policyholder exercise behavior for variable annuities ... · policyholder exercise behavior for...

TRANSCRIPT

Policyholder Exercise Behavior for Variable

Annuities including Guaranteed Minimum

Withdrawal Benefits1

Thorsten Moenig2

Department of Risk Management and Insurance, Georgia State University35 Broad Street, 11th Floor; Atlanta, GA 30303; USA

Email: [email protected]

June 2011

1We gratefully acknowledge sponsorship by the Society of Actuaries.2Joint work with Dr. Daniel Bauer, Georgia State University

Page 2 / 23 Overview

1 Introduction

2 A Lifetime Utility Model for Variable Annuities

3 Results

4 Conclusions and Future Research

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 3 / 23 Introduction

1 Introduction

Motivation

Risk-Neutral Valuation Approach

2 A Lifetime Utility Model for Variable Annuities

3 Results

4 Conclusions and Future Research

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 4 / 23 Introduction

Motivation

• Variable Annuities:

I Popular long-term investment vehicles

I Tax-deferred growth

I Investment evolves according to underlying (risky) portfolio

I Uncertain payout

• Guaranteed Minimum (Death / Income / Accumulation /Withdrawal) Benefits

I Insurers offer guaranteed payments

I Policyholders can purchase security

I Similar to (combination of) financial options

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 5 / 23 Introduction

Motivation

• Withdrawal uncertainty

I Could mitigate or intensify insurer’s exposure to investment and/ormortality risks

I Interactions non-trivial

I Affects pricing and risk management

• Insurers in trouble

I Disintermediation in 1970s

I Equitable Life closed to new business in 2000

I The Hartford accepted $3.4B in TARP money in June 2009 afterlosing $2.75B in 2008, hurt by investment losses and the cost of VAguarantees

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

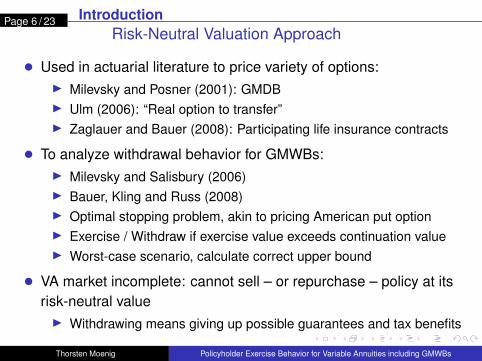

Page 6 / 23 IntroductionRisk-Neutral Valuation Approach

• Used in actuarial literature to price variety of options:I Milevsky and Posner (2001): GMDBI Ulm (2006): “Real option to transfer”I Zaglauer and Bauer (2008): Participating life insurance contracts

• To analyze withdrawal behavior for GMWBs:I Milevsky and Salisbury (2006)I Bauer, Kling and Russ (2008)I Optimal stopping problem, akin to pricing American put optionI Exercise / Withdraw if exercise value exceeds continuation valueI Worst-case scenario, calculate correct upper bound

• VA market incomplete: cannot sell – or repurchase – policy at itsrisk-neutral valueI Withdrawing means giving up possible guarantees and tax benefits

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 7 / 23A Lifetime Utility Model for Variable Annuities

1 Introduction

2 A Lifetime Utility Model for Variable Annuities

The Model

Bellman Equation

Implementation in a Black-Scholes Framework

Parameter Assumptions

3 Results

4 Conclusions and Future Research

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

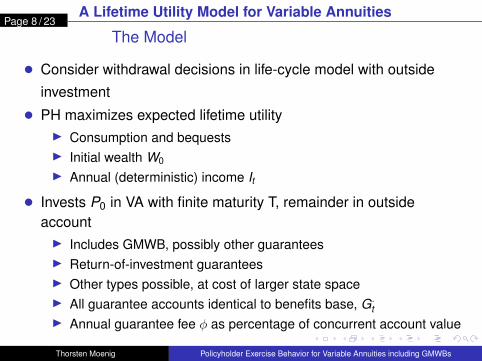

Page 8 / 23A Lifetime Utility Model for Variable Annuities

The Model

• Consider withdrawal decisions in life-cycle model with outside

investment

• PH maximizes expected lifetime utilityI Consumption and bequestsI Initial wealth W0

I Annual (deterministic) income It

• Invests P0 in VA with finite maturity T, remainder in outsideaccountI Includes GMWB, possibly other guaranteesI Return-of-investment guaranteesI Other types possible, at cost of larger state spaceI All guarantee accounts identical to benefits base, G·

tI Annual guarantee fee φ as percentage of concurrent account value

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 9 / 23A Lifetime Utility Model for Variable Annuities

The Model

• VAs grow tax-deferredI Withdrawals taxed on last-in first-out basisI Early withdrawal tax (10%) if PH withdraws prior to age 59.5

• Restrict all actions to policy anniversary datesI Four state variables

? VA account X−t? Outside account A−t? Benefits base G·t? Tax base Ht

I Three choice variables? Withdrawal amount wt

? Consumption Ct

? Risk allocation in outside account νt

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

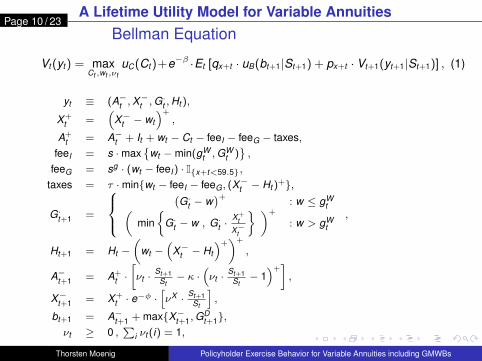

Page 10 / 23A Lifetime Utility Model for Variable Annuities

Bellman Equation

Vt(yt) = maxCt ,wt ,νt

uC(Ct)+e−β ·Et [qx+t · uB(bt+1|St+1) + px+t · Vt+1(yt+1|St+1)] , (1)

yt ≡ (A−t ,X−t ,G

·t ,Ht ),

X+t =

(X−t − wt

)+,

A+t = A−t + It + wt − Ct − feeI − feeG − taxes,

feeI = s ·max{

wt −min(gWt ,GW

t )},

feeG = sg · (wt − feeI) · I{x+t<59.5},

taxes = τ ·min{wt − feeI − feeG, (X−t − Ht )

+},

G·t+1 =

(G·t − w

)+: w ≤ gW

t(min

{G·t − w , G·t ·

X+t

X−t

} )+

: w > gWt

,

Ht+1 = Ht −(

wt −(

X−t − Ht

)+)+

,

A−t+1 = A+t ·[νt ·

St+1St− κ ·

(νt ·

St+1St− 1)+]

,

X−t+1 = X+t · e

−φ ·[νX · St+1

St

],

bt+1 = A−t+1 + max{X−t+1,GDt+1},

νt ≥ 0 ,∑

i νt (i) = 1,

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 11 / 23A Lifetime Utility Model for Variable Annuities

Implementation in a Black-Scholes Framework

• Solve by recursive dynamic programming:

(I) Create appropriate state space grid

(II) For t = T : for all grid points (A,X ,G·,H), compute V−T (A,X ,G·,H).

(III) For t = T − 1,T − 2, . . . ,1: Given V−t+1, calculate V−

t (A,X ,G·,H)

recursively for each (A,X ,G·,H) on the grid using anapproximation of the integral in (1)

I Discretize return space and evaluate via Green’s function

I Gauss-Hermite quadrature

(IV) For t = 0: For the given starting values A0 = W0 − P0, X0 = P0,G·

0 = G·1 = P0 and H0 = H1 = P0, compute

V−0 (W0 − P0,P0,P0,P0) recursively from Equation (1)

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 12 / 23A Lifetime Utility Model for Variable Annuities

Parameter Assumptions

• Policyholder is 55 years old, T = 15 years to maturity

• P0 = 100K ; W0 = 2 · P0 = 200K ; It = 40K

• CRRA(γ = 3) utilities; B = 1; β = r

• τ = 30%, κ = 15%

• Guarantee fee φ = 50 bps

• Surrender fee s = 5%,

gWt =

{0 : t ≤ 5

20,000 : t > 5

• r = 4%, µ = 8%, σ = 15%I Merton ratio: µ−r

σ2·γ = 0.08−0.040.152·3 ≈ 0.5926

• νX = 100% equity exposure in VA

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 13 / 23 Results

1 Introduction

2 A Lifetime Utility Model for Variable Annuities

3 Results

Withdrawal Behavior

Pricing and Sensitivities

4 Conclusions and Future Research

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 14 / 23 Results

Withdrawal Behavior

• Little withdrawal activity (approx. 12K per PH on average)I No withdrawals during accumulation periodI No premature withdrawals in 67% of casesI PH empties guarantee account in 6% of casesI < 1% chance of excessive withdrawal during contract phase

• Two main reasons to withdraw prematurely:I VA account below tax base (approx. 7K on average)

? Nuanced patterns? Interaction of in-the-moneyness of guarantee, tax considerations and

excess withdrawal charge

I VA account much greater than outside account (approx. 5K onaverage)? To reduce overall risk exposure (Merton ratio)

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 15 / 23 Results

Withdrawal Behavior

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

x 104

0

2

4

6

8

10

12

14

15x 10

4

Fig. 1: t=14, At = 180K , G.

t = 100K, H

t = 100K.

Xt−

wt

wt

max(Guarantee,Xt−)

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 16 / 23 Results

Withdrawal Behavior

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

x 104

0

2

4

6

8

10

12

14

15x 10

4 Fig. 3: t=10, At = 180K , G.

t = 100K, H

t = 100K.

Xt−

wt

wt

max(Guarantee,Xt−)

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 17 / 23 Results

Withdrawal Behavior

0 1 2 3 4 5 6 7 8 9 10 11 12 13

x 105

0

1

2

3

4

5

6

7

8x 10

4 Fig. 7: t=10, At = 20K , G.

t = 100K, H

t = 100K.

Xt−

wt,c

t

wt

Ct A

t− + I

t = 60K

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 18 / 23 ResultsPricing and Sensitivities

• Guarantee fee of φ = 50 bps sufficient to cover expected costs• In-the-moneyness appears to be OK proxy for pricing

I Different source to withdrawals

• Eliminating excess withdrawal fee increases net profits (win-win)

Base Case w/d if X−t ≤ G·t s = 0%

EQ[Fees] 6, 252 5, 925 5, 907EQ[Excess-Fee] 19 0 0EQ[Guarantee] 4, 558 4, 761 2, 136

%(Guarantee > 0) 24.34% 33.97% 31.94%

E[agg. w/d] 12, 084 14, 180 16, 374E[agg. w/d & t ≤ 6] 0 0 4, 374

E[agg. w/d & X−t ≤ Ht ] 6, 953 14, 119 6, 047E[agg. w/d & X−t > Ht ] 5, 030 0 5, 816

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

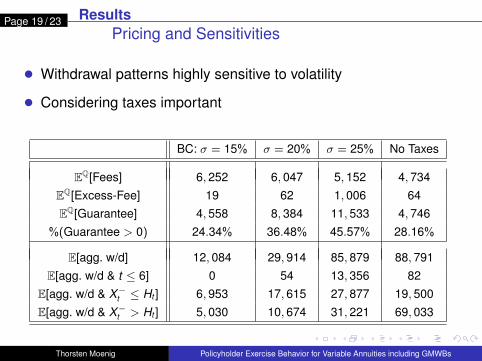

Page 19 / 23 ResultsPricing and Sensitivities

• Withdrawal patterns highly sensitive to volatility

• Considering taxes important

BC: σ = 15% σ = 20% σ = 25% No Taxes

EQ[Fees] 6, 252 6, 047 5, 152 4, 734EQ[Excess-Fee] 19 62 1, 006 64EQ[Guarantee] 4, 558 8, 384 11, 533 4, 746

%(Guarantee > 0) 24.34% 36.48% 45.57% 28.16%

E[agg. w/d] 12, 084 29, 914 85, 879 88, 791E[agg. w/d & t ≤ 6] 0 54 13, 356 82

E[agg. w/d & X−t ≤ Ht ] 6, 953 17, 615 27, 877 19, 500E[agg. w/d & X−t > Ht ] 5, 030 10, 674 31, 221 69, 033

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 20 / 23 Conclusions and Future Research

1 Introduction

2 A Lifetime Utility Model for Variable Annuities

3 Results

4 Conclusions and Future Research

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 21 / 23 Conclusions and Future Research

• Develop lifetime-utility model to analyze withdrawal behavior for

VA with guarantees

• Numerically solve policyholder’s decision making problem inBlack-Scholes frameworkI Return-of-investment GMWB

• Infrequent withdrawals

• PH withdraws when VA account is below tax baseI Interaction of in-the-moneyness of guarantee, tax considerations

and excess w/d fee

• PH withdraws when VA account is largeI To lower overall risk exposure

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 22 / 23 Conclusions and Future Research

• Extend policyholder environment

I Unemployment Risk

I Subjective mortalities

• Withdrawal patterns highly sensitive w.r.t. volatility σ

I Stochastic volatility framework

• Alternatives to EUT

I Epstein-Zin preferences

I Correlation Aversion

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs

Page 23 / 23

THANK YOU!

Thorsten Moenig Policyholder Exercise Behavior for Variable Annuities including GMWBs