powerpoint presentation template - venturex resources€¦ · · 2016-09-24smelter/refinery ....

TRANSCRIPT

Ernest Henry copper concentrator, Australia

Investor Day 10 December 2014

08:00 - Welcome and Overview | Ivan Glasenberg

08:20 - Finance Update | Steven Kalmin

08:45 - Copper | Telis Mistakidis

09:15 - Coal | Tor Peterson & Peter Freyberg

09:45 - Break

10:05 - Zinc | Daniel Maté & Chris Eskdale

10:35 - Nickel | Kenny Ives & Peter Johnston

11:05 - Oil | Alex Beard

11:45 - Break

12:00 - Agricultural products | Chris Mahoney

12:30 - Conclusion and Q&A

08:00 - Welcome and Overview | Ivan Glasenberg

08:20 - Finance Update | Steven Kalmin

08:45 - Copper | Telis Mistakidis

09:15 - Coal | Tor Peterson & Peter Freyberg

09:45 - Break

10:05 - Zinc | Daniel Maté & Chris Eskdale

10:35 - Nickel | Kenny Ives & Peter Johnston

11:05 - Oil | Alex Beard

11:40 - Break

12:00 - Agricultural products | Chris Mahoney

12:30 - Conclusion and Q&A

2

Forward looking statements

This document contains statements that are, or may be deemed to be, “forward looking statements” which are prospective in nature. These forward looking statements may be identified

by the use of forward looking terminology, or the negative thereof such as "plans", "expects" or "does not expect", "is expected", "continues", "assumes", "is subject to", "budget",

"scheduled", "estimates", "aims", "forecasts", "risks", "intends", "positioned", "predicts", "anticipates" or "does not anticipate", or "believes", or variations of such words or comparable

terminology and phrases or statements that certain actions, events or results "may", "could", "should", “shall”, "would", "might" or "will" be taken, occur or be achieved. Such statements

are qualified in their entirety by the inherent risks and uncertainties surrounding future expectations. Forward-looking statements are not based on historical facts, but rather on current

predictions, expectations, beliefs, opinions, plans, objectives, goals, intentions and projections about future events, results of operations, prospects, financial condition and discussions

of strategy.

By their nature, forward looking statements involve known and unknown risks and uncertainties, many of which are beyond Glencore’s control. Forward looking statements are not

guarantees of future performance and may and often do differ materially from actual results. Important factors that could cause these uncertainties include, but are not limited to, those

discussed under “Principal risks and uncertainties” of Glencore’s Annual Report 2013 and “Risks and uncertainties” in Glencore’s 2014 Half-Year Report.

Neither Glencore nor any of its associates or directors, officers or advisers, provides any representation, assurance or guarantee that the occurrence of the events expressed or implied

in any forward-looking statements in this document will actually occur. You are cautioned not to place undue reliance on these forward-looking statements which only speak as of the

date of this document. Other than in accordance with its legal or regulatory obligations (including under the UK Listing Rules and the Disclosure and Transparency Rules of the Financial

Conduct Authority and the Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong Limited and the Listing Requirements of the Johannesburg Stock Exchange

Limited), Glencore is not under any obligation and Glencore and its affiliates expressly disclaim any intention, obligation or undertaking to update or revise any forward looking

statements, whether as a result of new information, future events or otherwise. This document shall not, under any circumstances, create any implication that there has been no change

in the business or affairs of Glencore since the date of this document or that the information contained herein is correct as at any time subsequent to its date.

No statement in this document is intended as a profit forecast or a profit estimate and no statement in this document should be interpreted to mean that earnings per Glencore share for

the current or future financial years would necessarily match or exceed the historical published earnings per Glencore share.

This document does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for any securities. The making of this

document does not constitute a recommendation regarding any securities.

Copper Telis Mistakidis

Alumbrera copper concentrator, Argentina

Topics

1. Glencore Copper Department

• Overview

• Description

2. Katanga Mining

• Production issues

• Power

3. Antapaccay

• Tintaya concentrator restart

• Antapaccay mini expansion

4. Copper Market – where is the surplus?

4

Glencore copper in context

• Third largest global mined copper producer and the world’s largest copper supplier

• Integrated assets (mines, smelters and refineries) and marketing

5

2013 copper production (kt)

0

500

1,000

1,500

2,000

2,500

3,000

Competitor 1 Competitor 2 Glencore Competitor 3 Competitor 4 Competitor 5 Glencore 2014Fsupply

Source: Glencore, annual reports.

Glencore copper assets

6

Mined Cu

N America 90k MT

Asia 60k MT

Australia 260k MT Africa 500k MT S America 660k MT

Horne/CCR 300k MT

Isa/Pasar 600k MT Mopani 200k MT Altonorte 300k MT

Kazzinc 70k MT

Smelter/Refinery

Capability across the copper raw materials chain

Mt Isa Cobar Antapaccay Katanga Nkana

Townsville

Altonorte Horne Pasar Mopani Mt Isa

CCR Pasar Mopani

EHM

Marketing

3rd party 3rd party

3rd party

Alumbrera

Collahuasi

Antamina

3rd party

3rd party

3rd party

Lomas Bayas

3rd party

Mopani SXEW

3rd party

Mutanda Mufulira

• Integrated industrial assets and marketing

• One million MT custom smelting and refining

• Capability to process complex concentrates with precious metals and deleterious elements.

Min

ing

S

me

ltin

g

Re

fin

ing

7

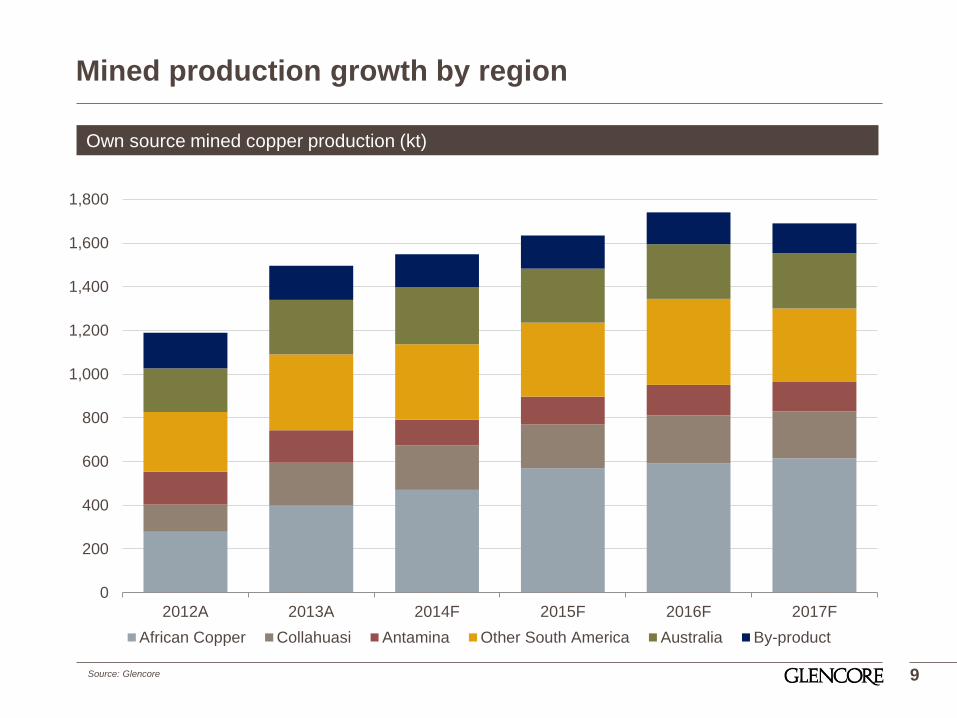

Mined production growth

8

Own source mined copper production (kt)

Note: does not include copper from Kidd, Kazzinc and Ni operations

Merger

2008 2009 2010 2011 2012 2013 2014F 2015F 2016F 2017F 2018F

Total copper Former Xstrata

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2012A 2013A 2014F 2015F 2016F 2017F

African Copper Collahuasi Antamina Other South America Australia By-product

Mined production growth by region

9

Own source mined copper production (kt)

Source: Glencore

210

165F

16

16

2 8

2

120

130

140

150

160

170

180

190

200

210

220

Cu produtionbudget

Power direct Power (indirect)& Mechanical

Electrical Projects delays Reducedsulphide / ASCu

Cu productionactual

Cu

Ca

tho

de (‘000)

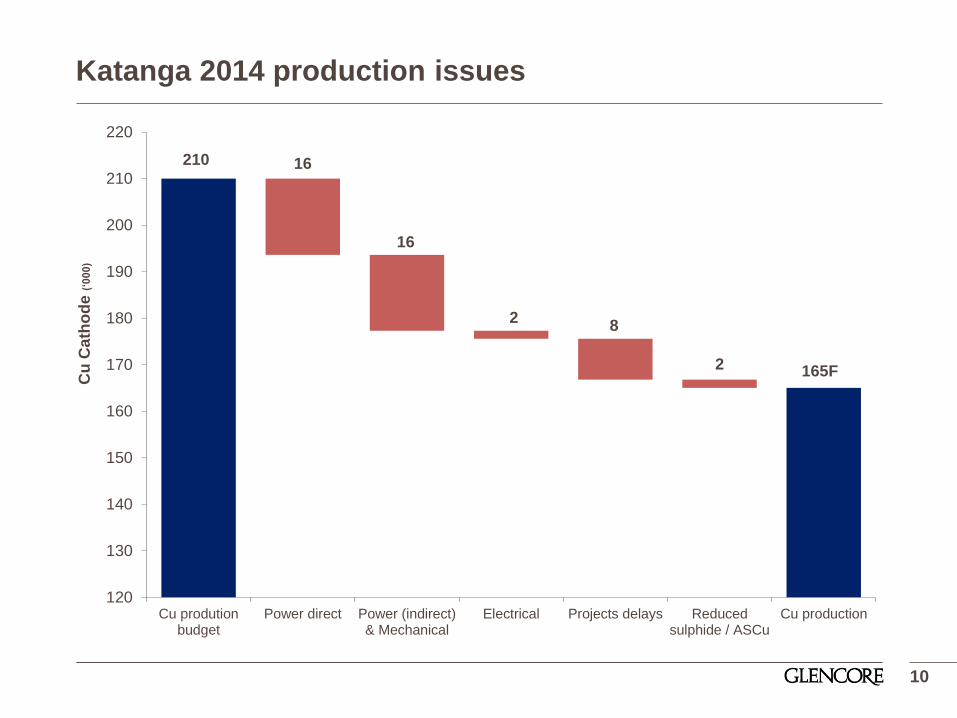

Katanga 2014 production issues

10

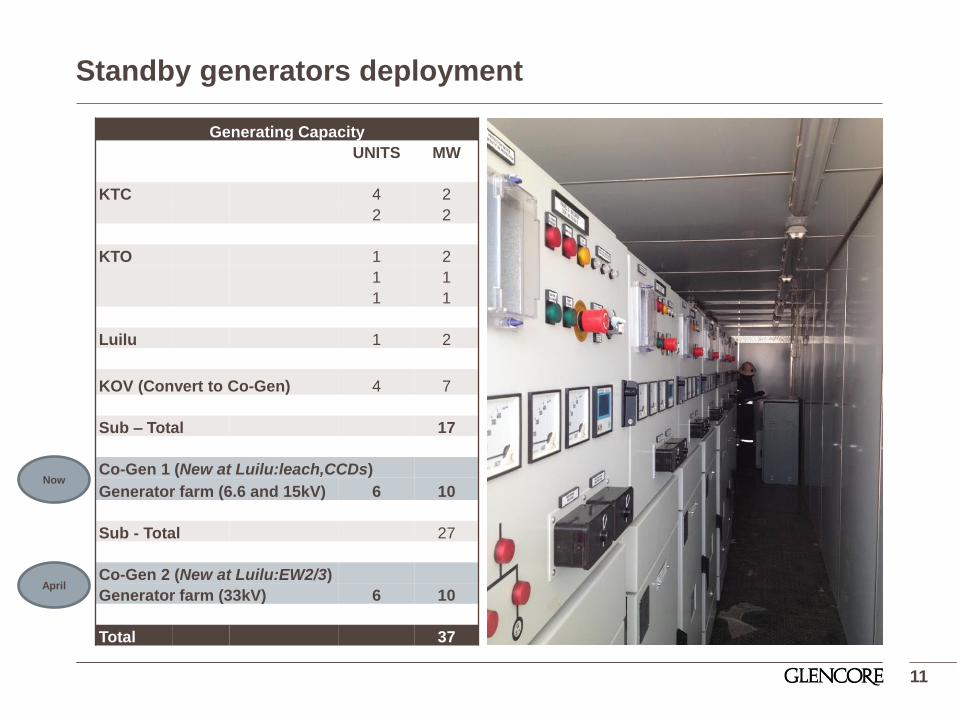

Standby generators deployment

11

Generating Capacity

UNITS MW

KTC 4 2

2 2

KTO 1 2

1 1

1 1

Luilu 1 2

KOV (Convert to Co-Gen) 4 7

Sub – Total 17

Co-Gen 1 (New at Luilu:leach,CCDs)

Generator farm (6.6 and 15kV) 6 10

Sub - Total 27

Co-Gen 2 (New at Luilu:EW2/3)

Generator farm (33kV) 6 10

Total 37

Now

April

Global Power Project – update

12

Description

• 450MW for Kamoto Copper Company and partners

• 350MW of new power and 1000MW transmission

from INGA to Kolwezi

• Project cost – $368M, Lots 1 to 14

• Reimbursed via 40% credit to power bills

• Additional 10% withheld for maintenance fund

• 75MW available to the population

Power milestones

• Transmission from INGA to Kolwezi from 40MW to

250MW Q1 2013

• 25MW (Nzilo) Q4 2014

• 165MW (G-27) Q4 2015

• 165MW (G-28) Q2 2017

Project status

• G27 disassembled and shipped to factory for repair

• 60% of transformers for the converter station have

passed factory acceptance. Remaining 40% to be

tested before year end. Commissioning expected

January 2016

• Synchronous condenser #2 awaiting confirmation

from SNEL, expected December 2014

• Fungurume transformer being commissioned now

Global Power Project – timeline

13

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Lot 3 Unit 3 - Nzilo Quick Fix

Lot 4 Unit G27 Inga refurbishment

Lot 5 Unit G28 Inga refurbishment

Lot 6 Convertor transformer DC Link Pole 1

Lot 7 Convertor transformer DC Link Pole 2

Lot 8 OHL PDI-SCI Reinforcement

Lot 9 Additional Harmonic filters

Lot 10 Additional Synchronous compensator

Lot 11 RO Upgrading HV equipment

Lot 12 Auto-transformer SCK-RO #1 Installation

Lot 13 Auto-transformer SCK-RO #1 Installation

Lot 14 Studies and Final design

Additional power from lots 3, 4 & 5

Additional power available on the grid 25

Cumulative power added 25

2013 2014 2015 2016 2017

25 165

165

190

165

165

355

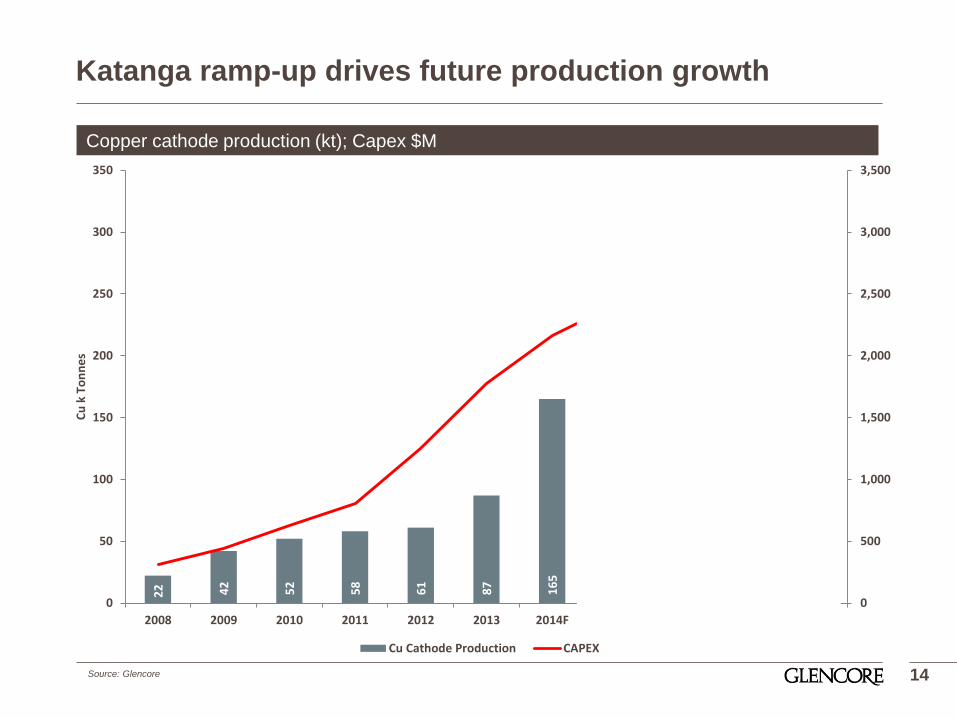

Katanga ramp-up drives future production growth

14

Copper cathode production (kt); Capex $M

Source: Glencore

22

42

52

58

61

87

16

5

24

2

27

4

28

6

30

1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014F 2015F 2016F 2017F 2018F

Cu

k T

on

ne

s

Cu Cathode Production CAPEX

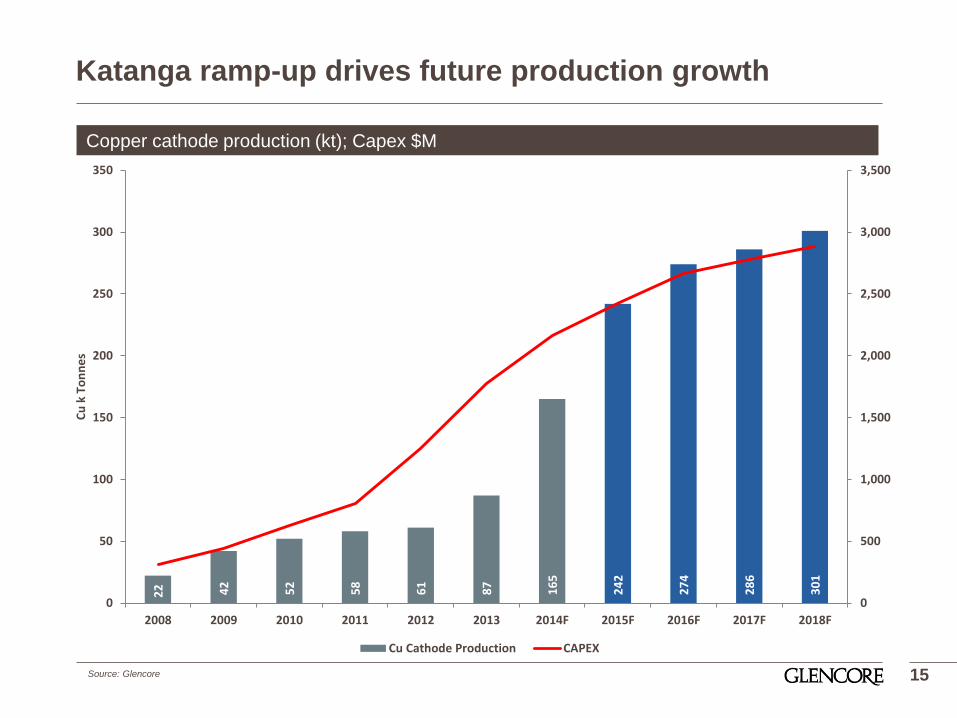

Katanga ramp-up drives future production growth

15

Copper cathode production (kt); Capex $M

Source: Glencore

22

42

52

58

61

87

16

5

24

2

27

4

28

6

30

1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014F 2015F 2016F 2017F 2018F

Cu

k T

on

ne

s

Cu Cathode Production CAPEX

New CM5 SAG Mill installed and commissioned

16

New oxide floatation cells installed and commissioned

17

New concentrate roaster commissioned

18

Solvent Extraction commissioned

19

200ktpa EW2 in production

20

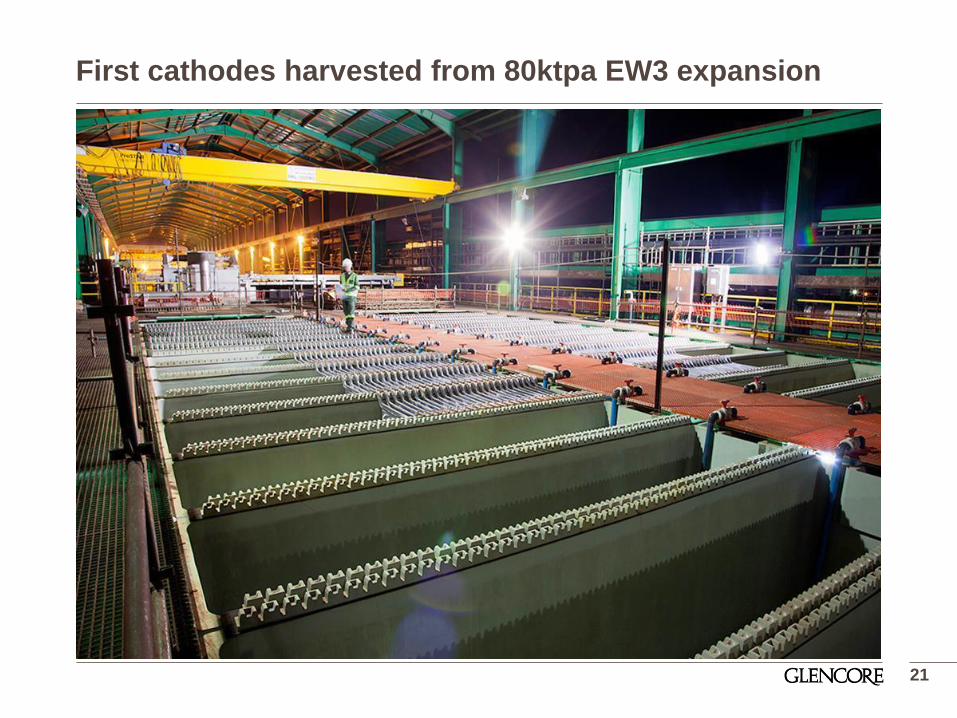

First cathodes harvested from 80ktpa EW3 expansion

21

Antapaccay – Tintaya Concentrator Restart

Tintaya restart

• Existing Tintaya concentrator to process 20 ktpd of ore from Antapaccay mine

• Startup in May 2015

• 34kt per year Cu in concs for LOM avg. 43kt per year Cu in concs for the first 5 years

• Capex of $64M:

• Mining: $25M

• Concentrator: $27M

• Infrastructure & Other: $12M

• Capital Intensity: $1.9M per 1,000t of Cu production

• Project NPV10% of $290M

• Project IRR of 119%

• Government approvals received this month

22

Antapaccay – Incremental Plant Expansion

Expansion of Antapaccay plant:

• Process 82 ktpd of ore from Antapaccay mine using existing infrastructure in 2016

• capacity incrementally increased; 70 ktpd (design) to 77 ktpd (current) and now 82 ktpd

• total Cu in concs >200ktpa (inc Tintaya)

• 9kt per year Cu in concs for LOM avg. 11kt per year Cu in concs for the first 5 years

• Capex of $34M:

• Mining: $7M

• Plant: $27M

• Capital Intensity: $3.8M per 1,000t of Cu production

• Project NPV 10% of $140M

• Project IRR of 117 %

23

42 10

157

209

0

50

100

150

200

250

77 ktpdAntapaccay

20 ktpdTintaya

5 ktpdAntapaccay

Cu C

on

t. in

Con

c. (k

t p

er

yr)

Cu in concentrate

per year

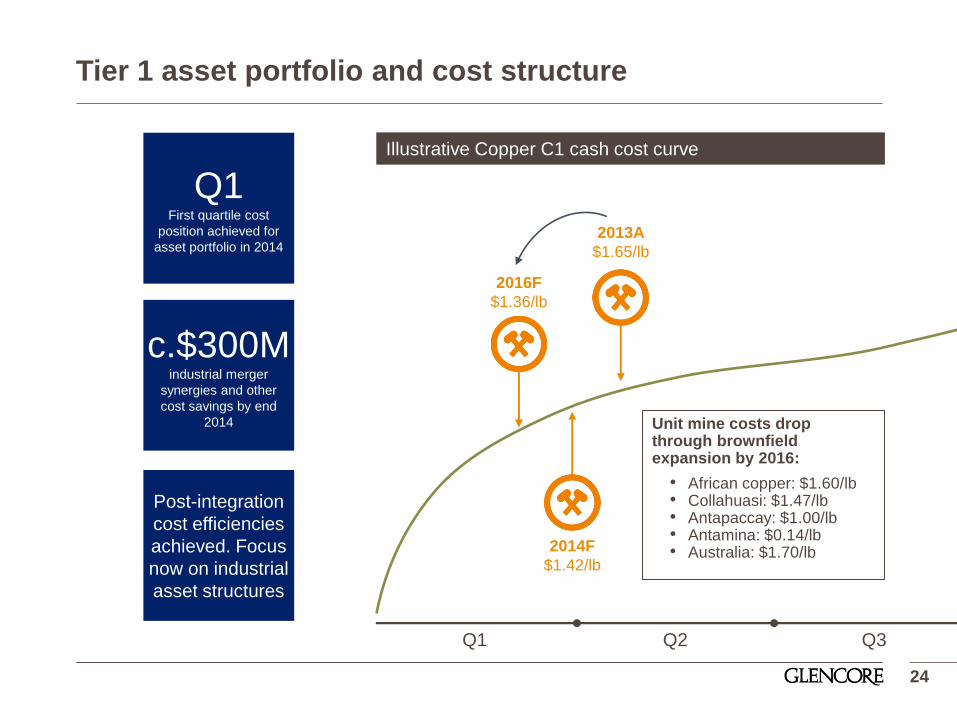

Tier 1 asset portfolio and cost structure

24

Q1 First quartile cost

position achieved for

asset portfolio in 2014

Post-integration

cost efficiencies

achieved. Focus

now on industrial

asset structures

Q1 Q2 Q3 Q4

Illustrative Copper C1 cash cost curve

2013A

$1.65/lb

Unit mine costs drop through brownfield expansion by 2016:

• African copper: $1.60/lb • Collahuasi: $1.47/lb • Antapaccay: $1.00/lb • Antamina: $0.14/lb • Australia: $1.70/lb 2014F

$1.42/lb

2016F

$1.36/lb

c.$300M industrial merger

synergies and other

cost savings by end

2014

Copper market

Altonorte anodes, Antofagasta Port, Chile

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000Jul-0

8

Sep-0

8

No

v-0

8

Jan-0

9

Ma

r-0

9

Ma

y-0

9

Jul-0

9

Sep-0

9

No

v-0

9

Jan-1

0

Ma

r-1

0

Ma

y-1

0

Jul-1

0

Sep-1

0

No

v-1

0

Jan-1

1

Ma

r-1

1

Ma

y-1

1

Jul-1

1

Sep-1

1

No

v-1

1

Jan-1

2

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Sep-1

2

No

v-1

2

Jan-1

3

Ma

r-1

3

Ma

y-1

3

Jul-1

3

Sep-1

3

No

v-1

3

Jan-1

4

Ma

r-1

4

Ma

y-1

4

Jul-1

4

Sep-1

4

LME SHFE COMEX

Global Exchange stocks are at lowest levels since 2008

26 Source: Bloomberg, Reuters

Global copper warehouse stocks are reducing further

27

722k

245k

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jan 2013 Jun 2013 Jan 2014 Jun 2014 Dec 2014

LME COMEX SHFE CHINA BONDED

Global warehouse copper stocks (kt Cu)

Source: Bloomberg, Reuters, Glencore estimates

0

500

1,000

1,500

2,000

2,500

3,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

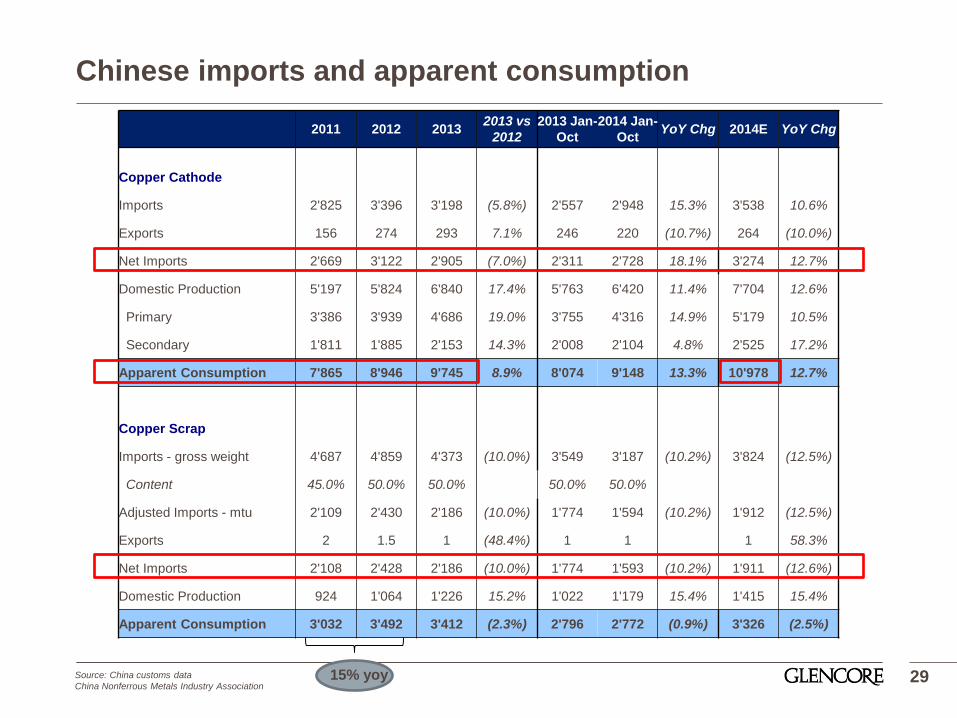

Chinese Copper scrap imports are falling

28

19% yoy

13% yoy

Chinese copper scrap net imports (kt contained Cu)

Source: China customs data

2011 2012 2013 2013 vs

2012

2013 Jan-

Oct

2014 Jan-

Oct YoY Chg 2014E YoY Chg

Copper Cathode

Imports 2'825 3'396 3'198 (5.8%) 2'557 2'948 15.3% 3'538 10.6%

Exports 156 274 293 7.1% 246 220 (10.7%) 264 (10.0%)

Net Imports 2'669 3'122 2'905 (7.0%) 2'311 2'728 18.1% 3'274 12.7%

Domestic Production 5'197 5'824 6'840 17.4% 5'763 6'420 11.4% 7'704 12.6%

Primary 3'386 3'939 4'686 19.0% 3'755 4'316 14.9% 5'179 10.5%

Secondary 1'811 1'885 2'153 14.3% 2'008 2'104 4.8% 2'525 17.2%

Apparent Consumption 7'865 8'946 9'745 8.9% 8'074 9'148 13.3% 10'978 12.7%

Copper Scrap

Imports - gross weight 4'687 4'859 4'373 (10.0%) 3'549 3'187 (10.2%) 3'824 (12.5%)

Content 45.0% 50.0% 50.0% 50.0% 50.0%

Adjusted Imports - mtu 2'109 2'430 2'186 (10.0%) 1'774 1'594 (10.2%) 1'912 (12.5%)

Exports 2 1.5 1 (48.4%) 1 1 1 58.3%

Net Imports 2'108 2'428 2'186 (10.0%) 1'774 1'593 (10.2%) 1'911 (12.6%)

Domestic Production 924 1'064 1'226 15.2% 1'022 1'179 15.4% 1'415 15.4%

Apparent Consumption 3'032 3'492 3'412 (2.3%) 2'796 2'772 (0.9%) 3'326 (2.5%)

Chinese imports and apparent consumption

29 15% yoy Source: China customs data

China Nonferrous Metals Industry Association

Minus:

Kennecott 100k

Escondida 150k

Alumbrera 50k

Surplus

now 90k

MT?

Demand vs Supply per ICSG and Wood Mackenzie

30 Source: ICSG, Wood Mackenzie Global copper short-term outlook, November 2014

Implications of the estimates:

• Implied mine production growth of ~1 million MT between 2014 and 2015

(6% growth)

• Where is the supply coming from?

2014 2015

ICSG Apr ‘14 Estimate

~400 kt

surplus

~600 kt

surplus

ICSG Oct ‘14 Estimate

~300 kt

deficit

(Δ 700 kt lower)

~390 kt

surplus

(Δ 210 kt lower)

WoodMac Nov ‘14

Estimate

180 kt

surplus

202 kt

surplus

Copper Demand/Supply balance estimates

Latest 2015 supply forecasts may still be very optimistic

31 Source: Wood Mackenzie Global copper short-term outlook, November 2014

+320kt?

• Production double counted Frontier at Mopani. 2014 production

is 720 kt;

• Production and commissioning issues. 2015 to be 850 kt

+87kt?

• OT phase 2 not next year as company states only open pit next

year

+72kt? Where does this come from?

+328kt?

• Major projects commissioned in 2014 (DMH, Caserones, Sierra

Gorda)

• Escondida lower by ~150kt

• Codelco lower by ~90kt (cathodes)

• Toromocho operating at 25% capacity

• Las Bambas delayed to 2016

• Constancia commissioning?

+353kt?

• Major projects commissioned in 2014 (Morenci, Eagle, Mt

Milligan, Nunavik)

• Operational incidents (Mt Polley tailings dam failure – mine shut

down, Buenavista- spillage in river and schedule pushed out

into 2016)

• Kennecott lower production (100kt)

+350kt?

• Indonesian concentrates export permits

• Production and labour issues at Grasberg - operating at 80%

+50kt? Alumbrera lower production

+200kt?

• DRC running at 950kt in 2014. To go to just over 1 mt in 2015

~1.8 million MT?

2015 copper supply forecast keeps changing

22,000

22,500

23,000

23,500

24,000

24,500

25,000

2010 Q1 2010 Q3 2011 Q1 2011 Q3 2012 Q1 2012 Q3 2013 Q1 2013 Q4 2014 Q2

32

2015 supply forecast as estimated in each period (kt Cu)

Source: Wood Mackenzie Global copper long-term outlook Q1 2010 to Q3 2014, Glencore estimates

-1.6Mt

• Project deferrals;

• Commissioning delays;

• Revised mine plans.

• Brookhunt and ICSG give 390 kt surplus guidance

• Taking the previous slide, deduct 1.8 Mt = Deficit of 1.4 - 1.6 Mt for 2015?

• Consumption - the world is emerging from the biggest recession in 100 years

Make your

own mind up?

Thank you

33

Appendix: Copper asset update

Kantanga Phase V, EW3 under commissioning, DRC

Katanga expansion nearing completion

New KOV pit crusher completed

36

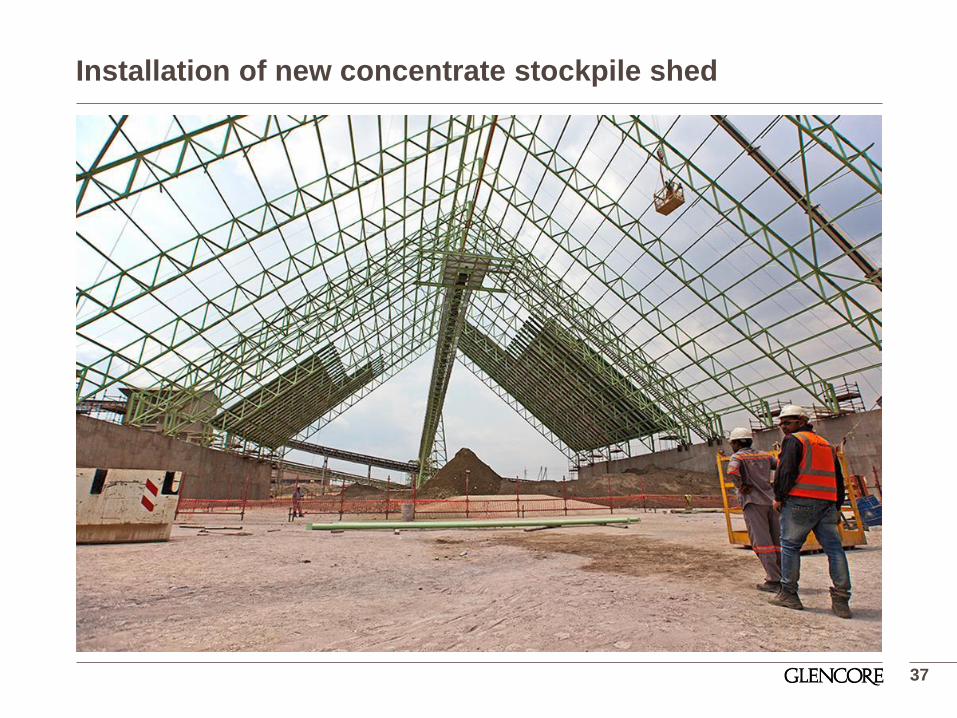

Installation of new concentrate stockpile shed

37

Heap leach extension complete

38

39

DRC power project

Refurbishment of Inga Unit G27, DRC

Mopani – synclinorium and deeps project update

New acid plant, Mufilira smelter, Zambia

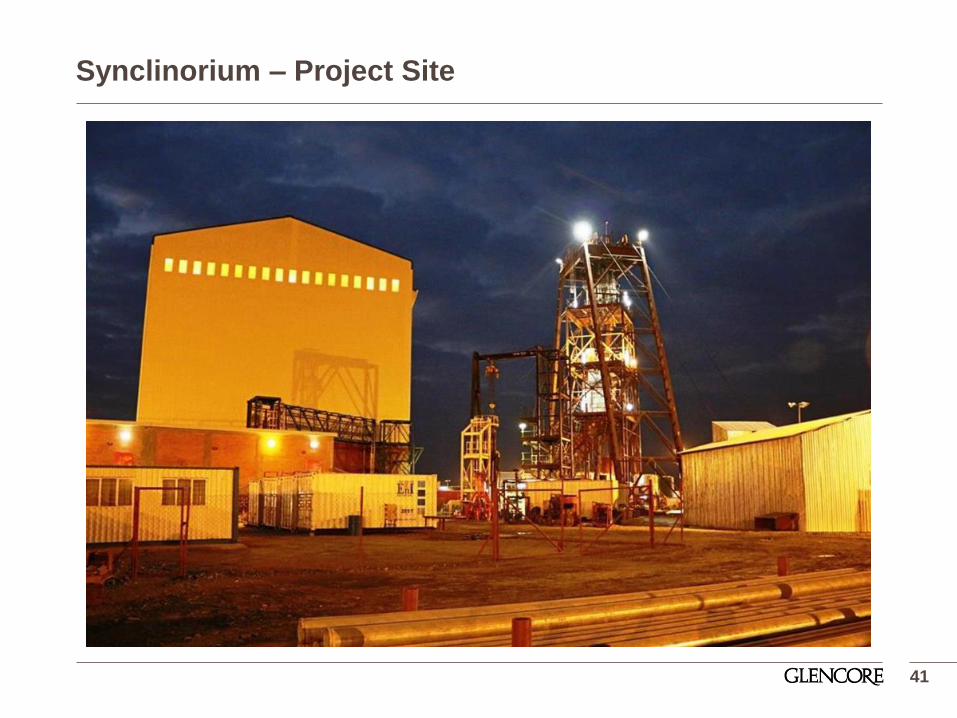

Synclinorium – Project Site

41

Synclinorium – New Winder Main Shaft

42

Synclinorium – New Winder

43

Synclinorium – New Winder House

44

Synclinorium – Sub Station

45

Synclinorium – New Generator Building

46

Synclinorium – Loading Station – 1231m level

47

Synclinorium – Loading Station – 1231m Level

48

Synclinorium – Ventilation Shaft

49

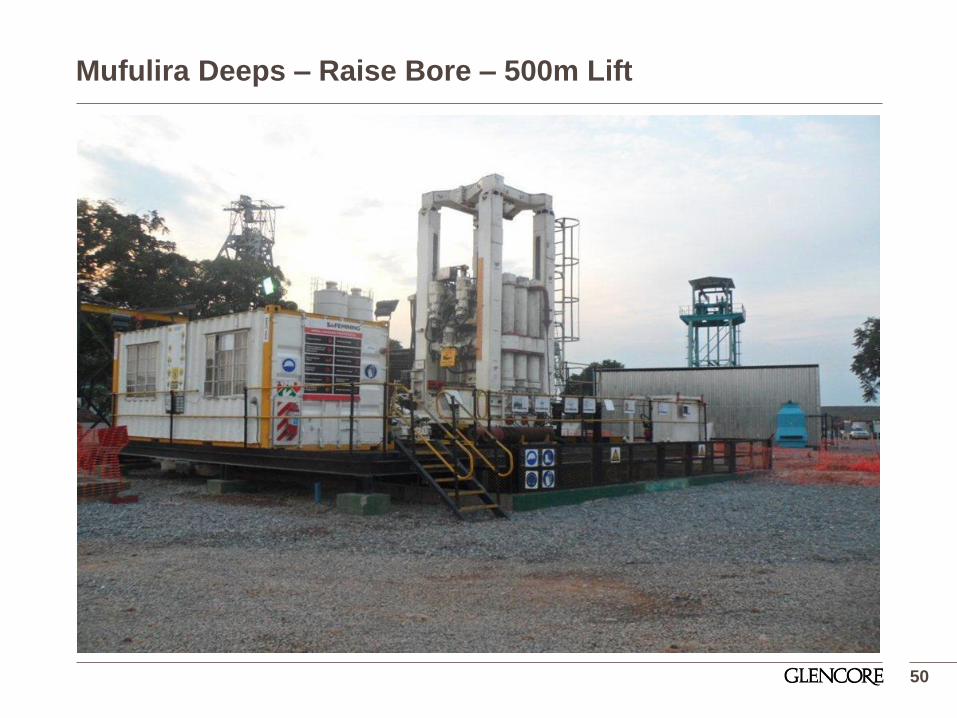

Mufulira Deeps – Raise Bore – 500m Lift

50

Mindola Deeps – 4960L

51