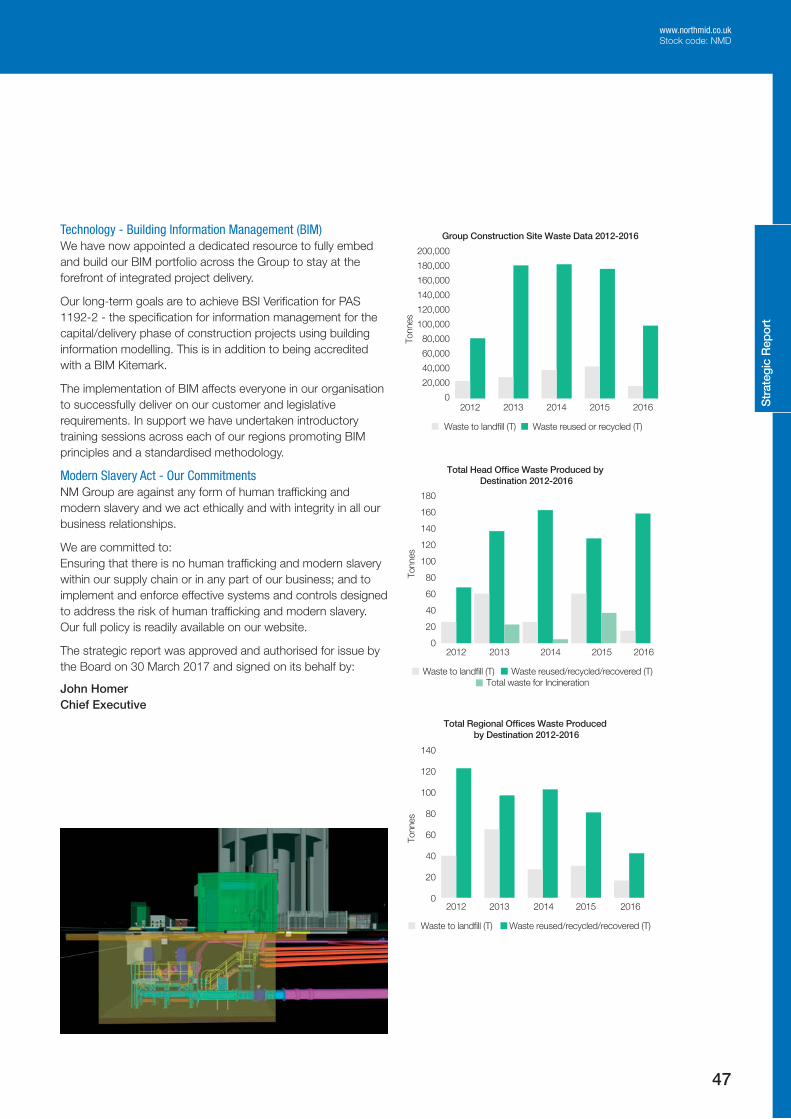

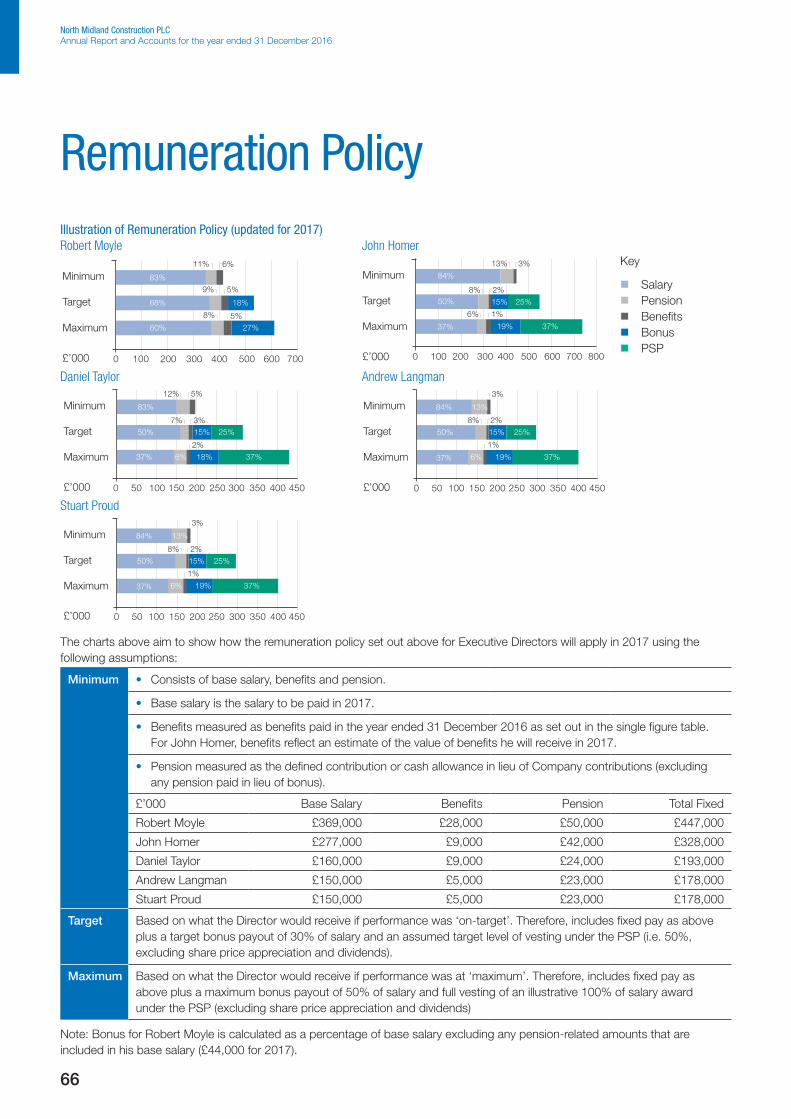

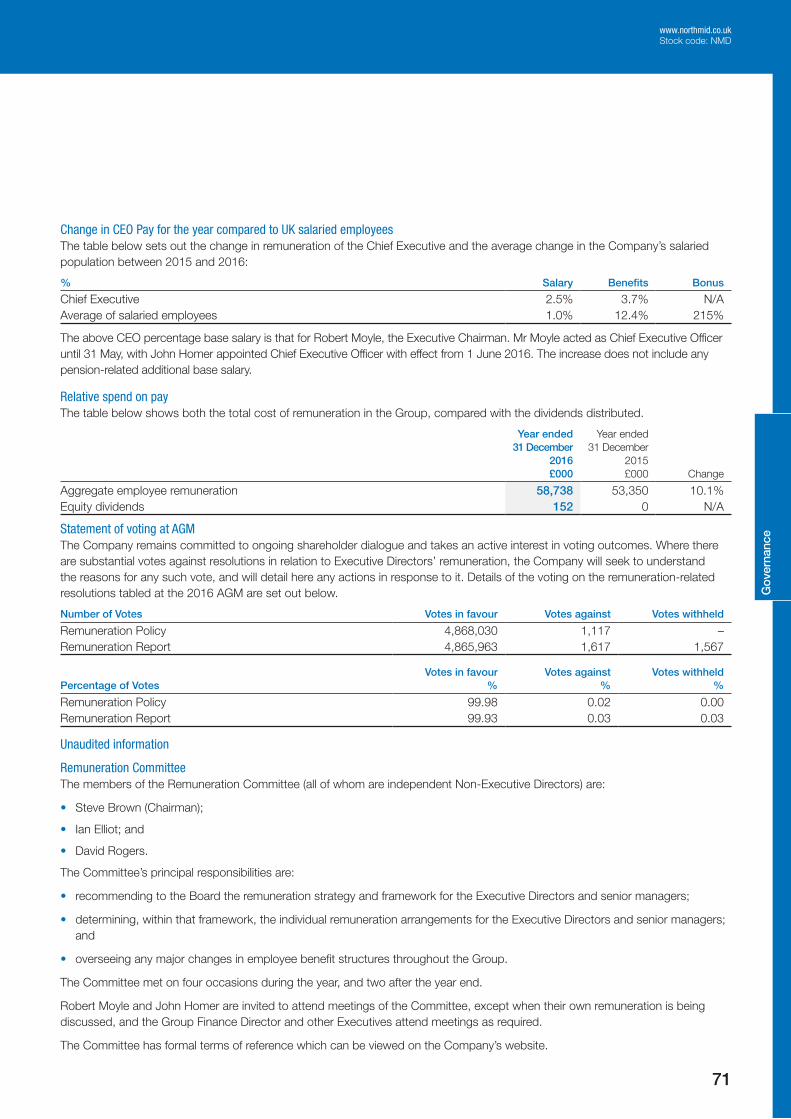

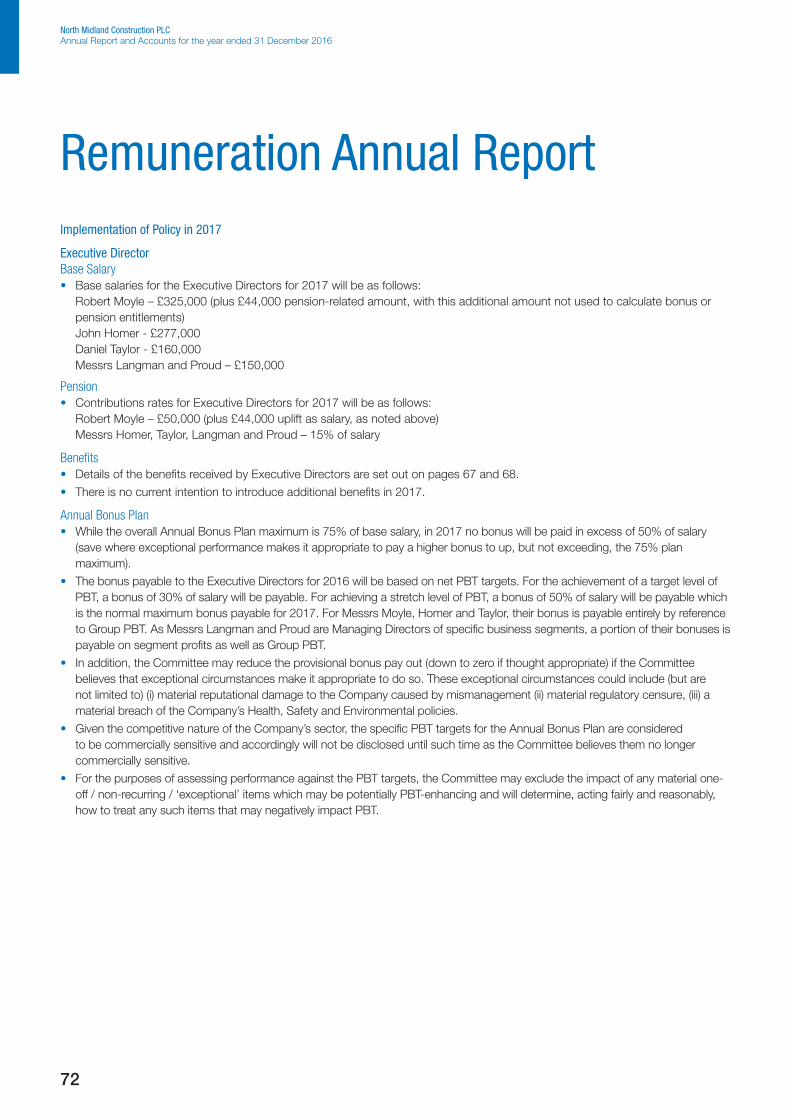

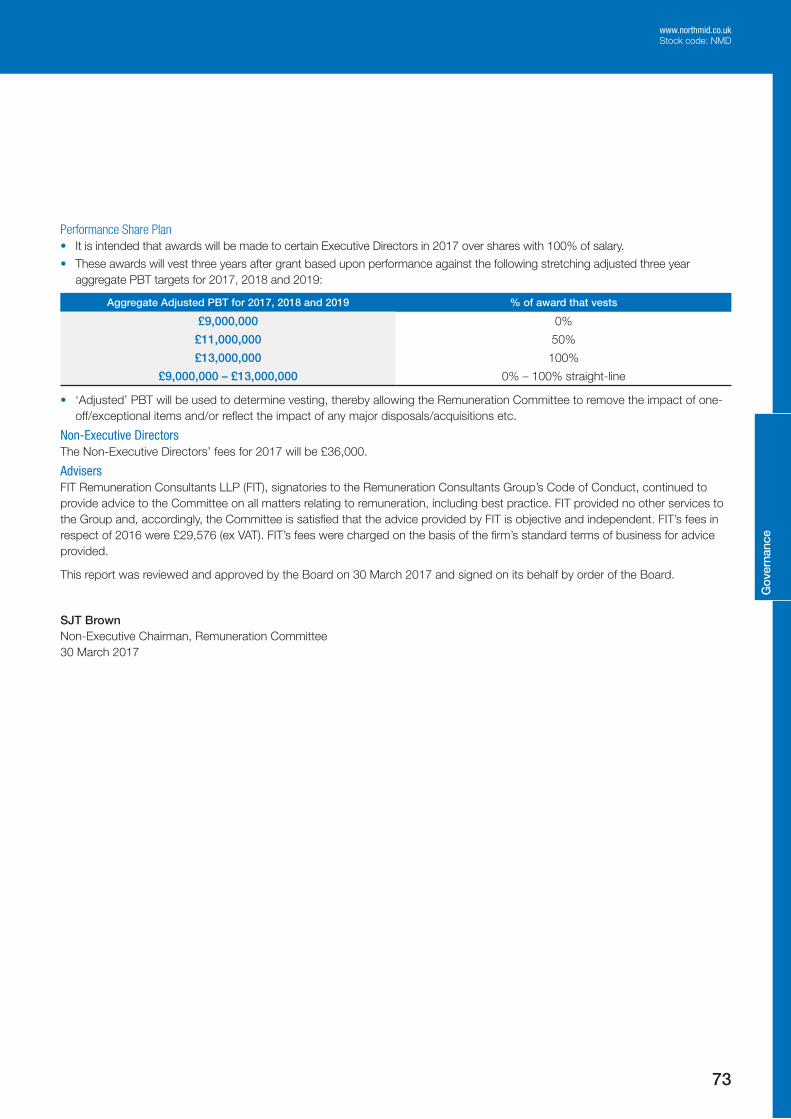

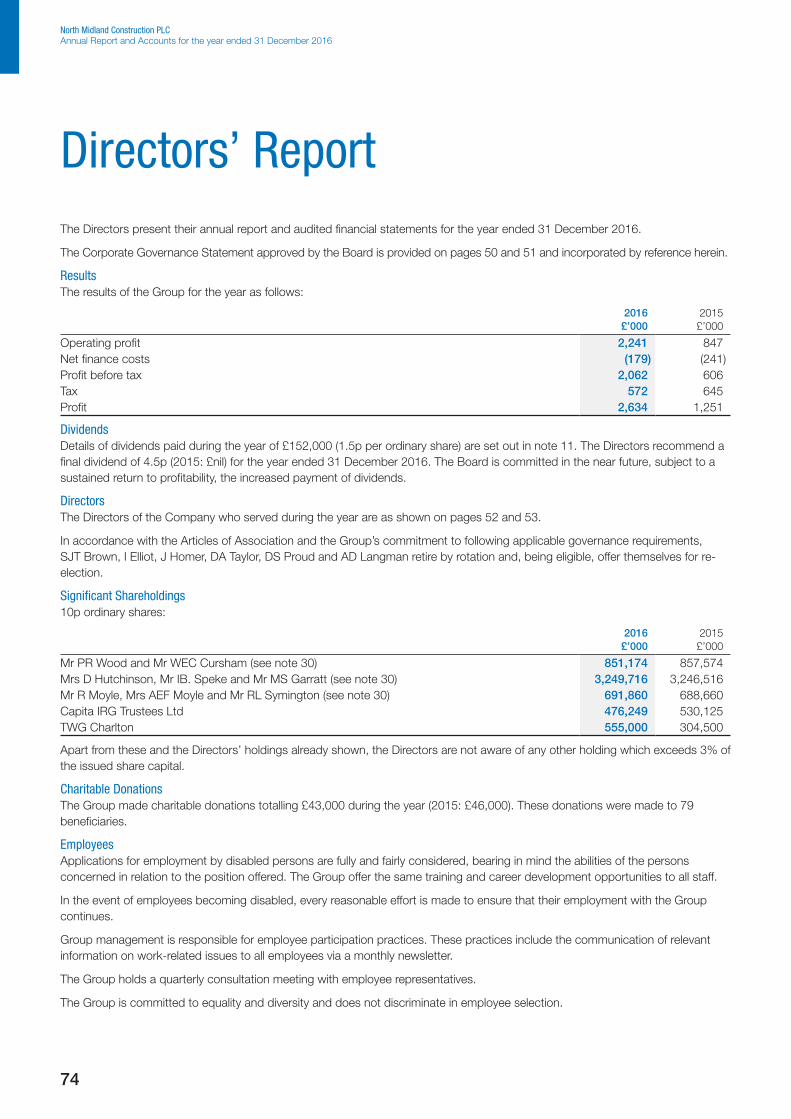

people inspire excellence - s3.eu-west-2.amazonaws.com

TRANSCRIPT

25203.04 7 April 2017 4:53 PM proof 14 25203.04 7 April 2017 4:53 PM proof 14

Annual Report and Accountsfor the year ended 31 December 2016

www.northmid.co.ukStock code: NMD

NORTH MIDLAND CONSTRUCTION PLC

No

rth Mid

land C

onstructio

n PLC

Annual R

eport and Accounts for the year ended 31 D

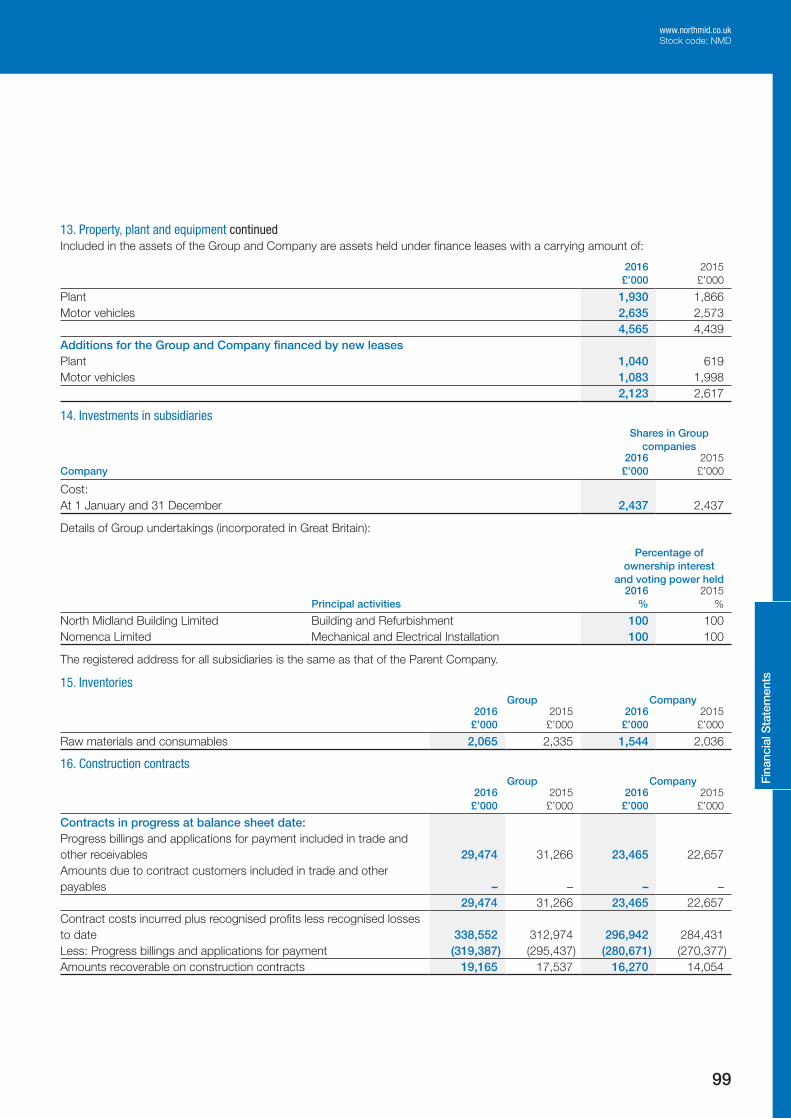

ecember 2016

People Inspire Excellence

CONSTRUCTION POW

ER

WAT

ER

TELECOM

MUNICATIONS

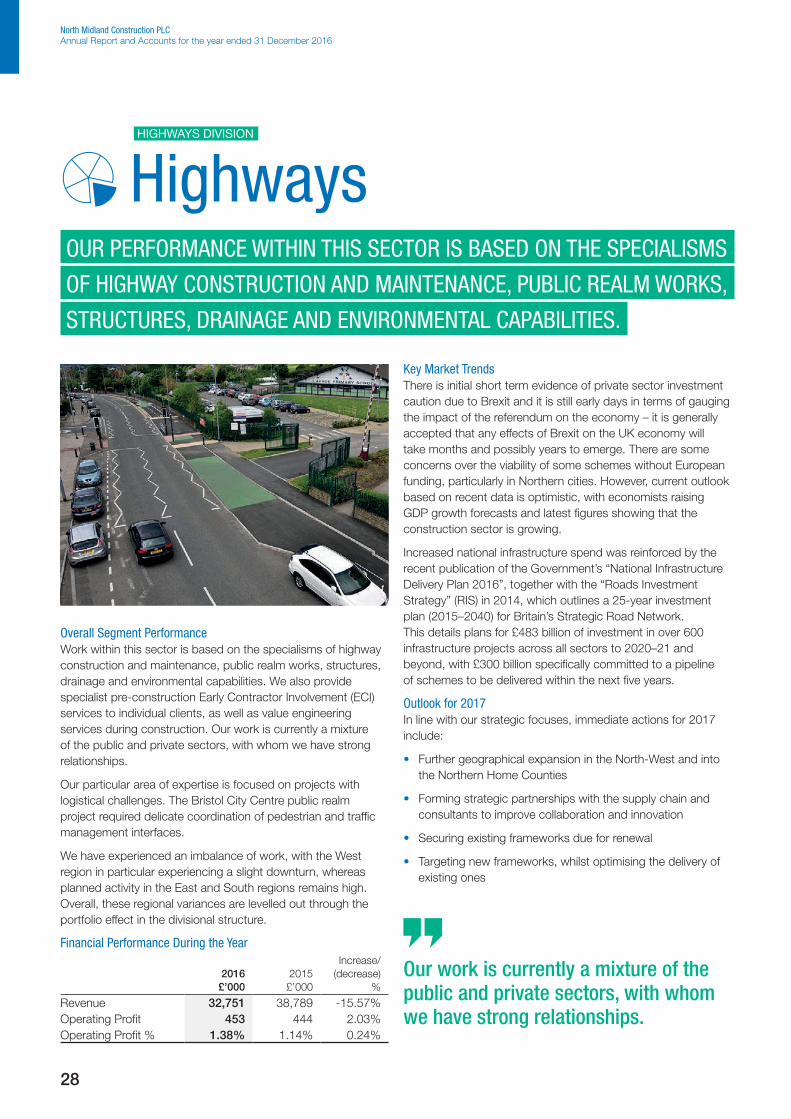

HIGHWAYS

25203.04 7 April 2017 4:53 PM proof 14

Welcome to our 2016 Annual Report NORTH MIDLAND CONSTRUCTION PLC (NM GROUP) OPERATES

NATIONALLY WITH 11 REGIONAL OFFICES AND WORKSHOPS

ENABLING US TO PROVIDE A LOCAL SERVICE TO OUR CUSTOMERS

PROMOTING SUSTAINABLE WORKING RELATIONSHIPS.

www.northmid.co.uk Stock code: NMD

Corporate WebsiteOur website has a wealth of additional information and case studies showcasing our expertise. Please head over to www.northmid.co.uk and take a look.

We provide a complete service offering to the construction industry from conception to optimisation, delivering best value and innovation. Our six operational divisions provide focused services to customers across our five chosen core market sectors of: Construction, Power, Highways, Telecommunications and Water; providing engineering, construction management and frontline delivery services.

We operate within our values of: People, Inspire, Excellence, which remain key to our strategic aims and objectives for growth. We are immensely proud of our family ethos which we are committed to maintaining throughout our business.

OVEVIEWFinancial and Operational Highlights 01

Our Group Direction 02

STRATEGIC REPORTChairman’s Statement 06Q&A with the Chief Executive 08Our Business Model 10

Our Strategy 12Our Key Performance Indicators 14Keeping People Safe 16Our Strategy in Action

– Prevent Losses 18– Develop Our People 20– Effective Communication 22

Our Operational and Financial Review 23– Construction 26– Power 27– Highways 28– Telecommunications 29– Water 30

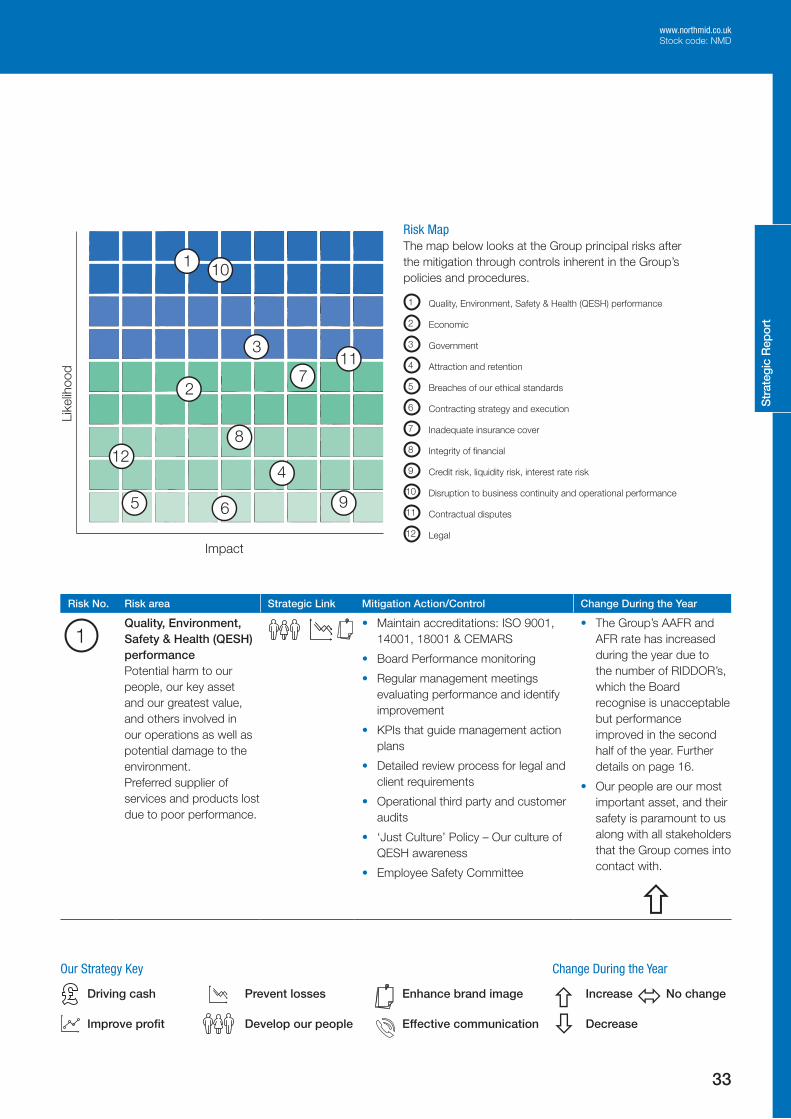

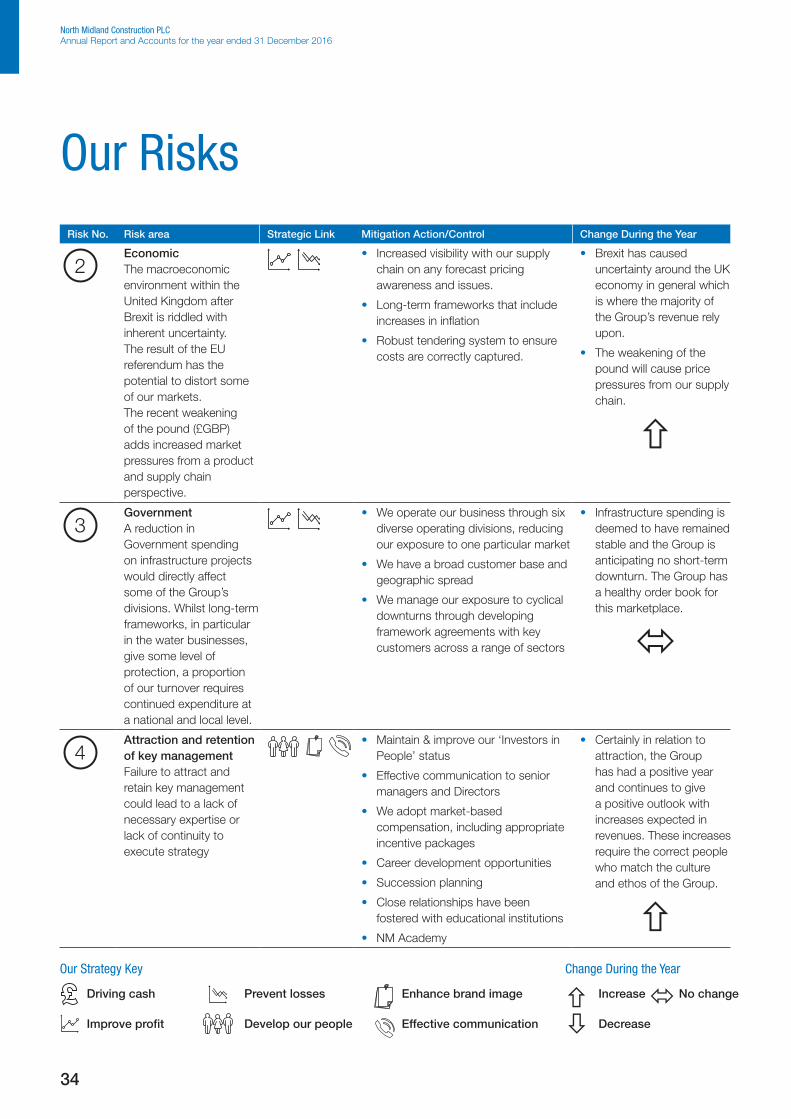

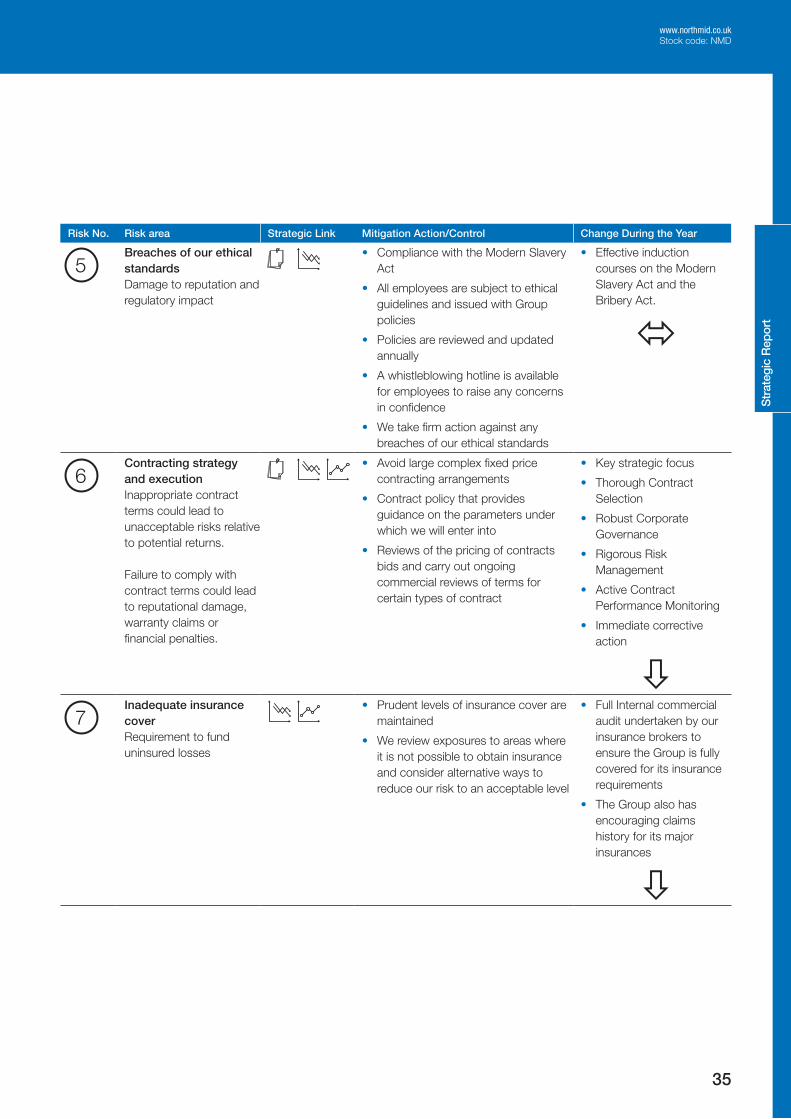

Our Risks 32Our Corporate Social Responsibility 38

GOVERNANCE

Corporate Governance 50Board of Directors 52Audit Committee Report 54Remuneration Report 57Remuneration Introduction and Policy 58Remuneration Annual Report 67Directors’ Report 74

FINANCIAL STATEMENTS

Independent Auditor’s Report 80Group Statement of Comprehensive Income 85Statements of Changes in Equity 86Balance Sheets 87Statements of Cash Flows 88Notes to the Financial Statements 89

SHAREHOLDER INFORMATION

Notice of Meeting 108Financial Calender 110Company Information IBC

Contents

25203.04 7 April 2017 4:53 PM proof 14

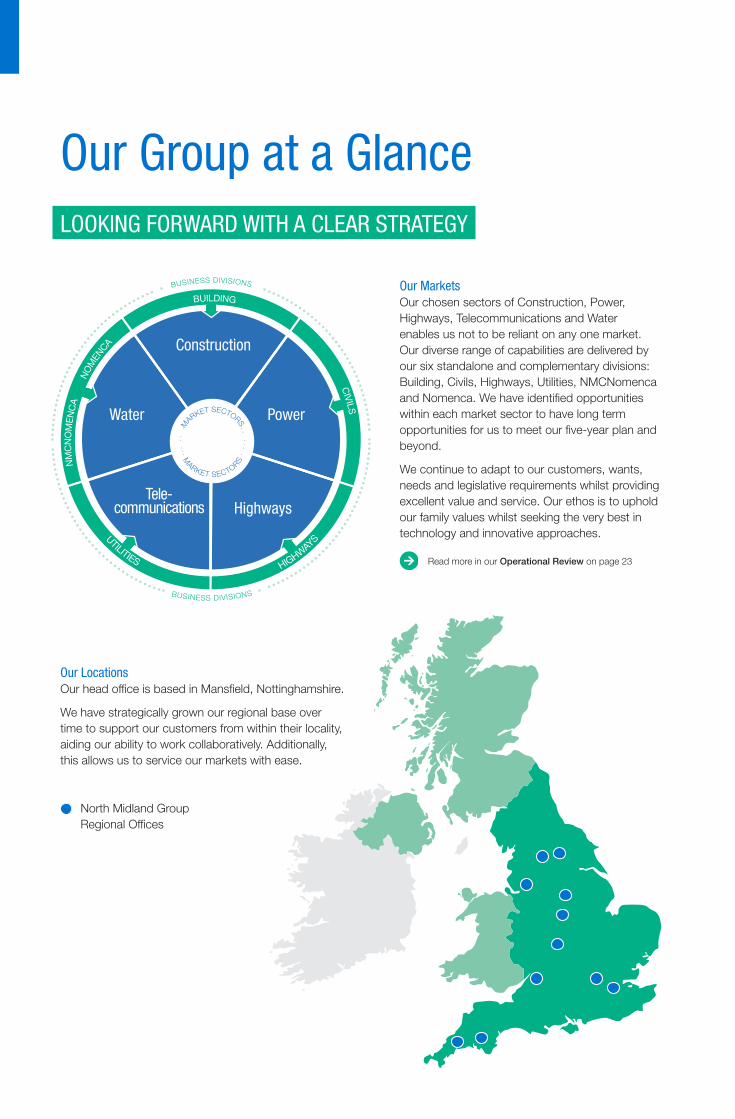

Our Group at a Glance

North Midland Group Regional Offices

Our LocationsOur head office is based in Mansfield, Nottinghamshire.

We have strategically grown our regional base over time to support our customers from within their locality, aiding our ability to work collaboratively. Additionally, this allows us to service our markets with ease.

Our MarketsOur chosen sectors of Construction, Power, Highways, Telecommunications and Water enables us not to be reliant on any one market. Our diverse range of capabilities are delivered by our six standalone and complementary divisions: Building, Civils, Highways, Utilities, NMCNomenca and Nomenca. We have identified opportunities within each market sector to have long term opportunities for us to meet our five-year plan and beyond.

We continue to adapt to our customers, wants, needs and legislative requirements whilst providing excellent value and service. Our ethos is to uphold our family values whilst seeking the very best in technology and innovative approaches.

Read more in our Operational Review on page 23

BUILDING CIVILS

N

MC

NO

ME

NC

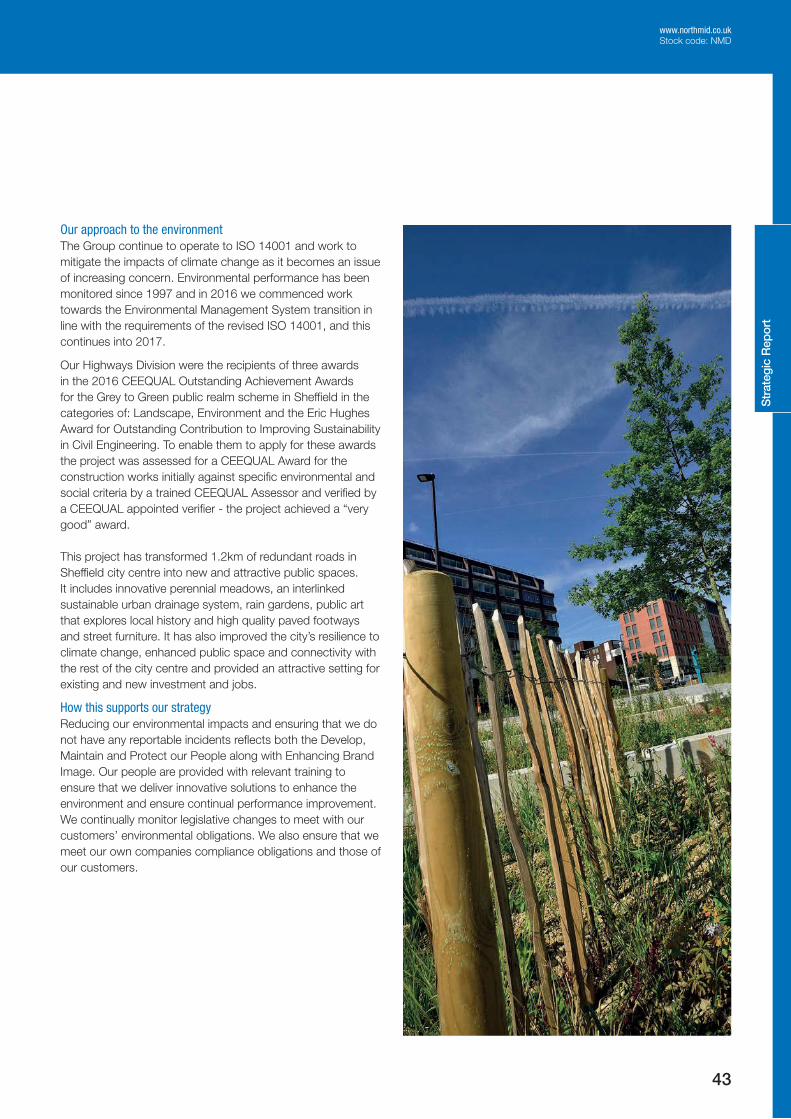

A

NO

MEN

CA

UTILITIES

HIGHWAY

S

Construction

PowerWater

HighwaysTele-

communications

M

ARKET SECTORS

MARKET SECTORS

BUSINESS DIVISIONS

BUSINESS DIVISIONS

LOOKING FORWARD WITH A CLEAR STRATEGY

25203.04 7 April 2017 4:53 PM proof 14 25203.04 7 April 2017 4:53 PM proof 14

Our Sectors

Read more in our Operational Review on page 30 and 31

Our market offering comprises of new build and refurbishment projects for the private and public sectors predominantly across the Midlands region. Construction projects vary from complex multi-storey city centre developments to specialist refurbishment schemes working within challenging live environments.

What we do• New build and

refurbishment• Social housing

• Student accommodation• Health and primary

care centres

Construction

We work within the power generation, power distribution, waste to energy and infrastructure works for both public and private sectors. Projects we deliver are both on a “design and build”, and “build only” basis.

What we do• Energy from waste plants• Infrastructure works• Distribution Network

Operator (DNO) substations

• Gas Insulated Substations (GIS)

• Air Insulated Substations (AIS)

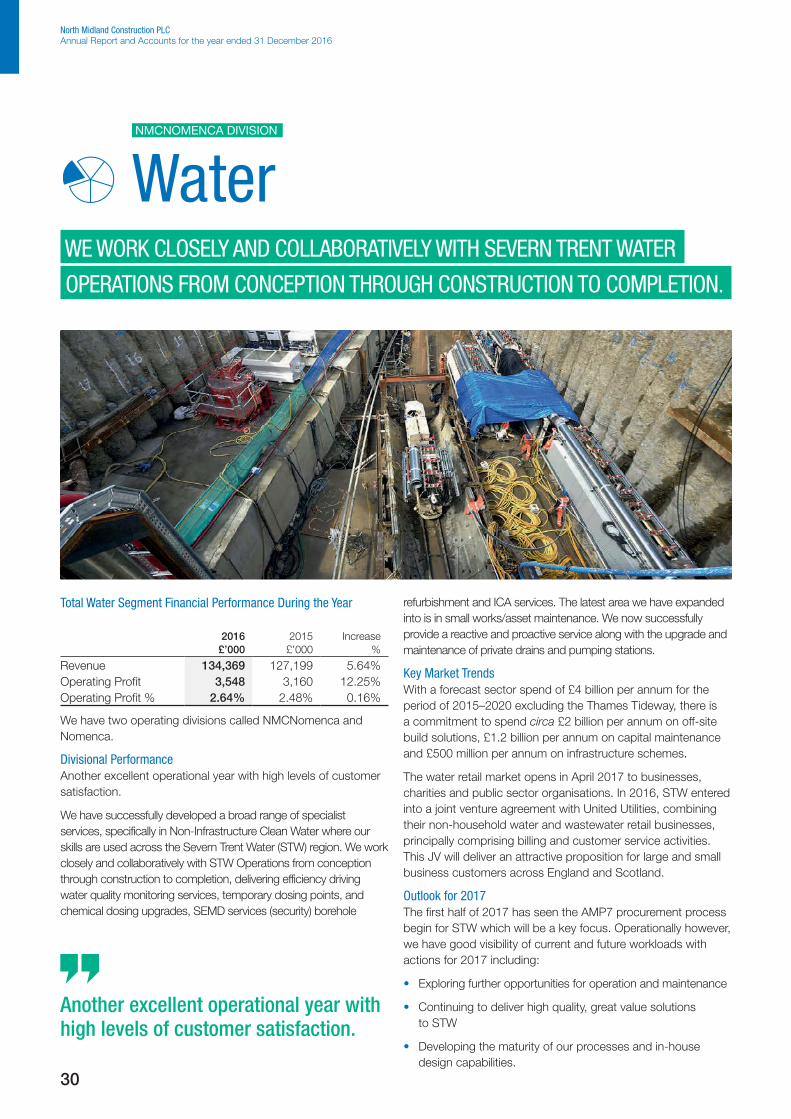

Our capabilities within this market is vast, serving almost all of the water utilities across the country. We have the ability to deliver infrastructure and non-infrastructure projects, operation, service and maintenance.

What we do• Design services including

3D modelling and visualisation

• Civil and specialist MEICA

• Programme management, feasibility, optioneering

• Product portfolio• Service and maintenance

Water

Within the telecommunications market we provide the management and delivery of national and regional network infrastructure to major communications providers, including network maintenance for high-speed fibre. This has included providing installations, improvements, repairs and 24 hour emergency response services.

With unique insight into multiple stakeholders’ involvement and statutory requirements, we apply this at each stage of the project life cycle to ensure smooth delivery for our clients.

What we do• Feasibility studies and site

surveys• Full network planning and

design

• Special engineering difficulties

• Planning and construction phasing strategies

Telecommunications

We deliver design and construction of large-scale complex projects spanning major highway construction on the trunk and minor road network to high specification public realm works for some of the UK’s largest cities.

Our extensive knowledge and understanding of complex challenges include traffic management that maintains peak traffic flows to stakeholder consultation that builds positive relations with local communities to delivery of challenging sustainability requirements.

What we do• New construction and

improvement works on major highways schemes

• Design and build of public realm schemes

• Creating and enhancing natural open spaces for public use

BUILDING DIVISION

PowerCIVILS DIVISION

HighwaysHIGHWAYS DIVISION

NMCNOMENCA AND NOMENCA DIVISIONS

UTILITIES DIVISION

Our ethos is to uphold our family values whilst seeking the very best in technology and innovative approaches.

Read more in our Operational Review on page 26

Read more in our Operational Review on page 28

Read more in our Operational Review on page 27

Read more in our Operational Review on page 29

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

25203.04 5 April 2017 3:16 PM proof 14

2016 HighlightsFinancial Highlights

Revenue growth£250.49m +15.11%

2016 £250.49

2015 £217.61m

2014 £193.18m

2013 £177.56m

2012 £168.92m

Cash £11.41m +72.36%

2016 £11.41m

2015 £6.62m

2014 £5.28m

2013 £4.88m

2012 £5.10m

Operating profit/(loss)£2.24m +163.53%

2016 £2.24m

2015

£(2.86)m2014

£(5.85)m2013

£0.78m

£0.85m

2012

Net cash**

£7.43m +210.88%

2016 £7.43m

2015 £2.39m

2014 £1.68m

2013 £3.43m

2012 £3.26m

Underlying profit*£5.91m +32.81%

2016 £5.91m

2015 £4.45m

2014 £4.35m

2013 £3.75m

Secured workload 2017£225m +24.31%

2016 £225m

2015 £181m

2014 £155m

2013 £150m

2012 £130m

Operational Highlights

Cash Balance

Corporate Governance and Risk Management

Improvement in Operational Performance

Our People

• We are pleased to report an increase in profitability by 163.53% and a 15.11% increase in revenue across the Group for 2016.

• Underlying profit continues to improve along with turnover and our strategic priority of improving profitability.

• We have retained our Gold accreditation to Investors in People against the new sixth generation standard. More can be read about this on page 38.

• 2016 has seen a record year of new people joining us, which is particularly encouraging in a competitive market.

• Our cash balance has increased by 72.36% between 2015 and 2016 which we are encouraged by. Cash is a key element to our strategy and informs our actions within the business. Our strategy in detail can be found on page 12.

• In order to address historical issues and to improve our financial performance we revised our strategy on contract and market selection. This has been coupled with pre-pricing assessment procedures, project monitoring and peer reviews. Our full strategy can be read on page 12.

* Underlying profit is profit before tax, excluding legacy contract losses of £3.85million (2015: £3.84million). Legacy contracts are construction contracts entered into at the height of the recession, before 31 December 2013, and which carried a high commercial and contracted risk. These contracts have negatively impacted the Group’s income statement in 2013 and subsequent years.

**Net cash is cash at the bank at year end less any obligations under finance leases.

01

www.northmid.co.uk Stock code: NMD

Ove

rvie

w

North Midland Construction AR2016 front proof 14.indd 1 05/04/2017 15:18:35

25203.04 5 April 2017 3:16 PM proof 14

Our Group Direction

Our Values

• Be a name not a number

• Be the best

• One team, one goal

Our family values are and always have been at the core of our business. We recognise that it is our people who are better together and inspire each other and the wider community, so that we can aspire to deliver excellence in everything we do.

• We inspire each other and the wider community

• We care

• We deliver innovation

We offer a range of placements, internships, work experience schemes and positions for graduates and apprenticeships because we believe that by inspiring each other and the community around us, we can continue to deliver excellence in everything we do. Inspiring the wider community is very important to us as we continue to educate and inspire people to enter the construction industry and offer them career paths within our growing business.

People Inspire

OUR VISION IS TO BE THE BEST PERFORMING COMPANY IN OUR

CHOSEN MARKETS BY DELIVERING EXCEPTIONAL

CUSTOMER SERVICE.

Our Vision

Our Business ModelUsing our key resources: People, systems, assets, materials

To perform key activities: Construction, installation, design

Across five segments: Construction, Power, Highways, Telecommunications and Water

Delivering value for stakeholders: Our Company, our customers, our Shareholders, our people and our communities

Read more in Our Corporate Social Responsibility on page 38

Read more about our Business Model on page 10

02

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 2 05/04/2017 15:18:36

25203.04 5 April 2017 3:16 PM proof 14

• To be the top performer

• Continuous improvement

• Exceptional customer service

We strive to provide excellence in the quality of all our work. We aim to always meet and exceed their expectations. This is achieved through our adoption of the latest quality standards, ISO 9001, 14001, 18001 and 27001. We believe that with excellent people and an excellent ethos, we can deliver an excellent service to all of our clients. Delivering excellent results through our people and growing talent from within continues to be our strategy.

Excellence

THE GROUP WILL BE A GREAT PLACE TO WORK, SO THAT OUR

PEOPLE PERFORM TO THE PEAK OF THEIR CAPABILITIES,

WHILST ENJOYING IT.

Our Mission

We are committed to sustained organic growth by delivering, in partnership with our customers, a quality product at an economic price, constructed to premium environmental standards, in accordance with the best health and safety practice.

Our Strategy

Driving cash

Improve profit

Prevent losses

Develop our people

Enhance brand image

Effective communication

Read more about our Strategy on page 12

Read more in our Chairman’s Statement on page 07

03

www.northmid.co.uk Stock code: NMD

Ove

rvie

w

North Midland Construction AR2016 front proof 14.indd 3 05/04/2017 15:18:37

25203.04 5 April 2017 3:16 PM proof 14North Midland Construction AR2016 front proof 14.indd 4 05/04/2017 15:18:37

25203.04 5 April 2017 3:16 PM proof 14

STRATEGIC REPORTChairman’s Statement 06

Q&A with the Chief Executive 08

Our Business Model 10

Our Strategy 12

Our Key Performance Indicators 14

Keeping People Safe 16

Our Strategy in Action

Prevent Losses 18

Develop our People 20

Effective Communication 22

Our Operational and Financial Review 23

Construction 26

Power 27

Highways 28

Telecommunications 29

Water 30

Our Risks 32

Our Corporate Social Responsibility 38

Str

ateg

ic R

epor

t

North Midland Construction AR2016 front proof 14.indd 5 05/04/2017 15:18:38

25203.04 5 April 2017 3:16 PM proof 14

Chairman’s Statement

My new role of Executive Chairman will permit me to spend more time with the Group’s customers, both existing and potentially new, to seek further opportunities to promote the Group.

GOOD GOVERNANCE IS ESSENTIAL FOR THE EFFECTIVE MANAGEMENT

OF THE GROUP AND THE PROTECTION OF SHAREHOLDER INTERESTS.

Robert Moyle Chairman

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

06

North Midland Construction AR2016 front proof 14.indd 6 05/04/2017 15:18:38

25203.04 5 April 2017 3:16 PM proof 14

Overview of 2016The improved profitability reported at the half-year has been maintained in spite of losses incurred in the Utilities division and on the ongoing resolution of the one outstanding legacy contract, as defined on page 25 of these Accounts.

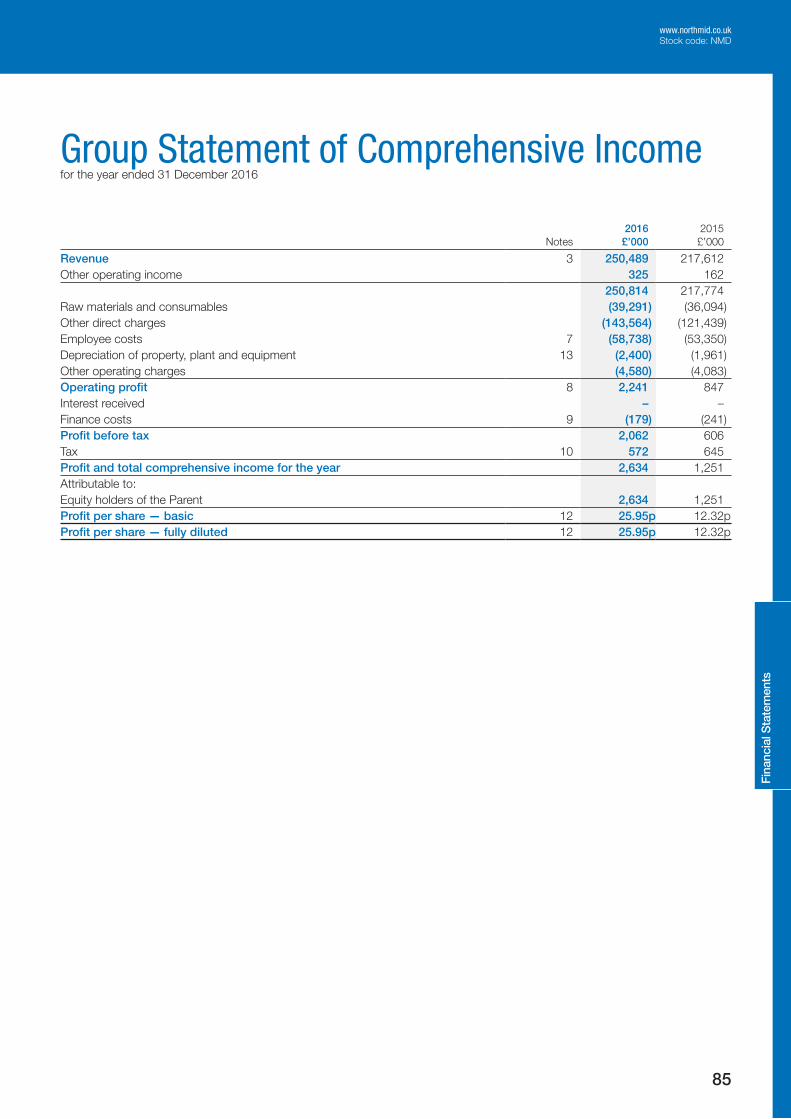

Group revenue increased by 15.11% to £250.49 million (2015: £217.61 million), with operating profit increasing by 163.53% to £2.24 million (2015: £0.85 million). Excluding the impact of the legacy contract normal trading profitability improved by 32.81% to £5.91 million (2015: £4.45 million). Earnings per share improved by 113.8% to 25.95p (2015: 12.32p).

The Board is proposing an enhanced dividend of 3.0p per share, increasing the full year dividend to 4.5p (2015: Nil).

CashCash generation has improved and the net cash position at the year end was £7.43 million (2015: £2.39 million). The Group credit facilities continue to remain adequate for the foreseeable future.

Our Values and Our PeoplePeople, Inspire, Excellence are the three key values that drive the Group’s culture. The attraction and retention of high quality staff to facilitate both the growth of the Group and the high levels of customer service that key clients demand is of paramount importance. Investment in our people is at the top

of the Group’s agenda and the retention of the Investors in People Gold accreditation during the year is a significant achievement. It is of paramount importance to provide a healthy and safe environment for both our employees and our supply chain. The Group has been the recipient of several awards and these are testament to the constantly improving culture that is embedded within the Group. The Group “Accident Frequency Rate” of 0.11 is significantly lower than the industry average, albeit not at the level that is satisfactory to the Board.

Corporate GovernanceGood governance is essential for the effective management of the Group and the protection of Shareholder interests. The Board is committed to ensuring that robust governance is applied throughout the Group and that its procedures and controls are reviewed on a regular basis.

Appointment of John HomerAs previously announced, John Homer was appointed as Chief Executive in June 2016 and has settled into the role well. He has wide experience of the industry and is driving enhanced performance both operationally and financially, whilst maintaining the existing strong core values of the Group.

My New Role in the BusinessThe appointment of John Homer has facilitated the division of my previously combined roles of Chairman and Chief Executive.

My new role of Executive Chairman will permit me to spend more time with the Group’s customers, both existing and potentially new, and to seek further opportunities to promote the Group.

The quality of our people and their leadership will fuel the growth of the Group and it is my intention to engage and interact more with the existing and potentially new employees now that operational control has been ceded to John Homer.

OutlookIncreased infrastructure spend and the upturn cycle of expenditure in the water companies AMP6 programme gives the Board confidence to forecast an increase in both profitability and revenue for this forthcoming financial year. The secured order book to date is £225 million (2016: £181 million) and this represents a significant proportion of the 2017 budget.

Robert Moyle Chairman 30 March 2017

Revenue

2015: £217.61m

£250.49m+15.11%

Operating profit

2015: £0.85m

£2.24m+163.53%

Read more about Governance on page 50

Str

ateg

ic R

epor

t

07

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 7 05/04/2017 15:18:39

25203.04 5 April 2017 3:16 PM proof 14

Chief Executive’s Q&A

WE REALLY DO LIVE OUR VALUES OF: PEOPLE, INSPIRE, EXCELLENCE. THEY

ARE A SOLID FOUNDATION FOR OUR BUSINESS BUT FROM THE SHORT TIME

I’VE BEEN HERE, THEY ARE GENUINELY EVIDENT IN OUR ACTIVITIES EVERY DAY.

John Homer Chief Executive

I have received an incredibly warm welcome from everyone in the Group. Our people are very positive with a practical, ‘can do’ approach to doing business.

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

08

North Midland Construction AR2016 front proof 14.indd 8 05/04/2017 15:18:39

25203.04 5 April 2017 3:16 PM proof 14

WE REALLY DO LIVE OUR VALUES OF: PEOPLE, INSPIRE, EXCELLENCE. THEY

ARE A SOLID FOUNDATION FOR OUR BUSINESS BUT FROM THE SHORT TIME

I’VE BEEN HERE, THEY ARE GENUINELY EVIDENT IN OUR ACTIVITIES EVERY DAY.

YOU HAVE BEEN AT THE HELM SINCE JULY, WHAT ARE

YOUR FIRST IMPRESSIONS?

I have received an incredibly warm welcome from everyone in the Group. Our people are very positive with a practical, ‘can do’ approach to doing business.

We have a stable and talented workforce from our directly employed tradespeople to Senior Managers and Directors. It’s a good blend of long serving employees and new people joining us.

I’ve had a great deal of support from Robert Moyle in splitting his role and moving to Executive Chairman.

I see a lot of great potential for a successful future, a very positive start to the role for me.

HOW HAVE YOU SEEN THE PREVAILING CULTURE IN THE GROUP?

We really do live our values of: People, Inspire, Excellence. They are a solid foundation for our business but from the short time I’ve been here, they are genuinely evident in our activities every day. I have managed to travel around the country to meet our people and visit our workshops, factories, offices and sites. There is a real customer-centric attitude to do the best for the customers that we serve.

Over the 70-year history of the business, a paternal feel of family-based values has continued to prevail. It is essential that we maintain this legacy as we continue to grow and bring in new people.

WHAT ARE THE BIGGEST CHALLENGES YOU SEE AHEAD?

The skills shortage is an issue that we must continue to tackle, along with attracting and retaining our people. This is coupled with digital requirements of our clients along with managing supplier contribution.

WHAT ARE THE KEY TRENDS THAT YOU ARE NOTICING

IN THE MARKETPLACE

All customers are seeking efficiency in the way that they procure work. The mantra “more for less” is prevalent across the complete public and private sectors. Our ability to consistently deliver to time, cost and quality standards is now merely the starting point. Other value adding benefits need to be offered in order to attract and retain the best customers.

The whole customer experience concept is coming more to the forefront in a way that has been seen in B2C sectors in the past. Customers are now requiring a blended offering of feasibility/design/install/operate/maintain. It is essential that we

look to collaborate with our supply chain to gain advantage from their specialist skills and knowledge and be at the front of the queue for their resources and the preferred partner for collaboration when pitching for new business.

HOW DO YOU INTEND TO TAKE ADVANTAGE OF THESE CHANGES?

We have established a customer experience panel and appointed a customer experience manager. They are looking holistically at our offering and enhancing the services that we offer, both at the front end in feasibility and design together with growing our activities in operation and maintenance of facilities.

We are also investing heavily in the potential that exists to gain benefit from digital technology and the way that we can benefit from the more efficient use of information technology.

Continuing our drive for prefabrication and modular construction techniques will require a manufacturing mindset to be applied to realise the full efficiency potential.

IF YOU LOOK FORWARD THREE YEARS WHAT WOULD YOU LIKE

TO SEE?

• An exciting place to work with motivated people delivering exceptional customer service.

• A recognised brand with a solid reputation for consistent delivery and flair for creating efficiency across the range of our operations to the benefit of all our stakeholders.

• Continue with our growth in direct employment delivery teams.

• The efficiency of our off-site fabrication / modular build to be progressed with more factory facilities in place.

• Made advancements to the point where we are truly working in a digital environment and using this information to drive tangible benefits.

• Above everything else we need to have some fun and truly enjoy what we do.

John Homer Chief Executive 30 March 2017

Str

ateg

ic R

epor

t

09

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 9 05/04/2017 15:18:40

25203.04 5 April 2017 3:16 PM proof 14

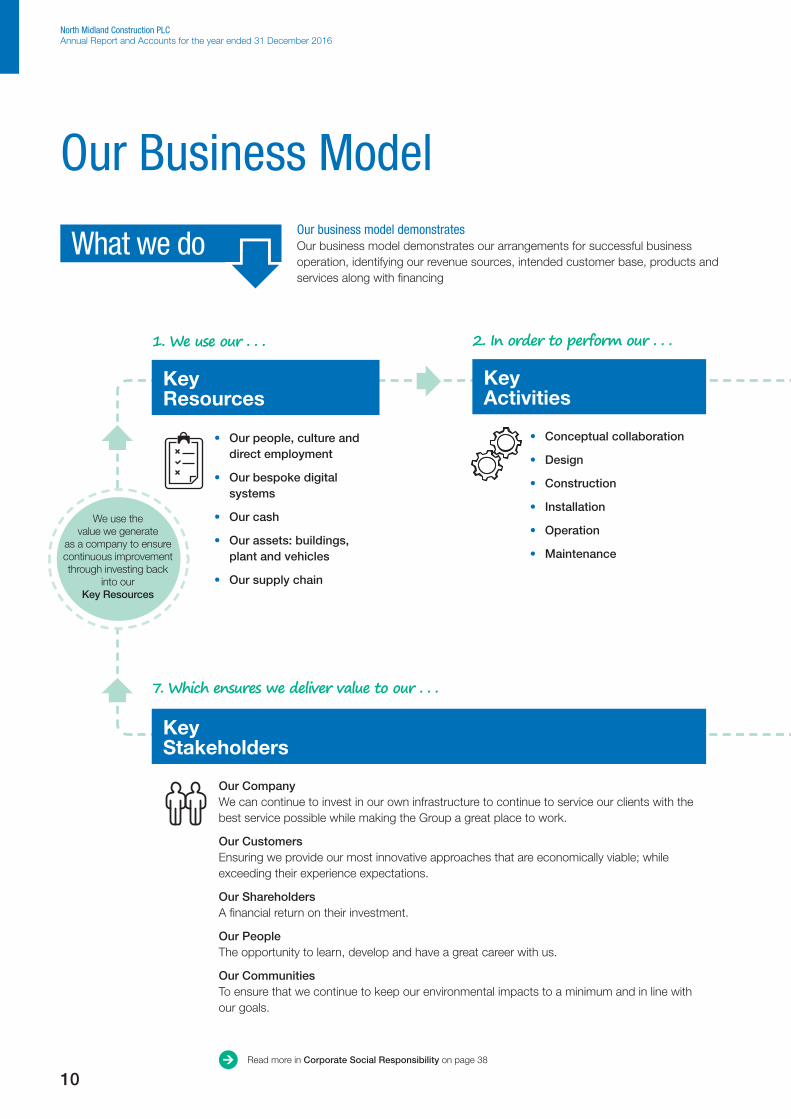

Our Business Model

What we do

• Our people, culture and direct employment

• Our bespoke digital systems

• Our cash

• Our assets: buildings, plant and vehicles

• Our supply chain

• Conceptual collaboration

• Design

• Construction

• Installation

• Operation

• Maintenance

Our CompanyWe can continue to invest in our own infrastructure to continue to service our clients with the best service possible while making the Group a great place to work.

Our CustomersEnsuring we provide our most innovative approaches that are economically viable; while exceeding their experience expectations.

Our ShareholdersA financial return on their investment.

Our PeopleThe opportunity to learn, develop and have a great career with us.

Our CommunitiesTo ensure that we continue to keep our environmental impacts to a minimum and in line with our goals.

1. We use our . . . 2. In order to perform our . . .

Key Resources

Key Activities

7. Which ensures we deliver value to our . . .

Key Stakeholders

Read more in Corporate Social Responsibility on page 38

We use the value we generate

as a company to ensure continuous improvement through investing back

into our Key Resources

Our business model demonstrates Our business model demonstrates our arrangements for successful business operation, identifying our revenue sources, intended customer base, products and services along with financing

10

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 10 05/04/2017 15:18:40

25203.04 5 April 2017 3:16 PM proof 14

Our revenue streams are a combination of recurring frameworks, standalone projects and service revenue.

• Frameworks: water sector, highways, telecommunications and power

• Repeat orders

• Standalone projects for existing and new customers within the construction sector

We seek to build collaborative, long term relationships with our customer base to provide added value across all stakeholders.

• Customer experience panel

• Customer satisfaction survey

• Social media

• Customers customer concepts

Fully integrated collaborative model with all stakeholders.

Stimulate Innovation through:

• Understanding our customers’ needs

• Working collaboratively to provide solutions

• Embracing IT enhancements

• Expertise in our markets, collaborating with all stakeholders

• Providing infrastructure in a variety of new markets

• Construction

• Power

• Highways

• Telecommunications

• Water sectors

3. Across key segments for our . . . 4. Which provides us with . . .

Our Revenue Streams

Value Proposition

Customer Relationships

6. Providing us with our . . . 5. Which enables us to build . . .

Customers who require our Services

Read more in Group at a Glance

Str

ateg

ic R

epor

t

11

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 11 05/04/2017 15:18:40

25203.04 5 April 2017 3:16 PM proof 14

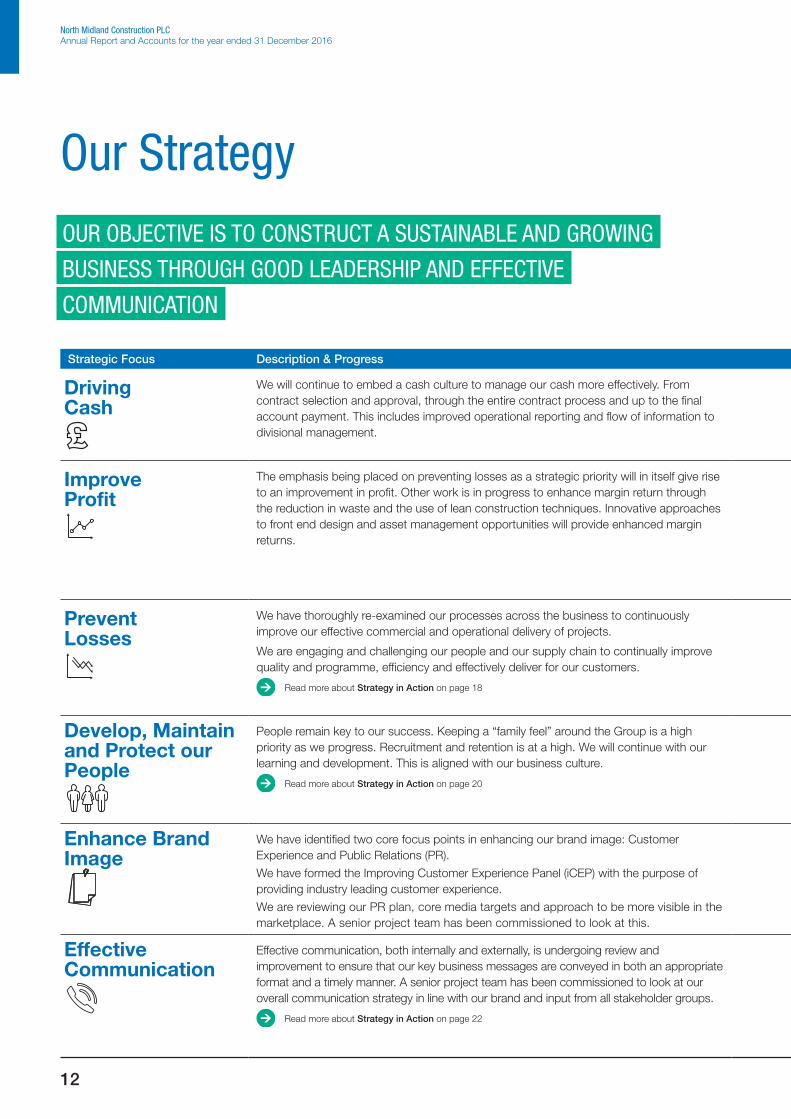

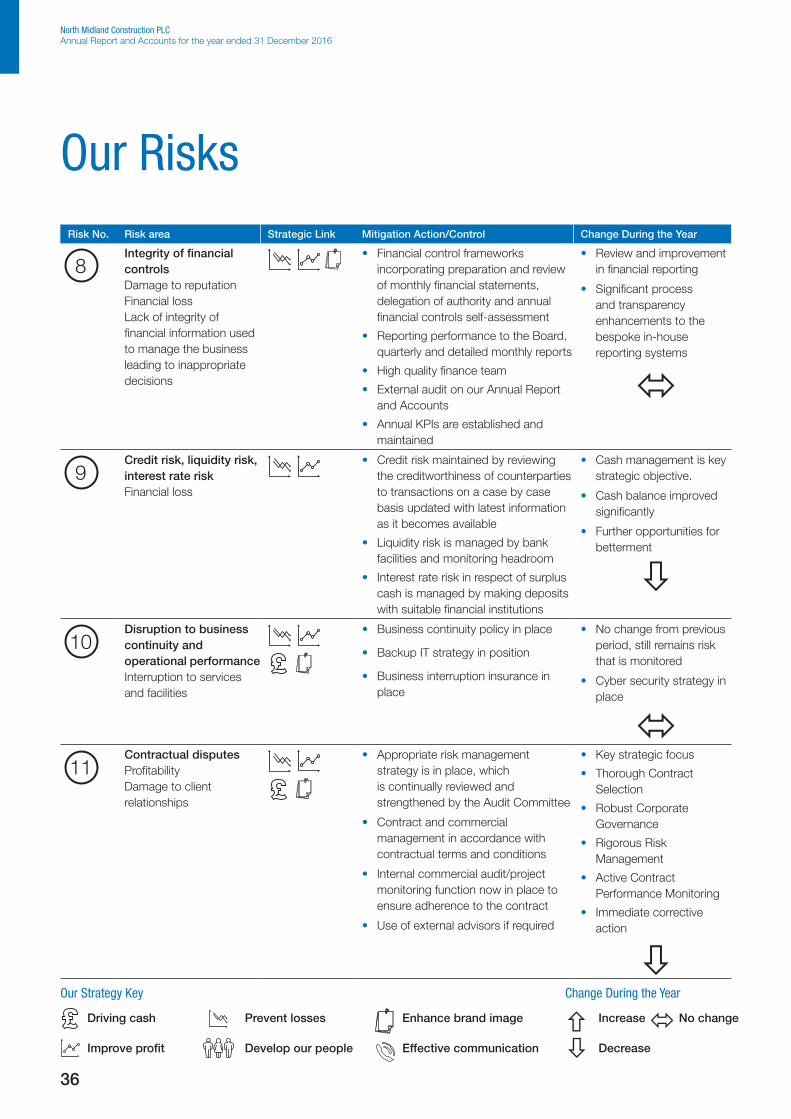

Our Strategy

Strategic Focus Description & Progress Priorities for 2017 Our measures (KPIs) Associated Risks

Driving Cash

We will continue to embed a cash culture to manage our cash more effectively. From contract selection and approval, through the entire contract process and up to the final account payment. This includes improved operational reporting and flow of information to divisional management.

• Daily cash bulletins• Weekly cash dashboards• Improve payment terms from

customers• Process efficiency execution to invoice

• WIP/Debtor days • Cash collection against forecast• Overdue balances• Overdue retentions

Credit risk, liquidity risk,interest rate risk, financial loss

Improve Profit

The emphasis being placed on preventing losses as a strategic priority will in itself give rise to an improvement in profit. Other work is in progress to enhance margin return through the reduction in waste and the use of lean construction techniques. Innovative approaches to front end design and asset management opportunities will provide enhanced margin returns.

• In-house design and build offering• Off-site manufacture • Service and maintenance • Finance and investment offering• Profit enhancement plans

embedded • Planning/programme reporting

enhancement

• Margin by contract• Risks and opportunities identified and

monitored• Procurement savings• Programme management

Contracting strategy and executionInappropriate contract terms could lead to unacceptable risks relative to potential returns.

Failure to comply could lead to reputational damage, warranty claims or financial penalties.

Prevent Losses

We have thoroughly re-examined our processes across the business to continuously improve our effective commercial and operational delivery of projects.

We are engaging and challenging our people and our supply chain to continually improve quality and programme, efficiency and effectively deliver for our customers.

Read more about Strategy in Action on page 18

• Thorough contract selection• Robust corporate governance• Rigorous risk management• Active contract performance

monitoring• Immediate corrective action

• Contract risk level review• Project monitoring assessments• Margin by contract• Risks and opportunities identified and

monitored

Integrity of financial controlsDamage to reputation.

Financial loss.

Lack of integrity of financial information used to manage the business leading to inappropriate decisions.

Develop, Maintain and Protect our People

People remain key to our success. Keeping a “family feel” around the Group is a high priority as we progress. Recruitment and retention is at a high. We will continue with our learning and development. This is aligned with our business culture.

Read more about Strategy in Action on page 20

• Develop a learning culture• Continuous performance appraisal• Promotion opportunities from within• Address underperformance• Learning is for everyone• Mentor and Buddy arrangements

• Employee stability index• Training across the Group• Employee engagement• Learning and development• Recruitment

Attraction and retention of key managementFailure to attract and retain key management could lead to a lack of necessary expertise or lack of continuity to execute strategy.

Enhance Brand Image

We have identified two core focus points in enhancing our brand image: Customer Experience and Public Relations (PR).

We have formed the Improving Customer Experience Panel (iCEP) with the purpose of providing industry leading customer experience.

We are reviewing our PR plan, core media targets and approach to be more visible in the marketplace. A senior project team has been commissioned to look at this.

• Customer Experience and iCEP• Reduce customer complaints• Effective PR campaign• Consistent high quality image

• Increase in PR article take up• Defined processes and proformas

developed for Customer Experience• Review branding

Potential damage to reputation and customer relationships.

Effective Communication

Effective communication, both internally and externally, is undergoing review and improvement to ensure that our key business messages are conveyed in both an appropriate format and a timely manner. A senior project team has been commissioned to look at our overall communication strategy in line with our brand and input from all stakeholder groups.

Read more about Strategy in Action on page 22

• Effective use of social media• Face-to-face meetings• Effective cascade of information• Prioritise key messages`

• Increase in social media interactivity • External newsletter• Review of internal communication: alerts,

newsletter, Blueprint etc.• Employee engagement surveys and

subsequent implementation of feedback• Senior management roadshows

Potential damage to reputation and customer relationships.

OUR OBJECTIVE IS TO CONSTRUCT A SUSTAINABLE AND GROWING

BUSINESS THROUGH GOOD LEADERSHIP AND EFFECTIVE

COMMUNICATION

12

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 12 05/04/2017 15:18:40

25203.04 5 April 2017 3:16 PM proof 14

Strategic Focus Description & Progress Priorities for 2017 Our measures (KPIs) Associated Risks

Driving Cash

We will continue to embed a cash culture to manage our cash more effectively. From contract selection and approval, through the entire contract process and up to the final account payment. This includes improved operational reporting and flow of information to divisional management.

• Daily cash bulletins• Weekly cash dashboards• Improve payment terms from

customers• Process efficiency execution to invoice

• WIP/Debtor days • Cash collection against forecast• Overdue balances• Overdue retentions

Credit risk, liquidity risk,interest rate risk, financial loss

Improve Profit

The emphasis being placed on preventing losses as a strategic priority will in itself give rise to an improvement in profit. Other work is in progress to enhance margin return through the reduction in waste and the use of lean construction techniques. Innovative approaches to front end design and asset management opportunities will provide enhanced margin returns.

• In-house design and build offering• Off-site manufacture • Service and maintenance • Finance and investment offering• Profit enhancement plans

embedded • Planning/programme reporting

enhancement

• Margin by contract• Risks and opportunities identified and

monitored• Procurement savings• Programme management

Contracting strategy and executionInappropriate contract terms could lead to unacceptable risks relative to potential returns.

Failure to comply could lead to reputational damage, warranty claims or financial penalties.

Prevent Losses

We have thoroughly re-examined our processes across the business to continuously improve our effective commercial and operational delivery of projects.

We are engaging and challenging our people and our supply chain to continually improve quality and programme, efficiency and effectively deliver for our customers.

Read more about Strategy in Action on page 18

• Thorough contract selection• Robust corporate governance• Rigorous risk management• Active contract performance

monitoring• Immediate corrective action

• Contract risk level review• Project monitoring assessments• Margin by contract• Risks and opportunities identified and

monitored

Integrity of financial controlsDamage to reputation.

Financial loss.

Lack of integrity of financial information used to manage the business leading to inappropriate decisions.

Develop, Maintain and Protect our People

People remain key to our success. Keeping a “family feel” around the Group is a high priority as we progress. Recruitment and retention is at a high. We will continue with our learning and development. This is aligned with our business culture.

Read more about Strategy in Action on page 20

• Develop a learning culture• Continuous performance appraisal• Promotion opportunities from within• Address underperformance• Learning is for everyone• Mentor and Buddy arrangements

• Employee stability index• Training across the Group• Employee engagement• Learning and development• Recruitment

Attraction and retention of key managementFailure to attract and retain key management could lead to a lack of necessary expertise or lack of continuity to execute strategy.

Enhance Brand Image

We have identified two core focus points in enhancing our brand image: Customer Experience and Public Relations (PR).

We have formed the Improving Customer Experience Panel (iCEP) with the purpose of providing industry leading customer experience.

We are reviewing our PR plan, core media targets and approach to be more visible in the marketplace. A senior project team has been commissioned to look at this.

• Customer Experience and iCEP• Reduce customer complaints• Effective PR campaign• Consistent high quality image

• Increase in PR article take up• Defined processes and proformas

developed for Customer Experience• Review branding

Potential damage to reputation and customer relationships.

Effective Communication

Effective communication, both internally and externally, is undergoing review and improvement to ensure that our key business messages are conveyed in both an appropriate format and a timely manner. A senior project team has been commissioned to look at our overall communication strategy in line with our brand and input from all stakeholder groups.

Read more about Strategy in Action on page 22

• Effective use of social media• Face-to-face meetings• Effective cascade of information• Prioritise key messages`

• Increase in social media interactivity • External newsletter• Review of internal communication: alerts,

newsletter, Blueprint etc.• Employee engagement surveys and

subsequent implementation of feedback• Senior management roadshows

Potential damage to reputation and customer relationships.

Our strategy reflects the restoration of a respectable profit margin in the short term. This will be reflected in a progressive dividend payment to the shareholders being declared. It is built with a clear focus on quality of earnings and improved cash management together with a sensible growth profile being pursued.

Read about our KPIs on page 14 Read about our Risks and Uncertainties on page 32

Str

ateg

ic R

epor

t

13

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 13 05/04/2017 15:18:40

25203.04 5 April 2017 3:16 PM proof 14

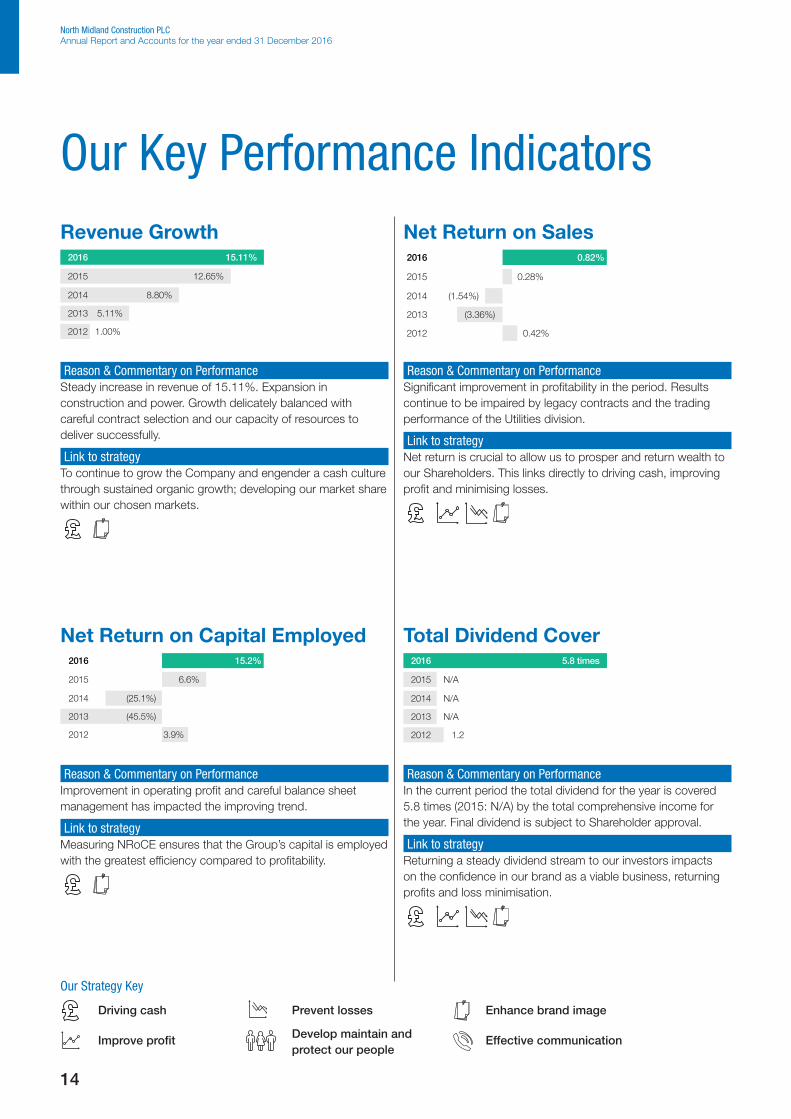

Our Key Performance IndicatorsRevenue Growth

2016 15.11%

2015 12.65%

2014 8.80%

2013 5.11%

2012 1.00%

Reason & Commentary on PerformanceSteady increase in revenue of 15.11%. Expansion in construction and power. Growth delicately balanced with careful contract selection and our capacity of resources to deliver successfully.

Link to strategyTo continue to grow the Company and engender a cash culture through sustained organic growth; developing our market share within our chosen markets.

Net Return on Capital Employed2016 15.2%

2015 6.6%

2014 (25.1%)

2013 (45.5%)

2012 3.9%

Reason & Commentary on PerformanceImprovement in operating profit and careful balance sheet management has impacted the improving trend.

Link to strategyMeasuring NRoCE ensures that the Group’s capital is employed with the greatest efficiency compared to profitability.

Net Return on Sales2016 0.82%

2015 0.28%

2014 (1.54%)

2013 (3.36%)

2012 0.42%

Reason & Commentary on PerformanceSignificant improvement in profitability in the period. Results continue to be impaired by legacy contracts and the trading performance of the Utilities division.

Link to strategyNet return is crucial to allow us to prosper and return wealth to our Shareholders. This links directly to driving cash, improving profit and minimising losses.

Total Dividend Cover2016 5.8 times

2015 N/A

N/A

N/A

2014

2013

2012 1.2

Reason & Commentary on PerformanceIn the current period the total dividend for the year is covered 5.8 times (2015: N/A) by the total comprehensive income for the year. Final dividend is subject to Shareholder approval.

Link to strategyReturning a steady dividend stream to our investors impacts on the confidence in our brand as a viable business, returning profits and loss minimisation.

Our Strategy Key

Driving cash

Improve profit

Prevent losses

Develop maintain and protect our people

Enhance brand image

Effective communication

14

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 14 05/04/2017 15:18:41

25203.04 5 April 2017 3:16 PM proof 14

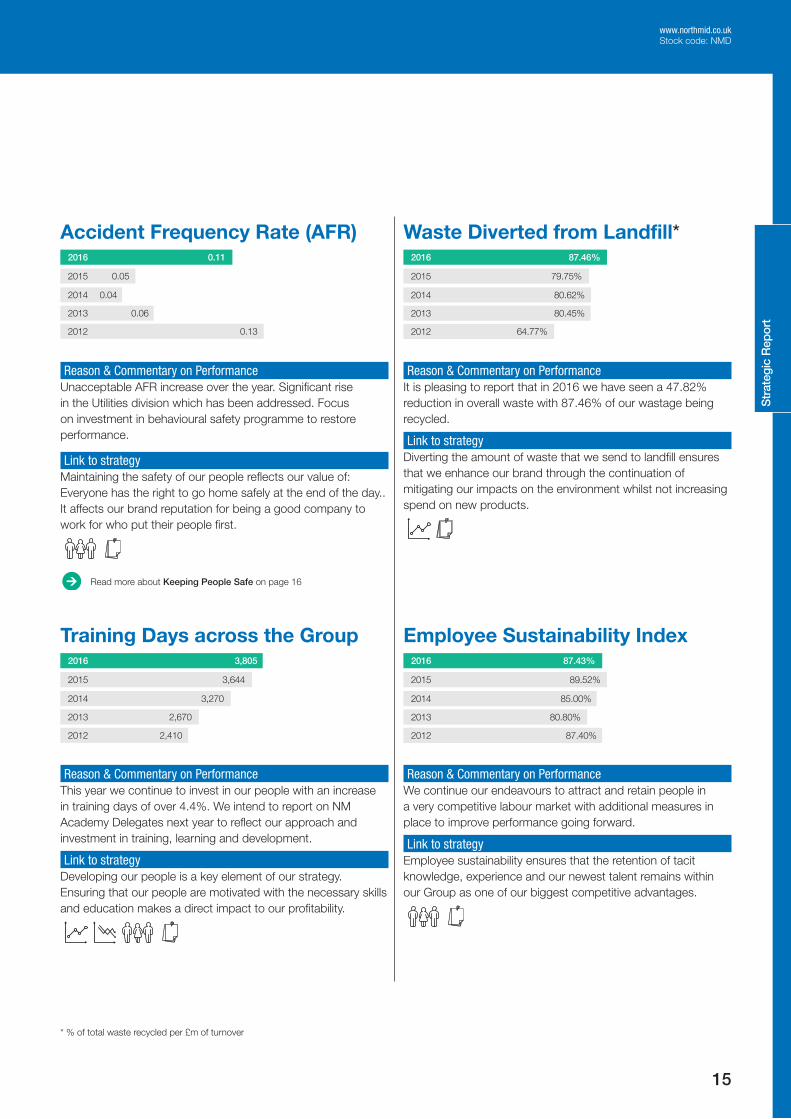

Accident Frequency Rate (AFR)2016 0.11

2015 0.05

2014 0.04

2013 0.06

2012 0.13

Reason & Commentary on PerformanceUnacceptable AFR increase over the year. Significant rise in the Utilities division which has been addressed. Focus on investment in behavioural safety programme to restore performance.

Link to strategyMaintaining the safety of our people reflects our value of: Everyone has the right to go home safely at the end of the day.. It affects our brand reputation for being a good company to work for who put their people first.

Training Days across the Group 2016 3,805

2015 3,644

2014 3,270

2013 2,670

2012 2,410

Reason & Commentary on PerformanceThis year we continue to invest in our people with an increase in training days of over 4.4%. We intend to report on NM Academy Delegates next year to reflect our approach and investment in training, learning and development.

Link to strategyDeveloping our people is a key element of our strategy. Ensuring that our people are motivated with the necessary skills and education makes a direct impact to our profitability.

Waste Diverted from Landfill*2016 87.46%

2015 79.75%

2014 80.62%

2013 80.45%

2012 64.77%

Reason & Commentary on PerformanceIt is pleasing to report that in 2016 we have seen a 47.82% reduction in overall waste with 87.46% of our wastage being recycled.

Link to strategyDiverting the amount of waste that we send to landfill ensures that we enhance our brand through the continuation of mitigating our impacts on the environment whilst not increasing spend on new products.

Employee Sustainability Index2016 87.43%

2015 89.52%

2014 85.00%

2013 80.80%

2012 87.40%

Reason & Commentary on PerformanceWe continue our endeavours to attract and retain people in a very competitive labour market with additional measures in place to improve performance going forward.

Link to strategyEmployee sustainability ensures that the retention of tacit knowledge, experience and our newest talent remains within our Group as one of our biggest competitive advantages.

Read more about Keeping People Safe on page 16

* % of total waste recycled per £m of turnover

Str

ateg

ic R

epor

t

15

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 15 05/04/2017 15:18:41

25203.04 5 April 2017 3:16 PM proof 14

Our 2016 Performance and Strategy for ImprovementThis is an overarching business priority.

Unfortunately, last year showed a deterioration in performance which occurred during the first seven months of the year. Whilst the majority of divisions demonstrated exemplary performance with regards to accidents, with Building, Civils, Highways and Nomenca all being free from all but very minor accident, the Utilities division suffered a significant drop in performance over the first few months of 2016. As a result of thorough investigation and in order to address this a number of key changes were implemented. The health and safety team was strengthened with increased resource dedicated to the Utilities division, increased senior manager site visits and the implementation of monthly health and safety stand downs with the workforce to ensure that effective communication and engagement is achieved. The last five months of 2016 were more positive and were without significant accidents across all divisions. However, we remain vigilant and continue to strive for improvement across the business.

In line with our strategy we are increasing the focus on the areas that surround health and wellbeing with particular focus on the issues associated with dust and mental health.

How this links to our strategyPeople remain our most important asset and are key to our success. We cannot deliver without our people being safe and well. The learning and development aspect of this initiative ensures that we continually learn and progress with our behavioural approach to safety and do not stand still. Health and safety incidents affect individuals, wider teams, morale and how we are perceived as a compnay within the marketplace. Being a safe company to work for supports recruiting new people into our Group.

What we didDuring 2016 we reassessed our behavioural safety approach and began a culture change initiative by introducing the Safety Culture Team (SCT). The SCT are also being furnished with further training to build their skills and confidence in talking about and understanding operational issues.

The team is made up of a core group of enthusiastic volunteers from across our business, at all levels. Their focus is on positive

aspects of safety and driven by being engaged in conversations with the rest of our people. This allows for an operational led approach to better understanding the challenges involved in changing beliefs and behaviours and in turn having a positive impact on our culture, which is longer lasting than solely implementing initiatives from the top down. The team have been coached in, amongst other things, the undertaking of positive conversations and promoting engagement in order to allow them to develop their role.

One of the roles of the SCT is to use the skills they have learnt to gather intelligence to understand the areas of health, safety and wellbeing where we perform well, as well as areas for improvement. This information will then be used to challenge how we do things and lead to robust, practical solutions to any issues. This will provide them with more skills to carry out their role in improving the safety culture at the Company and increase engagement. By talking about safety and decision making processes, more time will be spent with a focus on safe behaviour and effective operational safety planning.

The team will also be supporting larger presentations and creating campaigns in the future in regards to behavioural safety.

How we will use this moving forwardThe understanding that the SCT will gain from operations will provide us not only with safety information that can inform our continuous improvement but also within our health and wellbeing strategy. Our continuing objectives for 2017 include integrating health and wellbeing into our business processes.

What was the outcome? The SCT have shaped their role within the business and have been given full ownership with guidance from the QESH team. This allows for idea generation and fresh approaches to be put forward as solutions. As the team is built up of non-safety employees it allows for further honesty in what is and isn’t working, contributing to the overall improvement in safety performance.

OUR OVERARCHING BUSINESS PRIORITY IS KEEPING PEOPLE

SAFE AND CONTINUING TO INVEST OUR TIME AND RESOURCES

IN PERFORMANCE IMPROVEMENT

Read more online at www.northmid.co.uk

Read more about Corporate Social Responsibility on page 38

Keeping People SafeHEALTH AND SAFETY

16

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 16 05/04/2017 15:18:42

25203.04 5 April 2017 3:16 PM proof 14

The last five months of 2016 were more positive and were without significant accidents across all divisions.

Str

ateg

ic R

epor

t

17

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 17 05/04/2017 15:18:43

25203.04 5 April 2017 3:16 PM proof 14

Our Strategy in ActionPREVENT LOSSES

How this links to our strategy The Group has suffered from numerous Legacy Contracts which have impacted, not only the income statement and balance sheet but also deflected key management time and Group resources in their resolution. The term “Legacy Contracts” is one that has been widely used in the construction industry over the last few years without being specifically defined. The Group uses the term to refer to contracts entered into at the height of the recession and which carried a high contractual and commercial risk. More specifically, these are contracts that were entered into before 31 December 2013 and which had become loss making.

The losses and poor use of Senior Management time could not continue. Preventing our losses has a direct correlation from a Group point of view with growing our margins.

What we didStrategyThe starting point was to reduce the significant loss making division (specifically the old BCE division) where three of the major legacy contracts had resided. In 2014, the division was split into the relevant disciplines of building and civil engineering. The strategy for both divisions was redefined and refocused based on the Group’s vision of choosing which markets and what customers we want to work for and deliver excellence with.

Risk Management and GovernanceAligned with the revised strategy, the Group enhanced its initial (pre-pricing assessment) and ongoing (project monitoring and peer reviews) Risk Management processes.

The pre-pricing assessment procedures were to ensure assessments and understanding of risk were completed at an earlier stage in the process and our Governance strengthened to involve divisional and Main Board Directors as required. The processes were not developed to be restricted but were imbedded to drive a culture of transparency and team involvement ethos. The Group is progressive and thus these systems have continued to be developed and enhanced over the last three years.

The project monitoring and peer reviews are undertaken by the Commercial Forum, which is headed by the Group Finance Director and includes all the commercial heads of each division. For all intents and purposes, these reviews are internal audits managed in a way to develop teams and help learning and understanding of how each specific contract needs to be administered. The results are communicated back to the Group Finance Director and the divisional Managing Director along with the forum itself and opportunities for improvements identified and changed through a progressive learning cycle. Where necessary, Group procedures are adapted and/or training delivered on the specific items raised.

What was the outcome? The Group operates in the construction industry which has inherent risks. Through strategy adjustments and the enhancements noted above we have “derisked” our works accordingly. We believe that discussing and understanding the potential risks at an earlier stage and engaging with the right skilled people, means that we are able to better plan and mitigate accordingly. Since the introduction of the items noted above we have not had the magnitude of losses as recognised during the recession and directly from the legacy contracts.

How we will use this moving forwardWe will continue to utilise the procedures set out whilst developing our people and sharing cross divisional best practice. One of the Group projects for 2017 is to review key deliverable, planning and programmes which were identified throughout the year as areas we could strengthen and improve upon.

Read more online at www.northmid.co.uk

THE PRE-PRICING ASSESSMENT PROCEDURES WERE TO ENSURE

ASSESSMENTS AND UNDERSTANDING OF RISK WERE COMPLETED AT AN

EARLIER STAGE IN THE PROCESS AND OUR GOVERNANCE STRENGTHENED

TO INVOLVE DIVISIONAL AND MAIN BOARD DIRECTORS AS REQUIRED.

18

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 18 05/04/2017 15:18:44

25203.04 5 April 2017 3:16 PM proof 14

The Group is progressive and thus these systems have continued to be developed and enhanced over the last three years.

Str

ateg

ic R

epor

t

www.northmid.co.uk Stock code: NMD

19

North Midland Construction AR2016 front proof 14.indd 19 05/04/2017 15:18:45

25203.04 5 April 2017 3:16 PM proof 14

Our Strategy in Action DEVELOP OUR PEOPLE

How this links to our strategyOur people are the core element to our values. We therefore recognise that our people are the key to our success and we make it our priority to appreciate and value them. If our people are motivated and performing, so will our business.

What we didOur strategic development plan ensures that we attract, recruit, engage, develop and retain the best people. This is fundamental to the continuing success of the Group and its long term viability to drive performance and enable effective change.

We have approximately 1,350 people in our offices and on our sites, with a number of additional sub-contractors engaged to create a strong, supporting and successful team. The quality of our work is entirely dependent on the quality of our people, ensuring everyone is motivated, developed and rewarded for their contribution and commitment.

Developing our people and nurturing our talent is the key to us realising our vision and to support this, in 2003, we began our journey with Investors in People (IIP). We have since worked tirelessly to implement recommendations for improvement and IIP has formed an integral aspect of our business planning strategy. The measure of our success was in 2014 when we were awarded Gold status.

In 2016 we were assessed under the new sixth generation framework which focuses on nine high performance indicators under the headings of Leading, Supporting and Improving. It is a reflection of latest workplace trends, fundamental skills and successful structures that demonstrate high performance.

The nine high performance indicators:

Leading1. Leading and inspiring people

2. Living the organisation’s values and behaviours

3. Empowering and involving people

Supporting4. Managing Performance

5. Recognising and rewarding high performance

6. Structuring work

Improving7. Building capability

8. Delivering continuous improvement

9. Creating sustainable success

The above performance indicators are designed to assess organisations who put people management at their heart and are a reflection of latest workplace trends, fundamental skills and successful structures that demonstrate high performance.

What was the outcome? We successfully retained the prestigious Gold status accreditation in 2016 and are very proud of this achievement. We are among 1,541 companies in the UK who have achieved Gold and are one of just 260 companies in the Central England region.

The attainment of this status, under the new sixth generation framework, is a significant milestone on our journey and is testament to our continuous improvement to people development through implementation, review and effective change.

How we will use this moving forwardOver the last year we have enhanced our Leadership and Management programmes to include the implementation of an Introduction to Management. This is for people aspiring to be a leader or manager and to realise and unleash their potential. We also commenced a bespoke Business Leadership Programme for senior managers to empower innovation and make an impact within the Group for our strategic goals.

Our Leadership and Management strategy will help develop our leadership culture which will lead us to achieve our business ambitions and give us the focus for supporting the learning and development of our people. This in turn will put us in a strong position to realise our objective, to achieve Platinum status with IIP, within five years.

Read more online at www.northmid.co.uk

OUR STRATEGIC DEVELOPMENT PLAN ENSURES THAT WE ATTRACT,

RECRUIT, ENGAGE, DEVELOP AND RETAIN THE BEST PEOPLE. THIS IS

FUNDAMENTAL TO THE CONTINUING SUCCESS OF THE GROUP AND

ITS LONG TERM VIABILITY.

20

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 20 05/04/2017 15:18:45

25203.04 5 April 2017 3:16 PM proof 14

Our people are the core element to our values. We therefore recognise that our people are the key to our success and we make it our priority to appreciate and value them.

Str

ateg

ic R

epor

t

21

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 21 05/04/2017 15:18:46

25203.04 5 April 2017 3:16 PM proof 14

Our Strategy in Action EFFECTIVE COMMUNICATION

How this links to our strategyEffective communication and enhancing our brand are key elements of our strategy. Both intrinsically link to our relationships with stakeholders and directly have an impact on our perception within the marketplace. As a leader within our field, this will enhance the attraction of new talent and motivate our people. We are aware that we need to promote ourselves further to assist us with our presence to our customers in terms of service developments.

What we didOur 2016 Autumn roadshows gave our employees a chance to hear from our Directors on how the Group is performing and our focus areas for 2017. We asked for feedback on many areas, one of which was communication. This presented a mix of opinions and areas of improvement.

Each year we have a number of our senior leaders who embark on the Institute of Leadership and Management (ILM) Level 7 qualification. The outcomes of this benefit both individual development as well as allowing business improvement to take place through critical analysis, debates on leadership, developing a world class delivery model and understanding engagement. The team works on projects that are of strategic importance to our organisation. One of the focuses for this year is how we use effective communication to our people and externally to stakeholders.

What was the outcome? Following this feedback the team is in the process of developing protocol for dissemination of information and knowledge that supports our vision, values and strategy. Analysis of purpose, intention and efficacy will be ongoing.

How we will use this moving forwardThe findings and new processes will be utilised to effectively manage our relationships internally and externally with a positive influence on our reputation.

This will inform a number of immediate changes to our lines of internal communication including corporate inductions, the timely release of positive messages and face-to-face briefings. The effective cascade of information to relevant parties by a range of media will be put into action. Our workforce is diverse with different communication preferences and needs. We realise that by strengthening our communication strategy and tailoring it this will increase morale.

Our public relations strategy will also be informed by the findings, including our social media presence, relationship with the media on a national level and communicating more effectively with our clients.

Our intent is to prioritise our key messages to best influence our brand profile as a leader in our chosen markets.

Read more online at www.northmid.co.uk

EFFECTIVE COMMUNICATION AND ENHANCING OUR BRAND ARE KEY S

ELEMENTS OF OUR STRATEGY. BOTH INTRINSICALLY LINK TO OUR S

RELATIONSHIPS WITH STAKEHOLDERS AND DIRECTLY HAVE ANS

IMPACT ON OUR PERCEPTION WITHIN THE MARKETPLACE.S

As a leader within our field, this will enhance the attraction of new talent and motivate our people.

22

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 22 05/04/2017 15:18:46

25203.04 5 April 2017 3:16 PM proof 14

Our Operational and Financial Review

Further significant investment has been made in implementing governance controls to manage risk and into the development of our people to meet the increasing demands of our customers for a high-quality service.

Overview of 2016 This year has been a period of strengthening the business in preparation for a sustainable growth in quality of earnings and respectable dividend yields. Further significant investment has been made in implementing governance controls to manage risk and into the development of our people to meet the increasing demands of our customers for a high-quality service. The Group is now well positioned to take advantage of the increase in infrastructure spending plans that prevail.

Group Structure Our operational activities are divided into six operating divisions working in five distinct market sectors (our segments). Each segment has a clear focused offering to the customers that they serve. These divisions have the skills and experience to meet the needs of the customers and work effectively in these markets. This allows them to provide expert contribution and innovation to achieve added value to the work streams.

Overall co-ordination of our activities is carried out through the Executive Administration Board (EAB) which is chaired by the Chief Executive. Membership consists of the Directors of the divisions and the central services functions.

The overarching purpose of this body is to ensure consistency of best practice and to drive performance improvement across all of our activities.

Group Financial Performance The growth in turnover of 15.11% to £250.49 million (2015: £217.61 million) is encouraging and is borne from our vision of growing revenues in our chosen markets with our repeat and framework clients. It is also very encouraging to see the level of new customers and enquiries in 2016 achieved through the quality of customer experience NM Group deliver.

Although not at the level the Board finds acceptable, the operating profit of £2.24 million (2015: £0.85 million) is a significant increase on the previous year. The impact of the Legacy Contracts has once again reduced the net margin return to Shareholders as highlighted on page 25.

The confidence of the Board in the Group continuing to report periods of profitability has led to the full recognition of the previous years’ losses as a deferred tax asset (see note 22). This has been the contributing factor on the current tax credit of £0.57 million (2015: £0.65 million).

The increased performance and recognition of the brought forward losses has meant the total comprehensive income for the year has more than doubled to £2.63 million (2015: £1.25 million) and in turn the earnings per share increased to 25.95p (2015: 12.32p).

It is therefore with great pleasure that the Board is proposing a restoration of the final dividend at 3.0p, taking the total dividend for the year to 4.5p. In the current period the total dividend for the year is covered 5.8 times (2015: N/A) by the total comprehensive income for the year.

The Board anticipate an improving performance for 2017 and beyond.

Health and Safety Unfortunately, we have seen an increase in our Accident Incident Rate due to the number of RIDDOR (Reporting of Injuries, Diseases and Dangerous Occurrences Regulations 1995) incidents during the year, which is disappointing for the Group. These incidents have not shown any particular trend in cause or type other than the challenges faced by our industry as a whole as a consequence of the increase in demand for suitable labour. Corrective action was immediately taken to address any specific issues in the divisions concerned. We continue to focus on this as the subject of utmost priority with

Operating profit

2015: £0.85m

£2.24m+163.53%

Revenue

2015: £217.61m

£250.49m+15.11%

Str

ateg

ic R

epor

t

23

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 23 05/04/2017 15:18:46

25203.04 5 April 2017 3:16 PM proof 14

ongoing awareness and training programmes being provided. These incidents all occurred in the first seven months of the year and since then we have seen a marked improvement in our performance.

To complement the traditional policing approach to health and safety we have embarked on a Behavioural Culture approach with representatives from across the business being trained and acting as advocates. This is to encourage people to think about the approach to inherent hazards that they come across in a much more proactive and conscious way. It is expected that this programme will further enhance our overall performance in this field.

PeopleThere is no doubt that our people and our culture are the largest influence in the way that we serve our customers and ultimately to the overall success of the business. During the year we recruited a total of 413 new employees to the Group. Against the backdrop of a very competitive market for resources we have managed to hold a steady position on our employee stability ratio. We continue to invest heavily in the development of our people across the complete spectrum of skills and experience. Our training and development academy approach continues to be refined and is delivering the results that are required. Our leadership across the business is clear that we constantly need to put people at the top of the agenda in order to achieve the best results.

Segment Performance The following pages 26 to 31 contain an assessment of our performance based on the markets we choose to serve and inclusive of analysis of the division that serve those markets (our segments). The key driver that the segments are assessed on is net profit contribution, along with opportunities for future workload through turnover growth.

We continue to maintain our strong position of market leadership in the Water sector. Both turnover and margin growth has been achieved and great potential exists for further progress. Our customers in this sector include Severn Trent Water, United Utilities, South West Water and Yorkshire Water. Notable projects carried out in the period are the Elan Valley tunnel and the Ambergate reservoir both for Severn Trent. Investment is being made in our design capability, off-site manufacture and our product supply offering. Preparations are underway for the AMP7 renewal cycle which will come to the market in the next two years. We are well positioned to take advantage of this potential stream of work to fuel our future growth.

The construction division has performed well in the year. We are now in a period of consolidation to ensure that we have the correct people and management systems in place to continue with this success. Notable projects undertaken in the year include the completion of the Allen House student accommodation scheme in the centre of Leicester. The division is well placed for further controlled growth in the regional building market.

Our activities in the Power sector have achieved an improvement in performance over the year. Work continues to be carried out on our Western Power Distribution framework and key projects for Alstom and Siemens. Growth potential exists for the services that we provide into this market on a national basis.

Our highways division has continued to improve performance over the year. Notable schemes completed include the Leeds to Bradford Cycle Superhighway and the Bristol Western relief road improvements. We have been successful in securing a place on a number of notable framework arrangements including Highways England Area 7 and Lincolnshire County Council.

Our Operational and Financial Review

24

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 24 05/04/2017 15:18:47

25203.04 5 April 2017 3:16 PM proof 14

The telecommunications division has undergone considerable restructuring and change following several years of unsatisfactory performance. A new management structure is in place and relationships with all of the customers have been reviewed. Notable works have been carried out for Virgin Media on both their regular and strategic expansion programmes. The market is very strong in this sector with significant spending plans in place across the whole country. The performance of this division is under careful scrutiny to ensure that the changes made achieve the desired results and achieve an acceptable margin return.

Legacy Legacy contracts are construction contracts entered into at the height of the recession, before 31 December 2013, and which carried a high contractual and commercial risk. These contracts have negatively impacted the Group’s income statement in 2013 and subsequent years. As at 31 December 2016, there is only one legacy contract remaining.

In the year to 31 December 2016, the total loss before tax recognised on legacy contracts was £3.85 million (2015: £3.84 million). As at 31 December 2015, onsite works were still ongoing and therefore there was uncertainty over costs to complete and a further loss was recognised in 2016. However, during the year the Group completed all onsite works for the one remaining legacy contract, therefore removing any further uncertainty around costs to fulfil the contract.

Contract revenue on the one remaining legacy contract has been recognised based on the prudent best estimate of the Directors as at 31 December 2016 of the amount recoverable from the client, with an amount outstanding included with construction contract assets. The Group is and will be pursuing claims with the client for sums greater that the carrying value and is in negotiations to settle this balance. The Directors have sought to make the estimate as precise as possible by reflecting the views of independent quantum and legal experts who were appointed by the Directors for their ability, qualifications and experience in this field.

The independent quantum and legal experts, in conjunction with management, considered a number of factors when making their assessment, such as contractual terms, work performed, claims for variations, submissions for extensions of time, claims for loss and expense and expected time frames in which settlement is likely.

Whilst the Directors are making every effort to seek a swift resolution to the matter, they are committed to achieving the best possible result for the Group. The ultimate settlement of this matter may take in excess of 12 months to achieve. Further details of the legacy contract can be found on page 94.

Group Financial Position It is very pleasing to report that our key strategic focus around driving cash is evident in the increase in the year end cash balance of £11.41 million (2015: £6.62 million). The Group has integrated further visibility for the divisions, highlighting the importance of cash and improved discipline around cash collection and upfront agreement of contractual terms.

This has meant that despite the 15.11% increase in revenue the Group has reduced the average credit period taken by its customers to 33 days (2015: 41 days) and the inflow of cash to £0.69 million (2015: £1.88 million). This inflow is due to trade and other receivables reducing to £30.71 million (2015: £31.40 million). The average credit period taken on credit purchases has also reduced to 52 days (2015: 60 days) due to shorter terms being offered to maintain the best supply chain and achieve the most commercial pricing. The inflow of cash of £4.56 million (2015: £5.12 million) due to the increase in trade and other payables to £61.15 million (2015: £56.59 million) is also due to the increase in revenue. The Group ensures it has a sustainable working capital mix for all contracts across all segments.

It is also pleasing to report that the net cash has increased to £7.43 million (2015: £2.39 million) which is due to the increase in cash above and a reduction in finance lease borrowings. The net investment during the year on fixed assets increased to £1.30 million (2015: £1.03 million) as a result of the Group’s growth.

The investment in capital assets increased during the year with the closing net book value of £13.65 million (2015: £12.78 million), which again is a result of the required growth and the Company’s strategy to purchase equipment where possible, rather than expense through operating leases.

Outlook The UK construction industry is struggling to keep up with the demand to maintain the existing infrastructure and the need for investment to support future economic growth. The Group has established positions in these markets and is well situated to take advantage of the potential for further growth.

A significant proportion of our 2017 turnover has already been secured and it is expected that the balance will be achieved from carefully selected projects during the first half of this year.

We remain confident the outlook and expect the positive progress achieved to continue into 2017 and beyond. Key successes will continue in water, and improvement will be seen in the other divisions. The strategic focus in telecommunications will enhance the performance of the Group in the short term.

John Homer Chief Executive

Str

ateg

ic R

epor

t

25

www.northmid.co.uk Stock code: NMD

North Midland Construction AR2016 front proof 14.indd 25 05/04/2017 15:18:47

25203.04 5 April 2017 3:16 PM proof 14

BUILDING DIVISION

Construction

The pipeline of opportunities for this sector is increasing across our existing customer base and is also supported by a range of new customer prospects to strengthen the portfolio.

A GOOD TRADING YEAR WITH IMPROVED PROFITABILITY.

Overall Segment PerformanceWithin the construction sector, the Building division has had a good trading year with improved profitability on the back of a rapid period of growth over the last three years.

Notable schemes completed in 2016 have included: the £16 million Allen House student accommodation project for Victoria Halls; the £3 million refurbishment of the North Laboratory for the University of Nottingham; the £2 million extension and external refurbishment for CARE partnerships in Edgbaston; and a £1 million new training centre and kennels block for Nottinghamshire Police.

The pipeline of opportunities for this sector is increasing across our existing customer base and is also supported by a range of new customer prospects to strengthen the division’s portfolio.

Our area of operation is predominantly in the Midlands region offering new build and refurbishment to the public and private sectors. Main contract capability exists for schemes up to £50 million, and focused general works operation for projects from £200k to £2 million.

Financial Performance During the Year2016£’000

2015£’000

Increase%

Revenue 23,386 11,253 107.82%Operating Profit 575 186 209.14%Operating Profit % 2.46% 1.65% 0.81%

Key Market TrendsWe have an expertise in delivering student accommodation projects and this market is still buoyant with a regular stream of enquiries for a variety of projects being received. Currently, both university and further education providers have significant investments to make in their sites and a general increase in student numbers is fuelling further need for suitable accommodations. This is a key target across the region moving forward.

Many education projects are carried out via regional or national frameworks, and the intent is to engage with a view to bidding for a place on such frameworks in the future to provide a robust stream of enquiries.

From a commercial and industrial perspective, there is activity within the regional market which we are well placed to bid for, with opportunities presenting themselves regularly.

Leisure providers are active and, with a shortage of regional contractors, this is an area of exploration which we are well placed to target.

Outlook for 2017In line with our strategic focuses, the current actions to realise our potential to grow in this market include:

• Becoming a more prominent regional contractor by improving the division’s visibility within the locality

• Further growing the team with recruitment and the development of current staff

• Expanding the client base with commercial opportunities, balancing the portfolio with public sector opportunities and enhancing existing relationships.

26

North Midland Construction PLC Annual Report and Accounts for the year ended 31 December 2016

North Midland Construction AR2016 front proof 14.indd 26 05/04/2017 15:18:48

25203.04 5 April 2017 3:16 PM proof 14

CIVILS DIVISION

Power

A fully implemented risk analysis procedure with regards to proposals, contract management and commercial assurance is ensuring that the financial return is optimised.

OUR OFFERING NOW ALSO INCORPORATES A FULL TURNKEY DELIVERY MODEL

INCLUDING DESIGN, BROADENING THE SCOPE OF OPPORTUNITY GREATLY.

Overall Segment PerformanceThe past financial year has seen continued efforts in rejuvenating this part of the business to fulfil its true potential. This has included continued efficiencies in overheads, and re-establishing a delivery model which complements the sectors in which the division operates.

Our offering now also incorporates a full turnkey delivery model including design, broadening the scope of opportunity greatly. A fully implemented risk analysis procedure with regards to proposals, contract management and commercial assurance is ensuring that the financial return is optimised.

We completed the successful delivery of the £13 million Biomethane to Grid project awarded by Severn Trent Green Power. The project was a fully integrated design and build contract delivered on three sites and is testament to the new delivery model now embedded in the division.

Financial Performance Suring the Year2016£’000

2015£’000

Increase%

Revenue 30,427 7,794 290.39%Operating Profit 256 -826 n/aOperating Profit % 0.84% -10.60% 11.44%

Key Market TrendsThe power and energy market is poised to rapidly expand and with core “blue chip” clients currently in our portfolio we should be able to improve our client base and enhance our return to the business.