polyolefins - fpa8).pdf · polyolefins “here and around ... prod. int. light naphtha west europe...

TRANSCRIPT

FPA 10-07FPA 10-07SingaporeSingapore ShanghaiShanghai HoustonHouston New YorkNew York LondonLondon DüsseldorfDüsseldorf DubaiDubai

Polyolefins “Here and Around the World”

Polyolefins Polyolefins ““Here and Around the WorldHere and Around the World””

Nick VafiadisNick VafiadisBusiness Director Business Director ––

[email protected]@cmaiglobal.com

Flexible Packaging Flexible Packaging AssociationAssociation

October 3, 2007October 3, 2007

FPA 10-07FPA 10-07

WHAT HAPPENS OVER THERE…

MATTERS HERE!

WHAT HAPPENS OVER THERE…

MATTERS HERE!

FPA 10-07FPA 10-07

AgendaAgendaAgenda

•Energy •Ethylene•Polyethylene•Propylene•Polypropylene

•Energy •Ethylene•Polyethylene•Propylene•Polypropylene

FPA 10-07FPA 10-07

World GDP Growth Rates(Constant 2004 U.S. Dollars)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

88 90 92 94 96 98 00 02 04 06 08 10 12

Percent (%)

Most Likely ScenarioAlternate Scenario

Forecast

FPA 10-07FPA 10-07

U.S. GDP Growth - Annualized RatesOffsetting Factors (70%)

U.S. GDP Growth - Annualized RatesOffsetting Factors (70%)

%% QtrQtr--11 QtrQtr--22 QtrQtr--33 QtrQtr--44 Year Year (1)(1)

20022002 2.72.7 2.22.2 2.42.4 0.20.2 1.61.620032003 1.21.2 3.53.5 7.57.5 2.72.7 2.52.520042004 3.93.9 4.04.0 3.13.1 2.62.6 3.93.920052005 3.43.4 3.33.3 4.24.2 1.81.8 3.23.2

(1) Change in average GDP for the year(1) Change in average GDP for the year

20062006 4.84.8 2.42.4 1.11.1 2.12.1 2.92.9

Updated: September 2007Updated: September 2007

20072007 0.60.6 3.83.8 1.91.9 2.02.0 1.91.920082008 2.32.3 2.62.6 2.92.9 3.13.1 2.52.5

FPA 10-07FPA 10-07

WTI Crude Oil PricesWTI Crude Oil Prices

Source: Purvin & Gertz

U.S. Dollars Per BarrelsU.S. Dollars Per Barrels

0

10

20

30

40

50

60

70

80

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

66.0066.00ForecastForecast

57.3057.30

FPA 10-07FPA 10-07

U.S. Burner Tip Natural Gas PricesU.S. Burner Tip Natural Gas Prices

Source: Purvin & Gertz

Dollars Per MMbtuDollars Per MMbtu

0

1

2

3

4

5

6

7

8

9

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

7.007.007.607.60

ForecastForecast

FPA 10-07FPA 10-07

North America Energy Price Trends(Constant 2007 Dollars)

00

22

44

66

88

1010

1212

9090 9191 9292 9393 9494 9595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111

Dollars Per Million BtuDollars Per Million Btu

00

22

44

66

88

1010

1212

1414Crude/Gas RatioCrude/Gas Ratio

ForecastForecast

Crude (WTI)Crude (WTI) Crude / Gas RatioCrude / Gas RatioNatural GasNatural Gas

Arbitrage OpportunitiesArbitrage Opportunities……

FPA 10-07FPA 10-07

Ethane Delta Over Fuel Value(U.S. Gulf Coast)

Ethane Fuel Value Purity Ethane Ethane Price Delta Above Fuel

-20

0

20

40

60

80

100

120

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Cents Per Gallon

-20

0

20

40

60

80

100

120Cents Per Gallon

Fuel Value ofPurity Ethane

Purity Ethane,Cents Per Gallon,

Mont Belvieu, Texas

Delta Between Ethane Price and Fuel Value, Cents Per Gallon

Forecast

FPA 10-07FPA 10-07

EthyleneEthylene

FPA 10-07FPA 10-07

2006 Production = 110.2 Million Metric Tons2006 Production = 110.2 Million Metric Tons

World Ethylene Supply/Demand Profile

World Ethylene Supply/Demand Profile

Production by Feedstock Demand by End-Use

EDC12%

Ethylene Oxide

14%

PE59%

Others8% EBZ

7%

Others2%

Butane4%

Gas Oil5%

Propane7%Ethane

28%

Naphtha54%

FPA 10-07FPA 10-07

Global Ethylene Cash CostsGlobal Ethylene Cash CostsAnnual Comparison BasisAnnual Comparison BasisUnit-by-Unit Cost CurveUnit-by-Unit Cost Curve

50

250

450

650

850

1050

1250

0 20 40 60 80 100 120 140

Dollars Per Metric Ton

Average U.S. Feedstock Basis

Cumulative Ethylene Capacity (Million Tons)Total Cash Cost Middle EastNorth America

Northeast Asia

Southeast AsiaWest Europe

20052006

(NAM – MDE) = $525 / MT

FPA 10-07FPA 10-07

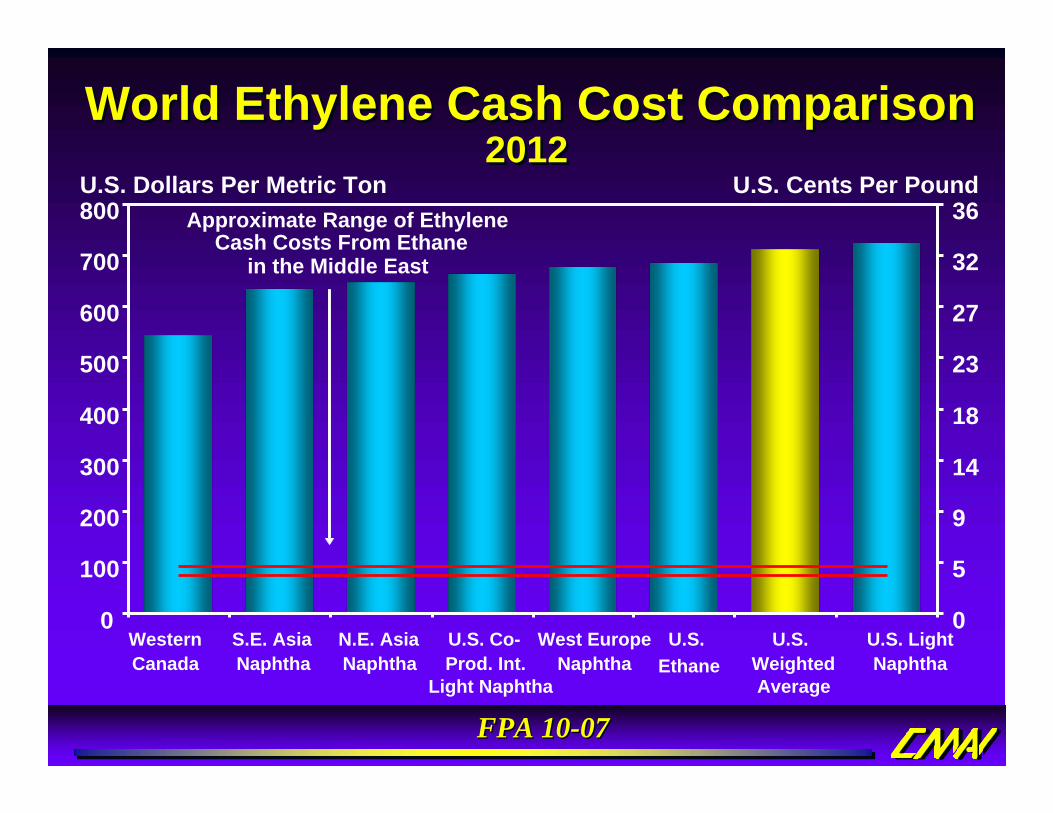

WesternCanada

S.E. AsiaNaphtha

N.E. AsiaNaphtha

U.S. Co-Prod. Int.

Light Naphtha

West EuropeNaphtha

U.S. Ethane

U.S.WeightedAverage

U.S. LightNaphtha

0

100

200

300

400

500

600

700

800

0

5

9

14

18

23

27

32

36U.S. Dollars Per Metric Ton U.S. Cents Per Pound

Approximate Range of EthyleneCash Costs From Ethane

in the Middle East

World Ethylene Cash Cost ComparisonWorld Ethylene Cash Cost Comparison2012 2012

FPA 10-07FPA 10-07

Global Ethylene Capacity GrowthGlobal Ethylene Capacity GrowthGlobal Ethylene Capacity Growth( -000- Tons )( -000- Tons )

America'sAmerica's 40,39340,393 40,76140,761 368368EuropeEurope 30,97030,970 31,85431,854 884884

Major RegionMajor Region2007 2007

CapacityCapacity2012 2012

Capacity Capacity '07 to '12 '07 to '12

Delta Delta

Middle East / Africa Middle East / Africa 16,83316,833 35,97835,978 19,14519,145Asia PacificAsia Pacific 37,94037,940 52,09752,097 14,15714,157

World TotalWorld Total 126,136126,136 160,690160,690 34,55434,554

FPA 10-07FPA 10-07

Ethylene Equivalent Trade Surplus From Middle East

Ethylene Equivalent Trade Surplus From Middle East

0

5

10

15

20

25

30

00 01 02 03 04 05 06 07 08 09 10 11 12

Middle East Net Equivalent Exports

Million Metric Tons

Asia/Pacific Net Equivalent Imports

FPA 10-07FPA 10-07

Vinyls Styrenics Polyethylene GlycolOthers Ethylene Net Trade

-1

0

1

2

3

4

5

02 03 04 05 06 07 08 09 10 11 12

Million Metric Tons

Net ExportsNet Exports

Net ImportsNet Imports

North AmericaNorth AmericaEthylene Net Equivalent TradeEthylene Net Equivalent Trade

FPA 10-07FPA 10-07

U.S. Large Buyer Contract Price WEP Contract Price SEA CFR Spot Price

200300400500600700800900

1,0001,1001,2001,300

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Dollars Per Metric Ton

Global Annual Ethylene PricesGlobal Annual Ethylene Prices(Constant 2007 Dollars)(Constant 2007 Dollars)

Forecast

FPA 10-07FPA 10-07

Wtd. Average Cash Margin Average Acquisition PriceAverage Spot Price

05

101520253035404550

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Cents Per Pound

01102203304405506607708809901,100

ForecastDollars Per Metric Ton

U.S. Ethylene Market Annual EconomicsU.S. Ethylene Market Annual EconomicsLarge Buyer Contract Cash MarginsLarge Buyer Contract Cash Margins

ReRe--Investment RangeInvestment Range

FPA 10-07FPA 10-07

PolyethylenePolyethylene

FPA 10-07FPA 10-07

-29-152287287-164Inventory change MM LBS . YTD 2007

94.294.694.892.4Avg. Op. Rate- YTD 072.42.43.03.02.92.9--0.50.5Total SalesTotal Sales

30.630.685.685.612.712.7--3.53.5Exports (est.)Exports (est.)--3.13.1--6.06.0--0.10.1--0.30.3Domestic SalesDomestic Sales1.51.51.51.54.14.1--2.72.7Total SupplyTotal Supply

--51.051.0--71.271.2--13.313.3--50.650.6ImportsImports2.52.53.13.14.44.4--2.02.0ProductionProduction

Total PETotal PEHDPEHDPELLDPELLDPELDPELDPEU.S. and Canada, Percent Change YTD August 2007 Vs. 2006U.S. and Canada, Percent Change YTD August 2007 Vs. 2006

PE: Strong YTD...PE: Strong YTD...PE: Strong YTD...

FPA 10-07FPA 10-07

Film & Sheet50%

Injection Molding13%

Pipe & Extrusion7%

Extrusion Coating3%

Raffia1%Fiber

1%Rotomolding1%Wire & Cable

2%

Blow Molding12%

Other10%

Consumption = 68.3 Million Metric TonsConsumption = 68.3 Million Metric Tons*Excluding Exports

WorldWorld2007 Total PE Consumption by End Use2007 Total PE Consumption by End Use

FPA 10-07FPA 10-07

Million Metric Tons% AAGR 2007-12

World Total PE Demand Growth By RegionWorld Total PE Demand Growth By Region

0 5 10 15 20 25 30

20072012

9.9%

5.7%

8.3%

5.6%

6.7%4.5%

7.9%

3.2%5.3%

2.0%

2007 Total Demand = 68.3 Million Metric Tons2007 Total Demand = 68.3 Million Metric Tons

ISCISCSEASEANEANEAMDEMDEAFRAFRCISCIS

CEPCEPWEPWEPSAMSAMNAMNAM

World AAGR % 2007World AAGR % 2007--2012 = 5.1%2012 = 5.1%

FPA 10-07FPA 10-07

Other

Rotomolding

Wire & Cable

Blow Molding

Extrusion Coating

Pipe & Extrusion

Injection Molding

Film & Sheet

0 1 2 3 4 5 6 7

20072012

1.8%

2.8%

3.4%

3.1%

1.5%

2.8%

1.5%

1.4%

Million Metric Tons

2007 Domestic Demand = 14.5 Million Metric Tons2007 Domestic Demand = 14.5 Million Metric Tons

% AAGR 2007-12

U.S./Canada PE Demand by IndustryU.S./Canada PE Demand by Industry

FPA 10-07FPA 10-07

High Energy Prices Hit NAMHigh Energy Prices Hit NAM

0

200

400

600

800

1,000

1,200

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Dollars Per Metric Ton

NAM Ethane NAM Light Naphtha

Middle East PE Cash Cost Range

FPA 10-07FPA 10-07

NAM HDPE Total Cash Costs WEP HDPE Total Cash CostSEA HDPE Total Cash Costs

1000

1200

1400

1600

1800

Jan-06

Apr-06

Jul-06

Oct-06

Jan-07

Apr-07

Jul-07

Oct-07

Jan-08

Apr-08

Jul-08

Oct-08

Global Monthly HDPE Blow Molding Cash Costs, Dollars Per Ton

NAM: Low Cash CostNAM: Low Cash Cost

FPA 10-07FPA 10-07

N. America S. AmericaW. Europe C. Europe/CIS & Baltic StatesAfrica/M. East Asia/Pacific

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012

Million Metric Tons

World PolyethyleneWorld PolyethyleneNet Capacity AdditionsNet Capacity Additions

FPA 10-07FPA 10-07

0123456789

10

2007 2008 2009 2010 2011 20120102030405060708090100

World Middle East ME % of Total

Volume, Million Metric TonsVolume, Million Metric Tons

MDE = 46% of World Expansions 07MDE = 46% of World Expansions 07--1212

World Capacity, PercentWorld Capacity, Percent

Nearly Half of “New” PE Capacity To be Built in the Middle East

Nearly Half of “New” PE Capacity To be Built in the Middle East

FPA 10-07FPA 10-07

NPC-Iran SABIC Qatar PetroleumNat'l Chev/Phil Tasnee Petrochemical

SIPCHEM

Sumitomo Chem. Saudi Aramco Japanese MEGUAE Government Other

Sabic & NPC Leaders In New CapacitySabicSabic & NPC Leaders In New Capacity& NPC Leaders In New Capacity

0.0

0.51.0

1.52.0

2.5

3.03.5

4.0

2007 2008 2009 2010 2011 2012

ME Total PE Capacity Increases by Company, Million Metric TonsME Total PE Capacity Increases by Company, Million Metric Tons

FPA 10-07FPA 10-07

LDPE Expansions in MDE2007-2011

LDPE Expansions in MDELDPE Expansions in MDE20072007--20112011

Q1 2011250Umm Said, QAQAPCOQ4 2009350Al Jubail, SAKayanQ1 2009250Rabigh, SAPetro-Rabigh

Q3 2011500Al Jubail, SASIPCHEM

2007300Bandar Imam, IRAmir Kabir PCTimingCapacity (kt)LocationCompany

2,350 2,350 Total LDPE Net Capacity IncreaseTotal LDPE Net Capacity Increase

Q3 2008400Al Jubail, SATasnee/SaharaQ4 2007300Bandar Assaluyeh, IRArya Sasol PC

FPA 10-07FPA 10-07

LLDPE Expansions in MDE2007-2011

LLDPE Expansions in MDELLDPE Expansions in MDE20072007--20112011

TimingCapacity (kt)LocationCompany

2,1252,125Total LLDPE Net Capacity IncreaseTotal LLDPE Net Capacity Increase

Q2 2009500Mesaieed, QAQatofinQ1 2009350Rabigh, SAPetro-RabighQ4 2008400Al Jubail, SASHARQQ3 2008500Yanbu, SAYansabQ3 2008225Shuaiba, KWTKOCQ3 2007150Bandar Assaluyeh, IRJam PC

FPA 10-07FPA 10-07

Q1 2009300Bandar AssaluyehMehr PC

Q3 2010300Ilam, IRIlam PC

5,5155,515Total HDPE Net Capacity Increase Total HDPE Net Capacity Increase Q3 2011350Al Jubail, SAQ3 2011350Al Jubail, SANat'l Chev/PhilQ3 2011400Al Jubail, SASIPCHEMQ3 2010540Abu Dhabi, Ruwais, AEBorouge

Q4 2009400Al Jubail, SAKayanQ2 2009400Mesaieed, QAQ-Chem II

Q1 2009300Rabigh, SAPetro-RabighQ4 2008400Al Jubail, SASHARQQ3 2008400Yanbu, SAYansabQ3 2008225Shuaiba, KWTKOCQ3 2008400Al Jubail, SATasnee/SaharaQ4 2007150Bandar Assaluyeh, IRQ4 2007300Bandar Assaluyeh, IRJam PCQ4 2007300Bandar Assaluyeh, IRArya Sasol PCTimingCapacity (kt)LocationCompany

HDPE Expansions in MDE2007-2011

HDPE Expansions in MDEHDPE Expansions in MDE20072007--20112011

FPA 10-07FPA 10-07

U.S. vs. Saudi Supplied HDPE Resins to US2007

U.S. vs. Saudi Supplied HDPE Resins to US2007

Note: Integrated producersNote: Integrated producers

Saudi Cost AdvantageSaudi Cost Advantage

Total Mfg & Delivered CostsTotal Mfg & Delivered Costs

3. Domestic Logistics3. Domestic Logistics

2. Import Logistics/Duties2. Import Logistics/Duties

1. Manufacturing Cash Costs1. Manufacturing Cash Costs

Saudi Saudi ProducerProducer

U.S. U.S. ProducerProducer$ 840/MT$ 840/MT $ 305/MT$ 305/MT

$ 265/MT$ 265/MT--------

$ 75/MT$ 75/MT$ 75/MT$ 75/MT

$ 915/MT$ 915/MT $ 645/MT$ 645/MT

29.5%29.5%

FPA 10-07FPA 10-07

New Capacity in China (2006-2007)New Capacity in China (2006-2007)

Startup scheduled for Dec 06Startup scheduled for Dec 06End/06End/06150150Lanzhou, GansuLanzhou, GansuLanzhou PCLanzhou PCChinaChina

Mechanical completion Mechanical completion scheduled for Jul 06scheduled for Jul 06Oct 06Oct 06350350MaomingMaoming, ,

GuangdongGuangdongMaomingMaoming PCPCChinaChina

Plant installation completed Plant installation completed in Oct 05 but startup in Oct 05 but startup postponed to Apr 06postponed to Apr 06

Apr 06Apr 06300300Jilin, JilinJilin, JilinJilin PCJilin PCChinaChinaHDPEHDPE

Started up in Feb 06Started up in Feb 06Feb 06Feb 06200200Huizhou, Huizhou, GuangdongGuangdong

CNOOC & Shell CNOOC & Shell PCPCChinaChina

Startup scheduled for Dec 06Startup scheduled for Dec 06End/06End/06150150Lanzhou, GansuLanzhou, GansuLanzhou PCLanzhou PCChinaChinaLLDPELLDPE

Mechanical completion in Mechanical completion in Feb/Mar 07Feb/Mar 07Apr 07Apr 07250250MaomingMaoming, ,

GuangdongGuangdongMaomingMaoming PCPCChinaChina

Startup scheduled for Dec 06Startup scheduled for Dec 06End/06End/06200200Lanzhou, GansuLanzhou, GansuLanzhou PCLanzhou PCChinaChinaLDPELDPE

Started up in Apr 06Started up in Apr 06Apr 06Apr 06250250Huizhou, Huizhou, GuangdongGuangdong

CNOOC & Shell CNOOC & Shell PCPCChinaChina

RemarksRemarksExpected Expected StartupStartup

New Capacity New Capacity (Thousand (Thousand

Metric Tons)Metric Tons)LocationLocationProducerProducerCountryCountryProductProduct

FPA 10-07FPA 10-07

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2007 2008 2009 2010 2011 2012SINOPEC CNPC SK Holdings Liaoning HuajinChengdu PC Various Investors Shenhua Group Exxon Mobil Corp.Saudi Aramco Jilin Petrochemica Other

Sinopec & CNPC Leaders in Capacity Expansions in NEASinopec & CNPC Leaders in Sinopec & CNPC Leaders in Capacity Expansions in NEACapacity Expansions in NEA

NEA PE Capacity Increases By Company, Million Metric TonsNEA PE Capacity Increases By Company, Million Metric Tons

FPA 10-07FPA 10-07

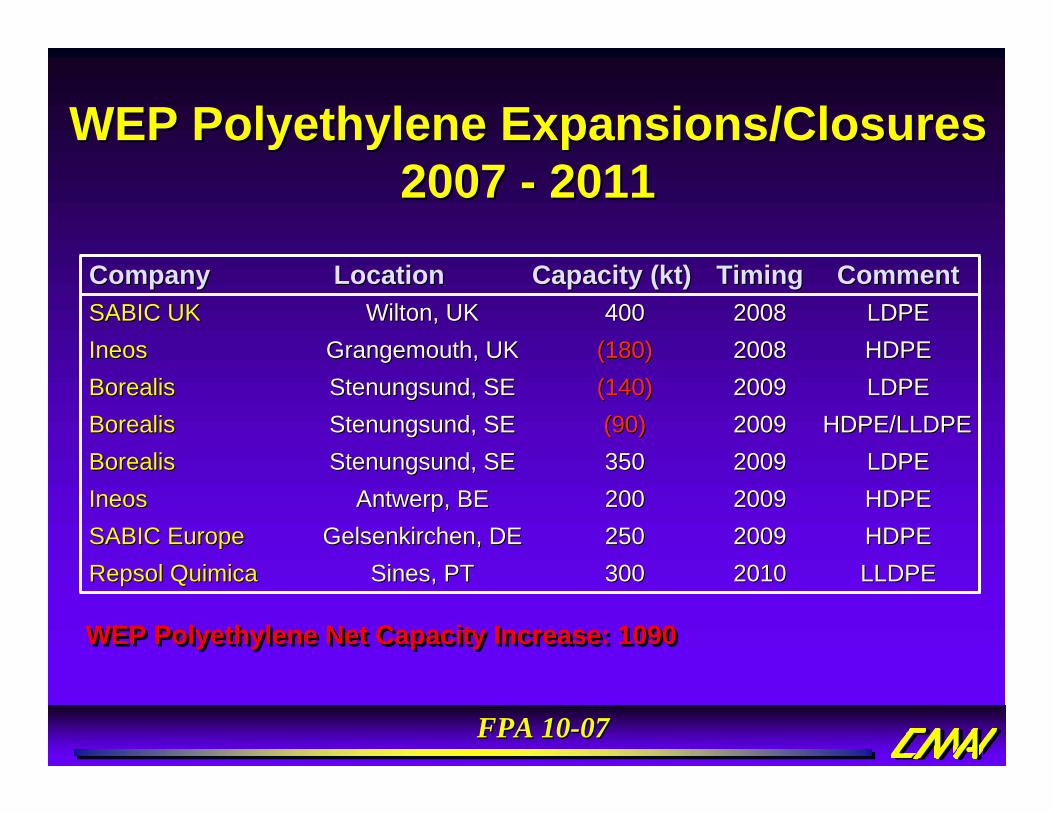

WEP Polyethylene Expansions/ClosuresWEP Polyethylene Expansions/Closures2007 2007 -- 20112011

HDPEHDPE20092009200200Antwerp, BEAntwerp, BEIneosIneosHDPEHDPE20092009250250Gelsenkirchen, DEGelsenkirchen, DESABIC EuropeSABIC EuropeLLDPELLDPE20102010300300Sines, PTSines, PTRepsol Quimica Repsol Quimica

LDPELDPE20092009350350Stenungsund, SEStenungsund, SEBorealisBorealisHDPE/LLDPEHDPE/LLDPE20092009(90)(90)Stenungsund, SEStenungsund, SEBorealisBorealis

HDPEHDPE20082008(180)(180)Grangemouth, UKGrangemouth, UKIneosIneosLDPELDPE20092009(140)(140)Stenungsund, SEStenungsund, SEBorealisBorealis

20082008TimingTiming

LDPELDPECommentComment

400400Wilton, UKWilton, UKSABIC UKSABIC UKCapacity (kt)Capacity (kt)LocationLocationCompanyCompany

WEP Polyethylene Net Capacity Increase: 1090WEP Polyethylene Net Capacity Increase: 1090

FPA 10-07FPA 10-07

Degradables, Bio-Polymers & PLADegradables, BioDegradables, Bio--Polymers & PLAPolymers & PLA•• Global consumptionGlobal consumption of bioof bio--degradable pkg. totaled over degradable pkg. totaled over

40 thousand metric tons40 thousand metric tons last yearlast year•• ProjectionProjection -- approach 120 thousand metric tons by 2011 approach 120 thousand metric tons by 2011 •• Europe leads consumptionEurope leads consumption at almost 20 thousand metric at almost 20 thousand metric

tons, North America consumed around 15 thousand tons, North America consumed around 15 thousand metric tons in 2006metric tons in 2006

•• PLAPLA represents about 40% of the global market todayrepresents about 40% of the global market today

40 Kta40 Kta

120 Kta120 Kta

20062006 20112011

FPA 10-07FPA 10-07

•• PLA (polylactic acid) represents over 40% of the PLA (polylactic acid) represents over 40% of the ““nonnon--petroleum basedpetroleum based”” polymer market todaypolymer market today

•• Projection Projection -- PLA consumption could exceed 100 PLA consumption could exceed 100 thousand metric tons by 2011thousand metric tons by 2011

Degradables, Bio-Polymers & PLADegradables, BioDegradables, Bio--Polymers & PLAPolymers & PLA

FPA 10-07FPA 10-07

Top Global Polyethylene Producers/MarketersTop Global Polyethylene Producers/Marketers(Based on Estimate of Marketed Capacity)(Based on Estimate of Marketed Capacity)

20022002CapacityCapacity % Capacity% Capacity--000000-- MTMT ShareShare

ExxonMobilExxonMobil 70257025 11.3311.33Dow ChemicalDow Chemical 69586958 11.2211.22Chevron PhillipsChevron Phillips 27602760 4.454.45EquistarEquistar 26082608 4.214.21BasellBasell 23302330 3.763.76BorealisBorealis 23162316 3.733.73BP ChemicalBP Chemical 18831883 3.043.04SinopecSinopec 18531853 2.992.99ATOFINA ATOFINA 17451745 2.812.81SABICSABIC 17081708 2.752.75TotalTotal 3118631186 50.2950.29

Total CapacityTotal Capacity 6567465674

20122012

CapacityCapacity % Capacity% Capacity--000000-- MTMT ShareShare

Dow ChemicalDow Chemical 84658465 8.328.32ExxonMobilExxonMobil 82658265 8.128.12SABICSABIC 67886788 6.676.67SinopecSinopec 67356735 6.626.62China China -- NPCNPC 45854585 4.514.51Chevron PhillipsChevron Phillips 43534353 4.284.28NPC NPC -- IranIran 36753675 3.613.61IneosIneos 32863286 3.233.23BorealisBorealis 31983198 3.143.14LyondellLyondell 25362536 2.492.49TotalTotal 5188651886 51.0151.01

Total CapacityTotal Capacity 101726101726

FPA 10-07FPA 10-07

North America PE ProducersYear End 2007 Capacities

North America PE ProducersYear End 2007 Capacities

DowExx

onMobil

Lyondell

(Bas

ell)

Chevro

n Phillips

Nova C

hemica

lWes

tlake

Formosa

Ineos

PEMEXTotal

PCFlin

t Hills

Du PontPetr

omontAT Plas

tics

0.00.51.01.52.02.53.03.54.04.5

LLDPELDPEHDPE

Million Metric TonsNote: CPChem/Ineos JV capacity split to partners

Imperial Oil included with ExxonMobil

FPA 10-07FPA 10-07

ChinaChina MexicoMexico Latin AmericaLatin AmericaRest of AsiaRest of Asia EuropeEurope Africa Mid EastAfrica Mid EastForecast ExportsForecast Exports Forecast ImportsForecast Imports Net TradeNet Trade

Record First Half PE ExportsRecord First Half PE ExportsRecord First Half PE Exports

--200200

00

200200

400400

600600

800800

10001000

20052005 Q2 Q2 Q3 Q3 Q4 Q4 20062006 Q2 Q2 Q3 Q3 Q4 Q4 20072007 Q2 Q2 Q3 Q3 Q4 Q4

ExportsExports

ImportsImports

U.S. and Canada PE Trade, Thousand Metric TonsU.S. and Canada PE Trade, Thousand Metric Tons

FPA 10-07FPA 10-07

00

1010

2020

3030

4040

5050

6060

7070

1Q/011Q/01 4Q/014Q/01 3Q/023Q/02 2Q/032Q/03 1Q/041Q/04 4Q/044Q/04 3Q/053Q/05 2Q/062Q/06 1Q/071Q/0700

1010

2020

3030

4040

5050

6060

7070

8080

9090

100100Billion UnitsBillion Units PercentPercent

China Share of TotalChina Share of Total WorldWorld ChinaChina

U.S. Bag Imports CollapseU.S. Bag Imports Collapse

FPA 10-07FPA 10-07

0

20

40

60

80

100

120

02 03 04 05 06 07 08 09 10 11 1240

50

60

70

80

90

100

Demand 5.1* Capacity 5.2* Operating Rate

Million Metric Tons Operating Rate, Percent

* %AAGR 2007-12

PE Global Operating RatesPE Global Operating Rates

FPA 10-07FPA 10-07

Production -0.6* Demand 1.9* Capacity -0.3* Operating Rate

0

1

2

3

4

5

6

7

8

02 03 04 05 06 07 08 09 10 11 1260

65

70

75

80

85

90

95

100Million Metric Tons Operating Rate, Percent

* %AAGR 2007-12

LLDPE Supply/Demand BalanceLLDPE Supply/Demand BalanceNorth AmericaNorth America

FPA 10-07FPA 10-07

Cash MarginCash Margin LLDPE Discounted PriceLLDPE Discounted Price Cash CostsCash CostsNote: Contract price is discountedNote: Contract price is discounted

--101000

10102020303040405050606070708080

JanJan--0505

AprApr--0505

JulJul--0505

OctOct--0505

JanJan--0606

AprApr--0606

JulJul--0606

OctOct--0606

JanJan--0707

AprApr--0707

JulJul--0707

OctOct--0707

JanJan--0808

AprApr--0808

JulJul--0808

OctOct--0808

Cents Per PoundCents Per Pound

ForecastForecast

~~

NAM LLDPE Butene Film Price Vs. Cash CostNAM LLDPE Butene Film Price Vs. Cash Cost

FPA 10-07FPA 10-07

HDPE Margin Ethylene Cash Margin HDPE Discounted Price

NAM PE Chain Margins (Annual)NAM PE Chain Margins (Annual)

-10

0

10

20

30

40

50

60

70

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Cents Per PoundCents Per Pound

FPA 10-07FPA 10-07

Polyethylene Take-AwayPolyethylene TakePolyethylene Take--AwayAway

• Currently: NAM highly competitive PE exporter

• NAM domestic demand improving; Exports keeping NAM operating rates high.

• Export opportunities will remain attractive through mid-2008

• Excess capacity increases peak 2009-2010 period; operating rates expected to suffer

•• Currently: NAM highly competitive PE Currently: NAM highly competitive PE exporterexporter

•• NAM domestic demand improving; Exports NAM domestic demand improving; Exports keeping NAM operating rates high.keeping NAM operating rates high.

•• Export opportunities will remain attractive Export opportunities will remain attractive through midthrough mid--20082008

•• Excess capacity increases peak 2009Excess capacity increases peak 2009--2010 period; operating rates expected to 2010 period; operating rates expected to suffersuffer

FPA 10-07FPA 10-07

Polyethylene Take-AwayPolyethylene TakePolyethylene Take--AwayAway

• Saudi Arabia & Iran lead capacity increases in ME; NPC & Sabic = major impact on global markets

• Asian Market cannot take all ME exports –other global markets will be affected

• Resin prices near peak levels during forecast period

• Bio-Polymers small market today but becoming increasingly significant

•• Saudi Arabia & Iran lead capacity Saudi Arabia & Iran lead capacity increases in ME; NPC & increases in ME; NPC & SabicSabic = major = major impact on global marketsimpact on global markets

•• Asian Market cannot take all ME exports Asian Market cannot take all ME exports ––other global markets will be affectedother global markets will be affected

•• Resin prices near peak levels during Resin prices near peak levels during forecast periodforecast period

•• BioBio--Polymers small market today but Polymers small market today but becoming increasingly significantbecoming increasingly significant

FPA 10-07FPA 10-07

PropylenePropylenePropylene

FPA 10-07FPA 10-07

Propylene Key IssuesPropylene Key IssuesPropylene Key Issues

• Generally a by-product of making ethylene and gasoline

• Propylene use growing faster than ethylene use and gasoline consumption

• On purpose propylene more important• Supply sources vary from region to

region• P/E ratio rising

•• Generally a byGenerally a by--product of making product of making ethylene and gasolineethylene and gasoline

•• Propylene use growing faster than Propylene use growing faster than ethylene use and gasoline consumptionethylene use and gasoline consumption

•• On purpose propylene more importantOn purpose propylene more important•• Supply sources vary from region to Supply sources vary from region to

regionregion•• P/E ratio risingP/E ratio rising

FPA 10-07FPA 10-07

North AmericaNorth America2006 PG/CG Propylene Supply/Demand2006 PG/CG Propylene Supply/Demand

StmStm. Crackers. Crackers49%49%

OthersOthers3%3%

FCC/SplittersFCC/Splitters48%48%

OthersOthers6%6% AcryloAcrylo--

nitrilenitrile10%10%

CumeneCumene1%1%

Acrylic Acrylic AcidAcid6%6%

OxoOxo AlcAlc..6%6%

Propylene Propylene OxideOxide12%12%

PPPP59%59%

Production by SourceProduction by Source Demand by EndDemand by End--UseUse

Domestic Demand = 16 Million Metric TonsDomestic Demand = 16 Million Metric Tons

FPA 10-07FPA 10-07

Global Propylene Supply TrendsGlobal Propylene Supply TrendsGlobal Propylene Supply Trends

00

1010

2020

3030

4040

5050

6060

7070

8080

9090

100100

9090 9191 9292 9393 9494 9595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111

Propylene Supply Propylene Supply Million TonsMillion Tons

0.0%0.0%

2.0%2.0%

4.0%4.0%

6.0%6.0%

8.0%8.0%

10.0%10.0%

12.0%12.0%

14.0%14.0%

Alternative Alternative Technologies Technologies

ProportionProportion

Alternative TechnologiesAlternative Technologies

RefineriesRefineries

Steam CrackersSteam Crackers

Alternative TechnologiesAlternative TechnologiesAmountAmount

FPA 10-07FPA 10-07

Propylene to Ethylene Price RatiosPropylene to Ethylene Price RatiosPropylene to Ethylene Price Ratios

0.50.5

0.60.6

0.70.7

0.80.8

0.90.9

1.01.0

1.11.1

1.21.2

1.31.3

9090 9191 9292 9393 9494 9595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212 1313 1414 1515

RatioRatio

0.50.5

0.60.6

0.70.7

0.80.8

0.90.9

1.01.0

1.11.1

1.21.2

1.31.3RatioRatio

ForecastForecast

Southeast AsiaSoutheast Asia West EuropeWest Europe North AmericaNorth America

FPA 10-07FPA 10-07

NAM Contract PriceNAM Contract Price WEP Contract PriceWEP Contract Price SEA CFR Spot PriceSEA CFR Spot Price

Global Long-Term Propylene PricesGlobal Long-Term Propylene Prices

200200300300

400400500500600600

700700800800900900

1,0001,000

1,1001,1001,2001,200

9090 9191 9292 9393 9494 9595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212 1313 1414 1515

Dollars Per TonDollars Per Ton

ForecastForecast

FPA 10-07FPA 10-07

!! Tight suppliesTight supplies expected expected through 2008through 2008

!! The Middle EastThe Middle East emerging emerging as a global propylene as a global propylene suppliersupplier

!! Alternative technologiesAlternative technologies for for propylene have come of agepropylene have come of age

!! Propylene pricesPropylene prices impacted impacted by incremental supplies of by incremental supplies of onon--purpose propylenepurpose propylene

Propylene ConclusionPropylene ConclusionPropylene Conclusion

FPA 10-07FPA 10-07

PolypropylenePolypropylene

FPA 10-07FPA 10-07Thousand Metric TonsThousand Metric Tons% AAGR, 07% AAGR, 07--1212

00 500500 10001000 15001500 20002000 25002500 30003000 35003500

OtherOther

Fiber & FilamentFiber & Filament

Film & SheetFilm & Sheet

Blow MoldingBlow Molding

Injection MoldingInjection Molding

2012201220072007

3.3%3.3%

4.8%4.8%

4.1%4.1%

1.5%1.5%

3.1%3.1%

Total Growth Rate = 3.0%Total Growth Rate = 3.0%

North America PP IndustryNorth America PP IndustryDemand 2007-2012Demand 2007-2012

FPA 10-07FPA 10-07

20022002CapacityCapacity ShareShare

CompanyCompany (000's MT)(000's MT) %%BasellBasell 62076207 16.7016.70BP ChemicalBP Chemical 22422242 6.036.03SinopecSinopec 21062106 5.675.67ExxonMobilExxonMobil 17721772 4.774.77ATOFINAATOFINA 17121712 4.614.61BorealisBorealis 14001400 3.773.77Reliance IndustriesReliance Industries 12001200 3.233.23DSMDSM 985985 2.652.65Formosa Plastics Formosa Plastics 980980 2.642.64PetroChinaPetroChina 880880 2.372.37TotalTotal 1948419484 52.4352.43

Total CapacityTotal Capacity 3715937159

Top Global Polypropylene Producers/MarketersTop Global Polypropylene Producers/MarketersTop Global Polypropylene Producers/Marketers(Based on Estimate of Marketed Capacity)(Based on Estimate of Marketed Capacity)(Based on Estimate of Marketed Capacity)

20122012CapacityCapacity ShareShare

CompanyCompany (000's MT)(000's MT) %%BasellBasell 67836783 10.1110.11SinopecSinopec 48494849 7.237.23SABICSABICSABIC 347034703470 5.175.175.17PetroChinaPetroChina 28632863 4.274.27Reliance IndustriesReliance Industries 27802780 4.144.14BorealisBorealis 27452745 4.094.09ExxonMobilExxonMobil 26252625 3.913.91IneosIneos 25952595 3.873.87Total PCTotal PC 25802580 3.853.85Formosa PlasticsFormosa Plastics 20822082 3.103.10TotalTotal 3337233372 49.7549.75

Total CapacityTotal Capacity 6707667076

FPA 10-07FPA 10-07

North America Polypropylene Industry North America Polypropylene Industry 2007 Propylene F/S Integration - Basell Acquires Lyondell2007 Propylene F/S Integration - Basell Acquires Lyondell

(Propylene Consumption Capacity - Billion Lbs)(Propylene Consumption Capacity - Billion Lbs)

0.00.00.50.51.01.01.51.52.02.02.52.53.03.03.53.54.04.04.54.5

Basell

Basell

Ineos

Ineos

ExxonMobil

ExxonMobil

Sunoco (E

psilon)

Sunoco (E

psilon)

Total PC

Total PC

FPC USA

FPC USA

DowDow

Flint H

ills R

esource

s

Flint H

ills R

esource

sPhilli

ps

Phillips S

umika

Sumika

Pinnacle

Polymers

Pinnacle

Polymers

ConocoPhilli

ps

ConocoPhilli

psIndelp

ro

Indelpro

NonNon--Integrated PP ProductionIntegrated PP ProductionIntegrated PP ProductionIntegrated PP Production

66% Integrated Production for Total Industry66% Integrated Production for Total Industry

FPA 10-07FPA 10-07

--11

00

11

22

33

20072007 20082008 20092009 20102010 20112011 20122012

44

55

66

77

N. AmericaN. America S. AmericaS. America W. EuropeW. EuropeC. Europe/CIS & Baltic.C. Europe/CIS & Baltic. Africa/M. EastAfrica/M. East Asia PacificAsia Pacific

World PP Net Capacity Additions, Million Metric TonsWorld PP Net Capacity Additions, Million Metric Tons

Announced PP AdditionsAnnounced PP Additions

FPA 10-07FPA 10-07

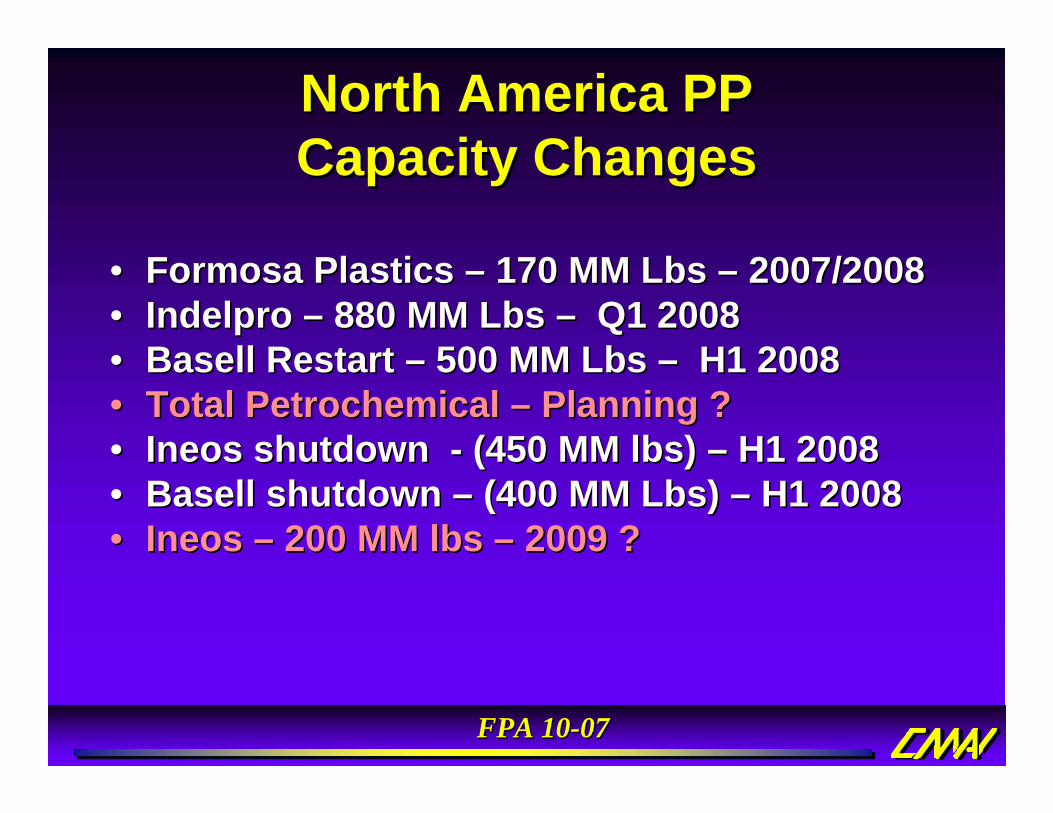

North America PP Capacity ChangesNorth America PP North America PP Capacity ChangesCapacity Changes

•• Formosa Plastics Formosa Plastics –– 170 MM Lbs 170 MM Lbs –– 2007/20082007/2008•• IndelproIndelpro –– 880 MM Lbs 880 MM Lbs –– Q1 2008Q1 2008•• Basell Restart Basell Restart –– 500 MM Lbs 500 MM Lbs –– H1 2008H1 2008•• Total Petrochemical Total Petrochemical –– Planning ?Planning ?•• IneosIneos shutdown shutdown -- (450 MM lbs) (450 MM lbs) –– H1 2008H1 2008•• BasellBasell shutdown shutdown –– (400 MM Lbs) (400 MM Lbs) –– H1 2008H1 2008•• IneosIneos –– 200 MM lbs 200 MM lbs –– 2009 ?2009 ?

FPA 10-07FPA 10-07

00

1010

2020

3030

4040

5050

6060

7070

0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 12126565

7070

7575

8080

8585

9090

9595

100100Million Metric TonsMillion Metric Tons Operating Rate, PercentOperating Rate, Percent

Demand 6.0*Demand 6.0* Capacity 7.2*Capacity 7.2* Operating RateOperating Rate* %AAGR 2007* %AAGR 2007--1212

WorldPP Supply/Demand Balance

WorldWorldPP Supply/Demand BalancePP Supply/Demand Balance

FPA 10-07FPA 10-07

00

22

44

66

88

1010

1212

0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 12127070

7575

8080

8585

9090

9595

100100

Production 0.5*Production 0.5* Demand 3.0*Demand 3.0* Capacity 1.0*Capacity 1.0* Operating RateOperating Rate

Million Metric TonsMillion Metric Tons Operating Rate, PercentOperating Rate, Percent

* %AAGR 2007* %AAGR 2007--1212

North AmericaPolypropylene Supply/Demand Balance

North AmericaNorth AmericaPolypropylene Supply/Demand BalancePolypropylene Supply/Demand Balance

FPA 10-07FPA 10-07Note: PP price represents a nonNote: PP price represents a non--discounted delivered invoice price; contract propylene pricediscounted delivered invoice price; contract propylene price

Contract PropyleneContract Propylene InjInj MldgMldg HomopolymerHomopolymerPP PP -- C3 DifferentialC3 Differential

00

1010

2020

3030

4040

5050

6060

7070

8080

0505 AprApr JulJul OctOct 0606 AprApr JulJul OctOct 0707 AprApr JulJul OctOct 0808 AprApr JulJul OctOct00

220220

440440

660660

880880

11001100

13201320

15401540

17601760Dollars Per Metric TonDollars Per Metric Ton

PEAKPEAKCents Per PoundCents Per Pound

U.S. Polypropylene/Propylene PricingU.S. Polypropylene/Propylene PricingMonthly 2005-2008Monthly 2005-2008

FPA 10-07FPA 10-07

--1010

00

1010

2020

3030

4040

5050

6060

7070

8080

9090 9191 9292 9393 9494 9595 9696 9797 9898 9999 0000 0101 0202 0303 0404 0505 0606 0707 0808 0909 1010 1111 1212

ForecastForecast

Cents Per PoundCents Per Pound

AdjAdj PP DomesticPP Domestic PG Propylene PG Propylene -- C3C3 Cash MarginCash MarginAdjusted PP Price = Estimated Actual Injection Molding HomopolymAdjusted PP Price = Estimated Actual Injection Molding Homopolymer Price; PG Propylene = Contract Benchmark Priceer Price; PG Propylene = Contract Benchmark Price

Margin over FeedstockMargin over Feedstock

PP versus PropylenePP versus Propylene

FPA 10-07FPA 10-07

Polypropylene Key Messages• PP demand will continue to

grow despite high propylene costs

• But.. propylene sourcing issues exist

• North America = reduced investment - expect some consolidation

• Major investments in Asia Pacific and Middle East

• Margin peak likely in 2007-early 2008

• Middle East will become largest net exporter, but not a big player in North America

Polypropylene

FPA 10-07FPA 10-07

And Finally……

• Reports available….• K-Fair presentations