personal property security reform – what you need … · allens is an independent partnership...

TRANSCRIPT

1Allens is an independent partnership operating in alliance with Linklaters LLP.

Personal Property Security reform –what you need to know

Karla Fraser, Paul Brittain & Sarah Kuman

Port Moresby, April 2015

2

Overview

• Objectives of the reform and Current Status• Key concepts under the PPSA• PPSA in practice• The proposed register• What do you need to do to be ‘PPS ready’?• Questions

3

Objectives (a recap)

• Explanatory memorandum: ‘to promote commerce’• Codify and simplify law• Single straightforward registration of security instruments• Consistent ‘in substance’ approach regardless of form• Consistency with US, Canada, Australia, NZ and others

4

Current Status – April 2015

• Personal Property Security Act 2011 – enacted but not yet commencedLegislation

• Registry provider selected – Investment Promotion Authority• Registrar of Companies to be Registrar of PPS Register• Some testing in progress

Registry

• Draft to be released for public comment shortly (May 2015)Regulations

• Treasury has flagged intent to commence in September/October 2015Commencement

• Existing security interests – six month transition period to register• New security interests – registration to commence straight awayTransition

5

Introduction to the PPSA

• widgets: who has priority? product: who has priority?

• old law – owner has the best title (supplier on retention of title terms)

• new law (PPSA) – retention of title, leases and charges are all security interests – PPSA priority rules apply to determine who has priority to

product and proceeds of sale

Supplier

Manufacturer

Bank (1)

supplies widgets on retention of title terms

All assets fixed and floating charge

Retailer

Bank (2)

All assets fixed and floating charge

incorporates widgets into product and sells on retention of title terms

leases product to customer

Customer

6

What is a PPS security interest?

every transaction thatin substance

creates a security interest

a security interest meansa legal interest in personal property

that secures payment or performance of an obligation Definition: ‘goods, chattel paper, investment property, a document of title, an instrument, money or an intangible’

(almost everything - except land and certain statutory interests) It includes:

tangible goods, vehicles, hard cash, inventory intangible things: intellectual property, contractual rights, bank accounts,

trade debts, investment property (shares, units)

Functional definition – it includes: retention of title arrangements hire purchase commercial consignments finance leases ……………and more

(without regard to its form and without regard to the person who has title to the property).

7

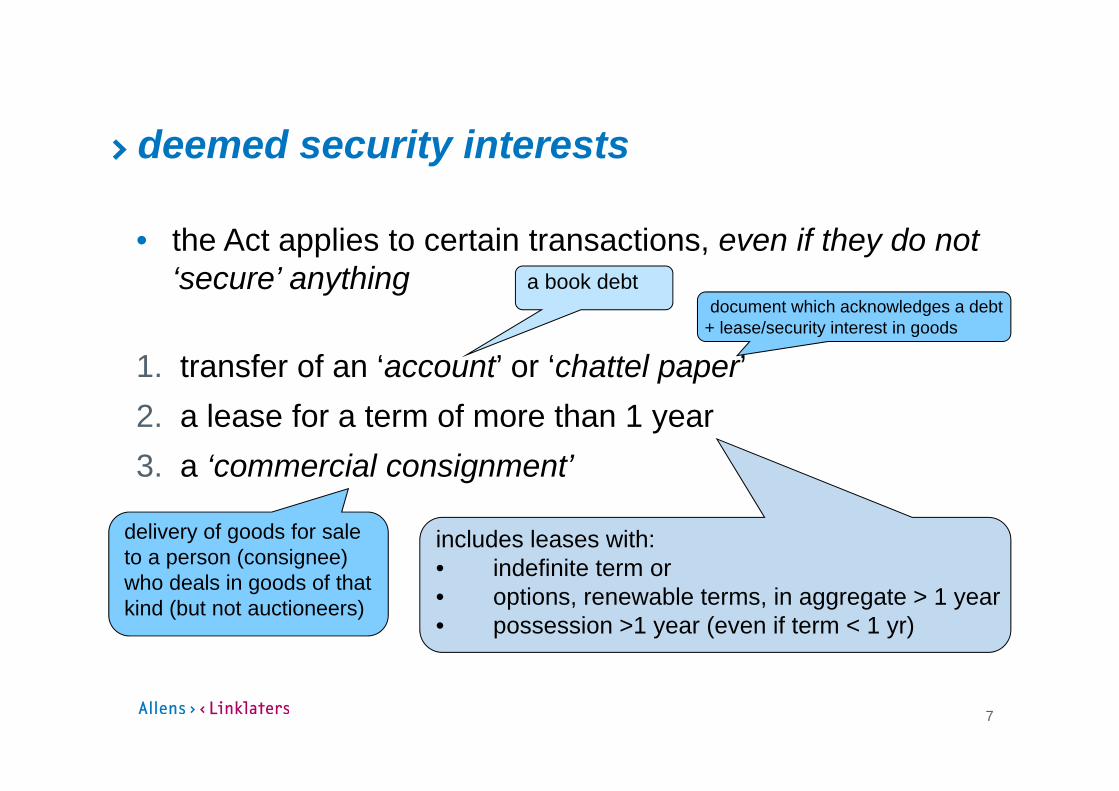

deemed security interests

• the Act applies to certain transactions, even if they do not ‘secure’ anything

1. transfer of an ‘account’ or ‘chattel paper’2. a lease for a term of more than 1 year3. a ‘commercial consignment’

a book debtdocument which acknowledges a debt

+ lease/security interest in goods

includes leases with:• indefinite term or • options, renewable terms, in aggregate > 1 year• possession >1 year (even if term < 1 yr)

delivery of goods for sale to a person (consignee) who deals in goods of that kind (but not auctioneers)

8

What is a PPS security interest?

‘in substance’ security interests

e.g.retention of titlehire purchasefinance leases

deemed security interests

- transfer of account or chattel paper

- commercial consignment- leases >1 year

traditional security interests

e.g.:- fixed charge- floating charge- chattel mortgages- pledges/liens

exclusionsnegotiable bills of lading - set-off - interests in land or payments in connection with land - transfer of unperformed contracts - transfers of remuneration for services - transfers of accounts for collection - sale of account or chattel paper as part of sale

of business – transfers of superannuation interests - excluded statutory licences (Mining Act; Oil & Gas Act)

9

Key concepts – new terminology

Debtor Secured Party

‘security interest’ (in a ‘security agreement’)

over personal property(the ‘collateral’)

1. value is given, and2. Debtor has rights in collateral,

and3. one of

• possession, • control, or• signed security agreement

1. attachment, and2. one of

• possession, • control, or• registration

‘attachment’ ‘perfection’

10

Key concepts – Security Agreements

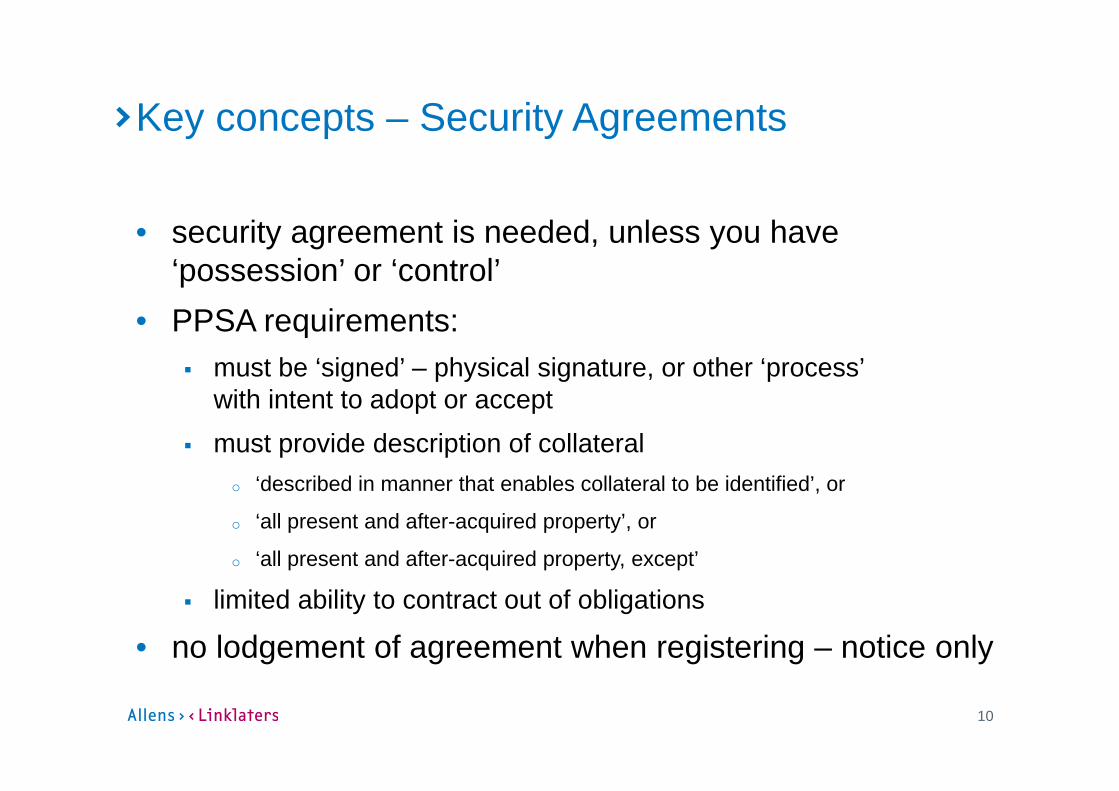

• security agreement is needed, unless you have ‘possession’ or ‘control’

• PPSA requirements: must be ‘signed’ – physical signature, or other ‘process’

with intent to adopt or accept must provide description of collateral

o ‘described in manner that enables collateral to be identified’, or

o ‘all present and after-acquired property’, or

o ‘all present and after-acquired property, except’

limited ability to contract out of obligations

• no lodgement of agreement when registering – notice only

11

Key concepts – Perfection

• Three ways to perfect: ‘possession’ ‘control’ (only deposit accounts / investment property) registration

• Three important consequences if you don’t: taking free – transferee for value without knowledge

takes free of unperfected security interest priority – unperfected security interest ranks after

perfected security interests liquidation – unperfected security interest subordinated

to interest of liquidator or trustee in bankruptcy

12

Key concepts – Priorities under the PPSA

unperfected security interest

registered later in time

registered first in time

purchase money security interest (PMSI)

perfected by control

13

Key concepts – Purchase Money Security Interests (PMSIs)

• PMSI – purchase-money security interest security interest to secure purchase price (eg retention of title) security interest given to person who provides value to enable

collateral to be acquired (eg acquisition financier) lessor – lease for term of one year or more consignor – commercial consignment

• generally, ‘super’ priority but (other than for inventory) only if perfected when debtor

receives possession, or within 7 days thereafter for inventory, in relation to the proceeds of sale of inventory, only

if certain notices are given in accordance with the PPSA

14

Key concepts – Transition

• Commencement of PPSA expected to now be late 2015• Security interests:

arising under transaction concluded prior to date of commencement of PPSA (a ‘prior transaction’)

‘transitional notice’ registered within 180 days from commencement of PPSA

takes priority over security interests arising after commencement of PPSA

• After 6 months, lose priority to other perfected interests

15

PPSA in practice – broad application

• Secured lending• Leasing• Manufacturing and supply chain• Construction• Mining, oil & gas

16

Some scenarios…

• No: no interest in personal property – contractual only

Guarantees

• Probably not, unless there is identifiable collateral (ie money held in a segregated account)

Retention amounts

• Yes: NZ portaloo case – lease for a term of more than one year

Equipment leased by contractors

• Yes: NZ Mainzeal case

Step-in rights: principal taking over equipment

17

Some more scenarios…

• Probably: dilution rights and purchase options secure performanceCross-charge needs to be registered in any event

Joint venture agreements or joint operating agreements

• No: no interest in personal property – contractual only

Performance bonds, letters of credit

• Yes: retention of title terms and leases for a term of more than one year• Make sure registration also covers future purchase orders/invoices/leases

Master Supply Agreements or Master Lease Agreements

• Yes, if lease is for a term of more than one year (or indefinite term)

Operating leases of office equipment

18

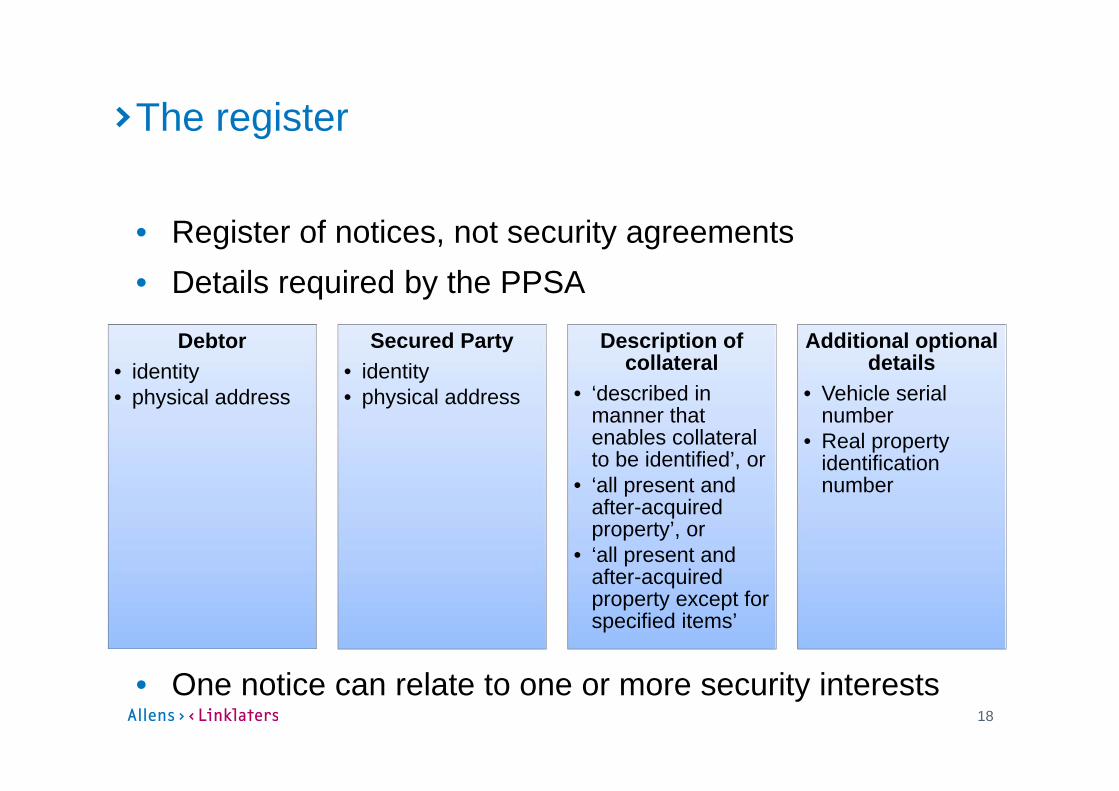

The register

• Register of notices, not security agreements• Details required by the PPSA

• One notice can relate to one or more security interests

Debtor• identity• physical address

Secured Party• identity • physical address

Description of collateral

• ‘described in manner that enables collateral to be identified’, or

• ‘all present and after-acquired property’, or

• ‘all present and after-acquired property except for specified items’

Additional optional details

• Vehicle serial number

• Real property identification number

19

The register

• Debtor authorisation: Registration must be authorised by debtor (before or

after registration) Signing security agreement is taken to constitute

authorisation• Timing: best before signing, or at least before debtor

draws down or takes possession of financed equipment• Term of registration:

Initial term designated by person registering Subsequent extensions are 5 years

20

What the registry might look like

five year registration

term

brief Debtor details

brief Secured

Party details

Collateral Description

(note: shouldn’t be necessary to identify

or lodge the document)

21Allens is an independent partnership operating in alliance with Linklaters LLP. 21

What do you need to do?

22

Where to start…

• Scoping Understand the PPSA Know your timeframes Develop a PPS plan Determine impact on business Implement plan

23

Know your enemy

• Understand the PPSA (or find a lawyer who does!) Critical to assess risk to business Internal legal – key role as educator and spotter of risk

• Know your timeframes

Intended commencement date.• The PPSA applies to all new security

interests entered into after this date.• Existing security interests must be

registered within 6 months• Transition provisions cover the 180 day

transition period

December2011

June 2014

April / May 2015

September / October

2015

March / April 2016

Act passed

PPSA becomes law

2014 originally anticipated to be commencement time

<< Register developed >>Proposed

publication of Regulations

Transition period ends. All security interests must be registered or risk losing priority.

Transition period ends

Proposed start date

Transition period Full operation

24

Develop a PPS Plan – the building blocks

• Educate (understand issues; stakeholder interest)

• Resource (project team / budget)

• Assess potential impact

• Risk / Reward Analysis (what to do, in what order and when)

• Implement: o Policies

o Processes

o Documentation

• Compliance; audit

25

Your PPS plan

Educate

Resource

Risk Assess

Analyse Risk

Implement

Compliance

March / April 2016September / October 2015April / May 2015

Act is passed

December 2011

Proposed start date Transition period endsRegulations to be released

26

Risk Assessment

• Identify potential ‘hits’ (risk) and quantify it in real terms• Start broad; focus in• Don’t half bake it – potential for large commercial losses• Remember:

it goes both ways (you may be ‘secured party’ or ‘debtor’) applies to all current and future transactions

• How? do it yourself (go it alone; or get someone to facilitate with

questionnaires and checklists) get someone in (secondees / contractor) send it out (focused audits and advice; arrangement specific)

27

Risk Assessment

• What are you looking for?• Understand your position (perfection, priority)

Currently During transitional period After transitional period Will it (or should it) change; can you improve it? Should you worry about your customers exposure too?

28

Risk Assessment

• Existing security interests identify existing security interests obtain/compile the details to complete registrations Complete registrations within 6 month transition

period• New security interests

identify transactions in your business that will give rise to security interests

implement policies and procedures for registrations be ready to go from commencement of Act

29

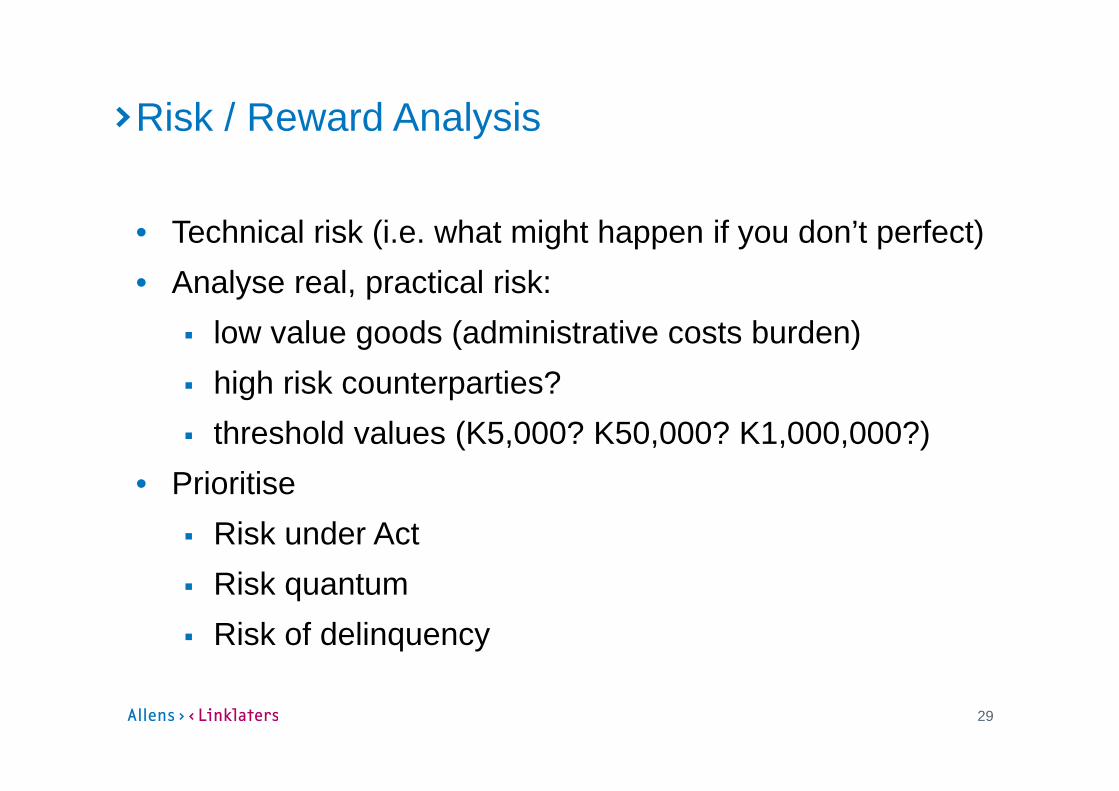

Risk / Reward Analysis

• Technical risk (i.e. what might happen if you don’t perfect)• Analyse real, practical risk:

low value goods (administrative costs burden) high risk counterparties? threshold values (K5,000? K50,000? K1,000,000?)

• Prioritise Risk under Act Risk quantum Risk of delinquency

30

Implementation and documentation

• Documentation Identify: standard security agreements in your

business, and update for PPSA Charges: cover assets in which debtor has rights Include: authority to register, contracting out of certain

PPSA obligations (eg notices), perhaps some terms• Policies

Perfection (Registration and Renewals) Releases Enforcement Role of internal counsel/external counsel

31

Compliance / Audit

• Remember that you may also grant security interests contractual restrictions (negative pledges?) procurement activities – new policies and process registration monitoring – monitor and challenge (if

necessary) registrations; demand releases of expired interests

32Allens is an independent partnership operating in alliance with Linklaters LLP. 32

Questions?

33

PPS help!

Karla Fraser - Banking & FinancePartner+61 7 3334 3251+61 420 936 [email protected]

Paul Brittain - Banking & FinanceManaging Associate, Brisbane+61 7 3334 3203+61 411 255 [email protected]

Sarah KumanSenior Associate, Port Moresby+675 305 [email protected]

34Allens is an independent partnership operating in alliance with Linklaters LLP.