asb operations manual - bellevue school district operations manual effective: september 1, 2011 ......

TRANSCRIPT

1

To Table of Contents

Bellevue School District

ASB Operations Manual

Effective: September 1, 2011

Staff:

Simone Sangster, Ed.D.

Assistant Superintendant of Finance and Operations

Marie Telecky

Director of Finance and Budget

Marlyn Keating

Director of Fiscal Services

Fred Johnson, CPA Consultant

Note: Parts of this manual are still under construction. Updates will be issued as quickly as possible. Contact Marlyn Keating or Marie Telecky in the Business Office if you have questions. Also, if you see something that should be changed or is unclear, please let us know.

2

- 3 -

Bellevue School District ASB Manual

Table of Contents Part Title Section Description Page l Introduction 1 Introduction 2 How to Navigate This Manual 3 Definitions 4 Legal References

ll Guidance Topic Sections

1 Supervision 2 Constitutions and Charters 3 Student Involvement 4 Uses of ASB Funds

5 Budgeting 6 Cash Handling 7 Activities/Fundraising - ASB 8 Auto Shop Donations 9 Found Property 10 Individual-type Fundraiser 11 Fundraising through Gambling and Raffles 12 Fundraising – Non-ASB 13 Ticket Sales 14 Student Stores 15 Refunds 16 Vending Machines 17 Fundraising – General Fund 18 Donations 19 Food 20 School Support Organizations 21 Purchasing Methods 22 Credit Cards 23 Consultant/Contractual Service Agreement 24 Travel 25 Gifts, Awards, Prizes, and Incentives 26 Employee Pay/Reimbursement 27 Internal Controls 28 Interest Earnings 29 Taxes 30 Records Retention III Appendix

1 Exhibit A – Sample ASB Group Constitutions 2 Exhibit B – Sample ASB Activity Group Charter 3 Exhibit C – ASB Meeting Minutes Template 4 Exhibit D – Activity/Fundraiser Approval Form 5 Exhibit E – Requisition for Goods or Services 6 Exhibit F – Parent-Student Fundraiser Acknowledgment Form 7 Exhibit G – Inventory Check-out and Check-in Sheet 8 Exhibit H – Sales Receipt Sheet

- 4 -

9 Exhibit I – Advisor‘s/Accountant‘s Cash Deposit Record 10 Exhibit J – Advisor‘s/Accountant‘s Cash Box Checkout Form 11 Exhibit K – Activity/Fundraiser Checklist 12 Exhibit L – Credit Card Memorandum of Understanding 13 Exhibit M – Donation Form 14 Exhibit N – ASB Manual Amendment Request Form 15 Exhibit O – Periodic Inventory Count Sheet 16 Exhibit P – Notice of Refund Receipt 17 Exhibit Q – Memo of Understanding 18 Exhibit R – Contract for Professional services 19 Exhibit S – Joint ASB/SSO Event Agreement [temporarily

removed] 20 Exhibit T – Lost or Missing Purchasing Card Receipt Form 21 Exhibit U – Extended Field Trip Approval Form 22 Exhibit V – High School Athletic Participation Fee

BSD ASB Manual

Introduction

Effective Date: 9/1/2011

- 5 -

Introduction To Table of Contents The purpose of the Bellevue School District (BSD) Associated Student Body (ASB) Manual is to present the regulatory requirements applicable to ASB governance and provide best practice guidelines, in the form of forms and procedures, for the operation of the ASB activities. The District‘s aim is to meet or exceed the standards and expectations for financial management, procedures, controls, and record keeping set forth by the Washington State Auditor‘s Office (SAO), the School District Accounting and Advisory Committee as set forth in the Accounting Manual for School Districts, and the Washington Association of Business Officials (WASBO). Adherence to District policy 7300, ―Associated Student Body‖, District procedure 7300, ―Associated Student Body‖, and this manual will provide students an education in good governmental and business practices, allow for the proper monitoring and control of ASB activities and funds, and create positive audit experiences at the school and District levels. The goal of the Bellevue School District‘s ASB organization and each of its activities is to provide students with:

1. Opportunities for enrichment through participation in extracurricular activities and 2. Rewarding experience in student government, business management, service and leadership.

Note: ASB operations involve all fundraisers involving deposit in the District‘s ASB Fund and all ASB activities requiring disbursement from the District‘s ASB Fund. Career and Technical Education (CTE) groups should refer to the Bellevue School District CTE manual for guidance related to CTE operations. While we realize that there may be topics in this manual that are not addressed in complete detail, the material provided herein is to be used as official operating guidance for all ASB Student Councils, athletic groups, classes and clubs (ASB Groups). Where further guidance is required, advisors and students are encouraged to contact the following individuals in the District‘s central Accounting Department during regular business hours:

Linda Jones, Senior Accountant - (425) 456-4014, [email protected]

Jessica Li, Senior Accountant - (425) 456-4012, [email protected] If an ASB group would like to suggest a revision or request that new guidance material be added to the

manual, they may request that such be presented to the District for consideration by completing an

Amendment Request Form and submitting it to the District for review (see the District‘s web page for an

electronic copy).

To Table of Contents

BSD ASB Manual

How to Navigate This Manual

Effective Date: 9/1/2011

- 6 -

How to Navigate This Manual The BSD ASB Manual is intended to be as accessible a reference as possible. Because of its size and

complexity, navigational tools have been incorporated into the design of the manual so that answers to

your ASB related questions can be easy to find.

Table of Contents

Readers are encouraged to start with the table of contents. If a term you have in mind is not found there,

you can press the Ctrl and F keys (at the same time) to access a tool you can use the search the document.

Try it! If you see what you are looking for in the table of contents, hold the Ctrl key and mouse over the

name of the section title. You will notice that section titles are quick links to each section and exhibit in the

document. Within the section you chose, there may be a section contents table that will help you locate a

more applicable subtopic within the section. These section tables of contents are also quick linked.

Legal References

The section for laws applicable to ASB governance includes links to sections that each law applies to.

Because laws may not reference all applicable sections, after gaining an understanding of a law you

should use judgment to determine whether it applies to other areas of concern as well as those referenced

after each law. Also, within each section, in the reference area, there are links to laws that pertain to it.

You can use these links to understand the laws that gave rise to the procedures you are learning about.

Section Cross Reference Links

A topic may be documented in more than one place. You should be sure to sure to follow the links within

section documentation or in the references area at the end of each section which will navigate you to other

sections, BSD policies or BSD procedures where materials may be discussed in further detail. Do this so

that you can get a complete understanding of both the guidance surrounding a topic and also associated

topics which you should be aware of. In addition to the laws linked in each section, you can use these

section and policy/procedure links to learn about related information so that you can get a more complete

understanding of guidance materials. Be aware that some links are to web pages where source materials

are located. You will need a web browser, such as Windows Internet Explorer to reach them.

Exhibits

There are many exhibits in the document. Each pertains to a specific procedure. References to the forms,

checklists, contracts, and other tools discussed in each section are linked therein. These forms have been

included to serve as references. Use these links to navigate to each tool discussed so that you can see

procedures illustrated through the tool. Note, they may not reflect the most up to date version so please

see the District‘s web site for copies to use throughout your ASB group operations.

Definitions

BSD ASB Manual

How to Navigate This Manual

Effective Date: 9/1/2011

- 7 -

ASB terminology can be confusing. In order to help clarify what the meaning of a term is, a section for

Definitions has been included for your convenience. Additionally, definitions have been included

throughout section documentation to help readers better understand instructions contained in the manual.

Ctrl H To return to the top of the document at any time, press the Ctrl and H keys at the same time. Try it!

Top of Section Links

To return to the top of the section you are in at any time, press Ctrl and mouse over the ―Back to top of

section‖ links located throughout the section.

Table of Contents Links

To return to the Table of Contents at any time, press Ctrl and mouse over the ―To Table of Contents‖ links

located at the top and bottom of each section.

Page Up / Page Down

Lastly, instead of scrolling with the mouse, you can more quickly return to a specific area within a section

by pressing the Page Up or Page Down keys.

We hope you find this manual useful and easy to navigate. Good luck!

Go to Table of Contents

BSD ASB Manual

Introduction: Definitions

Effective Date: 9/1/2011

- 8 -

To Table of Contents

ASB: An Associated Student Body organization is a formal organization of student interest groups formed at a District schools. It comprises both the ASB Student Council (in charge of the entire campus, often called ―ASB‖) and ASB Activity groups (such as athletics, classes (Junior, Senior, etc.) and clubs).

ASB Student Council: The ASB Student Council (sometimes called the ASB) is the prime student council, student activities board, or other officially recognized group of students appointed or elected to represent the entire associated student body within a school.

ASB Activity Group: The term ASB Activity Group (sometimes called activity) refers to smaller, extracurricular, interest-specific groups of students including athletics, classes and clubs.

ASB Group: Refers to every individual ASB organization, either an ASB Student Council or ASB Activity Group. The term is appropriate as Student councils and activity groups follow many of the same procedures and the term ―group‖ can inclusively refer to each.

Prime Advisor: The Prime Advisor is the District employee charged with campus-wide ASB oversight. By default, the Prime Advisor at each District School is the Principal. The Principal at District middle high schools may by law delegate his/her campus-wide ASB oversight responsibility. As such, the Prime Advisor is usually an Assistant Principal at a District middle school and the Athletic Director at District high schools. By law, the Prime Advisor is the Principal at District elementary schools. The rime has responsibility to 1) sign ASB group event approval forms, purchase requisitions and contracts, 2) supervise the operations of the ASB groups he/she is responsible for, and 3) intervene as deemed appropriate.

Advisor: When you see the term ―advisor‖ understand that this is the advisor who supervises your ASB group. If your group is the ASB Student Council, than the ―advisor‖ is the teacher or staff member who supervises the student council. If your group is the Spanish club, then the ―Advisor‖ is the teacher who supervises the Spanish club. So on and so forth.

ASB Accountant: The ASB Accountant is the person in your school‘s office who is handles ASB related forms, purchases, cash collection and deposit, accounts, calendars and so on. The office at your school may not have a person who has ―ASB Accountant‖ as their official title. However, if they perform the roles above, then they are your ASB accountant.

Event: An event is any single event produced by an ASB group including fundraisers (whose primary purpose is to raise funds, e.g., a sale, receiving donations etc.), an activity (whose primary purpose is not to raise funds, e.g., field trips, awards banquets, parties etc.) or a fundraiser/activity (where both fundraising and an activity take place on the same date (a dance, an athletic event, or a concert etc.).

ASB Moneys: Associated student body public moneys are fees collected from students and nonstudents as a condition of their attendance at any optional noncredit extracurricular event of the school district which is of a cultural, athletic, recreational or social in nature and any other moneys received by an associated student body for the support of an associated student body program other than those moneys specified in subsection (5) of WAC 392-138-010.

Non-ASB Moneys: Non-ASB, private moneys are generated by fundraising activities or solicitation of donations by student groups, in their private capacities, for private purposes and/or private gifts and contributions.

School Support Organization: The term school support organization refers to parent-staff-student associations including, but not limited to, Parent Teacher Associations (PTAs), Parent Teacher Student Associations (PTSAs) and Booster Groups. While encouraged by the district, these are legally separate organizations and care should be exercised in segregating school support organization assets from public ASB assets.

BSD ASB Manual

Introduction: Definitions

Effective Date: 9/1/2011

- 9 -

Policy Cross References 7300 – Associated Student Body

Procedure Cross References 7300.1 – Associated Student Body

Legal References

RCW 28A.320.030 Gifts, conveyances, etc., for scholarship and student aid purposes, receipt and administration

RCW 28A.325.010 Fees for optional noncredit extracurricular events– Disposition.

RCW 28A.325.020 Associated student bodies–Powers and responsibilities affecting

RCW 28A.325.030 Associated student body program fund–Fund raising activities- Non-associated student body program fund moneys

WAC 392-138-010 Definitions

To Table of Contents

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 10 -

To Table of Contents

REVISED CODE OF WASHINGTON (RCW’S)

Section Contents 1. RCW 28A.320.030 - Gifts, conveyances, etc., for scholarship and student aid purposes, receipt and

administration. 2. RCW 28A.325.010 - Fees for optional noncredit extracurricular events– Disposition. 3. RCW 28A.325.020 - Associated student bodies–Powers and responsibilities 4. RCW 28A.325.030 - Associated student body program fund–Fund raising activities- Non-associated

student body program fund moneys.

WASHINGTON ADMINISTRATIVE CODE (WAC’S)

Section Contents 1. WAC 392-138-003 - Authority.

2. WAC 392-138-005 - Purposes.

3. WAC 392-138-010 - Definitions.

4. WAC 392-138-011 - Formation of associated student bodies required.

5. WAC 392-138-013 - Powers – Authority and policy of board of directors.

6. WAC 392-138-014 - Accounting procedures and records.

7. WAC 392-138-017 - Segregation of public and private moneys.

8. WAC 392-138-018 - Petty cash funds.

9. WAC 392-138-019 - Compliance with bid law required.

10. WAC 392-138-021 - Title to property - Dissolution of associated student body or affiliated group.

11. WAC 392-138-105 - Associated student body public moneys – Fees optional noncredit extracurricular

events.

12. WAC 392-138-110 - Associated student body public moneys – Associated student body program

budget.

13. WAC 392-138-115 - Associated student body public moneys – Deposit and investment.

14. WAC 392-138-120 - Associated student body public moneys – Imprest bank checking account.

15. WAC 392-138-125 - Associated student body public moneys – Disbursement approval – Total

disbursements.

16. WAC 392-138-130 - Associated student body public moneys – League and other joint activities.

17. WAC 392-138-200 - Non-associated student body private moneys.

18. WAC 392-138-205 - Non-associated student body private moneys – Deposit and investment.

19. WAC 392-138-210 - Non-associated student body private moneys – Disbursement approval – Total

disbursements.

RCW 28A.320.030 - Gifts, conveyances, etc., for scholarship and student aid purposes, receipt and

administration.

The board of directors of any school district may accept, receive and administer for scholarship and

student aid purposes such gifts, grants, conveyances, devises and bequests of personal or real property, in

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 11 -

trust or otherwise for the use or benefit of the school district or its students; and sell, lease, rent or

exchange and invest or expend the same or the proceeds, rents, profits and income thereof according to

the terms and conditions thereof, if any, for the foregoing purposes; and enter into contracts and adopt

regulations deemed necessary by the board to provide for the receipt and expenditure of the foregoing.

Applicable Sections

Uses of ASB Funds

Back to top of section

RCW 28A.325.010 - Fees for optional noncredit extracurricular events–Disposition.

The board of directors of any common school district may establish and collect a fee from students and

nonstudents as a condition to their attendance at any optional noncredit extracurricular event of the district

which is of a cultural, social, recreational, or athletic nature: PROVIDED, That in so establishing such fee or

fees, the district shall adopt regulations for waiving and reducing such fees in the cases of those students

whose families, by reason of their low income, would have difficulty in paying the entire amount of such

fees and may likewise waive or reduce such fees for nonstudents of the age of sixty-five or over who, by

reason of their low income, would have difficulty in paying the entire amount of such fees. An optional

comprehensive fee may be established and collected for any combination or all of such events or, in the

alternative, a fee may be established and collected as a condition to attendance at any single event. Fees

collected pursuant to this section shall be deposited in the associated student body program fund of the

school district, and may be expended to defray the costs of optional noncredit extracurricular events of

such a cultural, social, recreational, or athletic nature, or to otherwise support the activities and programs

of associated student bodies.

Applicable Sections

Uses of ASB Funds

Activit ies/Fundraising - ASB

Back to top of section

RCW 28A.325.020 - Associated student bodies–Powers and responsibilities affecting.

As used in this section, an "associated student body" means the formal organization of the students of a

school formed with the approval of and regulation by the board of directors of the school district in

conformity to the rules and regulations promulgated by the superintendent of public instruction: PROVIDED,

That the board of directors of a school district may act or delegate the authority to an employee of the

district to act as the associated student body for any school plant facility within the district containing no

grade higher than the sixth grade.

The superintendent of public instruction, after consultation with appropriate school organizations and

students, shall promulgate rules and regulations to designate the powers and responsibilities of the boards

of directors of the school districts of the state of Washington in developing efficient administration,

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 12 -

management, and control of moneys, records, and reports of the associated student bodies organized in

the public schools of the state.

Applicable Sections:

Supervision

Constitutions and Charters

Student Involvement

Uses of ASB Funds

Internal Control

Back to top of section

RCW 28A.325.030 - Associated student body program fund–Fund raising activities- Non-associated

student body program fund moneys.

There is hereby created a fund on deposit with each county treasurer for each school district of the county

having an associated student body as defined in RCW 28A.325.020. Such fund shall be known as the

associated student body program fund. Rules adopted by the superintendent of public instruction under

RCW 28A.325.020 shall require separate accounting for each associated student body's transactions in

the school district's associated student body program fund.

All moneys generated through the programs and activities of any associated student body shall be

deposited in the associated student body program fund. Such funds may be invested for the sole benefit

of the associated student body program fund in items enumerated in RCW 28A.320.320 and the county

treasurer may assess a fee as provided therein. Disbursements from such fund shall be under the control

and supervision, and with the approval, of the board of directors of the school district, and shall be by

warrant as provided in chapter 28A.350 RCW: PROVIDED, That in no case shall such warrants be issued in

an amount greater than the funds on deposit with the county treasurer in the associated student body

program fund. To facilitate the payment of obligations, an imprest bank account or accounts may be

created and replenished from the associated student body program fund.

The associated student body program fund shall be budgeted by the associated student body, subject to

approval by the board of directors of the school district. All disbursements from the associated student

body program fund or any imprest bank account established thereunder shall have the prior approval of

the appropriate governing body representing the associated student body. Notwithstanding the provisions

of RCW 43.09.210, it shall not be mandatory that expenditures from the district's general fund in support

of associated student body programs and activities be reimbursed by payments from the associated

student body program fund.

Subject to applicable school board policies, student groups may conduct fund raising activities, including

but not limited to soliciting donations, in their private capacities for the purpose of generating non-

associated student body fund moneys. The school board policy shall include provisions to ensure

appropriate accountability for these funds. Non-associated student body program fund moneys generated

and received by students for private purposes to use for scholarship, student exchange and/or charitable

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 13 -

purposes shall be held in trust in one or more separate accounts within an associated student body

program fund and be disbursed for such purposes as the student group conducting the fund raising activity

shall determine: PROVIDED, That the school district shall either withhold an amount from such moneys as will

pay the district for its direct costs in providing the service or otherwise be compensated for its cost for such

service. Non-associated student body program fund moneys shall not be deemed public moneys under

section 7, Article VIII, of the state Constitution. Notice shall be given identifying the intended use of the

proceeds. The notice shall also state that the proceeds are non-associated student body funds to be held

in trust by the school district exclusively for the intended purpose. ―Charitable purpose‖ under this section

does not include any activity related to assisting a campaign for election of a person to an office or for

the promotion or opposition to a ballot proposition.

Applicable Sections

Student Involvement

Budgeting

Cash Handling

Activit ies/Fundraising - ASB

Fundraising – Non - ASB

Purchasing Methods

Back to top of section

WAC 392-138-003 Authority

The authority for this chapter is RCW 28A.325.020 which authorizes the superintendent of public instruction

to adopt rules and regulations regarding the administration and control of associated student body

moneys.

Back to top of section

WAC 392-138-005 Purposes.

The purposes of this chapter are to: (1) Implement RCW 28A.325.020, (2) designate the powers and

responsibilities of the board of directors of each school district regarding the efficient administration,

management, and control of moneys, records, and reports of associated student body funds, (3) encourage

the supervised self-government of associated student bodies, and (4) permit fundraising activities by

students in their private capacities for the purpose of generating non-associated student body private

moneys.

Back to top of section

WAC 392-138-010 Definitions.

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 14 -

(1) "Associated student body organization" means a formal organization of students, including

subcomponents or affiliated student groups such as student clubs, which is formed with the approval, and

operated subject to the control, of the board of directors of a school district in compliance with this

chapter.

(2) "Associated student body program" means any activity which (a) is conducted in whole or part by or in

behalf of an associated student body during or outside regular school hours and within or outside school

grounds and facilities, and (b) is conducted with the approval, and at the direction or under the

supervision, of the school district.

(3) "Central district office" means the board of directors and/or their official designee to whom authority

has been delegated to act in their behalf.

(4) "Associated student body public moneys" means fees collected from students and nonstudents as a

condition to their attendance at any optional noncredit extracurricular event of the school district which is

of a cultural, social, recreational or athletic nature, revenues derived from "associated student body

programs" as defined in subsection (2) of this section, and any other moneys received by an associated

student body, not specified in subsection (5) of this section and WAC 392-138-100, for the support of an

associated student body program.

(5) "Non-associated student body private moneys" means moneys generated by fundraising activities or

solicitation of donations by student groups in their private capacities for private purposes and/or private

gifts and contributions.

(6) "Associated student body governing body" means the student council, student activities board, or other

officially recognized group of students appointed or elected to represent the entire associated student

body within a school in accordance with procedures established by the board of directors of the school

district.

(7) ―Trust fund‖ means a fund used to account for assets held by the district in a trustee capacity for the

specific purpose designated by the fundraising group and described in the notice provided to donors prior

to the fundraising event. Such moneys must be accounted for separately from associated student body

public moneys

(8) ‖Held in trust‖ means held as private moneys either within a separate account within the associated

student body fund or in a trust fund to be disbursed exclusively for an intended purpose. [Statutory

Authority: RCW 28A.58.115. 84-13-025 (Order 84-15), § 392-138-010, filed 6/13/84; Order 4-76, §

392-138-010, filed 3/4/76, effective 7/1/76.]

Applicable Sections

Fundraising – Non - ASB

Back to top of section

WAC 392-138-011 Formation of associated student bodies required.

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 15 -

The formation of an associated student body shall be mandatory and a prerequisite whenever one or

more students of a school district engage in money-raising activities with the approval and at the direction

or under the supervision of the district: Provided, That the board of directors of a school district may act, or

delegate the authority to an employee(s) of the district to act, as the associated student body governing

body for any school facility within the district containing no grade higher than the sixth grade.

Applicable Sections

Constitutions and Charters

Student Involvement

Back to top of section

WAC 392-138-013 Powers – Authority and policy of board of directors.

(1) The board of directors of each school district shall:

(a) Retain and exercise the general powers, authority, and duties expressed and implied in law with

respect to the administration of a school district and regulation of actions and activities of the associated

student bodies of the district including, but not limited to RCW 28A.320.010 (Corporate powers), RCW

28A.150.070 (General public school system administration), RCW 28A.320.030 (Gifts, conveyances, etc.,

for scholarship and student aid purposes, receipts and administration), RCW 28A.600.010 (Government of

schools, pupils, and employees), RCW 28A.320.040 (Bylaws of board and school government), RCW

28A.400.030 (2) and (3) (Superintendent's duties), RCW 28A.600.040 (Pupils to comply with rules and

regulations), RCW 43.09.200 (Local Government Accounting — Uniform system of accounting), RCW

36.22.090 (Warrants of political subdivisions), and chapter 28A.505 RCW (School district budgets);

(b) Approve the constitution and bylaws of each district associated student body and establish policies and

guidelines relative to:

(i) The identification of those activities which shall constitute the associated student body program;

(ii) The establishment of an official governing body representing the associated student body;

(iii) The methods and means by which students shall be permitted to raise and otherwise acquire associated

student body moneys; and

(iv) The designation of the primary advisor to each associated student body and the authority of the

primary advisor to designate advisors to the various student subgroup organizations affiliated with an

associated student body;

(c) Assign accounting functions, or portions thereof, to the school building level to be performed by a

designated representative of an associated student body or centralize the accounting functions at the

district central administrative office level;

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 16 -

(d) Provide for the participation of the associated student body or bodies of the school district in the

determination of the purposes for which associated student body public moneys and non-associated

student body private moneys if held as private moneys within the associated student body fund shall be

budgeted and disbursed; and

(2) If the district permits students to conduct fundraising activities and solicitation of donations in their

private capacities they shall establish policies to permit such activities and the allowable uses of such

moneys. The board policy and/or procedures must include the approval process for such activities as well

as provisions to ensure appropriate accountability for these funds, which are required to be held in trust.

Applicable Sections

Supervision

Constitutions and Charters

Activities/Fundraisers - ASB

Internal Controls

Back to top of section

WAC 392-138-014 Accounting procedures and records.

Associated student body public and non-associated student body private moneys shall be accounted for as

follows:

(1) Accounting methods and procedures shall comply with such rules and regulations and/or guidelines as

are developed by the state auditor and the superintendent of public instruction and published in the

Accounting Manual for Public Schools in the State of Washington and/or other publications;

(2) Whenever two or more associated student bodies exist within a school district, the accounting records

shall be maintained in such a manner as to provide a separate accounting for the transactions of each

associated student body in the associated student body program fund;

(3) The fiscal and accounting records of associated student body program moneys shall constitute public

records of the school district, shall be available for examination by the state auditor, and shall be

preserved in accordance with statutory provisions governing the retention of public records; and

(4) Non-associated student body private moneys shall be held in trust by the school within the associated

student body fund or within a trust fund and be disbursed exclusively for such purposes as the student

group conducting the fundraising activity shall determine, subject to applicable school board policies. The

district shall either withhold or otherwise be compensated an amount from such moneys to pay its direct

costs in providing the service. Such funds are private moneys, not public moneys under section 7, Article VIII

of the state Constitution.

Applicable Sections

Activities/Fundraisers - ASB

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 17 -

WAC 392-138-017 Segregation of public and private moneys.

When a school district has associated student body organizations that receive both public and private

moneys as defined in WAC 392-138-010 (4) and (5), two separate sets of accounts shall be maintained. In

addition, separate accounting records shall be maintained by organization or purpose including clubs,

classes, athletic activities, private purpose fundraising events, and general associated student body.

Back to top of section

WAC 392-138-018 Petty cash funds.

The board of directors of a school district may authorize the establishment and maintenance of associated

student body petty cash funds for use in instances when it is impractical to make disbursement by warrant

or check, subject to the following conditions:

(1) A petty cash fund shall be initiated by warrant or check;

(2) Paid-out receipts shall constitute invoices for the purpose of vouchering; and

(3) An upper limit of the amount of the petty cash fund shall be established by the board of directors.

Applicable Sections

Cash Handling

Back to top of section

WAC 392-138-019 Compliance with bid law required.

The statutory provisions of RCW 28A.335.190, the so-called "bid law" governing school district purchasing

procedures, shall govern purchases payable from the associated student body funds. [Statutory Authority:

1990 c 33. 90-16-002 (Order 18), § 392-138-065, filed 7/19/90, effective 8/19/90; Order 4-76, §

392-138-065, filed 3/4/76, effective 7/1/76.]

Applicable Sections

Activities/Fundraisers - ASB

Purchasing Methods

Back to top of section

WAC 392-138-021 Title to property–Dissolution of associated student body or affiliated group.

Title to all property acquired through the expenditure of associated student body public moneys shall be

vested in the school district. In the event a member organization affiliated with an associated student body

elects to disband or ceases to exist for any reason, then (a) the school district and parent associated

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 18 -

student body shall cease carrying any money or account on behalf of or to the credit of the organization,

and (b) the records of the organization shall be retained and disposed of in accordance with applicable

state law regarding the retention and destruction of public records.

Applicable Sections

Purchasing Methods

Back to top of section

WAC 392-138-105 Associated student body public moneys—Fees optional noncredit extracurricular

events.

The board of directors of any common school district may establish and collect a fee from students and

non-students as a condition to their attendance at any optional noncredit extracurricular event of the

district which is of a cultural, social, recreational, or athletic nature: Provided, That in so establishing such

fee or fees, the district shall adopt regulations for waiving and reducing such fees in the cases of those

students whose families, by reason of their low income, would have difficulty in paying the entire amount

of such fees and may likewise waive or reduce such fees for nonstudents of the age of sixty-five or over

who, by reason of their low income, would have difficulty in paying the entire amount of such fees. An

optional comprehensive fee may be established and collected for any combination or all of such events or,

in the alternative, a fee may be established and collected as a condition to attendance at any single

event. The board of directors shall adopt policies which state that: (1) Attendance and the fee are

optional, and (2) the district will waive and reduce fees for students whose families, by reason of their low

income, would have difficulty in paying the entire amount of such fees. Fees collected pursuant to this

section shall be designated as associated student body public moneys and shall be deposited in the

associated student body program fund of the school district. Such funds may be expended to defray the

costs of optional noncredit extracurricular events of such a cultural, social, recreational, or athletic nature,

or to otherwise support the public activities and programs of associated student bodies.

Applicable Sections

Activities/Fundraisers - ASB

Ticket Sales

Back to top of section

WAC 392-138-110 Associated student body public moneys—Associated student body program

budget

Each associated student body of a school district, with the guidance of the primary advisor, and at such

time as is designated by the central district office, annually shall prepare and submit a financial plan

(budget) for support of the associated student body program to the district superintendent or his/her

designee for consolidation into a district associated student body program fund budget and then present

such budget to the board of directors of the district for its review, revision, and approval: Provided, That

revisions of the budget submitted by an associated student body and revisions of the budget approved by

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 19 -

the board of directors shall first be reviewed by the associated student body and, in the case of an

approved budget, shall be subject to the requirements of chapter 28A.505 RCW regarding emergency

expenditures or budget extensions. The budget as approved shall constitute an appropriation and

authorization for the disbursement of funds for the purposes established in the budget.

Applicable Sections

Student Involvement

Budgeting

Purchasing Methods

Student Stores

Back to top of section

WAC 392-138-115 Associated student body public moneys—Deposit and investment.

All associated student body public moneys, upon receipt, shall be transmitted intact to the district

depository bank and then to the county treasurer or directly to the county treasurer for deposit to the

credit of the "associated student body program fund" of the school district and shall be accounted for,

expended, and invested subject to the practices and procedures governing other moneys of the district

except as such practices and procedures are modified by or pursuant to this chapter.

Applicable Sections

Interest Earnings

Back to top of section

WAC 392-138-120 Associated student body public moneys—Imprest bank checking account.

The board of directors of a school district may authorize the establishment and maintenance of an

associated student body imprest bank checking account for convenience and efficiency in expediting

disbursements, subject to the following conditions:

(1) The maximum amount of such an account shall be no more than is necessary to provide for

disbursements at the level of the month of highest estimated demand for disbursements;

(2) An imprest bank checking account shall be initiated by deposit of, and replenished by, a warrant

drawn on the associated student body program fund;

(3) Disbursements from an imprest bank checking account shall be by check and shall be restricted to

payments of invoices bearing evidence of student approval in accordance with associated student body

bylaws;

(4) An imprest bank checking account shall be replenished at least once each month by a warrant drawn

on the associated student body program fund in payment of an approved voucher in an amount equal to

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 20 -

the sum total of the disbursements made by check from the imprest bank checking account during the

preceding interval; and

(5) The replenishment voucher shall reflect such information as the central district office shall prescribe

relative to identification of invoices, invoice approvals, codification of expenditures, cancelled checks, and

other information deemed pertinent.

Back to top of section

WAC 392-138-125 Associated student body public moneys—Disbursement approval – Total

disbursements.

Associated student body public moneys shall be disbursed subject to the following conditions:

(1) No disbursements shall be made except as provided for in the budget approved pursuant to WAC

392-138-040;

(2) Disbursements shall occur only upon presentation of properly prepared vouchers in such format and

design as the central district office shall prescribe;

(3) All disbursements from the associated student body program fund or any imprest bank account

established thereunder shall have the prior approval of the appropriate governing body representing the

associated student body. Supporting documentation of the vouchers shall bear evidence of approval by

the associated student body governing body in accordance with associated student body bylaws;

(4) When an account within the fund balance of an associated student body organization does not contain

a sufficient balance to meet a proposed disbursement, such disbursement shall be limited to the fund

balance: Provided, That a transfer of fund balance between associated student body organizations may

be made pursuant to the associated student body bylaws and as approved by the associated student

body governing body;

(5) Warrants shall not be issued in excess of the moneys on deposit with the county treasurer in the

associated student body program fund; and

(6) All disbursements shall be made by warrant except for disbursements from imprest bank accounts and

petty cash funds provided for in this chapter.

Applicable Sections

Student Involvement

Purchasing Methods

Student Stores

Back to top of section

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 21 -

WAC 392-138-130 Associated student body public moneys – League and other joint activities.

Athletic league and other forms of joint inter and intra school district associated student body programs

are not precluded by this chapter. In the case of such joint programs, a single school district or associated

student body or a board representing the participating associated student bodies shall manage associated

student body monies made available to it for the support of the joint program and received as a result of

the conduct of such program, in compliance with this chapter and a written cooperative agreement

authorized by the board(s) of directors of the district(s).

Back to top of section

WAC 392-138-200 Non-associated student body private moneys.

The board of directors of a school district may permit student groups to raise moneys through fundraising

or solicitation in their private capacities when the following conditions are met:

(1) Prior to solicitation of such funds, the school board approves policies defining the scope and nature of

fundraising permitted. School board policy includes provisions to ensure appropriate accountability,

including prompt deposit, holding the moneys in trust, and disbursement only for the intended purpose of

the fund-raiser;

(2) Such funds are used for scholarship, student exchange, and/or charitable purposes. Charitable

purposes do not include any activity related to assisting a campaign for election of a person to an office

or promotion or opposition to a ballot proposition;

(3) Prior to solicitation of such funds notice is given. Such notice identifies the intended purpose of the

fundraiser, further it states the proceeds are non-associated student body funds to be held in trust by the

school district exclusively for the intended purposes;

(4) The school district withholds or otherwise is compensated an amount adequate to reimburse the district

for its direct costs in handling these private moneys; and

(5) WAC 392-138-205 applies to moneys received, deposited, invested, and accounted for under this

section. Non-associated student body private moneys shall not be deemed public moneys under section 7,

Article VIII of the state Constitution.

Applicable Sections

Uses of ASB Funds

Activities/Fundraisers - ASB

Back to top of section

WAC 392-138-205 Non-associated student body private moneys—Deposit and investment.

BSD ASB Manual

Introduction: Legal References

Effective Date: 9/1/2011

- 22 -

All non-associated student body private moneys, upon receipt, shall be transmitted intact to the district

depository bank and then to the county treasurer or directly to the county treasurer for deposit to the

credit of the school district‘s trust fund or the associated student body fund, if held in trust within that fund

within accounts as defined in WAC 392-138-010 and shall be accounted for, expended, and invested

subject to applicable school board policy and/or procedures pursuant to WAC 392-138-200.

Applicable Sections

Cash Handling

Back to top of section

WAC 392-138-210 Non-associated student body private moneys—Disbursement approval—Total

disbursements

Non-associated student body private moneys shall be disbursed subject to the following conditions:

(1) If such funds are held in trust within the associated student body fund they shall be budgeted pursuant

to WAC 392-138-013(1)(d). No disbursements shall be made except as provided for in the budget

approved pursuant to WAC 392-138-110. All disbursements shall have the prior written approval of the

associated student body or such other authority designated in school district policy or procedures;

(2) If such funds are held in a trust fund they are not budgeted. Disbursements shall occur only upon

presentation of properly prepared vouchers in such format and design as the central district office shall

prescribe, and as provided for in subsection (3) of this section;

(3) Vouchers authorizing disbursements shall be accompanied by written evidence of approval of

disbursement by the associated student body or other authority designated in the school district‘s policies

and procedures; (4) Disbursements shall be made only for the intended purposes pursuant to WAC 392-

138-200.

Applicable Sections

Fundraising – Non - ASB

Purchasing Methods

Back to top of section

To Table of Contents

BSD ASB Manual

Supervision

Effective Date: 9/1/2011

- 23 -

To Table of Contents

The Board The Board of Directors (the Board) of the Bellevue School District (BSD) is responsible for District ASBs and their activities and also for the control and protection of the District‘s ASB Fund. Specifically, the Board:

Approves ASB Student Council constitutions and bylaws and approves updates or amendments thereto (see the Constitutions and Charters section of this manual).

Approves the consolidated budget of each school‘s ASB (see the Budgeting section of this manual).

Monitors ASBs to ensure that ASBs adhere to their constitutions and charters, state laws and District policies and procedures. The Board may require periodic financial or operational reports from ASBs and ASB accountants.

The Principal/Prime Advisors The Board delegates ASB administration and supervision to the principal at each school. By law, the Principal may delegate his/her ASB supervision responsibilities to a Prime Advisor. As such, in the Bellevue School District, the Prime Advisor is the Athletic Director at District high schools and the Prime Advisor is an Assistant Principal at District middle schools. At District elementary schools, by law, the principal remains the Prime Advisor and may not delegate his/her supervisory responsibilities (RCW 28A-325-020). The principal or Prime Advisor at each school is responsible for appointing school faculty to serve as teacher-advisors over ASB groups such as the student councils, athletics, classes and clubs (ASB groups).

ASB Group Advisors Advisors to ASB groups have authority and responsibility for the following:

Ensure that ASBs and ASB activity groups adhere to applicable law, their constitutions and charters, and district policy and procedures while planning and carrying out events, spending money and collecting and managing assets such as cash and inventory.

Interject with corrective direction anytime an activity is inconsistent with the law, District policy and procedure, ASB standards, student safety, or ordinarily accepted standards of behavior in the community. When in doubt, advisors shall consult the principal regarding the propriety of proposed student activities.

Students Although no student activity may be a part of the Associated Student Body program without the approval of the Board of Directors or their designees, the Board has no power to initiate Associated Student Body activities. It is the responsibility of the students at District middle and high schools to organize ASB groups, hold elections, meet as ASBs and record meting discussions, budget for and plan activities and fundraisers, approve disbursements from their ASB Fund account and self monitor and establish patterns for continual improvement. The Principal assumes these responsibilities at District elementary schools.

BSD ASB Manual

Supervision

Effective Date: 9/1/2011

- 24 -

ASB Student Councils are responsible for school athletic programs which do not have ASB student representation to the ASB Student Council. In their capacity as representatives of school athletic groups, ASB Student Council members are under the supervision of the School Athletic Director.

Legal References

RCW 28A.325.020 Associated student bodies - Powers and responsibilities affecting

WAC 392-138-013 Powers - Authority and policy of board of directors

ASB Manual Section Cross References Constitutions and Charters Budgeting Activities/Fundraising - ASB Fundraising - Non ASB Uses of ASB Funds

Policy Cross References 7300 – Associated Student Body

Procedure Cross References 7300.1 – Associated Student Body To Table of Contents

BSD ASB Manual

Constitutions and Charters

Effective Date: 9/1/2011

- 25 -

To Table of Contents

Contents

1. Definitions

2. Introduction

3. ASB Student Council Constitutions

4. ASB Activity Group Constitutions

Definitions An ASB group’s constitution is a formal document, written and approved by the ASB‘s founding officers and amended by subsequent officers as needed, which establishes the purpose, authority and scope of an ASB Student Council or ASB activity group. It establishes the existence of an ASB organization at a school and provides a framework for its activities. The word ―constitution‖ is used throughout this document in reference to an ASB group‘s constitution and by-laws combined. ASB group bylaws, written and approved by the ASB‘s founding officers and amended by subsequent officers as needed, set forth the accepted procedures by which an ASB operates. An ASB group’s charter is the document, created and awarded by a school‘s ASB Student Council, that grants an ASB activity group permission to operate as a unit within the school-wide ASB organization and establishes requirements to maintain that permission.

Back to top of section

Introduction An ASB Student Council must exist at each middle school and senior high school when students wish fundraise and carryout events that are cultural, athletic, recreational or social in nature. In addition to this school-wide ASB leadership team, schools should have ASB activity groups organized for cultural, athletic, recreational and social activities such as inter-school athletic teams; intra-school activities such as band, choir and orchestra, drama, and so on; clubs; and each class beginning with grade six. The Principal of Elementary schools is not required to create a constitution with accompanying by laws. No ASB group will be recognized by the school district until the they have created a constitution, with accompanying bylaws, and that constitution has been approved by the Board (in the case of ASB Student Councils) or the school ASB Student Council (in the case of ASB activity groups). No ASB group will be given an account in the ASB fund without presenting a properly approved constitution, with accompanying bylaws, to their school ASB accountant. Subject to the approval process, any lawful activity which promotes the educational, cultural, athletic, recreational or social growth of students as an optional extracurricular activity may be considered for recognition as an ASB activity. Back to top of section

BSD ASB Manual

Constitutions and Charters

Effective Date: 9/1/2011

- 26 -

Procedures

ASB Student Council Constitutions When a new school‘s student body wants to request recognition by the Board or an existing ASB Student Council wishes to update their constitutions: A new ASB shall:

1. Submit a copy of their constitution, in electronic format, to the District Accounting Department. The accounting department will include the constitution on the agenda or the next bi-weekly (twice per month) board meeting.

a. Students should consider using the ASB Student Council Constitution Template. An electronic copy of this template is located on the school web page.

2. The Board may accept the constitution as is or provide changes to the proposed version. a. In the case of an accepted-as-is-constitution, the Board shall evidence approval by

signature on the constitution and retain a copy of the Approved constitution at the district‘s offices.

b. In the case of revisions made by the board and communicated to the ASB, the ASB shall notify the Board in writing of its acceptance of the revisions made and return to the board a revised version of the constitution which incorporates the changes made by the Board. Upon approval of the revised version by the Board, the Board shall evidence approval by returning a signed copy of the constitution to the ASB. This record is to be kept by the ASB in perpetuity. See the Records Retention section for more information.

i. The District Accounting Department must also retain a copy of the approved constitution at the districts offices.

Existing ASB Student Councils proposing changes to their approved constitutions shall:

1. Submit to the Board an electronic copy of their constitution, highlighting what changes are

proposed and where they are proposed within the document. The changes will be considered at the next bi-weekly (twice per month) meeting of the Board.

a. For example, an ASB may wish to use the ―Track Changes‖ feature within a Microsoft Word document (see figure 1 below) to highlight proposed changes. Changes within this feature are either red or underlined and are easily identified.

2. The Board may accept the constitution as revised or provide changes to the proposed revisions.

Figure 1

BSD ASB Manual

Constitutions and Charters

Effective Date: 9/1/2011

- 27 -

3. The process for finalizing approval for revised ASB constitutions is the same as it is for the approval of constitutions for new ASBs above.

ASB Student Council constitutions should: 1. Identify how ASB officers are elected or appointed and the responsibilities of each. 2. Provide for participation by ASB representatives in the decisions to budget for and disburse ASB

moneys. 3. Identify how ASB Student Council or ASB activity group activities, the methods and means of raising

funds and uses of funds become approved by student body government. 4. Require compliance with District and school ASB policies and procedures. Back to top of section

ASB Activity Group Constitutions When an activity group of a school’s student body wants to request their ASB Student Council’s recognition of them as a new ASB activity group or if an ASB activity group wishes to update their constitutions:

1. ASB Student Councils and ASB activity groups follow similar procedures for approval or revision documented above in the ASB Student Council Constitutions sub-topic. The procedures for activity groups differ in that the ASB Student Council assumes the responsibilities of the Board and the activity group is the unit requesting recognition. Also, the constitution of an activity group is a little simpler than a student council‘s constitution in that there are fewer officers with fewer responsibilities, the scope of the ASB group is more narrow and so on. See an example of an activity group constitution in the appendix.

2. ASB activity group constitutions do not need to be approved by the Board. 3. Upon final approval by the ASB Student Council, the ASB Student Council shall provide written

notice notifying the activity group of Student council approval in the form of a written charter, permitting them to operate in their capacity as a activity group of their ASB.

a. Students are encouraged to use the BSD Sample ASB Activity Group Charter. See the District web page for an electronic copy.

After approval and recognition, ASB officers must exercise due diligence in ensuring that their ASBs adhere to their respective constitutions. ASB activity group Charters should:

1. Establish the ASB Student Council‘s approval of the constitution of the ASB activity group. 2. Approve the capacity of the ASB activity group to operate within the scope of their specific

purpose and under the supervision of the ASB Student Council and the Board of Directors. 3. State that the charter may be revoked by the ASB Student Council if sufficient evidence exists that

the ASB activity group is not adhering to their constitution, district policy and procedure or state law; the activity group has been instructed to correct the deviation; and the activity group has failed to correct the deviation.

Back to top of section

BSD ASB Manual

Constitutions and Charters

Effective Date: 9/1/2011

- 28 -

Legal References

RCW 28A.325.020 Associated student bodies - Powers and responsibilities affecting

WAC 392-138-011 Formation of associated student bodies required WAC 392-138-013 Powers – Authority and policy of board of directors

ASB Manual Cross References

Records Retention

Documents Sample ASB Group Constitutions Sample ASB Group Charter To Table of Contents

BSD ASB Manual

Student Involvement

Effective Date: 9/1/2011

- 29 -

To Table of Contents

Introduction Students‘ involvement in making decisions regarding ASB activities and funds is an integral part of the

education of the District‘s student body. It is also required by law (WAC 392-138-125). While adequate

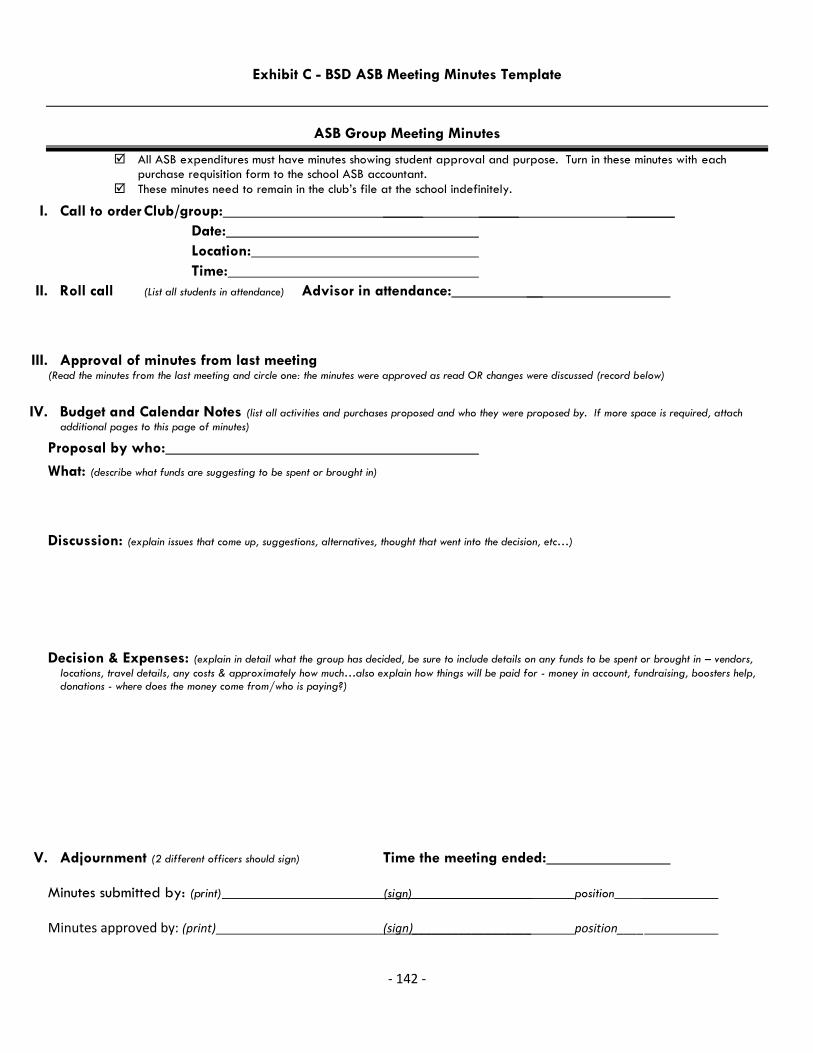

collaboration with supervising advisors is required by the Board of Directors, student ASB officers, through the formation of student government, shall administer associated student body programs and activities. All activities of ASBs involving student in grades 6 through 12 must have student approval. All expenditures by ASBs involving students in grades 6 through 12 are also to bear evidence of ASB student approval. Approval of each activity and expenditure must be documented in the minutes of the meetings of ASB Student Councils and ASB activity groups (see the BSD ASB Meeting Minutes Template for an example of how ASB groups may record their actions). Evidence of purchase approval should also be evidenced by student signature on purchase requisitions. See the purchasing methods section or more information related to purchasing.

Principals Planning and approval for activities, fundraisers, and purchases at the elementary school level is managed by the principal only, meaning that he/she completes the same forms as ASB groups and he/she approves them. In this way, elementary school ASB Fund accounts are under the same control as other District schools and the principal has a way to keep track of ASB related activities. Back to top of section

ASB Meeting Minutes As stated above, each middle school and high school‘s ASB Student Council and ASB activity group must record minutes for each meeting where events, expenditures and other ASB business is discussed. ASB groups must meet regularly enough to record and approve minutes before each event is planned and each purchase is requested or made. Student approval for all activities, fundraisers and purchases must be evident in these minutes. The following lists items, each requiring student approval, that should be recorded in the minutes of the meetings of ASB Student Councils and ASB groups:

Annual proposed budget levels.

The methods used to collect and use public and private moneys (see the Uses of ASB Funds section).

Purchase expenditures.

Contracts.

Changes to ASB constitutions and by-laws.

Appointment of the officers by the ASB group.

By law, budgets and expenditures require student approval. As such, minutes discussing either budget issues or purchasing must be detailed and specific so that accountants can be sure that purchase requisitions or budgets submitted reflect the purchase and budget details approved by ASB students.

BSD ASB Manual

Student Involvement

Effective Date: 9/1/2011

- 30 -

For example, concerning purchases, ASBs should record in their minutes:

A description of items or services to be purchased.

Prices to purchase them at.

The mane of the vendor from whom to purchase.

In the case of minutes that discuss ASB budgets, minutes should detail:

The beginning fund balance

Projected total revenues.

Projected total expenditures.

Projected inter-fund transfers.

Projected ending fund balance. ASB Meeting Minutes shall be retained in perpetuity. Each ASB shall keep on school premises all minutes pertaining to the current and the prior school year. Each year, minutes older than the previous school year shall be transferred to the BSD for archival. The elementary school ASB, administered by that school‘s Principal, is not required to produce minutes. However, because a record of fundraisers/activities, purchases, cash receipts etc. must be kept, each District Elementary school Principal should complete and approve fundraiser approval forms, purchase requisitions, event cash receipt forms and so on. This allows for elementary school ASB fund accounts to be under the same control as other schools and for the principal to have a record of the ASB related activities at his/her school. Back to top of section

Club Rosters

Each year, ASB groups, both ASB Student Councils as well as ASB activity groups, are required to supply their school accountant with a roster of the leadership of their ASB group. For each student officer of the ASB group, the roster shall include the following:

Office

Name

Graduating Class

Home Phone Number

Cell Phone Number

Email Address

Back to top of section

ASB Manual Section Cross References Uses of ASB Funds Purchasing Methods Supervision Records Retention

BSD ASB Manual

Student Involvement

Effective Date: 9/1/2011

- 31 -

Documents BSD ASB Meeting Minutes Template To Table of Contents

BSD ASB Manual

Uses of ASB Funds

Effective Date: 9/1/2011

- 32 -

To Table of Contents

Introduction Associated Student Body (ASB) funds are public funds in the custody of the school District. As such, the District must restrict, control and account for ASB money in accordance with state law.

Public vs. Private Funds In determining the appropriate uses and restrictions of moneys associated with ASB activities, an important distinction needs to be made between public and private monies. This differentiation is made as soon as money is received. Distinction and segregation of public and private monies needs to be made as follows:

Public Monies are: a) Fees collected from students and nonstudents as a condition to their attendance at any optional

noncredit extracurricular event of the school District which is of a cultural, athletic, recreational or social in nature, including revenues derived from activities during or outside regular school hours and within or outside school grounds and facilities,

b) Donations collected from students and nonstudents wherein the donor was made aware, at the time of the donation, that the donated funds would be deposited in the district‘s ASB Fund and used to finance ASB activities, or

c) Proceeds from the sale of goods and services carried out by ASB groups to fund ASB activities. Private Monies are: a) Intentional, genuine, charitable and voluntary donations not associated with any merchandise,

service or admittance to be received in exchange for the contribution (see the Activities / Fundraisers – Non ASB section of this manual for more information related to non-ASB Funds). These bona fide, voluntary contributions are wholly contributed to charitable causes, not spent on ASB activities or any other purpose.

Aside from the case of bona fide voluntary donations, all property and money acquired by Associated Student Bodies is public ASB money.

Guidelines for the Use and Restriction of Public, ASB Funds ASB Funds can only be used for legitimate and extracurricular Cultural, Athletic, Recreational or Social activities of the district‘s students (use the acronym of C-A-R-S).

The use of ASB money for curricular activities is prohibited - ASB money can only be used for optional, noncredit, extracurricular school activities. If participation in a school activity or fieldtrip etc. is required for a grade then ASB moneys cannot be used.

ASB money cannot be used for personal or private use.

ASB money cannot be used for gifts, charitable donations, scholarships or student exchanges (as these are of benefit to individuals, personally, and not the business of the District‘s ASB program or fund).

ASB Manual Section Cross References

BSD ASB Manual

Uses of ASB Funds

Effective Date: 9/1/2011

- 33 -

Activities/Fundraising-ASB Fundraising-Non ASB

To Table of Contents

BSD ASB Manual

Budgeting

Effective Date: 9/1/2011

- 34 -

To Table of Contents

Section Contents

1. Definitions

2. Introduction

3. ASB group Budget Preparation

4. Consolidated Budget

5. Ending Fund Balances / Spending Capacity

6. Excessive Beginning Fund Balances

7. Budget Maintenance

Definitions A budget is a Board-approved financial plan of an ASB Student Council or an ASB activity group and is central to each ASB group‘s annual operations. It sets the maximum amount of money an ASB group can expend in a year (―budget capacity‖). ASB budgets must be carefully planned and adhered to over the course of the school year. Budgeting is the process of estimating, as accurately as possible, the expected revenue and expenditures that will be associated with an ASB‘s activities for the coming school year. As such, accuracy in planning an ASB budget is critical. Students, with the support and supervision of advisors, shall be involved in budget development for their ASB Fund account or for the accounts within their consolidated school-wide budget.

Introduction WAC 392-138-125 states that No disbursements shall be made except as provided for in an approved budget. WAC 392-138-110 states that each ASB Student Council, with the guidance of the primary advisor, shall be involved in the preparation of its budgets. As such, students must be involved in budgetary decisions and plans, not just provide their signatures. Significant events or series of events (such as athletics, student stores, and other events with ongoing operations) must be planned well enough to be able to project annual revenues, expenses, and net cash flows in order to substantiate a reasonable annual budget. It is not reasonable to expect ASBs to accurately project all revenues and expenses up to a year in advance. As such, in each budget, it is expected that a large portion of revenues from and related expenses for unspecified fundraisers/activities be included. This allows for events that were not planned during the budget preparation period of the prior school year. Back to top of section

Budget Preparation and Submission Procedure

ASB group Budget Preparation Note: As budgeting and consolidation can be technical and require knowledge of district budgeting and accounting standards as well as proficiency in Excel, Advisors should work with students as necessary to ensure budgets are prepared in accordance with district requirements.

BSD ASB Manual

Budgeting

Effective Date: 9/1/2011

- 35 -

1. Each year, in early spring, each ASB Student Council and ASB activity group shall create their

budget for the next school year in electronic format.

a. ASB Student Council and activity group activities should be planned well enough so that each proposed budget can include the following for each account in their budget with reasonable accuracy: i. Actual beginning fund balance.

ii. Expected revenues including detail (as appropriate) of expected fees charged for

admission, prices per inventory item, prices per service provided, etc.

iii. Expected inter-fund account transfers.

iv. Expected expenditures (details not required but be sure to include tax and shipping costs in your totals).

v. Expected ending fund balance.

1. Note: Auto shop customers sometimes choose to make a donation to the school in

addition to the shop‘s charges for parts and service as a recognition of the students‘ labor. Since District CTE programs do not raise funds through receiving donations, these donations constitute donations to the ASB Auto Club and are to be deposited in that club‘s account within the ASB Fund. Donations of this kind expected to be received during any given school year must be included in the ASB group‘s budget.

b. To assist ASB Student Councils and activity groups in their planning the next year‘s revenues, expenses and transfers they are encouraged to develop their own budget template or use the BSD ASB Budget by Event Template (Excel spreadsheet, not included within this manual but included on the District‘s web page).

c. Each ASB group must approve their budget and this approval needs to be evidenced in the

minutes of the meetings of the ASB group.

2. During the budget planning phase, an ASB may choose to adopt a budget that is the same size as the prior year, expand its budget, or reduce its budget capacity.

a. Additional spending capacity will only be approved if an ASB has planned sufficiently to earn enough revenue to cover planned expenditures.

b. A decrease in spending capacity should accompany a decrease in expected revenue and should not result in an excessive ending fund balance unless the group is saving up for a large future expenditure.

Back to top of section

Consolidated Budget

3. The process for completing and submitting the annual, school-wide, consolidated ASB budget is as follows:

BSD ASB Manual

Budgeting

Effective Date: 9/1/2011

- 36 -

a. Annually, ASB activity groups submit their self-approved and finalized budgets to the ASB

Student Council in electronic format for ASB Student Council approval and consolidation into the school-wide ASB budget.

b. ASB Student Councils and advisors have the authority to determine, based on risk and materiality, the appropriate level of budget detail required for each activity group‘s annual budget on a case-by-case, year-by-year basis. The level of detail required for each activity group‘s budget needs to be communicated to the group in advance of the annual budget preparation process.

c. ASB Student Councils should notify ASB activity groups if and when their budgets have

been accepted by the ASB Student Council. Additionally, the Student Council should notify activity groups once the District has approved the school‘s consolidated budget at the end of the annual budget preparation process.

d. ASB groups should not plan activities or spend ASB moneys until they are notified of

budget approval.

4. Annually, the ASB Student Council shall submit the consolidated ASB budget, including both school-wide ASB budget items and ASB activity group budget items, to the Board of Directors for approval.

a. ASB Student Councils are to present their consolidated school-wide ASB Fund budgets to their school accountant in the district approved format employed currently by Advisors and accountants. The school accountant will submit the budget to the District‘s Budgeting Department. The Budgeting Department will submit the budgets to the Board.

b. This consolidated budget shall be submitted to the Board of Directors in late spring, before the end of the school year in a timely manner to allow for the Board's examination prior to formal approval in August.

5. The District business office will prepare budgets for the elementary schools.

Back to top of section

Ending Fund Balances / Spending Capacity Extreme care shall be given while planning activities and the annual budget to ensure a positive fund balance will exist at year end and that an ASB group does not exceed their budgeted and approved spending capacity. Neither an ASB nor an ASB activity group may have a negative fund balance at the end of the school year or spend more than they were authorized for the year. An ASB activity group must notify their Student council, and an ASB Student Council must notify the District‘s Budget Department immediately if there is any likelihood that a negative ending fund balance will exist and/or if overall expenditures will exceed approved spending capacity.

1. In the case of an imminent negative ending fund balance, a student council is permitted to borrow budget capacity from another school in the district which expects to have a positive ending ASB Fund balance or from one of their activity groups that expects to have a positive ending fund balance but to the extent that the lending school ASB or ASB activity group is able to maintain a positive ending balance at the end of the year.

BSD ASB Manual

Budgeting

Effective Date: 9/1/2011

- 37 -

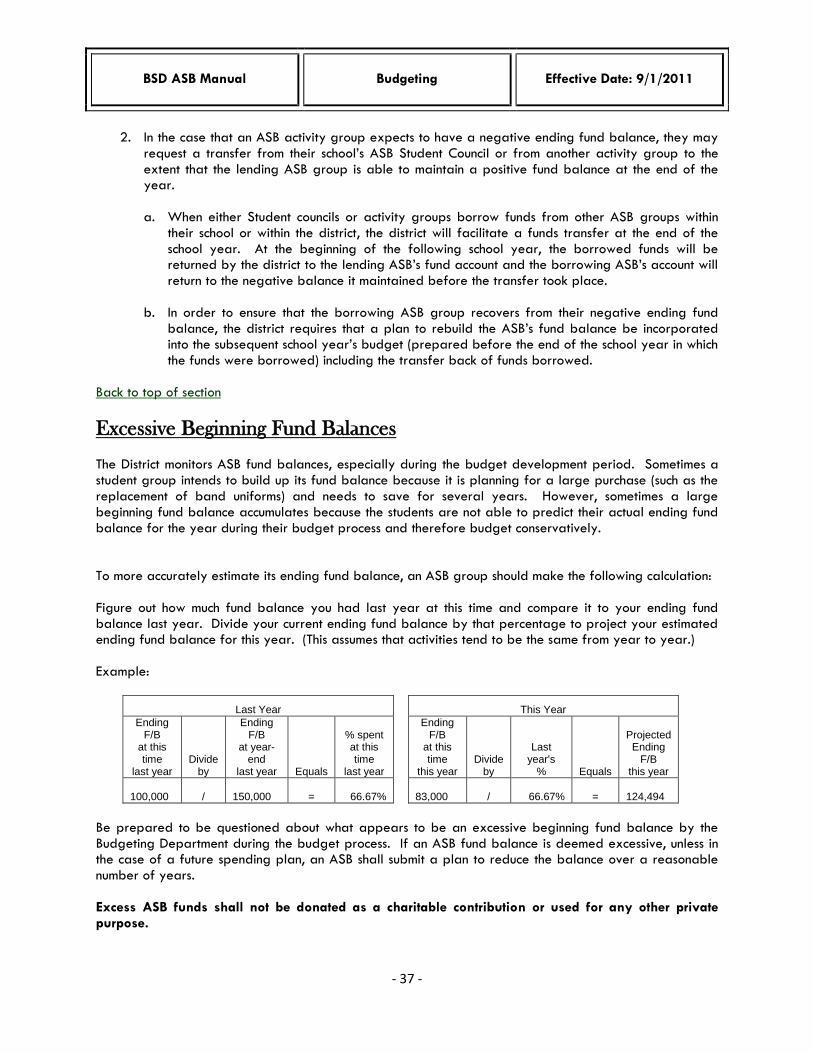

2. In the case that an ASB activity group expects to have a negative ending fund balance, they may request a transfer from their school‘s ASB Student Council or from another activity group to the extent that the lending ASB group is able to maintain a positive fund balance at the end of the year.

a. When either Student councils or activity groups borrow funds from other ASB groups within

their school or within the district, the district will facilitate a funds transfer at the end of the school year. At the beginning of the following school year, the borrowed funds will be returned by the district to the lending ASB‘s fund account and the borrowing ASB‘s account will return to the negative balance it maintained before the transfer took place.

b. In order to ensure that the borrowing ASB group recovers from their negative ending fund

balance, the district requires that a plan to rebuild the ASB‘s fund balance be incorporated into the subsequent school year‘s budget (prepared before the end of the school year in which the funds were borrowed) including the transfer back of funds borrowed.

Back to top of section