perspectives on redemption patterns across intermediary-sold distribution platforms september 15,...

TRANSCRIPT

Perspectives on Redemption Patterns Across Intermediary-Sold Distribution Platforms

September 15, 2011

Dennis Bowden, Senior Research [email protected]

2

Evolving Considerations in Intermediary-Sold Space – Growth vs. Stability

Continued expansion of fee-based advisory programs Within this, recent growth of Rep-as-PM programs, as well as

increasing influence of RIAs

Increasing consideration around asset stability features across platforms Evolving economics of intermediary-sold fund distribution

Asset velocity differences across platform and FA types Platform and FA characteristics Demand trends Portfolio construction methodology

Assessing holistic, long-term opportunity sets across different intermediary-sold distribution avenues

3

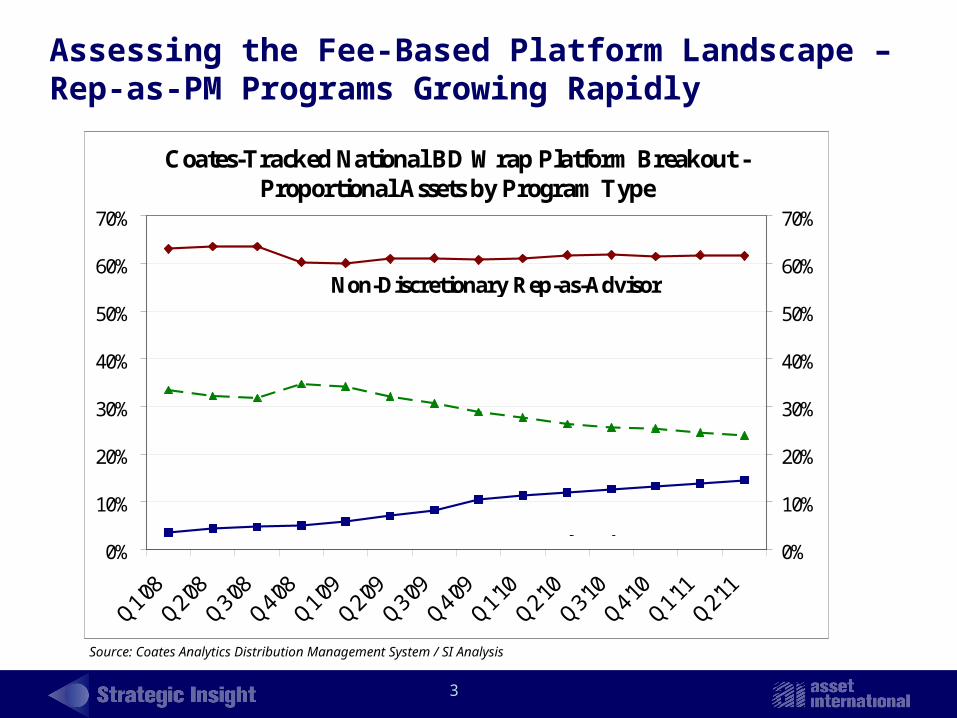

Assessing the Fee-Based Platform Landscape – Rep-as-PM Programs Growing Rapidly

Source: Coates Analytics Distribution Management System / SI Analysis

Coates-Tracked National BD Wrap Platform Breakout - Proportional Assets by Program Type

0%

10%

20%

30%

40%

50%

60%

70%

Q1'08

Q2'08

Q3'08

Q4'08

Q1'09

Q2'09

Q3'09

Q4'09

Q1'10

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

0%

10%

20%

30%

40%

50%

60%

70%

Non-Discretionary Rep-as-Advisor

Discretionary Rep-as-PM

Home Office Model Portfolio-Based

4

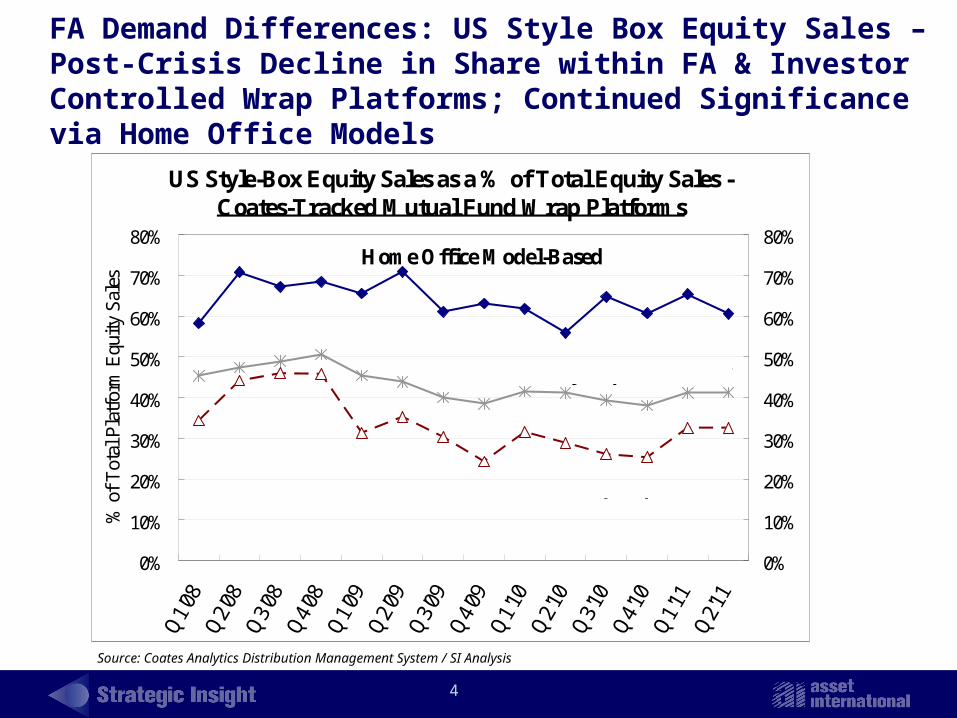

FA Demand Differences: US Style Box Equity Sales – Post-Crisis Decline in Share within FA & Investor Controlled Wrap Platforms; Continued Significance via Home Office Models

Source: Coates Analytics Distribution Management System / SI Analysis

US Style-Box Equity Sales as a % of Total Equity Sales - Coates-Tracked Mutual Fund Wrap Platforms

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q1'

08Q

2'08

Q3'

08Q

4'08

Q1'

09Q

2'09

Q3'

09Q

4'09

Q1'

10Q

2'10

Q3'

10Q

4'10

Q1'

11Q

2'11

% o

f T

otal

Pla

tfor

m E

quit

y Sa

les

0%

10%

20%

30%

40%

50%

60%

70%

80%Home Office Model-Based

Discretionary Rep-as-PM

Non-Discretionary Rep-as-Advisor

5

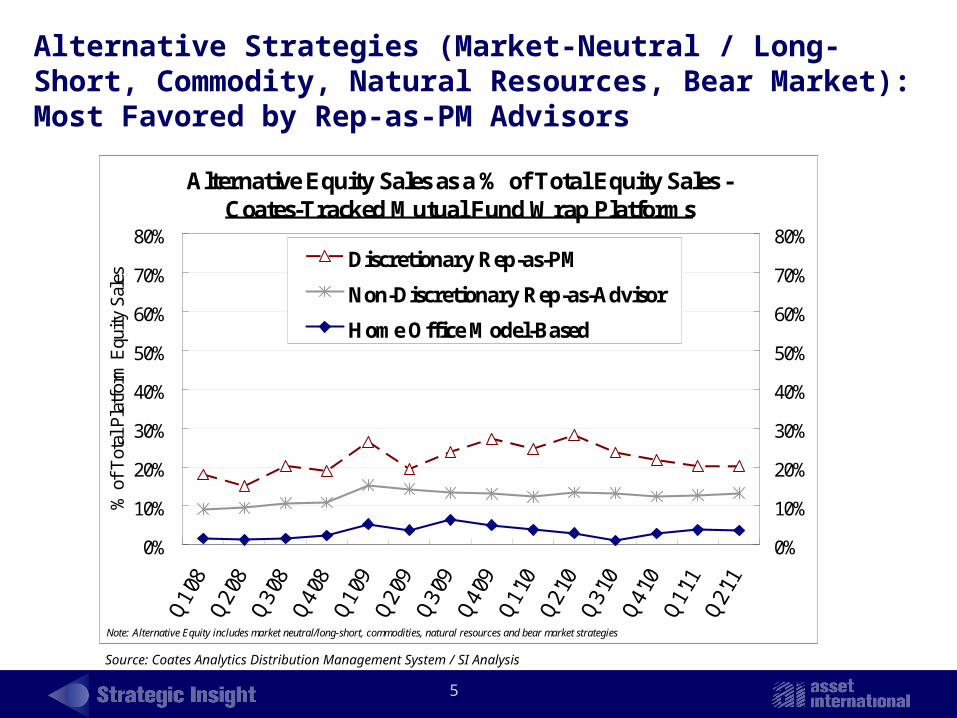

Alternative Strategies (Market-Neutral / Long-Short, Commodity, Natural Resources, Bear Market): Most Favored by Rep-as-PM Advisors

Source: Coates Analytics Distribution Management System / SI Analysis

Alternative Equity Sales as a % of Total Equity Sales - Coates-Tracked Mutual Fund Wrap Platforms

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q1'

08Q

2'08

Q3'

08Q

4'08

Q1'

09Q

2'09

Q3'

09Q

4'09

Q1'

10Q

2'10

Q3'

10Q

4'10

Q1'

11Q

2'11

% o

f T

otal

Pla

tfor

m E

quity

Sal

es

0%

10%

20%

30%

40%

50%

60%

70%

80%Discretionary Rep-as-PM

Non-Discretionary Rep-as-Advisor

Home Office Model-Based

Note: Alternative Equity includes market neutral/long-short, commodities, natural resources and bear market strategies

6

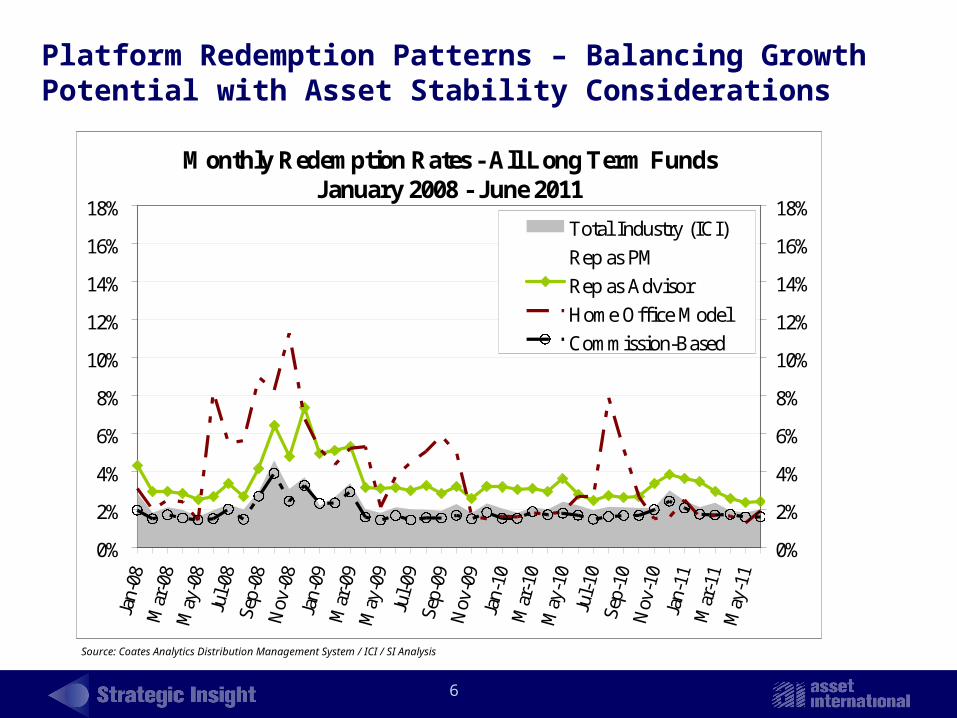

Source: Coates Analytics Distribution Management System / ICI / SI Analysis

Platform Redemption Patterns – Balancing Growth Potential with Asset Stability Considerations

Monthly Redemption Rates - All Long Term FundsJanuary 2008 - June 2011

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Jan-

08M

ar-0

8M

ay-0

8Ju

l-08

Sep-

08N

ov-0

8Ja

n-09

Mar

-09

May

-09

Jul-

09Se

p-09

Nov

-09

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep-

10N

ov-1

0Ja

n-11

Mar

-11

May

-11

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%Total Industry (ICI)

Rep as PM

Rep as Advisor

Home Office Model

Commission-Based

7

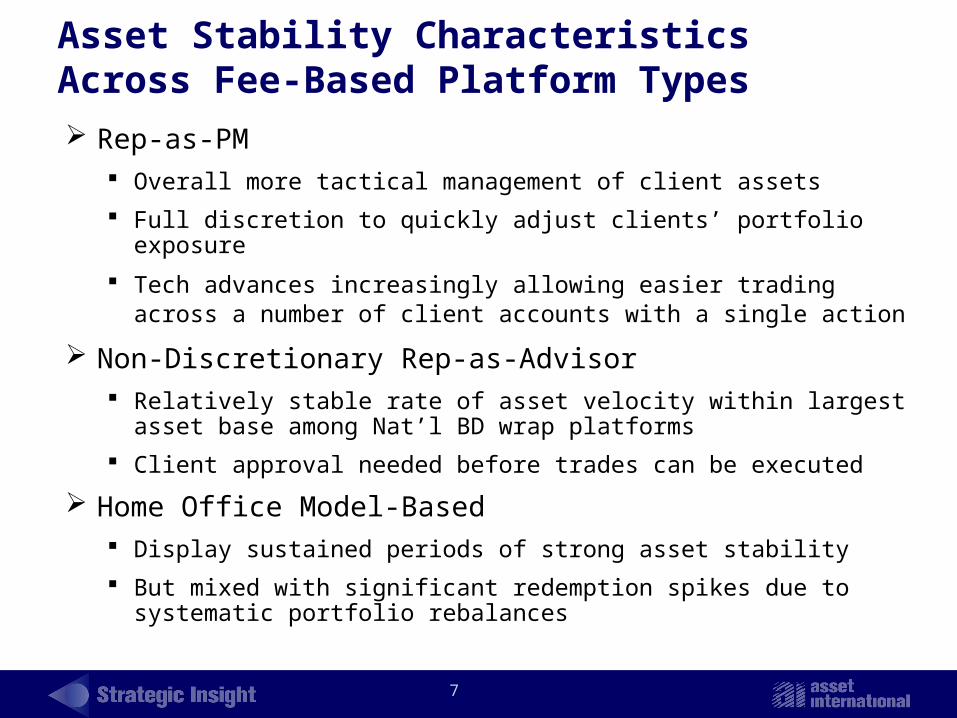

Asset Stability Characteristics Across Fee-Based Platform Types

Rep-as-PM Overall more tactical management of client assets

Full discretion to quickly adjust clients’ portfolio exposure

Tech advances increasingly allowing easier trading across a number of client accounts with a single action

Non-Discretionary Rep-as-Advisor Relatively stable rate of asset velocity within largest asset base

among Nat’l BD wrap platforms

Client approval needed before trades can be executed

Home Office Model-Based Display sustained periods of strong asset stability

But mixed with significant redemption spikes due to systematic portfolio rebalances

8

Source: Coates Analytics Distribution Management System / ICI / SI Analysis

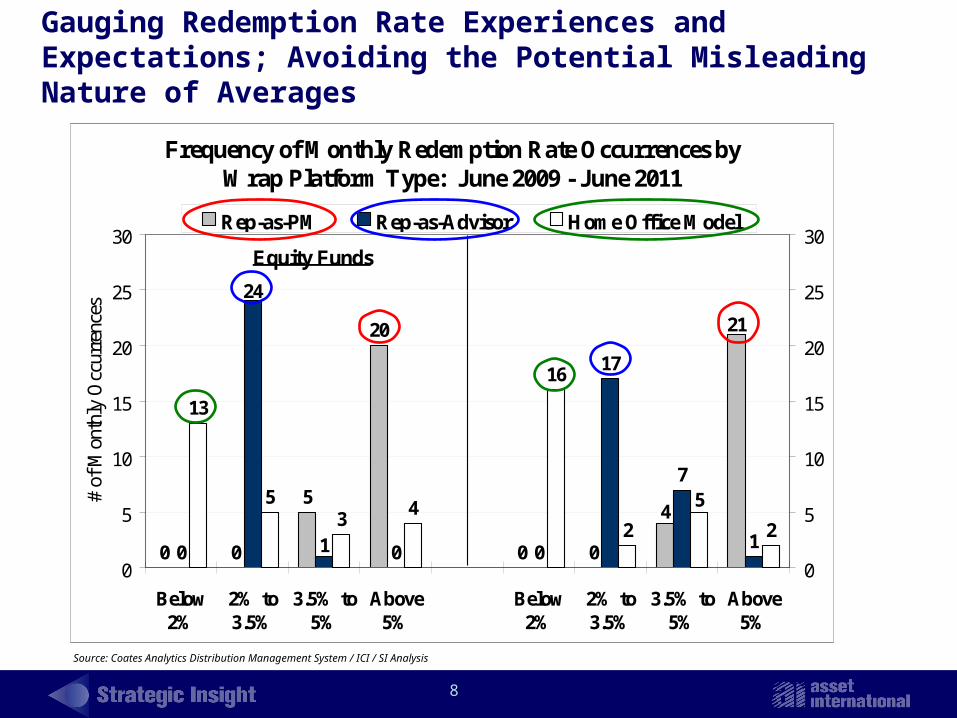

Gauging Redemption Rate Experiences and Expectations; Avoiding the Potential Misleading Nature of Averages

Frequency of Monthly Redemption Rate Occurrences by Wrap Platform Type: June 2009 - June 2011

0 0

5

20

0 00 0

17

7

1

13

53

4

16

2 2

21

4

1 0

24

5

0

5

10

15

20

25

30

Below2%

2% to3.5%

3.5% to5%

Above5%

Below2%

2% to3.5%

3.5% to5%

Above5%

# of

Mon

thly

Occ

urre

nces

0

5

10

15

20

25

30Rep-as-PM Rep-as-Advisor Home Office Model

Equity Funds Bond Funds

9

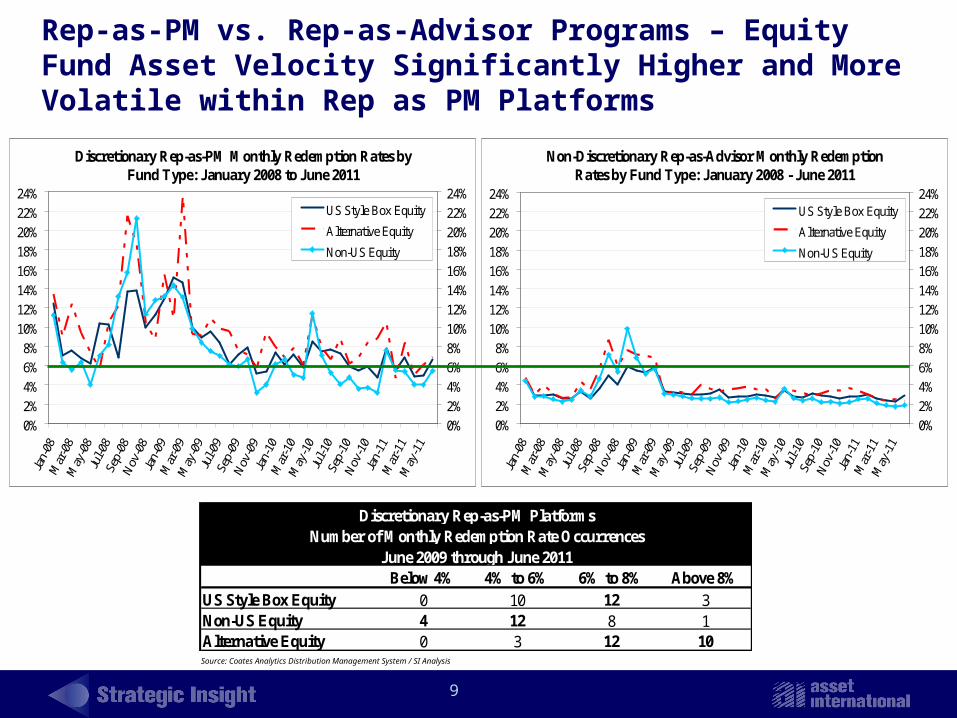

Rep-as-PM vs. Rep-as-Advisor Programs – Equity Fund Asset Velocity Significantly Higher and More Volatile within Rep as PM Platforms

Discretionary Rep-as-PM Monthly Redemption Rates by Fund Type: January 2008 to June 2011

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%US Style Box Equity

Alternative Equity

Non-US Equity

Non-Discretionary Rep-as-Advisor Monthly Redemption Rates by Fund Type: January 2008 - June 2011

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%US Style Box Equity

Alternative Equity

Non-US Equity

Below 4% 4% to 6% 6% to 8% Above 8%US Style Box Equity 0 10 12 3Non-US Equity 4 12 8 1Alternative Equity 0 3 12 10

Discretionary Rep-as-PM PlatformsNumber of Monthly Redemption Rate Occurrences

June 2009 through June 2011

Source: Coates Analytics Distribution Management System / SI Analysis

10

Source: Coates Analytics Distribution Management System / SI Analysis

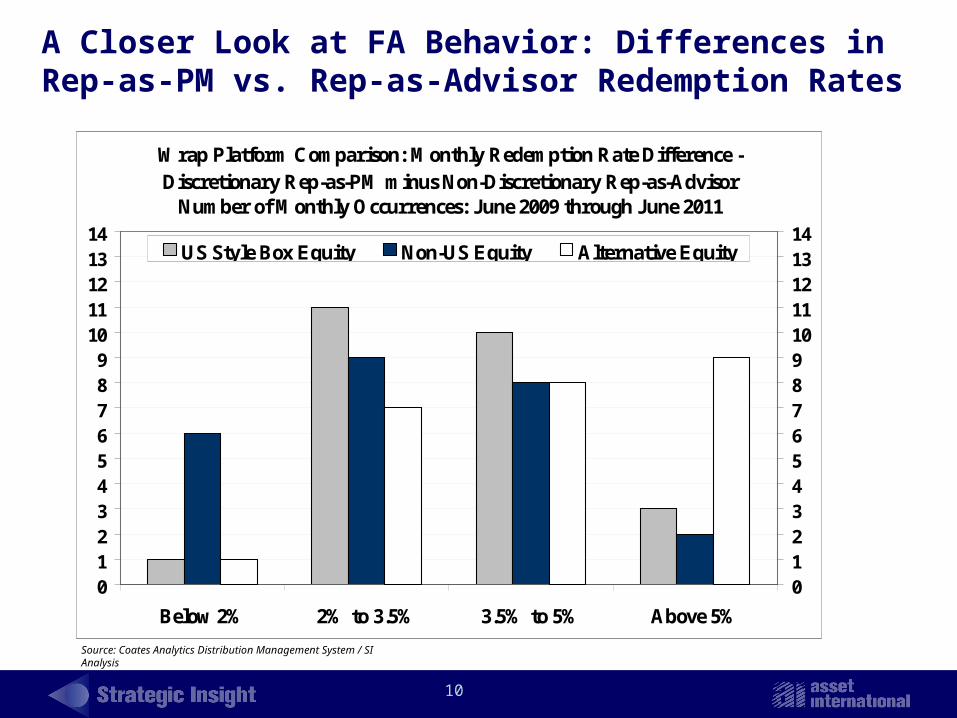

A Closer Look at FA Behavior: Differences in Rep-as-PM vs. Rep-as-Advisor Redemption Rates

Wrap Platform Comparison: Monthly Redemption Rate Difference -Discretionary Rep-as-PM minus Non-Discretionary Rep-as-Advisor

Number of Monthly Occurrences: June 2009 through June 2011

0123456789

1011121314

Below 2% 2% to 3.5% 3.5% to 5% Above 5%

01234567891011121314

US Style Box Equity Non-US Equity Alternative Equity

11

Source: Coates Analytics Distribution Management System / SI Analysis

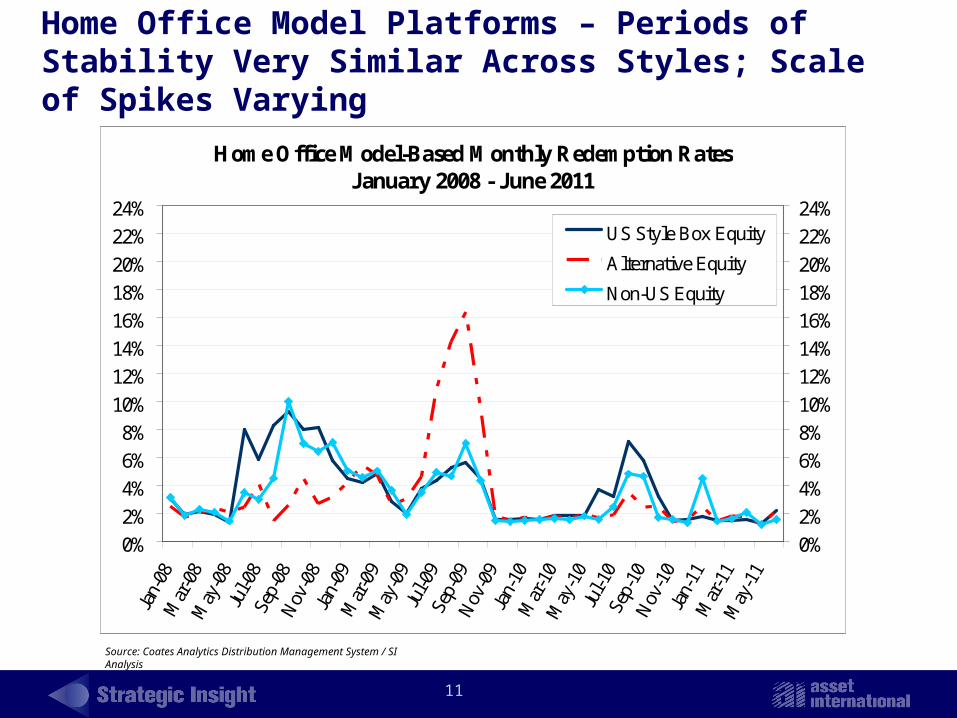

Home Office Model Platforms – Periods of Stability Very Similar Across Styles; Scale of Spikes Varying

Home Office Model-Based Monthly Redemption RatesJanuary 2008 - June 2011

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

Jan-

08M

ar-0

8M

ay-0

8Ju

l-08

Sep-

08N

ov-0

8Ja

n-09

Mar

-09

May

-09

Jul-0

9Se

p-09

Nov

-09

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep-

10N

ov-1

0Ja

n-11

Mar

-11

May

-11

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%US Style Box Equity

Alternative Equity

Non-US Equity

12

Source: Coates Analytics Distribution Management System / SI Analysis

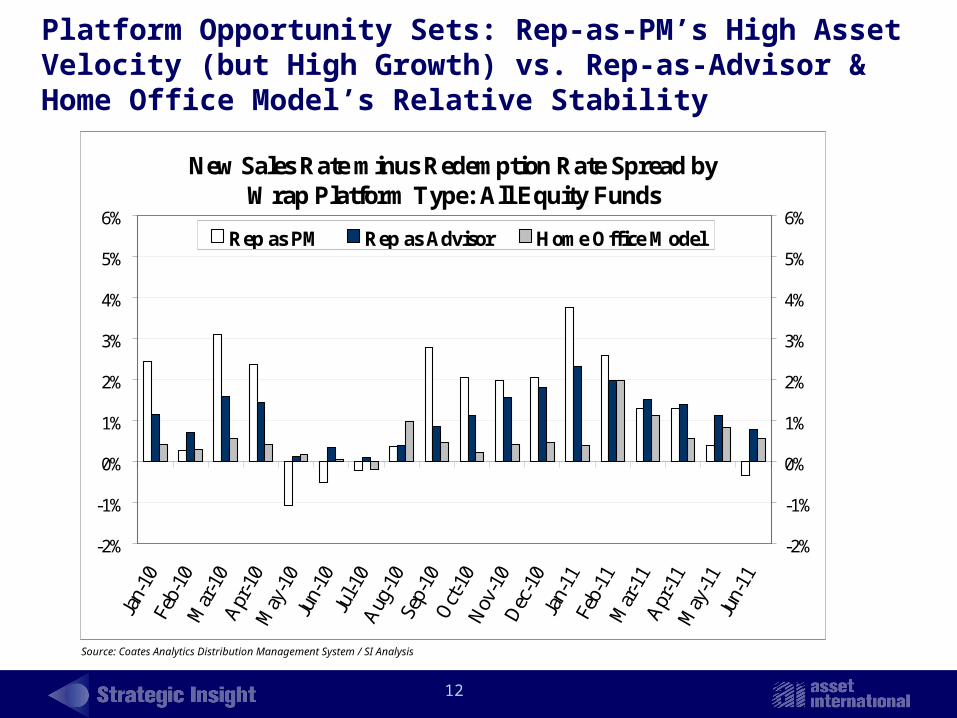

Platform Opportunity Sets: Rep-as-PM’s High Asset Velocity (but High Growth) vs. Rep-as-Advisor & Home Office Model’s Relative Stability

New Sales Rate minus Redemption Rate Spread by Wrap Platform Type: All Equity Funds

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Jan-

10Fe

b-10

Mar

-10

Apr

-10

May

-10

Jun-

10Ju

l-10

Aug

-10

Sep-

10O

ct-1

0N

ov-1

0D

ec-1

0Ja

n-11

Feb-

11M

ar-1

1A

pr-1

1M

ay-1

1Ju

n-11

-2%

-1%

0%

1%

2%

3%

4%

5%

6%Rep as PM Rep as Advisor Home Office Model

13

Source: Coates Analytics Distribution Management System / SI Analysis

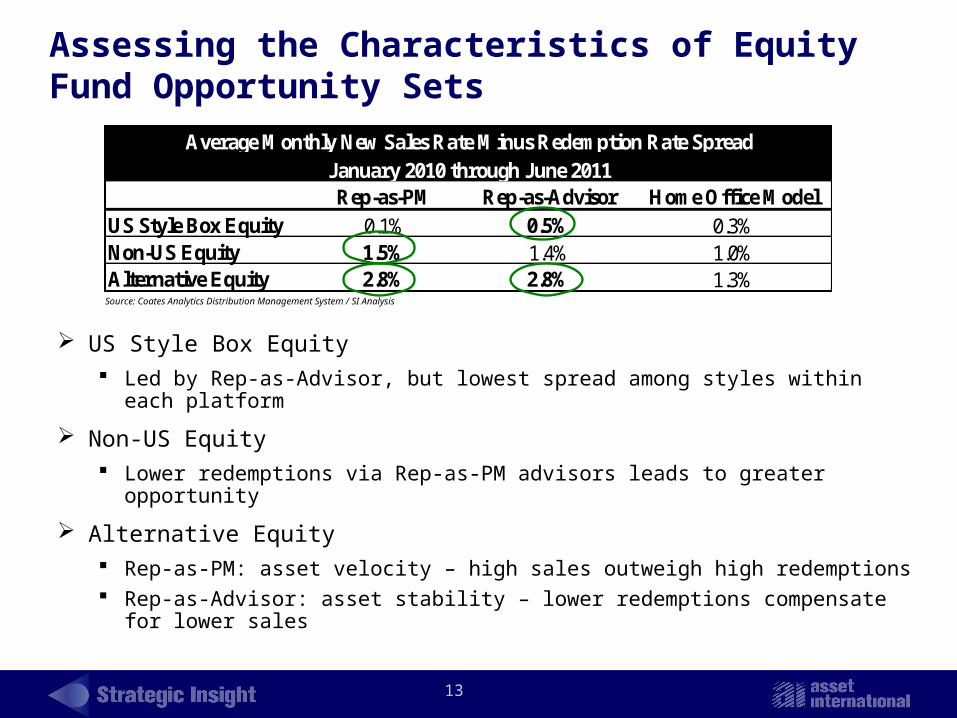

Assessing the Characteristics of Equity Fund Opportunity Sets

Rep-as-PM Rep-as-Advisor Home Office ModelUS Style Box Equity 0.1% 0.5% 0.3%Non-US Equity 1.5% 1.4% 1.0%Alternative Equity 2.8% 2.8% 1.3%

Average Monthly New Sales Rate Minus Redemption Rate SpreadJanuary 2010 through June 2011

US Style Box Equity Led by Rep-as-Advisor, but lowest spread among styles within each

platform

Non-US Equity Lower redemptions via Rep-as-PM advisors leads to greater opportunity

Alternative Equity Rep-as-PM: asset velocity – high sales outweigh high redemptions Rep-as-Advisor: asset stability – lower redemptions compensate for lower

sales

14

Implications Moving Forward

Expansion of fee-based advisory programs continues to bring higher asset velocity features to growing segments of fund business

Increasingly converse relationship between growth and asset stability within expanding segments of the FA-sold marketplace

Implications around product focus and development, sales force compensation, and other aspects of overall distribution strategy

Growing importance in analyzing holistic combination of new business and asset stability considerations

15

How Can Fund Firms Respond?

Aggregate redemption stats alarming, but Rep-as-PM advisors (and RIAs) can still represent valuable relationship opportunities

Influence of such advisors growing rapidly as trend toward greater FA discretion continues

High-net-worth client base

Increased importance of FA segmentation and targeting around both growth and asset stability considerations Particularly within high-velocity segments such as Rep-as-PM and RIA

Segments of these advisor bases with strong asset stability characteristics in your firm’s core strategies?

Ability to rethink / retool certain aspects of revenue sharing arrangements with key distribution partners?

Potential to tie payment levels more directly to redemption/holding period metrics?

Revenue sharing grid based on FA holding period?

16

© Copyright 2011 Strategic Insight, an Asset International company, and when referenced or sourced Coates Analytics, Morningstar Inc. and Lipper Inc. All rights reserved. The information, data, analyses and opinions contained herein (a) include confidential and proprietary information of the aforementioned companies, (b) are provided solely for information purposes, and (c) are not warranted or represented to be correct, complete, accurate, or timely. Past performance is no guarantee of future results. The aforementioned companies are not affiliated with each other.

This report has been prepared using information and sources we believe to be reliable; however,

we make no representation as to its accuracy, adequacy or completeness, nor do we assume responsibility for any errors or omissions or for any results obtained from the use of this report, including any action taken with respect to securities referred to in this report. Our employees may from time to time acquire, hold or sell a position in securities mentioned herein. We may from time to time perform services for any company mentioned in this report. This report is not a prospectus or representation intended to use in the purchase or sale of any securities mentioned in this report.

Strategic Insight is available by subscription and by single copy upon request to the publisher.

17

SI Research Services Already Used by Managers of 90% of U.S. Fund Industry Assets, B/D Distributors, Nearly All Key VA Providers, and Globally by over 100 Leading Managers, Distributors

Simfund, The World’s Databases for Mutual Fund Competitive Intelligence

Tracking ~ $25 Trillion: Flows, Innovations, and Much More

SIOnLine.com AnnuityInsight.com

StrategicInsightGlobal.com GlobalFundDistribution.com

FundInnovation.com

SimFundFiling.com

US Funds: [email protected] [email protected]@sionline.com [email protected]

15(c) and Board Research: [email protected], Subadvisory: [email protected] [email protected]

Global: [email protected] [email protected]