuskraa, PresidentADVANCED RESOURCES INTERNATIONAL, INC.Arlington, VA

September 21-23, 2009Grand Hyatt, Washington, DC

JAF028113.PPT2 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Presentation OutlinePresentation Outline

1. Where Are We and How Did We Get Here?

2. U.S. Natural Gas Resource Base

3. Role of Technology

4. What is the Outlook?

5. Challenges and Barriers

JAF028113.PPT3 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Where Are We?Where Are We?

• Gas storage is full and expected to reach record levels.

• We have a surplus of domestic natural gas production capacity.

• Gas prices (Henry Hub, spot) are down sharply from over $10/Mcf a year ago to about $3/Mcf today.

• The LNG terminals are mostly empty and the rig market has collapsed.

From expectations of scarcity and statements that “we cannot drill our way out” of the looming natural gas supply problem, today:

JAF028113.PPT4 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

How Did We Get Here?How Did We Get Here?

• Push for large-scale LNG (by Greenspan, Chairman of the Federal Reserve) to forestall shortages.

• Publication of “Diminishing Returns” (by CERA), projecting loss of natural gas production capacity, even at prices of $10/Mcf.

For many years, we were advised that shortages and high prices were the future of U.S. natural gas supply:

“With visions of sugar plums dancing in their heads”,industry invested massively in LNG and new drilling.

JAF028113.PPT5 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

How Did We Get Here?How Did We Get Here?

• Undue concentration on the challenges facing conventional gas supplies.

• Lack of understanding and acceptance of the potential offered by unconventional gas resources.

• Dismissal of the benefits from progress in technology.

To better understand today’s situation, we need to ask - -“Why was this past advice so off-base?”

JAF028113.PPT6 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

After A Decade of After A Decade of ““Running In PlaceRunning In Place””, Aggressive Pursuit of , Aggressive Pursuit of Unconventional Gas, Particularly Gas Shales, Has Led to IncreaseUnconventional Gas, Particularly Gas Shales, Has Led to Increased d

Production CapacityProduction Capacity

Source: DOE-EIA Short Term Energy Outlook (August 2009)

*Hurricane effects

*

*

*

40

42

44

46

48

50

52

54

56

58

60

Jan-1998

Jan-1999

Jan-2000

Jan-2001

Jan-2002

Jan-2003

Jan-2004

Jan-2005

Jan-2006

Jan-2007

Jan-2008

Jan-2009

Jan-2010

Month-Year

Dry

Gas

Pro

duct

ion

(Bcf

/d)

Actual Dry Gas (Bcf/d)

Projected Dry Gas (Bcf/d)

JAF2

0090

29.X

LS

JAF028113.PPT7 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

U.S. Natural Gas Resource BaseU.S. Natural Gas Resource Base

Conventional Gas Resources. While the undiscovered conventional gas resource base is large, much of it is costly and difficult to access:

• Much of Onshore Conventional Gas Resource, with 285 Tcf, is in small traps or on the margins of older fields, thus costly to develop.

• Offshore Conventional Gas Resources, with 309 Tcf, has not been able to replace production or reserves for the past 7 years.

• Production of Associated Gas, with 129 Tcf, has declined from 8 Bcfd (in 2001) to 5 Bcfd today, along with declines in oil production.

• The Alaskan Gas Resources, with 169 Tcf, remains locked in place.

JAF028113.PPT8 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Offshore (GOM) Natural Gas ResourcesOffshore (GOM) Natural Gas Resources

7.42.84.620077.53.04.52006

5.1

9.7

Shallow Water

2.8

3.7

Deep Water

7.9

13.4

TOTAL

Annual Production (Bcfd)

Base Year2001

Recent Years2005

Offshore GOM conventional natural gas reserves have declined by half and production has fallen by 6 Bcfd, since 2001.

14.06.57.52007

Proved Reserves (Tcf)

14.917.4

27.1

6.78.220069.4

15.9

ShallowWater

8.0

11.3

DeepWater TOTAL

Base Year2001

Recent Years2005

JAF028113.PPT9 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

U.S. Natural Gas Resource BaseU.S. Natural Gas Resource Base

• Started twelve years ago, with low cost coalbed methane from the San Juan Basin and high productivity tight gas wells at Jonah/Pinedale (Green River Basin).

• Presentations by our firm, Advanced Resources, entitled “The Future is Unconventional”, heralded the start of this shift.

• Momentum provided by horizontal drilling and intensive stimulation technology that first unlocked the Barnett Shale andthen did the same, but more quickly, for the Fayetteville Shale.

• The final push has been the emergence of numerous large, low-cost gas shale plays.

Unconventional Gas Resources. The large, commercial-scale pursuit of unconventional gas is behind a “paradigm shift” in U.S. natural gas supplies.

JAF028113.PPT10 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Paradigm Shift in U.S. Natural Gas SuppliesParadigm Shift in U.S. Natural Gas SuppliesThe Marcellus and Haynesville are two of the “rock star” shale

basins behind the “paradigm shift” in U.S. natural gas supplies.

Marcellus Shale Haynesville Shale

JAF028113.PPT11 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Ten Of The Twelve Largest U.S. Lower-48 Natural Gas “Fields” Produce Unconventional Gas

0.5Tight Gas SandsDenver, COWattenberg100.4Conventional GasOffshore GOMLower Mobile Bay11

1.0Conventional GasHugoton Basin, OKHugoton Gas Area60.7Tight Gas SandsEast Texas, TXFreestone Trend (Shallow Bossier)*7

1.1Tight Gas SandsPiceance, COS. Piceance Basin Gas Area (Mesaverde/Williams Fork)5

0.6Tight Gas SandsEast Texas, TXCarthage (Cotton Valley)8

0.4

0.5

1.21.93.03.6

Year 2007Production

(Bcfd)

Tight Gas SandsGGRB, WYPinedale/Jonah (Lance)3

Tight Gas SandsEast Texas, TXSavell/Amoruso (Deep Bossier)12

Tight Gas SandsUinta, UTNatural Buttes (Wasatch/MV)9

CBMPowder River, WYWyodak/Big George Fairway4

Gas ShaleFt. Worth, TXNewark East (Barnett)2CBM/Tight Gas SandsSan Juan, NM/CO

San Juan Basin Gas Area (Mesaverde/Fruitland)1

Type ofResourceBasin/StateField NameRank

*Includes Firestone, Bold Prairie, Bear Creek, Dowdy Ranch and Dew.Sources: EIA 2005 and 2007 Annual Reserve Reports; Advanced Resources Unconventional Gas Data Base.

Evidence for the Paradigm ShiftEvidence for the Paradigm Shift

JAF028113.PPT12 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Evidence for the Paradigm ShiftEvidence for the Paradigm Shift

Source: EnCana, 2009

While total working U.S. natural gas rigs have declined by more than half, the rig count in the Haynesville area has remained strong, pushing Haynesville Shale production over 1 Bcfd.

JAF028113.PPT13 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

0

5

10

15

20

25

30

35

2000 2004 2008 Mid-2009

Years

U.S

. Unc

onve

ntio

nal G

as A

nnua

l Pro

duct

ion,

Bcf

/d

Coalbed MethaneTight Gas Sands

Gas Shales

U.S. Natural Gas Resource BaseU.S. Natural Gas Resource Base

Unconventional Gas Resources Unconventional Gas Production*

UndevelopedResource Base

ProvedReserves

Source: Advanced Resources International*Current U.S. natural gas consumption is about 62 Bcf.

Driven by advances in geologic understanding and progress in extraction technology, the unconventional gas resources will increasingly dominate U.S natural gas production.

366

917

48140

0

200

400

600

800

1000

1996 2008 1996 2008

Unc

onve

ntio

nal G

as R

esou

rces

(Tcf

)

CBM

Tight Gas

Gas Shales

JAF028113.PPT14 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

The Powerful Role of TechnologyThe Powerful Role of Technology

Increased understanding of unconventional gas resources and advances in horizontal drilling and intensive well completion technology have been key:

• Increased the size and productivity of recoverable resources.

• Provided predictability and lower risk.

• Converted these resources to low-cost assets.

JAF028113.PPT15 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Progress in Well Completion TechnologyProgress in Well Completion Technology

Source: Questar (2009)

Conventional Reservoir

Tight SandsSingle‐stage HF

Tight SandsMulti‐stage HF

Shale – horiz well +Multi‐stage HF

1850’s to present 1950’s to 1990’s 1990’s to present 2000 to present

JAF028113.PPT16 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

S. S. PiceancePiceance Basin: Williams Fork/Basin: Williams Fork/MesaverdeMesaverdeTight Gas Sand PlayTight Gas Sand Play

UT CO

WY

PiceancePiceance BasinBasin

• 5,000 Wells Drilled To Date• 1.1 Bcfd Tight Gas Sand Production**Average for 2007

JAF028113.PPT17 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Intensive Resource DevelopmentIntensive Resource Development

Intensive Field Development Pilot, Sec. 20, Rulison Field*

Expected Results from Intensive Resource Development (Sec. 20, T6S-R94W, Rulison)

CLOUGH19

CLOUGH21

RMV3-20

RMV6-20

RMV25-20

RMV33-20

RMV40-20

RMV55-20

RMV58-20

RMV57-20

RMV65-20

RMV67-20

RMV201-20

RMV200-20

RMV202-20 RMV

203-20

RMV64-20

RMV66-20

NW-1

20

R94W

T6S

20 Acre Pilot Infill Wells

N

JAF01862.CDR

541.70.610 A/W32Latest

1101.71.064Total

EURCum. To

Date

1.1

1.2

1.7

1.8

Avg. Recovery/ Well(Bcf)

16

8

4

4

No. of Wells

251.620 A/W1997-2000

131.640 A/W1996-1998

92.280 A/W1995

92.2160 A/WInitial Wells

EUR/Section

(Bcf)Well Spacing(Acres/Well)Date

Intensive resource development, at spacings of 10 acres/well, have transformed the modest (<3Tcf, USGS 2002) tight gas play in the Piceance Basin into a major 50 Tcf resource.

JAF028113.PPT18 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Arkoma Basin: Fayetteville Gas Shale PlayArkoma Basin: Fayetteville Gas Shale Play

Western AreaWestern Area

Arkoma Basin Arkoma Basin –– Fayetteville Gas Shale PlayFayetteville Gas Shale Play

AR

OK

TX

MO

MS

Central AreaCentral Area

Eastern AreaEastern Area

• 1,000 Wells Drilled To Date• 1 Bcfd Gas Shale Production**End of 2008

JAF028113.PPT19 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Fayetteville Shale: Improving Well PerformanceFayetteville Shale: Improving Well Performance

3,8702,3102,5402,9901201st Qtr 2009

3,3001,9402,1502,340751st Qtr 2008

4,1202,6902,9503,6101112nd Qtr 2009

3,7202,2102,4802,9202442nd/3rd/4th Qtr 2008

1,770

1,260

AverageIP Rate(Mcf/d)

1,490

1,070

30th Day Rate

AverageLateralLength

60th DayRate

Wells on ProductionTime Frame

197

58

1,290

960

2,500-3,1902nd/3rd/4th Qtr 2007

2,1001st Qtr 2007

Longer laterals, more frac stages, and more intensive perforation clusters (plus 3-D seismic), have improved the performance of Fayetteville Shale wells by nearly three-fold in a period of just over 2 years.

JAF028113.PPT20 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

JAF02052.CDR

What Is The Outlook?What Is The Outlook?

The Paradigm Shift. This “paradigm shift”, with vastly larger unconventional gas resources, is changing the long held belief that unconventional gas is the high cost portion of the resource base.

Unconventional gas and particularly gas shales are today the dominant source of supply and have become the low cost portion of the resource base.

Prior PerceptionPrior Perception New UnderstandingNew Understanding

Resources Resources

F&D

Cos

ts

F&D

Cos

ts

ConventionalGas

UnconventionalGas

UnconventionalGas

ConventionalGas

JAF028113.PPT21 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

What is the Outlook?What is the Outlook?

Source: Bloomberg

Oil and Natural Gas Price Relationships. A fundamental disconnect exists today in the traditional 10 to 1 oil and natural gas price relationship.

Oil Natural Gas

JAF028113.PPT22 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

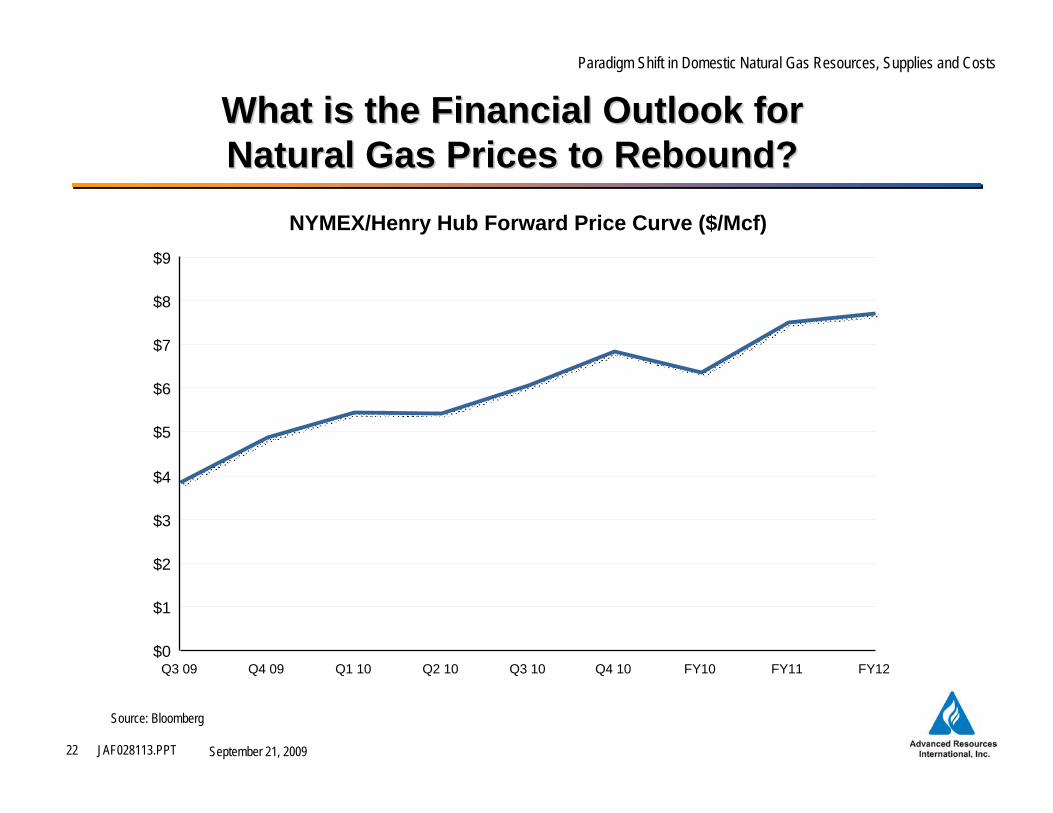

What is the Financial Outlook for What is the Financial Outlook for Natural Gas Prices to Rebound?Natural Gas Prices to Rebound?

Source: Bloomberg

NYMEX/Henry Hub Forward Price Curve ($/Mcf)

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 FY10 FY11 FY12

JAF028113.PPT23 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

What Is The Outlook?What Is The Outlook?

• EnCana, North America’s largest natural gas producer, expects long-term natural gas supply costs of $6 to $7/MMBtu.

• Anadarko, the third largest U.S natural gas producer, states that for its large Marcellus shale acreage “the economics are good” at $3/Mcf (NYMEX) (Oil and Gas Investor, August, 2009).

Source: EnCana (2009)

Producer Expectations.

JAF028113.PPT24 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Challenges and BarriersChallenges and Barriers

1. Build confidence in adequate and robust natural gas supplies.

2. Assure affordable future natural gas prices and underlying costs.

3. Address environmental barriers to natural gas development.

4. Increase demand for natural gas in a “carbon constrained” world.

The domestic natural gas supply base is diverse and abundant - -with theoretically producible resources sufficient to meet 100 years of demand, at today’s production levels.

However, a number of challenges need to be met before this theoretical potential can be converted to available and affordable natural gas production:

JAF028113.PPT25 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

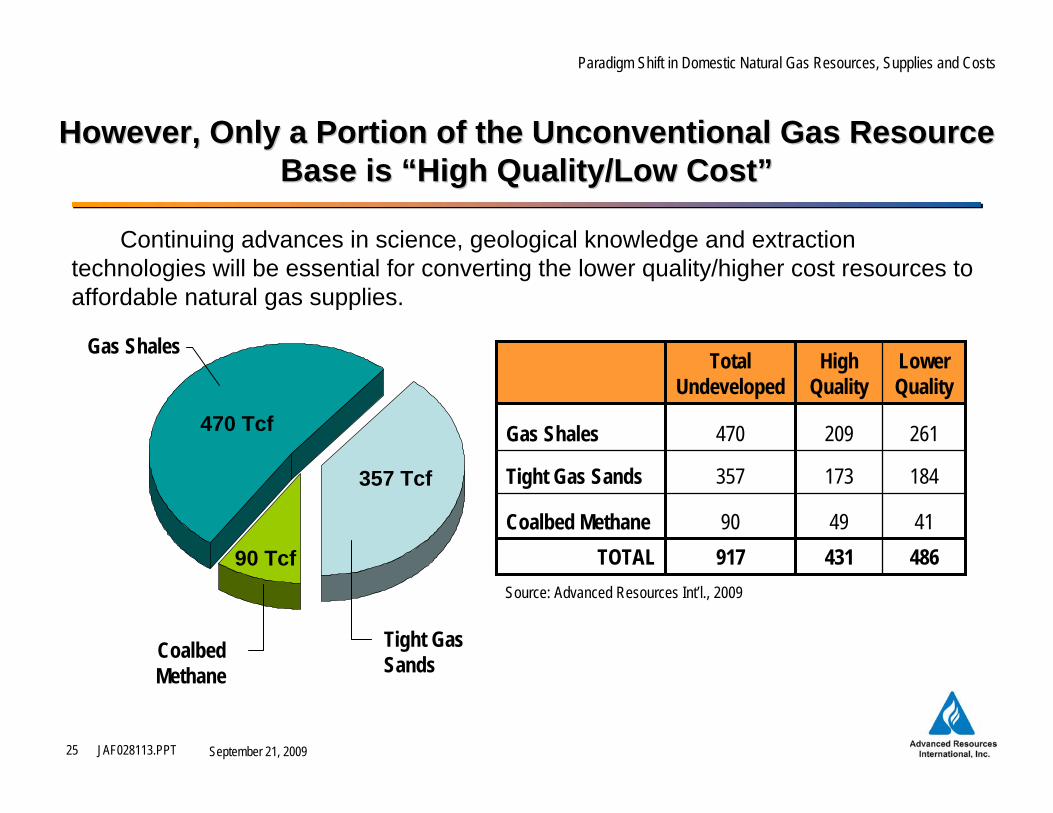

However, Only a Portion of the Unconventional Gas Resource However, Only a Portion of the Unconventional Gas Resource Base is Base is ““High Quality/Low CostHigh Quality/Low Cost””

261209470Gas Shales

91790

357

TotalUndeveloped

48641

184

LowerQuality

431TOTAL49Coalbed Methane

173Tight Gas Sands

HighQuality

Continuing advances in science, geological knowledge and extraction technologies will be essential for converting the lower quality/higher cost resources to affordable natural gas supplies.

Tight GasSandsCoalbed

Methane

Gas Shales

Source: Advanced Resources Int’l., 2009

470 Tcf

90 Tcf

357 Tcf

JAF028113.PPT26 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Addressing the Environmental Barriers to Addressing the Environmental Barriers to Greater Natural Gas DevelopmentGreater Natural Gas Development

• Capturing More Methane Emissions

• Further Reducing Surface Impacts

• Pursuing Safe Hydraulic Fracturing

As drilling increases and production grows, a harsher “spotlight” will fall on natural gas. “Green natural gas development” will help put a more environmentally friendly face on this activity.

JAF028113.PPT27 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

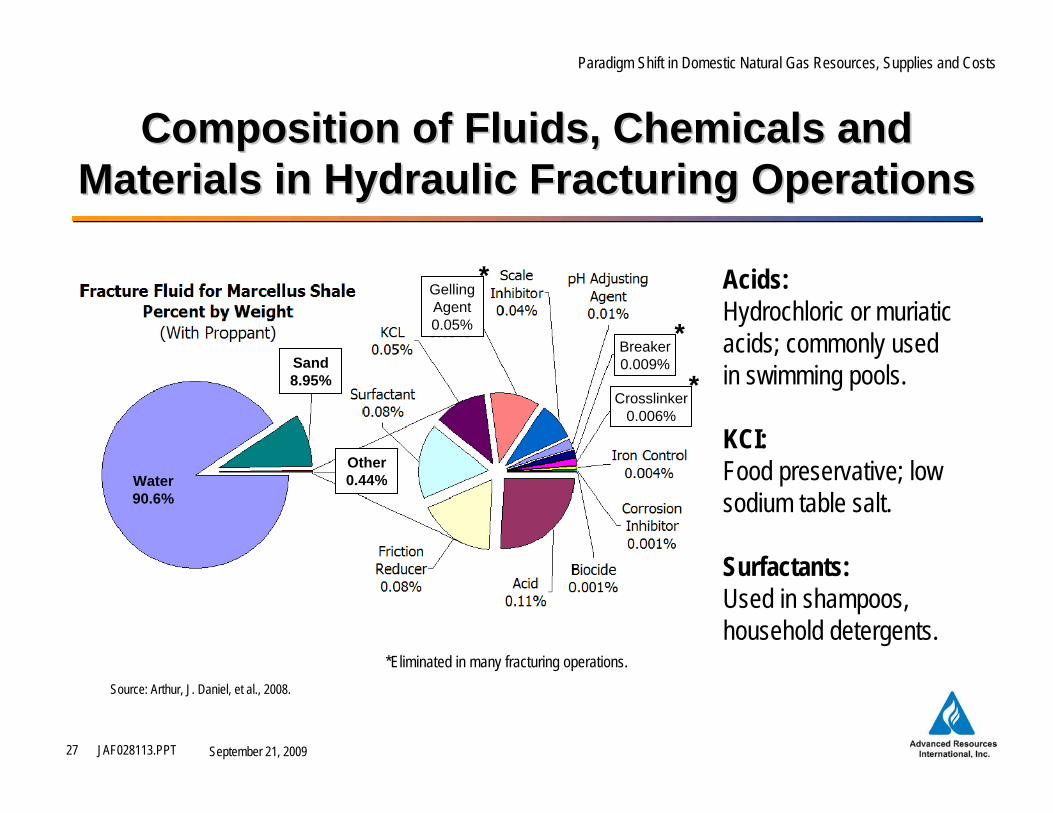

Composition of Fluids, Chemicals and Composition of Fluids, Chemicals and Materials in Hydraulic Fracturing OperationsMaterials in Hydraulic Fracturing Operations

Acids:Hydrochloric or muriatic acids; commonly used in swimming pools.

KCI:Food preservative; low sodium table salt.

Surfactants:Used in shampoos, household detergents.

Source: Arthur, J. Daniel, et al., 2008.

*Eliminated in many fracturing operations.

GellingAgent0.05%

Breaker0.009%

Crosslinker0.006%

*

*

*Sand8.95%

Other0.44%Water

90.6%

JAF028113.PPT28 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Building Demand for Natural Gas in a Building Demand for Natural Gas in a Carbon Constrained WorldCarbon Constrained World

Natural gas is a relatively “clean fuel” with lower emissions of CO2and SO2 than coal or oil. Still, producing and using natural gas contributes to overall emissions of greenhouse gases.

1.0

0.8

0.6

0.4

0.2

0Coal Natural Gas

# of C

O 2/kwh

0.99(32% E)

0.75(43% E)

0.34(54% E)

Source: EnCana 2009

CO2/SO2 Emissions Levelsby Fuel Type (lbs/BBtu)

CO2 Emissions Levels for Electricity (lbs/kwh)

JAF028113.PPT29 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

Closing Comments Closing Comments

Numerous studies by financial houses have projected that we will soon return to the “glorious days to yesteryear”, with expectations of high natural gas prices and unmet demand.

These outlooks will prove to be overly optimistic because of the fundamental “paradigm shift” that has taken place in the size of the natural gas resource base and its fundamental costs.

It is time to discard our prior perceptions and rigorously incorporate new understandings of the size and costs as well as the challenges facing domestic natural gas supplies into our business plans.

JAF028113.PPT30 September 21, 2009

Paradigm Shift in Domestic Natural Gas Resources, Supplies and Costs

AdvancedResources

Internationalwww.adv-res.com

Office LocationsWashington, DC4501 Fairfax Drive, Suite 910Arlington, VA 22203Phone: (703) 528-8420Fax: (703) 528-0439

Houston, Texas11490 Westheimer, Suite 520Houston, TX 77042Phone: (281) 558-6569Fax: (281) 558-9202