policy changes, trade tensions & disputes: focus on grains & pulses policy disputes...

TRANSCRIPT

Policy Changes, Trade Policy Changes, Trade Tensions & Disputes: Focus on Tensions & Disputes: Focus on

Grains & PulsesGrains & Pulses

Policy Disputes Information Consortium

April 23-26, 2003

Montreal, Quebec

Parr Rosson & Flynn Adcock

Texas A&M University

OverviewOverview

• Grain & Pulse Trade: Focus on World & North American Trends

• Farm Program Provisions Related to Pulses

• Potential for Trade Disputes– Corn– Pulses– Dry Beans

• Conclusions & Implications

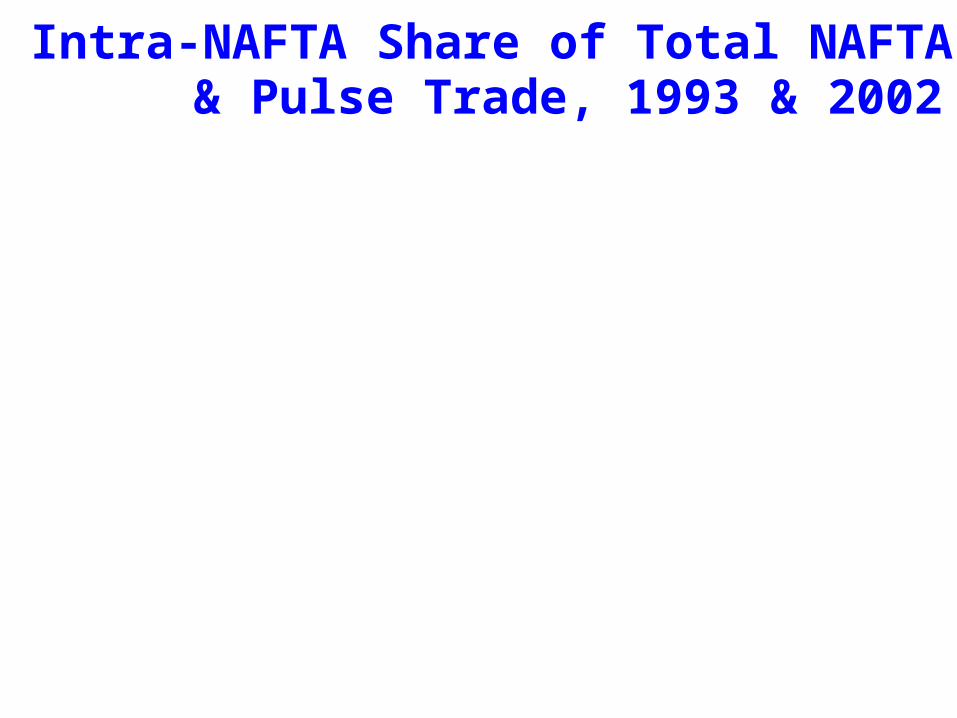

Intra-NAFTA Share of Total NAFTA Grain & Pulse Trade, 1993 & 2002

8.89.6

17.8

10.7

Grains Pulses0

5

10

15

20

Percent

1993 2002

Intra-NAFTA & ROW Grain Trade

10.920.7

112.3

95.3

123.2116.0

1993 20020.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

1,000 Metric Tons

NAFTA ROW Total

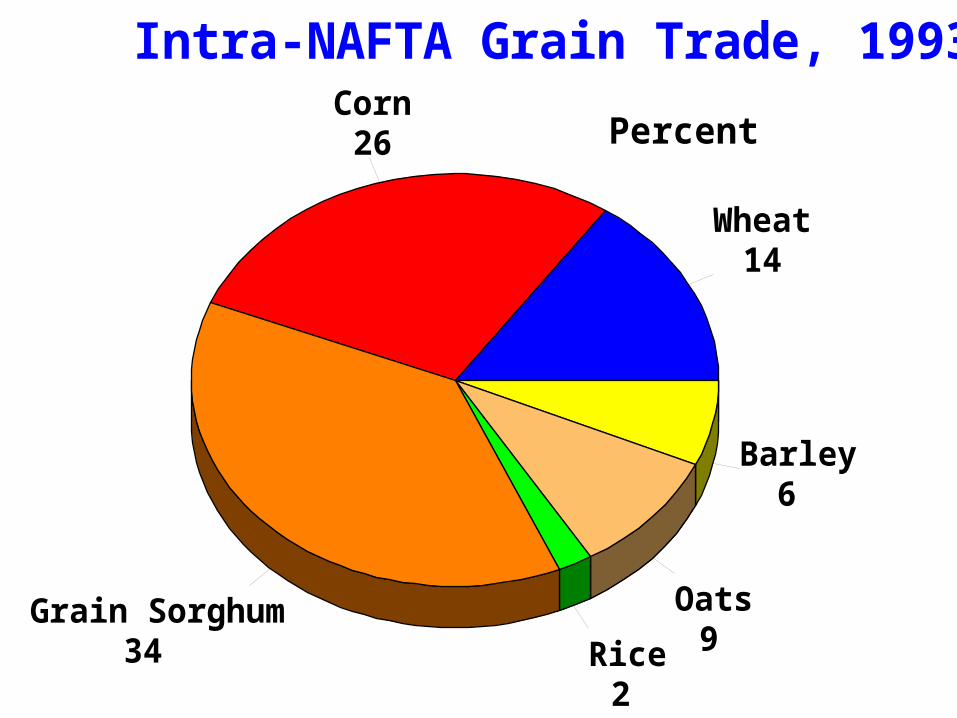

Intra-NAFTA Grain Trade, 1993

Percent

Wheat14

Corn26

Grain Sorghum34 Rice

2

Oats9

Barley6

Intra-NAFTA Grain Trade, 2002

Percent

Wheat11

Corn44

Grain Sorghum20 Rice

4

Oats4

Barley4

Mexican Corn Production

SAGARPA

11

10

12

1010

12 12

11

12 1312

13

34

5

89

66

76

5 5

3

1990 1995 20000

2

4

6

8

10

12

14

Million Metric Tons

Rainfed Irrigated

Intra-NAFTA & ROW Pulse Trade

144350

1359

2910

1503

3260

1993 20020

500

1000

1500

2000

2500

3000

3500

4000

1,000 Metric Tons

NAFTA ROW Total

U.S. Corn Exports to Mexico

Zahniser and Link, ERS, USDA and U. S. Census Bureau.

2.5 2.6 2.6 2.7 2.8 2.9 3.0 3.1 3.23.5

1.3 1.1

0.3

3.1 2.9

6.3

2.6

5.2 5.1 5.25.7

5.3

1990 1994 2000 20020.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Million Metric Tons

TRQ Imports

U.S. Corn Exports to Canada

US Census Bureau

0.7

0.2

0.8 0.8 0.71.0

0.91.0 1.2

1.0

1.5

3.0

4.1

1990 1994 2000 20020.0

1.0

2.0

3.0

4.0

5.0

Million Metric Tons

Intra-NAFTA Pulse Trade, 1993

Percent

Dry Beans50.4%

Dry Peas41.2%

Lentils8.4%

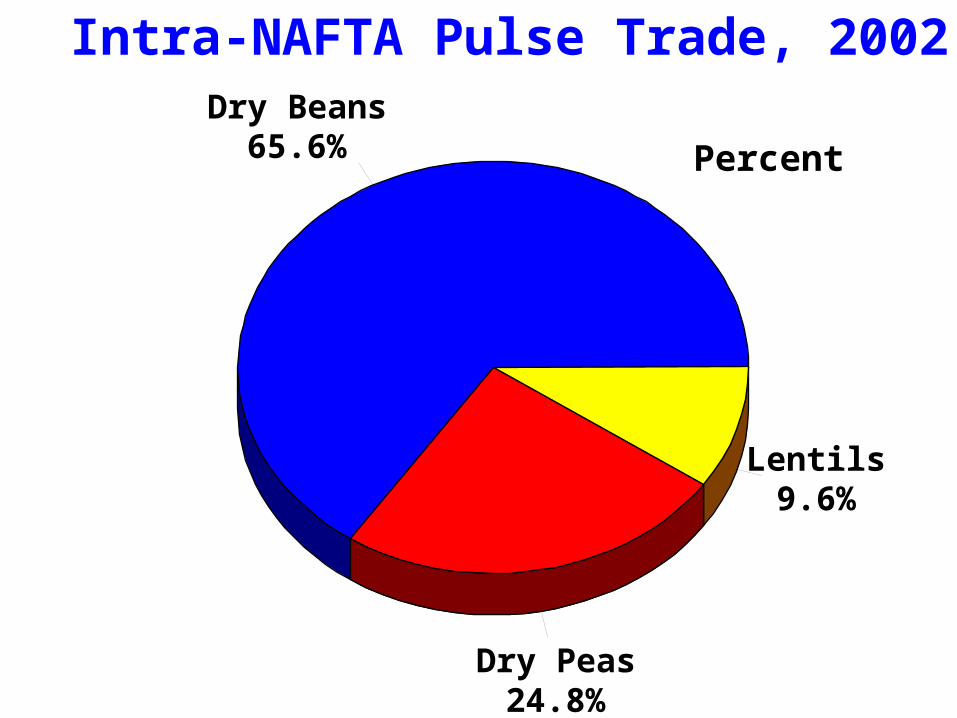

Intra-NAFTA Pulse Trade, 2002

Percent

Dry Beans65.6%

Dry Peas24.8%

Lentils9.6%

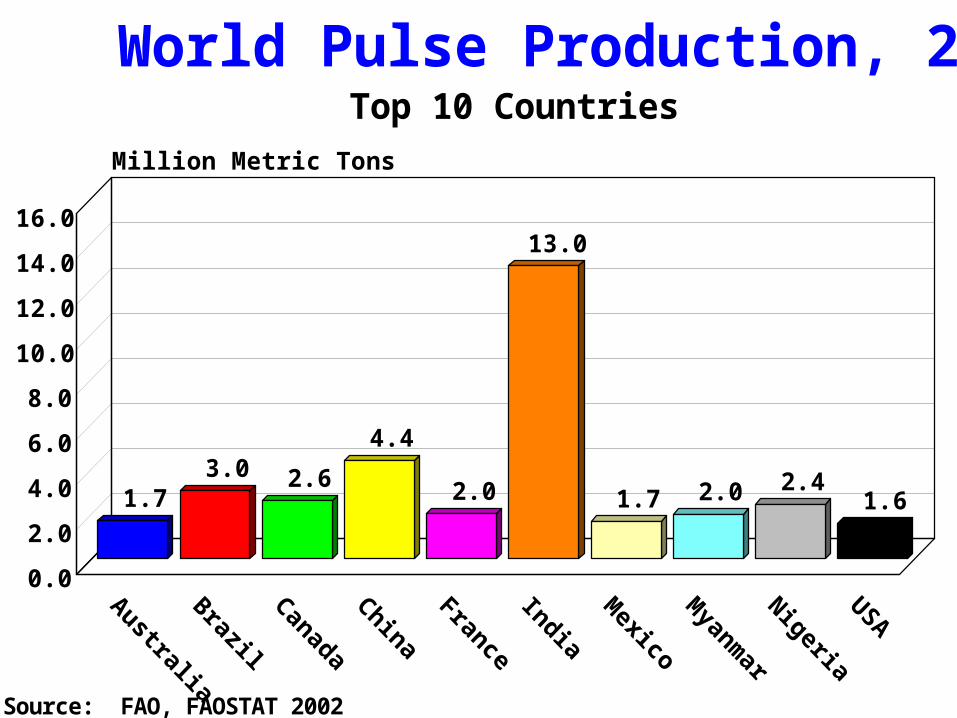

World Pulse Production, 2002Top 10 Countries

Source: FAO, FAOSTAT 2002

1.73.0 2.6

4.4

2.0

13.0

1.7 2.0 2.41.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Million Metric Tons

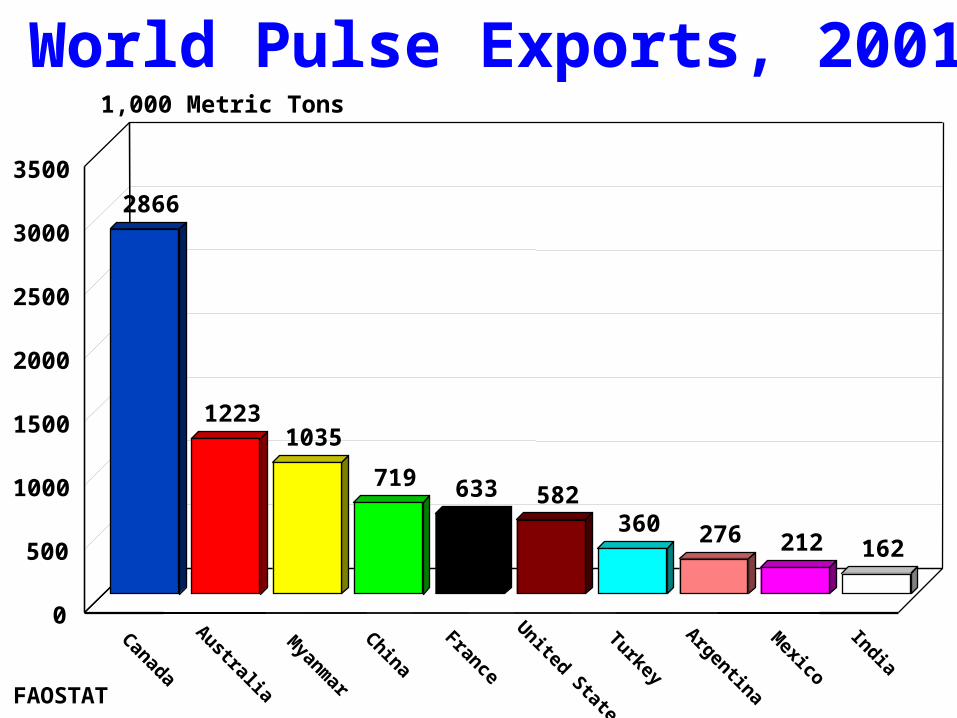

World Pulse Exports, 2001

FAOSTAT

2866

12231035

719 633 582360 276 212 162

Canada

Australia

Myanm

ar

China

France

United States

Turkey

Argentina

Mexico

India

0

500

1000

1500

2000

2500

3000

3500

1,000 Metric Tons

World Pulse Imports, 2001

FAOSTAT

2424

768

451 421 371 371 319 235 228 219

IndiaSpain

Belgium

ItalyPakistan

Egypt

Bangladesh

China

Netherlands

U.S.

0

500

1000

1500

2000

2500

3000

1,000 Metric Tons

World Pulse Trade & OutputWorld Pulse Trade & Output• Canada Dominates World Pulse

Exports, Volumes Nearly Triple Australia, Myanmar

• India Dominates Imports, EU, Middle East, United States

• China, France, United States Are Second Tier Exporters

• India Dominates Production, Triple China, Four Times Brazil

NAFTA Pulse Yields

Source: FAO, FAOSTAT Database

19901991

19921993

19941995

19961997

19981999

20002001

2002

0

0.5

1

1.5

2

2.5

Metric Tons per Hectare

Canada Mexico USA

NAFTA Pulse Production

Source: FAO, FAOSTAT Database

0

1

2

3

4

5

Million Metric Tons

Canada Mexico USA

NAFTA Yields & OutputNAFTA Yields & Output• Pulse Yields in Canada & U.S.

Double Yields in Mexico

• Influences of Ejidatarios on Technology Adoption, Productivity

• Inelastic Supply Response Hypothesis for Mexico

• Role of Mexico’s Farm Policy– $43/acre payment for < 5 hectares

NAFTA Pulse Imports

Source: FAO, FAOSTAT Database

19901991

19921993

19941995

19961997

19981999

20002001

0

50

100

150

200

250

300

350

400

1000 Metric Tons

Canada Mexico USA

NAFTA Pulse Exports

Source: FAO, FAOSTAT Database

19901991

19921993

19941995

19961997

19981999

20002001

0

500

1000

1500

2000

2500

3000

1000 Metric Tons

Canada Mexico USA

NAFTA Pulse TradeNAFTA Pulse Trade• Canada Dominates Trade: 80% of

Exports• U.S. & Mexico Growing as

Importers• U.S. Prices on Downward Trend

Over Most of 1990s• Drought in Canada & Stronger

Export Demand Stimulated Recent Price Increases

U.S. Farm Price for Pulses, 1994-03

ERS, USDA, Vegetables/Melons Outlook, VGS-295, Feb. 25, 2003

1994 1997 2000 2003$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

Lentils Yellow Peas Dry Beans Green Peas

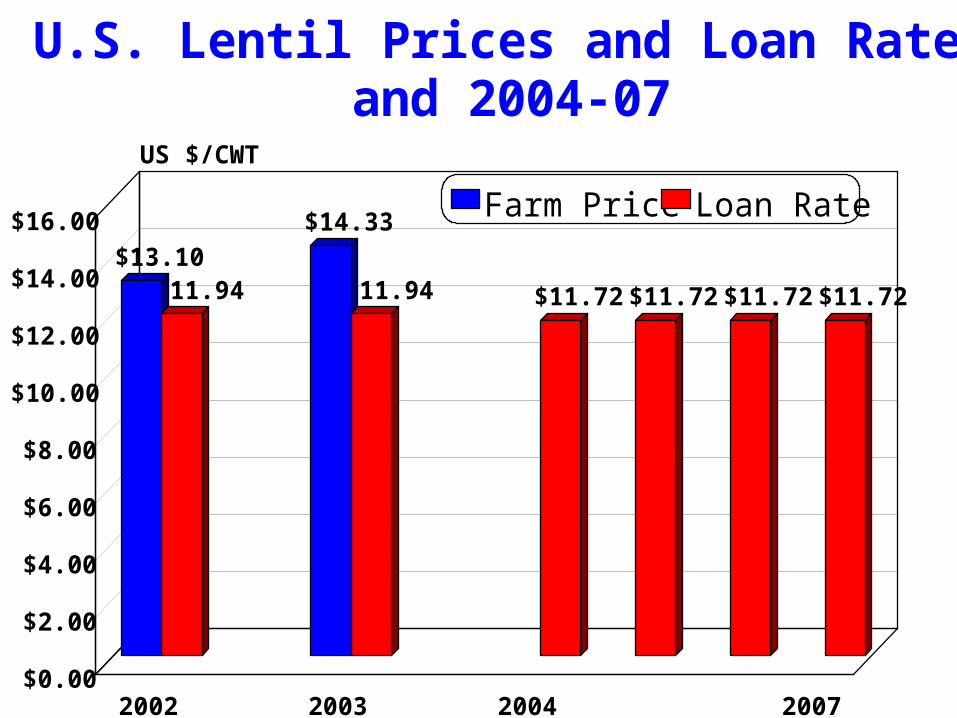

U.S. Lentil Prices and Loan Rates, 2002-03 and 2004-07

$13.10

$14.33

$11.94 $11.94 $11.72 $11.72 $11.72 $11.72

2002 2003 2004 2007$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

US $/CWT

Farm Price Loan Rate

U.S. Dry Pea Prices and Loan Rates, 2002-03 and 2004-07

$8.13$8.43

$6.33 $6.22 $6.22 $6.22 $6.22 $6.22

2002 2003 2004 2007$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

US $/CWT

Farm Price Loan Rate

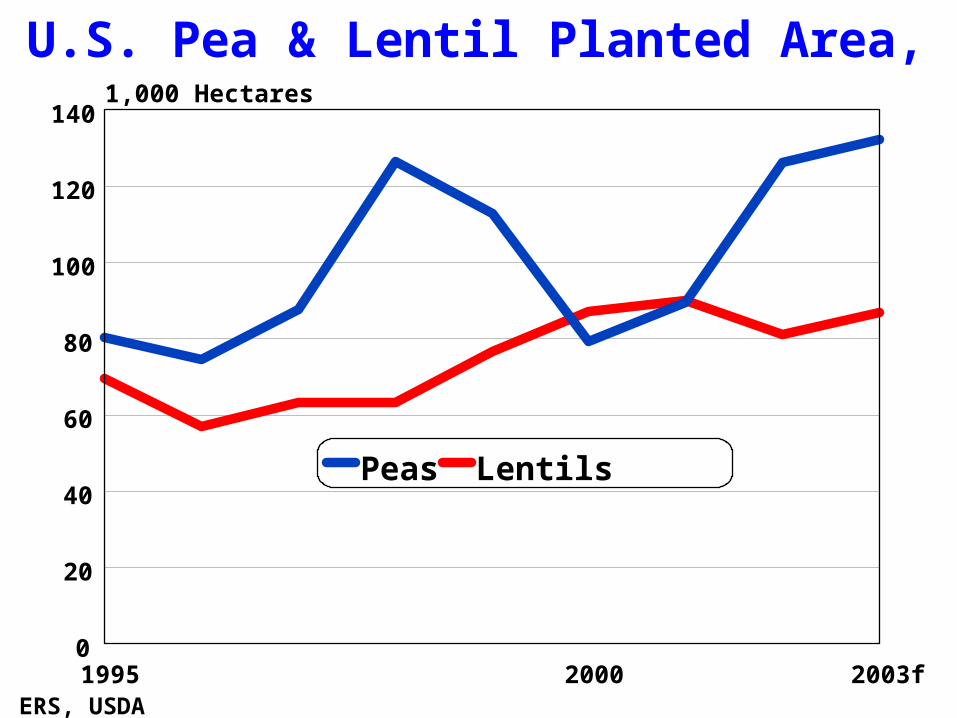

U.S. Pea & Lentil Planted Area, 1995-2003f

ERS, USDA1995 2000 2003f0

20

40

60

80

100

120

1401,000 Hectares

Peas Lentils

U.S. Lentil/Pea and Dry Bean Area

ERS, USDA, 4/17/03 & FAOSTAT: Dry Beans are Planted Area, others are Harvested Area.

1995 2000 2003f0

200

400

600

800

1000

1,000 Hectares

Total Lentils & Peas Dry Beans

Farm Programs & Pulse AreaFarm Programs & Pulse Area• U.S. Farm Prices Above Loan Rates for

Lentils & Peas in 2002 & 2003

• Dry Peas & Lentils Area Up 22% Since 2001/03, Follows Price Increase of 80%

• Dry Bean Area Up 55% Since 2001/02 and 22% 2001/03, After Price Increase of 40%

• Green Pea Prices Up 66% Same Period

• Expansion in Area Began Prior to 2002Expansion in Area Began Prior to 2002

Potential for Trade Disputes• Corn in Mexico: NAFTA Ten Year

Anniversary– U.S. Corn Exports Up 5 Fold since early 1990s– Social Unrest, But Duties Still 90.8%– Mexican Corn Output Down 6% Since 1993– Rainfed Corn Up 22%– Irrigated Corn Down 37%

• Prices in Mexico Down 38% since 1993• 30% of Rainfed Corn is Grown on Ejidos

– Rainfed Corn Represents 70-80% of Total

• 20% Tax on Soft Drinks Made w/HFCS

Corn Trade Issues• Highly Sensitive Issue for Mexico

– Calls to Renegotiate NAFTA

– Spawned ‘Agricultural Armor’ Program

– Permanent Import Limits Being Considered

– Impacts of Imports of Hybrids & GMOs on Traditional Corn Varieties

• Corn in Canada: U.S. Exports Up 4 Fold since mid-1990s, AD Duty Case, StarLink Concerns

• Concerns Focus on Price Impacts & GMOs

Pulse Crops in Farm ProgramPulse Crops in Farm Program

• U.S. Loan Rates Below Market

• Most of Area Expansion Driven by Higher Market Prices

• Drought in Canada & Increased Exports Stimulated Output

• Dry Beans & Peas Traded Most

• Situation Could Change Rapidly

Pulse Trade IssuesPulse Trade Issues• Crop Substitution or Rotation Appear Most

Likely if Pulse Area Expands• Limiting Factors:

– High Market Prices for Pulses & Program Crops– Loan Rates for U.S. No. 1 Quality– Specialized Handling & Market Information– Cultural Practices

• Positive Factors:– Loan Rates Set Lower Limit– Pulses Fix Nitrogen, so Used in Rotation– Cattle Prices

• No Immediate Expansion, Long Term More Difficult to Predict

Dry BeansDry Beans• Mexico Has Doubled Dry Bean Imports

– NAFTA Primary Source: 60-70%

• Prices Down 10-25%

• Expanding World Output Placed Downward Pressure on Prices

• Mexico Supports Dry Beans with Area Payments: $38/acre or $43/acre

Dry Bean Trade IssuesDry Bean Trade Issues• Dry Beans Used in Rotation to Fix

Nitrogen, Improve Soil Structure

• If Wheat, Corn Area Expand Due to U.S. Farm Programs, Will that Stimulate Dry Bean Area?

• Phytosanitary Issues & Under Invoicing by Exporters Noted As Problems by Mexico

Conclusions & ImplicationsConclusions & Implications

• Extent of Trade Disputes/Disruptions– Crop Substitution– Cattle Production Cycles, Herd Rebuilding

& More Normal Weather– Uses of Pulses in Rotation & as Animal

Feeds

• Farm Program Changes in Mexico & Canada May Mitigate Whatever Impacts Occur

• Can’t Ignore World Supply/Demand Balance

Conclusions & ImplicationsConclusions & Implications• Environmental Issues Important

– GMO Concerns– Maintaining Traditional Mexican Corn

Varieties• Protectionist Sentiment is Growing in NAFTA• Farm Programs But One Factor

– Weather, SPS, Exchange Rates• Very Surprised If Trade Disputes Don’t

Increase in Frequency