project feasibilty study and evaluation . aj. chaiyawat thongintr. mae fah luang university (mfu)...

DESCRIPTION

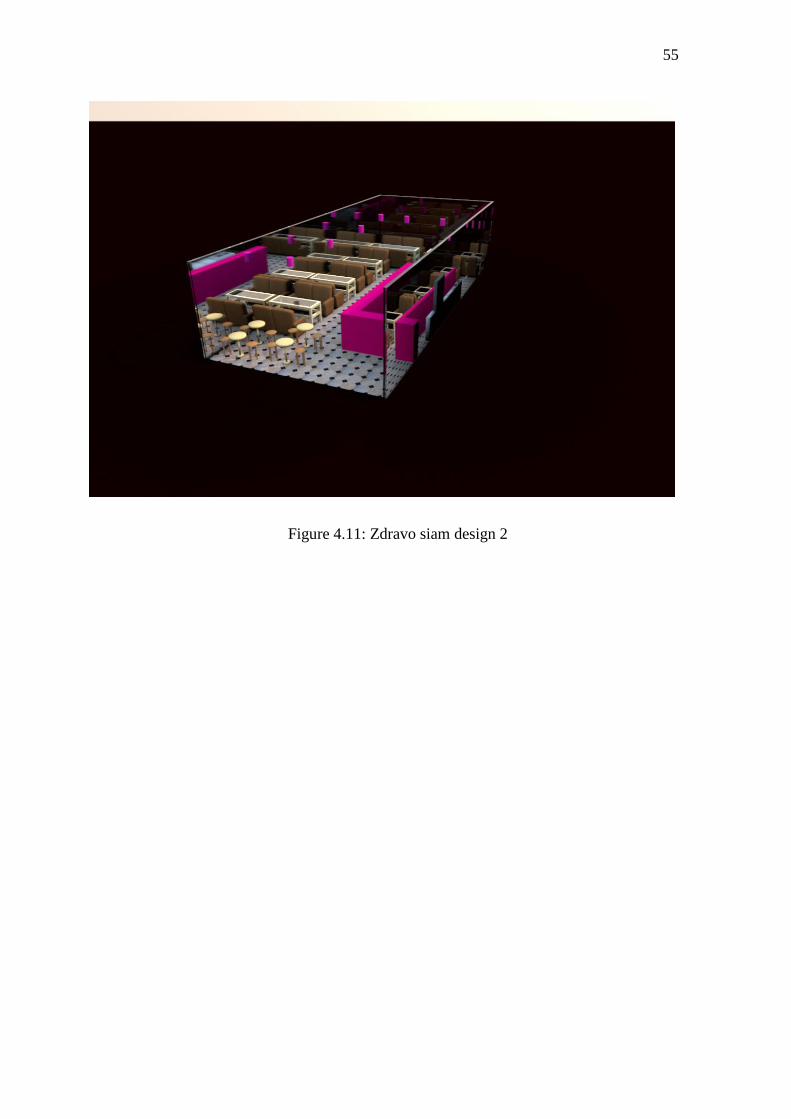

Zdravo Siam team1. Mr. SRIRAMET BOONTHANAROM ID:49312030982. Mr. WIWAT TANGPRASOPCHOT ID:49312031013. Miss SIRILUCK WONGMEEBOON ID:49312031084. Mr. SIWAT TANTALELAR ID:49312031105. Mr. JIRAYU BUTHKHUNTHONG ID:4931203174TRANSCRIPT

I

I

MEMBER

1. Mr. SRIRAMET BOONTHANAROM

ID:4931203098

2. Mr. WIWAT TANGPRASOPCHOT

ID:4931203101

3. Miss SIRILUCK WONGMEEBOON

ID:4931203108

4. Mr. SIWAT TANTALELAR

ID:4931203110

5. Mr. JIRAYU BUTHKHUNTHONG

ID:4931203174

Business Administration

Mae Fah Luang University

II

Preface

Zdravo siam are the project feasibility study in the term to study the feasibility

in opening up an ice cream business at ABAC Plaza. Which ice cream can be seen as

cold and sweet but the way in studying the feasibility of this Zdravo Siam project are

not as sweet as the project name. It is expected that the studying on this project

feasibility study will help any people who wanted to start ice cream business to read

and be a part of the inspiration of the reader.

III

Excutive summary

This consists of a feasibility study of an ice cream shop opening up as the ice

cream market in Thailand nowadays, ice-cream business still one of the business that

many people also interested to go for. The origins of ice cream can be traced back to

at least the 4th century B.C. Early references include the Roman emperor Nero (A.D.

37-68) who ordered ice to be brought from the mountains and combined with fruit

toppings, and King Tang (A.D. 618-97) of Shang, China who had a method of

creating ice and milk concoctions. Ice cream was likely brought from China back to

Europe. Over time, recipes for ices, sherbets, and milk ices evolved and served in the

fashionable Italian and French royal courts. Ice cream was imported to Thailand in

Phra Chulachom Klao Chaoyuhua or King Rama V era

Project Objective are to analyze The feasibility of an ice cream industry and to

provide the project feasibility study Thai people is consumption rate are at 6.0 liter

per year. The consumption rates are rising by 5.0% per year. When compare the

consumption rate of ice cream of Thai people to neighbor’s rate. Thailand ice cream

consumption rate are the lowest when compare with Malaysia which the ice cream

consumption rate is 3 liter per year or Japan which is 7 liter per year and still very low

when comparing to other country which are in Europe area the highest rate of ice

cream consumption is USA which reach to 24 liter for person per year and Australia

consumption rate is 18 liter for person per year.

So this are the interested point to show that there are an opportunity to built a

profit from ice cream in this report it will illustrate about what strategy that been use

how ice cream are made what is the marketing mix including the 3C analysis. Thus, it

also tell about the financial analysis and shown every financial statement in monthly

base. And in also provide the risk management that will tell how to deal with the

problem for the certainty risk and uncertainty risk.

IV

Table of content Chapter1 ......................................................................................................................... 2

1.1 Background and Significance of the Project ........................................................ 2

1.2 Project Objective .................................................................................................. 3

1.3 Benefits of Project................................................................................................ 3

1.4 Grant Chart........................................................................................................... 4

Chapter 2 ........................................................................................................................ 6

2.1 Nature of Industry ................................................................................................ 6

2.1.1 Frozen custard, French ice cream or French custard ice cream .................... 6

2.1.2 Low fat ice cream.......................................................................................... 6

2.1.3 Non fat ice cream .......................................................................................... 6

2.1.4 Gelato ............................................................................................................ 7

2.1.5 Bulky flavored ice cream .............................................................................. 7

2.1.6 Soft serve ...................................................................................................... 7

2.1.7 Fruit Sherbet.................................................................................................. 7

2.1.8 Sorbet ............................................................................................................ 7

2.1.9 Frozen yogurt ................................................................................................ 8

2.1.10 Granite......................................................................................................... 8

2.1.11 Water ice or ice ........................................................................................... 8

2.2 Situation of Industry ............................................................................................ 9

2.3 Product/Service (in General).............................................................................. 10

2.3.1 Ice Cream .................................................................................................... 10

2.4 Vision of your Organization .............................................................................. 11

2.5 Mission ............................................................................................................... 11

2.6 Strategy .............................................................................................................. 11

2.6.1 Corporate Level .......................................................................................... 11

2.6.2 Business Level ............................................................................................ 12

2.6.3 Functional Level ......................................................................................... 13

Chapter3 ....................................................................................................................... 16

3.1 Market Analysis ................................................................................................. 16

3.1.1 General Environment Analysis ................................................................... 16

3.1.2 Competition Analysis (3C Analysis) .......................................................... 17

3.2 STP Analysis ...................................................................................................... 20

3.2.1 Segment....................................................................................................... 20

3.2.2 Targeting ..................................................................................................... 20

3.2.3 Positioning .................................................................................................. 20

3.3 Marketing Mix Strategy ..................................................................................... 21

V

3.3.1 Product ........................................................................................................ 21

3.3.2 Price ............................................................................................................ 22

3.3.3 Place ............................................................................................................ 22

3.3.4 Promotion .................................................................................................... 22

3.4Five force model ................................................................................................. 22

3.5 Sales Forecast/Profit Estimation ........................................................................ 25

3.5.1 Time Series Analysis .................................................................................. 26

3.6 Sale Forecast ...................................................................................................... 27

3.7 Conclusion ......................................................................................................... 31

Chapter 4 ...................................................................................................................... 33

4.1 Production and Operations Analysis .................................................................. 33

4.1.1 Product Characteristics ............................................................................... 33

4.1.2Production process ....................................................................................... 34

4.1.3 Life Time .................................................................................................... 42

4.1.4 Ice cream recipe .......................................................................................... 45

4.1.5 Location ...................................................................................................... 51

4.1.6 Facility layout ............................................................................................. 53

4.1.7 Machine Tools and Equipment ................................................................... 58

4.1.8 Facility Management .................................................................................. 65

4.2 Cost of Investment ............................................................................................. 66

4.2.1 Rent ............................................................................................................. 66

4.2.2 Total Pre operation cost .............................................................................. 66

4.3 Investment Cost ................................................................................................. 66

4.3.1 Register’s Price. .......................................................................................... 67

4.3.2 A Fee for establishes a business [Co., ltd.] ................................................. 67

4.3.3 Depreciation ................................................................................................ 71

4.4 Operating Cost ................................................................................................... 72

4.4.1 Raw material Cost ....................................................................................... 72

4.4.2Overhead ...................................................................................................... 78

4.5 Management Analysis ........................................................................................ 78

4.5.1 Administration Cost .................................................................................... 78

4.6 Conclusion ......................................................................................................... 78

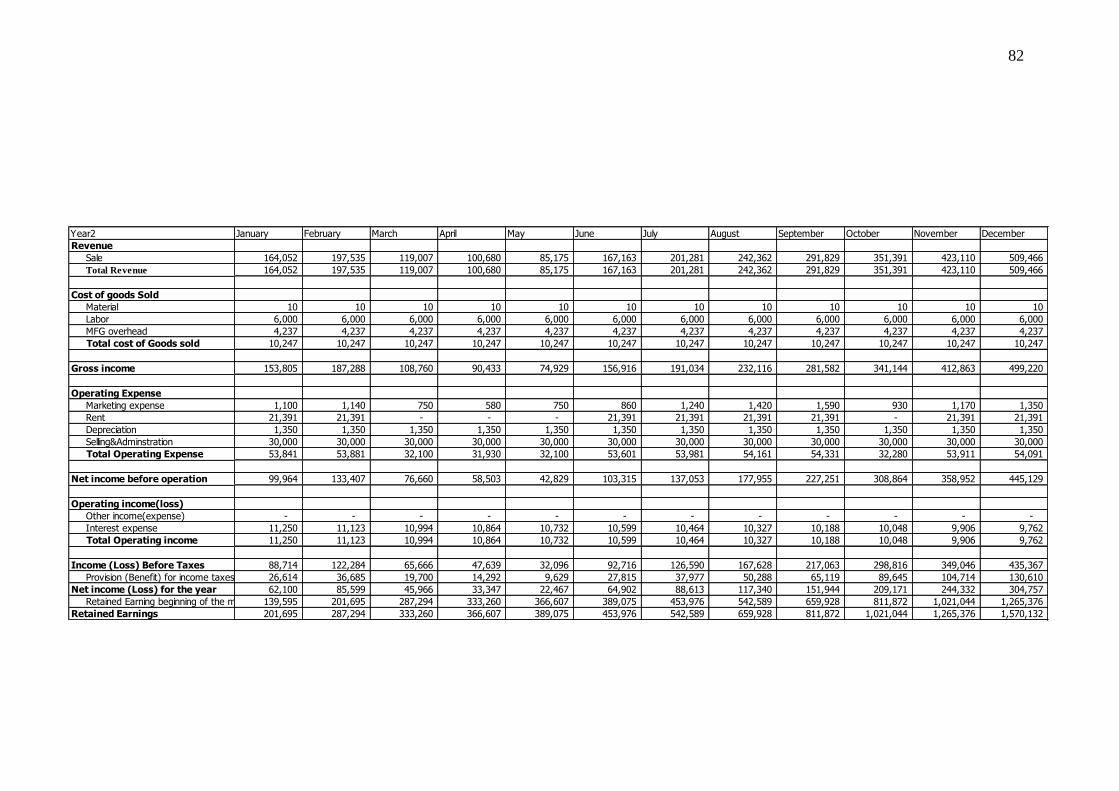

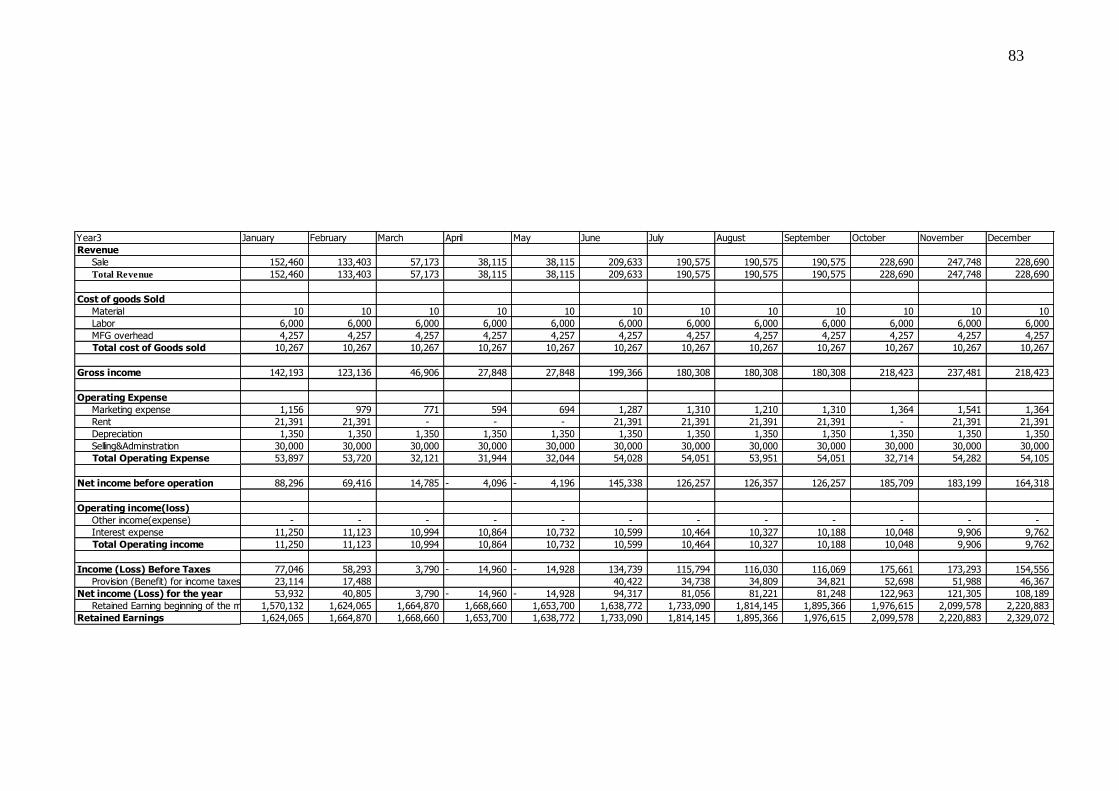

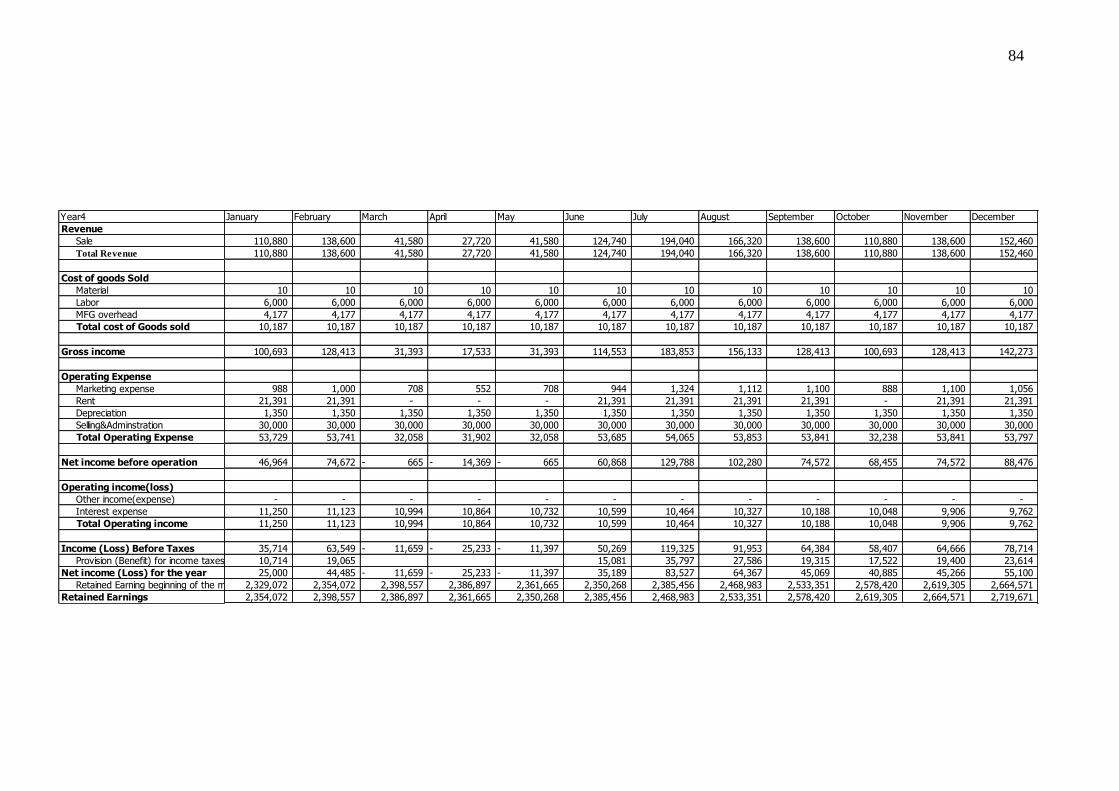

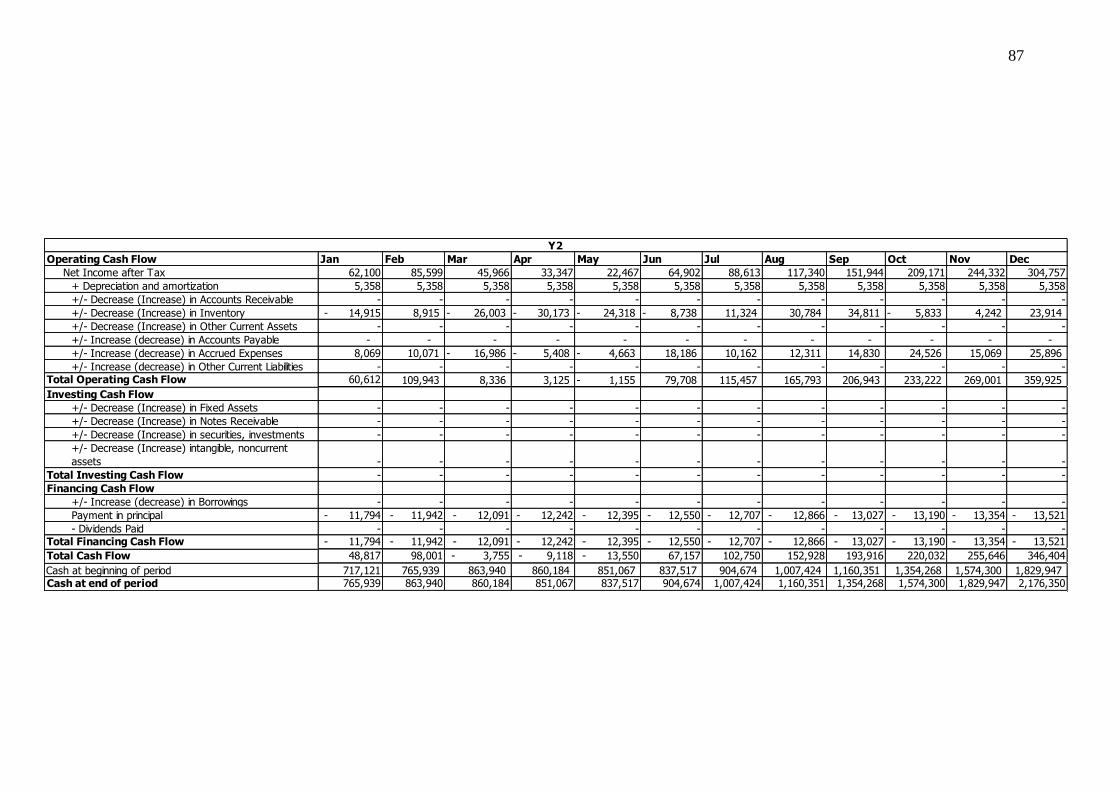

Chapter 5 ...................................................................................................................... 81

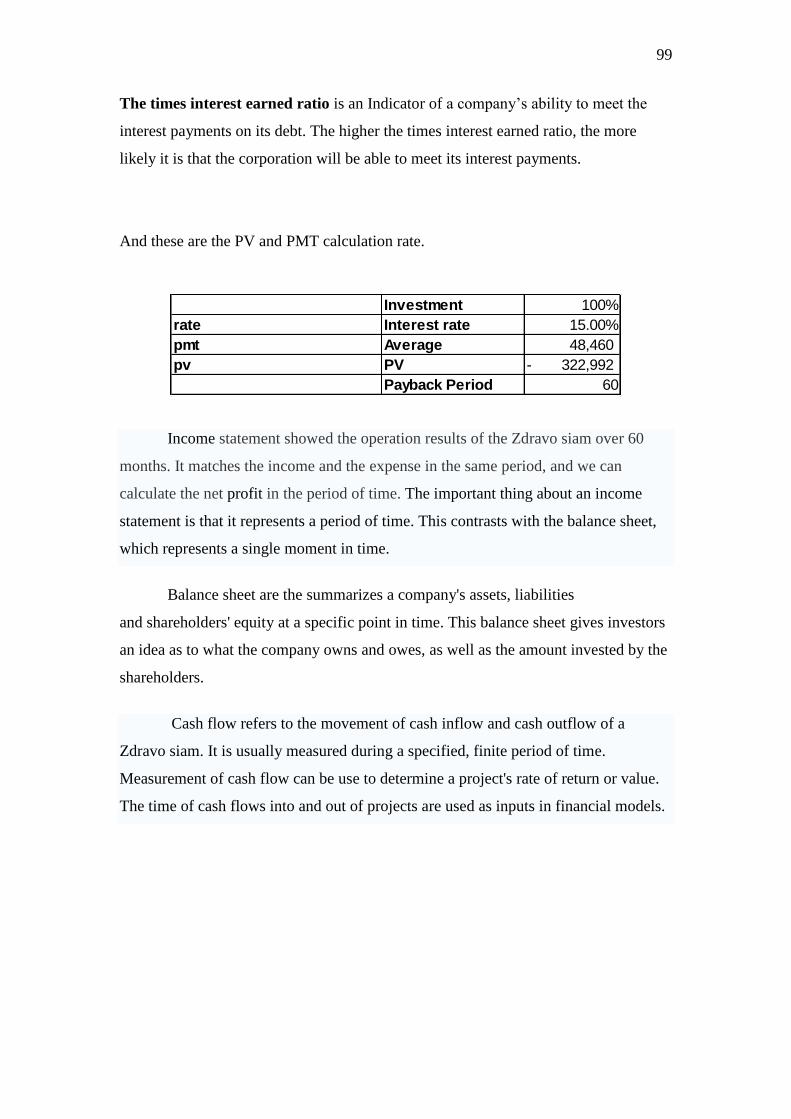

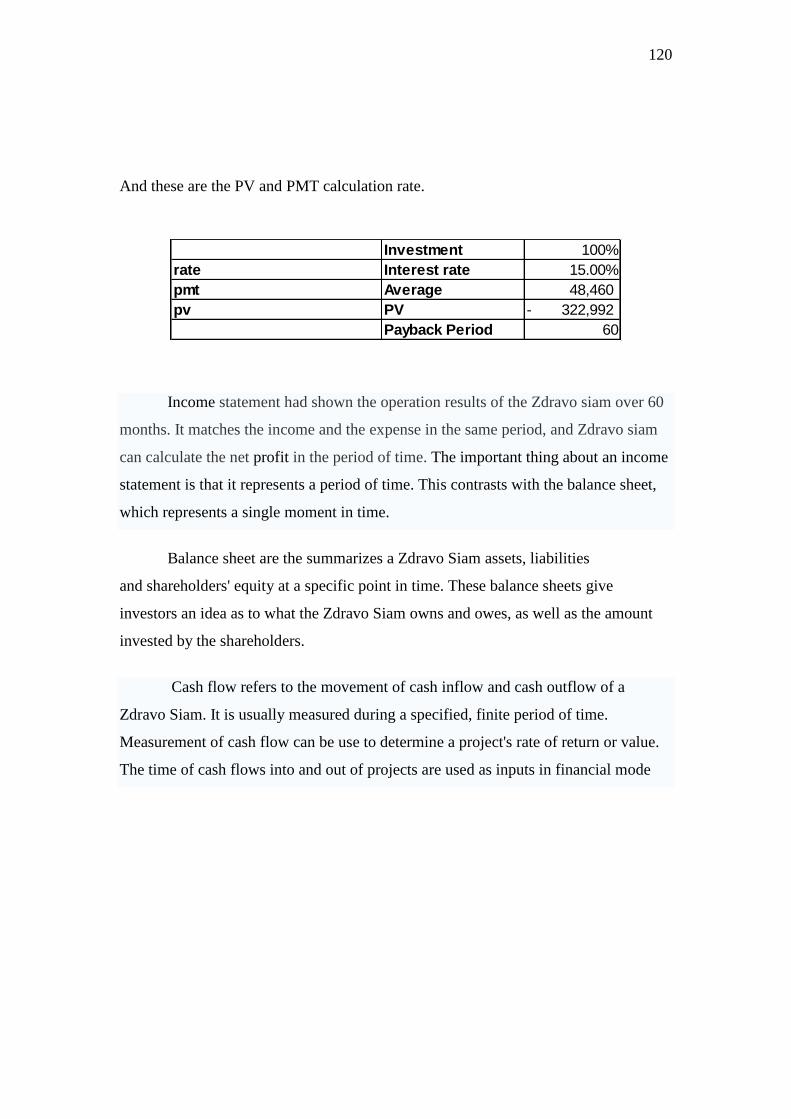

5.1 Profit and loss statement .................................................................................... 81

5.2Cash flow statement ............................................................................................ 86

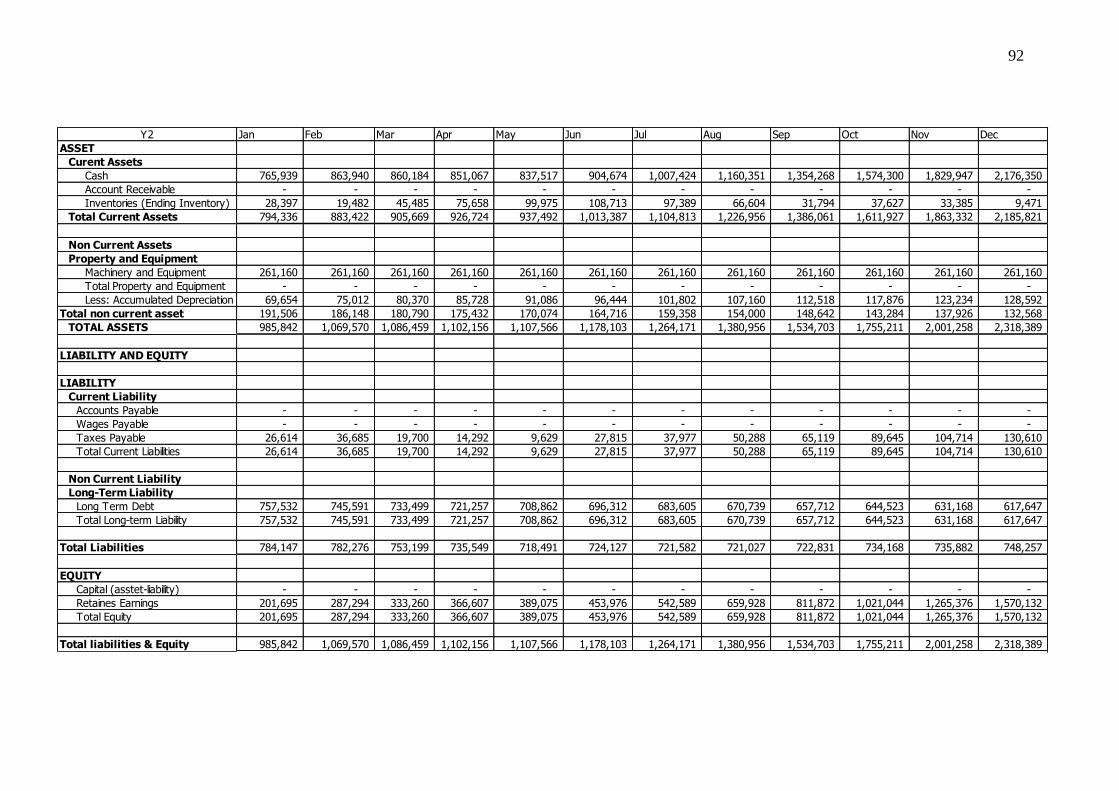

5.3 Balance sheet ..................................................................................................... 91

Chapter 6 .................................................................................................................... 101

VI

6.1. Risk analysis of projects ................................................................................. 101

6.1.1. Certainty Risk .......................................................................................... 101

6.1.2. Uncertainty Risk ...................................................................................... 101

6.1.3. Economic Condition ................................................................................... 102

6.1.4. Risks from natural disasters ....................................................................... 103

6.2 Risk management summary ............................................................................. 113

Chapter 7 .................................................................................................................... 115

Reference ................................................................................................................... 122

1

Chapter 1

Introduction

2

Chapter1

1.1 Background and Significance of the Project

People love to eat ice-cream, as same as we are. The origins of ice cream can

be traced back to at least the 4th century B.C. Early references include the Roman

emperor Nero (A.D. 37-68) who ordered ice to be brought from the mountains and

combined with fruit toppings, and King Tang (A.D. 618-97) of Shang, China who had

a method of creating ice and milk concoctions. Ice cream was likely brought from

China back to Europe. Over time, recipes for ices, sherbets, and milk ices evolved and

served in the fashionable Italian and French royal courts. Ice cream was imported to

Thailand in Phra Chulachom Klao Chaoyuhua or King Rama V era Thus; we plan to

make our own ice-cream shop under a name of “The Zdravo Siam”.

“Zdravo” is a word from Slovenian, which mean “Hello” in English. Every

day we meet other, we have to greet each other. As same as our ice-cream shop, when

every customer comes inside, “Zdravo” is a first word that they will hear from any

people who works in a shop.

One of a customer group who loves to eat ice-cream is a group of university

students. The Zdravo will be place in ABAC University bangna campus area which is

ABAC Plaza. The reason we choose this place is we have already make a discussion

from famous university in Bangkok, We decide that this university is a place where

people interest to use a brand name and always seek new things ,Which means we can

take more opportunity for open our brand.

As main products, it is ready to serve customers ice-cream and cake. The

Zdravo Siam proudly presents a variety of ice-cream, which home made by ice-cream

maker. Especially, an ice-cream that make from fruits in Thailand, a shop also has a

secret formula, which can win all of customer’s heart who love their health.

Customers can enjoy The Zdravo Siam with many type of home-made bakery; butter

cake, brownies etc.

All of foods and drinks are stand on a good reasonable price, which everybody

can pay for them. For our ice-cream shop’s style, The Zdravo Siam is put on a

concept of a modern and old-fashioned, which will mix together for the smoothness.

Black & White is main color of a shop’s theme. We designed to use any antiques for

decoration. The Zdravo Siam will serve customers a thousand of songs; Wi-Fi high

speed internet is available anytime.

3

1.2 Project Objective

To analyze The feasibility of an ice cream industry

To provide the project feasibility

1.3 Benefits of Project

Knowing feasibility of the project – Researchers study and analyze with real

situation.

Knowing the situation and the trends of ice cream industry, understanding

behavior of customer, and be able to select and identify the right customer.

To be able to calculate profits and expenses, and find the way to get maximize

profits.

4

1.4 Grant Chart

5

Chapter 2

Industry Profile

6

Chapter 2

2.1 Nature of Industry

Ice cream or ice-cream is a frozen dessert usually made from dairy products,

such as milk and cream, and often combined with fruits or other ingredients and flavors.

Most varieties contain sugar, although some are made with other sweeteners. In some

cases, artificial flavorings and colorings are used in addition to (or in replacement of)

the natural ingredients. This mixture is stirred slowly while cooling to prevent large ice

crystals from forming; the result is a smoothly textured ice cream.

There is no evidence of proofing how did ice cream came in to Thailand but it

might be came in to Thailand after Thailand can produce ice in the age of King

RAMAV the first ice cream that Thai people get usual with it is “Waan Yen” that made

from fruit juice and blend it to freezing point. After that POP Co., LTD, the first

manufacture of ice cream in Thailand, and it is called “PED Ice-Cream” started to use

the milk recipe. Thai people started to adapt the foreign ice cream to become the Thai

recipe ice cream and called coconut Ice cream. By using coconut cream combined with

sugar and spin it till harden. The coconut ice creams are eaten with sticky rice or sugar

palm or some people eat with bread. The homemade ice cream maker are now having

more competitive in the market by using their own brand name which consists of the

new flavor the new taste or a new kind of ice cream which gain the market share of 10%

in the market of premium ice cream which the key to success factor of ice cream

premium is to build the differentiation in the market and to be accepted from customer.

Ice cream can be divined in to 11 types

2.1.1 Frozen custard, French ice cream or French custard ice cream

The mainly ingredient of this ice cream type is yolk and have to use more than 1.4% of

yolk when you eat this kind of ice cream you will felt the smell of yolk

2.1.2 Low fat ice cream

There have to be cholesterol not more that 3g to 4 oz of ice cream

2.1.3 Non fat ice cream

There have to be cholesterol not more than 0.5 g per unit of serving

7

2.1.4 Gelato

Gelato, or the plural gelati, is Italy's regional variant of ice cream. As such, gelato is

made with some of the same ingredients as most other frozen dairy desserts. Milk,

cream, various sugars, flavoring including fruit nut purees and air are the main

ingredients. Gelato, or the plural gelati, is Italy's regional variant of ice cream. As such,

gelato is made with some of the same ingredients as most other frozen dairy desserts.

Milk, cream, various sugars, flavoring including fruit nut purees and air are the main

ingredients.

2.1.5 Bulky flavored ice cream

Bulky Ice-Cream is an ice-cream with any ingredients in maximum, such as fruits,

peanuts or cocoa. Some may have ingredient more than 1.4 of a hundred percent of ice-

cream.

2.1.6 Soft serve

Soft serve is generally lower in milk-fat (3% to 6%) than ice cream (10% to 18%) and is

produced at a temperature of about −4 °C compared to ice cream, which is stored at −15

°C. A warmer temperature allows the taste buds to detect more flavors. Soft serve

contains air introduced at the time of freezing. The air content, called overrun, can vary

from 0% to up to 60% of the total volume of finished product. The amount of air alters

the taste of the finished product. Product with low quantities of air has a heavy, icy taste

and appears more yellow. Product with higher air content tastes creamier, smoother and

lighter and appears whiter. The optimum quantity of air is determined by the other

ingredients and individual taste. It is generally accepted that the ideal air content should

be between 33% and 45% of volume. More than this and the product loses taste, tends

to shrink as it loses air and melts more quickly than that with less air.

2.1.7 Fruit Sherbet

a frozen fruit-flavored mixture, similar to an ice, but with milk, egg white, or gelatin

added.

2.1.8 Sorbet

Sorbet is a frozen dessert made from sweetened water flavored with iced fruit (typically

juice or puree), chocolate, wine, and/or liqueur. The sorbet originated as the Middle

8

Eastern drink charbet, made of sweetened fruit juice and water. Sorbet is sometimes

served between courses as a way to cleanse the palate before the main course.

2.1.9 Frozen yogurt

Also known as frozen yoghurt, froyo or frogurt is a frozen dessert made from, or

containing yogurt or other dairy products. It is slightly tarter than ice cream, as well as

lower in fat (due to the use of milk instead of cream). It differs from ice milk (more

recently termed low-fat or light ice cream), which does not include yogurt as an

ingredient.

2.1.10 Granite

Granite is a rough ice-cream like transparent ice, but, it is a sweetener or fruit juice

and bring it to freeze until it get to freezing point and slice it and mix it as and ice cube.

2.1.11 Water ice or ice

Ice or “Slow Train”, is made from juice that mix together with gelatin and freeze in low

temperat

9

2.2 Situation of Industry

The ice cream industry in Thailand has a stable growth rate in 2009 according to

the research of Kasikorn research center and uniliver company state that the

consumption of ice-cream per one Thai people is 6.0 liter per year. The consumption

rates are rising by 5.0% per year. When compare the consumption rate of ice cream of

Thai people to neighbor’s rate. Thailand ice cream consumption rate are the lowest

when compare with Malaysia which the ice cream consumption rate is 3 liter per year or

Japan which is 7 liter per year and still very low when comparing to other country

which are in Europe area the highest rate of ice cream consumption is USA which reach

to 24 liter for person per year and Australia consumption rate is 18 liter for person per

year (figure.1). Thailand ice cream industry have a lot’s of space to invest and gain

profit and in year 2009 the ice cream market industry is worth 18000 million bath or

when compare with the pass year the ice cream industry in Thailand growth 5% every

year .

Figure1.1: Ice cream consumption rate per person per liter

Ice-cream industry are now interest by the international firm which focused to

entered Thailand ice cream industry because now a days the ice cream industry have a

value of 18000million bath which split in to 3 kind the first one is Upper level have a

value of 3000 million bath and have a growth rate higher than 10% The second one is

10

mass level has a value of 7,000 million bath also have a growth rate between 3-5% the

last one is The lower level has a value of 1,000 million baht the ice cream industry in

Thailand is the most interest industry of the international ice cream manufacture which

occur the flow of premium ice cream into Thailand within several year(figure.2) and it

also expand the Thailand ice cream industry .

Figure1.2: import and export of Thai’s ice cream value

2.3 Product/Service (in General)

2.3.1 Ice Cream

Zdravo siam product are basely sale of an scoops of ice cream which are

guarantee of a high quality of product that come from the fresh material, and Zdravo

siam ice cream will match the need to the trend of the food industry for now.

IMPORT AND EXPORT OF THAI’s ICE-CREAM VALUE

Quantity: ton / value: million

Year Import Export

Quantity Value Quantity Value

2544 457.15 52.72 9335.82 428.14

2545 545.63 64.56 10473.05 491.23

2546 717.32 74.13 13841.00 718.82

2547 1377.10 116.70 14730.82 787.50

2548 1493.04 127.98 14262.27 730.44

Jan.-Nov. 2548 1391.48 118.54 13013.45 665.15

Jan.-Nov. 2549 1821.96 156.06 13972.12 678.20

Source: the Customs Department, collected: Thai Farmer Bank Researcher

11

2.4 Vision of your Organization

To be well known ice-cream shop in ABAC Bangna Campus.

2.5 Mission

Make all customers enjoy and satisfy by giving the best service. All Zdravo

Siam’s products are high quality, and use ingredients from Thai agricultural product.

Respond to ice-cream’s lovers, and also students who live in ABAC Bangna campus

area. Zdravo Siam will work with carefully by always drive out fresh products and seek

for successfully in every time. Customer’s need is the first thing we take care of, follow

by staffs. Zdravo Siam is interesting with a variety of ice-cream flavors. Staff is the

beginning of the way to success.

2.6 Strategy

2.6.1 Corporate Level

The strategy we choose to use in a corporate level is intensive strategies and

mainly focused on strategy that is Product development, because now a day’s ice cream

business has a high level of competition in the market which all of the ice cream shop

have the same taste of an ice cream. Way of making ice cream but for our ice cream

shop we are looking for the gap in the market which it has some space that we can grow

in the market such as a fresh homemade ice cream which we will bring out the new

flavor to the ice cream market by the product development .

The second aim is by the market development by sent the product to the higher

level of market and if our ice cream shops have a stable growth rate in the new upper

level we can aim to opened up a franchise.

12

2.6.2 Business Level

Figure2.1: Porter’s five generic strategies

According to figure.3 we choose to be type 3 which is a differentiation strategy

which now a day’s an ice cream industry are highly competing in cost but the flavor on

an ice-cream are still the same but our ice-cream shop are mainly focus on homemade

ice cream business which made from fruit and there are some gap in the ABAC plaza

market so we can built some differentiation by offering the new flavor of ice cream into

the market and at the same time we can built the differentiation of our brand can be

unique by the style of shop decoration.

13

2.6.3 Functional Level

Administration

For the Zdravo Siam, customer is the first one we care of. Thus, the shop should

be following the best quality of administration process, including the shop decoration

and service.

Business Strategies

- Good shop decoration

- Always offer new promotion for customers

- Build good relationship with customer

Marketing

Now our shop is set at ABAC University, so, the target market of the shop is

teenagers who live around ABAC university area. However, to expand our business to

be well known from many people, we have planned to promote and expand more

branches in the future.

Marketing Strategies

-Making any special Advertising and offer to customers, such as a discount promotion.

-Good service

-Expand more branches, over Bangkok area.

Production

To help Thai farmers and Thai economy, we also use all of Thai ingredient for

our product. A shop has fashionable ice-cream, such as Thai fruit ice-cream. However,

the production quantity will depend on weather and marketing. We will decrease the

production on summer because our customers have no class in the summer season so,

they did not come to the ABAC Campus so, and the demand will decrease. In winter

and rainy season our customer come back to ABAC Campus that is our shop location

so, the demand will increase related to the population of customer too.

Production Strategies

- Production must be support customer’s demand in a hundred percents.

- Cleanness Production

- Good quality of ingredients

- Stable taste of product

14

Human Resources

We pay attention of staff’s performance. They need to develop themselves in

every time, have a clear direction of work and can earn profit to the business. Moreover,

the relationship between staffs is very important, because it can drive the business to be

successful in quickly.

Human Resource Strategies

- Training and repeating all staffs to be always ready to work/.

- Motivating all staffs, by offer them extra cash.

Financial

We should have a good capital which high percentage of securely. It might be come

from entrepreneur or take on loan.

Financial Strategies

- Find the low interest of loan.

- Making a shop account

- Be economical [water and electricity]

15

Chapter 3

Market Feasibility Study

16

Chapter3

3.1 Market Analysis

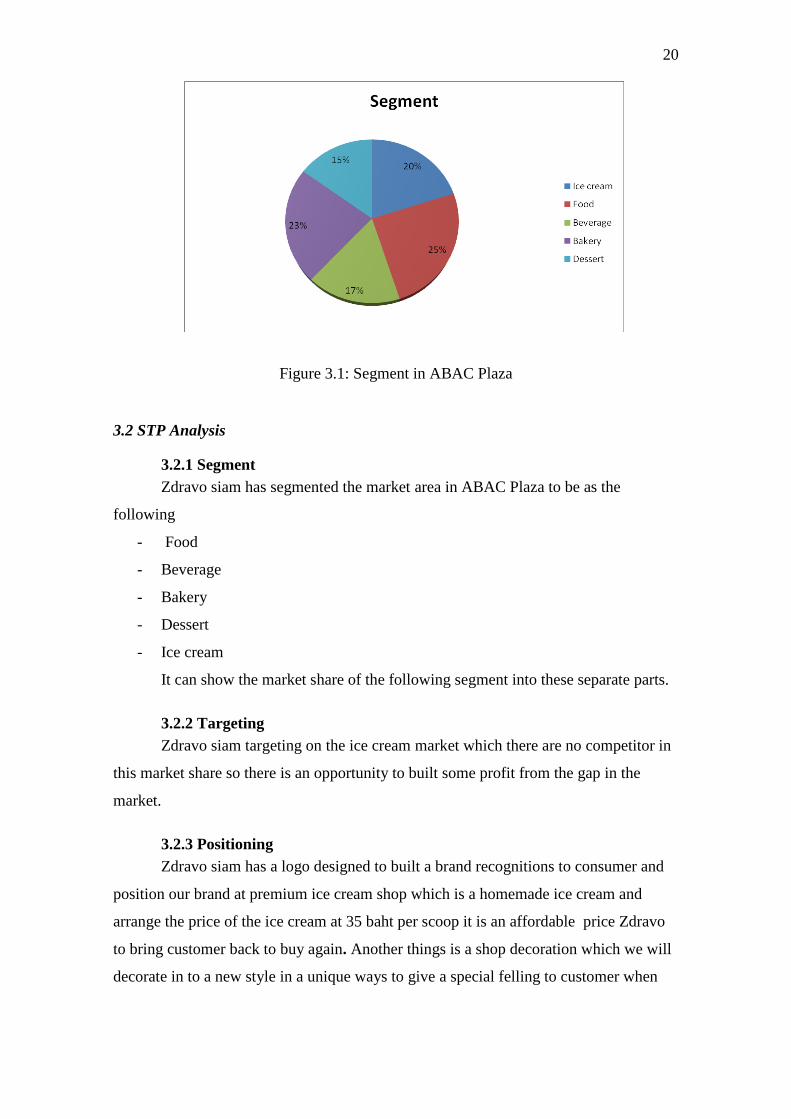

According to the survey of the area in ABAC Plaza we can divined the market

into main four part of the segment as the following

- Food

- Beverage

- Bakery

- Dessert

- Ice cream

Zdravo siam mainly focused to the Ice cream market share which from the

competitive analyses in the ABAC plaza which are highly compete in the food and

beverage. So, Zdravo Siam has seen the gap in the market which has no any ice-cream

shop in the ABAC plaza area. This is an opportunity in opening up an ice cream shop in

ABAC plaza area which we can see an opportunity that can built a profit for the

investor.

3.1.1 General Environment Analysis

Political

Today, the government has problems in agriculture by using price guarantee, so

result in agricultures have to improve quality to sell more. It makes the advantage for

company because raw materials in production are from domestic agricultural

production. When the outcomes have high quality, it enables to select raw materials to

produce more and better product quality with lower-cost.

Economic

The economic factor will not have an effect on the Zdravo siam because Zdravo

siam located in ABAC Plaza area Althrough, the economic factor didn’t have an effect

to the rate of ice cream consumption is also growing continuously , so it gives the

opportunity for company to get market share.

Social

Today, consumers attend to healthy, so the company has the opportunity to

develop useful products for health such as fruit ice cream, low fat ice cream, high

17

calcium milk ice cream, and sugar-free ice cream. It attract to the consumers of all ages,

whether children, teenager, adults until to the elderly.

Environment

Thailand is a country located in the tropical. It makes demand for consumption

ice cream all the year. Thailand also has fruits and agricultural raw materials to produce

the ice cream. These are strengths of the company to get the opportunities for product

development and export to foreign countries.

Technology

Now process of production for homemade ice cream has been improved by

technology development so the production for ice creams both looks and tastes to meet

the needs of customers who always want the innovation.

3.1.2 Competition Analysis (3C Analysis)

3.1.2.1 Competitor’s analysis

We have position in Zdravo Siam in ABAC plaza which is first mover

advantage because no exist of supply that provides ice cream to the demand on this

market. So, almost of our competitors are substitute competitors. We can analyze the

main competitor into the following which is

S&P

They produce and distribute bakery. Frozen food shelf Products, sausage and

ham pasta line and color, odor, used in food industry under the name "S & P" "Delio"

"Patio" "Vanilla" "Bluecup" and "Royallee" through branches and restaurants bakery

and Super Markets. and export to foreign countries. Almost price of their product start;

cookies 78 baht, cake 325 baht, snack 35 baht, coffee 55 baht and bakery 49 baht.

Coffee world

Coffee World is coffee house that offers a comprehensive range of hot and iced

coffees with fresh complementary foods such as waffles, sandwiches and signature

cakes, muffins and cookies. The company places a lot of emphasis on picking and

roasting the finest Arabica beans to create rich brews prepared by our highly trained

baristas (professional coffee makers).Almost of the price start; cake 70 baht and coffee

65 baht.

18

Deli House

The Deli house is Europe food style restaurant, which has food, bakery and

beverage. The Deli house is soft environment

The many product such as Soft bread texture, Sweet fresh butter, Fine dish,

Sweet Dumpling, cake and pork products such as Latin American Sausage, Smoked

sausage etc. Almost of the price start; foods are 69 baht, bakeries 39 baht and beverages

39 baht.

Blue Coffee

The company's business is the operation of coffee houses serving food and

coffee, located in ABAC plaza. Blue coffee's excellent reputation is based on serving

coffees of the highest quality, with the best aroma and taste, made from 100% fresh

coffee beans. Use the "Menu Explorer" at right to find out about some of the many

delicious beverage items on our menus. Almost of the price start; coffees are 65 baht

and cakes are 39 baht.

Take a Break

The take a break is comfortable style restaurant. The feature of restaurant is fast

but very delicious. Almost of the price start; foods are 49 baht and beverages 35 baht.

Mister Donut

Mister Donut is doughnut franchise shops. Almost of the price start; donuts 10

baht, bakeries 35 baht and beverages 35 baht.

Boost Juice

Boost Juice Bars is an international chain of retail outlets that specialize in

selling fruit juice. Boost Juice Bars was formed in 2000 with the first store located in

Adelaide, South Australia. The company has expanded internationally with stores in

Asia, Europe and the Middle East through franchising. Almost of the price start

beverage at 45 baht.

Squeeze

A subsidiary of Tipco Company mainly focused on sale of natural fruit

smoothies. Almost of the price start beverage at 35 baht.

Aunntie’s Ann

Auntie Anne's has a variety of pretzel products, dipping sauces, and beverages to

choose. Almost of the price start; bakeries are 59 baht and beverage 39 baht.

19

3.1.2.2 Competitive analysis

Ice cream market is a market that is constantly expanding. There are more

current operators because of operate easily. The observation that famous brand open

more branches and begin to development in production, marketing and expanding

distribution channels. Major reputation business has more capital is more aggressive in

market and create distribution channels and distribution to cover thoroughly. At present,

ice cream market in Thailand is quite capable of continuous growth. Benefits of ice

cream market in Thailand can be doing throughout the year because the weather is quite

hot and weather is not different. Many people like to eat ice cream because it makes

them relax and fresh.

Our company is homemade ice cream own position is in the premium ice cream

market. The market value of ice cream premium market is approximately 17% or

approximately 1800 million baths. Market conditions of premium ice cream are serving

sit eating patterns. The major are compete between big 2 companies; Swensen’s ice

cream, Hagen Daze’s ice cream. While the other competitor in ABAC Plaza area is

ignore to compete in the ice cream market.

3.1.2.3 Customer analysis

Company emphasizes in young and working age customers with an average age

ranging from 17-35 years with high purchasing power parity and want innovation. This

easy to bring the product into the consumers know.

From a target group, ABAC students who want to consume premium homemade

ice cream. Because of the gap area ABAC Plaza not supply ice cream to meet existing

demand. The opportunity to visit the company capture market share in this. The market

is a market that is very important due to its ability to target the high spending. Average

income per capita is 10000 baht per month based on the personal costs of ABAC

students. http://www.abaca.au.edu/Abaca/news-au/35abac.php. From expectations of

behavior based on the target, Research on Consumer perception of the nature and

quality of home-made and commercial dairy ice cream of John A. Bower, and Irene A.

Baxter, which shows demand is associated with income. That indicates the relationship

between demands for low cost products when consumers have more income. A position

appropriate its needs and profitable.

20

Figure 3.1: Segment in ABAC Plaza

3.2 STP Analysis

3.2.1 Segment

Zdravo siam has segmented the market area in ABAC Plaza to be as the

following

- Food

- Beverage

- Bakery

- Dessert

- Ice cream

It can show the market share of the following segment into these separate parts.

3.2.2 Targeting

Zdravo siam targeting on the ice cream market which there are no competitor in

this market share so there is an opportunity to built some profit from the gap in the

market.

3.2.3 Positioning

Zdravo siam has a logo designed to built a brand recognitions to consumer and

position our brand at premium ice cream shop which is a homemade ice cream and

arrange the price of the ice cream at 35 baht per scoop it is an affordable price Zdravo

to bring customer back to buy again. Another things is a shop decoration which we will

decorate in to a new style in a unique ways to give a special felling to customer when

21

they come Zdravo siam are focused on homemade ice cream to inform to customer that

they are the drive that push the company to the brighter future which it can build the

brand loyalty.

Zdravo siam will positioning by using the blue ocean strategy as shown below to

show that from the survey we can identify the variety of product in ABAC Plaza and

has a gap in the market to gain profit.

Figure 3.2: Blue ocean strategy

From the graph above it can illustrate that the gap in the Abac Plaza Market are

low supply in an ice cream product,so Zdravo Siam aim the gap in the market and will

positioning our self on the ice cream shop that give more supply of an ice cream product

according to the survey from questionnaire from date…-…. Shown that there are a

demand of an ice cream needs.

3.3 Marketing Mix Strategy

3.3.1 Product

Our ice-cream is ice cream for the health. It’s mixture between ice-cream with

many fruits. And the result is the delicious that is valuable for health. We have free

22

water enhance give with a customer. Which these things, we recruit for customer it

more than dessert or ice-cream. But it is modernism, flavors of ice-cream sweetness for

customer.

3.3.2 Price

The majority of the business’ sales will come from ice cream. We use price

strategy 35 Baht. Which we use psychology price in our products and price of our

products are appropriate. For basic price we fix a price by use the capital because almost

business use this method.

3.3.3 Place

We choose ABAC campus because it’s easy to sell image and ABAC bangna

campus is the place which students has influential in goods buying from statistics to

open the shop at ABAC and possibility to make profits by decorate the shop for

customer who wants to relax by provide the music to customer with the chilling music

to and the relaxation atmosphere while waiting to go to class or place to sit back and

relax after the class

3.3.4 Promotion

Zdravo siam will push all of the promotion to built the good relationship with

customer and give the customer good perception to the Zdravo siam brand. Such as a

discount or a promotion that will appeal customer to come and spend the money at

Zdravo siam.

3.4Five force model

Exist competitor

Overview of the ice cream market will find that there are many competitors. Both

small and large. Coupled with the ice cream market rates grasp how early in the 50-80%

level as well as market growth continued and potential future growth rates due to more

consumption of ice cream in Thailand. Current is low compared to other countries. But

the location of the shop area without any ice cream shop opens. So, there are no direct

competitor to compete with Zdravo siam this is the opportunity to gain high sale

volume.

23

New entry barrier

Access to ice cream markets is easy especially in the group of Home-made ice

cream as a less complex production technologies Ice cream business, but business is

similar to other food. Flavor is the highlight. And to derive methods to produce the best

ice cream flavor that require different techniques that have resulted from a long trial.

This may not simply be imitated. And take not less to do. Counterfeit goods to be

Quality, the same level together. For the protection of capital and competitive ability

more the company is focused on building relationships with customers. We have to

focus on marketing promotions that have access needs of students. Exit strategies and

large competitors cannot imitate or emulate difficult. To attract customers to stay with

us such as free print if the purchase of the stores scheduled.

Substitute product

Ice cream is a product that is easy to substitute products. Depending on whether

a product will look kind of ice cream. If any overview food that is sweet and kind one,

products to replace the food is sweet to all. Which a number, If we compare the prices

of existing competitors, we are also in line with cheaper quality compared. We also are

a feature. Home Made Ice Cream. The most competitive products are franchiser. That is

available generally. When viewed from the sweltering weather outside of the university

and ABAC. Ice cream seems to be popular than other dessert.

Power of buyer

The company brand is new and not yet well known and accepted in the market.

The Company is required in areas ABAC Plaza. And store sales. In the drive to

consume. Since the image area of the store is set to see a good image and thus help

support the good image of the store to customers. Later, when the goods have been

more popular. Will contribute to building the company's bargaining power increase.

However, the quality of ice cream flavors are the most important factors to Business in

the long term tend to increase the likelihood of repeat purchases of consumers.

24

Power of supplier

Because raw material production base of the product was not difficult to find,

such as milk, cream, eggs, fresh vegetables, fruits, etc., a product that provides easy and

has many manufacturers in the market for a Supplier bargaining power is low.

Especially the agricultural products. Normal price will fall when the season because of

low productivity into the market once substantial. However, to get a good quality of raw

material quality tests from some manufacturers. To facilitate the quality control of raw

materials.

From the above analysis showed that ice-cream business is an industry of

market has high gravity. Both the production cost per unit low. (Making a gross profit

margin high) into the market is doing. Easy because no barriers to entry. Especially in

the Ice Cream Home-made small and Supplier bargaining power is lower. Because

materials used in manufacturing a product purchased at general and sellers in the market

more. However, the qualities of ice cream flavors are the most important factors to

business in the long term.

25

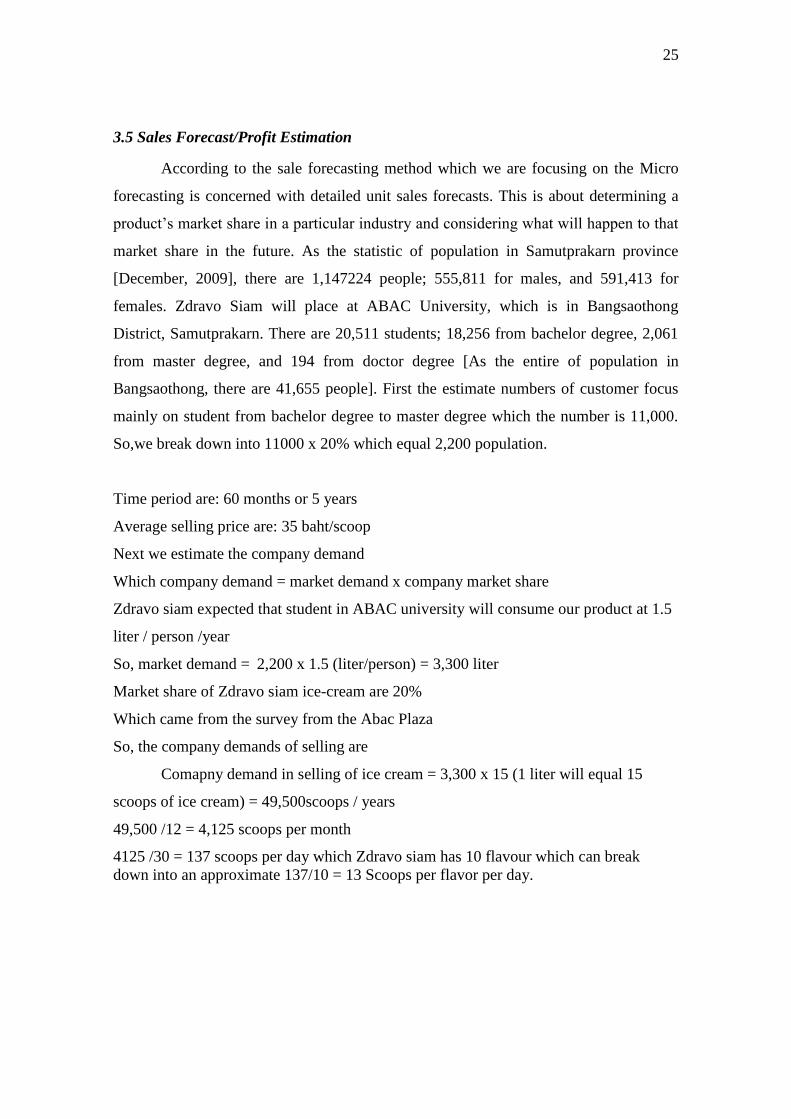

3.5 Sales Forecast/Profit Estimation

According to the sale forecasting method which we are focusing on the Micro

forecasting is concerned with detailed unit sales forecasts. This is about determining a

product’s market share in a particular industry and considering what will happen to that

market share in the future. As the statistic of population in Samutprakarn province

[December, 2009], there are 1,147224 people; 555,811 for males, and 591,413 for

females. Zdravo Siam will place at ABAC University, which is in Bangsaothong

District, Samutprakarn. There are 20,511 students; 18,256 from bachelor degree, 2,061

from master degree, and 194 from doctor degree [As the entire of population in

Bangsaothong, there are 41,655 people]. First the estimate numbers of customer focus

mainly on student from bachelor degree to master degree which the number is 11,000.

So,we break down into 11000 x 20% which equal 2,200 population.

Time period are: 60 months or 5 years

Average selling price are: 35 baht/scoop

Next we estimate the company demand

Which company demand = market demand x company market share

Zdravo siam expected that student in ABAC university will consume our product at 1.5

liter / person /year

So, market demand = 2,200 x 1.5 (liter/person) = 3,300 liter

Market share of Zdravo siam ice-cream are 20%

Which came from the survey from the Abac Plaza

So, the company demands of selling are

Comapny demand in selling of ice cream = 3,300 x 15 (1 liter will equal 15

scoops of ice cream) = 49,500scoops / years

49,500 /12 = 4,125 scoops per month

4125 /30 = 137 scoops per day which Zdravo siam has 10 flavour which can break

down into an approximate 137/10 = 13 Scoops per flavor per day.

26

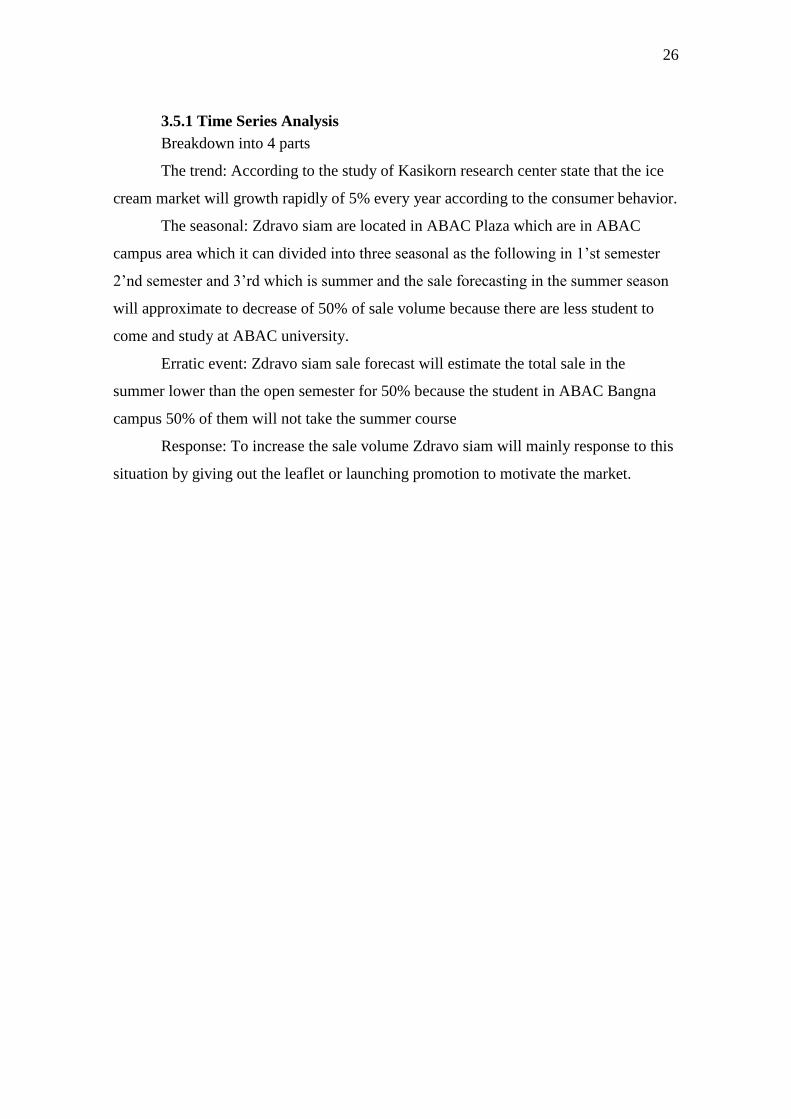

3.5.1 Time Series Analysis

Breakdown into 4 parts

The trend: According to the study of Kasikorn research center state that the ice

cream market will growth rapidly of 5% every year according to the consumer behavior.

The seasonal: Zdravo siam are located in ABAC Plaza which are in ABAC

campus area which it can divided into three seasonal as the following in 1’st semester

2’nd semester and 3’rd which is summer and the sale forecasting in the summer season

will approximate to decrease of 50% of sale volume because there are less student to

come and study at ABAC university.

Erratic event: Zdravo siam sale forecast will estimate the total sale in the

summer lower than the open semester for 50% because the student in ABAC Bangna

campus 50% of them will not take the summer course

Response: To increase the sale volume Zdravo siam will mainly response to this

situation by giving out the leaflet or launching promotion to motivate the market.

27

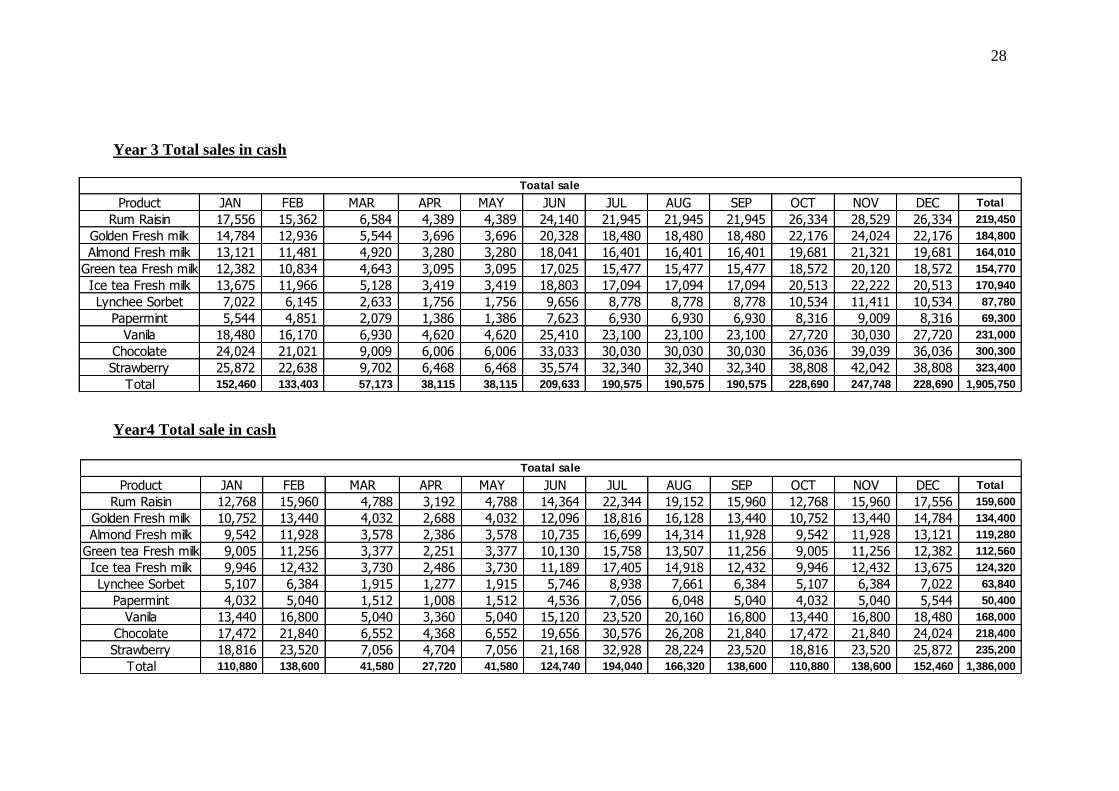

3.6 Sale Forecast

Year 1 Total sales in cash

Year 2 Total sales in cash

Product JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Total

Rum Raisin 7,182 8,379 3,591 2,394 2,394 11,970 9,576 11,970 14,364 16,758 15,561 15,561 119,700

Golden Fresh milk 6,048 7,056 3,024 2,016 2,016 10,080 8,064 10,080 12,096 14,112 13,104 13,104 100,800

Almond Fresh milk 5,368 6,262 2,684 1,789 1,789 8,946 7,157 8,946 10,735 12,524 11,630 11,630 89,460

Green tea Fresh milk 5,065 5,909 2,533 1,688 1,688 8,442 6,754 8,442 10,130 11,819 10,975 10,975 84,420

Ice tea Fresh milk 5,594 6,527 2,797 1,865 1,865 9,324 7,459 9,324 11,189 13,054 12,121 12,121 93,240

Lynchee Sorbet 2,873 3,352 1,436 958 958 4,788 3,830 4,788 5,746 6,703 6,224 6,224 47,880

Papermint 2,268 2,646 1,134 756 756 3,780 3,024 3,780 4,536 5,292 4,914 4,914 37,800

Vanila 7,560 8,820 3,780 2,520 2,520 12,600 10,080 12,600 15,120 17,640 16,380 16,380 126,000

Chocolate 9,828 11,466 4,914 3,276 3,276 16,380 13,104 16,380 19,656 22,932 21,294 21,294 163,800

Strawberry 10,584 12,348 5,292 3,528 3,528 17,640 14,112 17,640 21,168 24,696 22,932 22,932 176,400

Total 62,370 72,765 31,185 20,790 20,790 103,950 83,160 103,950 124,740 145,530 135,135 135,135 1,039,500

Toatal sale

Product JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Total

Rum Raisin 15,960 19,950 77,976 64,980 29,241 38,988 97,470 272,916 487,350 318,402 438,615 295,659 245,641

Golden Fresh milk 17,640 21,240 12,796 10,826 9,159 17,995 21,668 26,091 31,416 37,828 45,548 54,845 307,051

Almond Fresh milk 12,348 14,868 8,958 7,578 6,411 12,567 15,132 18,221 21,939 26,417 31,809 38,301 214,550

Green tea Fresh milk 22,932 27,612 16,635 14,074 11,906 23,364 28,133 33,875 40,789 49,114 59,138 71,208 398,781

Ice tea Fresh milk 22,932 27,612 16,635 14,074 11,906 23,364 28,133 33,875 40,789 49,114 59,138 71,208 398,781

Lynchee Sorbet 8,820 10,620 6,398 5,413 4,579 8,968 10,799 13,003 15,656 18,852 22,699 27,332 153,140

Papermint 19,404 23,364 14,076 11,908 10,074 19,779 23,816 28,676 34,529 41,577 50,062 60,280 337,546

Vanila 10,584 12,744 7,678 6,495 5,495 10,797 13,001 15,654 18,849 22,697 27,329 32,907 184,231

Chocolate 12,348 14,868 8,958 7,578 6,411 12,567 15,132 18,221 21,939 26,417 31,809 38,301 214,550

Strawberry 22,932 27,612 16,635 14,074 11,906 23,364 28,133 33,875 40,789 49,114 59,138 71,208 398,781

Total 164,052 197,535 119,007 100,680 85,175 167,163 201,281 242,362 291,829 351,391 423,110 509,466 2,853,051

Toatal sale

28

Year 3 Total sales in cash

Year4 Total sale in cash

Product JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Total

Rum Raisin 17,556 15,362 6,584 4,389 4,389 24,140 21,945 21,945 21,945 26,334 28,529 26,334 219,450

Golden Fresh milk 14,784 12,936 5,544 3,696 3,696 20,328 18,480 18,480 18,480 22,176 24,024 22,176 184,800

Almond Fresh milk 13,121 11,481 4,920 3,280 3,280 18,041 16,401 16,401 16,401 19,681 21,321 19,681 164,010

Green tea Fresh milk 12,382 10,834 4,643 3,095 3,095 17,025 15,477 15,477 15,477 18,572 20,120 18,572 154,770

Ice tea Fresh milk 13,675 11,966 5,128 3,419 3,419 18,803 17,094 17,094 17,094 20,513 22,222 20,513 170,940

Lynchee Sorbet 7,022 6,145 2,633 1,756 1,756 9,656 8,778 8,778 8,778 10,534 11,411 10,534 87,780

Papermint 5,544 4,851 2,079 1,386 1,386 7,623 6,930 6,930 6,930 8,316 9,009 8,316 69,300

Vanila 18,480 16,170 6,930 4,620 4,620 25,410 23,100 23,100 23,100 27,720 30,030 27,720 231,000

Chocolate 24,024 21,021 9,009 6,006 6,006 33,033 30,030 30,030 30,030 36,036 39,039 36,036 300,300

Strawberry 25,872 22,638 9,702 6,468 6,468 35,574 32,340 32,340 32,340 38,808 42,042 38,808 323,400

Total 152,460 133,403 57,173 38,115 38,115 209,633 190,575 190,575 190,575 228,690 247,748 228,690 1,905,750

Toatal sale

Product JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Total

Rum Raisin 12,768 15,960 4,788 3,192 4,788 14,364 22,344 19,152 15,960 12,768 15,960 17,556 159,600

Golden Fresh milk 10,752 13,440 4,032 2,688 4,032 12,096 18,816 16,128 13,440 10,752 13,440 14,784 134,400

Almond Fresh milk 9,542 11,928 3,578 2,386 3,578 10,735 16,699 14,314 11,928 9,542 11,928 13,121 119,280

Green tea Fresh milk 9,005 11,256 3,377 2,251 3,377 10,130 15,758 13,507 11,256 9,005 11,256 12,382 112,560

Ice tea Fresh milk 9,946 12,432 3,730 2,486 3,730 11,189 17,405 14,918 12,432 9,946 12,432 13,675 124,320

Lynchee Sorbet 5,107 6,384 1,915 1,277 1,915 5,746 8,938 7,661 6,384 5,107 6,384 7,022 63,840

Papermint 4,032 5,040 1,512 1,008 1,512 4,536 7,056 6,048 5,040 4,032 5,040 5,544 50,400

Vanila 13,440 16,800 5,040 3,360 5,040 15,120 23,520 20,160 16,800 13,440 16,800 18,480 168,000

Chocolate 17,472 21,840 6,552 4,368 6,552 19,656 30,576 26,208 21,840 17,472 21,840 24,024 218,400

Strawberry 18,816 23,520 7,056 4,704 7,056 21,168 32,928 28,224 23,520 18,816 23,520 25,872 235,200

Total 110,880 138,600 41,580 27,720 41,580 124,740 194,040 166,320 138,600 110,880 138,600 152,460 1,386,000

Toatal sale

29

Year 5 Total sale in cash

Product JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Total

Rum Raisin 19,950 15,960 5,985 3,990 3,990 27,930 23,940 15,960 19,950 19,950 21,945 19,950 199,500

Golden Fresh milk 16,800 13,440 5,040 3,360 3,360 23,520 20,160 13,440 16,800 16,800 18,480 16,800 168,000

Almond Fresh milk 14,910 11,928 4,473 2,982 2,982 20,874 17,892 11,928 14,910 14,910 16,401 14,910 149,100

Green tea Fresh milk 14,070 11,256 4,221 2,814 2,814 19,698 16,884 11,256 14,070 14,070 15,477 14,070 140,700

Ice tea Fresh milk 15,540 12,432 4,662 3,108 3,108 21,756 18,648 12,432 15,540 15,540 17,094 15,540 155,400

Lynchee Sorbet 7,980 6,384 2,394 1,596 1,596 11,172 9,576 6,384 7,980 7,980 8,778 7,980 79,800

Papermint 6,300 5,040 1,890 1,260 1,260 8,820 7,560 5,040 6,300 6,300 6,930 6,300 63,000

Vanila 21,000 16,800 6,300 4,200 4,200 29,400 25,200 16,800 21,000 21,000 23,100 21,000 210,000

Chocolate 27,300 21,840 8,190 5,460 5,460 38,220 32,760 21,840 27,300 27,300 30,030 27,300 273,000

Strawberry 29,400 23,520 8,820 5,880 5,880 41,160 35,280 23,520 29,400 29,400 32,340 29,400 294,000

Total 173,250 138,600 51,975 34,650 34,650 242,550 207,900 138,600 173,250 173,250 190,575 173,250 1,732,500

Toatal sale

30

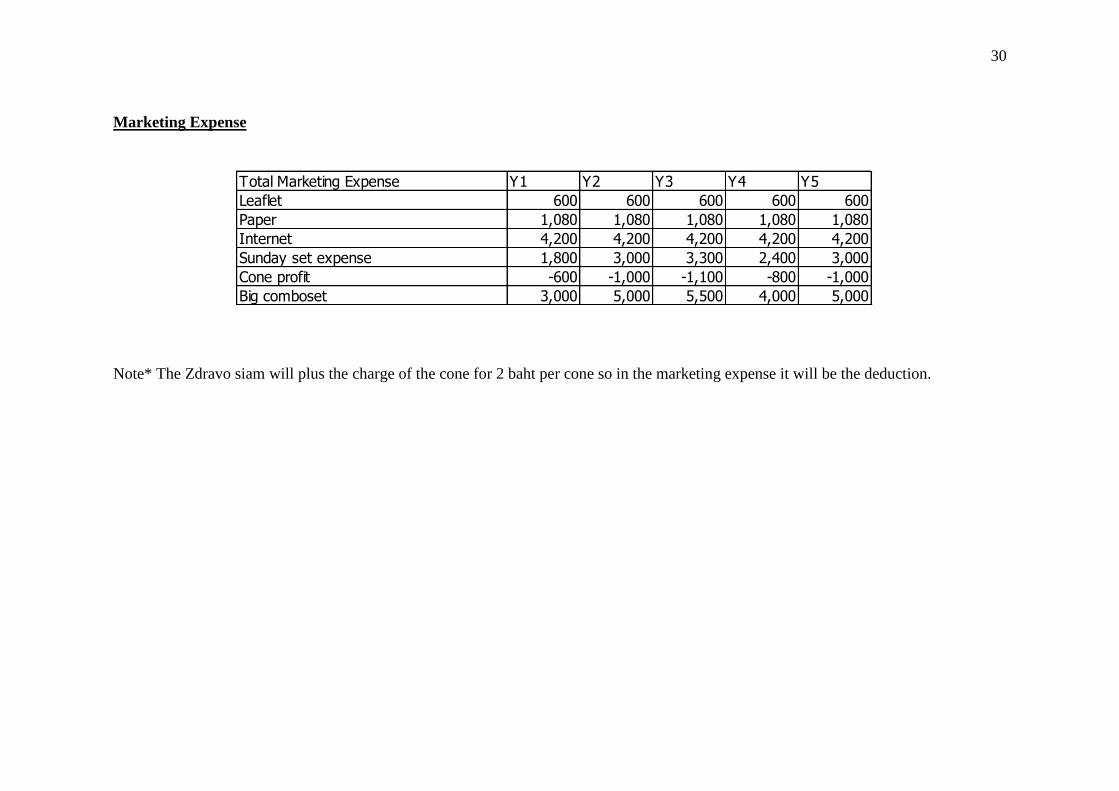

Marketing Expense

Note* The Zdravo siam will plus the charge of the cone for 2 baht per cone so in the marketing expense it will be the deduction.

Total Marketing Expense Y1 Y2 Y3 Y4 Y5

Leaflet 600 600 600 600 600

Paper 1,080 1,080 1,080 1,080 1,080

Internet 4,200 4,200 4,200 4,200 4,200

Sunday set expense 1,800 3,000 3,300 2,400 3,000

Cone profit -600 -1,000 -1,100 -800 -1,000

Big comboset 3,000 5,000 5,500 4,000 5,000

31

0%

5%

10%

15%

20%

25%

Mo

nth

1

Mo

nth

3

Mo

nth

5

Mo

nth

7

Mo

nth

9

Mo

nth

11

Mo

nth

13

Mo

nth

15

Mo

nth

17

Mo

nth

19

Mo

nth

21

Mo

nth

23

Mo

nth

25

Mo

nth

27

Mo

nth

29

Mo

nth

31

Mo

nth

33

Mo

nth

35

Mo

nth

37

Mo

nth

39

Mo

nth

41

Mo

nth

43

Mo

nth

45

Mo

nth

47

Mo

nth

49

Mo

nth

51

Mo

nth

53

Mo

nth

55

Mo

nth

57

Mo

nth

59

Sale

pe

rce

nta

ge

Zdravo siam Growth rate

Zdravo siam

3.7 Conclusion

According to the sale forecasting we it can conclude that the average income of

the total 60 month will be approximate 148,613 baht per month and the seasoning sale

will be shown as the following figure.

Figure 3.3: Zdravo siam Growth rath

As the figure shown above it will show the sharp decrease in sales this happened

because of the season of the university that close for summer. But the advantage are

even the sale are 50% lower than normal but The ABAC plaza will give an exception

not to gather the rent of the summer season.

The total of marketing expense is 60,900 baht and Zdravo siam will plus the

charge of the cone if customer wants to ice cream scoops on cone.

32

Chapter 4

Technical Feasibility Study

33

Chapter 4

4.1 Production and Operations Analysis

4.1.1 Product Characteristics

Zdravo siam product focused on only selling ice cream which generally can be dividend

in to ten flavors

4.1.1.1. Rum raisin

4.1.1.2. Golden ice-cream fresh milk

4.1.1.3. Almond ice-cream fresh milk

4.1.1.4. Green tea ice-cream fresh milk

4.1.1.5. Ice tea Ice-cream

4.1.1.6. Lynches Sorbet

4.1.1.7. Pepper mint ice-cream

4.1.1.8. Ice-cream vanilla

4.1.1.9. Ice-cream chocolate

4.1.1.10. Ice-cream Strawberry

All of Zdravo siam ice cream use a high quality ingredient inside Thailand.

34

4.1.2Production process

The basic steps in the manufacturing of ice cream are generally as follows:

blending of the mix ingredients

pasteurization

homogenization

aging the mix

freezing

packaging

hardening

Figure4.1: Process flow diagram for ice cream manufacture

Process flow diagram for ice cream manufacture: the red section represents the

operations involving raw, unpasteurized mix, the pale blue section represents the

operations involving pasteurized mix, and the dark blue section represents the

operations involving frozen ice cream.

35

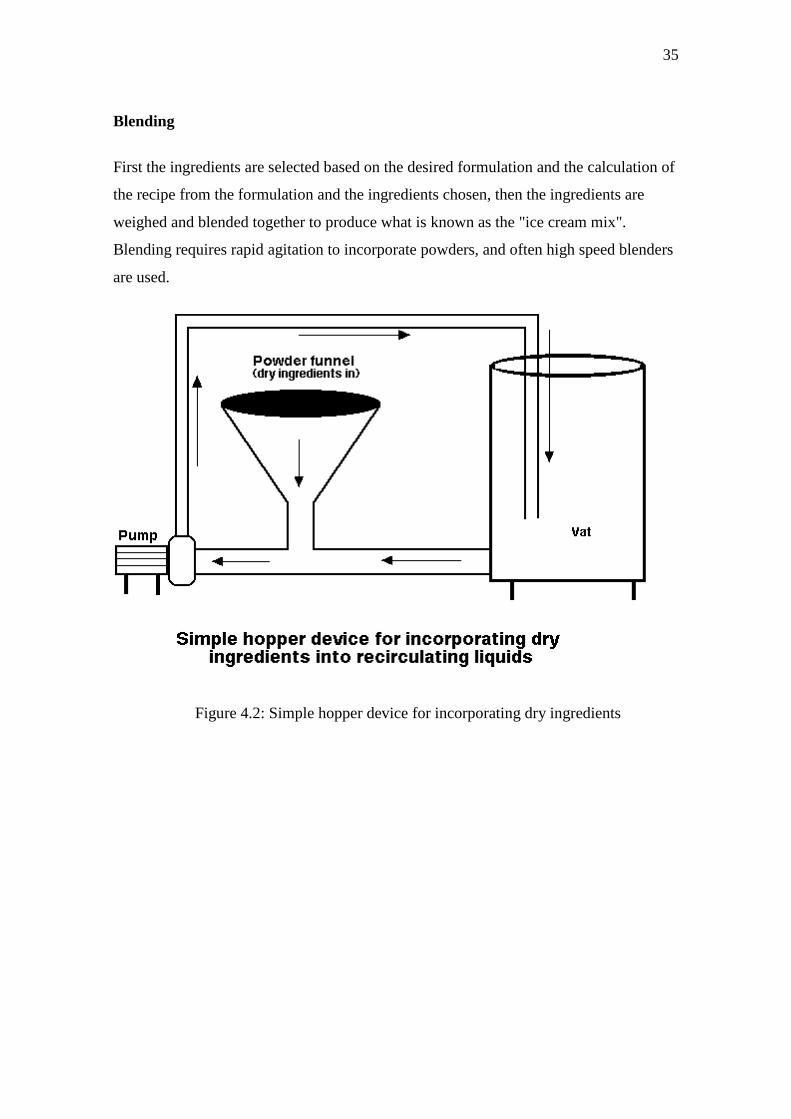

Blending

First the ingredients are selected based on the desired formulation and the calculation of

the recipe from the formulation and the ingredients chosen, then the ingredients are

weighed and blended together to produce what is known as the "ice cream mix".

Blending requires rapid agitation to incorporate powders, and often high speed blenders

are used.

Figure 4.2: Simple hopper device for incorporating dry ingredients

36

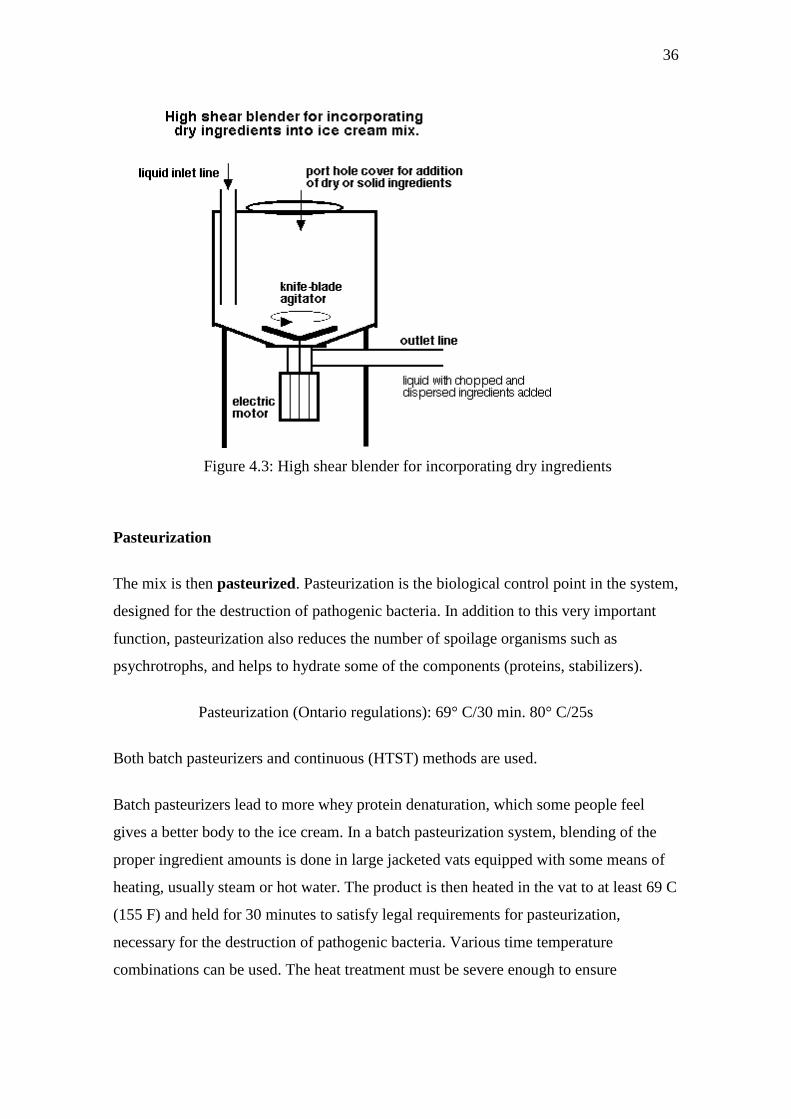

Figure 4.3: High shear blender for incorporating dry ingredients

Pasteurization

The mix is then pasteurized. Pasteurization is the biological control point in the system,

designed for the destruction of pathogenic bacteria. In addition to this very important

function, pasteurization also reduces the number of spoilage organisms such as

psychrotrophs, and helps to hydrate some of the components (proteins, stabilizers).

Pasteurization (Ontario regulations): 69° C/30 min. 80° C/25s

Both batch pasteurizers and continuous (HTST) methods are used.

Batch pasteurizers lead to more whey protein denaturation, which some people feel

gives a better body to the ice cream. In a batch pasteurization system, blending of the

proper ingredient amounts is done in large jacketed vats equipped with some means of

heating, usually steam or hot water. The product is then heated in the vat to at least 69 C

(155 F) and held for 30 minutes to satisfy legal requirements for pasteurization,

necessary for the destruction of pathogenic bacteria. Various time temperature

combinations can be used. The heat treatment must be severe enough to ensure

37

destruction of pathogens and to reduce the bacterial count to a maximum of 100,000 per

gram. Following pasteurization, the mix is homogenized by means of high pressures

and then is passed across some type of heat exchanger (plate or double or triple tube) for

the purpose of cooling the mix to refrigerated temperatures (4 C). Batch tanks are

usually operated in tandem so that one is holding while the other is being prepared.

Automatic timers and valves ensure the proper holding time has been met.

Continuous pasteurization is usually performed in a high temperature short time (HTST)

heat exchanger following blending of ingredients in a large, insulated feed tank. Some

preheating, to 30 to 40 C, is necessary for solubilization of the components. The HTST

system is equipped with a heating section, a cooling section, and a regeneration section.

Cooling sections of ice cream mix HTST presses are usually larger than milk HTST

presses. Due to the preheating of the mix, regeneration is lost and mix entering the

cooling section is still quite warm.

Homogenization

The mix is also homogenized which forms the fat emulsion by breaking down or

reducing the size of the fat globules found in milk or cream to less than 1 µ m. Two

stage homogenization is usually preferred for ice cream mix. Clumping or clustering of

the fat is reduced thereby producing a thinner, more rapidly whipped mix. Melt-down is

also improved. Homogenization provides the following functions in ice cream

manufacture:

Reduces size of fat globules

Increases surface area

Forms membrane

makes possible the use of butter, frozen cream, etc.

By helping to form the fat structure, it also has the following indirect effects: ---

- makes a smoother ice cream

- gives a greater apparent richness and palatability

- better air stability

- increases resistance to melting

38

Homogenization of the mix should take place at the pasteurizing temperature. The high

temperature produces more efficient breaking up of the fat globules at any given

pressure and also reduces fat clumping and the tendency to thick, heavy bodied mixes.

No one pressure can be recommended that will give satisfactory results under all

conditions. The higher the fat and total solids in the mix, the lower the pressure should

be. If a two stage homogenizer is used, a pressure of 2000 - 2500 psi on the first stage

and 500 - 1000 psi on the second stage should be satisfactory under most conditions.

Two stage homogenization is usually preferred for ice cream mix. Clumping or

clustering of the fat is reduced thereby producing a thinner, more rapidly whipped mix.

Melt-down is also improved.

Ageing

The mix is then aged for at least four hours and usually overnight. This allows time for

the fat to cool down and crystallize, and for the proteins and polysaccharides to fully

hydrate. Aging provides the following functions:

Improves whipping qualities of mix and body and texture of ice cream.

providing time for fat crystallization, so the fat can partially coalesce;

allowing time for full protein and stabilizer hydration and a resulting slight

viscosity increase;

allowing time for membrane rearrangement and protein/emulsifier interaction, as

emulsifiers displace proteins from the fat globule surface, which allows for a

reduction in stabilization of the fat globules and enhanced partial coalescence.

Aging is performed in insulated or refrigerated storage tanks, silos, etc. Mix temperature

should be maintained as low as possible without freezing, at or below 5 C. An aging

time of overnight is likely to give best results under average plant conditions. A "green"

or unaged mix is usually quickly detected at the freezer.

39

Freezing and Hardening

Following mix processing, the mix is drawn into a flavour tank where any liquid

flavors, fruit purees, or colours are added. The mix then enters the dynamic freezing

process which both freezes a portion of the water and whips air into the frozen mix. The

"barrel" freezer is a scraped-surface, tubular heat exchanger, which is jacketed with a

boiling refrigerant such as ammonia or freon. Mix is pumped through this freezer and is

drawn off the other end in a matter of 30 seconds, (or 10 to 15 minutes in the case of

batch freezers) with about 50% of its water frozen. There are rotating blades inside the

barrel that keep the ice scraped off the surface of the freezer and also dashers inside the

machine which help to whip the mix and incorporate air.

Figure 4.4: The Continuous Ice Cream Freezer

40

Ice cream contains a considerable quantity of air, up to half of its volume. This gives the

product its characteristic lightness. Without air, ice cream would be similar to a frozen

ice cube. The air content is termed its overrun, which can be calculated mathematically.

As the ice cream is drawn with about half of its water frozen, particulate matter such as

fruits, nuts, candy, cookies, or whatever you like, is added to the semi-frozen slurry

which has a consistency similar to soft-serve ice cream. In fact, almost the only thing

which differentiates hard frozen ice cream from soft-serve, is the fact that soft serve is

drawn into cones at this point in the process rather than into packages for subsequent

hardening.

Hardening

After the particulates have been added, the ice cream is packaged and is placed into a

blast freezer at -30° to -40° C where most of the remainder of the water is frozen. Below

about -25° C, ice cream is stable for indefinite periods without danger of ice crystal

growth; however, above this temperature, ice crystal growth is possible and the rate of

crystal growth is dependant upon the temperature of storage. This limits the shelf life of

the ice cream.

A primer on the theoretical aspects of freezing will help you to fully understand the

freezing and recrystallization process.

Hardening involves static (still, quiescent) freezing of the packaged products in blast

freezers. Freezing rate must still be rapid, so freezing techniques involve low

temperature (-40oC) with either enhanced convection (freezing tunnels with forced air

fans) or enhanced conduction (plate freezers).

41

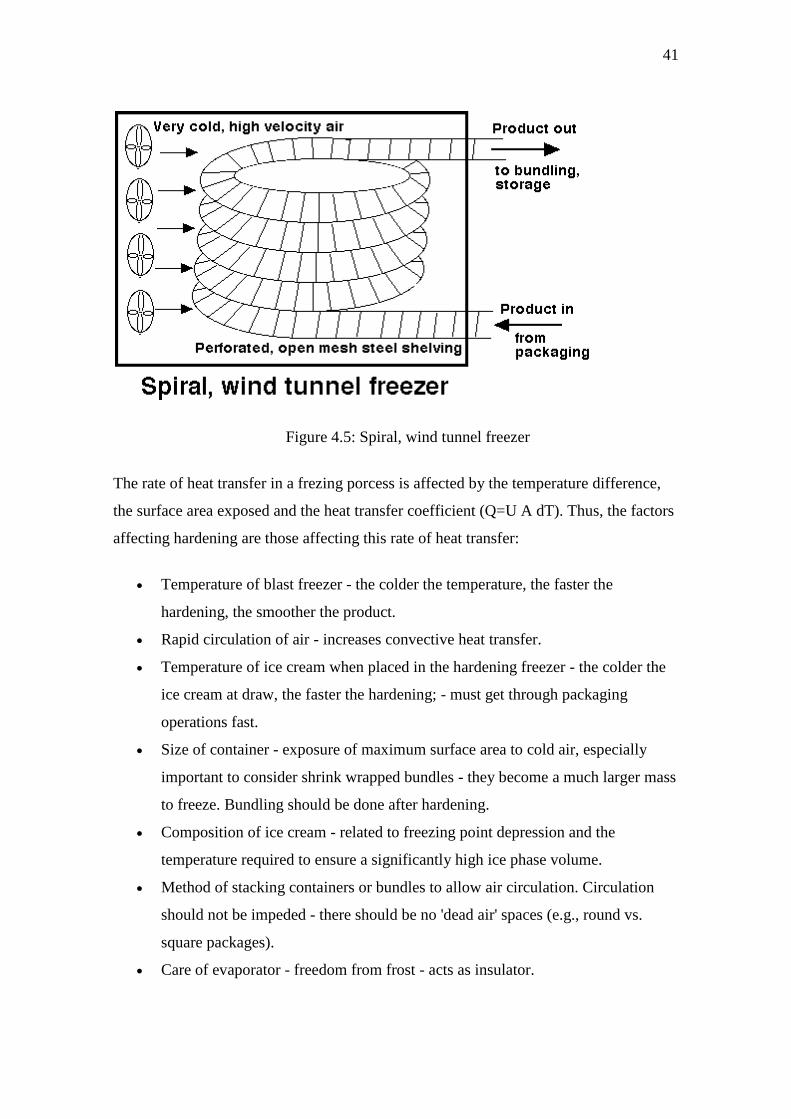

Figure 4.5: Spiral, wind tunnel freezer

The rate of heat transfer in a frezing porcess is affected by the temperature difference,

the surface area exposed and the heat transfer coefficient (Q=U A dT). Thus, the factors

affecting hardening are those affecting this rate of heat transfer:

Temperature of blast freezer - the colder the temperature, the faster the

hardening, the smoother the product.

Rapid circulation of air - increases convective heat transfer.

Temperature of ice cream when placed in the hardening freezer - the colder the

ice cream at draw, the faster the hardening; - must get through packaging

operations fast.

Size of container - exposure of maximum surface area to cold air, especially

important to consider shrink wrapped bundles - they become a much larger mass

to freeze. Bundling should be done after hardening.

Composition of ice cream - related to freezing point depression and the

temperature required to ensure a significantly high ice phase volume.

Method of stacking containers or bundles to allow air circulation. Circulation

should not be impeded - there should be no 'dead air' spaces (e.g., round vs.

square packages).

Care of evaporator - freedom from frost - acts as insulator.

42

Package type, should not impede heat transfer - e.g., styrofoam liner or

corrugated cardboard may protect against heat shock after hardening, but

reduces heat transfer during freezing so not feasible.

Ice cream from the dynamic freezing process (continuous freezer) can also be

transformed into an array of novely/impulse products through a variety of filling and

forming machines, which have ben identified on a separate page.

4.1.3 Life Time

The most frequently occurring textural defect in ice cream is the development of a

coarse, icy texture. Iciness is also the primary limitation to the shelf life of ice cream

and probably also accounts for countless lost sales through customer dissatisfaction with

quality. There is no answer to the question "What is the shelf-life of ice cream?", it

depends entirely on its conditions of storage. It might be one year, or it might be two

weeks or less. Although the source of and the contributing factors to the problem of

icincess are well known, it is also one of the defects about which I am most often asked.

Processor's have known for a long time how to prevent iciness and the answer is still the

same: formulate the ice cream properly to begin with, freeze the ice cream quickly in a

well-maintained barrel freezer, harden the ice cream rapidly, and avoid as much as

possible temperature fluctuations during storage and distribution. Ice crystals need to be

numerous and of small, uniform size so they are not detected when eaten. It is heat

shock, large temperature fluctuations, which is the greatest culprit to the loss of these

small, uniform ice crystal size distributions and resulting coarse, icy texture. Perhaps it

is time another message was added to the prevention of iciness and that is to educate the

retailer's and the consumer about the causes of iciness and preventative action to

maintain a smooth-textured ice cream.

Before we begin looking specifically at shelf-life, you need to re-acquaint yourself with

the freezing aspects of ice cream manufacturing, the structure of ice crystals in ice

cream, and the theoretical aspects of the freezing process.

43

Temperature Fluctuations and Ice Recrystallization

Ice crystals are relatively unstable, and during frozen storage, they undergo changes in

number, size, and shape, known collectively as recrystallization. This is probably the

most important reaction leading to quality losses in all frozen foods. Some

recrystallization occurs naturally at constant temperatures, but by far the majority of

problems are created as a result of temperature fluctuations. If the temperature during

the frozen storage of ice cream increases, some of the ice crystals, particularly the

smaller ones, melt and consequently the amount of unfrozen water in the serum phase

increases. Conversely, as temperatures decrease, water will refreeze but does not

renucleate. Rather, it is deposited on the surface of larger crystals, so the net result is

that the total numbers of crystals diminish and the mean crystal size increases.

Temperature fluctuations are common in frozen storage as a result of the cyclic nature

of refrigeration systems and the need for automatic defrosts. However, mishandling of

product is probably the biggest culprit. The sight of ice cream sitting unrefrigerated on a

loading dock, in the supermarket aisle, in a shopping cart, or in someone's grocery bag

is too common. If one were to track the temperature history of ice cream during

distribution, retailing, and finally consumption, one would find a great number of

temperature fluctuations. Each time the temperature changes, the ice to serum content

changes, and the smaller ice crystals disappear while the larger ones grow even larger.

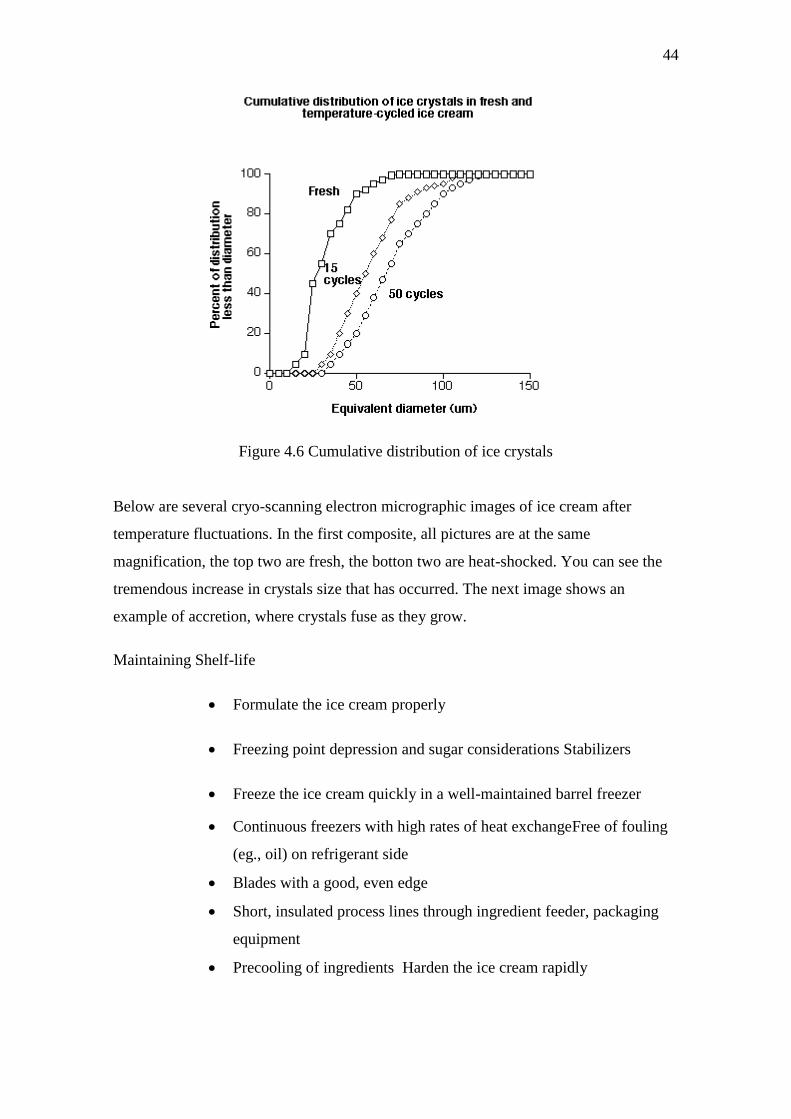

Recrystallization is minimized by maintaining low and constant storage temperatures.

The graph below provides data to show the increase in size of ice crystals that occurs

with temperature cycles (from the work of A. Flores and H. D. Goff).

44

Figure 4.6 Cumulative distribution of ice crystals

Below are several cryo-scanning electron micrographic images of ice cream after

temperature fluctuations. In the first composite, all pictures are at the same

magnification, the top two are fresh, the botton two are heat-shocked. You can see the

tremendous increase in crystals size that has occurred. The next image shows an

example of accretion, where crystals fuse as they grow.

Maintaining Shelf-life

Formulate the ice cream properly

Freezing point depression and sugar considerations Stabilizers

Freeze the ice cream quickly in a well-maintained barrel freezer

Continuous freezers with high rates of heat exchangeFree of fouling

(eg., oil) on refrigerant side

Blades with a good, even edge

Short, insulated process lines through ingredient feeder, packaging

equipment

Precooling of ingredients Harden the ice cream rapidly

45

High rates of heat transfer: convection (high ΔT and forced air with

free air flow) or conduction

Importance of thermal centre and shrink-wrapping of bundles

Avoid temperature fluctuations during storage and distribution

Importance of low, constant temperatures

Avoid mishandling at all stages

Educate retailers and consumers about shelf stability

Mishandling is usually not at the manufacturing level but quality

losses affect

4.1.4 Ice cream recipe

Rum raisin

White malt 2 teaspoons

Sugar 1/2 cup

Fresh milk 3 cup

Butter rum Syrup 20 ml

Rum ¼ teaspoon

Whip cream 1/3 cup

Guar Gum 1 tablespoon

Raisin

Directions:

How do the White malt mixed with the fresh milk sugar syrup mixed and rum

flavored cooking set fire hot enough fire gradually. First mixed together to mix. Then

put into cold enough. Mixed with milk, Whip cream, Guar Gum and mix then hold

together enough to cool the tank immersed in approximately time 4 hours and then put

ice cream in shaker. Take approximately time 30-40 minutes after completion may be

mixed currant. Then be refrigerated.

46

Pumpkin ice-cream fresh milk

White malt 2 teaspoons.

Sugar 1/2 cup.

Fresh milk 2 cup.

White chocolate syrup 10 ml.

Pumpkin 3/4 cup.

Whip cream 1/3 cup

Guar Gum 1 tablespoon

Directions:

Bring White malt mixed with sugar. And fresh milk white chocolate. Thereafter bring

pumpkin heated gradually put sugar. After that mix pumpkin and whipping cream and

mix Guar Gum. Thereafter be immersed in the ice tank approximately times 3-4 hours.

Bring ice cream in shaker and then approximately times 30-40 minutes to complete.

Almond ice-cream fresh milk

White malt 2 teaspoons.

Sugar 1/2 cup.

Fresh milk 3 cup.

White chocolate syrup 10 ml.

Caramel 30 ml

Whip cream 1/3 cup

Guar Gum 1 tablespoon

Almond 3/4 cup

Directions:

Bring White malt mixed with sugar. And fresh milk white chocolate. Thereafter bring

almond heated gradually put sugar. After that mix almond and whipping cream and mix

47

Guar Gum. Thereafter be immersed in the ice tank approximately times 4 hours. Bring

ice cream in shaker and then approximately times 30-40 minutes to complete.

Green tea ice-cream fresh milk

Powder green tea 1/3 cup.

White malt 2 teaspoons.

Sugar 1/2 cup.

Fresh milk 3 cup.

White chocolate syrup 15 ml.

Whip cream 1/3 cup

Guar Gum 1 tablespoon

Directions:

Bring White malt mixed with sugar. And fresh milk white chocolate. Thereafter bring

Green tea syrup heated gradually put sugar. After that mix Green tea syrup and

whipping cream and mix Guar Gum. Thereafter be immersed in the ice tank

approximately times 4 hours. Bring ice cream in shaker and then approximately times

30-40 minutes to complete.

Ice tea ice-cream

Ice tea powder 1/3 cup.

White malt 2 teaspoons.

Sugar 1/2 cup.

Fresh milk 3 cup.

White chocolate syrup 10 ml.

Whip cream 1/3 cup

Guar Gum 1 tablespoon

48

Directions:

Bring Ice tea powder and white malt mixed with sugar. And fresh milk white chocolate.

Thereafter bring Green tea syrup heated gradually put sugar. After that mix and

whipping cream and mix Guar Gum. Thereafter be immersed in the ice tank

approximately times 4 hours. Bring ice cream in shaker and then approximately times

30-40 minutes to complete.

Lynches Sorbet

Lynches in syrup 1 can (about 240g lynches and 200 ml syrup)

Castor sugar 20 g

1 egg white

Directions:

1. Puree the Lynches together with the sugar and the syrup.

2. Taste the mixture and adjust sugar if needed. Beat the egg white until almost stiff and

stir in the mixture. Make sure that all the ingredients are thoroughly mixed.

3. Transfer the complete mixture into an ice-cream maker and follow the manufacturer’s

instructions.

4. Puree the Lynches together with the sugar and the syrup. (Use a food processors or

blender)

5. Eat the egg white until almost stiff.

6. Mix the Leeches puree thoroughly with the egg white.

7. Make sure that all the ingredients are thoroughly mixed.

8. Preparation time: about 25-35 minutes.

49

Pepper mint ice-cream

White malt 1 teaspoons.

Sugar 1/3 cup.

Pineapple juice 1/2 cup

Fresh milk 3 cup.

Pepper mint syrup 30 ml.

White chocolate syrup 10 ml.

Whip cream 1/3 cup

Guar Gum 1.5 Tablespoon.

Directions:

Bring white malt mix with sugar. Thereafter bring fresh milk mix with white chocolate

syrup. And bring almonds syrup heated gradually. Mix with milk, whipping cream and

pineapple juice, put to Guar Gum. And cool the tank immersed about 4 hours. Put to

shaker. Approximately 30-40 minutes to complete.

Ice-cream vanilla

Fresh milk 3 cup

Egg 6 eggs

Sugar 1/3 cup

Whipping cream 1/3 cup

Vanilla powder 2 tablespoon

Guar Gum 1.5 Tablespoon.

White chocolate syrup 10 ml.

Directions:

Bring Vanilla powder mix with sugar. Thereafter bring fresh milk mix with white

chocolate syrup. And mix with milk, whipping cream and put to Guar Gum. And cool

the tank immersed about 4 hours. Put to shaker. Approximately 30-40 minutes to

complete.

50

Ice-cream Chocolate

Butter 1 cup

Fresh milk 1 cup

Sugar 1/3 cup

White chocolate syrup 10 ml.

Chocolate powder 2 tablespoon

Guar Gum 1.5 Tablespoon.

Whipping cream 1/3 cup

Directions:

Bring Chocolate powder mix with sugar. Thereafter bring fresh milk mix with white

chocolate syrup. And mix with milk, whipping cream and put to Guar Gum. And cool

the tank immersed about 4 hours. Put to shaker. Approximately 30-40 minutes to

complete.

Ice-cream Strawberry