prepare and process financial/business documentsnotes_+2012v2.pdfa receipt a cash register docket a...

TRANSCRIPT

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 1 of 16

Prepare and process banking documents

One of the key elements to success in business is to manage the money – both incoming and outgoing. All businesses operate a business cheque account and rarely pay for goods or services with cash – the exception is when purchasing low cost items (eg tea and coffee for the staff, courier fees and stationery items) payment for which comes from the Petty Cash fund. Larger amounts for payment of trade goods and expenses incurred in the day to day operation of the organisation will be paid with cheques, BPAY, internet banking, EFTPOS and/or Debit/Credit Cards.

Sales and services result in collection of monies commonly in the form of:

Cash (notes and coin) Cheques

Debit/Credit card payments (Visa, MasterCard) Internet banking

EFTPOS (Electronic funds transfer at point of sale)

Cash, Cheques, manual Debit/Credit card vouchers, and money orders are taken to the bank and deposited. These items are usually banked daily. Daily banking minimises the risk of theft and fraud.

Internet banking and electronic funds transfer using Debit/Credit cards or savings/cheque account cards will be processed directly by the bank and are therefore not recorded in the bank deposit book.

Organisations will have policies and procedures (written or practiced) for receiving and receipting money, balancing cash register drawers and forwarding funds for banking.

An organisation must comply with its bank‟s policies and procedures, which are agreed to when an organisation‟s account is established.

Important features of business cash control are:

An individual should be responsible for its security at all times. If responsibility moves from one person to another, the cash should be counted, verified correct, and signed for.

Bank daily the cash received on that day (or the previous day, depending on the type of business and its proximity to the bank). Businesses operating over the weekend and on public holidays should make separate deposits for each day‟s trading when the bank reopens.

Bank intact: that is, the whole of the cash received should be banked without any payments or expenses being taken out of it. This leaves a clear audit trail that proves the honesty of those handling the cash.

Regardless of whether an organisation is large or small, a complete record must be made of all monies received. Each transaction must be acknowledged by at least one of the following:

a receipt a cash register docket a credit card sales voucher

A receipt may be prepared electronically by a computer program such as MYOB or Quicken, a cash register or manually by using a carbonised receipt book.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 2 of 16

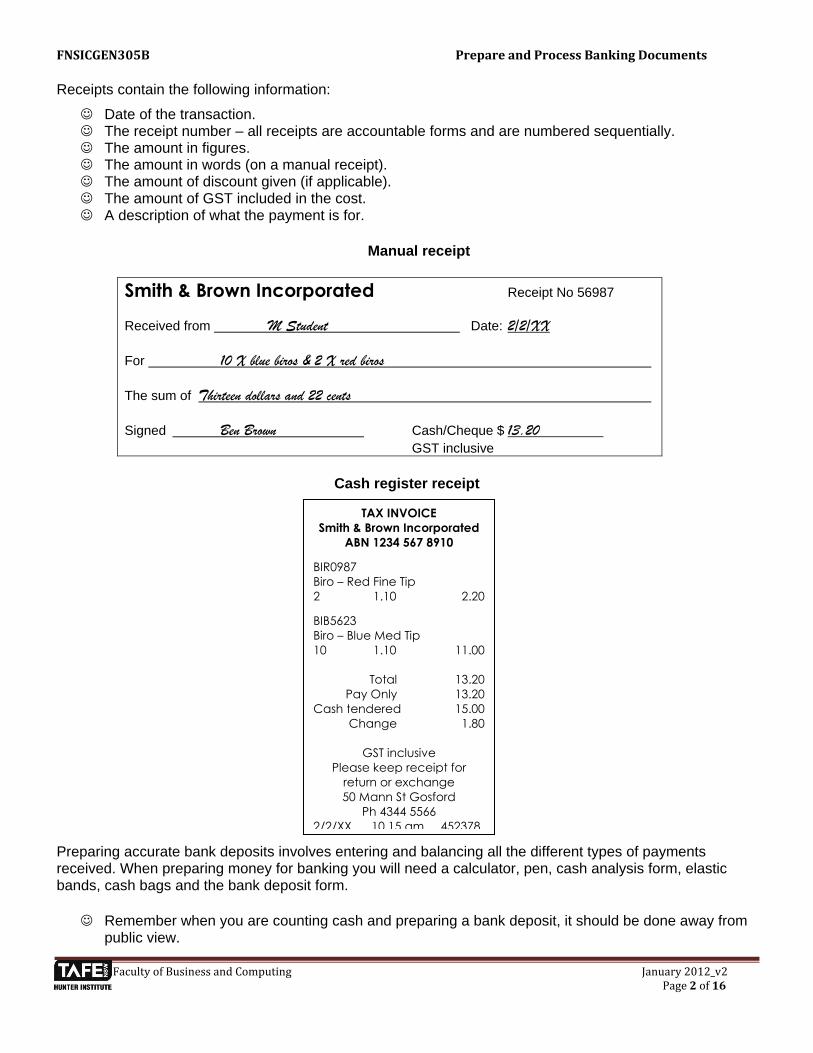

Receipts contain the following information:

Date of the transaction. The receipt number – all receipts are accountable forms and are numbered sequentially. The amount in figures. The amount in words (on a manual receipt). The amount of discount given (if applicable). The amount of GST included in the cost. A description of what the payment is for.

Manual receipt

Smith & Brown Incorporated Receipt No 56987

Received from M Student Date: 2/2/XX

For 10 X blue biros & 2 X red biros

The sum of Thirteen dollars and 22 cents

Signed Ben Brown Cash/Cheque $ 13.20

GST inclusive

Cash register receipt

Preparing accurate bank deposits involves entering and balancing all the different types of payments received. When preparing money for banking you will need a calculator, pen, cash analysis form, elastic bands, cash bags and the bank deposit form.

Remember when you are counting cash and preparing a bank deposit, it should be done away from public view.

TAX INVOICE

Smith & Brown Incorporated

ABN 1234 567 8910

BIR0987

Biro – Red Fine Tip

2 1.10 2.20

BIB5623

Biro – Blue Med Tip

10 1.10 11.00

Total 13.20

Pay Only 13.20

Cash tendered 15.00

Change 1.80

GST inclusive

Please keep receipt for

return or exchange

50 Mann St Gosford

Ph 4344 5566

2/2/XX 10.15 am 452378

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 3 of 16

Preparation of money for banking

Cash

As you are no doubt aware, cash consists of notes and coins.

Australian notes are made of polymer in denominations of

$100 $50 $20 $10 $5

When preparing the cash for banking the notes are batched. The process for this is:

Sort notes into the same denomination with the transparent window in the bottom right-hand corner Bundle each denomination into groups of ten and secure the flat with an elastic band. Each flat is then grouped into batches of ten flats known as a bundle and secured with two elastic

bands

Australian coins are sorted into the following denominations

$2 $1 50c 20c 10c 5c

The value of damaged notes is as follows:

If two-thirds of a note is present, it can be counted at full value. Half a banknote has half the face value. Less than half a note has no value at all.

Coin is batched into plastic bags in the quantity marked on the bag. These values are as follows:

A bag of $2.00 coins = $50.00

A bag of $1.00 coins = $20.00

A bag of 50c, 20c, or 10c coins = $10.00

A bag of 5c coins = $2.00

If there are insufficient coins for a bag, write the value of each denomination on a piece of paper marked with a red cross and put it in a separate bag. This indicates to the bank teller that it is not a complete bag.

Another method of batching coin is to use brown paper and roll the coins. There is quite a skill involved in this method and most people opt for the recyclable plastic bag method.

Use a cash analysis slip to help count the cash, then enter the information on the cash summary of the bank deposit.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 4 of 16

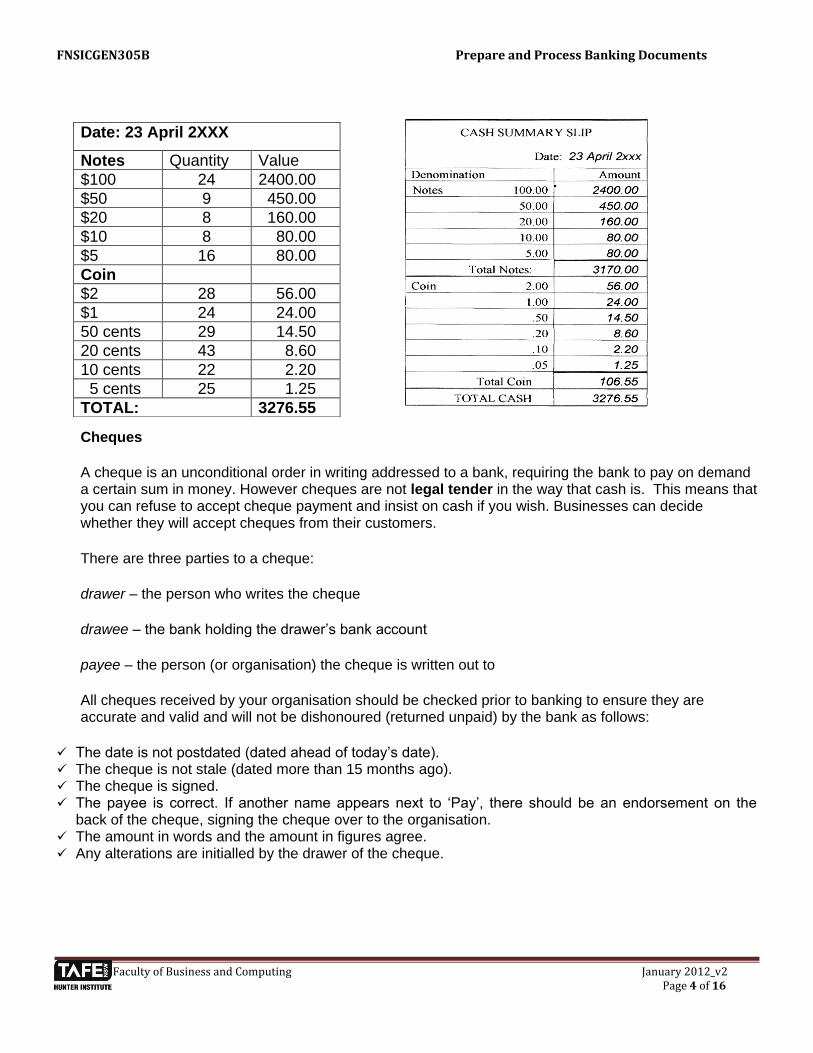

Cheques

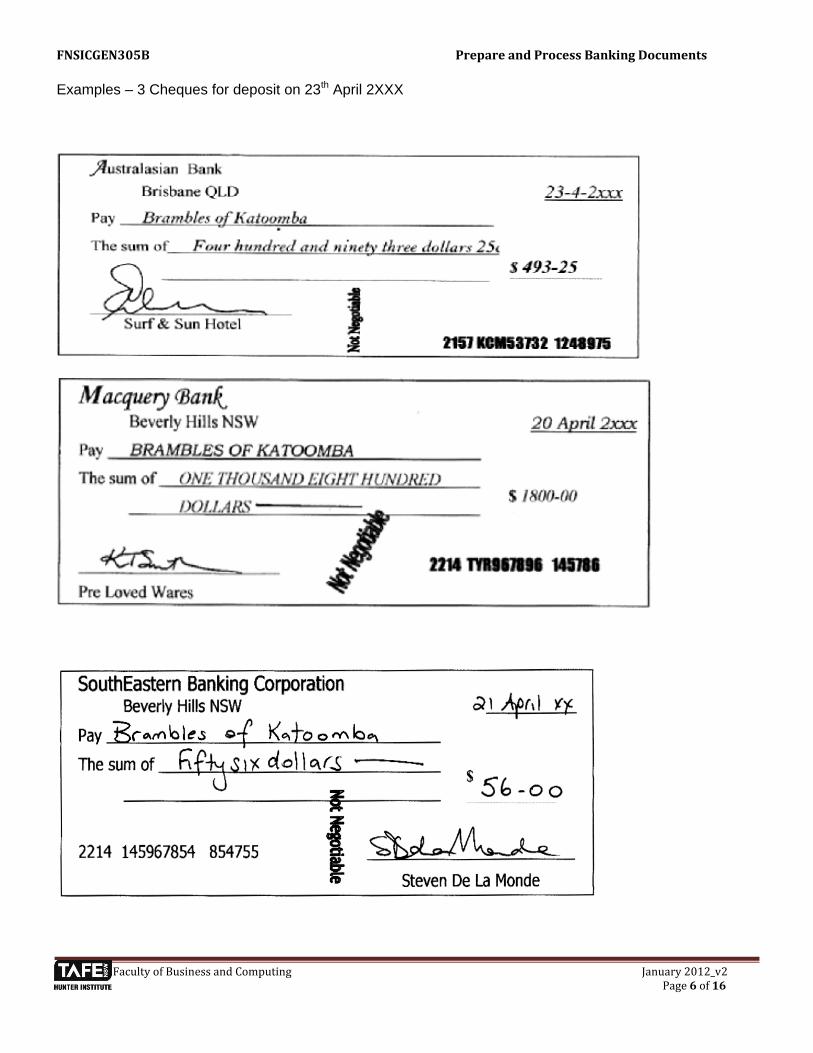

A cheque is an unconditional order in writing addressed to a bank, requiring the bank to pay on demand a certain sum in money. However cheques are not legal tender in the way that cash is. This means that you can refuse to accept cheque payment and insist on cash if you wish. Businesses can decide whether they will accept cheques from their customers.

There are three parties to a cheque:

drawer – the person who writes the cheque

drawee – the bank holding the drawer‟s bank account

payee – the person (or organisation) the cheque is written out to

All cheques received by your organisation should be checked prior to banking to ensure they are accurate and valid and will not be dishonoured (returned unpaid) by the bank as follows:

The date is not postdated (dated ahead of today‟s date). The cheque is not stale (dated more than 15 months ago). The cheque is signed. The payee is correct. If another name appears next to „Pay‟, there should be an endorsement on the

back of the cheque, signing the cheque over to the organisation. The amount in words and the amount in figures agree. Any alterations are initialled by the drawer of the cheque.

Date: 23 April 2XXX

Notes Quantity Value

$100 24 2400.00

$50 9 450.00

$20 8 160.00

$10 8 80.00

$5 16 80.00

Coin

$2 28 56.00

$1 24 24.00

50 cents 29 14.50

20 cents 43 8.60

10 cents 22 2.20

5 cents 25 1.25

TOTAL: 3276.55

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 5 of 16

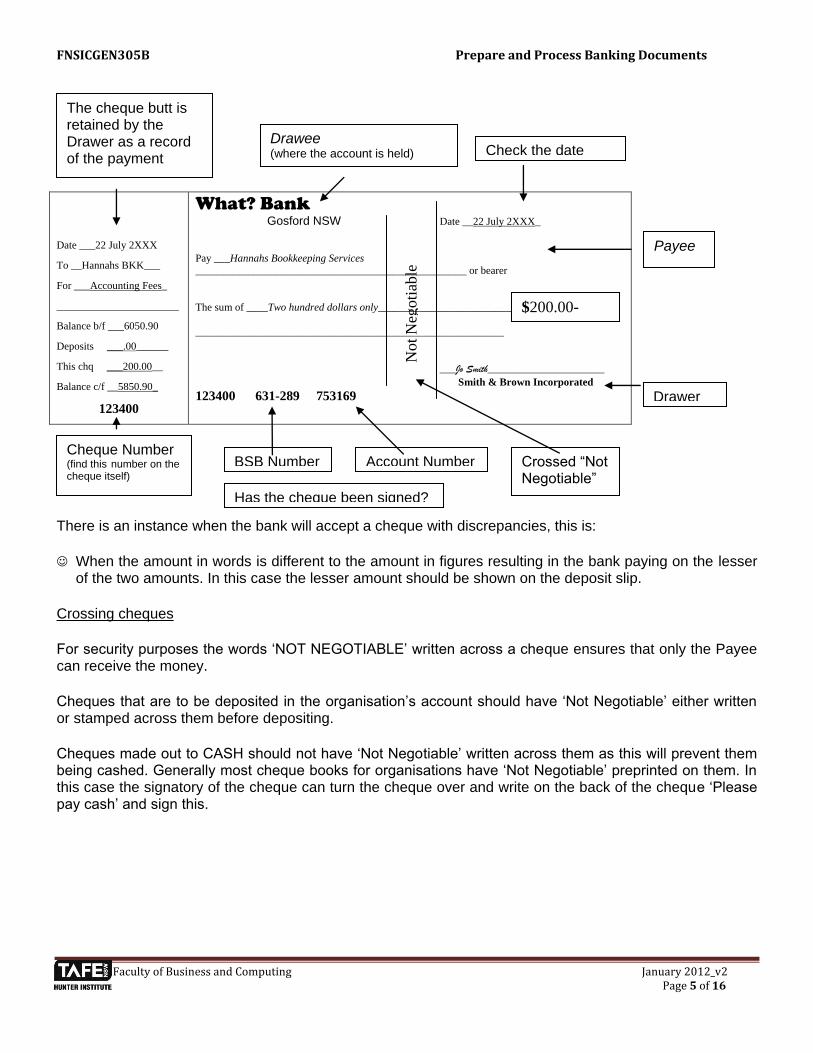

Date ___22 July 2XXX

To __Hannahs BKK___

For ___Accounting Fees_

_______________________

Balance b/f ___6050.90

Deposits ___.00______

This chq ___200.00__

Balance c/f __5850.90_

123400

What? Bank Gosford NSW Date __22 July 2XXX_

Pay ___Hannahs Bookkeeping Services

___________________________________________________ or bearer

The sum of ____Two hundred dollars only__________________________

__________________________________________________________

___Jo Smith______________________

Smith & Brown Incorporated

123400 631-289 753169

There is an instance when the bank will accept a cheque with discrepancies, this is:

When the amount in words is different to the amount in figures resulting in the bank paying on the lesser of the two amounts. In this case the lesser amount should be shown on the deposit slip.

Crossing cheques

For security purposes the words „NOT NEGOTIABLE‟ written across a cheque ensures that only the Payee can receive the money.

Cheques that are to be deposited in the organisation‟s account should have „Not Negotiable‟ either written or stamped across them before depositing.

Cheques made out to CASH should not have „Not Negotiable‟ written across them as this will prevent them being cashed. Generally most cheque books for organisations have „Not Negotiable‟ preprinted on them. In this case the signatory of the cheque can turn the cheque over and write on the back of the cheque „Please pay cash‟ and sign this.

$200.00-

22__200.00_

______

The cheque butt is retained by the Drawer as a record of the payment

Drawee (where the account is held) Check the date

Payee

Drawer

Cheque Number (find this number on the cheque itself)

BSB Number Account Number Crossed “Not Negotiable”

Has the cheque been signed?

Not

Neg

oti

able

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 6 of 16

Examples – 3 Cheques for deposit on 23th April 2XXX

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 7 of 16

Money orders

This is a no hassle alternative to using cheques and bank cheques and usually more affordable than a bank cheque. They are a convenient and safe way to pay your bills, transfer money or send amounts overseas.

Money orders are banked in exactly the same way cheques are banked.

Once the cheques and money orders have been validated (checked for errors) they are written up in the deposit book.

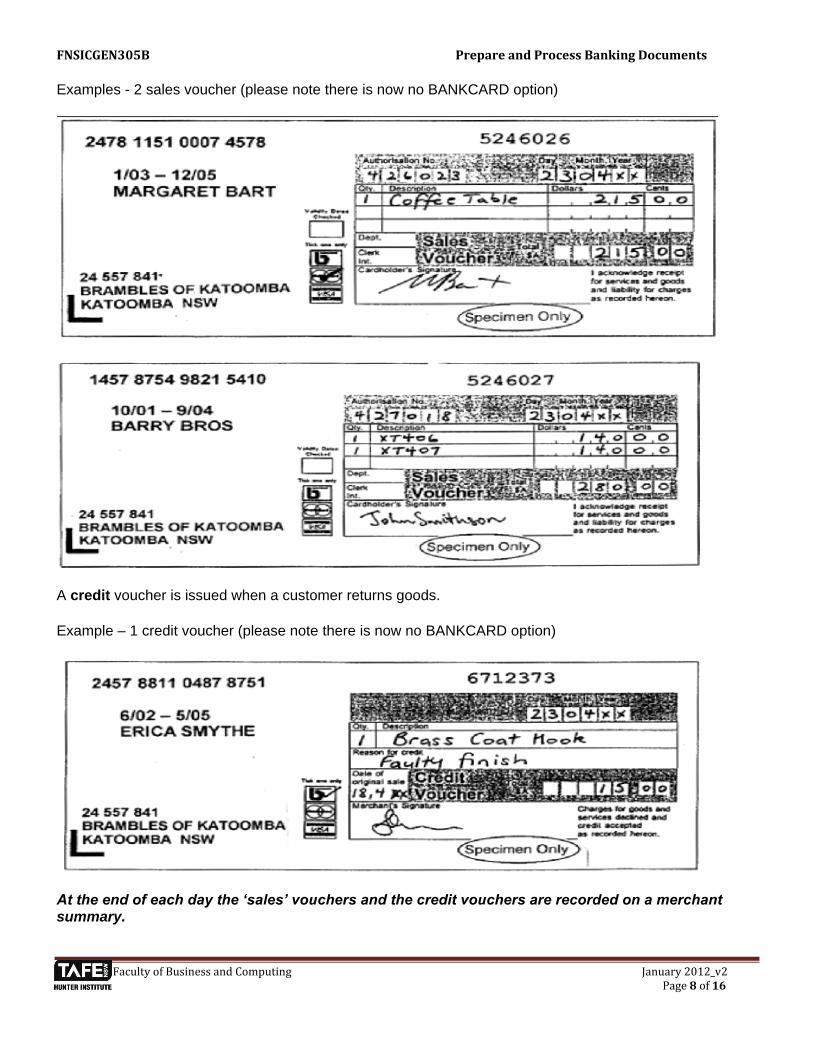

Credit card transactions

Credit card sales can be made in two ways:

1. Manually using a hand held machine or 2. Electronically, using EFTPOS (electronic funds transfer at point of sale)

Manual credit card transactions

Some businesses do not have on-line facilities so manual credit card transactions are made. These transactions are also made manually in cases where the on-line network is not operating.

A portable machine is used to swipe the card across a voucher so an imprint of the credit card details is made. Details of the sale are hand-written on the voucher and the buyer signs in the signature block.

There are two carbon copies - one for the cardholder (buyer), one for the merchant (seller). The original goes to the bank with a summary of all credit card sales for the day.

When accepting payment by credit card using the manual method, you should ensure that the transaction is valid by:

Comparing the customer‟s signature on the voucher with the signature on the card Checking the expiry date on the card – is it current? Telephone the merchant authorisation centre for approval if the amount is above the authorised credit

card limit for your organisation. Check the card number against the latest list of stolen and invalid cards issued through the banks.

If you suspect that the card is stolen or being used illegally, you should follow company policy in dealing with the situation.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 8 of 16

Examples - 2 sales voucher (please note there is now no BANKCARD option)

A credit voucher is issued when a customer returns goods.

Example – 1 credit voucher (please note there is now no BANKCARD option)

At the end of each day the ‘sales’ vouchers and the credit vouchers are recorded on a merchant summary.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 9 of 16

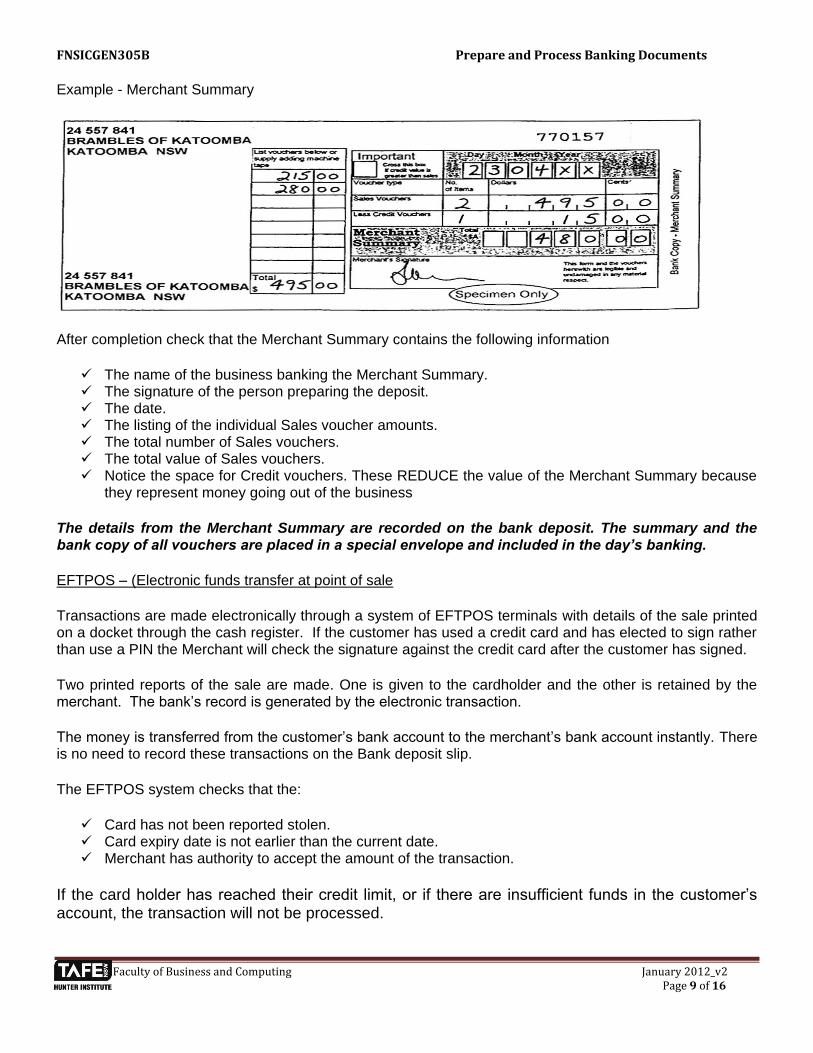

Example - Merchant Summary

After completion check that the Merchant Summary contains the following information

The name of the business banking the Merchant Summary. The signature of the person preparing the deposit. The date. The listing of the individual Sales voucher amounts. The total number of Sales vouchers. The total value of Sales vouchers. Notice the space for Credit vouchers. These REDUCE the value of the Merchant Summary because

they represent money going out of the business

The details from the Merchant Summary are recorded on the bank deposit. The summary and the bank copy of all vouchers are placed in a special envelope and included in the day’s banking.

EFTPOS – (Electronic funds transfer at point of sale

Transactions are made electronically through a system of EFTPOS terminals with details of the sale printed on a docket through the cash register. If the customer has used a credit card and has elected to sign rather than use a PIN the Merchant will check the signature against the credit card after the customer has signed.

Two printed reports of the sale are made. One is given to the cardholder and the other is retained by the merchant. The bank‟s record is generated by the electronic transaction.

The money is transferred from the customer‟s bank account to the merchant‟s bank account instantly. There is no need to record these transactions on the Bank deposit slip.

The EFTPOS system checks that the:

Card has not been reported stolen. Card expiry date is not earlier than the current date. Merchant has authority to accept the amount of the transaction.

If the card holder has reached their credit limit, or if there are insufficient funds in the customer‟s account, the transaction will not be processed.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 10 of 16

Benefits of EFTPOS for an organisation

Reduces the amount of cash taken (and therefore the amount of cash to be banked). Reduces paperwork and office time. Lowers the risk of theft or fraud. Reduces losses from dishonoured cheques. Reduces cash holdings. Is easier and safer than paper-based credit card processing. Increases the likelihood of a sale (impulse spending).

Benefits for a customer

Provides a safe, fast alternative to carrying cash. Reduces the number of transactions required to obtain cash.

Is convenient and easy to use.

Electronic banking

Many organisations now pay accounts using electronic banking facilities. Organisations submit data containing payment instructions on diskette, nine-track magnetic tape or by secure modem transfer to their bank. The bank processes the data. Files are then presented to other financial institutions (usually during the night) and cleared funds are available in the recipient‟s account the next day. This is a fast, efficient and inexpensive way for a computerised organisation to pay accounts. For the person or organisation receiving the money, payments received electronically have similar benefits to those listed above for EFTPOS. Transactions received electronically are identified on the monthly statement received from the bank. Codes for the various types of deposits are indicated on the statement. Many banks have a system of telephone banking for their customers, allowing them to pay accounts and transfer funds from one account to another by telephone. Some banks now have Internet services. These services allow people to transfer funds between accounts, pay regular accounts to certain institutions, review transactions and order statements from their home computer.

Night safe

Banks provide a night safe service for use by customers. Deposits are prepared in the normal way and placed in the safe outside the bank building. Most banks close at 4.00 pm Monday to Friday. By using the night safe an organisation can prepare the bank deposit at the close of training. This practice removes all funds from the premises overnight, reducing possible loss in the event of robbery or some other disaster. Bank staff will process the deposit on the next working day.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 11 of 16

Cash, cheques and credit cards are listed in banking forms in accordance with the banking institution’s guidelines

All banks produce their own deposit forms or slips. These are often encoded (printed) with the customer‟s name and account number, as well as the Bank and Branch and BSB (Bank, State, Branch) number. The size of the book is determined by the number of cheques the business is likely to deposit within a reasonable time period. Most business deposit books are designed so that a duplicate (carbon) copy of the deposit is left in the book. Smaller businesses will have a deposit book with a butt (similar to a cheque book) which is the organisation‟s record of the deposit.

While each bank‟s deposit slip looks slightly different, each requires the following information:

Name of the bank, the branch and the BSB number. Name of the depositor/account holder and the account number. Date of deposit. Total of coin/notes/cash. Total of credit card transactions/Merchant summary. A listing of the cheques showing drawer, bank and branch of each cheque. Total number of cheques. Total value of the deposit (cash, credit and cheque transactions). Signature of the person depositing/preparing the deposit slip. Space for the teller‟s signature, the number of cheques and other information for bank use only.

Deposit for account at

What? Bank Where this deposit is lodge at a bank or branch other than

shown below it will be transferred under internal procedures

of the Bank. The Bank will not be liable for delays in

transmission to branch or transfer to Nominated Bank.

Proceeds of cheques will not be available until cleared.

100 CREDIT 50 Date / / 20 Cash 10 Cheques 5 MC/Visa

Branch (where

Account kept) Total Notes Less charges

Paid in by

Signature Coin Total Deposit

Credit

A/c Number Total Cash Comm

Account

Name Total No of

Cheques Teller:

Particulars of cheques etc to be completed by the depositor

Drawer Bank Branch Amount

Total Cheques

This information is required

Itemise the cash being deposited

The totals being deposited

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 12 of 16

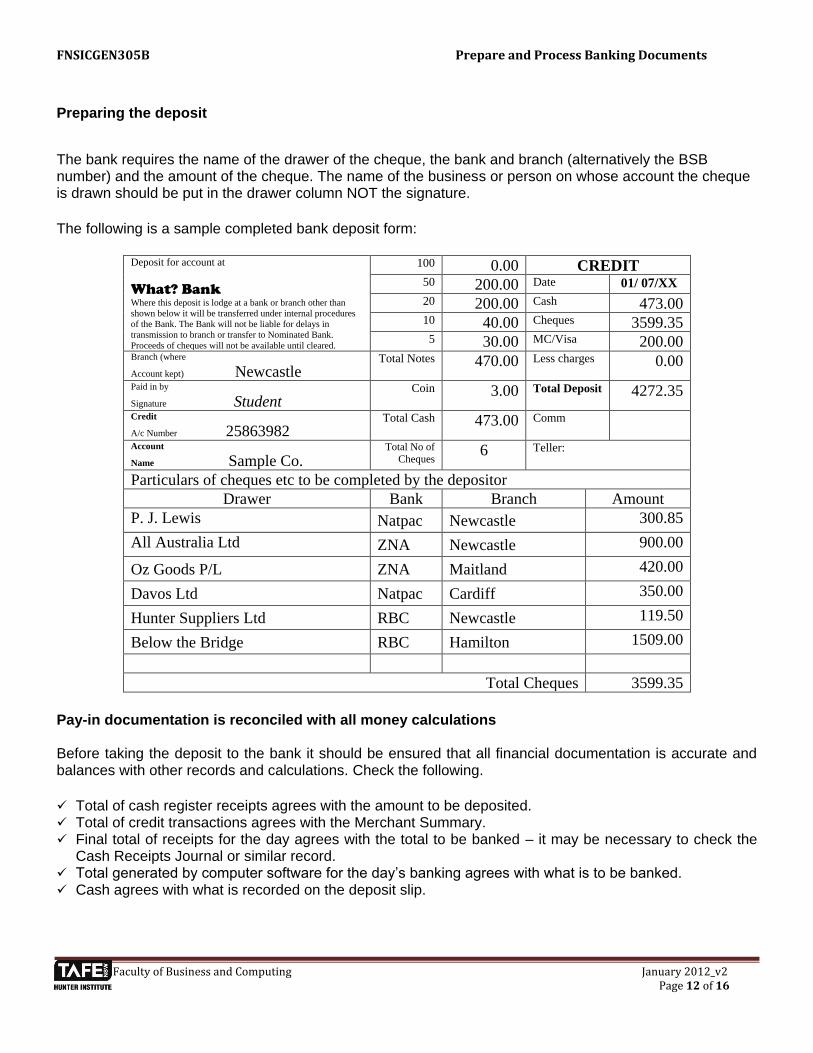

Preparing the deposit

The bank requires the name of the drawer of the cheque, the bank and branch (alternatively the BSB number) and the amount of the cheque. The name of the business or person on whose account the cheque is drawn should be put in the drawer column NOT the signature.

The following is a sample completed bank deposit form:

Deposit for account at

What? Bank Where this deposit is lodge at a bank or branch other than

shown below it will be transferred under internal procedures

of the Bank. The Bank will not be liable for delays in

transmission to branch or transfer to Nominated Bank.

Proceeds of cheques will not be available until cleared.

100 0.00 CREDIT 50 200.00 Date 01/ 07/XX

20 200.00 Cash 473.00 10 40.00 Cheques 3599.35 5 30.00 MC/Visa 200.00

Branch (where

Account kept) Newcastle

Total Notes 470.00 Less charges 0.00

Paid in by

Signature Student Coin 3.00 Total Deposit 4272.35

Credit

A/c Number 25863982

Total Cash 473.00 Comm

Account

Name Sample Co.

Total No of

Cheques 6 Teller:

Particulars of cheques etc to be completed by the depositor

Drawer Bank Branch Amount

P. J. Lewis Natpac Newcastle 300.85

All Australia Ltd ZNA Newcastle 900.00

Oz Goods P/L ZNA Maitland 420.00

Davos Ltd Natpac Cardiff 350.00

Hunter Suppliers Ltd RBC Newcastle 119.50

Below the Bridge RBC Hamilton 1509.00

Total Cheques 3599.35

Pay-in documentation is reconciled with all money calculations Before taking the deposit to the bank it should be ensured that all financial documentation is accurate and balances with other records and calculations. Check the following.

Total of cash register receipts agrees with the amount to be deposited. Total of credit transactions agrees with the Merchant Summary. Final total of receipts for the day agrees with the total to be banked – it may be necessary to check the

Cash Receipts Journal or similar record. Total generated by computer software for the day‟s banking agrees with what is to be banked. Cash agrees with what is recorded on the deposit slip.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 13 of 16

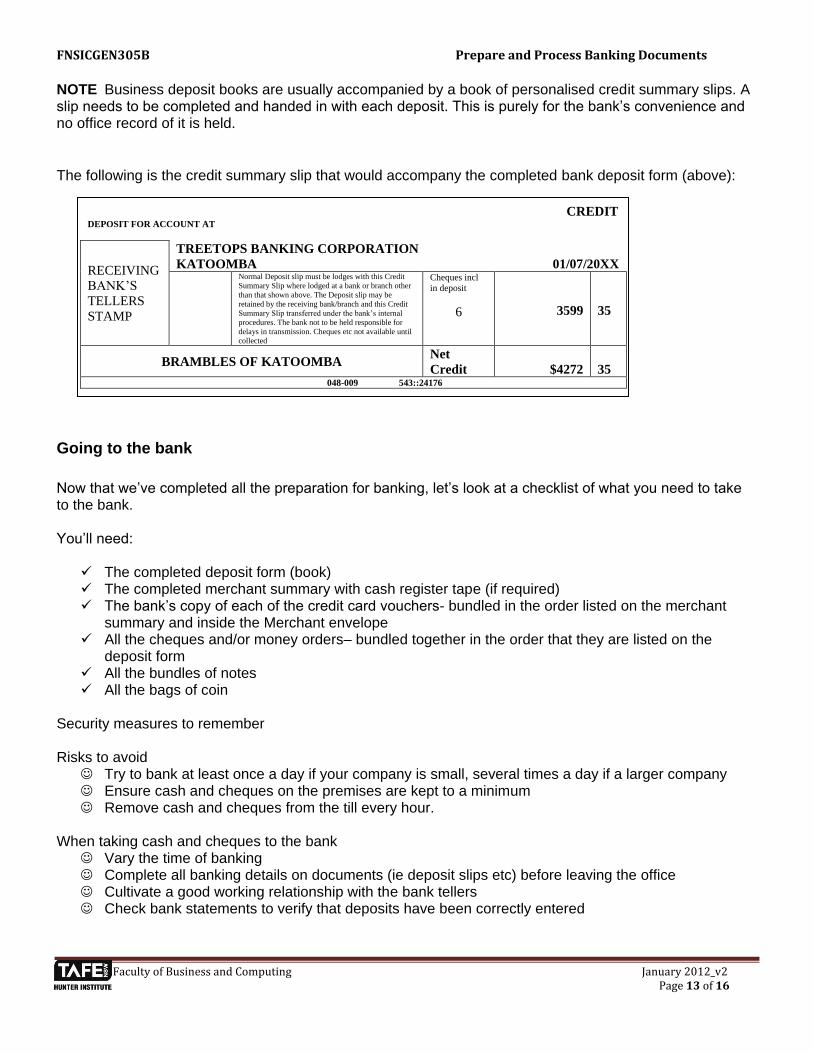

NOTE Business deposit books are usually accompanied by a book of personalised credit summary slips. A slip needs to be completed and handed in with each deposit. This is purely for the bank‟s convenience and no office record of it is held.

The following is the credit summary slip that would accompany the completed bank deposit form (above):

Going to the bank

Now that we‟ve completed all the preparation for banking, let‟s look at a checklist of what you need to take to the bank. You‟ll need: The completed deposit form (book) The completed merchant summary with cash register tape (if required) The bank‟s copy of each of the credit card vouchers- bundled in the order listed on the merchant

summary and inside the Merchant envelope All the cheques and/or money orders– bundled together in the order that they are listed on the

deposit form All the bundles of notes All the bags of coin

Security measures to remember Risks to avoid Try to bank at least once a day if your company is small, several times a day if a larger company Ensure cash and cheques on the premises are kept to a minimum Remove cash and cheques from the till every hour.

When taking cash and cheques to the bank Vary the time of banking Complete all banking details on documents (ie deposit slips etc) before leaving the office Cultivate a good working relationship with the bank tellers Check bank statements to verify that deposits have been correctly entered

CREDIT DEPOSIT FOR ACCOUNT AT

RECEIVING

BANK’S

TELLERS

STAMP

TREETOPS BANKING CORPORATION

KATOOMBA 01/07/20XX

Normal Deposit slip must be lodges with this Credit

Summary Slip where lodged at a bank or branch other

than that shown above. The Deposit slip may be

retained by the receiving bank/branch and this Credit

Summary Slip transferred under the bank’s internal

procedures. The bank not to be held responsible for

delays in transmission. Cheques etc not available until

collected

Cheques incl

in deposit

6

3599

35

BRAMBLES OF KATOOMBA Net

Credit

$4272

35 048-009 543::24176

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 14 of 16

The organisation’s financial records Making Cheque payments

As we have already discussed; a cheque is a form with pre-printed details of your bank account, on which you write a person‟s or organisation‟s name and an amount of money that you want to pay them. You must also date and sign the cheque. When the cheque is presented to the bank, the money is deducted from your bank account and paid to the person or organisation named on the cheque. Cheques are numbered consecutively and are issued by the bank either in a cheque book or in single pages. Company cheques can only be signed by a member of staff who is authorised to spend the company‟s money. It is often company policy that the signatures of two members of staff are required on a cheque to ensure that one person cannot write cheques to take money out of the company account without the knowledge of other staff. The cheque butt on the left side of the cheque is your record of your purchase and your account balance. You should keep these cheque butt records up to date, so that the information can be used as a quick reference as to the organisation‟s bank balance. The cheque butt shows: The date you write the cheque The payee‟s name A brief description of the payment The balance after the last cheque was written Any money deposited in the account since the last cheque was written The amount of the cheque you are writing The balance after the amount of the cheque is deducted

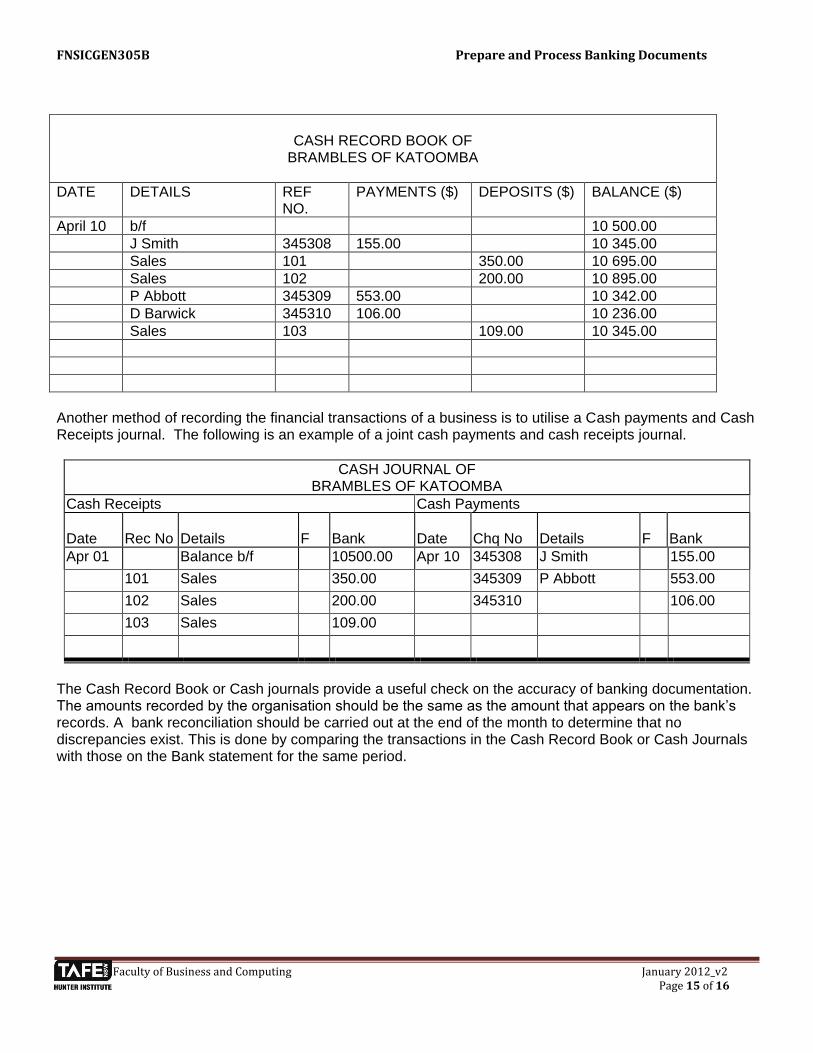

Reconciling the financial records In order to check the amount in a business bank account, a business must keep an accurate record of all deposits and withdrawals. The Cash Record Book is a method adopted by some business‟s which provides a record of the financial position of a business at any given time. Payments made by the business are by cheque or EFT; the amount appears in the Payments column and the cheque number appears in the Reference No. Column. Receipts, from all sources, appear in the Deposits column, and the corresponding receipt number appears in the Reference No. Column. The Balance shows an ongoing balance which is brought forward (b/f) from the previous period and carried forward (c/f) to the next period. An example of the Cash Record Book for Brambles of Katoomba is shown on the next page:

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 15 of 16

CASH RECORD BOOK OF

BRAMBLES OF KATOOMBA

DATE DETAILS REF NO.

PAYMENTS ($) DEPOSITS ($) BALANCE ($)

April 10 b/f 10 500.00

J Smith 345308 155.00 10 345.00

Sales 101 350.00 10 695.00

Sales 102 200.00 10 895.00

P Abbott 345309 553.00 10 342.00

D Barwick 345310 106.00 10 236.00

Sales 103 109.00 10 345.00

Another method of recording the financial transactions of a business is to utilise a Cash payments and Cash Receipts journal. The following is an example of a joint cash payments and cash receipts journal.

CASH JOURNAL OF BRAMBLES OF KATOOMBA

Cash Receipts Cash Payments

Date Rec No Details F Bank Date Chq No Details F Bank

Apr 01 Balance b/f 10500.00 Apr 10 345308 J Smith 155.00

101 Sales 350.00 345309 P Abbott 553.00

102 Sales 200.00 345310 106.00

103 Sales 109.00

The Cash Record Book or Cash journals provide a useful check on the accuracy of banking documentation. The amounts recorded by the organisation should be the same as the amount that appears on the bank‟s records. A bank reconciliation should be carried out at the end of the month to determine that no discrepancies exist. This is done by comparing the transactions in the Cash Record Book or Cash Journals with those on the Bank statement for the same period.

FNSICGEN305B Prepare and Process Banking Documents

Faculty of Business and Computing January 2012_v2 Page 16 of 16

Banking Discussion Points – what would you do in these situations?

1 You are given a cheque to bank that is dated 2 years ago. 2 You are told that you must go to the bank at 3 pm daily. 3 You are not able to get to the bank during business hours to deposit the daily takings. 4 You are asked to pay for some flowers out of the daily cash takings.

5 You find discrepancies between the entries in the cashbook and your bank deposit slip.

As you work through the pack, answer the following questions:

1 What is the purpose of a credit summary slip? 2 On a cheque who is the drawer, who is the drawee and who is the payee?

3 How are you able to avoid someone banking a lost or stolen cheque? 4 What security procedures should be followed when banking cash? 5 Why is it important that you reconcile your bank deposit to your cash book entries? The answers to these questions must be submitted to your facilitator by the completion of your exercises pack.