paypal: the global internet payment network

TRANSCRIPT

Scott ThompsonSeptember 17, 2009

2

This presentation may make forward-looking statements relating to our future performance that are based on our current expectations, forecasts and assumptions and involve risks and uncertainties. These statements include, but are not limited to, statements regarding expected financial results for the third quarter of 2009, and anticipated future stability and growth in the Marketplaces business unit.

Our actual results may differ materially from those discussed in this call for a variety of reasons, including, but not limited to, the impact of recent global economic events and the global economic downturn; foreign-exchange-rate fluctuations; changes in political, business, and economic conditions; the impact and integration of recent and future acquisitions; the impact of divestitures; our increasing need to grow revenues from existing users in established markets; an increasingly competitive environment for our businesses; the complexity of managing an increasingly large enterprise, with a broad range of businesses, our need to manage regulatory, tax, IP and litigation risks (including risks specific to PayPal, Bill Me Later and the financial industry, and risks specific to Skype’s technology and to the VoIP industry); and our need to upgrade our technology and customer service infrastructure at reasonable cost while adding new features and maintaining site stability.

You can find more information about factors that could affect our operating results in our most recent annual report on our Form 10-K and our subsequent quarterly reports on Form 10-Q (available at http://investor.ebay.com). You should not unduly rely on any forward-looking statements, and we assume no obligation to update them. All information in the presentation is as of July 22, 2009, and we do not intend, and undertake no duty, to update this presentation.

3

The Global InternetPayment Network

The Global InternetPayment Network

4

An evolving industry

1 Powering global eCommerce

2 Unmatched advantages

3 Significant opportunity ahead

5

6

Review &Complete

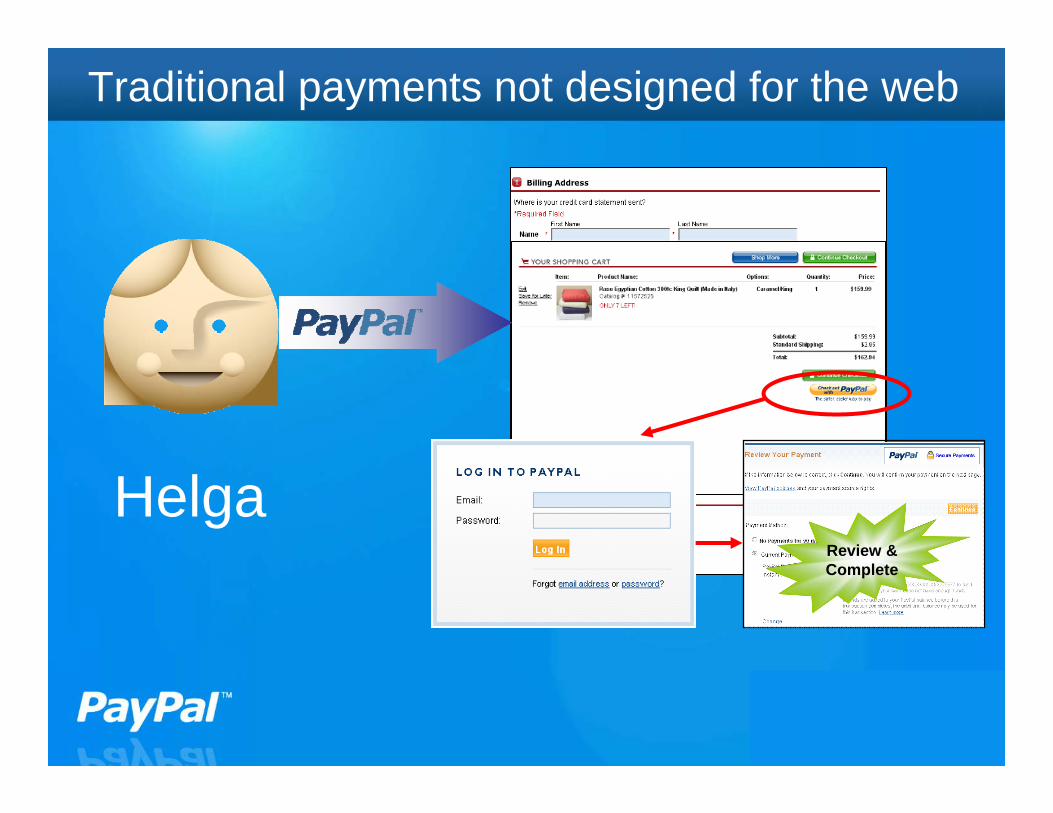

Helga

Traditional payments not designed for the web

7

Helga

Traditional payments not designed for the web

• Fraudsters• ID theft

8

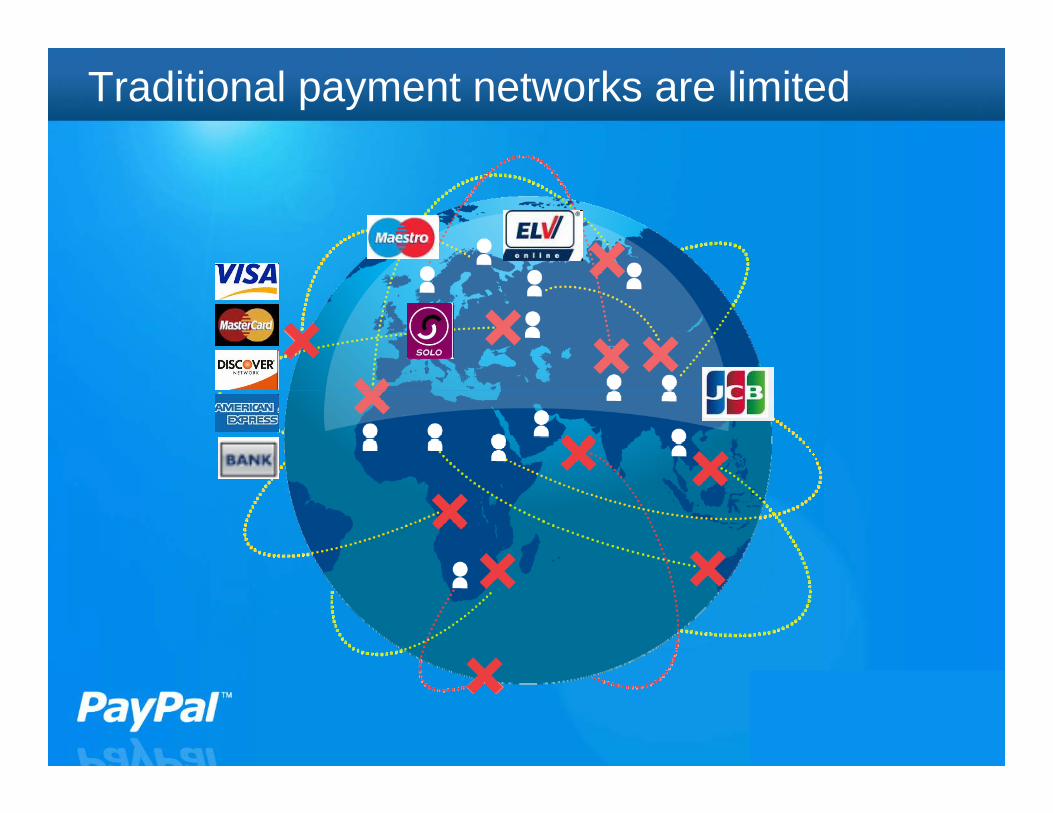

Traditional payment networks are limited

9

Worldwide accessibility

• 190 global markets

• 17 local language sites

• 19 currencies

10

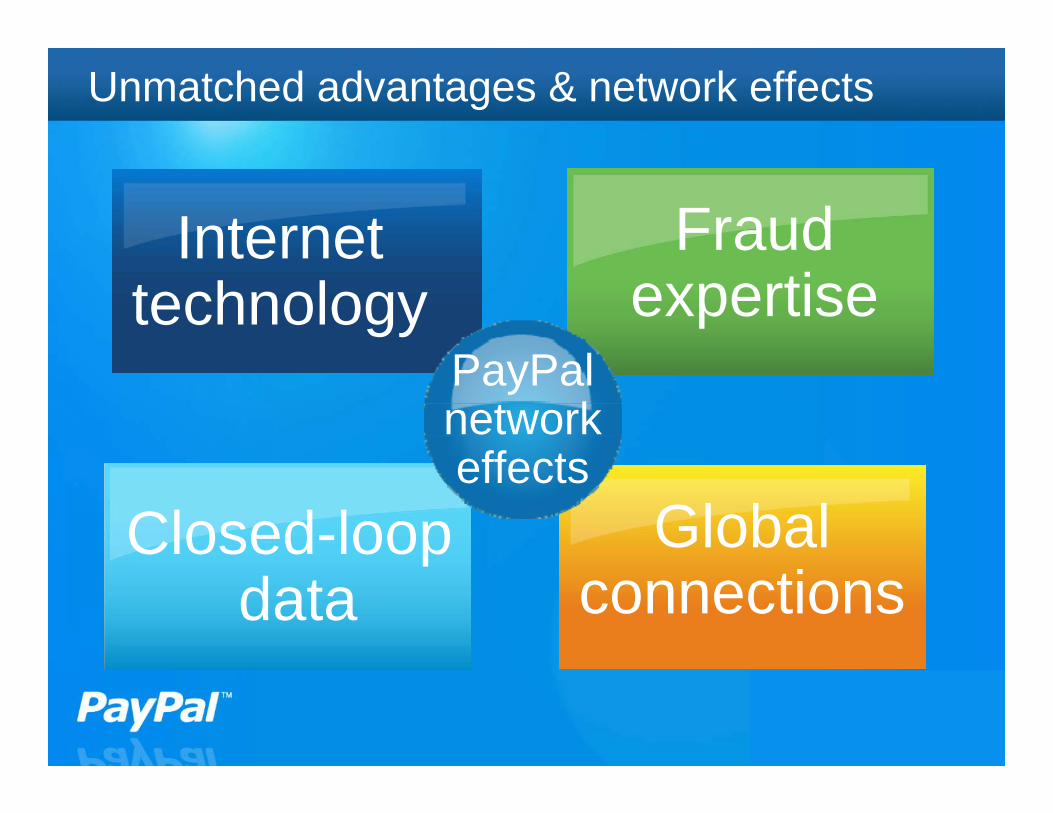

Unmatched advantages & network effects

Global connections

Internet technology

Closed-loop data

Fraudexpertise

PayPal network effects

11

Growth in active accounts

Q208 Q209

$48 Billion

$60 Billion

TPV growing 2-3X faster than competitors

49.4 Million

57.3 Million

70.4 Million

+16%+23%

2006 2007 2008

36 llion

$48 Billion

$60 Billion

49.4 Million

57.3 Million

70.4 Million

+16%+23%

62.6 Million

75.4 Million

+20%

12

2006 2007 2008

$36 Billion

$48 Billion

$60 Billion

Strong TPV growth with tremendous opportunity

TPV Growing 2-3XFaster than Competitors

$100-120BILLION

2011

$16.7b inQ209

13

How we’ll get there

Global eBayGlobal eBayGlobal Merchant Services

Global Merchant Services

Adjacent paymentsAdjacent payments

14

Global eBayGlobal eBay

15

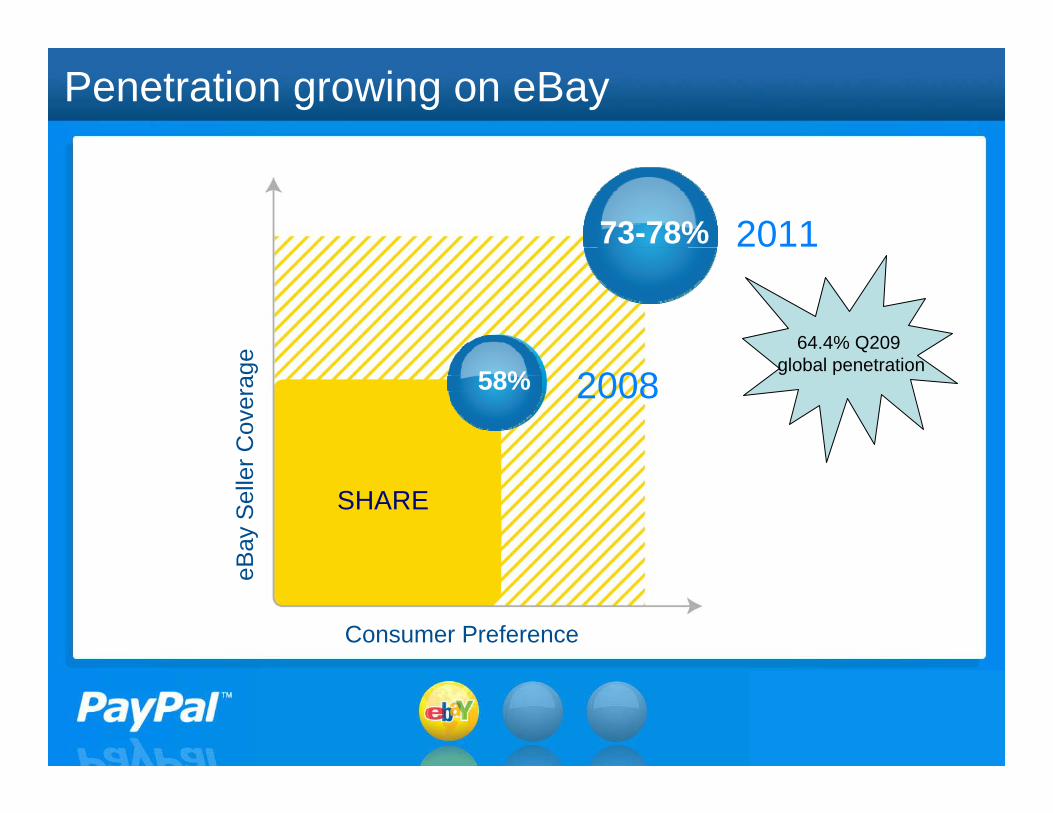

Penetration growing on eBay

Consumer Preference

eBay

Sel

ler C

over

age

2008

2011

SHARE

58%

73-78%

64.4% Q209global penetration

16

$24B$29B

41%

79%

North America International

Significant opportunity in international markets

2008 eBay aGMV & PayPal penetration*

*Includes shipping and handling

17

Global Merchant ServicesGlobal Merchant Services

18

Gaining share in Global Merchant Services

Consumer Preference

Mer

chan

t C

over

age

5% 2008

2011

SHARE

8-9%

19

Success across merchant segments

eCommerce volume

Largemerchants

Small/medium businesses

Soleproprietors

Total

PayPal TPV2006-08 CAGR

130%

71%

33%

77%

17%

6%54%

20

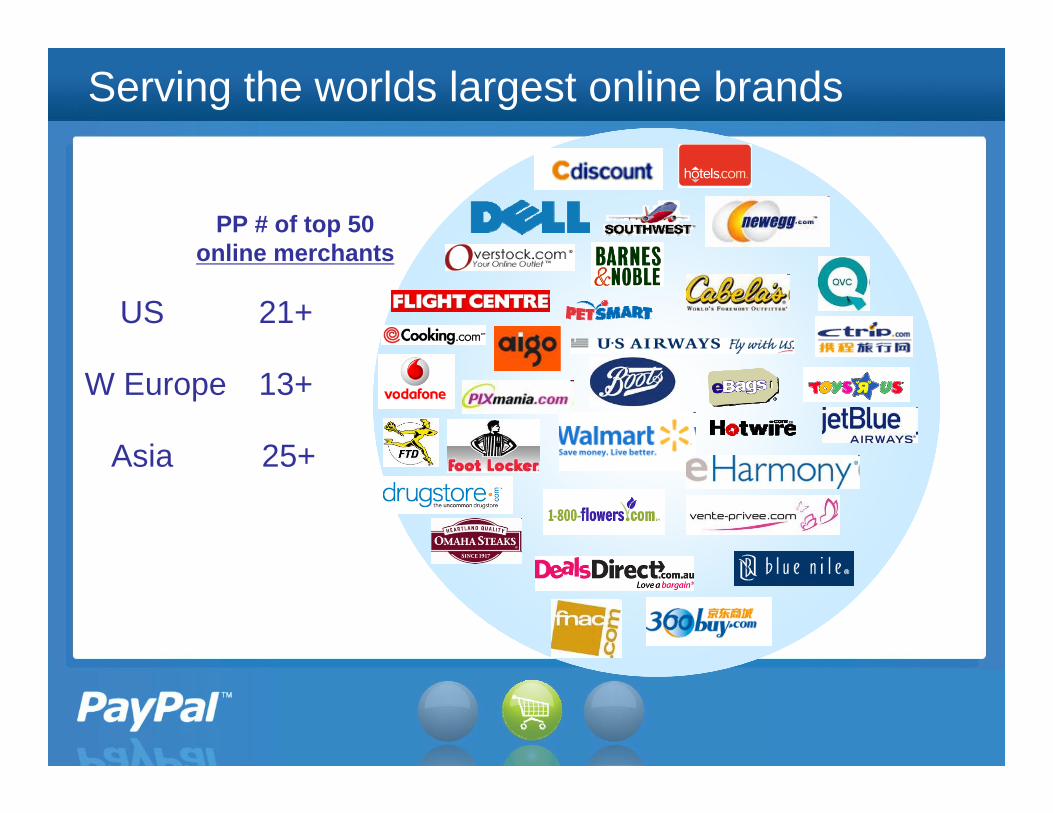

PP # of top 50online merchants

21+

W Europe

Serving the worlds largest online brands

13+

25+Asia

US

21

$293Billion

$460-480Billion

International

2008 2011

2% 5-6%

Opportunity in NA and International markets

2008 2011

$237Billion

$305-315Billion

North America

9% 13-14%Share

22

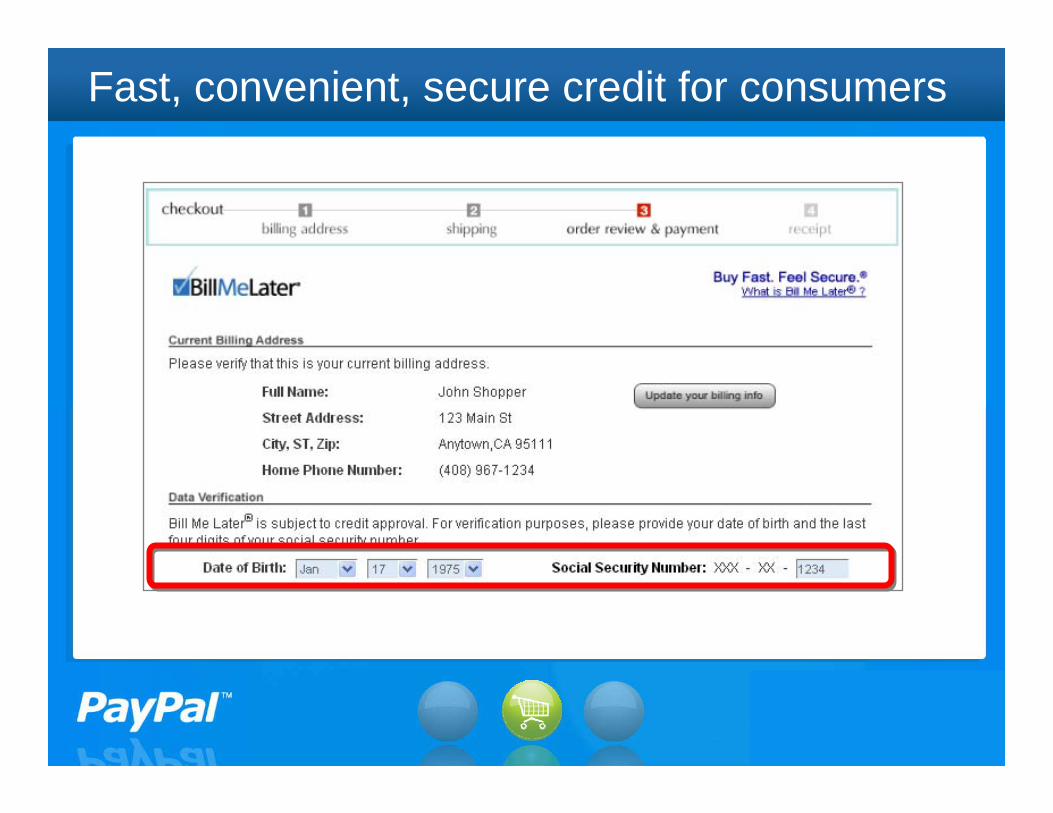

Bill Me Later complements PayPal

• Helps PayPal drive coverage & preference

• Helps merchants drive sales

23

Sales lift through promotional offers

Sales lift for merchants

24

Fast, convenient, secure credit for consumers

25

Credit card

Structural advantage in risk management

$

$$

$$$$$

26

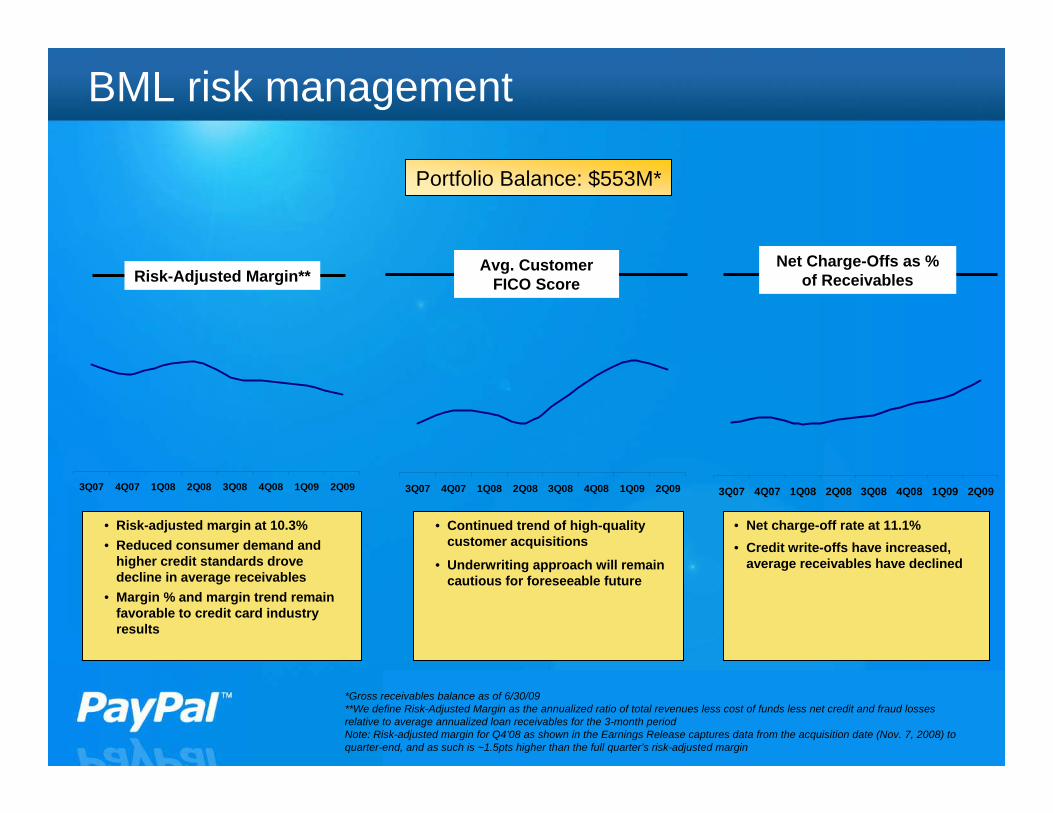

BML risk management

Risk-Adjusted Margin**Avg. Customer

FICO ScoreNet Charge-Offs as %

of Receivables

*Gross receivables balance as of 6/30/09**We define Risk-Adjusted Margin as the annualized ratio of total revenues less cost of funds less net credit and fraud losses relative to average annualized loan receivables for the 3-month periodNote: Risk-adjusted margin for Q4’08 as shown in the Earnings Release captures data from the acquisition date (Nov. 7, 2008) to quarter-end, and as such is ~1.5pts higher than the full quarter’s risk-adjusted margin

• Risk-adjusted margin at 10.3%• Reduced consumer demand and

higher credit standards drove decline in average receivables

• Margin % and margin trend remain favorable to credit card industry results

• Continued trend of high-quality customer acquisitions

• Underwriting approach will remain cautious for foreseeable future

• Net charge-off rate at 11.1%• Credit write-offs have increased,

average receivables have declined

Portfolio Balance: $553M*

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q093Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09

27

Grow eBay GMV

Accelerate merchant sales cycle

Speed Bill Me Later consumer acquisition

Significant PayPal – BML synergies

Turn transaction expense into revenue

Decrease Bill Me Later fraud losses

Reduce Bill Me Later cost of capital

28

Adjacent paymentsAdjacent payments

29

Mobile & other devices

Mobile & other devices

Social networksSocial networks

Businesses withspecializedpayment needs

Businesses withspecializedpayment needs

BanksBanks

Non-profitsNon-profits

GovernmentsGovernments

Many sectors need payment solutions

30

Platform

660k+ developers

225k+ developers

100k+ developers

Millions of .NET developers

PayPal platform enables developers

PayPal global Internet payments network

Global Merchant Services

eBay

Adjacent Payments

$100-120B

$60B

Tremendous growth ahead: TPV

Global Total Payment Volume

2008 2011

18-26%

CAGR

Tremendous growth ahead: metrics

‘05 ‘06 ‘07 Future

Global take rateGreat deals for

merchants

Transaction expenseConsumer funding choice

Transaction LossesRisk management

stable declines stable / down

… ~60% transaction margin business

‘08 ‘05 ‘06 ‘07 Future‘08 ‘05 ‘06 ‘07 Future‘08

33

Tremendous growth ahead: margins

2009-10: margin decrease due to BML integration

Medium term: margins return to 18-20%

Longer term: margin expansion as thebusiness scales over investments

34

Tremendous growth ahead: revenue

2008

$2.4BILLION

2011

$4-5BILLION

2009-2011 CAGRs

On eBaylow single digits

Merchant Services30% range

BML/Adjacent pmts40% range

35

An evolving industry

1 Powering global eCommerce

2 Unmatched advantages

3 Significant opportunity ahead

36

The world’s favorite way to pay and be paid