peza overview.aug 2006.ppt

DESCRIPTION

PEZA taxationTRANSCRIPT

TAXATION OF ECOZONE ENTREPRISES

PUNONGBAYAN & ARAULLO

2

This presentation covers

A. General Overview

B. Taxation

- Basic rules

- Updates

3

GOVERNING LAW & REGULATIONS

• Republic Act No. 7916 (Special Economic Zone Act of 1995)

• R.A. No. 8748 (amending R.A. No. 7916)

• Presidential Decree No. 66 as amended

• PEZA Implementing Rules & Regulations

• Executive Order No. 226, as amended

• BIR Revenue Regulations No. 12-97, as amended

• BIR Revenue Regulations No. 11-05

• BIR Revenue Memorandum Circular No. 74-99

• PEZA Board Resolutions

4

Types of ECOZONE Enterprises

Export Enterprises Free Trade Enterprises Domestic Market Enterprises Facilities Enterprises Utilities Enterprises Tourism Enterprises Developer/Operator Service Enterprises Ecozone IT Enterprises and Parks

5

Incentives for Export & Free Trade Enterprises

Income Tax Holiday (Corporate Tax Exemption) Special 5% Tax Rate on gross income in lieu of all

national and local taxes, after the lapse of the ITH Exemption from Duties and Taxes

Tax Credit for Import Substitution (under Export

Development Act) Additional Deduction for Training Expenses (Labor

and Management)

Additional labor expense deduction

6

Incentives….

Exemption from Wharfage Dues, Export Tax, Impost,

and Fees

Tax Credit on Domestic Capital Equipment Tax and Duty-Free Importation of Breeding Stocks

and Genetic Materials Tax Credit on Domestic Breeding Stocks and Genetic

Materials Unrestricted use of Consigned Equipment

7

Permanent Resident Status for Foreign Investors and Family

Employment of Foreign Nationals

Exemption from SGS inspection

Simplified import-export procedures

Incentives….

8

INCOME TAX HOLIDAY

9

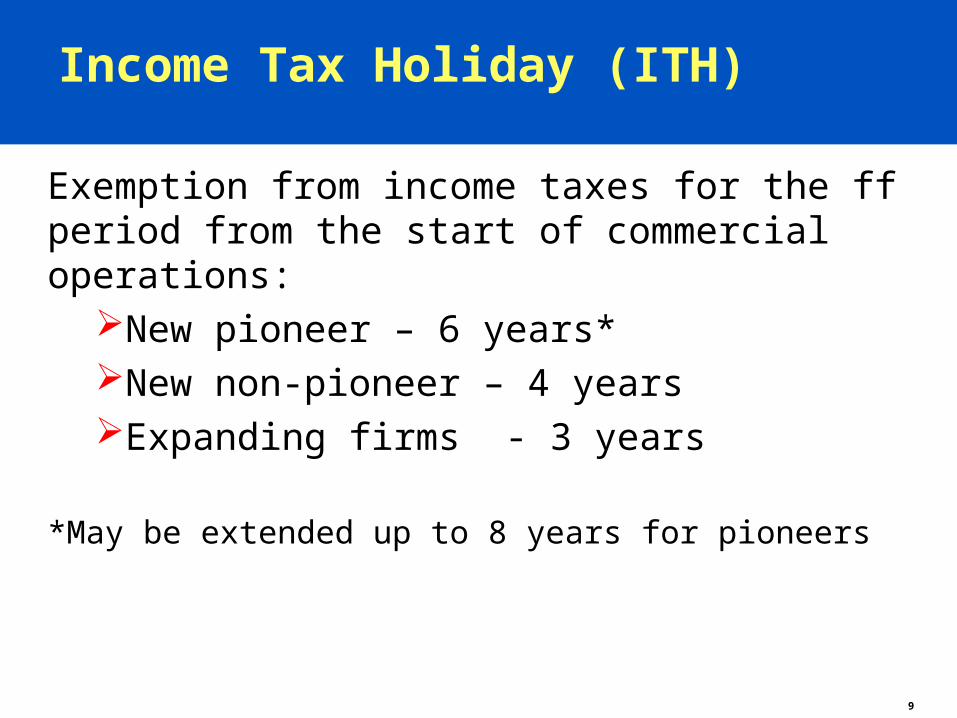

Income Tax Holiday (ITH)

Exemption from income taxes for the ff period from the start of commercial operations:

New pioneer – 6 years* New non-pioneer – 4 yearsExpanding firms - 3 years

*May be extended up to 8 years for pioneers

10

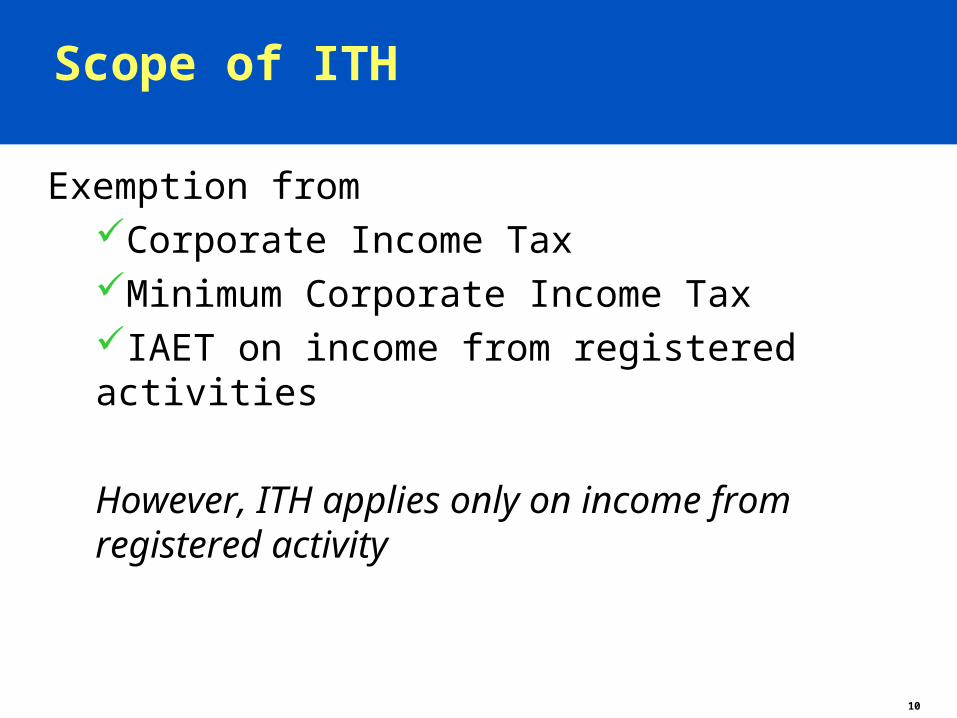

Scope of ITH

Exemption from Corporate Income TaxMinimum Corporate Income TaxIAET on income from registered activities

However, ITH applies only on income from registered activity

11

Firm under ITH is not exempt from:

• Corporate income tax and MCIT on income from unregistered activities

• Final income tax on Passive Incomes• IAET on income from unregistered activities• VAT (subject to RMC 74-99 & RR 16-05)• Documentary Stamp Tax• Liability as withholding agent• Real Estate Taxes (machineries exempt for first 3

years from operation)

12

ITH for new projects

13

New Projects

New activities distinct from their registered operations

– Separate book of accounts– ITH applies only on the sale of the new

products

14

Income Tax Holiday for Expansion Projects

15

What does “expansion” mean?[Rule I, Sec. 2(w)]

Installation of additional facilities and/or equipment

Increase in production capacity Expansion may include modernization and rehabilitation which may or may not result in

increased capacity.

16

Expansion…..

Stages to be modernized should be identifiable;

and

Will result in any of the following:

increased productive efficiency reduced production cost upgraded product quality state of the art production

17

ITH applies only on incremental increase in production

Rate of income tax exemption=

Incremental sales of the registered product

Total sales of the registered product

*Sales - in volume of homogenous product

- in value of heterogenous product

18

Computation of incremental sales

Incremental salesIncremental sales

= Total sales - highest sales in last 3 yrs*= Total sales - highest sales in last 3 yrs*

*Highest sales attained for any one year within last *Highest sales attained for any one year within last 3 years prior to expansion3 years prior to expansion

*Sales - in volume of homogenous product*Sales - in volume of homogenous product

- in value of heterogenous product - in value of heterogenous product

19

Computation of income tax exemption (homogenous products)

Total Sales = 100,000 units

Incremental Sales = 20,000 units

Rate of exemption = 20,000 = 20%

100,000

Gross Income = PhP 500,000.00

Exempt = Rate of exemption X Gross Income

= 20% X PhP500,000.00

= PhP 100,000

20

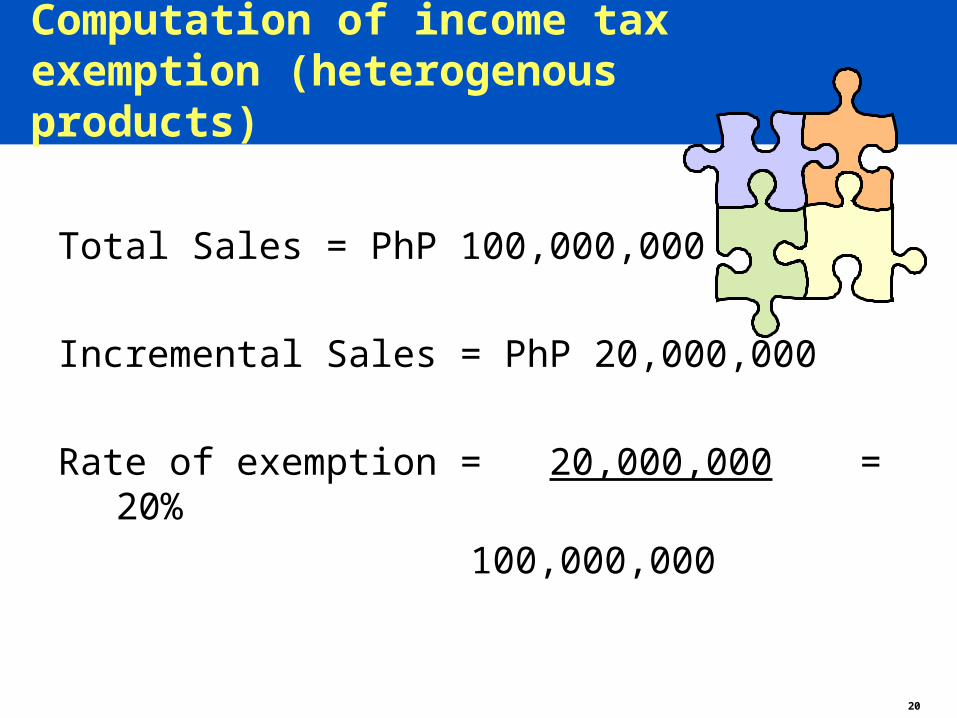

Computation of income tax exemption (heterogenous products)

Total Sales = PhP 100,000,000

Incremental Sales = PhP 20,000,000

Rate of exemption = 20,000,000 = 20%

100,000,000

21

EXTENSION OF INCOME TAX

HOLIDAY

22

ITH Extension

• Extension of the income tax holiday for one extra year each for qualifying under each of the criteria provided

• Extension year – any year within 3 years following the last year of ITH availment

23

ITH Extension Criteria

1. Capital equipment to labor ratio

Total imported or domestic

capital equipment_____ < US$10,000

Number of workers per worker

24

Direct labor...

• Includes personnel actually engaged in the production of the registered product.

• Does not include line supervisors, warehousemen, quality control personnel, utility and maintenance personnel and subcontracted labor.

25

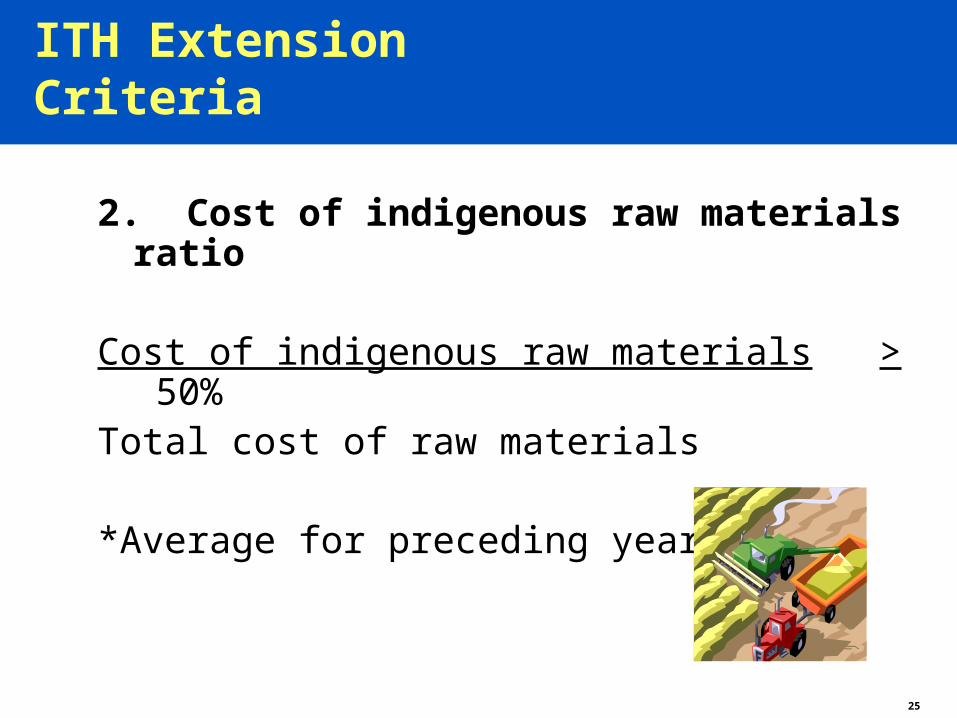

ITH Extension Criteria

2. Cost of indigenous raw materials ratio

Cost of indigenous raw materials > 50%Total cost of raw materials

*Average for preceding years

26

Indigenous raw materials...

• Local raw materials actually used as inputs in the manufacturing or processing of registered products

• Exclude chromite, gold limestone, copper and marble

27

ITH Extension Criteria

3. Net Foreign Exchange Earnings/Savings

NFEE or NFES > US$500,000

*Annual average during first three years of operation

28

Net foreign exchange earnings...

• Net forex earned from the export of products or services

Total forex proceeds minus

total forex costs (imported raw materials, depreciation of imported capital equipment, etc,)

29

Net foreign exchange savings...

• Net forex savings from domestic production and sale of products which used to be unavailable locally

Import value of local sales of the product

minus

Total forex cost (raw materials/depreciation

of imported capital equipment, etc.)

30

START OF COMMERCIAL OPERATIONS

PEZA MEMORANDUM CIRCULAR NO. 2002-02

04 April 2002

31

START OF COMMERCIAL OPERATIONS

For the purpose of the establishing the starting date of a PEZA-registered economic zone export enterprise’s availment of its ITH incentive, the date of the “Start of Commercial Operations” (SCO) shall be, whichever comes first:

• the date specified in its Registration Agreement with PEZA, or

• the verified actual date when it begins commercial production of its registered product.

32

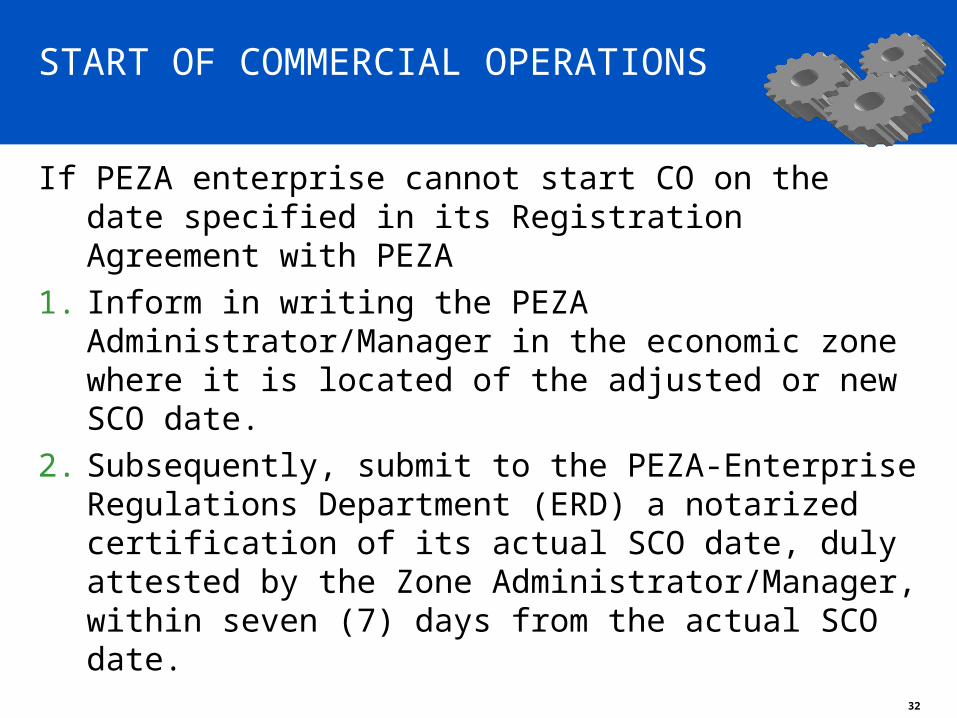

START OF COMMERCIAL OPERATIONS

If PEZA enterprise cannot start CO on the date specified in its Registration Agreement with PEZA

1. Inform in writing the PEZA Administrator/Manager in the economic zone where it is located of the adjusted or new SCO date.

2. Subsequently, submit to the PEZA-Enterprise Regulations Department (ERD) a notarized certification of its actual SCO date, duly attested by the Zone Administrator/Manager, within seven (7) days from the actual SCO date.

33

START OF COMMERCIAL OPERATIONS

If PEZA enterprise does not start commercial operations on the SCO date, and also fails to notify the PEZA of its adjusted or new SCO date, or where the actual SCO date cannot be clearly verified or determined:

The date of the first importation of raw materials by the export enterprise shall be adopted as its SCO date, for the purpose of establishing the starting date of the ITH incentive.

PEZA may imposefines or penalties on the export enterprise for its failure to formally inform PEZA of its adjusted/new and actual SCO, as required.

34

START OF COMMERCIAL OPERATIONS

• PEZA shall automatically cancel the registration of an economic zone export enterprise which has not started actual commercial operations after one (1) year from the SCO date in the RA or the adjusted/new SCO submitted to PEZA.

• PEZA Board may re-instate upon filing of a written request provided that project Implementation has actually commenced, as may be evidenced by any of the following: – importation of production equipment and machinery; – payment of lease rentals on the project site or

acquisition of land for the project site; and/or – such other undertakings that will indicate that the

economic zone export enterprise is intent on implementing its PEZA-registered project.

35

Gross Income Tax Regime

36

Gross Income Tax Regime

• Exemption from all national internal revenue taxes and local government taxes except real property taxes on land owned by developers

• 5% on gross income from business activities within the ECOZONE in lieu of all taxes

37

NATURE OF THE 5% GIT

The 5% GIT is income tax in nature and a national internal revenue tax in character.

- Rev. Regs. No. 1-2000

38

NATIONAL TAXES DEFINED RR 12-97

“ NATIONAL TAXES” shall refer to all internal revenue taxes, including the regular income taxes, otherwise due and collectible from a registered ECOZONE enterprise under the National Internal Revenue Code and customs duties and import charges under the Tariff and Customs Code. National taxes shall, however, not include withholding taxes on salaries of employees or on income payments to persons other than a registered ECOZONE enterprise, subject to the withholding tax at source under Section 50(b) of the Tax Code, as amended.

39

National Taxes Defined

All internal revenue taxes due and collectible under the National Internal Revenue Code,

Income Tax (RCIT, MCIT)Transfer taxesVAT and other Percentage TaxExcise taxesDocumentary Stamp Tax (*under BIR Review)

Exception: Withholding taxes on salaries of employees or on income payments to persons other than a registered ECOZONE enterprise, subject to the withholding tax at source

40

DST EXEMPTION*

ORIGNAL ISSUANCE OF SHARES

• Prior to PEZA registration – subject to DST

• After PEZA registration – exempt– Shareholder pays DST if he is not enjoying

exemption– Shareholder is exempt is nonresident

(BIR Ruling No. DA-111-06-15-01)*Under reconsideration

41

BPRT ON INDIRECT REMITTANCE OF BRANCH PROFITS

• Increasing the head office’s assigned capital to its Philippine branch by transferring net profits of the branch to the Assigned Capital account shall be subject to the 15% branch profit remittance tax (BPRT). Although the profits from operations will not be physically remitted to the head office abroad, the transfer to Assigned Capital is an indirect remittance to the head office.

• (BIR Ruling No. DA 039-2005, January 28, 2005)

42

NO EXEMPTION FROM MERALCO FRANCHISE TAX FOR PEZA ENTERPRISES

PEZA-registered enterprises under 5% GIT not exempt from amount passed on by Meralco and other electric utilities as franchise tax.

– The franchise tax is imposed on electric utilities; not passed on to the buyer as tax, unlike VAT

(BIR Ruling No. DA-120-2005, April 6, 2005)

43

GROSS INCOME DEFINITION (RR 11-2005, March 31, 2005)

Gross sales or gross revenues derived from business activity within the ECOZONE, net of sales discounts, sales returns and allowances and minus costs of sales or direct costs but before any deduction is made for administrative, marketing, selling and/or operating expenses or incidental losses during a given taxable period.

Deleted : [Allowable deductions from gross income]

Replace with: Direct costs included in the allowable deductions to arrive at gross income

44

GIE for PEZA ENTERPRISES(RR 11-2005, March 31, 2005)

Decrease in Goods in Process Account (Intermediate goods)

Decrease in Finished Goods Account

Depreciation of machinery and equipment used in production, and of that portion of the building owned or constructed [by an ECOZONE Enterprise] that is used exclusively in the production of goods

Rent and utility charges associated with building, equipment and warehouses [or handling goods] used in production

Financing charges associated with fixed assets used in production the amount of which were not previously capitalized

45

Allowable Deductions

1) For ECOZONE Export Enterprise

a. Direct salaries, wages or labor expenses

b. Production supervision salaries

c. Raw materials used in the manufacture of products

d. Decrease in Goods in Process Account (Intermediate goods)

e. Decrease in Finished Goods Account

f. Supplies and fuels used in production

46

g. Depreciation of machinery and equipment used in production, and of that portion of the building owned or constructed [by an ECOZONE Enterprise] that is used exclusively in the production of goods

h. Rent and utility charges associated with building, equipment and warehouses [or handling goods] used in production

i. Financing charges associated with fixed assets used in production the amount of which were not previously capitalize

For ECOZONE Export Enterprises……….

Allowable Deductions …..

47

2) For ECOZONE Developer/ Operator, Facilities, Utilities Enterprises :

a. Direct salaries, wages or labor expensesb. Service supervision salariesc. Direct materials, supplies used or resold to

another ECOZONE Enterprised. Depreciation of machinery, equipment and

buildings owned or constructed e. Financing charges associated with fixed assetsf. Rent and utility charges for buildings and capital

equipment

Allowable Deductions …..

48

DEDUCTION FOR ROYALTIES

Dependent on the nature of the royalty payment

• Royalties relating to a system or license supporting general and administrative functions or operations

• Royalties related to use or transfer of technical information and manufacturing know-how – cost of manufacturing goods sold– E.g., Product design, logo, formula, or process

49

CLARIFICATIONS….

50

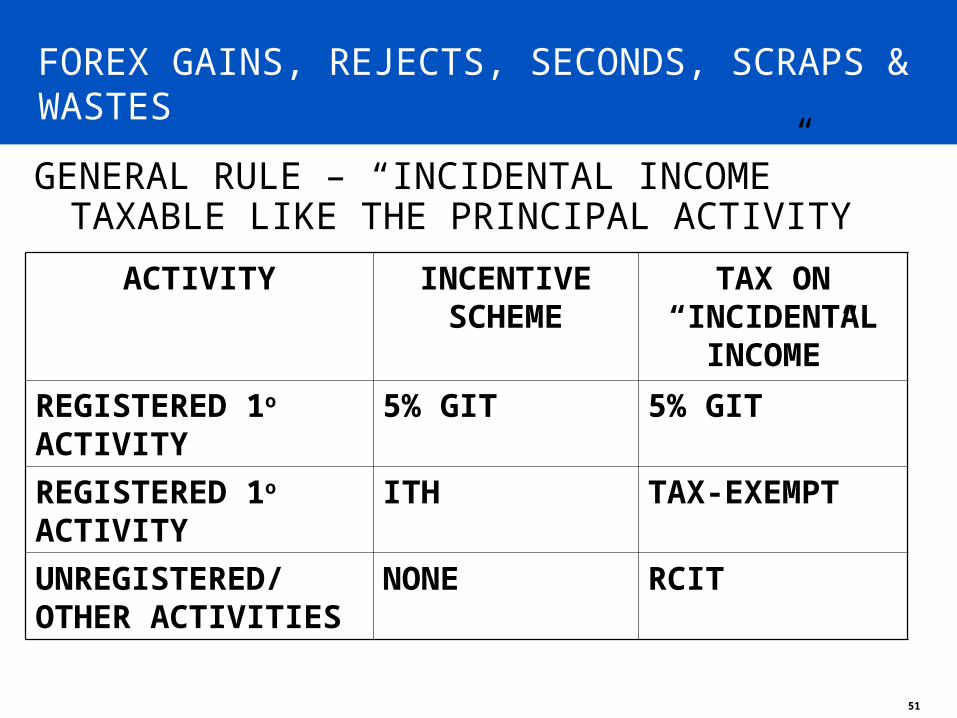

FOREX GAINS, REJECTS, SECONDS, SCRAPS & WASTES

GENERAL RULE:

“INCIDENTAL INCOME” TAXABLE LIKE

THE PRINCIPAL ACTIVITY

PEZA Memorandum Circular No. 2005-032

September 15, 2005

51

FOREX GAINS, REJECTS, SECONDS, SCRAPS & WASTES

GENERAL RULE – “INCIDENTAL INCOME” TAXABLE LIKE THE PRINCIPAL ACTIVITY

ACTIVITY INCENTIVE SCHEME

TAX ON “INCIDENTAL

INCOME”

REGISTERED 1o ACTIVITY

5% GIT 5% GIT

REGISTERED 1o ACTIVITY

ITH TAX-EXEMPT

UNREGISTERED/ OTHER ACTIVITIES

NONE RCIT

52

INCOME FROM: TAX TREATMENT

FOREX GAIN

PRODUCTION REJECTS & SECONDS

RECOVERED WASTES/SCRAPS FROM RAW MATS, PACKAGING, OTHER DIRECT/INDIRECT MATERIALS & SUPPLIES

UNPROCESSED, UNUSED, OBSOLETE OR “OFF-SPECS” PRODUCTION INPUTS

SAME AS

TAX ON

PRINCIPAL

ACTIVITY

RCIT

53

INCOME FROM UNREGISTERED ACTIVITIES

54

INCOME NOT RELATED TO THE REGISTERED ACTIVITY (RR 20-02; RMC 32-05)

Regular internal revenue taxes apply as follows:• 20% final income tax on interest from Philippine Currency

bank deposits and yield or any other monetary benefit from deposit substitutes, and from trust funds and similar arrangements

• 7.5% tax on foreign currency deposits • 5%/10% capital gains tax or ½ % stock transaction tax, as

the case may be, on the sale of shares of stock

55

INCOME PAYMENTS OF REGISTERED ENTITIES (RR 20-02; RMC 32-05)

Enterprise shall withhold tax on, among others:• Dividends paid to the shareholders of a registered

enterprise• Interest payments to creditors of such registered enterprise

(regardless of any tax provision for grossing up of taxes), and other such payments shall be subject to the appropriate rate of tax imposable on the recipient of such income.

56

EXEMPTION OF PEZA-REGISTERED

ECONOMIC ZONE ENTERPRISES

FROM LGU PERMITS AND LOCAL TAXES,

LICENSES AND FEES

PEZA MEMORANDUM CIRCULAR NO. 2004-024

24 September 2004

57

EXEMPTION FROM LOCAL TAXES

1. All PEZA-registered economic zone locator enterprises, which are entitled to any or all 3 fiscal incentives [ i.e., Income Tax Holiday Incentive; the option to pay to pay the special 5% Tax on Gross Income, in lieu of all national and local taxes except real property taxes on land owned by developers (5% GIT incentive); and / or tax-and duty-free importation of machinery and equipment, raw materials, supplies, spare parts and other production inputs], including Logistics Facilities Enterprises, are exempted from having to secure all LGU permits.

58

EXEMPTION OF PEZA ENTERPRISES FROM LGU PERMITSLegal Basis:

Republic Act No. 7916: “The Special Economic Zone Act of 1995”’as amended by R.A. No. 8748

• Section 13. General Powers and Functions of the Authority expressly vests PEZA with the power to “… operate, administer, manage and develop the ECOZONE” and “…register, regulate and supervise the enterprises in the ECOZONE in an efficient and decentralized manner”. This provision echoes

• Section 7 of R.A. No. 7916 which provides that the ‘ECOZONE shall be developed, as much as possible, into a decentralized, self-reliant and self-sustaining industrial, commercial / trading, agro-industrial, tourist, banking, financial and investment center with minimum government intervention” and that the ‘ECOZONE shall administer itself on economic, financial, industrial, tourism development and such other matters within the exclusive competence of the national government”.

59

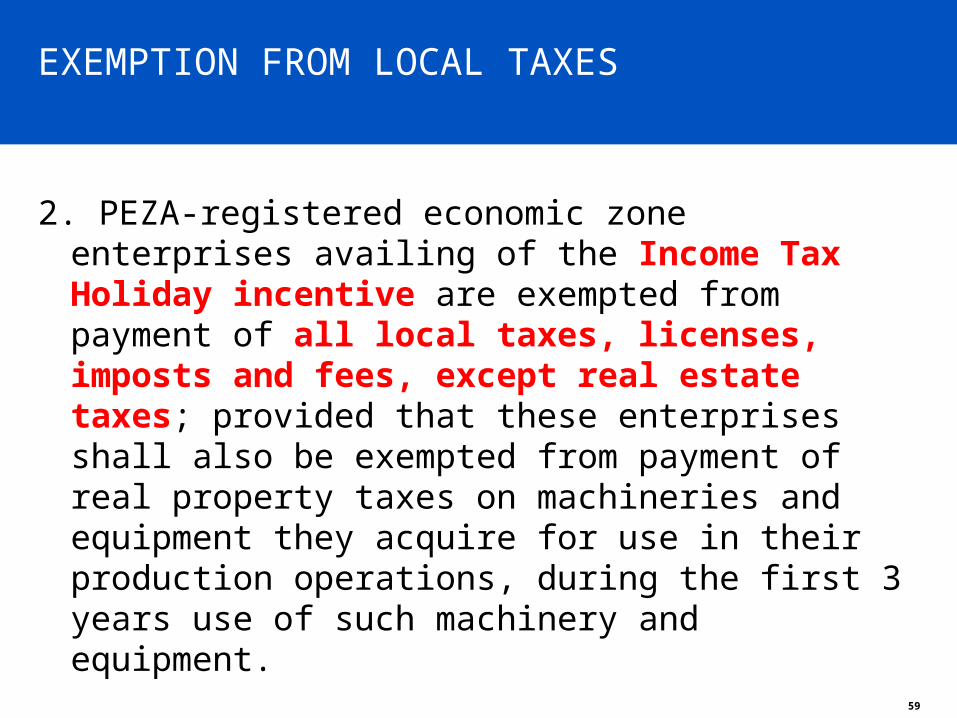

EXEMPTION FROM LOCAL TAXES

2. PEZA-registered economic zone enterprises availing of the Income Tax Holiday incentive are exempted from payment of all local taxes, licenses, imposts and fees, except real estate taxes; provided that these enterprises shall also be exempted from payment of real property taxes on machineries and equipment they acquire for use in their production operations, during the first 3 years use of such machinery and equipment.

60

LOCAL TAX EXEMPTION OF FIRMS UNDER ITH• Legal Basis:

Republic Act No. 7916: “The Special Economic Zone Act of 1995”, as amended by R.A. No. 8748

• Section 23. Fiscal Incentives provides that “Business establishments operating within the ECOZONES shall be entitled to the fiscal incentives as provided for under Presidential Decree No. 66, the law creating the Export Processing Zone Authority, or those provided under Book VI of Executive Order No. 226, otherwise known as the Omnibus Investment Code of 1987”.

Executive Order No. 226, “The Omnibus Investment Code of 1987”• “Article 78. Additional Incentives. – A zone enterprise shall also enjoy all the incentive

benefits provided in Article 39 hereof under the same terms and conditions stated therein. In addition, zone registered enterprises shall also be entitled to the following:

• (a) Exemption from Local Taxes and Licenses. – Notwithstanding the provisions of law to the contrary, zone registered enterprises shall, to the extent of their construction, operation or production inside the zone be exempt from the payment of any and all local government imposts, fees, licenses or taxes except real estate xxx machineries owned by zone registered enterprises which are actually installed and operated in the Zone for manufacturing, processing or for industrial purposes shall not be subject to the payment of real estate taxes for the first three (3) years of operation of such machineries xxx”

• (b) Production equipment or machineries, not attached to real estate, used directly or indirectly, in the production, assembly or manufacture of the registered product of the zone registered enterprise shall be exempt from real property taxes.”

61

EXEMPTION FROM LOCAL TAXES

3. PEZA-registered economic zone enterprises availing of the 5% GIT Incentive are exempted from payment of all national and local taxes, except real property tax on land owned by developers.

62

LOCAL TAX EXEMPTION OF FIRMS UNDER THE GIT REGIMELegal Basis:

Republic Act No. 7916: “The Special Economic Zone Act of 1995”, as amended by R.A. No. 8748

• Section 24. Exemption from National and Local Taxes.• Except for real property taxes owned by developers, no taxes, local and

national, shall be imposed on business establishments operating within the ECOZONE. In lieu thereof, five percent (5%) of the gross income earned by all business enterprise within the ECOZONE shall be paid and remitted. . .x x x. . .

• Bureau of Internal Revenue’s Revenue Regulations No. 12-97: “Regulations Implementing Section 24 of RA 7916 defines “local taxes”

• i. “Local Taxes” – shall refer to all local taxes, business taxes, real estate taxes, and other taxes, fees and charges imposed by local government units pursuant to the Local Government Code of 1991, as amended.”

63

SALE OF REAL PROPERTIESBIR Rulings

FIRM UNDER ITH REGIME– RCIT on gain if ordinary asset– 6% CGT if capital asset– DST

FIRM UNDER GIT REGIME– 5% on the net gain– No DST; DST payable by buyer if buyer is not

exempt

64

PEZA RULES ON IT ENTERPRISES, PARKS AND BUILDINGS

PEZA Board Resolution No. 00-411, December 29, 2000

65

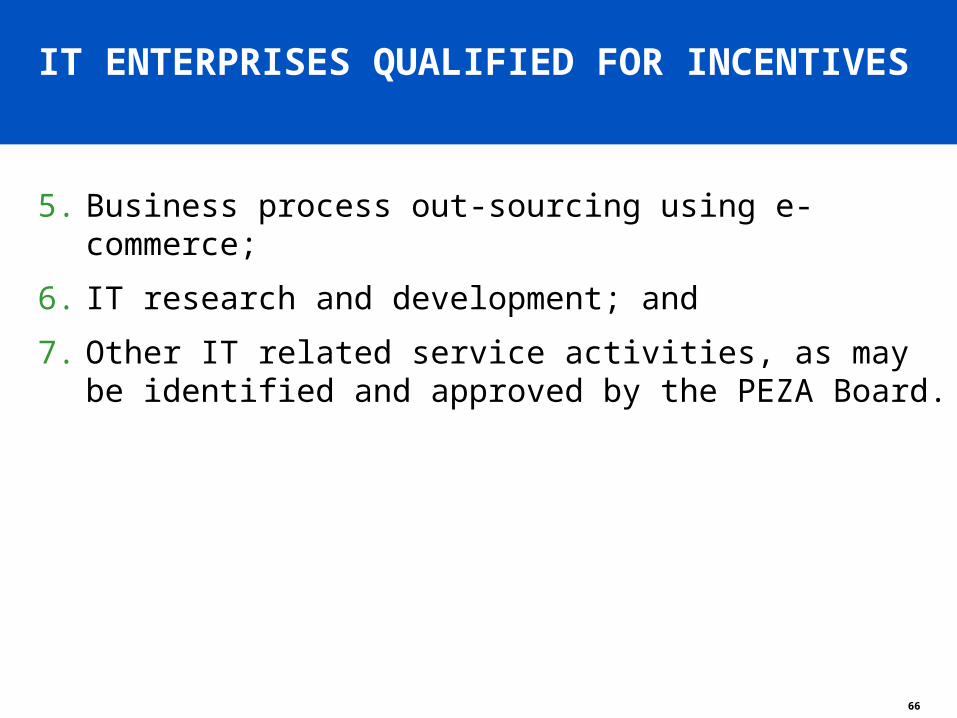

IT ENTERPRISES QUALIFIED FOR INCENTIVES

1. Software development and application, including programming and adaptation of system softwares and middlewares, for business, media, e-commerce, education, entertainment, etc.;

2. IT-enabled services, encompassing call center, data encoding, transcribing and processing; directories; etc.;

3. Content development for multi-media or internet purposes;

4. Knowledge-based and computer-enabled support services, including engineering and architectural design services, consultancies, etc.;

66

IT ENTERPRISES QUALIFIED FOR INCENTIVES

5. Business process out-sourcing using e-commerce;

6. IT research and development; and

7. Other IT related service activities, as may be identified and approved by the PEZA Board.

67

INCENTIVES TO IT ENTERPRISES

1. ITH - 4 years for non-pioneer, 6 years for pioneer 2. After ITH, 5% tax on GIE, in lieu of national and local

taxes, except RPT on land owned by developers;3. Exemption from import duties and taxes on imported

machinery and equipment and raw materials;4. Additional deduction equivalent to 50% of training

expense, chargeable against the 3% share of the NG5. Permanent resident status for foreign investors with initial

investments of US$ 150,000 or more6. Employment of non-resident aliens required in the

operation of IT enterprises; and7. Other incentives, as may be determined by the PEZA

Board.

68

IT BUILDINGS

• Required facilities (minimum)

1. High speed fiber optic telecommunication backbone and high-speed international gateway facilities or wide-area network (WAN); or any high -speed data telecommunication system that may become available in the future;

2. Clean uninterruptible power supply; and3. Computer security and building, monitoring and

maintenance systems .

69

IT PARKS & BUILDINGS

• IT Parks may be located within or outside Metro Manila

• IT building can only locate within Metro Manila.

70

IT PARKS & BUILDINGS

• An IT park or building in Metro Manila may be an existing, new or proposed complex or building with a minimum available business floor area of 5,000 sq. m. (excluding parking areas and roof gardens).

• Owners or developers of PEZA-registered IT Parks and Buildings in Metro Manila, except those already proclaimed prior to the approval of these guidelines including facilities providers, shall not be entitled to PEZA incentives.

• IT parks outside Metro Manila shall have a minimum land area of 5 hectares. They shall be entitled to the following incentives:

71

IT PARKS & BUILDINGS

IT parks outside Metro Manila shall have a minimum land area of 5 hectares. They shall be entitled to the following incentives:

1. ITH 4 or 6 years for IT zones located in less developed areas listed in the IPP, on income locator IT enterprises and related operations;

2. After ITH, the option to pay a special 5% tax on gross income earned from locator IT enterprises and related operations, in lieu of national and local taxes, except real property taxes on land owned by developers;

3. Permanent resident status of foreign investors with initial investment of US$ 150,000 or more; and

4. Employment of non-resident aliens required in the operation of IT enterprises

72

VAT REGIME FOR PEZA

73

VAT TREATMENT

PEZA- REGISTERED

WHETHERITH,5%, OR

RCIT

PEZA-REGISTERED

5%

PEZA- REGISTERED

ITHOr

RCIT

G & S

EXEMPT

S

G

0%

EXEMPT

G & S

0%

EXEMPT

VAT- REGISTERED

VAT- EXEMPT

G & S

VAT

74

INCOME TAX TREAMENT

PEZA- PEZA- REGISTEREDREGISTERED

WHETHERWHETHERITH,ITH,5%,5%,

GOODSGOODS

INCOME5% or ITHRCIT on excess over threshhold

BUYERBUYERFROM FROM

CUSTOMSCUSTOMSTERRITORYTERRITORY

SERVICSERVICEE

INCOME->RCIT

75

FILING AND PAYMENT . . .

76

Shall be paid and remitted as follows:

Payment of 5% Gross Income Tax

Three percent (3%) to the National Government

Two percent (2%) to the treasurer’s office of the municipality or city where the enterprise is located

- Rev. Regs. No. 1-2000

77

• After payment of 3% of the 5% tax to the BIR, all copies of the returns shall be stamped received .

• The enterprise pays 2% of the tax to the concerned city / municipal treasurer.

- Rev. Regs. No. 1-2000

Returns and Payment of the Tax

78

•Quarterly ITR - within sixty (60) days after the close of each of the first three (3) quarters

•Final adjustment ITR covering the entire taxable year - not later than the fifteenth (15) day of the fourth (4th) month following the close of its taxable year, whether calendar or a fiscal year accounting period.

- Rev. Regs. No. 1-2000

Returns and Payment of the Tax

79

Returns and Payment of the Tax

Quarterly and final adjustment income tax returns shall be accomplished in 5 copies showing among others:

1. Gross income for the period

2. Amount showing the 5% tax on such gross income earned

3. Amount representing the 2% share of the city/municipality

80

4. In case the enterprise occupies a parcel of land situated within the territorial boundaries of two or more cities/ municipalities, the area of land within the jurisdiction of each city/municipality and the share from the tax of each city / municipality.

Note: PEZA shall issue certification as to the exact share of the concerned cities/ municipalities from the 2% tax as allocated under the implementing rules of PEZA.

Returns and Payment of the Tax

81

Additional Attachments to the Return

All ECOZONE establishments shall secure on an annual basis a certification from PEZA stating that:

1. the establishment is a bona-fide PEZA-registered establishment entitled to the 5% special tax on gross income;

2. Whenever applicable, the percentage allocation of the 2% share in case of overlapping municipalities / cities.

- Rev. Regs. No. 1-2000

82

The power to audit & assess the 5% special income tax shall be under the exclusive jurisdiction of the Commissioner of Internal Revenue.

- Rev. Regs. No. 1-2000

Tax Examination

83

Authority of the BIR Commissioner over PEZA enterprises expanded to include the power -

To abate, cancel, or compromise the payment of the said tax

To implement special voluntary payment program/s for last priority in audit, subject to the approval of the Secretary of Finance in cases where such approval is necessary.

- Rev. Regs. No. 27-02

Tax Examination

84

Payment of Deficiency Tax

• Three-fifth (3/5th) ) or sixty percent (60%) of the 5% special income tax assessed, inclusive of increments shall be collected by the Commissioner or his duly authorized representative.

• Two-fifth (2/5th) or forty percent (40%) thereof shall be collected by the concerned city/municipality

– The same proportionate tax share shall be observed in case of abatement, cancellation, compromise or implementation of a special voluntary payment program.

- Rev. Regs. No. 27-02

85

Refund/Credit of Erroneously Paid 5% Special Tax

1) In the case of the 3% tax share of the National Government – Shall be refunded or credited by the BIR

2) In the case of the 2% tax share of the city / municipality– Shall be refunded by such city/ municipality.

- Rev. Regs. No. 27-02

86

Transition Issues

87

After ITH

PEZA enterprise is subject to 5% preferential tax regime.

88

ITH expired in the middle of the taxable period...

89

ITH expired in the middle of the taxable period...

90

NOLCO during ITH

Accumulated net operating losses incurred or sustained during the period when a person enjoys exemption from

income tax shall not qualify for purposes of NOLCO.

- Rev. Regs. No. 14-01

91

Any Questions?