presented by: dewayne osborn cga, cfp lawton partners financial planning services limited...

Post on 19-Dec-2015

216 views

TRANSCRIPT

Presented By:

DeWayne Osborn CGA, CFP

Lawton Partners Financial Planning Services Limited

Are You Ready for 2006?

My sincere thanks to Ian Barnes CGA – Jewish Foundation of Manitoba who co-wrote sections for our paper: Planned Giving Strategies Planned Giving Strategies currently posted on the currently posted on the

CGA Canada’s PD NetworkCGA Canada’s PD Network

M. Elena Hoffstein of Faskin Martneau DuMoulin LLP presentation to the Canadian Association of Gift Planners Advanced Gift Symposium, November 3, 2005 in Ottawa

Are You Ready for 2006?

Presentation Overview:Presentation Overview:

• Backgrounder and DefinitionsBackgrounder and Definitions

• Summary of New Legislation/Trends.Summary of New Legislation/Trends.

• Discuss Impact on Charity’s ActivitiesDiscuss Impact on Charity’s Activities

• Discuss New Sanctions and Penalties – Section 188Discuss New Sanctions and Penalties – Section 188

• Website Resources Available to YouWebsite Resources Available to You

• Through out the talk, your Questions!Through out the talk, your Questions!

Are You Ready for 2006?

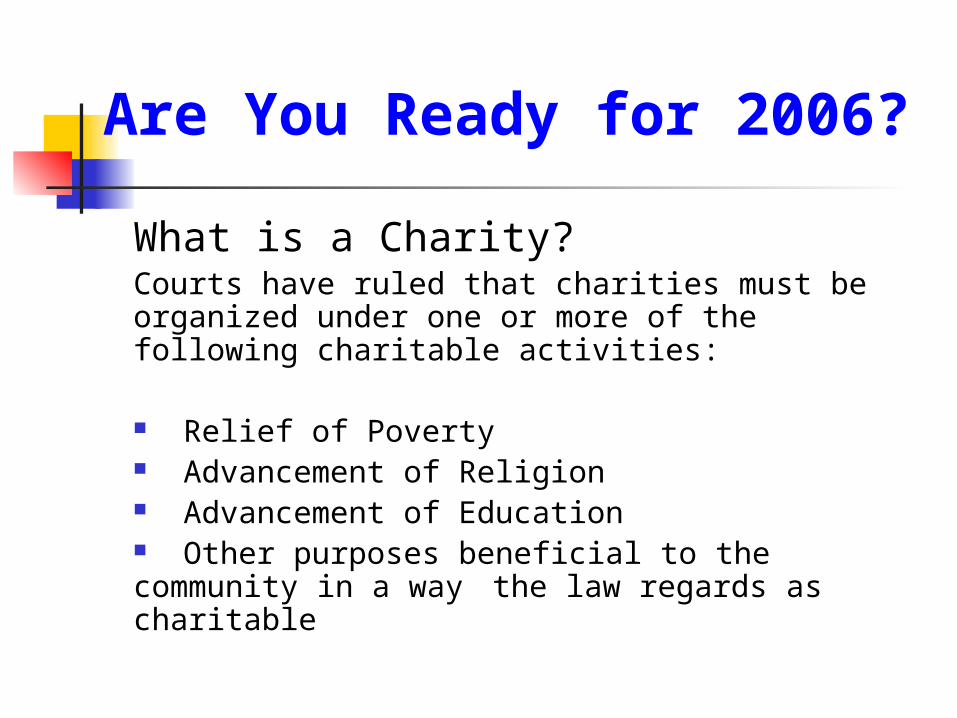

What is a Charity?Courts have ruled that charities must be organized under one or more of the following charitable activities:

Relief of Poverty Advancement of Religion Advancement of Education Other purposes beneficial to the community in a way the law regards as charitable

Are You Ready for 2006?

What are Charitable Activities?What are Charitable Activities?

• Salaries of those performing charitable activities (minister of church)

• Funds for equipment used to perform charitable activities

• Can use Agents, but need Guidelines

• Foundations granting property to other charities

What are NOT Charitable Activities?What are NOT Charitable Activities?

• Funds spent on general administration or fund raising

• Funds spent on political activities

Are You Ready for 2006?

161,227 organizations in Canada$112 Billion in Annual Revenues1/3 from Hospitals, Universities, and Colleges (1% of total) 1% have revenues in excess of $10 million $71 Billion are Registered Charities 56% are Registered Charities $5.6 million Cdns. gave $6.5 billion in 2003

Revenue Sources2003 Survey Nonprofit & Voluntary Sector - Canada

Are You Ready for 2006?

Gov

Earned $ - NonGovGifts &DonationsOther

49%

35%

13%

12%

Revenues

Are You Ready for 2006?

When you get that big, what happens??When you get that big, what happens??

Finance & CRA

Are You Ready for 2006?

According to Finance: FMV exceeds the Advantage received by donor; Advantage is: any consideration received by the

taxpayer Or any person related to the taxpayer;

What is a Gift:All CCRA Gift Brochures and Documents; ITA 248(30-31)

Transfer of property (not services) to charity; andTransfer must be voluntary; andNo benefit to donor, or someone selected by the

donor.Must be accepted by the charity.

A Gift must satisfy four conditions:

Are You Ready for 2006?

Summary of New Legislation 2002 to 2005Summary of New Legislation 2002 to 2005Stephen Rigby: Asst. Commissioner Policy and Planning Speech to CBA 4/14/2004Stephen Rigby: Asst. Commissioner Policy and Planning Speech to CBA 4/14/2004

• Budget 2004 finished investment of $24 million to implement regulatory reforms

• Most of the 75 reforms proposed by the Joint Regulatory Table

• Key CRA principles: ServiceService and PartnershipsPartnerships

• 5 key Elements over the next five years!

• We are now in Year Two?

Are You Ready for 2006?

Summary of New Legislation 2002 to 2005Summary of New Legislation 2002 to 2005

5 Key Elements:

• Strategic Approach to a new Compliance Regime

• More Accessible and Affordable Appeals Regime

• More Transparency and Accessibility to Information

• Improve Service

• Federal-Provincial-Territorial Collaboration

Are You Ready for 2006?

1. ABIL

2. Medical Expenses

3. Carrying Charges

4. Stock Option Deductions and deferrals

5. Province of Residence

A Few trends with the New Legislation

7. Installments

8. Disability Tax Credit

9. Rollovers for Deceased Individuals

10. Business expenses with personal element

Deloitte and Touche Top Ten items questioned by CRADeloitte and Touche Top Ten items questioned by CRA

6.6. Charitable DonationsCharitable Donations

Are You Ready for 2006?

Reliance on terms that have no readily applicable definition. E.g. gratuity, reasonable.

Use of long timelines for intangible things such as “intent to give”.

How stringently will advantageadvantage be enforced?

Where is the burden of proof? Now that cash is implicated, there is no safe asset anymore.

To be absolutely sure that FMV = Eligible amount, the donor needs to die, or gift only exempt property!

Dramatically beefed up ITA 188.1

A Few trends with the New Legislation

Are You Ready for 2006?

Gift of inventory from a Business

Gift of Real Property situated in Canada

Canadian Cultural Property (ITA 39(1)(a)(i.1))

Listed shares (ITA 38(a.1))

Ecological Property (ITA 38(a.2))

Or any gift resulting from death if completed within 36 months from date of death (bequest, RRSP or RRIF, Insurance death benefits).

Other Shares (including ITA 85(1) or 85(2)) or property acquired then gifted provided 248(35) did not apply to the original shares (AKA Exchanged Shares)

Are You Ready for 2006?

Exempt Property

Piece meal approach to drafting legislation

Approval spread out over years (interest deductibility)

Charities are giving up, Smallest are vulnerable.

Auditors are expected to be up to date? Auditors indemnifying opinions

Differing opinions of what will be enforced (proposed legislation, or current law)

Offering “carrots” that really are nearly impossible to achieve (e.g. capital gains pools)

“Seek and Destroy” theme – perpetrating charities

A Few trends with the New Legislation

Are You Ready for 2006?

Pre-Dec 2002 Post-Dec 20 2002 ITA SectionAll Gifts = FMV Eligible Amount >=

20% of Amount Gifted

248(30)

Eligible amount = amount that exceeds the advantage

248(31)

Advantage = total value of all property, services, gratitude, compensation, or other benefit.

Includes Limited-Includes Limited-recourse debt recourse debt (143.2(6.1)(143.2(6.1)

248(32)

Are You Ready for 2006?

Limited Recourse Debt 143.2(6.1), Fact Sheet November 2004

Investor applying for and receiving a loan to facilitate a Investor applying for and receiving a loan to facilitate a cash donation. cash donation.

Usually the investor makes a cash contribution to the Usually the investor makes a cash contribution to the promoter or another entity promoter or another entity (e.g. an off-shore insurance (e.g. an off-shore insurance company)company)

Includes Includes anyany unpaid amounts unpaid amounts eveneven if there is a guarantee, if there is a guarantee, security, or similar indemnitysecurity, or similar indemnity

All leverage cashAll leverage cash donations fall here now, or soon will be! donations fall here now, or soon will be!

FMV = Cash actually provided by DonorFMV = Cash actually provided by Donor

If repaid in an appropriate manner = Eligible amount.If repaid in an appropriate manner = Eligible amount.

Are You Ready for 2006?

Pre-Dec 2002 Post-Dec 20 2002 ITA SectionAll Gifts = FMV Cost = FMV when

property is acquired in course of making a gift

248(33)

Post Feb 18, 2003 ITA SectionRepay Limited-recourse = gift in year paid

248(34)

Post Dec 5, 2003 ITA SectionFMV= Lesser of Cost or FMV ifif: property acquired via tax shelter within 3 yrs of donating, or within 10 years with intent to donate

248(35)

Are You Ready for 2006?

Pre-Dec 2002 Post-July 17, 2005 ITA SectionAll Gifts = FMV With 248(35), if non-

arms length owned in time period, then lesser of cost to that person, or donor.

248(36)

Post-Dec 5, 2003 ITA SectionNon-application of 248(35) for gifts of: business inventory, real estate in Canada, public securities, cultural or ecological, exchanged shares

248(37)

Are You Ready for 2006?

Pre-Dec 2002 Post-Dec 5, 2003 ITA Section

All Gifts = FMV Artificial transx. where donor sells property subject to 248(35), then donates cash or other property received. FMV = cost of property

248(38)

Post-July 16, 2005 ITA Section

FMV = nil if purpose of transx is:Avoid 248(35), GAAR applies,

248(38 cont’d)

Are You Ready for 2006?

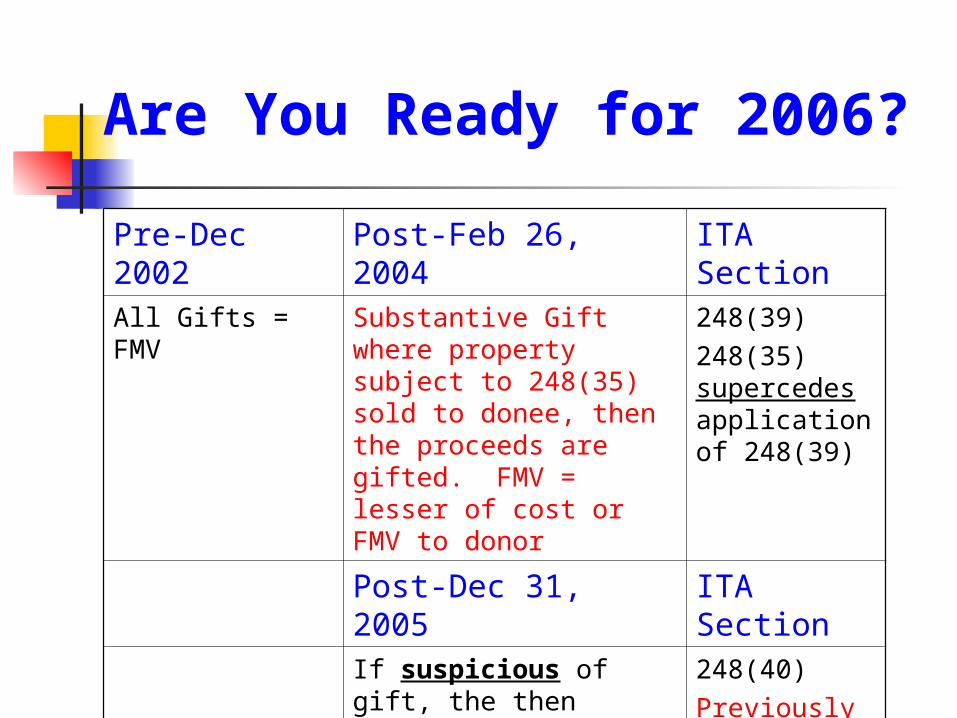

Pre-Dec 2002 Post-Feb 26, 2004 ITA SectionAll Gifts = FMV Substantive Gift where

property subject to 248(35) sold to donee, then the proceeds are gifted. FMV = lesser of cost or FMV to donor

248(39)248(35) supercedes application of 248(39)

Post-Dec 31, 2005 ITA SectionIf suspicious of gift, the then charity must make reasonable inquiry to determine of gift is caught by:248(31),(35),(36),(38),& (39).

248(40)Previously required for all gifts >$5,000

Are You Ready for 2006?

Pre-Dec 2002 Post-Dec 31, 2005 ITA SectionAll Gifts = FMV Failure of donor to

report situations where 248(31),(35),(336) or (39). Eligible amount = NIL

248(41)

Are You Ready for 2006?

Any arrangement where it may be reasonably considered that a person would enter the arrangement to: make a gift, or incur limited recourse debt.

If property was acquired at any time through a gifting arrangement that is a tax shelter, OR

Any gift is made less than 3 years from acquiring the property OR

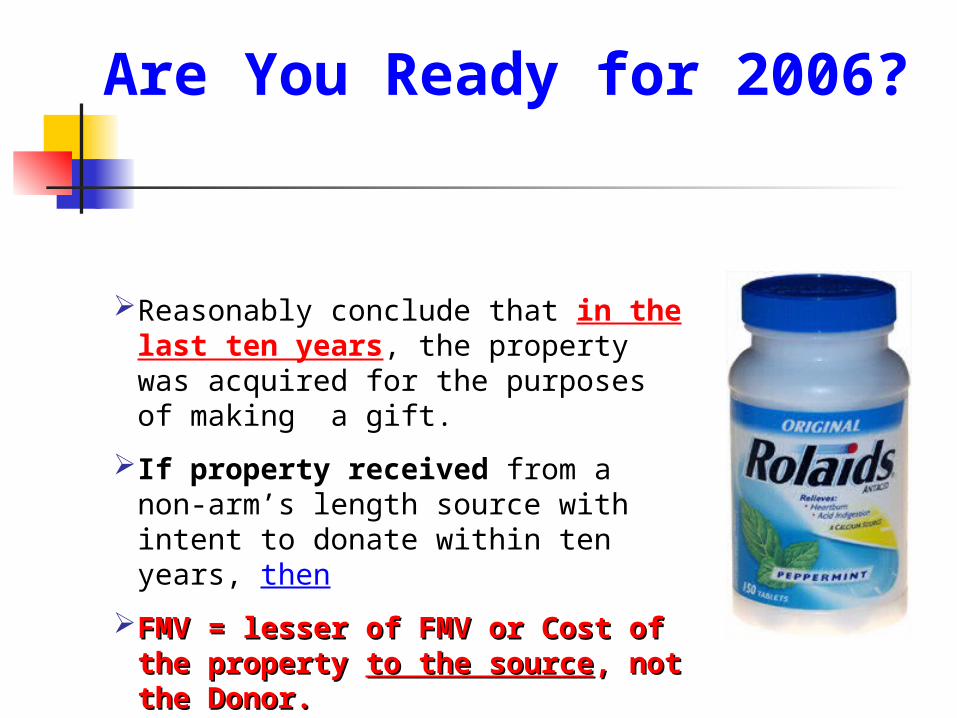

Reasonably conclude that in the last ten years, the property was acquired for the purposes of making a gift.

FMV = lesser of FMV or Cost to the Donor.FMV = lesser of FMV or Cost to the Donor.

Gifting Arrangement: December 5, 2003 and on

ITA 237.1, 248 (35), Fact Sheet November 2004

Are You Ready for 2006?

Are You Ready for 2006?

Reasonably conclude that in the last ten years, the property was acquired for the purposes of making a gift.

If property received from a non-arm’s length source with intent to donate within ten years, then

FMV = lesser of FMV or Cost of the FMV = lesser of FMV or Cost of the property property to the sourceto the source, not the Donor., not the Donor.

Typically, but not always, the investor becomes a beneficiary of a trust

The investor receives the property from the trust. The property may have a lien on it.

Investor donates property to charity

Typically, the donor used 30% of his or her own cash, the balance is provided from other means.

No matter, FMV = lessor of FMV or Cost to Donor.

Gifting Trust Arrangements – Nice Try?

Are You Ready for 2006?

A Gift is to be Made

Is it a Bequest, Proceeds from Life Insurance, RRSP, or RRIFYesIssue a Tax

Receipt

Eligible Amount = FMV less advantage

to donor (if any)

No

Is it Publicly Securities, Ecological or Cultural Property, Inventory from a Business, Real Estate in Canada?

Yes

No

Was it Acquired in the last 10 years?No

YesDonor intended to Gift? OR Acquired from a Tax Shelter in Last 3 Years, OR A loan was used to acquire property?

No

YesTax Receipt reduced to the amount actually paid by the donor to acquire property

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Definitions:

DISBURSEMENT QUOTA (DQ)

The disbursement quota is the minimum amount a registered charity has to spend to keep its registered status, including gifts to qualified donees.

In general, it is an expenditure test based on tax-receipted revenue (prior to March 23, 2004) of the previous fiscal period.

Certain investment assets and gifts from other registered charities must also be considered.

Are You Ready for 2006?

What Expenditures Counts Towards DQ?What Expenditures Counts Towards DQ?

• Own charitable activities or

• Disbursed to qualified donees which are:

• Registered charities

• Registered Cdn amateur athletic associations

• Housing corporations

• Canadian Municipalities

• UN and its agencies

• Schedule VIII foreign charities (typically universities)

• Registered national arts associations

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Definitions:

DISBURSEMENT QUOTA (DQ) - Continued

The purpose of the disbursement quota is to ensure that registered charities actively use their tax assisted donations to help others according to their charitable purposes.

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Activity (Pre March 23, 04)

Charitable Organizatio

n

Public Foundation

Private Foundation

Normal Tax Receipted Gifts(no bequest, 10-yr)

80% by end of next year

80% by end of next yr

80% by end of next yr

Receipted Beq, 10-year Gifts

nil 4.5% FMV 4.5% FMV

Beq, 10-year spent

80% current yr

80% current yr

80% current yr

Gifts From Other Charities

nil 80% by end of next yr

100% by end of next yr

Avrg Val of Inv Property

nil 4.5% FMV 4.5% FMV

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Activity (Post March 23, 2004)

Charitable Organizati

on

Public Foundation

Private Foundation

Normal Tax Receipted Gifts(no bequest, enduring)

80% by end of next year

80% by end of next yr

80% by end of next yr

Receipted Beq, or enduring prop.

3.5% FMV 3.5% FMV 3.5% FMV

Beq, 10-year spent

80% current yr

80% current yr

80% current yr

Gifts From Other Charities (non-specified)

80% by end of next yr

80% by end of next yr

100% by end of next yr

Avrg Val of Inv Property (if <25,001 = nil)

3.5% FMV 3.5% FMV 3.5% FMV

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Investment Property : Investment property for purposes of DQ is property that: - was not used directly for charitable programs or

administration; and- the charity owned at the beginning or end of the fiscal period

covered by the return Investment property For purposes of the DQ, includes any real estate or personal

property, or part of such that was NOT used directly for charitable programs or administration (e.g cash, investments, land).

The value is an average based on a specified number of periods over the previous 24 months.

One chosen, the registered charity must apply for written permission to the CRA to change the number of periods.

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Post Bill C33 – The New DQ Formula

A + A.1 + B + B.1 WHERE:

B.1 = C X .035[D-(E+F]/365

A+A.1+B+(C x .035[D-(E+F)]/365 and D must be > $25,000

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Post Bill C33 – The New DQ Formula

A = 80% of prior year gifts receipted (excluding enduring property and specified gifts)

A.1 = Amount by which:

a) Sum of:

I) 80% enduring property expended in the year (except specified gift, pre-1994 bequests or inheritances and property described in II, PLUS

II) 100% of total enduring property gifts transferred to qualified donees (except specified gifts)

Exceeds:

b) Amount claimed by charity that may not exceed lesser of 3.5% of investment assets and Capital Gains Pool

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Post Bill C33 – The New DQ Formula B = 100% gifts from other charities if private fdns and 80% if public charity

(except specified and enduring property)

C = # of Days on the Taxation Year

D = Prescribed amount of all or a portion of property owned by the charity at any time in the 24-months immediately preceding taxation year that was not used directly on charitable activities or administration if > $25,000. Otherwise, the amount is nil.

E = Total of Part a.1 (ii) PLUS 5/4 of A.1 (I)

F = If a private fdn, the amount determined for B. In all other cases, 5/4 the amount determined for B.

Are You Ready for 2006?

The DQ shall be extended to include charitable organizations, so that all registered charities shall be subject to the same disbursement obligations to fund charitable activities.

The proposed change is applicable to tax years that begin

after 2008 for charitable organizations registered before March 23, 2004.

For charitable organizations registered after March 23, 2004 the change is applicable for taxation years commencing after March 23, 2004.

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

SPECIFIED GIFT

Specified gifts allow for the transfer of gifts from one registered charity to another registered charity.

The gift is designated as a specified gift by mutual agreement between the organizations.

The recipient organization does not include the gift in the calculation of its DQ and the gifting organization may not use the gift to meet its DQ obligations.

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement QuotaTEN-YEAR GIFTS (prior to March 23, 2004 Budget)

Gifts subject to a donor’s written trust or direction that the registered charity holds the gift for a least ten years.

These gifts are excluded from the DQ until spent. Gifts with a ten-year direction are useful when a registered charity

wants to accumulate a capital (endowment) fund with the intention of distributing the income only.

When the stipulated period expires, the registered charity MAY choose to spend some or all of the funds. The expended amount spent must then be included when calculating the DQ

Trust issues, power to alter, etc., are important legal considerations

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

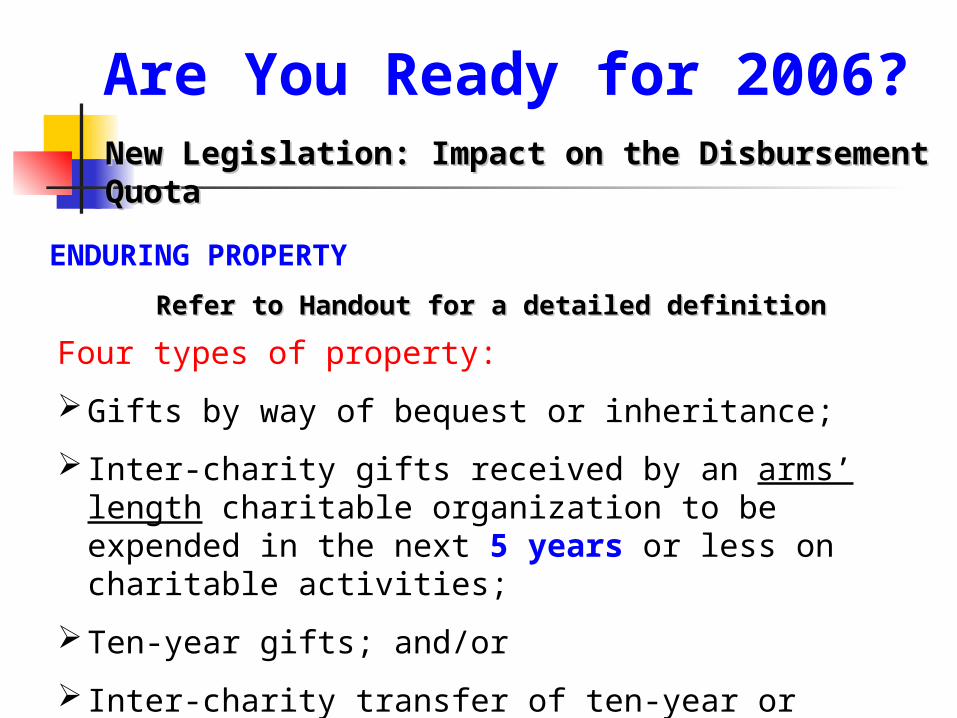

ENDURING PROPERTY

Refer to Handout for a detailed definitionRefer to Handout for a detailed definition

Four types of property:

Gifts by way of bequest or inheritance;

Inter-charity gifts received by an arms’ length charitable organization to be expended in the next 5 years or less on charitable activities;

Ten-year gifts; and/or

Inter-charity transfer of ten-year or gifts be way of bequest or inheritance. AKA Endowments?

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Gifts by Way of Bequest or Inheritance

Life insurance proceeds, and direct beneficiary designations of RRSP, RRIF plans

Applies for deaths after 1998. Retroactive application can be made.

Subject to 3.5% DQ while held, 80% when disbursed.

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Gifts Received by Charity to be Used on Charitable Activities within 5 years (AKA 5 Year Gifts)

Gift received by a charitable organization from another registered charity

Charities must be at arms length

Must be accompanied by a trust or direction to hold for not more than 5 years and to be used for charitable activities

Example foundation funding a building.

What happens if not Spent in 5 years??

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Inter-charity Transfers of 10-year and Gifts by Way of Bequest or Inheritance

If original gift was subject to trust or written direction, THEN that direction is binding on the recipient charity.

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

Charities are now allowed to access capital gains realized on endowments to reduce their disbursement quota.

Before, the DQ rules discouraged realization of capital gains because realized gains were subject to the 80% DQ rule and must be disbursed by the following year.

Effective for taxation years beginning after March 22, 2004, the charity’s 80% DQ requirement shall be reduced by the lesser of:

(a) The capital gains pool for the charity, OR

(b) 3.5% of the value of all property not directly used in charitable activity

Critical that the Charity’s policies permit limited encroachment?

Are You Ready for 2006?

New Legislation: Impact on the Disbursement QuotaNew Legislation: Impact on the Disbursement Quota

What is the Capital Gains Pool??

The capital gains pool is a cumulative calculation: The aggregate of capital gains realized from the disposition of

endowments after March 22, 2004 and before the end of the taxation year less the amount determined and utilized for the DQ calculation for a preceding taxation year.

Accessing the capital gains pool is at the discretion of the charity. Therefore it is prudent for the charity to aggregate and track the

capital gains pool on the Charity Return each year even if it does not access the pool in a given year.

Applies only to Gains after 1994

Are You Ready for 2006?

Inter-Charity Property TransfersInter-Charity Property Transfers

Three General Types of Transfers:

Ordinary gifts (non-specified, non enduring)

Specified gifts

Enduring property (non-specified)

Are You Ready for 2006?

Inter-Charity Property TransfersInter-Charity Property Transfers

Ordinary Gifts:

$10,000 in property transferred from Charity A to Charity B

Charity A satisfied its DQ obligations.

Charity B if charitable organization or public fdn, required to expend 80% next year. Private fdn required to spend 100%.

Are You Ready for 2006?

Inter-Charity Property TransfersInter-Charity Property Transfers

Specified Gifts

Transferor charity can not count toward DQ

Recipient Charity not required to include any amount in DQ.

If Charity B expends the property in the next year, it can count it toward fulfilling its DQ.

Are You Ready for 2006?

Inter-Charity Property TransfersInter-Charity Property Transfers

Enduring Property: 10-year, 5-year, Inheritance, Bequest, RRSP, RRIF

Transferor charity satisfies its 100% DQ obligation with the transfer

Recipient charity not required to expend in its DQ

If expended in another year, obligated to include 80% in DQ

Are You Ready for 2006?

Inter-Charity Property TransfersInter-Charity Property Transfers

Enduring Property Transferred as a Specified Gift

A bad thing for the transferor charity!

If Charity A designated enduring property as a specified gift, then it could not use it in its DQ

Charity B would receive it without creating a DQ obligation

When charity B expends the gift in the following year, Charity B would be able to use it for DQ obligations

Are You Ready for 2006?

Inter-Charity Property TransfersInter-Charity Property Transfers

Property Transferred as a Result of Part V Penalty

For fines > $1,000 charities can transfer funds to other arms-length, non-implicated charities

Such transfers do not qualify as a DQ expenditure for the purposes of the DQ calculation.

Are You Ready for 2006?

Quiz TimeQuiz Time

1. Charity A receives $100, issues a tax receipt, then spends $80, and saves the $20. How is that $20 treated for DQ purposes if:

a) the funds are placed in a bank acct reserve for administrative expenses?

b) invested in a 5-year GIC for operating expenses?

c) invested in capital growth mutual funds?

Are You Ready for 2006?

Quiz TimeQuiz Time

2. Charity in meeting its DQ disburses funds on the following:

a) Salary of an administrative director

b) Legal/accounting fees

c) Real property taxes

d) Permitted advocacy activities

3. Charity receives $100 for a gift in kind and sells it for $80?

4. Transfers a specified gift to Charity B for investment purposes

Are You Ready for 2006?

Quiz TimeQuiz Time

Issues around 5 year gifts: are these permitted?

1. Indv donor X gives a gift to charitable organization to spend over 5 years?

2. Charity A (public fdn) gives to charity B (char org) to underwrite the 5 year costs of hiring a professional fund raiser?

3. Charity A (public Fdn) gives to charity B (char org) to underwrite the 5 year costs of buying computers.

4. Charity A (Private fdn) gives to charity B (hospital fdn) funds to help charity C (hospital) build a building over 5 years?

Are You Ready for 2006?

Comprehensive DQ Problem with Solution is AttachedComprehensive DQ Problem with Solution is Attached

Are You Ready for 2006?

Prior to the September 2004: only official sanction was revocation of charitable status

Now, there are 11 new infractions each with a two level penalty – Became Law May 13, 2005

Most significant revision to charitable regulations in 20 years!

Your current registration may even be annulled? (ITA 149.1(23))

Revocation tax can be applied to persons that received property from charity

New Sanctions and Penalties (ITA 188.1)

CRA

Charity

Are You Ready for 2006?

If annulled, you keep assets, yet lose ability to If annulled, you keep assets, yet lose ability to issue receipts.issue receipts.

If guilty, you must remain clean for (5) years to If guilty, you must remain clean for (5) years to avoid second level sanctionavoid second level sanction

You can still be revoked for first infraction?You can still be revoked for first infraction?

You can appeal to CRA, then Tax Court of CanadaYou can appeal to CRA, then Tax Court of Canada

See handout for CRA listing Infractions and their See handout for CRA listing Infractions and their PenaltiesPenalties

New Sanctions and Penalties (ITA 188.1)

Are You Ready for 2006?

Appeal Process Overview (CSP-T09, CSP-S18)

The Charity receives Notice of Assessment from CRA Charity has 90 days from date the Notice was mailed to file

for Re-assessment of penalty or to object to annulment, suspension or revocation.

If a Notice of Objection or Re-assessment is filed, then the Charity can file to appeal to Tax Court of Canada. Such appeal must occur after either the Minister has acknowledged the charity’s notice, OR

90 days after the Charity’s notice of objection regardless of acknowledgement from CRA.

Are You Ready for 2006?

Any penalty over $1,000 can be paid to an non-implicated qualified donee.

If penalties are over $25,000, the charity is automatically suspended for one year.

Penalties (including Revocation Tax) are collected one year from the day after the date the notice is mailed (Policy CSP-C26)

Major Infractions - Continued

Are You Ready for 2006?

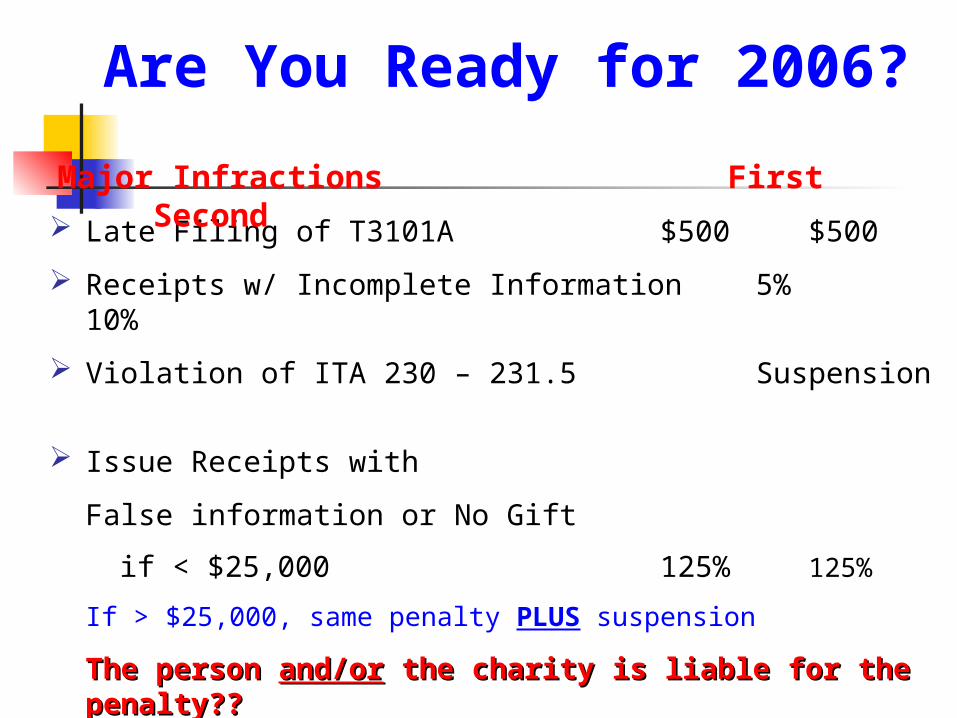

Late Filing of T3101A $500 $500

Receipts w/ Incomplete Information 5% 10%

Violation of ITA 230 – 231.5 Suspension

Issue Receipts with

False information or No Gift

if < $25,000 125% 125%

If > $25,000, same penalty PLUS suspension

The person The person and/orand/or the charity is liable for the penalty?? the charity is liable for the penalty??

Delay Expenditure between charities Amt transferred plus Jointly and Severally Liable 110% (susp likely)

Major Infractions First Second

Are You Ready for 2006?

CO or Pub Fdn carrying onCO or Pub Fdn carrying on

Business not related or PrivBusiness not related or Priv

Fdn doing any businessFdn doing any business 5% inc5% inc 100% & 100% & Susp Susp

Fdn Acquires control of CorpFdn Acquires control of Corp 5% div5% div 100% 100%

Undue Benefit conferred to a personUndue Benefit conferred to a person 105%105% 110% + 110% + susp susp

Major Infractions First Second

Are You Ready for 2006?

Are You Ready for 2006?

Samples of Potential Problems

• Charity A receives notice of intent to annul registration. Can it continue its operations?

• Donor gifts $50,000 cash to Charity A. Eight years later at a major donor reception, Charity A learns that the cash was derived from the donor’s brother with intent to donate (brother did not need the tax credits)?

• Same scenario as above, but donor is a company and cash was derived from the company’s operating line (unsecured)?

• Donor gifts $25,000 in artwork with proper valuation. Four years later, you find out that the art was obtained from a non-tax shelter gifting arrangement?

Are You Ready for 2006?

Samples of Potential Problems – Cont’d

• The donor’s Executor notifies you that you will be receiving $150,000 in artwork the donor received by virtue of a tax shelter arrangement two years ago. The artwork is fairly valued at $150,000.

• A donor donates $25,000 in IBM shares to your charity? Immediately prior to the gift, he tells you that he borrowed the funds to buy the shares.

• A new donor wants to gift to your charity $100,000 lump sum in cash. The donor rode the bus to the meeting, was wearing very “worn” clothes, did not have a telephone, and lived in a small one bedroom apartment in a low rent area of town. Should you ask about the$100,000?

Are You Ready for 2006?

Samples of Potential Problems – Cont’d

• A donor want to gift to your church $25,000 worth of pharmaceuticals for its work with the homeless. You know the donor is a professional fire fighter.

• A donor arrives at your charity and proudly states that she has taken your charity out of her will and hands you $25,000 in Microsoft shares that she meant to give you after her death. What do you do? Would your response be different if it was gold and diamonds?

• You get a message that a new donor want to gift some art prints to your charity that he recently acquired for a good price. What do you do?

• Donor want to gift to you a lot in Winnipeg he purchased four years ago using an unsecured credit line.

Are You Ready for 2006?

Samples of Potential Problems – Cont’d

• A donor gifts to your charity a car valued at $15,000. You know the donor likes new cars and has frequently traded in in new cars every two to three years.

• A long time, well known, generous donor wants to gift to you $100,000 in shares of his private company. The “preferred” shares were created during an estate freeze 3 years ago. The original common shares were acquired 12 years ago.

• An artist wants to gift several pieces he specifically created for your charity’s fund raising event. The pieces are fairly valued at $15,000. What is the Eligible amount of the tax receipt?

Web Based, Technical Resource for You.Web Based, Technical Resource for You.

Are You Ready for 2006?

Thanks You!Thanks You!

Are You Ready for 2006?