petronova inc.s1.q4cdn.com/071829534/files/q3 2011 mda fs_v001_d0kd3m.pdfpetronova inc....

TRANSCRIPT

PETRONOVA INC. MANAGEMENT’S DISCUSSION AND ANALYSIS

The following management’s discussion and analysis (“MD&A”) is a review of PetroNova Inc.’s (“PetroNova” or

the “Company”) financial condition and results of operations as at and for the three and nine month periods

ended September 30, 2011 and 2010. This MD&A has been prepared as at November 23, 2011 and should be

read in conjunction with the condensed interim consolidated financial statements of the Company as at and

for the three and nine months ended September 30, 2011 and 2010 and the audited consolidated financial

statements, related notes and MD&A as at and for the years ended December 31, 2010 and 2009. Additional

information relating to PetroNova, including the Company’s annual information form for the year ended

December 31, 2010 (the “Annual Information Form”), is available on SEDAR at www.sedar.com.

The condensed interim consolidated financial statements as at and for the three and nine months ended September 30, 2011 and 2010 and related notes have been prepared in accordance with International Financial Reporting Standards (“IFRS”), which are generally accepted accounting principles for publicly accountable enterprises in Canada. These condensed interim consolidated financial statements of the Company and its wholly owned subsidiaries, PetroNova International Inc. and PetroNova Colombia Inc. and its Colombian branch, have been prepared in accordance with International Accounting Standard (“IAS”) 34 Interim Financial Reporting. The condensed interim consolidated financial statements do not include all of the information required for full annual financial statements.

For the comparative periods presented (2010), the condensed interim consolidated financial statements include

the historical financial position, results of operations and cash flows of the assets and liabilities acquired by the

Company in June 2010 from the predecessor subsidiaries, which included direct and indirect wholly owned

subsidiaries of Inepetrol Corporation AB (the “Predecessor Subsidiaries”), in accordance with the continuity of

interest method of accounting.

Except as otherwise noted, all financial measures are expressed in United States dollars (U.S. dollars).

NON-IFRS MEASURES

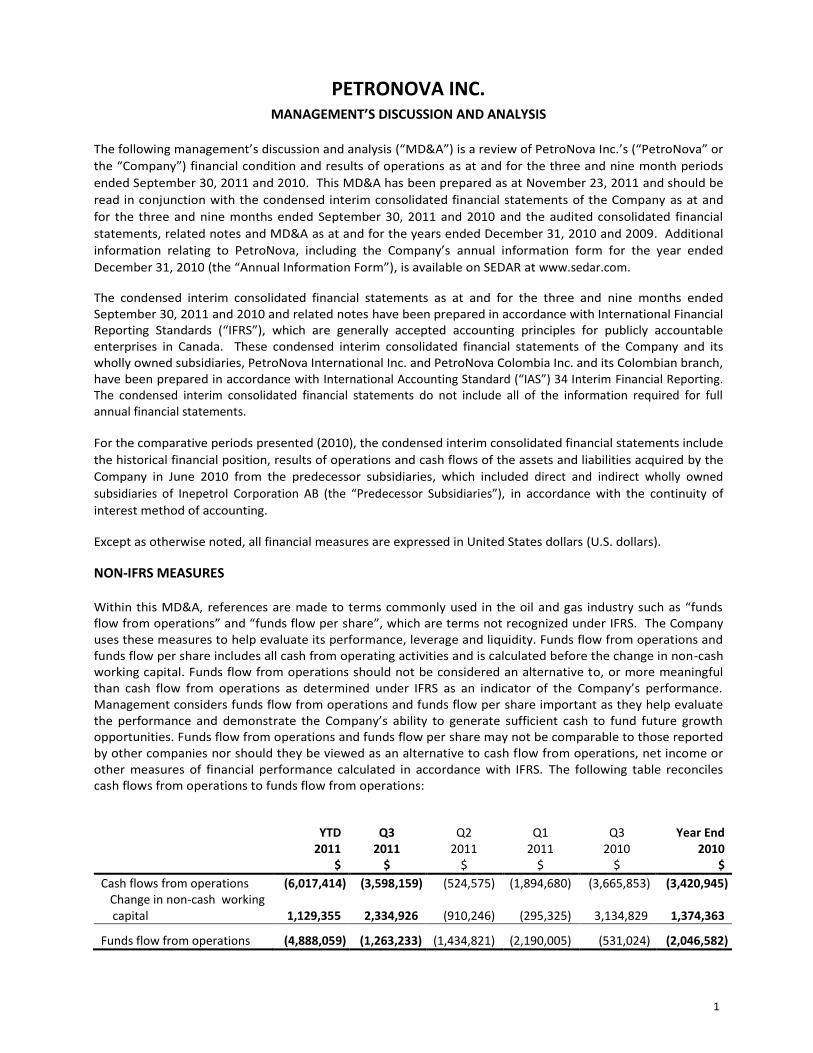

Within this MD&A, references are made to terms commonly used in the oil and gas industry such as “funds flow from operations” and “funds flow per share”, which are terms not recognized under IFRS. The Company uses these measures to help evaluate its performance, leverage and liquidity. Funds flow from operations and funds flow per share includes all cash from operating activities and is calculated before the change in non-cash working capital. Funds flow from operations should not be considered an alternative to, or more meaningful than cash flow from operations as determined under IFRS as an indicator of the Company’s performance. Management considers funds flow from operations and funds flow per share important as they help evaluate the performance and demonstrate the Company’s ability to generate sufficient cash to fund future growth opportunities. Funds flow from operations and funds flow per share may not be comparable to those reported by other companies nor should they be viewed as an alternative to cash flow from operations, net income or other measures of financial performance calculated in accordance with IFRS. The following table reconciles cash flows from operations to funds flow from operations:

YTD 2011

$

Q3 2011

$

Q2 2011

$

Q1 2011

$

Q3 2010

$

Year End 2010

$

Cash flows from operations (6,017,414) (3,598,159) (524,575) (1,894,680) (3,665,853) (3,420,945) Change in non-cash working

capital

1,129,355

2,334,926

(910,246)

(295,325)

3,134,829

1,374,363

Funds flow from operations (4,888,059) (1,263,233) (1,434,821) (2,190,005) (531,024) (2,046,582)

CAUTION REGARDING FORWARD-LOOKING INFORMATION

Certain statements contained in this MD&A constitute forward-looking statements. These statements relate to future events or the Company’s future performance. All statements other than statements of historical fact are forward-looking statements. The use of any of the words “anticipate”, “intend”, “plan”, “continue”, “estimate”, “budget”, “targeting”, “project”, “expect”, “may”, “will”, “might”, “should”, “could”, “believe”, “predict” and “potential” and similar expressions are intended to identify forward-looking statements. Such statements represent the Company’s internal projections, estimates, expectations, beliefs, plans, objectives, assumptions, intentions or statements about future events or performance. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. Management believes the expectations reflected in these forward-looking statements are reasonable but no assurance can be given that these expectations will prove to be correct and such forward-looking statements included in this MD&A should not be unduly relied upon. These statements speak only as of the date of this MD&A.

In particular, this MD&A contains forward-looking statements pertaining to the following: the Company’s business objectives and strategies; the Company’s intention to participate in future bid rounds in Colombia and elsewhere to acquire additional exploration acreage; the Company’s expected capital and exploration expenditures; the Company’s future exploration and development activities including the Company’s seismic acquisition and drilling plans; the Company’s plans for, and anticipated results of, exploration and development activities; the timing of commencement of certain of the Company’s operations; the source of funding for the Company’s activities and the Company’s ability to raise capital; future liquidity and future financial resources; contractual commitments pertaining to the Colombian Blocks (as defined herein); the Company’s dependence on third party operators and key personnel; the expected impact of new accounting policies; the Company’s interest rate, credit, foreign exchange, liquidity and market risks management activities; and the Company’s treatment under governmental regulatory regimes and tax laws. In addition, statements in this MD&A relating to “resources” and “reserves” are deemed to be forward-looking statements as they involve the implied assessment, based on certain estimates and assumptions, that the resources and reserves described exist in the quantities predicted or estimated, and that the resources and reserves described can be profitably produced in the future.

With respect to forward-looking statements contained in this MD&A, assumptions have been made regarding, among other things: general economic, market and business conditions in Colombia and globally; future crude oil and natural gas prices; the continued availability of capital, undeveloped lands and skilled personnel; the ability to obtain equipment in a timely manner to carry out exploration and development activities; the regulatory framework governing royalties, taxes and environmental matters in Colombia and any other jurisdictions in which the Company may conduct its business in the future; the ability of the Company to obtain the necessary approvals, permits and licences to conduct its operations; the applicability of technologies for recovery and production of the Company’s oil and natural gas resources; the recoverability of the Company’s oil and gas resources; future capital and exploration expenditures to be made by the Company; future sources of funding for the Company’s exploration program; the Company’s future debt levels; the geography of the areas in which the Company is exploring; adequate weather and environmental conditions; the impact of increasing competition on the Company; and the Company’s ability to obtain financing on acceptable terms.

Actual results could differ materially from those anticipated in these forward-looking statements as a result of the risk factors outlined below and elsewhere in PetroNova’s continuous disclosure documents, including: general economic, market and business conditions; volatility in market prices for crude oil and natural gas and hedging activities related thereto; risks related to the exploration, development and production of oil and natural gas; risks inherent in the Company’s international operations, including security and legal risks in Colombia; risks related to the timing of completion of the Company’s projects; competition for, among other things, capital, the acquisition of resources and skilled personnel; actions by governmental authorities, including changes in government regulation and taxation; the failure of the Company to obtain the necessary approvals, permits and licences to conduct its operations; environmental risks and hazards; risks inherent in the exploration, development and production of oil and natural gas which may create liabilities to the Company in excess of the Company’s insurance coverage, if any; failure to accurately estimate and to establish adequate cash reserves for abandonment and reclamation costs; the availability of capital on acceptable terms; political risks; the failure of the Company or the holder of certain licenses or leases to meet specific requirements of such licenses or leases; adverse claims made in respect of the Company’s properties or assets; failure to engage or retain key personnel; uncertainties inherent in estimating quantities of oil and natural gas reserves and resources; failure to acquire or develop oil and natural gas resources and reserves; geological, technical, drilling and processing problems, including the availability of equipment and access to properties; failure by counterparties to make payments or perform their operational or other obligations to the Company in compliance with the terms of contractual arrangements between the Company and such counterparties; current global financial conditions, including fluctuations in interest rates, foreign exchange rates and stock market volatility; and the other factors discussed under the headings “Risk Factors” in the Annual Information Form and the Company’s other continuous disclosure documents filed from time to time with applicable securities regulatory authorities in Canada.

Readers are cautioned that the foregoing lists of factors are not exhaustive. The forward-looking statements included in this MD&A are expressly qualified by this cautionary statement and are made as of the date of this MD&A. The Company does not undertake any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws.

BUSINESS PROFILE

The Company, through its subsidiaries, is engaged in the exploration, acquisition and development of, oil and natural gas resources in South America, specifically in Colombia. The Company’s assets currently include various participating interests in five Colombian Blocks. The Colombian Blocks consist of the Putumayo 2 block (the “PUT-2 Block”) and the Tinigua block (the “Tinigua Block”) located in the Caguan-Putumayo Basin, both of which are operated by the Company, and the non-operated CPO-6, CPO-7 and CPO-13 blocks located in the Llanos Basin (the “Llanos Blocks”). The PUT-2 Block, the Tinigua Block and the Llanos Blocks are collectively referred to herein as the “Colombian Blocks”.

BUSINESS STRATEGY IN COLOMBIA

PetroNova’s business objective is to build a diversified oil and gas exploration and production company, initially focused on Colombia, with a view to expanding into additional countries in the future. The Company’s strategy is to develop its existing portfolio of assets and to pursue further exploration opportunities in areas with proven hydrocarbon systems that the Company considers to be cost-effective and of low to moderate risk.

In addition, the Company will continue to evaluate strategic acquisition or business combination opportunities of oil and natural gas companies or properties from time to time where it believes further exploration and development opportunities exist. To this effect, the Company may participate in future bid rounds in Colombia and elsewhere to acquire additional exploration acreage. The Company hopes to generate returns for its shareholders, principally through capital growth, and intends to take advantage of opportunities to acquire acreage and prospects suitable for exploration and development.

The Company has established the following fundamental guidelines pursuant to which the Company evaluates the selection and participation in new areas in an attempt to mitigate the geological risk inherent to high potential exploration:

• the presence of a proven hydrocarbon system in the area is known; • the existence and availability of technical information allows preliminary evaluations; • the proximity to existing or underdeveloped infrastructure will allow the shipment of oil and gas; and • the economics are attractive under conservative price forecasts.

COMMITMENTS

At September 30, 2011, according to provisions of agreements with the ANH and others, the Company has estimated the following commitments:

Remaining 2011

$

2012

$

2013

$

Total

$

Tinigua Block (Phase 1) 5,683,647 3,681,350 - 9,364,997

PUT-2 Block (Phase 1) 1,249,183 9,135,553 - 10,384,736

Llanos Blocks (Phase 1) 2,490,514 9,444,835 - 11,935,349

Finance Lease obligation 5,997 28,175 8,263 42,435

Total 9,429,341 22,289,913 8,263 31,727,517

The E&P Contracts with the ANH are subject to a sliding scale royalty rate on oil and gas production. The E&P Contracts for the PUT-2, CPO-6, CPO-7 and CPO-13 Blocks are also subject to additional rights payable to the ANH of 1%, 39%, 47%, and 32%, respectively.

The expenditures provided in the above table represent the estimated costs to complete contracted requirements. The company updated its estimations during the three month period ended September 30, 2011. Actual expenditures to satisfy these commitments may differ significantly from these estimates.

On July 21, 2011, the ANH extended the term of phase one of the exploratory period for the Tinigua block to January 22, 2012. On October 24, 2011, a new request for an additional five months extension was submitted to ANH and is pending for approval.

On October 4, 2011 the ANH extended the term of phase 1 of the exploratory period for block CPO-13 to July 13, 2014. Requests for a 12 month extension for phase 1 on CPO-6 and CPO-7 were submitted to the ANH and are pending for approval. Even though these contractual extensions have been requested, current plans are conducted to complete all obligations under current contractual terms.

In addition, the Company has the following commitments over the next five years relating to office and apartment leases and other commitments:

2011 204,764

2012 391,587

2013 189,150

2014 10,126

2015 10,126

The Company plans to fulfill its commitments by using its current balances held as cash and cash equivalents.

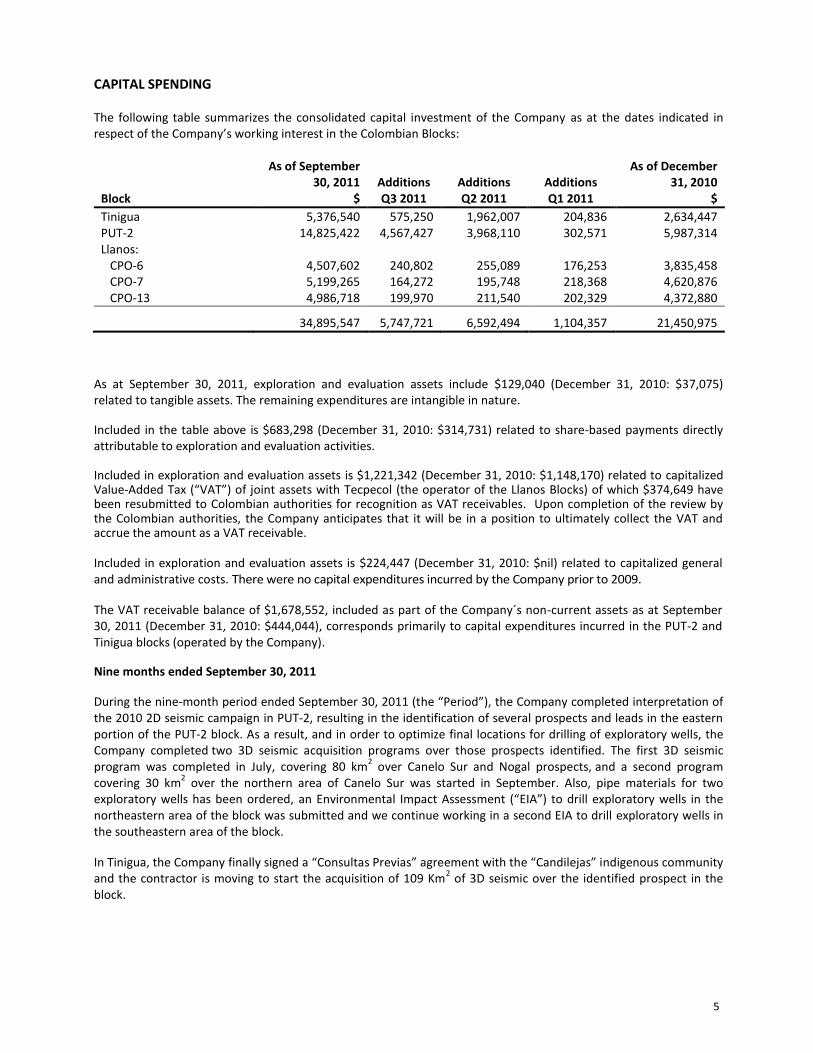

CAPITAL SPENDING

The following table summarizes the consolidated capital investment of the Company as at the dates indicated in respect of the Company’s working interest in the Colombian Blocks:

Block

As of September 30, 2011

$

Additions Q3 2011

Additions Q2 2011

Additions Q1 2011

As of December 31, 2010

$

Tinigua 5,376,540 575,250 1,962,007 204,836 2,634,447 PUT-2 14,825,422 4,567,427 3,968,110 302,571 5,987,314 Llanos: CPO-6 4,507,602 240,802 255,089 176,253 3,835,458 CPO-7 5,199,265 164,272 195,748 218,368 4,620,876 CPO-13 4,986,718 199,970 211,540 202,329 4,372,880

34,895,547 5,747,721 6,592,494 1,104,357 21,450,975

As at September 30, 2011, exploration and evaluation assets include $129,040 (December 31, 2010: $37,075) related to tangible assets. The remaining expenditures are intangible in nature.

Included in the table above is $683,298 (December 31, 2010: $314,731) related to share-based payments directly attributable to exploration and evaluation activities.

Included in exploration and evaluation assets is $1,221,342 (December 31, 2010: $1,148,170) related to capitalized Value-Added Tax (“VAT”) of joint assets with Tecpecol (the operator of the Llanos Blocks) of which $374,649 have been resubmitted to Colombian authorities for recognition as VAT receivables. Upon completion of the review by the Colombian authorities, the Company anticipates that it will be in a position to ultimately collect the VAT and accrue the amount as a VAT receivable.

Included in exploration and evaluation assets is $224,447 (December 31, 2010: $nil) related to capitalized general and administrative costs. There were no capital expenditures incurred by the Company prior to 2009.

The VAT receivable balance of $1,678,552, included as part of the Company´s non-current assets as at September 30, 2011 (December 31, 2010: $444,044), corresponds primarily to capital expenditures incurred in the PUT-2 and Tinigua blocks (operated by the Company).

Nine months ended September 30, 2011

During the nine-month period ended September 30, 2011 (the “Period”), the Company completed interpretation of the 2010 2D seismic campaign in PUT-2, resulting in the identification of several prospects and leads in the eastern portion of the PUT-2 block. As a result, and in order to optimize final locations for drilling of exploratory wells, the Company completed two 3D seismic acquisition programs over those prospects identified. The first 3D seismic program was completed in July, covering 80 km

2 over Canelo Sur and Nogal prospects, and a second program

covering 30 km2 over the northern area of Canelo Sur was started in September. Also, pipe materials for two

exploratory wells has been ordered, an Environmental Impact Assessment (“EIA”) to drill exploratory wells in the northeastern area of the block was submitted and we continue working in a second EIA to drill exploratory wells in the southeastern area of the block.

In Tinigua, the Company finally signed a “Consultas Previas” agreement with the “Candilejas” indigenous community and the contractor is moving to start the acquisition of 109 Km

2 of 3D seismic over the identified prospect in the

block.

In Los Llanos Blocks, the Company continues the interpretation of more than 2,000 km of 2D seismic acquired in 2010, resulting in the identification of several ready-to-drill prospects and additional leads. The environmental licence to drill several exploratory wells in CPO-6 was obtained and a rig has been contracted to drill 3 exploratory wells in CPO-6, 3 exploratory wells in CPO-7 and 3 exploratory wells in CPO-13. The construction of drilling locations in CPO-6 started and materials have been ordered. In CPO-7 and CPO-13 we adjusted the EIA´s according to the comments received from Environmental Ministry and we expect to receive approval for environmental licenses in the near future to commence construction of drilling locations and drilling of exploratory wells.

In addition, prior to the interpretation of recently acquired 3D seismic data in PUT-2, our Independent Engineer (Petrotech Engineering) updated the Company´s prospective resources estimate, resulting in a total increase of 63% in the blocks subject to revision (PUT-2 and Los Llanos). The results are summarized in the table below:

Blocks***

Unrisked prospective resources – Best case (mmbls) Risked prospective resources – Best case (mmbls)

2010* 2011** Variance 2010* 2011** Variance

PUT-2 (100% W.I.) 53.4 75.5 41.4 % 16.2 22.5 38.6%

CPO-6 (20% W.I.) 2.0 4.5 124.5% 0.6 1.3 120.0%

CPO-7 (20% W.I.) 6.9 21.2 206.7% 2.0 7.0 249.5%

CPO-13 (20% W.I.) 7.6 13.2 73.0% 1.6 5.4 236.9%

Sub-total 69.9 114.3 63.5% 20.4 36.2 77.3%

Tinigua (90% W.I.) 177.1 177.1 N/A 64.1 64.1 N/A

Total net resources 247.0 291.4 18.0% 84.5 100.3 18.7%

* Independent engineer report (Petrotech Engineering Ltd.) issued April 30, 2010 ** Independent engineer report (Petrotech Engineering Ltd.) issued September 8, 2011 *** PetroNova’s working interest (W.I.) share before deduction of royalties

Subsequent to September 30, 2011

The Company has:

Completed the construction of two CPO-6 well locations

Obtained the Environmental license to drill up to 5 exploration wells in CPO-7

Completed the “Consultas Previas” process with “El Tigre” indigenous community in the CPO-13 block

Completed the acquisition of 30 Km2 of 3D seismic in the North region of Canelo Sur prospect of the PUT-2

block and received most of the pipe materials required to drill two exploratory wells.

OUTLOOK

In the PUT-2 Block, the Company plans to complete processing and interpretation of the recently acquired 3D seismic data to define final well locations, obtain the required environmental licenses and drill two (2) exploratory wells in 2012.

In the Tinigua Block, the Company plans to complete the acquisition of 109 km2 of 3D seismic data, submit an EIA to

drill exploratory and outpost wells and start drilling during the second half of 2012.

In the Llanos Blocks, the Company plans to commence a drilling campaign of nine (9) exploratory wells in December 2011 (three wells for each block), starting with CPO-6, and continuing throughout 2012. Depending on the results obtained from those exploratory wells, the Company would continue drilling of appraisal and/or additional exploratory wells throughout the end of 2012.

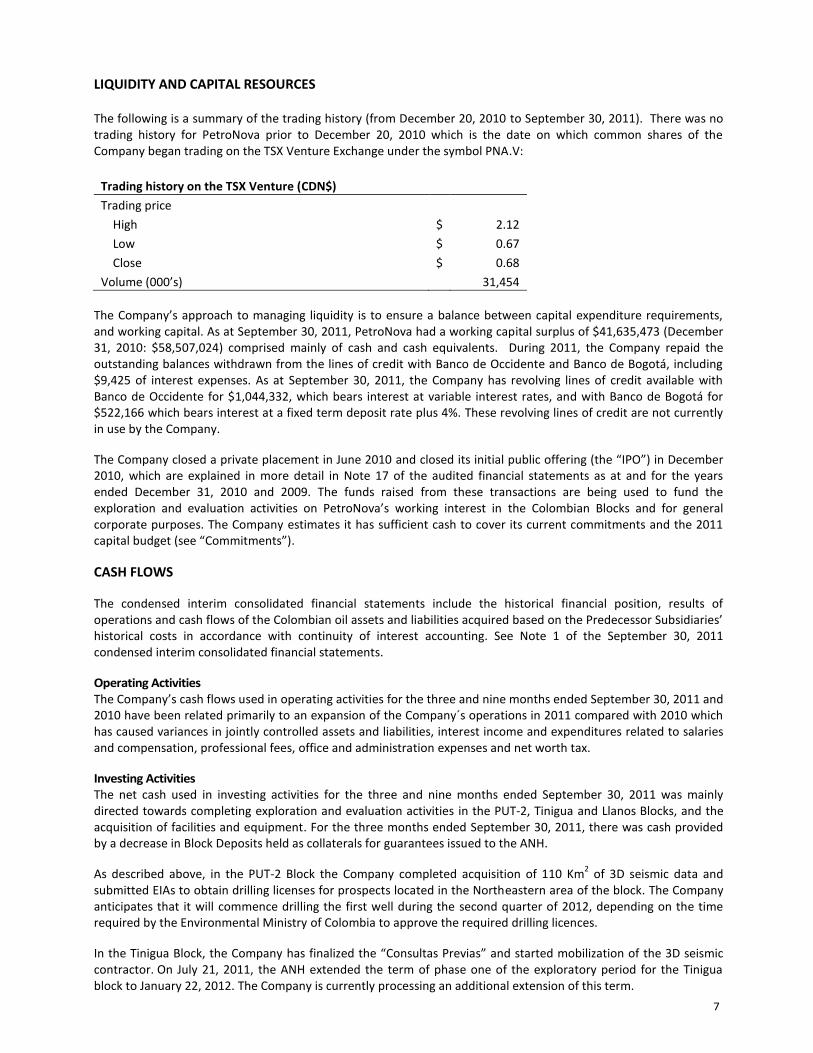

LIQUIDITY AND CAPITAL RESOURCES

The following is a summary of the trading history (from December 20, 2010 to September 30, 2011). There was no trading history for PetroNova prior to December 20, 2010 which is the date on which common shares of the Company began trading on the TSX Venture Exchange under the symbol PNA.V:

Trading history on the TSX Venture (CDN$)

Trading price

High $ 2.12

Low $ 0.67

Close $ 0.68

Volume (000’s) 31,454

The Company’s approach to managing liquidity is to ensure a balance between capital expenditure requirements, and working capital. As at September 30, 2011, PetroNova had a working capital surplus of $41,635,473 (December 31, 2010: $58,507,024) comprised mainly of cash and cash equivalents. During 2011, the Company repaid the outstanding balances withdrawn from the lines of credit with Banco de Occidente and Banco de Bogotá, including $9,425 of interest expenses. As at September 30, 2011, the Company has revolving lines of credit available with Banco de Occidente for $1,044,332, which bears interest at variable interest rates, and with Banco de Bogotá for $522,166 which bears interest at a fixed term deposit rate plus 4%. These revolving lines of credit are not currently in use by the Company.

The Company closed a private placement in June 2010 and closed its initial public offering (the “IPO”) in December 2010, which are explained in more detail in Note 17 of the audited financial statements as at and for the years ended December 31, 2010 and 2009. The funds raised from these transactions are being used to fund the exploration and evaluation activities on PetroNova’s working interest in the Colombian Blocks and for general corporate purposes. The Company estimates it has sufficient cash to cover its current commitments and the 2011 capital budget (see “Commitments”).

CASH FLOWS

The condensed interim consolidated financial statements include the historical financial position, results of operations and cash flows of the Colombian oil assets and liabilities acquired based on the Predecessor Subsidiaries’ historical costs in accordance with continuity of interest accounting. See Note 1 of the September 30, 2011 condensed interim consolidated financial statements.

Operating Activities The Company’s cash flows used in operating activities for the three and nine months ended September 30, 2011 and 2010 have been related primarily to an expansion of the Company´s operations in 2011 compared with 2010 which has caused variances in jointly controlled assets and liabilities, interest income and expenditures related to salaries and compensation, professional fees, office and administration expenses and net worth tax.

Investing Activities The net cash used in investing activities for the three and nine months ended September 30, 2011 was mainly directed towards completing exploration and evaluation activities in the PUT-2, Tinigua and Llanos Blocks, and the acquisition of facilities and equipment. For the three months ended September 30, 2011, there was cash provided by a decrease in Block Deposits held as collaterals for guarantees issued to the ANH.

As described above, in the PUT-2 Block the Company completed acquisition of 110 Km2 of 3D seismic data and

submitted EIAs to obtain drilling licenses for prospects located in the Northeastern area of the block. The Company anticipates that it will commence drilling the first well during the second quarter of 2012, depending on the time required by the Environmental Ministry of Colombia to approve the required drilling licences.

In the Tinigua Block, the Company has finalized the “Consultas Previas” and started mobilization of the 3D seismic contractor. On July 21, 2011, the ANH extended the term of phase one of the exploratory period for the Tinigua block to January 22, 2012. The Company is currently processing an additional extension of this term.

In the CPO-06 Block, the Company continues the interpretation of the 600 km 2D seismic acquired in 2010 and is ready to commence drilling of three exploratory wells starting in December 2011.

In the CPO-07 Block, the Company continues the interpretation of 729 km 2D seismic acquired and has submitted updated EIAs for the approval of environmental license to drill three exploratory wells.

In the CPO-13 Block, the Company continues the interpretation of 679 km 2D seismic and has submitted updated EIAs for the approval of environmental license to drill three exploratory wells. Consultas Previas with the “El Tigre” indigenous community have been finalized and the acquisition of the remaining 2D seismic lines is expected to start in 2011.

During 2011, the ANH requested the Company to increase the Llanos Blocks´ guarantees and then agreed to reduce them to their current levels.

Financing Activities Cash used in financing activities for the three and nine months ended September 30, 2011 and 2010 is primarily related to repayment of bank indebtedness and payments to related parties and financial leases.

OFF-BALANCE SHEET ARRANGEMENTS

The Company does not have any off-balance sheet arrangements.

NO SIGNIFICANT REVENUE

The Company is currently in the exploration and evaluation phase and, therefore, has not generated significant revenue to date. The information related to amounts capitalized and expensed for exploration and development costs and general and administrative expenses is disclosed in the condensed interim consolidated financial statements as at and for the nine month period ended September 30, 2011 and other sections of this document.

SELECTED QUARTERLY INFORMATION

The following table sets out selected quarterly financial information of PetroNova since its inception and is derived from quarterly financial data prepared by management in accordance with IFRS:

2011

2010

2009

($ except for per-share amounts) Q3 Q2 Q1 Q4 Q3 Q2 Q1 Q4 Revenues 99,175 77,012 81,655 23,586 56,032 44,400 44,400 55,900

Net income (loss) (1,379,449) (1,503,962) (2,755,894) (2,392,785) (635,918) (1,552,330) 280,751 50,357

Income (loss) per share – basic and diluted (0.01) (0.01) (0.02) (0.02) (0.01) (0.66) 280.75 174.85

Weighted average shares outstanding – basic and diluted 165,301,302 165,301,302 165,301,302 119,209,867 112,781,302 2,369,798 1,000 288

Working capital 41,635,473 46,479,990 50,110,297 58,507,024 151,279 6,375,971 (12,118,959)

(12,080,946)

Exploration and evaluation assets 34,895,547 29,147,826 22,555,332 21,450,975 17,763,844 13,498,686 3,731,503 3,731,503

Block deposits 5,124,983 8,009,853 13,191,427 7,913,610 7,792,350 7,728,800 7,728,800 7,728,800

Total assets 86,452,411 89,688,617 89,578,291 91,350,206 29,340,984 31,442,756 19,275,750 11,795,379

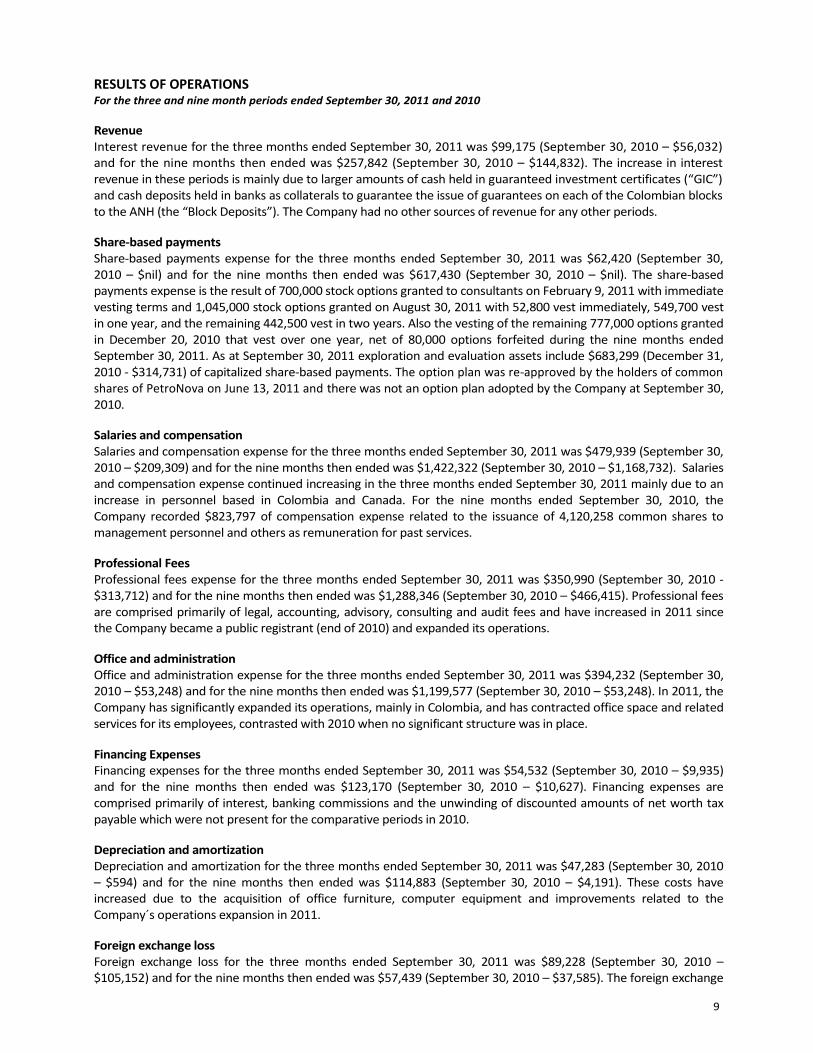

RESULTS OF OPERATIONS For the three and nine month periods ended September 30, 2011 and 2010

Revenue Interest revenue for the three months ended September 30, 2011 was $99,175 (September 30, 2010 – $56,032) and for the nine months then ended was $257,842 (September 30, 2010 – $144,832). The increase in interest revenue in these periods is mainly due to larger amounts of cash held in guaranteed investment certificates (“GIC”) and cash deposits held in banks as collaterals to guarantee the issue of guarantees on each of the Colombian blocks to the ANH (the “Block Deposits”). The Company had no other sources of revenue for any other periods.

Share-based payments Share-based payments expense for the three months ended September 30, 2011 was $62,420 (September 30, 2010 – $nil) and for the nine months then ended was $617,430 (September 30, 2010 – $nil). The share-based payments expense is the result of 700,000 stock options granted to consultants on February 9, 2011 with immediate vesting terms and 1,045,000 stock options granted on August 30, 2011 with 52,800 vest immediately, 549,700 vest in one year, and the remaining 442,500 vest in two years. Also the vesting of the remaining 777,000 options granted in December 20, 2010 that vest over one year, net of 80,000 options forfeited during the nine months ended September 30, 2011. As at September 30, 2011 exploration and evaluation assets include $683,299 (December 31, 2010 - $314,731) of capitalized share-based payments. The option plan was re-approved by the holders of common shares of PetroNova on June 13, 2011 and there was not an option plan adopted by the Company at September 30, 2010.

Salaries and compensation Salaries and compensation expense for the three months ended September 30, 2011 was $479,939 (September 30, 2010 – $209,309) and for the nine months then ended was $1,422,322 (September 30, 2010 – $1,168,732). Salaries and compensation expense continued increasing in the three months ended September 30, 2011 mainly due to an increase in personnel based in Colombia and Canada. For the nine months ended September 30, 2010, the Company recorded $823,797 of compensation expense related to the issuance of 4,120,258 common shares to management personnel and others as remuneration for past services.

Professional Fees Professional fees expense for the three months ended September 30, 2011 was $350,990 (September 30, 2010 - $313,712) and for the nine months then ended was $1,288,346 (September 30, 2010 – $466,415). Professional fees are comprised primarily of legal, accounting, advisory, consulting and audit fees and have increased in 2011 since the Company became a public registrant (end of 2010) and expanded its operations.

Office and administration Office and administration expense for the three months ended September 30, 2011 was $394,232 (September 30, 2010 – $53,248) and for the nine months then ended was $1,199,577 (September 30, 2010 – $53,248). In 2011, the Company has significantly expanded its operations, mainly in Colombia, and has contracted office space and related services for its employees, contrasted with 2010 when no significant structure was in place.

Financing Expenses Financing expenses for the three months ended September 30, 2011 was $54,532 (September 30, 2010 – $9,935) and for the nine months then ended was $123,170 (September 30, 2010 – $10,627). Financing expenses are comprised primarily of interest, banking commissions and the unwinding of discounted amounts of net worth tax payable which were not present for the comparative periods in 2010.

Depreciation and amortization Depreciation and amortization for the three months ended September 30, 2011 was $47,283 (September 30, 2010 – $594) and for the nine months then ended was $114,883 (September 30, 2010 – $4,191). These costs have increased due to the acquisition of office furniture, computer equipment and improvements related to the Company´s operations expansion in 2011.

Foreign exchange loss Foreign exchange loss for the three months ended September 30, 2011 was $89,228 (September 30, 2010 – $105,152) and for the nine months then ended was $57,439 (September 30, 2010 – $37,585). The foreign exchange

loss arose primarily as a result of translating assets and liabilities denominated in Colombian pesos and Canadian dollars to the Company`s presentation currency of U.S. dollars.

Net worth tax expense Net worth tax expense for the three months ended September 30, 2011 was $nil (September 30, 2010 – $nil) and $1,073,980 for the nine months ended September 30, 2011 (September 30, 2010 – $nil). The net worth tax is based on the Company’s net worth in Colombia at January 1, 2011 and is payable in eight equal installments between 2011 and 2014. The amount recognized is calculated by discounting the future net worth tax payments by the Colombian risk-free interest rate.

Net Loss, Total Comprehensive Loss and Funds Flow from Operations For the three months ended September 30, 2011 and 2010, the Company generated a net loss of $1,379,449 ($0.01 loss per share) and $635,918 ($0.01 per share), respectively, and a total comprehensive loss of $1,536,097 and $605,674 for the same periods.

For the nine months ended September 30, 2011 and 2010, the Company generated a net loss of $5,639,305 ($0.03 loss per share) $1,595,966 ($0.04 loss per share), respectively, and a total comprehensive loss of $5,994,518 and $1,635,029 for the same periods.

For the three and nine months ended September 30, 2011, the Company generated negative funds flow from operations of $1,263,233 (September 30, 2010 - $531,024) and $4,888,059 (September 30, 2010 - $731,245), respectively. Negative funds flow from operations per share was $0.01 (September 30, 2010 - $0.005) and $0.03 (September 30, 2010 - $0.02) for the same periods.

RELATED PARTY TRANSACTIONS

Related Parties The consolidated interim financial statements of the Company disclose transactions with the related parties listed in the following table:

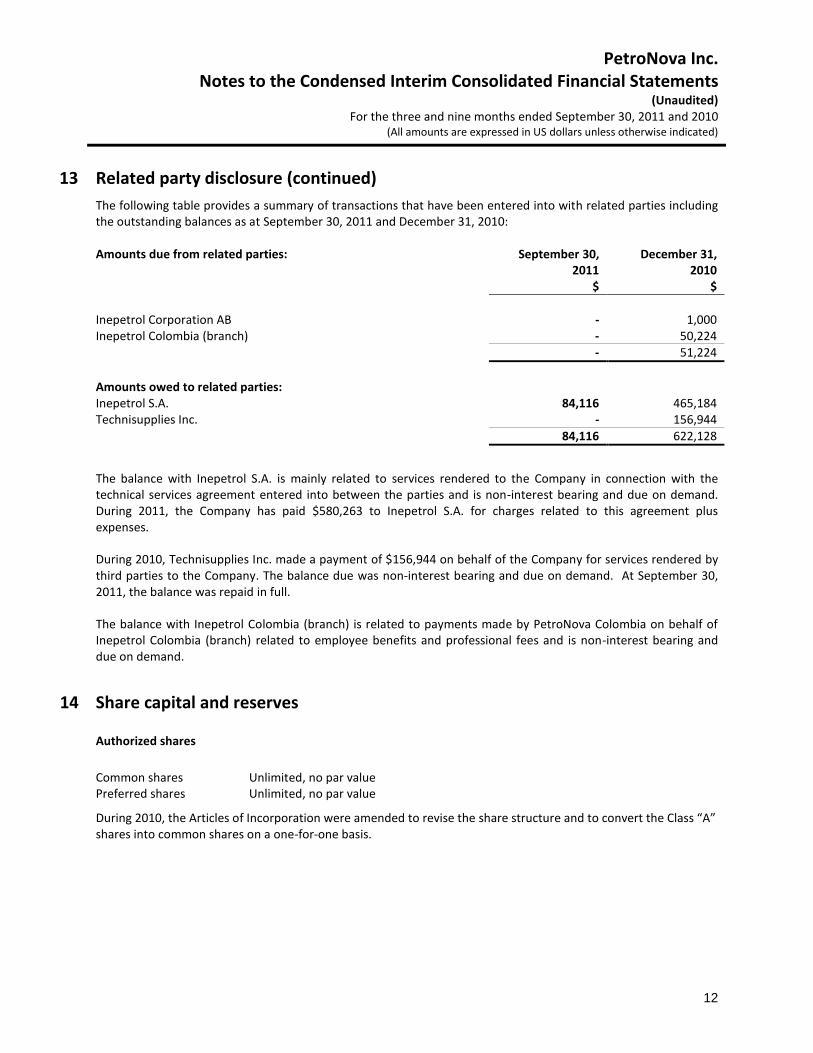

The following table provides a summary of transactions that have been entered into with related parties including the outstanding balances as at September 30, 2011 and December 31, 2010:

Amounts due from related parties:

September 30,

2011 $

December 31,

2010 $

Inepetrol Corporation AB - 1,000 Inepetrol Colombia (branch) - 50,224

- 51,224

Amounts owed to related parties: Inepetrol S.A. 84,116 465,184 Technisupplies Inc. - 156,944

84,116 622,128

Name Country of incorporation

Relationship

Inepetrol Corporation AB Sweden Common Shareholders Inepetrol S.A. Venezuela Common Shareholders Inepetrol Colombia (branch) Colombia Common Shareholders Technisupplies Inc. British Virgin Islands Common Shareholders

The balance with Inepetrol S.A. is mainly related to services rendered to the Company in connection with the technical services agreement entered into between the parties and is non-interest bearing and due on demand. During the year 2011, the Company has paid $580,263 to Inepetrol S.A. for charges related to this agreements plus expenses.

During 2010, Technisupplies Inc. made a payment of $156,944 on behalf of the Company for professional services rendered by third parties to the Company. The balance due was non-interest bearing and due on demand. At September 30, 2011, the balance was repaid in full.

The balance with Inepetrol Colombia (branch) is related to payments made by PetroNova Colombia Inc. on behalf of Inepetrol Colombia (branch) related to employee benefits and professional fees and is non-interest bearing and due on demand.

All transactions with related parties are made at fair value.

ACCOUNTING POLICIES

Certain new standards, interpretations, amendments and improvements to existing standards were issued by the International Accounting Standards Board (“IASB”) or International Financial Reporting Interpretations Committee (“IFRIC”) that are mandatory for accounting periods beginning after January 1, 2011 or later periods. The standards that may have an impact to the Company are as follows:

IAS 24 - Related party disclosure – revised definition of related parties

The new IAS 24 requires entities to disclose in their financial statements information about transactions with related parties. IAS 24 has simplified the definition of related party and removed certain disclosures required by the predecessor standard. The adoption of this amendment has had no effect on the financial position or the performance of the Company.

IAS 32 - Financial Instruments: Presentation (Amendment)

The amendment alters the definition of a financial liability in IAS 32 to enable entities to classify rights issues and certain options or warrants as equity instruments. The amendment is applicable if the rights are given pro rata to all of the existing owners of the same class of an entity’s non-derivative equity instruments, to acquire a fixed number of the entity’s own equity instruments for a fixed amount in any currency. The amendment has had no effect on the financial position or performance of the Company.

Improvements to IFRSs (issued May 2010)

In May 2010, the IASB issued its third omnibus of amendments to its standards, primarily with a view to removing inconsistencies and clarifying wording. There are separate transitional provisions for each standard. The following improvements did not have any impact on the accounting policies, financial position or performance of PetroNova:

IFRS 3 – Business Combinations: included different changes mainly related to contingent consideration arrangements, measurement of non-controlling interests and applicability of the IFRS 3 guidance to share-based payments in a business combination.

IFRS 7 – Financial Instruments – Disclosures: the amendment was intended to simplify the disclosures provided by reducing the volume of disclosures around collateral held and improving disclosures by requiring qualitative information to put the quantitative information in context.

IAS 27 – Consolidated and Separate Financial Statements: the consequential amendments to IAS 21, IAS 28 and IAS 31 resulting from the 2008 revisions to IAS 27 are to be applied prospectively.

In addition, the Company has considered the following improvements:

IAS 1 – Presentation of Financial Statements: Entities may present either in the statement of changes in equity or within the notes and analysis of the components of other comprehensive income by item. Impact analysis: since the cumulative foreign currency translation is the only item included in other comprehensive income, the Company has

disclosed this fact. This change has been included in Note 14 to the interim consolidated financial statements as at and for the three and nine months ended September 30, 2011.

IAS 34 – Interim Financial Reporting: Greater emphasis has been placed on the disclosure principles in IAS 34 involving significant events and transactions, including changes to fair value measurements, and the need to update relevant information from the most recent annual report. Impact analysis: the Company has considered these additional requirements in its interim consolidated financial statements as at and for the three and nine months ended September 30, 2011.

New standards and amendments not yet applicable:

IFRS 9 - Financial Instruments: issued in October 2010, is the first phase in the replacement of IAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 revises the current multiple classification and measurement models for financial assets and liabilities and limits the models to two: amortized cost or fair value. The new standard is effective for the Company’s interim and annual financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements.

IFRS 10 - Consolidated Financial Statements: issued in May 2011, identifies the concept of control as the determining factor in whether an investee should be included within the consolidated financial statements of the parent. The guidance requires an entity to consolidate an investee when it has exposure or rights to variable returns from its involvement with the investee and has the ability to affect those returns. The standard applies to all investees, including special purpose entities and replaces SIC- 12 Consolidation Special Purpose Entities and parts of IAS 27 Consolidated and Separate Financial Statements. The new standard is effective for the Company’s interim and annual consolidated financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements.

IFRS 11 - Joint Arrangements: issued in May 2011 and addresses two forms of joint arrangements where there is joint control: joint operations and joint ventures. In a joint operation, each venturer will recognize its share of the operation’s assets, liabilities, revenues and expenses. Joint ventures will be required to use the equity method of accounting. IFRS 11 replaces IAS 31 Interests in Joint Ventures and SIC-13 Jointly-controlled Entities Non-Monetary Contributions from Venturers. The new standard is effective for the Company’s interim and annual consolidated financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its financial statements.

IFRS 12 - Disclosure of Interests in Other Entities: issued in May 2011. It is a comprehensive standard addressing disclosure requirements for all forms of interests in other entities, including joint arrangements, associates, subsidiaries, special purpose entities and unconsolidated structured entities. The standard aims to provide information to enable users to evaluate the nature of an entity’s interest in other entities and the associated risks. IFRS 12 is effective for the Company’s interim and annual financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements.

IFRS 13 - Fair Value Measurement: issued in May 2011, replaces fair value measurement and disclosure guidance throughout individual IFRS standards with one comprehensive source of fair value measurement guidance. IFRS 13 defines fair value as the price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date. The standard also provides a framework for measurement of fair value and establishes required disclosures. It is effective for the Company’s interim and annual financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements.

IAS 19 - Employee benefits: issued in June 2011, makes significant changes to the recognition and measurement of defined benefit pension expense and termination benefits, and to the disclosures for all employee benefits. The amendment is effective for annual periods beginning on or after 1 January 2013. The Company estimates there will be no impact from this amendment on its financial statements.

In addition, there have been amendments to existing standards, including IAS 28 Investments in Associates and Joint Ventures, as a result of the introduction of IFRS 10 through 13 discussed above.

SHARE CAPITAL

As at November 23, 2011, the Company has 165,301,302 common shares, 10,200,000 warrants and 6,675,000 options outstanding. The warrants entitle the holder to purchase one common share at a price of CDN$1.50 and expire on June 29, 2013. No warrants have been exercised to date. As at November 23, 2011, 5,045,800 options were exercisable at an average price of CDN$1.30 and the remaining 1,629,200 options will vest as follows: December 20, 2011 637,000 August 30, 2012 549,700 August 30, 2013 442,500

INTERNAL CONTROL OVER FINANCIAL REPORTING (“ICFR”)

The Company´s Chief Executive Officer and Chief Financial Officer have designed, or caused to be designed under their supervision, internal controls over financial reporting related to the Company to provide reasonable assurance regarding the reliability of PetroNova’s financial reporting and preparation of financial statements for external purposes in accordance with IFRS. As at September 30, 2011 PetroNova´s Chief Executive Officer and Chief Financial Officer have evaluated, or caused to be evaluated under their supervision, the design of the Company’s internal controls over financial reporting and have concluded that these controls are designed properly.

RISK FACTORS

The Company is subject to business and other risks, many of which are beyond its control and which could have a material adverse effect on the business and operations of the Company. Please refer to the Company’s audited consolidated financial statements as at and for the years ended December 31, 2010 and 2009 and the Annual Information Form for a description of the business and other risk factors affecting the Company which are available on www.sedar.com.

PetroNova Inc. Condensed Interim Consolidated Financial Statements

(Unaudited) (in United States dollars)

September 30, 2011 and 2010

The accompanying notes are an integral part of these condensed interim consolidated financial statements. 1

PetroNova Inc.

Consolidated Statement of Financial Position

(unaudited)

(in United States dollars)

As at

September 30, December 31,

2011 2010

$ $

ASSETS

Current assets

Cash and cash equiva lents (Note 3) 43,710,654 60,710,250

Restricted cash (Note 4) 256,884 497,260

Other receivables (Note 5) 205,043 197,455

Prepaid expenses 13,202 23,446

Due from related parties (Note 13) - 51,224

44,185,783 61,479,635

Non-current assets

Value added tax 1,678,552 444,044

Faci l i ties and equipment (Note 6) 543,612 56,375

Exploration and evaluation assets (Note 7) 34,895,547 21,450,975

Intangible asset 23,934 5,567

Block depos i ts (Note 8) 5,124,983 7,913,610

42,266,628 29,870,571

Total assets 86,452,411 91,350,206

LIABILITIES AND SHAREHOLDERS' EQUITY

Current liabilities

Bank loans (Note 9) - 940,031

Trade and other payables (Note 10) 2,174,316 1,410,452

Net worth tax payable (Note 12) 291,878 -

Due to related parties (Note 13) 84,116 622,128

2,550,310 2,972,611

Non-current liabilities

Deferred lease inducement 6,620 14,063

Finance lease obl igation (Note 11) 13,931 8,806

Net worth tax payable (Note 12) 535,345 -

555,896 22,869

3,106,206 2,995,480

Shareholders' equity

Share capita l (Note 14) 89,617,793 89,617,793

Share based payment reserve (Note 14) 3,315,980 2,329,983

Accumulated other comprehens ive income (Note 14) 933,218 1,288,431

Defici t (10,520,786) (4,881,481)

Total shareholders' equity 83,346,205 88,354,726

Total liabilities and shareholders' equity 86,452,411 91,350,206

The accompanying notes are an integral part of these condensed interim consolidated financial statements. 2

PetroNova Inc.

Consolidated Statement of Comprehensive Loss

(unaudited)

(in United States dollars)

For the three and nine months ended September 30

2011 2010 2011 2010

$ $ $ $

REVENUES

Interest income 99,175 56,032 257,842 144,832

EXPENSES

Share-based payments (Note 14) 62,420 - 617,430 -

Sa laries and compensation 479,939 209,309 1,422,322 1,168,732

Profess ional fees 350,990 313,712 1,288,346 466,415

Office and adminis tration 394,232 53,248 1,199,577 53,248

Financing expenses (Note 15) 54,532 9,935 123,170 10,627

Depreciation and amortization 47,283 594 114,883 4,191

Total expenses 1,389,396 586,798 4,765,728 1,703,213

(1,290,221) (530,766) (4,507,886) (1,558,381)

Foreign exchange loss (89,228) (105,152) (57,439) (37,585)

Net worth tax expense (Note 12) - - (1,073,980) -

(89,228) (105,152) (1,131,419) (37,585)

(1,379,449) (635,918) (5,639,305) (1,595,966)

OTHER COMPREHENSIVE LOSS

Foreign currency trans lation (Note 14) (156,648) 30,244 (355,213) (39,063)

Total other comprehensive income (loss) (156,648) 30,244 (355,213) (39,063)

Total comprehensive loss (1,536,097) (605,674) (5,994,518) (1,635,029)

Bas ic and di luted loss per share (Note 16) (0.01) (0.01) (0.03) (0.04)

Nine months ended September 30,

Net loss before other items and income tax

Net loss

OTHER ITEMS

Three months ended September 30,

The accompanying notes are an integral part of these condensed interim consolidated financial statements. 3

PetroNova Inc.

Consolidated Statement of Changes in Equity

(unaudited)

(in United States dollars)

For the nine months ended September 30, 2011 and 2010

Share

capital

Share based

payment

reserve

Accumulated

Other

Comprehensive

Income (loss) Deficit Total

$ $ $ $ $

Balance at January 1, 2010 1,000 - - (581,199) (580,199)

Net loss for the period - - - (1,595,966) (1,595,966)

Other comprehens ive income (loss ) - - (39,063) - (39,063)

Is suance of shares 29,159,120 - - - 29,159,120

Fa i r va lue of warrants i ssued 94,543 - - - 94,543

Debt forgiveness 320,571 - - - 320,571

Balance at September 30, 2010 29,575,234 - (39,063) (2,177,165) 27,359,006

Net loss for the period - - - (2,704,316) (2,704,316)

Other comprehens ive income (loss ) - - 1,327,494 - 1,327,494

Share based payment reserve - 2,329,983 - - 2,329,983

Issuance of shares 59,946,137 - - - 59,946,137

Fair value of warrants issued 96,422 - - - 96,422

Balance at December 31, 2010 89,617,793 2,329,983 1,288,431 (4,881,481) 88,354,726

Net loss for the period - - - (5,639,305) (5,639,305)

Other comprehens ive income (loss ) - - (355,213) - (355,213)

Share based payment reserve - 985,997 - - 985,997

Balance at September 30, 2011 89,617,793 3,315,980 933,218 (10,520,786) 83,346,205

The accompanying notes are an integral part of these condensed interim consolidated financial statements. 4

PetroNova Inc.

Consolidated Statement of Cash Flows

(unaudited)

(in United States dollars)

For the three and nine months ended September 30

Nine months ended September 30,

2011 2010 2011 2010

$ $ $ $

Operating activities

Net loss (1,379,449) (635,918) (5,639,305) (1,595,966)

Non-cash i tems:

Share-based payments (Note 14) 62,420 - 617,430 -

Sa laries and compensation - - - 823,797

Lease inducement (2,481) - (7,443) -

Net unreal ized foreign exchange 8,994 104,300 26,376 36,733

Depreciation and amortization 47,283 594 114,883 4,191

Change in non-cash working capita l (Note 17) (2,334,926) (3,134,829) (1,129,355) (2,736,699)

Tota l cash flows used in operating activi ties (3,598,159) (3,665,853) (6,017,414) (3,467,944)

Investing activities

Intangible asset (1,741) - (19,884) -

Purchase of faci l i ties and equipment (Note 6) (10,751) (2,224) (563,923) (2,224)

Purchase of exploration and development assets (Note 7) (5,618,985) (3,753,113) (13,076,004) (3,753,113)

Block depos i ts (Note 8) 2,884,870 (63,550) 2,788,627 (63,550)

Restricted cash (Note 4) 100,317 - 240,376 -

Change in non-cash working capita l (Note 17) (18,022) - 1,505,941 -

Tota l cash flows used in investing activi ties (2,664,312) (3,818,887) (9,124,867) (3,818,887)

Financing activities

Is suance of shares , net of share i ssue costs - - - 8,697,857

Repayment of bank indebtedness - 79,592 (940,031) 79,592

Finance lease obl igation (Note 11) (13,390) - (31,555) -

Advances (repayments) from (to) related parties (Note 13) 625 (503,900) (482,818) (482,562)

Tota l cash flows from (used in( financing activi ties (12,765) (424,308) (1,454,404) 8,294,887

(6,275,236) (7,909,048) (16,596,685) 1,008,056

Foreign exchange loss on cash held in foreign currency (189,356) (20,358) (402,911) (20,358)

Total changes in cash (6,464,592) (7,929,406) (16,999,596) 987,698

Cash and cash equiva lents , beginning of period 50,175,246 8,973,785 60,710,250 56,681

Cash and cash equivalents, end of period 43,710,654 1,044,379 43,710,654 1,044,379

Interest pa id 5,159 - 20,808 -

- - - - Income tax pa id

Three months ended September 30,

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

5

1 Basis of presentation

The condensed interim consolidated financial statements of PetroNova Inc. and its subsidiaries (collectively, “PetroNova” or the “Company”) for the three and nine months ended September 30, 2011 were authorized for issue in accordance with a resolution of the Directors on November 23, 2011. The registered office of PetroNova is 1900, 520 3

rd Avenue S.W., Calgary, Alberta, Canada. PetroNova was incorporated under the Business

Corporations Act (Alberta) on September 17, 2009 as a wholly owned subsidiary of Inepetrol Corp AB (“Inepetrol”). Prior to incorporation, PetroNova’s business, being the exploration for oil in Colombia, was carried on by other direct and indirect wholly owned subsidiaries of Inepetrol (the “Predecessor Subsidiaries”). In June 2010, the Predecessor Subsidiaries transferred oil exploration assets and related liabilities to PetroNova’s Colombian branch. On December 20, 2010, PetroNova successfully completed its initial public offering (“IPO”) and is listed on the TSX Venture Exchange under the symbol PNA.V.

For all periods presented, these condensed interim consolidated financial statements include the historical financial position, results of operations and cash flows of the Colombian oil assets and liabilities acquired based on the Predecessor Subsidiaries’ historical costs in accordance with continuity of interest accounting.

Statement of compliance The condensed interim consolidated financial statements have been prepared in accordance with International Accounting Standard (“IAS”) 34 Interim Financial Reporting issued by the International Accounting Standard Board (“IASB”). The condensed interim consolidated financial statements do not include all of the information required for full annual financial statements and should be read in conjunction with the Company’s annual consolidated financial statements, also prepared in accordance with International Financial Reporting Standards (“IFRS”), as at and for the years ended December 31, 2010 and the Company´s March 31 and June 30, 2011 condensed interim consolidated financial statements.

2 Recent accounting pronouncements

Certain new standards, interpretations, amendments and improvements to existing standards were issued by the IASB or International Financial Reporting Interpretations Committee (“IFRIC”) that are mandatory for accounting periods beginning after January 1, 2011 or later periods. The standards changes that may have an impact to the Company are as follows:

IAS 24 - Related party disclosure – revised definition of related parties The new IAS 24 requires entities to disclose in their financial statements information about transactions with related parties. IAS 24 have simplified the definition of related party and removed certain disclosures required by the predecessor standard. The adoption of this amendment has had no effect on the financial position or the performance of the Company.

IAS 32 - Financial Instruments: Presentation (Amendment) The amendment alters the definition of a financial liability in IAS 32 to enable entities to classify rights issues and certain options or warrants as equity instruments. The amendment is applicable if the rights are given pro rata to all of the existing owners of the same class of an entity’s non-derivative equity instruments, to acquire a fixed number of the entity’s own equity instruments for a fixed amount in any currency. The amendment has had no effect on the financial position or performance of the Company.

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

6

2 Recent accounting pronouncements (continued)

Improvements to IFRSs (issued May 2010) In May 2010, the IASB issued its third omnibus of amendments to its standards, primarily with a view to removing inconsistencies and clarifying wording. There are separate transitional provisions for each standard. The following improvements did not have any impact on the accounting policies, financial position or performance of PetroNova: IFRS 3 – Business Combinations: included different changes mainly related to contingent consideration arrangements, measurement of non-controlling interests and applicability of the IFRS 3 guidance to share-based payments in a business combination.

IFRS 7 – Financial Instruments – Disclosures: the amendment was intended to simplify the disclosures provided by reducing the volume of disclosures around collateral held and improving disclosures by requiring qualitative information to put the quantitative information in context.

IAS 27 – Consolidated and Separate Financial Statements: the consequential amendments to IAS 21, IAS 28 and IAS 31 resulting from the 2008 revisions to IAS 27 are to be applied prospectively.

In addition, the Company has considered the following improvements: IAS 1 – Presentation of Financial Statements: Entities may present either in the statement of changes in equity or within the notes an analysis of the components of other comprehensive income by item. Impact analysis: since the cumulative foreign currency translation is the only item included in other comprehensive income, the Company has disclosed this fact. This change has been included in Note 14 to the interim consolidated financial statements. IAS 34 – Interim Financial Reporting: Greater emphasis has been placed on the disclosure principles in IAS 34 involving significant events and transactions, including changes to fair value measurements, and the need to update relevant information from the most recent annual report. Impact analysis: the Company has considered these additional requirements in its interim consolidated financial statements.

New standards and amendments not yet applicable:

IFRS 9 - Financial Instruments: issued in October 2010, is the first phase in the replacement of IAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 revises the current multiple classification and measurement models for financial assets and liabilities and limits the models to two: amortized cost or fair value. The new standard is effective for the Company’s interim and annual financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements. IFRS 10 - Consolidated Financial Statements: issued in May 2011, identifies the concept of control as the determining factor in whether an investee should be included within the consolidated financial statements of the parent. The guidance requires an entity to consolidate an investee when it has exposure or rights to variable returns from its involvement with the investee and has the ability to affect those returns. The standard applies to all investees, including special purpose entities and replaces SIC- 12 Consolidation Special Purpose Entities and parts of IAS 27 Consolidated and Separate Financial Statements. The new standard is effective for the Company’s interim and annual consolidated financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements.

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

7

2 Recent accounting pronouncements (continued)

IFRS 11 - Joint Arrangements: issued in May 2011 and addresses two forms of joint arrangements where there is joint control: joint operations and joint ventures. In a joint operation, each venturer will recognize its share of the operation’s assets, liabilities, revenues and expenses. Joint ventures will be required to use the equity method of accounting. IFRS 11 replaces IAS 31 Interests in Joint Ventures and SIC-13 Jointly-controlled Entities Non-Monetary Contributions from Venturers. The new standard is effective for the Company’s interim and annual consolidated financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its financial statements.

IFRS 12 - Disclosure of Interests in Other Entities: issued in May 2011. It is a comprehensive standard addressing disclosure requirements for all forms of interests in other entities, including joint arrangements, associates, subsidiaries, special purpose entities and unconsolidated structured entities. The standard aims to provide information to enable users to evaluate the nature of an entity’s interest in other entities and the associated risks. IFRS 12 is effective for the Company’s interim and annual financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements.

IFRS 13 - Fair Value Measurement: issued in May 2011, replaces fair value measurement and disclosure guidance throughout individual IFRS standards with one comprehensive source of fair value measurement guidance. IFRS 13 defines fair value as the price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date. The standard also provides a framework for measurement of fair value and establishes required disclosures. It is effective for the Company’s interim and annual financial statements commencing January 1, 2013. The Company is currently assessing the impact of this standard on its consolidated financial statements. IAS 19 - Employee benefits: issued in June 2011, makes significant changes to the recognition and measurement of defined benefit pension expense and termination benefits, and to the disclosures for all employee benefits. The amendment is effective for annual periods beginning on or after 1 January 2013. The Company estimates there will be no impact from this amendment on its financial statements. In addition, there have been amendments to existing standards, including IAS 28 Investments in Associates and Joint Ventures, as a result of the introduction of IFRS 10 through 13 discussed above.

3 Cash and cash equivalents September 30,

2011 $

December 31, 2010

$

Cash at banks 9,127,242 4,206,770 Cash held in trust - 201,080 Guaranteed investment certificates (GIC’s) 34,583,412 56,302,400

43,710,654 60,710,250

Cash at banks earns interest at floating rates based on daily bank deposit rates. The GIC’s earn interest at rates ranging from 0.08% - 1.25% with maturities for periods no larger than 90 days.

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

8

4 Restricted cash

At September 30, 2011, the balance of $256,884 (December 31, 2010: $497,260) presented as restricted cash corresponds to the Company's 20% participation in the cash of the Llanos joint assets. This cash will be used only in activities related with the Llanos CPO-6, CPO-7 and CPO-13 blocks (collectively, the “Llanos Blocks”).

5 Other receivables September 30,

2011 $

December 31, 2010

$

Current Advances Interest receivable

71,508 47,342

104,475 17,078

Joint venture other receivables 41,591 4,464 GST receivable 44,602 71,438

205,043 197,455

The Company does not have trade receivables at each reporting date.

6 Facilities and equipment

Computer and

telecommunication equipment

$

Furniture and

fixture $

Asset under Finance

Lease $

Leasehold

improvements $

Total $

Cost December 31, 2010 17,410 35,019 18,336 - 70,765 Additions during the period 129,078 106,742 36,680 339,850 612,350 Disposals during the period (2,214) (15,931) - - (18,145)

At September 30, 2011 144,274 125,830 55,016 339,850 664,970

Accumulated depreciation December 31, 2010 (6,020) (6,078) (2,292) - (14,390) Charge for the period (15,388) (5,186) (15,599) (74,784) (110,957) Disposals during the period 812 3,177 - - 3,989

At September 30, 2011 (20,596) (8,087) (17,891) (74,784) (121,358)

Net book value At December 31, 2010 11,390 28,941 16,044 - 56,375

At September 30, 2011 123,678 117,743 37,125 265,066 543,612

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

9

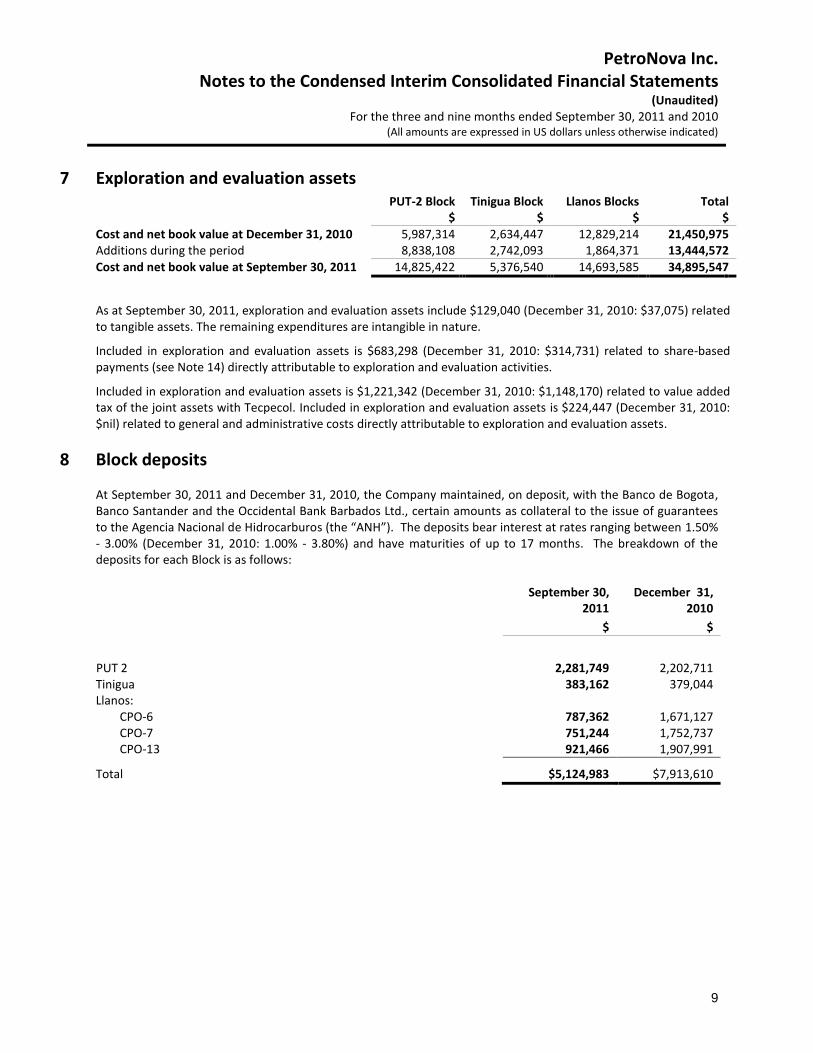

7 Exploration and evaluation assets PUT-2 Block Tinigua Block Llanos Blocks Total $ $ $ $

Cost and net book value at December 31, 2010 5,987,314 2,634,447 12,829,214 21,450,975 Additions during the period 8,838,108 2,742,093 1,864,371 13,444,572

Cost and net book value at September 30, 2011 14,825,422 5,376,540 14,693,585 34,895,547

As at September 30, 2011, exploration and evaluation assets include $129,040 (December 31, 2010: $37,075) related to tangible assets. The remaining expenditures are intangible in nature.

Included in exploration and evaluation assets is $683,298 (December 31, 2010: $314,731) related to share-based payments (see Note 14) directly attributable to exploration and evaluation activities.

Included in exploration and evaluation assets is $1,221,342 (December 31, 2010: $1,148,170) related to value added tax of the joint assets with Tecpecol. Included in exploration and evaluation assets is $224,447 (December 31, 2010: $nil) related to general and administrative costs directly attributable to exploration and evaluation assets.

8 Block deposits

At September 30, 2011 and December 31, 2010, the Company maintained, on deposit, with the Banco de Bogota, Banco Santander and the Occidental Bank Barbados Ltd., certain amounts as collateral to the issue of guarantees to the Agencia Nacional de Hidrocarburos (the “ANH”). The deposits bear interest at rates ranging between 1.50% - 3.00% (December 31, 2010: 1.00% - 3.80%) and have maturities of up to 17 months. The breakdown of the deposits for each Block is as follows:

September 30, 2011

December 31, 2010

$ $

PUT 2 2,281,749 2,202,711 Tinigua 383,162 379,044 Llanos:

CPO-6 787,362 1,671,127 CPO-7 751,244 1,752,737 CPO-13 921,466 1,907,991

Total $5,124,983 $7,913,610

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

10

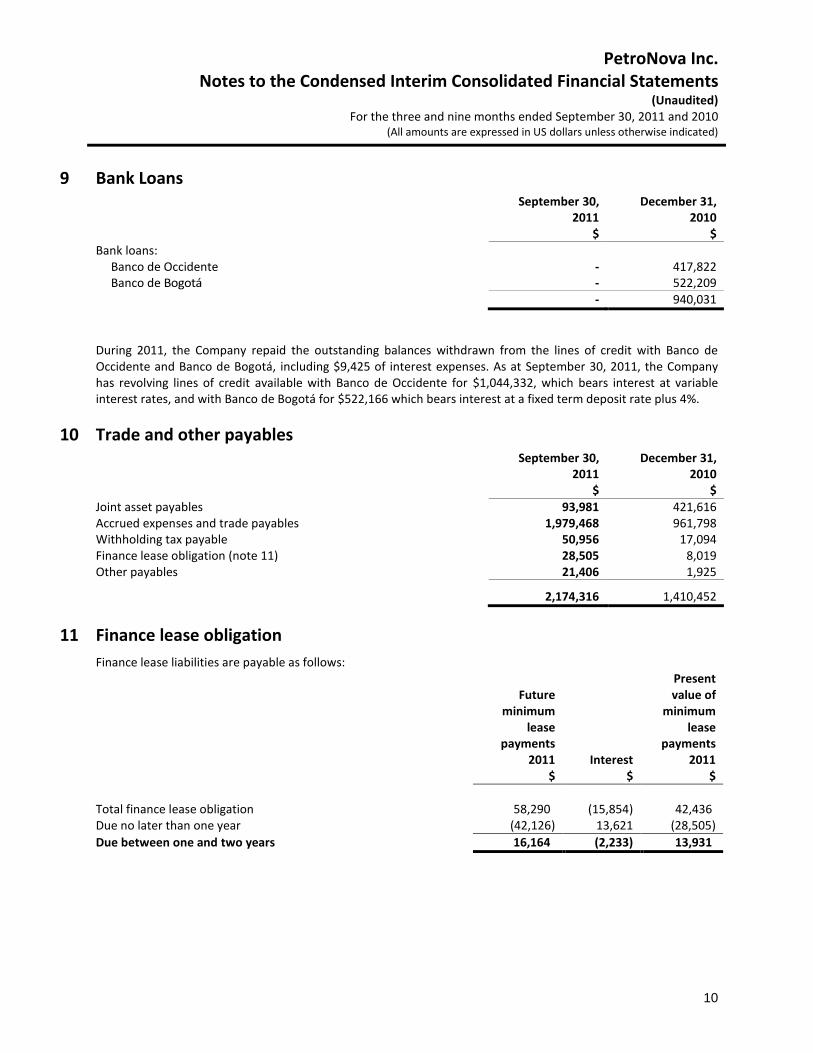

9 Bank Loans September 30,

2011 December 31,

2010 $ $

Bank loans: Banco de Occidente - 417,822 Banco de Bogotá - 522,209

- 940,031

During 2011, the Company repaid the outstanding balances withdrawn from the lines of credit with Banco de Occidente and Banco de Bogotá, including $9,425 of interest expenses. As at September 30, 2011, the Company has revolving lines of credit available with Banco de Occidente for $1,044,332, which bears interest at variable interest rates, and with Banco de Bogotá for $522,166 which bears interest at a fixed term deposit rate plus 4%.

10 Trade and other payables September 30,

2011 $

December 31, 2010

$

Joint asset payables 93,981 421,616 Accrued expenses and trade payables 1,979,468 961,798 Withholding tax payable 50,956 17,094 Finance lease obligation (note 11) 28,505 8,019 Other payables 21,406 1,925

2,174,316 1,410,452

11 Finance lease obligation

Finance lease liabilities are payable as follows:

Future minimum

lease payments

2011 $

Interest $

Present value of

minimum lease

payments 2011

$

Total finance lease obligation 58,290 (15,854) 42,436 Due no later than one year (42,126) 13,621 (28,505)

Due between one and two years 16,164 (2,233) 13,931

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

11

12 Net worth and income taxes

Net worth tax On December 29, 2010, the Colombian Congress passed a law which imposes a 6% net worth tax levied on Colombian operations, which is based on the Company’s net worth in Colombia at January 1, 2011 and is payable in eight equal installments between 2011 and 2014. The total amount of net worth tax payable is $1,220,410 and the amount recognized in 2011 of $1,073,980 was calculated by discounting the future net worth tax payments by the Colombian risk free interest rate Net worth tax payable

$

December 31, 2010 - Amount expensed in 2011 1,073,980

Unwinding of discount (Note 16) 58,812 Foreign exchange difference (467)

Payments (305,102)

September 30, 2011 827,223 Current portion (291,878)

Non-current portion 535,345

Income taxes Deferred income tax assets have not been recognized given this stage of the Company’s development, it is not determinable that future taxable profit will be available against which the Company can utilize such deferred income tax assets.

13 Related party disclosure

The consolidated interim financial statements of the Company involve transactions with the related parties listed in the following table:

Name Country of incorporation Relationship

Inepetrol Corporation AB Sweden Common shareholders Inepetrol S.A. Venezuela Common shareholders Inepetrol Colombia (branch) Colombia Common shareholders Technisupplies Inc. British Virgin Islands Common shareholders

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

12

13 Related party disclosure (continued)

The following table provides a summary of transactions that have been entered into with related parties including the outstanding balances as at September 30, 2011 and December 31, 2010: Amounts due from related parties:

September 30,

2011 $

December 31,

2010 $

Inepetrol Corporation AB - 1,000 Inepetrol Colombia (branch) - 50,224 - 51,224

Amounts owed to related parties: Inepetrol S.A. 84,116 465,184 Technisupplies Inc. - 156,944

84,116 622,128

The balance with Inepetrol S.A. is mainly related to services rendered to the Company in connection with the technical services agreement entered into between the parties and is non-interest bearing and due on demand. During 2011, the Company has paid $580,263 to Inepetrol S.A. for charges related to this agreement plus expenses.

During 2010, Technisupplies Inc. made a payment of $156,944 on behalf of the Company for services rendered by third parties to the Company. The balance due was non-interest bearing and due on demand. At September 30, 2011, the balance was repaid in full.

The balance with Inepetrol Colombia (branch) is related to payments made by PetroNova Colombia on behalf of Inepetrol Colombia (branch) related to employee benefits and professional fees and is non-interest bearing and due on demand.

14 Share capital and reserves

Authorized shares

Common shares Unlimited, no par value Preferred shares Unlimited, no par value

During 2010, the Articles of Incorporation were amended to revise the share structure and to convert the Class “A” shares into common shares on a one-for-one basis.

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

13

14 Share capital and reserves (continued)

Issued common shares

Number of common shares

Amount $

Issued upon incorporation at September 17, 2009 1,000 1,000

At December 31, 2009 1,000 1,000

Issued as remuneration shares 4,120,258 823,797 Issued as part of a debt purchase and sale agreement 76,160,044 15,232,009 Issued as part of a debt purchase and sale agreement 22,500,000 4,500,000 Issued pursuant to private placement 10,000,000 9,396,631 Forgiveness of debt - 320,571 Issued to directors 200,000 101,398 Issued on initial public offering 52,320,000 64,255,500 Share issue costs - (5,204,078)

At December 31, 2010 and September 30, 2011 165,301,302 89,426,828

Number of

Warrants Amount

$

Issued common share purchase warrants Issued pursuant to private placement 10,000,000 101,369 Issued to directors 200,000 96,422 Warrant issue costs - (6,826)

At December 31, 2010 and September 30, 2011 10,200,000 190,965

Total common shares and common share purchase warrants 175,501,302 89,617,793

Each warrant entitles the holder thereof to purchase one Common Share at a price of Cdn$1.50 per common share on or before June 29, 2013.

Accumulated other comprehensive income Foreign currency translation adjustment is the only item recognized in accumulated other comprehensive income and arises on the translation of the financial statements of PetroNova from its Canadian dollar functional currency to U.S. dollar reporting currency.

Share-based payments In accordance with the policies of the TSX Venture Exchange, PetroNova has adopted a stock option plan under which it is authorized to grant options to directors, employees and consultants to acquire up to 10% of its shares issued and outstanding (on a non-diluted basis). Under the terms of the option plan, the exercise price of each option cannot be lower than the market price of PetroNova’s common shares on the date of grant and the options can be granted for a maximum term of 5 years. The option plan was re-approved by the holders of common shares of PetroNova on June 13, 2011.

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

14

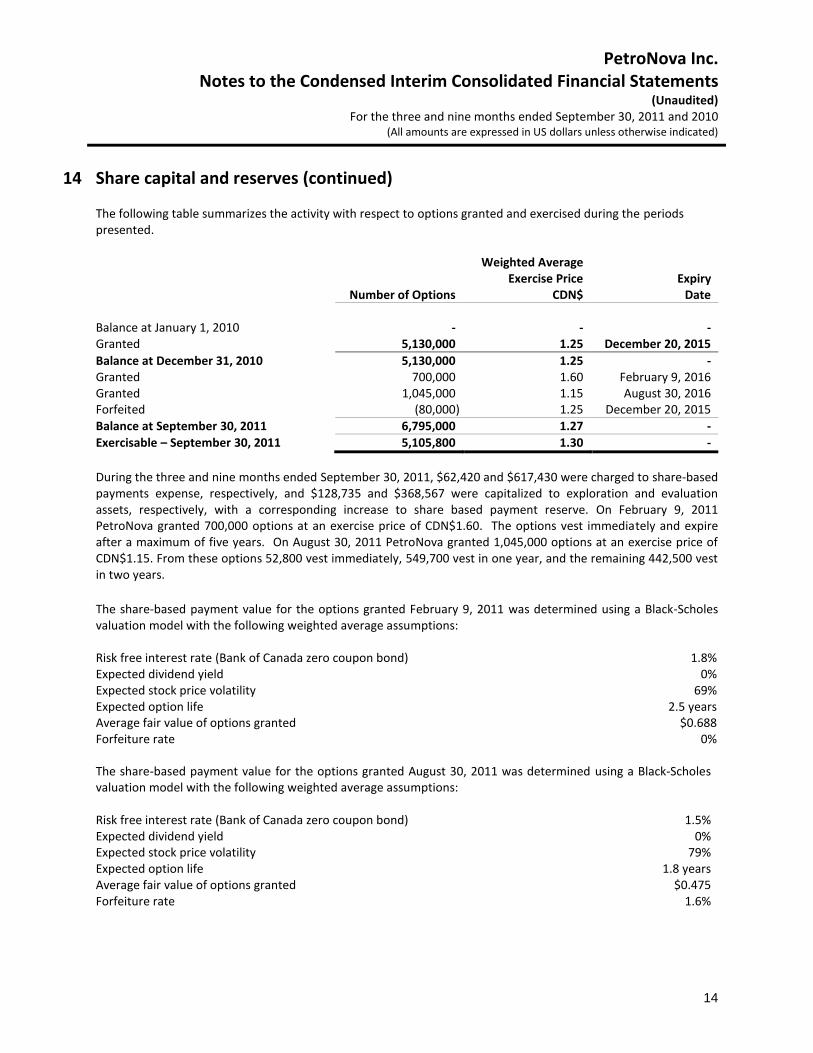

14 Share capital and reserves (continued) The following table summarizes the activity with respect to options granted and exercised during the periods presented.

Number of Options

Weighted Average Exercise Price

CDN$ Expiry

Date

Balance at January 1, 2010 - - - Granted 5,130,000 1.25 December 20, 2015

Balance at December 31, 2010 5,130,000 1.25 - Granted 700,000 1.60 February 9, 2016 Granted 1,045,000 1.15 August 30, 2016 Forfeited (80,000) 1.25 December 20, 2015

Balance at September 30, 2011 6,795,000 1.27 -

Exercisable – September 30, 2011 5,105,800 1.30 -

During the three and nine months ended September 30, 2011, $62,420 and $617,430 were charged to share-based payments expense, respectively, and $128,735 and $368,567 were capitalized to exploration and evaluation assets, respectively, with a corresponding increase to share based payment reserve. On February 9, 2011 PetroNova granted 700,000 options at an exercise price of CDN$1.60. The options vest immediately and expire after a maximum of five years. On August 30, 2011 PetroNova granted 1,045,000 options at an exercise price of CDN$1.15. From these options 52,800 vest immediately, 549,700 vest in one year, and the remaining 442,500 vest in two years.

The share-based payment value for the options granted February 9, 2011 was determined using a Black-Scholes valuation model with the following weighted average assumptions: Risk free interest rate (Bank of Canada zero coupon bond) 1.8% Expected dividend yield 0% Expected stock price volatility 69% Expected option life 2.5 years Average fair value of options granted $0.688 Forfeiture rate 0%

The share-based payment value for the options granted August 30, 2011 was determined using a Black-Scholes valuation model with the following weighted average assumptions:

Risk free interest rate (Bank of Canada zero coupon bond) 1.5% Expected dividend yield 0% Expected stock price volatility 79% Expected option life Average fair value of options granted

1.8 years $0.475

Forfeiture rate 1.6%

PetroNova Inc. Notes to the Condensed Interim Consolidated Financial Statements

(Unaudited) For the three and nine months ended September 30, 2011 and 2010

(All amounts are expressed in US dollars unless otherwise indicated)

15

15 Financing expenses Three months ended Nine months ended September

30, 2011 $

September 30, 2010

$

September 30, 2011

$

September 30, 2010

$

Unwinding of net worth tax payable (Note 12) 17,427 - 58,812 - Interest and bank charges 37,105 9,935 64,358 10,627

54,532 9,935 123,170 10,627