potential of high accruals through managed credits

TRANSCRIPT

September 2014

Potential of High Accrual

through Managed Credit

We recommend you read the presentation in entirety

1

Why does an investor invest?

The Prudent Investor manages risk in order to generate return

Aim of an Investor: To generate returns so as to grow his purchasing power

Investment Returns Inflation Destroy purchasing power

Investment Returns Inflation Maintain purchasing power

Investment Returns Inflation Enhance purchasing power

< <

CLICK HERE TO INVEST NOW

This risk is less apparent to an investor as it is an indirect

risk.

India has seen high levels of Consumer Price Inflation in

the past 2.5 years.

2

What are the key Risks, an investor needs to be aware of?

7.55%

11.24%

7.31%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

12.00%

1-J

an-1

2

1-M

ar-

12

1-M

ay-1

2

1-J

ul-1

2

1-S

ep-1

2

1-N

ov-1

2

1-J

an-1

3

1-M

ar-

13

1-M

ay-1

3

1-J

ul-1

3

1-S

ep-1

3

1-N

ov-1

3

1-J

an-1

4

1-M

ar-

14

1-M

ay-1

4

CPI Inflation in India

CPI Inflation (Y-o-Y)

An obvious risk from the perspective of an

investor.

In case of some investment products, the value

of investment can rise or fall depending on the

market conditions.

Volatility of Capital is the risk that value of

investment may fall when the investor needs

the capital

While making investment decisions, investors should take into account both risks:

The Volatility of Capital and The Risk of Inflation reducing the purchasing power. Source (latest available date): CPI Inflation RBI – from Jan 2012 – June 2014

VOLATILITY OF CAPITAL RISK OF INFLATION REDUCING THE

PURCHASING POWER

CLICK HERE TO INVEST NOW

What are the Components of Return?

3

The Invested Capital Remains constant, income is

earned in the form of regular payments

The Value of Invested Capital fluctuates with no regular

income

For a detailed explanation of Accrual and Capital Return, please refer Appendix

Capital

Gain/Loss

Accrual

Income Total Return

The Accrual – Capital Appreciation Spectrum

TOTAL

RETURN

The Accrual Component of Return

The Capital Gain/Loss on the Invested Capital

ACCRUAL

CAP

GAIN/LOSS

CLICK HERE TO INVEST NOW

4

What are the Investment Options available?

Typical Investment Options

Bank Fixed Deposits

Where do these Investments lie along the Accrual – Capital Appreciation Spectrum?

Public Provident Fund

National Savings Certificate

Corporate Deposits

Corporate Bonds

Government Bonds

Debt Mutual Funds

Debt Equity Real Estate Gold

Listed Shares

Equity Mutual Funds

Private Equity

Self-Occupied

Let-out Property

Physical Gold

Gold ETFs

CLICK HERE TO INVEST NOW

5

Accrual – Capital Gains Spectrum

TOTAL

RETURN

ACCRUAL

CAP

GAIN/LOSS

Increased Volatility of Capital

• Debt Mutual

Funds

• Corporate

Bonds

• Government

Bonds

• Bank Fixed

Deposits

• PPF

• NSC

• Corporate

Deposits

• Listed

Shares

• Equity

Mutual

Funds

• Private Equity

• Self-Occupied

Real Estate

• Physical Gold

& Gold ETFs

Potential to Generate Higher Returns

Dividend

component of

Equity Products

CLICK HERE TO INVEST NOW

6

How do Debt Mutual Funds Generate α? By Managing Risks

Man

ag

ing

Cre

dit

Ris

k

Managing Interest Rate Risk

Accrual Return can be generated

by investing in fixed-income

securities with Higher Yield

Capital Gains can be generated

by actively managing portfolio*

in line with Interest Rate

movement

*Actively managing Maturity of the portfolio to capitalize on opportunities. For example,

• if market yields are expected to fall, increase the portfolio maturity with an aim to benefit from the rise in value of the bonds.

• If market yields are expected to rise, reduce the portfolio maturity with an aim to minimize capital losses

This slide is for illustration purposes only and should not be construed as an investment strategy / investment advice.

CLICK HERE TO INVEST NOW

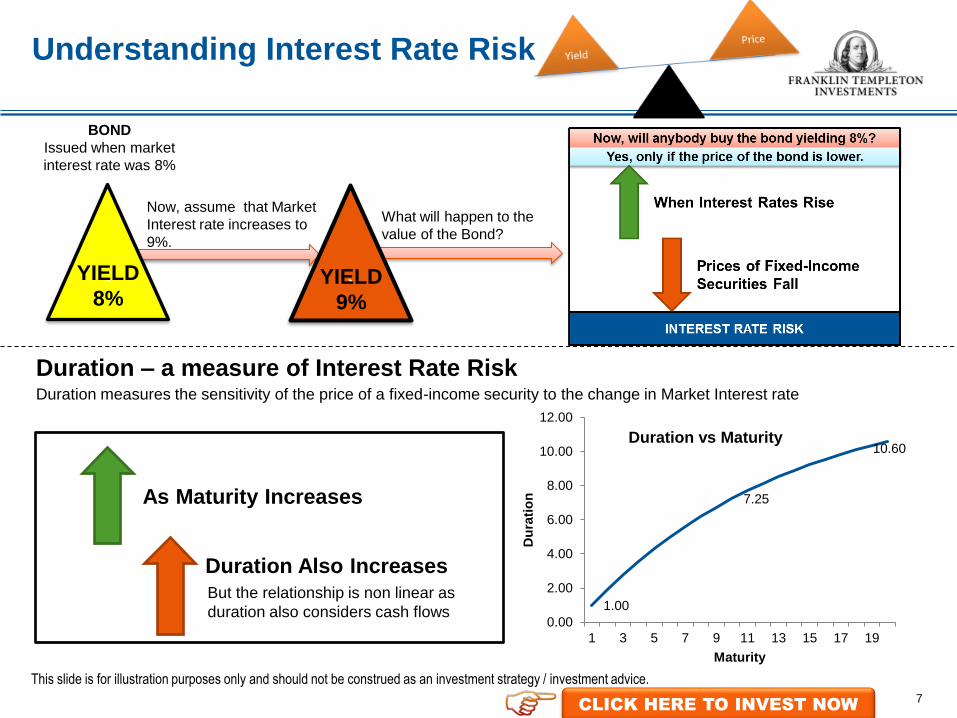

Duration – a measure of Interest Rate Risk Duration measures the sensitivity of the price of a fixed-income security to the change in Market Interest rate

Understanding Interest Rate Risk

1.00

7.25

10.60

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1 3 5 7 9 11 13 15 17 19

Du

rati

on

Maturity

Duration vs Maturity

As Maturity Increases

Duration Also Increases

But the relationship is non linear as

duration also considers cash flows

` YIELD

8% `

YIELD

9%

BOND

Issued when market

interest rate was 8%

Now, assume that Market

Interest rate increases to

9%.

What will happen to the

value of the Bond?

This slide is for illustration purposes only and should not be construed as an investment strategy / investment advice.

7 CLICK HERE TO INVEST NOW

8

Popular Strategies followed by Debt Mutual Funds to generate α

High Accrual-led Strategies aim to generate α by managing Credit Risk while minimizing Interest Rate Risk

High Accrual Led Strategies

TOTAL RETURN

Primary objective is to generate returns by actively

managing portfolio duration based on market

outlook without taking substantial credit risk

Higher Yield is obtained by Managing Credit

Risk through bottom-up security selection

Capital Gains are obtained by Managing

Interest Rate Risk through top-down Macro

analysis

Buy & Hold – Investments are generally held till

Maturity

Active Management based on Market Outlook

Accrual strategies are generally market timing

agnostic

Capital appreciation strategies focus on market

timing

ACCRUAL CAP GAIN/LOSS

TOTAL RETURN

CAPITAL GAINS ACCRUAL

Primary objective is to generate accrual returns

by investing in securities with higher yields and

potential for capital gains over the long term.

Capital Appreciation Led strategies

This slide is for illustration purposes only and should not be construed as an investment strategy / investment advice.

CLICK HERE TO INVEST NOW

9

Why High Accrual Led Strategies?

• Bank Fixed

Deposits

• PPF

• NSC

• Dividend

Paying

Stocks

• Equity

Mutual

Funds

• Private Equity

• Self-Occupied

Real Estate

• Physical Gold

& Gold ETFs

Increased Volatility of Capital

• Debt Mutual

Funds

• Corporate

Bonds

• Government

Bonds TOTAL

RETURN

ACCRUAL

CAP APP

High

Accrual

Led

Strategies

Capital

Appreciation

Led

Strategies Anchor Your Portfolio

Managed Credit Helps identifying securities with Higher Yields

Potential of generating less Volatile Returns across Market

Conditions

Potential of Capital Gains in the Long Term

Advantages of High

Accrual Led Strategies

Potential to Generate Higher Returns

CLICK HERE TO INVEST NOW

10

Higher Yields through Managed Credit But isn’t Managed Credit inherently Risky?

Source

of α

Level of Risk

Credit

Risk

Interest

Rate Risk

Capital

Gains Low High

Cre

dit

Ris

k

Interest Rate Risk

Source

of α Level of Risk

Higher

Yield +

Capital

Gains

Credit Risk Interest

Rate Risk

Medium Low to

Medium

High Accrual Led Strategies

Capital Appreciation Led strategies

through G-Sec/AAA bonds

Level of Risk for High Accrual Led strategies may be relatively lower than the risk for High

Credit (through G-Sec/AAA bonds) Capital Appreciation Led funds

CLICK HERE TO INVEST NOW

11

High Accrual Led Strategies tend to generate stable Returns

The aforesaid portfolios are for illustration purposes only and should not be construed as investment strategies / investment advice. Investors should

consult their investment advisor and construct their portfolios based on their risk appetite, time horizon, investment goals, etc.

Returns – High Accrual Led vs Capital Appreciation Led Strategies Hypothetical Returns over an Interest rate Cycle assuming that Interest Rates increased by 50bps in Years 4,8,10 and

decreased by 50 bps in Years 2,5,6 and remained constant in other years.

Due to lower volatility of Capital and Higher Yields, High Accrual Led

Strategies aim to deliver less volatile returns

-10%

-5%

0%

5%

10%

15%

20%

Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

Accrual Led Strategy

Accrual Return Capital Return Total Return

-10%

-5%

0%

5%

10%

15%

20%

Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

Capital Appreciation Led Strategy

Accrual Return Capital Return Total Return

Lower Volatility of Capital Gains/Losses

Higher Yields

Compounded Annual Return: 9.55%

Standard Deviation: 0.71% Compounded Annual Return: 9.55%

Standard Deviation: 5.28%

12

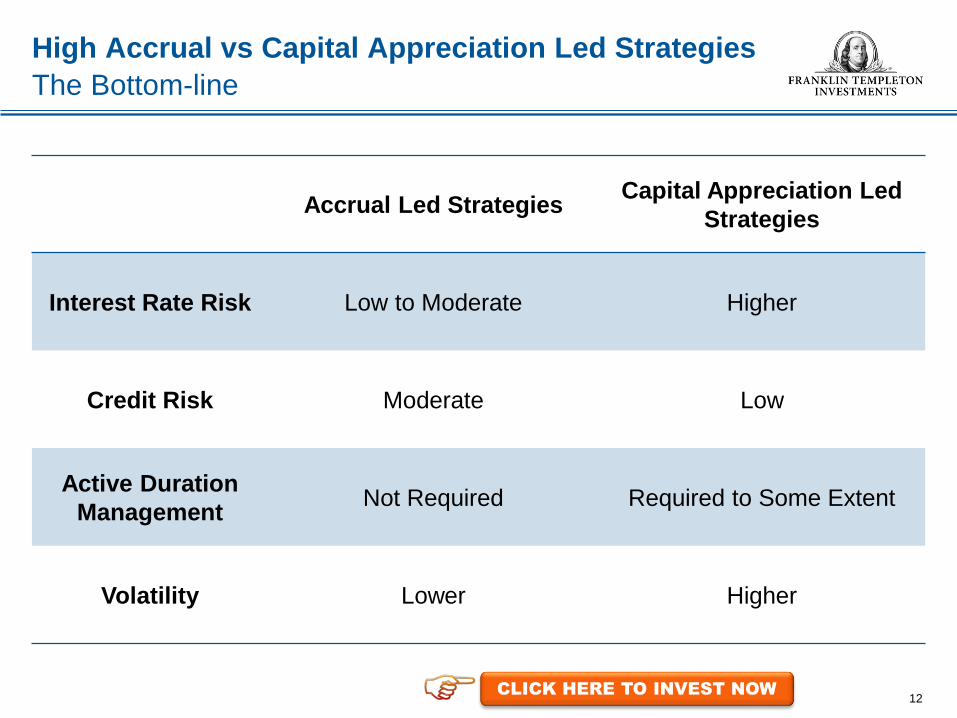

Accrual Led Strategies Capital Appreciation Led

Strategies

Interest Rate Risk Low to Moderate Higher

Credit Risk Moderate Low

Active Duration

Management Not Required Required to Some Extent

Volatility Lower Higher

High Accrual vs Capital Appreciation Led Strategies

The Bottom-line

CLICK HERE TO INVEST NOW

Factor Open-Ended Closed-Ended

Liquidity Management Does the fund need active liquidity management to meet redemptions? Yes No

Portfolio Management Does the fund manager have flexibility to benefit from market opportunities? Yes Limited

(buy & hold strategy)

Maturity profile constraints Does the constraint of maturity date restrict the investment opportunities? No Yes

Relative ease of redemption Can an investor redeem in case of emergency? Yes

Limited (has to be sold over the

stock exchange)

Open-Ended Accrual Led Debt Funds – Stand to benefit

In light of the recent tax-amendments in Union Budget FY15

The change in holding period for Long Term Capital Gain benefit will reduce liquidity pressures/risk,

especially for short term debt funds.

13

Open-ended debt funds: Offer liquidity and LTCG benefit (for >36 months) without any re-investment hassles

Close-ended debt funds: Require re-deployment of maturity receipts for minimum 36 months to qualify for LTCG.

CLICK HERE TO INVEST NOW

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

11.00%

0 1.5 3 4.5 6 7.5 9

Duration

Yie

ld t

o M

atu

rity

Franklin Templeton’s Fixed Income Product Range

YTM and Duration as of 28-August-2014

14

Past performance may or may not be sustained in the future.

Depending on the investment horizon and risk appetite, an investor can choose any of

Franklin Templeton’s Accrual Led Products

Accrual Led Products

FILDF

FIUBF

FISTIP

FIIOF

FICBOF

FIIBA FIINCF

FIGSF-LT

FIBPDF

FIGSF - CP/PF FISPF

FITMA

CLICK HERE TO INVEST NOW

Product Labels

15

BROWN: Investors understand that their principal will be at high risk

YELLOW: Investors understand that their principal will be at medium risk

BLUE: Investors understand that their principal will be at low risk

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them. **Note: Risk may be represented as:

Historical Fund Name Name w.e.f. June 30, 2014 This product is suitable for investors who are seeking* (level of risk)

Templeton India Income Fund (TIIF)

Franklin India Income Fund (FIINCF)

• Medium term capital appreciation with current income • A long bond fund investing in quality fixed income instruments across segments.

Templeton India Income Builder Account (TIIBA)

Franklin India Income Builder Account (FIIBA)

• Medium term capital appreciation with current income • A long bond fund – focuses on Corporate/PSU Bonds.

Templeton India Short-Term Income Plan (TISTIP)

Franklin India Short Term Income Plan (FISTIP)

• Regular income for medium term • A fund that invests in short term corporate bonds including PTCs

Templeton India Ultra-short Bond Fund (TIUBF)

Franklin India Ultra Short Bond Fund (FIUBF)

• Regular income for short term • A fund that invests in short term debt and money market instruments

Franklin India Savings Plus Fund (FISPF)

- • Regular income for short term • A fund that invests primarily in floating and short term fixed rate debt instruments

Templeton India Government Securities Fund (TGSF)

Franklin India Government Securities Fund (FIGSF)

• Medium term capital appreciation with current income • A fund that invests in Indian government securities

Templeton India Low Duration Fund (TILDF)

Franklin India Low Duration Fund (FILDF)

• Regular income for short term • An income fund focusing on low duration securities.

FT India Monthly Income Plan (FTIMIP) (with no assured returns)

Franklin India Monthly Income Plan (FIMIP) (with no assured returns)

• Medium term capital appreciation with current income • An MIP investing predominantly in debt instruments with marginal equity exposure

Templeton India Income Opportunities Fund (TIIOF)

Franklin India Income Opportunities Fund (FIIOF)

• Medium term capital appreciation with current income • A fund that invests across the yield curve - focusing on high accrual securities

Templeton India Corporate Bond Opportunities Fund (TICBOF)

Franklin India Corporate Bond Opportunities Fund (FICBOF)

• Medium to long term capital appreciation with current income • A bond fund focusing on corporate securities

Templeton India Treasury Management Account (TITMA)

Franklin India Treasury Management Account (FITMA)

• Regular income for short term • A liquid fund that invests in short term and money market instruments

Franklin India Banking & PSU Debt Fund (FIBPDF)

- • Regular Income for medium term • An income fund that invests predominantly in debt and money market instruments

issued by Banks and Public Sector Undertakings.

16

Franklin Templeton’s Accrual Led Products Overview

Franklin India Short Term

Income Plan

Franklin India Income

Opportunities Fund

Franklin India Corporate Bond

Opportunities Fund

Positioning Matrix

Investment Objective

Nature of Scheme

Risks: Interest Rate Risk

Risks: Credit Risk

12-15 Months 18-21 Months >30 Months

To Provide Stable returns

by investing in fixed

income securities

Regular income and capital

appreciation by investing in

fixed income securities

across the yield curve

Regular income and capital

appreciation by investing

predominantly in corporate

securities

Regular Income

Capital

appreciation with

current income

Capital

appreciation with

current income

Low to Moderate Low to Moderate Moderate

Low to Moderate Moderate Moderate

Indicative Investment

Horizon

CLICK HERE TO INVEST NOW

17

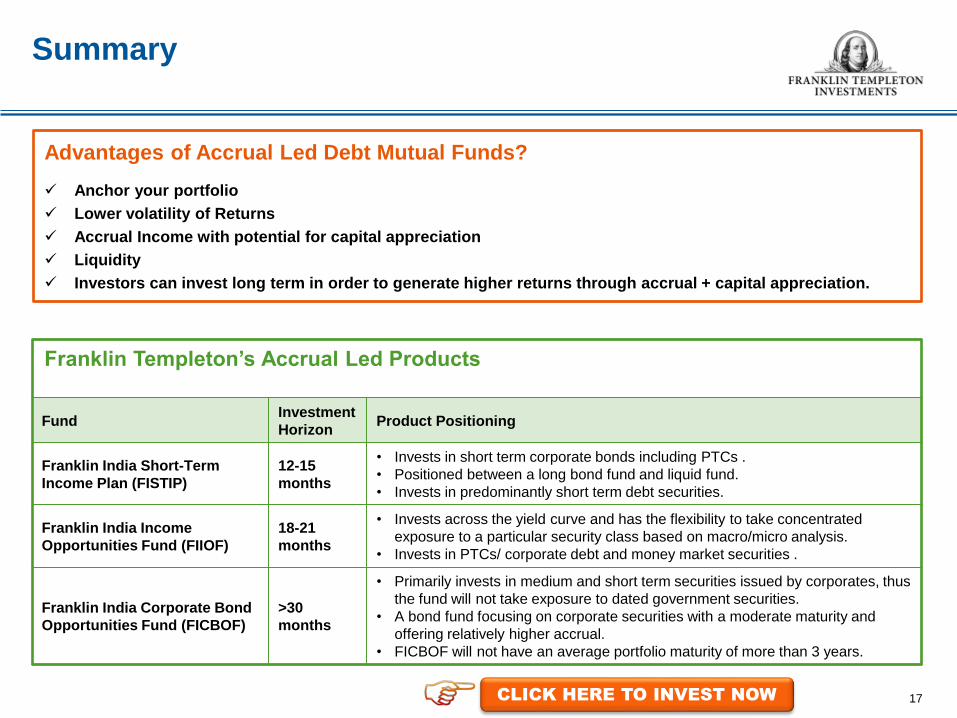

Summary

Advantages of Accrual Led Debt Mutual Funds?

Anchor your portfolio

Lower volatility of Returns

Accrual Income with potential for capital appreciation

Liquidity

Investors can invest long term in order to generate higher returns through accrual + capital appreciation.

Franklin Templeton’s Accrual Led Products

Fund Investment

Horizon Product Positioning

Franklin India Short-Term

Income Plan (FISTIP)

12-15

months

• Invests in short term corporate bonds including PTCs .

• Positioned between a long bond fund and liquid fund.

• Invests in predominantly short term debt securities.

Franklin India Income

Opportunities Fund (FIIOF)

18-21

months

• Invests across the yield curve and has the flexibility to take concentrated

exposure to a particular security class based on macro/micro analysis.

• Invests in PTCs/ corporate debt and money market securities .

Franklin India Corporate Bond

Opportunities Fund (FICBOF)

>30

months

• Primarily invests in medium and short term securities issued by corporates, thus

the fund will not take exposure to dated government securities.

• A bond fund focusing on corporate securities with a moderate maturity and

offering relatively higher accrual.

• FICBOF will not have an average portfolio maturity of more than 3 years.

CLICK HERE TO INVEST NOW

18

The information contained in this presentation is not a complete representation of every material fact regarding any industry,

security or the fund and is neither an offer for units nor an invitation to invest. This communication is meant for use by the

recipient and not for circulation/reproduction without prior approval. The views expressed by the portfolio managers are

based on current market conditions and information available to them and do not constitute investment advice.

Scheme Classification and Objective: Franklin India Short Term Income Plan (FISTIP) is an open end income scheme

with an objective to provide stable returns by investing in fixed income securities. Franklin India Income Opportunities

Fund (FIIOF) is an open end income fund that seeks to provide regular income and capital appreciation by investing in fixed

income securities across the yield curve. Franklin India Corporate Bond Opportunities Fund (FICOBF) is an open-end

income fund which seeks to provide regular income and capital appreciation through a focus on corporate securities.

Load Structure: The investors are requested to check the prevailing load structure of the scheme before investing. Please

refer website/latest SID/addenda for the latest load structure of the respective schemes.

Risk Factors: Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

The NAVs of the schemes may go up or down depending upon the factors and forces affecting the securities market. The

Mutual Fund is not guaranteeing or assuring any dividend under any of the schemes and the same is subject to the

availability and adequacy of distributable surplus. The past performance of the mutual funds managed by the Franklin

Templeton Group and its affiliates is not necessarily indicative of future performance of the schemes. Investors are

requested to review the prospectus carefully and obtain expert professional advice with regard to specific legal, tax and

financial implications of the investment/participation in the scheme.

Risk Factors

18

© 2014 Franklin Templeton Investments. All rights reserved.

Franklin Templeton Asset Management (India) Pvt. Ltd.

Indiabulls Finance Centre, Tower 2,

12th and 13th floor, Senapati Bapat Marg,

Elphinstone (W)

Mumbai 400013

Tel (91-22) 6751 9100

Fax (91-22) 6639 1281

www.franklintempletonindia.com

19