post-retirement: models, markets and products - models markets... · post-retirement: models,...

TRANSCRIPT

© Oliver Wyman

Post-Retirement: Models, Markets and Products

11th May 2015

Phil Joubert [email protected]

CONFIDENTIALITY

Our clients’ industries are extremely competitive. The confidentiality of companies' plans and data is obviously critical. Oliver Wyman will protect the confidentiality of all such client information.

Similarly, management consulting is a competitive business. We view our approaches and insights as proprietary and therefore look to our clients to protect Oliver Wyman's interests in our presentations, methodologies and analytical techniques. Under no circumstances should this material be shared with any third party without the written consent of Oliver Wyman.

Copyright © Oliver Wyman

Modelling aging populations 1

3 © Oliver Wyman 3

Human mortality

1 What does human mortality look like currently?

2 How has it changed in the past?

3 How might it develop in the future?

4 © Oliver Wyman 4

Infant mortality Linear increase in log hazard rates with age

Males Females 81.17 86.75

Life expectancy at birth1:

1 Calculated from the same series of tables

1 Current human mortality Lets take Hong Kong as an example

Suggests a survivor function “something like”:

5 © Oliver Wyman 5

Historic development of human mortality Steady decrease of mortality rates at all ages

2

6 © Oliver Wyman 6

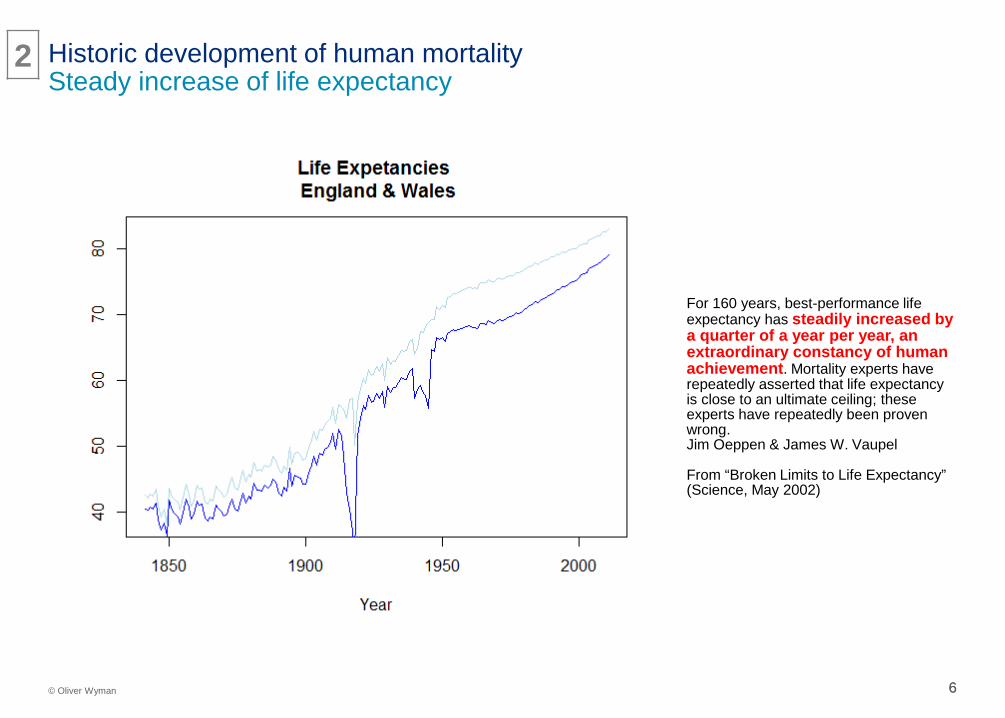

For 160 years, best-performance life expectancy has steadily increased by a quarter of a year per year, an extraordinary constancy of human achievement. Mortality experts have repeatedly asserted that life expectancy is close to an ultimate ceiling; these experts have repeatedly been proven wrong. Jim Oeppen & James W. Vaupel From “Broken Limits to Life Expectancy” (Science, May 2002)

Historic development of human mortality Steady increase of life expectancy

2

7 © Oliver Wyman 7

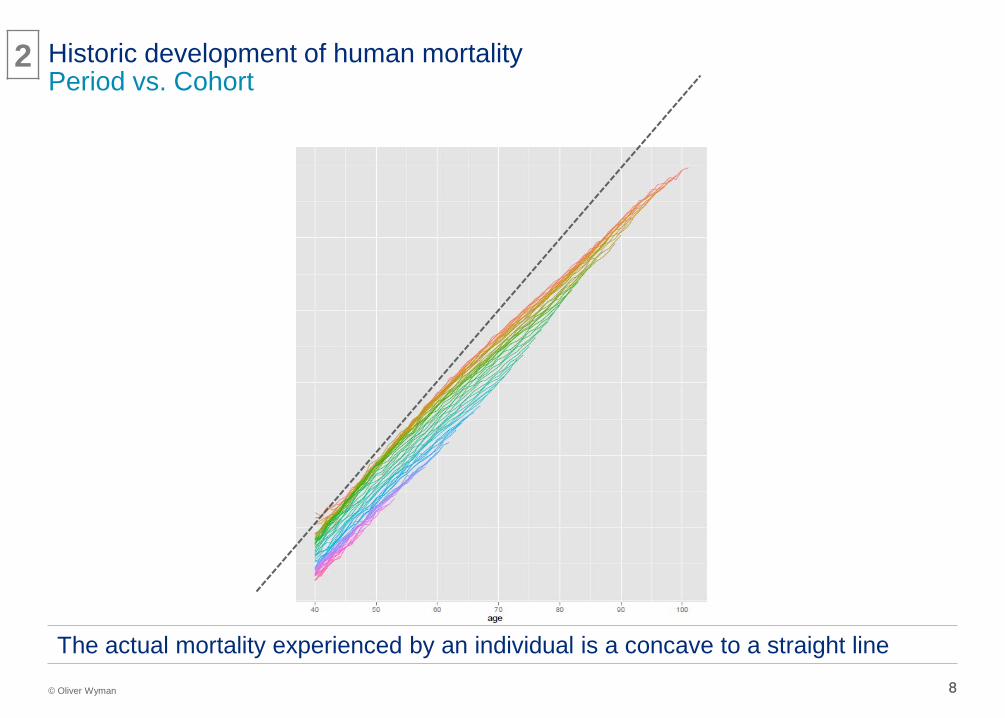

Historic development of human mortality Period vs. Cohort

Expectancies based on longitudinal mortality will underestimate the true picture

2

8 © Oliver Wyman 8

Historic development of human mortality Period vs. Cohort

2

The actual mortality experienced by an individual is a concave to a straight line

9 © Oliver Wyman 9

M1 Lee-Carter Explanatory models developed by demographers

M2 Lee-Carter + cohort effect

M3 Age, Period, Cohort

M4 CMI spline model Interpolation model developed by UK actuaries (not stochastic)

M5 CBD log-linear in age Explanatory models developed by actuaries M6 M5 + cohort

M7 M6 + quadratic term in age

M8 M5 + decreasing cohort effect

Future human mortality Stochastic models of future mortality

Cairns, Blake & Dowd define a “standard suite” of models:

3

10 © Oliver Wyman 10

Future human mortality Structural models of future mortality

As with credit models, I would expect stochastic models to outperform structural ones

3

11 © Oliver Wyman 11

Future human mortality Projecting future mortality

κ1

κ2

A: Fit model to historic data

B: Fit a n-dim random walk to

parameters

C: Run MC projections of random walk

D: Reconstruct qx and life tables

3

You can now estimate the mean values of future mortality, and the risk associated

12 © Oliver Wyman 12

3 Future human mortality Despite all this data and all these models, there is a long tradition of under-estimating future improvements in longevity

“The main source of longevity risk is (the) discrepancy between expected and actual life spans, which have been large and one-sided; forecasters, regardless of the techniques they use, have consistently underestimated how long people will live.” (IMF, Global Financial Stability Report 2012)

The role of insurance at- and post-retirement

2

14 © Oliver Wyman 14

The need for retirement products

1 Demographics and the changing nature of aging

2 Mis-estimation of life expectancy by retirees

3 Large variance of life spans after retirement

15 © Oliver Wyman 15

Source: United Nations, World Population Prospects: The 2012 Revision

0

10

20

30

40

50

1950 1975 2000 2025 2050 2075 2100

China

Eastern Asia

Japan

Western Europe

US

Popu

latio

n 60

and

ove

r (%

)

Demographics and the changing nature of aging Asian populations are aging rapidly

Population 60 and over around the world

1

16 © Oliver Wyman 16 11 May 2015

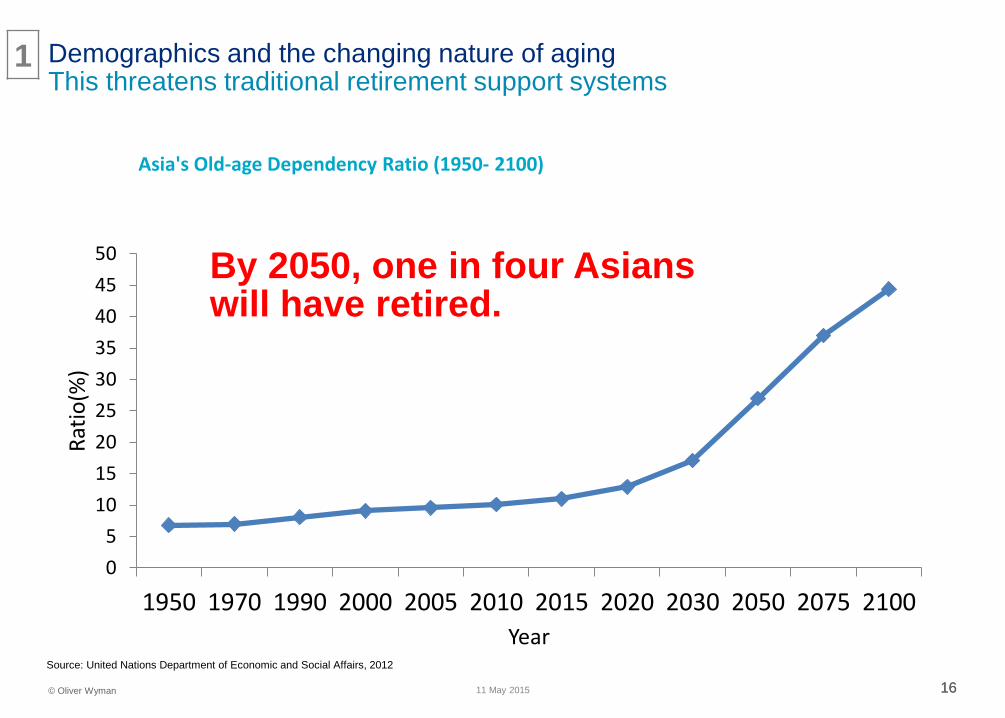

Source: United Nations Department of Economic and Social Affairs, 2012

By 2050, one in four Asians will have retired.

05

101520253035404550

1950 1970 1990 2000 2005 2010 2015 2020 2030 2050 2075 2100

Ratio

(%)

Year

Asia's Old-age Dependency Ratio (1950- 2100)

Demographics and the changing nature of aging This threatens traditional retirement support systems

1

17 © Oliver Wyman 17

Present morbidity

Extension of Longevity

Compression of Morbidity AND Extension of Longevity

Morbidity Death

75y 55y

80y 55y

75y 60y

80y 70y

Compression of morbidity

Demographics and the changing nature of aging The main goal in health is compression of Morbidity AND Extension of Longevity

Are we achieving this goal?

1

18 18 © Oliver Wyman

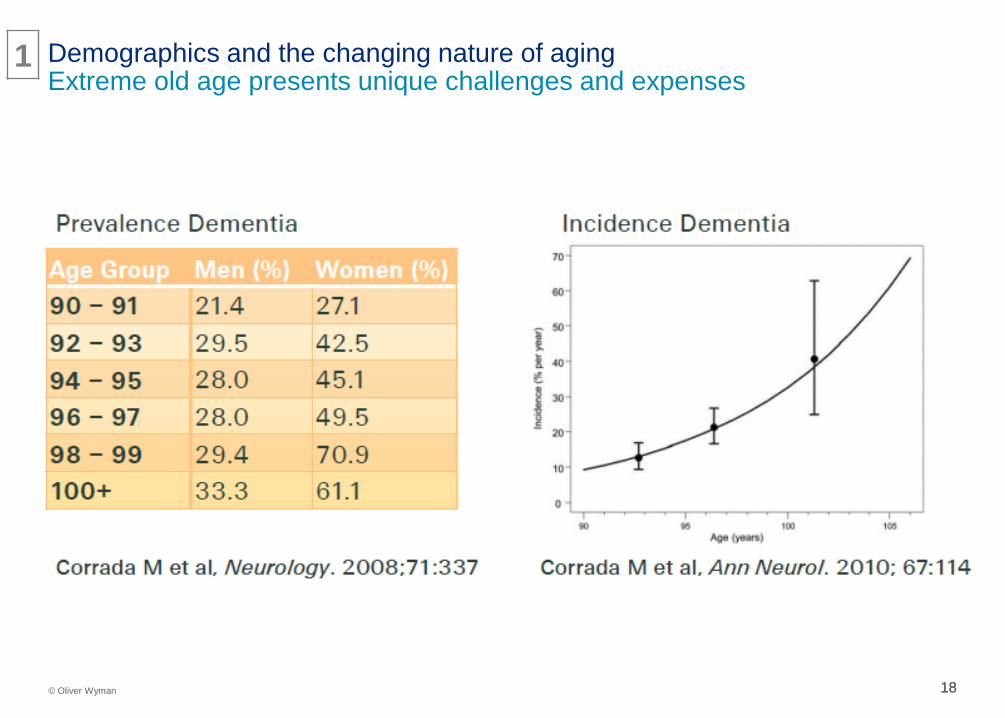

Demographics and the changing nature of aging Extreme old age presents unique challenges and expenses

1

19 © Oliver Wyman 19

2 Mis-estimation of life expectancy by retirees Studies consistently show that people tend to under-estimate life spans

This creates a genuine risk that they will outlive their savings – but also presents a communication problem

20 20 © Oliver Wyman

131415161718192021

1988 1992 1996 2000 2004 2008

Expe

cted

num

ber o

f yea

rs

of li

fe re

mai

ning

Male at age 65 Female at age 65

Survival probabilities of 65 year olds Segmented by gender, 2010

Men’s and Women’s longevity risk over time 1988–2008

17.3

20.0

0%10%20%30%40%50%60%70%80%90%

100%

65 70 75 80 85 90 95 100Female Male

18%

16%

13%

9%

9%

7%

2%

Biggest concern about retirement Having enough money

Staying productive and useful Providing for your own/spouse's/partner's long-term care needs

Outliving retirement money Being able to afford health care in your retirement years

Having to work full or part-time to live comfortably in retirement Having a comprehensive financial plan for retirement

Source: GfK custom research with MetLife, HLTC4

3 Large variance of life spans after retirement Even if they had perfect life expectancy forecasts, pensioner still have a large chance of outliving their savings

21 21 © Oliver Wyman

The supply side: reasons for insurers to get involved

Customers’ needs change as they age and transition into retirement: • They no longer need traditional protection

products

• They do need longevity and care insurance

• They remain the wealthiest segment of the population in most economies

Pensioners are a large and attractive group of customers

Products, market infrastructure & manufacturing

3

23 © Oliver Wyman 23

LIF/RIF with institutional pooled funds

GMWB products

“Ideal” product combination

Life annuities, deferred annuities

Fixed term annuities

The retirement trilemma Low cost, high return and flexible products…

Access to capital

Protection from risk

Good returns

… delivered by the Easter Bunny

24 © Oliver Wyman 24

Innovation in post-retirement products – the buzz New products launched every week, much innovation expected in the UK

"iPipeline Launches New Retirement Planning Solution”

“Allianz Life introduces two new annuity investment options”

“Cooking up a storm with a new recipe for retirement income solutions”

“Canada Life […] will launch three retirement income products…”

“New York Life debuted its Clear Income Fixed Annuity”

“Voya Financial unveils new deferred index-linked variable annuity”

“New PIMCO head convenes task force to tackle retirement income solutions”

25 © Oliver Wyman 25

Focus on distribution, communication and lowering costs, rather than innovation?

Innovation in post-retirement products – the reality The current industry suite

26 26 © Oliver Wyman

Offer components – examples

Offer components – considerations Example players

• Home assistance • Travel • Lifestyle

• Sourcing service providers

• Economics/ Payment model

• Role in customer acquisition/retention

• Banking • Direct share trading • Own portfolio mgt. • Home equity release • Planning, advice and

education

• De-siloing FS conglomerates

• Single customer view • Integration with

advice model

• Lifetime annuities (immediate and deferred)

• Variable annuities • Enhanced annuities

• Risk appetite • Balance sheet

strength • Pricing and

source of value

• Income funds • Lifecycle funds • Risk-managed funds

(CPPI, managed vol etc.)

• Breadth of fund range vs. focus of offer

• Price vs. value • Income vs. growth

Fund products

Balance sheet products

Personal financial management

Retirement lifestyle services

Expanding scope of retirement offer

The current suite, seen from a different angle Insurers must use their balance sheets to differentiate themselves

27 27 © Oliver Wyman

• Tax treatment

• Capital requirements

• Risk of mis-selling Tax & Regulation

• Long bond market

• Illiquids

• Equity index Futures

• Swaps

• Reinsurance Hedging Markets

• Risk Appetite

• Risk Management

• Systems & Processes

Internal Capability

Branding & Distribution

• Access to retirees

• Trusted name

Building a post-retirement business Internal and external factors play a part

Customer

• Segmentation

• Channel

• Analytics

• Customer experience

Alternatives • Fund

managers

• Banks

28 28 © Oliver Wyman

• The UK was the world’s largest annuity market

• Annuitisation at retirement was forced by law

• Most retirees rolled their savings over into the default annuity offered by the same provider who managed their accumulation phase

• The market was ripe for disruption

Case Study: UK enhanced annuity and equity release players

• Several niche players started offering annuities at favourable rates to smokers and those in poor health

• They backed the annuity liabilities by a combination of corporate bonds and equity release mortgages

• Hannover Re supported them with reinsurance and technical knowhow

• Just Retirement grew its balance sheet from zero to over £10Bn in under ten years

• Together the EA / ER players were capturing significant chunks of the open-market annuity flow

• Several were backed by PE money and floated / traded in 2013

• Then came the budget of 2014…

The initial situation The disrupting model The result

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

29 29 © Oliver Wyman

Guarantee types

Move to CPPI style Prudential HDL John Hancock

Innovative underlyings

Capped vol Target vol Internal fund hedging Restricted fund choice

AXA GMIBs Met GMIB Max Transamerica

Activity based adjustments

Shift to a lower risk fund strategy when policyholder triggers a higher cost event

Ameriprise SS

Benefit innovations

Variable fees …

SunAmerica benefits

• Risk management options are available in the various markets (active futures exchange, liquid swaps market)

• Product launches outside the US have failed – customer interest has been muted, perhaps due to the complicated nature of the products

• Japan has a large market for VA’s, and products have recently been launched in Korea

1. VA’s represent an attractive client proposition

2. But have not been great for providers

3. Modern designs try to mitigate the risks, but retain the attractiveness

4. Things to consider in the Asian context:

Case Study: Variable Annuities

Summary & Questions 4

31 © Oliver Wyman 31

Summary

A Longevity risk – can be modelled

B Insurance post-retirement – mutual interest?

C Products – packaging, manufacturing and delivery

? Questions or comments?

32 © Oliver Wyman 32

Speaker Bio

11 May 2015

Phil Joubert is a principal in the Financial Services practice of Oliver Wyman, based in Hong Kong Office. Phil has fifteen years of experience in the financial services industry, having worked in areas as diverse as actuarial consulting and derivatives trading. He has worked in both Europe and Asia-Pac for a variety of insurers, banks and software houses, and specialises in risk and capital modelling and systems design Recent experience

• Regulatory capital model design and implementation for several insurers in Europe • Economic capital implementation for leading pan-Asian insurance group • Derivatives trading and market risk management • Capital aggregation systems design for leading ESG provider • Actuarial automation implementation project for specialist life insurer

Phil holds an MSc in Finance & Mathematics from Imperial College and is a Fellow of the Faculty of Actuaries. He joined Oliver Wyman in 2014, having spent several years as an independent actuarial consultant. Previously he worked at Deutsche Bank and Natixis as a trader and he started his career with Deloitte Actuarial.

QUALIFICATIONS, ASSUMPTIONS AND LIMITING

CONDITIONS

This report is for the exclusive use of the Oliver Wyman client named herein. This report is not intended for general circulation or publication, nor is it to be reproduced, quoted or distributed for any purpose without the prior written permission of Oliver Wyman. There are no third party beneficiaries with respect to this report, and Oliver Wyman does not accept any liability to any third party.

Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been independently verified, unless otherwise expressly indicated. Public information and industry and statistical data are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information. The findings contained in this report may contain predictions based on current data and historical trends. Any such predictions are subject to inherent risks and uncertainties. Oliver Wyman accepts no responsibility for actual results or future events.

The opinions expressed in this report are valid only for the purpose stated herein and as of the date of this report. No obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

All decisions in connection with the implementation or use of advice or recommendations contained in this report are the sole responsibility of the client. This report does not represent investment advice nor does it provide an opinion regarding the fairness of any transaction to any and all parties.