powerpoint presentation - no slide...

TRANSCRIPT

Presenter:Gene IsenbergChairman & CEO

LEHMAN BROTHERS

19TH ANNUAL CEO ENERGY/POWER

CONFERENCE

September 7, 2005

2

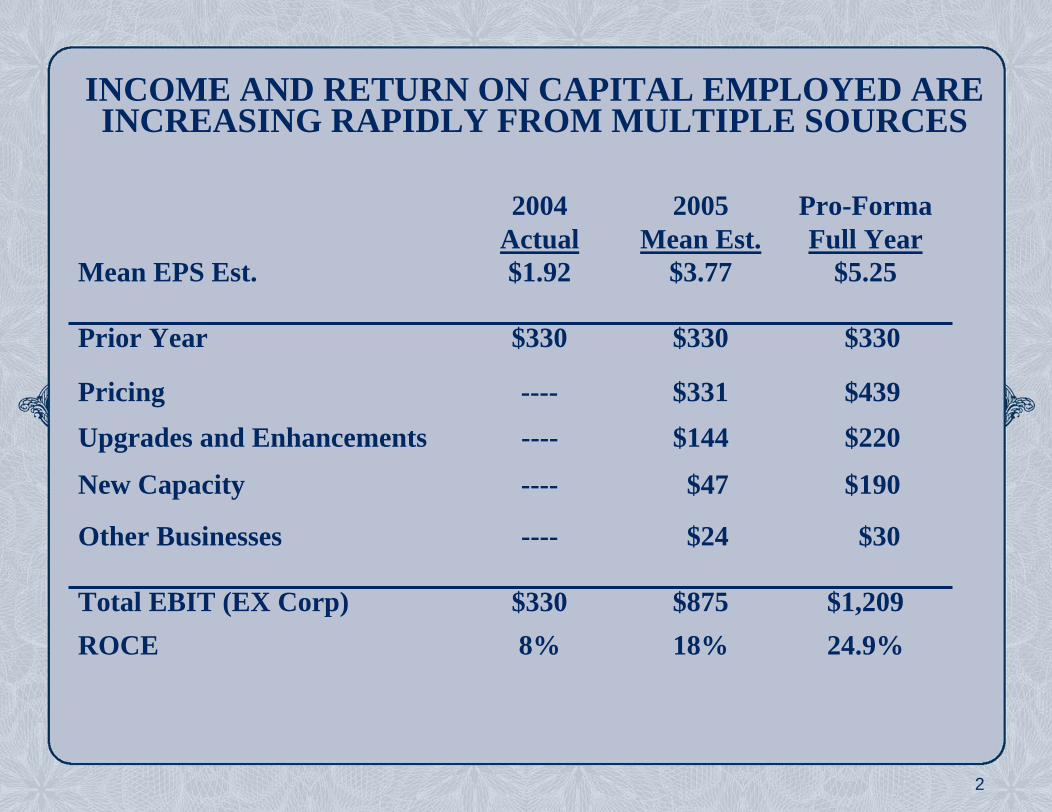

INCOME AND RETURN ON CAPITAL EMPLOYED ARE INCREASING RAPIDLY FROM MULTIPLE SOURCES

2004Actual

2005Mean Est.

Pro-FormaFull Year

Mean EPS Est. $1.92 $3.77 $5.25

Prior Year $330 $330 $330

Pricing ---- $331 $439Upgrades and Enhancements ---- $144 $220

New Capacity ---- $47 $190

Other Businesses ---- $24 $30

Total EBIT (EX Corp) $330 $875 $1,209ROCE 8% 18% 24.9%

3

2005 CAPITAL PROGRAM

Forecasted Capital Expenditures for 2005 = $1.1 Billion

$370 mm New Construction$320 mm Upgrades and Enhancements$280 mm Maintenance$100 mm Acquisitions and Oil & Gas Investments

$67 mm Mfg. & Logistics, Oil & Gas

$400 mm International$320 mm US Lower 48 Drilling$140 mm Canada$110 mm US Well Service$33 mm US Offshore and Alaska

4

Balance Sheet Data as of June 30, 2005

A CONSERVATIVE AND FLEXIBLE FINANCIAL POSITION

(1) Some debt issues are unrated

ActualCash & Securities 1,580Accounts Receivable 619Working Capital 591Property, Plant and Equipment, Net 3,461Total Assets 6,309Total Debt 2,018Stockholders’ Equity 3,291Total Debt to Total Capitalization 38%Net Debt to Capitalization 12%Weighted Average Shares Outstanding 161Moody’s Rating (1) A3Standard & Poors A-Indexes S&P 500, OSX

($ in millions)

5

Drilling2004Avg.

2Q05Avg. Today

1Q06Expected

North America6

2461550

7219

408

450125575

Alaska 7 7 10US 48 Drilling 199 229 260GOM Offshore 14 17 19Canada 47 26 70InternationalInt’l Land (1) 52 66 78Int’l Offshore (1) 16 18 20

Total Drilling 335 363 457

W.O./Well ServicingUS Lower 48 400 438 462Canada 138 110 138

Total W.O./Well Servicing 538 548 600

FLEET STATUS AS OF SEPTEMBER 3, 2005

(1) Represents Nabors’ Net Interest in J.V. Rigs in Saudi @ 50%, operating rig count includes those leased from GOM Offshore(2) Represents current firm and prospective near-term contract committments

6

North American gas decline rates imply 20+ BCFPD/year

Timing of the supply impact of stranded and imported gas

Additional drilling is required in US & Canadian Basins

Longer term, LNG will ultimately become the marginal supply

Global oil supply challenges and increasing demand

STRONG FUNDAMENTALS UNDERPIN POSITIVE OUTLOOK

Supply challenges point to a more orderly and sustainable cycle

7

Strong and sustaining rig demand- North America- Internationally

Nabors best positioned to capture disproportionate shareTerm contracts are underwriting capacity and efficiency investmentsOngoing reactivation programAccelerating new build program

RIG MARKET DYNAMICS

8

U.S. LOWER 48 LAND DRILLING DOMINATED BY GAS

TODAY – 1220Y-T-D – 1161

Source: Baker Hughes, Bloomberg

376463

564 563484

717691

939870

1025PEAK = 1068

Land Rigs 2001 2005

Now N/A 1,319

Avg. 981 1,214

High 1114 1,319

Low 743 1,117

9

650

700

750

800

850

900

950

1000

1050

1100

1150

1200

1/3/031/24/032/14/03

3/7/033/28/034/18/03

5/9/035/30/036/20/037/11/03

8/1/038/22/039/12/0310 /3/0310 /24 /0311 /14 /03

12 /5/0312 /26 /03

1/16/042/6/042/27/043/19/04

4/9/044/30/045/21/046/11/04

7/2/047/23/048/13/04

9/3/049/24/0410 /15 /04

11 /5/0411 /26 /0412 /17 /04

1/14/052/4/052/25/053/18/05

4/8/054/29/055/20/056/10/05

7/1/057/21/058/12/05

100110120130140150160170180190200210220230240250

1/3/03 08/26/05 Increase

BHI 675 1165 490 73%

NBR 108 248 140 129%

NBR Incremental Share = 29% since 1/3/03

NABORS US LOWER 48 VS. BHI LAND RIG COUNTAverage well depth and complexity is increasing

Source: Baker Hughes – Excludes N.E. States, California and Alaska

NBR Rigs

BHI NBR Area

10

REACTIVATIONS AND NEW BUILDS

Strength and breadth of demand for additional higher capability rigs

Adequate cash flow and multi-year contracts are underwriting investments

Strongest rig demand is for mid-depth rigs where inventory is depleted

Evolution and advantages of A/C drive technology

Drilling efficiency improvements driving demand for upgraded rigs– Higher hydraulic horsepower– Automated systems; pipe handling, BOP’s, etc.– Faster moving capability

Escalating cost of reactivations versus favorable cost of new construction

11

ECONOMICS OF CURRENT RIG REACTIVATIONS

Seven rigs currently being reactivated/refurbished

– (2) 2,000 HP, (1) 1,500 HP, (1) 900 HP, (2) 750 HP

Total expected cost = $11.5 million ($250K - $3.5MM)

Estimated annual cash flow = $24 million

Average years to cash payout = 0.50 years

12

NABORS’ EDGE IN NEW CAPACITY

Advantageous cost and availability of capitalAdvantageous operating costs

– Established infrastructure in 22 countries– Economies of Scale– Synergies among subsidiaries

Advantageous capital costs of new and reactivated rigs– Procuring for over 400 operating rigs yields favorable

price and delivery– Multiple sourcing of major components and rig delivery

Advantageous delivery schedule•Multiple rigs in multiple venues, quicker

13

NEW PACE RIG PROGRAM TYPICAL RETURNSAFTER TAX CASH PAYOUT IN YEARS

Rig Capacity North America International

750 HP 3.0 3.0

1,000/1,500 HP 3.0 3.0

2,000 HP ---- 3.3

3,000 HP ---- 4.1

14

Innovative new rig configurations•Pad development (lift and roll moving system)•Fast moving “FMLR” Class PACE Rigs•New A/C Coiled Tubing/STEM Drilling Rig•MODS (Modular Offshore Dynamics Series) Platform Rig for deepwater SPAR & TLP platforms

•New generation workover rigs

40 – 500 horsepower rigs

20 – 200 horsepower rigs

DRILLING EFFICIENCY INITIATIVES ENABLE LOWER WELL CYCLE TIMES AND COSTS

15

INCREASED INTERESTIN PAD DRILLING

Multiple wells drilling directionally from sites in environmentally sensitive areasNabors pioneered pad drilling in the 1970’s –1990’s on the North Slope of AlaskaAdapting new generation “Lift and Roll” skid systems from North Slope applicationsApplications:– McKenzie Delta– Tar Sands– US Rocky Mountains – Various International venues

Advantages:– Faster moves– Smaller environmental impact– Faster field development

16

Fast moving “PACE” (programmable A/C electric class rigs)

750–3,000 horsepower electric A/C drive. PLC (Programmable Logic Controls)

Nabors proprietary “Commander”Drawworks and “Academy” A/C VFD

Modularized skidded rigs for pad drilling

EFFICIENCY EMPHASIS LEADSTO LAND RIG INNOVATION

Building leading edge rigs, utilizing existing components, yields favorable returns

17

-

50.0

100.0

150.0

200.0

250.0

300.0

$-$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000$9,000NABORS' RIG COUNT AVG MARGIN PER RIG DAY

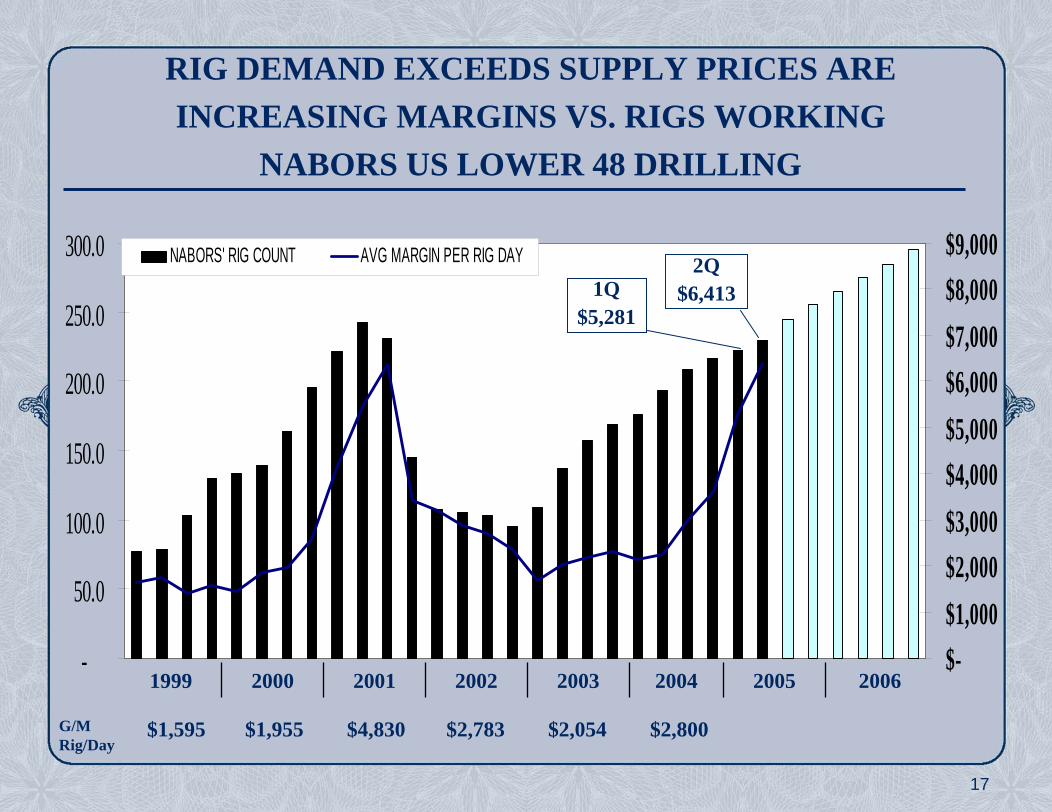

RIG DEMAND EXCEEDS SUPPLY PRICES ARE INCREASING MARGINS VS. RIGS WORKING

NABORS US LOWER 48 DRILLING

1Q$5,281

2Q$6,413

1999 2000 2001 2002 2003 2004 2005 2006

G/M Rig/Day

$1,595 $1,955 $4,830 $2,783 $2,054 $2,800

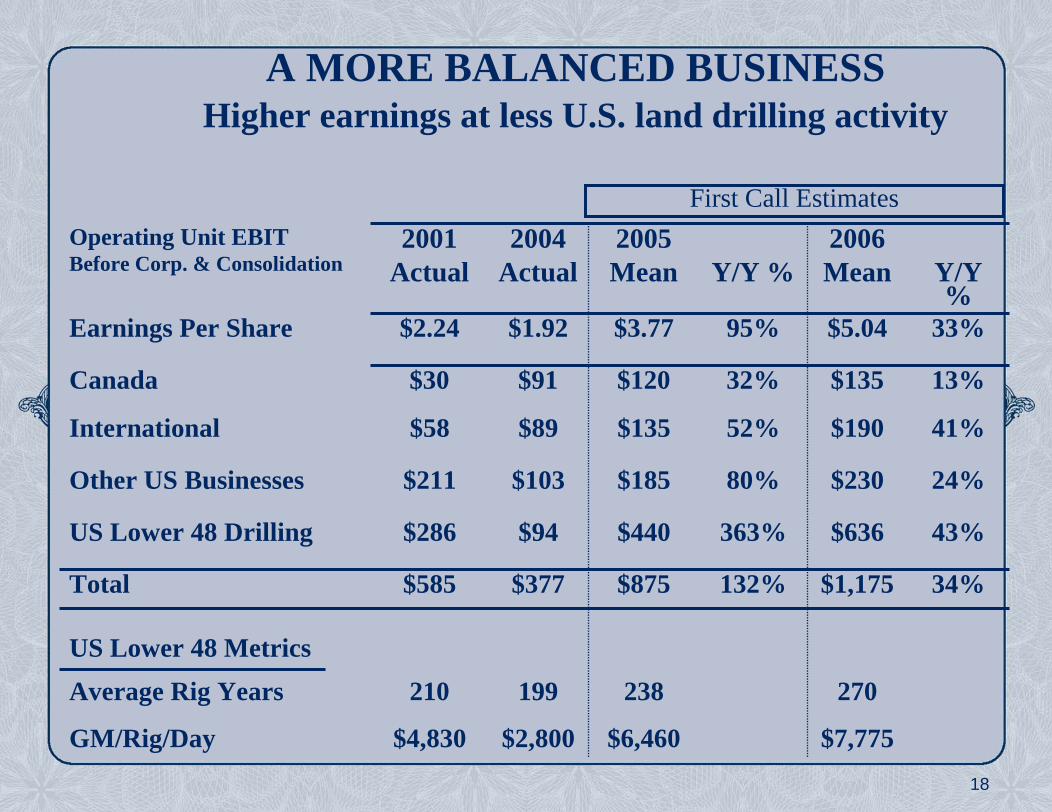

18

Operating Unit EBITBefore Corp. & Consolidation

2001Actual

2004Actual

2005Mean Y/Y %

2006Mean Y/Y

%Earnings Per Share $2.24 $1.92 $3.77 95% $5.04 33%

Canada $30 $91 $120 32% $135 13%

International $58 $89 $135 52% $190 41%

Other US Businesses $211 $103 $185 80% $230 24%

US Lower 48 Drilling $286 $94 $440 363% $636 43%

Total $585 $377 $875 132% $1,175 34%

US Lower 48 MetricsAverage Rig Years 210 199 238 270

GM/Rig/Day $4,830 $2,800 $6,460 $7,775

First Call Estimates

A MORE BALANCED BUSINESSHigher earnings at less U.S. land drilling activity