pitchbook a4us template - investor relations - todayir.com · 2011-08-15 · do not refresh this...

TRANSCRIPT

Do not refresh this file

Agenda

Page

K:\Share\Design\For Presentations Use\Template Design_Stylesheet.ppt

2011 Interim Results Announcement

August 2011

Do not refresh this file

1

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Disclaimers

These materials and the subsequent discussion are not an offer for sale of any securities of China Hongqiao Group Limited (the

“Company”). The distribution of these materials in certain jurisdictions may be restricted by law and therefore persons into whose

possession of these should inform themselves about and observe any such restrictions. Any failure to comply with these

restrictions may constitute a violation of the securities laws of such jurisdiction.

Certain financial information contained herein has not been audited, comforted, confirmed or otherwise covered by a report by

independent accountants. In addition, past performance of the Company cannot be relied on as a guide to future performance.

These materials and the subsequent discussion contain statements about future events, projections, forecasts and expectations

that are forward-looking statements. Any statement in these materials that is not a statement of historical fact is a forward-looking

statement that involves known and unknown risks, uncertainties and other factors which may cause our actual results,

performance or achievements to be materially different from any future results, performance or achievements expressed or

implied by such forward-looking statements. The Company makes no representation on the accuracy and completeness of any

of the forward-looking statements, and, except as may be required by applicable law, assumes no obligations to supplement,

amend, update or revise any such statements or any opinion expressed to reflect actual results, changes in assumptions or in

the Company‟s expectations, or changes in factors affecting these statements. Accordingly, any reliance you place on such

forward-looking statements will be at your sole risk.

Do not refresh this file

2

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

2. Financial Review

4. Operations Review

5. Future Plans

1. Major Achievements

6. Q&A

3. Industry Overview

Do not refresh this file

3

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Major achievements

Significant growth in

revenue and profits

2

Strengthened production

capacity and market position

3

Successful listing on SEHK

1

Do not refresh this file

4

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Successful listing on SEHK

China Hongqiao (―CHQ‖) was successfully listed on

the Main Board of SEHK on 24 March 2011

Market cap*:HKD 35.6 billion

Enhanced international profile and market position

Strengthened financial position to accommodate

future expansion

Optimized shareholder base

* Based on closing price on 12 August 2011

Do not refresh this file

5

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

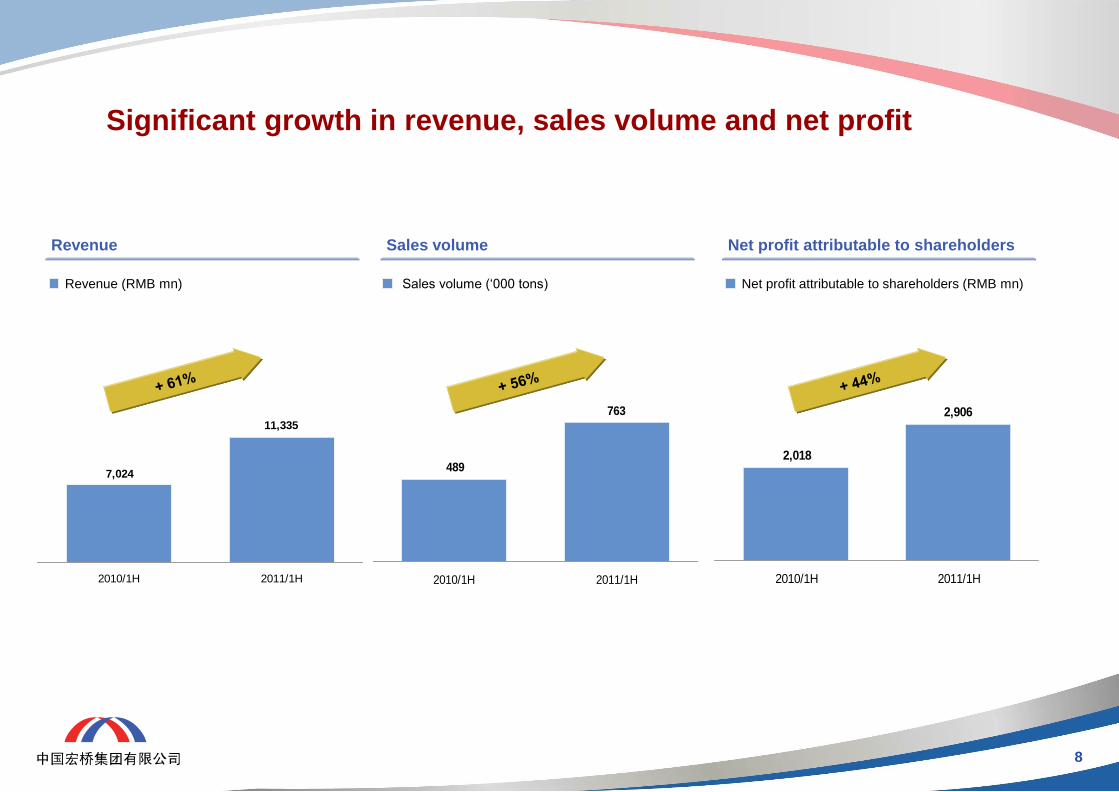

Significant growth in revenue, sales volume and profits

Major reasons:

Strategically located within an end-to-end

aluminum industry cluster, resulting in

overall cost savings

Proven cost structure advantage with large

scale, highly efficient captive power plant

and self-constructed power grid, as well as

cost-competitive and stable alumina supply

Significant increase in sales volume and

average selling price (ASP) driven by

vigorous industry demand

Expanded production capacity to

successfully capture market opportunities

Revenue

+ 61%

Volume

+ 56%

Net profit

attributable to

shareholders

+ 44%

Do not refresh this file

6

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Strengthened production capacity and market position

CHQ has successfully become the 4th largest aluminum producer in China

Source: Antaike

Chinese aluminum producers by capacity as of 30 June 2011

4 China Hongqiao Group Ltd 1481 Private company

Rank C ompany Capacity (ktpa) Ownership background

1 CHALCO 4,560 State owned enterprise

2 China Power Investment Corp. 2,135 State owned enterprise

3 Shandong Xinfa 1,800 Private company

4 China Hongqiao Group Ltd 1,481 Private company

5 He nan Shenhuo Group 900 Local state owned enterprise

6 Henan Yulian Energy Group 850 Private company

7 Yichuan Power Industry Group 840 Local state owned enterprise

8 East Hope Baotou Rare Earth 800 Local state owned enterprise

Do not refresh this file

7

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

2. Financial Review

4. Operations Review

5. Future Plans

1. Major Achievements

6. Q&A

3. Industry Overview

Do not refresh this file

8

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Significant growth in revenue, sales volume and net profit

11,335

7,024

2010/1H 2011/1H

Revenue (RMB mn)

Revenue

763

489

2010/1H 2011/1H

Sales volume („000 tons)

Sales volume

2,906

2,018

2010/1H 2011/1H

Net profit attributable to shareholders (RMB mn)

Net profit attributable to shareholders

Do not refresh this file

9

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

2,735

4,049

38.9%35.7%

2010/1H 2011/1H

3,032

4,454

43.2%39.3%

2010/1H 2011/1H

2,751

4,073

39.2% 35.9%

2010/1H 2011/1H

2,011

2,906

28.6% 25.6%

2010/1H 2011/1H

Profitability

¹ From continuing operations

Gross profit¹ EBITDA¹

EBIT¹ Net profit¹

EBIT margin EBIT (RMB mn)

Gross margin Gross profit (RMB mn) EBITDA margin EBITDA (RMB mn)

Net margin Net profit (RMB mn)

Do not refresh this file

10

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

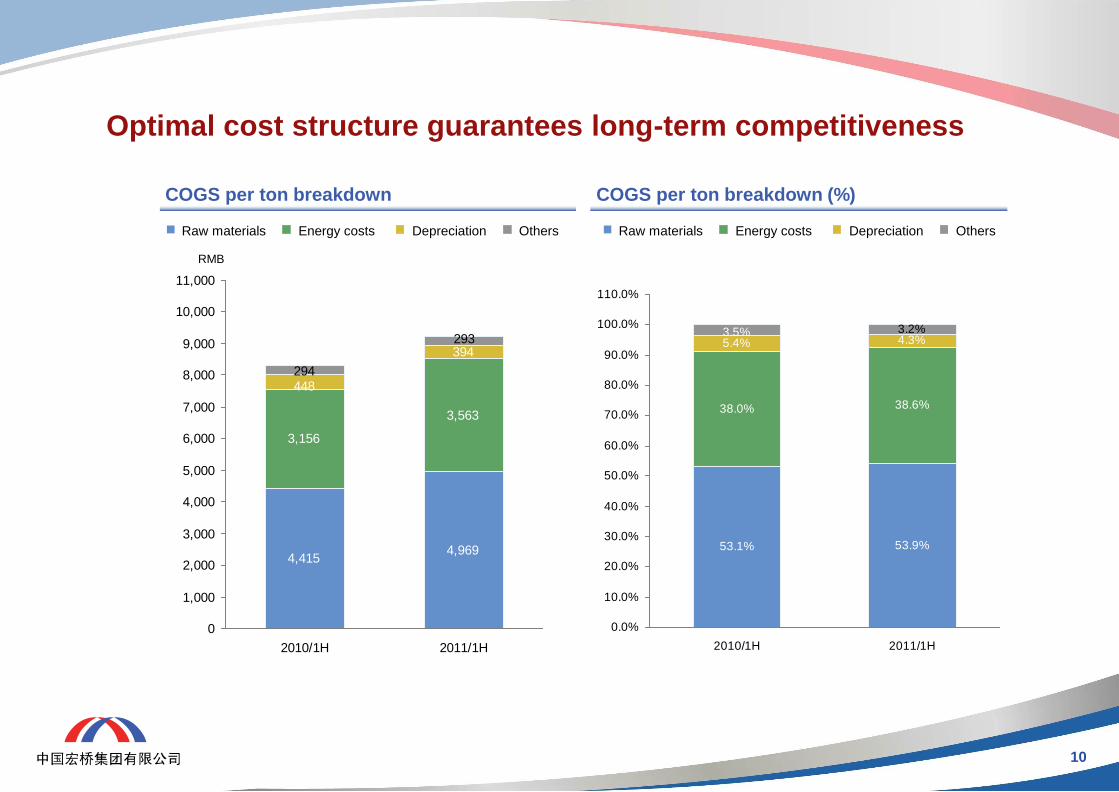

Optimal cost structure guarantees long-term competitiveness

Depreciation

COGS per ton breakdown COGS per ton breakdown (%)

Raw materials Energy costs Depreciation Others Others Raw materials Energy costs

4,4154,969

3,156

3,563

394

448294

293

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

2010/1H 2011/1H

53.1% 53.9%

38.0% 38.6%

5.4% 4.3%3.2%3.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

110.0%

2010/1H 2011/1H

RMB

Do not refresh this file

11

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Prudent financial management

As of 30 Jun 30 2011

RMB mn 2011 2010 Change (%)

Cash & cash equivalents 7,575 1,039 + 629.1

Total capital (equity book value + total

debt)

20,089 9,586 + 109.6

EBITDA / Interest expense (times) 30.9 43.3 - 12.4 times

Debt / EBITDA (times) 0.52 0.74 - 0.22 times

Debt / Total capital 23% 47% - 24 p.p.

Trade receivables turnover days (day) 0.1 0.6 - 0.5 day

Trade payables turnover days (day) 30 14 + 16 days

Inventory turnover days (day) 33 31 + 2 days

Do not refresh this file

12

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

2. Financial Review

4. Operations Review

5. Future Plans

1. Major Achievements

6. Q&A

3. Industry Overview

Do not refresh this file

13

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0 Current gap between production and consumption of

primary aluminum in China and the world

Source: Antaike

„000 tons

Production volume

Consumption volume

Production volume

Consumption volume „000 tons

Global production & consumption of primary aluminum China‘s production & consumption of primary aluminum

3,8603,905

3,7573,793

3,372

3,699

4,0073,979

3,8513,849

3,339

3,599

2,500

3,000

3,500

4,000

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

1,494

1,357

1,571 1,5901,662 1,660

1,496

1,379

1,6611,731

1,800

1,897

500

1,000

1,500

2,000

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

+100

+33

-56 -94

-74 -147

-2 -22

-90 -141

-138 -237

Production / consumption gap Production / consumption gap

Do not refresh this file

14

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

London Metal Exchange (LME)

Shanghai Futures Exchange (SHFE)

Source: LME, SHFE, Antaike

Aluminum prices in 1H 2011

Aluminum prices have remained strong since 2H 2010 as a result of the vigorous market demand

ASP of CHQ‟s aluminum products increased by 5.5%, from RMB13,655 / ton in 1H 2010 to

RMB14,405 / ton in 1H 2011

1,500

1,700

1,900

2,100

2,300

2,500

2,700

2,900

Jul-

10

Aug-

10

Sep-

10

Oct-

10

Nov-

10

Dec-

10

Jan-

11

Feb-

11

Mar-

11

Apr-

11

May-

11

Jun-

11

13,500

14,000

14,500

15,000

15,500

16,000

16,500

17,000

Jul-

10

Aug-

10

Sep-

10

Oct-

10

Nov-

10

Dec-

10

Jan-

11

Feb-

11

Mar-

11

Apr-

11

May-

11

Jun-

11

USD/ton RMB/ton

Do not refresh this file

15

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

China continues to drive world consumption

China‘s primary aluminum consumption

breakdown – by industry (2010) Global primary aluminum consumption (2010)

Construction

40.0%

Transportation

15.5%

Electrical

15.5%

Durables

12.0%

Machineries

4.9%

Others

8.0%

China

41%

Japan

5% Other Asia

12%

Germany

5%

Other Europe

16%

Mid East & Africa

5%

U.S.

10%

Other N. America

& S. America

6%

Packaging

4.1%

Source: Antaike

Do not refresh this file

16

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Widening gap between supply and demand

Ex-China supply growing ahead of demand

The unbalanced supply and demand in China

Source: China Zhongjing

Global supply & demand balance (‗000 tons)

Ex-China global supply & demand balance (‗000 tons)

China‘s supply & demand balance (‗000 tons)

8,000

6,000

4,000

2,000

0

-2,000

2,000

0

-2,000

-4,000

-6,000

-8,000

-10,000

Do not refresh this file

17

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

2. Financial Review

4. Operations Review

5. Future Plans

1. Major Achievements

6. Q&A

3. Industry Overview

Do not refresh this file

18

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Revenue breakdown – by product

Aluminum

products

Steam TOTAL

Revenue (RMB mn) 1H 2011 10,987 348 11,335

1H 2010 6,673 351 7,024

% of total revenue 1H 2011 96.9 3.1 100

1H 2010 95.0 5.0 100

Volume (ton) 1H 2011

766,019 2,623,080

1H 2010 496,973 2,645,040

GP margin (%) 1H 2011

36.0 26.7 35.7

1H 2010 39.1 35.3 38.9

Do not refresh this file

19

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

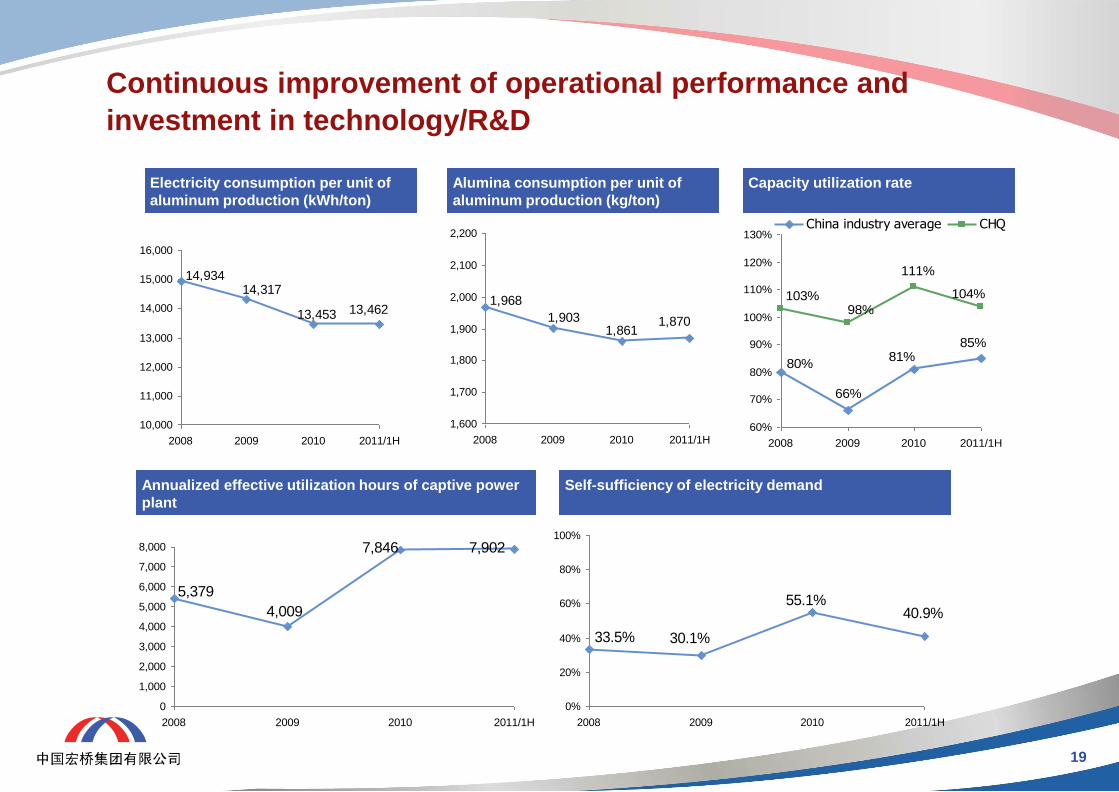

0 Continuous improvement of operational performance and

investment in technology/R&D

13,46213,453

14,31714,934

10,000

11,000

12,000

13,000

14,000

15,000

16,000

2008 2009 2010 2011/1H

1,8701,861

1,903

1,968

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2008 2009 2010 2011/1H

5,379

4,009

7,846 7,902

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2008 2009 2010 2011/1H

40.9%55.1%

30.1%33.5%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011/1H

Electricity consumption per unit of

aluminum production (kWh/ton)

Alumina consumption per unit of

aluminum production (kg/ton)

Capacity utilization rate

Annualized effective utilization hours of captive power

plant

Self-sufficiency of electricity demand

80%

66%

81%85%

103%98%

111%

104%

60%

70%

80%

90%

100%

110%

120%

130%

2008 2009 2010 2011/1H

China industry average CHQ

Do not refresh this file

20

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0 Low cost electricity supply – large scale, highly efficient

captive power plant & self-constructed power grid

Self-generated electricity in 1H 2011 ~RMB0.22/kWh,

significantly cheaper than procured from state grid

40.9% energy self-sufficient for 1H 2011

Capex planned to further increase self-sufficiency

Connects CHQ‟s three manufacturing facilities with external

supplier, Gaoxin

Long term contract @ RMB0.29/kWh1

Purchased 88% of Gaoxin‟s output in 1H 2011

1 Assuming that the base price of coal with a heat value of 5,000 kilocalorie per kilogram is RMB700 per ton (inclusive of VAT), which is subject to adjustment through negotiation

if the price fluctuation of coal exceeds 20% 2 Source: Antaike; 2011 data

Captive power plant External electricity supply from Gaoxin

1,080 MW thermal power plant Private self-constructed power grid

20

Resulting in electricity cost saving of RMB2,150 / ton at RMB26 cents/kWh (excluding VAT),

16 cents/kWh2 lower than China average

Do not refresh this file

21

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Method of external

electricity purchase

On-grid electricity charge Direct supply agreement + Wheeling

charge to state grid

Direct supply agreement + Self-owned

power grid

Direct electricity

supply agreement

No Yes Yes

Self-owned power

grid

No No Yes

Features Direct purchase from state grid in

accordance with stipulated pricing

policies

Have large scale power generating

companies nearby with abundant

supply

Have large scale power generating

companies nearby with abundant

supply

Private power grid and electricity

supply network

Entry barrier Low Medium High

Price Minimum price ~ RMB0.55/kWh1; price controlled by government Over RMB0.405/kWh1 (wheeling cost of

RMB0.15-0.20/kWh1 required)

~ RMB0.25-0.30/kWh1; price mainly

determined by electricity cost & mutual

business agreement; relatively low policy

risks

1. Directly purchase from state grid

Primary aluminum

producers

Electricity

supply

company 1

Electricity

supply

company 2

Electricity

supply

company

N

…

On-grid charge

2. Direct supply agreement +

wheeling charge to state grid

Direct electricity

supply companies

Wheeling

charge

3. Direct supply agreement +

Self-owned power grid

Primary aluminum

producers

Direct electricity

supply companies

Off-grid

electricity

charge Self-constructed

power grid

CHQ‘s unique

power supply

model

Off-grid

electricity

charge

Primary aluminum

producers

CHQ‘s unique external power supply model

1Forecasts of management

Do not refresh this file

22

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Reliable and cost-competitive alumina supply

Alumina cost comparison (RMB/t)¹

¹ Average market price based on Antaike data; VAT excluded

Strong partnership with key alumina

supplier — Binzhou Gaoxin

Consumes 60% of its alumina output

Purchased 1,449kt alumina in 1H 2011

Long-term contract

Competitive costs

Approx. RMB500/t below the price at

which Gaoxin sells to others

Geographic proximity

Saves freight, packaging, loading and

offloading costs

Reliable alumina supply

Gaoxin‟s long-term contract for importing

bauxite

CHQ‟s well-planned policy to secure

stable alumina supply in long-term

1,795

1,6211,712

2,4952,379

3,148

2,885

2,332

2,350

2,0002,106

1,982

2,752

2,980

2,345

1,000

1,500

2,000

2,500

3,000

3,500

2007 2008 2009 2010 2011/1H

CHQ (long-term agreement)

Industry average

Gaoxin selling to others

Do not refresh this file

23

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

2. Financial Review

4. Operations Review

5. Future Plans

1. Major Achievements

6. Q&A

3. Industry Overview

Do not refresh this file

24

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Urbanization &

Infrastructure

Development

Critical stage for China‟s rapid urbanization to reach the level of moderately developed

countries. Increase in per capital income will lead to rapid domestic consumption growth.

Urbanization rate in China is expected to reach 54.7% by 2015. Growing at an average of

18.87mn, newly added urban population amounts to 94.35mn. Urbanization will drive an

increase in average living area by 566mn sq.m annually, creating a demand of 370,000

tons of aluminum for housing construction (assuming 30 sq.m of living area per capita);

350mn people will migrate to the cities by 2025.

China‟s total construction area amounts to 50bn sq.m, of which 10% needs to be

refurbished each year, demanding 3.3mn tons of aluminum products p.a.

36mn units of affordable housing to be developed in 5 years (10mn to be started in 2011),

generating a demand of 1.66mn tons of aluminum (assuming each unit is 70 sq.m. in size)

Transportation

Largest auto and rail transportation market in the world.

Auto production reached 18.26mn tons in 2010, with aluminum usage per vehicle of

127.5kg, which is 12% lower than that in US (145kg), and 13% lower than Japan and

Germany.

Auto production is expected to reach over 30mn vehicles by 2020. Assuming China‟s

aluminum usage per vehicle will reach the current level of developed countries (i.e. 150kg),

aluminum consumption of China‟s auto industry will amount to 4.5mn tons, almost doubling

that in 2010 (2.35mn tons).

Key industry trends in China

Substitute for

other metals

Aluminum replacing copper in the power industry and appliance production.

Replacing steel due to lighter weight (e.g. components in cars).

Solid underlying fundamentals to drive growth

Source: China Zhongjing

Others Growing aluminum demand by packaging industry (e.g. beverage packaging), accounting

for 4% of total processed aluminum in downstream markets.

Do not refresh this file

25

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Expanding production capacity and electricity production facilities

to further enhance market penetration and cost structure

产能扩张(万吨) Captive power plant production capacity expansion (MW)

New captive thermal power plant with capacity 1,320 (4 x 330) MW

Capex: approximately RMB4.6bn

Expected to increase self-sufficiency to approx. 65-70% based on

estimated electricity consumption requirement of 1,776ktpa aluminum

production capacity

New primary aluminum capacity of 300ktpa at Zoupin and Weiqiao

production base in 2H 2011

Aluminum downstream processing with capacity of 30ktpa at Binzhou

production base

Capex: approximately RMB3.8bn

Production capacity expansion (ktpa)

1,776

1,481

Jun 2011 End of 2011

2,400

1,740

1,080

Jun 2011. 2H 2011 2H 2012

Do not refresh this file

26

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Extending its reach into upstream and downstream markets

Generate plans to enter the upstream resources market (e.g. bauxite, alumina and coal), in

order to secure stable supply of raw materials

Further enhance profitability and market competitiveness by prudently extending into the

downstream market

Aluminum downstream processing is expected to commence in 2H 2012, with an aggregate

designed annual production capacity of 30,000 tons

Coal Alumina Bauxite Feedstock for

aluminum foil

Do not refresh this file

27

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

Strategies

Increase market penetration

through capacity expansion

Optimize cost structure via

continuous R&D improvements

Extend into upstream and

downstream markets

1

3

4

CHQ mission:

To become the

strongest

manufacturer of

integrated

aluminum

products in China

Expand captive power plant to

enhance self-sufficiency and

stability of electricity

2

Do not refresh this file

28

JP

M c

olo

r 1

R1

00

.G1

44

.B20

3

JP

M c

olo

r 2

R9

5.G

163

.B10

0

JP

M c

olo

r 3

R2

14

.G1

88

.B5

6

JP

M c

olo

r 4

R1

49

.G1

21

.B1

61

JP

M c

olo

r 5

R2

13

.G1

39

.B70

JP

M c

olo

r 7

R1

71

.G1

31

.B65

JP

M c

olo

r 6

R9

1.G

165

.B16

3

JP

M c

olo

r 8

Co

nc

lus

ion

R1

50

.G15

0.B

150

Hig

hlig

ht

R153.G

0.B

0

White

R2

55

.G2

55

.B25

5

2nd, 3

rd&

4th

leve

l Bulle

t

Lt. d

ivid

er lin

e

R1

92

.G1

92

.B19

2

Text

R0

.G0

.B0

1st le

vel b

ulle

t

R1

00

.G1

44

.B20

3

Ta

ble

co

lum

n

he

ad

ing

sh

ad

ing

R2

34

.G2

34

.B2

34

Connecto

r lines

Dk. d

ivid

er lin

e

128.G

128

.B12

8

Object Foundation

Ta

ble

hig

hlig

ht

R2

14

.G2

24

.B2

36

Slid

e title

s

R1

51

.G1

6.B

13

Obje

ct T

itles

Age

nd

a h

ighlig

ht

R6

0.G

92.B

17

0

2. Financial Review

4. Operations Review

5. Future Plans

1. Major Achievements

6. Q&A

3. Industry Overview